Embed Size (px)

Citation preview

Practical ROI Goes Beyond the Math

Track 1 Session 5

2

Dan Goudey

Director, DC Storage and Throughput

– Email:

– Phone:

– Website: www.grainger.com

W.W. Grainger, Inc.

Marc Wulfraat

President & Founder

– Email: [email protected]

– Phone: (514) 482-3572 x 100

– Website: www.mwpvl.com

– LinkedIn: Marc Wulfraat

MWPVL International Inc.

Abstract

3

The case for capital investment has to include

a demonstrable return to the shareholders.

However, a holy war rages on as to what values

can be utilized on either side of the equation

(investment vs. return). This hybrid session

consists of a fact-based presentation on the

science of justification followed by an

insightful panel discussion among real

practitioners who remain employed because

they consistently deliver returns on

investment. It will enlighten, educate, and

perhaps provide the impetus needed to

advance your next project.

Agenda

4

• ROI Overview

• Aging Populations, Shrinking Labor Pools

• The Next Great Migration

• Impacts on the Grocery Industry

• Impacts on E-Commerce

• Key Takeaways

• Conference Cloud

• Questions

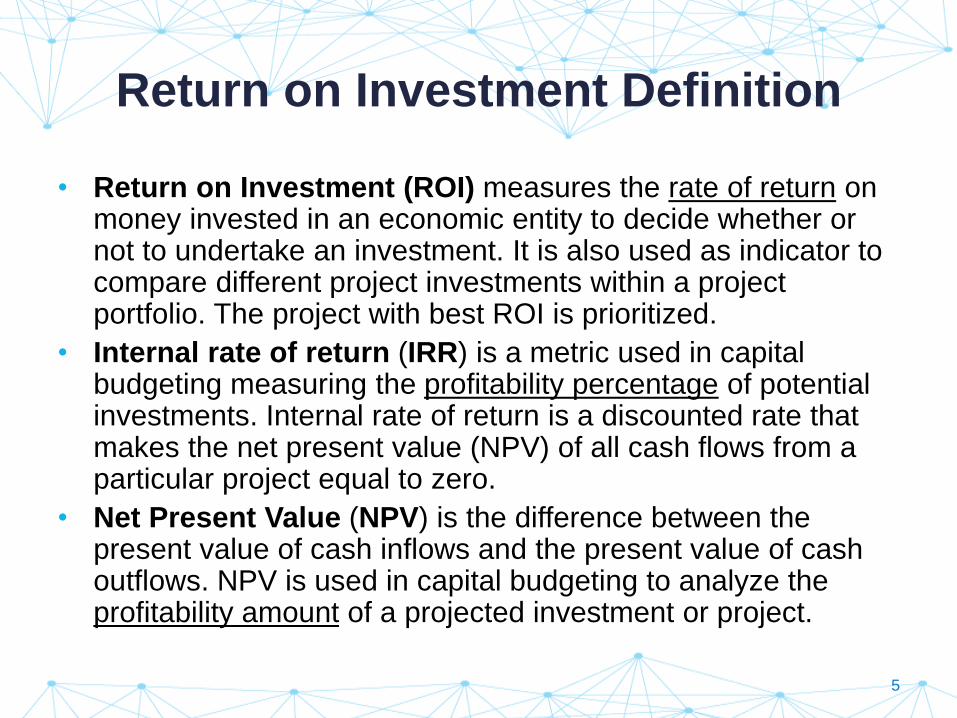

Return on Investment Definition

• Return on Investment (ROI) measures the rate of return on money invested in an economic entity to decide whether or not to undertake an investment. It is also used as indicator to compare different project investments within a project portfolio. The project with best ROI is prioritized.

• Internal rate of return (IRR) is a metric used in capital budgeting measuring the profitability percentage of potential investments. Internal rate of return is a discounted rate that makes the net present value (NPV) of all cash flows from a particular project equal to zero.

• Net Present Value (NPV) is the difference between the present value of cash inflows and the present value of cash outflows. NPV is used in capital budgeting to analyze the profitability amount of a projected investment or project.

5

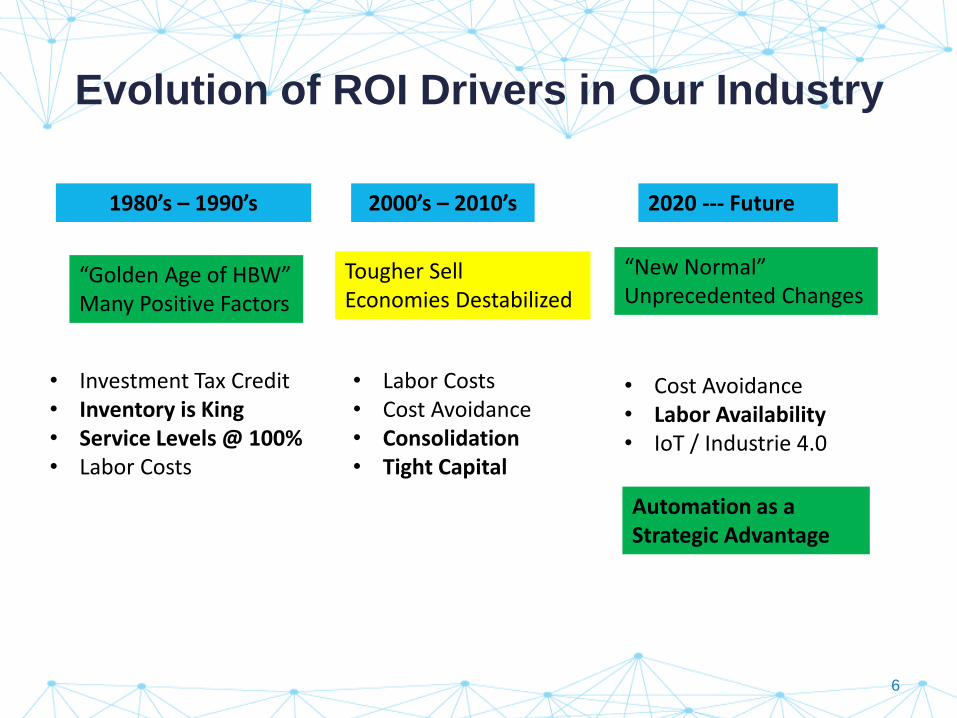

Evolution of ROI Drivers in Our Industry

6

1980’s – 1990’s 2000’s – 2010’s 2020 --- Future

• Investment Tax Credit• Inventory is King• Service Levels @ 100%• Labor Costs

• Labor Costs• Cost Avoidance• Consolidation• Tight Capital

• Cost Avoidance• Labor Availability• IoT / Industrie 4.0

“Golden Age of HBW”Many Positive Factors

Tougher SellEconomies Destabilized

“New Normal”Unprecedented Changes

Automation as a Strategic Advantage

Weakness of ROI

• ROI assumes a plentiful supply of resources to achieve capital expenditure objectives

– However labor or capital scarcity conditions significantly

influence traditional ROI decisions

– E.g. During the recent 2008 – 2009 recession, many companies

held off spending on healthy ROI projects due to a sharp scarcity

of capital in the market.

• As baby boomers reach retirement and companies face a significant forthcoming labor shortage, ROI calculations will be similarly influenced

– E.g. Companies will increasingly invest in automation solutions

that replace human labor and ensure business continuity,

regardless of the ROI associated with the investment

7

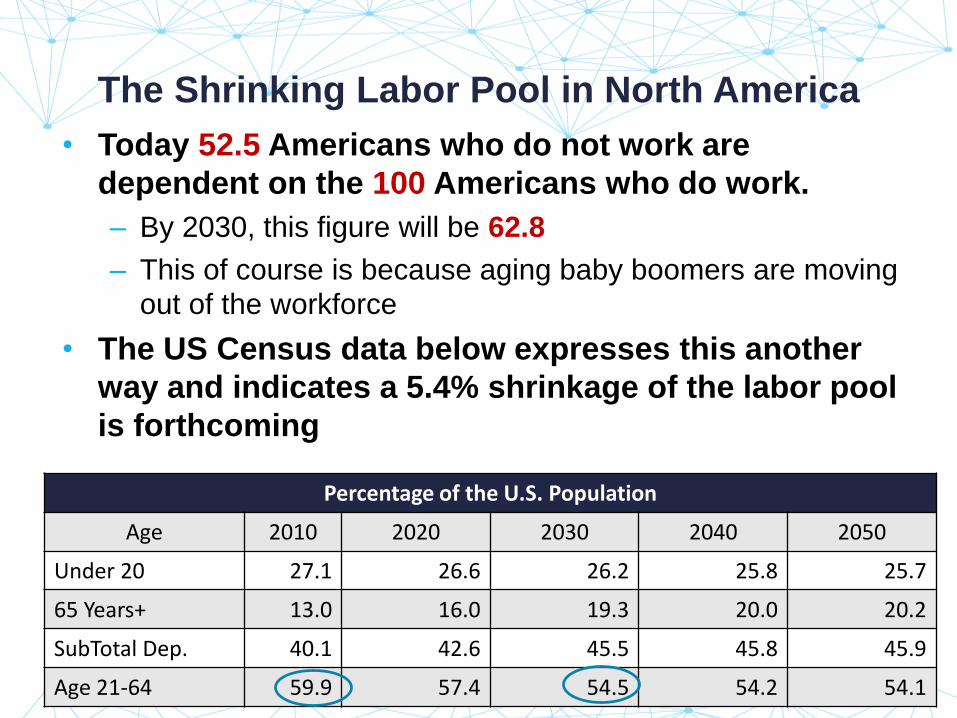

The Shrinking Labor Pool in North America

• Today 52.5 Americans who do not work are

dependent on the 100 Americans who do work.

– By 2030, this figure will be 62.8

– This of course is because aging baby boomers are moving

out of the workforce

• The US Census data below expresses this another

way and indicates a 5.4% shrinkage of the labor pool

is forthcoming

Percentage of the U.S. Population

Age 2010 2020 2030 2040 2050

Under 20 27.1 26.6 26.2 25.8 25.7

65 Years+ 13.0 16.0 19.3 20.0 20.2

SubTotal Dep. 40.1 42.6 45.5 45.8 45.9

Age 21-64 59.9 57.4 54.5 54.2 54.1

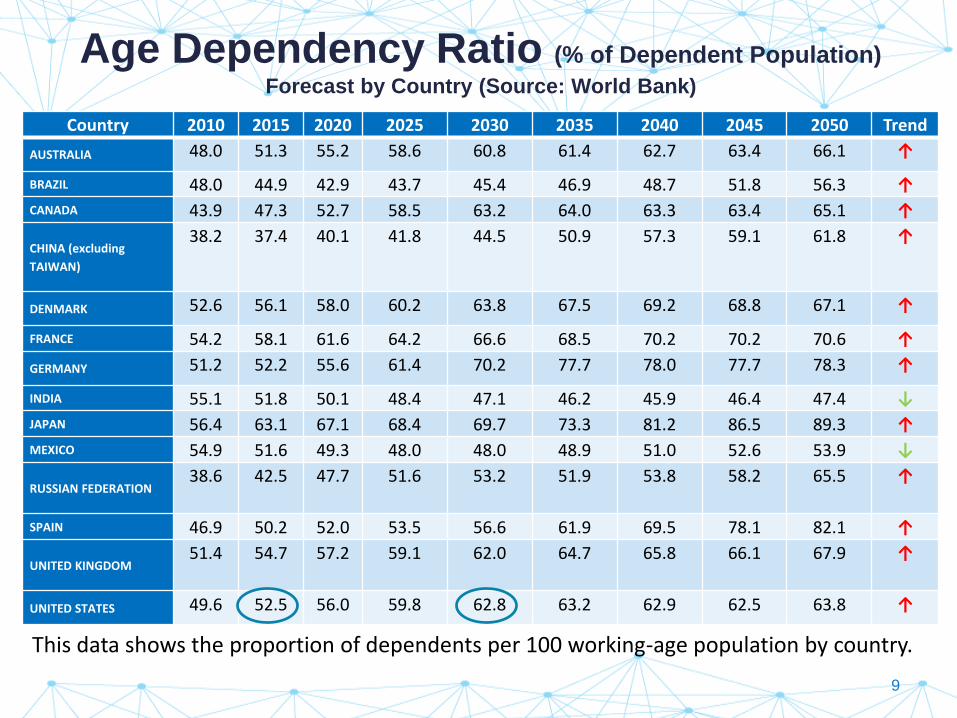

Age Dependency Ratio (% of Dependent Population)

Forecast by Country (Source: World Bank)

Country 2010 2015 2020 2025 2030 2035 2040 2045 2050 Trend

AUSTRALIA 48.0 51.3 55.2 58.6 60.8 61.4 62.7 63.4 66.1 ↑

BRAZIL 48.0 44.9 42.9 43.7 45.4 46.9 48.7 51.8 56.3 ↑

CANADA 43.9 47.3 52.7 58.5 63.2 64.0 63.3 63.4 65.1 ↑

CHINA (excluding

TAIWAN)

38.2 37.4 40.1 41.8 44.5 50.9 57.3 59.1 61.8 ↑

DENMARK 52.6 56.1 58.0 60.2 63.8 67.5 69.2 68.8 67.1 ↑

FRANCE 54.2 58.1 61.6 64.2 66.6 68.5 70.2 70.2 70.6 ↑

GERMANY 51.2 52.2 55.6 61.4 70.2 77.7 78.0 77.7 78.3 ↑

INDIA 55.1 51.8 50.1 48.4 47.1 46.2 45.9 46.4 47.4 ↓

JAPAN 56.4 63.1 67.1 68.4 69.7 73.3 81.2 86.5 89.3 ↑

MEXICO 54.9 51.6 49.3 48.0 48.0 48.9 51.0 52.6 53.9 ↓

RUSSIAN FEDERATION38.6 42.5 47.7 51.6 53.2 51.9 53.8 58.2 65.5 ↑

SPAIN 46.9 50.2 52.0 53.5 56.6 61.9 69.5 78.1 82.1 ↑

UNITED KINGDOM51.4 54.7 57.2 59.1 62.0 64.7 65.8 66.1 67.9 ↑

UNITED STATES 49.6 52.5 56.0 59.8 62.8 63.2 62.9 62.5 63.8 ↑

This data shows the proportion of dependents per 100 working-age population by country.

9

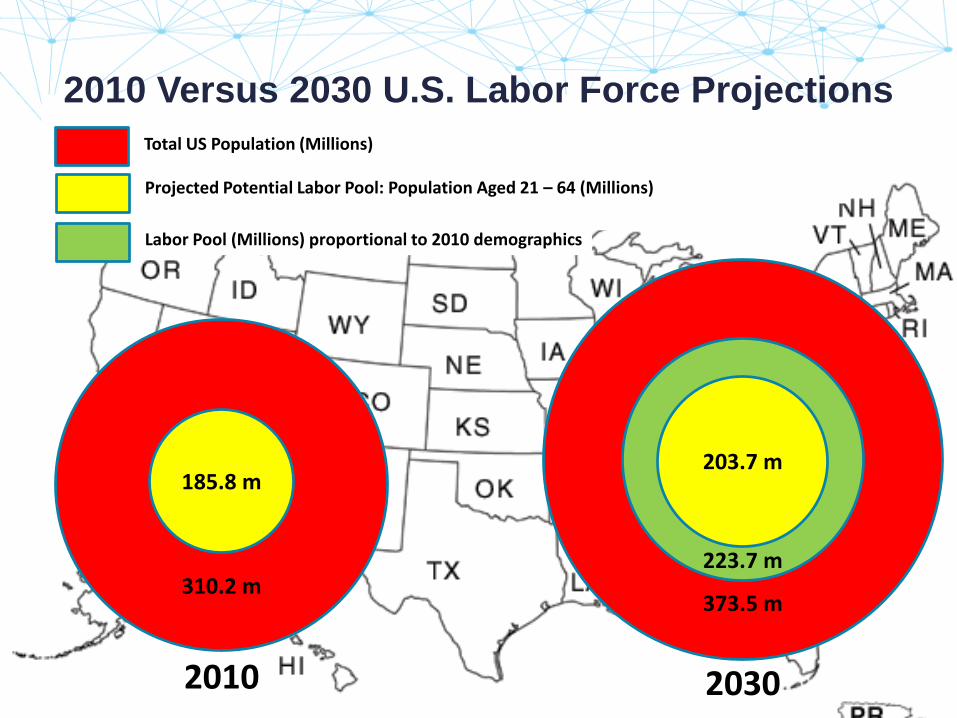

2010 Versus 2030 U.S. Labor Force Projections

310.2 m

2010

185.8 m

373.5 m

223.7 m

2030

203.7 m

Total US Population (Millions)

Projected Potential Labor Pool: Population Aged 21 – 64 (Millions)

Labor Pool (Millions) proportional to 2010 demographics

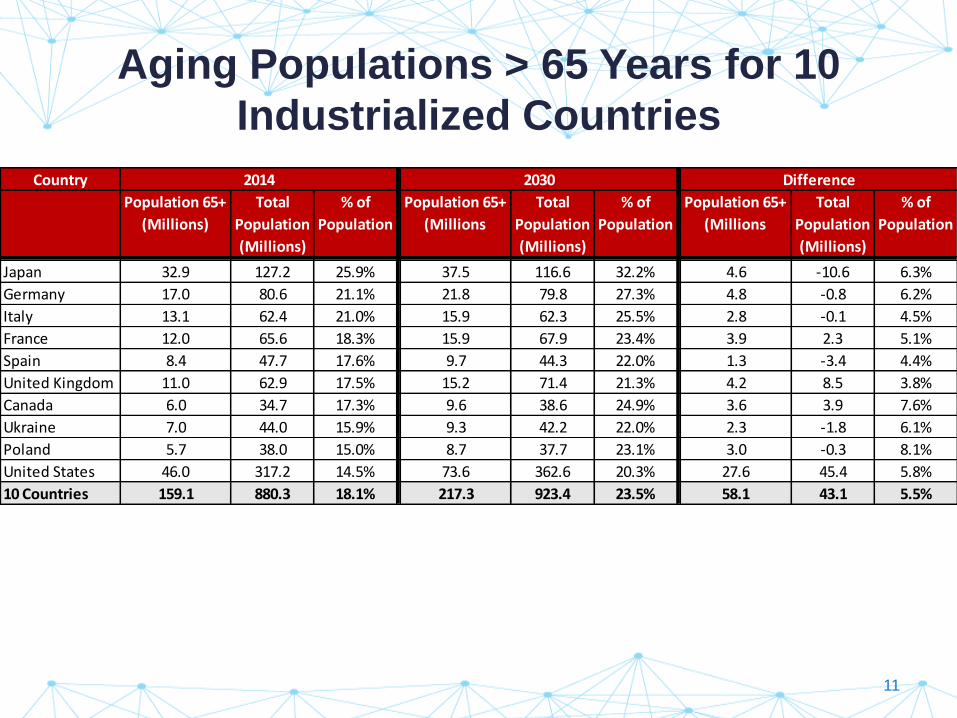

Aging Populations > 65 Years for 10

Industrialized Countries

Country

Population 65+

(Millions)

Total

Population

(Millions)

% of

Population

Population 65+

(Millions

Total

Population

(Millions)

% of

Population

Population 65+

(Millions

Total

Population

(Millions)

% of

Population

Japan 32.9 127.2 25.9% 37.5 116.6 32.2% 4.6 -10.6 6.3%

Germany 17.0 80.6 21.1% 21.8 79.8 27.3% 4.8 -0.8 6.2%

Italy 13.1 62.4 21.0% 15.9 62.3 25.5% 2.8 -0.1 4.5%

France 12.0 65.6 18.3% 15.9 67.9 23.4% 3.9 2.3 5.1%

Spain 8.4 47.7 17.6% 9.7 44.3 22.0% 1.3 -3.4 4.4%

United Kingdom 11.0 62.9 17.5% 15.2 71.4 21.3% 4.2 8.5 3.8%

Canada 6.0 34.7 17.3% 9.6 38.6 24.9% 3.6 3.9 7.6%

Ukraine 7.0 44.0 15.9% 9.3 42.2 22.0% 2.3 -1.8 6.1%

Poland 5.7 38.0 15.0% 8.7 37.7 23.1% 3.0 -0.3 8.1%

United States 46.0 317.2 14.5% 73.6 362.6 20.3% 27.6 45.4 5.8%

10 Countries 159.1 880.3 18.1% 217.3 923.4 23.5% 58.1 43.1 5.5%

2014 2030 Difference

11

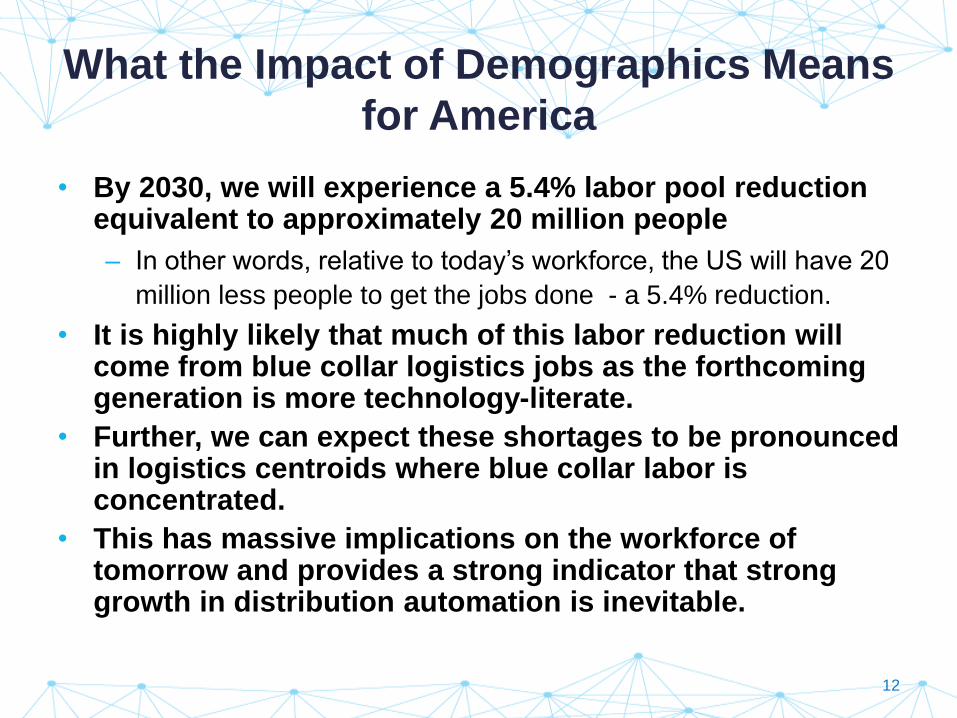

What the Impact of Demographics Means

for America

• By 2030, we will experience a 5.4% labor pool reduction equivalent to approximately 20 million people

– In other words, relative to today’s workforce, the US will have 20

million less people to get the jobs done - a 5.4% reduction.

• It is highly likely that much of this labor reduction will come from blue collar logistics jobs as the forthcoming generation is more technology-literate.

• Further, we can expect these shortages to be pronounced in logistics centroids where blue collar labor is concentrated.

• This has massive implications on the workforce of tomorrow and provides a strong indicator that strong growth in distribution automation is inevitable.

12

The Migration of Automation

from Europe to North America• Over the past 20 years,

automation has been slowly migrating from Europe to North America

– Western and Eastern European

Fast Moving Consumer Goods

(FMCG) companies have for many

years viewed automation as a

critical requirement to maintaining

competitive advantage due to the

high cost of labor and land.

– We now are witnessing the same

trend starting to take place in North

America

13

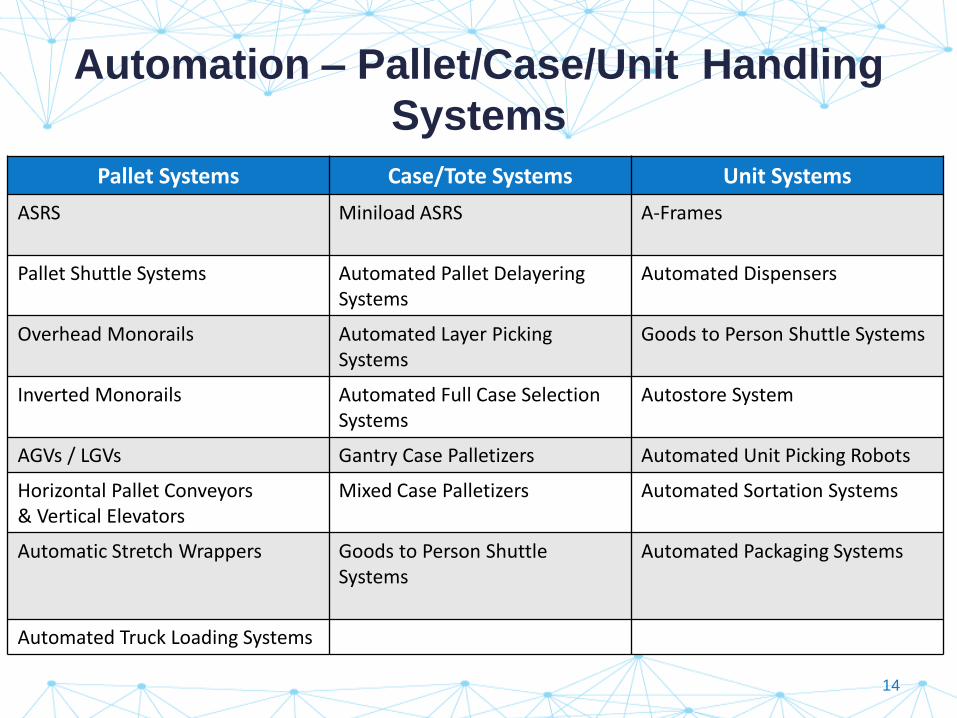

Automation – Pallet/Case/Unit Handling

Systems

Pallet Systems Case/Tote Systems Unit Systems

ASRS Miniload ASRS A-Frames

Pallet Shuttle Systems Automated Pallet Delayering Systems

Automated Dispensers

Overhead Monorails Automated Layer Picking Systems

Goods to Person Shuttle Systems

Inverted Monorails Automated Full Case Selection Systems

Autostore System

AGVs / LGVs Gantry Case Palletizers Automated Unit Picking Robots

Horizontal Pallet Conveyors& Vertical Elevators

Mixed Case Palletizers Automated Sortation Systems

Automatic Stretch Wrappers Goods to Person Shuttle Systems

Automated Packaging Systems

Automated Truck Loading Systems

14

North American Grocery Industry

• Research of the top 75 Grocery companies in North

America has yielded a detailed database of all

distribution centers for these companies that

represents over $1 Trillion of annual sales

15

North American Grocery Industry

• The North American grocery industry has traditionally been slow to embrace automated material handling systems due to the industry’s slim net margins that are typically in the range of 2.0% or less.

• In the 1980s, the top 75 North American grocery companies were almost exclusively operating with conventional distribution centers. Early attempts at automation and mechanization were largely being dismantled because the costs to operate equipment were higher than using manual labor.

• Fast forward to 2016 and we see a noticeable change in adoption rate taking place in an industry that has traditionally been very conservative.

16

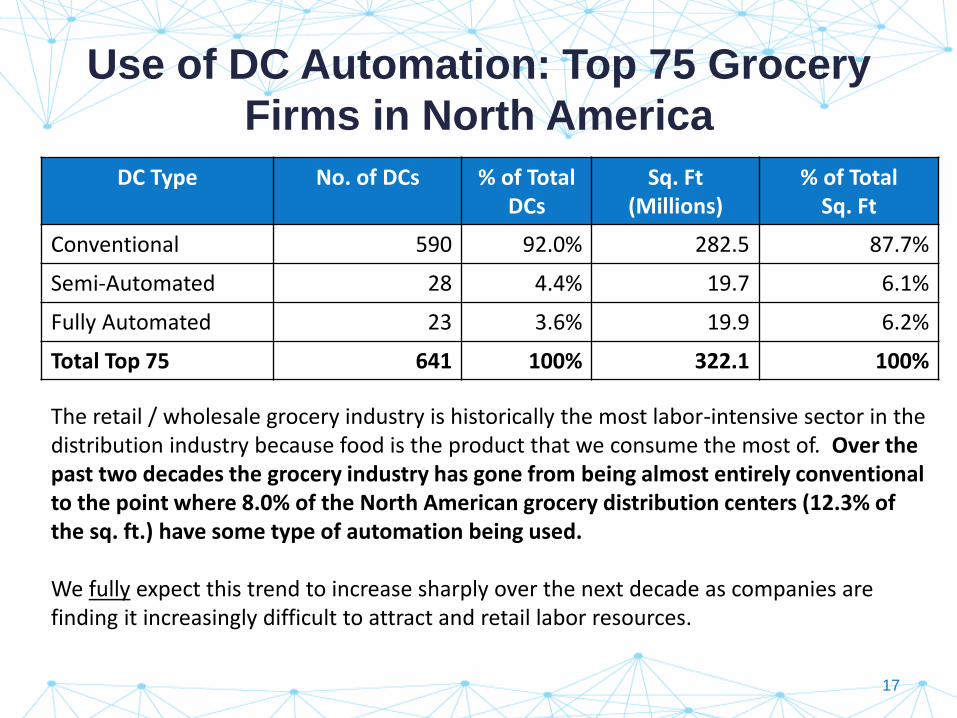

Use of DC Automation: Top 75 Grocery

Firms in North America

DC Type No. of DCs % of TotalDCs

Sq. Ft(Millions)

% of TotalSq. Ft

Conventional 590 92.0% 282.5 87.7%

Semi-Automated 28 4.4% 19.7 6.1%

Fully Automated 23 3.6% 19.9 6.2%

Total Top 75 641 100% 322.1 100%

The retail / wholesale grocery industry is historically the most labor-intensive sector in the distribution industry because food is the product that we consume the most of. Over the past two decades the grocery industry has gone from being almost entirely conventional to the point where 8.0% of the North American grocery distribution centers (12.3% of the sq. ft.) have some type of automation being used.

We fully expect this trend to increase sharply over the next decade as companies are finding it increasingly difficult to attract and retail labor resources.

17

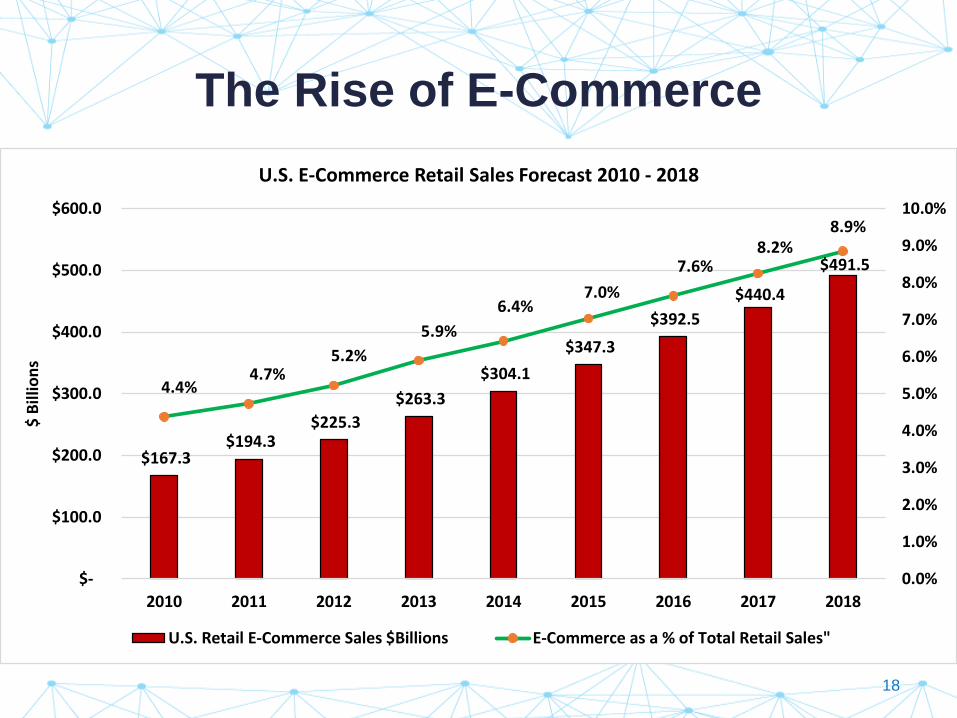

The Rise of E-Commerce

$167.3 $194.3

$225.3

$263.3

$304.1

$347.3

$392.5

$440.4

$491.5

4.4%4.7%

5.2%

5.9%

6.4%7.0%

7.6%8.2%

8.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

$-

$100.0

$200.0

$300.0

$400.0

$500.0

$600.0

2010 2011 2012 2013 2014 2015 2016 2017 2018

$ B

illio

ns

U.S. E-Commerce Retail Sales Forecast 2010 - 2018

U.S. Retail E-Commerce Sales $Billions E-Commerce as a % of Total Retail Sales"

18

Amazon Fulfillment & Sortation Center

Facilities in North America

19

2 2 8 9 9 7 8 8 12 13 18

22 24 27

38 46

58

67

82

106 114

-

20

40

60

80

100

120

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Amazon Fulfilment Distribution Centers in North America

Amazon Fulfilment Centers

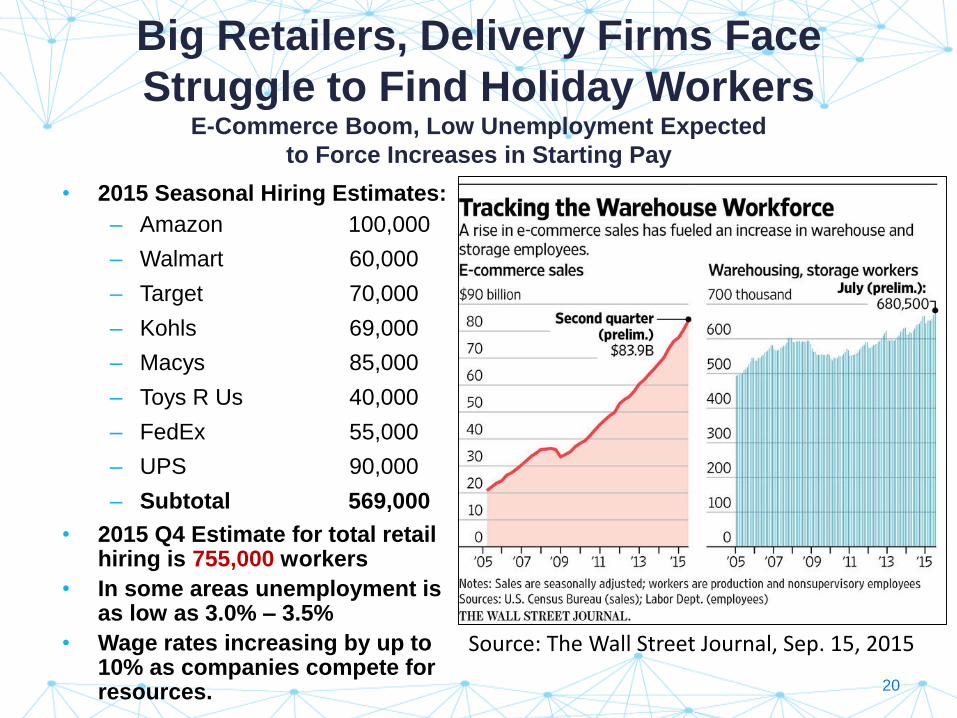

Big Retailers, Delivery Firms Face

Struggle to Find Holiday WorkersE-Commerce Boom, Low Unemployment Expected

to Force Increases in Starting Pay

• 2015 Seasonal Hiring Estimates:

– Amazon 100,000

– Walmart 60,000

– Target 70,000

– Kohls 69,000

– Macys 85,000

– Toys R Us 40,000

– FedEx 55,000

– UPS 90,000

– Subtotal 569,000

• 2015 Q4 Estimate for total retail hiring is 755,000 workers

• In some areas unemployment is as low as 3.0% – 3.5%

• Wage rates increasing by up to 10% as companies compete for resources.

Source: The Wall Street Journal, Sep. 15, 2015

20

Growth in E-Commerce is Driving Growth

in Automation

• Amazon is the driving force behind growth in the

e-commerce sector

• At least 40 of Amazon’s fulfillment centers in the

USA have 1,000+ people working inside the building

• Handling of retail units is extremely labor intensive

so as e-commerce grows the demand for more

warehouse and trucking labor will increase

disproportionately faster

• This trend will further increase the demand for

automation technologies

21

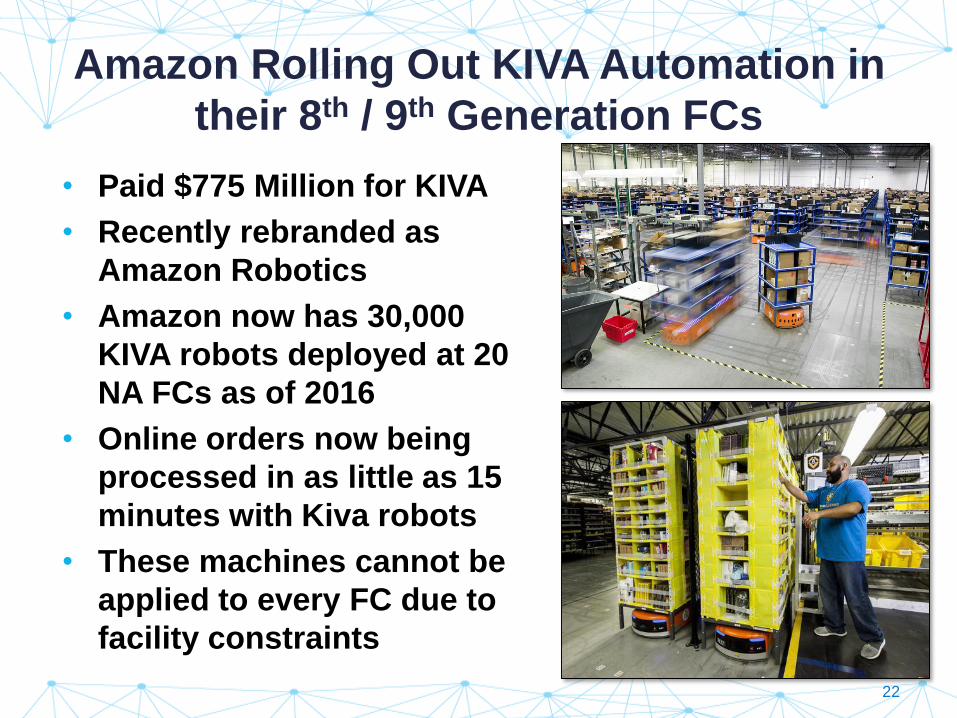

Amazon Rolling Out KIVA Automation in

their 8th / 9th Generation FCs

• Paid $775 Million for KIVA

• Recently rebranded as

Amazon Robotics

• Amazon now has 30,000

KIVA robots deployed at 20

NA FCs as of 2016

• Online orders now being

processed in as little as 15

minutes with Kiva robots

• These machines cannot be

applied to every FC due to

facility constraints

22

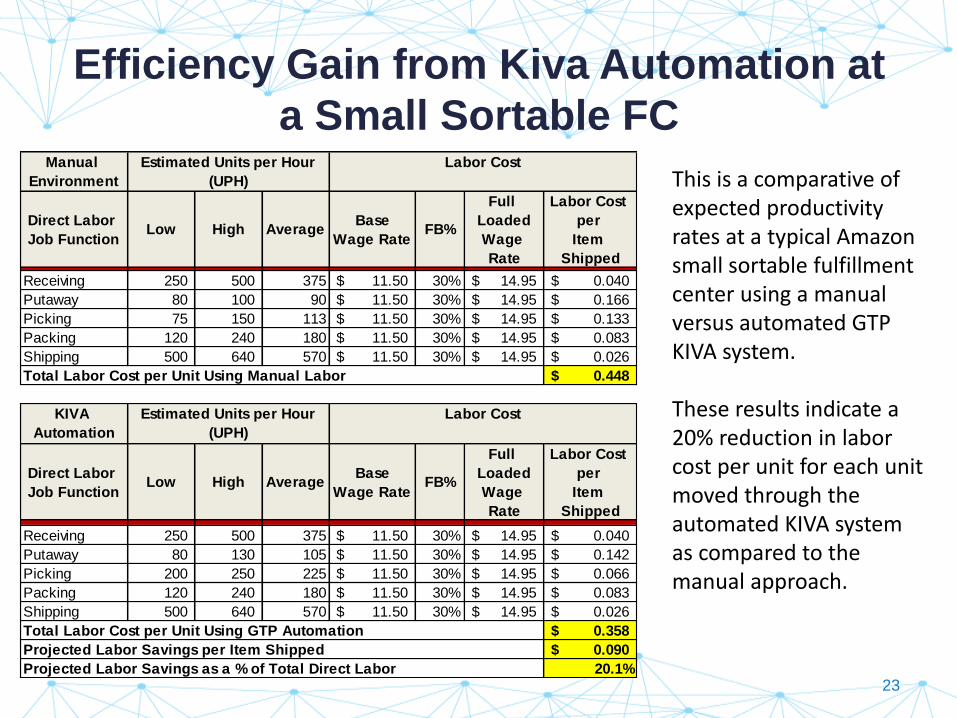

Efficiency Gain from Kiva Automation at

a Small Sortable FC

This is a comparative of expected productivity rates at a typical Amazon small sortable fulfillment center using a manual versus automated GTP KIVA system.

These results indicate a 20% reduction in labor cost per unit for each unit moved through the automated KIVA system as compared to the manual approach.

Manual

Environment

Direct Labor

Job FunctionLow High Average

Base

Wage RateFB%

Full

Loaded

Wage

Rate

Labor Cost

per

Item

Shipped

Receiving 250 500 375 11.50$ 30% 14.95$ 0.040$

Putaway 80 100 90 11.50$ 30% 14.95$ 0.166$

Picking 75 150 113 11.50$ 30% 14.95$ 0.133$

Packing 120 240 180 11.50$ 30% 14.95$ 0.083$

Shipping 500 640 570 11.50$ 30% 14.95$ 0.026$

0.448$

KIVA

Automation

Direct Labor

Job FunctionLow High Average

Base

Wage RateFB%

Full

Loaded

Wage

Rate

Labor Cost

per

Item

Shipped

Receiving 250 500 375 11.50$ 30% 14.95$ 0.040$

Putaway 80 130 105 11.50$ 30% 14.95$ 0.142$

Picking 200 250 225 11.50$ 30% 14.95$ 0.066$

Packing 120 240 180 11.50$ 30% 14.95$ 0.083$

Shipping 500 640 570 11.50$ 30% 14.95$ 0.026$

0.358$

0.090$

20.1%

Total Labor Cost per Unit Using GTP Automation

Projected Labor Savings per Item Shipped

Projected Labor Savings as a % of Total Direct Labor

Estimated Units per Hour

(UPH)

Labor Cost

Total Labor Cost per Unit Using Manual Labor

Estimated Units per Hour

(UPH)

Labor Cost

23

Concluding Thoughts

• More than ever before, companies are investing

capital into automated material handling for reasons

other than pure ROI. This is a strong departure from

traditional behavior which is driven by:

– Strong impetus to be technologically advanced as a

competitive advantage

– Need to handle future throughput and growth with less

reliance on human labor

– Desire to stay ahead of the market and be in a position of

strength as the pending labor pool shortage becomes an

increasing issue for North American companies,

particularly in the logistics industry.

24

ROI Panel Discussion

25

Key Takeaways

26

• North American companies are already having a tough time attracting and retaining people to work for their logistics and distribution operations.

• The North American labor shortage issue is starting to impact distributors and retailers.

• Growth in e-commerce is adding fuel to the fire.

• North America is starting to look like Europe 20 years ago when automation started to become the ‘norm’.

• Changing demographics will drive major growth in the North American automated material handling industry and the automation of unit/piece handling will be in significant demand due as companies look for ways to reduce their reliance on labor, particularly in the retail e-commerce sector.

Conference Cloud

27

• Get from RICH

RODGERS

Additional Resources

Questions?

![[INFOGRAPHIC] ROI](https://img.pdfslide.us/doc/110x75/5400af278d7f728b408b49aa/infographic-roi.jpg)