Embed Size (px)

Citation preview

1Confidential

Mark Tyler

PRACTICAL DEBT FINANCING

STRUCTURES, SOURCES AND AVAILABILITY

2Confidential

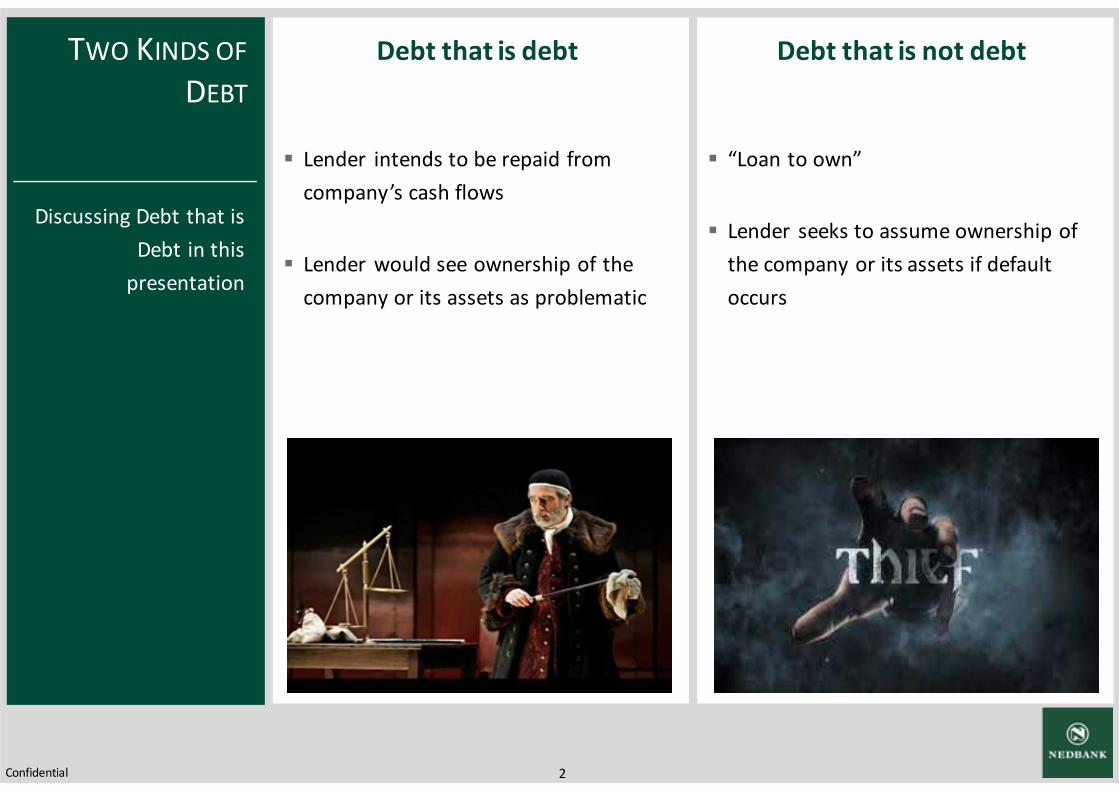

Debt that is not debt

� “Loan to own”

� Lender seeks to assume ownership of

the company or its assets if default

occurs

Debt that is debt

� Lender intends to be repaid from

company’s cash flows

� Lender would see ownership of the

company or its assets as problematic

Discussing Debt that is

Debt in this

presentation

TWO KINDS OF

DEBT

3Confidential

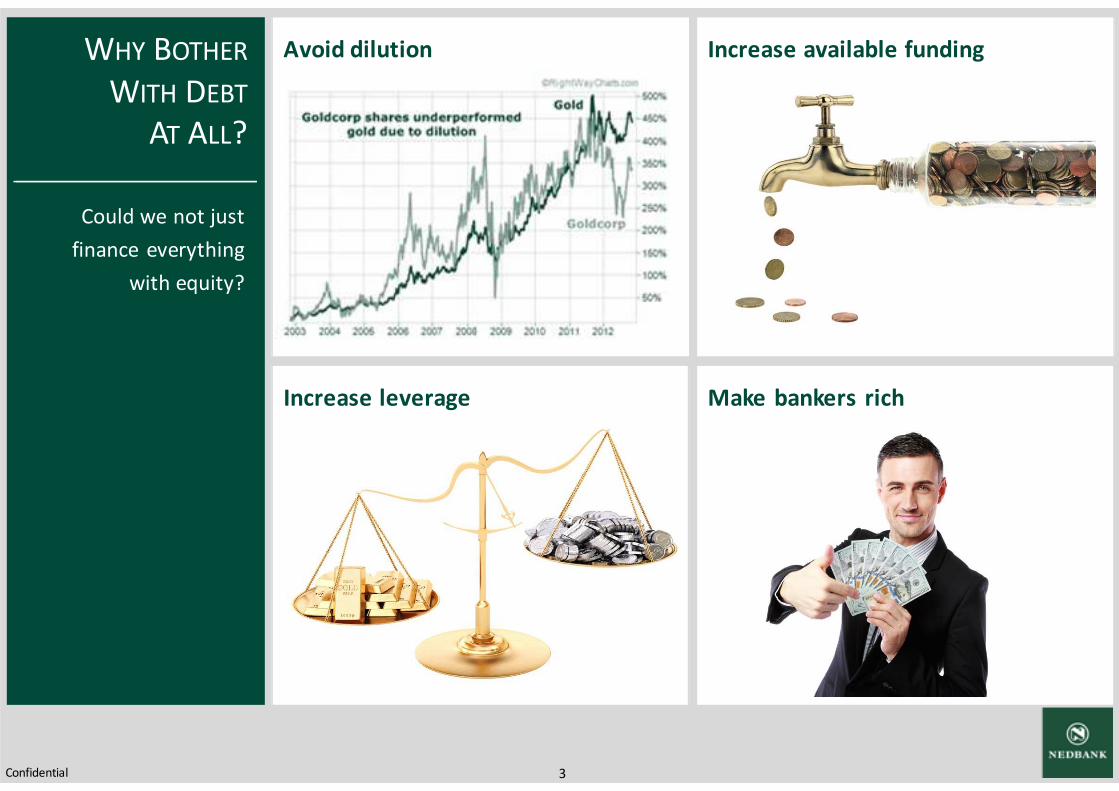

Make bankers richIncrease leverage

Increase available fundingAvoid dilution

Could we not just

finance everything

with equity?

WHY BOTHER

WITH DEBT

AT ALL?

4Confidential

� Ranks ahead of equity

� Generally (but not always) has a fixed term

� Generally has a more or less fixed interest rate

� Can have embellishments

� Should cost less than equity

CHARACTERISTICS

OF DEBT

5Confidential

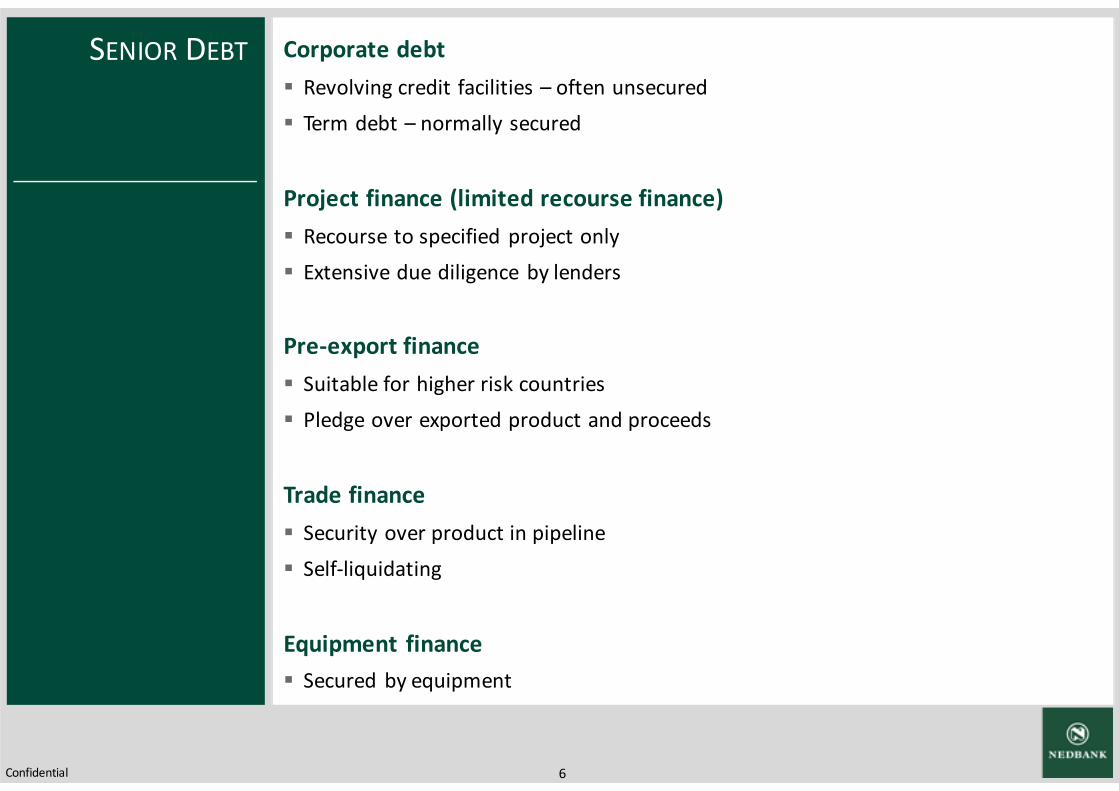

SENIOR DEBT

6Confidential

Corporate debt

� Revolving credit facilities – often unsecured

� Term debt – normally secured

Project finance (limited recourse finance)

� Recourse to specified project only

� Extensive due diligence by lenders

Pre-export finance

� Suitable for higher risk countries

� Pledge over exported product and proceeds

Trade finance

� Security over product in pipeline

� Self-liquidating

Equipment finance

� Secured by equipment

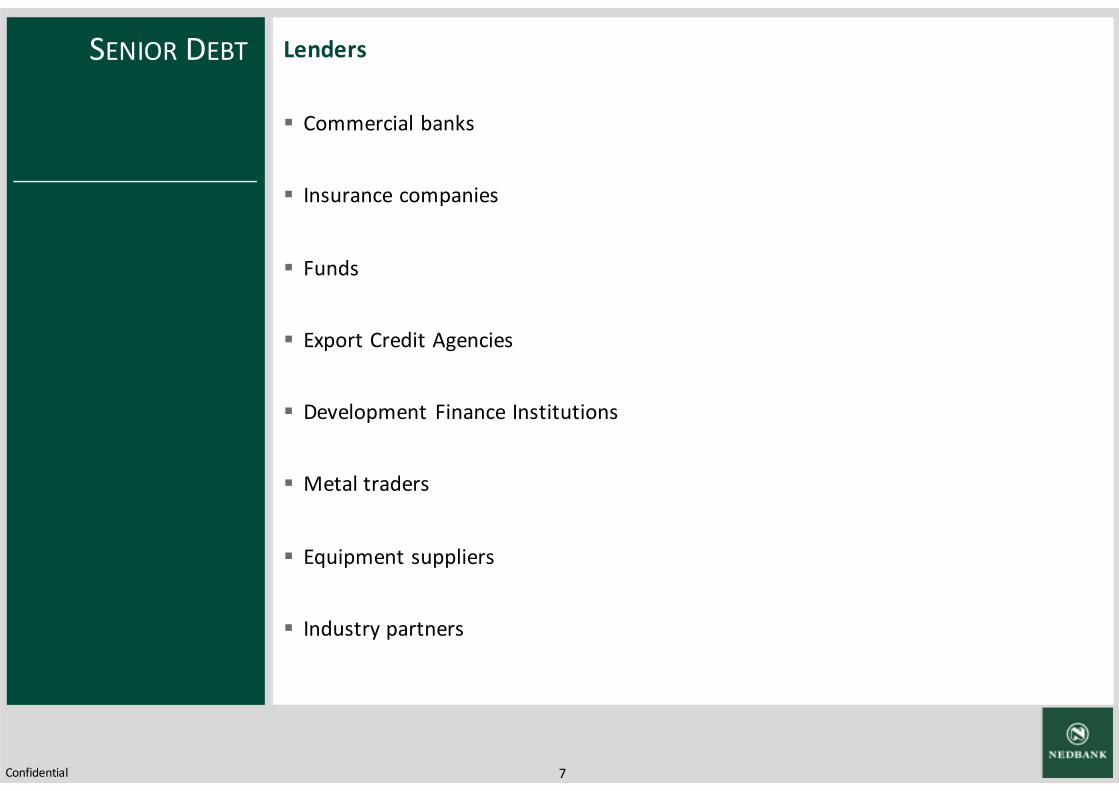

SENIOR DEBT

7Confidential

Lenders

� Commercial banks

� Insurance companies

� Funds

� Export Credit Agencies

� Development Finance Institutions

� Metal traders

� Equipment suppliers

� Industry partners

SENIOR DEBT

8Confidential

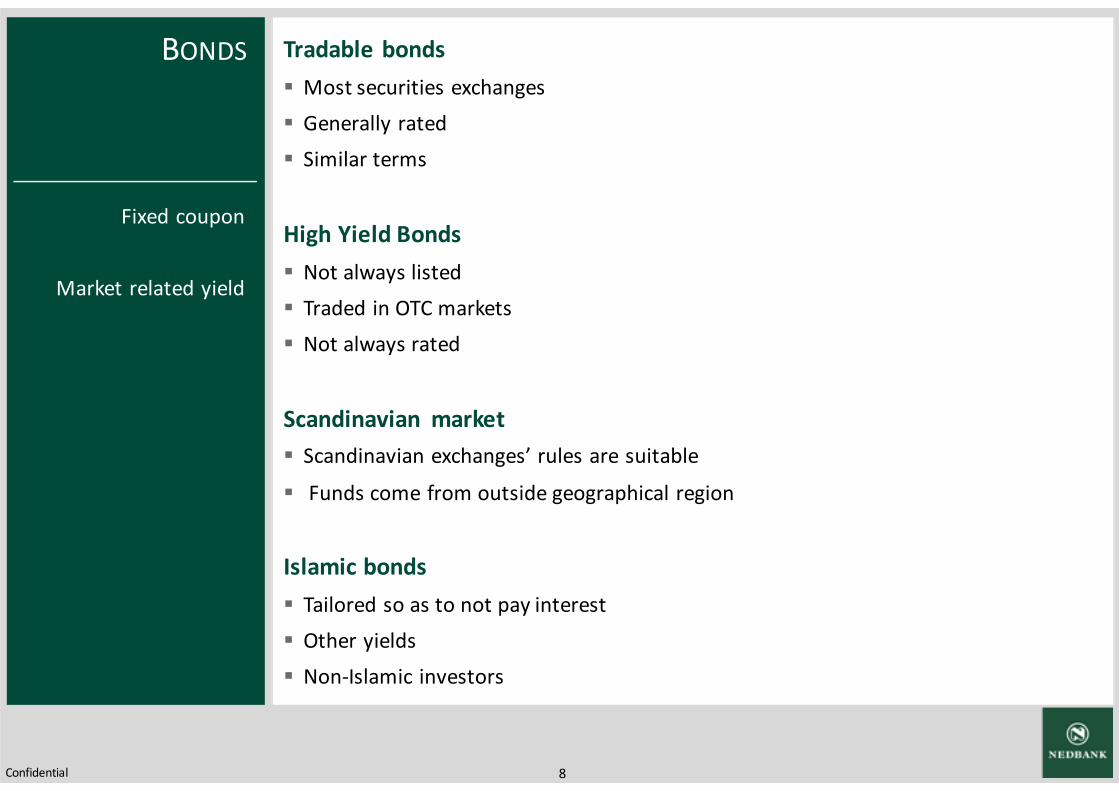

Tradable bonds

� Most securities exchanges

� Generally rated

� Similar terms

High Yield Bonds

� Not always listed

� Traded in OTC markets

� Not always rated

Scandinavian market

� Scandinavian exchanges’ rules are suitable

� Funds come from outside geographical region

Islamic bonds

� Tailored so as to not pay interest

� Other yields

� Non-Islamic investors

Fixed coupon

Market related yield

BONDS

9Confidential

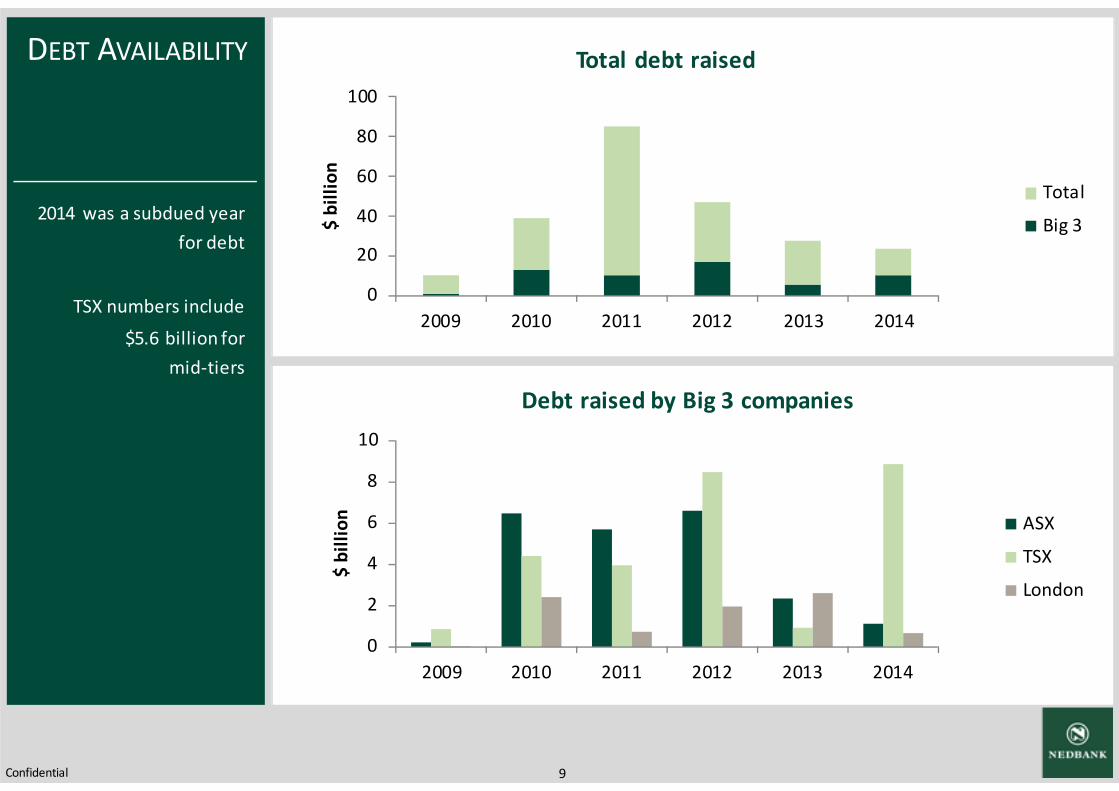

DEBT AVAILABILITY

0

2

4

6

8

10

2009 2010 2011 2012 2013 2014

$ b

illi

on

Debt raised by Big 3 companies

ASX

TSX

London

0

20

40

60

80

100

2009 2010 2011 2012 2013 2014$

bil

lio

n

Total debt raised

Total

Big 32014 was a subdued year

for debt

TSX numbers include

$5.6 billion for

mid-tiers

10Confidential

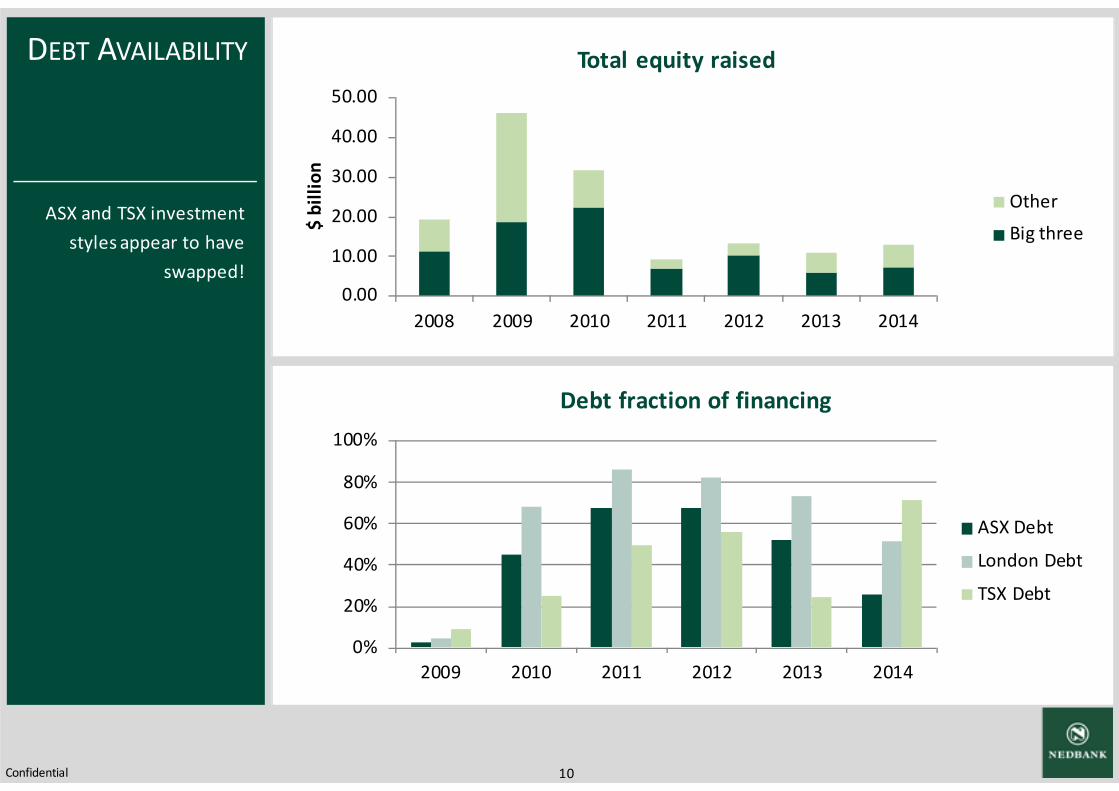

DEBT AVAILABILITY

0.00

10.00

20.00

30.00

40.00

50.00

2008 2009 2010 2011 2012 2013 2014$

bil

lio

n

Total equity raised

Other

Big three

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014

Debt fraction of financing

ASX Debt

London Debt

TSX Debt

ASX and TSX investment

styles appear to have

swapped!

11Confidential

CONVERTIBLE SECURITIES

12Confidential

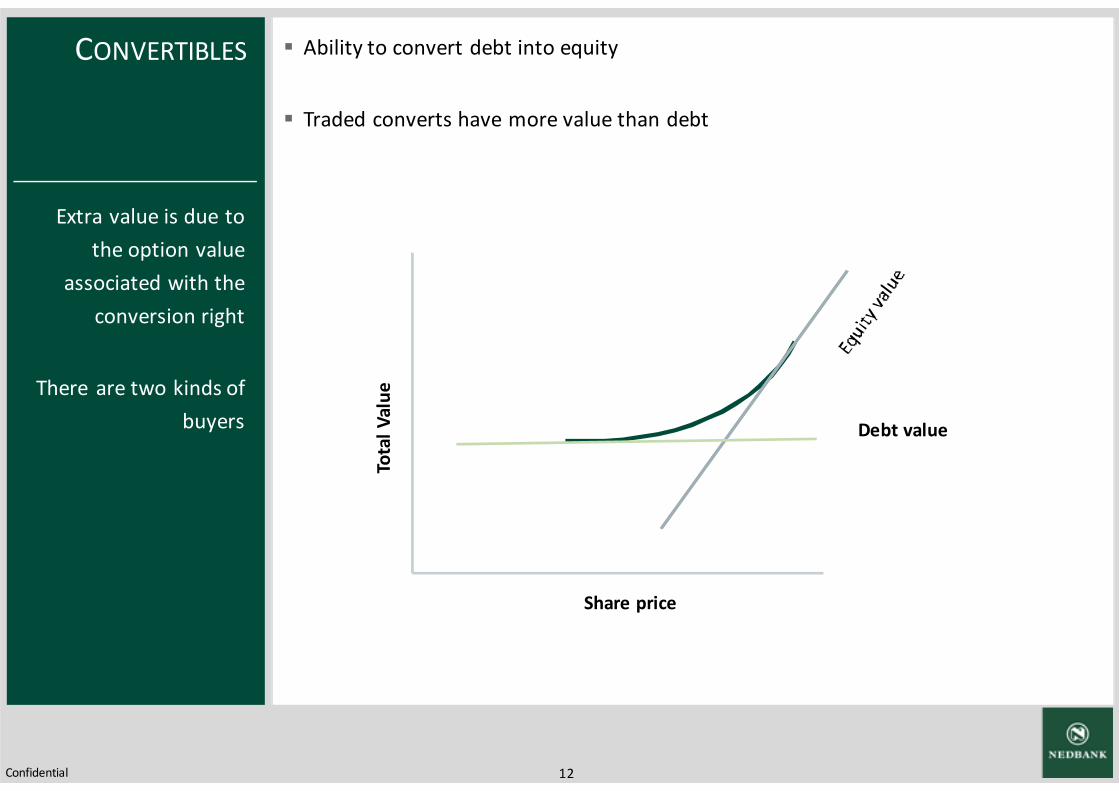

� Ability to convert debt into equity

� Traded converts have more value than debt

Extra value is due to

the option value

associated with the

conversion right

There are two kinds of

buyers

CONVERTIBLES

Debt value

Share price

Tota

l V

alu

e

13Confidential

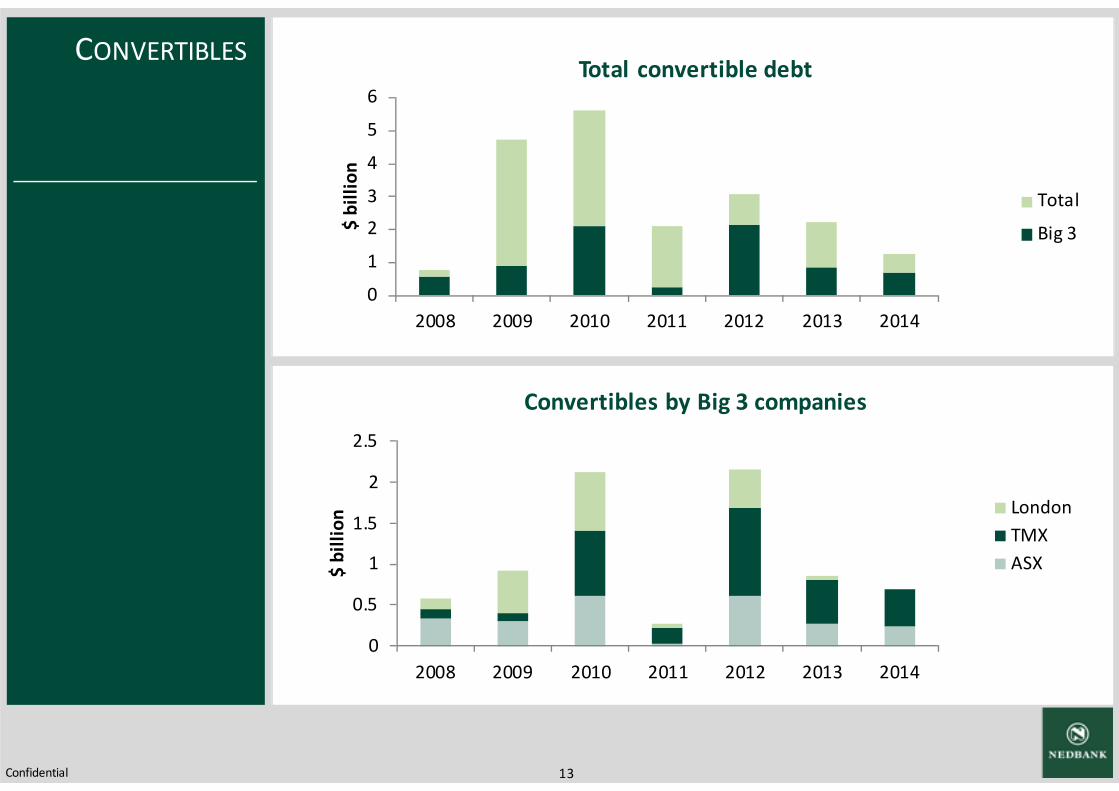

CONVERTIBLES

0

1

2

3

4

5

6

2008 2009 2010 2011 2012 2013 2014

$ b

illi

on

Total convertible debt

Total

Big 3

0

0.5

1

1.5

2

2.5

2008 2009 2010 2011 2012 2013 2014

$ b

illi

on

Convertibles by Big 3 companies

London

TMX

ASX

14Confidential

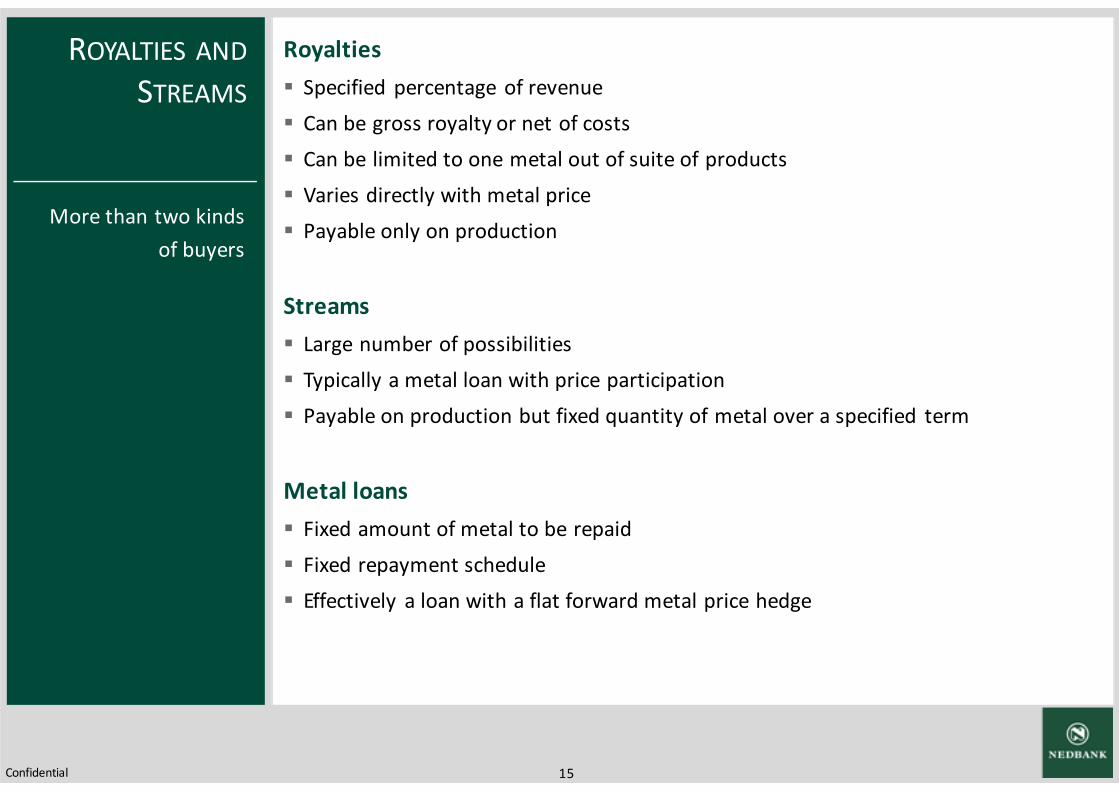

ROYALTIES AND STREAMS

15Confidential

Royalties

� Specified percentage of revenue

� Can be gross royalty or net of costs

� Can be limited to one metal out of suite of products

� Varies directly with metal price

� Payable only on production

Streams

� Large number of possibilities

� Typically a metal loan with price participation

� Payable on production but fixed quantity of metal over a specified term

Metal loans

� Fixed amount of metal to be repaid

� Fixed repayment schedule

� Effectively a loan with a flat forward metal price hedge

More than two kinds

of buyers

ROYALTIES AND

STREAMS

16Confidential

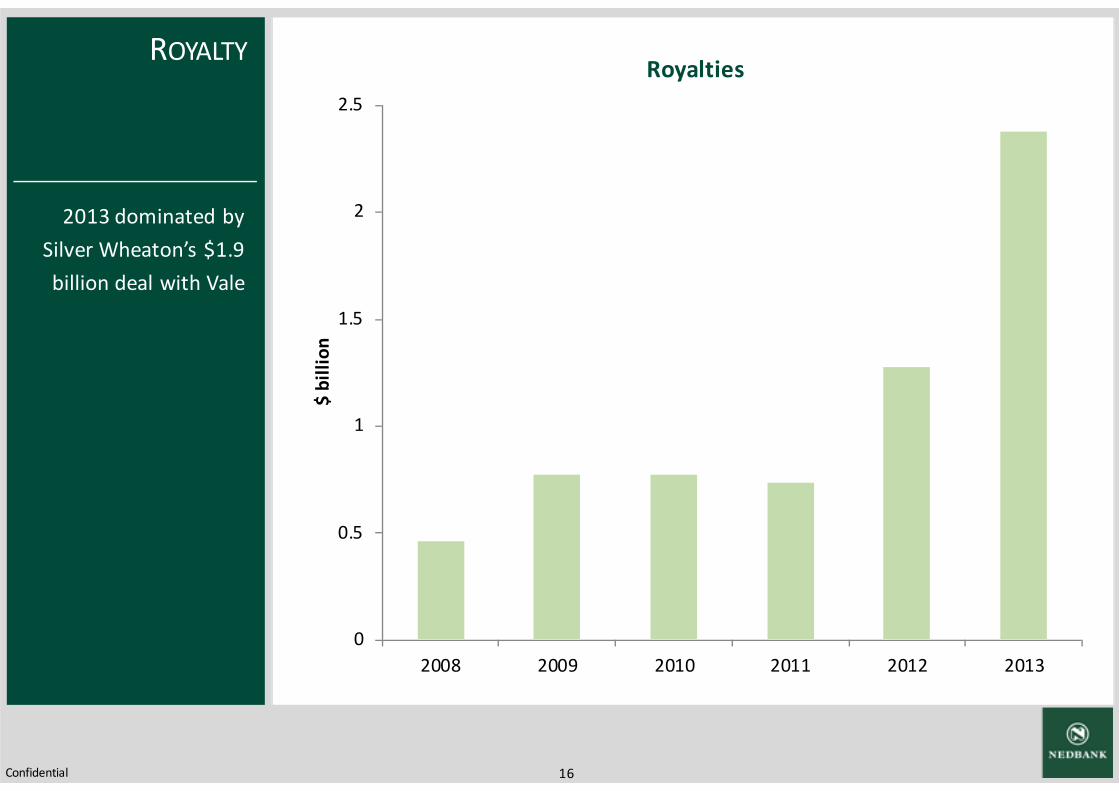

2013 dominated by

Silver Wheaton’s $1.9

billion deal with Vale

ROYALTY

0

0.5

1

1.5

2

2.5

2008 2009 2010 2011 2012 2013

$ b

illi

on

Royalties

17Confidential

SUMMARY AND OUTLOOK

18Confidential

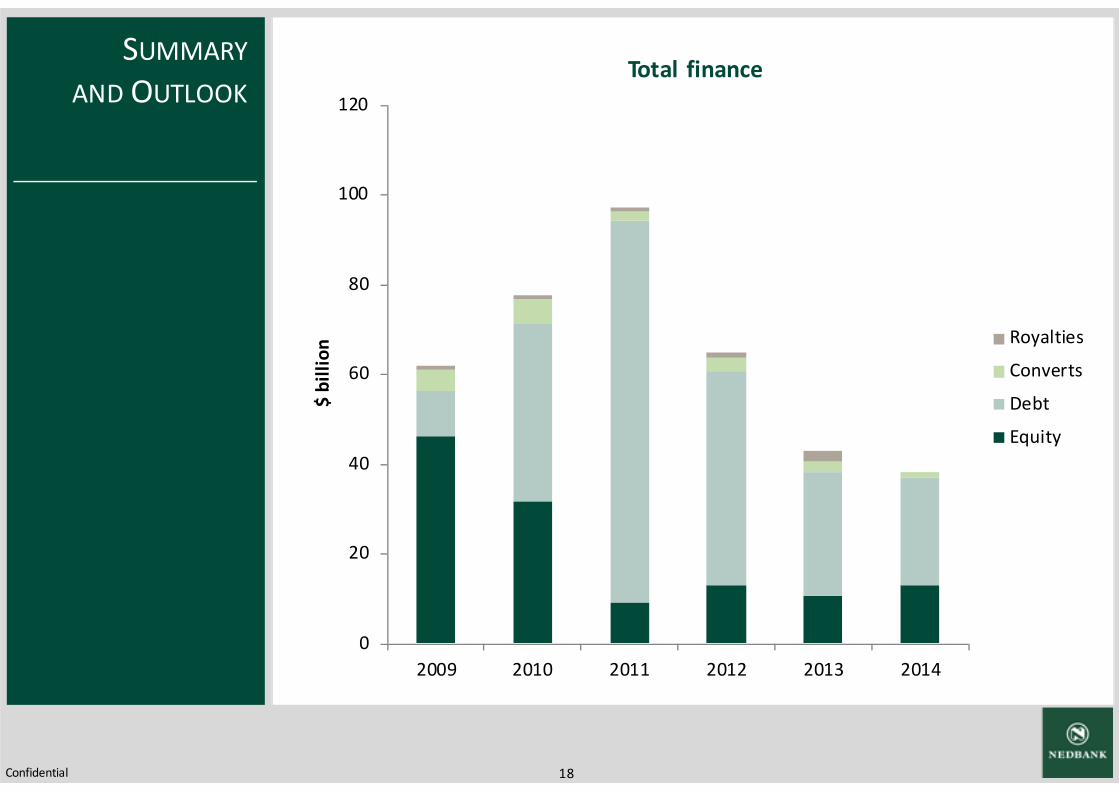

SUMMARY

AND OUTLOOK

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014

$ b

illi

on

Total finance

Royalties

Converts

Debt

Equity

19Confidential

Debt becomes relatively more attractive in tough equity markets

Banks and other lenders have liquidity and are seeking investments

Debt availability for producers is high

Debt availability for developers is limited by equity availability

Good producers and good developers will get funding

SUMMARY

AND OUTLOOK

20Confidential

THANK YOU