-

COPYRIGHT 2002 PRINCIPIA PARTNERS

Inside this Issue...

Natural fiber composites seegrowing use in autos Page 2

Auto build rates expected torebound in 2002 Page 2

EPA and wood treaters agree toeliminate CCA Page 3

Retailers prepared to sellalternative materials Page 3

Treaters ready to switch to CCAalternatives Page 4

Marth starts second wood fiberplant Page 4

News from the InternationalBuilders Show Page 5

AERT secures Lowes deckingbusiness Page 6

Events calendar Page 6

Principia Partners completesstudy of additives Page 7

In the next Issue...

Additives suppliers deliverinnovation to boostperformance and

lower cost...

Housing starts and the impacton demand for woodcomposites...

Natural and wood fibercomposites expanding intooutdoor living

accessories...

NATURAL & WOOD FIBER COMPOSITESNATURAL & WOOD FIBER

COMPOSITESFebruary 27, 2002 Volume I, Number 2

Automakers Driving Use of Natural Fibers Increasingly Replacing

Mineral and Glass Polypropylene

The use of natural fiber composites in automobiles is not

new-Henry Fordbegan using the materials in interior applications in

the early 1930s. Today,automotive OEMs and the major Tier 1

producers are working hard to harnessthe advantages that natural

fibers offer and put them to new uses.

Natural fiber-based polymer composites are proving to offer much

more than ameans for automakers to demonstrate the use of

eco-friendly materials. Theyare realizing the added benefits of

weight reduction, while offering goodmechanical properties

previously seen only in mineral-filled plastics or

glassfiber-reinforced composites. The natural materials are

delivering as much as25% improvement in strength and flex modulus

compared to some of theincumbents used over the past 20 years.

Demand for natural fiber composites in the transportation market

has increasedfrom 6 million lb in 1998 to nearly double the volume

in 2001. PrincipiaPartners projects that the demand will increase

to 32 million lb by 2003 asmore car platforms implement the use of

parts designed in the late 1990s.

Parts that will experience the most growth in usage of these

materials includeinstrument panels, door panels, bootliners, parcel

shelves, dashboards andother interior trim. Designers are

alsobeginning to work on exterior partsfor underhood and underbody

of thecar. For example, DaimlerChryslerwill equip the new

Mercedes-BenzTravego travel coach with a naturalfiber-reinforced

engine andtransmission cover as standardequipment, the first

natural fiber-reinforced exterior vehicle componentto go into

production.

The choice and preference of natural fibers differs somewhat

among theautomakers. However, all automakers are investigating the

advantages anddisadvantages of these materials. Ford has focused

its work on bast fibersincluding hemp, jute, ramie, and flax.

DaimlerChrysler has focused its effortson flax and sisal fiber in

polyurethane resins. A continued concern is thevariation in

material consistency. New fiber processing technology tominimize

the variation continues to be developed.

Next-generation development goals will drive the use of

co-mingled fibersystems. Natural fibers will be used in conjunction

with glass and othersynthetics to tune the thermal and acoustic

performance of interior parts. Forecasts indicate that vehicles

made in the U.S. in model year 2006 willconsume 50 million lb of

natural fiber composites.

-

Vol. 1, No. 2/Page 2 NATURAL & WOOD FIBER COMPOSITESNATURAL

& WOOD FIBER COMPOSITES February 27, 2002

COPYRIGHT 2002 PRINCIPIA PARTNERS

NATURAL & WOOD FIBER COMPOSITESNATURAL & WOOD FIBER

COMPOSITES

For Subscription or Editorial inquiries:James T. Morton,

EditorP.O. Box 611Exton, PA 19341717-741-3565; 484-214-0172

(Fax);[email protected]

Natural & Wood Fiber Composites is published 12 times ayear

by Principia Partners. World rate is US$700; discountavailable for

electronic delivery. A subscription entitlesreaders to share this

newsletter with any colleagues at thesame physical address. Please

contact publisher foradditional off-site subscriptions.

Publisher and Editor-in-chief James MortonCopyright 2002

Principia Partners All Rights Reserved.

www.principiaconsulting.com

Auto Industry News

Auto Parts Use Natural SolutionStrong Growth Expected to

Continue in 2002

Leading parts producers are excited about the strongautomotive

sales forecast and the greater number ofprograms implementing

natural fiber composites.

Flexform Technologies (Elkhart, IN), formerly

KafusBio-Composites, a leading producer of composite

sheetexperienced significant growth in 2001, with salesdoubling

since 2000. It expects additional growth of75% in 2002. Flexform is

in the process of expandingits plant from the original 55,000 SF to

nearly 150,000SF in 2002. The greater manufacturing capability

willenable it to support and grow its programs with leadinginterior

parts manufacturers like Findlay, JCI, andVisteon. The company is

working with Delphi andJapanese and European Transplant suppliers

as well.

JCI (Holland, MI) purchases sheets of long fiber hempand kenaf

reinforced PP which it uses to compressionmold interior parts.

Larry Cross, JCIs Sales Managersays, The use of natural fiber

composites in Daimler-Chryslers 2001 Sebring convertible has been

asuccessful program as a door trim panel part. Thissuccess has lead

us to using the material in instrumentpanel parts for the GM Saturn

2002 SUV..

JCI also continues to work with wood fiber compositesin its

Battle Creek, MI facility for parts includingpurse/map shelves and

door trim. Its joint venturecompany with Toyota, Trim Masters

(Harrodsburg, KY)works with both wood and natural fiber based

products. Mr. Cross states, No new wood fiber compositeprograms are

underway, but evaluation in other naturalfiber composite parts for

various automakers is ongoingat both the MI and KY facilities.

Harry Hickey, Flexforms Sales and MarketingManager, states Our

growth has required us to obtainkenaf fiber from crop fields

outside of Texas. We haverecently secured additional crop fields in

NorthCarolina.

Flexform is remaining focused at this time on kenaf andhemp. It

has not commercialized flax fiber, butperiodically will use jute

fiber. The company has alsobegun to introduce compounded sheet for

exteriorpanels and other parts for the RV and furniture

partsindustries.

Flexform: Harry Hickey, 574/295-3777JCI: Larry Cross,

616/392-5151

Automakers Cautiously Optimistic2002 Sales Rebounding

GM and Ford are raising U.S. automotive sales forecastsfor 2002

on the strength of continuing consumerconfidence. Economists from

General Motors and Fordare optimistic that the recession is over.

G. MustafaMohatarem, GMs chief economist says, We clearlyseem to

have a global recovery under way with theUnited States leading.

Economic indicators suggest thedeveloping strength of the U.S.

economy can besustained throughout calender year 2002.

Overall, the Big 3 producers are increasing their industrysales

forecasts to 15.7 to 15.8 million light vehicles. This revised

forecast is 1 million vehicles greater thanthe 14.7 million level

expected in November.

In contrast, Japans new vehicle sales have continued

toexperience a weak start in 2002. Japans shakyconsumer confidence

and high unemployment (highestin 45 years) are reflected in poor

domestic sales by 4 ofthe 5 automakers. Honda is the only strong

gainer, witha nearly 15% rise in Japanese sales in January.

After fairing well in 2001, new vehicle sales haveexperienced

drop in Western Europe, mainly weigheddown by weakness in Germany

and Italy. However,automakers in this region remain bullish about

theexpected years sales reaching at least 15.5 million units.

Southeast Asia remains a bright star for continuedgrowth. New

vehicle sales in the four largest markets ofSoutheast Asia freached

a record 2001 level of nearly1.1 million units.

The continued strength of the global automotive industrywill

positively impact the demand for natural-fibercomposites.

GM: G. Mustafa Mohaterem, 313/556-5000

-

February 27, 2002 NATURAL & WOOD FIBER COMPOSITESNATURAL

& WOOD FIBER COMPOSITES Vol. 1, No. 2/Page 3

COPYRIGHT 2002 PRINCIPIA PARTNERS

Regulatory/Testing

EPA to Amend Registration for CCAAlternatives to be Phased in

through Dec 2003

Early this month, the three domestic manufacturers ofchromated

copper arsenate (CCA) requested the EPA tomodify their materials

registrations to exclude manyresidential applications of

CCA-treated wood, includingplayground equipment, decks, and

landscape timbers.

The request came as a result of months of negotiationsbetween

the EPA and the producers of the pesticide,which has been used for

50 years to treat wood. The useof CCA for these applications will

be phased out byDecember 31, 2003, while use for various

industrialapplications, such as guardrail components, utility

poles,and pilings, will continue.

The producers initiated the talks in response to

mountingpressure from environmentalists who fear that thepotential

for arsenic, a known human carcinogen, toleach out from treated

wood puts children at risk ofdeveloping cancer. The EPA noted that

it has notconcluded thatarsenic-treatedwood, whichtypicallycontains

2 lbof CCA per100 bd-ft,posesunreasonablerisks to thepublic.

Thehazard associated with arsenic is well known, saidSteve Johnson,

head of the EPA's pesticide office. Butthe issue for CCA-treated

lumber is: Are children beingexposed to the materials in

CCA-treated lumber? At thispoint we don't know.

The agency, which banned most uses of inorganicarsenic

pesticides in 1984, will publish a preliminaryrisk assessment in

2003 after it has completed testing ofthe product.

The agreement applies to all forms of

arsenic-containingpreservatives, including chromate copper

arsenate(CCA), ammoniacal copper arsenate (ACA) andammoniacal

copper zinc arsenate (ACZA). CCArepresents 95% of the preservative

market volume. Therecent voluntary action by CCA producers in the

UnitedStates follows similar actions in Switzerland, Vietnamand

Indonesia. Other countries have also limited the useof CCA in

treating wood, including Japan, Denmark,Sweden, Germany, Australia

and New Zealand.

This voluntary change came after years of pressure fromthe

Environmental Working Group and the HealthyBuilding Network to ban

the use of CCA-treated woodfor playground equipment. Florida and

Californialegislatures have considered several bills since 2000

tolimit or ban the use of CCA-treated wood in waterfrontstructures

(boardwalks, sea walls, docks), playgroundequipment, and park

fixtures (picnic tables).

California State Senator Gloria Romero (D-LosAngeles) has pushed

for legislation that would ban allarsenic-treated wood in

California and reclassify thelumber as a hazardous waste that must

be disposed of inspecial facilities. Florida State Representative

LarryCrow (R-Dunedin) filed legislation in 2001 to

banarsenic-treated wood from playgrounds in Florida, butthe bill

was killed in committee after the treated-wood,forestry and

construction industries testified against it.

Rep. Crow and the Florida Public Interest ResearchGroup are now

jointly sponsoring billboards in theTampa Bay area that warn

parents about CCA-treatedwood. The first billboard shows children

on playgroundequipment and reads Arsenic is poison.

CPSC: Ken Giles, 301/504-0990 AWPI: Mel Pine, 703/204-0500

Retailers Responding to EPAReady to Sell CCA Alternatives

Home Dept and Lowes are the largest retailers of CCA-treated

lumber in the United States, which represents 7%and 9% of annual

revenues, respectively, for the homecenters. Home Depot and Lowe's

currently sellalternatives to CCA-treated wood alternatives,

includingredwood (in select market regions) and wood

compositedecking; however, the available supply of thesematerials

is not sufficient to replace the volume of CCA-treated wood

used.

The companies will begin stocking more of thealternatives as

they become available and will stopselling CCA-treated wood prior

to the January 2004deadline. Menards, the third largest home center

chain,has been offering an ACQ-treated product since 1998,although

the company also sells CCA-treated wood. The phase-out is dependent

on how quicklymanufacturers are able to transition their

treatmentfacilities, said Lowe's spokeswoman Chris Ahearn.

The problem they're going to have is getting access to

areplacement, said Gary Donnelly, president of theNational Lumber

and Building Material DealersAssociation in Washington. If they

stopped sellingCCA-treated lumber tomorrow, they wouldn't

haveanything to replace it with.

NLBMDA: Gary Donnelly, 202-547-2230

-

Vol. 1, No. 2/Page 4 NATURAL & WOOD FIBER COMPOSITESNATURAL

& WOOD FIBER COMPOSITES February 27, 2002

COPYRIGHT 2002 PRINCIPIA PARTNERS

Check out the story on page 7 highlighting theresults of

Principia Partners latest industry studyon Additives for Natural

Fiber and WoodComposites. The study of the demand for anduse of

additives is now available from Principia.

For more information about this study, visit the the following

web page:

www.principiaconsulting.com/reports_woodadd.html

Materials

Marth Adds New Wood Flour FacilityCapacity Reaches 45 Million

lb

Marth Manufacturing Inc. (MMI; Athens, WI)announces the initial

production processing at theirstate-of-the-art wood flour plant.

MMI began as MarthWood Shaving Supply and remains a privately

ownedcompany that has served the wood fiber market for over40

years.

MMI focuses on wood fiber as renewable fillers forplastics,

compounds and chemical processing. MMIsfirst composites-focused

facility has been in operationsince 1998. The new facility is

unique in its pioneeringblending abilities for custom fiber

requirements.

In 1998, MMI initiated its 5-year development plan forits

composites-related wood flour business. A pilotplant for the firms

high performance wood flour was setup in 1998 at the Marathon

facility. After the processwas proven, the company began to

successfully market their products. MMI then built a larger second

plant inAthens, WI about 15 miles away which opened inDecember 2001

. Both plants will continue to makewood flour for composites to

ensure a reliable andflexible supply to their customers. The total

capacity ofboth plants will be ramped up during 2002 to reachabout

20,000 lb an hour or 45 million lb a year. MMIhas long term supply

contracts for pine and hardwoodshavings from larger lumber mills in

the Northcentralregion

Tony Morice noted that Marth has no standard on-the-shelf wood

flour products for composites, but isworking closely with customers

to develop custom woodflour blends of different types of wood and

differentmesh sizes. Morice added Our goal is to producemixtures of

wood flour that perform best for specificcustomers, given their

processing equipment andfinished products.Marth: Tony Morice,

715/842-9200 [email protected]

Regulatory/Testing

Shift to CCA Alternatives UnderwayConversion by Treaters Started

in 1994

The total U.S. market for chemically treated wood for

allapplications is estimated at 7 billion bd-ft in 2001, ofwhich an

estimated 95% employs CCA. Of this total,about 5 billion bd-ft are

used in decking, railings, andfoundation beams. Only 1% is used in

playgroundequipment for homes, schools, and community parks.

Two alternative pesticides are available to replace

thearsenic-based products, including ACQ (alkaline

copperquaternary) and CBA (copper boron azole). ACQ hasbeen used as

a biocide for years in such applications asswimming pool chemicals,

hair shampoos, and soaps. Over the past 5 years, sales of

ACQ-treated wood haveheld steady at 25 to 30 million bd-ft per

year, while littleCBA is used for wood treatment. The cost of ACQ

is$4.50 to $5.00 a lb, or 20% higher than CCA. Thesechemicals are

produced by three companies in theUnited States, including:

q Chemical Specialties (Charlotte, NC) makes CCAand ACQ under

the Preserve brand

q Arch Chemicals (Smyrna, GA) makes CCA and hashad CBA under the

Wolmanized Natural Selectbrand on the market since 2000

q Osmose (Montreal, PQ) which makes CCA andACQ under the

NatureWood brand

In order to begin producing a non-arsenic alternative,

thetreaters will have to clean up their facilities at a cost

of$40,000 to $200,000 depending on the number oftreatment tanks.

The conversion is fairly simple. Inorder to make the conversion,

the treatment tank mustbe completely cleaned, and piping, pumps and

otherprocessing equipment too contaminated to be cleanedmust be

replaced to eliminate any residual CCA fromthe system. The system

must then be tested to ensure itas CCA free.

In addition to these capital costs, pressure treaters willalso

face higher costs for treatment chemicals. ACQ ispriced 20% higher

than CCA. As treaters convert toACQ, initial retail pricing for

treated wood will be 25%to 30% higher than CCA-treated products.

However,those treaters with significant experience with

ACQcurrently market their products at just a 10% premium,and expect

the cost of the treatment chemicals to declineas production volume

increases.

About 350 plants across the country pressure-treatlumber. A few

have been using ACQ for some time. Sunbelt Forest Products (Bartow,

FL) began using ACQ

-

February 27, 2002 NATURAL & WOOD FIBER COMPOSITESNATURAL

& WOOD FIBER COMPOSITES Vol. 1, No. 2/Page 5

COPYRIGHT 2002 PRINCIPIA PARTNERS

in May 2001 at its Ocala, FL plant. This Ocala plant isthe only

ACQ wood treatment facility in FL certified bythe State as CCA

free. The company has also converted50% of capacity at its Bartow,

FL plant to ACQtreatment. We've been preserving wood with ACQnow

for almost 10 months, and our customer base forPreserve and

Preserve Plus (with water repellent) hasgrown dramatically over the

last few months inparticular, said Carl Holland, Sunbelt Forest

Productspresident.

Northern Crossarms (Chippewa Falls, WI) has usedACQ since 1994

to treat wood, and discontinued use ofCCA in 1997 due to growing

public concerns aboutCCA in the environment. In 1998, Northern

opened asecond plant for ACQ treated wood. Patrick Bischel,owner of

Northern Crossarms, related that his firm wasa pioneer in ACQ use

and is the largest and mostexperience treater using ACQ today. It's

been anamazing turnaround over the last six months, Bischelsaid.

Because of their experience in ACQ and thevolumes produced, the

cost of the ACQ-treated lumberis only about 10% higher than CCA

treated lumber.

Sunbelt: Cliff Daniels, [email protected]: Patrick

Bische, [email protected]

Company News

From the Builders Show in AtlantaNew Products Profilerate

The show floor at the International Builders Show inAtlanta held

February 8 to 11 was the hotspot for bothlongtimeexhibitorsand

newcompositeproducers. Theindustry israpidlymaturingfrom ahandful

ofdeckboardsuppliers showing their wares only a few years ago.

Today, the material category is exploding in railing,porches, and

fencing. The producers are beginning totalk very seriously about

the inevitable expansion intosiding.

Builders and homeowners are gravitating to the categoryas the

proliferation of decking and outdoor accessoriesbased on wood

composites occurs. Furthermore, the

Environmental Protection Agencys decision aboutphase out of CCA

(see page 3 for further info) willresult in explosive growth.

CertainTeed announced a variety of new tools to helpcontractors

better serve customers of Boardwalkcomposite lumber. CertainTeed

has created two newstyles of composite railing assemblies which

arenationally approved for Boardwalk decks. The company also

announced the creation of its patent-pending Boardwalk Deck Square.

The 3-sided tool is astraight edge, a gapping tool and a baluster

spacercombined into one.

TimberTech introduced two new colors at the show. The new colors

- Grey and Cedar- complement thecompanys only current shade:

Natural. Stu Kemper,TimberTechs President, explains, We have

invested innew technology to ensure uniformity and maintainprecise

color of the formula from batch to batch. Ourgoal is to meet the

expectations of homeowners lookingfor their deck to look just like

it does right after its beeninstalled. TimberTech is considering

other colors forrelease in Fall 2002.

Trex also introduced new products and profiles at theshow,

including the addition of Saddle, a deep tan colorthat weathers

only slightly while maintaining a rich tone. For more railing

options, the company showed achamfered railing profile and new

decorative post capsin two classic designs. Andrew Ferrari,

Executive VP,remains very upbeat about Trexs future growth

statingthat with less than 10% of the decking being wood-plastic

composite, the real growth still lies ahead.

Louisiana Pacific is also thrilled with the salesperformance of

its WeatherBest brand of decking. Thecompany noted that by the end

of January 2002 it hadbooked sales accounting for 60% of its

annualproduction capacity. The company is adding extrusionlines and

blending capacity at its two locations in Selma,AL, and Meridian,

ID. The company has beensuccessful in providing a product that

allowsreversibility in the boards pattern. One side features

arandom graining pattern while the other side is a moreuniform

rough-sawn look. The product will satisfy thediffering tastes of

consumers and limit the productSKUs that must be stocked.

Tendura (Troy, AL) has entered an interesting niche byproducing

front porch profiles. The company is runningsix lines. Ned

Lawrence, National Sales Manager, says,We are satisfying an area

that has not been adequatelyaddressed by the suppliers competing in

the deckingsegment.

-

Vol. 1, No. 2/Page 6 NATURAL & WOOD FIBER COMPOSITESNATURAL

& WOOD FIBER COMPOSITES February 27, 2002

COPYRIGHT 2002 PRINCIPIA PARTNERS

If you would like to have your event listed on theWood

Composites calendar, please call us at

717/741-3565 or send the information

to:[email protected]

Events Calendar

April 10-11, 4TH INTERNATIONAL WOOD ANDNATURAL FIBRE COMPOSITES

SYMPOSIUM Kassel, Germany Sponsored by the University ofKassel,

this event focuses on new applications,production technology, and

end markets for woodcomposites. For info: contact Dr. Ing. A.K.

Bledzki,[43]561/804-3690, [email protected]

May 14-16, WOOD-PLASTIC COMPOSITES: ASUSTAINABLE FUTURE Vienna,

AustriaSponsored by AMI Plastics, the event will highlight

alldevelopments in the industry. For info: visit AMI

atwww.amiplastics.com

May 14-16, AUTO INTERIORS SHOW CoboConference Center, Detroit,

MI Sponsored by AutoInteriors, the will include several papers on

natural-fibercomposites used in automobiles. For info:

visitwww.autointeriorexpo.com

May 23-24, 2002 PROGRESS IN WOOD FIBRE-PLASTIC COMPOSITES

Toronto, ON Sponsored byMaterials & Manufacturing Ontario (MMO)

and theUniversity of Toronto, this conference focuses on

newdevelopments in wood composites. For registration,program, or

exhibitor info: call Valeri Iannaci at905/823-2020 x226,

[email protected]

June 26-28, PCBC 2002 - The Premier Building Show Moscone

Center, San Francisco, CA The showattracts over 21,500 industry

professionals and 625exhibitors for 4 days of education, exhibits,

andnetworking. For info: visit www.pcbc.com

November 5-7, InterAUTO 2002 Cologne, GermanySponsored by

Automotive Interiors, this conference andexhibition will address

the latest in interior materials anddesign. For info: visit

www.interauto.co.uk

Marketing

AERT Gets Contract with Lowe'sWeyerhaeuser Plays Distribution

Role

Advanced Environmental Recycling Technologies(AERT; Springdale,

AR) announced at the InternationalBuilders Show in Atlanta this

month that it secured acontract to sell its products nationwide

through Lowe's,the second largest home center chain in the

UnitedStates.

Lowe's has an exclusive contract to carry AERT'sChoiceDek

Premium line of deck materials, whileAERTs other decking products

will continue to beavailable through established dealers.

Weyerhaeuserwill distribute the product to Lowe's locations

aroundthe country. Until this agreement, Lowe's carried a fewAERT

products, but only in select locations. The chainhas carried the

ChoiceDek line since January, and notedthat the product will be in

all of its stores by mid-March.

Joe Brooks, AERT CEO, said The contract is a majorboon for the

company. Brooks went on to compare itto the contract Tyson Foods

won years ago to supplyMcDonald's restaurants with chicken nuggets.

Thisdeal with Lowe's is at least as big for us as that was forthem,

Brooks said.

Also at the BuildersShow, AERT announceda new railing

systemunder the ChoiceDekbrand. The new railingsystem offers many

anumber of novel features,including lighted rails anddeck posts,

turnedarchitectural spindles, ahidden fastening systemand full

deckingaccessories. The railingsystem will be availablenationwide

to all AERTdealers by the end of 2002.

AERT: Joe Brooks, 866-396-3737

-

February 27, 2002 NATURAL & WOOD FIBER COMPOSITESNATURAL

& WOOD FIBER COMPOSITES Vol. 1, No. 2/Page 7

COPYRIGHT 2002 PRINCIPIA PARTNERS

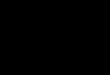

45%

29%

7%2%

5%4%

3%2%

1%4%

42.2 Million lb

53%

16%

8%

7%

4%3%

3%1% 1%

4%

$57.2 Million

ColorantsLubricantsCoupling agents

Light stabilizersHeat stabilizersImpact modifiers

Flame retardantsAntimicrobials

CFAsOthers-a

Demand of Specialty Additives in Natural/Wood Polymer

CompositesNorth America, 2001

New Market Studies

$57 Million Market for AdditivesGrowth in Usage Driven by Cost

Reduction

The market size for specialty additives used in naturaland wood

fiber composites is 42 million lb, valued at$57 million, in 2001

(see chart).

Colorants find widespread, almost universal, usageacross all

applications, and consequently represent thesingle largest category

of specialty additives consumedin these composites. Inorganic and

organic colorpigments accounted for 19.1 million lb valued at

$30.5million.

Lubricants ranked second with 12.3 million lb valued at$9.3

million, primarily based on the increasing role forstearate-based

chemistry used at many compositedecking producers.

Coupling agents like maleated polyolefins are gainingacceptance

as a key chemistry to impart improvedadhesion between polymer and

fiber, thus creatinggreater strength of the composite. This

additivecategory accounted for 2.8 million lb valued at $4.5million

in 2001.

Light stabilizers find relatively limited usage today at0.7

million lb valued at $3.9 million primarily based ontheir high

price even at very low loading levels. Composite producers find the

price too high to justifyusing the UV protection, and question

whether theadditive can properly protect color fastness over

manyyears. Nonetheless, increased use of UV absorbers andhindered

amines is expected, as customer expectationsfor longer lasting

color durability will drive futuredemand.

Heat stabilizers and impact modifiers are primarily usedby the

few PVC-based wood composite producers activein the business today,

and accounted for 2 million lb and1.6 million lb, respectively in

2001.

All other specialty additives, including antimicrobialagents,

chemical foaming agents, and flame retardantswill find greater use

in the future. A significant amountof R&D activity specifically

in antimicrobials andblowing agents is already underway at many

wood fiber-based polymer composite producers, primarily fordecking

and other building products.

The market for additives natural fiber and woodcomposites will

grow from 42 million lb, valued at$57 million in 2001, to over 87

million lb, valued atmore than $120 million by 2006. The 16%

averageannual growth rate over this five-year period exceeds

theexpected rate of growth for the composite industryoverall, due

to the greater usage of the materials.

Several major application areas within buildingproducts,

including decking and window/door lineals,will use more

antimicrobials to prevent mildew staining,more chemical foaming

agents for lighter weight andthinner walls; coupling agents for

superior strength byimproving the bond between polymer and fiber;

andcolorants/UV stabilizers for improved color fastness. While

these additives generally add to the overallformulation cost, the

performance improvements aredeemed necessary to improve the

long-term viability incurrent and targeted uses.

Chemical foaming agents (CFAs) are largelydevelopmental at this

stage. Some composite producersare experimenting with formulations

containing theseadditives to reduce weight, increase yield, and

providegreater wood like attributes through the cellularstructure

imparted by CFAs.

Greater color stability through improved pigment andUV

stabilizer technology, particularly for outdoor usessuch as

decking, railing, and windows. Colorants areused to provide color

even to non-aesthetic compositeapplications. In these cases, black

is widely used, but srange of earth tone colors (e.g., grey, brown,

slate,redwood) are also used to provide initial color for

manyproducts.

Specialty plastics additives in composites is one of themost

dynamic segments of the plastics industry. Severaladditive types,

including colorants and lubricants, arereasonably well established

but other additives haveonly penetrated 9% to 25% of their

respective potential. Opportunities exist for additive suppliers to

work withcomposite producers to utilize more additives in

theirformulations. The value proposition needs to be basedon ease

of processing (i.e. cost reduction) or in-servicefunctionality

(i.e. performance enhancement).

Principia Partners: Lou Rossi, 610/458-3738

-

Corporate: P.O. Box 611 Exton, PA 19341 USA l 888/680-2199 (U.S.

only) or 610/458-3738 Fax: 484/214-0172 l e-mail:

[email protected] l www.principiaconsulting.com

Principias Expertise

Subscription Information

Principia Partners is owned and managed by highly skilled

business information professionals with extensive experiencein

materials consumed in building products and automotive markets. In

particular, the Firms principals have closelymonitored the market

for natural/wood fiber polymer composites through various single

client engagements andsyndicated research. The Firm utilizes its

own professional staff to keep abreast of leading edge developments

in themarketplace.

NATURAL & WOOD POLYMER COMPOSITES is the latest product

offering related to the natural/wood fiberpolymer composites

industry conducted by Principia Partners, the Exton, PA-based

market research and businessconsulting firm. The newsletter is

prepared by consultants from Principia's professional staff who

have monitored thebusiness development activities in the dynamic

and growing synthetic wood products since the business was

firstestablished over ten years ago.

Jim Morton and Carl Eckert will be key regular contributors to

the newsletter. Jim, a principal at Principia Partners, isa

well-recognized industry expert in polymer-wood composites, and has

authored several relevant syndicated researchstudies, as well as

speaking at various conferences on the topic. Carl, formerly with

Kline & Company, is an expert onnatural fibers, and has spoken

at numerous conferences about the emerging opportunities for these

fibers. These twoindividuals will join other occasional

contributors to the newsletter.

To subscribe to NATURAL & WOOD POLYMER COMPOSITES, please

print and fill out the subscription formbelow and return to us. The

newsletter will be issued electronically (optional delivery by

regular mail, if no e-mail isavailable) to each subscriber 12 times

a year. The first issue will be distributed in January 2002. The

annualsubscription price is US$650 for electronic delivery

subscribers. A US$50 premium will be charged for regular

mailsubscribers for printing, and shipping/handling costs.

detach and return by fax or mailBILL TO: DELIVER TO:

NAME: ______________________________ NAME:

____________________________TITLE: ______________________________

TITLE: ____________________________COMPANY:

___________________________ COMPANY:

_________________________ADDRESS: ___________________________

ADDRESS: _________________________CITY:

_______________________________ CITY:

_____________________________STATE: ____________ ZIP: _____________

STATE: ____________ ZIP: ____________PHONE:

(______)________-_____________ PHONE:

(______)________-____________FAX: (______)________-_______________

FAX: (______)________-_______________E-MAIL:

_____________________________ E-MAIL:

____________________________

DELIVERY METHOD: E-MAIL_______ HARD COPY_______

PAYMENT CAN BE MADE BY CHECK DRAWN ON U.S. BANK OR MAJOR CREDIT

CARD (AMEX, VISA, M/C, DISCOVER). IfCREDIT CARD METHOD IS USED,

PLEASE FILL OUT THE FOLLOWING INFORMATION:

Account #: _______________________________________Exp. date:

___________/___________Signature:

_______________________________________