Embed Size (px)

Citation preview

Spiceland | Thomas | Herrmann

Financial Accounting

Current Liabilities

Chapter 8

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-2

Learning Objectives

• Distinguish between current and long-term liabilities

• Account for notes payable and interest expense• Account for employee and employer payroll

liabilities• Explain the accounting for other current liabilities• Apply the appropriate accounting treatment for

contingencies• Assess liquidity using current liability ratios

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Part A

Current Liabilities

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-3

8-4

Current Liabilities

• Liability: a present responsibility to sacrifice assets in the future due to a transaction or other event that happened in the past

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Learning Objective 1

Distinguish between current and long-term liabilities

8-5

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-6

Current vs. Long-Term Liabilities

Current• Payable within

one year or an operating cycle

Long-Term

• Payable more than one year or an operating cycle

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Learning Objective 2

Account for notes payable and interest expense

8-7

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-8

Notes Payable

• Note signed by a firm promising to repay the amount borrowed plus interest

• Interest on notes is calculated as:

Interest Face value

Annualinterest rate ×=

Fractionof the year×

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Recording Notes Payable8-9

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-10

Recording Interest Payable and Repayment of Notes Payable

• Interest payable

• Repayment of note

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-11

Notes Payable Recorded as Notes Receivable for Lender

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-12

Line of Credit & Commercial Paper

• Line of credit:• Informal agreement• Permits a company to borrow up to a prearranged

limit• No formal loan procedures and paperwork

• Commercial paper:• Company borrows from another company rather than

from a bank• Sold with maturities normally ranging from 30 to 270

days• Interest rate is usually lower than on a bank loan

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-13

Accounts Payable

• Amounts owed to suppliers of merchandise or services

• Sometimes called trade accounts payable

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Learning Objective 3

Account for employee and employer payroll liabilities

8-14

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-15

Illustration 8.3—Payroll Costs forEmployees and Employers

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-16

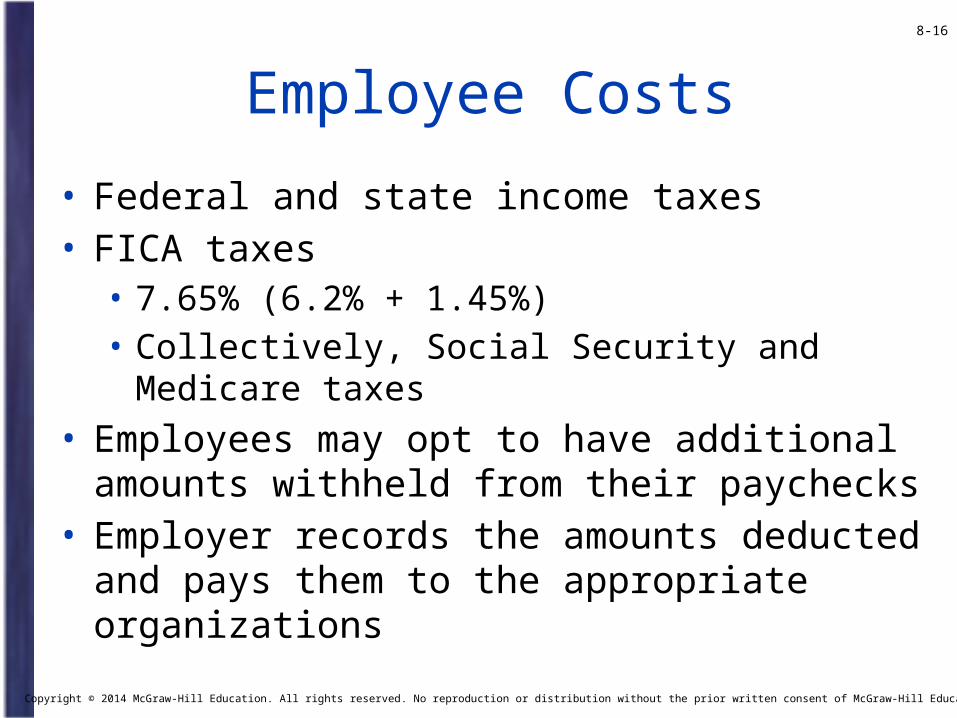

Employee Costs

• Federal and state income taxes• FICA taxes

• 7.65% (6.2% + 1.45%)• Collectively, Social Security and Medicare taxes

• Employees may opt to have additional amounts withheld from their paychecks

• Employer records the amounts deducted and pays them to the appropriate organizations

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-17

Employer Costs

• Additional (matching) FICA tax on behalf of the employee

• Employers also pay federal and state unemployment taxes on behalf of its employees

• FUTA and SUTA• Fringe benefits: Additional employee benefits

paid for by the employer

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Illustration 8.4—Payroll Example8-18

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-19

Recording Fringe Benefits and Employer Payroll Taxes

• Recording employer-provided fringe benefits

• Recording employer payroll taxes

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Learning Objective 4

Explain the accounting for other current liabilities

8-20

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-21

Other Current Liabilities

• Unearned revenues: liability account used to record cash received in advance of the sale or service

• Sales tax payable: collected from customers by the seller

• Current portion of long-term debt: debt that will be paid within the next year

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Example—Unearned Revenues8-22

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Example—Sales Tax Payable8-23

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-24

Current Portion of Long-Term Debt• Debt that will be paid within the next year• Provides information about a company’s

bankruptcy risk

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-25

Illustration 8.6—Current Portion ofLong-Term Debt

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Part B

Contingencies

8-26

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Learning Objective 5

Apply the appropriate accounting treatment for contingencies

8-27

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-28

Contingent Liabilities

• An existing uncertain situation that might result in a loss

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-29

Illustration 8.8—Accounting Treatment of Contingent Liabilities

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-30

Warranties

• Most common example of contingent liabilities• Help increase sales• Warranty expense is recorded in the same

accounting period as the sale• It should be probable and the amount can be

reasonably estimated

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Accounting Warranties8-31

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-32

Contingent Gains

• An existing uncertain situation that might result in a gain

• Not recorded until the gain is certain• Conservative reasoning

• Not recorded in the accounts• Firms sometimes disclose them in notes to the

financial statements

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Learning Objective 6

Assess liquidity using current liability ratios

8-33

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-34

Liquidity Analysis

• Liquidity: refers to having sufficient cash or other current assets to pay currently maturing debts

• Lack of liquidity can result in financial difficulties or even bankruptcy

• Three liquidity measures:• Working capital• Current ratio• Acid-test ratio

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-35

Working Capital

• A large positive working capital is an indicator of liquidity

• Not the best measure of liquidity for comparison

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-36

Current Ratio

• Ratio of 1 or higher often reflects an acceptable level of liquidity

• Higher the current ratio, the greater the company’s liquidity

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-37

Acid-Test Ratio or Quick Ratio

• Based on a more conservative measure• Quick assets are readily convertible into cash

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-38

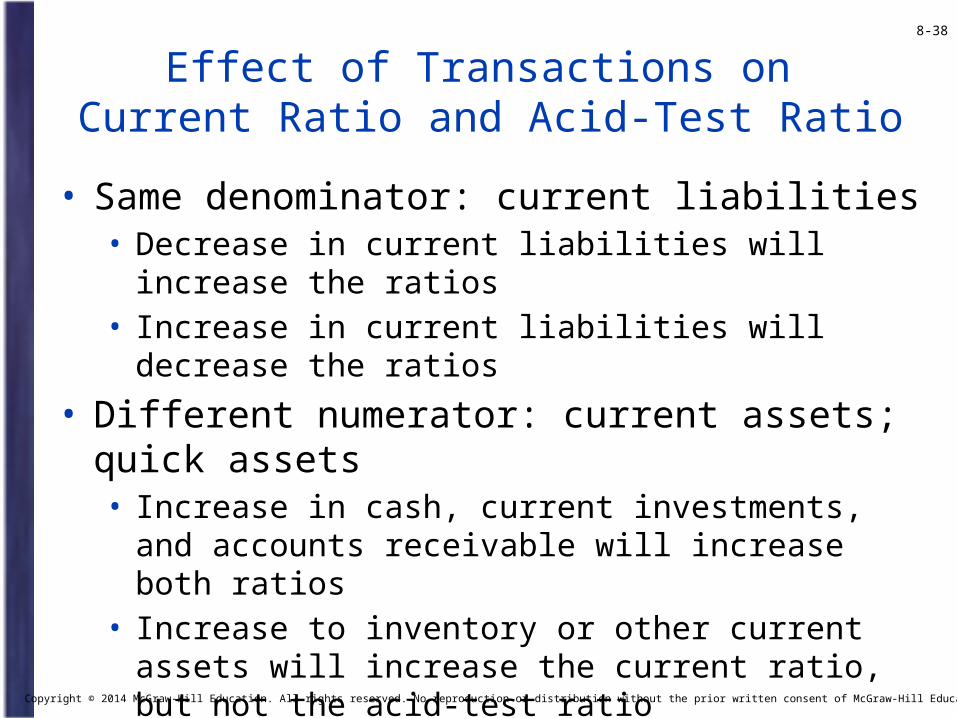

Effect of Transactions on Current Ratio and Acid-Test Ratio

• Same denominator: current liabilities• Decrease in current liabilities will increase the ratios• Increase in current liabilities will decrease the ratios

• Different numerator: current assets; quick assets• Increase in cash, current investments, and accounts

receivable will increase both ratios• Increase to inventory or other current assets will

increase the current ratio, but not the acid-test ratio

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

8-39

Liquidity Management

• Management can influence the ratios that measure liquidity

• Debt covenant: agreement between a borrower and a lender that requires certain minimum financial measures be met or the lender can recall the debt

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

End of Chapter 8

8-40

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

![[MS-PPTX]: PowerPoint (.pptx) Extensions to the Office ...interoperability.blob.core.windows.net/files/MS-PPTX/[MS-PPTX... · 1 / 76 [MS-PPTX] — v20140428 PowerPoint (.pptx) Extensions](https://img.pdfslide.us/doc/110x75/5ae7f6357f8b9a6d4f8ed3b3/ms-pptx-powerpoint-pptx-extensions-to-the-office-ms-pptx1-76-ms-pptx.jpg)