Embed Size (px)

Citation preview

POTUS 45Tax reform investment implications

Chief Investment Office Americas, Wealth Management | 20 December 2017 8:11 pm GMTJeremy Zirin, CFA, Head of Investment Strategy Americas, [email protected]; David Lefkowitz, CFA, Senior Equity Strategist Americas,[email protected]; Edmund Tran, Equity Strategist Americas, [email protected]; Leslie Falconio, Senior Fixed Income Strategist Americas,[email protected]; Barry McAlinden, CFA, Senior Fixed Income Strategist Americas, [email protected]; Kathleen McNamara, CFA, CFP®,Senior Municipal Strategist Americas, [email protected]; Justin Waring, Investment Strategist Americas, [email protected]

• Following months of debate and negotiations, Republicanleaders are on the verge of passing the most sweeping taxlegislation in more than 30 years, highlighted by a largereduction in corporate tax rates and extensive changes topersonal income tax rates and deductions.

• We expect the tax package to boost US real GDP growthby about 0.25-0.50% per year in both 2018 and 2019. Thisreduces the already-low recession risk over this period.

• The solid economic backdrop underpins our global equityoverweight. It also strengthens the case for our overweightto US large-cap value stocks, which stand to benefit from anacceleration in economic growth.

• With tax benefits included, we forecast S&P 500 earnings pershare to rise by 15% in 2018 to USD 151. As such, we lift our6 month S&P 500 forecast to 2800 and expect further marketgains to the 2850-2950 range by the end of next year.

• While added fiscal stimulus could boost inflationary pressures,we still expect only a gradual rise in interest rates. Selectprovisions in the bill have resulted in a year-end jump inmunicipal bond issuance. We expect this effect to fade in theNew Year.

• Be sure to read the Advanced Planning team's guide for howtax reform may impact your personal and business taxes

Economics

The legislation will modestly stimulate the US economy, addingabout 0.25-0.50% per year to real GDP in 2018 and 2019 andfurther diminish the probability of a recession over the next coupleof years. In addition to providing more disposable income forconsumers, stronger growth momentum, a lower corporate tax rateand accelerated depreciation of capital expenditures should alsoboost business spending. At an expected cost of about USD 1 trillionover the next 10 years, the cumulative federal government debtincrease amounts to less than 5% of GDP, so we don't expect this tomaterially alter the outlook for government finances.

POTUS 45The acronym POTUS (President of the UnitedStates) came into use during the late 1800s bytelegraph operators and is now commonly usedin media. Donald Trump is the 45th POTUS.

This report has been prepared by UBS Financial Services Inc. (UBS FS). Please see important disclaimers and disclosuresat the end of the document.

Equities

All told, we estimate that the tax reform package will boost S&P 500earnings per share (EPS) by 6-10% next year. We had been forecasting2018 S&P 500 EPS of USD 141 (+8% year-over-year) without any taxbenefits and we now raise our forecast to USD 151 (+15%) – thefastest pace of earnings growth since the early years of the expansion.The lower corporate tax rate, which falls to 21%, is the primary driverof this earnings boost. Earnings growth will also benefit from therepatriation of USD 1 trillion of overseas cash, as much of this willlikely be used for corporate share repurchases.

Offsetting some of these benefits, there are a number of "baseerosion" provisions, which aim to limit the ability of US multi-nationalsto shift income into low-tax, overseas jurisdictions. These provisionsare complex and publicly-traded companies don't disclose enoughinformation for outside analysts to fully assess their implications.Therefore, investors will be keenly interested in management com-mentary about tax reform impacts, which we expect will be forth-coming during the fourth quarter reporting season that begins in mid-January. Our EPS estimates incorporate higher international taxes forUS multi-nationals as a result of these provisions.

Still, other uncertainties remain. It is unclear how much of the taxbenefits will be retained by shareholders. Our forecasts have assumedthat nearly all of the benefits flow to shareholders. However, in verycompetitive industries, companies may decide to reinvest some of thetax savings into lower prices or to boost investments in marketing,research and development, or capital spending. In less-competitiveindustries, shareholders should capture the lion's share of the ben-efits. But our forecasts should not be seen as a "best case" scenariofor corporate profits; we have not accounted for a potential increasein economic growth stemming from the tax bill.

Further upside potential for stocks – but it may take timeWe believe US markets have priced in about half of tax reform'searnings benefit. As we show in Fig.1, a sector-neutral basket ofstocks with the highest tax rates has outperformed the broadermarket by about 5% since the November 2016 election. We estimateabout a 20% tax reform earnings boost for these stocks, so this basketcould outperform by another 5% as the market fully appreciates theuplift. From another perspective, the S&P 500 is up about 4% sincethe House passed its tax bill in mid-November, which is about half ofthe earnings boost we expect for the broader market.

While we do see additional tax-driven upside for the market, it maynot materialize right away. As we highlighted above, investors willneed further disclosure from corporate management teams in orderto fully understand all of the implications of the tax reform package.Companies may not offer this guidance until the fourth quarterreporting season in January and February. In addition, it may take evenlonger for the second-round effects of potentially faster economicgrowth to materialize. So it may take at least a couple of months –

Fig. 1: High-tax firms have outperformed as thebill reaches the finish linePerformance of stocks with high tax rates relative tothe market

0%

1%

2%

3%

4%

5%

6%

Oct-16 Dec-16 Feb-17 Apr-17 Jun-17 Aug-17 Oct-17 Dec-17

November2016 election

Source: FactSet, UBS, as of 18 December 2017

POTUS 45

Chief Investment Office Americas, Wealth Management 20 December 2017 2

if not longer – for the equity market to fully reflect the upside thatwe expect. Nonetheless, we raise our rolling six month S&P 500 pricetarget to 2800 and target a range of 2850-2950 by year-end 2018.

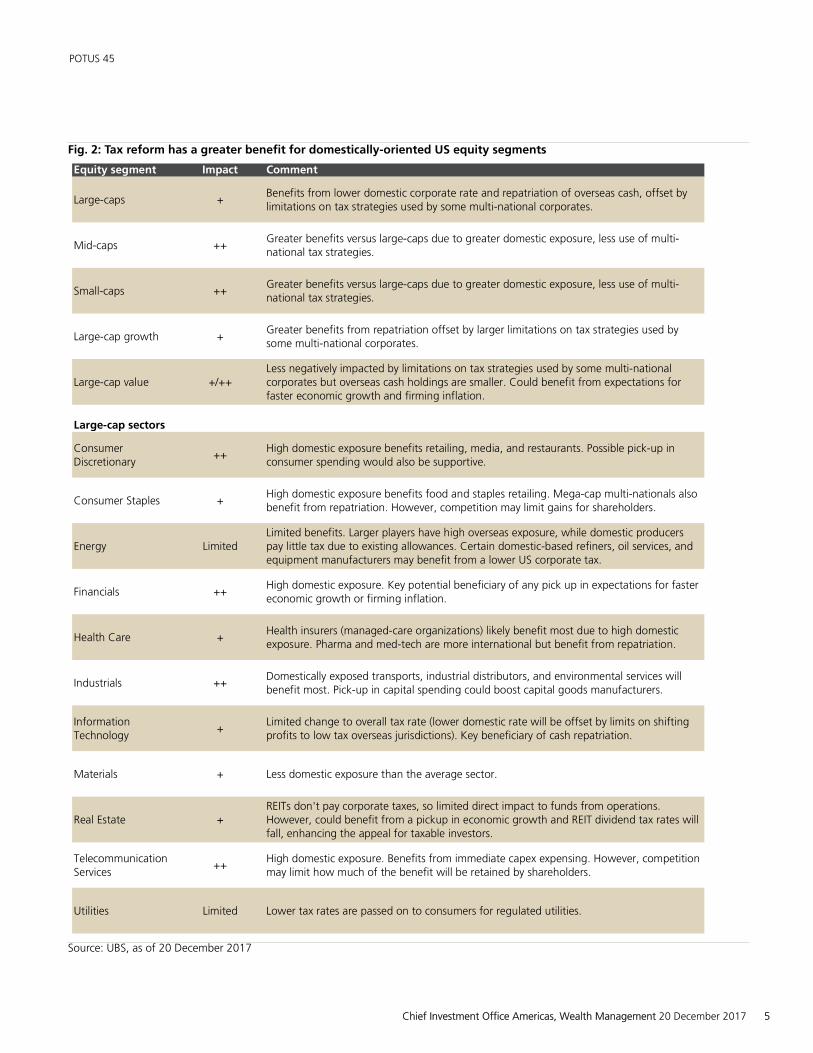

Fig. 2 summarizes our assessment of the impact of tax reform acrossequity market segments. With a greater proportion of total earningsproduced domestically, small- and mid-caps should benefit more thanlarge-caps. And value stocks also look well-positioned, given botha larger domestic footprint as well as their tendency to outperformduring a cyclical growth acceleration. Within large-caps, financials,consumer discretionary (specifically media, retailers and restaurants),industrials (transports), and telecom stand to benefit the most. Butit's important to note that the impact can vary dramatically withinsectors.

What we'll be watchingWe'll be closely watching management guidance and how this getsincorporated into analysts' earnings expectations. In our view, thecurrent consensus "bottom-up" S&P 500 EPS estimates for 2018 and2019 largely excludes any tax benefits. If profits next year increase by15% to USD 151 as we suspect, the market is trading at a forwardP/E of 17.8x.

Fixed Income

To the extent that the economic stimulus leads to firmer inflation, thiscould provide additional support for central banks' normalization ofmonetary policy. We maintain our view that the Fed will raise ratestwice more in 2018, and three times in 2019. We also expect the10-year Treasury yield to remain largely range-bound around 2.5%in 2018.

Municipal bondsIt's important to stress that the small decrease in the top marginalincome rate (from 39.6% to 37%) doesn't materially impact thedemand for tax-free income from individual investors, the dominantbuyer base for munis. In fact, the USD 10,000 cap on state andlocal tax (SALT) deductions should increase the demand for in-statemunicipal bonds, especially for high-tax states such as California, NewYork, and New Jersey. Municipal bond income remains tax-exempt,so the SALT limit could make this tax advantage marginally moreattractive. By contrast, the cut in the corporate tax rate to 21% from35% may prompt institutional investors (banks and insurance com-panies) to curtail their future purchases of tax-free muni bonds in favorof taxable securities.

On the supply side, there were two important provisions that we werewatching throughout the debate. The first was a proposed change tothe issuance of Private Activity Bonds – in the final version of the bill,tax exemption for these bonds is preserved. But there was a changeto Advance Refunding Bonds: existing bonds are grandfathered, butafter 31 December 2017 newly issued bonds will no longer be eligiblefor federal tax exemption. Municipal bond issuers will be permittedto refund outstanding bonds on a current basis but may not issue

POTUS 45

Chief Investment Office Americas, Wealth Management 20 December 2017 3

tax exempt refunding bonds more than 90 days in advance of thefirst call date. This change prompted a significant burst in municipalbond supply in recent weeks, but this effect will likely fade in the NewYear. We believe that this limited supply of tax-exempt bonds will besupportive of bond prices.

Corporate bondsAlthough we view the overall tax reform as positive for investmentgrade (IG) credit, we believe the net impact on spreads will be mar-ginal. The reduction in the corporate tax rate will result in a higherafter tax income and when combined with access to repatriatedfunds, should lower the amount of leverage through less corporateborrowing. This overall is a positive for credit spreads, as it reducesthe large corporate supply the market has witnessed over the pastfew years. However, we do see other factors that will limit thecredit benefits. First, while the lower leverage may ultimately enhancethe underlying credit, we still see the bulk of funds being used forinvestment and shareholder rewards. Second, risks such as increasedM&A activity may counter the slight spread benefit via tax reform.Nonetheless, the expectation over the longer term is for an approx-imate 40bps of IG tightening over a 10 year period due to the recentreform.

For high yield (HY) companies, the effects will be more bifurcated.The benefit of the lower tax rate and immediate capex expensing isgenerally greater than the limit on interest expense for most double-B rated companies and some single-B rated issuers. These companiesalso have time to adjust to the stricter EBIT threshold that occursafter 2021. On the other hand, the most highly leveraged issuers thatfall largely in the CCC rating category stand to be hurt most by theinterest limitation. The spreads for CCC issuers have underperformedsince earlier this year, which should limit the extent of further tax-related re-pricing. CIO turns to the overall economic fundamentals asthe main guide to our credit outlook. We remain neutral on IG andHY corporates and anticipate tepid, but positive total returns over thenext year.

POTUS 45

Chief Investment Office Americas, Wealth Management 20 December 2017 4

Fig. 2: Tax reform has a greater benefit for domestically-oriented US equity segments

Equity segment Impact Comment

Large-caps +Benefits from lower domestic corporate rate and repatriation of overseas cash, offset bylimitations on tax strategies used by some multi-national corporates.

Mid-caps ++Greater benefits versus large-caps due to greater domestic exposure, less use of multi-national tax strategies.

Small-caps ++Greater benefits versus large-caps due to greater domestic exposure, less use of multi-national tax strategies.

Large-cap growth +Greater benefits from repatriation offset by larger limitations on tax strategies used bysome multi-national corporates.

Large-cap value +/++Less negatively impacted by limitations on tax strategies used by some multi-nationalcorporates but overseas cash holdings are smaller. Could benefit from expectations forfaster economic growth and firming inflation.

Large-cap sectors

ConsumerDiscretionary

++High domestic exposure benefits retailing, media, and restaurants. Possible pick-up inconsumer spending would also be supportive.

Consumer Staples +High domestic exposure benefits food and staples retailing. Mega-cap multi-nationals alsobenefit from repatriation. However, competition may limit gains for shareholders.

Energy LimitedLimited benefits. Larger players have high overseas exposure, while domestic producerspay little tax due to existing allowances. Certain domestic-based refiners, oil services, andequipment manufacturers may benefit from a lower US corporate tax.

Financials ++High domestic exposure. Key potential beneficiary of any pick up in expectations for fastereconomic growth or firming inflation.

Health Care +Health insurers (managed-care organizations) likely benefit most due to high domesticexposure. Pharma and med-tech are more international but benefit from repatriation.

Industrials ++Domestically exposed transports, industrial distributors, and environmental services willbenefit most. Pick-up in capital spending could boost capital goods manufacturers.

InformationTechnology

+Limited change to overall tax rate (lower domestic rate will be offset by limits on shiftingprofits to low tax overseas jurisdictions). Key beneficiary of cash repatriation.

Materials + Less domestic exposure than the average sector.

Real Estate +REITs don't pay corporate taxes, so limited direct impact to funds from operations.However, could benefit from a pickup in economic growth and REIT dividend tax rates willfall, enhancing the appeal for taxable investors.

TelecommunicationServices

++High domestic exposure. Benefits from immediate capex expensing. However, competitionmay limit how much of the benefit will be retained by shareholders.

Utilities Limited Lower tax rates are passed on to consumers for regulated utilities.

Source: UBS, as of 20 December 2017

POTUS 45

Chief Investment Office Americas, Wealth Management 20 December 2017 5

AppendixDisclaimerResearch publications from Chief Investment Office Americas, Wealth Management, formerly known as CIO Wealth Management Research,are published by UBS Wealth Management and UBS Wealth Management Americas, Business Divisions of UBS AG or an affiliate thereof(collectively, UBS). In certain countries UBS AG is referred to as UBS SA. This publication is for your information only and is not intended asan offer, or a solicitation of an offer, to buy or sell any investment or other specific product. The analysis contained herein does not constitutea personal recommendation or take into account the particular investment objectives, investment strategies, financial situation and needs ofany specific recipient. It is based on numerous assumptions. Different assumptions could result in materially different results. We recommendthat you obtain financial and/or tax advice as to the implications (including tax) of investing in the manner described or in any of the productsmentioned herein. Certain services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors. All information and opinions expressed in this document were obtained from sources believedto be reliable and in good faith, but no representation or warranty, express or implied, is made as to its accuracy or completeness (other thandisclosures relating to UBS). All information and opinions as well as any prices indicated are current only as of the dateof this report, and aresubject to change without notice. Opinions expressed herein may differ or be contrary to thoseexpressed by other business areas or divisions ofUBS as a result of using different assumptions and/or criteria. At any time, investment decisions (including whether to buy, sell or hold securities)made by UBS and its employees may differ from or be contrary to the opinions expressed in UBS research publications. Some investments maynot be readily realizable since the market in the securities is illiquid and therefore valuing the investment and identifying the risk to whichyou are exposed may be difficult to quantify. UBS relies on information barriers to control the flow of information contained in one or moreareas within UBS, into other areas, units, divisions or affiliates of UBS. Futures and options trading is considered risky. Past performance of aninvestment is no guarantee for its future performance. Some investments may be subject to sudden and large falls in value and on realizationyou may receive back less than you invested or may be required to pay more. Changes in FX rates may have an adverse effect on the price,value or income of an investment. This report is for distribution only under such circumstances as may be permitted by applicable law.Distributed to US persons by UBS Financial Services Inc. or UBS Securities LLC, subsidiaries of UBS AG. UBS Switzerland AG, UBS DeutschlandAG, UBS Bank, S.A., UBS Brasil Administradora de Valores Mobiliarios Ltda, UBS Asesores Mexico, S.A. de C.V., UBS Securities Japan Co.,Ltd, UBS Wealth Management Israel Ltd and UBS Menkul Degerler AS are affiliates of UBS AG. UBS Financial Services Incorporated of PuertoRico is a subsidiary of UBS Financial Services Inc. UBS Financial Services Inc. accepts responsibility for the content of a report prepared by anon-US affiliate when it distributes reports to US persons. All transactions by a US person in the securities mentioned in this report shouldbe effected through a US-registered broker dealer affiliated with UBS, and not through a non-US affiliate. The contents of this report havenot been and will not be approved by any securities or investment authority in the United States or elsewhere. UBS Financial Services Inc. isnot acting as a municipal advisor to any municipal entity or obligated person within the meaning of Section 15B of the Securities ExchangeAct (the "Municipal Advisor Rule") and the opinions or views contained herein are not intended to be, and do not constitute, advice withinthe meaning of the Municipal Advisor Rule.UBS specifically prohibits the redistribution or reproduction of this material in whole or in part without the prior written permission of UBS.UBS accepts no liability whatsoever for any redistribution of this document or its contents by third parties.Version as per September 2017.© UBS 2017. The key symbol and UBS are among the registered and unregistered trademarks of UBS. All rights reserved.

POTUS 45

Chief Investment Office Americas, Wealth Management 20 December 2017 6