Embed Size (px)

Citation preview

Potential Profit MechanismsFactors which erode value for

money/sustainability

Event 16

Deakin University CRICOS Provider Code: 00113B

16.1 Outline

• Introduction

• Profit mechanisms

– Basic cost factors

– Contract dependent

– Business structure dependent

• Case studies (small groups)

• Summation

2

16.2 Introduction

Profit is Goodness

‘Contractors should receive a reward thatis consistent with the risk and investmentthey take and the complexity involved in

their project’

3

16.3 Profit Mechanisms

Profit mechanisms can be grouped into three categories:• Basic cost factors

• Contract dependent

• Business structure dependent

4

16.4 Basic Cost Factors

• Defined profit margin

• Management reserve

• Contingency

• Provision for warranty and latent defects

• Fortuitous savings against cost estimates

5

16.5 Defined Profit

Definition:• Percentage of designated profit added

to estimated or documented cost ofproduction item

Watch for:• Profit not commensurate with risk, investment

and complexity

• Low risk 3-5%, medium risk 6-10%, high risk 10-15%

6

16.6 Management Reserve

Definition:• Undisclosed percentage reserve to manage the

contract (may be wrapped up within cost estimates)

• Contingency, based on experience to cover gap between bid cost and performance cost

Watch for:• Goodness if knowledge used to reduce bid price

or estimator originated

• Watch for reserves unsupported by metrics/ performance history

7

16.7 Contingency

Definition:• A provision for risk based on past performance to

cover identified possible adverse events andunforeseen eventualities

Watch for:• Contingency for risks that have already been mitigated

• Contingencies provided for worst case scenariowithout probability

• Double accounting - already included in workbreakdown structure

• Double accounting - “excusable delay claim” alreadyin contingency

8

16.8 Provision for Warrantyand Latent DefectsDefinition:• Where a warranty is required and the

expected cost has been estimated and a provision made

Watch for:• Warranty provisions unsupported by

data/historical performance

9

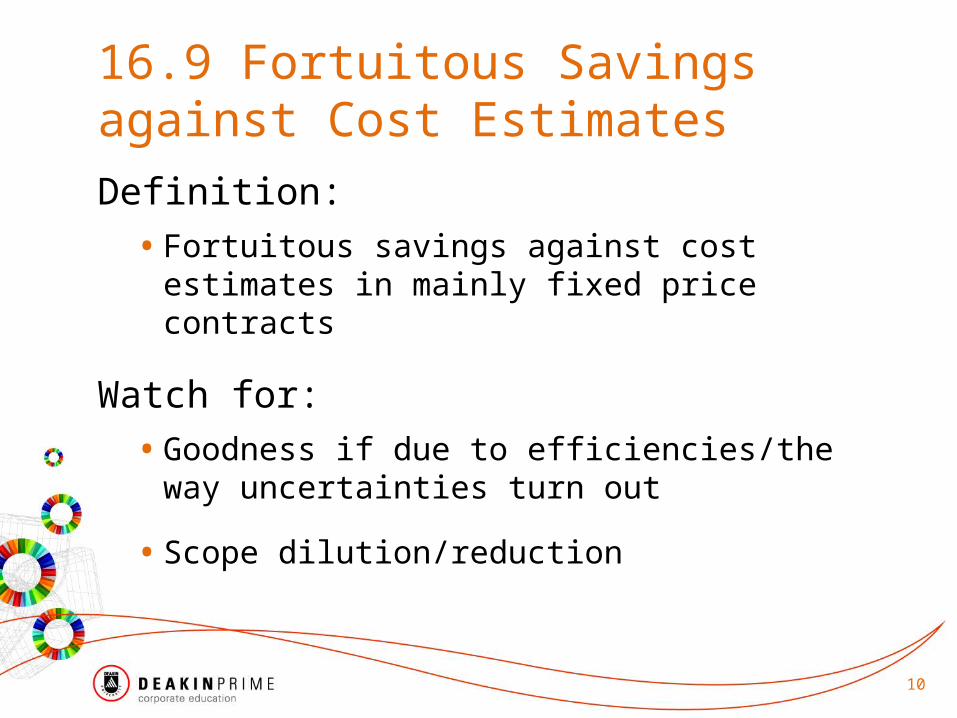

16.9 Fortuitous Savingsagainst Cost EstimatesDefinition:• Fortuitous savings against cost estimates in

mainly fixed price contracts

Watch for:• Goodness if due to efficiencies/the way

uncertainties turn out

• Scope dilution/reduction

10

16.10 Contract dependent

• Provision for liquidated damages forlate delivery

• Potential postponement claims

• Potential excusable delays

• Margins on variations and contractchange proposals

• Earnings from positive cash flow

• Use of intellectual property to exclude competition

11

16.11 Provision for Liquidated Damages for Late DeliveryDefinition:• Provision made by provider to pay damages

as a result of postponement/late delivery

Watch for:• Large provisions – indicate lack of confidence

in schedule

12

16.12 PotentialPostponement ClaimsDefinition:• Claims on purchaser to recover opportunity cost

of provider’s staff/plant/facilities being idle due to project postponements

Watch for:• Contractor not using best endeavours to

reallocate resources to other projects

• Contractor’s staff/plant/facilities not entirely idle– Catching up time on project

– Working on other projects

13

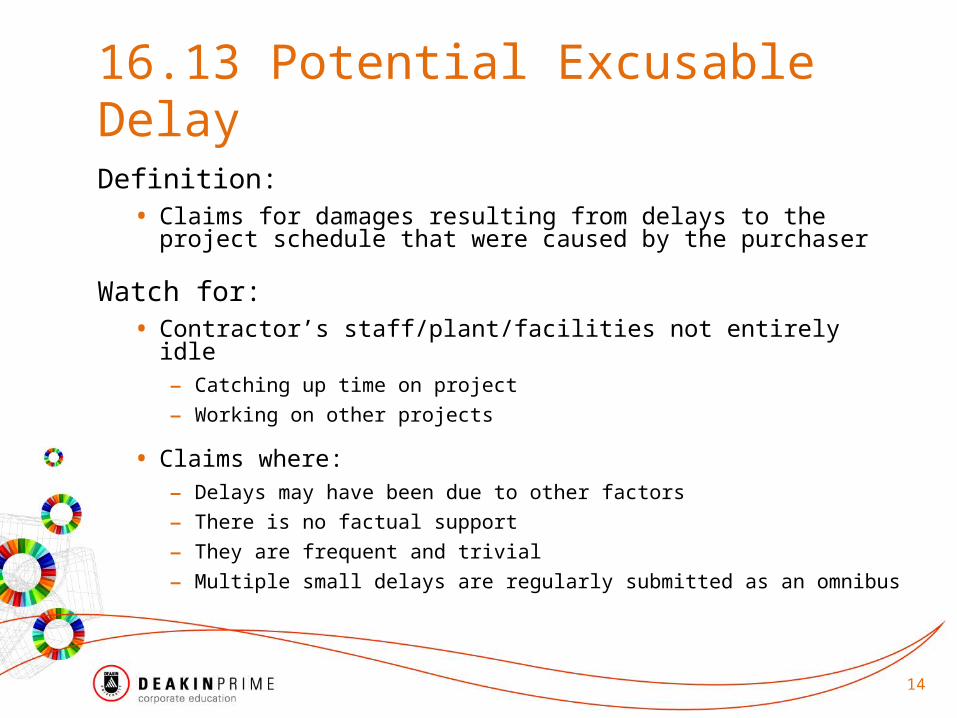

16.13 Potential Excusable Delay

Definition:• Claims for damages resulting from delays to the project

schedule that were caused by the purchaser

Watch for:• Contractor’s staff/plant/facilities not entirely idle– Catching up time on project

– Working on other projects

• Claims where:– Delays may have been due to other factors

– There is no factual support

– They are frequent and trivial

– Multiple small delays are regularly submitted as an omnibus

14

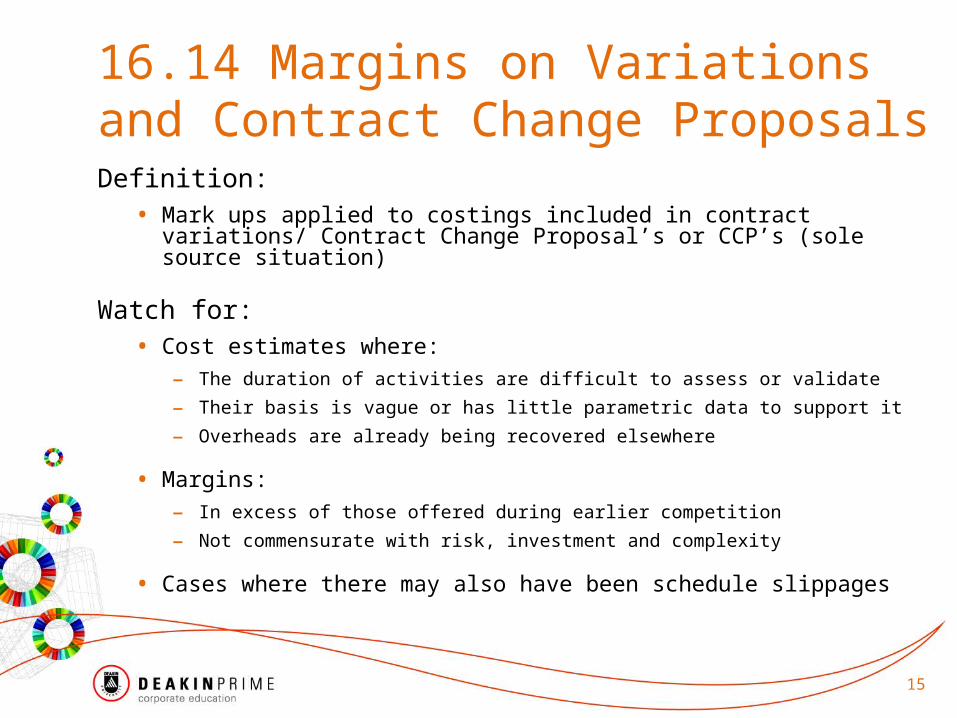

16.14 Margins on Variationsand Contract Change ProposalsDefinition:• Mark ups applied to costings included in contract variations/

Contract Change Proposal’s or CCP’s (sole source situation)

Watch for:• Cost estimates where:

– The duration of activities are difficult to assess or validate

– Their basis is vague or has little parametric data to support it

– Overheads are already being recovered elsewhere

• Margins:– In excess of those offered during earlier competition

– Not commensurate with risk, investment and complexity

• Cases where there may also have been schedule slippages

15

16.15 Earnings from PositiveCash FlowDefinition:• Cash positive – cash inflows are greater than

outflows over a given period (e.g. paymentsare ahead of requirement to meet expenses)

• Surplus cash can be invested to earn income/reduce interest payments

Watch for:• Disclosure of internal financial programmes

• Pressure to meet internal budgeted cash flow requirements

16

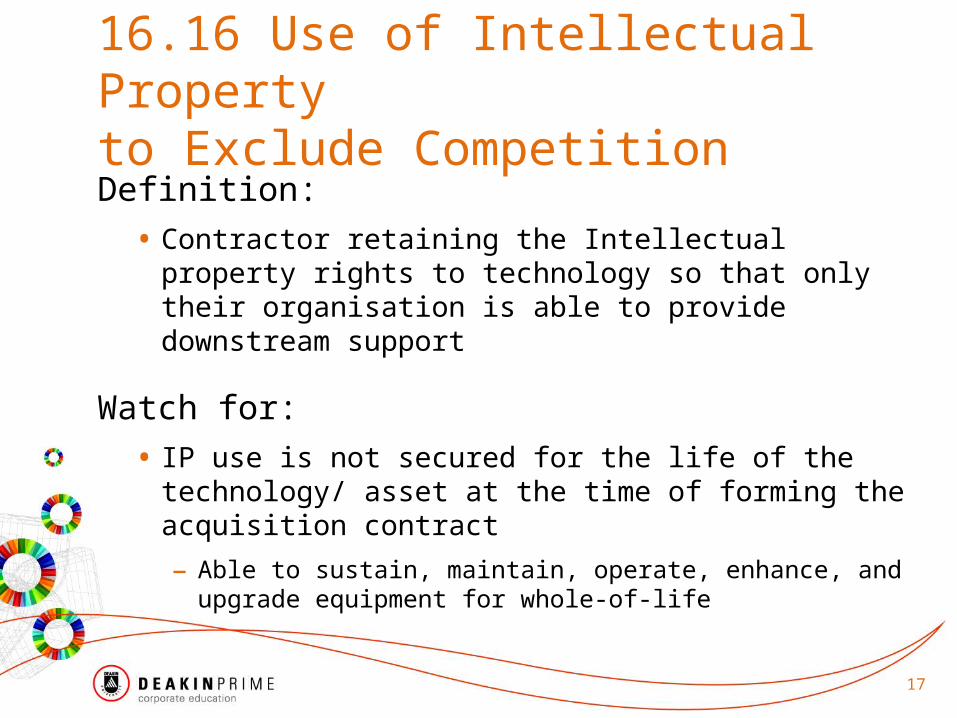

16.16 Use of Intellectual Propertyto Exclude CompetitionDefinition:

• Contractor retaining the Intellectual property rights to technology so that only their organisation is able to provide downstream support

Watch for:

• IP use is not secured for the life of the technology/ asset at the time of forming the acquisition contract

– Able to sustain, maintain, operate, enhance, and upgrade equipment for whole-of-life

17

16.17 Business structure dependent• Related company transactions

• International transfer pricing profit

• Primes taking margins from their suppliers

• Primes passing risk to their suppliers

• Asymmetric payment terms

18

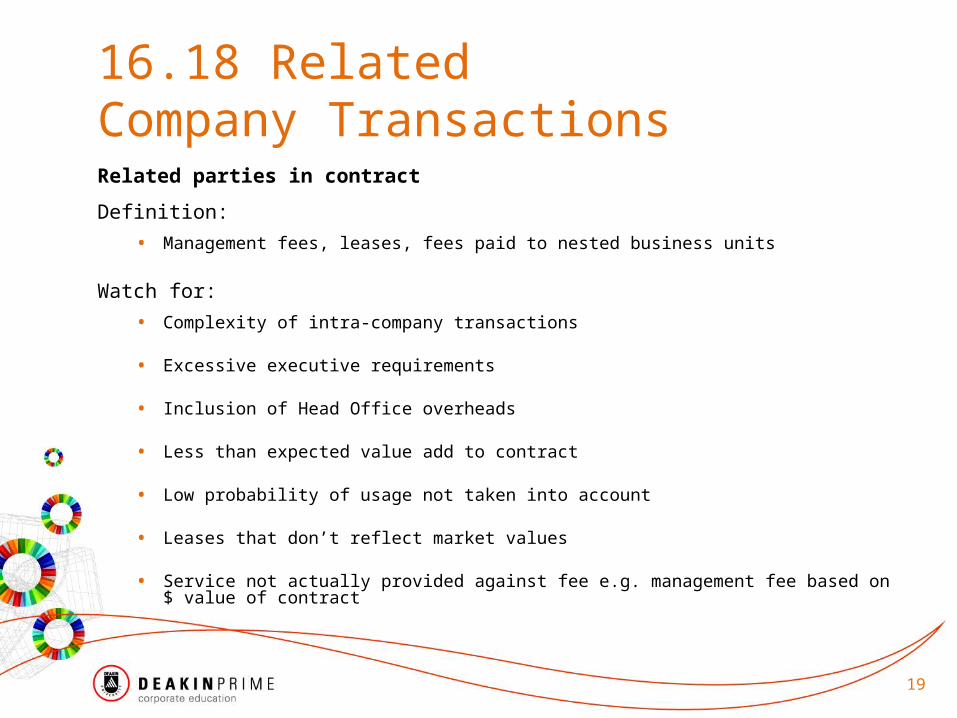

16.18 RelatedCompany TransactionsRelated parties in contract

Definition:

• Management fees, leases, fees paid to nested business units

Watch for:

• Complexity of intra-company transactions

• Excessive executive requirements

• Inclusion of Head Office overheads

• Less than expected value add to contract

• Low probability of usage not taken into account

• Leases that don’t reflect market values

• Service not actually provided against fee e.g. management fee based on $ value of contract

19

16.19 International TransferPricing ProfitInternational conglomerate

Definition:• Transfer price is the price charged by one division in a company to

another (e.g. goods sold from production to marketing). In this case it is the price charged to a division in another country (e.g. parent to OS subsidiary)

• These prices are judged rather than set in the market. The level at which they are set can affect the cost recovery/profitability of divisions or businesses in different countries

Watch for:• Complexity of intra-company transactions

• Work is performed in place specified

• Avoid overhead on overhead or profit on profit (clause in original contract)

• Legality of transactions

20

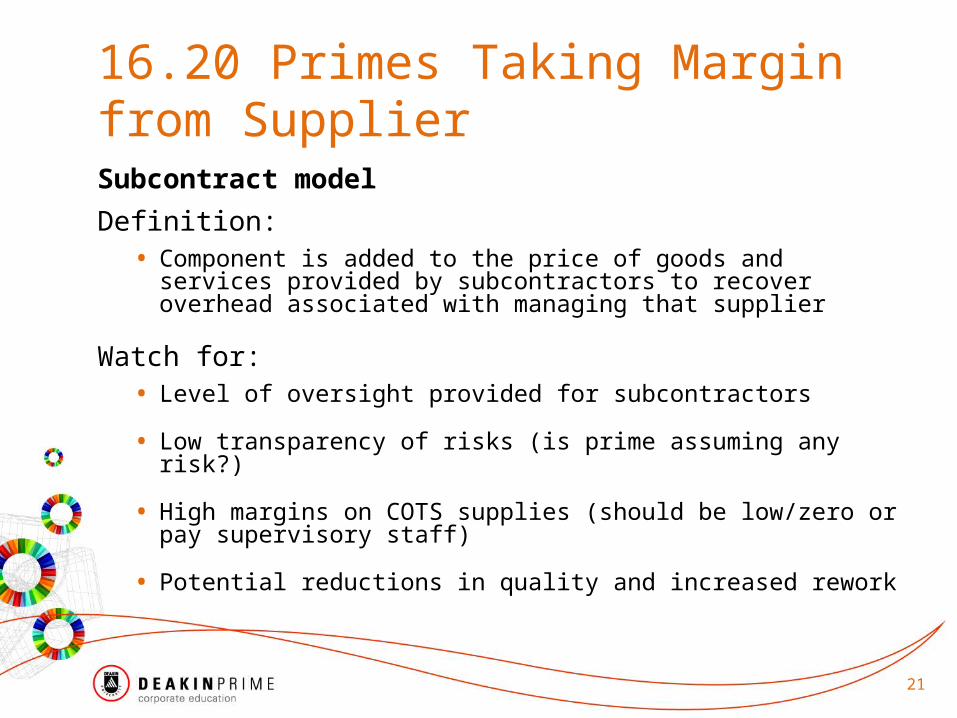

16.20 Primes Taking Marginfrom SupplierSubcontract model

Definition:• Component is added to the price of goods and services

provided by subcontractors to recover overhead associated with managing that supplier

Watch for:• Level of oversight provided for subcontractors

• Low transparency of risks (is prime assuming any risk?)

• High margins on COTS supplies (should be low/zero or pay supervisory staff)

• Potential reductions in quality and increased rework

21

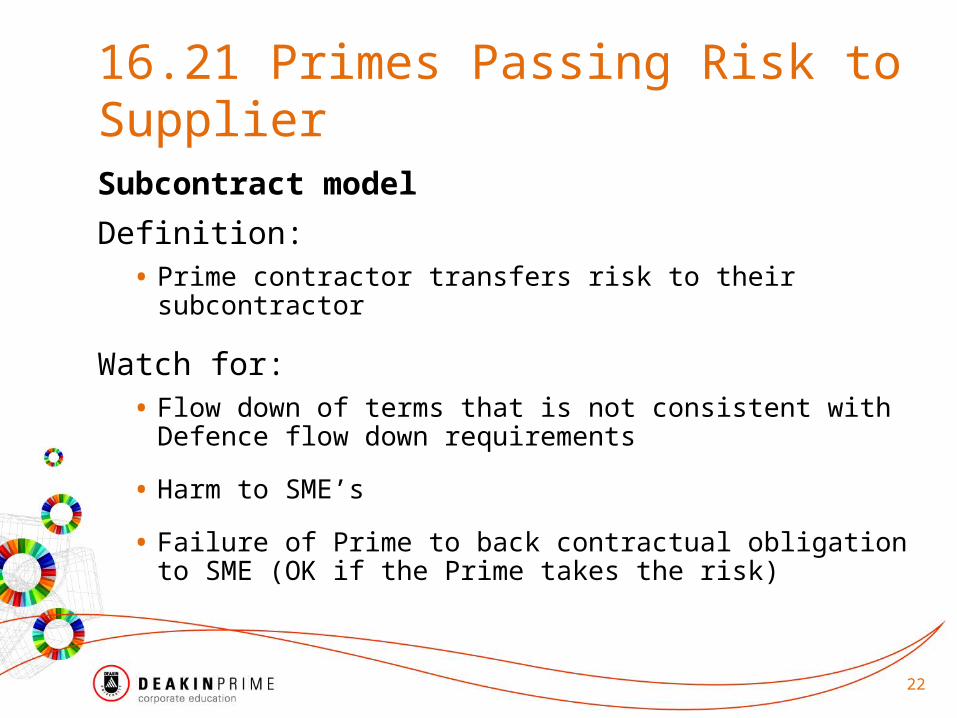

16.21 Primes Passing Risk to SupplierSubcontract model

Definition:• Prime contractor transfers risk to their

subcontractor

Watch for:• Flow down of terms that is not consistent with

Defence flow down requirements

• Harm to SME’s

• Failure of Prime to back contractual obligation to SME (OK if the Prime takes the risk)

22

16.22 Asymmetric Payment Terms

Subcontract model

Definition:

• Prime contractor receives payment within 30 days but pays their subcontractors on terms >30days

• Creates positive cash flow that can be invested/ working capital reduced

Watch for:

• Flow down of terms that is not consistent with Defence flow down requirements

23

16.23 Case studies

In small groups discuss each of the cases(in your Participant’s Guide) and answerthe accompanying questions. Be prepared to report back your findings and proposed actions.

1. Software Support

2. Excusable Delay

3. Excusable Delay (Omnibus claim)

4. Contract Change Proposal

24

16.28 Summation

Remember• Profit is goodness but should be proportional to risk,

investment and complexity

• Competition is good but if that is not possible, thenapply the value for money test – benchmark costs(get a second quote … imagine it’s your money)

• Be an informed buyer. Don’t be afraid to get broader input from people with experience/specific expertise

• Expect claims to be proven. For example, on excusable delay claims, was there a financial impact/ were staff idle (experience suggests that its unusual to have a full team idle for any significant time)?

25

16.29 Summation

26

While many of the mechanisms have their genesis in the design and negotiation of the original contract/ specification, they often have an impact later in the contract cycle

Delivery Specification

RFT

Tender

ContractNegotiation

DeliveryContract

Development

ContractVariation

Production

DMOContract

Cycle

How Profit Sharing Mechanisms Affect Discussions with

Suppliers

Event 16

16.30 The Nature of Profit

• What makes up price?

– Fixed and variable cost recovery

– Profit

• What makes up ‘profit’ at project level?

– Contribution to corporate overheads

– Provision for identified risks

– Return on investment (may include a gain share/incentive component)

28

16.31 Common Profit Mechanisms

Providing behavioural motivation in specific areas• % contract payments/revenue

• % cost

• % savings

• Agreed profit

• Performance bonus – based on KPIs, completion etc.

• Return on investment/return on assets

• Risk/reward formula

29

16.32 Profit Mechanismand BehaviourVariable price

• How would a contractor, who had offered a variable price where their profit was proportional to the value of contract payments, accept or resist the following proposed reductions in scope?

– Reduction in quantity ordered

– Reduced quality/functionality

– Elimination of a deliverable e.g. the training component

– Refusal to buy an option e.g. the maintenance package

30

16.33 Profit Mechanismand BehaviourFixed price• How would a contractor who had offered a

fixed price accept or resist the following proposed reductions in scope?

– Reduction in quantity ordered

– Reduced quality/functionality

– Elimination of a deliverablee.g. the training component

– Refusal to buy an optione.g. the maintenance package

31