Embed Size (px)

Citation preview

Poste Vita GROUP

Consolidated Financial Statements Management Report

2

INDEX

GROUP STRUCTURE

MANAGEMENT REPORT

Corporate Bodies of the Parent Company ………………………………………………………………4

Introduction………………………………………………………………………………………………….5

Reclassified Financial Statements and Key Management Indicators………………………………...6

Economic and Market Environment………………………………………………………………………9

Management trend summary……………………………………………………………………………..17

Industrial activity…………………………………………………………………………………………...20

Asset and Financial Management…………………………………………………………………….....26

Poste Vita Group’s organization……………………………………………........................................32

Risk Governance and Management System…………………………………………………………...38

Relationships with the Holding Company and with other Poste Italiane Group companies……….53

Other information…………………………………………………………………………………………..54

Significant Events occurred after Year-End……………………………………………………………..59

Outlook………………………………………………………………………………………………………60

CONSOLIDATED FINANCIAL STATEMENTS

Balance Sheet………………………………………………………………………………………………61

Income Statement………………………………………………………………………………………….63

Statement of Comprehensive Income…………………………………………………………………...64

Statement of Changes in Equity………………………………………………………………………….65

Statement of Cash Flows………………………………………………………………………………… 66

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENT

Transition to International Financial Reporting Standards - Part A…………………………………..69

Basis of preparation and accounting standards - Part B……………………………………………….74

Notes to the Consolidated Balance Sheet - Part C…………………………………………………....100

Notes to the Consolidated Income Statement - Part D……………………………………………….116

Other information – Part E……………………………………………………………………………….124

Notes on transactions with Related Parties – Part F………………………………………………….126

REPORT OF THE INDEPENDENT AUDITORS………………………………………………………128

STATEMENT OF THE MANAGER IN CHARGE OF FINANCIAL REPORTING…………………131

APPENDIXES TO THE FINANCIAL STATEMENTS………………………………………………..133

GROUP STRUCTURE

The Insurance Group’s current structure is briefly described below as well as its scope of

consolidation.

The Parent Company Poste Vita almost exclusively operates in the Life insurance sector, and only

marginally in the Non-Life sector.

The scope of consolidation exclusively includes its subsidiary Poste Assicura S.p.A, an insurance

company founded in 2010 that operates in Non-Life insurance excluding the auto sector, 100%

owned by the Parent Company. This shareholding is totally consolidated.

The Parent Company also holds a minority interest in Europa Gestioni Immobiliari S.p.A., a

company operating in the real estate sector that manages and exploits Poste Italiane’s non-

operating assets. This shareholding is not fully consolidated and is valued with the equity method.

3

CORPORATE BODIES OF THE PARENT COMPANY BOARD OF DIRECTORS(1)

Chairman Roberto Colombo CEO Maria Bianca Farina Director Antonio Nervi Director Paolo Martella Director Pasquale Marchese Director Claudio Picucci Director Michele Scarpelli

BOARD OF AUDITORS(1)

Chairman Gianfranco Vignola

Statutory Auditor Francesco Caldiero Statutory Auditor Maurizio De Matteo Alternate Auditor Libero Candreva Alternate Auditor Mauro De Angelis

INDIPENDENT AUDITORS PricewaterhouseCoopers S.p.A.

1. The Board of Directors and the Board of Auditors were appointed on the Shareholder’s Meeting of May 20, 2011 and will remain

in office for three years, until the approval of the 2013 Financial Statements. The Chief Executive Officer was approved by the

Board of Directors in the Meeting of May 23, 2011.

4

INTRODUCTION

As part of the transaction aimed at the issuance of a subordinated loan expected by the first half

of 2014, the Poste Vita Group that includes the Parent Company Poste Vita S.p.A. and the

subsidiary Poste Assicura S.p.A. presents for the first time its consolidated financial statements for

the year ended as of December 31, 2013, drafted according to the IAS/IFRS international

standards issued by the International Accounting Standards Board (IASB). Such standards were

approved by the EU and are also based on the provisions of the Isvap Regulations (now IVASS)

no. 7 dated July 13, 2007 and subsequent modifications and integrations thereto. The Poste Vita

Group did not present any consolidated financial statements in the previous years, benefitting from

an exemption according to article 21, paragraph 1, of the above-mentioned ISVAP Regulations

(now IVASS) no. 7.

In order to provide exhaustive information according to the IAS/IFRS standards, comparative data

is presented for 2012, as well as the transition chart to the International accounting standards as

reported in the specific section of the Notes to the Financial Statements.

5

RECLASSIFIED FINANCIAL STATEMENTS AND KEY MANAGEMENT INDICATORS

The Reclassified Financial Statements and Key Management Indicators are reported here below:

(data in million Euros)

ASSETS 31/12/2013 31/12/2012

Investments 69,852.2 58,307.4 11,544.7 19.8%

Investments in subsidiaries, associated companies and joint ventures197.0 198.7 1.6 - -0.8%

Loans and receivables 11.5 102.1 90.7 - -88.8%

Available for sale financial assets 59,159.9 47,924.9 11,235.0 23.4%

Financial assets at fair value through profit or loss 10,483.8 10,081.7 402.1 4.0%

Amounts ceded to reinsurers from technical provisions 40.3 27.9 12.4 44.3%

tangible and intangible assets 13.5 7.3 6.2 85.4%

Receivables and other assets 2,097.6 1,846.6 251.0 13.6%

TOTAL ASSETS 72,003.6 60,189.2 11,814.4 19.6%

(data in million Euros)

LIABILITIES 31/12/2013 31/12/2012

Shareholders' equity 2,763.5 2,108.4 655.1 31.1%

Insurance provisions 68,005.2 56,770.9 11,234.3 19.8%

Provisions 10.1 8.6 1.4 16.7%

Payables and other liabilities 1,224.9 1,301.3 76.4 - -5.9%

TOTAL LIABILITIES 72,003.6 60,189.2 11,814.4 19.6%

Change

Change

RECLASSIFIED INCOME STATEMENT 31/12/2013 31/12/2012

Net premiums earned 13,200.2 10,535.6 2,664.6 25.3%

Gross earned premiums 13,234.4 10,561.9 2,672.5 25.3%

Earned premiums ceded (34.2) (26.3) (7.9) 30.1%

Fee and commission income 0.0 0.2 (0.2) -100.0%

Net financial income from assets related to traditional

products 2,195.1 1,796.3 398.8 22.2%

Net financial income from assets related to index and

unit linked products717.2 1,360.3 (643.1) -47.3%

Net change in insurance provisions (15,275.3) (12,996.5) (2,278.9) 17.5%

Claims paid (5,178.5) (5,548.5) 370.0 -6.7%

Change in insurance provisions (10,116.8) (7,459.6) (2,657.2) 35.6%

Reinsurers' share 20.0 11.6 8.4 72.7%

Investment management expenses (26.5) (21.5) (5.0) 23.4%

Acquisition and administration costs (369.9) (276.5) (93.4) 33.8%

Net commissions and other acquisition costs (329.8) (238.8) (91.0) 38.1%

Operating expenses (40.2) (37.7) (2.5) 6.5%

Other net revenues/costs (17.0) (18.7) 1.6 -8.8%

EBITDA 423.8 379.3 44.4 11.7%

Net financial income related to available assets 101.3 93.4 7.9 8.4%

Interest expenses on subordinated debts (18.5) (22.8) 4.4 -19.1%

EARNINGS BEFORE TAXES 506.6 449.9 56.7 12.6%

Income taxes (250.5) (176.4) (74.1) 42.0%

EARNINGS AFTER TAXES 256.1 273.5 (17.4) -6.4%

(data in million Euros)

Change

6

7

Dear Sirs,

The results obtained in 2013 were excellent, with a total gross earned premium exceeding €13.2

billion (+25.3% compared to 2012), despite a national and international macroeconomic context

characterized by ongoing uncertainty that consequently affected consumers’ expectations and

families’ saving capacity.

This confirmed the validity and effectiveness of the business model adopted by the Group that

aimed at increasingly enhancing its social role as an insurance market operator. Despite this

period of uncertainty regarding public protection and welfare and the family as a central figure for

providing social services, the Group has become a promoter in offering investment, saving and

protection services for maintaining and managing citizens’ welfare.

In 2013, the Life business continued its development, particularly regarding pensions allowing the

Group to consolidate its growth trend of the last three years and placing the Poste Vita pension

fund at the top of the ranking according to the total number of subscribers (over 630 thousand)

among all pension funds present in Italy.

Excellent results were also obtained in the Non-Life business, with commercial activities aimed at

developing a balanced collection among product lines (Property, Personal and Business) mainly to

cover the customers’ principal needs, also considering the current macro-economic situation.

Satisfactory results were achieved in financial management, while always maintaining a low-risk

profile for investments; at year-end, latent capital gains in portfolio amounted to nearly 3 billion

Euros. The segregated management of Posta Valore Più obtained a 4.19% gross return, while

Posta Previdenza Valore ended with 5.21%. Results obtained in managing the available assets

were positive and benefitted from the capital gains realized from the sale of government bonds.

The organizational structure underwent constant upgrading to allow reaching the growth and

innovation levels obtained and promoting an ongoing and diversified development of the

Company’s business and value.

Based on the above, the Consolidated Financial Statements submitted include gross profits equal

to € 506.6 m, an increase of € 56.8 m compared to 2012. However, it should be noted that

calculations for net profits for the period, equal to € 256.1 m (€ 273.4 m in 2012) were negatively

affected by the new tax measures introduced in November, that established an 8.5% IRES

surcharge for 2013, with additional tax expenses equal to nearly € 50m.

With reference to the Group’s solvency, in July and December, two capital increase transactions

were finalized for the Parent Company Poste Vita, both subscribed by the Holding Poste Italiane,

for a total of € 350m. The solvency ratio on a consolidated basis stood at 122%. Moreover, the

following paragraph “Significant Events occurred after Year-End” should be referred to regarding

the expected transaction for the issuance of a subordinated loan.

8

ECONOMIC AND MARKET ENVIRONMENT

The International Economy

In 2013, the global economy was characterized by limited growth, slightly lower than in 2012. The

most significant slowdown was registered in emerging countries, while industrial economies were

once again characterized by very different growth modalities. Among the major OECD countries,

the US continued their expansion, even though at a lower rate compared to 2012. Japan

maintained stable growth levels, while Europe continued to register a downturn that started

showing improvement only in the last months of the year, despite a significant decrease in its debt

crisis. Based on the most recent IMF’s estimates, global growth at the end of 2013 should settle at

approximately 2.9% (compared to 3.2% in 2012), again driven by emerging countries (4.5%), while

the major OECD countries should follow a more balanced trend: US +1.6%, Europe -0.4%, Japan

+2.0% (IMF Source, World Economic Outlook, October 2013).

The year just ended was once again characterized by significant activity on the part of central

banks, due to the implementation of various direct and indirect monetary policy measures within a

scenario of overall inflation slowdown, mainly in advanced economies.

On the other hand, the absence of inflationary risks was determined by a weak demand,

particularly in Europe, where price trends registered a marked deceleration mostly in the last two

quarters of 2013, and especially in periphery countries, mainly due to low rate of consumer

spending and more generally to a consistent appreciation of Euros against principal global

currencies and to raw material price trends.

In the US, mainly due to a series of restrictive tax measures, the economic expansion rate

decreased compared to 2012 (1.7% vs. 2.8%), while business confidence indexes and the real

estate sector continued to recover. This situation was aided by the slow yet constant improvement

of the labor market, which in 2013 registered a gradual increase in the number of jobs (standing at

nearly 200 thousand units per month, reducing the unemployment rate at the end of 2013 to 7%

(compared to 8% at the beginning of the year). Within this scenario, the inflation trend remained

below the 2% target set by the Fed, due to the moderate increase of salaries and unit labor costs.

The US economy’s general improvement in the last months of the year led the Federal Reserve to

announce its exit from Quantitative Easing, while maintaining an accommodative policy. In 2013,

Democrats and Republicans clashed on the approval of the federal budget and overrunning the

debt limit. Difficulties in reaching an agreement on rising the public debt limit led to the temporary

closure of the federal public sector in the first weeks of October, with the risk of having potentially

negative impacts on the growth trend. The agreement on increasing the public debt limit was

reached in mid-October, determining immediately resuming federal activities; the effects of the

suspension of activities were not significant.

In Japan, growth in 2013 stood at nearly 2% (stable compared to 2012), supported by the positive

effects of Abe’s economic policy, as demonstrated by the significant recovery of the Tankan index,

which stood back at the highest levels of the last 5 years.

In China, in 2013, growth stood, on average, at higher levels than in other emerging Asian

countries, essentially stable compared to 2012 (7.6%). The increase in exports and consumption

allowed offsetting the investment slowdown, particularly private investments. As planned by the

authorities, the increase in the domestic demand is favoring a balance in accounts with foreign

9

countries: the current account surplus decreased from over 10% to 3%. Inflation also gradually

decreased, standing between 2 and 3%, while the unemployment rate stood below 4%.

The Eurozone continued to have a weak economic growth (-0.4%) in most member countries,

despite the considerable reduction of negative effects related to the debt crisis. 2013 marked the

end of the recession that begun in 2011, also thanks to small recovery signs in periphery countries

as of the second quarter, later confirmed during the third quarter. GDP results technically

interrupted the recession both in Spain and Italy (despite closing 2013 respectively with -1.3% and

-1.8%). At year-end, Ireland (+0.6% at the end of 2013) officially exited the International bailout

program; encouraging signs came from Portugal (-1.8%). Despite a temporary weak phase in the

first months of the year, Germany (+0,5%) showed a step up in its economy, confirmed by leading

economic indicators, and a good performance despite a strengthened Euro. In the UK, 2013 was

characterized by a sharp economic recovery (1.4%). Growth was a surprise in all main sectors

(residential investments, consumption, exports and corporate investments), despite the fact that

budget and public debt levels continued to be worrying and the labor market did not significantly

improve. The unemployment rate decreased slowly and went back below 7.5% only at the end of

2013. Elements of Eurozone growth were negatively impacted by public spending, though less

than in 2012, and affected by restrictive tax policies implemented in all major countries; private

expenditures were affected by a decrease in consumer purchasing power deriving from both a

decrease in labor income and employment (that continued to drop until the third quarter of 2013).

Foreign demand was the only element that did not drop last year. Within this scenario, inflation

continued to decrease, particularly in the last two quarters and mainly in periphery countries,

standing below 1% at the end of 2013, well below ECB targets. Fears of a deflationary trend

caused ECB to act directly on the reference rate, (decreasing it from 0.75% to 0.5% in May and

from 0.5% to 0.25% in November), thus increasing chances of further action by the ECB with

nontraditional monetary instruments. These include long-term refinancing operations to banks

(LTRO) to support conditions for the supply and demand of credit for businesses and families, with

10

the objective of improving the transmission of monetary policy and lowering the level of bank

fragmentation.

In Italy, 2013 ended with a -1,9% negative economic growth, thus marking a second consecutive

year of recession, lesser compared to 2012 (when the GDP decreased by -2,5%). Supported by

exports and by stock replenishment, the GDP interrupted its drop only in the third quarter of 2013.

In December, business confidence indexes were on the rise, standing at the same levels of early

2011, projecting an improvement in industrial activities also for early 2014, even if strongly affected

by a weak domestic demand due to the fragile labor market, by disposable income trends and by a

credit crunch. Within this scenario, the trend growth of consumer prices1 decreased from 2.4% in

January to 0.7% in December, affected by both a drop in energy prices and a by weak domestic

demand.

1 Measured according to FOI (National consumer price index for blue- and white collar worker households).

11

Financial Market Trend

In 2013, the Eurozone bond market was characterized by a narrowing of the spread of peripheral

versus core government bonds with any maturities, as a combined effect of the overall decrease of

peripheral bond returns and of the increase of the German bond returns. The downward trend of

peripheral countries’ returns is attributed mostly to purchases made by domestic investors, but

also to an increasing interest by non-domestic investors, looking for higher returns in the European

Monetary Union’s reduced break up risk scenario. After an early stage where the spread of

periphery countries increased (the BTP-Bund spread on 10-year maturities reached its peak in

March 2013 at 350 basis points, in a context of increasing returns), in spring, the ECB’s decision to

implement additional monetary easing measures favored a reversal in the spread’s trend. In May,

the 25 basis point reduction in the reference rate (from 75 to 50 basis points) coincided with the

minimum annual returns both for 10-year BTPs (3.76%) and for 10-year Bunds (1.16%).

12

Following macroeconomic data improvement in the US, the Federal Reserve announced a

possible reduction in the purchase of government bonds as of the year’s last quarter (tapering):

this resulted in a sale phase of US government bonds and a subsequent increase in returns in the

EU, both for bonds issued in core countries and in peripheral countries. Afterwards, the Federal

Reserve eased the timeframe for the beginning of tapering, emphasizing that removal of

expansion stimuli will take place gradually, thereby reassuring investors on the long-term keeping

of zero interest rates. Despite this, US government bond returns only showed a partial variation,

maintaining the overall upward trend accentuated by the announcement, during the December

meeting, that tapering would start as of January 2014. The increase in US government bond

returns, combined with an improvement in EU macroeconomic data, led to a rate rise in German

government bonds, where, during the year, the ‘flight to quality’ effect characterizing the 2011-

2012 period was progressively reduced. During 2013, market uncertainty decreased significantly

both for core and for peripheral bonds, also due to a lower impact of potential crisis outbreak

compared to the recent past. In particular, the need for a bailout plan for Cyprus and Slovenia at

the beginning of the year, uncertainty on the outcome of Italy’s political elections, negotiations to

grant another bailout installment to Greece and, lastly, Portugal’s potential political crisis last July,

led to rises in returns that were however limited in amount and duration. At the same time the ECB

committed to keep the cost of money low for a lengthy period of time (‘forward guidance’), thus

leading to an additional cut in the reference rate in November (from 50 to 25 basis points), aimed

at stopping the downturn trend of inflation determined by the continuing consumption drop and

severe tax measures (particularly in Europe’s peripheral countries). The yield on ten-year bund,

from 1.3% in January 2013, reached their all time low of 1.17% in June coinciding with the

consolidation process slowdown at European level. The year ended at 1.9%, with a 60 bps

increase.

10-year btp returns decreased from 4.5% in January 2013 to 4.1% at the end of December, while

2-year btp returns from 2% at the beginning of the year to 1.3% at year-end. The return curve

flattened during the year, due to a strong demand from domestic and foreign investors linked to a

decrease in credit risk perception due to ECB’s actions and to an improvement in the fundamental

elements. The btp – bund spread on 10 year maturities consequently decreased from 318 bps at

the beginning of 2013 to 219 bps at year-end.

13

In 2013, the stock markets positive trend that had started in 2012 continued, and some listings,

i.e. US and Germany, reached new historical peaks, (Dow Jones above 16,000 points, S&P500

above 1,800 and Dax above 9,600 points). Reasons for the market increase were mainly linked to

expansionary monetary policies carried out by the main central banks who injected high cash

amounts into the system, and to a progressive improvement of the macro scenario in some major

global economies.

Despite easing tensions in Europe regarding the sovereign debt of peripheral and some core

countries, the European listings’ performance was positive, yet lower than those registered in the

US and Japan, due to the weak macroeconomic context. An exception to this was the German

stock market reaching its historical peak above 9,600 points. This result was due to a relatively

more solid economic recovery and by Angela Merkel’s reelection as government head in April’s

political elections.

Japan’s brilliant stock market trend, that reached 16,175 points, its best performance since

November 2007, is mainly attributable to the extraordinary expansionary monetary policy

measures announce by Japan’s Central Bank (BoJ) in April (a new significant asset purchase

program), to the implementation of a new Abe government reform plan aimed at relaunching the

economy and to a weak yen which favored exports. In China, the economy slowdown continued,

with growth standing at 7.6% in 2013, lower that the 7.7% rate of 2012, but higher than the

expected 7.5% rate. Even if China continued to have high growth rates, it was almost half what it

was in 2009 (14.2%), decreasing for the third consecutive year. Among the reasons for the

reduction are an increase in labor costs, environmental problems, a weak global demand and an

excessive production capacity in certain sectors.

With regard to currencies, in particular the Euro, in 2013, a different trend was registered in the

first half compared to the second half of the year. In the first six months, the Euro was relatively

weak and, after reaching its peak above 1.37 at the beginning of the year, it started a decline in the

following months. However, the trend was not uniform and the Euro rose again to nearly

1.28/1.30. The second part of the year was characterized by a gradual appreciation of the

European currency supported by positive macro European data (even though it was not

unidirectional) during the summer, leading to a return of foreign investors; subsequently, the

currency was supported by the introduction of the ECB’s forward guidance (with favorable

monetary conditions maintained as well as low rates) and by the increasing possibility of the US

beginning tapering.

In 2014, global expansion is expected to continue, even though at a moderate pace. Emerging

countries, particularly China, should undergo a structural economic reform process in order to

achieve a more balanced development. However, such process could cause an additional growth

slowdown, at least temporarily. Despite the above, having the Eurozone definitely overcome

recession, the US situation improvement with Japan consolidating its economic cycle should favor

a recovery in the global trade, thus subsequently providing positive inputs to emerging economies.

In this scenario, inflationary pressures should continue to be limited, since the system’s abundant

liquidity does not seem to threaten a price overheating. This holds truth, in particular, for the

Eurozone where, even though the situation is improving, the context is still weak, requiring

favorable action by the ECB, perhaps including additional expansionary monetary policy

measures, both traditional and nontraditional. Priority is given to recovering the credit market which

would allow better monetary policy implementation, and lower the level of bank fragmentation. In

14

this scenario, ECB efforts in defining and carrying out a Comprehensive Assessment of bank

budgets in the Eurozone were fundamental. This assessment started in November 2013 and will

be completed by November 2014.

Insurance Market Trend

Total premiums collected in 2013 in Life and Non-Life classes amounted to € 119 billion, rising by

13% compared to the previous year and significantly recovering the 2011 reduction.

Life Classes

In the difficult macroeconomic context that affected Italy once again in 2013, the insurance market

registered a decidedly positive trend. A forecast based on early available data, shows that total

turnover of companies operating in Italy (Italian, extra EU and EU) should be equal to nearly € 85

billion, +18.1% compared to 2012. If this figure is confirmed, it would represent the highest Life

Class turnover ever, after the record-breaking € 91 billion collection in 2010, as well as a trend

reversal compared to the decrease registered in both 2011 and 2012 ( an average of -11% in the

period).

This result can essentially be attributed to approximately € 74 billion in new collection (+31%) and

to nearly € 12 billion of premiums related to subsequent yearly installments (+2%) issued in 2013,

but referring to contracts written in previous years. The new collection’s important growth is mainly

attributable, for 16% of its total amount, to € 12 billion (+38%) of premiums issued by EU

companies operating in Italy under the LPS- Freedom to Provide Services system, essentially

belonging to Italian banking and insurance groups but not subject to the same regulatory systems

as Italian companies, particularly with regard to distribution.

In addition to the EU companies, the large growth result of the new collection was significantly

favored by the “postal” channel (that increased its market share from 14.6% in 2012 to 15,5% in

2013) as well as by the “Insurance banking” channel that represented nearly 44% of the total Life

collection. A positive growth – even if lower compared to the market average – was obtained by

the “agent” channel (+6.8%) with an incidence on the total collection dropping to nearly 23.6%

compared to 27% in 2012. On the other hand, collection in the “promoter” channel also dropped

(by nearly -15% ) after the significant growth registered in 2012.

Regarding the new collection’s structure, Class I increased by 36%, accounting for nearly two

thirds of the total new premiums. Class III increased at a slower pace compared to the average

increase (+22%) and slightly reduced its share to one third of the total amount. A little less than

80% of this Class’ collection, equal to nearly € 19.5 billion in absolute value, was attributable to

products such as “Unit-linked” policies, mainly sold by the bank channel (+57%, € 5.3 billion in

absolute value). The collection of the so-called “Protected Unit-Linked policies” soared, reaching €

4.2 billion in absolute value, of which 3.2 sold by companies operating under the LPS- Freedom to

Provide Services system. “Index Linked” policies collection was irrelevant and essentially these

policies are no longer distributed in Italy.

Total policies sold in 2013 were equal to nearly 3.3 million contracts (+9% compared to 2012).

Pure risk policies continued to decrease, by -2.2%, which added to -13% registered in 2012,

accounting for 17% of the total. Supplementary pension plans also showed a decline and for the

first time in years, the collection of new individual pension plans dropped by nearly two percentage

15

points, standing at 356,000 in absolute value. Contract collection in Class IV, relative to critical

illness insurance policies, was absolutely insignificant, with slightly more than 30,000 contracts

sold throughout the year, less than 1% of the total.

Based on the type of offers, the single premium collection accounted for slightly more than 50% of

new contracts and for nearly 95% of the new premiums group, with a significant increase in the

average premium that rose to € 42k against € 26k in 2012. The other 50% of contracts had

recurrent premiums for lower amounts which however allowed operators to automatically rely on a

high number of new premiums in future years.

General data analysis shows a few conflicting aspects. The figure growth seems to be structurally

solid, with a more defined trend not depending on “technical rallies”. The Class mix is once again

more balanced compared to the past, as well as the mix between annual premium and single

premium policies. Less positive aspects were found regarding the market of the most typical

insurance policies with an immediate social importance that registered a decline. This is formed by

risk protection insurance against risks linked to ageing – pensions and non self-sufficiency – on

which an inadequate activity was carried out by both the bank channel, with a few important

exceptions, and by the financial promoter channel. Good results were instead obtained in this

segment by traditional channels. However, their contribution was nonetheless limited in absolute

value compared to the size of the social need expressed by the demand. On the whole, the Life

market seemed to have found its own balance and growth. In 2013, however, this market did not

show its ability to effectively play the role of “third pillar” that the new welfare system expected, on

the basis of which the most economically relevant issues were expected to be fully integrated

between the public and the private sector, being our country undeniably heading in the latter’s

direction.

Non-Life Classes

Non-Life classes ended 2013 with a collection reduction. Data pertaining to Italian and extra EU

companies indicated collection volumes of nearly € 33.7 billion, showing a nominal value

reduction of 4.9% compared to 2012.

In 2013, premium collection for classes not linked to the auto business reached € 15 billion,

essentially in line compared to 2012. With reference to the main aggregates, collection relative to

Personal Accident Insurance (Injury and Illness) was essentially stable as was Property Insurance

(Fire and other damages); classes that were mostly linked to the economic situation (Auto, more

Commercial) registered a significant reduction, while the general Third Party Liability insurance

rose also thanks to insurance obligations introduced in various professional categories. Legal

Protection and Counseling classes also rose, confirming a multi-year positive trend attributable to

the increasing diffusion of this coverage in various areas. With reference to distribution trends, the

main 2013 element was the increase in the amount dealt with by banks and post offices, which

rose to over 6% after the contraction registered in 2012, as a result of the sharp production

slowdown linked to the disbursement of mortgages and loans.

Forecasts for 2014 do not generally expect a collection increase in the Non-Life sector. Price

reductions continue to condition the development of Third Party Liability insurance, also affected

by various regulatory measures aimed at reducing the Automobile Third Party Liability insurance

(such as the possibility of installing a car black box upon signing the contract; the possibility of

including a clause prohibiting the transfer of damage rights to third parties without the insurer’s

consent, etc); moreover, the significant stagnation expected for the car market will not represent

16

an expansionary driver for the element linked to auto body repair insurance. The Non-Life, Non-

Auto sector foresees a moderately positive trend, equal to 1.5% in nominal terms, dropping to

below 1% for Italian and extra EU companies. Positive expectations mainly concern home

insurance characterized by an increasing spread of risk perception, while business insurance

should still be affected by the continuously complex economic situation. Within this context,

distribution through banks and post offices is expected to increase further.

MANAGEMENT TREND SUMMARY

Group activity is divided into two business areas: Life and Non-Life. The Group’s main activity is

carried out by the Parent Company Poste Vita in the “Life” sector, while “Non-Life” activity is

carried out by the subsidiary Poste Assicura and, marginally, also by Poste Vita.

(data in million Euros)

RECLASSIFIED INCOME STATEMENT

Non-life insurance Life insurance Total Non-life insuranceLife insurance Total

Net premiums earned 38.7 13,161.5 13,200.2 28.1 10,507.6 10,535.6

Gross earned premiums 61.8 13,172.6 13,234.4 45.3 10,516.7 10,561.9

Earned premiums ceded (23.1) (11.1) (34.2) (17.2) (9.1) (26.3)

Fee and commission income 0.0 0.2 0.2

Net financial income from assets related to traditional products 3.2 2,191.9 2,195.1 2.9 1,793.4 1,796.3

Net financial income from assets related to index and unit linked

products717.2 717.2 1,360.3 1,360.3

Net change in insurance provisions (14.7) (15,260.6) (15,275.3) (9.1) (12,987.4) (12,996.5)

Claims paid (12.5) (5,166.0) (5,178.5) (8.9) (5,539.6) (5,548.5)

Change in insurance provisions (9.9) (10,106.9) (10,116.8) (6.7) (7,452.9) (7,459.6)

Reinsurers' share 7.7 12.3 20.0 6.6 5.0 11.6

Investment management expenses (0.3) (26.2) (26.5) (0.2) (21.4) (21.6)

Acquisition and administration costs (12.4) (357.5) (369.9) (12.4) (264.1) (276.5)

Net commissions and other acquisition costs (4.7) (325.0) (329.8) (6.0) (232.8) (238.8)

Operating expenses (7.6) (32.5) (40.2) (6.5) (31.2) (37.7)

Other net revenues/costs (2.1) (14.9) (17.1) (0.9) (17.8) (18.6)

EBITDA 12.4 411.3 423.7 8.4 370.8 379.3

Net financial income from available assets 101.3 101.3 93.4 93.4

Interest expenses on subordinated debts (18.5) (18.5) (22.8) (22.8)

EARNINGS BEFORE TAXES 12.4 494.2 506.6 8.4 441.4 449.9

Income taxes (5.1) (245.4) (250.5) (2.6) (173.9) (176.4)

EARNINGS AFTER TAXES 7.3 248.8 256.1 5.9 267.6 273.4

2013 2012

17

Life Business

Data in mill ion Euros

RECLASSIFIED INCOME STATEMENT

31/12/2013 31/12/2012

Net premiums earned 13,161.5 10,507.6 2,654.0 25%

Gross earned premiums 13,172.6 10,516.7 2,656.0 25%

Earned premiums ceded (11.1) (9.1) (2.0) 22%

Fee and commission income 0.2 (0.2) -100%

Net financial income from assets related to traditional products 2,191.9 1,793.4 398.5 22%

Net financial income from assets related to index and unit linked

products717.2 1,360.3 (643.1) -47%

Net change in insurance provisions (15,260.6) (12,987.4) (2,273.2) 18%

Claims paid (5,166.0) (5,539.6) 373.6 -7%

Change in insurance provisions (10,106.9) (7,452.9) (2,654.0) 36%

Reinsurers' share 12.3 5.0 7.3 146%

Investment management expenses (26.2) (21.4) (4.8) 27%

Acquisition and administration costs (357.5) (264.1) (93.5) 34%

Net commissions and other acquisition costs (325.0) (232.8) (92.2) 42%

Operating expenses (32.5) (31.2) (1.3) 6%

Other net revenues/costs (14.9) (17.8) 2.8 -17%

EBITDA 411.3 370.8 40.5 11%

life insurance

Change

With reference to the production and portfolio trend, as indicated earlier, in 2013, earned

premiums, net of the reinsurance share, reached € 13,162m at year-end, rising by 25.3%

compared to € 10,508m in 2012.

Net financial income relative to assets related to traditional products amounted to € 2,192m, on the

rise compared to € 1,793m in 2012 thanks to the increase in the amounts traded. Coverage for

index and unit linked products showed positive financial results in 2013 for nearly € 717m, almost

entirely reflected in the corresponding technical provision variation.

The change in the insurance provision, equal to € 10,107m (€ 7,453m in 2012), mainly refers to

the increase in insurance liabilities linked to the aforesaid commercial trends and to the

corresponding revaluation based on the positive financial results obtained.

Settlements for insurance services to customers in the period were equal to nearly € 5.2 billion and

included policy expirations for nearly € 2.2 billion. With regard to surrenders, data indicates a total

of nearly € 2.4 billion, in line with 2012 data. The impact of surrenders, with respect to the initial

reserves, is around 4.3%, down from 4.9% in 2012 and much lower than the market average.

The intermediary Poste Italiane received commissions for distribution and collection activity equal

to nearly € 339m (€ 244m as of December 31, 2012), with an accrual of € 325m (€ 233m as of

December 31, 2012). Total operating costs amounted to € 33m, a 6% increase compared to € 31m

in 2012, due to both the strengthening of the workforce and to costs incurred during the year

relative to major IT projects aimed at a functional/infrastructural upgrade of the most important

business supporting systems.

18

Non-Life Business

Data in mill ion Euros

RECLASSIFIED INCOME STATEMENT

31/12/2013 31/12/2012

Net premiums earned 38.7 28.1 10.6 38%

Gross earned premiums 61.8 45.3 16.6 37%

Earned premiums ceded (23.1) (17.2) (5.9) 35%

Fee and commission income 0.0

Net financial income from assets related to traditional products 3.2 2.9 0.3 11%

Net financial income from assets related to index and unit linked

products0.0

Net change in insurance provisions (14.7) (9.1) (5.7) 71%

Claims paid (12.5) (8.9) (3.6) 44%

Change in insurance provisions (9.9) (6.7) (3.2) 47%

Reinsurers' share 7.7 6.6 1.1 17%

Investment management expenses (0.3) (0.2) (0.1) 44%

Acquisition and administration costs (12.4) (12.4) 0.1 11%

Net commissions and other acquisition costs (4.7) (6.0) 1.2 -22%

Operating expenses (7.6) (6.5) (1.2) 23%

Other net revenues/costs (2.1) (0.9) (1.3) 146%

EBITDA 12.4 8.4 3.9 30%

Non-life insurance

Change

Annual portfolio premiums for Non-Life Business referred to policies sold in 2013 amounted to

nearly € 42.5 m. Moreover, considering the characteristics of Poste Assicura S.p.A.’s portfolio,

which provide that 92% of the premium payments related to the “Protezione beni & patrimonio”

(Goods and Property protection) Line and “Persona” (Personal) Line be paid in monthly

installments, premiums issued in 2013 amounted to € 71.4 m. In terms of accrual accounting, due

also to the premium variation (calculated pro rata temporis based on each product’s contract

duration as a portion of premiums issued, detracting acquisition expenses) this means that

premiums issued in 2013 amounted to nearly € 61.8 m (€ 38.7 m net of reinsurance).

During the year, charges for claims were equal to € 22.4 m. This figure refers to the provisions for

outstanding claims during the year (including provisions for claims incurred but not reported), equal

to € 9.9 m, and to claims paid including settlement charges, amounting to nearly € 12.5 m during

the year. Considering the reinsurance portion, equal to € 7.7 m, the variation in technical

provisions amounted to € 14.7 m at year-end.

The intermediary Poste Italiane received commissions for distribution and fund collection activities

for nearly € 15m (€ 11m as of December 31, 2012), that, net of reinsurance commissions and the

variation in deferred acquisition costs registered in the period, amounted to a total of € 4.7 m (€ 6m

as of December 31, 2013)

Operating costs were equal to € 7.6 m (€ 6.5 m as of December 31, 2012) and referred to the

development of the Group’s organizational structure. Moreover, implementation activities of the

current IT system continued.

19

INDUSTRIAL ACTIVITY

Business trends

With reference to the production and portfolio trend, as indicated earlier, in 2013, earned

premiums, net of the reinsurance share, reached € 13,200.2 m at year-end, rising by 25.3%

compared to € 10,535.6 m in 2012. Premium details, according to Life and Non-Life sectors, are

included here below:

31/12/2013 31/12/2012

Class I 13,029.8 9,392.3 3,637.5 38.7%

Class III 79.2 1,097.8 (1,018.6) (92.8%)

Class IV 0.8 0.1 0.7 1340%

Class V 62.9 26.5 36.4 137.0%

“Life” gross premiums 13,172.6 10,516.7 2,656.0 25.3%

Life premiums ceded to reinsurers (11.1) (9.1) (2.0) 21.8%

“Life” total net earned premiums 13,161.5 10,507.5 2,654.0 25.3%

“Non-life” gross premiums 71.4 51.2 20.1 39.3%

Earned premiums ceded (23.6) (17.5) (6.0) 34.4%

Change in provision for unearned premiums (9.6) (6.0) (3.6) 59.6%

Change in the reinsurers' provision for unearned premiums 0.4 0.3 0.1 30.5%

“Non-life” total net earned premiums 38.7 28.1 10.6 37.9%

Total net earned premiums 13,200.2 10,535.6 2,664.6 25.3%

(data in million Euros)

Change

Life Business

As previously mentioned, considering the economic context in which the Group has been

operating, Life insurance commercial results were excellent, with a total production of € 13,173 m

(+25.3% compared to 2012) which allowed the Group to consolidate the growth trend of the last

three years. Considering also that Italian market production stood at nearly € 85 billion, in terms of

market share on total premiums, the market share rose from 14.6% in 2012 to the 15.5%

expected at the end of 2013.

The composition of gross “Life” premiums was as follows:

“Life” gross premiums composition 31/12/2013 31/12/2012

Periodical premiums 814.8 559.6 255.2 45.6%

- of which first annuity 305.3 162.7 142.6 87.6%

- of which subsequent annuities 509.5 396.9 112.6 28.4%

Single premiums 12,357.8 9,957.1 2,400.7 24.1%

Total 13,172.6 10,516.7 2,655.9 25.3%

(data in million Euros)

Change

20

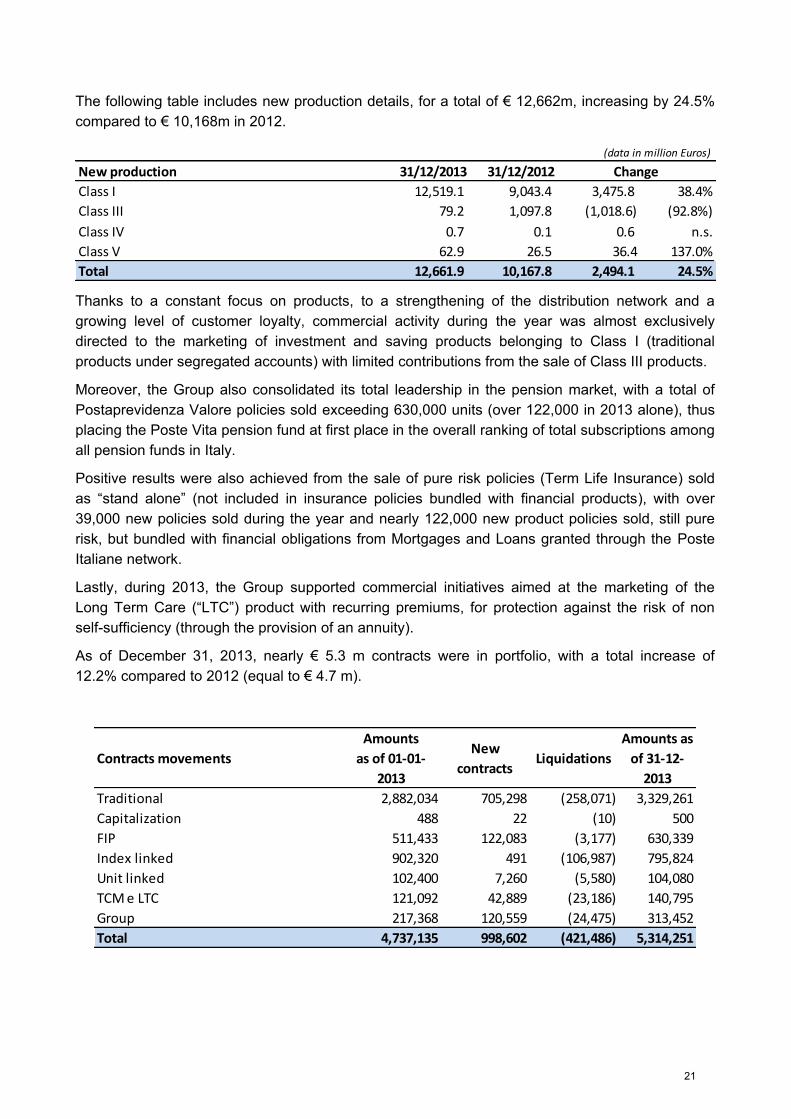

The following table includes new production details, for a total of € 12,662m, increasing by 24.5%

compared to € 10,168m in 2012.

New production 31/12/2013 31/12/2012

Class I 12,519.1 9,043.4 3,475.8 38.4%

Class III 79.2 1,097.8 (1,018.6) (92.8%)

Class IV 0.7 0.1 0.6 n.s.

Class V 62.9 26.5 36.4 137.0%

Total 12,661.9 10,167.8 2,494.1 24.5%

(data in million Euros)

Change

Thanks to a constant focus on products, to a strengthening of the distribution network and a

growing level of customer loyalty, commercial activity during the year was almost exclusively

directed to the marketing of investment and saving products belonging to Class I (traditional

products under segregated accounts) with limited contributions from the sale of Class III products.

Moreover, the Group also consolidated its total leadership in the pension market, with a total of

Postaprevidenza Valore policies sold exceeding 630,000 units (over 122,000 in 2013 alone), thus

placing the Poste Vita pension fund at first place in the overall ranking of total subscriptions among

all pension funds in Italy.

Positive results were also achieved from the sale of pure risk policies (Term Life Insurance) sold

as “stand alone” (not included in insurance policies bundled with financial products), with over

39,000 new policies sold during the year and nearly 122,000 new product policies sold, still pure

risk, but bundled with financial obligations from Mortgages and Loans granted through the Poste

Italiane network.

Lastly, during 2013, the Group supported commercial initiatives aimed at the marketing of the

Long Term Care (“LTC”) product with recurring premiums, for protection against the risk of non

self-sufficiency (through the provision of an annuity).

As of December 31, 2013, nearly € 5.3 m contracts were in portfolio, with a total increase of

12.2% compared to 2012 (equal to € 4.7 m).

Contracts movements

Amounts

as of 01-01-

2013

New

contractsLiquidations

Amounts as

of 31-12-

2013

Traditional 2,882,034 705,298 (258,071) 3,329,261

Capitalization 488 22 (10) 500

FIP 511,433 122,083 (3,177) 630,339

Index linked 902,320 491 (106,987) 795,824

Unit linked 102,400 7,260 (5,580) 104,080

TCM e LTC 121,092 42,889 (23,186) 140,795

Group 217,368 120,559 (24,475) 313,452

Total 4,737,135 998,602 (421,486) 5,314,251

21

Non-Life Business

In 2013, nearly 323 thousand new Non-Life contracts were sold, with a 30% increase compared to

the previous year and an approximate daily average of 1,060 contracts sold. As of December 31,

2013, gross written premiums were equal to nearly € 71.4 m (+39% compared to the same period

in the previous year).

2013 Inc% 2012 Inc% Change Change %

Personal Accident 28.8 40% 21.8 43% 7.0 32%

Health 6.1 9% 5.6 11% 0.5 9%

Any other damage to property 4.4 6% 4.0 8% 0.4 11%

Fire and natural perils 6.0 8% 4.0 8% 2.0 51%

Other Liabilities 10.0 14% 7.0 14% 3.0 43%

Financial loss of various nature 11.9 17% 6.1 12% 5.8 94%

Legal expenses 1.6 2% 1.2 2% 0.4 36%

Travel Assistance 2.5 4% 1.5 3% 1.0 64%

Total 71.4 100% 51.2 100% 20.1 39%

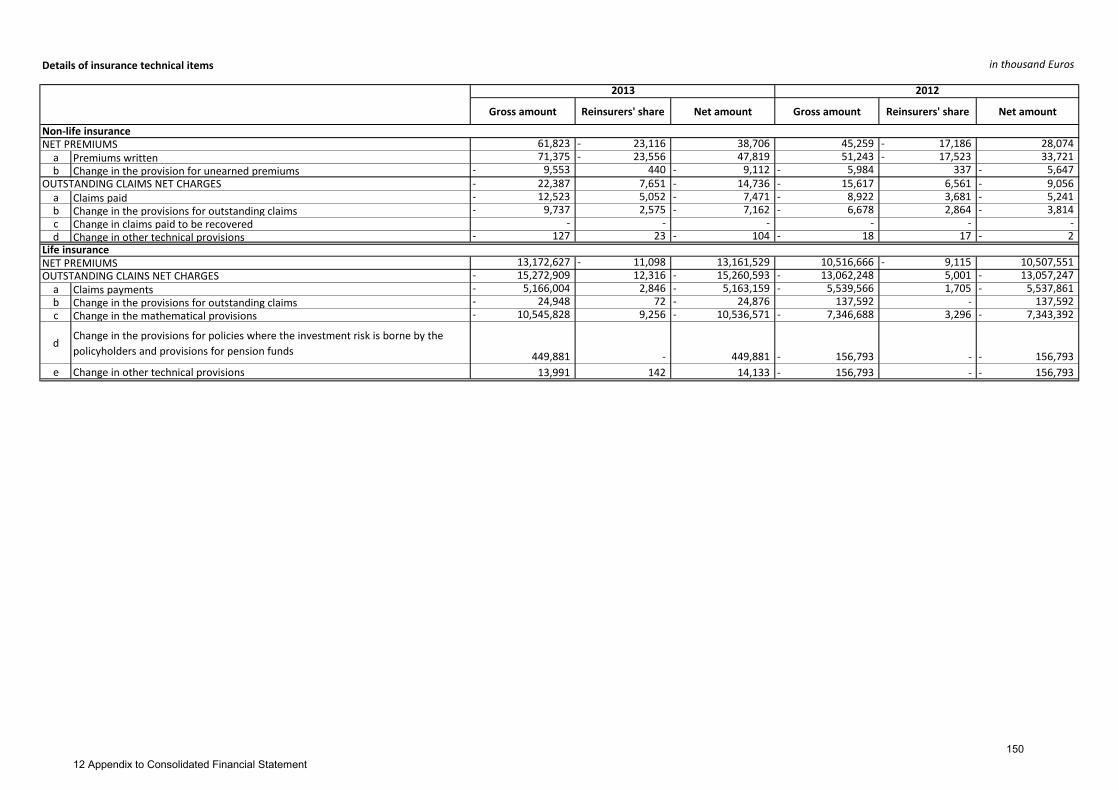

Payments and changes in the insurance provisions

Claims paid during the year amounted to a total of € 5,178.5 m compared to € 5,548.5 m in 2012,

divided as follows:

Non-life insurance 31/12/2013 31/12/2012

Claims paid 10.9 7.6 3.4 44.4%

Claims expenses 1.6 1.4 0.2 18.0%

Total paid 12.5 8.9 3.6 40.4%

Claims paid 5,157.6 5,532.5 (374.9) -6.8%

of which:

Surrenders 2,356.1 2,472.1 (115.9) -4.7%Maturities 2,145.1 2,476.2 (331.0) -13.4%

Claims 656.4 584.2 72.1 12.3%

Claims expenses 8.4 7.1 1.3 18.6%

Total paid 5,166.0 5,539.6 (373.6) -6.7%

Total 5,178.5 5,548.5 (370.0) -6.7%

(data in million Euros)

Change

Life insurance

Regarding Life business, the figure amounted to € 5,166 m as of December 31, 2013, compared to

€ 5,539.6 m in 2012.

Surrender costs amounted to nearly € 2,356.1 m, in line with the 2012 figure (€ 2,472.1 m);

incidence on initial reserves was equal to nearly 4.3%, compared to 5.3% in the previous year

lower, than market levels.

22

The change in the insurance provisions, equal to € 10,116.8 m (€ 7,459.6 m in 2012), mainly

referred to a corresponding increase in liabilities due to the above-mentioned commercial trends.

31/12/2013 31/12/2012

Non-life insurance provisions 9.9 6.7 3.1 46.8%

Mathematical provisions Class I and V 10,545.8 7,346.7 3,199.1 44%

Mathematical provisions Class III (449.9) 156.8 (606.7) -387%

Provisions for outstanding claims 24.9 (137.6) 162.5 -118%

DPL provision (1.4) 92.6 162.5 -118%

Other insurance provisions (12.6) (5.6) (6.9) 123%

Total Life insurance provisions 10,106.9 7,452.9 2,654.0 35.6%

Total 10,116.8 7,459.6 2,657.2 35.6%

(data in million Euros)

Change

Changes in the “Life” insurance provisions, equal to € 10,106.9 m, included changes in the

mathematical provisions relative to Classes I and V for € 10,545.8 m, changes in the insurance

provisions for Class III products for € -449.9 m, changes in the provisions for amounts to be paid

for € 24.9 m, changes in the provisions for Deferred Profit Liability (DPL) for € -1.4 m and changes

in the other isnurance provisions for € -12.6 m.

Considering that production in the year was absolutely limited, the change in the insurance

provisions made for Class III products should be attributed to cash outflow for surrenders and

policy expirations, only partially offset by revaluation following the positive trend of financial

markets.

With reference to reinsurance ceded, charges for claims in the period, that included a change in

the insurance provisions, were equal to € 20m compared to €11.6 m registered in the previous

period, € 12.3 m of which for Life management (€ 5m as of December 31, 2012), as indicated

below:

Non-life insurance 31/12/2013 31/12/2012

Claims paid 4.9 3.4 1.4 42.2%

Claims expenses 0.2 0.3 (0.1) -25.5%

Total paid 5.1 3.7 1.4 37.3%

Change in the insurance provisions 2.6 2.9 (0.3) -9.5%

Non-life total 7.7 6.6 1.1 16.7%

Claims payments 2.8 1.7 1.1 66.6%

Claims expenses 0.0 - 0.0 n.s

Total paid 2.8 1.7 1.1 66.9%

Change in the insurance provisions 9.5 3.3 6.2 187.3%

Life total 12.3 5.0 7.3 146.3%

Total claims paid and change in the insurance provisions 20.0 11.6 8.4 72.6%

Change

Life insurance

(data in million Euros)

23

Distribution

For its product placement, the Poste Vita Insurance Group used the Post Offices of the Holding

Poste Italiane S.p.A., a Company with only one partner - Patrimonio BancoPosta, duly registered

under letter D in the single register of insurance intermediaries as per ISVAP Regulation no. 5 of

October 16, 2006 whose validity was extended until March 2019, with tacit renewal at expiration.

Poste Italiane S.p.A.’s sales network is formed by over 13,000 Post Offices throughout the national

territory. Insurance contracts are signed in the Post Offices by qualified and properly trained

personnel.

Training activity for personnel in charge of product sales continued according to regulation

guidelines. Professional training programs throughout 2013 focused both on new products and on

technical-insurance and pension modules. The latter were created to develop the expertise of

personnel acting as intermediaries, not only in terms of specific skills in relation to the products

offered, but also of general welfare issues and of defining customer needs. Each training initiative

was designed, approved and carried out by the Poste Vita Insurance Group’s competent Business

Department according to Poste Italiane S.p.A.’s training references (in some instances with the

support of external training companies, specialized in the insurance sector).

From an organizational point of view, the territorial monitoring structure within the Poste Vita

Groups was strengthened during 2013. This structure is formed by Area Supervisors who focus

on specific Territorial Areas belonging to Poste Italiane’s network. Area Supervisors carry out a

support and field-training role focused on insurance expertise as well as technical and commercial

know-how.

Moreover, the Company also strengthened its service model for customer support based on a

multi-channel criteria and through an improved website which includes customer services, an area

reserved for the company’s portfolio customers and an upgraded call center that can be reached

through a toll free phone number. The multi-channel service model was developed also to support

the distribution network, in synergy with and integrating the central role carried out by Post Office

personnel.

Reinsurance policy

Life insurance

With reference to Life insurance, reinsurance policies adopted in the past years remained

essentially unaltered in 2013 and therefore the effects of ongoing agreements continued. In

particular, the Parent Company Poste Vita’s reinsurance policy with regard to Life business is

based on risk sharing (“cessioni in quota”) for products that include life insurance coverage or are

linked to the loss of self-sufficiency (LTC); facultative reinsurance (“cessioni in facoltativo”) was

also included for life insurance coverage and for permanent disability by illness (IPM) for Medio

Credito Centrale managers.

The economic effects of these reinsurance policies are described in the Notes.

Non-Life insurance

In 2013, the subsidiary Poste Assicura’s administrative body approved a new reinsurance policy

for the three-year 2013-2015 period that aims at:

24

Optimizing the technical result of the insurance management and the cost of capital, by

complying with the solvency requirements established by Solvency II;

Providing coverage of any irregular trends in the loss ratio, typical of growing portfolios, as well

as any significant events (so-called large losses);

Optimizing the end to end operating management of reinsurance agreements.

In summary, the main changes compared to the previous insurance cession strategy were the

following:

Reinsurance by class – For home, condominium, business and accident products, the 2013

reinsurance policy included cessions implemented through a “bouquet”2 agreement according

to Classes and with commercial premiums, rather than with pure premiums as it had been up

to last year. Only some particular products (i.e.: in the Credit Protection field and the

Postaprotezione SiCura product) continued to include reinsurance cession per product and per

pure premiums.

Retention strategy – According to difference scenario analyses relative to capital consumption

and the effects of reinsurance, it was decided to gradually reduce the stakes sold. This

resulted in a greater risk retention held by the Company. Particularly for the accident class,

share reinsurance integrated with excess coverage for claims was replaced exclusively by

excess reinsurance. This approach was also favored by the possibility of obtaining significant

and reliable figures on the trend characterized by an important growth and by a positive

technical trend. For this purpose, as resolved by the Company’s Board of Directors, an

agreement was reached during the year for withdrawing the portfolio ceded to Catlin Syndicate

2003 at Lloyd’s. The effects of this transaction, described in the Notes to the Financial

Statements, were included in the technical account for the year.

The economic benefits described in the reinsurance policy review will take place in future years,

but are already present in the 2013 financial statement. The total effects on the income statement

for the current year are illustrated in the Notes.

2 In the field of proportional reinsurance, it refers to a reinsurer’s participation in contracts covering more Classes, even different from

one another.

25

ASSET AND FINANCIAL MANAGEMENT

Financial investments

Investment strategies and guidelines are defined by the Boards of Directors through "framework

resolutions", which identify both the essential characteristics, in qualitative and quantitative terms,

of durable and non-durable investment sectors and the strategies for derivative transactions. The

investment process also includes a governance system with corporate bodies (Investment

Committee and Risk Committee).

The Group’s financial investments are mainly those aimed at covering contractual obligations to

policyholders which concern traditional re-valuable life insurance policies whose insured benefit is

prorated to the returns from the management of financial assets enrolled in funds within Poste

Vita’s total assets (so-called Segregated Accounts). The Company guarantees a minimum rate of

return ranging from 0% and 1.5%.on these products payable upon policy maturity.

Investment policies adopted in 2013 showed that the Group maintained an investment

management strategy aimed at combining the need to relate investments to the structure of

obligations to policyholders while preserving a portfolio that ensured return continuity in line with

main competitors. Also according to market trends, investment choices were based on utmost

caution, with a portfolio principally invested in Eurozone government bonds and in “corporate”

bonds with good standing. More specifically, purchases essentially concerned Italian government

bonds, also inflation-indexed ones. Particular attention was also given to the selection and

diversification of the portfolio into non-governmental bonds. To diversify risk according to sector,

and better exploit the earning opportunities offered by the positive economic growth and corporate

receivables trends, the extent of financial, banking and industrial issuers was increased. Moreover,

in order to obtain geographical diversification, there was an increase in the incidence of European

(mainly French, German and Spanish), and US issuers. The drop in Italian government returns

characterizing 2013, offered the opportunity of achieving capital gains on long-term securities. In

December, as foreseen by management strategy, guaranteed ‘Available for Sale’ capital funds

were sold, in the exclusive interest of policyholders. The aim of this transaction was to increase

and level off the future return of segregated accounts. The transfer of these investments generated

losses from disposal for € 11.9 m compared to unrealized losses equal to nearly € 76m in 2012 on

these funds.

Despite commercial and market trends, financial investments as of December 31, 2013 amounted

to a total of € 69,852.2 m, rising by 19.8% compared to € 58,307.4 m in 2012.

Financial investments 31/12/2013 31/12/2012

Investments in subsidiaries, associated companies and joint ventures 197.0 198.7 (1.6) (0.8%)

Loans and receivables 11.5 102.1 (90.7) (88.8%)

A vailable for sale financial assets 59,159.9 47,924.9 11,235.0 23.4%

Financial assets at fair value through profit or loss 10,483.8 10,081.7 402.1 4.0%

Total financial investments 69,852.2 58,307.4 11,544.7 19.8%

Change

Shareholdings referred to the investment in the affiliated company EGI, valued with the equity

method. The Company, owned for 45% by Poste Vita S.p.A and for 55% by Poste Italiane S.p.A,

26

operates in the real estate sector by managing and exploiting non-operating assets that the Parent

Company transferred in 2001. 2013 data show the Company’s equity equal to € 437.8 m with a

negative net result for € 3.7 m, determined by provisions for risks and charges equaling € 5.8 m,

that the Company allocated following a Judgment of the Court of First Instance issued on March 6,

2014 by Rome’s Civil Court. On the basis of this judgment, the Company was sentenced to pay an

indemnity with charges corresponding to that amount. Without this exceptional event, EGI’s EBIT

would have been positive for € 1.4 m, higher than the objective set with the Parent Company.

Loans and receivables mainly referred to the balance of Poste Italiane’s current account and to

provisions for subscriptions linked to capital calls on mutual funds of which the corresponding

stakes had not yet been issued.

Available for Sale financial assets (AFS) mainly referred to securities attributed to segregated

accounts (nearly € 54.1 billion) and also to securities for covering products with contracts linked to

specific assets (nearly € 2.7 billion); the share that refers to the available assets was equal to

nearly € 2.4 billion. The nearly € 11.2 billion growth compared to 2012 is attributed to the positive

commercial results and to returns obtained in the period, together with a fair value increase as a

consequence of the financial markets’ positive trends. As of December 31, securities classified as

AFS showed net capital gains from assessments for nearly € 2,913m, compared to nearly €

1,733m at the end of 2012. Of these, € 2,688m were attributed to policyholders through the

shadow accounting mechanism, as established by the IFRS 4, and referred to financial

instruments included in segregated accounts. The remaining € 225m (€141m in 2012), referred to

net capital gains on AFS securities, which are part of the Company’s “available assets”, and were

therefore attributed to a specific net equity reserve (equal to €148m) net of the relative tax effect.

Financial Assets at Fair Value Through Profit or Loss (FVTPL) amounted to nearly € 10.5 billion (€

10.1 billion as of December 31, 2012) and mainly referred (€ 9.3 billion compared to € 9.7 billion at

the end of 2012) to financial instruments to cover “Unit and Index linked” policies. Of these, nearly

€ 6.1 billion referred to financial instruments to cover Index Linked-type policies for which Poste

Vita directly guaranteed customer capital refund as well as a minimum rate of return. Structured

securities were also present for € 3.2 billion, used to cover "Index Linked"-type policies and for

parts of investments funds used to cover "Unit Linked”-type policies for which Poste Vita did not

offer any guarantee on the capital nor a minimum rate of return. Financial risks for these

investments are totally borne by customers.

Financial Assets at Fair Value Through Profit or Loss also included issuer’s early redemption

bonds and new CMS-type issuances (Constant Maturity Swap) included in the Company’s

segregated accounts for a total of € 1.2 billion. Financial markets’ positive trends recorded capital

gains from assessments for nearly € 10.6 m entirely attributable to policyholders through the

shadow accounting mechanism.

The Group’s security portfolio, in its entirety, was invested mainly in Government bonds (78.6% of

the total) and in corporate bonds (17.8% of the total); the portfolio’s remaining part included UCITS

stakes (Undertakings for the collective investment in transferable securities), shares and warrants.

With regard to derivative transactions, at December 31, 2013 the only derivatives were formed by

Warrants to cover the indexed part of a few Index Linked policies.

The following table includes financial investment distribution according to budget category:

27

Available for sale financial assets 31/12/2013 31/12/2012

Equities 5.3 4.5 0.8 16.8%

Bonds 57,617.7 45,752.2 11,865.5 25.9%

Of which: government bonds 48,853.2 38,759.0 10,094.2 26.0%

corporate 8,764.5 6,993.2 1,771.3 25.3%

Investment Fund units 1,536.9 2,168.2 (631.3) (29.1%)

Total 59,159.9 47,924.9 11,235.0 23.4%

(data in million Euros)

Change

Financial assets at fair value through profit or loss 31/12/2013 31/12/2012

Bonds 6,560.7 6,152.6 408.2 6.6%

Of which: government bonds 5,888.9 5,794.0 94.9 1.6%

corporate 671.8 358.5 313.3 87.4%

Structured bonds 2,983.3 3,102.4 (119.1) (3.8%)

Other financial investments 729.8 708.7 21.2 3.0%

Derivatives 210.0 118.1 91.8 77.7%

Total 10,483.8 10,081.7 402.1 4.0%

(data in million Euros)

Change

Portfolio composition according to issuing country was in line with 2012 and was characterized by

a strong prevalence of Italian government bonds.

Country issuer FVTPL AFS

Australia - 205,8

Austria 17,3 26,0

Belgium 31,0 74,3

Denmark 40,7 37,1

Finland - 33,3

France 263,0 2.089,2

Germany 34,4 398,4

Japan - 9,5

Hong Kong/China - 86,3

Ireland 251,0 183,1

Italy 7.328,8 50.950,4

Luxembourg 382,0 100,8

Malta 239,4 -

Mexico - 30,2

Norway - 37,9

New Zealand - 19,8

Netherlands 224,6 1.403,0

United Kingdom 906,7 752,3

Czech Republic - 5,5

Supranational - 48,2

Spain 56,3 826,8

United States of America 121,1 1.603,7

Sweden 18,6 179,4

Switzerland 566,8 61,0

total 10.481,8 59.161,9

(data in million Euros)

Distribution according to portfolio duration classes is included as of December 31, 2013:

28

(data in million Euros)

Duration AFS FVTPL

up to 1 4.844,2 1.871,4

from 1 to 3 10.627,9 1.180,5

from 3 to 5 8.129,1 5.995,4

from 5 to 7 14.333,9 277,5

from 7 to 10 9.643,6 173,6

from 10 to 15 7.989,9 45,9

from 15 to 20 2.004,2

from 20 to 30 45,9

Total 57.618,6 9.544,3

Net proceeds from financial instruments obtained in 2013 amounted to a total of € 3,004m,

decreasing by nearly € 232m compared to 2012, mainly due to less favorable financial market

conditions compared to those registered at the end of the previous year. A limited part of the net

charges, equal to a total of nearly € 10.6 m (€ 8.8 m in 2012) referred to interest accrued on the

subordinated loan subscribed with Poste Italiane, to interests on bank and post office current

accounts and to the subsidiary EGI’s loss of accrual based accounting registered during the year.

Details on financial proceeds and expenses are included here below:

Interest/Income

Other

income and

expenses

Net

realized

gains

Net

unrealize

d losses

Total income

and expenses

2013

Total income

and expenses

2012

From available for sale financial assets 2,080.9 30.5 148.2 - 2,259.5 1,770.7 488.9 27.6%

From financial assets at fair value through profit or loss 308.2 (0.1) 15.9 420.5 744.5 1,465.2 (720.6) -49.2%

From cash and cash equivalents 9.54 - - - 9.5 14.2 (4.7) -32.9%

From other financial liabilities (18.5) - - - (18.5) (22.8) 4.4 -19.1%

From interests in associated companies - - - (1.6) (1.6) (0.2) (1.4) 635.7%

Total 2,380.2 30.3 164.1 418.9 2,993.5 3,227.0 (233.5) -7.2%

(data in million Euros)

Change

Returns from the Company Poste Vita’s segregated accounts, in the specific periods under

examination (from January 1, 2013 to December 31, 2013), were as follows:

Segregated funds Gross result Average invested capital

Poste Valore Più 4,19% 45.730,2

Posta Pensione 5,21% 1.769,9

(data in million Euros)

Investment activity continued to be monitored also through the use of advanced risk analysis

methods (of a statistical type), carried out with the help of an internal financial-actuarial model. In

the hypothesis of a “central scenario” (based on current commercial and financial situations) as

well as of stress scenarios and of different commercial developments, these methods aimed at

assessing compatibility of risk assessments – implemented with reference to both the guaranteed

minimum rate of return established by contract, and to possible consequences on the budget - as

well as their sustainability, attributable to the assets and returns that were expected each time.

The guaranteed minimum rate of return established by contract ranged from 1.0% and 1.5% on

non consolidated events, therefore it included a very low risk possibility, taking into account

returns obtained to date from segregated and future accounts.

29

Insurance Provisions

As a result of the aforementioned business trends, in accordance with the laws and regulations on

this matter and on the basis of appropriate actuarial assumptions, insurance provisions analytically

calculated for each contract totaled € 68,005m. Based on favorable commercial trends, they

showed a growth of nearly 19.8% compared to € 56,771m in 2012, divided as follows:

Technical provisions 31/12/2013 31/12/2012

Non-l i fe classes :

Provisions for unearned premiums 31.8 25.5 6.3 24.8%

Provisions for outstanding claims 26.1 16.4 9.7 59.5%

Other insurance provisions 4.8 1.4 3.4 233.0%

Total non-life classes 62.7 43.3 19.4 44.9%

Li fe classes : - -

Mathematical provisions 55,723.8 45,175.8 10,548.0 23.3%

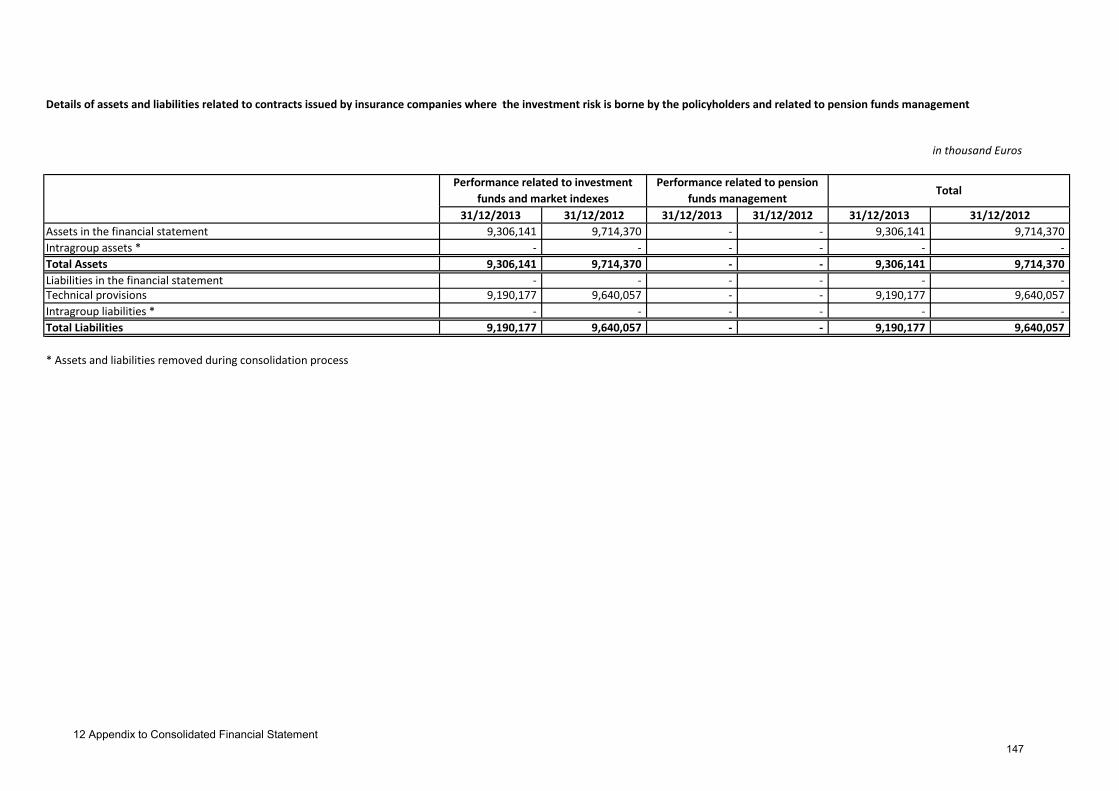

Provisions for policies where the investment risk is

borne by the policyholders9,190.2 9,640.1 (449.9)

-4.7%

Provisions for outstanding claims 229.3 204.4 24.9 12.2%

DPL provision 2,723.6 1,619.3 1,104.4 68.2%

Other insurance provisions 75.5 88.1 12.6 - -14.3%

Total life lines 67,942.5 56,727.6 11,214.8 19.8%

Total 68,005.2 56,770.9 11,234.3 19.8%

(data in million Euros)

Change

In particular, provisions for “Life” classes totaled € 67,942.5 m with a 20% increase compared to

the end of 2012 (€ 56,727.6 m). These provisions were accrued in order to meet all Company’s

obligations and included the mathematical provisions, (€ 55,723.8 m), insurance provisions to

meet Linked products (€ 9,190.2 m), provisions for amounts payable (€ 229.3 m), provisions for

deferred liabilities to policyholders -accrued based on the shadow accounting criteria (DPL) for €

2,723.6 m - and other different insurance provisions (€ 75.5 m). The latter included provisions for

future charges (art. 31 ISVAP Regulations No. 21/2008) for € 72.2 m and provisions for unearned

premiums for supplementary insurance equal to € 3.3 m.

With reference to the shadow accounting method, Class-I products whose revaluation were linked

to the returns of segregated accounts, the financial component of technical provisions was

determined on the basis of actual proceeds and expenses, as established by national accounting

standards. Therefore, capital gains/losses were not considered, generating a time mismatching

between the liabilities assessment and their relative covering assets, included in IAS 39, that were

accounted for at fair value.

This event was monitored, as in previous years, through “shadow accounting”, an accounting tool

introduced by the IFRS 4 to uniformly specify related assets and liabilities; in particular, latent

capital losses and gains identified in financial instruments forming Segregated Accounts were

written among liabilities in technical provisions and were limited to policyholders’ share prorated to

the percentage of retrocession established by contract in Segregated Accounts. This assessment

took into account the impact on the minimum rate of return levels currently applied in contracts.

Criteria used for shadow accounting are illustrated in the Notes.

Contracts classified as “insurance contracts” and those classified as “financial instruments with a

discretionary participation feature”, for which the same accounting and evaluation criteria are used

30

as in Italian balance sheets, were subjected to a LAT - Liability Adequacy Test established by

comma 15 of IFRS4. The test was conducted by taking into account the current value of future

cash flows, obtained by projecting the expected cash flows generated by the existing portfolio as of

year-end, based on adequate hypotheses, over expiration causes (death, termination, surrender,

reduction) and expense trends.

Insurance provisions for Non-Life business totaled € 62.7 m at year-end (€ 43.3 m at 31 December

2012) net of reinsurance ceded, and were formed by: provisions for unearned premiums for € 31.8

m , provisions for outstanding claims for € 26.1 m and other provisions for € 4,8 m. “Other

technical provisions” also included provisions for increasing age for € 0,4 m, as well as provisions

written after assessing the consistency of provisions for unearned premiums for € 4.4 m, as

described in the Notes.

Provisions for incurred but not reported claims (IBNR) totaled € 4.8 m.

The trends of Provisions for unearned premiums and for outstanding claims reflected the growth of

collection trends.

Shareholders’ equity and solvency margin

The Group’s equity as of December 31, 2013 amounted to € 2,763.5 m with a variation of € 655.1

m compared to the beginning of the year, exclusively referring to: i) the share capital increase

undertaken by the Holding Poste Italiane and paid, respectively, in July for € 200m and in

December for € 150m, ii) result of the period and iii) the variation in retained earnings for available

for sale financial assets. For the latter, € 0.5 m were transferred to the income statement during the

year.

As of December 31, 2013, subordinated loans entered into by Poste Vita with the Holding Poste

Italiane amounted to € 540m, (of which € 400m with indefinite maturity), were repaid at market

conditions and governed according to the provisions of article 45, chapter IV, title III of Legislative

Decree No. 209 of September 7, 2005 and subsequent modifications. These are fully available for

the calculation of elements covering the consolidated solvency margin.

The elements forming the solvency margin, calculated with the consolidated method, amounted

to € 3,102m compared to a required solvency margin equal to € 2,545m; consequently, the

solvency ratio at the end of 2013 was equal to 1.22.

31

POSTE VITA GROUP ORGANIZATION

Corporate Governance

This paragraph also describes the “Report on corporate management” established by art. 123 Bis

of Legislative Decree 58/1998 (Consolidated Text on Finance) only for information required under

paragraph 2, letter b. The Governance Model adopted by the Parent Company Poste Vita is

“traditional”, i.e. characterized by the traditional dichotomy between the Board of Directors and

Board of Statutory Auditors.

The Board of Directors meets periodically to review and decide management, results, and

proposals regarding the operational structure, strategic relevance transactions and any other

obligation under current industry legislation. This body therefore represents the central element to

define the Group’s strategic objectives and addresses the policies needed to achieve them. The

Board of Directors is responsible for governing corporate risks and approves the strategic plans

and policies to be pursued. It promotes the culture of control and ensures its distribution to the

various company levels.

The Chairman’s powers are conferred by Company Bylaws and by the Board of Directors’ Meeting

of May 23, 2011. In the same session the Board of Directors awarded to the Chief Executive

Officer the powers of Company management, with the exception for the powers reserved to

themselves by the Board of Directors.

The Board of Auditors is made up of 3 standing members appointed by the Shareholders’ Meeting.

Pursuant to art. 2403 of the Civil Code, the Board of Auditors monitors compliance with the law and

the Bylaws, with the principles of proper administration and, in particular, with the adequacy of the

organizational, administrative and accounting structure adopted by the Company and its actual

operation.

The Group also has a system of conduct and technical rules that ensures consistent corporate

governance through the coordinated management of the decision-making process regarding

aspects, issues and activities of interest and/or of strategic importance or that could generate

significant financial risks.

The governance system is further enhanced by a series of Company Committees chaired by the

CEO, aimed at addressing and controlling corporate policies on issues of strategic value. In

particular, the following committees were established: (i) an Insurance Product Committee, which

analyzes, ex ante, the proposals regarding insurance product offers with related technical and

financial characteristics and verifies, ex post, technical and profit performance and the limits of

risk taking for product portfolios, (ii) a Project Committee, that is responsible for ensuring the

master plan monitoring for the Insurance Group’s strategic projects, of assessing its progress, of