Embed Size (px)

Citation preview

Speaker NameTitle

Organization

Positioning for the Future of Managed Care

Richard S. Edley, PhDPresident and CEO

Rehabilitation and Community Providers Association

Welcome

• Purpose/ Objective– Understanding the Changing Managed Care and HealthCare

Landscape

– Transformation of the MCO Role

– Impact on and Direction for Providers

– MCO- Provider Partnerships

– And More…

• Format– Opening Presentations

– Guided Questions

– Audience Interaction and Participation

• Introductions

RCPA

• Health and Human Services Trade Association

based in PA

• 325 Members/ Agencies/ Hospital Systems

• Mental Health, Drug & Alcohol, Intellectual and

Developmental Disabilities, Criminal Justice,

Children’s Services, Medical Rehabilitation (incl.

Pediatric), Brain Injury, Long Term Services and

Supports

• Provider (Full), Associate, Business, and

Government Members

History of PA Association Managed Care

• Mid 1990’s Association Founded Community

Behavioral HealthCare Network of PA

(CBHNP)

• BH-MCO

• Commercial and Medicaid Business

• Full Risk, Shared Risk, ASO

• $300+ M Revenue; Multi-State

• Sold in 2008

Today

• IDD Managed Care- Future

• Managed Long Terms Services and Supports

(MLTSS)- Today

• RCPA has Founded the Rehabilitation and

Community Services Organization (RCP-SO)

• Brain Injury, Service Coordination Entities

(SCE), Personal Attendant Services (PAS)

• Capitalized and Incorporated

• Partnering with MCOs: Seat at the Table

Future of Managed Care

• Provider-Based Systems (ACO)

• New Risk and Risk/Reward Models

• Value-Based Payment Systems

• Payer-Provider Partnerships

• Transitioning of Traditional BH-MCO Role

• PH/BH/IDD/LTSS Coordination/Integration

• Diversification of Business Lines at the MCO

and Provider Level

• This Leads to the Panel Discussion Today

Speaker NameTitle

Organization

Positioning for the Future of Managed Care

Managed Care, Disrupted.

Dan CavePresident & CEO

Envolve PeopleCare™

We are made wise not by the recollection of our past, but by the responsibility for our future.

George Bernard Shaw

Let’s get it started

It’s about behavioral health…

6-7%of adults suffer from depression annually

5.7 million have bipolar disorder

Anxiety disorders affect

40 million1 in 5

experience mental illness in any given year

17 million dependent on or abuse alcohol

including 1 major depressive episode

…or is it physical health?

Countless undiagnosed | 1x-2x | with diabetes, heart disease and COPD

1 in every 4 DEATHS caused by heart failure

5 million with heart failure

11 million with COPD

1 in every 12 have asthma

29 million with diabetes

…wait…it’s about multiple chronic

conditions, right?

117had one or more

chronic conditions

1 in 4had two or more

million

0% 20% 40% 60% 80% 100%

45% of people with 2 or more chronic conditions have diabetes

78% have high blood pressure

Over and another

of individuals with diabetes also have coronary heart disease

20% 15% have some other form of heart disease

of people with heart disease also have arthritis

49%

Ok, so it’s physical/behavioral

integration?

of people with diabetes also have depression

27% 17% Depression occurs in 17%of people with cardiovascular disease

Rate of depression among individuals post-mi is between 40-65%

0% 20% 40% 60% 80% 100%

adults with mental illness and asthma

6.9million

with substance abuse disorders have co-occurring mental illness

40%of adults

People with substance abuse disorders are

50-300% more likely to have chronic conditions and/or HIV/AIDS

…oh…almost forgot, these are real

people…

29% personally involved in

legal matters in last 3 years

of elder caregivers were simultaneously employed while providing care2/3

Roughly half

of all marriages end in divorce

at work by personal financial matters

distracted1 in 3

hours/week

16 Median of

spent by elder caregivers on hands-on care

The Past

How’s that working out?

The Future

It starts with a question.

Why aren’t we in better health?

Be honest.

Why aren’t I in better health? Why aren’t you?

Think about it…now hold that thought.

Remember these?

What about these?

The future of managed care?

Let’s shape it…

PAST PRESENT FUTURE

• Eligibility• Claim

Adjudication• Claim Payment

• Utilization Management

• Case Management

• Medical Necessity

• Incremental Innovation

?

Environmental Trends

• Lifestyle

• Entitlement culture

• New healthcare

technologies and

treatments

Personal Factors

• Lack of knowledge

• Everyday demands

• Insufficient motivation

19© 2016 Envolve.

Back to that thought you are holding

Let’s be honest…

What gets in the way of health?

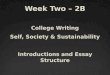

Emergence of health consumer

Consumer

Market

Choices

Information

Consequences

Toto, I’ve got a feeling we’re not in

Kansas anymore…

Seismic shifts

Selected Dynamics Implications

Government Deficits/Debts Cost-sharing, cost-control, prevention

Provider, payor consolidation Scale economies in maturing market, margin protection

Public and Private Exchanges Financing shift to defined contribution vs. defined benefit

Mobile technologies Rising consumer service expectations –“an app for that”

Obesity, Diabetes, Stress – going global Greater % of dollars spent on lifestyle-related conditions

Managed Care 2.0

The next disruption

Indemnity

• Eligibility

• Claim adjudication

• Claim payment

Managed Care 1.0

Unnecessary Supply

• Utilization

management

• Case management

• Provider networks,

discounts

• Provider risk sharing

PASTTransaction -

focus

PRESENTProvider-focus

FUTUREConsumer-

Focus

Managed Care 2.0

Preventable Demand

• Sustainable

consumer behavior

change

• Health and wellbeing

• Physical, behavioral,

legal, financial, etc.

• Motivational science

• Expert teams

• Adaptive technology

The emergence of a consumer

Igniting and sustaining behavior change

Sustainable Behavior Change

• Educate• Enable• Motivate

Modifiable or Preventable Demand

Managed Care 2.0…or,

Managed Care…disrupted. • Consumerism

– Choices

– Information

– Consequences

– Rising expectations,

consumer-centric

• The walls come tumbling down

• Defined contribution financing

• Providers as consultants to

consumers or primary

caregivers

• Re-imagined industry

– People analytics, consumer

marketing

– New entrants, strange

bedfellows

– Community involvement

– Wave of product

development, pilots, new

models

– Kodak moments

Fastest, easiest path to healthy wins

Speaker NameTitle

Organization

Positioning for the Future of Managed Care

Anne McCabePresident, Public Markets

Magellan Healthcare

The Changing Role of MCOs

Magellan: One Model of Healthcare

Evolution Serving Special Populations

Pre-2006

Behavioral health

2006-2009

Specialty solutions/ pharmacy

2013

Pharmacy benefits mgmt

2013

Integrated care-special populations

2014-2016

Special populations/ MLTSS

Acquisitions of AlphaCare, TMG

Integrated health homes, Magellan Complete Careof Florida

Acquisition of Partners Rx

Acquisitions of National Imaging Associates (NIA), First Health and ICORE specialty pharmacy

Market leader inbehavioral healthmanagement

Managed Care Trends

• Population management: Integrated care

models for specialty populations

• Member choice, direction & control/social

determinants

• Value-based purchasing

• Federal funding opportunities

• Provider challenges and potential solutions

Integrated Care ModelsIowa Integrated Health Home Initiative

An adaptation of the medical home model by creating IHH specifically aimed at

serving individuals with complex behavioral health & chronic medical conditions

Integrated Care ModelsIowa Integrated Health Home Initiative

Integrated Care ModelsIowa Integrated Health Home Initiative

Outcomes

Integrated Care Models Co-Located Integrated Health Program: Outpatient BH Provider

Within Offices of a Neighborhood Health Center

Goals

• Improved/elevated independence of individuals with mental illness while

supporting recovery and enhancing the individual’s quality of life

• Establishment and enhancement of relationships with medical providers to realize

improved overall health outcomes

• Decreased frequency, intensity, duration of negative health symptoms

Outcomes

• Increased access to care in 27% of members who had not previously received BH

services

• 50% of members had a score consistent with fewer depressive symptoms

• Self-reported improvement in provider relationship (9% increase), improved blood

pressure (9%), improved overall physical/BH (14%)

Provider Model

• Contracted BH outpatient provider co-located staff in the FQHC

• Increases access and coordination of services for members

NEW YORK

• Medicaid Managed Long-Term

Care Plan

• For those with chronic illness and

disabilities who want to continue to live

in their home

• Participant in the FIDA Duals

Demonstration

Integrated Care Models

FLORIDA

• Florida Medicaid specialty health plan

• For those living with serious mental

illness

• Results-driven, community-based

approach

• Holistically addresses all healthcare

needs

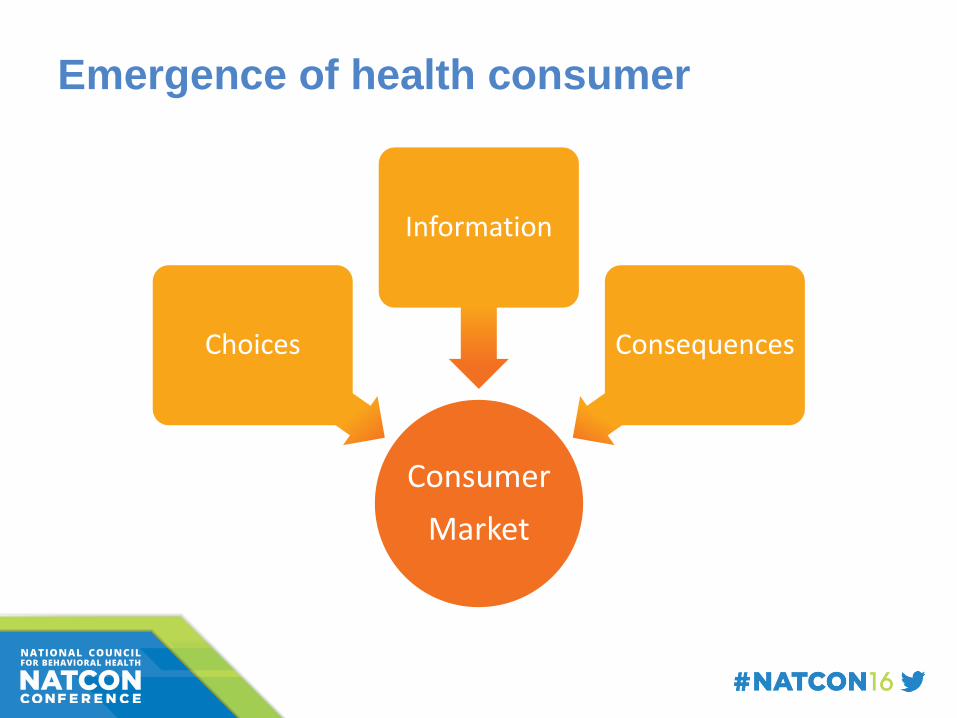

Integrated Care ModelsMagellan Complete Care of Florida

• Team members make

appointments, arrange

transportation to appointments

and help members to adhere

to treatment regimens

• Peer support programs can

help support the member’s

health and wellness between

appointments

Resulting in improvement to

the member’s overall health –

mental and physical

Members of the Care Coordination Team

Integrated Care ModelsComplete Care of Florida

Understanding

the unique mental

and physical

health needs of

individuals living

with serious

mental illness.

Members receive

personalized, high-

quality healthcare

that is tailored to

their physical

health, mental

health and social

needs.

Member Choice, Direction & Control

• Individual empowerment: Taking charge of services,

supports, and resources

• Self-directed care: Expanding real choice and control

• Decision support tools: Psychiatric advance

directives, WRAP®, life and goal-planning resources

• Empowering relationships: Built on strengths and

respect

Member Choice, Direction & Control Social Determinants of Health

Education and housing

Employment, living wages

Access to healthy foods and green spaces

Access to healthcare

Member Choice, Direction & Control Disparities and Inequities in Health

Disparities in Health

Differences in access to health services

Differences in health outcomes

Sadana and Blas, 2013

Health Inequities

are systematic, socially produced (and therefore modifiable) and unfair.

World Health Organization, 2010

Member Choice, Direction & Control Adding it all up…

Combined Healthcare Systems

Justice and Equity

Choices and

Decision Support

Social and Community Supports & Resources

Member Choice, Direction & Control Eight Dimensions of Wellness

Adapted from Swarbrick, M. (2006). A wellness approach. Psychiatric Rehabilitation Journal, 29,(4) 311- 314. (used with permission)

Member Choice, Direction & Control

• Annual Community Integration and Recovery Academy conference

attended by providers, peers, and family advocates provided

education about social inclusion and the 8 dimensions of wellness

• Peer support whole health and resiliency support groups:

– Facilitator development program

– Saw improvements in healthy eating habits among support group

participants, along with improvements in other health domains, including

better social support networks

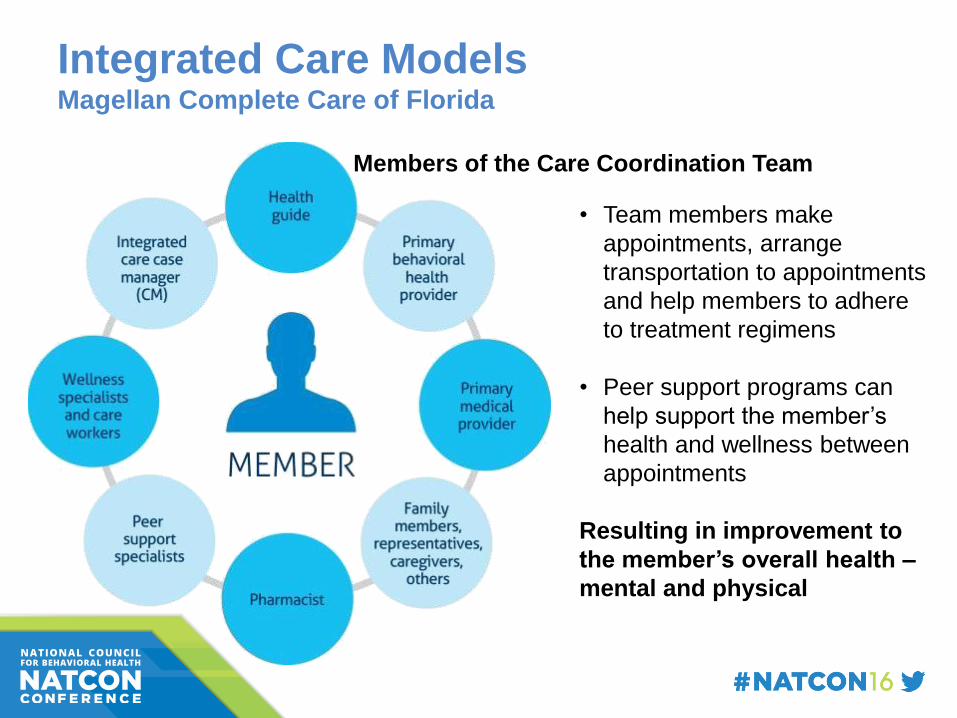

Member Choice, Direction & Control

Invested in mini-grant initiative over 3 years:

• Community provider focused on stigma reduction and education (relates to social

determinants around rights, social justice, freedom from exclusion, etc.)

• Conducted research to support stigma reduction and education re: mental illness;

implementation of community based support groups/trainings that addressed and

counter stigma and discrimination

• Participated in collaborative trainings and meetings with partnering organizations,

peer organizations, and stakeholders in order to address and counter stigma and

discrimination; students, teachers, parents and adults attended the collaborative

meetings

• Trained college campus professors/instructors and community-based agencies

owners, administrators, managers and staff on implementing a project-based activity

to support addressing the issues centered around stigma and discrimination

• Recruited volunteers/graduate student interns to work with community-based groups

to implement the support groups

• Developed and provided a calendar of scheduled trainings, events, and/or groups;

shared with the community in various forms

Value-Based Purchasing

• Defining value through data

analytics that are transparent and

standardized to equitable measure

• Early and ongoing provider

engagement

• Transparency through sharing

provider performance

• Payment alignment by

reimbursing based on

performance and incentives

aligned with measurements of

value

Value-Based Purchasing

Defining Value Provider data

AnalyticsAlgorithms

Provider engagement

TransparencyVisualization ScorecardsDashboards

Member Choice

Payment alignment

Pay for Performance

Key Components

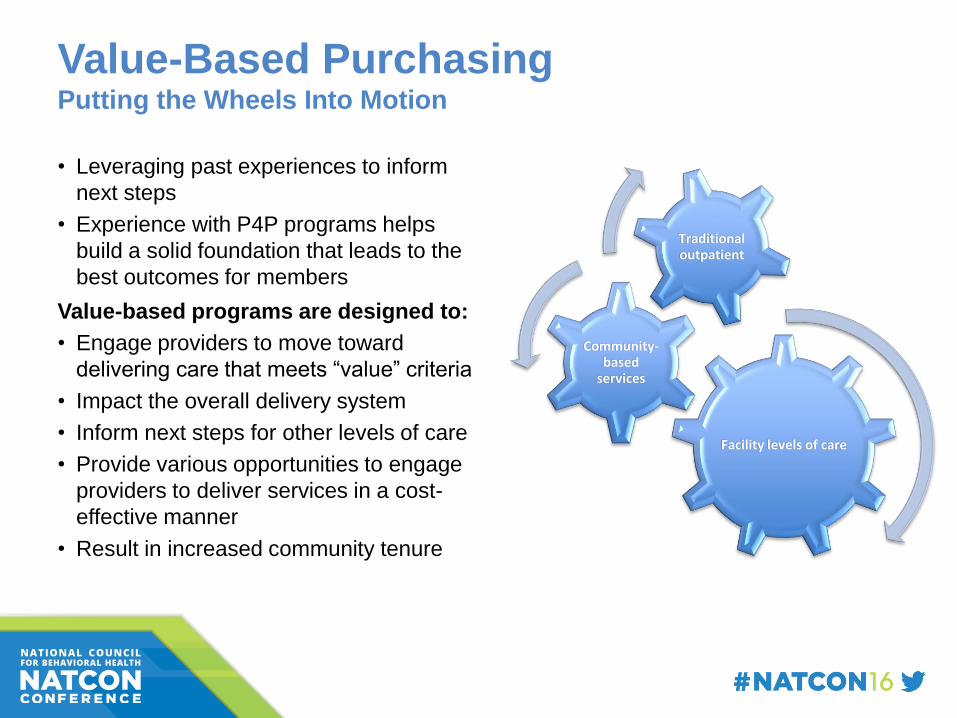

Value-Based PurchasingPutting the Wheels Into Motion

• Leveraging past experiences to inform

next steps

• Experience with P4P programs helps

build a solid foundation that leads to the

best outcomes for members

Value-based programs are designed to:

• Engage providers to move toward

delivering care that meets “value” criteria

• Impact the overall delivery system

• Inform next steps for other levels of care

• Provide various opportunities to engage

providers to deliver services in a cost-

effective manner

• Result in increased community tenure

Facility levels of care

Community-based

services

Traditional outpatient

Pay for PerformanceMental Health Inpatient (MH IP) Partners in Care

Goal• Entire program focused on collaboration with psychiatric inpatient facilities to improve outcomes

Outcomes/ Provider Impact• Two performance measures include follow-up after hospitalization and 30-day readmission rates

• 7-day follow-up after hospitalization (FUH) increased for providers in this program over one year

– MH IP Partners in Care providers outperformed inpatient facilities that were not part of the

program, with higher 7-day FUH in five of six quarters reviewed

• 30-day readmission rates for 10 program providers improved in a year, declining from 17% to 14%

Value-Add for Providers• More time focused on caring for members – less time on the phone doing UM

• Shared ownership in outcomes

• Facility leaders share best practices as well as discuss strategies for interventions and breaking

down barriers

• Develops transparency between providers

• Shared upside

• Good performance = good outcomes for members and success for providers

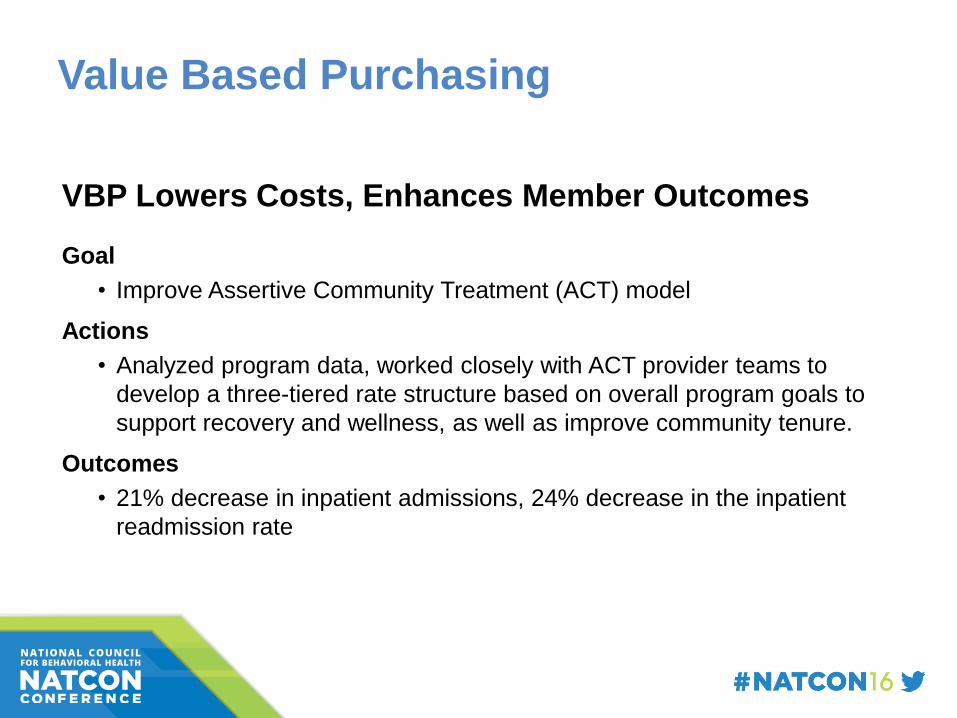

Value Based Purchasing

VBP Lowers Costs, Enhances Member Outcomes

Goal

• Improve Assertive Community Treatment (ACT) model

Actions

• Analyzed program data, worked closely with ACT provider teams to

develop a three-tiered rate structure based on overall program goals to

support recovery and wellness, as well as improve community tenure.

Outcomes

• 21% decrease in inpatient admissions, 24% decrease in the inpatient

readmission rate

Value-Based Purchasing

Inpatient

• Reduced 30-day readmissions from 11.9 to 9.8 for large hospital system in network

• Increased 30-day AFU from 79.8% to 83.88% for large hospital system in network

Assertive Community Treatment (ACT)

• Reduced from 7% to 1% acute inpatient readmissions for largest provider team in

network

• Increased from 52% to 81% medical care coordination for largest provider team in

network

Dual-diagnosis adult residential pilot project, stretch goals: 7% and 80%

• 5.26% annual program readmission rate

• 84.21% successful program completion rate

Value-Based Purchasing Key Components of Magellan’s VBP Model(s)

The use of data, algorithms,

standardized equitable measures

and actionable information to

identify and define provider value

Early and ongoing engagement

through data and an

understanding of what is being

measured, and why and how it’s

being measured

Public reporting to drive

performance improvement

Consumer transparency for

selection of highest quality

providers

Reimbursement is based upon

performance

Incentives are aligned with

definition of value

Defined value Provider engagement

Payment alignment

High-performance networks

Care coordination member-facing provider profiles Member outcomes data

Transparency Informed choice

Consumers, customers and

payers have the right

information to make informed

decisions about choice of care,

network and contracting.

Commonwealth of Pennsylvania: Pay-

for-Performance

• Program: PA DHS began Integrated Care Pay for Performance Program (P4P) 1/1/16

for all primary contractors. $10m funding pool. Incentive paid based on combined

PH/BH MCO performance

• Goals: Greater integration between BH and PH services; quality of care improvement

for Medicaid recipients with SPMI and SUD; enhanced care coordination to reduce

Medical Assistance expenditures

• Provider requirements: Meet three process measures for financial incentive

eligibility: Stratification of members with SPMI; use integrated care plans/member

profiles with BH/PH information; and hospital notification to PHMCO within one

business day of acute inpatient hospitalization/discharge notification

• Five outcome measures: 1) Initiation and engagement of alcohol/other drug

treatment; 2) adherence to antipsychotic medications for individuals with schizophrenia;

3) combined BH/PH inpatient 30-day readmission rate for individuals with SPMI; 4)

emergency dept utilization for individuals with SPMI; and 5) combined BH/PH inpatient

admission utilization for individuals with SPMI

State of Virginia: Governor’s Access Plan

(GAP)

Goal

• To help more uninsured Virginians with a serious mental illness (SMI) access needed

BH services (serves 6,000 members; projected to increase to 20,000 at peak)

• Provides limited benefit plan for individuals with SMI covering BH, medical and Rx

with a focus on community-based care

• Includes peer specialist services (F2F, warmline) provided by Magellan employees

and care coordination

Progress/Provider Impact

• No reductions of State General Funding to providers as a result of this program

• Prior to GAP, providers (particularly Medicaid) provided services to the uninsured as

unreimbursed, indigent care

• Under GAP, providers bill Magellan like all other plans in VA using unique Medicaid ID

#s. Billing process mirrors that of all other claims

• Only exception: provider billing assessments bill with SSN as the member may/may

not become enrolled, but assessment from an allowed screener is payable regardless

of enrollment

Federal Funding

Substance Abuse And Mental Health Services Administration

(SAMHSA)

• $22.9 million awarded nationwide by the U.S. Substance Abuse and

Mental Health Services Administration (SAMHSA), the Centers for

Medicare & Medicaid Services

• Purpose: Strengthen community-based mental health and substance use

disorder programs through the development of new Certified Community

Behavioral Health Clinics (CCBHC) to:

– Improve health outcomes by increasing access to quality care for all

Medicaid eligible individuals

– Reduce avoidable hospital use and complications through the

development of intermediate levels of service

– Foster better partnerships between primary care and mental health

and substance use disorder providers through co-location

– Improve the fiscal outlook for mental health and substance use

disorder care providers by improving Medicaid reimbursement

Federal Funding Available to Providers

Health Resources and Services Administration (HRSA) Behavioral Health

Integration (BHI) Grants

• 210 Behavioral Health Integration (BHI) grants in 2015, worth $51.3M.

• ACA initiative at 210 health centers in 47 states, DC and Puerto Rico

• Goal: hire new mental health professionals; add substance use disorder

health services; employ integrated models of primary care

Health Resources and Services Administration (HRSA) Substance Abuse

Service Expansion Grants (Fiscal Year 2016)

• Competitive supplement for grant funds to improve and expand delivery

of SA services provided by Health Center Programs

• Focus on Medication-assisted Treatment (MAT) in opioid use disorders.

• HRSA plans to award approximately $100 million to an estimated 310

applicants in FY 2016.

Federal Funding Available to Providers

Department of Health and Human Services

• HHS included a proposal to add certain behavioral health providers to

Electronic Health Record (EHR) Incentive Programs in its FY 2017

budget submission

• Providers include psychiatric hospitals, community mental health centers,

residential and outpatient mental health and substance abuse disorder

treatments facilities and psychologists

Administration Requests Additional $1.1B to Combat Prescription

Painkiller/Heroin Abuse in FY 2017

• Opiods involved in 30,000 deaths in US in 2014

• $500M earmarked for expansion of treatment facilities – addressing

access challenges

• Remaining $600M – prevention programs; naloxone distribution

programs; other programs

Changing Role of Providers: Challenges

and Solutions

Challenges

• Multiple standalone agencies/

safety net providers

• Dependent in large part on

state general funding

• Limited infrastructure (e.g.

technology, data analytics)

• Limited expertise with

backroom functions (e.g.

billing claims)

Solutions

• Partner, collaborate, merge

with other agencies

• Diversify funding through

mergers/new service creation

• Partnership arrangements with

an MCO

• Develop an MSO

arrangement/partner with an

MCO

Thank you!

Speaker NameTitle

Organization

Positioning for the Future of Managed Care

Dr. Lawrence GoldmanSVP, Government Relations

Beacon Health Options

Beacon’s National Scope

About Beacon Health Options

• Headquartered in Boston;

more than 70 US locations

and a London office

• 225 employer clients,

including 45 Fortune 500

companies

• Partnerships with more than

95 health plans

• Leader serving dual-eligible

beneficiaries in six states

Programs serving Medicaid recipients in 26 states and the District of Columbia

Serving 8.6 million military personnel, federal civilians and their families

Accreditation by both URAC and NCQA

Discussion Issues

• Value Based Payments

• Provider collaboration models

• Outcomes

– What can we measure

– What is really important

– How is the information used

• Challenges and opportunities ahead

Value Based Payments

“ Moving to Value – Easy to Say &

Hard to do” *

* - Monica Oss, Open Minds Daily Executive Briefing, February 22, 2016

Payment Methodologies

Fee-for-service

• One service

• One payment

Case Rate

• Group of services

• Combined payment

• Monthly/weekly paymentEpisode Bundle

• Group of services

• Combined payment

• Quality goals

• Defined time period

Total Health Outcomes

• Shared risk on total

member experience

Behavioral Health Outpatient Services

Care Management

Behavioral HealthDiversion

Behavioral HealthInpatient

Social Supports

Medical Outcomes

Behavioral Health Capitation

• Risk for providers

• Full behavioral health payment

• Defined coverage set

Transactional Relationship Model is Reinforced by

Fee-for-Service Reimbursement

Barriers to Alternative Payment Methodologies

Payer

Provider

Government

Consumer

Provider

“WE’VE ALWAYS DONE IT THIS WAY”

Alternative Payment Models Currently Used in

Several Markets

1. Outpatient Case Rates with Quality Incentive (Texas)

Treatment variability, minimal MCO pre-authorization and encouraged member movement along

treatment continuum

Incentive targets include: OP visits with 7 days of discharge, time in community standard, completion

of 340B integrated care assessments

Providers must accept all patients and submit encounters equal to 90-95% of case rates received

Case rate is significantly discounted for growth above 3-5% and are prepaid on monthly basis

2. Inpatient Case Rates (New York)

Case rate developed with each provider; is some cases-separate rate for adults v. children

Incorporates targeted LOS and reimbursement rates

No additional payment if readmission occurs within 30 days of original stay

May be reduced if target population contains certain higher end diagnosis

3. Modified Block Grant (Kansas)

Each provider negotiates annual maximum budget target and are reimbursed on FFS basis up to

this target

Providers must agree to “no eject/no reject” provisions

Per state’s discretion, additional payments can be made to providers who rendered services in

excess of budget target

Alternative Payment Models (continued)

4. Provider Partner Sub Cap (Colorado)

Full risk “down stream” (CMHCs)

BHO manages care rendered by external providers

Recipients must encounter 90-95% of capitation (maintenance of effort)

CMHC’s equity holder and board member of CMHC

5. Provider Sub-Cap (New Hampshire)

Partial risk down streamed to key CMHC’s

BHO managed care rendered by external providers

Recipients must encounter 90% of payment received (maintenance of effort)

Escalating annual quality withholds tied to achievement of specific measures; hospital

remittance, follow-up after hospitalization, care planning.

6. Risk Pool (Massachusetts)

Providers can achieve additional earnings if certain targets are met

Pools limited to specific dollar amounts and target specific levels of care

65

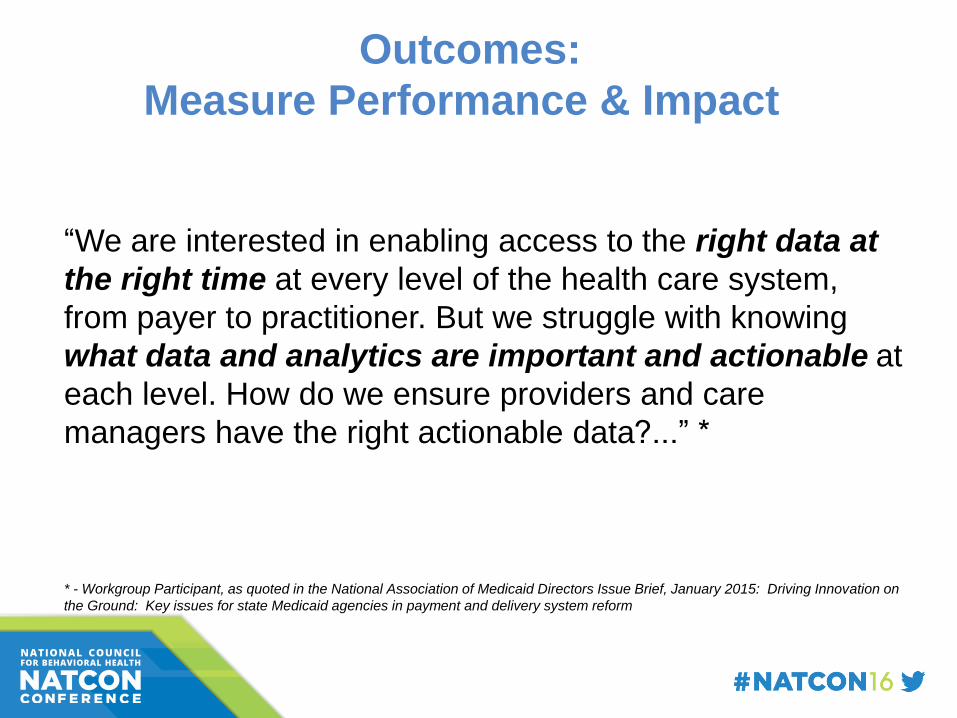

Outcomes:

Measure Performance & Impact

“We are interested in enabling access to the right data at

the right time at every level of the health care system,

from payer to practitioner. But we struggle with knowing

what data and analytics are important and actionable at

each level. How do we ensure providers and care

managers have the right actionable data?...” *

* - Workgroup Participant, as quoted in the National Association of Medicaid Directors Issue Brief, January 2015: Driving Innovation on

the Ground: Key issues for state Medicaid agencies in payment and delivery system reform

One solution – Outcomes Management

System (Maryland)

• Beacon Health Options (working with the Department of Mental

Hygiene) developed programming for the Outcomes Measurement

System (OMS)

– which collects information from individuals, age 6-64,

– receiving outpatient mental health treatment services in the Public

Behavioral Health System.

• OMS interviews are conducted by the clinician at the beginning of

treatment and approximately every six months during the course of

treatment.

• OMS data is displayed in the OMS Datamart and either statewide or

local jurisdiction information can be selected.

• This outcome information is integral data to informing policy and

improving consumer engagement and outcomes.

What is the future in

performance measures?

As Monica Oss wrote:

“Is one set of performance

measures possible?” *

• Can information be shared across payers?

• Will this lead to increased transparency?

• Will this allow consumer choice?

• And more….

* - Monica Oss, Open Minds Daily Briefing, February 22, 2016

The Future State of Managed

(Behavioral Health) Care

Consolidations MCO and/or Provider

Payment Reform Budget vs capitation vs global vs prospective

Outcomes Social determinants, clinical, life style, evidence based

Care integration Primary care and the specialty system

Care Coordination Connectivity to care – data analytics

The success of the Future State will be enhanced alignment of all stakeholders in the system, with transparency and collaboration around the main mission:

improve the life and health of those we serve

Thank [email protected]

Speaker NameTitle

Organization

Positioning for the Future of Managed Care

Ken AndersonVP Business Development, Government Solutions

OPTUM

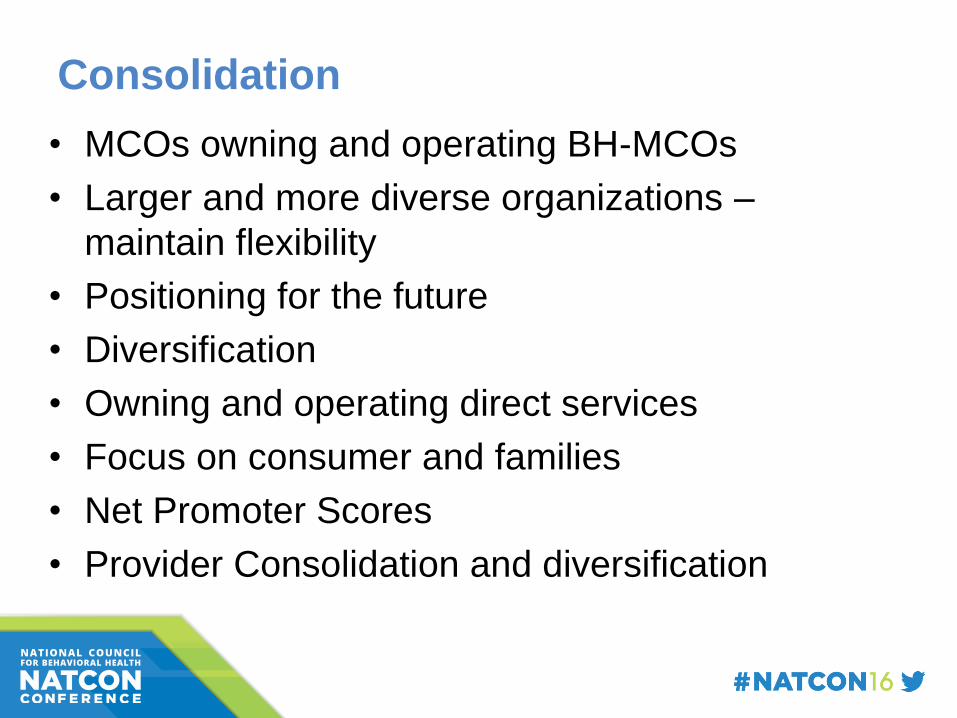

Consolidation

• MCOs owning and operating BH-MCOs

• Larger and more diverse organizations –

maintain flexibility

• Positioning for the future

• Diversification

• Owning and operating direct services

• Focus on consumer and families

• Net Promoter Scores

• Provider Consolidation and diversification

Integration

• Point of Service integration

• MCO integration – single case plans and record

systems

• Population Health Management – view of the

member(s)

• Promotion and prevention

• Care Coordinator roles – linked to risk stratification

• New alignment models with provider organizations

Single Payer

• 3 Ms --- Medicaid – Medicare – Marketplace

• Dual Eligibles

• Waiver consolidation

• Population Inclusion– IDD

– LTSS

– Corrections and justice involved

– Foster Care

• Social Determinants of Health

Technology and Data

• Data, data, and more data collection and

sharing

• Aps, aps and more aps

• Multi-party service plans

• Cloud technology and telehealth

• Redesigning networks

• New payment and reimbursement models

• New integrated quality measures

Workforce

• Lack of prescribers

• Expanding roles for Peers, family members

and non-traditional providers

• Integrated health teams

• Focus on whole person

• Working with varied populations

• Community services and resources