Embed Size (px)

Citation preview

Policy & Procedure

RISK MANAGEMENT HANDBOOK

Contact details

Risk Management is the responsibility of all members of staff, but maintenance of this document is the

responsibility of the Group Risk Manager. The corresponding policies and procedures have been

approved by the Board Risk Committee and implemented by the Group Management Risk Committee. This

document will be reviewed at least annually and as needed to ensure it remains appropriate to the needs

of the business.

RISK MANAGEMENT HANDBOOK

Owner: Board Risk Committee Issued: May 2017 Supersedes: N/A

Review date: April 2018 Page 1 of 18

RISK MANAGEMENT HANDBOOK | Page 2

Section 1 Establishing the Culture of Risk Management

1.1 Introduction

We know the environment is highly competitive and uncertain, all businesses are susceptible to crises which

could lead to operational disruptions, financial loss, reputational damage and in extreme cases, failure. At the

same time, businesses must seek and take risks in order to succeed and grow. We genuinely believe risk

management, embedded and used effectively, can improve our chance of success, make us more resilient, and

improve the bottom line. To this end, all staff need to work together to strengthen our risk management.

This applies across the Group ranging from our decisions in the Boardroom, across every region and in every

hotel. Every member of staff has a part to play.

This handbook sets out the risk management framework and is divided into 3 key sections:

Section 1: Establishing the culture of risk management - getting the culture right is the first step.

Regardless of the methodology, the culture will determine whether we achieve the benefits of risk

management. Key Sections include: Guiding Principles, Risk Management Strategy and Vision, Risk

Governance Structure and Risk Management Policy

Section 2: Understanding, defining and using risk appetite – making sense of this abstract but

fundamental topic.

Section 3: Risk management process – setting out a simple but consistent way the Group will manage risks

at the Board level and in Regions and Functions, seeking to join up risk throughout the business whilst

providing flexibility for other approaches within specific risk areas (e.g. information security, fraud, compliance

etc.) and at hotel level. The Risk Management Process comprises Risk Identification, Risk Assessment, Risk

Treatment and Risk Monitoring.

The appendix contains support tools which help us put risk management into practice including the Risk

Reporting Cycle, Tools and Templates, the GMRC Terms of Reference and a Glossary of Risk Management

Terms.

1.2 Guiding Principles

Irrespective of the process and tools adopted, there are fundamental principles for risk management that we

wish to embed into the culture. These will ensure we are effectively managing risks, considering risk in our

decision making and acting responsibly:

Take accountability

We all have roles, projects and tasks to deliver and each of us must take accountability for risks that could

impact on our success. Risk management is everyone’s job, and not just for the Board and senior

management. Everyone should be aware of and consider risks throughout their activities and in particular

when making decisions. Some risk accountabilities are the responsibility of the senior people in the

Group and they need to set the right culture to ensure that processes are challenged and key risks are

understood and acted upon.

Do it like you mean it

Risk management is not a ‘tick-box exercise’. The risks we face as a Group are real and significant, and

may have a personal impact on us and the people around us. The efforts we take to manage risk should

be intended to achieve real risk reduction, or to help us make decisions to take further action.

Be proactive, innovative and challenge the status quo

If we’ve identified a risk that we’re genuinely worried about, it probably means we aren’t satisfied with

what we’re currently doing. In these cases, we need to find the best solutions which may involve different

perspectives, innovations, cross-regional teams and challenges to the status quo.

Prove it with data

In most cases, it won’t be enough to simply say that an identified risk is a high risk that requires fixing, or

that an identified risk will not happen. Risk treatment solutions (i.e. mitigating, reducing, transferring or

accepting the risk) may require financial investment, management time and resources. We need to use

data and analytics proportionately to monitor the risk, inform the need for actions, or to develop a

business case for change.

Think holistically

When building a comprehensive picture of risks, look at the business area from different perspectives.

Consider longer term external trends across different stakeholders, be commercially minded, think about

change, our guests, people and day-to-day operational risks.

Embed risk management

Effective risk management does not happen in isolation, risks should be considered whenever decisions

are made and formal risk consideration should be integrated into other business activities such as

business and budget planning, performance management, reporting and governance, decision making

committees and processes, project management, policies, controls, and compliance activities.

Open and transparent culture

The Group has an open, transparent and blame-free culture and expects all staff to freely identify and

discuss risks. Where there are sensitive risks, appropriate channels are available, including reaching out to

Group Management Risk Committee (“GMRC”) members, to members of the Board Risk Committee

(“BRC”) or consider the Group’s Whistleblowing Policy.

Mr Gervase MacGregor, Non-Executive Director Mr Tan Kian Seng, CEO

Chairman, Board Risk Committee Chairman, Group Management Risk Committee

May 2017 May 2017

RISK MANAGEMENT HANDBOOK | Page 4

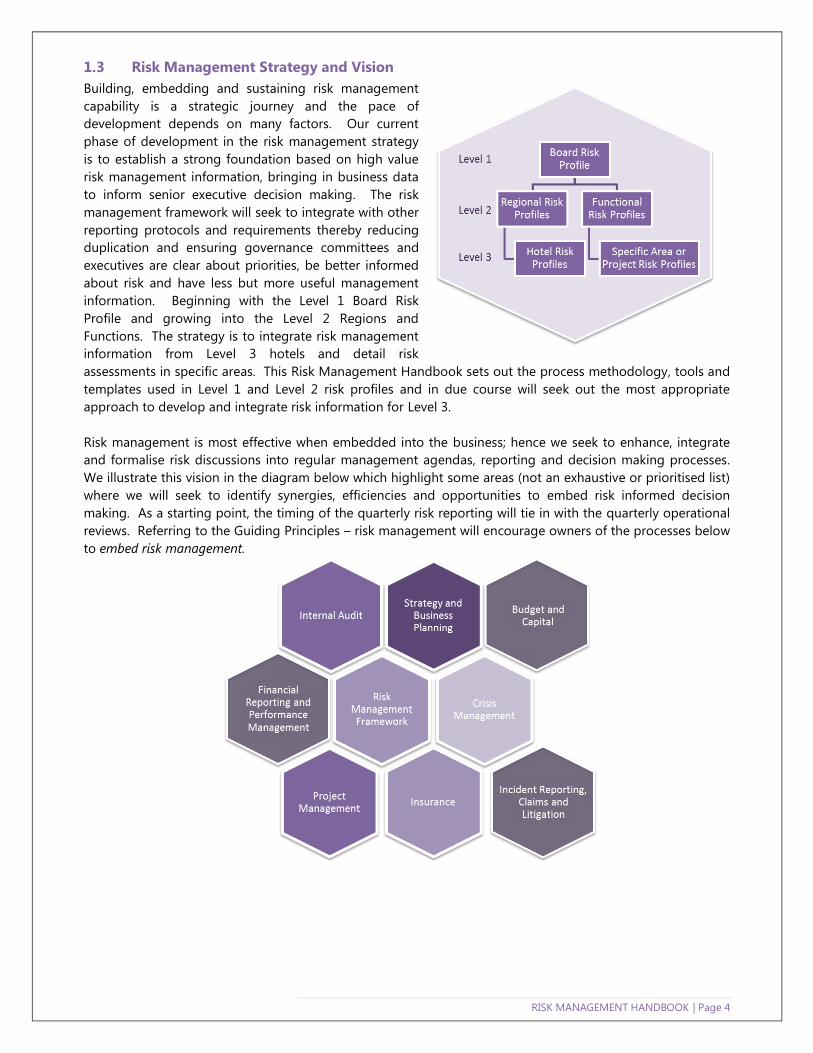

1.3 Risk Management Strategy and Vision

Building, embedding and sustaining risk management

capability is a strategic journey and the pace of

development depends on many factors. Our current

phase of development in the risk management strategy

is to establish a strong foundation based on high value

risk management information, bringing in business data

to inform senior executive decision making. The risk

management framework will seek to integrate with other

reporting protocols and requirements thereby reducing

duplication and ensuring governance committees and

executives are clear about priorities, be better informed

about risk and have less but more useful management

information. Beginning with the Level 1 Board Risk

Profile and growing into the Level 2 Regions and

Functions. The strategy is to integrate risk management

information from Level 3 hotels and detail risk

assessments in specific areas. This Risk Management Handbook sets out the process methodology, tools and

templates used in Level 1 and Level 2 risk profiles and in due course will seek out the most appropriate

approach to develop and integrate risk information for Level 3.

Risk management is most effective when embedded into the business; hence we seek to enhance, integrate

and formalise risk discussions into regular management agendas, reporting and decision making processes.

We illustrate this vision in the diagram below which highlight some areas (not an exhaustive or prioritised list)

where we will seek to identify synergies, efficiencies and opportunities to embed risk informed decision

making. As a starting point, the timing of the quarterly risk reporting will tie in with the quarterly operational

reviews. Referring to the Guiding Principles – risk management will encourage owners of the processes below

to embed risk management.

1.4 Risk Governance Structure

Clarity on roles and responsibilities and hence having clear accountability is fundamental to effective risk

management. For the avoidance of doubt, we have set out a Governance Structure supported by Risk

Management Policy (see 1.5).

The Board is ultimately accountable for Risk Management including establishing the Group’s risk appetite and

ensuring risks are effectively managed. To fulfil this mandate and recognising the importance, the Board

established a dedicated Board Risk Committee (“BRC”) in 2016 who has a mandate to oversee the effective

management of the most significant risks to the Group, these are captured in the Level 1 Board Risk Profile

and are summarised in the Annual Report and Accounts. The Board Risk Committee - Terms of Reference can

be found on the Investor Relations section website (see here).

Whilst the BRC will provide oversight, a dedicated Group Management Risk Committee (“GMRC”) has been

established to own and manage the Board Risk Profile. The GMRC is chaired by the Group Chief Executive

Officer with membership comprised of the Regional and Functional heads, Chief Financial Officer and the

Company Secretary and General Counsel. The GMRC will be supported by the Group Risk Manager who shall

provide secretariat support while the Head of Internal Audit will have an open invitation. The GMRC shall

meet at least quarterly. The GMRC Terms of Reference are included in the Appendix.

Underpinning these formal structures, each Region and Functional Head is accountable for risk within their

respective areas. This may be managed as part of existing senior management meetings or by forming risk

sub-committees. For example, New Zealand has established a separate Audit Committee to which risk

management is one of its mandates.

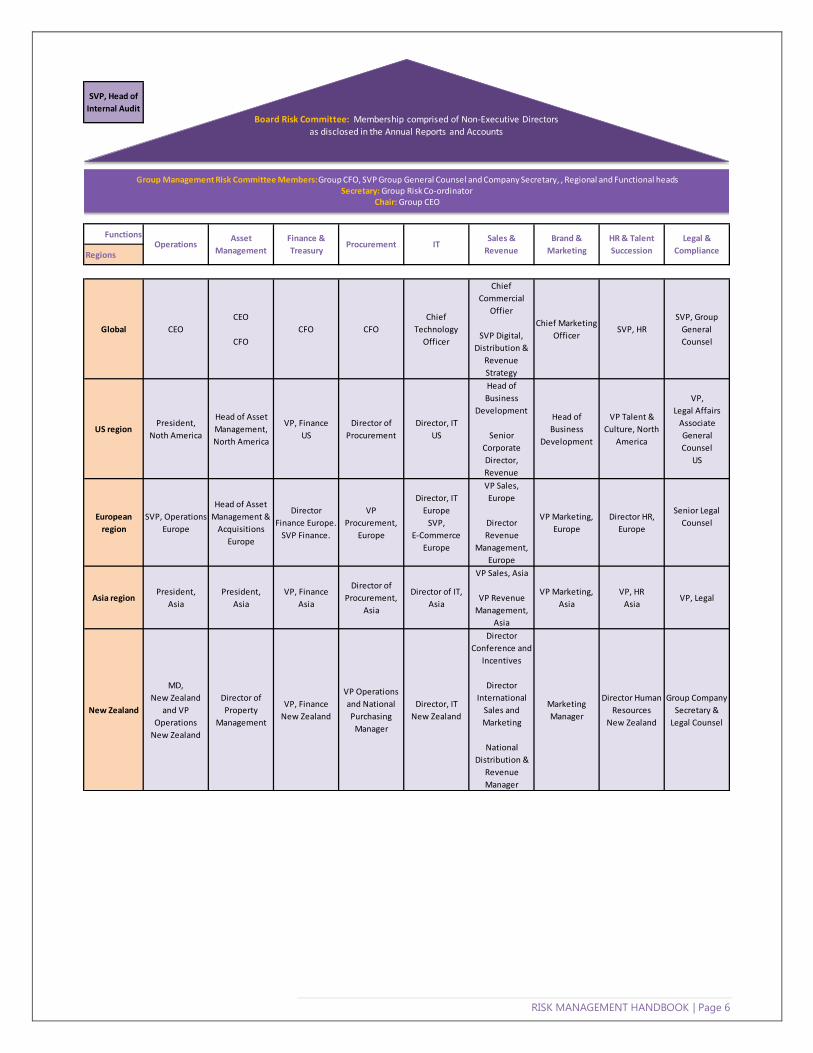

This structure is represented pictorially below, and the risk related reporting cycle is shown in the Appendix 1:

RISK MANAGEMENT HANDBOOK | Page 6

Functions

Regions

Global CEO

CEO

CFO

CFO CFO

Chief

Technology

Officer

Chief

Commercial

Offier

SVP Digital,

Distribution &

Revenue

Strategy

Chief Marketing

OfficerSVP, HR

SVP, Group

General

Counsel

US regionPresident,

Noth America

Head of Asset

Management,

North America

VP, Finance

US

Director of

Procurement

Director, IT

US

Head of

Business

Development

Senior

Corporate

Director,

Revenue

Head of

Business

Development

VP Talent &

Culture, North

America

VP,

Legal Affairs

Associate

General

Counsel

US

European

region

SVP, Operations

Europe

Head of Asset

Management &

Acquisitions

Europe

Director

Finance Europe.

SVP Finance.

VP

Procurement,

Europe

Director, IT

Europe

SVP,

E-Commerce

Europe

VP Sales,

Europe

Director

Revenue

Management,

Europe

VP Marketing,

Europe

Director HR,

Europe

Senior Legal

Counsel

Asia regionPresident,

Asia

President,

Asia

VP, Finance

Asia

Director of

Procurement,

Asia

Director of IT,

Asia

VP Sales, Asia

VP Revenue

Management,

Asia

VP Marketing,

Asia

VP, HR

AsiaVP, Legal

New Zealand

MD,

New Zealand

and VP

Operations

New Zealand

Director of

Property

Management

VP, Finance

New Zealand

VP Operations

and National

Purchasing

Manager

Director, IT

New Zealand

Director

Conference and

Incentives

Director

International

Sales and

Marketing

National

Distribution &

Revenue

Manager

Marketing

Manager

Director Human

Resources

New Zealand

Group Company

Secretary &

Legal Counsel

SVP, Head of

Internal Audit

IT Brand &

Marketing

HR & Talent

Succession

Legal &

ComplianceOperations

Asset

Management

Finance &

TreasuryProcurement

Sales &

Revenue

Board Risk Committee: Membership comprised of Non-Executive Directors

as disclosed in the Annual Reports and Accounts

Group Management Risk Committee Members:Group CFO, SVP Group General Counsel and Company Secretary, , Regional and Functional headsSecretary: Group Risk Co-ordinator

Chair: Group CEO

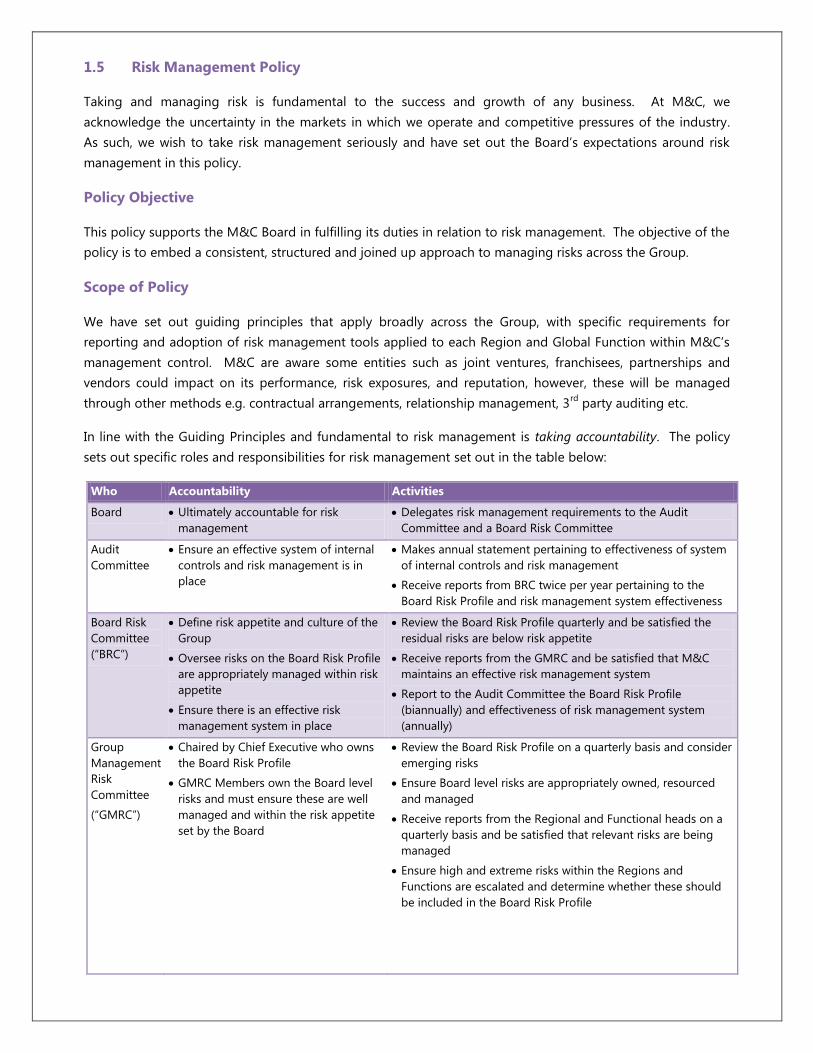

1.5 Risk Management Policy

Taking and managing risk is fundamental to the success and growth of any business. At M&C, we

acknowledge the uncertainty in the markets in which we operate and competitive pressures of the industry.

As such, we wish to take risk management seriously and have set out the Board’s expectations around risk

management in this policy.

Policy Objective

This policy supports the M&C Board in fulfilling its duties in relation to risk management. The objective of the

policy is to embed a consistent, structured and joined up approach to managing risks across the Group.

Scope of Policy

We have set out guiding principles that apply broadly across the Group, with specific requirements for

reporting and adoption of risk management tools applied to each Region and Global Function within M&C’s

management control. M&C are aware some entities such as joint ventures, franchisees, partnerships and

vendors could impact on its performance, risk exposures, and reputation, however, these will be managed

through other methods e.g. contractual arrangements, relationship management, 3rd

party auditing etc.

In line with the Guiding Principles and fundamental to risk management is taking accountability. The policy

sets out specific roles and responsibilities for risk management set out in the table below:

Who Accountability Activities

Board Ultimately accountable for risk

management

Delegates risk management requirements to the Audit

Committee and a Board Risk Committee

Audit

Committee

Ensure an effective system of internal

controls and risk management is in

place

Makes annual statement pertaining to effectiveness of system

of internal controls and risk management

Receive reports from BRC twice per year pertaining to the

Board Risk Profile and risk management system effectiveness

Board Risk

Committee

(“BRC”)

Define risk appetite and culture of the

Group

Oversee risks on the Board Risk Profile

are appropriately managed within risk

appetite

Ensure there is an effective risk

management system in place

Review the Board Risk Profile quarterly and be satisfied the

residual risks are below risk appetite

Receive reports from the GMRC and be satisfied that M&C

maintains an effective risk management system

Report to the Audit Committee the Board Risk Profile

(biannually) and effectiveness of risk management system

(annually)

Group

Management

Risk

Committee

(“GMRC”)

Chaired by Chief Executive who owns

the Board Risk Profile

GMRC Members own the Board level

risks and must ensure these are well

managed and within the risk appetite

set by the Board

Review the Board Risk Profile on a quarterly basis and consider

emerging risks

Ensure Board level risks are appropriately owned, resourced

and managed

Receive reports from the Regional and Functional heads on a

quarterly basis and be satisfied that relevant risks are being

managed

Ensure high and extreme risks within the Regions and

Functions are escalated and determine whether these should

be included in the Board Risk Profile

RISK MANAGEMENT HANDBOOK | Page 8

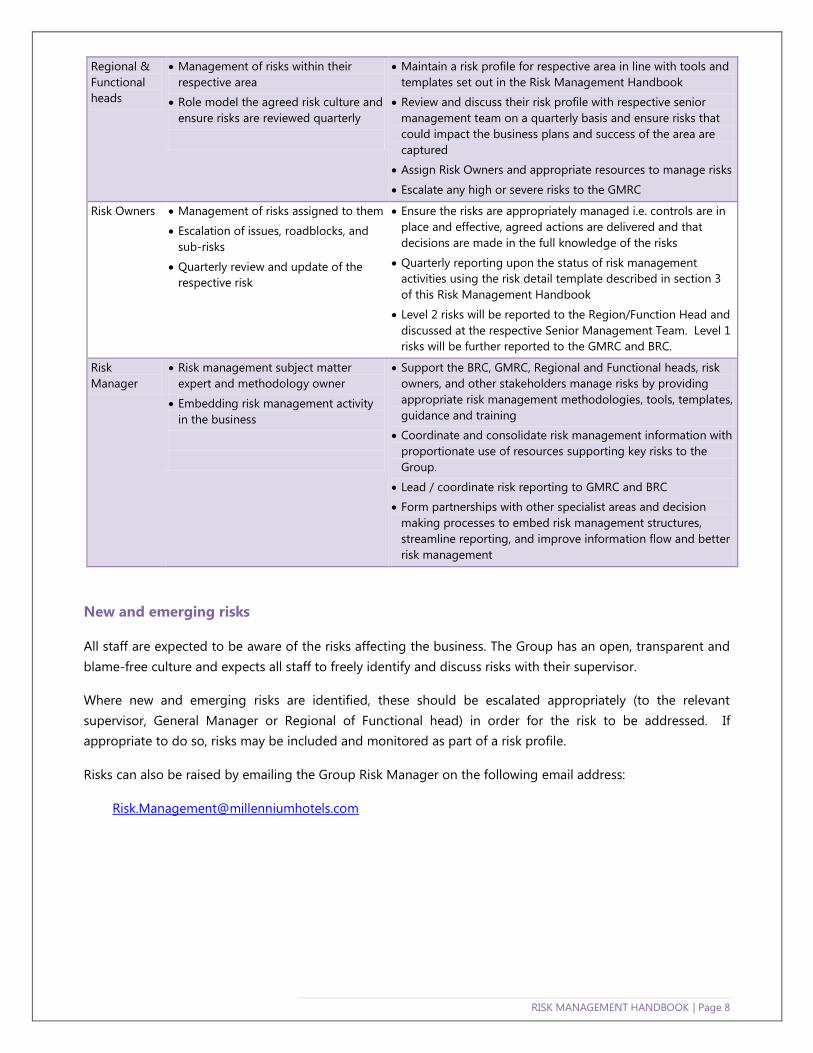

Regional &

Functional

heads

Management of risks within their

respective area

Role model the agreed risk culture and

ensure risks are reviewed quarterly

Maintain a risk profile for respective area in line with tools and

templates set out in the Risk Management Handbook

Review and discuss their risk profile with respective senior

management team on a quarterly basis and ensure risks that

could impact the business plans and success of the area are

captured

Assign Risk Owners and appropriate resources to manage risks

Escalate any high or severe risks to the GMRC

Risk Owners Management of risks assigned to them

Escalation of issues, roadblocks, and

sub-risks

Quarterly review and update of the

respective risk

Ensure the risks are appropriately managed i.e. controls are in

place and effective, agreed actions are delivered and that

decisions are made in the full knowledge of the risks

Quarterly reporting upon the status of risk management

activities using the risk detail template described in section 3

of this Risk Management Handbook

Level 2 risks will be reported to the Region/Function Head and

discussed at the respective Senior Management Team. Level 1

risks will be further reported to the GMRC and BRC.

Risk

Manager

Risk management subject matter

expert and methodology owner

Embedding risk management activity

in the business

Support the BRC, GMRC, Regional and Functional heads, risk

owners, and other stakeholders manage risks by providing

appropriate risk management methodologies, tools, templates,

guidance and training

Coordinate and consolidate risk management information with

proportionate use of resources supporting key risks to the

Group.

Lead / coordinate risk reporting to GMRC and BRC

Form partnerships with other specialist areas and decision

making processes to embed risk management structures,

streamline reporting, and improve information flow and better

risk management

New and emerging risks

All staff are expected to be aware of the risks affecting the business. The Group has an open, transparent and

blame-free culture and expects all staff to freely identify and discuss risks with their supervisor.

Where new and emerging risks are identified, these should be escalated appropriately (to the relevant

supervisor, General Manager or Regional of Functional head) in order for the risk to be addressed. If

appropriate to do so, risks may be included and monitored as part of a risk profile.

Risks can also be raised by emailing the Group Risk Manager on the following email address:

Section 2 Understanding and Defining Risk Appetite

Risk appetite is the nature and extent of risk an organisation is prepared to take to achieve its objectives. For

UK listed businesses such as M&C, setting risk appetite is a Board level responsibility and requirement set out

in the UK Corporate Governance Code. Whilst this topic is slightly abstract, interpreted correctly, it provides

clarity of expectations set out at the highest levels of an organisation. The benefits of clearly articulating risk

appetite are:

Clarity to all stakeholders, better transparency and alignment on expectations;

Less requirement for personal judgement, exposure to personal biases and lower chance of rogue

behaviour; and

Fewer operational surprises.

Risk appetite varies depending on the type of risk and can be influenced by a number of factors including

potential for returns, past experiences and personal attitudes. As such M&C will look at risk appetite at an

individual risk-by-risk perspective rather than developing a single overarching risk appetite statement.

Each risk appetite will be a statement setting out the direction and attitude the Board has towards this

particular risk including setting out how it wishes the risk to be managed and controlled. Where appropriate,

the risk appetite may link to the measures and levels set out in the key risk indicators.

Defined well, the risk appetite statement can provide fundamental guidance to the risk owner. For example if

the Board determines its appetite for a particular risk was low, it may also require implementing robust

controls. The risk appetite statement might go onto clarify the measures it seeks to see and that it recognises

that such a solution could have cost implications which it is prepared to accept.

The above example aims to illustrate the importance of risk appetite and how it can influence management

decision making, allocations of resources and the handling of trade-offs. In practice, these appetite

statements should be drafted by the Risk Owners and discussed with the Region and Functional Head. Risk

appetite for Level 1 risks will be further discussed at the GMRC and finally agreed at the BRC. Risk appetite

supports the Guiding Principle around an open and transparent culture.

RISK MANAGEMENT HANDBOOK | Page 10

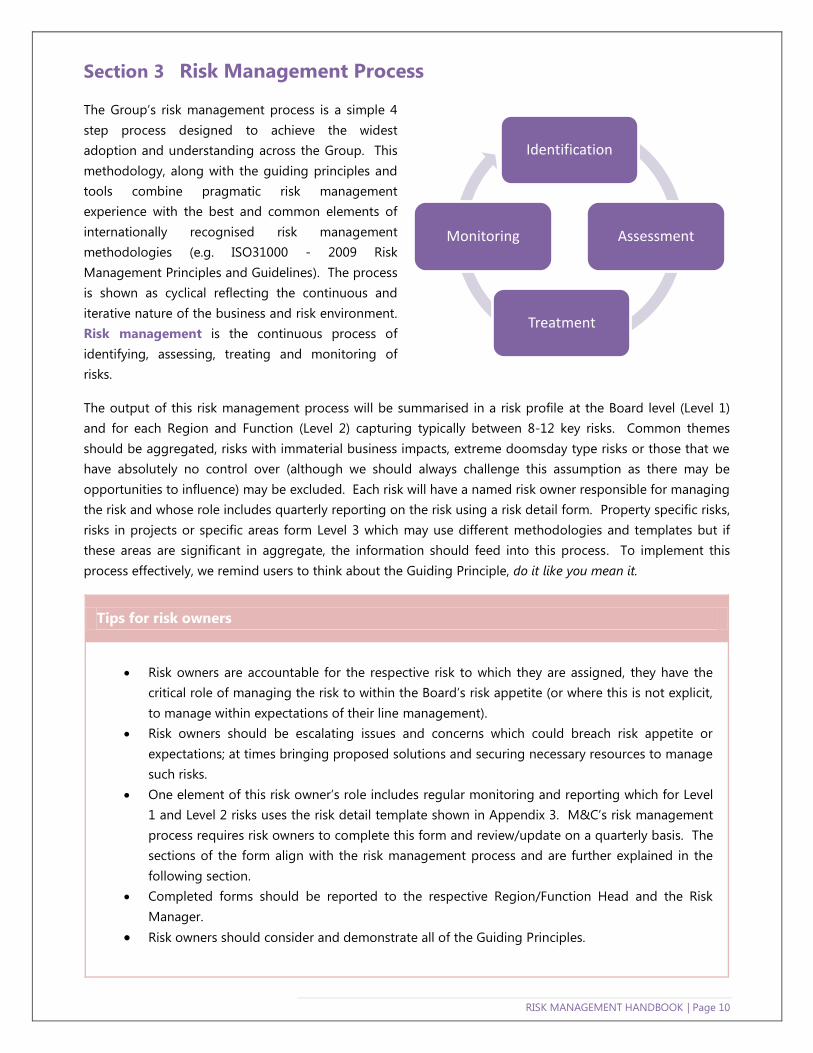

Section 3 Risk Management Process

The Group’s risk management process is a simple 4

step process designed to achieve the widest

adoption and understanding across the Group. This

methodology, along with the guiding principles and

tools combine pragmatic risk management

experience with the best and common elements of

internationally recognised risk management

methodologies (e.g. ISO31000 - 2009 Risk

Management Principles and Guidelines). The process

is shown as cyclical reflecting the continuous and

iterative nature of the business and risk environment.

Risk management is the continuous process of

identifying, assessing, treating and monitoring of

risks.

The output of this risk management process will be summarised in a risk profile at the Board level (Level 1)

and for each Region and Function (Level 2) capturing typically between 8-12 key risks. Common themes

should be aggregated, risks with immaterial business impacts, extreme doomsday type risks or those that we

have absolutely no control over (although we should always challenge this assumption as there may be

opportunities to influence) may be excluded. Each risk will have a named risk owner responsible for managing

the risk and whose role includes quarterly reporting on the risk using a risk detail form. Property specific risks,

risks in projects or specific areas form Level 3 which may use different methodologies and templates but if

these areas are significant in aggregate, the information should feed into this process. To implement this

process effectively, we remind users to think about the Guiding Principle, do it like you mean it.

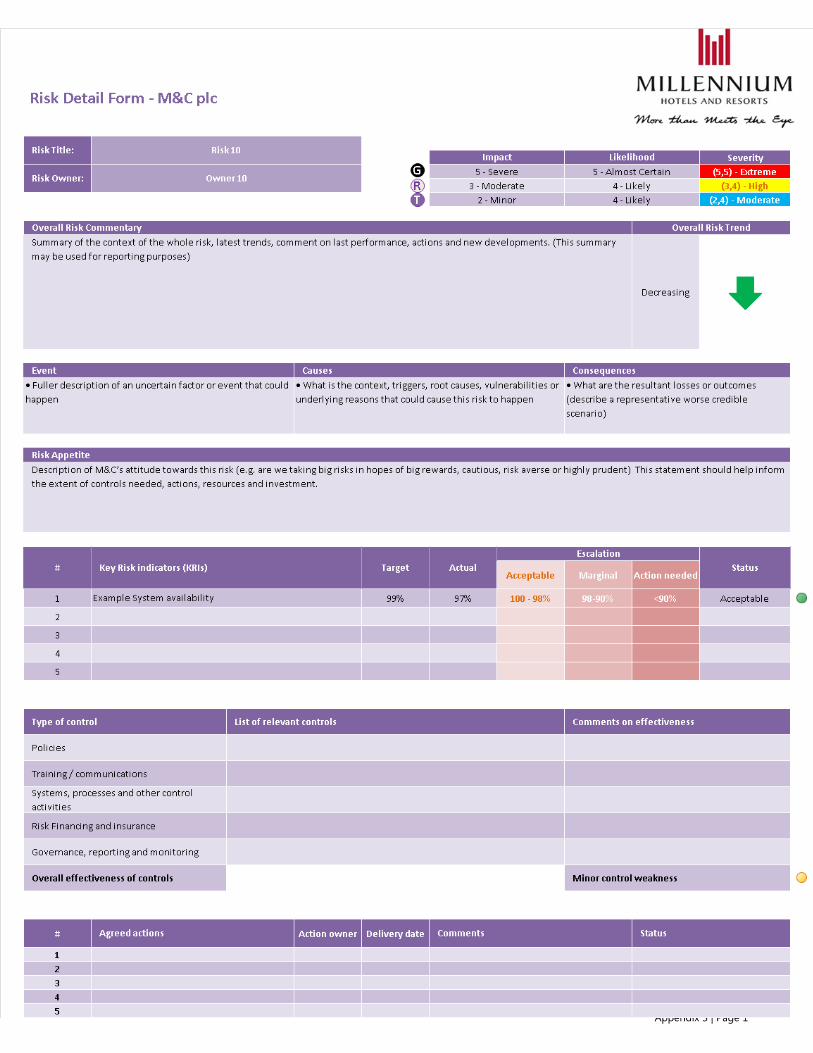

Tips for risk owners

Risk owners are accountable for the respective risk to which they are assigned, they have the

critical role of managing the risk to within the Board’s risk appetite (or where this is not explicit,

to manage within expectations of their line management).

Risk owners should be escalating issues and concerns which could breach risk appetite or

expectations; at times bringing proposed solutions and securing necessary resources to manage

such risks.

One element of this risk owner’s role includes regular monitoring and reporting which for Level

1 and Level 2 risks uses the risk detail template shown in Appendix 3. M&C’s risk management

process requires risk owners to complete this form and review/update on a quarterly basis. The

sections of the form align with the risk management process and are further explained in the

following section.

Completed forms should be reported to the respective Region/Function Head and the Risk

Manager.

Risk owners should consider and demonstrate all of the Guiding Principles.

Identification

Assessment

Treatment

Monitoring

S

T

O

3.1 Risk Identification

The objective of this stage is simply to identify, understand, and describe risks (uncertain factors or events that

could impact on the achievement of business objectives) so that others have a shared understanding; and

then to agree the most appropriate risk owner. The section of the risk detail form corresponding to risk

identification is shown below including a short title, fuller description, causes of the risk and the description of

consequences:

Risk Title: <A short title for this risk>

Risk Owner: <A named individual>

Event Causes Consequences

<Fuller description of an uncertain

factor or event that could happen>

<What is the context, triggers, root

cause(s), vulnerabilities or underlying

reasons that could cause this risk to

happen>

<What are the resultant losses or

outcomes (describe the impact of the

worse credible scenario)>

Types of Risk

Although there are many types of risks, the ones we are most interested in are those that could have the

biggest impact on the business objectives. One model used to differentiate risks and aid risk identification

addresses the Guiding Principle to think holistically, the model shows three different types of risks that all

organisations and teams face:

Strategic Risks – Strategic risks are usually driven by external factors or

market conditions and can have an effect on strategic objectives. These risks

are often viewed over a longer time horizon (+5 years) and best identified

through PESTLE and SWOT types of analysis (see Glossary) impacting on the

Group.

Tactical Risks – Tactical risks impact the business over a medium time

horizon (usually 12-36 months) and can be sub-divided into financial risks and

project risks.

Operational risks – Operational risks impact on M&C’s day to day operations including the running of

owned and managed hotels, central systems and websites and support to franchisees. As the Group’s

operations include the supply chain and external stakeholders, operational risk analysis should include

consideration for suppliers, partners, the wider community and risks affecting our guests.

RISK MANAGEMENT HANDBOOK | Page 12

Tips for risk identification

Risks to what? The achievement of business objectives. It is most helpful to be clear about the

business objectives the organisation or team is working towards (however, be mindful that objectives

should include “business as usual” activities in addition to incremental/growth).

Consider holding a risk identification workshop involving diverse stakeholders with different

perspectives to gain a comprehensive view of all risk affecting the area.

In addition to either the above simple holistic model, there are other models with numerous risk

categories designed to help aid thinking, ensure breadth of coverage. We could also consider

different perspectives (e.g. customer/guests, regulatory, media, local vs. global etc.).

To articulate the risk properly, try completing this sentence: “There is a risk that (event description)

happens due to (list of causes); and as a result, we could experience (list of consequences).”

3.2 Risk Assessment

The purpose of this stage is to prioritise the risks by comparing the

impact of the risk occurring and the likelihood that it would occur

against pre-defined impact and likelihood parameters. This is a

simplification of the risk and is meant to be a quick and broad

estimation. We understand the same risk may have different

impacts and likelihoods. For example, if the curve shown on the

left represents Fire risk in hotels, point A which has a high

likelihood of occurrence but low impact, might be small electrical

fires or near misses (e.g. kettles and hairdryers) while point B

representing a high impact and low likelihood, might be an

extreme event involving fire caused by M&C negligence, involving multiple fatalities and the total loss of the

largest hotel in the estate.

It is up to the risk owner to decide which scenario is the most concerning. For consistency, we encourage risk

owners to think about the ‘worse credible scenario’ which might be represented by point C. In this example, it

might be a scenario where the risk of a serious fire involving at least one fatality and loss of the building.

Risk Assessment from different perspectives

Gross or inherent risk – this is the impact and likelihood of the risk occurring without taking into account

any efforts or controls in place to manage it. This hypothetical (and usually much higher) risk assessment

is necessary in cases where management controls prove to be ineffective. It is most commonly used to

inform audit programmes as it does not assume controls are in place or effective.

Residual or net risk – this is the impact and likelihood of the risk occurring taking into account the

existing efforts and controls in place to manage the particular risk. This relies on the risk owner knowing

what controls are in place and making judgements on the effectiveness of these.

Target risk – Where there is desire (or appetite) for significant change to the risk level, a third perspective

is considered representing the desired impact and likelihood risk level.

Impact

Lik

elih

oo

d

A

B C

To make an informed residual risk assessment, there is a need to understand how effective the current

controls are. This might be informed by internal audit or independent reviews of the related processes. To

aid the thinking around controls, we have set out various types of controls, asking risk owners to list out items

that are in place for each control type. The risk owner is also asked to comment on the effectiveness of these

controls and to make an overall assessment on the collective effectiveness of controls. The residual risk

assessment is informed by this analysis but it is not a formulaic reduction.

Type of control List of relevant controls Comments on effectiveness

Policies

Training / communications

Systems, processes and other control activities

Risk Financing and insurance

Governance, reporting and monitoring

Overall effectiveness of controls Where = Significant control deficiencies = Minor control weaknesses = Effective controls

RISK MANAGEMENT HANDBOOK | Page 14

Risk Assessment Definitions

For consistency, and to enable comparison and aggregation, risks will be assessed against the categories and

definitions set out below. As there are multiple impact categories, risk owners are expected to choose a single

representative impact score taking account all aspects (i.e. considering the financial, reputational, operational

impacts etc.) that best describes the impact if the ‘worse-credible scenario’ were to happen and the

corresponding likelihood to such an outcome. This should be done by gross, residual and target perspectives.

IMPACT

RATING

Financial

Impact (PBT) Reputational Impact Operational Impact Safety Impact People Impact

5

Severe Over £50m

Prominent, enduring

negative global media

coverage, major

investigation by

authorities, and/or >40%

share price impact

Permanent or long-

term loss of key

facilities, multiple

hotels, or central

services

Severe incident

resulting in loss of

life or multiple

severe injuries with

probable M&C

negligence

N/A

4

Major

£50m

-

£15m

Negative global media

coverage, investigation

by authorities and/or 15-

40% share price impact

Permanent or long-

term loss of 1-3 key

hotels or prolonged

outage of a key

central service

Major incident

resulting in serious

injury / illness with

probable M&C

negligence

Global employee

dissatisfaction

resulting in higher

than normal churn

including key roles

3

Moderate

£15m

-

£5m

Short lived regional

media coverage,

warnings by authorities,

and/or up to 15% share

price impact

Permanent loss of a

non-key hotel or

short-term delay in

central services

affecting all/or

significant group of

hotels

Moderate incident

with implied or

potential M&C

negligence

Regional employee

dissatisfaction,

resulting in higher

than normal staff

churn

2

Minor

£5m

-

£1m

Local media

coverage, negative

customer or investor

feedback requiring press

release

Major disruption to a

single hotel or minor

impact on multiple

(not all) hotels

Incident resulting in

loss of life or severe

injury with no

purported M&C

negligence

Employee

dissatisfaction in a

hotel or department

resulting in localised

churn

1

Insignificant Less than £1m

Negative customer or

investor feedback

Secondary system or

process disrupted in

a hotel for a short

period

Incident involving

injury or illness and

no implied M&C

negligence

Staff tensions

impacting

engagement in hotel

or department

LIKELIHOOD Probability of Occurrence Description

5

Almost

Certain

Over 70% chance or

a less than 2 year event

An event that can be expected to happen or is already occurring at

M&C

4

Likely

50-70% chance or

2-3 year event

A likely event that can be anticipated at M&C or has happened in

similar organisations

3

Possible

30-50% chance or

3-7 year event

A possible event that has never occurred at M&C but has happened in

other organisations

2

Unlikely

5-30% chance or

7-20 year event

An unlikely event that can be envisaged but hasn’t occurred at M&C

or other organisations

1

Rare

Less than 5% chance or

Over 20 year event

A rare event that can be conceived but only under exceptional

circumstances

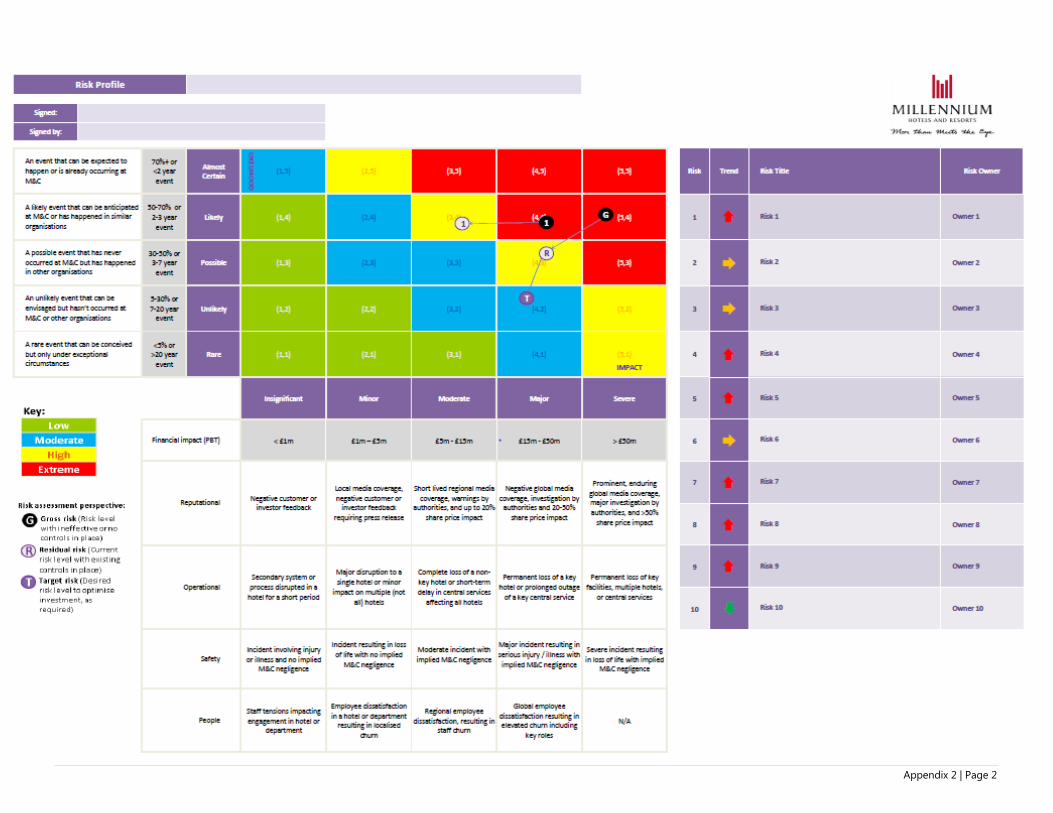

The risk score is plotted on the risk profile showing the representative impact (1-5) and likelihood scores

(1-5) as (impact, likelihood) or (x, y) coordinates. The colour key determines how the resultant assessment

should be treated or escalated.

Gross risk i.e. risk level with ineffective or no risk controls in place

Assess the risk if all the controls have failed or there are no controls in place

Consider the worse credible scenario or risk event which you are most concerned about, the impact of this

scenario and then determine the corresponding likelihood of this happening

Residual risk i.e. current risk level with existing controls in place

Identify the current controls in place that reduce this risk, are they effective?

Has the impact and likelihood of this risk changed due to these controls?

Target risk (if applicable) i.e. desired risk level to opitomise investment, as required

Is the net risk level acceptable, is there a need to reduce the risk or is there opportunity to take more risk?

Are there projects or additional opportunities to feasibly alter the impact and / or likelihood?

G

G

R

T

RISK MANAGEMENT HANDBOOK | Page 16

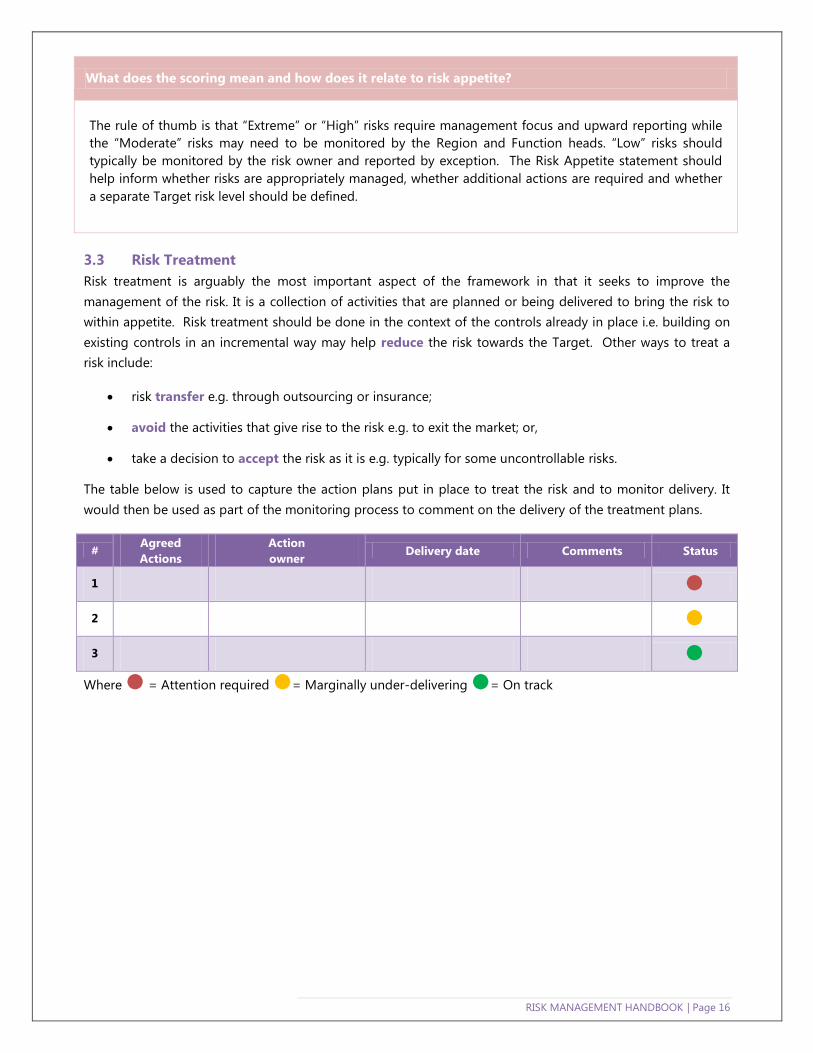

What does the scoring mean and how does it relate to risk appetite?

The rule of thumb is that “Extreme” or “High” risks require management focus and upward reporting while

the “Moderate” risks may need to be monitored by the Region and Function heads. “Low” risks should

typically be monitored by the risk owner and reported by exception. The Risk Appetite statement should

help inform whether risks are appropriately managed, whether additional actions are required and whether

a separate Target risk level should be defined.

3.3 Risk Treatment

Risk treatment is arguably the most important aspect of the framework in that it seeks to improve the

management of the risk. It is a collection of activities that are planned or being delivered to bring the risk to

within appetite. Risk treatment should be done in the context of the controls already in place i.e. building on

existing controls in an incremental way may help reduce the risk towards the Target. Other ways to treat a

risk include:

risk transfer e.g. through outsourcing or insurance;

avoid the activities that give rise to the risk e.g. to exit the market; or,

take a decision to accept the risk as it is e.g. typically for some uncontrollable risks.

The table below is used to capture the action plans put in place to treat the risk and to monitor delivery. It

would then be used as part of the monitoring process to comment on the delivery of the treatment plans.

# Agreed

Actions

Action

owner Delivery date Comments Status

1

2

3

Where = Attention required = Marginally under-delivering = On track

Tips for risk treatment

Where residual risks are assessed to be “Extreme” or “High” in the risk profile, action plans are to be

expected particularly where there is a low risk appetite

Thinking about incremental risk treatments is where the Guiding Principle to be proactive, innovative

and challenge the status quo can help and where real benefits of risk management are realised. Most

challenging business problems now require cross-functional teams that are prepared to challenge the

status quo.

When thinking about the actions needed, it may be helpful to address the causes articulated in the

risk identification section. Further root cause analysis techniques can be employed to identify the

specific problem to solve.

For material risks, the actions are likely to be carefully managed projects with defined budgets and

scope. These may further have project delivery risks to be managed.

3.4 Monitoring The final step in the risk management process is Risk Monitoring. This includes:

the identification of related emerging risks, issues and updated management information;

the assumptions related to existing risk analysis;

delivery of actions;

key risk indicators (“KRIs”).

The risk trend is identified during the regular assessment stage, informed by the above factors and shown as

an arrow pointed up for increasing risks, pointing down for decreasing risks and pointing to the right for the

same level of risk or N for a new risk.

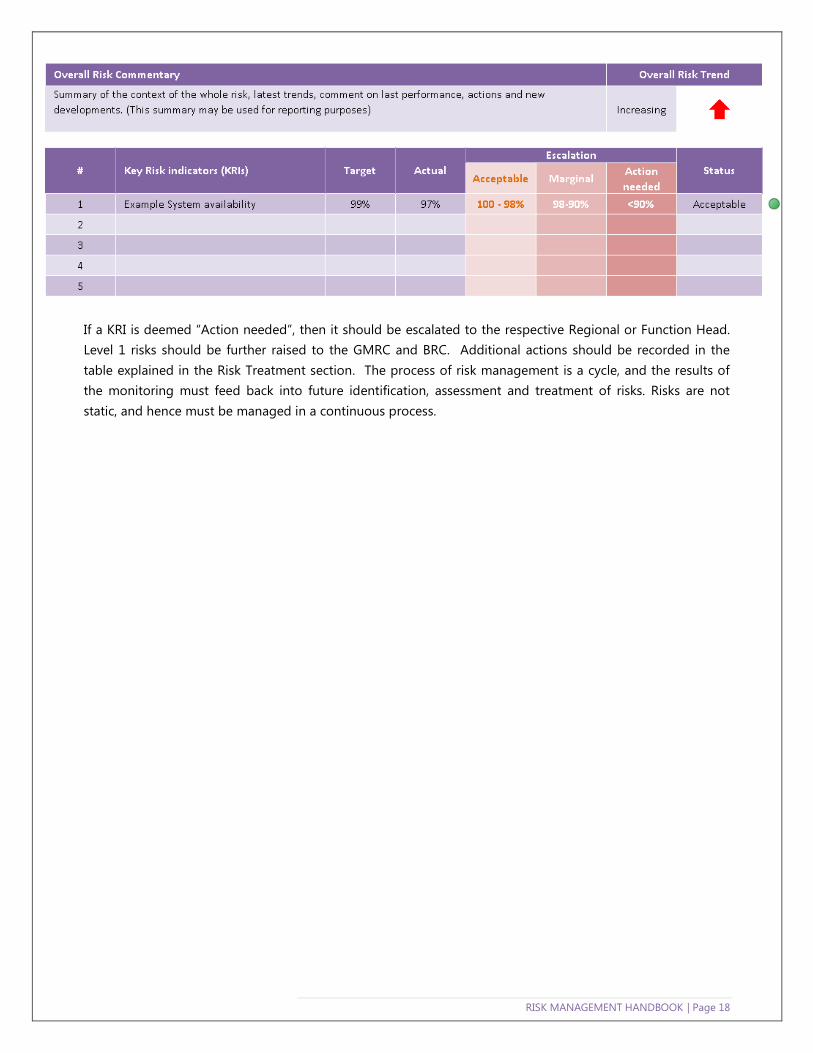

KRIs are a set of leading or lagging data points that gives insight into how the risk is trending and could

include measures of control effectiveness, incident history or performance. The KRIs support the Guiding

Principle around Prove it with data and is critical in making risk management discussions engaging and

valuable to senior stakeholders. These could be in varying formats and recorded in the following table which

include consideration of acceptable outcomes and points of escalation.

RISK MANAGEMENT HANDBOOK | Page 18

If a KRI is deemed “Action needed”, then it should be escalated to the respective Regional or Function Head.

Level 1 risks should be further raised to the GMRC and BRC. Additional actions should be recorded in the

table explained in the Risk Treatment section. The process of risk management is a cycle, and the results of

the monitoring must feed back into future identification, assessment and treatment of risks. Risks are not

static, and hence must be managed in a continuous process.

Appendix 1 | Page 1

Appendix 1: Risk Reporting Cycle

Risk reporting is aligned with the governance structures and embedded into the existing business planning process is an important aspect of operationalising

the Group’s risk management process. Exact dates and requirements will be set and communicated throughout the year and as meetings are planned.

Jan

Feb

Mar

Apr

May

Jun Jul

Aug

Sep

Oct

Nov

Dec

Annual report & accounts

Quarterly BRC and Board meeting

Quarterly BRC and Board meeting

Major Risks reviewed by GMRC as part of business

planning

CDL Risk Committee Meeting

CDL Risk Committee Meeting

CDL Risk Committee Meeting

CDL Risk Committee Meeting

Personal Development

reviews

GMRC meeting

Quarterly BRC and Board meeting

GMRC meeting

Quarterly BRC and Board meeting

GMRC meeting

CDL annual IT Risk reporting

Legal report Legal report

Legal report

Legal report

SHE report SHE report

SHE report

SHE report

Strategy session

Audit committee

Audit committee

Appendix 2 | Page 1

Appendix 2: Tools and Templates

Risk Profile

Risk Detail Form

Appendix 2 | Page 2

Appendix 3 | Page 1

Appendix 3 | Page 1

Appendix 3: Glossary of Risk Management Terms

Inherent (gross) risk the impact and likelihood of the risk occurring without taking into account any efforts or

controls the firm has put in place to manage it.

Key risk indicators – a set of leading or lagging data that gives insight into how the risk is trending and could

include measures of control effectiveness, incident history or performance

Residual (net) risk is the impact and likelihood of the risk occurring taking into account the existing efforts and

controls in place.

Risk appetite is the nature and amount of risk an organisation is prepared to take to achieve its objectives

Risks are uncertain events or factors that can affect the achievement of business objectives. It is measured in terms

of impact and likelihood and can include both up-side (opportunities) and down-side (threats).

Risk management is the continuous process of identifying, assessing, treatment and monitoring of risks.

Risk profile is the summary view of the key 8-12 risks affecting an area (i.e. the Board, Region, Function or individual

hotel), plotted against a matrix around the impact and likelihood of the key risks.

Risk owner is the named individual best placed and accountable for managing the respective risk and whose duty

includes the quarterly reporting of the risk details

Risk transfer is passing on of risk exposure to an external 3rd

party through contractual agreement, insurance or

outsourcing of the risk. Note that even if liabilities get transferred, there may still be reputation impact that remains

with the Group.

Appendix 4 | Page 1

Appendix 4: GMRC Terms of Reference

Group Management Risk Committee

Terms of Reference

GMRC – terms of reference

Owner: Group Risk Manager Issued: June 2017 Supersedes: N/A

Review date: June 2018 Page 1 of 3

GMRC – Terms of Reference | Page 2

Group Management Risk Committee (the “GMRC”) – Terms of Reference

Chairman Group Chief Executive Officer

Members Chief Financial Officer, Group General Counsel and Company Secretary, Chief

Commercial Officer and/or at least two Regional or Functional heads

Attendees Group Internal Audit (open invitation) and external risk consultants (as required)

Secretary Group Risk Manager

Quorum Chairman and two members of the Committee

Meeting frequency A minimum of three meetings per year

Approval date June 2017

1. Overall Purpose / Objectives

The GMRC has been established by the Chief Executive to ensure there is sufficient accountability and

management of key risks across the Group. These are reflected in the Board Risk Profile agreed by the Board

Risk Committee (the “BRC”). The GMRC is authorised to make decisions (decisions will be based on majority

rule) to manage risks within the appetite set by the BRC, however must do so in the context of other policies

and procedures i.e. budget, delegation of authorities, procurement etc. The GMRC will meet at least three

times a year, will receive reports of risks from within the business and will seek assurance these are

appropriately managed from the Heads of Regions and Functions. The GMRC must also determine whether

any new, emerging or escalated risks should be further reported to the BRC.

2. Roles and Responsibilities

The GMRC will:

2.1. Ensure key risks to the Group are appropriately owned, assessed, resourced and managed. Record

these risks and corresponding details in a Board Risk Profile.

2.2. Review the Board Risk Profile on a quarterly basis and consider emerging risks or changes to existing

risks.

2.3. Receive reports from the Regional and Functional heads on risks within their respective areas on a

quarterly basis and be satisfied that these risks are being managed. Ensure Regions and Functions are

reviewing and engaging with risk management.

2.4. Provide guidance, resource or any suitable support to the Regions and Functions to help address risks

in the business and determine whether these risks should be reported to the Board Risk Committee.

2.5. Annually review and assess the effectiveness of the risk management policy and the Group’s approach

to risk management and whether changes or improvements to processes and procedures are necessary.

GMRC – Terms of Reference | Page 3

3. Reporting Responsibilities

3.1. The Chairman will report formally to the BRC after each GMRC meeting on all matters within the

Committee’s duties and responsibilities. This report shall include:

An update on the Board Risk Profile, highlighting any changes and significant developments

since the previous report

An update on any new or emerging risks affecting the Group and any action plans being put in

place to manage them

The extent to which the business has reviewed and updated its risks in-line with the risk

management policy

4. Other Responsibilities

4.1. Annually review and propose the overall levels of insurance for the group including directors' & officers'

liability insurance and indemnification of directors to the Board Risk Committee.