Embed Size (px)

Citation preview

Poland:The business outlook

For members of the East European Group

August 2009

Corporate Network

Sponsored by:

Contents

• Corporate comment

• Executive summary

• Business outlook

• Policy outlook

• Economic outlook

• Key economic indicators

• Market size indicators

Corporate comment

“Even in crisis mode, Poland is still one of the best-performing markets in Europe.”

-Country manager, US consumer durables firm

“We see great opportunity for expansion in Poland. The local market is still underdeveloped. Infrastructure is slowly improving and companies are becoming more advanced. It is a huge, young consumer market with significant growth potential.”

-Regional director, Asian consumer durables firm

“Poland leads CEE in terms of quality of talent…Cash expectations were in the past extremely high but they are now coming down to more reasonable levels.”

-Regional director, European professional services firm

Executive summary

• Poland’s economy is contracting this year, but the recession will be mild at less than -1%

• Despite weak exports and sluggish private consumption, government spending is relatively strong

• Poland will retain its stature as one of the stars of CEE as it bounces back from the crisis faster and stronger than other markets

• While the business outlook is muted it has remained relatively steady throughout 2009

• After a steep depreciation at the beginning of the year the zloty has stabilised along with other CEE currencies

Business outlook – performance benchmarking

• The business outlook in Poland has remained relatively steady throughout the year even while tumbling in neighbouring countries

• 38% of respondents expect sales to improve this year, and 27% expect them to remain at 2008 levels, while 35% foresee decline

• The median forecast for baseline sales growth climbed from +3% in February to +5% in May

• A quarter of firms tell us they are having more difficulty collecting receivables

• On cost cuts, 46% say they are planning to trim advertising budgets16% say they will lay off white-collar staff and 14% plan to delay manufacturing investments

Business outlook – performance benchmarking

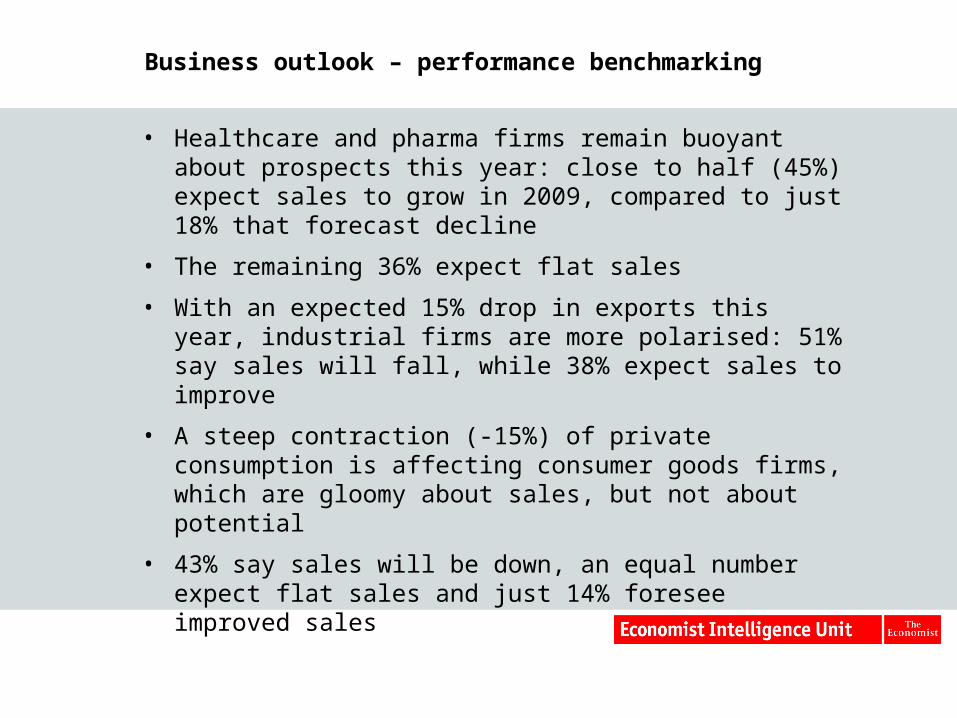

• Healthcare and pharma firms remain buoyant about prospects this year: close to half (45%) expect sales to grow in 2009, compared to just 18% that forecast decline

• The remaining 36% expect flat sales

• With an expected 15% drop in exports this year, industrial firms are more polarised: 51% say sales will fall, while 38% expect sales to improve

• A steep contraction (-15%) of private consumption is affecting consumer goods firms, which are gloomy about sales, but not about potential

• 43% say sales will be down, an equal number expect flat sales and just 14% foresee improved sales

Business outlook - business environment

• Reforms happen slowly and are often delayed, but the government is committed to improving investment conditions

• It recently unveiled an online tax portal which allows business to file all forms electronically rather than in paper

• However, cumbersome and non-standardised regulations continue to impede business

• Infrastructure remains a headache…

• … but work on motorways and bottlenecks is accelerating ahead of the 2012 Euro Championships

Policy outlook

• The centre-right government came into office on a market-friendly platform, though it has proceeded cautiously with economic reform…

• …due to constraints from coalition partners and the deteriorating economic climate

• The budget deficit will widen from 3.9% last year to around 6%, as revenue falls and with the elimination of the top 40% personal income tax bracket

• The government wants to resume progress in budget consolidation in 2010 as the economy begins to recover

• Authorities have announced plans for a wave of privatisations this year and next, as a means of plugging revenue holes in the state budget

Economic outlook – IMF intervention

• In May, Poland signed a US$20.6bn, one-year Flexible Credit Line (FCL) with the IMF

• The FCL, a precautionary facility that can be drawn upon at any time, was available only to the most stable emerging-market states with solid fundamentals

• It comes without any need to meet specified fiscal conditions, making it radically different from the IMF facilities taken up by other east European states

• The funds are not needed to plug a hole in the budget…

• …rather, they would go straight to the central bank's reserves, bolstering the position of the zloty

• Poland has yet to draw from the facility

Economic outlook – growth

• Despite strong fundamentals, growth in Poland will contract this year by about 0.8%

• The economy has taken a blow from exceptionally weak external demand in western Europe, a steep fall in the zloty which dented corporate confidence, and continued strains on global credit

• However, there are already signs of a minor recovery in industrial output

• The economy is likely to post subdued growth of around 1.5% in 2010 as a degree of consumer and business confidence returns

• Private consumption and exports will remain limited, but fixed investment is expected to pick up

Economic outlook – currency volatility

• The zloty was a popular speculative currency when times were good and it strengthened too much…

• …at least 10-15% stronger than the fundamentals would suggest

• When portfolio investors and speculators started to panic about CEE, the zloty fell more than it deserved

• The zloty has since stabilised, but market sentiment towards the region’s emerging markets remains fragile…

• …which means the currency will continue to be volatile

• If there are no more shocks to the global economy, the zloty should average 4.51 to the euro, before appreciating slightly to 4.22 in 2010

Economic outlook – external sector

• The Polish economy has been run prudently: the current account, external debt, budget deficit and public debt were within manageable benchmarks going into the crisis

• However, large repayments of short- and medium-term debt due in 2009, easily serviceable in relatively normal credit times, spooked markets

• Poland’s signing of the FCL with the IMF effectively quelled these fears

• FDI flows are expected to halve in 2009 to around $8bn and pick up slowly in 2010 with global investment remaining fragile

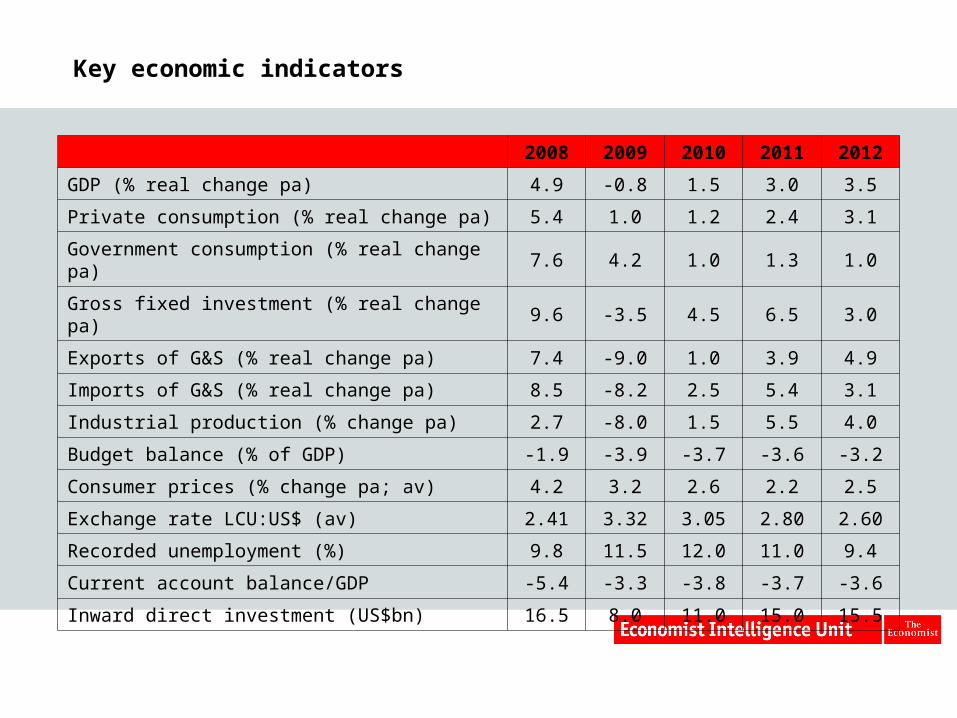

Key economic indicators

2008 2009 2010 2011 2012

GDP (% real change pa) 4.9 -0.8 1.5 3.0 3.5

Private consumption (% real change pa) 5.4 1.0 1.2 2.4 3.1

Government consumption (% real change pa) 7.6 4.2 1.0 1.3 1.0

Gross fixed investment (% real change pa) 9.6 -3.5 4.5 6.5 3.0

Exports of G&S (% real change pa) 7.4 -9.0 1.0 3.9 4.9

Imports of G&S (% real change pa) 8.5 -8.2 2.5 5.4 3.1

Industrial production (% change pa) 2.7 -8.0 1.5 5.5 4.0

Budget balance (% of GDP) -1.9 -3.9 -3.7 -3.6 -3.2

Consumer prices (% change pa; av) 4.2 3.2 2.6 2.2 2.5

Exchange rate LCU:US$ (av) 2.41 3.32 3.05 2.80 2.60

Recorded unemployment (%) 9.8 11.5 12.0 11.0 9.4

Current account balance/GDP -5.4 -3.3 -3.8 -3.7 -3.6

Inward direct investment (US$bn) 16.5 8.0 11.0 15.0 15.5

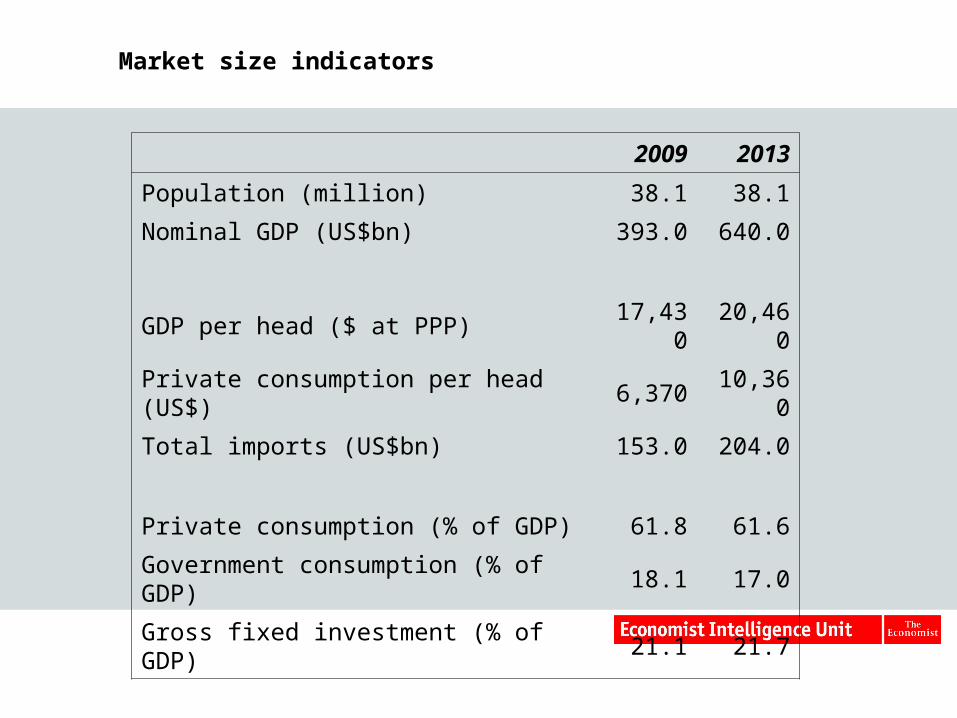

Market size indicators

2009 2013

Population (million) 38.1 38.1

Nominal GDP (US$bn) 393.0 640.0

GDP per head ($ at PPP) 17,430 20,460

Private consumption per head (US$) 6,370 10,360

Total imports (US$bn) 153.0 204.0

Private consumption (% of GDP) 61.8 61.6

Government consumption (% of GDP) 18.1 17.0

Gross fixed investment (% of GDP) 21.1 21.7

Corporate Network is the Economist Intelligence Unit's exclusive, membership-based senior executive briefing and networking service. Independent, thought provoking, and opinion-leading, Corporate Network is led by experts who share a profound knowledge and understanding of business issues. It has regional business groups in Central and Eastern Europe, Middle East & Africa, and Asia Pacific.

Economist Intelligence UnitCorporate NetworkOelzeltgasse 3/71030 Vienna, AustriaTelephone: (43 1) 712 41 61 40Fax: (43 1) 714 67 69www. corporatenetwork.com

Copyright

© 2009 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior permission of The Economist Intelligence Unit Limited.