Embed Size (px)

Citation preview

4

Planning and Retail Statement

Caerphilly Road, Cardiff 17/3402N

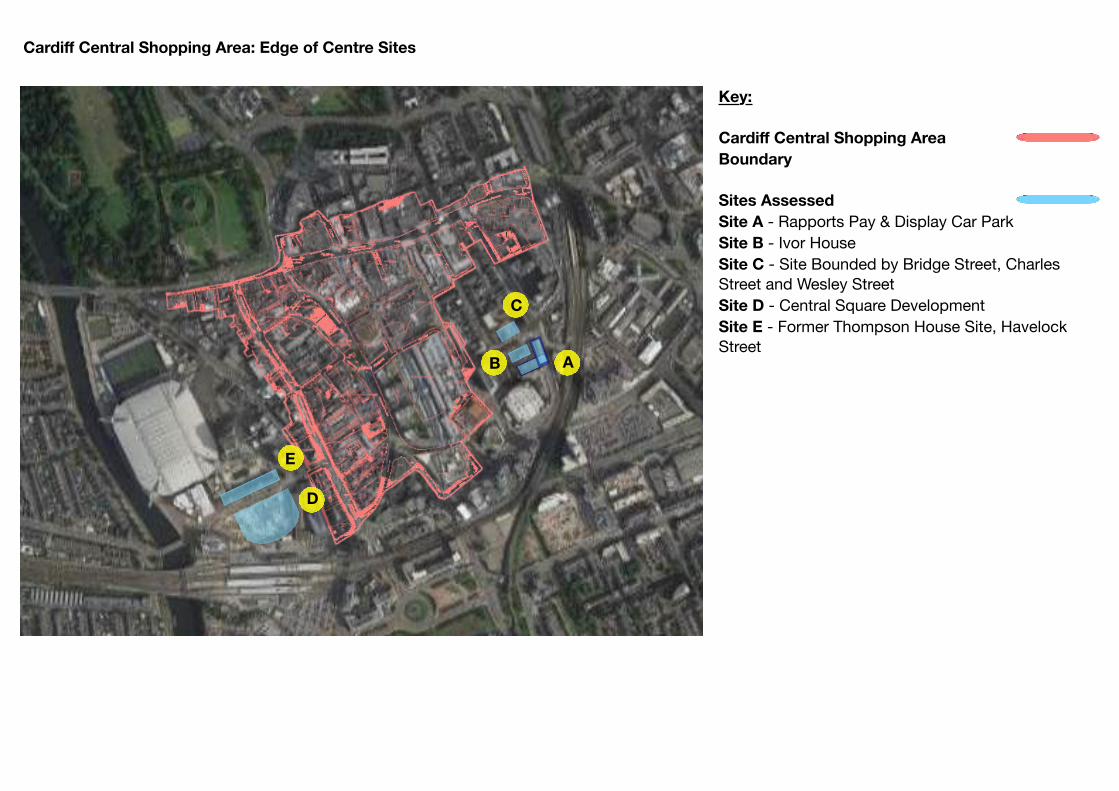

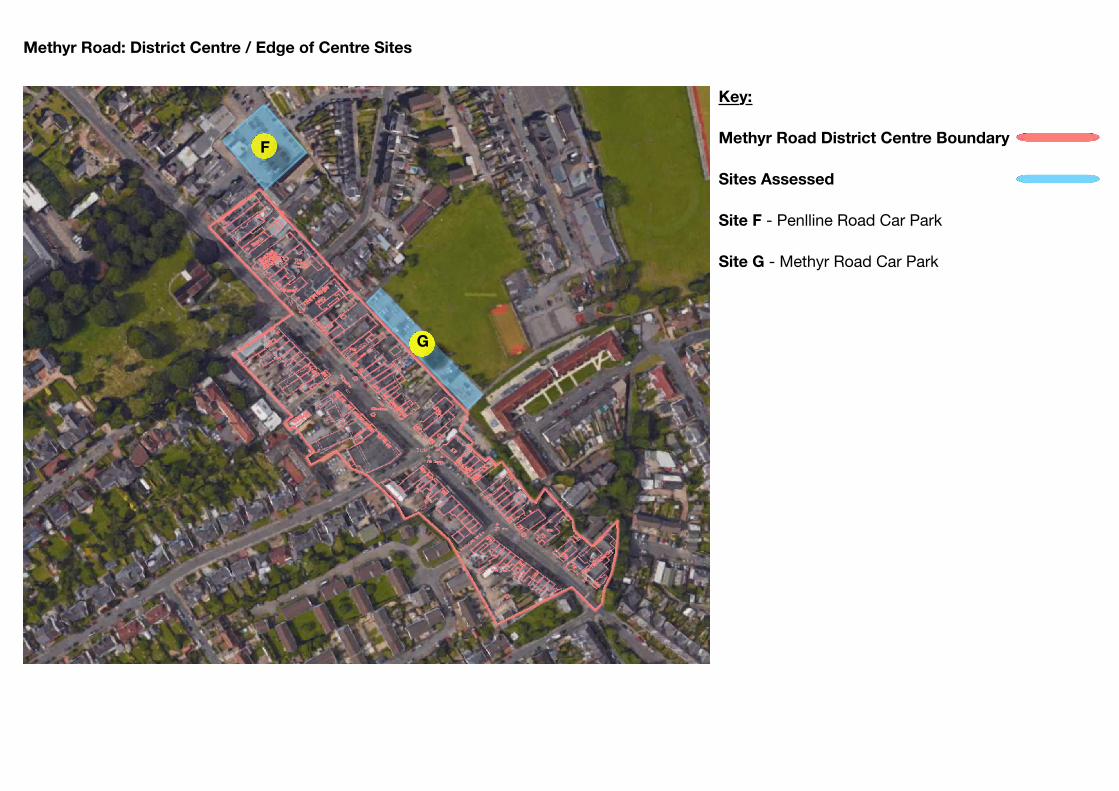

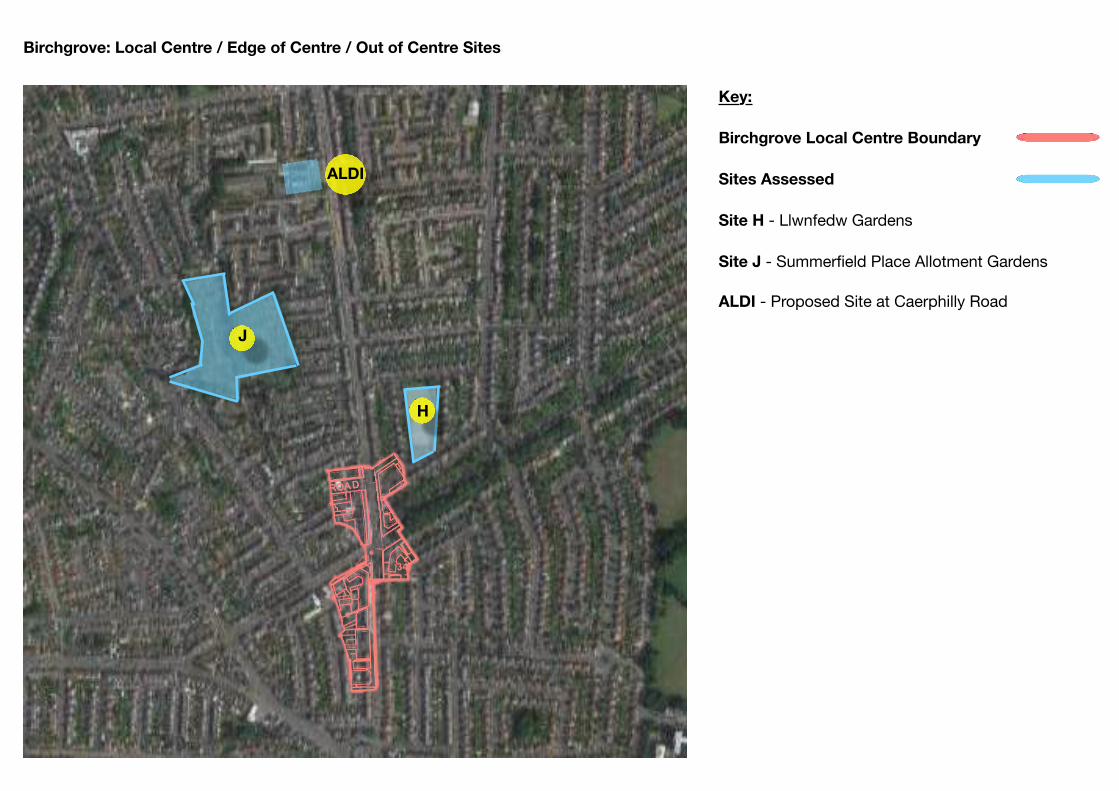

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page i

Contents

Executive Summary

1. Introduction

2. Site Context and Development Proposals

3. Planning Policy Context

4. Retail Context

5. The Sequential Approach

6. Retail Need and Impact Assessment

7. Other Material Considerations

8. Summary and Conclusions

Appendix 1: Site Location Plan

Appendix 2: Retail Provision Plans

Appendix 3: Sequential Assessment Maps

Appendix 4: Retail Impact Assessment Tables

Planning Potential Ltd

Bristol 13-14 Orchard Street Bristol BS1 5EH T: 0117 214 1820

Report Author: [email protected]

Report Reference: 17/3402N

ALDI FOODSTORES LTD May 2017

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page ii

Executive Summary

This Statement has been prepared on behalf of ALDI Stores Ltd in support of the significant investment proposed at Caerphilly Road, Cardiff. The development will comprise a discount foodstore, with associated car parking and landscaping.

ALDI’s interest in the site has arisen through the requirement for a store to serve the northern Cardiff area.

This Planning and Retail Statement considers the relevant national and local planning policy issues that are pertinent to the consideration of the proposed development. Specifically, this Statement sets out and demonstrates the proposal’s compliance with the retail needs test, sequential approach to site selection, and the retail impact tests.

The statement also demonstrates that the proposal would make efficient use of the vacant site by proposing a deliverable ALDI foodstore scheme which would enhance the amenity of the site and improve the streetscene of the wider area.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 1

1. Introduction

1.1. This Planning and Retail Statement is submitted by Planning Potential, on behalf of ALDI Stores Ltd (ALDI), in support of a full planning application for the erection of a Class A1 retail foodstore, and associated access, car parking, and landscaping at Caerphilly Road, Cardiff.

1.2. The application proposal is described as follows:

“The demolition of existing buildings and erection of a Class A1 foodstore (1,717sqm gross floor area) with associated access, car parking and landscaping.”

1.3. This Statement addresses all of the relevant planning policy considerations associated with the proposed development, but should be read in conjunction with other documents and drawings submitted in support of this application.

1.4. Prior to submitting this application proposal, ALDI held discussions with Council Officers and statutory consultees.

1.5. This assessment is set out as follows:

Section 2 – Summarises the site context and the development proposals;

Section 3 – Sets out the planning and retail policy context against which the proposal should be assessed, including national policy and the Development Plan;

Section 4 – Outlines the retail context, the ALDI business model, and considers the relevant centres, drawing on information from the Council’s retail evidence base;

Section 5 – Sets out our assessment of key planning issues relating to the proposed development, in particular the Sequential Test;

Section 6 – Sets out our retail need and impact assessment;

Section 7 – Considers other relevant planning issues associated with the proposed development; and

Section 8 – Presents our summary and conclusions.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 2

2. Site Context and Development Proposals

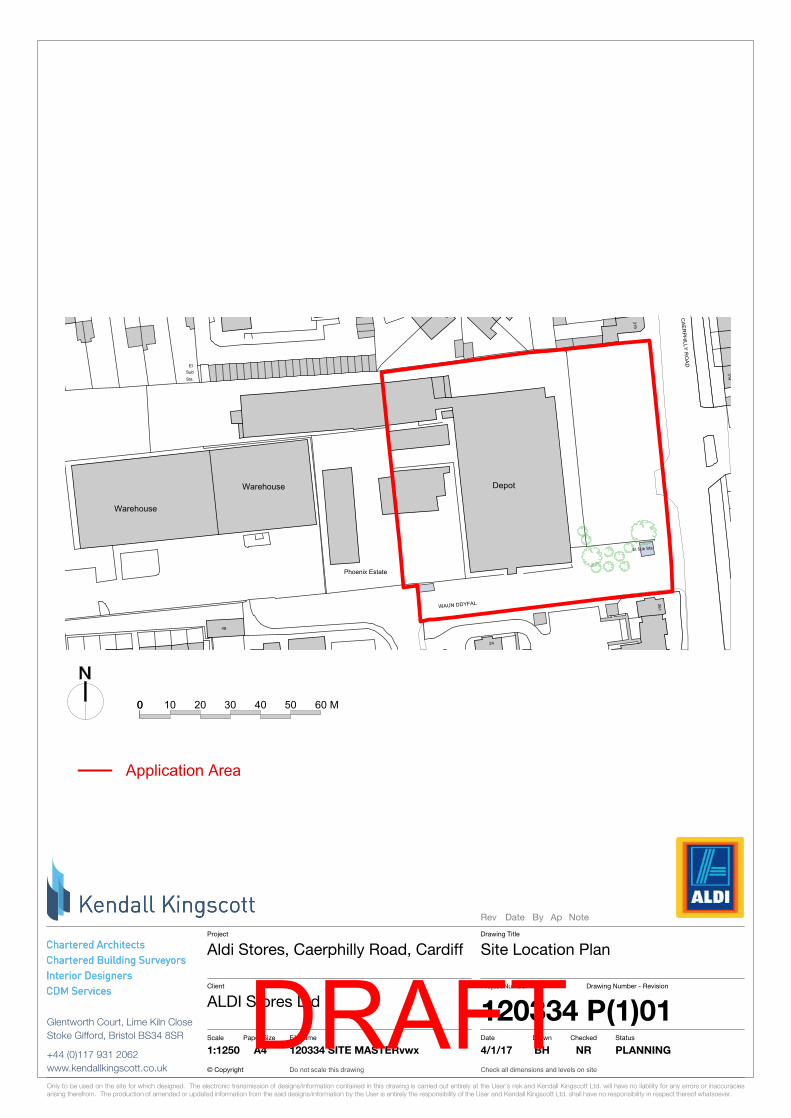

The Site

2.1. The proposed ALDI site extends to approximately 0.7 hectares. This is the front portion of a larger former industrial site of 1.6 hectares. The proposed ALDI site comprises a number of vacant and/or derelict commercial buildings and warehouses. These include a series of single storey industrial units and one two storey building. These provide approximately 4,000sq m gross floorspace.

2.2. There is a group of large trees located within the south-eastern corner of the site.

2.3. The site is located on the western side of Caerphilly Road and also incorporates part of Waun Ddyfal to the south. The site is surrounded by a mixture of uses from residential dwellings, retirement accommodation, a hot food takeaway, offices, a healthcare clinic, pharmacy and commercial warehouse buildings.

2.4. In retail terms, the site occupies an out-of-centre location and is situated approximately 2.9 miles to the north of Cardiff’s defined Central Shopping Area shown on the Local Development Plan (LDP) Proposals Map (adopted January 2016).The site is also located:

0.5 miles (0.8km) to the north of Birchgrove Local Centre,

0.7 miles (1.1km) to the south-east of Riwbina Village Local Centre,

1.2 miles (1.9km) to the south-west of Station Road, Llanishen Local Centre

1.3 miles (2.1km) to the north-east of Merthyr Road District Centre.

0.2 miles (0.3km) from the Cardiff Business Park which contains a (amongst other commercial uses) a Lidl Supermarket, a Tesco express, and Domino’s Pizza. The business park is not designated as a ‘shopping centre’ in retail policy terms

Site Planning History

2.5. A review of the City Council’s online planning resources indicates that the site was used as a petrol filling station between the late 1980’s and approximately 2008 and there have been various small scale applications related to the filling station use (i.e. signage, jet wash, ATM). Planning permission was also granted on 17th January 2007 (ref. 06/01441/E) to demolish the existing TEXACO filling station and erect four town houses and twelve residential flats.

2.6. There is no available planning history for the remainder of the site. However, it is understood that the site was most recently occupied by Electrocoin, who manage and distribute coin operated gaming machines.

2.7. The land to the south of the site was a former industrial location (known as Phoenix Works) redeveloped by a major housebuilder in the late 90s / early 2000s. We understand that the stopping up of Waun Ddyfal was a condition or obligation of the planning permission. As a result, the land owners of the proposed ALDI site

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 3

surrendered their access rights through Waun Ddyfal in exchange for a right of access through the new development via Phoenix Way.

2.8. In addition to the above stopping up of Waun Ddyfal, a bus stop has been created outside of the proposed ALDI site, together with the installation of bollards and a vehicle parking bay accommodating 5-6 vehicles.

2.9. A bus lane has also been created on Caerphilly Road, which runs from the junction with Phoenix Way to the junction with Ty-Wern Road.

Other Relevant Planning History

2.10. A Morrisons Superstore and a Marks and Spencer Simply Food store are located within 1 mile (1.6km) to the north of the site on Ty-Glas Road which is off the Thornhill Road/Beulah Road roundabout.

2.11. The Morrisons Superstore was established via planning permission in September 1989 (ref: 89/01470/N) for a retail development to include food store and DIY store.

2.12. The Marks and Spencer Simply Food store was granted planning permission (Ref:

00/01081/N) in November 2002 as part of a wider retail development along with associated car parking access and landscaping works.

2.13. It is unclear exactly when the existing Lidl supermarket on Caerphilly Road was

established, but permission was granted in July 1999 (ref: 99/00723/N) for 997 square metres of retail floorspace with 174 parking spaces. Permission was granted in July 2007 (ref:07/00016/E) for the demolition of existing factory and change of use to A1 retail, with the construction of a single storey warehouse extension together with car parking and landscaping alterations. This application was subsequently renewed in November 2011 (ref:11/00311/DCO) which extended the application for a further five year period.

2.14. A further planning permission was granted in February 2015 (ref:14/00971/DCO)

for the demolition of the existing store and the redevelopment of the site to provide a larger store which would extend over the adjacent former ice cream factory site to the east. The proposal resulted in the gross internal area increasing from 1,270sq m to 2,419sq m and retail floor space increasing from 985sq m to 1,407sq m, with revised associated parking.

The Proposed Scheme

2.15. This planning application proposes the erection of a Class A1 foodstore with approximately 1,717sq m gross floor area with a net sales area of 1,254sq m, 337sqm of warehouse space, and a 126sqm staff welfare area. The proposal also involves associated access, car parking, and landscaping works.

2.16. The proposed ALDI foodstore would consist of the main retail area, a warehouse which includes a loading bay and freezers, and a staff welfare area (staff room, kitchen, and toilets). The building would be of a mono-pitched roof design that would increase in height from north to south. The maximum height of building would be 7.84m to the roof and 4.18m to the canopy measured from ground level.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 4

2.17. The proposal includes hard and soft landscaping, which will complement the site and surrounding environment. The landscaping proposed will include a number of new trees and planting along the Caerphilly Road frontage which will significantly enhance the appearance of the site when compared to the current and previous appearance of the site which consists of vacant and derelict industrial buildings. The landscaping scheme will also include a number of street frontage trees, further enhancing the appearance of the site and the wider street scene.

2.18. The proposed car park will provide 125 customer car parking spaces. The parking provision includes ten parent and child spaces and four designated spaces for blue badge users. Ten cycle parking spaces are also proposed. The proposal will result in more local provision and could result in linked trips to adjacent local businesses.

2.19. The proposed site access and car park entrance would be established from Caerphilly Road. Highways works are also proposed including the provision of a right turn lane within the southbound carriageway.

2.20. The proposed ALDI foodstore would employ approximately 40 staff and would be open to customers on Monday to Saturday 8am -10pm and on Sundays between 10am and 5pm.

Pre-Application Dialogue

2.21. Prior to submitting the application, ALDI sought pre-application advice from Officers at Cardiff City Council. The issues discussed focused on the recent highways works, access to the site, the housing allocation which covers part of the site, and retail policy considerations.

2.22. Discussion was undertaken regarding the recent highways works along Caerphilly Road which included on-street parking, a bus stop and bus lane, and bollards across the frontage of the site. Council Officers confirmed that highways works were progressed to reduce congestion along Caerphilly Road.

2.23. Other access options were suggested by Council (rather than off Caerphilly Road) including Phoenix Way to the south. ALDI noted that this would not be suitable due to HGV/servicing access being impeded by unrestricted on-street parking in the residential estate. Furthermore, such an arrangement would create a convoluted access for customers.

2.24. The discussion also covered the housing allocation for 20 Units (Policy H1.8) that covers part of the ALDI site. The designation covers the Electrocoin land ownership and excludes the former petrol station site and land to the rear.

2.25. ALDI acknowledged the allocation. However, it was stressed that the deliverable ALDI proposal could kick-start wider development, and that the housing allocation would be difficult to develop in isolation, due to its unusual shape. The proposal would demonstrate that the ALDI proposal will encourage and not constrain the development of the land to the rear.

2.26. The matters raised above will be considered and addressed in the subsequent sections of this report.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 5

3. Planning Policy Context

3.1. The following section provides a summary of the relevant national and local planning policy relevant to the proposed development of an ALDI foodstore at the application site.

Planning Policy Wales (2016)

3.2. Planning Policy Wales (PPW), Edition 9, was published in November 2016 and sets out the land use planning policies of the Welsh Government. The PPW translates the Government’s commitment to sustainable development into the planning system so that it can play an appropriate role in moving toward sustainability.

3.3. The PPW is supplemented by a series of Technical Advice Notes (TANs) which will be discussed in more detail below.

Retail Guidance

3.4. National policy applying to proposals involving retail development is set out at Chapter 10 of the PPW.

3.5. Clause 10.1.2 states that the Welsh Government’s objectives for retail and commercial centres are to:

Promote viable urban and rural retail and commercial centres as the most sustainable locations to live, work, shop, socialise and conduct business;

Sustain and enhance retail and commercial centres’ vibrancy, viability and attractiveness; and

Improve access to, and within, retail and commercial centres by all modes of transport, especially walking, cycling and public transport.

3.6. Clause 10.1.4 introduces the Government’s adopted ‘town centres first’ principle whereby consideration should always be given in the first instance to locating new retail and commercial development within an existing centre.

3.7. Paragraph 10.2.14 states that ‘first preference should be for a site allocation or development proposal located in a retail and commercial centre defined in the development plan hierarchy of centres.’

3.8. Paragraph 10.2.14 sets out the sequential assessment process: ‘If a suitable site or building is not available within a retail and commercial centre or centres, then consideration should be given to edge of centre sites and if no such sites are suitable or available, only then should out-of-centre sites in locations that are accessible by a choice of travel modes be considered.’

3.9. The same paragraph then emphasises that ‘Developers should demonstrate that all potential retail and commercial centre options, and then edge-of-centre options, have been thoroughly assessed using the sequential approach before out-of-centre sites are considered.’

3.10. Paragraph 10.2.16 states that new out-of-centre retail developments or extensions to existing out-of-centre developments should not be of a scale, type

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 6

or location likely to undermine the vitality, attractiveness and viability of those retail and commercial centres that would otherwise serve the community well, and should not be allowed if they would be likely to put development plan retail strategy at risk.

3.11. Paragraph 10.4 of PPW focuses on Development Management of retail proposals. Paragraph 10.4.1 lists 10 factors that LPAs should take into account when determining retail, commercial and leisure applications. These are:

compatibility with the development plan;

quantitative and qualitative need for the development/extension, unless the proposal is for a site within a defined centre or one allocated in an up-to-date development plan;

the sequential approach to site selection;

impact on existing centres;

net gains in floorspace where redevelopment is involved and whether or not it is like-for-like in terms of comparison or convenience;

rate of take-up of allocations in any adopted development plan;

accessibility by a variety of modes of travel;

improvements to public transport;

impact on overall travel patterns; and

best use of land close to any transport hub, in terms of density and mixed use.

3.12. Paragraph 10.4.2 encourages developers of larger schemes to consider how they integrate into the wider public realm, and whether this can be improved.

3.13. Paragraph 10.4.3 clarifies that LPAs should consider the likely cumulative effects of recently completed development, planning permissions and planned commitments within a catchment area.

3.14. Paragraph 10.4.4 sets a 2,500sqm national gross floorspace threshold, above which a retail impact assessment is required for edge-of-centre and out-of-centre proposals, while also giving LPAs scope to assess whether smaller developments should present proportionate impact assessments.

3.15. Paragraph 10.4.5 clarifies that need, sequential and impact assessments may be applied to new retail proposals, aside from where they are in accordance with an up to date development plan.

3.16. Paragraph 10.4.15 concludes the section on development management and states that ‘planning application for retail development should not normally be permitted on land designated for other uses.’ In particular, it specifies that retail development can limit the range and quality of sites allocated for industry, employment and housing.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 7

Technical Advice Notes (TANs) Relevant to Retail Development

3.17. TAN 4 (2016) specifically relates to retail and commercial development.

3.18. Objective 1 of TAN 4 reflects the ‘town centre first’ approach of the PPW and states that viable urban and rural retail and commercial centres need to be promoted as the most sustainable locations to live, work, shop, socialise and conduct business.

3.19. Part 6 sets out the Tests of Retail Needs. The retail needs tests are of a quantitative and qualitative nature, and are required to be undertaken for any application in an edge-of-centre or out-of-centre location which is not in accordance with an adopted development plan. It is also notes that this is the starting point for planning new retail development in both development plans and development management.

3.20. Paragraph 6.3 clarifies that there is no particular methodology prescribed by the Welsh Government, instead developers and LPAs are encouraged to prepare assessments in a clear logical and transparent way, with robust and realistic evidence.

3.21. Paragraph 6.5 confirms that quantitative retail need should be established, before other, qualitative aspects of need are considered. Paragraph 6.6 states that the latter is harder to justify and will be subject to close scrutiny. It notes that the overall aim of assessing qualitative need is to achieve an appropriate distribution and range of sites for stores to meet the need of all communities, particularly where provision is inadequate.

3.22. Part 7 identifies the sequential test approach which requires that only when retail and commercial centres and edge of centre locations have been considered and found to be unsuitable can out-of-centre options within, and then outside, a settlement area be considered.

3.23. Paragraph 7.4 provides guidance on the application of the Test, noting that edge-of-centre proposals should not normally be located more than 200 to 300 metres from the edge of the centre.

3.24. The same paragraph also states that the size of the retail and commercial centre, local topography and presence of physical barriers to access may influence any assessment. For example it may limit the area that can be considered edge-of-centre for a smaller or more constrained centre.

3.25. Finally on this issue, paragraph 7.5 states that ‘developers and retailers should be flexible and innovative about the format, design and scale of proposed development and the amount of car parking needed, tailoring these to fit local circumstances.’

3.26. Paragraph 8.2 outlines the requirements for retail impact assessments. Retail applications of 2,500 sq. metres or more gross floorspace that are proposed on the edge of or outside retail and commercial centres should be supported by a retail impact assessment provided by the developer. It notes that smaller retail planning applications or site allocations may also be assessed where local planning authorities believe it will have a significant impact on a retail and commercial centre.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 8

3.27. TAN18 (Transport) states that Planning applications for development schemes for food retail over 1,000sq m GFA will need to be supported by a Transport Assessment (TA). The TA will provide the basis for assessing all the potential travel impacts of developments including their effect on the highway network and the likely modal split of the trips that would be generated. This assessment will help establish the gaps in existing transport provision and the measures necessary to make a development accessible by sustainable modes.

Cardiff Local Development Plan 2006-2026

3.28. Policy KP5 (Good Quality Sustainable Design) requires that all new development will be required to be of a high quality sustainable design, and make a positive contribution to the creation of distinctive communities, places and spaces.

3.29. Policy KP8 (Sustainable Transport) states that the purpose of this Key Policy is to ensure that developments are properly integrated with the transport infrastructure necessary to make developments accessible by sustainable travel modes and achieve a necessary shift away from car-based travel.

3.30. Policy KP15 (Climate Change) states that a core function of the Plan is to ensure that all development in the city is sustainable, taking full account of the implications of reducing resource use and addressing climate change. The policy promotes development that mitigates the causes of climate change and which is able to adapt to its likely effects.

3.31. Policy R1 (Retail Hierarchy) sets out the retail hierarchy, stating that any new retail development should be prioritised first within the Central Shopping Area (CSA), then within a district or local centre. Any proposed retail development outside of one of these centres must be assessed against Policy R6.

3.32. Policy EC3 (Alternative Use of Employment Land and Premises) states that development of business, industrial and warehousing land and will only be permitted if:

The land or premises are no longer well located for business, industrial and warehousing use; or

There is no realistic prospect of employment use on the site and/or the property is physically unsuitable for employment use, even after adaption/refurbishment or redevelopment; or

There is no need to retain the land or premises for business, industrial or warehousing use, having regard to the demand for such land and premises and the requirement to provide for a range and choice of sites available for such use; and

There will be no unacceptable impact on the operating conditions of existing businesses.

3.33. Policy R6 (Retail development (Out of Centre) states that retail development will only be permitted outside of the CSA, District, and Local Centres where:

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 9

there is a need for the proposed floorspace, and cannot satisfactorily be accommodated within or adjacent to the CSA, or within a District or Local Centre;

the proposal would not cause unacceptable harm to the vitality, attractiveness or viability of the CSA, a District or Local centre or a proposal or strategy including the Community Strategy, for the protection or enhancement of these centres;

the site is accessible by a choice of means of transport; and

the proposal is not on land allocated for other uses.

3.34. Paragraph 5.284 states that the aim of Policy R6 is to control the nature and size of out-of-centre retail development so as to minimise competition with, and impact on the vitality and viability of shopping centres identified in the Plan.

3.35. Paragraph 5.286 sets out the sequential test order of preference. In Cardiff the order of preference is:

Within the Central Shopping Area;

On the edge of the Central Shopping Area;

Within a District or Local Centre;

On the edge of a District of Local Centre;

An out-of-centre location accessible by a choice of means of transport.

3.36. Paragraph 5.288 states that Impact will be assessed in terms of both the direct commercial impact of a proposal on neighbouring designated centres, and of the impact on the retail strategy itself. Harm will be assessed in terms of individual and cumulative effects.

3.37. Policy H1 (Non-Strategic Housing Sites) provides a list of sites to provide 572 dwellings, and identifies that part of the site is located within a designated non-strategic housing site (H1.8: Electrocoin Automatics Ltd). This designated site is 0.61 hectares and has been considered acceptable in principle for residential use with a capacity for approximately 20 units.

3.38. Paragraph 5.2 states that the proposed number of units shown for each site is indicative only and may be subject to change depending on details of planning application for the site.

Retail Evidence Base

3.39. The retail evidence base for the document comprises:

Local and District Centre Floorspace Survey (September 2008) (Colliers);

District and Local Centres Strategy (2012)

Retail Capacity Study (March 2009) (Colliers);

Retail Capacity Study Update (March 2011) (Colliers); and

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 10

Cardiff Out-of-centre Retail Monitoring Schedule (July 2013) (Cardiff City Council).

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 11

4. Retail Context

4.1. This Section provides further context in respect of the retail background to the proposals, where relevant to the need, impact and sequential tests as outlined in Section 3.

ALDI Stores Limited

4.2. The nature and scale of the retail floorspace proposed and, accordingly, its intended role and function, is a key consideration.

4.3. In this instance, the application relates to a new ALDI foodstore, which will primarily serve the Northern area of Cardiff, but will also improve local choice and competition generally.

4.4. ALDI provides a mainly convenience retail offer and functions primarily to complement a weekly destination shop.

4.5. As well as having a limited number of product lines, ALDI do not have in-store kiosks (e.g. cigarettes) or specialist concessions, such as an in-store butcher, fishmonger or pharmacy. Therefore, unlike other supermarkets, ALDI stores do not act as a ‘one-stop-shop’.

4.6. This means that in order to complete their weekly shop, ALDI customers will also generally visit other retail premises elsewhere. Consequently, the introduction of an ALDI within a local market catchment means customers will be shopping at a store in addition to, rather than instead of, other shops. The result and reality is that ALDI complements a catchment, particularly in respect of local shops and services.

4.7. Crucial to the function of an ALDI store is a tried and tested business model, and indeed this is recognised by retail industry classifications. These identify ALDI as a Limited Assortment Discounter (LAD), or ‘Deep Discounter’.

4.8. The ALDI store format and layouts are consistent throughout the property portfolio, and this is essential for ALDI to provide their retail offer. This is a further difference between ALDI and their main convenience competitors, who all offer a range of store formats and sizes.

4.9. ALDI recognises the need for flexibility in promoting sites for development and pursue non-standard stores where this will assist in meeting planning policy requirements. When considering the scope for flexibility, however, the inherent nature of ALDI’s operation as a discount food retailer must be borne in mind. Accordingly, there are a number of key areas where it is not possible to alter the core design of the store; as to do so would undermine the operational efficiency of the business and hence its viability.

4.10. Specific areas of the design and layout of an ALDI store are as follows:

Retail sales area: this is the most critical aspect of store building design. A 1,254sqm floor area is required to provide approximately 1,500-2,000 product lines, and the dimensions of the retail area are determined by the need to ensure that adequate and consistent product display space is provided. The retail sales area is also specifically designed to enable

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 12

efficient transfer of products (it has been demonstrated that a rectangular store design is necessary for appropriate stock transfer, retail display and security).

We acknowledge the requirement to show flexibility in the format, design and scale of proposed development as advocated in TAN4. ALDI have developed smaller stores in the past, but are also in the process of undergoing an estate renewal programme to reflect the evolution of the business model. The remaining stock of small stores has been or will be upgraded or extended where the site context allows. Stores without such scope are now less efficient and pose more frequent operational challenges.

Storage and ancillary non-retail floorspace: where the size and shape of a particular site requires less than optimal configuration, ALDI can exhibit some flexibility, such as the location of the service pod and size of the storage area, although in all cases adequate levels of storage will be required.

Urban design: ALDI recognises that the external appearance of its buildings needs to respond to their design context. In appropriate circumstances ALDI is able to be flexible regarding siting, the exterior design and external finishes.

Parking: ALDI is committed to ensuring that its stores are accessible by a variety of modes of transport and seek to locate stores where they are most accessible. However, it is recognised that most customers visit ALDI to carry out a weekly shop and will wish to travel by car. ALDI typically do not consider developing new stores that share dedicated customer parking with pay and display style public car parking. Such arrangements are likely to limit sales and generate operational and management difficulties.

Existing Retail Provision and Shopping Pattern

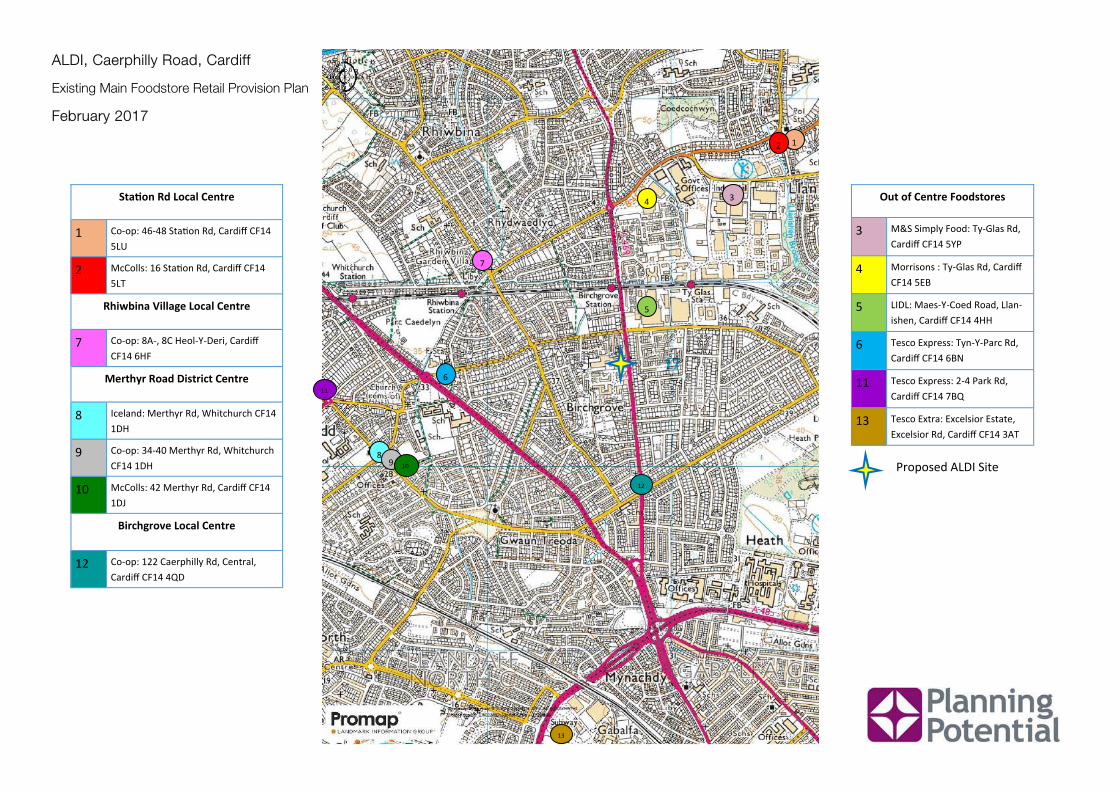

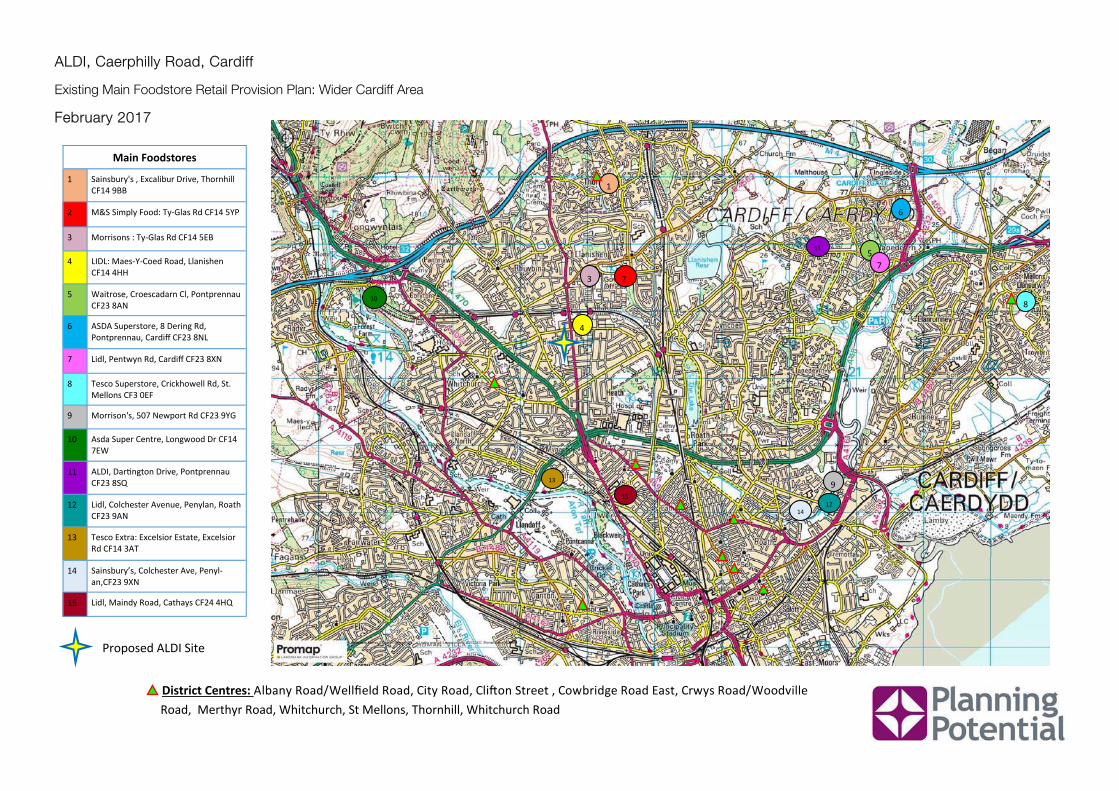

4.11. As set out in Section 2 of this Statement, the application sites is located in relative close proximity to a District Centre (Merthyr Road), together with three Local Centres (Brirchgrove, Station Road Llanishen, and Rhiwbina Village).

4.12. The site is located within Zone 3 of the City, according to the Study Area in the Council’s Retail Study update by Colliers (2011). Within the remainder of the Zone, there is a further District Centre, Thornhill, which is anchored by a Sainsbury’s superstore, together with two further Local Centres. These are Station Road Llandraff North and Gabalfa Avenue, which are both located to the west of the Zone.

4.13. The Retail Study Update reports that Zone 3 is dominated by the ASDA superstore at the Coryton roundabout in the far north west of the zone, while a range of other out-of-centre stores, such as the Morrisons at Ty-Glas Road also accounts for a large proportion of spending in the zone.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 13

Heath Check

4.14. In order to inform consideration of the application proposals with particular reference to the retail tests, we set out below a baseline assessment of the health of the relevant centres.

4.15. This health check is based on earlier survey data provided within the District and Local Centre Floor Space Survey (September 2008) and the District Centre Strategy (2012).

4.16. The below health check for the principal commercial centres in Cardiff that are situated close to the proposed ALDI site.

(i) Merthyr Road District Centre

4.11. Merthyr Road District Centre has a linear layout.

Diversity of Uses

4.12. The District Centre has a variety of commercial uses with a mix of national retailers and small independent retailers. It also comprises a bank and a pharmacy. It is served by two public car parks and on-street parking spaces.

Proportion of vacant Street Level Property

4.13. Merthyr Road District Centre consists of 95 units, 12 of which contain convenience uses and two of these are supermarkets, Co-op and Iceland. The Health Check conducted in April 2017, informed that there are two vacant units within Merthyr Road, both small in size and hardly noticeable. In 2008, nine units were vacant, with this figure being reduced to two by 2012. This indicated that the attractiveness of the area has improved and the figure from 2017 proves the stability of the district centre.

Accessibility and Town Centre Environmental Quality

4.14. The District Centre is easily accessible by car, and there is a bus service going through Merthyr Rd as well as on-street parking.

4.15. Merthyr District Centre is characterised by a wide pavement on one side, with the commercial properties set back from the road.

4.16. Merthyr Rd District Centre is not served by any street furniture nor a community centre or park.

Conclusion

4.17. The District Centre appears to be performing well and appears to be healthy. The diversity of uses and services, strengthen the district centre and boost its popularity.

(ii) Birchgrove Local Centre

4.18. The Town Centre is linear and the main shopping street is Caerphilly Road. There are no designated frontages within the local centre boundary.

Diversity of Uses

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 14

4.19. Birchgrove Local Centre also comprises a diversity of uses, more limited than Methyr Rd District Centre. It is served by a Co-Op and a Lloyd’s Pharmacy but the rest of the centre comprises smaller businesses and local ones. A range of medical services are also offered such as, a dental clinic, a psysiotherapy space, a medical clinic and opticians.

Proportion of vacant Street Level Property

4.20. Birchgrove Local Centre contains 49 units, three of the units contain convenience uses, one being a Co-op supermarket. Five of the 49 units are vacant or unoccupied. In 2008, four units were vacant or unoccupied. Although the figure has increased, ome natural fluctuation is common in such a centre.

Accessibility and Town Centre Environmental Quality

4.21. The Local centre is served by frequent public transport services.

4.22. The recent health check undertaken in April 2017, observed that a main, wide road goes through the local centre, and crossing for pedestrians is not comfortable. The local centre has wide pavements on both sides of the street but has no street furniture, parks or a community centre.

4.23. The local centre was observed to be busy in terms of traffic, lacking in pedestrian flow.

Conclusion

4.24. Overall it can be seen that the traffic volume and road size is impacting the pedestrian flow of this local centre.

4.25. It is served by a wide variety of uses, but the more limited offer reflects its position in hierarchy. Birchgrove Local Centre is not served by a public car park and on-street parking is limited. The environmental and access quality could be improved.

(iii) Rhiwbina Local Centre

4.26. Rhiwbina Local Centre is generally of a linear formation with the main shopping street being Hed-Y-Deri. There are no designated frontages within the local centre boundary.

Diversity of Uses

4.27. Rhiwbina Local Centre comprises a diversity of uses, mostly local. It also includes a community centre and a gallery space. Additionally, it is served by barbers, local flower shops, butchers, a dental clinic and independent retail shops.

Proportion of Vacant Street Level Property

4.28. Rhiwbina Local Centre consists of 46 units in total with three units containing convenience uses of which one is a Co-op supermarket. Only one of the 46 units is vacant, but currently under offer. This is an improvement from the figure reported in 2008, which was two vacant units.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 15

Accessibility and Town Centre Environmental Quality

4.29. Access to Rhiwbina Local Centre is easy and it is served by on-street parking. The area is a calm traffic area.

4.30. The Local Centre is also served by street furniture (benches) as well as trees and plantings. The street-art present, in combination with the flower installations proved a unique and vibrant atmosphere.

4.31. The Rhiwbina Local Centre is also in close proximity to a train station, which adds to its level of accessibility.

Conclusion

4.32. The Rhiwbina Local Centre is small and attracts a moderate flow of pedestrians, but it can be characterised as healthy. It is comprised mostly by local businesses and a community centre. The fact that there are no vacant units indicates that it is an attractive area to operators.

(iv) Station Road, Llanishen Local Centre

4.33. The main shopping street within the Llanishen Local Centre is Station Road. While Kimberly Terrace and Llanishen Court feed into the Local Centre, the majority of the shops front on to Station Road.

Diversity of Uses

4.34. Station Road comprises a diversity of uses, taking into consideration its size, the fact that there is a post office, a Co-op supermarket, both Natwest and Barclays banks, a local bakery, a café, a chemist and a beauty salon is a successful mix.

Proportion of vacant Street Level Property

4.35. Llanishen Local Centre consists of 29 units, of which two are convenience uses including one supermarket. None of the units were vacant when surveyed in September 2008 and none were vacant when checked in April 2017.

Accessibility and Town Centre Environmental Quality

4.36. Station Road Local Centre is easily accessible and there are on-street parking spaces available. The surrounding roads and associated traffic do not dominate the local centre and allows a steady flow of pedestrians.

4.37. The Local Centre is served by street furniture (benches) and flower pots, which generates a pleasant environment for shoppers and visitors. There is also a bus stop on the road, offering public transport facilities.

Conclusion

4.38. Station Road Local Centre is the smallest in the area, but it offers a diverse mix of facilities, especially for its small size. The street furniture, flower planters and bus stop make the area more attractive, accessible and seem healthy and popular.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 16

5. The Sequential Approach

5.1 This Section of the report assesses the proposed foodstore in relation to the ‘sequential test’, as outlined in Chapter 10 of Planning Policy Wales (clauses 10.2.13 to 10.2.16), TAN 4, and Policy R6 of the Cardiff LDP.

5.2 A sequential assessment has been undertaken for the proposal, which proposes a main town centre use in an ‘out-of-centre’ location.

5.3 The assessment is based on research undertaken by Planning Potential and an analysis of available secondary evidence, which includes the Council’s LDP evidence base.

5.4 We conclude that the application site is the only site that is suitable, available and viable for the foodstore proposed in this case; and that it is the only site suitable for the development proposed.

Parameters

5.5 The 2016 version of PPW confirms that, in reviewing alternative sites, regard should be given to suitability and availability of those sites. These can be defined as follows:

Availability – whether sites are available now or are likely to become available for development within a reasonable period of time (determined on the merits of a particular case).

Suitability – a site or building’s attributes and whether these are sufficient to meet the development requirements of a particular proposal.

Viability – whether there is a reasonable prospect that development will occur on the site at a particular point in time. Again, the importance of demonstrating the viability of alternatives depends in part on the need that is to be addressed.

5.6 Whilst ‘viability’ is not expressly referenced by PPW in relation to planning applications, it is our view that viability remains relevant to the consideration of whether sites are ‘suitable’ (for completeness we have therefore included viability within our consideration of sequentially preferable sites).

5.7 The above parameters provide a robust and policy-compliant basis for assessment.

5.8 In considering the sites, we have had regard to case law that has influenced the interpretation of the sequential test. This case law has included the principles established by the Supreme Court in their judgment with regard to a challenge by Tesco Stores Limited in Dundee, which was further clarified by the Secretary of State decision at Rushden Lakes.

5.9 More recent guidance has been provided with regard to the application of the sequential test through a High Court judgment relating to an out-of-centre food retail proposal in Mansfield (Aldergate Properties Limited and Mansfield District Council and Regal Sherwood Oaks Limited; CO/6256/2015; 8 July 2016). This judgment builds on a Secretary of State decision relating to a mixed-use retail

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 17

proposal in Exeter (Land North of Honiton Road and West of Fitzroy Road; APP/Y1110/W/15/3005333) dated 30 June 2016.

5.10 Both decisions re-emphasise the ‘town centres first’ principle. They provide further clarity with regard to the assessment of potential sequentially preferable sites in terms of their ‘suitability’, ‘availability’ and the need for the applicant to demonstrate flexibility. In particular, the Mansfield decision confirms that when reviewing potential alternative sites:

The terms ‘suitable’ and ‘available’ mean suitable and available for the “broad type of development which is proposed in the application by approximate size, type and range of goods.” (paragraph 35).

This is to include the requirement for flexibility and “excludes, generally, the identity and personal or corporate attitudes of an individual retailer” (paragraph 35).

In terms of a site ‘availability’, this relates to a site’s availability for the type of retail use for which permission is sought and not to its availability to a particular retailer (paragraph 42).

5.11 The Mansfield decision therefore confirms that the sites covered by the sequential test search should not vary from applicant to applicant depending on the identity or specific retail model proposed. It is clear, for example, that the requirements of an individual retailer, their commercial attitudes, site preferences and competitive preferences should not dictate those sites that are ‘suitable’ or ‘available’ (paragraph 38). In other words, sequential sites in town centres cannot be dismissed simply because an operator does not wish to compete with its own existing or committed stores located in or close to that centre.

5.12 In the Exeter case, the Inspector concluded (and the Secretary of State agreed) that ‘availability’ did not require a site to be on the open market to any developer (IR 11.39) and that the requirement to develop other parts of the site did not mean the area identified for retail was not ‘available’ (IR 11.40).

5.13 The sequential assessment set out below has been undertaken in the context set by both relevant policy and the clarification provided through these decisions.

The Development Proposed and Flexibility

5.14 Paragraph 7.5 of TAN4 states that ‘developers and retailers should be flexible and innovative about the format, design and scale of proposed development and the amount of car parking needed, tailoring these to fit local circumstances.’

5.15 The application proposal is for a food retail store with a net sales area of 1,254sqm. This sales area would display largely prepacked convenience goods alongside a small range of comparison goods under time-limited special offers. No ancillary services or concessions are to be provided (e.g. café, tobacconist, dry cleaning, pharmacy), nor would any specialist food counters (e.g. butcher, fishmonger, deli) be provided.

5.16 A food store of this scale and type would typically require a minimum of 100 parking spaces.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 18

5.17 The size of a site that could accommodate such a store varies with context, but it is considered that sites extending to approximately 0.7 hectares would best allow the reasonable requirements of a food retail store of this nature to be accommodated (access, parking, servicing, and landscaping).

5.18 In practical terms, such a store is at the lowest end of what would be reasonably considered a modern supermarket or main-food shopping destination. A store of this size would enable a retailer to provide and display a streamlined range of convenience goods, while also taking into account the space requirements for lobbies, walkways checkouts, back of house storage space, staff and customer facilities.

5.19 Notwithstanding this, while undertaking the sequential assessment, consideration was given to whether a store could reasonably be accommodated on a smaller site, where appropriate.

Assessment Parameters

5.20 The Primary Catchment Area (PCA) adopted for our sequential site exercise is consistent with the impact assessment study area. This is focused on the central portion of Zone 3 of the City, which is largely made up of residential areas.

5.21 This has been the focus of ALDI’s site search. However, in line with the town centre first approach advocated by TAN4, regard has been given to the retail hierarchy outlined in the LDP (Policy R6 and Paragraph 5.286) and summarised in section 3.

5.22 During pre-application discussions, the Council did not identify any specific sites to be assessed. As a result, we have undertaken a broad search, focusing on the Central Shopping Area, together with District and Local Centres located within the PCA. These were agreed with the LPA during pre-application discussions and are: Merthyr Road District Centre; Birchgrove Local Centre; Rhiwbina Local Centre, and Station Road Llanishen Local Centre.

5.23 Appendix 3 provides a diagram of each of the relevant centres, showing the LDP shopping centre boundary, highlighting the principal sites considered in the below text.

Assessment of Alternative Sites

(i) Central Shopping Area

Within Central Shopping Area

5.24 The CSA, as defined by the LDP Proposals Map (2016) extends to approximately 30 hectares. At its north western extent, the CSA covers the area along Duke Street, to the south of Cardiff Castle. The northern boundary is located to the north of Queen’s Street, a historic portion of the townscape covered by a Conservation Area designation. The north eastern boundary is located at the edge of the Capitol Shopping Centre.

5.25 The CSA’s eastern boundary is to the east of the St. David’s Shopping Centre. The southern boundary is located to the south of John Lewis and is demarcated by Bute Terrace. The western portion of the CSA comprises the historic area

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 19

around St Mary Street (also a Conservation Area). The western boundary runs to the east of the Principality Stadium, which is located alongside the River Taff.

5.26 The CSA is made up of a number of traditional ‘High Street’ style shopping areas covered by heritage designations, together with a number of more recent modern shopping mall style developments. This pattern of development means that there are a lack of obvious large scale development opportunities within the CSA.

5.27 The former areas such as St Mary Street and Queen Street are characterised by historic buildings with retail and entertainment uses at street level, and mixed uses at upper floor levels. These areas are predominantly pedestrianised, meaning that even if a suitably sized unit was available, a modern foodstore proposal to serve a main food shopping purpose would suffer from operational issues due to the lack of vehicle access.

5.28 Land within the CSA has generally been used efficiently, with car parking accommodated within multi-storey buildings and within the modern mall developments. This further limits available development plots. The LDP does not allocate any sites for redevelopment within the CSA

5.29 In conclusion, the configuration of the centre is unlikely to yield any vacant units or indeed any amalgamation of vacant units to accommodate a foodstore of the nature proposed, even when applying an appropriate degree of flexibility.

Edge of Central Shopping Area

5.30 In accordance with the sequential test, and the order of preference set out in the LDP (para 5.286), we have also considered the suitability and availability of other sites in edge-of-centre locations.

5.31 At the northern edge of the CSA, the presence of established administrative, educational, and recreational land uses indicate that there are no suitable or available sites for the proposed development in this location. The majority of this area is also covered by a combination of ‘Sheduled Ancient Monument’, Conservation Area, and ‘Historic Parks and Gardens’ designations.

5.32 To the east of the CSA, the A4161 road and railway infrastructure pose physical constrains to movement and limit the area that can reasonably be considered edge-of-centre to the land either side of Churchill Way.

5.33 On the western side, this includes Charles Street, which is a Conservation Area, including 11 Listed Buildings. The area has a fine urban grain, which does not lend its self to comprehensive redevelopment.

5.34 On the eastern side of Churchill Way, modern high-rise hotel and residential developments have been undertaken within the last 20 years. In addition, the listed Masonic Hall is located on Guildford Crescent. Similarly, these areas do not provide suitable sites for the proposed development.

5.35 Further to the south is the Motorpoint Indoor Arena and the adjacent Rapports surface level pay and display Car Park (Appendix 3, Site A). The latter site is approximately 0.3 hectares in area and therefore would not be suitable for the proposed development, even when applying flexibility.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 20

5.36 Ivor House (Site B) occupies the immediately adjacent plot of approximately 0.1 hectares. The 3 storey building houses a mix of uses. An amalgamation of these two plots, would similarly not be of a suitable size to accommodate the proposed development. Notwithstanding this, Ivor house is occupied by multiple businesses, although the tenancy or ownership status is not known, it is considered unlikely that this site is available.

5.37 The 0.2 hectare site to the north (Site C), bounded by Bridge Street, Charles Street and Wesley Street, is subject to a recent planning permission (15/03097/MJR) and NMA (17/00173/MJR) for redevelopment as student accommodation. The site is now hoarded for construction work.

5.38 The edge of centre area to the south of the CSA is also limited in size by the road network and railway infrastructure. The land to the south of Bute Terrace (and John Lewis) comprises modern high-rise residential and hotel development.

5.39 To the west of the CSA, the majority of the edge of centre area is also included within the Strategic Site Allocation KP2(A). This 78.8 hectare site is known as the Cardiff Central Enterprise Zone and Regional Transport Hub. To the south of Wood Street, construction work has commenced on the Central Square Development (Site D). It will include a new bus interchange and predominantly office accommodation. Planning permission was granted under the reference 14/02405/MJR. Condition 5 of the planning permission restricts the total retail floorspace of the development to 862sqm. It is understood that a number of A1, A2, and A3 retail units will be provided within this scope. The site is therefore unsuitable to accommodate the development proposed, even when applying a reasonable degree of flexibility.

5.40 To the north of the Central Square Development, there is a vacant 0.4 hectare site bounded by Havelock Street and Park Street (Site E). This is to the south east of the Principality Stadium, and immediately to the east of the Media Wales Building. The site was previously occupied by Thompson House, a part two part three storey office building. The site has been subject three outline planning permissions (06/01385/C for a 259 bed hotel, 06/01379C for 231 residential units, and 06/01378/C for 6,000sqm office accommodation), which were renewed in 2011. However, its current status is not known. The site is considered to be unsuitable for the development proposed due to its small size and incompatibility with the recently permitted schemes.

5.41 Following a search of the CSA and edge-of-centre areas of Cardiff, there are considered to be no sites that are suitable and available for the development proposed.

(ii) Merthyr Road District Centre

Within Merthyr Road District Centre

5.42 Merthyr Road District Centre is the closest District Centre to the application site. It is located approximately 1.8km to the west of the site. It is configured either side of Merthyr Road in the form of small retail and service use units within two storey terraced buildings.

5.43 The Council’s 2012 District and Local Centres Strategy reported that there were two vacant units. This was confirmed by a site visit in April 2017.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 21

5.44 The character of development within the District Centre does not lend itself to amalgamation and/or land assembly, meaning that the available units in the centre are not considered suitable for the development proposed.

Edge of Merthyr Road District Centre

5.45 Immediately adjacent to the eastern boundary of the District Centre are two surface level pay and display car parks. These are the 0.25 hectare Penlline Road Car Park (Site F) and the 0.15 hectare Merthyr Road Car Park (Site G). These represent two potential development opportunities. However, the size of each site is far below what would be required for the development proposed. Notwithstanding this, both car parks provide valuable parking facilities for the District Centre, which is otherwise limited. The sites are therefore unlikely to be available for development.

5.46 The wider areas surrounding the District Centre are made up of predominantly medium density, early to mid-20th Century residential development, in the form of detached, semi-detached, and detached two-storey houses. This includes a conservation area along Church Road, to the west of the District Centre.

5.47 In addition, large areas of land surrounding the District Centre provide premises for Whitchurch Primary School, Whitchurch High School (Upper and Lower School campuses) and the associated recreational land.

5.48 The character and pattern of development in the surrounding areas, therefore does not yield any suitable or available sites for the proposed development.

5.49 Following a search of the centre and edge-of-centre areas of Merthyr Road District Centre, there are considered to be no sites that are suitable and available for the development proposed.

(iii) Birchgrove Local Centre

Within Birchgrove Local Centre

5.50 Birchgrove Local Centre is located 560m to the south of the application site. The Centre is clustered around the junction between the A469 Caerphilly Road and the Birchgrove Road/heathwood Road. The northern portion of the Centre is configured in two retail parades either side of Caerphilly Road, while the southern portion of the centre is formed by shopping parades on the western side of Caerphilly Road only.

5.51 The Centre has a similar character to Merthyr Road DC due to small retail and service use units within predominantly two storey terraced buildings. The largest units are the Co-op and two public houses.

5.52 The recent visit to the Centre indicated that there were 5 small scale vacant units, none of which would be suitable for the development proposed.

Edge of Birchgrove Local Centre

5.53 The areas immediately surrounding the Local Centre boundary include principally terraced housing to the west of Caerphilly Road and lower density semi-detached dwellings set in larger plots to the east of Caerphilly Road.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 22

5.54 Uses other than residential are scarce. However, Birchgrove Primary School is located immediacy adjacent to the western boundary of the local centre, to the South of Birchgrove Road on a 0.4 hectare site.

5.55 In addition, Llwnfedw Gardens (Site H) is located 100m to the north west of the Local Centre boundary. The 0.75 hectare site accommodates a bowls club and other recreational facilities.

5.56 Following a search of the local centre and edge-of-centre areas of Birchgrove Local Centre, there are considered to be no sites that are suitable and available for the development proposed

(iv) Rhiwbina Local Centre

Within Rhiwbina Local Centre

5.57 Rhiwbina Local Centre is located approximately 1.2km to the north west of the application site. The local centre is clustered around the junction between Beulah Road/Pen-Y-Dre and Heol-Y-Deri/Pantbach Road.

5.58 The centre includes a purpose built shopping parade to the east of Heol-Y-Deri and a series of two storey terraced buildings on the western side of the road.

5.59 A recent visit to the centre observed that there was a single vacant unit. However, this was stated to be under offer.

Edge of Rhiwbina Local Centre

5.60 Immediately to the east of the local centre boundary is a 0.2 hectare allotment garden (Site I). This site is unsuitable for the proposed development due to its size and single track vehicle access, while the site is not considered to be available due to its ongoing recreational use.

5.61 The wider areas surrounding the local centre that can reasonably be considered edge of centre are constrained by the railway line to the south, and areas of recreational land to the west of the centre.

(v) Station Road Llanishen Local Centre

Within Station Road Llanishen Local Centre

5.62 Station Road Llanishen Local Centre is located approximately 1.8km to the north east of the application site. The local centre is located to the east of the Ty Glas Road / Station Road Roundabout. The centre includes a number of small retail and service units either side of station road, together with St Isan’s Church and the local Police Station.

5.63 No vacant units were observed during a visit to the centre in April 2017.

Edge of Station Road Llanishen Local Centre

5.64 The wider area surrounding the local centre accommodates a mix of uses including medium density residential development, Llanishen High School, Glas Primary School, the Llanishen Leisure Centre, Cardiff City Council administrative buildings and a Cemetery.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 23

5.65 Approximately 600m to the south west of the local centre is the Cardiff Lifestyle Retail Park, which has been trading for at least 10 years and is undesignated in retail policy terms. The Retail Park accommodates a number of convenience and comparison goods retailers such as M&S Foodhall, Boots, DW Sports, and Pets at Home. The location of this development indicates that there are a lack of suitable development sites for uses of this nature in Birchgrove / Llanishen area.

(vi) Out of Centre Sites

5.66 The proposed ALDI store site is approximately 560m north of the nearest designated shopping centre, the Birchgrove Local Centre. Accordingly, a sequential site search of the wider area surrounding the centre has been undertaken, using this distance as a benchmark and considering other sites that might be better connected to the centre.

5.67 The resulting search area suffers from similar development constraints to those discussed above. Principally, the predominantly residential pattern of development surrounding the Birchgrove Local Centre yields limited development opportunities.

5.68 The largest area of open land in the vicinity is the allotment gardens (Site J) to the north of Summerfield Place. The site extends to over 3 hectares and is located approximately 400m to the north east of Birchgrove Local Centre. While the site is clearly large enough to accommodate the proposed development, the site is in use and not considered to be available. In addition, the site has no road frontage and is surrounded by the rear gardens of residential properties on all sides. It would therefore be considered unsuitable and unviable for the proposed development.

Sequential Assessment Conclusions

5.69 On the basis of the information set out above, we conclude that there are no alternative sequentially preferable sites within the town centre or in edge-of-centre locations elsewhere within the primary catchment area.

5.70 The proposed development site is, therefore, considered to represent the only site that is suitable, viable and available for the type of development proposed. On this basis, we conclude that the site should be considered to comply with the sequential approach to site selection.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 24

6. Retail Need and Impact Assessment

6.1 This section of the report sets out our assessment of the economic implications of the proposed ALDI development. The retail need and impact analysis is presented as a series of tables, which are included in Appendix 4.

6.2 It is accepted that the application site represents an out-of-centre site in retail policy terms and that it is therefore subject to the retail need and sequential site assessment tests set by PPW, TAN4 and Cardiff LDP Policy R6. The proposed floorspace is below the relevant threshold for the retail impact test set by national policy (2,500sqm gross), and the LDP does not set a local threshold. However, to aid determination of the application, a proportionate assessment has been prepared.

6.3 In this case the current retail policy evidence for Cardiff is the Retail Capacity Study (March 2009) (by Colliers) and Retail Capacity Study Update (March 2011) (also by Colliers).

6.4 The March 2011 Retail Study Update by Colliers was informed by telephone survey carried out in August / September 2008. These documents formed the principal retail evidence when the LDP was adopted in January 2016. It is therefore considered a suitable basis to undertake this assessment. However, population and expenditure forecasts have been updated based on current Pitney Bowes Map Info data.

6.5 As a result, we have undertaken a quantitative impact assessment that continues to use the results of the 2008 household survey to model ‘existing’ shopping patterns, with appropriate adjustments made to reflect the opening of more recent development, where necessary. The assessment adopts 2017 as the base year and considers retail need and impact in 2022. This is considered to represent an appropriate timeframe for the nature of development proposed.

6.6 In accordance with PPW paragraph 10.4.4, we consider this represents a clear, logical and transparent method using robust and realistic evidence (as required by TAN4 paragraph 6.3).

6.7 In undertaking this process, we have calculated the ‘existing’ turnover of convenience goods facilities based on the results of the household survey. We have then assessed the implications of the stores developed more recently to establish a new ‘baseline’ turnover position in 2017. We have then assessed the implications of the ALDI store development from this baseline position.

6.8 Our analysis relates only to the convenience goods impact of the proposed ALDI store. ALDI stores are a predominantly convenience goods shopping destination with only a small element of floorspace given over to comparison goods (typically 20%). The anticipated comparison goods turnover of the ALDI store is forecast to be only £2.3m per annum in 2017 and £2.5m pa in 2022 (Appendix 4, Table 9).

6.9 Capacity of Comp Goods Analysis

Assessment

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 25

6.10 The proposed development is a discount foodstore with a gross floorspace of 1,700 sq m and a net sales area of 1,254sqm. The application is submitted on the basis that ALDI will be the end-user, and this is reflected in our assumptions below.

6.11. The assessment directly addresses the policy context as set out in Section 3 above, including the retail need and impact ‘tests’ identified in both PPW and TAN4. Although the proposal falls well below the 2,500sqm gross threshold for the retail impact ‘test’ set by both PPW (paragraph 10.4.4) and TAN4 (paragraph 8.2), a proportionate assessment has been undertaken in response to comments received at the pre-application stage.

Methodology

6.12. Drawing on available published data (updated as described above), we have adopted a conventional step-by-step, trade draw methodology to assess retail impact. This is based on an estimate of store turnover (and supporting catchment area expenditure) in the ‘design’ year, and a series of judgements relating to the proportion of turnover estimated to be diverted from existing centres and stores.

6.13. These judgements reflect factors such as scale, nature of retail offer, location/distance, and extent of ‘trading overlap’ (or competition), underpinned by the principle of ‘like competing with like’. Proximate facilities with a similar catchment, and trading in the same market sector, will experience the greatest impacts applying these assumptions. Conversely, distant facilities of a differing scale and nature (such as local facilities and convenience stores catering for day-to-day needs) will be far less likely to experience diversion of trade.

6.14. This methodology is widely applied in retail assessment work and reflects that advocated in relevant national policy (e.g. TAN4 paragraph 6.3). The approach is considered to be logical, robust, transparent and proportionate.

6.15. There are seven main steps underlying this approach:

Step 1: define a catchment area and quantify population and spending

Step 2: identify base and design years for the assessment

Step 3: estimate the turnover of existing centres and retail destinations

Step 4: identify the benchmark turnover of existing facilities based on published information relating to company average turnover, and compare this with survey derived turnover. This provides an assessment of retail capacity and ‘need’ for additional floorspace

Step 5: estimate the turnover of the proposal

Step 6: apportion the turnover of the subject proposal to stores/centres using a trade draw methodology, based on an understanding of location/proximity and the extent to which the proposal will compete with existing facilities (centres and schemes in the same market sector having the greatest propensity to divert trade from comparable facilities).

Step 7: quantify trade diversion (impact) and assess the significance of the predicted impacts for established centres.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 26

6.16. Impact is expressed as a percentage of existing centre/retail destination turnover diverted to the proposal in the design year.

6.17. If retail capacity is identified through Step 4 of the process, this is an indication that existing floorspace is trading at levels higher than might normally be expected and is an indication of quantitative need for additional floorspace in the relevant catchment area.

Assumptions and Assessment Parameters

6.18. The principal supporting assumptions and assessment parameters are as follows:

6.19. Base and design years: base year of 2017 and design year of 2022. The base year is the current year and reflects the earliest year in which planning permission might be granted. Should planning permission be forthcoming for the proposal, ALDI intends to build and open the store in 2018, and a mature trading position is expected to be established fully by 2022.

6.20. Price Year: constant 2014 prices. This is consistent with the current Pitney Bowes Map Info data.

6.21. Catchment Area: based on the characteristics of the proposal (i.e. a discount foodstore) the catchment area adopted reflects that used within previous assessments and adopts a primary catchment area based on (Zones 3 and 1 from the Cardiff retail evidence base).

6.22. Population and Expenditure: derived from MapInfo (Appendix 4, Table 1). This data takes into account local socio-economic factors. In calculating future retail expenditure within the catchment area, we have projected expenditure growth on the basis of the recommended ultra-long trend (+0.5% per annum). Total available expenditure in the study area in forecast years is a product of both population change and spending growth. The Map Info data shows a large uplift in expenditure, when compared to the forecasts in the Colliers Retail Study Update (2011) and recent studies supporting food store applications (GVA – Lidl in Splott, GVA – Lidl in Llandraff North, and Peacock & Smith – Morrisons in Rhymney).

6.23. Turnover of existing convenience stores: derived directly from the results of the household survey prepared in support of the 2011 Retail Study Update.

6.24. Retail Capacity: by comparing the benchmark (or Company Average) turnover of existing facilities with survey-derived turnover, an assessment of retail floorspace capacity can be identified in future years (Appendix 4, Table 7).

6.25. Turnover of proposal: calculated from net floorspace and the sales density of ALDI derived from Mintel Retail Rankings. The resulting sales densities are £11,091/sq. m. for convenience goods and £9061/sq. m. for comparison goods, both at 2014 prices.

Need and Impact Assessment

6.26. The analysis is set out in a series of tables in Appendix 4. The assessment shows the following:

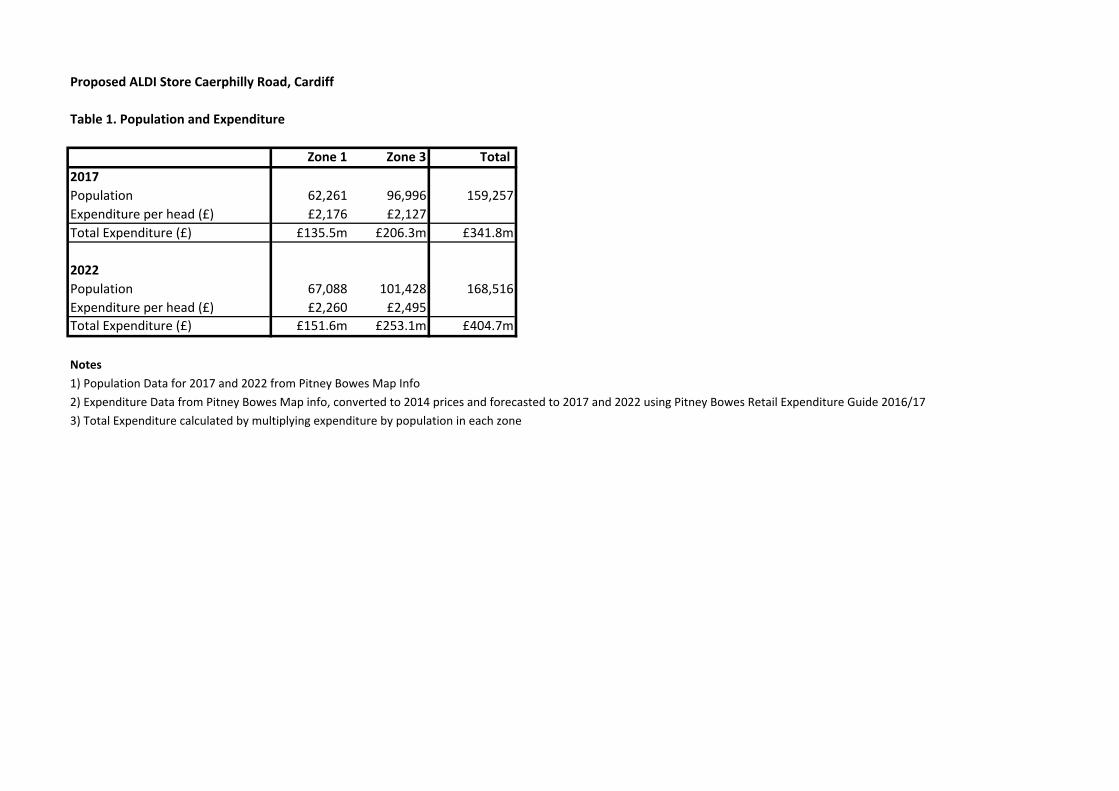

Population and Expenditure (Table 1, Appendix 4)

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 27

6.27. Table 1 shows the available convenience goods expenditure generated by the resident population within the catchment area. From 2017, total available convenience goods expenditure is projected to increase from £341.8 million in 2017 to £404.7 million in 2022.

Shopping Patterns (Table 2, Appendix 4)

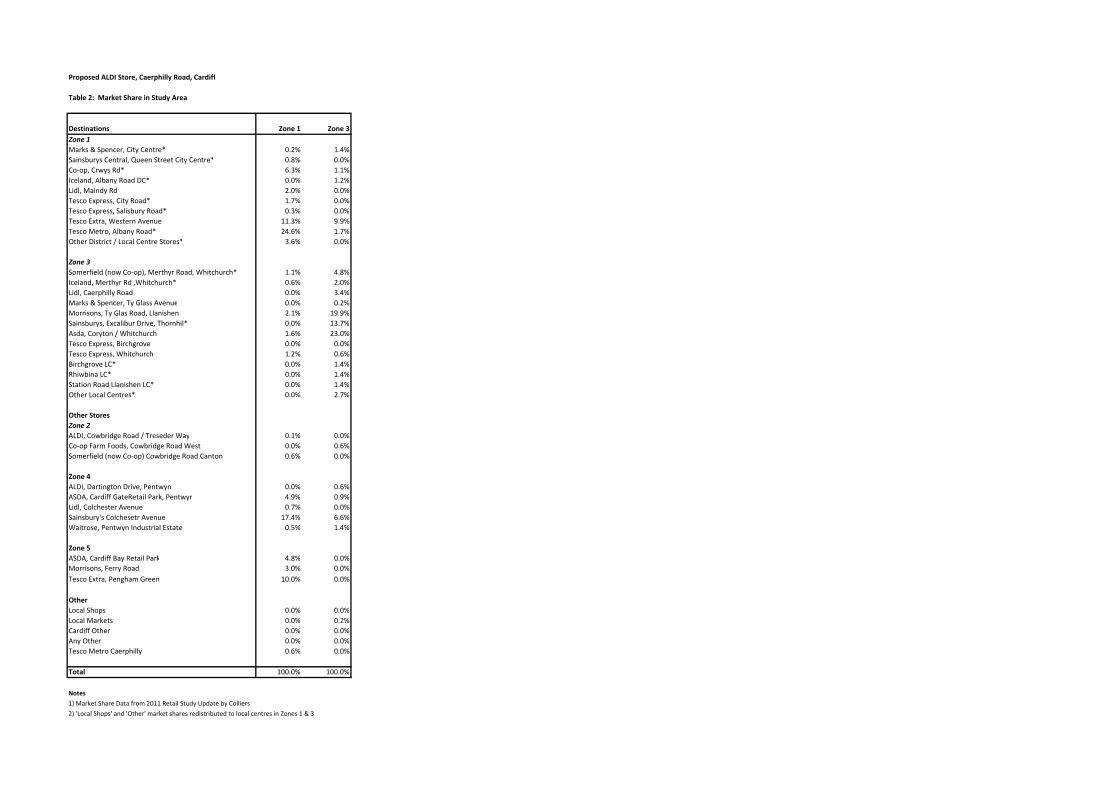

6.28. Table 2 shows the existing convenience goods shopping patterns as derived from the Cardiff Retail Study Update. This illustrates the distribution of total convenience goods expenditure to ‘existing’ facilities, rather than showing a ‘main-food’ / ‘top-up’ split. Some minor adjustments have been made to the trading patterns, including re-apportioning the generic local shops categories to the relevant local centres within the study area.

Convenience Turnover of Existing Stores (Table 3, Appendix 4)

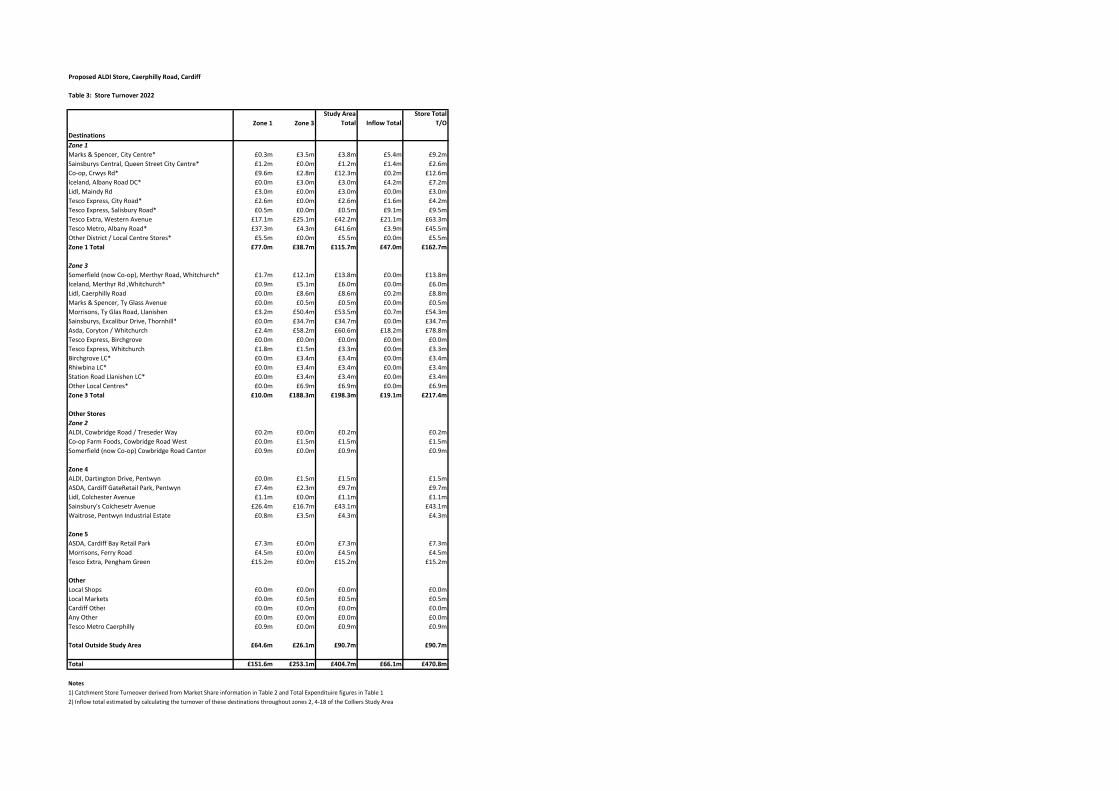

6.29. Table 3 shows the estimated convenience goods market share of existing stores in the catchment area and is derived from Tables 1 and 2.

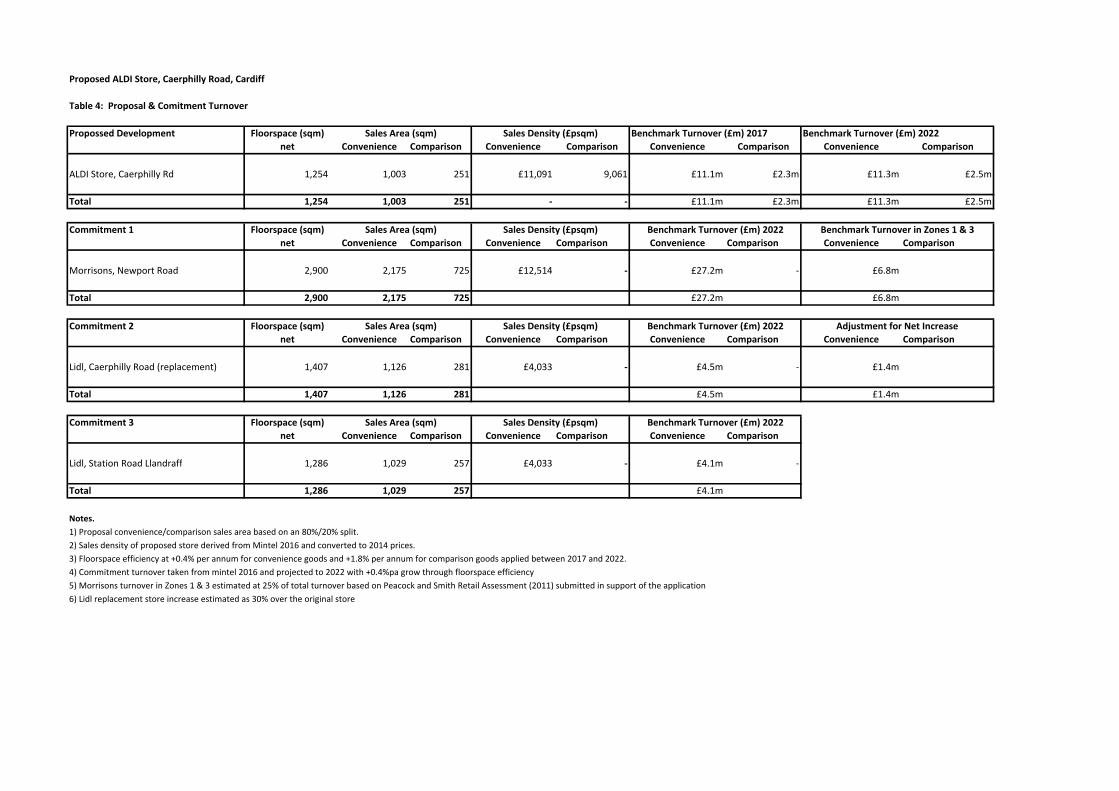

Turnover of the Proposal and Commitments Table 4, Appendix 4)

6.30. Table 4 sets out the estimated convenience and comparison goods turnovers of the ALDI store proposal in both the base year (2017) and design year (2022). These are based on data published by Mintel Retail Rankings (and verified by ALDI), which has been used to calculate convenience and comparison goods sales densities. As indicated above, the proposed operator is ALDI and the turnover has therefore been calculated applying an ALDI average sales density.

6.31. Applying a turnover ratio of £11,091/sq. m. to net convenience floorspace generates a total convenience turnover estimate of £11.1 million in 2017, increasing to £11.3 million per annum in 2022 (with allowance for floorspace efficiency increases).

6.32. Three commitments have been included, which represent major stores that have been consented and constructed since the 2011 Study.

Retail Impact of Proposed Floorspace 2022 (Table 5, Appendix 4)

6.33. Table 5 sets out our estimates of trade draw from existing centres and stores first to each of the three commitments and then to the ALDI proposal.

6.34. This accounts for the uplift in floor area provide by the replacement Lidl store to the east of Caerphilly Road; the development of the Morrisons store at Rhymney, which is estimated to draw 30% of its turnover from Zones 1 & 3; and the newly trading Lidl store at Llandraff north.

6.35. Trade draws to the ALDI proposal are based on the methodology outlined above, in particular the strength, proximity and nature of competing provision, and the premise that ‘like competes with like’. These draws form the basis for the impact calculation.

6.36. Stores catering primarily for main food shopping, such as the Lidl store at Caerphilly Road and the Morrisons store at Ty Glas Road are therefore estimated to experience the greatest competitive effects (and trade diversion) following the

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 28

introduction of the new ALDI store. As competing stores, ASDA at Coryton and Sainsbury’s at Excalibur Drive are also expected to experience trade diversion.

6.37. Table 5 provides an impact analysis of the application proposal. The impact of the ALDI proposal on stores within the CSA is very limited, with a maximum solus impact of minus 1.3% on the M&S (in 2022). The level of diversion from the centre as a whole is considered negligible and, in our view, will not have a significantly adverse effect on their trading performance and function.

6.38. In Merthyr Road District Centres, there will be similarly low impacts on Iceland and Co-op Stores (-1.9% and -2.1% respectively).

6.39. The higher impacts are observed at Lidl, Caerphilly Road and Marks & Spencer Food Hall, Ty Glas Avenue. However, the later appears to have a severely underestimated turnover based on the household survey results. Notwithstanding this, these stores are not located within the town centre or benefit from policy protection.

6.40. Reflecting their positions in the retail hierarchy, Birchgrove, Rhiwbina and Station Road Local Centres largely provide small scale top-up convenience provision for local residents. Due to this factor, a low level of trade draw would be anticipated, which would not have a significant adverse impact on the performance and function of the centres, which are generally in good health.

Assessment of Convenience Goods Capacity (Tables 6 and 7, Appendix 4)

6.41. Table 6 of our assessment considers the turnover of existing stores/floorspace within the catchment area based on a ‘benchmark’ (or company average) turnover ratio, derived from Mintel. This allows an identification of the trading performance of existing facilities if they were trading at company average levels.

6.42. Once this benchmark turnover is compared with the survey-derived turnovers (Table 3), a consideration can be made regarding the stores’ performance. In this case, Table 4.

6.43. This shows that stores within the study area are trading at an average of 160% of the benchmark figures.

6.44. Table 7 sets out a specific capacity analysis when the survey-derived turnover of existing facilities (with allowances for expenditure inflow to the catchment area) is compared with the ‘benchmark’ turnover.

6.45. This represents capacity well in excess of that required to support the ALDI store development and when considered against the identified ‘overtrading’ in stores is a clear demonstration of quantitative need for additional floorspace.

Conclusions on Quantitative and Qualitative Need

6.46. Based on the assessment set out above and in Appendix 4, we conclude that there is clear quantitative capacity for additional convenience goods floorspace, both currently and in 2022. The level of capacity is a clear indication of quantitative need and is well in-excess of that required to support the proposed ALDI foodstore at Caerphilly Road.

ALDI FOODSTORES LTD May 2017

www.p l ann i ngpo ten t i a l . co . uk

Page 29

6.47. We therefore consider that both a quantitative and qualitative need exists for the application proposals.

Assessing the Significance of Impact for Existing Centres

6.48. As noted above, TAN4 (paragraph 8.3) identifies the impact considerations against which planning applications for retail uses (on the edge of or outside retail and commercial centres) should be assessed.

6.49. These tests apply to all proposals for retail development above 2,500sqm gross. Smaller proposals (such as the application proposals) may also be assessed where LPAs believe they will have a significant impact on a retail or commercial centre. Although a lower threshold for assessment is not set by the Cardiff LDP, a proportionate assessment has been undertaken in order to assist with the decision making process.