Embed Size (px)

Citation preview

Plan Your Rollover StrategyUnderstanding Your Distribution Options

Louis Ventura, Insurance & Financial Services

6 Centerpointe DriveSuite 600, La Palma, CA 90623

Office(714) 228-2723 Fax (714) 228-2799

NYLIM-A012621 MSWM32l-03/08

Click Mouse to Move Forward

Understanding Your Needs

• How long have you been contributing to your company plan?

• Are you changing jobs or looking for a new one?• Are you retiring or considering early retirement?• Do you have a need for current income?• Do you know how much to expect from Social

Security?

Social Security Statements

• Annual statement • Mailed to all workers age

25 or older• Includes an estimate of

what you will get in return as monthly retirement benefits

• Statement mailed three months prior to your birthday

• What does it all mean?

Things to Consider

• The rollover distribution options available to you• The advantages and disadvantages of each

option• The ability to access investments for income.• Impact of current taxes and penalties• Level of control you want over you investment

options

Don’t dip into your retirement savings. You’ll lose principal and interest, and you may lose tax benefits. If you change jobs, roll over your savings directly into an IRA or your new employer’s retirement plan.

–U.S. Department of Labor “Top 10 Ways To Prepare For Retirement” , March 2008.

“

”

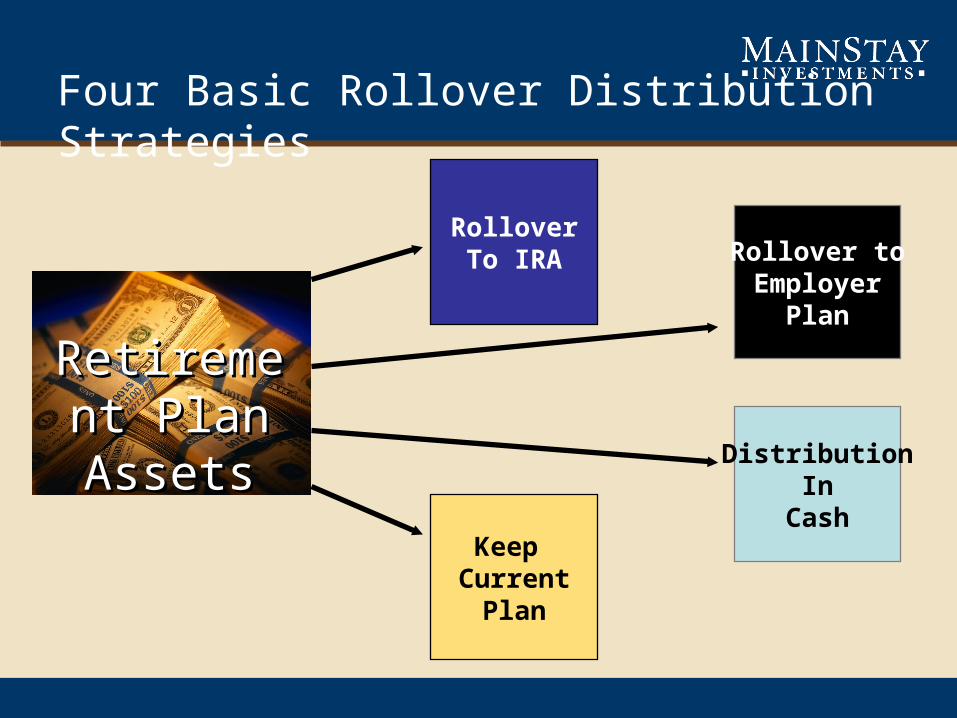

Four Basic Rollover Distribution Strategies

Rollover toEmployer

Plan

RolloverTo IRA

Keep Current

Plan

DistributionIn

Cash

Retirement Retirement Plan AssetsPlan Assets

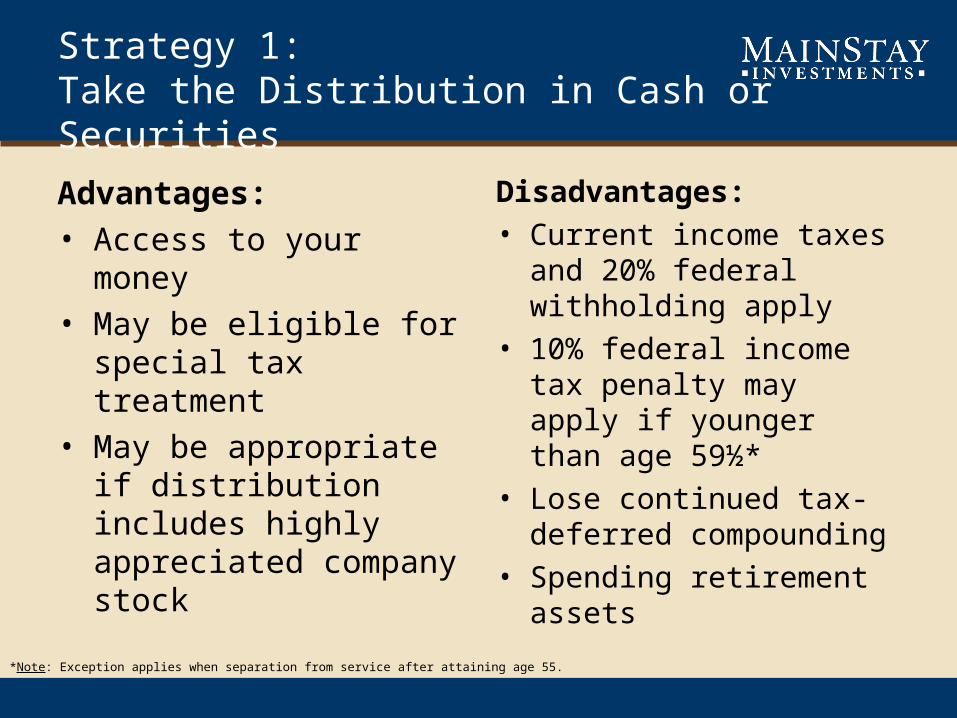

Strategy 1:Take the Distribution in Cash or Securities

Advantages:• Access to your money• May be eligible for special

tax treatment• May be appropriate if

distribution includes highly appreciated company stock

Disadvantages:• Current income taxes and

20% federal withholding apply

• 10% federal income tax penalty may apply if younger than age 59½*

• Lose continued tax-deferred compounding

• Spending retirement assets

*Note: Exception applies when separation from service after attaining age 55.

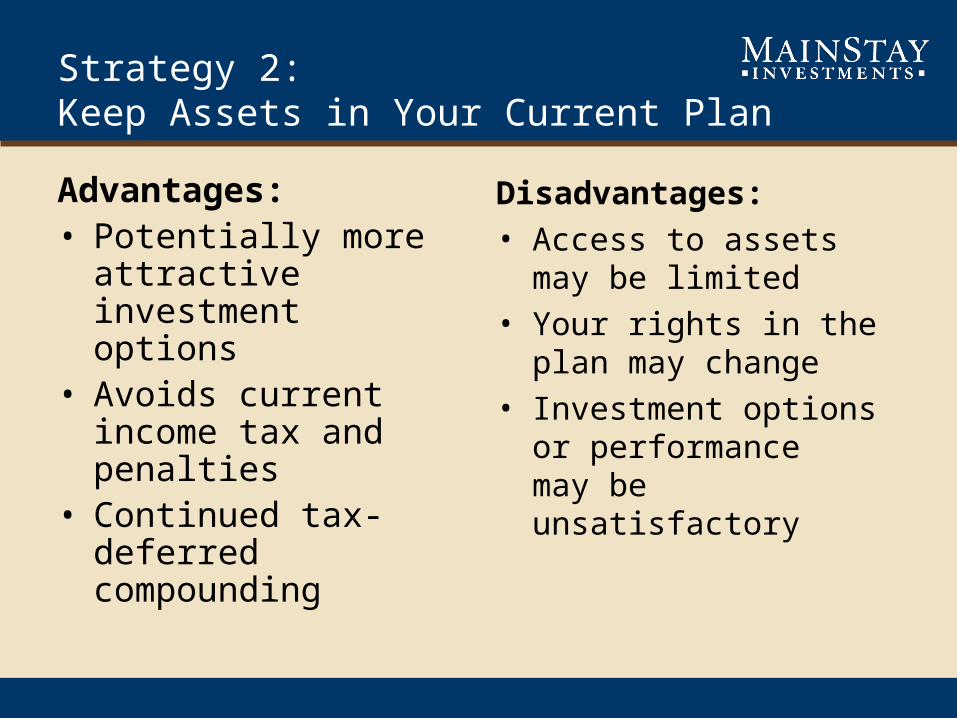

Strategy 2:Keep Assets in Your Current Plan

Advantages:• Potentially more

attractive investment options

• Avoids current income tax and penalties

• Continued tax-deferred compounding

Disadvantages:• Access to assets may be

limited • Your rights in the plan

may change• Investment options or

performance may be unsatisfactory

Strategy 3: Rollover the Distribution Into an IRA

Two methods:• Indirect rollover to an IRA• Direct rollover to an IRA

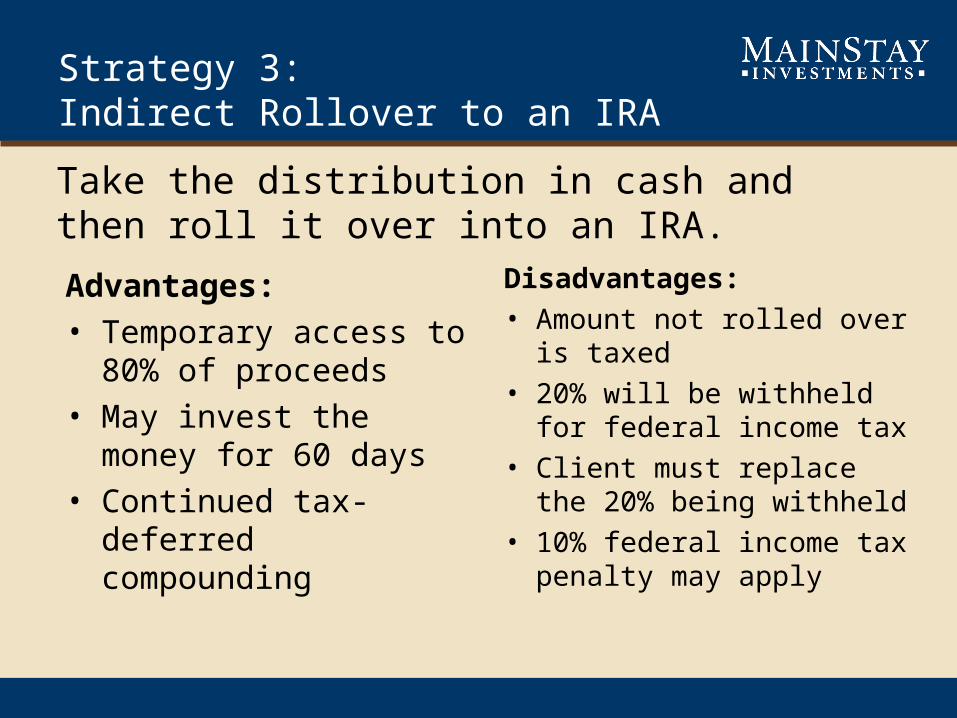

Strategy 3: Indirect Rollover to an IRA

Advantages:• Temporary access to

80% of proceeds• May invest the money for

60 days• Continued tax-deferred

compounding

Disadvantages:• Amount not rolled over is

taxed • 20% will be withheld for

federal income tax • Client must replace the

20% being withheld• 10% federal income tax

penalty may apply

Take the distribution in cash and then roll it over into an IRA.

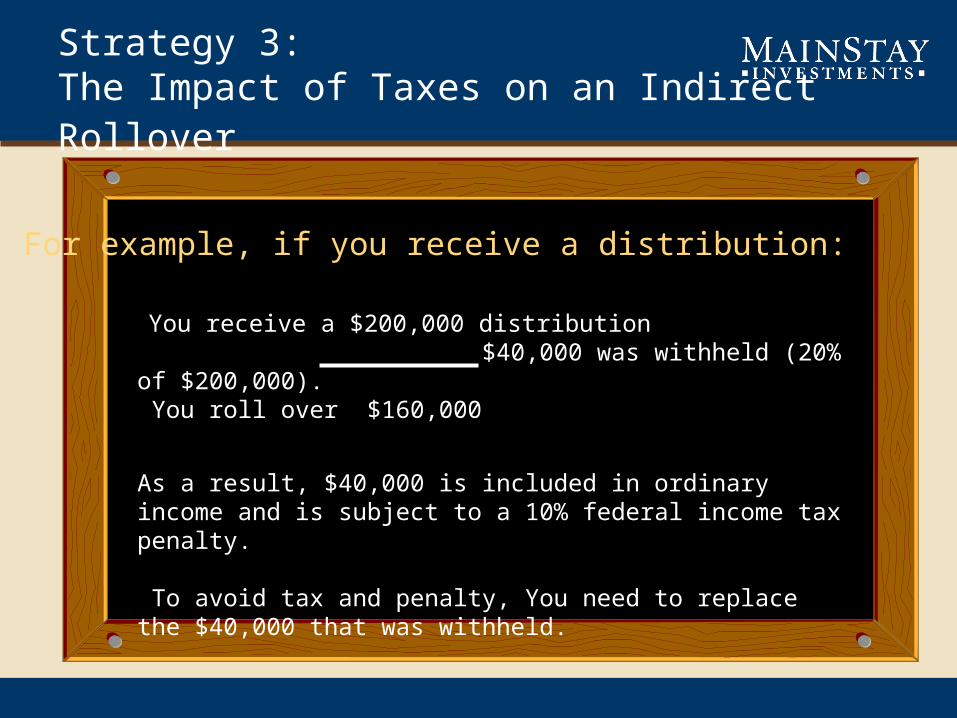

Strategy 3:The Impact of Taxes on an Indirect Rollover

You receive a $200,000 distribution $40,000 was withheld (20% of $200,000). You roll over $160,000

As a result, $40,000 is included in ordinary income and is subject to a 10% federal income tax penalty.

To avoid tax and penalty, You need to replace the $40,000 that was withheld.

For example, if you receive a distribution:

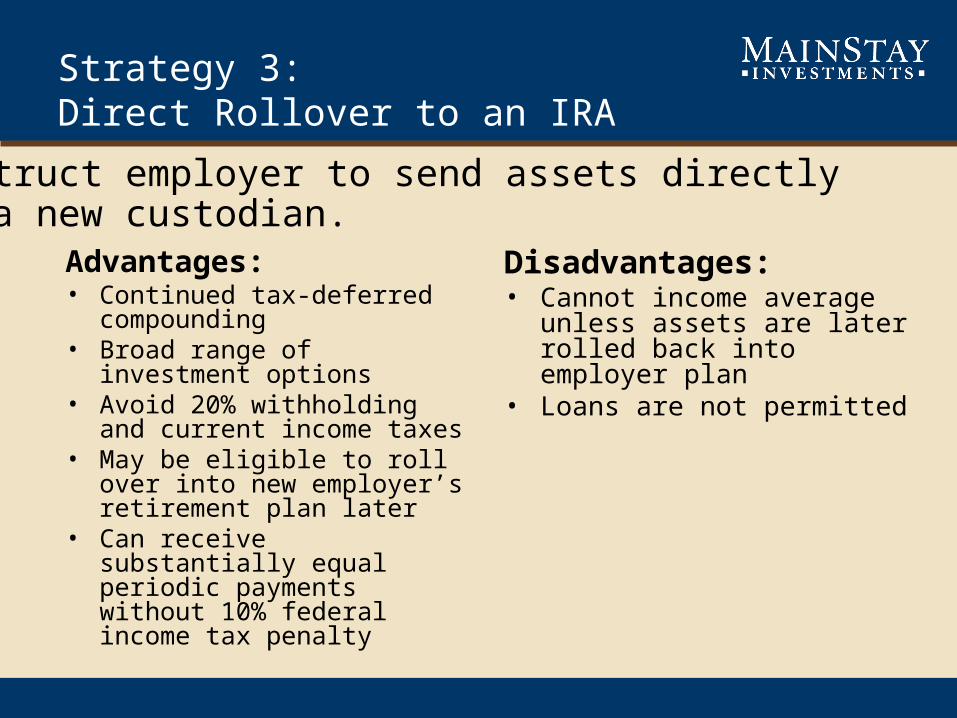

Strategy 3: Direct Rollover to an IRA

Advantages:• Continued tax-deferred

compounding• Broad range of investment

options• Avoid 20% withholding and

current income taxes• May be eligible to roll over into

new employer’s retirement plan later

• Can receive substantially equal periodic payments without 10% federal income tax penalty

Disadvantages:• Cannot income average unless

assets are later rolled back into employer plan

• Loans are not permitted

Instruct employer to send assets directly to a new custodian.

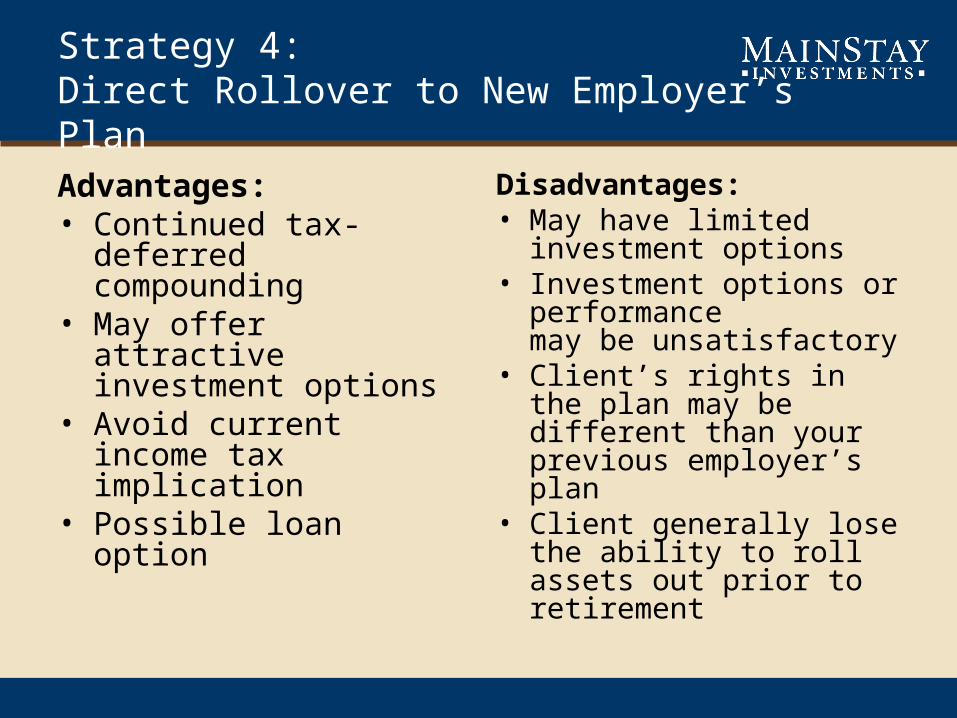

Strategy 4: Direct Rollover to New Employer’s Plan

Advantages:• Continued tax-deferred

compounding • May offer attractive

investment options• Avoid current income tax

implication• Possible loan option

Disadvantages:• May have limited

investment options • Investment options or

performance may be unsatisfactory

• Client’s rights in the plan may be different than your previous employer’s plan

• Client generally lose the ability to roll assets out prior to retirement

Reminder

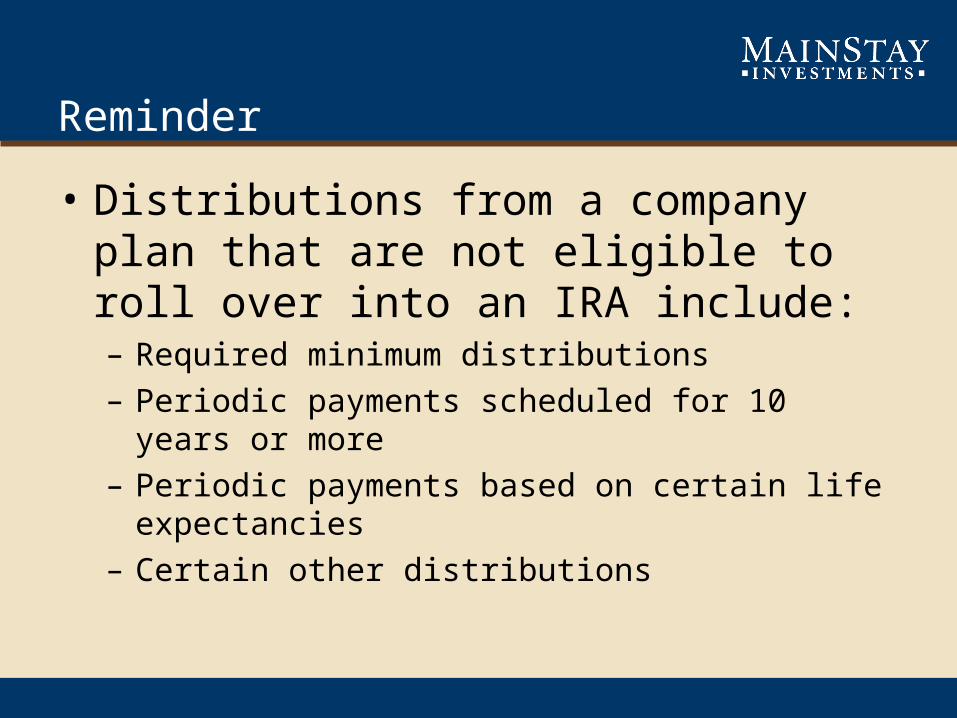

• Distributions from a company plan that are not eligible to roll over into an IRA include:– Required minimum distributions– Periodic payments scheduled for 10 years or more– Periodic payments based on certain life expectancies– Certain other distributions

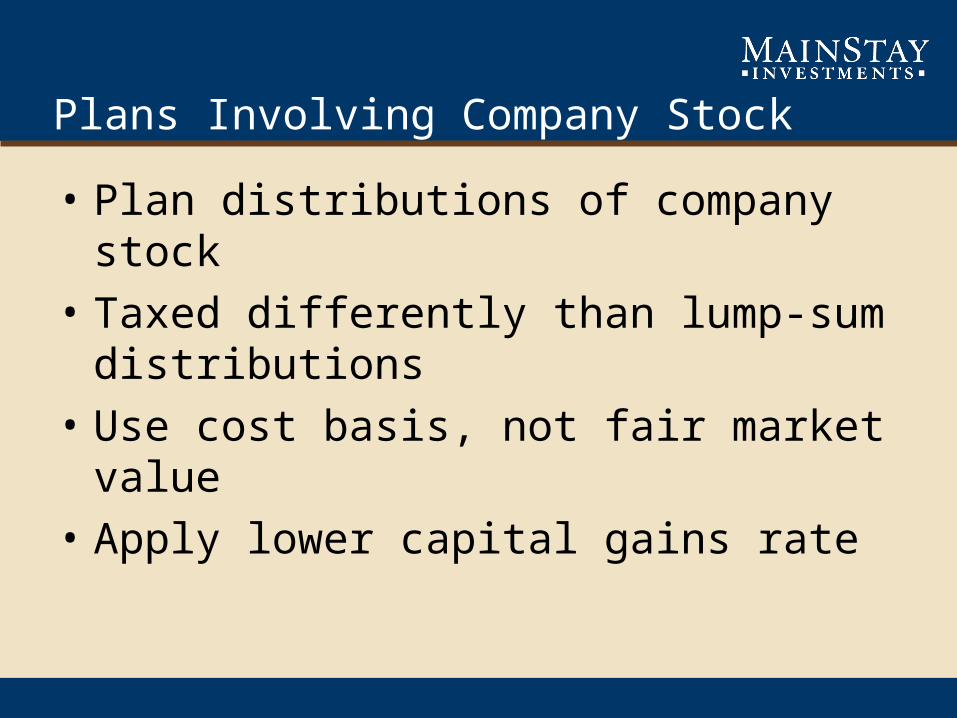

Plans Involving Company Stock

• Plan distributions of company stock

• Taxed differently than lump-sum distributions

• Use cost basis, not fair market value

• Apply lower capital gains rate

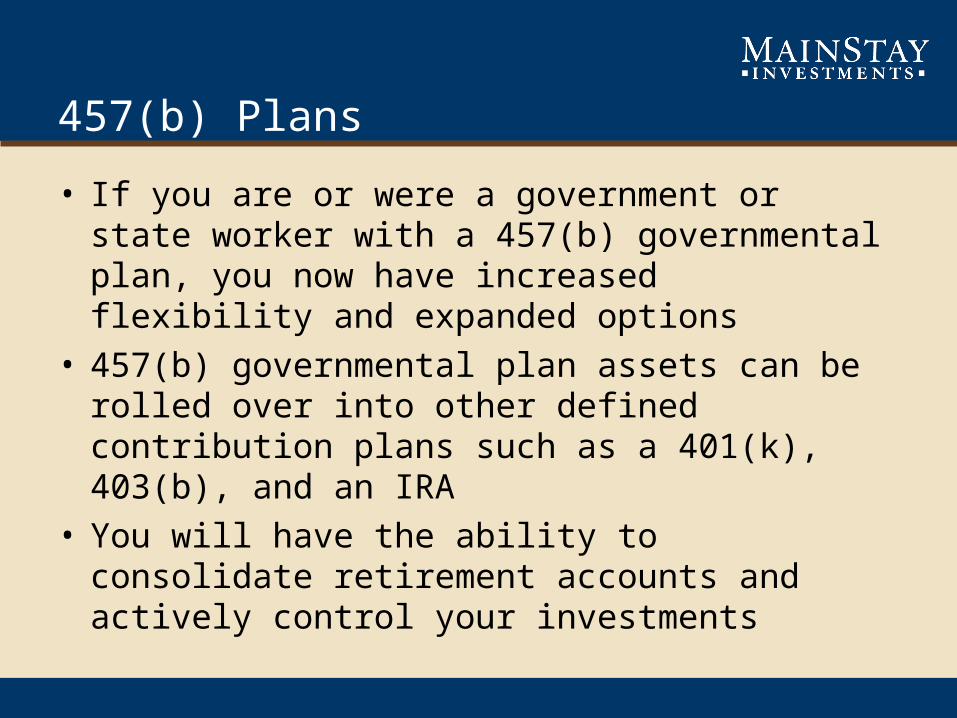

457(b) Plans

• If you are or were a government or state worker with a 457(b) governmental plan, you now have increased flexibility and expanded options

• 457(b) governmental plan assets can be rolled over into other defined contribution plans such as a 401(k), 403(b), and an IRA

• You will have the ability to consolidate retirement accounts and actively control your investments

Additional Factors to Consider

• Size of the distribution

• Retirement needs

• Time horizon

• Investment options

• Asset allocation

Internal Revenue Code Section 72(t): Substantially Equal Periodic Payments

• Allows for periodic payments without 10% federal income tax penalty

• Available through IRA or company plan

• Not appropriate for everyone

The Importance of Professional Guidance

• Retirement planning analysis

• Personalized asset allocation

• Sophisticated financial tools

• Monitor strategy

The information contained herein is general in nature and is provided solely for educational and informational purposes. Financial professionals are not tax, accounting, or legal advisers. You should consult your own tax, accounting, or legal professional regarding your particular circumstances.

Thank You

Presented by MainStay Investments, a division of New York Life Investment Management LLC.Securities distributed by NYLIFE Distributors LLC, 169 Lackawanna Avenue, Parsippany, NJ 07054.

Louis Ventura, Insurance & Financial Services6 Centerpointe Drive, Suite 600, La Palma, CA 90623

Office(714) 228-2723 Fax (714) [email protected]

For more information visit www.LouisVentura.Com