Embed Size (px)

Citation preview

Pivotal Research Group 853 Broadway, Suite 1406 New York, NY 10003

Important Disclosures Are Located In The Appendix

PIVOTAL Pivotal Research Group

U.S. Equity Research Advertising

Advertising Agency Holding Companies Initiating Sector Coverage; WPP is Our Top Pick

January 27, 2012

BOTTOM LINE: We are initiating coverage on global agency holding companies with a BUY rating on IPG and WPP and a HOLD rating on OMC. SECTOR DURABILITY UNDER-APPRECIATED; AGENCIES ARE PRIMARY BENEFICIARIES OF DIGITAL MEDIA. Investor concern about the threat of disintermediation by the likes of Google is generally unwarranted. Agencies offer unique services to their clients, namely “service” itself in helping navigate ideas through marketers’ organizations. This competency is not typically developed by media technology companies. While agencies are unlikely to ever see operating margins like those of the media owners given the fragmented and highly competitive nature of the industry, their ability to adapt should not be underestimated. Digital media is increasing the importance of agencies and service providers as filters and navigators of ideas. As such, the agency sector is literally a “digital dividend” on the application of technology to marketing. TOP PICK: WPP, DARING TO DREAM. We like the company’s long-term exposure to China – possibly the most significant of any western media-related company – its independent digital platform and its dominant media services business. We have a BUY rating and a target price of 960p for the U.K. listed shares (or $75 for the American Depository Receipts, which trade as WPPGY and represent five ordinary shares each). This represents a 28% premium to the current stock price. At target, the company would be trading at a 13.4x P/E multiple, with a 2.6% dividend yield, and sustained growth to that dividend and earnings more broadly. IPG: A STRONG STORY STOCK. We believe there is also significant upside in Interpublic, as the company continues to build confidence with the investor community about its ability to bring operating margins up to peer levels and sustain competitive organic revenue growth. Our experience with the company’s senior management gives us conviction about the company’s ability to execute against the goals it has set for itself. Generation of cash flow from improved working capital policies should be a meaningful – and, we believe, under-appreciated – source of value as well. However, as the company improves operating margins and reduces perceived risk, investors will look for IPG to produce more international exposure. We have a BUY rating and target price of $13.00 for IPG, or 27% upside. OMC: A BELLWETHER APPROACHING FAIR VALUE. While we - and much of the agency industry – have long been impressed by Omnicom the holding company and its component business units, the stock is closer to “fair value” than either of IPG and WPP. As a stable bellwether on the sector, investors can still gain low near-term risk-adjusted exposure to agencies through OMC. However, as with IPG the company needs sustained efforts in Asia Pacific and other faster growing markets to out-perform in the long-term. As well, when compared against its best peer example, WPP, the company’s focus on “culture” rather than strategy means that OMC is not as well future-proofed as WPP and thus faces incrementally higher long-term risks. We have a HOLD rating and target price for OMC is $51, or 9% upside.

Brian Wieser, CFA 212-514-4682 [email protected]

WPP (WPP.L / WPPGY)

RATING: BUY (Previous: N/A)

Target Price: 960p / $75.00 (Previous: N/A)

Price (1/26/12): 751.5p / $59.04

IPG (IPG)

RATING: BUY (Previous: N/A)

Target Price: $13.00 (Previous: N/A)

Price (1/26/12): $10.25

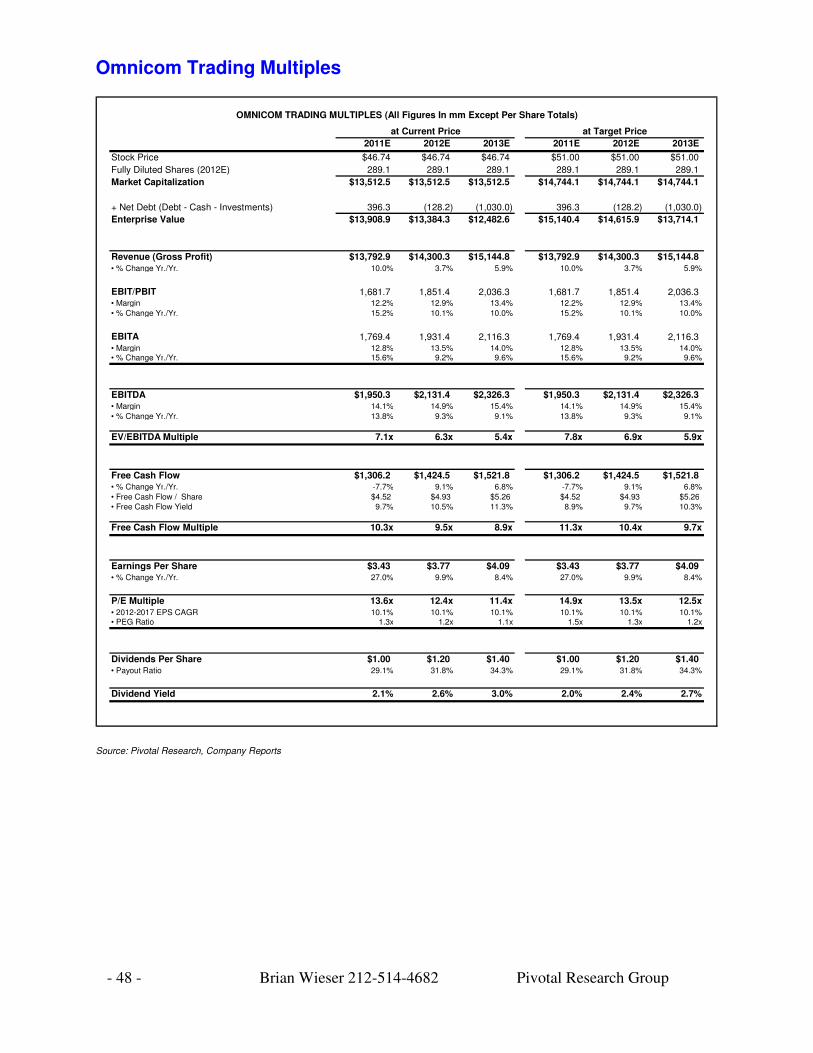

OMNICOM (OMC)

RATING: HOLD (Previous: N/A)

Target Price: $51.00 (Previous: N/A)

Price (1/26/12): $46.74

- 2 - Brian Wieser 212-514-4682 Pivotal Research Group

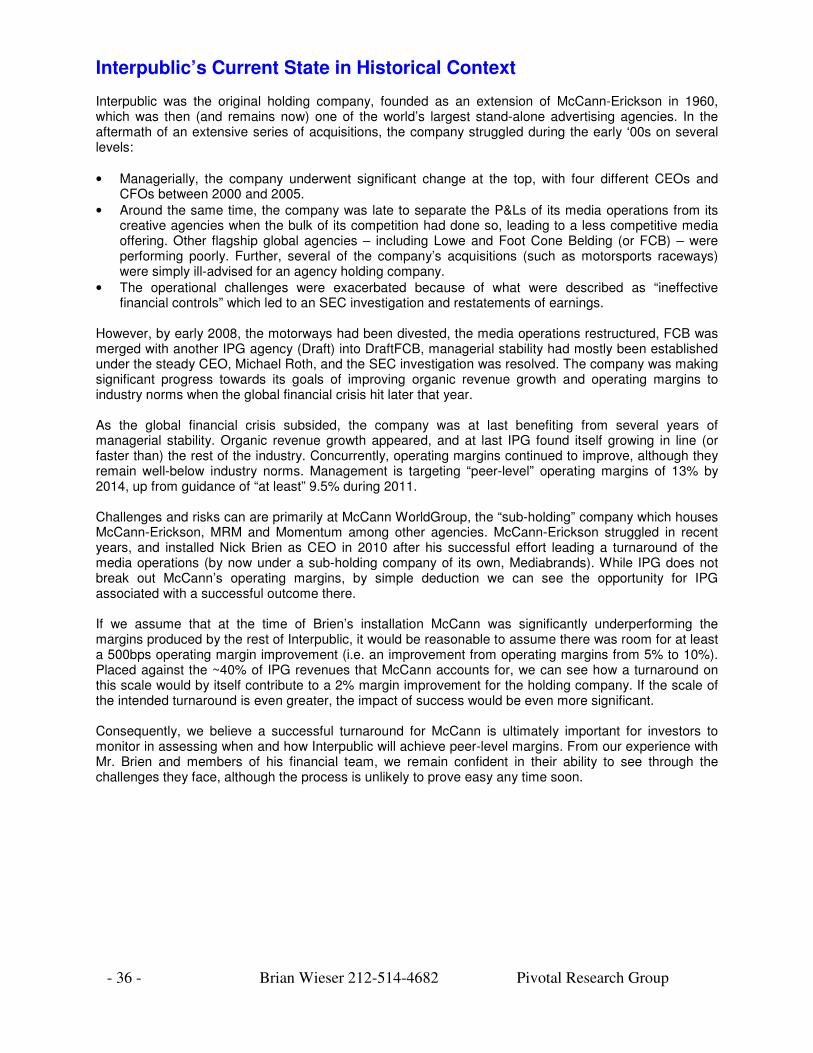

INITIATING ON ADVERTISING AGENCY HOLDING COMPANIES WITH BUY RATING ON WPP/WPPGY AND IPG, HOLD ON OMC DIGITAL MEDIA IMPACT UNDER-APPRECIATED; AGENCIES ARE PRIMARY BENEFICIARIES. Advertising agencies are primary beneficiaries of the rise of digital, as increasing fragmentation of consumer media choices significantly expands the range of ways in which marketers can allocate budgets. This makes an external filter increasingly important, and agencies are uniquely positioned to serve as this role. Further, the need to “socialize” ideas and new ways of marketing through large companies is increasingly crucial. In any given company there are many stakeholders who influence and are affected by marketing choices. They may work in a product development unit, a trade sales function or other areas. It is the responsibility of a CMO and their team to ensure buy-in for the marketing activities the company undertakes. Regardless of type of agency, marketing services companies’ unique competency is supporting clients’ efforts to perform this socialization function. SIGNIFICANT INTERNATIONAL EXPOSURE; UNIQUE CHINA OPPORTNITY. The holding companies are disproportionately exposed to markets outside of the United States, which under normalized macro-economic circumstances should contribute to higher growth (through participation in faster economic growth generated by emerging markets) and lower risk (by virtue of diversifying country exposure). While WPP generates fully two thirds of its revenues outside of North America, even the nominally American holding companies Interpublic and Omnicom generate approximately half of their revenues outside of the United States. Slower growing western continental European markets account for a significant share of this international exposure, but still only account for 25% of WPP revenues, and less for IPG and OMC. For point of comparison, among the global media conglomerates only News Corp. comes close to this level of international focus, with less than half of revenues coming from abroad, and much of this from Europe and Australia. CBS, Disney, Time Warner, Viacom and Discovery only generate 15-33% of their revenues outside of the United States. More importantly, the agency business appears to be one of few western media-related industries capable of capturing a significant foothold in China. Content production and distribution businesses are highly restricted from operating in the country; paid search from foreign providers (via Google) have mostly been pushed out; domestic social media and other online publishers are already well-entrenched. By contrast, agencies are mostly unencumbered to compete in their industry, which is generating revenues of $4bn annually on double digit growth rates. While Omnicom and Interpublic generate only modest revenues in that market today, WPP is already approaching $1bn in annual revenue from China. DURABLE LONG-TERM OPERATING MARGINS. Although the “standard” 15% commission is a thing of the past, the standard 15% operating margin is alive and well. In the world of marketing services, there is an implicit (and sometimes explicit) understanding between marketers and their agencies that the agencies should make a “reasonable” profit if their businesses are well run. Conventionally, many services (such as those offered by creative and media agencies) are organized to generate a 15% operating margin. This holds even when marketers’ procurement teams involve themselves in designing an agency’s processes for servicing an account, and even when clients aim to reduce total fees they pay agencies for like-for-like services every year. In this context, it becomes evident why well-run agencies need to constantly deploy new higher margin services (which today include Corporate Barter or Trading Desks) and look for savings in other areas (such as by outsourcing creative production to countries with lower costs). The development of new businesses and cost-saving initiatives are a steady-state feature of the business, and do not by themselves lead to higher margins for the companies as a whole.

- 3 - Brian Wieser 212-514-4682 Pivotal Research Group

Risks Investors will also need to consider the following among the industry’s risks: SQUEEZING FEES. As we described it above, marketers are typically squeezing their agencies for operational efficiencies on an ongoing basis. Agencies have historically proven resilient in finding cost saving opportunities to perform like-for-like services. However at some point such efforts may no longer yield incremental benefits, and as long as agencies operate in a competitive manner they will suffer. In a similar light, high margin services offered today are typically likely to become standard-margin services in the future, as the more a service becomes standardized, the more that marketers’ procurement teams seek to standardize processes and drive agency margin out of the activity. COMPETITION FROM ADJACENT INDUSTRIES. We remain skeptical that today’s digital media companies such as Google or Microsoft will ever actively compete with agencies. This should hold not least because digital media companies will want to retain their margins (significantly higher than those for agency services) but also because clients generally want some perceived independence from advisors making marketing budget recommendations. However, agencies are increasingly placed up against IT services firms. This type of competition is likely to increase in the future, although not across all marketing-related disciplines. Companies such as Accenture and IBM are positioning parts of their businesses adjacent to agencies as they seek to build platforms which can manage the execution of media campaigns, monitor the impact of those campaigns and integrate those efforts with an array of marketing data within a company’s ERP (enterprise resource planning) system. Sapient’s business lines represent the strongest balance between these functions today, although they have not yet materially impacted the holding companies. Further, media suppliers (such as Hearst and Meredith) and software developers (such as Adobe) have also established competitive positions in some fields previously reserved for agencies, such as in search engine marketing. Given the extremely long selling cycles and the duration of agency-marketer contracts (usually several years in length) as well as the operational considerations for marketers in changing their own processes, no upstart can transform the agency industry overnight. The bigger issue is whether or not agencies are able to sufficiently adapt their own offerings in the time they have before a new service becomes a standard expectation. REDUCED COMPETITION BETWEEN MARKETERS. We have previously identified that advertising spending – and marketing in general – is primarily driven by the competitive intensity that is present within a given category. To the extent that industries evolve to feature reduced levels of competitive intensity, marketing services would generally suffer.

- 4 - Brian Wieser 212-514-4682 Pivotal Research Group

An Existential Question: Why Do Agencies Exist? As media and marketing platforms have become increasingly pervasive and fragmented, the imperative for marketers to rely upon intermediaries for marketing advisory services and executions has grown. Marketers could choose to do almost anything an agency does (including media buying, as occurs today at some companies such as InBev’s Anheuser-Busch in the United States). But the scale at which even the world’s largest marketers operate is usually insufficient to manage many marketing services as well or as inexpensively as the agencies. Consequently, they tend to perform functions themselves which are either highly strategic or which require deep integration with brand/product or sales functions. In general, marketers usually outsource:

• The aggregation of data and development of consumer insights which inform marketing choices

• The translation of branding ideas into advertising campaigns, including the production of creative assets

• The filtering of sales pitches from owners of media assets for thousands of potential executions into perhaps dozens or fewer

• The cost-effective execution of advertising campaigns through media owners Other functions frequently outsourced in whole or in part to agencies include:

• Design of customer-facing elements (stores, websites or the look-and-feel of the underlying products occasionally)

• Management of internet-related assets (such as a brand’s website) • Management of marketing events • Search engine marketing and website design (except when these functions are highly

strategic to a business, as with an e-commerce site) • Brand development • Public relations management • CRM (customer relationship management) strategy, data management and program

execution

- 5 - Brian Wieser 212-514-4682 Pivotal Research Group

Agencies And the Risk of Dis-intermediation The most critical element supporting the durability of the marketing services industry relates to the complexity of the marketers’ own organizations. In recent decades, as marketers became bigger and bigger, they pursued more efficient structures for their operating divisions. Often this meant separating common functions where economies of scale might be realized, or where best practices might best be established. As a result, large marketers typically established centralized marketing groups. These groups were usually headed by a CMO who had no responsibility for business units, indirect responsibility for revenue or share growth and complete responsibility for marketing costs. From the outset these centralized marketing groups needed to interact with other centralized functions, including IT and finance, in addition to business unit functions more directly related to marketing. But as marketers have come to face more and more choices for their marketing strategies, they increasingly rely upon external and ostensibly neutral partners – such as agencies – to both filter ideas and support the socialization of initiatives or process changes across the broader organization. This factor is the most critical one which explains why agencies face no credible threat of disintermediation from technology-driven marketing or media platforms. However, there are some areas impacted by the rise of digital media that increasingly places agencies up against today’s IT services firm. Companies such as Accenture and IBM have become increasingly adjacent to agencies as they seek to build platforms which can both manage the execution of media campaigns and monitor the impact of those campaigns, both by measuring external media exposures and by integrating an array of marketing data within the company’s ERP (enterprise resource planning) systems. Sapient’s business lines are the strongest balance between these functions today, although their impact on the broader industry has not yet been material to the holding companies. Further, media suppliers (such as Hearst and Meredith) and software developers (such as Adobe) have also established competitive positions in some fields previously reserved for agencies, such as search engine marketing. Given the extremely long selling cycles and the duration of agency-marketer contracts (usually several years in length), no IT services firm can transform the agency industry overnight. The bigger threat is whether or not over the extended period of time it takes for this blending of services to become mainstream agencies are able to sufficiently adapt their own offerings.

- 6 - Brian Wieser 212-514-4682 Pivotal Research Group

The Purpose of The Global Holding Company Agency services touch core functions which marketers use to compete within their categories. As a result, most marketers have long been concerned about trusting third parties (such as their agencies) with sensitive information. The underlying concern relates to the risk that information could be shared with a competitor at the present time or in the future. In part to mitigate this concern, individual agencies agreed to refrain from working with a defined group of competitors. So while marketers with global operations were originally supportive in helping their agencies open up around the world (especially when they mirrored the marketer’s needs), they effectively limited the size of their agencies in any one country by limiting the pursuit of new business. But the issue of conflict management was largely solved by 1960 when the first holding company, Interpublic, was created to house what was then -- and now – one of the world’s largest agencies, McCann-Erickson. Some of McCann’s former acquisitions were to be subsequently managed as separate entities. In this way clients could be assured that sensitive information would not be shared, and the agency’s holding company was not constrained in terms of its size. Unfortunately for agencies, some marketers continued to encumber their agencies with some restrictions. For example, conflict lists occasionally extended to the holding company’s subsidiaries (illustrated by DraftFCB’s former client SC Johnson, which as recently as last year obliged Draft’s parent Interpublic to restrict its units around the world from working with similar packaged goods companies as well as some in adjacent industries). But for the most part, marketers accepted this model, and other holding companies were eventually established. Over time, the agencies with larger clients were able to establish sufficient scale to provide clients with world-class tools and processes. From there, agencies increasingly diversified their client bases, which in turn made an agency more appealing to marketers because the diversified client base reduced the chances that the agency would go out of business while it was working on a campaign. The larger client bases also availed marketers to a wider breadth of world-class talent who could be allocated at least on a part-time basis to an account. Agencies then expanded their domestic offerings with a broader array of marketing services, mirroring their clients’ interests in undertaking different approaches to marketing. New services were then rolled out around the world, and the services were often bundled together. These circumstances have all led to the structure of the modern-day global marketing services holding company, and largely explain why most global marketers allocate the bulk of their outsourced marketing services to global agency holding companies. As a consequence, each of the holding companies is more globally-oriented than all but a handful of large media companies.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

WP

P

Goo

gle

Om

nic

om

Ne

ws

Co

rp

Inte

rpub

lic

Dis

covery

Via

com

Tim

e W

arn

er

Wa

lt D

isn

ey

CBS

Media Company Exposure to International Revenues (2010A)

Source: Company Reports

- 7 - Brian Wieser 212-514-4682 Pivotal Research Group

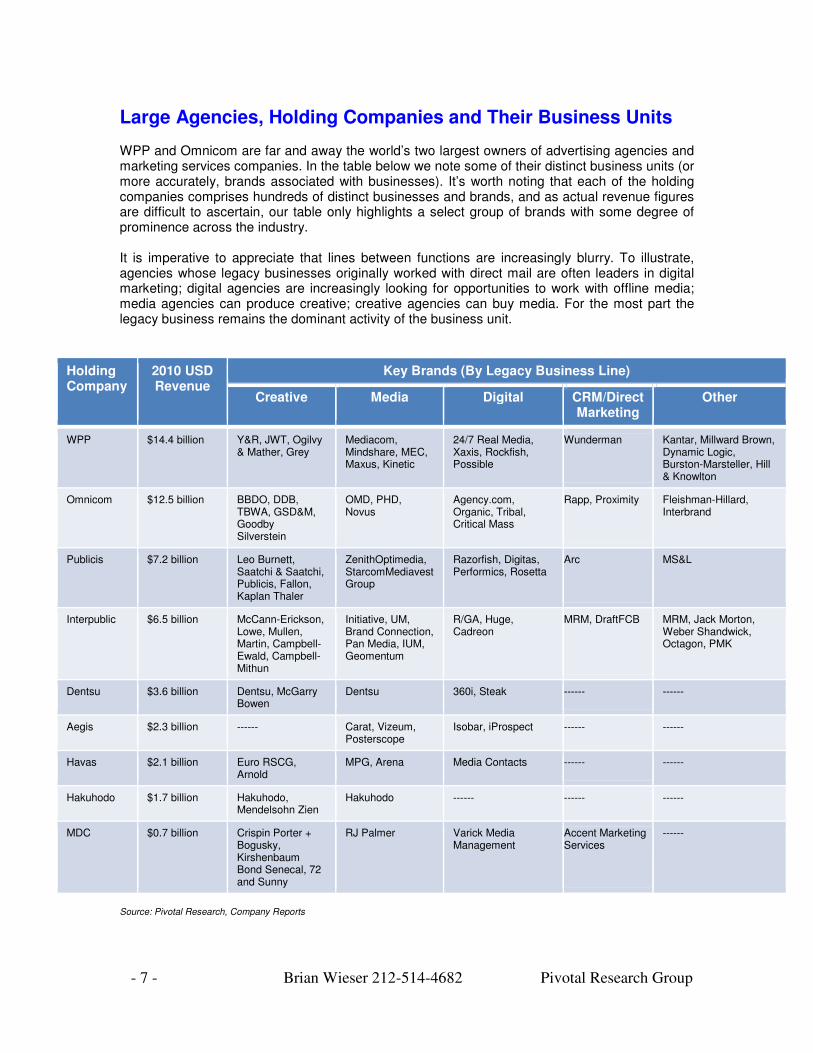

Large Agencies, Holding Companies and Their Business Units WPP and Omnicom are far and away the world’s two largest owners of advertising agencies and marketing services companies. In the table below we note some of their distinct business units (or more accurately, brands associated with businesses). It’s worth noting that each of the holding companies comprises hundreds of distinct businesses and brands, and as actual revenue figures are difficult to ascertain, our table only highlights a select group of brands with some degree of prominence across the industry. It is imperative to appreciate that lines between functions are increasingly blurry. To illustrate, agencies whose legacy businesses originally worked with direct mail are often leaders in digital marketing; digital agencies are increasingly looking for opportunities to work with offline media; media agencies can produce creative; creative agencies can buy media. For the most part the legacy business remains the dominant activity of the business unit.

Holding Company

2010 USD Revenue

Key Brands (By Legacy Business Line)

Creative Media Digital CRM/Direct Marketing

Other

WPP $14.4 billion Y&R, JWT, Ogilvy & Mather, Grey

Mediacom, Mindshare, MEC, Maxus, Kinetic

24/7 Real Media, Xaxis, Rockfish, Possible

Wunderman Kantar, Millward Brown, Dynamic Logic, Burston-Marsteller, Hill & Knowlton

Omnicom $12.5 billion BBDO, DDB, TBWA, GSD&M, Goodby Silverstein

OMD, PHD, Novus

Agency.com, Organic, Tribal, Critical Mass

Rapp, Proximity Fleishman-Hillard, Interbrand

Publicis $7.2 billion Leo Burnett, Saatchi & Saatchi, Publicis, Fallon, Kaplan Thaler

ZenithOptimedia, StarcomMediavest Group

Razorfish, Digitas, Performics, Rosetta

Arc MS&L

Interpublic $6.5 billion McCann-Erickson, Lowe, Mullen, Martin, Campbell-Ewald, Campbell-Mithun

Initiative, UM, Brand Connection, Pan Media, IUM, Geomentum

R/GA, Huge, Cadreon

MRM, DraftFCB MRM, Jack Morton, Weber Shandwick, Octagon, PMK

Dentsu $3.6 billion Dentsu, McGarry Bowen

Dentsu 360i, Steak ------ ------

Aegis $2.3 billion ------ Carat, Vizeum, Posterscope

Isobar, iProspect ------ ------

Havas $2.1 billion Euro RSCG, Arnold

MPG, Arena Media Contacts ------ ------

Hakuhodo $1.7 billion Hakuhodo, Mendelsohn Zien

Hakuhodo ------ ------ ------

MDC $0.7 billion Crispin Porter + Bogusky, Kirshenbaum Bond Senecal, 72 and Sunny

RJ Palmer Varick Media Management

Accent Marketing Services

------

Source: Pivotal Research, Company Reports

- 8 - Brian Wieser 212-514-4682 Pivotal Research Group

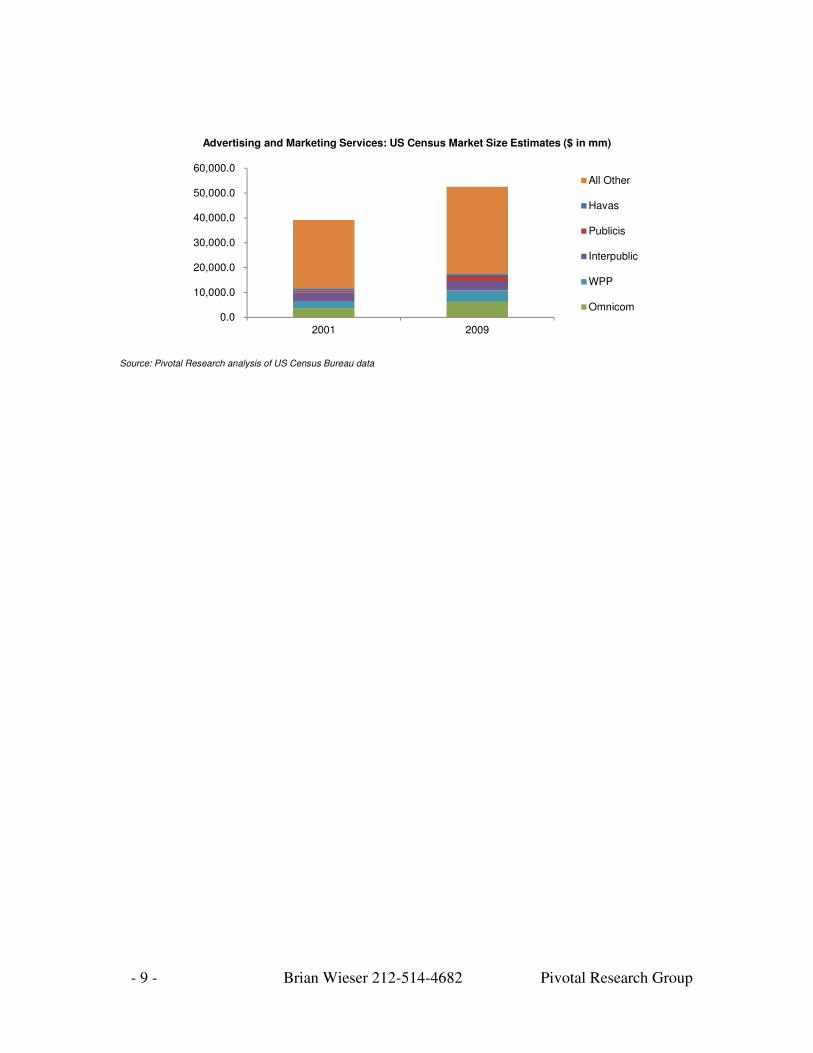

Industry Size for Marketing Services in the US and Globally Advertising and marketing services agencies generate revenues in excess of $100 billion annually around the world, although the absolute size is dependent upon how the industry is defined. For points of reference, media owners generate approximately $400 billion in advertising revenues globally, according to Magna Global, and closer to $500 billion according to Group M. GroupM estimates total expenditures incurred by marketers at more than $800 billion annually. The global holding companies (WPP, Omnicom, Publicis, Interpublic and Havas) dominate the marketing services industry, collectively generating nearly $45 billion in revenues. Other large entities such as Dentsu, Hakuhodo, Aegis and MDC Partners represent another ~$7 billion in annual revenues. The rest of the industry is highly fragmented. There are more than 12,000 advertising agencies – including more than 2,000 with more than 10 employees – in the United States alone, according to the US Census Bureau. In China, agency search and selection consultancy R3 estimates that there are more than 143,000 local agencies (but only 202 multinationals). The US is certainly the largest market, although defining its size is also subject to definition. Leading trade magazine Ad Age pegged the size of the US industry at $30 billion in 2010, up from $20 billion in 2001. But the US Census Bureau estimated that the combined Advertising, PR, Media Buying and Direct Mail agency industries totaled $52 billion for the most recent year in which they published estimates, 2009. This was down from $57 billion in 2008, but well ahead of the $39 billion generated in 2001. Many of these businesses thrive at a small scale, as much of the industry is centered around developing new ideas, creatively applying data or insights to marketing problems, or performing tasks we would describe as “general contracting,” or patching together other small-scale suppliers of services. Equally important, even the largest global marketers tend to look for best-in-class suppliers (or sometimes merely suppliers with whom they have past working relationships) of these services, and require all of their suppliers to work together. This leads to circumstances where the holding companies come to know potential acquisitions from recurring collaboration, and allows them to identify synergistic opportunities. It also leads them to pursue acquisitions in order to prevent competing agency holding companies from buying these smaller entities and gaining footholds with new accounts. As a result, the agency industry is highly acquisitive as the holding companies incrementally grow their share of the industry’s revenues every year. This also means it remains clear that the agency holding companies are unlikely to run out of acquisition opportunities any time soon.

0.0

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

35,000.0

2001 2010

All Other

Havas

Publicis

Interpublic

WPP

Omnicom

Advertising and Marketing Services: Ad Age Total US Market Size Estimates ($ in mm)

Source: Ad Age

- 9 - Brian Wieser 212-514-4682 Pivotal Research Group

0.0

10,000.0

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

2001 2009

All Other

Havas

Publicis

Interpublic

WPP

Omnicom

Advertising and Marketing Services: US Census Market Size Estimates ($ in mm)

Source: Pivotal Research analysis of US Census Bureau data

- 10 - Brian Wieser 212-514-4682 Pivotal Research Group

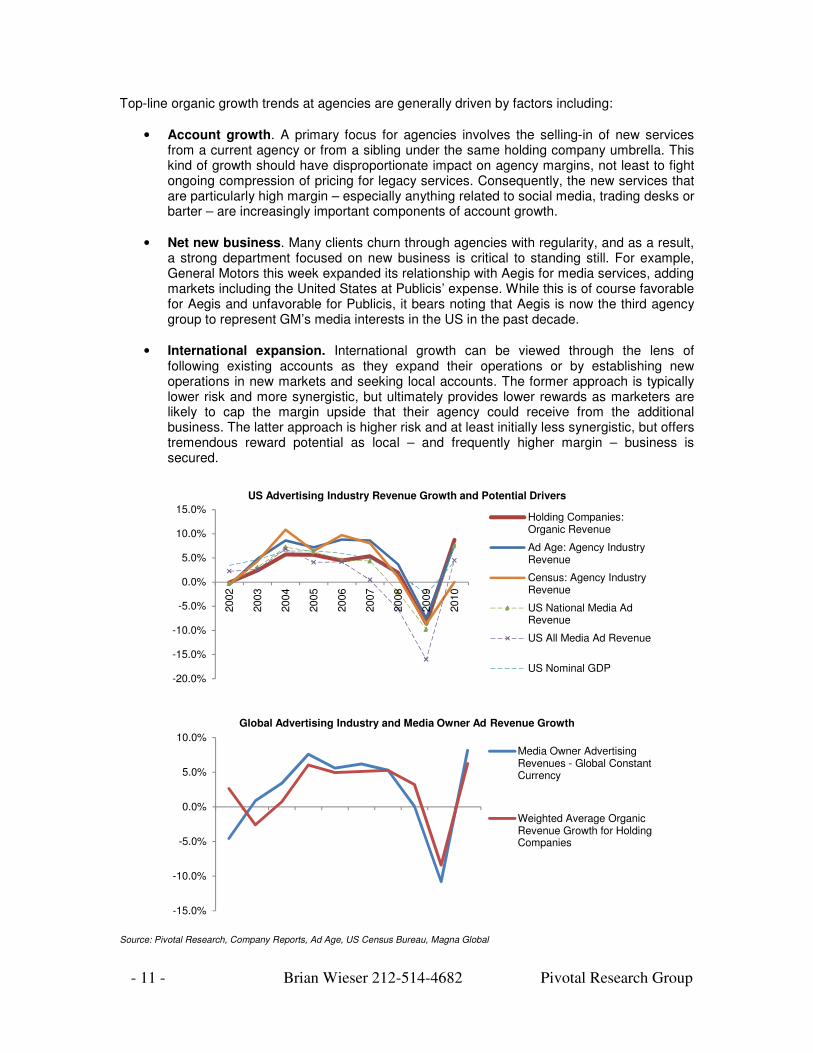

Industry Growth And Agency Growth Drivers We have a range of historical data points to consider when contemplating the future pace of growth of the industry, although none are conclusive as drivers. GDP growth and media spending are two of the most common benchmarks investors – and agency managers – rely upon. However, these figures are somewhat compromised as business drivers for a number of reasons. Agencies’ revenue streams aren’t directly tied to nominal GDP because marketing touches an increasing share of activities in any given economy, and agencies can offer services for many of these activities. Further, agencies’ revenue streams aren’t directly tied to media spending or media owners’ ad revenues because an increasing share of their activities relate to unpaid media or marketing-related activities. These activities cannot be reflected in any study of historical media owner revenues. Quantifying total marketing services expenditures is also difficult to do because of the very fragmented (and often privately held) nature of the industry.

Nonetheless, for our approach we consider the 2001-2010 period, where we can see that the US agency industry grew at a CAGR of 4-4.5% in the US according to the Census Bureau and Ad Age, respectively. This compares to US media owners growing their ad revenues by closer to 2% over the same period, and the overall American economy growing by just under 4% on a nominal basis. At a global level, data will necessarily be more spotty given the absence of data on agencies other than those which are public. However, between 2001 and 2010, we can see that organic growth of agencies averaged approximately 2%, behind global media owner advertising revenues, which rose by closer to 3%.

In forecasting the future, these figures serve as useful reference points, although any reference of “average” holding company organic revenue growth must account for unusual circumstances at Interpublic and Havas during much of this time. Further, we believe the global data here understates global advertising agency growth, as the holding companies’ organic growth rates have not necessarily been reflective of the countries in which they operated in any past year. As their footprints grow around the world, growth rates should converge towards some notional global average. Thus we are inclined to reference the Census / Ad Age figures as a starting point. But with marketers increasingly reliant on higher margin / higher services-based digital media, organic revenue growth should be impacted favorably. Consequently, would be use the high side of the last decade’s rate in the United States – 4.5% -- as a long-term benchmark growth rate for the industry. Relative to this reference point, we expect faster growth in Asian and Latin American markets, and slower – if not flat or slightly down – growth in Europe. The UK should fall somewhere in between growth in the United States and in Europe, mirroring its geography and broader business interests. Weighted against each holding company’s regional exposures, this implies 4.5-5.5% organic growth for the holding companies worldwide over a medium and long-term basis.

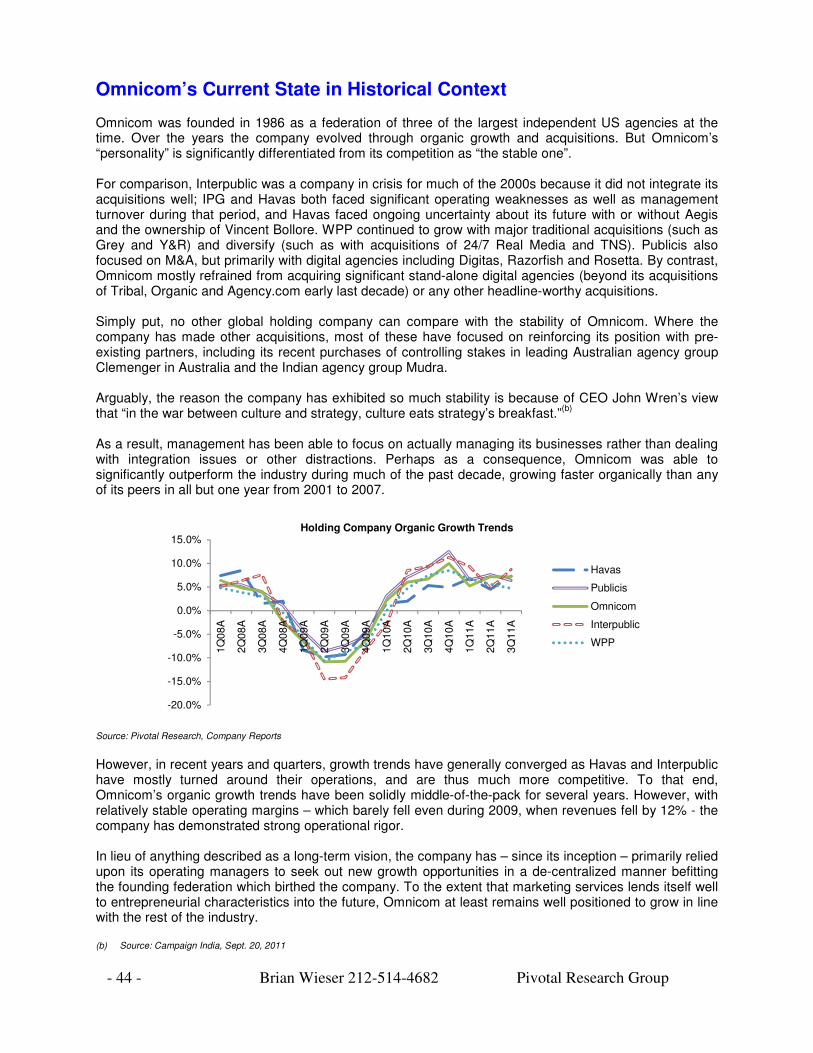

- 11 - Brian Wieser 212-514-4682 Pivotal Research Group

Top-line organic growth trends at agencies are generally driven by factors including:

• Account growth. A primary focus for agencies involves the selling-in of new services from a current agency or from a sibling under the same holding company umbrella. This kind of growth should have disproportionate impact on agency margins, not least to fight ongoing compression of pricing for legacy services. Consequently, the new services that are particularly high margin – especially anything related to social media, trading desks or barter – are increasingly important components of account growth.

• Net new business. Many clients churn through agencies with regularity, and as a result,

a strong department focused on new business is critical to standing still. For example, General Motors this week expanded its relationship with Aegis for media services, adding markets including the United States at Publicis’ expense. While this is of course favorable for Aegis and unfavorable for Publicis, it bears noting that Aegis is now the third agency group to represent GM’s media interests in the US in the past decade.

• International expansion. International growth can be viewed through the lens of

following existing accounts as they expand their operations or by establishing new operations in new markets and seeking local accounts. The former approach is typically lower risk and more synergistic, but ultimately provides lower rewards as marketers are likely to cap the margin upside that their agency could receive from the additional business. The latter approach is higher risk and at least initially less synergistic, but offers tremendous reward potential as local – and frequently higher margin – business is secured.

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

Holding Companies:Organic Revenue

Ad Age: Agency IndustryRevenue

Census: Agency IndustryRevenue

US National Media AdRevenue

US All Media Ad Revenue

US Nominal GDP

US Advertising Industry Revenue Growth and Potential Drivers

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

Media Owner AdvertisingRevenues - Global ConstantCurrency

Weighted Average OrganicRevenue Growth for HoldingCompanies

Global Advertising Industry and Media Owner Ad Revenue Growth

Source: Pivotal Research, Company Reports, Ad Age, US Census Bureau, Magna Global

- 12 - Brian Wieser 212-514-4682 Pivotal Research Group

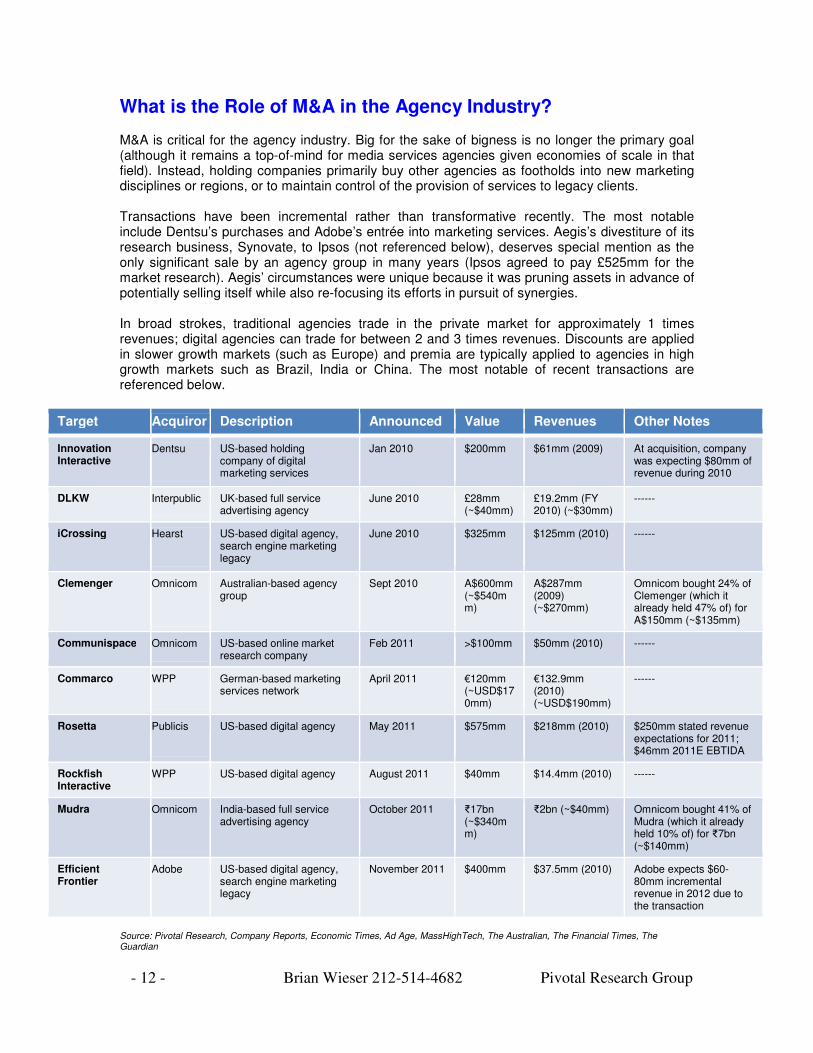

What is the Role of M&A in the Agency Industry? M&A is critical for the agency industry. Big for the sake of bigness is no longer the primary goal (although it remains a top-of-mind for media services agencies given economies of scale in that field). Instead, holding companies primarily buy other agencies as footholds into new marketing disciplines or regions, or to maintain control of the provision of services to legacy clients. Transactions have been incremental rather than transformative recently. The most notable include Dentsu’s purchases and Adobe’s entrée into marketing services. Aegis’s divestiture of its research business, Synovate, to Ipsos (not referenced below), deserves special mention as the only significant sale by an agency group in many years (Ipsos agreed to pay £525mm for the market research). Aegis’ circumstances were unique because it was pruning assets in advance of potentially selling itself while also re-focusing its efforts in pursuit of synergies. In broad strokes, traditional agencies trade in the private market for approximately 1 times revenues; digital agencies can trade for between 2 and 3 times revenues. Discounts are applied in slower growth markets (such as Europe) and premia are typically applied to agencies in high growth markets such as Brazil, India or China. The most notable of recent transactions are referenced below.

Target Acquiror Description Announced Value Revenues Other Notes

Innovation Interactive

Dentsu US-based holding company of digital marketing services

Jan 2010 $200mm $61mm (2009) At acquisition, company was expecting $80mm of revenue during 2010

DLKW Interpublic UK-based full service advertising agency

June 2010 £28mm (~$40mm)

£19.2mm (FY 2010) (~$30mm)

------

iCrossing Hearst US-based digital agency, search engine marketing legacy

June 2010 $325mm $125mm (2010) ------

Clemenger Omnicom Australian-based agency group

Sept 2010 A$600mm (~$540mm)

A$287mm (2009) (~$270mm)

Omnicom bought 24% of Clemenger (which it already held 47% of) for A$150mm (~$135mm)

Communispace Omnicom US-based online market research company

Feb 2011 >$100mm $50mm (2010) ------

Commarco WPP German-based marketing services network

April 2011 €120mm (~USD$170mm)

€132.9mm (2010) (~USD$190mm)

------

Rosetta Publicis US-based digital agency May 2011 $575mm $218mm (2010) $250mm stated revenue expectations for 2011; $46mm 2011E EBTIDA

Rockfish Interactive

WPP US-based digital agency August 2011 $40mm $14.4mm (2010) ------

Mudra Omnicom India-based full service advertising agency

October 2011 ₹17bn (~$340mm)

₹2bn (~$40mm) Omnicom bought 41% of Mudra (which it already held 10% of) for ₹7bn (~$140mm)

Efficient Frontier

Adobe US-based digital agency, search engine marketing legacy

November 2011 $400mm $37.5mm (2010) Adobe expects $60-80mm incremental revenue in 2012 due to the transaction

Source: Pivotal Research, Company Reports, Economic Times, Ad Age, MassHighTech, The Australian, The Financial Times, The Guardian

- 13 - Brian Wieser 212-514-4682 Pivotal Research Group

Future Consolidation The topic of consolidation is periodically an issue for the industry, and sometimes emerges as a topic of intense focus. This is unsurprising given the nature of today’s holding companies as the products of past roll-ups. Aegis and Havas are typically referenced in the context of further consolidation given a perceived lack of commitment to independence by the companies’ boards of directors. The catalyst for this uncertainty usually resolves back to French investor Vincent Bollore, who owns a plurality of shares in both companies (although Aegis has blocked Bollore’s operational involvement with Aegis on several occasions). Many scenarios have been contemplated in the past, including a merger between Havas and Aegis, or a sale of one or both, most likely involving Interpublic and Publicis (although WPP and Omnicom’s involvement should not be ruled out if an active sale process for either company were ever undertaken). However, with Aegis’ divestiture of its research division Synovate last year and subsequent statements by the company’s CEO, Jerry Buhlmann, the company reaffirmed its status as an independent entity…unless the price is right to make a transaction happen. Further consolidation would be favorable to the holding companies, if only because it may contribute to a reduced degree of competition when services are priced for clients. When pitches for new business occur one or two holding companies are inevitably ruled out because of insurmountable conflict issues, leaving (often) three or four competitors for every pitch. This contributes to highly competitive pricing, especially in servicing the world’s largest clients (which are often serviced at or below cost in order to secure a basic level of operating scale in some markets). To the extent that future pitches involved only two competitors, it is more likely that pricing discipline would be exercised. However, antitrust concerns may limit consolidation without some divestitures, as concentration levels in some countries – especially with respect to media buying on certain key media, such as television – would be very high.

- 14 - Brian Wieser 212-514-4682 Pivotal Research Group

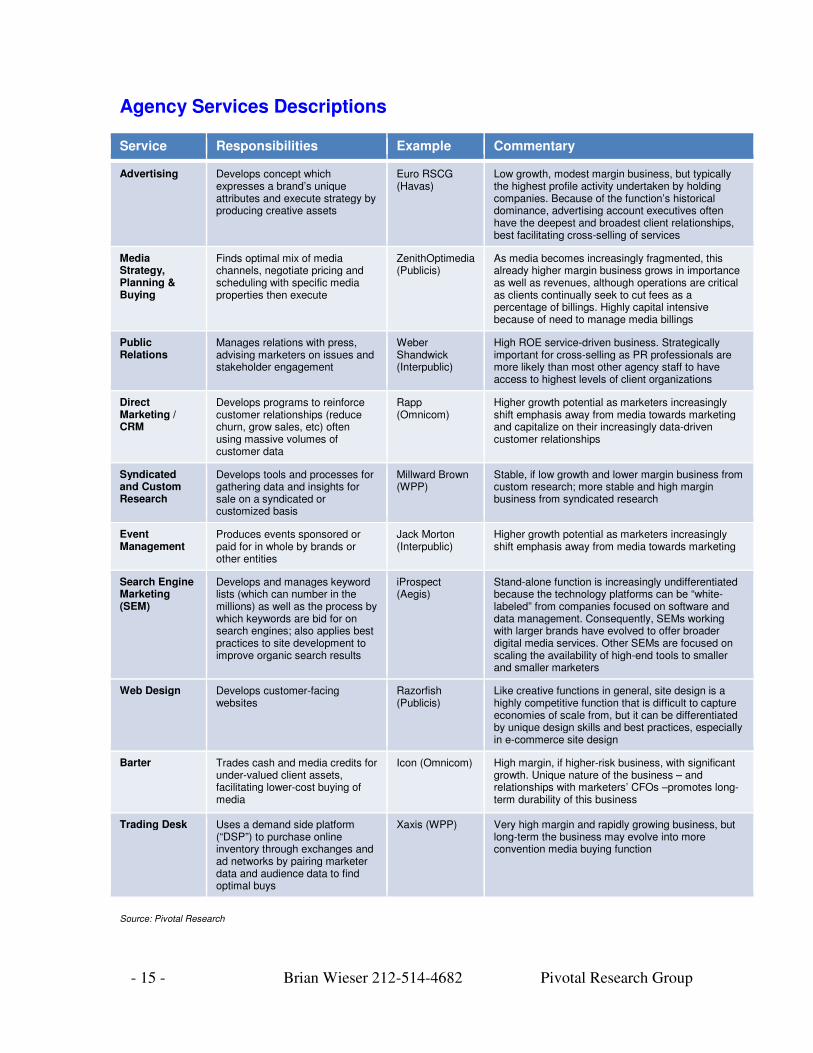

How Do Agencies Generate Revenue? What do marketing services agencies actually do to generate revenue? The industry has evolved substantially from the time when they provided ad sales representation for newspaper publishers in the 1860s. However, some aspects of the business remain constant: the industry remains highly entrepreneurial, and primarily services-driven. Just as the process of finding advertisers to fill newspaper pages begat the copy-writing business, and copy-writing begat art direction, creative strategy and media buying across multiple platforms, practitioners are constantly looking for ways to extend their client relationships in new ways. Consequently, while the global creative agency remains the archetypical business unit of the holding companies, these entities are increasingly diminishing in importance. At Interpublic, McCann-Erickson, Lowe and DraftFCB represents less than half of Interpublic’s revenues; at Publicis, Leo Burnett, Saatchi & Saatchi and the eponymous Publicis agency account for a similar share of their parent company’s activities. The figures are much lower, below a third, at WPP (whose global agencies include JWT, Y&R, Grey and Ogilvy & Mather) and Omnicom (which includes BBDO, DDB and TBWA). Agent-based activities now undertaken by distinct business types include “advertising” (referring to the overall brand development and related creative services), media strategy, planning & buying (often described in short-hand as “media buying”), public relations, direct marketing/customer relationship management (“CRM”), syndicated & custom research, event management, search engine marketing and web design. Barter and the concept of the Trading Desk represent modern-day returns to the original role of agencies, whereby these entities typically take principal positions in media inventory and re-sell it at a mark-up to (primarily) their parent company’s clients. Notably, these business models are not new in returning to agencies’ origins on the sell-side of the media industry: Publicis still operates a traditional newspaper and outdoor advertising representation unit called Medias et Regies, and Japanese agencies typically perform sales/representation tasks across most Japanese media. At a functional level, there remain many similarities across these otherwise diverse business units. Almost every agent-based function in marketing services firms features the following:

• The account manager has responsibility for services for specific clients. These individuals are critical to agencies as they are charged with managing – and growing -- the P&L attached to their clients. Their primary value is in helping clients to navigate their own organizations, and socializing new ideas that generate an agency more revenue.

• As a right-hand to account management, “strategy” roles focus upon tying any given activity to brand goals, or at least upon developing clever themes around which an execution is designed. This strategy function would in other industries be referred to as “product” development. Varying names may be used for this function, including “account planning” at advertising agencies or “communications planning” at media agencies, a role which is distinct from “media planning”

• Every discipline also involves some capacity to perform research, which in turn informs strategy and assess the impact of the executions.

Every discipline pursues activities associated with broadly-defined “digital” activities because every discipline can find new opportunities to grow through digital communications platforms. In part because of the novelty of digital media and myriad ways in which new platforms can serve as marketing vehicles, roles and responsibilities can get blurry, and are not necessarily provided for otherwise comparable marketers in similar ways. While this fragmentation of responsibilities strikes many observers as inefficient, it is a reaction to a continuous evolution of the industry. It is also reaction by holding companies’ agencies to the ongoing creation of independent agencies which continue to find new and often profitable niches.

- 15 - Brian Wieser 212-514-4682 Pivotal Research Group

Agency Services Descriptions

Service Responsibilities Example Commentary

Advertising Develops concept which expresses a brand’s unique attributes and execute strategy by producing creative assets

Euro RSCG (Havas)

Low growth, modest margin business, but typically the highest profile activity undertaken by holding companies. Because of the function’s historical dominance, advertising account executives often have the deepest and broadest client relationships, best facilitating cross-selling of services

Media Strategy, Planning & Buying

Finds optimal mix of media channels, negotiate pricing and scheduling with specific media properties then execute

ZenithOptimedia (Publicis)

As media becomes increasingly fragmented, this already higher margin business grows in importance as well as revenues, although operations are critical as clients continually seek to cut fees as a percentage of billings. Highly capital intensive because of need to manage media billings

Public Relations

Manages relations with press, advising marketers on issues and stakeholder engagement

Weber Shandwick (Interpublic)

High ROE service-driven business. Strategically important for cross-selling as PR professionals are more likely than most other agency staff to have access to highest levels of client organizations

Direct Marketing / CRM

Develops programs to reinforce customer relationships (reduce churn, grow sales, etc) often using massive volumes of customer data

Rapp (Omnicom)

Higher growth potential as marketers increasingly shift emphasis away from media towards marketing and capitalize on their increasingly data-driven customer relationships

Syndicated and Custom Research

Develops tools and processes for gathering data and insights for sale on a syndicated or customized basis

Millward Brown (WPP)

Stable, if low growth and lower margin business from custom research; more stable and high margin business from syndicated research

Event Management

Produces events sponsored or paid for in whole by brands or other entities

Jack Morton (Interpublic)

Higher growth potential as marketers increasingly shift emphasis away from media towards marketing

Search Engine Marketing (SEM)

Develops and manages keyword lists (which can number in the millions) as well as the process by which keywords are bid for on search engines; also applies best practices to site development to improve organic search results

iProspect (Aegis)

Stand-alone function is increasingly undifferentiated because the technology platforms can be “white-labeled” from companies focused on software and data management. Consequently, SEMs working with larger brands have evolved to offer broader digital media services. Other SEMs are focused on scaling the availability of high-end tools to smaller and smaller marketers

Web Design Develops customer-facing websites

Razorfish (Publicis)

Like creative functions in general, site design is a highly competitive function that is difficult to capture economies of scale from, but it can be differentiated by unique design skills and best practices, especially in e-commerce site design

Barter Trades cash and media credits for under-valued client assets, facilitating lower-cost buying of media

Icon (Omnicom) High margin, if higher-risk business, with significant growth. Unique nature of the business – and relationships with marketers’ CFOs –promotes long-term durability of this business

Trading Desk Uses a demand side platform (“DSP”) to purchase online inventory through exchanges and ad networks by pairing marketer data and audience data to find optimal buys

Xaxis (WPP) Very high margin and rapidly growing business, but long-term the business may evolve into more convention media buying function

Source: Pivotal Research

- 16 - Brian Wieser 212-514-4682 Pivotal Research Group

Media Agencies Have Been a Key Source of Top-Line Growth Among the holding companies’ core businesses, media agencies and related services have been critical in driving organic revenue growth for holding companies. Each has placed a significant focus on this business over the past decade, and has placed its stand-alone media agencies into what we describe as “sub-holding” companies (WPP’s Mediacom, MEC, Mindshare and Maxus to GroupM; Starcom, Mediavest, Zenith and Optimedia to Vivaki; Omnicom’s OMD and PHD to OMG; Aegis’ Carat and Vizeum to Aegis Media; Interpublic’s UM and Initiative to Mediabrands; and Havas’ MPG to Havas Media). RECMA data

(a) indicates that media agency billings from the holding companies have grown far

faster than the billings of the media industry as a whole. While each of WPP, Omnicom, Publicis, Aegis and Havas were able to benefit from weakness at Interpublic’s media agencies over this period – each of the former five almost doubled in size during a period while IPG’s agencies essentially remained the same size – collectively the holding companies’ media agencies’ billings rose by a compounded annual growth rate of 5.9% in over the period between 2001 and 2010.

0.0

10,000.0

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

70,000.0

80,000.0

90,000.0

WPP -GroupM

Publicis -Vivaki

Omnicom -OMG

Aegis - AegisMedia

Interpublic -Mediabrands

Havas - HavasMedia

2001

2010

Pro Forma Global Media Agency Annual Billings (mm of nominal USD)

Source: Pivotal Research analysis of RECMA data

By contrast, media owners’ revenues around the world increased by a CAGR of 4.6% over the same period, according to Magna Global. The global agencies’ share of total media owners’ revenues grew from 56% to 62% as a result. In absolute terms, the global agencies accounted for $151 billion in annual billings in 2001, which rose to $254 billion in 2010. Per Magna, global media owners’ revenues were $254 billion in 2001, and this total rose to $408 billion by 2010. As most of the world’s largest marketers were already working with the holding companies prior to this period of analysis, we believe much of this growth has occurred as global agencies have taken market share from smaller, single country media agencies (or single country full-service agencies). This increase in share has occurred primarily because marketers perceive that larger media agencies are better able to secure superior pricing on paid media, based on the (often erroneous) belief that more size equates to more negotiating clout. More unambiguously, larger agencies are almost certainly able to offer more and better tools to their clients and can bring world-class talent and experience to the clients they work with. The trend among large marketers – whether single-country or multi-national – to using global media agencies is unlikely to abate as long as marketers perceive that they can secure superior media pricing with the global agencies. As a result, the global media agencies should be able to continue increasing their shares of business from single-country marketers. (a) We base our analysis on data from French research firm RECMA, which is generally regarded as the only primary source of data on

the media agency industry. While their data requires some subjective interpretation, the underlying trends associated with their figures are directionally correct.

- 17 - Brian Wieser 212-514-4682 Pivotal Research Group

Compensation Structures Agency compensation models reflected their historical origins for many years: commissions, as a percentage of media billed. For one flat rate, often 15% of billings, agencies provided traditional creative and media services, and focused on managing their costs. However, less opaque – and typically lower – pricing for media services was prompted by the rise of the independent media agency beginning in the 1980s. As pricing fell, and the procurement function came into vogue for marketers, many clients replaced commissions with fee structures designed to ensure that agencies earned a mutually agreed upon operating margin, subject to pre-defined operating choices. Under these structures, as long as the account is well-managed, pre-defined margins are all but certain. Fees are far and away the dominant form of compensating agencies. A 2010 study for the ANA (the trade association for marketers) conducted by Jones Lundin Beals (a consultancy specializing in agency search and selection) indicated that commissions accounted for only 3% of compensation plans at advertising agencies that year, down from 16% in 2007. Sales commissions – whereby the agency is paid in part or in whole depending upon how the marketer’s business performs – accounted for 15% of compensation models. The consequences of compensation structures can be significant across the broader advertising industry. Marketing choices and spending on specific media platforms for many marketers can be effectively pre-determined in large part because of the contracts they agree to with their agencies. Importantly, conventions around fees may vary by country and by medium. In many markets around the world, clients expect their agencies to generate revenue through the volume-based rebates – also known as AVBs, or “Agency Volume Bonnifications” – they are encouraged to seek out from media owners. However, in many instances these AVBs are rebated back to clients (often in a contractually pre-determined manner) and the agency is then paid conventionally through fees. Media agencies may also be able to earn income from interest generated by effective management of the money they use for media billings. In all cases, these compensation structures are tacitly or – at least for Sarbanes-Oxley compliant companies – actively agreed to by the clients themselves, who typically account for these alternative compensation structures by reducing how much they pay the agency in commissions or other fees. One trend which has gained some prominence in recent periods relates to incentive fees. Many marketers have come to the conclusion that a utility-like fee structure may produce utility-like results, which may or may not be desirable. As a consequence, enterprising account executives and their finance teams often seek to incorporate fee structures which establish some mutually agreed-upon activity as a primary goal, and to ensure bonus payments to the agency in exchange for meeting or beating goals.

- 18 - Brian Wieser 212-514-4682 Pivotal Research Group

Illustrative Account Staffing Model Regardless of the discipline, account managers are tasked with managing their firm’s relationship with a client towards a goal of earning better than a 15% operating margin. Sometimes the workflows by which that margin can be earned is explicitly designed by the marketer’s procurement teams, but more generally the art of account management is in setting client expectations and managing the delivery of services to outperform those expectations. If the client has goals with respect to being seen to be an industry leader, the account executive is doing his or her job in providing potentially high-profile initiatives which will serve those goals. If the client is primarily focused on driving down media costs, the account executive will focus on finding cost savings in allocating media budgets. If the client is tasked internally with building buy-in around their organization for key marketing initiatives, the account executive will be the client’s right hand, and drive the agency team to support that goal too. These points are important considerations in assessing how and why marketers and their agencies make decisions and allocate budgets. To convey the way in which an account may be managed, we illustrate a staffing plan for a media services account with ~$50mm in annual spending on media including digital ($1.5mm), print ($3mm on magazines), radio ($4mm on network radio) and TV ($33mm on national and $9mm on local). Fees in this example could equate to approximately $2mm for slightly more than 11 full time-equivalent employees, including part of the time for 29 different employees. Depending upon the structure of the final contract with a marketer, we can see how a marketer’s budgeting may be affected by the terms they agree to with their agencies. We can further imagine the workflows associated with managing these activities, and that a marketer may need to pay different fees for different kinds of services given the varying labor intensity associated with each medium. In this instance, five distinct people and one FTE are required to execute a small digital budget. But seven distinct people and four FTEs are required to execute a television budget that is 20 times larger. As marketers continue to deploy budgets into digital media, they will also continue to push for operational efficiencies. However, it is highly unlikely that digital campaigns can ever become as labor-efficient as television given television’s absolute scale and the homogenous nature of creative assets, in contrast to the fragmented nature of digital media both in terms of the media platforms and the creative assets. As a result, we anticipate that as marketers allocate increasing shares of their budgets to digital media, a larger and larger share of marketers’ budgets will be required for agency services.

Illustrative $50mm Media Account Staffing Plan

Functions # of Staff/Sub-Functions Total Staff

Account Management 1 Account Executive 0.20 FTE

Account Planning & Management 9 People: Media Planners and Researchers 4.00 FTE

Digital Buying 5 People: Account Oversight, Ad Operations, Digital Planning and Negotiating

1.00 FTE

Print Buying 1 Person: Negotiator 0.20 FTE

National Broadcast Buying 7 People: Account Oversight, Negotiating and Traffic 4.00 FTE

Local Broadcast Buying 6 People: Account Oversight, Negotiating and Traffic 2.00 FTE

Source: Pivotal Research

- 19 - Brian Wieser 212-514-4682 Pivotal Research Group

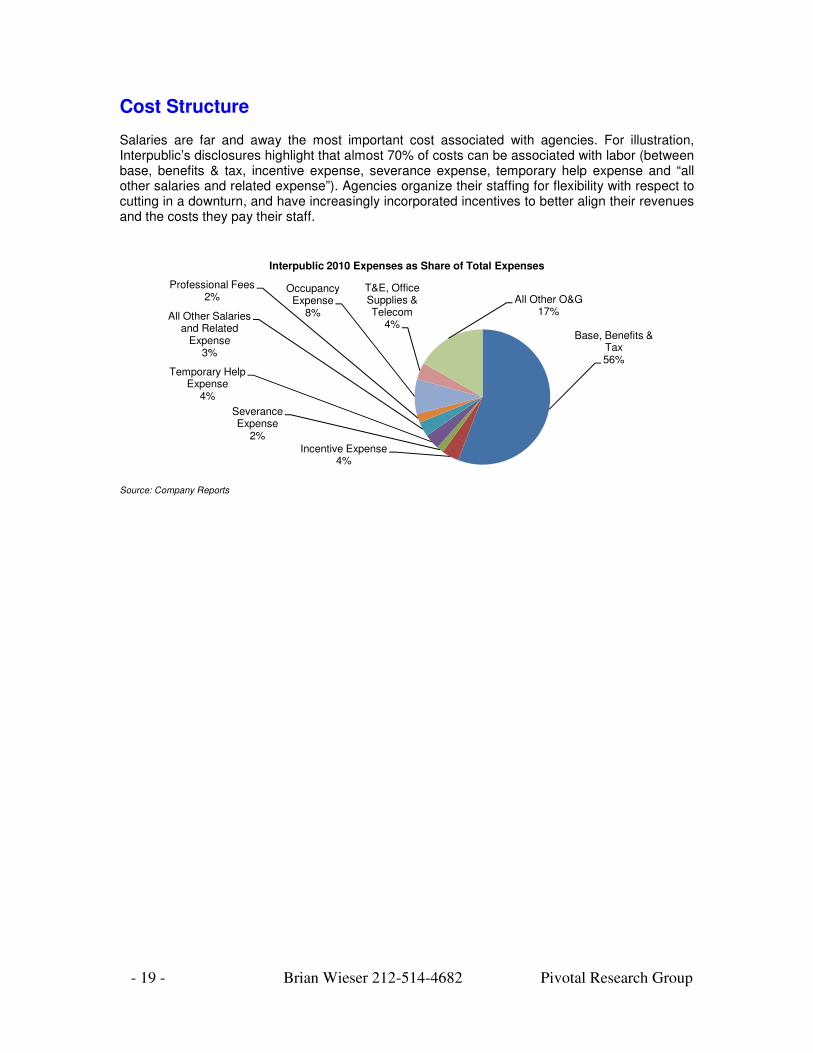

Cost Structure Salaries are far and away the most important cost associated with agencies. For illustration, Interpublic’s disclosures highlight that almost 70% of costs can be associated with labor (between base, benefits & tax, incentive expense, severance expense, temporary help expense and “all other salaries and related expense”). Agencies organize their staffing for flexibility with respect to cutting in a downturn, and have increasingly incorporated incentives to better align their revenues and the costs they pay their staff.

Base, Benefits & Tax56%

Incentive Expense4%

Severance Expense

2%

Temporary Help Expense

4%

All Other Salaries and Related

Expense3%

Professional Fees2%

Occupancy Expense

8%

T&E, Office Supplies & Telecom

4%

All Other O&G17%

Interpublic 2010 Expenses as Share of Total Expenses

Source: Company Reports

- 20 - Brian Wieser 212-514-4682 Pivotal Research Group

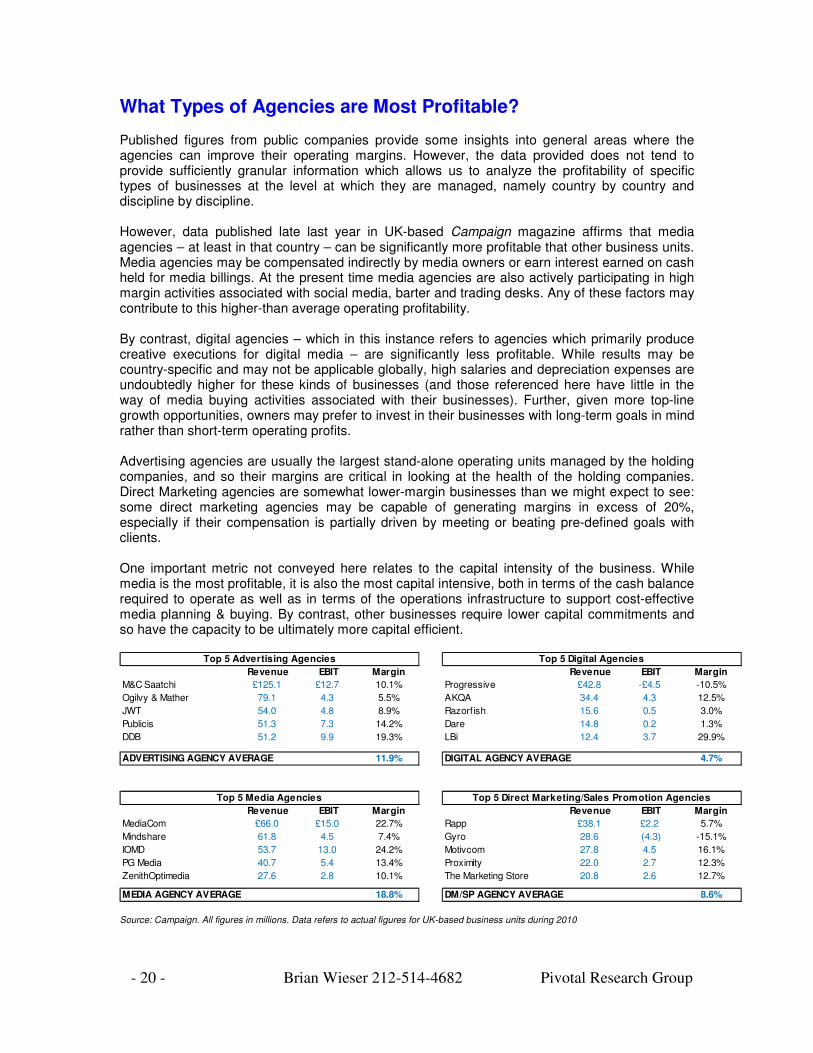

What Types of Agencies are Most Profitable? Published figures from public companies provide some insights into general areas where the agencies can improve their operating margins. However, the data provided does not tend to provide sufficiently granular information which allows us to analyze the profitability of specific types of businesses at the level at which they are managed, namely country by country and discipline by discipline. However, data published late last year in UK-based Campaign magazine affirms that media agencies – at least in that country – can be significantly more profitable that other business units. Media agencies may be compensated indirectly by media owners or earn interest earned on cash held for media billings. At the present time media agencies are also actively participating in high margin activities associated with social media, barter and trading desks. Any of these factors may contribute to this higher-than average operating profitability. By contrast, digital agencies – which in this instance refers to agencies which primarily produce creative executions for digital media – are significantly less profitable. While results may be country-specific and may not be applicable globally, high salaries and depreciation expenses are undoubtedly higher for these kinds of businesses (and those referenced here have little in the way of media buying activities associated with their businesses). Further, given more top-line growth opportunities, owners may prefer to invest in their businesses with long-term goals in mind rather than short-term operating profits. Advertising agencies are usually the largest stand-alone operating units managed by the holding companies, and so their margins are critical in looking at the health of the holding companies. Direct Marketing agencies are somewhat lower-margin businesses than we might expect to see: some direct marketing agencies may be capable of generating margins in excess of 20%, especially if their compensation is partially driven by meeting or beating pre-defined goals with clients. One important metric not conveyed here relates to the capital intensity of the business. While media is the most profitable, it is also the most capital intensive, both in terms of the cash balance required to operate as well as in terms of the operations infrastructure to support cost-effective media planning & buying. By contrast, other businesses require lower capital commitments and so have the capacity to be ultimately more capital efficient.

Top 5 Advertising Agencies Top 5 Digital Agencies

Revenue EBIT Margin Revenue EBIT Margin

M&C Saatchi £125.1 £12.7 10.1% Progressive £42.8 -£4.5 -10.5%

Ogilvy & Mather 79.1 4.3 5.5% AKQA 34.4 4.3 12.5%

JWT 54.0 4.8 8.9% Razorfish 15.6 0.5 3.0%

Publicis 51.3 7.3 14.2% Dare 14.8 0.2 1.3%

DDB 51.2 9.9 19.3% LBi 12.4 3.7 29.9%

ADVERTISING AGENCY AVERAGE 11.9% DIGITAL AGENCY AVERAGE 4.7%

Top 5 Media Agencies Top 5 Direct Marketing/Sales Promotion Agencies

Revenue EBIT Margin Revenue EBIT Margin

MediaCom £66.0 £15.0 22.7% Rapp £38.1 £2.2 5.7%

Mindshare 61.8 4.5 7.4% Gyro 28.6 (4.3) -15.1%

IOMD 53.7 13.0 24.2% Motivcom 27.8 4.5 16.1%

PG Media 40.7 5.4 13.4% Proximity 22.0 2.7 12.3%

ZenithOptimedia 27.6 2.8 10.1% The Marketing Store 20.8 2.6 12.7%

MEDIA AGENCY AVERAGE 18.8% DM/SP AGENCY AVERAGE 8.6% Source: Campaign. All figures in millions. Data refers to actual figures for UK-based business units during 2010

- 21 - Brian Wieser 212-514-4682 Pivotal Research Group

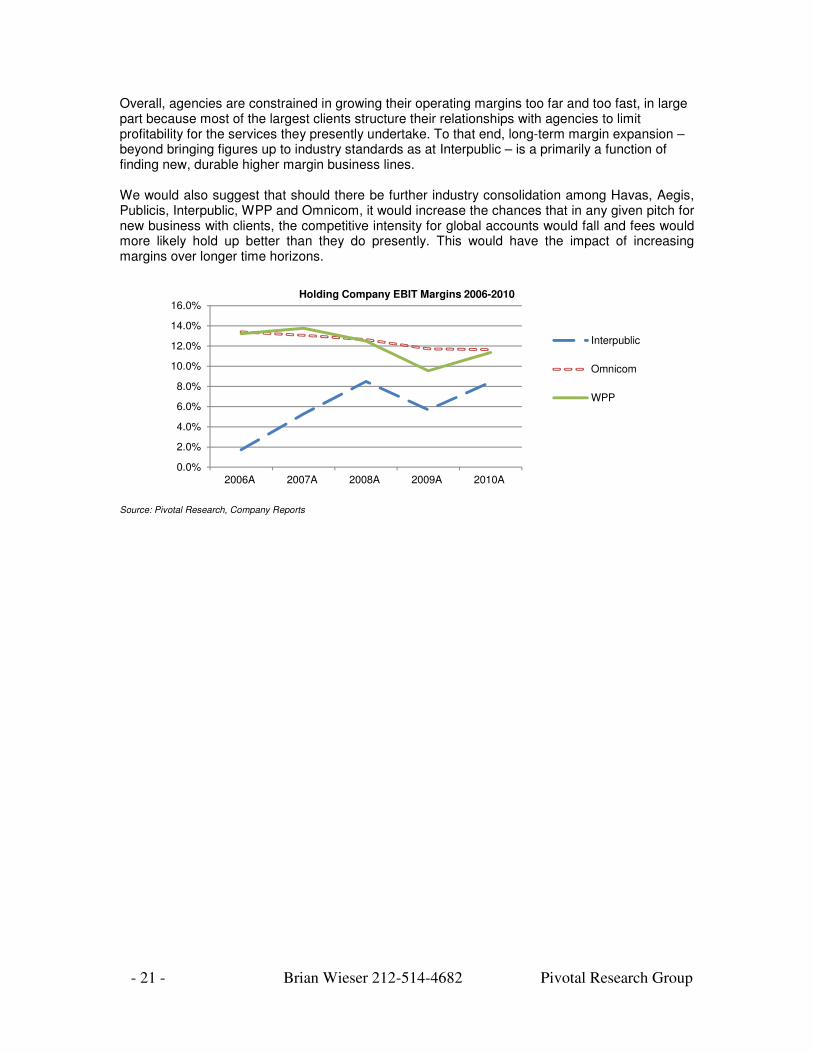

Overall, agencies are constrained in growing their operating margins too far and too fast, in large part because most of the largest clients structure their relationships with agencies to limit profitability for the services they presently undertake. To that end, long-term margin expansion – beyond bringing figures up to industry standards as at Interpublic – is a primarily a function of finding new, durable higher margin business lines. We would also suggest that should there be further industry consolidation among Havas, Aegis, Publicis, Interpublic, WPP and Omnicom, it would increase the chances that in any given pitch for new business with clients, the competitive intensity for global accounts would fall and fees would more likely hold up better than they do presently. This would have the impact of increasing margins over longer time horizons.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2006A 2007A 2008A 2009A 2010A

Interpublic

Omnicom

WPP

Holding Company EBIT Margins 2006-2010

Source: Pivotal Research, Company Reports

- 22 - Brian Wieser 212-514-4682 Pivotal Research Group

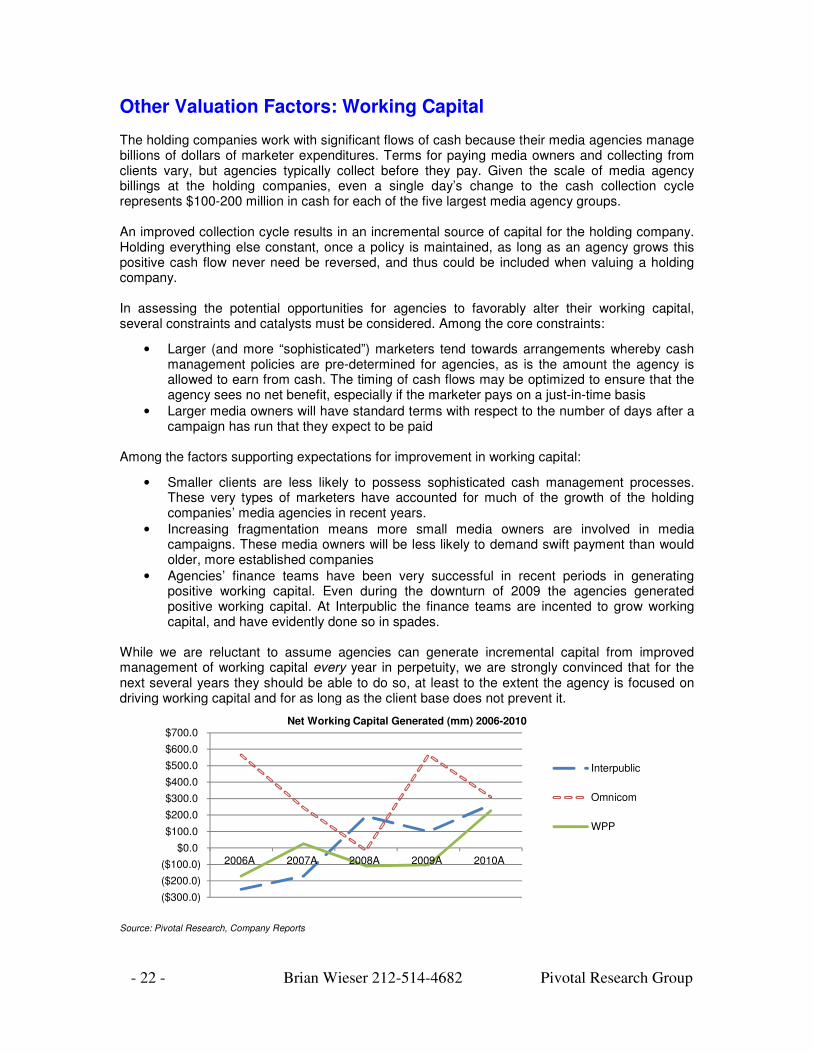

Other Valuation Factors: Working Capital The holding companies work with significant flows of cash because their media agencies manage billions of dollars of marketer expenditures. Terms for paying media owners and collecting from clients vary, but agencies typically collect before they pay. Given the scale of media agency billings at the holding companies, even a single day’s change to the cash collection cycle represents $100-200 million in cash for each of the five largest media agency groups. An improved collection cycle results in an incremental source of capital for the holding company. Holding everything else constant, once a policy is maintained, as long as an agency grows this positive cash flow never need be reversed, and thus could be included when valuing a holding company. In assessing the potential opportunities for agencies to favorably alter their working capital, several constraints and catalysts must be considered. Among the core constraints:

• Larger (and more “sophisticated”) marketers tend towards arrangements whereby cash management policies are pre-determined for agencies, as is the amount the agency is allowed to earn from cash. The timing of cash flows may be optimized to ensure that the agency sees no net benefit, especially if the marketer pays on a just-in-time basis

• Larger media owners will have standard terms with respect to the number of days after a campaign has run that they expect to be paid

Among the factors supporting expectations for improvement in working capital:

• Smaller clients are less likely to possess sophisticated cash management processes. These very types of marketers have accounted for much of the growth of the holding companies’ media agencies in recent years.

• Increasing fragmentation means more small media owners are involved in media campaigns. These media owners will be less likely to demand swift payment than would older, more established companies

• Agencies’ finance teams have been very successful in recent periods in generating positive working capital. Even during the downturn of 2009 the agencies generated positive working capital. At Interpublic the finance teams are incented to grow working capital, and have evidently done so in spades.

While we are reluctant to assume agencies can generate incremental capital from improved management of working capital every year in perpetuity, we are strongly convinced that for the next several years they should be able to do so, at least to the extent the agency is focused on driving working capital and for as long as the client base does not prevent it.

($300.0)

($200.0)

($100.0)

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

$600.0

$700.0

2006A 2007A 2008A 2009A 2010A

Interpublic

Omnicom

WPP

Net Working Capital Generated (mm) 2006-2010

Source: Pivotal Research, Company Reports

- 23 - Brian Wieser 212-514-4682 Pivotal Research Group

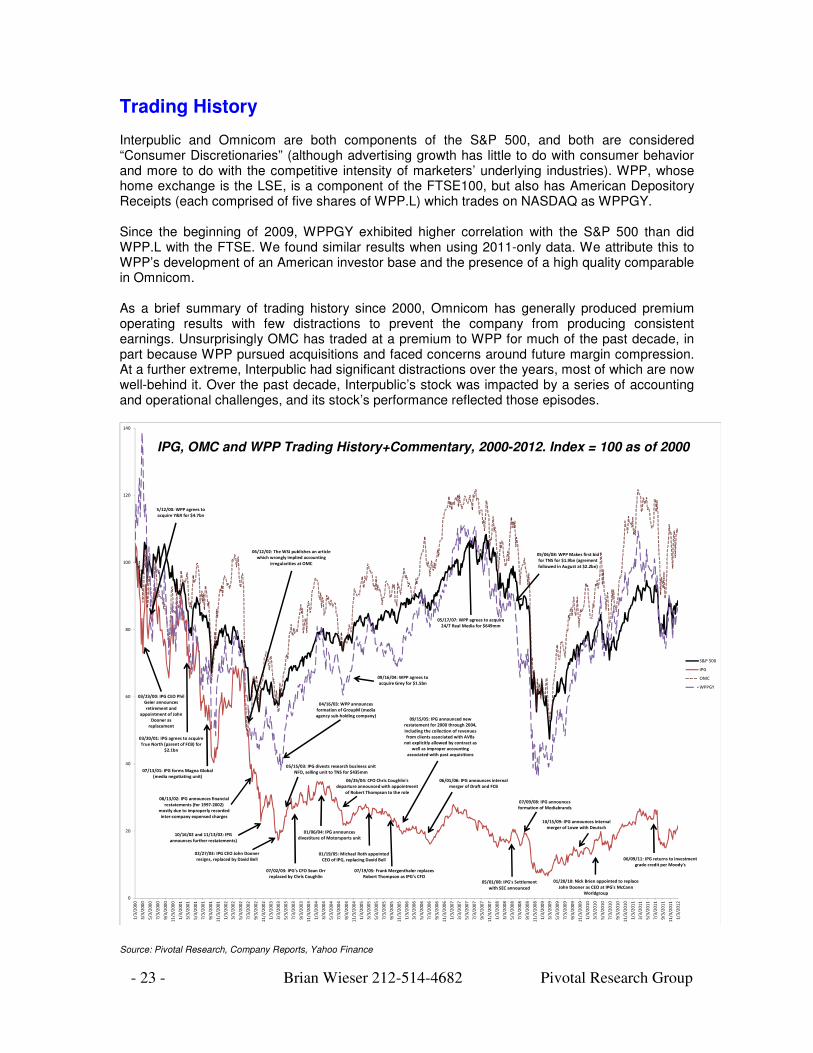

Trading History Interpublic and Omnicom are both components of the S&P 500, and both are considered “Consumer Discretionaries” (although advertising growth has little to do with consumer behavior and more to do with the competitive intensity of marketers’ underlying industries). WPP, whose home exchange is the LSE, is a component of the FTSE100, but also has American Depository Receipts (each comprised of five shares of WPP.L) which trades on NASDAQ as WPPGY. Since the beginning of 2009, WPPGY exhibited higher correlation with the S&P 500 than did WPP.L with the FTSE. We found similar results when using 2011-only data. We attribute this to WPP’s development of an American investor base and the presence of a high quality comparable in Omnicom. As a brief summary of trading history since 2000, Omnicom has generally produced premium operating results with few distractions to prevent the company from producing consistent earnings. Unsurprisingly OMC has traded at a premium to WPP for much of the past decade, in part because WPP pursued acquisitions and faced concerns around future margin compression. At a further extreme, Interpublic had significant distractions over the years, most of which are now well-behind it. Over the past decade, Interpublic’s stock was impacted by a series of accounting and operational challenges, and its stock’s performance reflected those episodes.

0

20

40

60

80

100

120

140

1/3

/20

00

3/3

/20

00

5/3

/20

00

7/3

/20

00

9/3

/20

00

11

/3/2

00

0

1/3

/20

01

3/3

/20

01

5/3

/20

01

7/3

/20

01

9/3

/20

01

11

/3/2

00

1

1/3

/20

02

3/3

/20

02

5/3

/20

02

7/3

/20

02

9/3

/20

02

11

/3/2

00

2

1/3

/20

03

3/3

/20

03

5/3

/20

03

7/3

/20

03

9/3

/20

03

11

/3/2

00

3

1/3

/20

04

3/3

/20

04

5/3

/20

04

7/3

/20

04

9/3

/20

04

11

/3/2

00

4

1/3

/20

05

3/3

/20

05

5/3

/20

05

7/3

/20

05

9/3

/20

05

11

/3/2

00

5

1/3

/20

06

3/3

/20

06

5/3

/20

06

7/3

/20

06

9/3

/20

06

11

/3/2

00

6

1/3

/20

07

3/3

/20

07

5/3

/20

07

7/3

/20

07

9/3

/20

07

11

/3/2

00

7

1/3

/20

08

3/3

/20

08

5/3

/20

08

7/3

/20

08

9/3

/20

08

11

/3/2

00

8

1/3

/20

09

3/3

/20

09

5/3

/20

09

7/3

/20

09

9/3

/20

09

11

/3/2

00

9

1/3

/20

10

3/3

/20

10

5/3

/20

10

7/3

/20

10

9/3

/20

10

11

/3/2

01

0

1/3

/20

11

3/3

/20

11

5/3

/20

11

7/3

/20

11

9/3

/20

11

11

/3/2

01

1

1/3

/20

12

S&P 500

IPG

OMC

WPPGY

5/12/00: WPP agrees to

acquire Y&R for $4.7bn

04/16/03: WPP announces

formation of GroupM (media

agency sub-holding company)

09/16/04: WPP agrees to

acquire Grey for $1.5bn

05/06/08: WPP Makes first bid

for TNS for $1.9bn (agrement

followed in August at $2.2bn)

05/17/07: WPP agrees to acquire

24/7 Real Media for $649mm

06/12/02: The WSJ publishes an article

which wrongly implied accounting

irregularities at OMC

07/13/01: IPG forms Magna Global

(media negotiating unit)

08/13/02: IPG announces financial

restatements (for 1997-2002)

mostly due to improperly recorded

inter-company expensed charges

01/19/05: Michael Roth appointed

CEO of IPG, replacing David Bell

10/15/09: IPG announces internal

merger of Lowe with Deutsch

07/09/08: IPG announces

formation of Mediabrands

03/20/01: IPG agrees to acquire

True North (parent of FCB) for

$2.1bn

02/27/03: IPG CEO John Dooner

resigns, replaced by David Bell

07/02/03: IPG's CFO Sean Orr

replaced by Chris Coughlin

07/19/05: Frank Mergenthaler replaces

Robert Thompson as IPG's CFO05/01/08: IPG's Settlement

with SEC announced

06/09/11: IPG returns to investment

grade credit per Moody's

05/15/03: IPG divests research business unit

NFO, selling unit to TNS for $435mm

01/06/04: IPG announces

divestiture of Motorsports unit

06/01/06: IPG announces internal

merger of Draft and FCB

03/23/00: IPG CEO Phil

Geier announces

retirement and

appointment of John

Dooner as

replacement

01/20/10: Nick Brien appointed to replace

John Dooner as CEO at IPG's McCann

Worldgroup

10/16/02 and 11/13/02: IPG

announces further restatements)

09/15/05: IPG announced new

restatement for 2000 through 2004,

including the collection of revenues

from clients associated with AVBs

not explicitly allowed by contract as

well as improper accounting

associated with past acquisitions

06/25/04: CFO Chris Coughlin's

departure announced with appointment

of Robert Thompson to the role

Source: Pivotal Research, Company Reports, Yahoo Finance

IPG, OMC and WPP Trading History+Commentary, 2000-2012. Index = 100 as of 2000

- 24 - Brian Wieser 212-514-4682 Pivotal Research Group

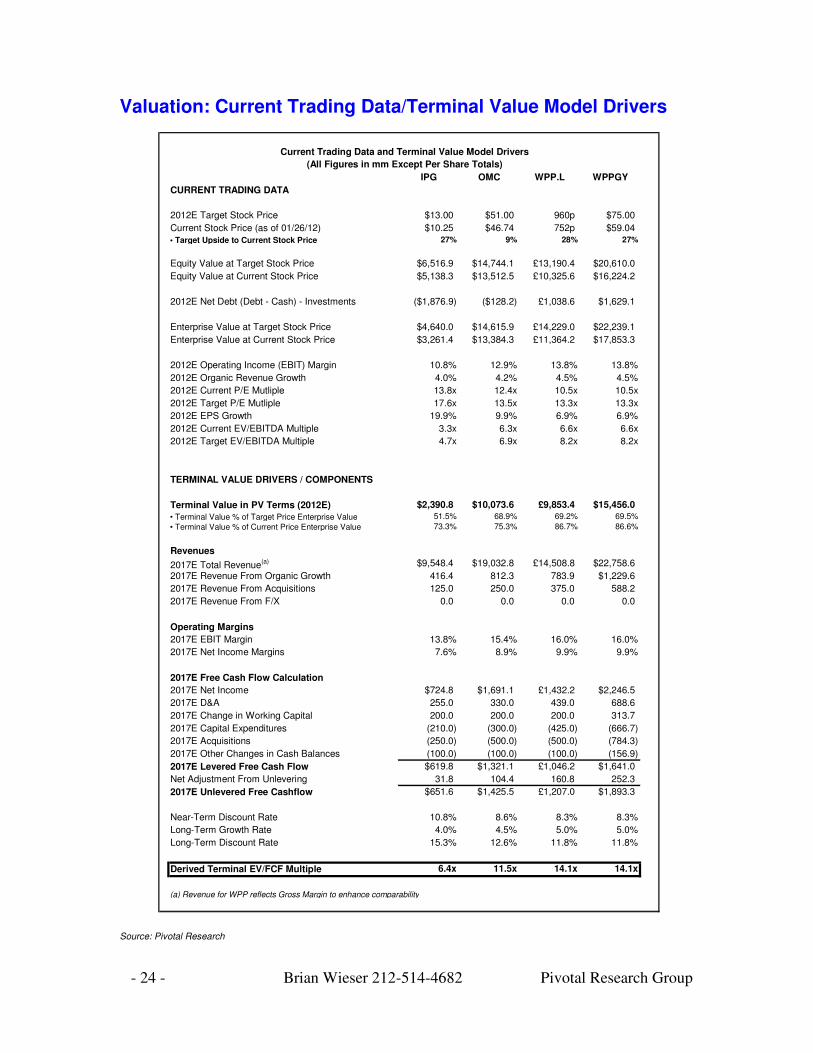

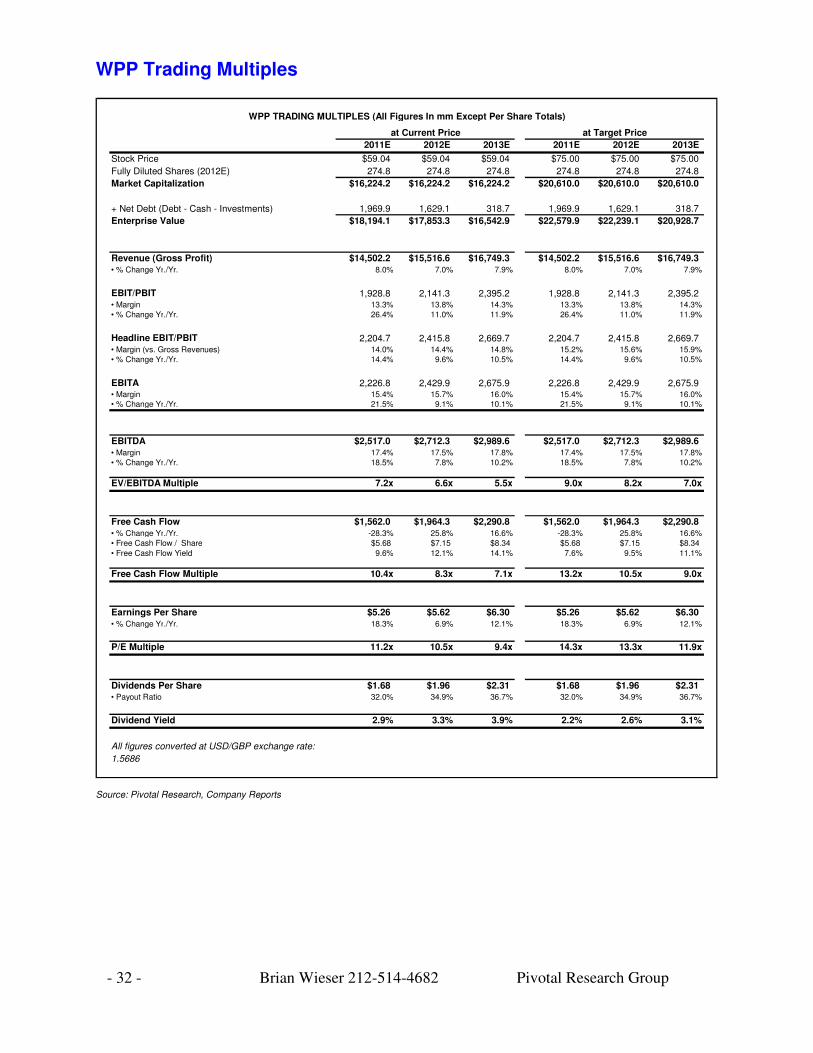

Valuation: Current Trading Data/Terminal Value Model Drivers

Current Trading Data and Terminal Value Model Drivers

(All Figures in mm Except Per Share Totals)

IPG OMC WPP.L WPPGY

CURRENT TRADING DATA

2012E Target Stock Price $13.00 $51.00 960p $75.00

Current Stock Price (as of 01/26/12) $10.25 $46.74 752p $59.04

• Target Upside to Current Stock Price 27% 9% 28% 27%

Equity Value at Target Stock Price $6,516.9 $14,744.1 £13,190.4 $20,610.0

Equity Value at Current Stock Price $5,138.3 $13,512.5 £10,325.6 $16,224.2

2012E Net Debt (Debt - Cash) - Investments ($1,876.9) ($128.2) £1,038.6 $1,629.1

Enterprise Value at Target Stock Price $4,640.0 $14,615.9 £14,229.0 $22,239.1

Enterprise Value at Current Stock Price $3,261.4 $13,384.3 £11,364.2 $17,853.3

2012E Operating Income (EBIT) Margin 10.8% 12.9% 13.8% 13.8%

2012E Organic Revenue Growth 4.0% 4.2% 4.5% 4.5%

2012E Current P/E Mutliple 13.8x 12.4x 10.5x 10.5x

2012E Target P/E Mutliple 17.6x 13.5x 13.3x 13.3x

2012E EPS Growth 19.9% 9.9% 6.9% 6.9%

2012E Current EV/EBITDA Multiple 3.3x 6.3x 6.6x 6.6x

2012E Target EV/EBITDA Multiple 4.7x 6.9x 8.2x 8.2x

TERMINAL VALUE DRIVERS / COMPONENTS

Terminal Value in PV Terms (2012E) $2,390.8 $10,073.6 £9,853.4 $15,456.0

• Terminal Value % of Target Price Enterprise Value 51.5% 68.9% 69.2% 69.5%

• Terminal Value % of Current Price Enterprise Value 73.3% 75.3% 86.7% 86.6%

Revenues

2017E Total Revenue(a) $9,548.4 $19,032.8 £14,508.8 $22,758.6

2017E Revenue From Organic Growth 416.4 812.3 783.9 $1,229.6

2017E Revenue From Acquisitions 125.0 250.0 375.0 588.2

2017E Revenue From F/X 0.0 0.0 0.0 0.0

Operating Margins

2017E EBIT Margin 13.8% 15.4% 16.0% 16.0%

2017E Net Income Margins 7.6% 8.9% 9.9% 9.9%

2017E Free Cash Flow Calculation

2017E Net Income $724.8 $1,691.1 £1,432.2 $2,246.5

2017E D&A 255.0 330.0 439.0 688.6

2017E Change in Working Capital 200.0 200.0 200.0 313.7

2017E Capital Expenditures (210.0) (300.0) (425.0) (666.7)

2017E Acquisitions (250.0) (500.0) (500.0) (784.3)

2017E Other Changes in Cash Balances (100.0) (100.0) (100.0) (156.9)

2017E Levered Free Cash Flow $619.8 $1,321.1 £1,046.2 $1,641.0

Net Adjustment From Unlevering 31.8 104.4 160.8 252.3

2017E Unlevered Free Cashflow $651.6 $1,425.5 £1,207.0 $1,893.3

Near-Term Discount Rate 10.8% 8.6% 8.3% 8.3%

Long-Term Growth Rate 4.0% 4.5% 5.0% 5.0%

Long-Term Discount Rate 15.3% 12.6% 11.8% 11.8%

Derived Terminal EV/FCF Multiple 6.4x 11.5x 14.1x 14.1x

(a) Revenue for WPP reflects Gross Margin to enhance comparability

Source: Pivotal Research

Pivotal Research Group 853 Broadway, Suite 1406 New York, NY 10003

Important Disclosures Are Located In The Appendix

PIVOTAL Pivotal Research Group

U.S. Equity Research Advertising

WPP (WPPGY) Initiating Coverage With BUY Rating and Our Top Pick: Dare to Dream

January 27, 2012

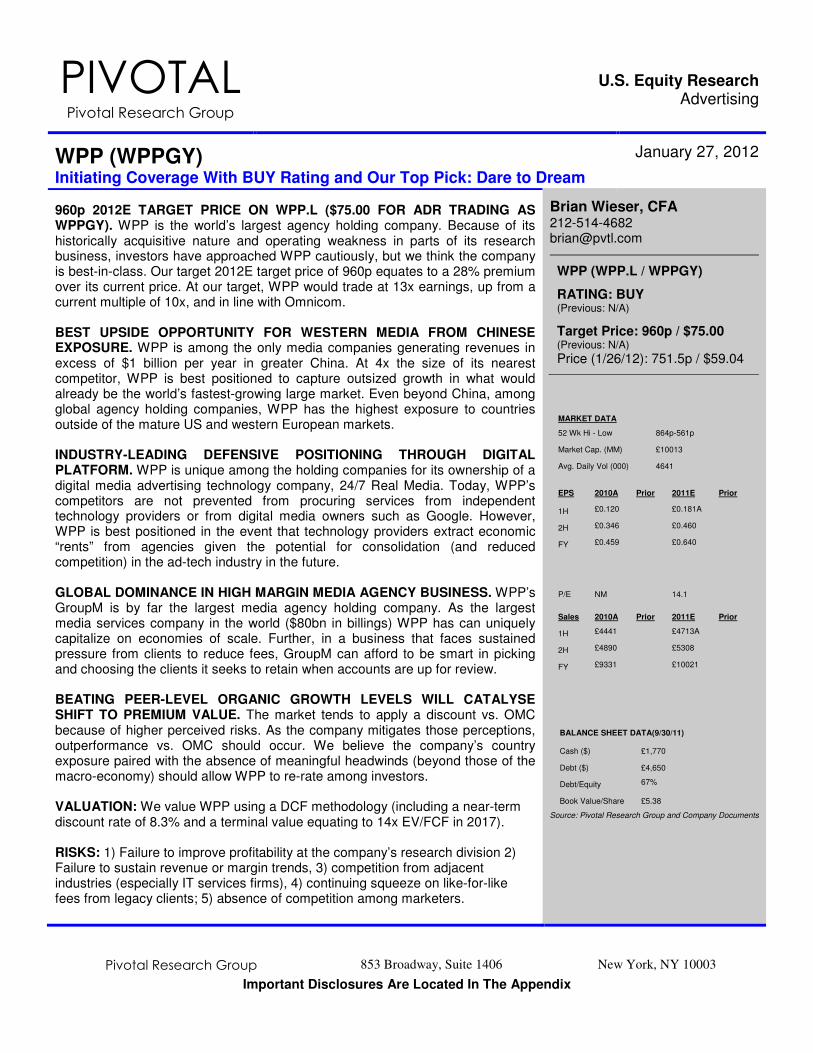

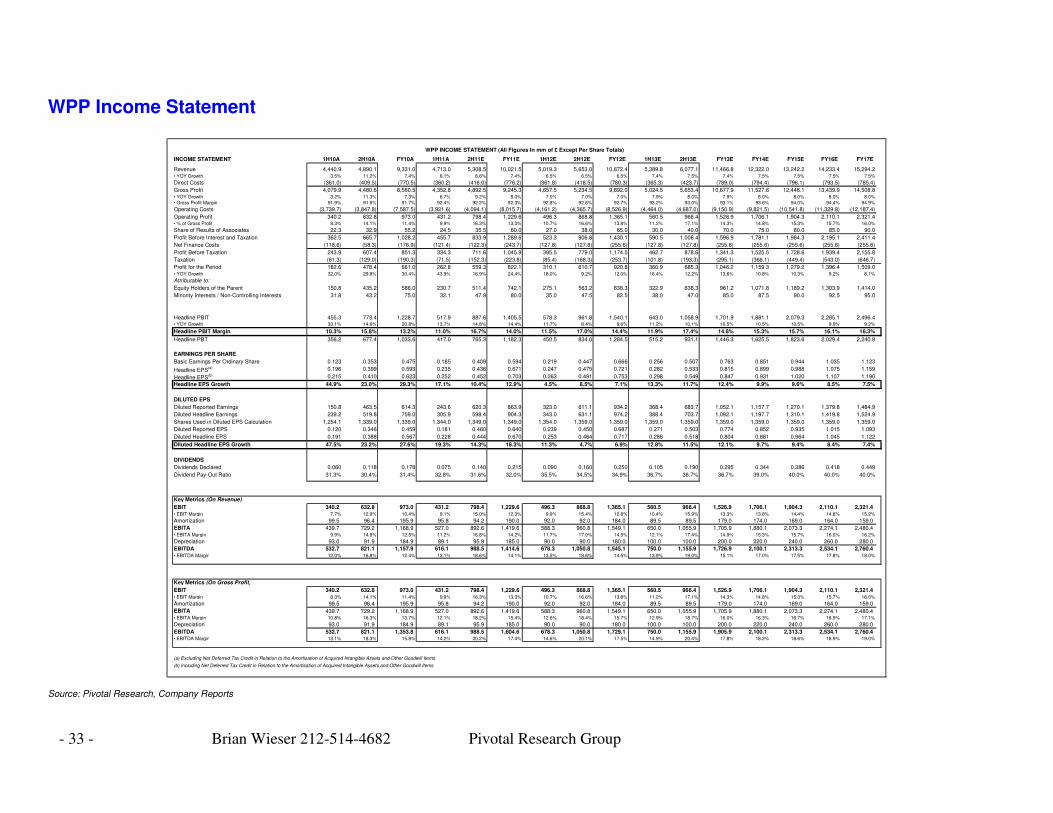

960p 2012E TARGET PRICE ON WPP.L ($75.00 FOR ADR TRADING AS WPPGY). WPP is the world’s largest agency holding company. Because of its historically acquisitive nature and operating weakness in parts of its research business, investors have approached WPP cautiously, but we think the company is best-in-class. Our target 2012E target price of 960p equates to a 28% premium over its current price. At our target, WPP would trade at 13x earnings, up from a current multiple of 10x, and in line with Omnicom. BEST UPSIDE OPPORTUNITY FOR WESTERN MEDIA FROM CHINESE EXPOSURE. WPP is among the only media companies generating revenues in excess of $1 billion per year in greater China. At 4x the size of its nearest competitor, WPP is best positioned to capture outsized growth in what would already be the world’s fastest-growing large market. Even beyond China, among global agency holding companies, WPP has the highest exposure to countries outside of the mature US and western European markets. INDUSTRY-LEADING DEFENSIVE POSITIONING THROUGH DIGITAL PLATFORM. WPP is unique among the holding companies for its ownership of a digital media advertising technology company, 24/7 Real Media. Today, WPP’s competitors are not prevented from procuring services from independent technology providers or from digital media owners such as Google. However, WPP is best positioned in the event that technology providers extract economic “rents” from agencies given the potential for consolidation (and reduced competition) in the ad-tech industry in the future. GLOBAL DOMINANCE IN HIGH MARGIN MEDIA AGENCY BUSINESS. WPP’s GroupM is by far the largest media agency holding company. As the largest media services company in the world ($80bn in billings) WPP has can uniquely capitalize on economies of scale. Further, in a business that faces sustained pressure from clients to reduce fees, GroupM can afford to be smart in picking and choosing the clients it seeks to retain when accounts are up for review. BEATING PEER-LEVEL ORGANIC GROWTH LEVELS WILL CATALYSE SHIFT TO PREMIUM VALUE. The market tends to apply a discount vs. OMC because of higher perceived risks. As the company mitigates those perceptions, outperformance vs. OMC should occur. We believe the company’s country exposure paired with the absence of meaningful headwinds (beyond those of the macro-economy) should allow WPP to re-rate among investors. VALUATION: We value WPP using a DCF methodology (including a near-term discount rate of 8.3% and a terminal value equating to 14x EV/FCF in 2017). RISKS: 1) Failure to improve profitability at the company’s research division 2) Failure to sustain revenue or margin trends, 3) competition from adjacent industries (especially IT services firms), 4) continuing squeeze on like-for-like fees from legacy clients; 5) absence of competition among marketers.

Brian Wieser, CFA 212-514-4682 [email protected]

WPP (WPP.L / WPPGY)

RATING: BUY (Previous: N/A)

Target Price: 960p / $75.00 (Previous: N/A)

Price (1/26/12): 751.5p / $59.04

MARKET DATA

52 Wk Hi - Low 864p-561p

Market Cap. (MM) £10013

Avg. Daily Vol (000) 4641

EPS 2010A Prior 2011E Prior

1H £0.120 £0.181A

2H £0.346 £0.460

FY £0.459 £0.640

P/E NM 14.1

Sales 2010A Prior 2011E Prior

1H £4441 £4713A

2H £4890 £5308

FY £9331 £10021

BALANCE SHEET DATA(9/30/11)

Cash ($) £1,770

Debt ($) £4,650

Debt/Equity 67%

Book Value/Share £5.38

Source: Pivotal Research Group and Company Documents

- 26 - Brian Wieser 212-514-4682 Pivotal Research Group