Embed Size (px)

Citation preview

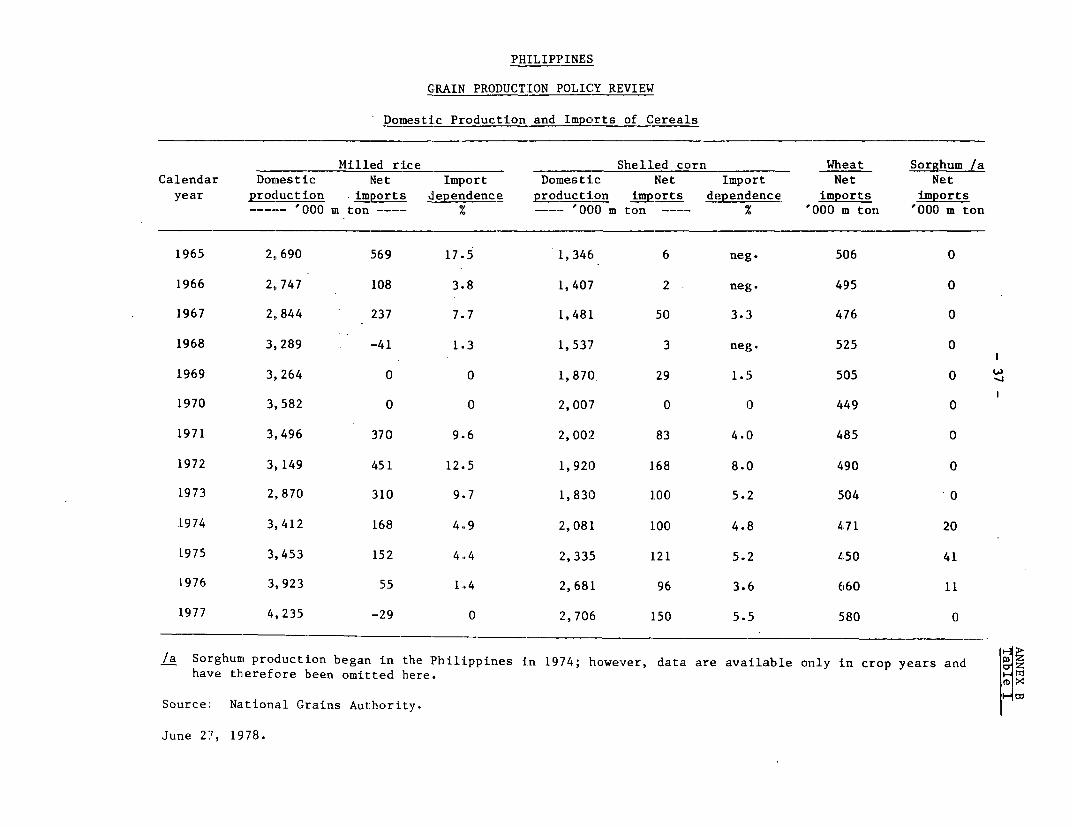

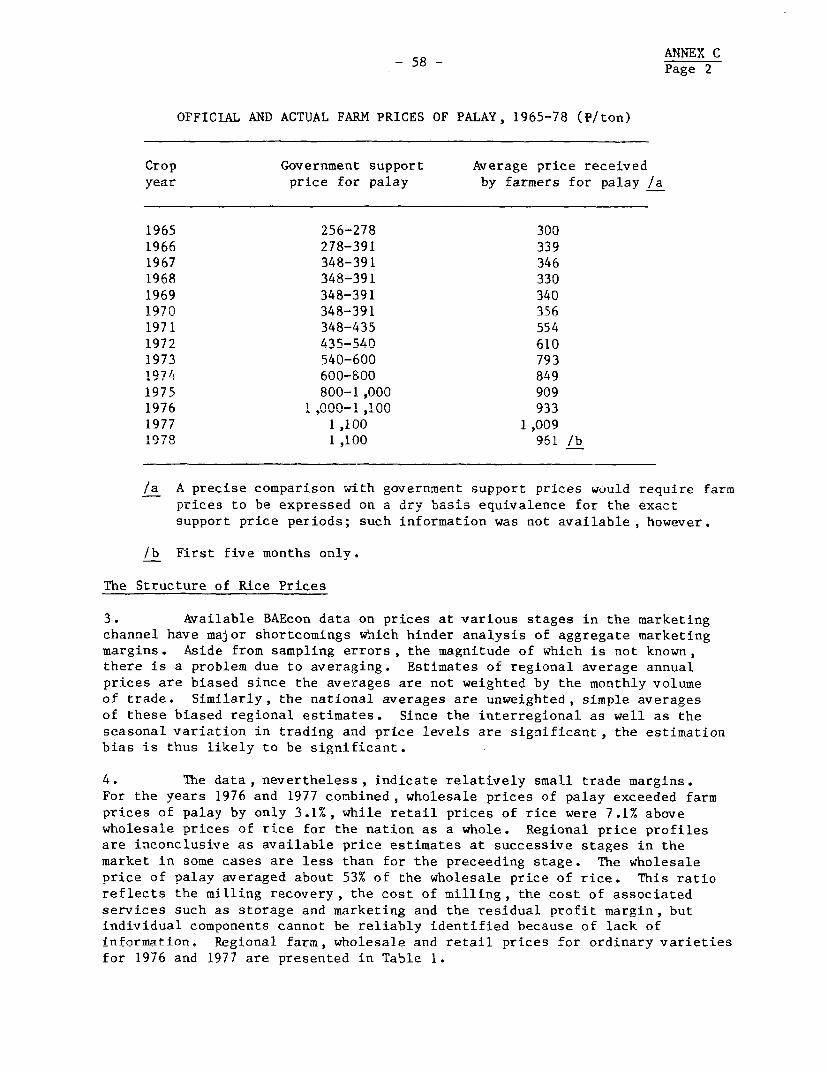

Report No. 2192a-PH

Philippines Sector Study FilE CJOPYC rqrn Dri-'r4i .- ;- De-%1;,-w D1-,x A PGaJ CAII I IProdJuLL1U1I P olic-y RVIeview(in Two Volumes)

Volume II: AnnexesJanuary 22, 1979

Projects DepartmentEast Asia and Pacific Reg,ion

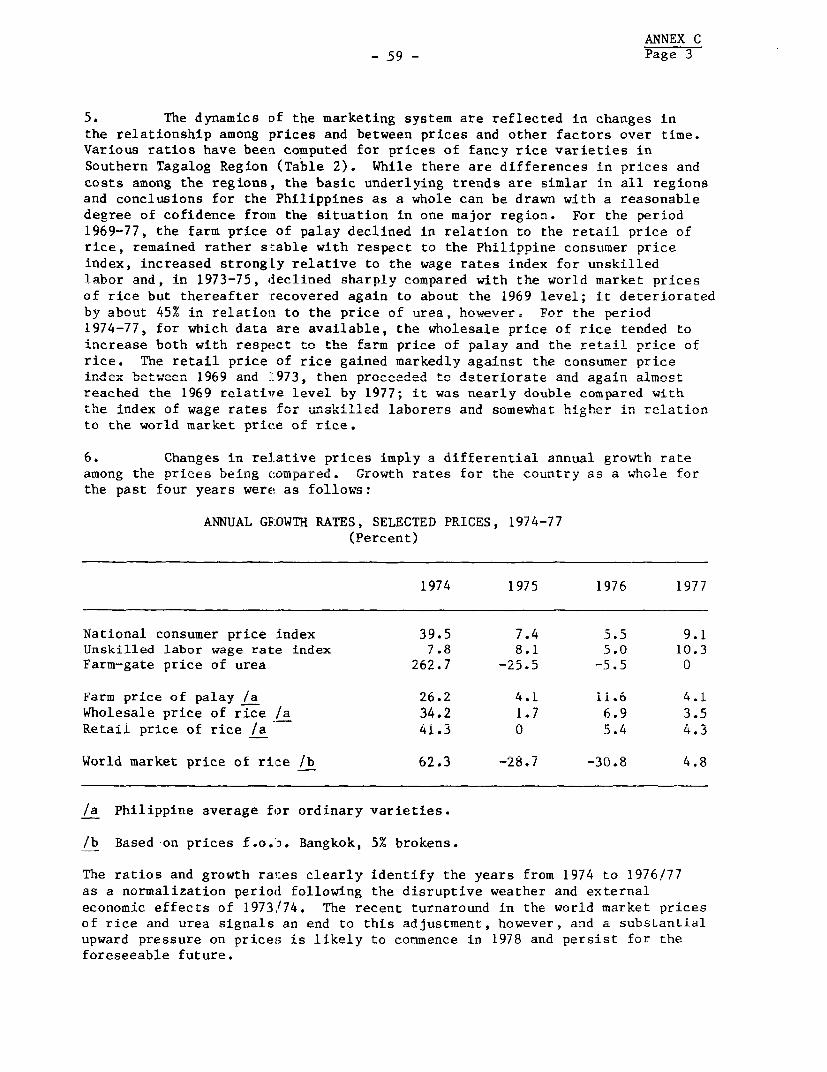

FOR OFFICIAL USE ONLY

D)ocument o6 the World Sauk

I r c J)CUrneni nas S fa sce disribuEtin and may be usea by recipientsonly in the performance of LIhW oVici*l dutesI 13 cortents may nototherwise be disclosed without Wofiisank authonzation.-

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

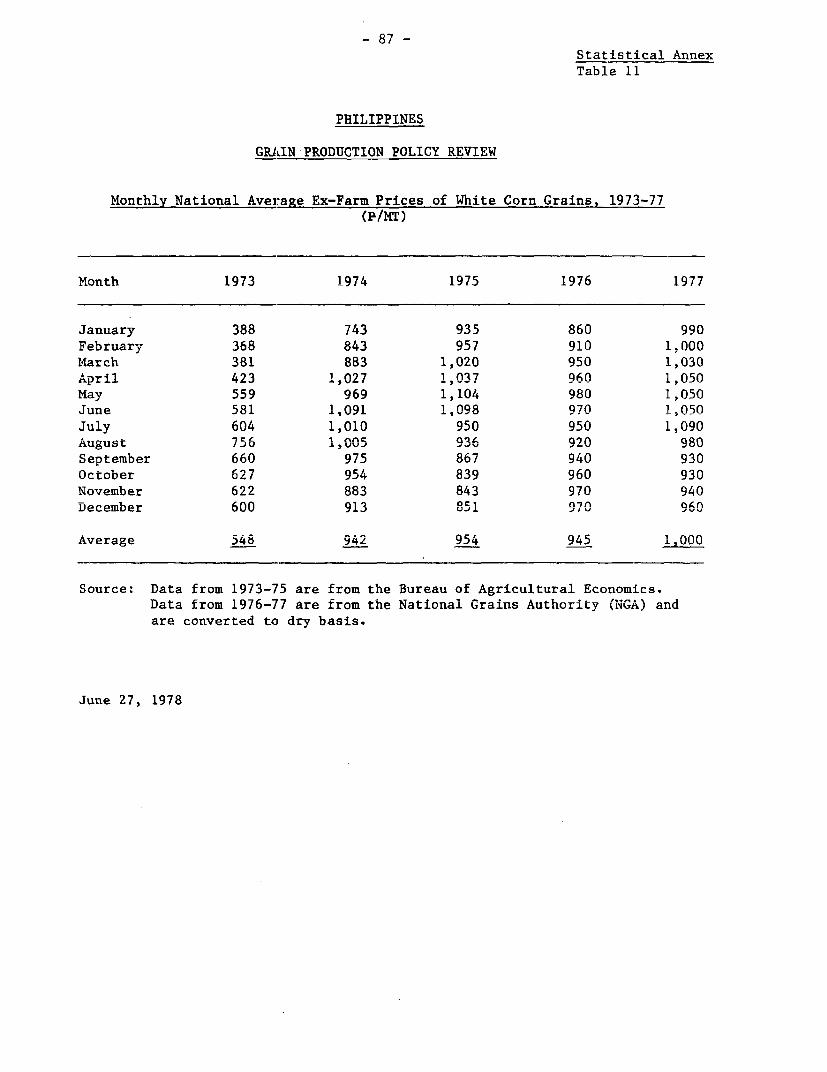

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY AND UNITS

Unit nf cturrency = Peso (P)

US$1.00 = P 7.4P 1=00 = US$0.1351 cavan = 50 kilograms

ADBBRVIATTTAIOTN AND GOTSASCADV11DJJIjj%_V £L4I.V £'.JI t,'LJ4U .IJUOAJ.%L%

BAEcon = Bureau of Agricultural EconomicsTAML - T%--, 44 MIAdew ResistantIJJLL% J~ ~l IflJ.- SA -C%-OLx C .L

FIES = Family Income Expenditure SurveysFNRC = Food andu L'4utrition, Re-search CenterFSDC = Farm Systems Development Corporationniv = 'n.LgLL YiL.LL.ng VCLLiety

IRRI International Rice Research InstitutehMTDDA = Natior,al "conomic and Developmer,t A.uthoity

NFAC National Food and Agriculture CouncilNGA = Ll- Nat'Lonal aGL 1raiLns Authority

NIA = National Irrigation AdministrationPalay U - unmilled riceUPLB University of the Philippines at Los Baffos

Crop Year = July to June

FOR OFFICIAL USE ONLY

PHILIPPINES

SECTOR STUDY

GRAIN PRODUCTION POLICY REVIEW

VOLUME II: ANNEXES

TABLE OF CONTENTS

Page No.

ANNEX A - Technology for Grain Production 1

ANNEX B - The Demand for Grains 23

ANNEX C - Rice: Prices and Market Margins 57

Statistical Annex 76

This document has a restricwd distibution and may be _e by fuciplents only in the performanceI th ; ,4,a,i*.& Iii r'Afttd.IIe g m.s may* not*oteMge he dWIe eItkni Wtrld Rank authnriymtinn(v VIw fl*v w~5bU __ w.w _l ,~* * . _ . _ _ . _ ._.. __ __.

AINNEXA A

-Il - Page 1

PHILIPPINES

GRAIN PRODUCTION POLICY REVIEW

TECHNOLOGY FOR GRAIN PRODUCTION

Part I: Technology Assessment

1. The technology for grain production in the Philippines varieswidely as between rice and the other cereals. On the one hand, by virtue ofthe location of the International Rice Research Institute (IRRI) at Los Baffos,the country has access to the considerable volume of information on riceproduction in the country's most important rice growing area generatedwithin the past two decades. On the other, because of inadequate attentionpaid to national research programs until very recently, improved technologyfor production of corn, the country's second cereal, is lacking./l At thepresent time most corn Earmers in the Philippines do not have access to atechnology package whicah has been proven to be technically or economicallyviable. Nor has there 'been much work of substance on sorghum, the thirdpotentially important cereal.

2. The general weakness of national research services has limitedthe extent to which improved technology for rice production developed atIRRI has been tested and fine tuned under conditions outside the Institute'ssponsored program of trials in the Philippines. In consequene,- whereastrials under simulated :1armers conditions indicate the feasibility of yieldlevels in excess of six tons unmilled rice (nalav) ner ha. farmers utilizingthe recommended package of inputs rarely obtain more than four tons, orsliRhtlv more ner ha. fin the dry senaon u_nder full irrigation, and 3I5 t/haunder rainfed conditions. Further, national yields of palay have increasedat a low rate in recrnt vearo rane-hint an averaaa of 2 9fl s-/kh 4i-rr4--ga anA

1.44 t/ha rainfed in the period 1974/77 which was characterized by generallyQisperinr grnwtang condfttton.s The followIng paragrap- InAicate in moredetail the problems and prospects for improving grain production technologysuitable for exten.sion l:o the fal populaLtor. -vCL LLC periUU LU 1990.

Technnolngy for Ri ce

34. A-alys4's of the componlents of r'ce produotion technology available01 ~ =X ~ li LI. f AUjIJILLOli L .L 1 uut LUL LLiili±~ dVd.±dD±

to Filipino farmers reveals that, whereas about half of the national lowlandrice crop, i.e., irrigat:ed -ar rainfed was plar,ted LU modet varieties \flV)

in 1969/70, this proportion had increased to over 86% of irrigated and 68% ofrailuedu areas uy 1917. .L'LLprjUVementLL couLU Ue mdaUt tU arrarigements tor mului-plication, seed quality control and distribution of improved varieties,currentl may domiLLId Di Jo3, out overall neither the availability nor thequality of planting material are major limiting factors to rice yields.Aualtiouanly, supplies of new varieties aesigned to nave resistance to newstrains of such serious pests and diseases as Brown Plant Hopper and Tungroappear likely to continue to be produced and released by IRKI for subsequentdissemination throughout the period ahead.

/i According to information obtained from government sources in November1978 there has been significant progress recently in selecting a DownyMildew resistant variety and also in developing seed treatments effectiveagainst that disease. This information has not been taken into account inthe evaluation presented in this annex, however.

A V I A.n.NEX a- 2 - Page 2

4. The use of fertilizers and pesticides generally is well belowrecomuienueu levels. A4 natLionafl survey of some 96u farmers w'no obtainedcredit and technical assistance under Phases VII and VIII of the Masaganaprogram indicated that 99% of tneir irrigated farms received fertilizer at arate averaging 4.7 bags (50 kg bag) per ha. Some 92% of their rainfed farmsreceived fertilizer at an average rate of 4 bags per ha. These levelscompare with a typical recommended package of 6 bags per ha, and are unques-tionably above rates applied by the majority of farmers who do not receiveMasagana loans. Survey results are supported by research conducted at anumber of sites in Central Luzon by workers at IRRI in the mid-1970s seekingto establish and isolate the factors constraining yields on farmers' plots.This work has demonstrated that a physical yield gap between average farmers'yields and average maximum attainable yields under farmers' conditionswith presently available technology ranges from one to two tons/ha in thewet season and around two tons/ha in the dry season. About half of thisyield gap is attributable to inadequate rates and inappropriate timing offertilizer application. Insect damage accounted for 30 to 50 percent of thegap, again because of low application rates. Farmers' weed control measuresgenerally are satisfactory.

5. Farmers do not follow the recommended application rates for avariety of reasons. In many cases, the returns do not justify the expenditureas shown in the subsequent part of this section of the report. Also, rela-tively few farmers growing rice do so under conditions which approach theideal water control conditions which tend to be assumed in current technicalpackages. Hence, fertilizer responses are suboptimal and farmers sensiblyreduce their rates of application.

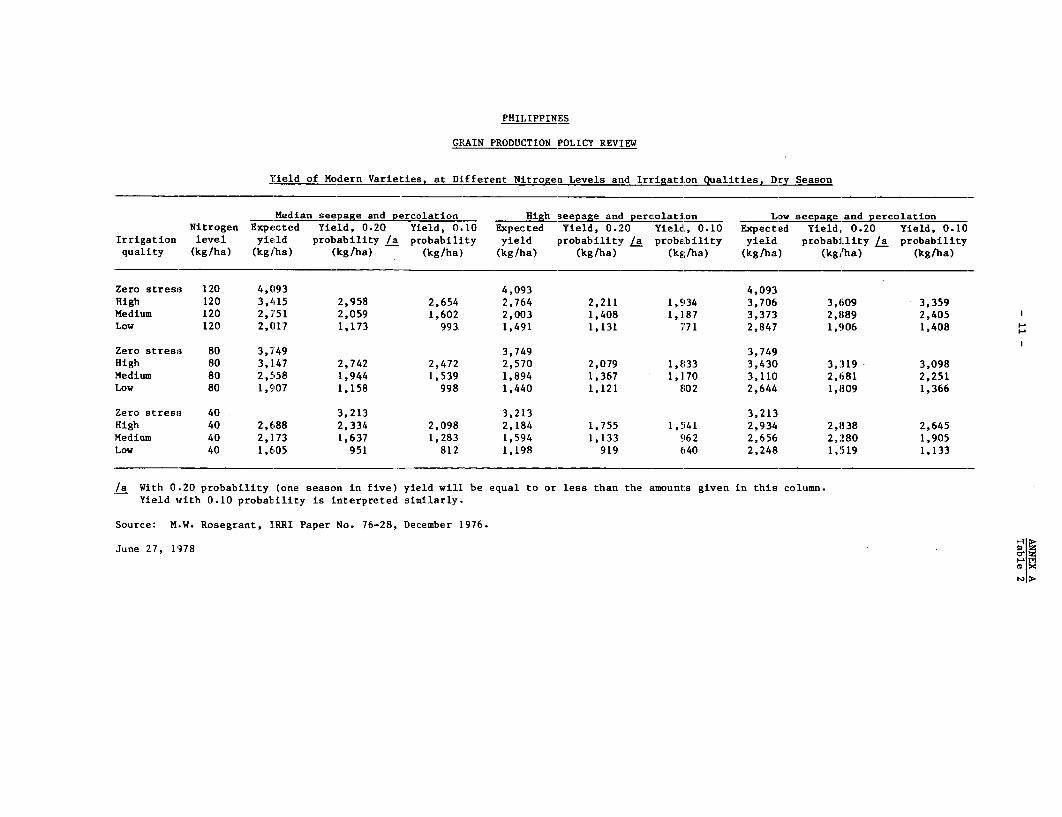

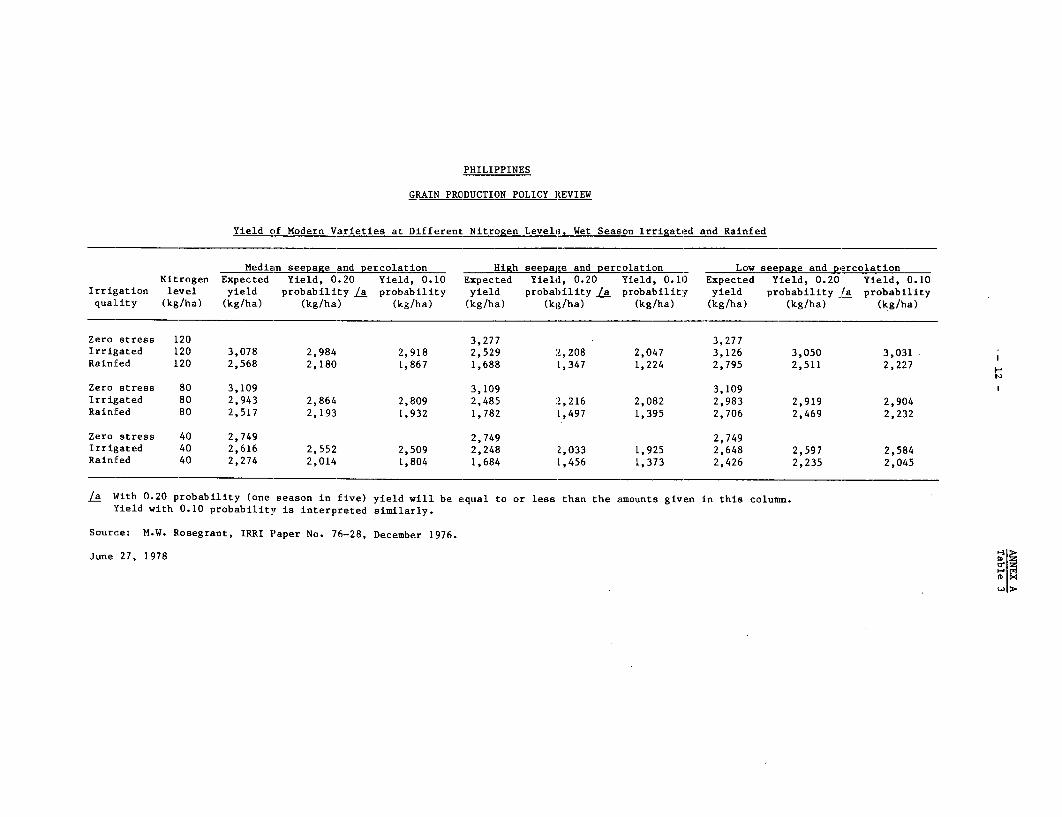

6. Research on the impact of irrigation on the yield of modern varietiesof rice conducted by IRRI worker Mark Rosegrant /1 simulated a large numberof seasons of irrigation flows and rainfall and utilized a water balancemodel to estimate stress day numbers in each season. Because of the largevariation in seepage and percolation rates prevalling tinder field conditionsseparate analyses were made for median, low and high seepage and percolationrates as defined in Annex A. Table 1.

7. Yields of …alay were computed by substituting appropr4ate stresslevels into the seasonal response functions. Results obtained are indicativeof the large yield benefits possible in the dry season from improvements toexisting irrigation systems. Thus, a shift from low quality to mediumquality irrigation at median seepage and percolation cou'ld ue expected togive a yield benefit of 500 kg/ha of palay at an application rate of 40 kgN/ha (about 2 bags of urea). the yield benefit Increased to 750 kg palay/haat an application rate of 120 kg N/ha. A shift from medium to high qualityirrigation gitves similar results. Thus, at median seepage and percolationthe expected yield increment is 500 kg palay/ha at 40 kg N/ha, increasing tomore thLanl 650 kg palay/ha when 10U Kg N/ha is applied (Annex A, Table 2).

/I Rosegrant, M. W.: The Impact of Irrigation on the Yield of ModernVarieties, Paper No. 76-28, December 1976.

ANNEX A- 3 - Page 3

8. As could be anticipated, rice production under high quality irriga-tion is much less risky than under lower quality. At 0.10 probabilityof reduced yields, yields are 800 kg/ha higher at 40 kg N/ha and 1,000 kg/hahigher at 120 kg N/ha. 'Under ideal, zero stress, conditions expected yieldsare 500-600 kg/ha greater than would be obtained under high qualit:y irrigationregardless of the rate oE application of N. The latter assumes a mean of 4.9stress days in the dry season and 9.7 and 15.0 stress days assumed undermedium and low quality irrigation respectively. Under wet season conditions,numbers of stress days vary significantly less between the different qualitiesof irrigation. Numbers of stress days under rainfed conditions range from amean of 16.8 under high seepage and percolation to 5.1 under low seepage andpercolation compared withl 7.9 and 1.6 stress days resnpctively with mediumquality irrigation.

9. The yield beneEits of a shift from rainfed to irrigated farmingare considerable, ranging from about 350 kg palay/ha at 40 kg N/ha to some500 kg/ha at 120 kg N/ha under median seepage and percolation. Irrigation isnartirularly effertive il reducing wet season risk. At 0.10 probability ofreduced yields, yields under irrigation are 700 kg/ha higher than rainfedyields at 40 kg N/ha an1d !,000 kg/tha higher a-t 120 kg Nj/ha (Annex A, 'Ta'kle I)

…~~~~0 N'L. .I~. h. 1 nnna n% AnC

10. The ImplIcatIonls of the foregong for irrigation management areimportant since the analysis shows not only the anticipated high benefitobtair.able from the exte;:io 0f 4rrgtion lo new lar.d if -water 's available,0~ 0Jfl.~J1 J. . L . LIO.J.L L L. LLC .L U Li . L~ L L V ± d i

but also the very large ,iry season yield benefits which could be achieved byimprovement of existing Lrrigatior. systems. Field studies show that highquality irrigation sites are usually on the upstream sections of main canalswhile downLstream siLtes tend to be of lower quality. A basic weakness is lackof intermediate structures. In addition, management programs to prevent theloss of excess water froma high quality sites and to redistribute such waterdownstream would help upgrade these low quality sites and result in someyield benefits. Such programs would be primarily a matter of placement ofappropriately trained wailer management personnel within irrigation systemsand would therefore be much cheaper than infrastructure development. However,in many systems, their use would not be effective without structures neededfor water control. Current estimates for the physical works required for newirrigation construction Ln the Philippines approximate $2,500/ha, and forrehabilitation of physical works some $1,000/ha.

11. Both the National Irrigation Administration (NIA) and the FarmSystems Development Corporation (FSDC) have programs for improving theoperation of existing irrigation schemes through Water Management Technicians.These should be expanded and complement to the extent possible other technicalassistance services proviLded through the Department of Agriculture. It isimportant that both arms of the technical assistance services work togetherin view of the interrelationship between fertilizer response and irrigationquality, and the need to educate most rice farmers of its benefits.

ANNEX A

_ 4 _ Paie 4

12. Ln auuLtion, expanded progams of field trials at local levels

on fertilizer responses, and pest and weed control, are needed to provide the

l.ocation specific information for extension to farmers= Cou-led with nlanned

improvements in delivery systems for technical assistance and supervisedproduction credit the 'orego'ng should result in a substantially more efficientuse of available and developing technology for irrigated rice. Its impact isunlikely to be dramatic on a national scale but it appears not unreasonable topredict a progression from the 2.20 t/ha level of 1974/77 to around 2.55 t/ha

by 1982 and to a yield of some 3.30 thl'a by 1990.

13. Some potential exists for developing technology for nonirrigated

lowland rice in selected areas utilizing direct seeding of short maturing

varieties (102-105 days) planted in May followed by a second rice crop, and

possibly a third, such as mung beans or sorghum, utilizing residual water.

Problems identified in pilot projects to date include harvest and drying of

the first crop at the height of the rains, timely land preparation and

planting of the second and third crops. Experience with drought conditions

in 1977 underlines the importance of careful analysis of historical rainfall

data to identify suitable areas. Also, participants need efficiently organized

credit, input supply and marketing services for successful operation of the

system. It is likely that management systems along these lines will be

perfected and introduced on some scale in the years to come in rainfed

areas such as parts of Western Visayas. However, the overall picture for

rainfed lowland rice is one of declining area, as irrigation development

advances, and of yields increasing slowly at rates approximating recent

historical trends.

14. Upland rice, occupying some 11% of total area planted to the crop,

and grown for the most part in areas badly served by technical and related

delivery mechanisms is unlikely to benefit significantly from technology

advances. New varieties being developed by IRRI will find their way into

these areas and together with limited use of agricultural chemicals will

result in a slow upward trend in yield levels. However, it is unlikely that

the upland rice crop will undergo anything approaching a quantum jump in

productivity in the coming decade and the prospects for improving the level of

vivnfg for upland farm households depends largely on the introduction of

supplementary products into the cultivation pattern. These could well include

corn or sorahum when the technology is better formed.

15. It is impossible to put an accurate figure on the impact of efficient

extension activities on yields, particularly on a crop such as rice for which

the big breakthrough in technology, with the Introduction of modern varieties,

occurred over ten years ago. The key factors now are fine tuning of packages

to suit local conditions, improving the extension delivery to producers, and

monitoring the organization of input and related services so as to deal

effectively w-th farmers. Without services to perform these functions,

farmers' yields would be unlikely to rise over present levels and could well

decline as a result of such factors as pest and disease attack for which

farmers may be unprepared and ill-equipped to overcome.

ANNEX A-5- Page 5

Technology for Corn

16. Philippine farmers grow both white and yellow corn but have atraditional preference for white. Grown under rainfed conditions, generally

on small holdings without recourse to improved planting material or fertilizer

and pest control chemLcals, average yields are among the lowest in Asia.

17. The Philippines does not have a viable technical package for corn

despite its Masagana M4aisan and more recent Maisan 77 production programs.

Evidence to support this contention is provided by their results. Thus,

harvest area under the former dropped from 711,000 ha in Phase I to 254,000 ha

in Phase V with average yields of 1,500 kg/ha of white corn and 1,100 kg/ha of

yellow corn compared with a target of 2,000 kg/ha. The Maisan 77 programlaunched in carefully selected areas with close extension coverage and full

technical and credit support has been similarly disappointing. With 24% of

the program area harvested (27,000 ha) yields averaged 1.400 kg/ha for white

corn and 1,050 kg/ha for yellow (Maisan 77 Sustaining Area Monthly Status

Renort fernember 1977". The declared break-even yield for the technology

package recommended is 2,050 kg/ha.

18. Reasons for this state of affairs are several, however they aredoiminated by the ahserce of improved planting material with sustained toler-

ance to Downy Mildew, an endemic disease throughout all corn growing areas.

Disease impact is such that even mild attacks can halve yields. Additionally,

such improved planting material as is available, for example the DMR seriesproAuceA by the natior,al Tnstitute of Pi-lt Breeding (TIPB), has a yield

potential under good farm conditions including chemical fertilizer and pesti-cid'es ofp no more tha 2,500-3,000 kg-/I, ass- ing freedom From Downy Mildew

attack. Yield potential of this magnitude provides an inadequate return onin-cvestment Lin thLe chemicals and other inputL reedeAu for its realization.

In U _L L - L '~~~A 2.. ..- pr… o.uct-..-.. .-..-- .- Ie g n r

19. Ad-itionat constraLnts to ±LLcreased corrL pructiLViLLy aeth L glL ner

ally sketchy data on fertilizer response. As for rice, few location specificdata are ava4±aule. But until new planting material 1has been developed

it will be impossible to generate such information. Technical information onpest control is reasonably well established ho-wever. Fnaly, because most

corn is grown rainfed, often in scattered small plots, difficult: of access totecnnical assistance staff and input suppliers, it is -unfiLlkely that improvedtechnology when developed will make a rapid impact on producers.

20. The Institute of Plant Breeding plans to produce hybrid Downy Mildew

Resistant (D-M) corns with yielu potentials of aro-ud 7 t/ha by 1979 and istargeting 10 t/ha DMR hybrids by 1982. Work is also continuing on production

of DMK composites with 90-day maturity periods and yields in the 4-5 t/harange. Additionally, two commercial firms with strong technical links to

well known US corn breeding organizations plan to produce and market DIRR

white and yellow corn laybrids by the early 1980's.

21. The structure of corn production and current support services

are such that the case for a large program via hybrids in the near term is

ANNEX A- 6 - Page 6

weak. However, in terms of yield potential, disease resistance and other

desirable qualities such as fertilizer responsiveness and pest tolerance thehybrid route is probably preferable to synthetics. Experience in countries

such as Mexico and Kenya has demonstrated the speed at which small cornproducers have accepted hybrids into their farming systems. Essential

concomitants are intial selection of discrete development areas, adequatetechnical assistance in both number and competence, efficient input andcredit delivery systems and appropriate marketing services.

22. If the foregoing principles are accepted, corn production could beboosted significantly in traditional corn growing areas at a rate directlyrelated to provision of the staff and services required once the technology isin hand. Initial areas for testing techniques miRht be in the CaRavan Valley,

Western Visayas and accessible locations in Mindanao. Further, the use ofcorn as a second or third crop to utilize residual water after rainfed ricehas substantial possibilities in many areas.

23. However, it is unlikely that the Philippines will have viable cornnarkAoR hrforp 1982. Assuming that these are develoDed and subseauentlv

extended to smallholders, their impact on national production will begin tobecome aDparent towards the end of the 1980s. Commercial scale operators willobviously react much more rapidly, but their contribution to national cornnrAdlrctinn is rlat1vv1v qmall.

Technologv for Sorohlm

24. The Department nf Aariculture hns been looking at sorghum as a feed

grain for some years. Area harvested is small and varies widely. Yields andproduction have also seesa,-ed Tiolntl. T- I a new crop in the country;technology is still being developed and refined, and farmers themselves aresti'll fCamiliarizing themselves with 4ts characteristics. Nionetheless Jt has

L.L.A L 1 _Lamttt L A.L II LtIL U CL vC L_LL .L_O .. na L C LLtLO fL ICUIJ.OO .L. ka

many attractive features including drought and flood tolerance, absence ofma orn iUigenu-ub pests and diseuases,I exiLstence of large volUmeUs of hi

yielding germ plasm requiring comparatively minor adaptation trials and, byvirtue of being a new crop, no "fLarmer folk 'Lore" to co,fo-u.d productiLon

recommendations.

25. Its principal potential value is as a second or third crop utilizingresidual moisture and plant nutrients after rice or corn. Under such condi-tions and with minimal fertilizer, yields of over 2 t/ha can be expected fromexisting planting material. Development of high yieiding hybrids by commerciaiinterests, already underway in the south of Mindanao, is likely to result inwell adapted short maturing (70-80 days) material having a 2-3 t/ha yieldpotential under farm conditions and available for wide-scale distribution by1980. Its rate of spread in corn growing areas will be governed, assumingsuch factors as technical support, continued attractive pricing and adequatemarketing facilities for output, by the extent to which farmers can producerequired subsistence corn in their first and/or second crops.

26. As for hybrid corn, the appropriate approach would be to select discreteareas for promotion of the crop providing the full package of services needed to

ANNEX A- 7 - Page 7

develon acceDtance and Dopnularitv with growers. Logically these might initiallybe located in the south oE Mindanao, in areas chosen for development of directlyseeded rainfed rice. such as Darts of Western Visayas and in other locationswhere interest is displayed and production potential has been demonstrated.qiihSuequient upntanPAhl u:ake onnA a w1e scale will be conditionaI on attractiveprice relationships and ef-ficient output marketing arrangements. Given these

conditior.s a*olehear noprogrm rf Irlocal AdtantAtnin trlnals anti the initiaqtion

of cropping systems investigations, it is possible that area planted to sorghumcould increase to 20,000 hta by 1982 and to 75,000 ha by 1990 with avYerage yield

increasing from 2 t/ha in 1982 to 2.5 t/ha by 1990, and production approximating40,000 ton.s by 1982 an.d 1I0,00 tons hy !990=

tcLs I. .LXL. Ja.LLLLxO '.VJ0L0 L IA'.L^ L\C-UJLLA0 X.L V * SV&'.&%.LJ.JI

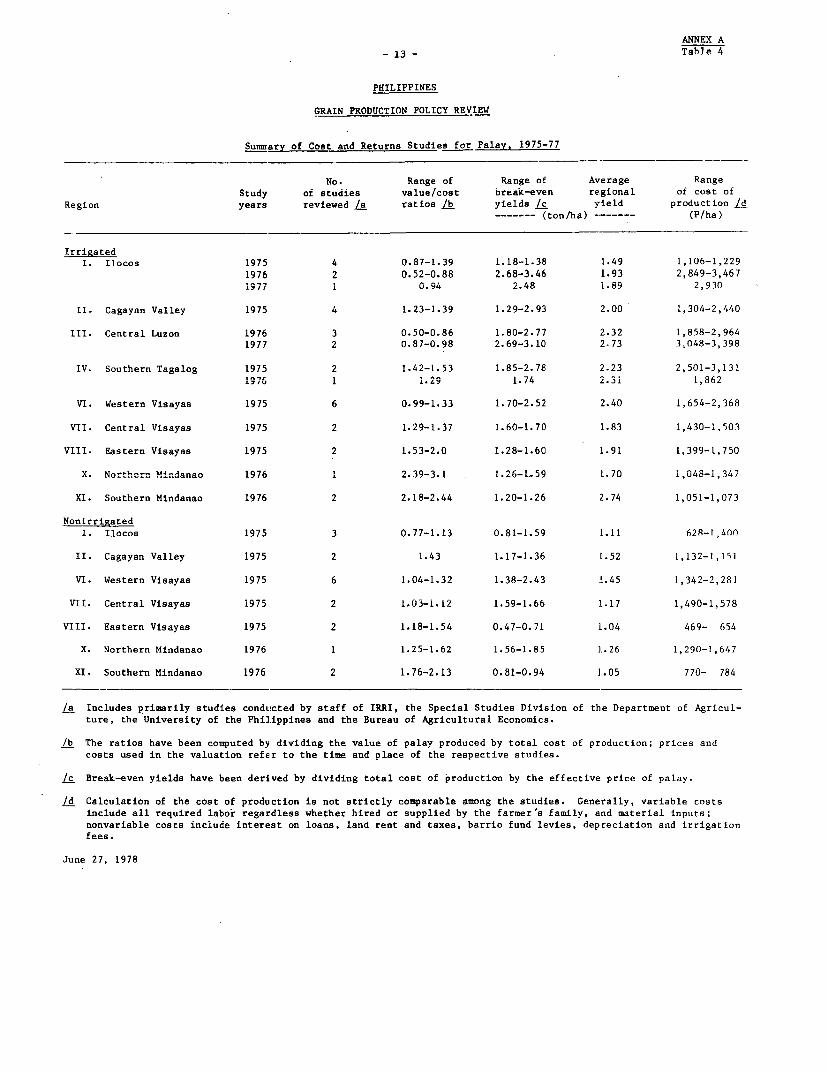

27. A.nexL~' l, abULe 4W -WLLAich su ariLzes costs an.d ret,urns stLudiUes fJor

palay for the years 1975-77 indicates that most farmers operate at low returns,thle notble exceptiLons be.r.g L.LU1eL Von LLLLg±aeLU areas LU &WL LLIL ind

Southern Mindanao. Further, in a number of regions, as in Ilocos, Central.,~~ ~ ~~~ ~ ~ ~ ., t. A -. ., . -_ I A - - - -_- J _ _ _ _ _ _ L J _ L _ -_ Visayas and Northern HindaHnao, nonilrrigaUtd riXe yiLeldbs ar e noUt [high1 U gLUhLl xto

pay back costs.

28. Studies for corri (Annex A, Table 5) show a similar situation, with onaverage only Southern Mindanao indicating adequate returns.

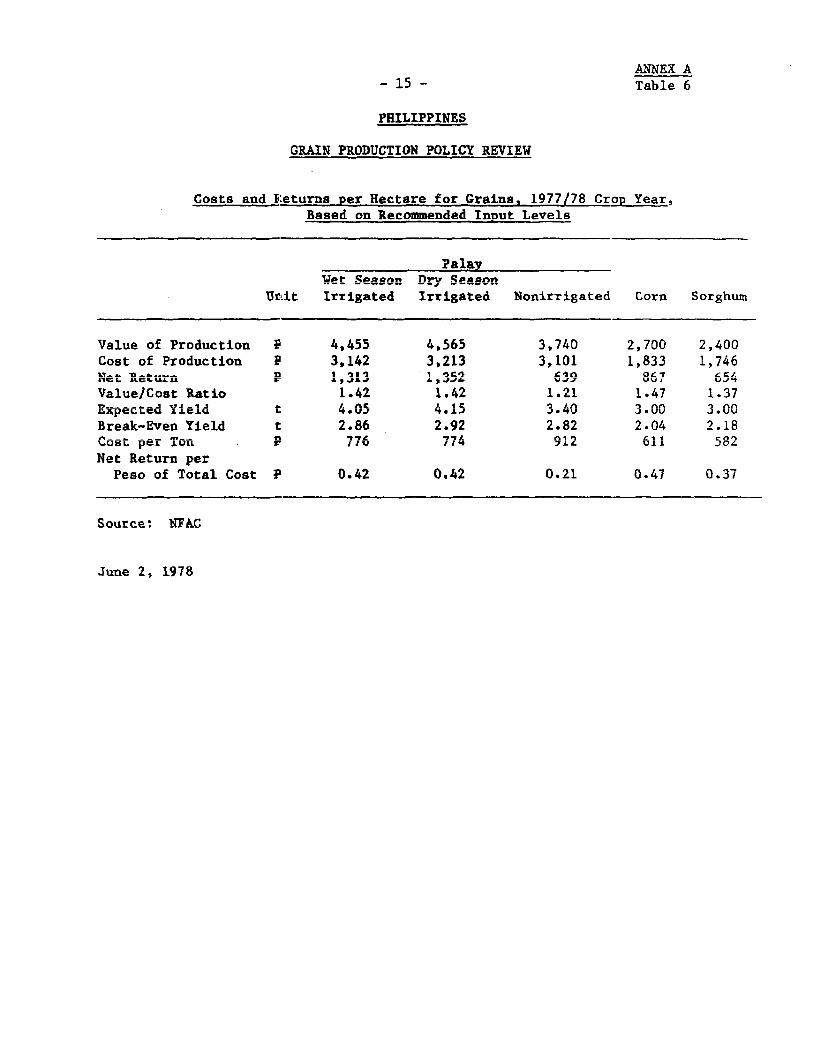

29. Little information is available on the statistical distribution ofpalay and corn farms by level of net income from the respective crops.Since the variation in yields and incomes is known to be large, even withinrelatively small and seemingly homogeneous areas, reported averages concealthe incidence both of failures and of high earners among palay and cornproducers. The National Eood and Agriculture Council (NFAC) has preparedindicative national crop budgets purported to reflect representative cost!return relationships. The budgets were arrived at by applying 1977 prices tothe government recommended package of production technology. A sumnary ofthese budgets appears in Annex A, Table 6.

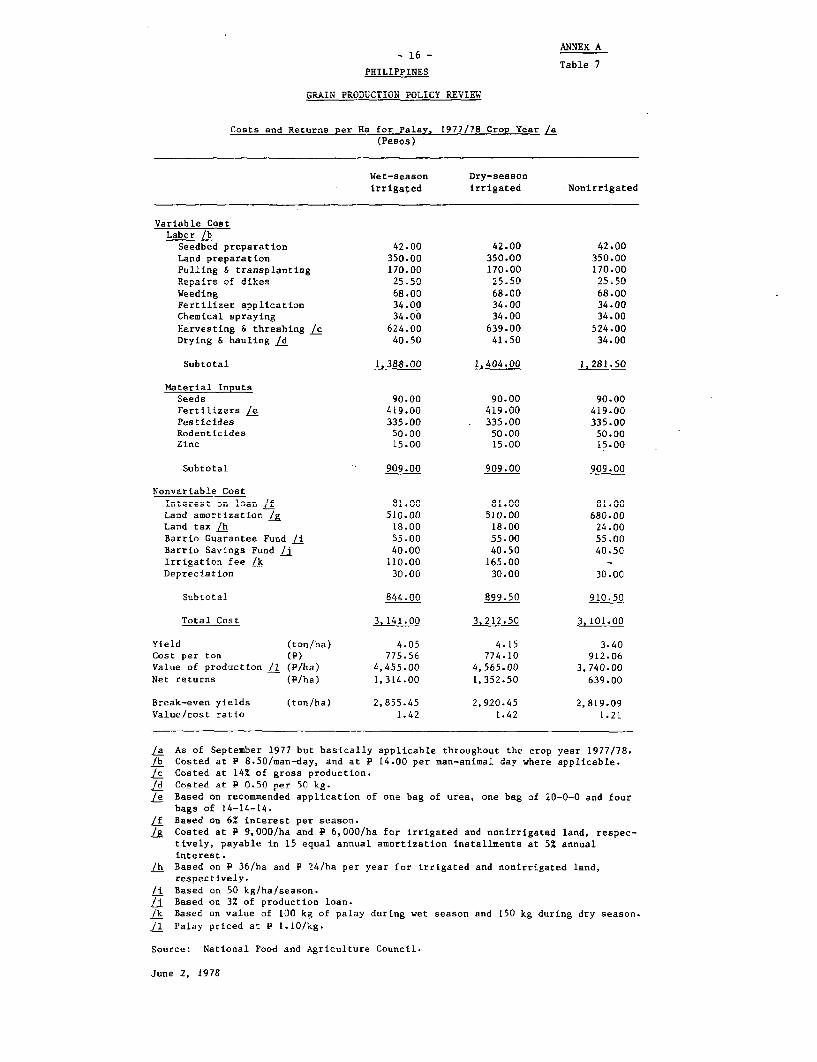

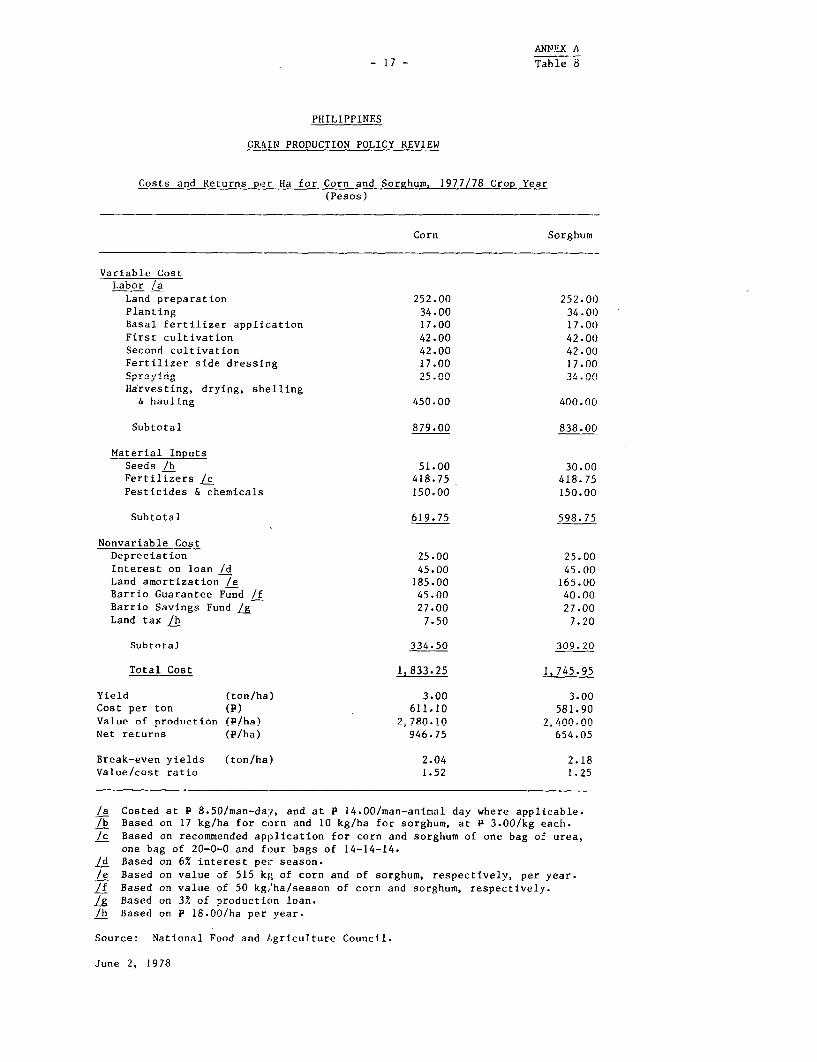

30. The expected yield levels in these budgets, while achievable bysome farmers in certain areas, are far above present national averages forthese crops. Furthermore, costs and prices vary throughout the country whilethe budgets reflect the most favorable combination of these important factors.Since the physical response to the indicated input levels and husbandrypractices is insufficiently known throughout the country, and given thedegree of variability in yields and farm incomes in the sector, the reliabilityand usefulness of aggregate indicative crop budgets is limited. NFAC budgetsare presented in greater detail in Annex A, Table 7 for palay and Table 8 forcorn and sorghum.

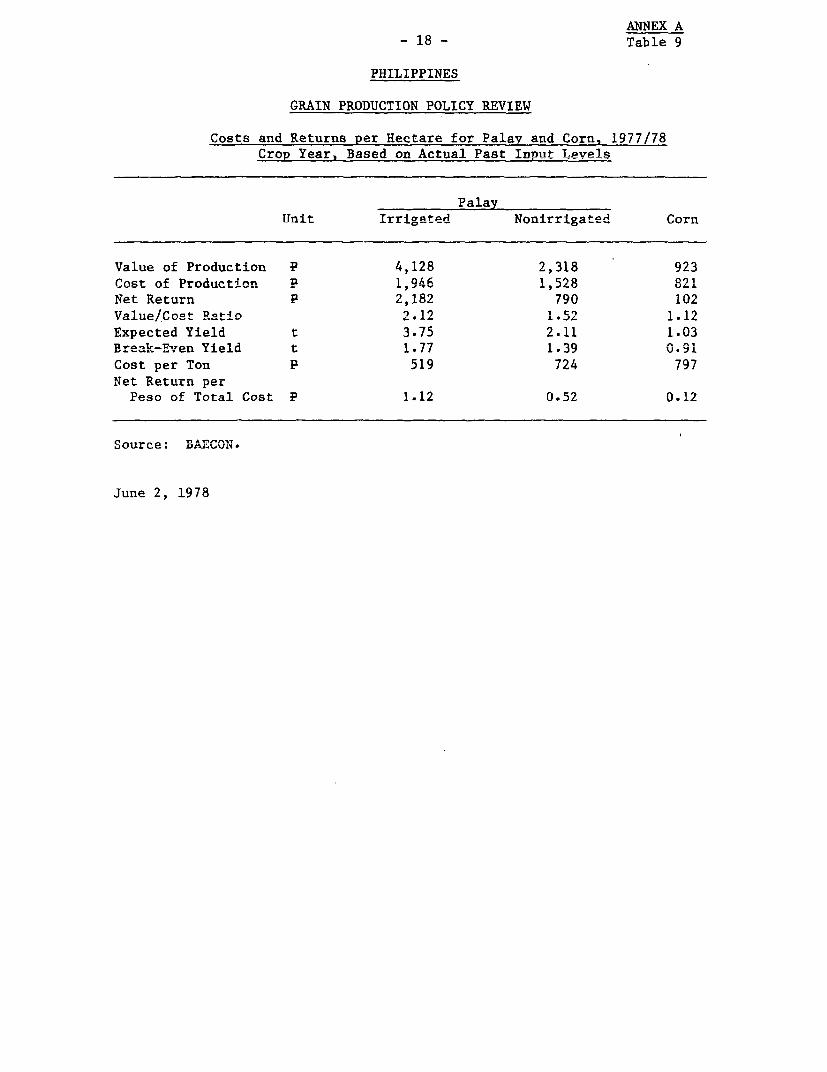

31. An alternative set of crop budgets was prepared by the Bureau ofAgricultural Economics usinag the results of the Bureau's 1974 survey ofphysical inputs costed at 1977 official prices (Annex A, Table 9). While thecost structure of these bulgets seems realistic when compared with survey

AMV.WY A

-8 - Page 8

data obtained from 1975-77, the assumed yield levels also far exceed theUat'LouaL averages, and-h uthe..derlying crop prices are higher t.han actual farmgate prices.

Production Response to Nitrogen and Farm Profitability

32. Because there are high risks of reduced yields and loss of outlaysfor fertilizer associated with grain production in the Phiiippines, incentivesto farmers to pursue advanced technology need to be quite high. In general,this suggests that as a rough rule of thumb, the expected value of incrementalproduction should be about 2.5 times the added costs of fertilizers.

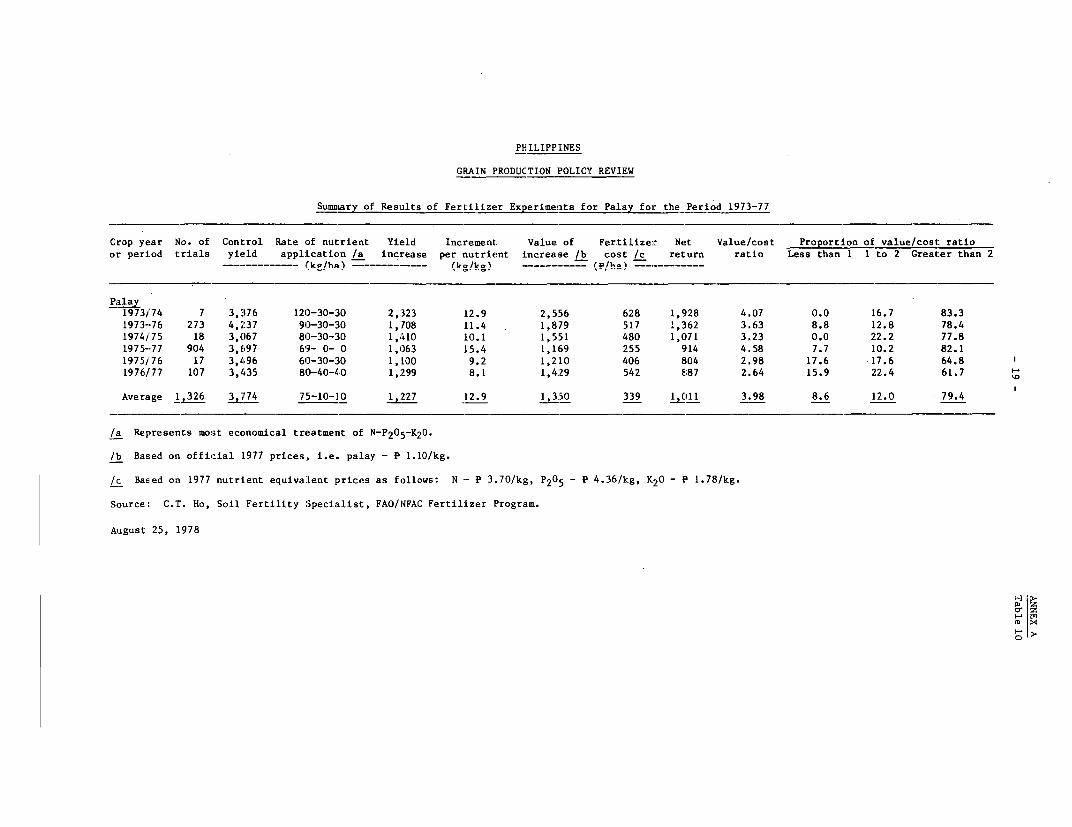

33. Production responses to fertilizer application are being investigatedunder the FAO/NFAC fertilizer program which became operational in 1972 withthe Bureau of Agricultural Extension as the executing agency. Under the program,field trials and demonstrations in farmers' fields had been carried out in morethan 3,000 sites by the end of 1977. The results of 1,326 rice trials aresummarized in Annex A, Table 10./1

34. For palay, on average for experiments in the crop years 1974-77,one kg of plant nutrient brought an increment of 12.9 kg of palay, althoughthe trend was downward, averaging 8.1 in the 1977 crop year. In the latteryear, the increase in value of palay over the cost of fertilizer was 2.64, butalmost 40% of the experiments showed a ratio of less than 2.0. It should benoted that the experimental yields shown are far higher than those obtained inactual farm practices.

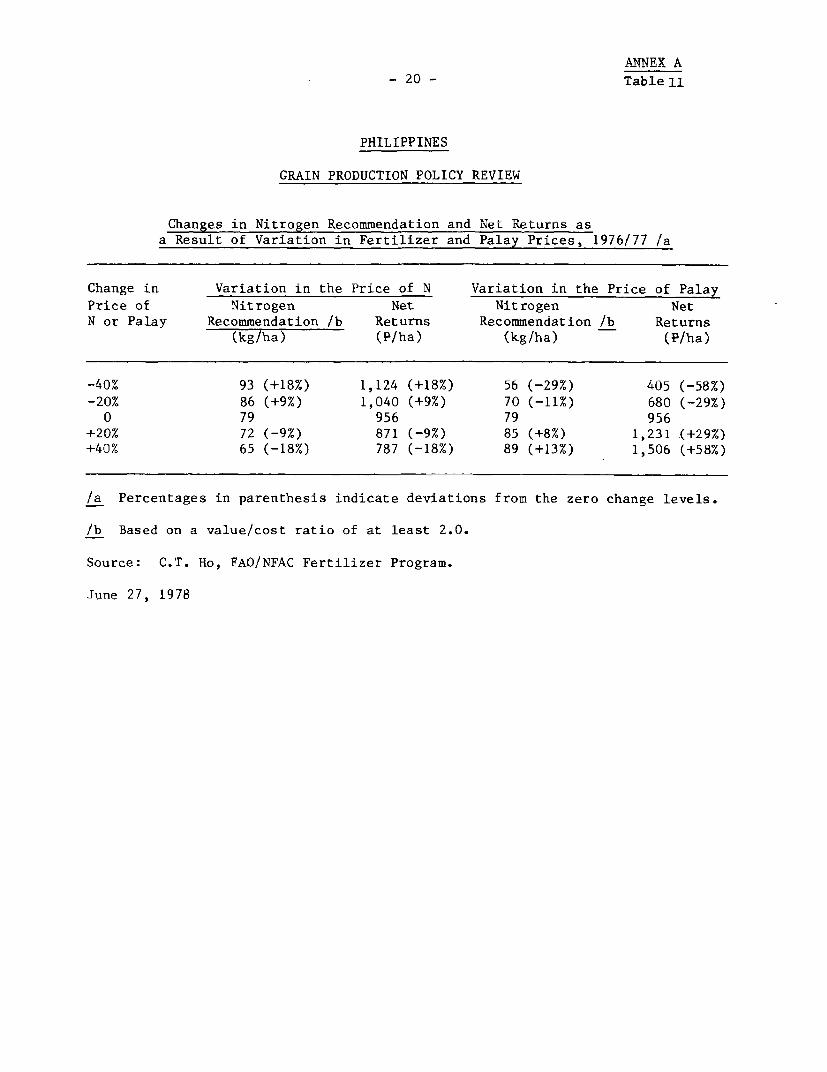

35. Actual profitability is less than indicated in these experimentaltrials since farmers generallv receive prices below the official supportprice. As would be expected, variations in the prices of palay induce greaterrhange8 nliiR or minus in npt rpturns than Asmilar ehanges in the nriePes offertilizers (Annex A, Table 11). This suggests that in improving the grain-fertilizer nrl rrla,tionnQhip, pnrpfprpnrp ho,ltid bp given tn raising grainprices.

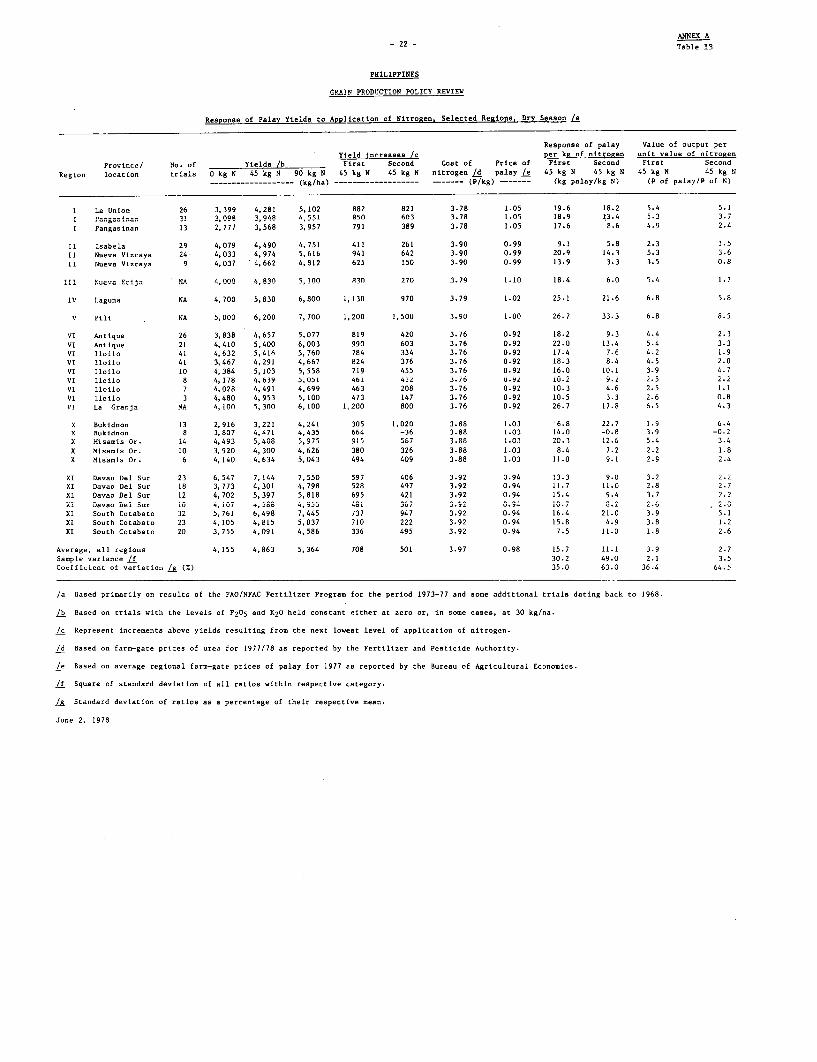

36. In considering the experimental findings above, it should be keptin mindLa t1hatal a.verag ee us L. of f S.,. pala is about 2) bags p er ha (4R kg

N). As shown in Annex A, Tables 12 and 13 for wet and dry season palay, the yieldresponse 'Lrom appLyi.g ar. adLLi.LrjL L. 2bags ol urea 'Ls significantly ess tLan

from the first 2 bags. At current fertilizer-palay price relationships, showniu T-ablie 7 Main Report, it ils uneconomcU tLU appyly aUUddlLtLoal f XL;XErtlizerL unless th eLUt

yield response is at least 9:1. A significant number of the trials listed showresponses below that level. Further, the incremental yields from increasinguse from 2 to 4 bags of fertilizer per ha as simulated by Rosegrant of IRRIfor dry season irrigated land are;

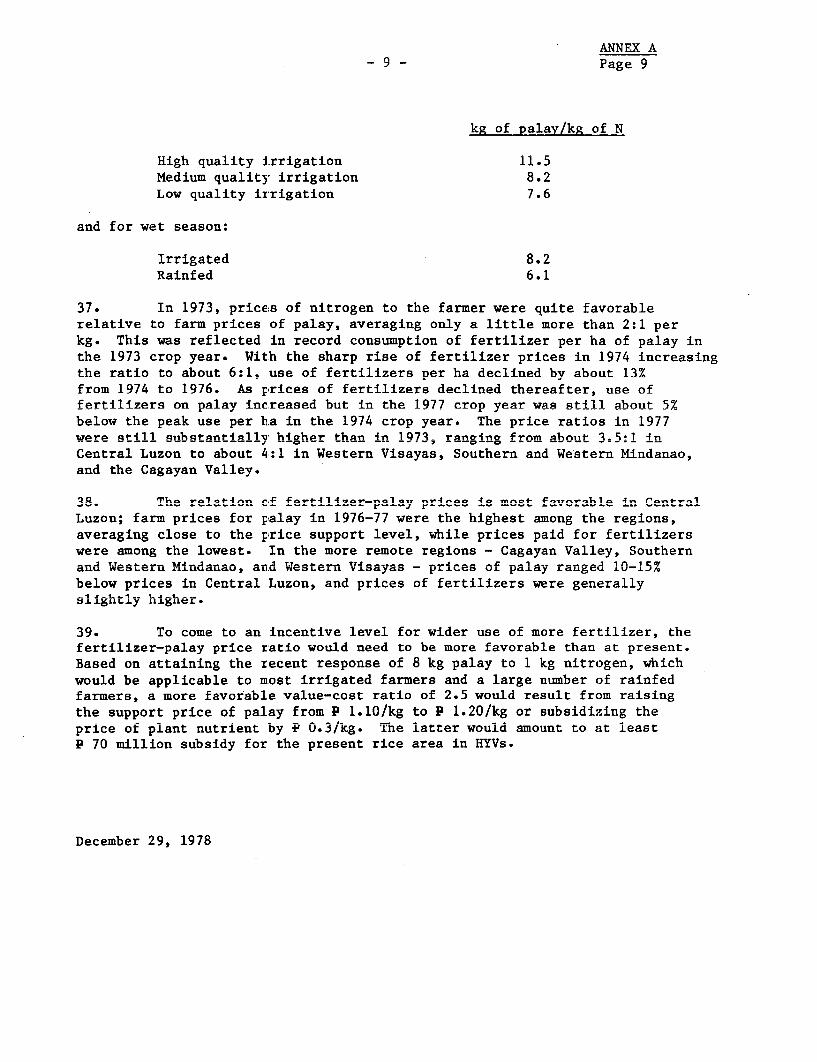

Lt This summary is trom C.T. Ho, economic Return Anailsis of Yieid Data underthe FAO/NFAC Fertilizer Program in the Philippines, Unpublished Paper, 1977.

ANNEX APage 9

kg of palay/kg of N

High quality irrigation 11.5Medium quality irrigation 8.2Low quality irrigation 7.6

and for wet season:

Irrigated 8.2Rainfed 6.1

37. In 1973, prices of nitrogen to the farmer were quite favorablerelative to farm prices of palay, averaging only a little more than 2:1 perkg. This was reflected in record consumption of fertilizer per ha of palay inthe 1973 crop year. With the sharp rise of fertilizer prices in 1974 increasingthe ratio to about 6:1, use of fertilizers per ha declined by about 13%from 1974 to 1976. As prices of fertilizers declined thereafter, use offertilizers on nalav increased but in the 1977 crop year was still about 5%below the peak use per ha in the 1974 crop year. The price ratios in 1977were still substntially h4gher than in 1973, ranging frnm ahniit- 3 in

Central Luzon to about 4:1 in Western Visayas, Southern and Western Mindanao,and the Cagayan Valley=

38. The relation cf fertilizer-palay prices is most favorable in CentralLuzon; farm prices for palay in 1976-77 were the highest among the regions,avreraging cs -- . 1r--n support lev e .4,4 in pr-4ice -4A for ferl-41z4 ers

were among the lowest. In the more remote regions - Cagayan Valley, Southernar.U Wes nLU ir.daLU.aoL, anLdUester LLL Visayas = LL. p e L palay ranLged 10-15%

below prices in Central Luzon, and prices of fertilizers were generallysLighlL.Ly uL ±guLer.

39. To come to an incentive level for wider use of more fertilizer, thefertilizer-palay price ratio would need to be more favorable than at present.Based on attaining the recent response of 8 kg palay to 1 kg nitrogen, wnichwould be applicable to most irrigated farmers and a large number of rainfedfarmers, a more favorable value-cost ratio of 2.5 would result from raisingthe support price of palay from P 1.10/kg to P 1.20/kg or subsidizing theprice of plant nutrient by e 0.3/kg. Tne iatter wouid amount to at ieastP 70 million subsidy for the present rice area in HYVs.

December 29, 1978

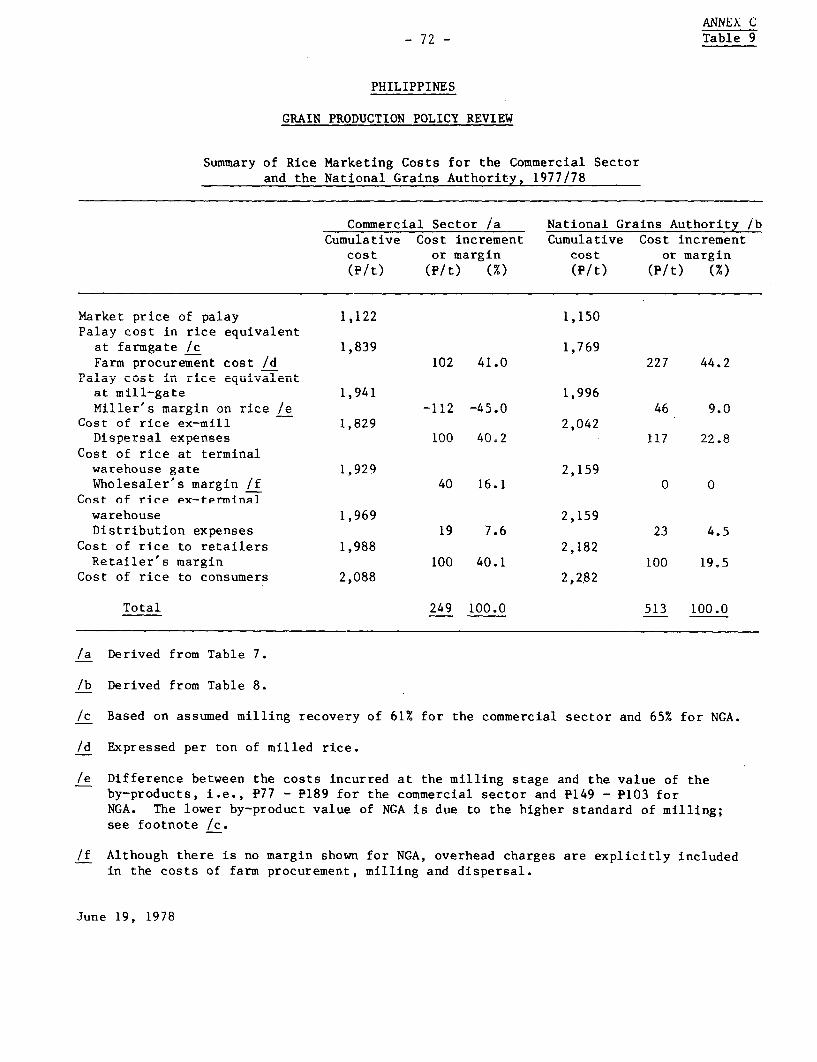

PHILIPPINES

GRAIN PRODUCTION POLICY REVIEW

Distribution of Stress Days Under Dififerent Qualities of Irrigation, 100 Simulated Seasons

Median seepage and percolation l lih seepage and percolation Low seepage ani percolationIrrigation MearL S,tress days, Stress days, MSean Stress days, Stress days, MeaLn Stress dayis, Stress dayEs,

Season qualLty streEss 0.20 0.10 stress 0.20 0.10 stress 0.20 O.]LOdays probability /a probability days probability /a. probability days probability /a probability

Dry lLigh 4.5' 8.2 10.4 9.6 13.6 15.6 2.6 3.5 5.3

Dry MSedium 9.7 14.7 18.0 15.1 19.4 21.0 5.2 8.7 12.2C)

Dry Low 15.0 21.1 22.4 18.8 21.4 24.0 9.0 15.8 19.4

Wet High 1.cl 2.5 3.1 4.7 7.3 9.1 1.5 2.3 2.4

Wet lSedium 2.1 3.1 3.8 7.9 11.3 13.0 1.6 2.4 2.6

Wet Low 2.2 3.4 4.3 9.9 13.7 15.4 1.8 2.5 3.2

Wet Rainfed 7.5 11.6 14.9 16.8 20.4 Z1.7 5.1 8.1 11.1

/a With 0.20 probability (one season in five) the number of streEss days will be equal to or greater than the number of stress daysgiven in this ccolumn. Stress days with 0.10 probabiLlity is interpreted similarly.

Source: M.W. Rosegrant, IRRI Paper No. 76-28, December 1976,.

June 27, L978

PHILIPPINES

GRAIN P'RODUCTION POLIC'Y REV'IEW

Yield of Modern Varieties, at Different Nitrogen Levels and Irrigation Qualities, Dry Season

Median seepage and percolation High seepag%e andI percolation Lw SeePae and iercolationNitrogen Expected Yield, 0.20 Yield, 0.10 Expected Yield, 0.20 Yield., 0.10 Expected Yield,, 0.20 Y'ield, 0.10

Irrigation level yield probability /a probability yield probability /a probaLbility yield probabi lity /aL probabilityquality (kg/ha) (kg/'ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha)

Zero stress 120 4,093 4,093 4,093High 120 3,415 2,958 2,654 2,764 2,211 1,934 3,706 3,609 3,359Medium 120 2,751 2,059 1,602 2,003 1,408 1,187 3,373 2,889 2,405Low 120 2,017 1,173 993 1,491 1,131 771 2,847 1,906 1,408

Zero stress 80 3,749 3,749 3,749High 130 3,147 2,742 2,472 2,570 2,079 1,833 3,430 3,319 3,098Medium 80 2,558 1,944 13,539 1,894 1,367 1,170 3,110 2,681 2,251Low 130 1,5107 1,158 998 1,440 1,121 802 2,644 1,1309 1,366

Zero stress 40 3,213 3,213 3,213High 40 2,688 2,334 2,098 2,184 1,755 1,541 2,934 2,838 2,645IMedium 40 2,173 1,637 1,283 1,594 1,133 962 2,656 2,280 1,905Low 40 1,605 951 812 1,198 919 6 40 2,248 1,519 1,133

/a With 0.20 probability (one season in five) yield will be equal to or less than the amounts given in this column.Yield with 0.10 probability is interpreted similarly.

Source: M.W. Rosegrant, IRRI P'aper No. 76-28, December 1976.

June 27, 1978

a1 D

PHILIPPINE S

GRAIN PRCDUCTION POLICY REVIEW

Y:Leld of Modern Varieties at Difi.erent Nitrogen Levels, Wet: Season IrriRated and Rain,fed

Median seepage and percolation _High seepaite andl percolation _ Low seepaRge and percolationNitrogen Expected Yield, 0.20 Yie:Ld, 0.10 Expected Yield, 0.20 Yield, 0.10 Expected Yield, 0.20 YiLeld, 0.10

Irrigation level yield probability /a probabiliLty yield probability /a probability yield probability ,a probabilityquality (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha) (kg/ha)

Zero stress 120 3,277 3,277Irrigated 120 3,ti78 2,984 :2,918 2,529 2,208 2,047 :3,126 3,050 3,031Rainfed 120 2,568 2,180 L,867 1,688 1,347 1,224 .2,795 2,511 2,227

Zero stress 80 3,109 3,109 :3,109Irrigated 80 2,'343 2,864 2,809 2,485 2,216 2,082 2,983 2,919 2,904RainfEed 80 2,517 2,193 L,932 1,782 L,497 1,395 2,706 2,469 2,232

Zero stresis 40 2,749 2,749 2,749Irrigated 40 2, 616 2,552 '2,509 2,248 :2,033 1,925 2,648 2,597 2,5834RainfEed 40 2,274 2,014 L,804 1,684 L,456 1,373 2,426 2,235 2,045

/a With 0.20 probability (one season in five) yield will be equal to or less than the amounts given in this column.Yield with 0.10 probability is interpreted similarly.

Source: M.W. Rosegrant, IRRI Paper No. 76-28, December :1976.

June 27, 1.978

(D X4u-. >1

ANNEX A

-13- Table 4

PHILIPPINES

GRAIN PRODUCTION POLICY REVIEW

Sumnary of Cost and Returns Studies for Palay, 1975-77

No. Range of Range of Average RangeStudy of studies value/cost break-even regional of cost of

Region years reviewed /a ratios /b yields /c yield production /d------- (ton/ha) ------- (P/ha)

IrrieatedI. Ilocos 1975 4 0.87-1.39 1.18-1.38 1.49 1,106-1,229

1976 2 0.52-0.88 2.68-3.46 1.93 2,849-3,4671977 i 0.94 2.48 1.89 2,930

II. Cagayan Valley 1975 4 1.23-1.39 1.29-2.93 2.00 1,304-2,440

III. Central Luzon 1976 3 0.50-0.86 1.80-2.77 2.32 1,858-2,9641977 2 0.87-0.98 2.69-3.10 2.73 3,048-3,398

IV. Southern Tagalog 1975 2 1.42-1.53 1.85-2.78 2.23 2,501-3,1311976 1 1.29 1.74 2.31 1,862

VI. Western Visayas 1975 6 0.99-1.33 1.70-2.52 2.40 1,654-2,368

VII. Central Visayas 1975 2 1.29-1.37 1.60-1.70 1.83 1,430-1,503

VIII. Eastern Visayas 1975 2 1.53-2.0 1.28-1.60 1.91 1,399-1,750

Xa Northern Mindanao 1976 1 2.39-3.1 1.26-1.59 .70 1,048-1,347

XI. Southern Mindanao 1976 2 2.18-2.44 1.20-1.26 2.74 1,051-1,073

NonirrigatedI. Ilocos 1975 3 0.77-1.13 0.81-1.59 1.11 628-1,400

II. Cagayan Valley 1975 2 1.43 1.17-1.36 [.52 1,132-1,151

VI. Western Visayas 1975 6 1.04-1.32 1.38-2.43 1.45 1,342-2,281

'vlI. Central Visayas 1975 2 1.03-1.12 1.59-1.66 1.17 1,490-1,578

VIII. Eastern Visayas 1975 2 1.18-1.54 0.47-0.71 1.04 469- 654

X. Northern Mindanao 1976 1 1.25-1.62 1.56-1.85 1.26 1,290-1,647

XI. Southern Mindanao 1976 2 1.76-2.13 0.81-0.94 ].05 770- 784

/a Includes primarily studies conducted by staff of IRRI, the Special Studies Division of the Department of Agricul-ture, the University of the Philippines and the Bureau of Agricultural Economics.

/b The ratios have been computed by dividing the value of palay produced by total cost of production; prices andcosts used in the valuation refer to the time and place of the respective studies.

/c Break-even yields have been derived by dividing total cost of production by the effective price of palay.

/d Calculation of the cost of production is not strictly comparable among the studies. Generally, variable costsinclude all required labor regardless whether hired or supplied by the farmer's family, and material inputs;nonvariable costs include interest on loans, land rent and taxes, barrio fund levies, depreciation and irrigationfees.

June 27, 1978

PHILIPPINES

GRAIN PRODUCT]ION POLICY RE'VIEW

Summary of Cost and Returns Studies for Corn, 1975-77

No. Range of Range of ALverage Range

Study of studies value/cost break-even regional of cost of

Region years reviewed /a ratios /b yields /C yield production /d(ton/ha) -------- (P/ha)

I. Ilocos 1975 2 1.1.3-1.43 0.47-0.81 0.50 :377- 628

1976 2 0.51-1.13 0.58-1.58 0.50 436-1,595

1977 1 0.88 0.99 0.'56 1,078

II. Cagayan Val:Ley 1975 3 0.33-1.25 0.78-0.94 0. 80 783- 940

III. Central Luzon 1976 1 0.90 1.06 0.64 877

1977 1 0.62 0.57 0.7i1 504

VI. Western Visayas 1975 4 0.47-1.39 0.62-1.42 0.64 489-1, 316

VII. Central Visayas 1975 2 1.06-2.65 0.37-0.72 0.5iO 362- 71CI

XI. Southern Mindanao 1976 3 1.91-2.08 0.59-0.70 1.33 447- 548

/a Includes primarily studlies conducted by staf f of IRRI, the Special Studies Division of the Department of Agricul-

tLure, the University of the Philipp-ines and the Bureau of- Agricultural Economics.

/b Tlhe ratios have been computed by dividing the value of palay produced by total. cost of production; prices and

costs used in the valuation refer to the tirrie and place of the respective studlies.

/c_ Break-even yields have been derived by dlividing total cost of production by the effective price of palay.

/d Calculation of the cost of production is not strictly comparable among the studies. Generally, variable costs

include all required labor regardless whether hired Dr supplied by thle farmer's family, andi material inputs; ra x

nonvariable costs include interest on loans, land rent and taxes, barrio fund levies, depreciation and irrigation n >

fees .

June 2, 1978

ANNEX A-15 - Table 6

PHILIPPINES

GRAIN PRODUCTION POLICY REVIEW

Costs and Returns per Hectare for Grains, 1977/78 Crop Year,Based on Recommended Innut Levels

T!JPt 5A,M 1n Pv Sna

Ur3it Irrigated Irrigated Nonirrigated Corn Sorghum

Valu e of Poductio n A, , 4 5R n 4,56 3 0 27

Cost of Production P 3,142 3,213 3,101 1,833 1,746£LII L%=4LU.L" J. UUf UJ"t

Value/Cost Ratio 1.42 1.42 1.21 1.47 1.37apected Yield : 4.0~ ~ ~~~~ ~ ~~~~5 4.' 34 30 30

Break-Even Yield t 2.86 2.92 2.82 2.04 2.18Cost per Ton I 776 774 912 611 582Net Return per

Peso of Total Cost P 0.42 0.42 0.21 0.47 0.37

Source: NFAC

June 2, 1978

ANNEX A-16 -

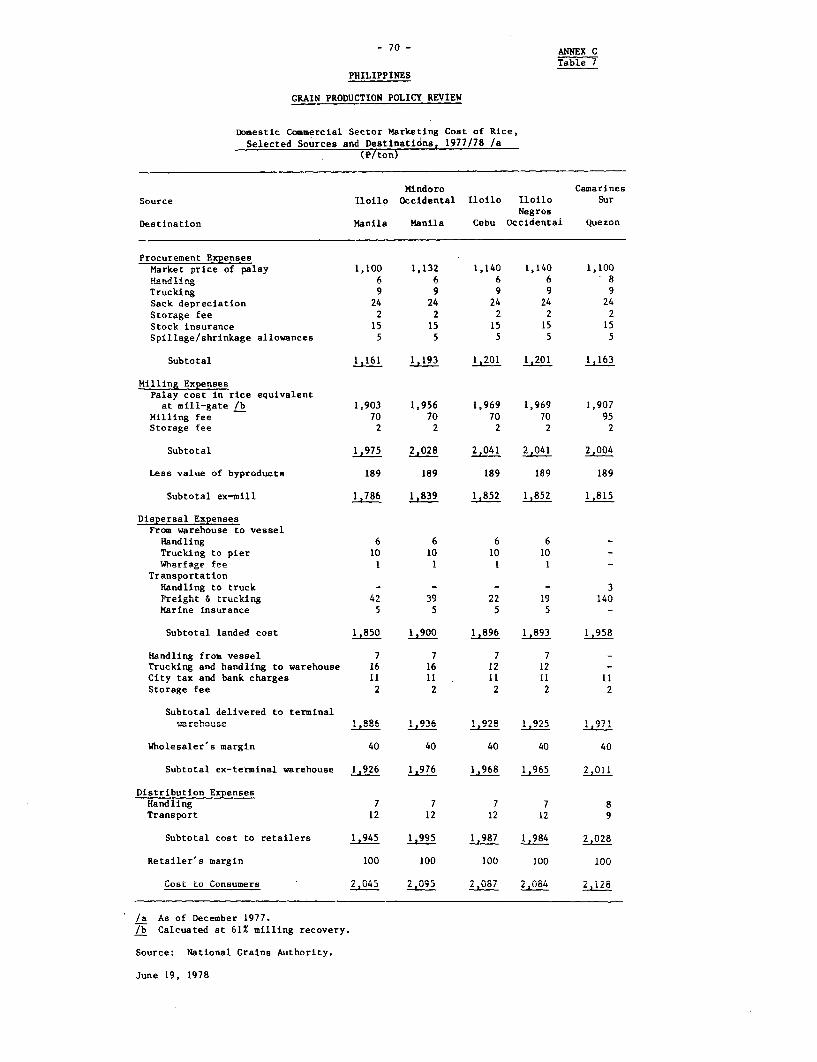

Table 7PHILIPPINES

GRAIN PRODUCTIOn POLICY REVIEw

Costs and Returns per Ha for Palay. 1977/78 Crop Year /a(Pesos)

Wet-season Dry-season

irrigated irrigated NonirrigLated

Variable CostLabor /b

Seedbed preparation 42.00 42.00 42.00Land preparation 350.00 350.00 350.00Pulling &, transplanting 170.00 170.00 170.00Repairs of dikes 25.50 25.50 25.50Weeding 68.00 68.00 68.00Fertilizer application 34.00 34.00 34.00Chemical spraying 34.00 34.00 34.00

Harvesting & threshing /C 624.00 639.00 524.00Drying & hauling /d 40.50 41.50 34.00

Subtotal 1,388.00 1,404.00 1,281.50

Material InputsSeeds 90.00 90.00 90-00Fertilizers /e 419.00 419.00 419.00Pesticides 335.00 335.00 335.00Rodenticides 50.00 50.00 50.00Zinc 15.00 15.00 15.00

Subtotal 909.00 909.00 909.00

Nonvariable Cost…----es or. la /f 8. 810 81

Land amortization /9 510.00 510.00 680.00Land tax /h 18.00 18.00 24.00Barrio Guarantee Fund /i 55.00 55.00 55.00Barrio Savings Fund Li 40.00 40.50 40.50Irrigation fee /k 110.00 165-00 -Depreciation 30.00 30-00 30.00

Subtotal 844.00 n899.50 910.50

Total Cost 3,141.00 3,212.50 3,101.00

Yield (ton/ha) 4.05 4.15 3.40Cost per ton (P) 775.56 774.10 912.06Value of production /1 (P/ha) 4,455.00 4,565.00 3,740.00

Net returns (P/ha) 1,314.00 1,352.50 639.00

Break-even yields (ton/ha) 2,855.45 2,920.45 2,819.09Value/cost ratio 1.42 1.42 1.21

/a As of September 1977 but basically applicable throughout the crop year 1977/78./b Costed at P 8.50/man-day, and at P 14.00 per man-animal day where applicable./c Costed at 14% of gross production.Id CoRted at P 0.50 ner Sn ka./e Based on recommended application of one bag of urea, one bag of 20-0-0 and four

bags of 14-14-14.Lf Based on 6% interest per season./g Costed at P 9,000/ba and P 6,000/ba for irrigated and nonirrigated land, respec-

tively, payable in 15 equal annual amortization installments at 51 annualinterest.

/h Based on P 36/ha and P 24/ha per year for irrigated and nonirrigated land,respectively.

fi Based on 50 kg/ha/season./j Based on 3% of production loan.ifk Based an value of 100 kg of palay during *zet season and 150 kg during dry season.

/1 Palay priced at P 1.10/kg.

Source: National Food and Agriculture Council.

June 2, 1978

ANNEX A

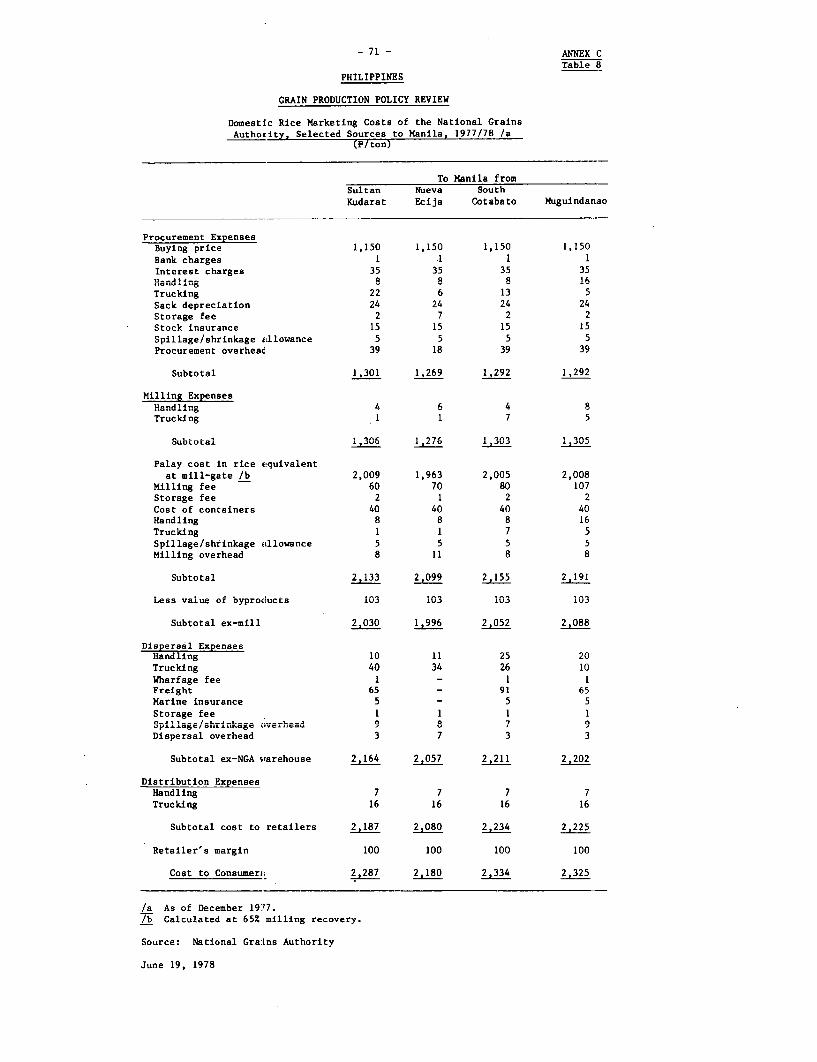

-17 - Tabie 8

PHILIPPINES

GRAIN PRODUCTION POLICY REVIEW

Costs and Returns per Ha for Corn and Sorghum, 1977/78 Crop Year(Pesos)

Corn Sorghum

Variable CostLabor /a

Land preparation 252.00 252.00Plantrin 34.00 34.00Basal fertilizer application 17.00 17.00First cultivation 42.00 42.00Second cultivation 42.00 42.00Fertilizer side dressing 17.00 17.00SprayinIg 250 nn 34. 0Harvesting, drying, shelling& hauling 450.00 400.00

Subtotal 879.00 838.00

Material InputsSeeds /b 51.00 30.00Fertilizers /c 418.75 418.75Pesticides & chemicals 150.00 150.00

Subtotal 619.75 598.75

Nonvariable CostDepreciation 25.00 25.00Interest on loan /d 45.00 45.00Land amortization /e 185.00 165.00Barrio Guarantee Fund /f 45.00 40.00Barrio Savings Fund /g 27.00 27.00Land tax /h 7.50 7.20

Subtotal 334.50 309.20

Total Cost 1,833.25 1,745.95

Yield (ton/ha) 3.00 3.00Cost per ton (P) 611.10 581.90Value nf nroduction (PIha) 2j7R0.10 2,400.00Net returns (P/ha) 946.75 654.05

Break-even yields (toniha) 2.04 2.18Value/cost ratio 1.52 1.25

/a Costed at P 8.50/man-day, and at P 14.00/man-animal day where applicable./b Based on 17 kg/ha for corn and 10 kg/ha for sorghum, at P 3.00/kg each./c Based on recommended application for corn and sorghum of one bag of urea,

one hba of 20n-0-0 an f--r hbag of !4-14-14.

/d Based on 6% interest per season./e Based on value of 515 kg of corn and of sorghum, respectively, per year.If Based on value of 50 kg,'ha/season of corn and sorghum, respectively./g Based on 3% of production loan./h Based on P 18.00/ha per year.

Source: National Food and Agriculture Council.

June 2, 1978

ANNEX A- 18 - Table 9

PHILIPPINES

GRAIN PRODUCTION POLICY REVIEW

Costs and Returns per Hectare for Palay and Corn, 1977/78Crop Year. Based on Actual Past Input Levels

PalayUnit Trrigated Nonirrigated Corn

Value of Production P 4,128 2,318 923Cost of Production P 1,946 1,528 821Net Return P 2,182 790 102Value/Cost Ratio 2.12 1.52 1.12Expected Yield t 3.75 2.11 1.03Break-Even Yield 177 1.39 0.91Cost per Ton P 519 724 797Net 'Returnl per

Peso of Total Cost P 1.12 0.52 0.12

- f A - - - -Source; DZIXI.UIX

June 2, 1978

PHILIPPINES

GRAIN PRODUCTION POLICY REVIEW

Summary of Results of Fertilizer Experiments for Palay for the Period 1973-77

Crop year No. of Control Rate of nutrient Yield Increment Value of Fertilizer Net Value/cost Proport:Lon of value/cost: ratioor period trials yield applLcation /a increase per nutrient increase /b cost /c return rat:io Less than 1 1 to 2 Greater than 2

_ ,_______ ikp/ha)!=-- (kgNg)° ---------- = rP!v =-------

Palay

1973/74 7 3,376 120-30-30 2,323 12.9 2,556 628 1,928 4.07 0.0 16.7 83.31973--76 273 4,237 90-30-30 1,'708 11.4 1,879 517 1,362 3.63 8.8 12.8 78.41974/'75 18 3,067 80-30-30 1,410 10.1 1,551 480 1,071 3.23 0.0 22.2 77.81975--77 904 3,697 6'3- 0- 0 1,063 15.4 1,1659 255 9I14 4.58 7.7 10.2 82.11975/76 17 3,496 60-30-30 1,LOO 9.2 1,210 406 E804 2.98 17.6 17.6 64.81976/77 107 3,435 80-40-40 1,299 8.1 1,429 542 E887 2.64 15.9 22.4 61.7

AveraLge 1,326 3,774

75-10-10 1,227 12.9 1,350 339 1,CIl1 3.98 8.6 12.0 79.4

/a Represents most economical treatment of N-P 2 0,5-K2 0.

/b Based on official 1977 prices, i.e. palay - P 1.10/kg.

/c Based on 1977 nutrient equivalent prices as follows: N -- P 3.70/kg, P2 0,5 - P 4.36/kg, K90 - P 1.78/kg.

Source: C.T. Ho, Soil Fertility Specialist, FAO/NFAC Fertilizer P'rogram.

Auigust 25, 1978

AWEX A

- 20 - Table ll

PHILIPPINES

GRAIN PRODUCTION POLICY REVIEW

Changes in Nitrogen Recommendation ana Net Returns asa Result of Variation in Fertilizer and Palay Prices, 1976177 /a

Change in Variation in the Price of N Variation in the Price of Paiay

Price of Nitrogen Net Nitrogen Net

N or Palay Recommendation /b Returns Recommendation lb Returns

(kg/ha) (P/ha) (kg/ha) (P/ha)

-40% 93 (+18%) 1,124 (+18%) 56 (-29%) 405 (-58%)

-20% 86 (+9%) 1,040 (+9%) 70 (-11%) 680 (-29%)

0 79 956 79 956

+20% 72 (-9%) 871 (-9%) 85 (+8%) 1,231 (+29%)

+40% 65 (-18%) 787 (-18%) 89 (+13%) 1,506 (+58%)

/a Percentages in parenthesis indicate deviations from the zero change levels.

/b Based on a value/cost ratio of at least 2.0.

Source: C.T. Ho. FAO/NFAC Fertilizer Program.

June 27. 1978

PHILIPPINE!

GRAIN PRODIUCTION POLLCY REVIEW

Response of Palay Yields to Application of Nitrogen, Selected Regions, Wet Season /a

Response of palay Value of output perYiLeld increases /c per kg of nitrogen unit value of nitroenPlrovince/ Nco. of Yields lb First Second Cost of Price of First Second First SecondRegion location trials 0 kg N 45 kg N CO kg N 45 kg NT 45 kg N nitrogen /d palaly /e 45 kg N 45 kg N 45 kg N 45 kg N__ _______________-(kg/ha) ------- ------- (P/kg) (kg palay/kg N) (PF of palay/P of N)

II IsEibels 20 3,789 4,361 4,570 572 209 3.90 0.99 12.7 4.6 3.2 1.2II Isabela 11 3,704 4,265 4,631 561 366 3.90 0.99 12.5 8.1 3.2 2.1II Isabela 11 4,300 4,754 4,809 454 55 3.90 0.99 10.1 1.2 2.6 0.3II Nueva Vizcaya 25 2,967 3,589 3,668 622 79 3.90 0.99 13.8 1.8 3-. 0-4II Nueva Vizcaya 26 3,115 3,941 4,382 826 441 3.90 0.99 18.4 9.8 4.6 2.5II Nueva Vizcaya 12 2,818 3,479 3,965 661 486 3.90 0.99 14.7 10.8 3.7 2.7

III Nueva Ecija NA 3,1300 4,850 5,100 1,050 250 3.79 1.10 23.3 5.5 6.8 1.6

IV Laguna NA 4,000 4,350 4,400 350 50 3.79 1.02 7.8 1.1 2.1 0.3

V Pili NA 3, 500 4,100 4,500 600 400 3.90 0.99 13.3 8.9 3.4 2.3 r

VI Iloilo 26 4,880 5,775 6,363 895 588 3.76 0.92 19.9 13.1 4.8 3.2VI Iloilo 3 4,037 4,945 5,330 908 385 3.76 0.92 20.2 8.6 4..9 2.1VI, Iloilo 39 4,2397 5,321 5,900 924 579 3.76 0.92 2D.5 12.9 5.0 3.1VI Iloilo 9 4,1526 5,203 5,799 577 596 3.76 0.92 12.8 13.2 3.1 3.2VI GuiLmaras Island 3 4,103 4,967 5,033 864 66 3.76 0.92 19.2 1.5 4.7 0.4VI Guiimaras Island 8 3,358 3,671 3,830 313 159 3.76 0.92 7.0 3.5 1.7 0.9VI Antique 13 5,253 6,279 7,270 1,026 991 3.76 0.92 22.8 22.0 5.6 5 4VI AntWique 28 3,928 4,706 5,420 778 714 3.76 0.92 17.3 15.9 4.2 3.9VI La Granja NA 3,800 5,100 6,100 1,300 1,000 3.76 0.92 28.8 22.2 7.0 5.4

X Misamis Oriental 7 5,026 5,645 6,153 619 508 3.88 1.03 13.8 11.3 3.7 3.0

XI Davao Del Sur 17 5,262 5,741 6,522 479 781 3.92 0,94 13.3 9.0 3.9 5.1XI Davao Del Sur 28 5, 204 5,852 6,232 648 380 3.92 0.94 14.4 8.4 3.5 2.0

Average, all regions 4,089 4,804 5,237 715 433 3.83 0.96 15.9 9.6 4.0 2.4Sample variLance /f 29.0 37.2 1.8 2.6Coefficient of variation /L (x) 33.6 66.2 33.4 65.8

/a Based primarily on results of the FAO/NFAC Fertilizer Prograim for the period 1973--77 and some additional trials dating back to 19618./b Based on trials with the levels oif P2 0g, and K20 held constant either at zero or, iDn some cases, at 30 kg/ha./c Represent increments above yields resulting from the next lowest :Level of application of nitrogen./d Based on farm-gate prices of urea for 1977/78 as reported by the Fertilizer and Pesticide Authority./e Based on average regional farm-gate prices of palsy for 1977 as reported by the Buireau of Agricult:ural Economics./f Square of standard deviation of all ratios within respective category./g Standard deviation of ratios as a percentage of their respective mean.

June 2, 1978

ANNEX A- 22 - Table 13

PHILIPPINES

GRA1Y pRODUCTlON POLTCY REYVIE

Response of Palay Yields to Application of Nitrogen, Selected Regions, Dry Season /a

Response of palay Value of output per

Yield incrennne ...oe kA of nitrosen. unit value of nitro.en

Province/ No. of Yields /b First Second Cost of Price of First Second First Second

Region location trials 0 kg N 45 kg N 90 kg N 45 kg N 45 kg N nitrogen /d palay /e 45 kg N 45 kg N 45 kg N 45 kg N------------------ (kg/ha) ------------------- - (P/kg) ------- (kg palay/kg N) (P of palsy/P of N)

I La Union 26 3,399 4,281 5,102 882 821 3.78 1.05 19.6 18.2 5.4 5.1I Par.gastr.an 3! 3,098 3,948 4,551 850 603 3.78 1.05 18.9 13.4 5.3 3.7

I Pangasinan 13 2,777 3,568 3,957 791 389 3.78 1.05 17.6 8.6 4.9 2.4

II Isabela 29 4,079 4,490 4,751 411 261 3.90 0.99 9.1 5.8 2.3 1.5

I1 Nueva Vizcaya 24- 4,033 4,974 5.616 941 642 3.90 0.99 20.9 i4.3 5.3 3.6

II Nueva Vitcaya 9 4.037 4.662 4,812 625 150 3.90 0.99 13.9 3.3 3.5 0.8

III Nue-:a Eci3a NA 4,000 4,8830 SjlO 830 270 3.79 1.10 18.4 6.0 5.4 1.7

IV Laguna NA 4,700 5,830 6,800 1,130 970 3.79 1.02 25.1 21.6 6.8 5.8

V Pili NA 5,000 6,200 7,700 1,200 1,500 3.90 1.00 26.7 33.3 6.8 8.5

VI Antique 26 3,838 4,657 5,077 819 420 3.76 0.92 18.2 9.3 4.4 2.3

Vi An tique 21 4,410 5,400 6i003 990 603 3.76 0.92 22.0 13.4 5.4 3.3

VI Iloilo 41 4,632 5,416 5,760 784 334 3.76 0.92 17.4 7.6 4.2 1.9

VI iloilo 41 3,467 4,291 4,667 824 376 3.76 0.92 18.3 8.4 4.5 2.0

VI Iloilo 10 4,384 5,103 5,558 719 455 3.76 0.92 16.0 10.1 3.9 4.7VI lIoilo 8 4,178 4,639 5,051 461 412 3.76 0.92 10.2 9.2 2.5 2.2

VI Iloilo 7 4,028 4,491 4,699 463 208 3.76 0.92 10.3 4.6 2.5 1.1

VI Iloilo 3 4,480 4,953 5,100 473 147 3.76 0.92 10.5 3.3 2.6 0.8VT La iranja NA 4l100 5,300 6 100 1,200 800 3.76 0.92 26.7 17.8 6.5 4.3

X Bukidnon 13 2,916 3,221 4,241 305 1,020 3.88 1.03 6.8 22.7 1.9 6.4X Bukidnon 8 3,807 4,471 4,435 664 -36 3.88 1.03 14.0 -0.8 3.9 -0.2

X Misaoin Or. .4 4,493 5,408 5,975 915 567 ;.88 1.03 20.3

X Misanis Or. 10 3,920 4,300 4,626 380 326 3.88 1.03 8.4 7.2 2.2 1.8

X Misamis Or. 6 4,140 4,634 5,043 494 409 3.88 1.03 11.0 9.1 2.9 2.4

Xi Davao Del Sur 23 6,547 7,144 7,550 597 406 3.92 0.94 13.3 9.0 3.2 2.2XI Davao Del Sur 18 3,773 4,301 4,798 528 497 3.92 0.94 11.7 11.0 2.8 2.7

XI Davao Del Sur 12 4,702 5,397 5,818 695 421 3.92 0.94 15.4 9.4 3.7 2.2

Xi Davao Del ur 10 4, 107 4,588 4,955 481 367 3.92 0.94 10.7 8.2 2.6 2.0

Xl South Cotabato 32 5,761 6,498 7,445 737 947 3.92 0.94 16.4 21.0 3.9 5.1

Xi South Cotabato 23 4,105 4,815 5,037 710 222 3.92 0.94 15.8 4.9 3.8 1.2

XI South Cotahato 20 3,755 4,091 4,586 336 495 3.92 0.94 7.5 11.0 1.8 2.6

Average, all regions 4,155 4,863 5,364 708 501 3.97 0.98 15.7 11.1 3.9 2.7

Sample variance /f 30.2 49.0 2.1 3.5

C-ffi,;<;ei-t of a o, -(7,) 35.0 63.0 36.4 64.5

/a Based primarily on results of the FAO/NFAC Fertili.er Program for the period 1973-77 and sone additional trials dating back to 1968.

/b Based on trials with the levels of P2 05and K2 0 held constant either at cer. or, in sose cases, at 30 kg/ha.

/L Represent increments above yIelds resulting from the next lowest levei of appl.cation of nitrogen.

/d Based on faro-gate prices of orea for 1977/78 as reported by the Fertilieer and Pesticide Authority.

/e Based on average regional farn-gate prices of palay for 1977 as reported by the Bureau of Agricultural Economics.

/f Square of standard deviation of all ratios within respective category.

/A Standard deviation of ratios as a percentage of their respective mean.

.June 2, 1978

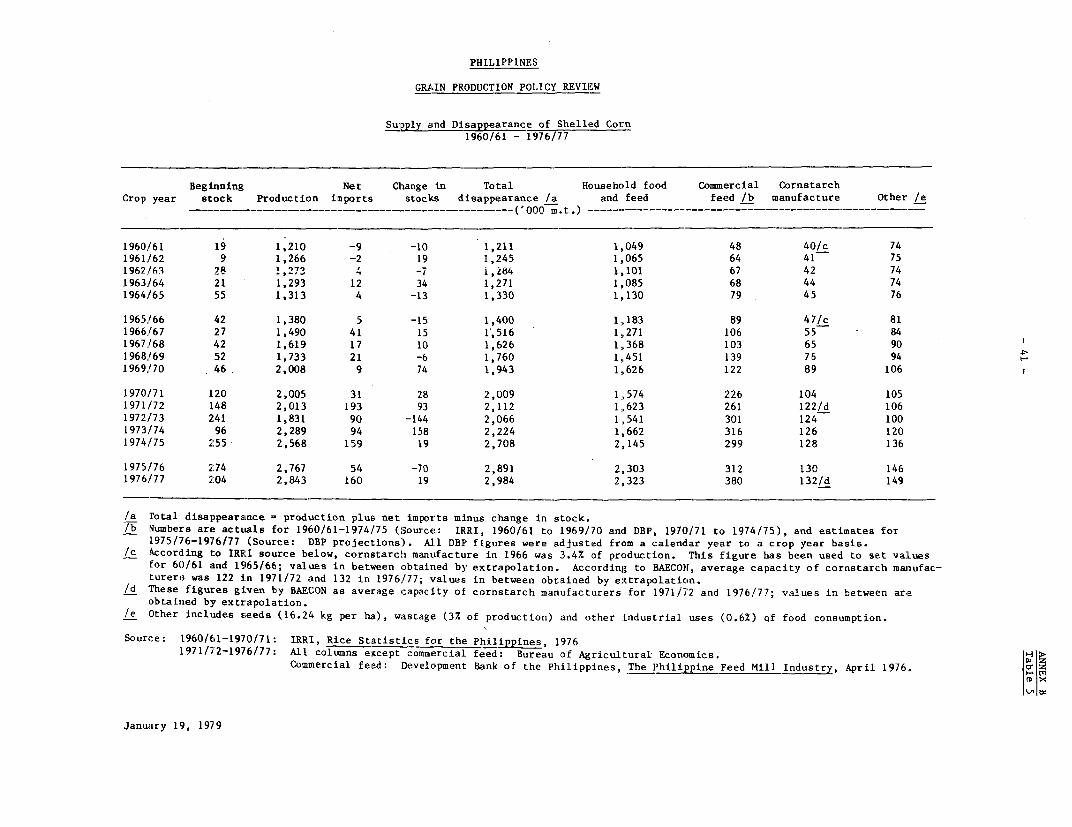

ANNEX B

- 23 - Page 1

PHILIPPINES

GRAIN PRODUCTION POLICY REVIEW

The Demand for Grains

1. The maior foodgrains - rice, corn, and wheat - have always been

the primary source of energy and nutrients for the Philippine population.

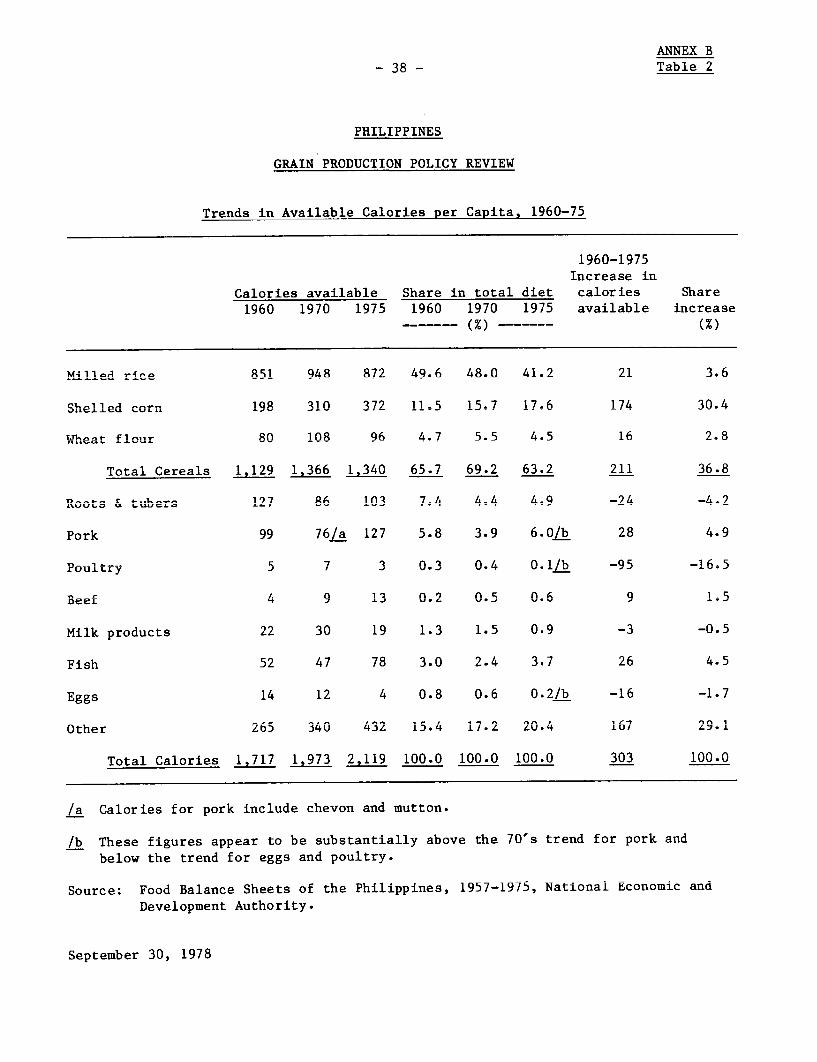

In 1975, thev provided 64% of total calories and 43% of total grams of

protein consumed./l Both rice and corn are generally consumed in raw milled

form, whereas wheat is consumed mainly in the form of bakery goods. White

corn is preferred for human consumption, and yellow corn is preferred for

feed use (although both types are currently used for feed). In addition,

corn, sorghum and grain byproducts have become increasingly important in

recent years as bulk feedstuffs for -oultrv and hogs raised in both hackvard

and commercial units. Some corn and wheat is also processed into inter-

medi4ate r.on-foA goods 3uch as cornstarch and glue, but the total amounts

involved are relatively small.

2. Historically, imports of cereals have been necessary to supplement

domest'c production; ir, the early fifi the value of cereal imports was lO0

of total import value. Cereal imports have tended to cost the Government

roughly twice that of dairy product imports, the second major food import.In recent years, however, the share of cereals in total import value has

been reduced to less thnan five percent, due to tiLe increasing importance

of industrial imports a:; well as to increasing domestic production of rice

spurred by tne self-sufificiency programs of the Government. During the

seventies, rice imports which were as high as 569,000 tons in 1965, have been

gradually reduced and, in good years, even replaced by exports, e.g. over

90,000 tons in 1978. On the other hand, other cereal imports have shown no

consistent decreasing trend despite increased domestic production of corn anrd

increasing retail prices of wheat, a cereal not currently produced in the

Philippines./2 Although the Philippines has approached self-sufficiency

levels in rice and white corn in recent years, imports of wheat, yellow corn

and sorghum remain high (see Table i). Tnus, prospects for decreased foreign

exchange savings as well as higher farmer incomes will depend as much on

future trends in domestic grain consumption as on the potential for continued

increased production through irrigation, extension and development of new

technology.

3. Data on grain consumption in the Philippines are available from

several different sources, including census and survey data. Long-term

availability data, often used as a surrogate for consumption, is estimated

/1 See Food Balance Sheets, 1953-75, National Economic and Development

Authority (NEDA), Manila, Philippines.

/2 Research into the potential of wheat production in certain areas is

being conducted; however, the climate in the Philippines is not

generally suitable, and whatever wheat production may be possible

is not expected to reduce import requirements significantly.

ANNEX B2 24- Page 2

through disappearance methods and summarized in food balances by the Bureauof Agricultural Economics (BAEcon) and by the National Economics and Develop-ment Authority (NEDA). The Food and Agricultural Organization (FAO) hasalso compiled provisional food balances for the Philippines for the periods1960-1962 and 1972-1974. In addition, survey data on per capita consumptionis available from four different sources: National Food and AgricultureCouncil (NFAC) surveys of food consumption conducted in the seventies; calorieintake surveys of the Food and Nutrition Research Center (FNRC) conductedduring the fifties and sixties and late seventies; Family Income and ExpenditureSurveys (FIES) conducted by the National Census and Statistics Office (NCSO)for the years 1961, 1965, 1971, and 1975; and surveys of consumption of riceand corn conducted by the National Grains Authority in 1975 and 1976. Becauseof inconsistencies between disappearance data and survey data, the two datasources are used for different purposes in this report./1 The discussion ofaggregate trends in the first section of this annex relies on the disappearancedata, which are consistent with production and stocks data. The latter nartof the annex, however, which examines the structure of demand, relies primarilyon the survey data.

Past Trends in Grain ConsumDtion

4. The sixtieq and spuenties saw major improvements inr availailityof grain for food, feed and manufacture. While population and annual calorierq-uiirpmentQ Drew by an averao annniinl rate of 3% frnm 1QA0 to- 1070, d44

appearance of rice, corn, and wheat grew by 3.9%, 5.2% and 2.2% respectively./2The experience f rnm 1q7n 0t 1Q77 was less favorable, reflecting majr dr oAp_

r -~ ---- LVs |bX - -- -11, -- J-- - - L - U'Up

in consumption in 1972/73 which accompanied the production shortfall broughton by typhoon and floods. Du r ing L t'h is p-eri, Ltlt puulatUi growth r at

fell to less than 2.8%,/3 while disappearance of rice and corn grew by 2.9%and 7 7, - respectively. 'he. d4 Af what de e sl -au It.1/o tC~,tL VV.LV±.Y LIlM UibZDapWtaLLdiLt UlL WIitdL, Ut~LtVCU SUit!iy ILOLO

imports, grew at about the same rate during the seventies as during thesixties, refL±LectiLrg the ir.fluence of higher prices aintaLined by the National

Grains Authority in 1974-1976. (International prices of wheat actuallyuroppedu ir recent years). Importation and local production of sorghum began

for the first time in the seventies. Most of the increase in disappearance ofcorn and all of that of sorgnum derived from increased feed requirements forthe Philippine hog and poultry production industry, while food use accountedfor the boost in rice and wheat disappearance.

/1 The survey data indicate 30-40% higher consumption levels than the disap-pearance data; there is disagreement among the various agency officialsas to the reasons for this discrepancy, however.

/2 These annual growth rates were based on three year moving averages covering1960/61 to 1971/72 for rice and corn and on individual years from 1959/60to 1969/70 for wheat.

/3 This decrease was, however, counteracted by a continuing growth in calorierequirements of 3% (due to an increase in the proportion of populationaccounted for by adults.)

ANNEX B

-25- Page 3

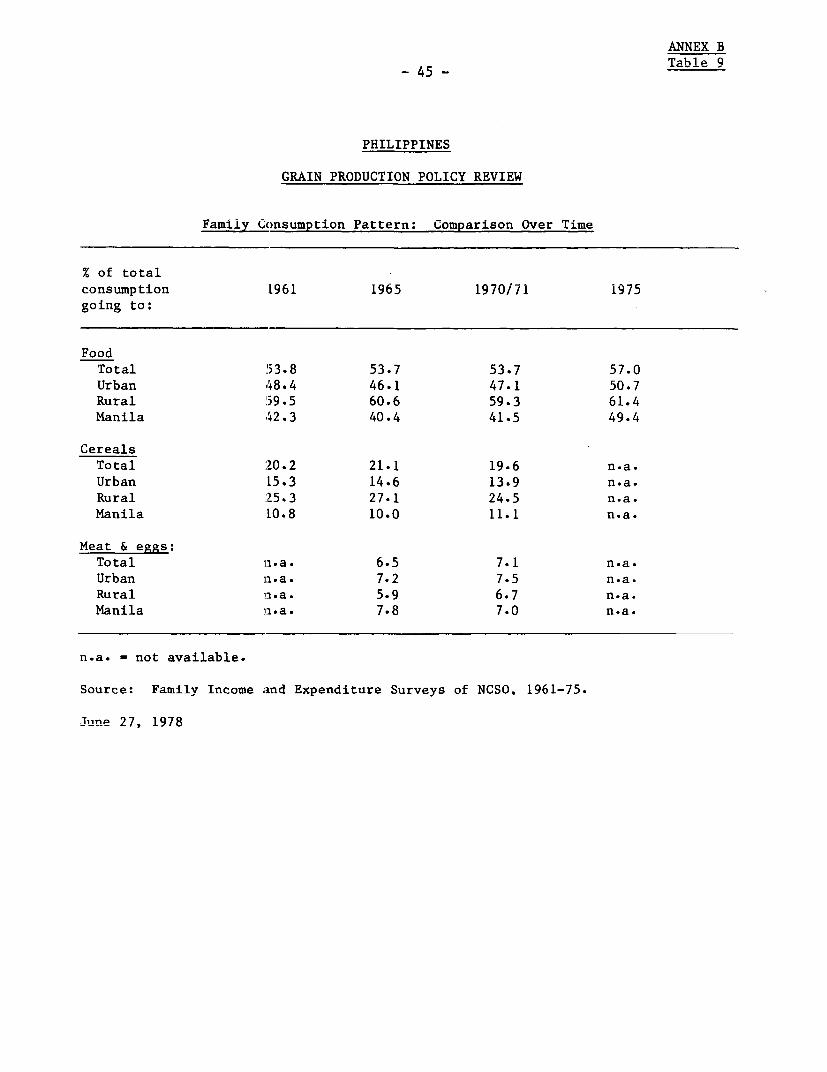

5. Consistent with these trends, the share of foodgrains in the dietdecreased in the seventies,/l while the share of meat, chiefly pork, fish andbeef, increased (see Table 2). This probably reflects increases in income andincreased urbanization, and is also consistent with the trends in prices, ascereal prices led price increases in 1970-77, while meat and egg Dricesincreased at a slower than average rate. Among the foodgrains, the trendin per capita consumption of rice, still the main stanle in the F'hilinpinpneappears to have changed little during the seventies./2 Year-to-year variationaround the average rice consumntion of 74.1 kg per canita is within 15% inall years, even including the shortage period in 1972 to 1974.

6. Data on per capita availability of corn shows an average increasener -ear of almost 5% in ons,imption during the seventies, w4it the largesr s1 kVLL Lf'.1a~

increase occurring in 1974/75. An increasing trend is hard to explain,however, since corn is consumed by humans only in certain parts of' the countryand it is often considered an inferior substitute for rice because it ischeaper and consumeu mo;e uy poorer groups./3 jJL* e iLncrease shlown Ln the datais probably due to a combination of factors: (a) a decrease in the retailprice of corn relative ;:o rice uring the seveftiLes; (b) lack of statisticalmeasurement of increased use of corn as feed by small commercial and backyardlivestock growers; and ;c) migration into corn-eating and corn-growing areasin Mindanao./4 Although there is some evidence that shows that the numbers ofthe absolute poor may have increased slightly in the seventies,/5 this factorcould have only accounted for a very small amount of the increase in corndisappearance.

/1 This represents a reversal of the trend in the sixties, when the dietshare of cereals increased.

/2 Disappearance data show a slight decrease while food consumption surveysshow a slight increase.

/3 Consumption surveys show a decreasing trend in per capita corn consump-tion as well as large negative income elasticities for corn products(-0.5 to -0.7).

/4 The population growth rate in Southern Mindanao, one of the majorcorn-eating areas, was the highest of all the regions for the period1960-1970, and secornd only to Metro Manila during the period 1970-75.

/5 See Mahar Mangahas et al, "A Critique of the NCS0 1975 Family Incomeand Expenditure Survey," University of the Philippines, September 1977.

ANNEX B- - Page 4

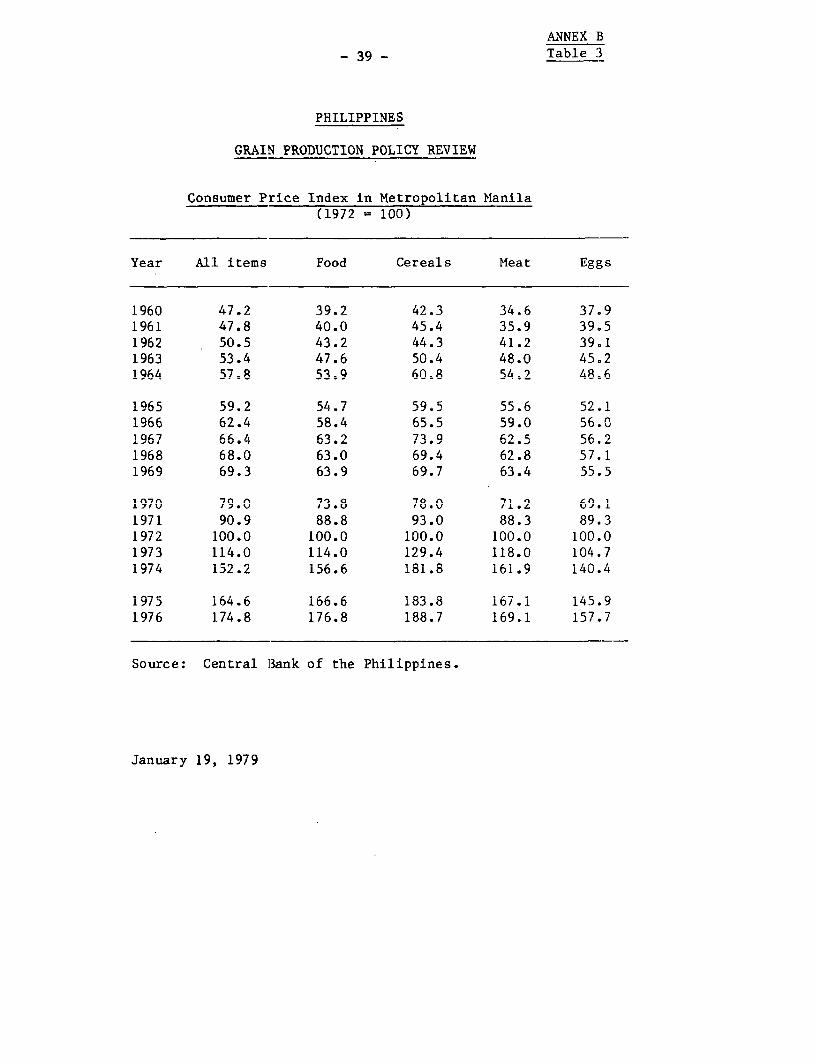

7. Total calorie consumption increased by an average of about 1.9%- peryear,in the seventies in response to increases in real GNP and personalconsumption per capita ot 3.5% and 1.5% per year, respectively./i -Tnus, in1975 for the first time, the average per capita daily consumption of caloriescame within 95% of the target of 2,187 calories recommended by the Food andNutrition Research Center of the Philippines. In general, yearly variationsin total-calorie consumption followed trends in prices and availability with alow in calorie consumption during 1973/74 accompanying the 37% rise in foodprices caused by shortages of cereal supplies (see Table 3).

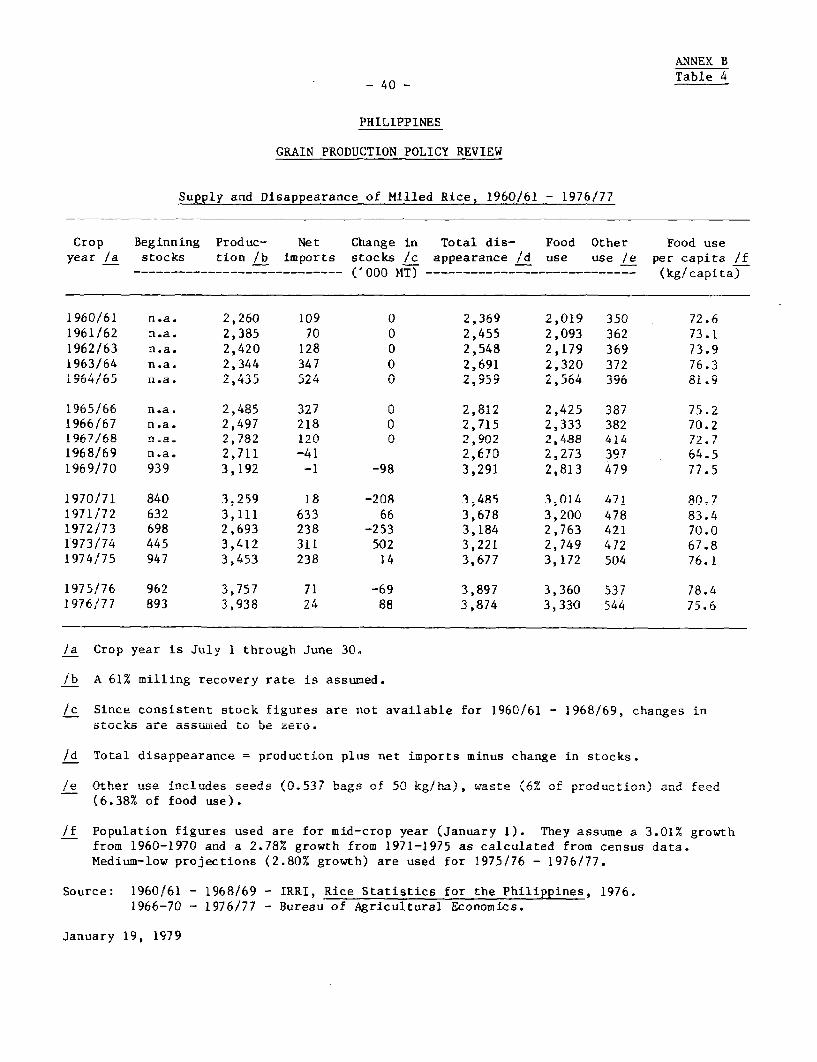

8. Annual per capita consumption of rice and corn has tended to beclosely related to supply since these cereals comprise the main staples in thePhilippines. As can be seen in Tables 4 and 5, annual domestic productionsupplied 85-100% of total rice disappearance during the seventies, and an evenhigher proportion, 90-100%, of total corn disappearance, with the remaindermade up from carryover stocks and imports. Prices also vary primarily withdomestic supply although the influence of exchange rate variations and importprices may have occasionally been important as well.

9. The years 1970 and 1971 were exceptional years for agriculture, asboth foodgrain production and consumption reached historical peaks. Thefollowing two to three years saw decreases in consumption as production laggedand food prices soared, but levels of corn and rice consumption were stillhigher than in the sixties. As the inflation abated in 1975, and favorableweather spurred production, cereal consumption revived, helping to push totalcalorie consumption closer to the FNRC minimum daily requirements in 1976 and1977.

The Structure of Foodgrain Demand

10. The aggregate demand for foodgrains in the Philippines is a complexfuinctio%n whic-h depeands on income trendsj relative nrires and avAilabilitv of

different foodstuffs, regional preferences and social attitudes, populationgrowth a- d change in family ast ucture, and t-he dcgree of iirhbnizntion nAnd/or

development in the rural areas. The previous examination of aggregate trendsin nutritional adequacy, foodgrain consumption, s,pics, and income give some

indication of overall causal relationship between key variables. However,aggregate trendUs can mask A variations in cor.sumpti on patterns which are offten

important in making aggregate projections and in assessing the distributionalconsequences of these prUjecLions. II fUolLoJwiLL, analysisb Uo. VriaLtiLLUL iLr

consumption patterns relies primarily on the food consumption surveys whichprovide our only source of disaggregated consumption data.

/1 National Accounts of the Philippines, 1970-77, National Economicand Development Authority, Manila, Philippines.

ANNEX B-27 - Page 5

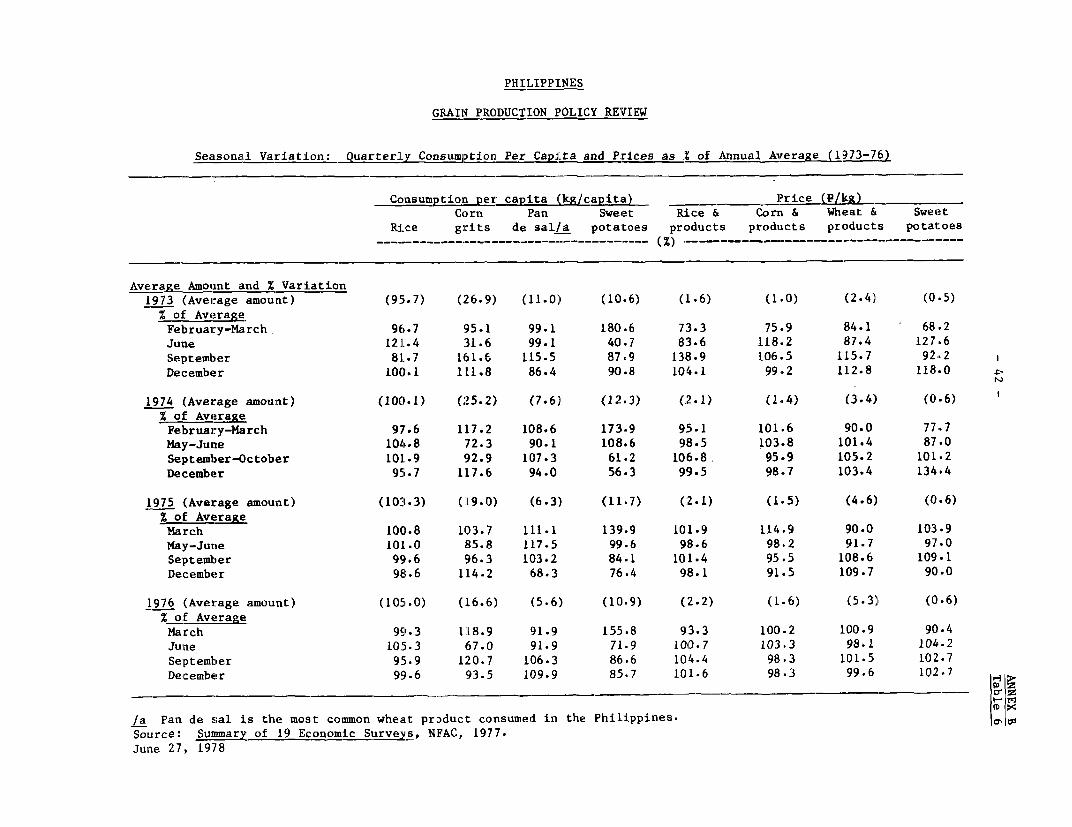

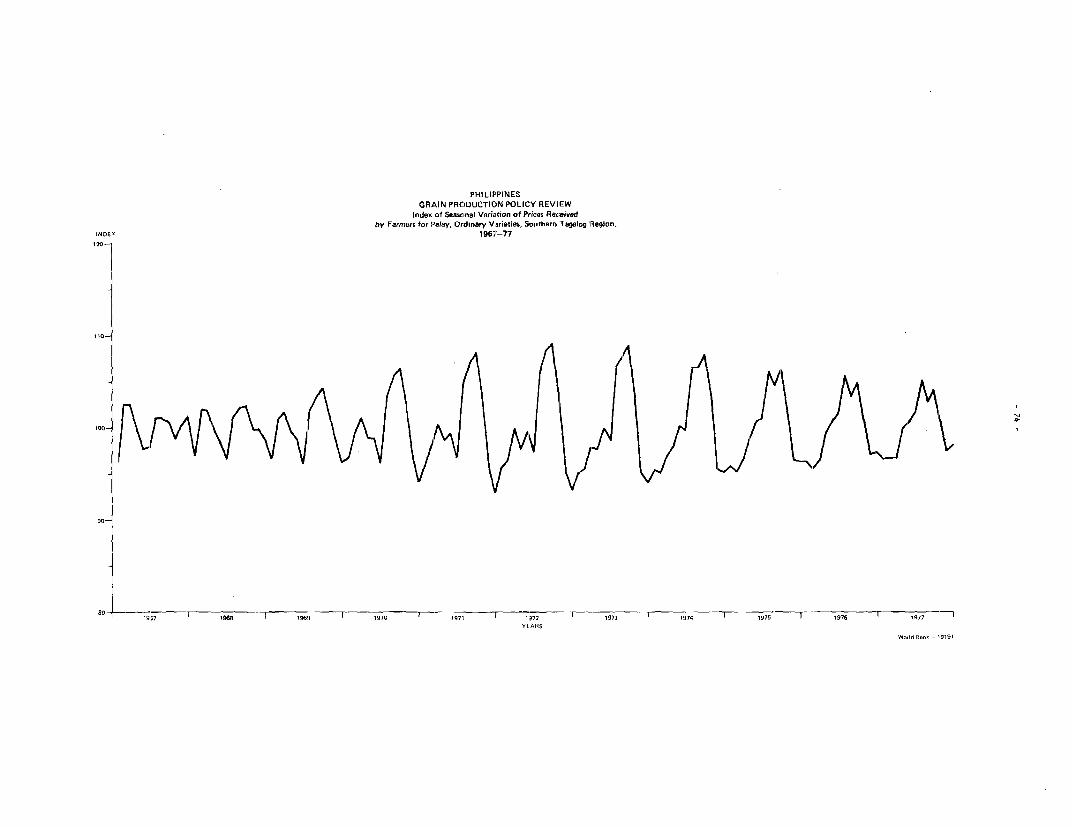

11. Variation in ConsumDtion Patterns bv Season. Evidence on seasonalvariation is scarce prior to the seventies; the only study conducted, whichwas in a surplus rice area with a high percentage of multicropning, showed asmall seasonal variation in conflict with results in other similar countries.In the early seventies contrasting evidence on seasonal variation in consump-tion is available from the consumption surveys conducted by the National Foodand Agriecuilfturp oniunril (see Tablhe 6). These surveys show a consistentpattern over several years of high rice consumption in May-June, when hardlabohr isi requlratd ir. lantd preannrst4or. Seasonal va-nr4atior. Aduring o thear par-ts

of the year is less consistent, but consumption is often low in September,4ust prior t- harvesti-ng Seasonral v-ristion ir. con.sumptiorn app...r to havedecreased in the later years when rice supplies were relatively abundant.

12. The seasonal pattern is opposite for corn, with June showing thelowest consumpt'on levels, and December and M.arch sometimes shownrg thehighest levels. Consumption of roots and tubers also shows a strikingseasonal variation with consumption in tne iarcn quarter often reachinglevels twice as high as during other quarters. As would be expected, wheatproduct consumption, being dependent on imported wneat, exhibits no discernibleseasonal variation. These individual seasonal patterns combine to produce arelatively stable year-round consumption of calories derived from cereals andstarchy vegetables.

13. Regional Variation in Consumption Patterns. Information on regionalvariation is also available from the NFAC surveys. Regional patterns inconsumption of foodgrains reflect regional preferences, relative incomelevels, and concentration of production in certain areas. Total calories ofcarbohydrate foods consumed are fairly consistent among the regions, withvariations explained by differences in urban population and income levels.The distribution of calorLc consumption among the various foodgrains showsconsiderable variation, however (see Table 7).

14. Regional preferences for rice vs. corngrits are most striking, withonly 9% of all families surveyed consuming both rice and corngrits. Luzonand the Western Visayas are the major rice-eating areas; within these regions,only in Metro Manila does the rice consumption per capita fall lower than 100kg. Only two regions of this group - Cayagan Valley and Western Visayas -contain a significant numlber of families who consume corngrits (17% and 9% ofthose surveyed, respectively).

15. The major corn consuming area is the Central Visayas region whereconsumption of corn is twice that of rice, and over 50% of all familiessurveyed consumed only cor'ngrits. In other regions in the Visayas and inMindanao. more rice than corn is consumed. and only about 20% of the familiesprefer corngrits only. Thus, the surveys indicate that 63.3% of the rice andonly 9% of the rnrnarits are annqiimet in TLunn and WPetern Visayas, whilp91.% of the corngrits and 36.7% of the rice are consumed in the remainingregions of the Philippines=

ANNEX B- 28 - Page 6

16. Consumption of pan de sal (a roll-like product) is relativelyuniform in areas outside Metro Manilasa and Soiitheprn Tagcralon. (Average onimn-tion in these two regions is twice as high as in other regions.) For othercarbohydrates, however, connumption patterns roughly follow the rice/cornpreference pattern, with Bicol, the Visayas and Mindanao showing less depen-dence on ricear.daricher varlety of energy sources. Luzon (excludingBicol),with 70.8% of the population in 1975, consumed only 15.3% of the nationallevel ofcns. ..~JLamUL ofl sweet potatos, 11.4T of the caooava roo, and 2.5%of bananas. Eastern Visayas, a region with a relatively low per capitaLucome, cousumued the highest amounts of swe-et potato ar.d cassava roots.

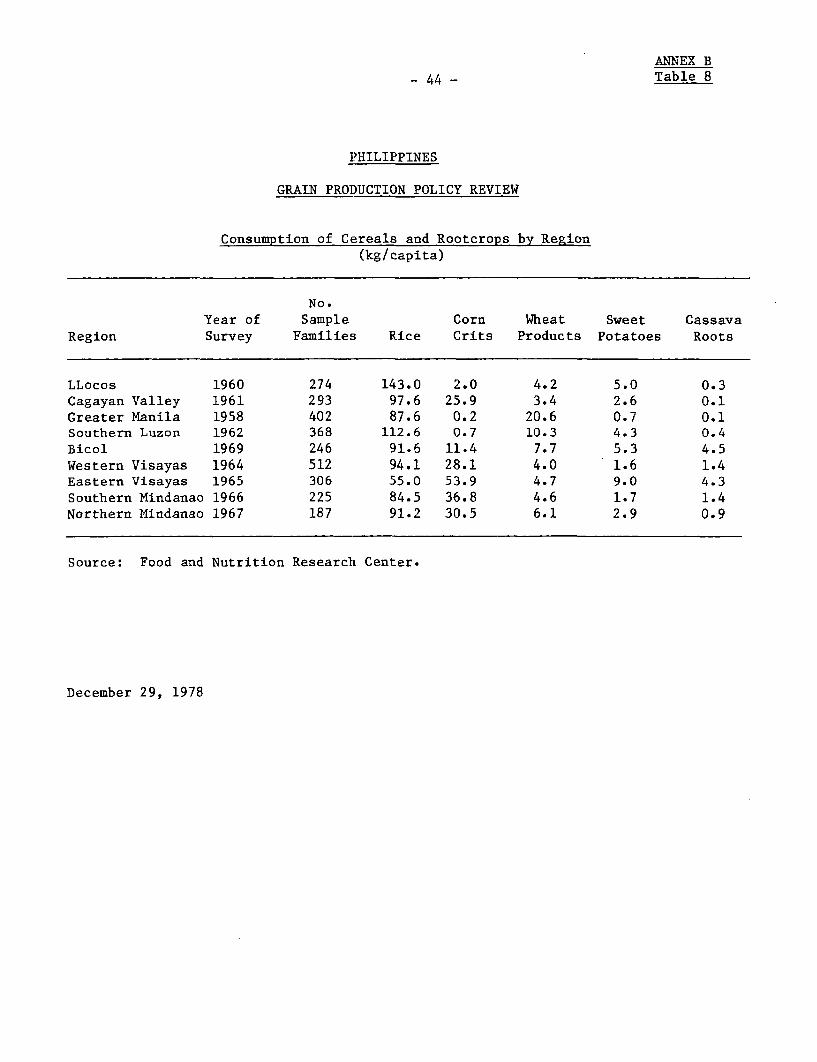

17. *lhe only othler source ol iLniormation On consumptLon by region comes

from food intake surveys conducted in different years for most regions by theFood and Nutrition Center (FNRC) during the fifties and sixties (see Table 8).These surveys show similar regional patterns in consumption of rice and corn.The FNRC figures for consumption of cassava roots and sweet potato are muchlower, however, possibly indicating an increase in consumption of these cerealsubstitutes in the seventies, particularly in the Visayas and Mindanao.

18. These regional consumption variations are explained partially byregional variations in production. Luzon and the Western Visayas accountedfor 74% of value added in palay production in 1974 and only 29% of valueadded in corn production. In contrast, the rest of the Visayas and Mindanaoaccounted for 70.7% of the value added in corn production in 1974. Despitethis seeming correlation between production and consumption by region,certain regions experience chronic deficits in rice and/or white corn andmust rely on interregional shipments of private traders and the NationalGrains Authority. For rice, the main deficit regions have been SouthernTagalog, Central and Eastern Visayas and Mindanao. The latter three areashave also been white corn deficit regions on occasion. Cagayan Valleyappears to be a major supplier of both rice and white corn to the deficitareas.

19. Consumption Patterns in Urban and Rural Areas. Comparative data onfood consumption of the urban and rural populations are scarce in the Philip-pines, which is unfortunate since surveys in other similar countries showstriking differences in diet. Data from the Family Income and ExpenditureSurveys (FIES) are limited to expenditure figures broken down into broadclasses of food items. Intake data from FNRC surveys are available byurban/rural breakdowns, but only for the period 1958-1969. The NFAC surveysprovide the most vrecnt data nan thp most dptniled in terms of food itpms,

but only Greater Manila is singled out. These three sources provide roughcross-sectIonal information on A-If rr-nroa an onsumptirn n:ttPrn. hptErtRn

urban and rural populations, but no information on the trend over time, whichwould be particularly useful since the uvrhbn piopiuntion 4n then Philippines

grew at rates of 4% and 4.5% in the 60's and 70's respectively.

20. The FIES surveys show that people living in urban areas in thePhilippiues bLIU se aUsmLaL.L=L pJrJoJpo.LtoLL of tLhei income -r.- f - - th---

in rural areas, even when data is subdivided into income classes. The percen-tage of total expenuditures tends to be an even smaller percentage for Metro

ANNEX B-29 - Page 7

Manila thlan for other urbuan areas. T.hle percer.tages chane litt Lrom 1961in4to 1970/71, but in the latest census in 1975, the percentage of food expendi-tures ofL a'l'l groups increL ased p YUU, probablyL- d mr to prce increases LtlaLl

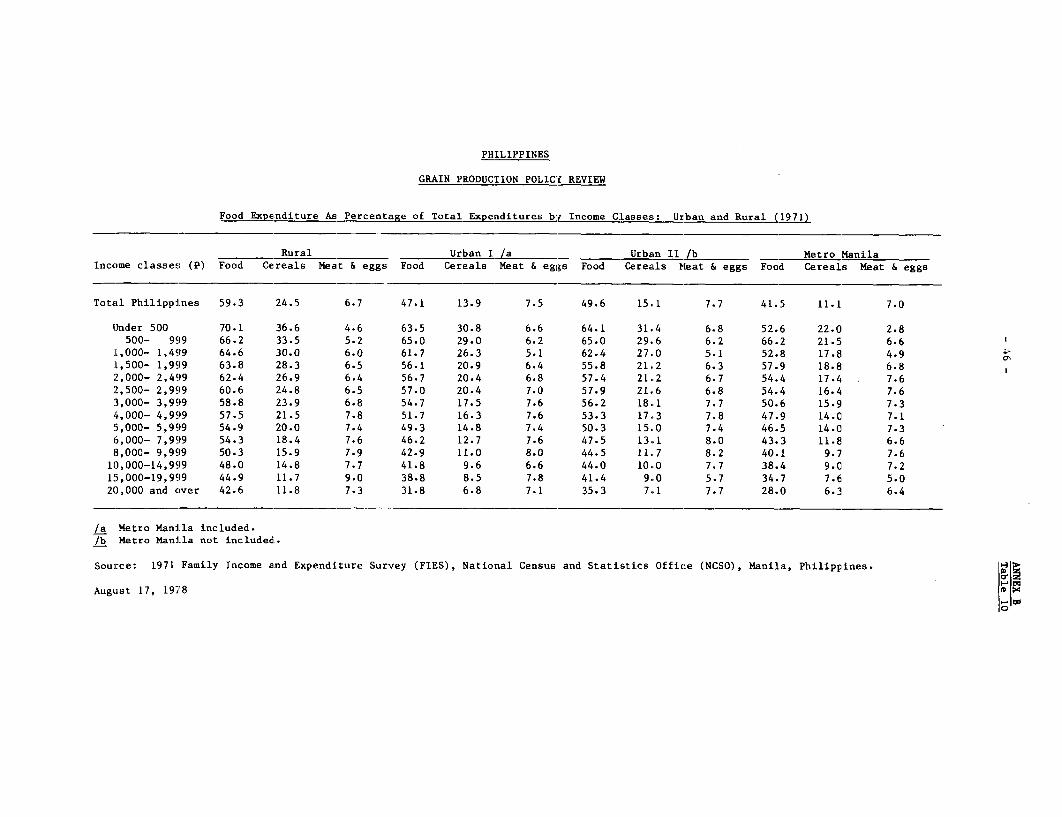

quantity increases (see Table 9). In 1971, the urban population spent 47.1%of its Lncome on average on rood (Metro Manila spent 41.5%) wnhle cne ruralpopulation spent 59.3%. These averages reflect variation from 70.1% to 42.6%for the rural population (iowest to highnest income ciass) vs. 63.5% to 31.8%for the urban population (see Table 10). The percentage of total expendituresspent on cereals shows similar variations. In 1971 the urban population spentonly 13.9% on cereals whiereas the rural population spent 24.5%. In contrast,the urban population spent 7.5% on meat and eggs compared to 6.7% for therural population.

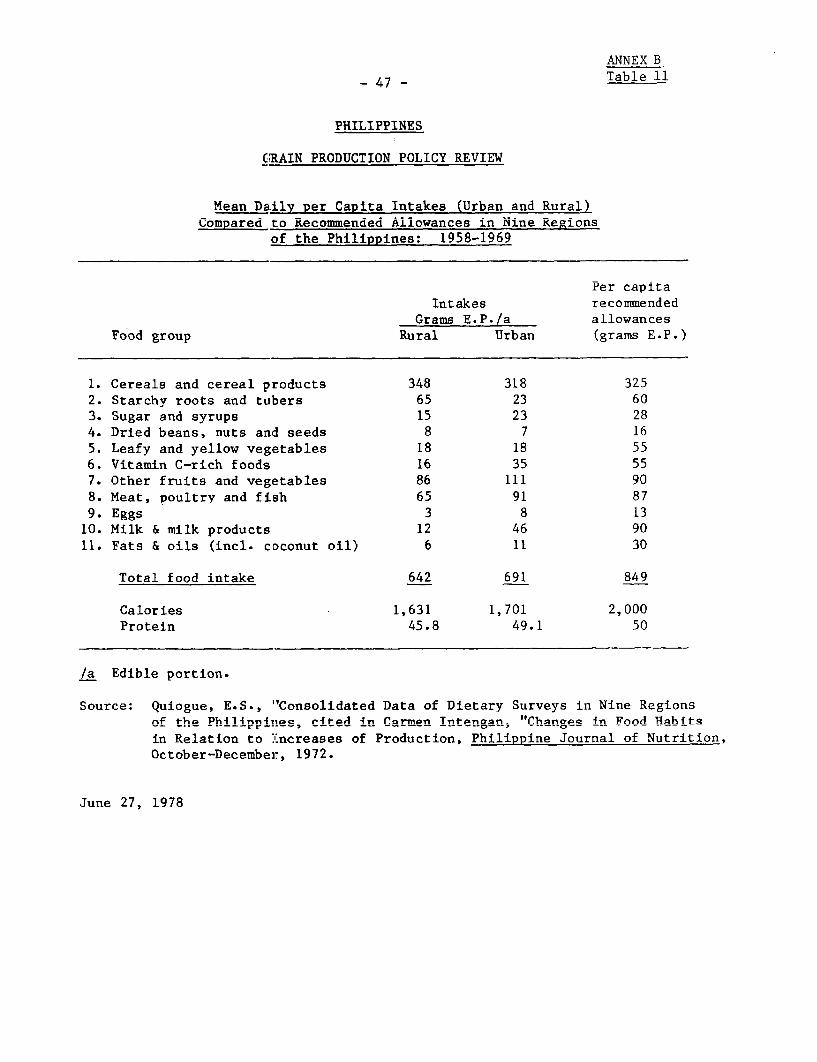

21. The FNRC surveys show that most of the difference in expenditurescan be explained by differences in intake (see Table 11). These surveysshowed the urban population consuming 4.2% more calories than the ruralpopulation. Consumption of cereals, starchy roots and tubers, and driedbeans, nuts and seeds were higher in the rural areas, whereas consumption ofall other items were higher in urban areas. Consumption of meat, poultry andfish was 40% higher in urban areas than in rural areas, and consumption ofeggs and dairy products was more than double in urban areas.

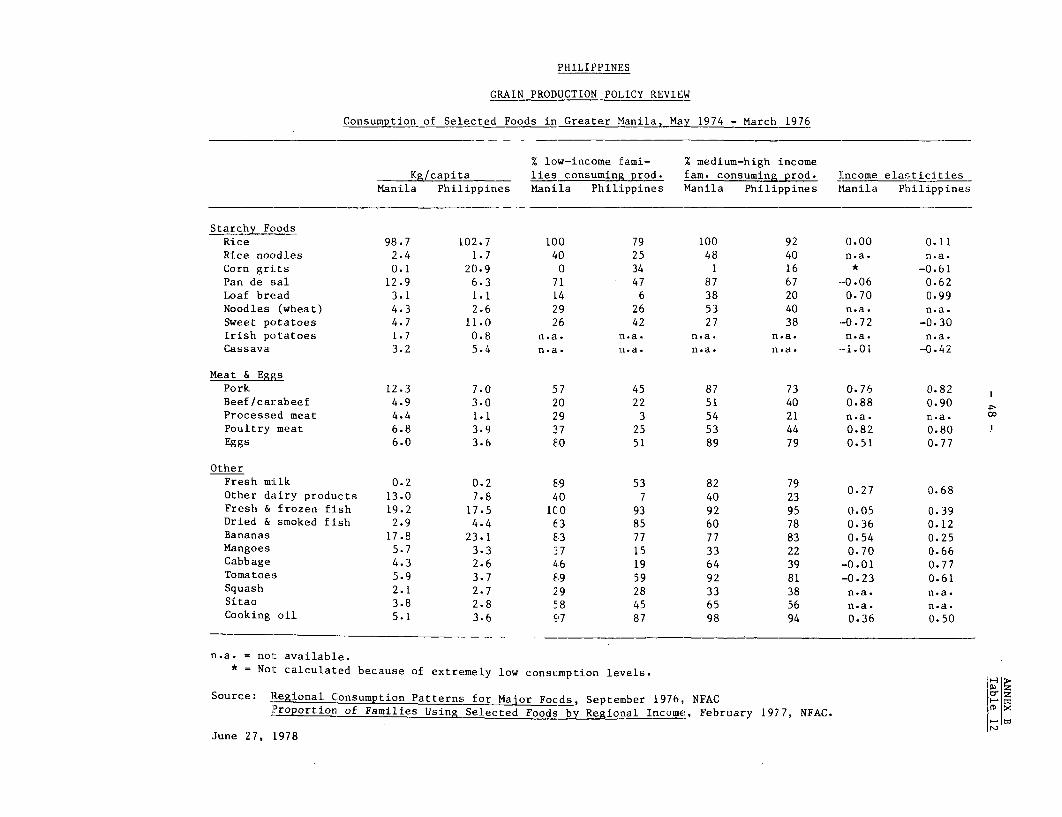

22. These broad trends are also reflected in the NFAC surveys which arebased on more recent data (1974-1976) and which provide detailed breakdownsby food item (see Table 12). The data show that, especially among low incomegroups, families in Metro Manila enjoy a more diversified diet and one whichcontains higher percentapes of processed foods as well (e.g., rice, noodles,loaf bread, processed meat).

23. While average per capita consumption of rice and corngrits is lowerin Manila than in the Phi.lippines as a whole, consumption of pan-de-sal andloaf bread is much higher. Because the low income groups in urban areas havemore access to certain goods, income elasticities of normal goods are lowerin Manila and even negative in some cases (pan-de sal, cabbage, tomatoes).Income elasticities of irnferior goods, particularly those which tend to behome grown (sweet potatoes, cassava). are even more negative in Manila than inthe Philippines as a whole. Among the meats, income elasticities are lowerfor nork and eggs and roughlv enual for beef/rarabeef and noiiltrv Theincome elasticity of rice in Manila is 0, reflecting the fact that allfamilies in Manila eat rice regardless of income group. Because of regionalpreferences regarding rice and corn, however, this should not be interpretedas tvniral of tho noverall uirhan pnnnOlat-oin

24. Variations i4n Cons-u2ption Patterns by Income Class q. fly two"sources of data provide information on food consumption by income class: theVFIE Expend,iture Surveys and thbe L*U A fSurveys. The LTLI curveys indicate thatas income increases, the percentage of expenditures on food and cereals bothLrop con .I 0E. aUera bly Wi Lt Li lo aWest L Ur X V U Ln both case ULsocur Ur L1 LLr L XI VI Li LManila. In 1971, the percentage expenditure on food dropped 25-30 percentage

ANNEX B-30 - Page 8

points from the lowest income group to the highest, and the percentage expendi-ture on cereals dronned 15-25 Doints (see Table 10). In contrast the nercenta2eof expenditures on meat and eggs rose. These variations respect Engel's law,aQnd fnllnw nptrPrns exnpect-e for stanles (rtersalR) and lulxuirv item.s (meats andeggs).

25. The series of NFAC surveys conducted from October 1970 to June 1976ic t-ho he-et eata sniirrc for nn1l uinc unariations inn mwnntif i-u nnaiim hr

income class, as opposed to expenditure. In each survey, the families weredivided int-n fnor income gronsn AdfineA in current prices (income for 19 months

prior to each survey date):

Low income - Less than P 400 per capitaVLed- ir.4ncome - n A0-700 per capi4ta

Medium-high income - P 799-1,499 per capita114g b-4. = ro 1 ,50 an' over per capita

26. * tsWbCompar'Uiks of theIU VdtL.LdLJLUL1 ueweeti CoisbULmpLtoU paLLernLs of LLth

four income classes over time is broadly valid, assuming price rises duringthe seventies a'iecteu all groups equally. nowever, caution must be exercisedin comparing trends over time since the average income of each group inconstant values decreased considerably over the period.

27. Tne highest income class consumed on average 15 to 20% more ricethan the lowest income class, and during the most severe shortage period inSeptember 1973, the hignest income class consumed 40% more rice than thelowest class. The difference in wheat product consumption, which is more ofa luxury item, is even more striking. Consumption increased considerablywith each new income class until the highest income class consumed from twoto three times as much of the wheat products as did the lowest class. Incontrast, the poorest class consumed more than three times the corn productsof the highest income class during most years.

28. There are also differences among the income classes in consumptionof raw milled grains vs. more highly processed products. Per capita consump-tion of rice noodles and rice cakes are still very low in the Philippines,but the surveys show a clear tendency for these products to be consumed moreby higher income classes. Similarly, consumption of wheat-based noodles andloaf bread recorded in the surveys were significantly higher in absoluteamounts among the upper income classes.

29. The data from the NFAC surveys were used to calculate cross-sectionalincome elasticities for cereal products and other foods and these elasticitiesare given in Table 13 to summarize the variations found in the surveys in

ANNEX B

- 31 - Page 9

food consumption by inccome classes. These elasticities should be interpretedwith some caution, however, since the real incomes of the income classeschanged considerably during the seventies. Since consumption of cerealsgenerally levels off and sometimes declines at high income levels, the elasti-cities may be biased uprards (in absolute value) for normal goods and downwardsfor inferior goods since the patterns of the highest income classes areincreasingly left out of the sample with each new consecutive survey. However,this bias is probably nct significant enough to cause errors in projections ofcereal demand since the upper income classes are a very small proportion ofthe population and they consume an even smaller proportion of the cereals.

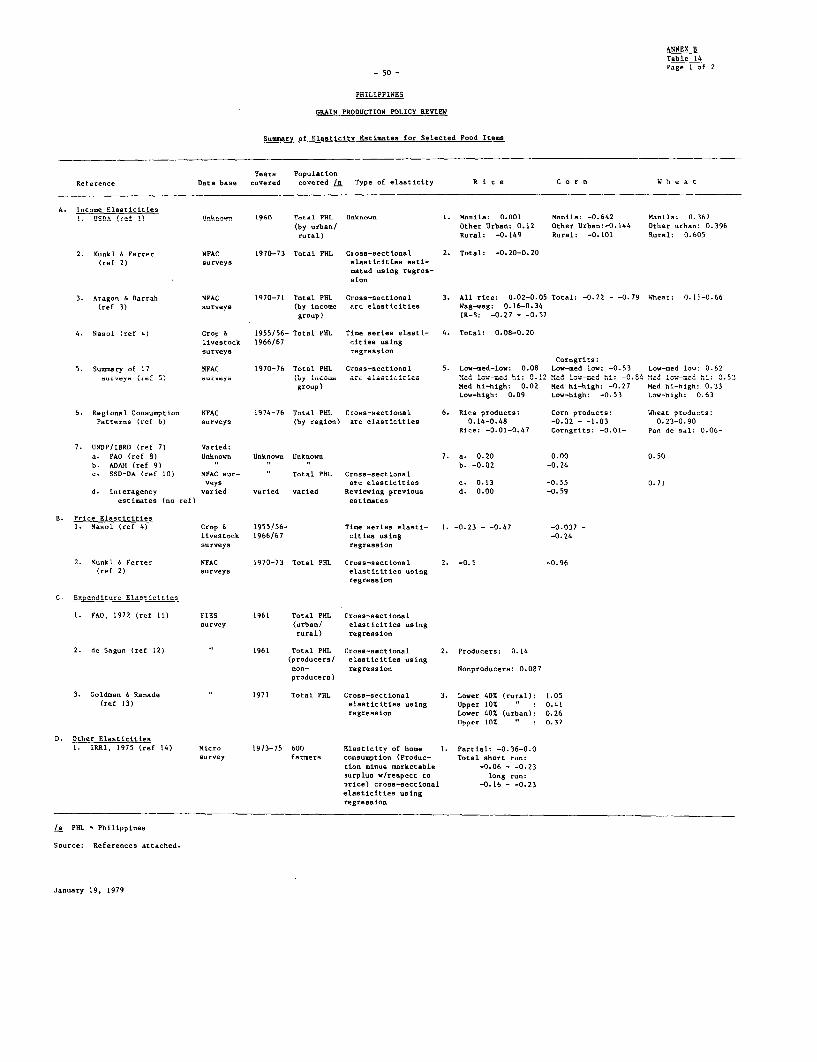

30. Estimates of Elasticities of Cereal Products and Substitutes.Berause of the relative wealth of data on food consumntion natterns in thePhilippines, numerous studies have been conducted to estimate income, expendi-ture, and nrire elastirities which ran be used to nroiect demand for differentfood items. The studies vary considerably in their data sources, methodologi-canl naproachc nne cnmnlo hronkAnranc* A suymmnar of thp celidioc And the

elasticities estimated is presented in Table 14. Only two studies havenattmpteA to meaure nprice elatrinitiae; most studieics hnave boor nimed at