Embed Size (px)

Citation preview

Pacific First Mortgage Fund(Formerly City Pacific First Mortgage Fund)

ARSN 088 139 477

Annual Financial ReportFor the year ended June 30 2016

BTI 5510 Annual Report 2016.indd 1 6/09/2016 10:20 AM

This page is intentionally blank

BTI 5510 Annual Report 2016.indd 2 6/09/2016 10:20 AM

017-8139-3829/1/AUSTRALIA

27 September 2016 Dear Unitholder, PACIFIC FIRST MORTGAGE FUND UPDATE The Annual Financial Report for the year ended 30 June 2016 is also available on the website www.balmaintrilogy.com.au. If you have an email address or regular access to a computer we recommend that you update your Annual Report preference to email, or alternatively view the report on the website. This will assist in reducing the cost of print and postal communication attributable to the Fund. If you would like to update your method of receiving a copy of the report you can change your preference by contacting Balmain Trilogy Investor Relations on 1800 194 500 or via email: [email protected]. LITIGATION UPDATE KPMG In our last update in April, we advised that the claim against KPMG was scheduled to go to mediation. The initial claim against KPMG was in relation to their role as compliance plan auditor of the Fund. A confidential and without prejudice mediation was held recently and more information will be provided shortly. Sullivan & Ors The final orders in regards to the Judgement made in December 2015 awarded the Fund $73.5 million in compensation and interest to be paid by the former directors and officers of City Pacific Limited. This claim was for breaching Section 601FD of the Corporations Act in relation to one loan. This Judgement was appealed by the former directors of City Pacific Limited in March and the hearing for the Appeal has been set over three days in November 2016. The determination of the appeal may be made over these dates, or judgement could be reserved until a later date. For Unitholders who wish to attend the hearing in Sydney at the Federal Court of Australia, details are listed below:

Judges: Gilmour, Farrell and Gleeson JJ Time: 10:15 AM Date: Monday, 14 November to Wednesday, 16 November 2016 Place: Law Courts Building, 184 Philip Street, Sydney Duration: 3 days

The courtroom allocated for these hearings will be shown on a notice board in the foyer of the ground floor of the Law Courts Building. OTHER FUND MATTERS Next Payment When the litigation matters mentioned above are complete the Responsible Entity will review the Fund’s cash position with the aim of assessing whether it is acting prudently, is in a position to make a further distribution and whether some monies previously set aside, but unused, for funding litigation can be included in the next distribution Any announcement regarding a distribution rate and date for a payment will be made on the website prior to being paid. Redemption Requests The Fund receives a numbers of enquiries from Unitholders wanting to redeem their remaining units. As the Fund is in the process of being wound up, it is considered a non-liquid registered managed investment scheme and is unable to process any requests to redeem or withdraw units. Declining Unit Price

017-8139-3829/1/AUSTRALIA

As the Fund is in the process of being wound up and has sold all remaining real estate assets, any available surplus funds are paid to Unitholders when they become available. This will result in a decline of the net asset value per unit (unit price) as assets are sold or return of capital payments are made. When all litigation issues have been finalised the process for winding up the Fund will then commence and value of the Fund will be reduced to zero. We will continue to update investors via the website when further information regarding litigation and Fund issues become available. If you need to update any of your details on your holding, forms can be downloaded at www.balmaintrilogy.com.au. Should you have any queries with your holding or the Fund, please contact Balmain Trilogy Investor Relations on 1800 194 500 or email [email protected]. Yours sincerely, Rodger Bacon Andrew Griffin Joint Chief Executive Joint Chief Executive Disclaimer: The information provided herein is provided by Trilogy Funds Management Limited ACN 080 383 679 (Trilogy Funds), AFS Licence 261425 in its capacity as Responsible Entity of the Pacific First Mortgage Fund ARSN 088 139 477 (Fund). The information contained herein is of a general nature and does not constitute financial product advice. This update has been prepared without taking into account any person’s objectives, financial situation or needs. Because of that, each person should, before acting on this update, consider its appropriateness, having regard to their own objectives, financial situation and needs. The information contained in this update is current as at the date of this update and is subject to change without notice. Past performance is not an indicator of future performance. Investment in the Fund is subject to investment risk, including possible delays in payment and loss of income and principal invested. Neither Trilogy Funds nor its associates, related entities or directors guarantee the performance of the Fund or the repayment of monies invested.

Pacific First Mortgage FundARSN 088 139 477

Annual Financial Report - 30 June 2016

Page

Directors' report 1

Auditor's independence declaration 7

Statement of profit or loss and other comprehensive income 8

Statement of financial position 9

Statement of cash flows 10

Notes to the financial statements 11

Directors' declaration 26

Independent auditor's report 27

Pacific First Mortgage FundContents page

Member of the Audit, Compliance and Risk ManagementCommitteeMember of the Lending CommitteeConsultant to several major public and private companiesproviding development management servicesDirector – Responsible Entity since 29 July 2008

Robert M WillcocksIndependent Non-Executive ChairmanBA, LL.B, LL.M

Member of the Audit, Compliance and Risk ManagementCommitteeFormer executive director of Challenger International LimitedMr Bacon is a former director of several public and privatecompanies including, Financial Services Institute ofAustralasia.Director – Responsible Entity since 9 July 2004

John C BarryExecutive DirectorBA, FCA

Chairman of the Audit, Compliance and Risk ManagementCommitteeFormer executive director of Challenger International LimitedMr Barry is a director of several public and privatecompanies, including Chairman of Westpac RE LimitedDirector – Responsible Entity since 9 July 2004

46

Member of the Audit, Compliance and Risk ManagementCommitteeFormer partner with Mallesons Stephen Jaques (now King &Wood Mallesons)Mr Willcocks has been a non-executive director (sometimesChairman) of a number of listed public companies and iscurrently such a director of three such companiesChairman - Responsible Entity since 9 October 2009

Rodger I BaconExecutive Deputy ChairmanBCom(Merit), AICD, SFFin

Peter J ArnoldDirector

Director of CYRE Trilogy Investment Management PtyLimited, a joint venture formed in 2011 between theResponsible Entity and Notgrove Holdings Pty LimitedDirector of Trilogy Property Partners (Briars) Pty LimitedFormer Executive Director of Austgrowth PropertySyndicates Limited and Austgrowth Investment ManagementPty LimitedDirector - Responsible Entity since 4 September 2014

67

70

64

55Philip A RyanExecutive Director and Company SecretaryLL.B, Grad Dip Leg Prac, FTIA, FFIN

Member of the Compliance CommitteeMr Ryan is a solicitor and member of the Queensland LawSociety Inc.Former partner of a Brisbane law firmMr Ryan is a director of several private companiesDirector – Responsible Entity since 13 October 1997

Rohan C ButcherNon-Executive DirectorGrad Dip PM, BASc(QS), Registered Builder, Licensed Real Estate Agent

56

Pacific First Mortgage FundDirectors' report

The Directors of Trilogy Funds Management Limited (Responsible Entity), the Responsible Entity of the PacificFirst Mortgage Fund (Scheme), present their report together with the financial statements of the Scheme forthe year ended 30 June 2016.

The Responsible Entity is incorporated and domiciled in Australia. The registered office and principal place ofbusiness of the Responsible Entity and the Scheme is Level 23, 10 Eagle Street, Brisbane, QLD, 4000.

The names of the directors in office at any time during, or since the end of the financial year are:

30 June 2016

Experience and special responsibilitiesName and qualifications

Responsible Entity

Directors

Age

1

Units on issue

During the year the Responsible Entity on behalf of the Scheme processed return of capital payments totalling$50,033,050 to unitholders (2015: $13,186,841). The return of capital did not result in any redemption ofunits.

Litigation recovery right (LRR)All unitholders were issued a LRR, for nil value, for each ordinary unit held in the Scheme on 15 March 2011.The LRR is a separate and transferrable entitlement that has been created to ensure all unitholders retain theright to their pro rata share of any net proceeds resulting from successful litigation undertaken. The Schemehad on issue 887,040,412 LRR units as at 30 June 2016 (2015: 887,040,412), and no further LRR units wereissued during the year (2015: nil), nor were any redeemed (2015: nil).

Pacific First Mortgage Fund

Total assets of the Scheme totalled $15,792,038 as at 30 June 2016 (2015: $54,888,395). The Scheme's totalasset position will continue to reduce as the litigation matters detailed in the Litigation and contingent liabilitiessection below are finalised and net Scheme assets are returned to unitholders.

The Responsible Entity processed two return of capital payments to unitholders during the year out ofproceeds received from sale of the remaining mortgage securities held by the Scheme during the 30 June2015 financial year, coupled with the settlement proceeds received from the Minter Ellison Gold Coast claimdetailed above. The first return of capital payment totalling $39,033,050 ($0.0444 per unit) was paid tounitholders on 16 September 2015, with the second payment totalling $11,000,000 ($0.0125 per unit) beingpaid on 17 December 2015.

Non-liquid SchemeThe Directors of the Former Responsible Entity resolved on 13 October 2008 that the Scheme was a non-liquid registered managed investment scheme in accordance with the Constitution and the Corporations Act2001.

Distributions to unitholders

30 June 2016

Income distributions to unitholders were suspended by the Directors of City Pacific Limited (FormerResponsible Entity), the previous responsible entity of the Scheme, in July 2008. Consequently no incomedistributions were paid or payable to unitholders during the financial year (2015: nil).

Hardship policy

Principal activities

Review of operations and results

Directors' report

The Scheme is a registered managed investment scheme domiciled in Australia. Following the sale of the lastremaining security property held by the Scheme over its mortgage loans in May 2015, the Scheme's principalactivity during the financial year has been to continue with the realisation of remaining Scheme assets whilethe ongoing litigation involving the Scheme is resolved (refer Litigation and contingent liabilities section below).The Scheme did not have any employees during the year.

The net profit attributable to unitholders for the year ended 30 June 2016 totalled $10,531,743 (2015: loss$3,984,344). The profit for the year is primarily attributable to proceeds received from the settlement of variouslitigation matters involving the Scheme, particularly the claim against Minter Ellison Gold Coast in respect oftheir involvement in a number of lending transactions which resulted in substantial losses for the Scheme. Thematter was settled on 9 September 2015.

During the year no units were issued (2015: nil), or redeemed from the Scheme (2015: nil). The Scheme had879,122,759 units on issue as at 30 June 2016 (2015: 879,122,759).

The Responsible Entity suspended the Scheme's ASIC approved hardship policy and as a result no hardshippayments were made during the year, nor were any units redeemed (2015: nil).

2

2016 2015$ $

382,280 986,834 (16,800) (230,589)

365,480 756,245 481,575 457,561 847,055 1,213,806

Indirect cost ratio (ICR)

Pacific First Mortgage Fund

Review of operations and results (continued)

Directors' report

Claim against former directors and officers of City Pacific Limited The Responsible Entity is pursuing a claim against former credit committee members and directors of CityPacific Limited (Former Responsible Entity), the former Responsible Entity of the Scheme.

The ICR for the Scheme for the year ended 30 June 2016 is 3.78% p.a. (2015: 2.01% p.a.).

ExpensesResponsible Entity management fees - gross (i)

30 June 2016

The ICR is the ratio of the Scheme's management costs over the Scheme's average net assets for the year,expressed as a percentage.

Litigation and contingent liabilities

Interests of the Responsible EntityThe following fees were paid to the Responsible Entity and its associates out of the Scheme property duringthe financial year (refer Note 11(c)).

The Responsible Entity (including its associates) does not hold any units in the Scheme as at 30 June 2016(2015: nil).

Significant changes in the state of affairs

(i) The Responsible Entity is entitled to a management fee of 1.50% p.a. (plus GST less RITC) calculated on the monthly gross asset value of the Scheme.

Other than the matters described in the Litigation and contingent liabilities section below, there has not arisenin the interval between the end of the financial year and the date of this report any item, transaction or eventof a material and unusual nature likely, in the opinion of the Responsible Entity, to affect significantly theoperations of the Scheme, the results of those operations, or the state of affairs of the Scheme, in futurefinancial years.

Responsible Entity management fees - reduction (ii)

In the opinion of the Responsible Entity there were no significant changes in the state of affairs of the Schemethat occurred during the period.

Events subsequent to the end of the reporting year

Expenses reimbursed (iii)

(ii) The Responsible Entity has only brought to account a reduced management fee in accordance with itscommitment to firstly return $0.04 per unit to unitholders in April 2011, and a further $0.04 per unit in October2011. At both of those times a reduced payment of only $0.01 per unit was paid to unitholders. Accordingly,the Responsible Entity has excluded the unpaid portion of the scheduled capital repayments from the grossasset value of the Scheme for purposes of calculating the management fee. Following the return of capitalpayments processed during the year the adjustment will no longer be required in future financial years.(iii) The Responsible Entity incurs costs on behalf of the Scheme for which it is reimbursed in accordance with the Constitution.

3

Principal

Daily accruing

interestTotal interest

accrued Total payable$ $ $ $

62,947,487 13,759 1,637,321 64,584,808 10,565,043 2,309 274,771 10,839,814

Pacific First Mortgage Fund

30 June 2016

Litigation and contingent liabilities (continued)

Claim against former directors and officers of City Pacific Limited (continued)Class action law firm Maurice Blackburn has been retained by the Responsible Entity to act for the Scheme.The original $60 million claim was filed on 27 April 2012 in the Federal Court in Sydney. The claim allegedbreaches by the former directors and officers of their statutory duties under the Corporations Act 2001. At thecentre of the original claim were loans provided by the Former Responsible Entity to borrowing entities BullishBear Holdings Pty Ltd (Receiver and Manager Appointed) (In Liquidation) (Bullish Bear) and Atkinson GoreAgricultural Pty Ltd (Receiver and Manager Appointed) (AGA) between 2006 and 2009, which culminated insubstantial losses to the Scheme.

On 18 December 2015, Justice Wigney awarded judgement in favour of the Scheme. Former Directors of CityPacific Limited; Mr Phil Sullivan, Mr Steve McCormick, Mr Ian Donaldson and Mr Thomas Swan were all foundto have breached section 601FD of the Corporations Act.

Subsequent hearings of the trial took place before Justice Wigney over two three-day periods, commencing15 April 2014 and 2 June 2014, with closing oral submissions being heard on 16, 17 and 18 July 2014.

(2) Mr Donaldson and Mr Swan are jointly and severally liable for $10.84 million in damages plus interest.

The total compensation owing, plus accrued interest as at 30 June 2016 is set out as follows:

On 16 March 2016 the Former Directors of City Pacific Limited lodged a Notice of Appeal. Additionally, thejudgement from the final orders was stayed, pending the hearing and determination of the appeal and certainconditions being met. It is understood that orders have been made for preparation of the appeal hearing,which is likely to be heard in November 2016.

On 22 May 2013 the Responsible Entity narrowed its original claim by removing the $16.9 million (plusinterest) claim in respect of the Bullish Bear loan facility to focus on the core claims arising from loanadvances made to AGA, which amount to $37.1 million (plus interest). The Responsible Entity was able toresist an application lodged by the defendants on 15 May 2013 to transfer the action to the Supreme Court ofQueensland, where a separate action is pursued by the Responsible Entity against the guarantors of theBullish Bear loan facility.

The initial phase of the matter commenced on 10 March 2014 and was conducted over an 8-day period (InitialHearing) before his Honour Justice Wigney in the Federal Court in Sydney. The Initial Hearing dealt withmatters relating to lending decisions made by former directors and officers of the Former Responsible Entity inregard to the Scheme’s loan to AGA. 890 documents, comprising over 9,300 pages, were tendered to thecourt in the Initial Hearing. The issues addressed in the Initial Hearing included the conduct of former directorsand officers at the time of approving increases in the AGA facility and the decision process undertaken bythem.

Judgement debtorMr Phil Sullivan & Mr Steve McCormick (1)Mr Ian Donaldson & Mr Thomas Swan (2)

Directors' report

(1) Mr Sullivan and McCormick are jointly and severally liable for $64.58 million in damages plus interest;

4

Based on advice from the Scheme's legal advisers, the Responsible Entity has resolved to retain $15,000,000of settlement proceeds within the Scheme as a safeguard against the potential costs, including adverse costs,that could arise from the litigation and also to satisfy the costs of operations while the litigation is finalised.Litigation retention funds will be paid out as and when the litigation matters are finalised. Following all fundsbeing repaid the Responsible Entity will commence the wind-up of the Scheme.

The operations of the Scheme are not subject to any particular or significant environmental regulation under alaw of the Commonwealth or of a State or Territory. There have been no known significant breaches of anyother environmental requirements applicable to the Scheme.

Environmental regulation

Further to the above, the Former Directors of City Pacific Limited are required to pay $144,000 by way ofsecurity for the Responsible Entity's costs for the appeal as part of the security of costs. The Former Directorsof City Pacific Limited also filed and served an Amended Notice of Appeal on 17 June 2016 incorporating anapplication to adduce further evidence.

At the date of this report, the outcome of all litigation involving the Former Directors of City Pacific Limited isunable to be determined, nor is it possible to determine the recoverability of the compensation if the originaljudgement stands.

Claim against former directors and officers of City Pacific Limited (continued)

Likely developments and expected results of operationsAs the Scheme's remaining mortgage security properties have now been sold it is the intention of theResponsible Entity to return the net proceeds to unitholders. The ability to return further capital to unitholdersis contingent upon the outcome of the various litigation currently involving the Scheme (refer Litigation andcontingent liabilities section above).

Directors' report30 June 2016

Litigation and contingent liabilities (continued)

Claim against the Scheme by King Tide Company Pty Ltd and Arawak Holdings Pty LtdDuring the year a claim was served on the Scheme by King Tide Company Pty Ltd and Arawak Holdings PtyLtd (plaintiff), a former borrower of the Scheme seeking damages of $5.23 million (plus interest and costs) onthe basis of non-performance by City Pacific Limited in relation to its role as lender for a transactionundertaken in 2007. The Responsible Entity has retained Maurice Blackburn to defend the claim who haveobtained an order for security for costs from the plaintiff. Maurice Blackburn have sought orders that securitybe in the form of cash or bank guarantee. A cross claim has been filed for the Responsible Entity seeking$20.2 million from the plaintiff for the outstanding principal owing on the loan transaction. At the date of thisreport the security for costs had not yet been paid.

Court proceedings against KPMGA claim against KPMG was filed in the Federal Court relating to their role as compliance plan auditor of theScheme. To ensure any potential action could be pursued and not time barred following KPMG’s 2008compliance plan audit, it was considered in the best interests of the Scheme to file the claim. This matter hasbeen set down for mediation in Sydney on 31 August 2016.

Pacific First Mortgage Fund

5

(i)(ii)

(a)

(b)

30 August 2016 30 August 2016

Philip A RyanManaging Director

Brisbane

Rodger I BaconExecutive Deputy Chairman

During the financial year, the Responsible Entity paid an insurance premium in respect of a contract insuringeach of the officers of the Responsible Entity. The amount of the premium is, under the terms of theinsurance contract, confidential. The liabilities insured include costs and expenses that may be incurred indefending civil or criminal proceedings that may be brought against the officers in their capacity as officers ofthe Responsible Entity or related body corporates. This insurance premium does not cover auditors. TheScheme has not indemnified any auditor of the Scheme.

Indemnification

Insurance premiums

A copy of the auditor’s independence declaration as required under section 307C of the Corporations Act2001 is set out on page 7.

This report is made in accordance with a resolution of the Directors of the Responsible Entity.

Auditor’s independence declaration

Brisbane

Granted to the Responsible Entity.

No unissued units in the Scheme were under option as at the date on which this report is made.

No units were issued in the Scheme during or since the end of the financial year as a result of the exercise ofan option over unissued units in the Scheme.

Indemnification of officers

any liability for costs and expenses which may be incurred by that person in defending civil or criminalproceedings in which judgement is given in that person’s favour, or in which the person is acquitted, orin the connection with an application in relation to any such proceedings in which the court grants reliefto the person under the Corporations Act 2001; anda liability incurred by the person, as an officer of the Responsible Entity or of a related body corporate,to another person (other than the Responsible Entity or a related body corporate) unless the liabilityarises out of conduct involving a lack of good faith.

Pacific First Mortgage FundDirectors' report30 June 2016

OptionsNo options were:

Granted over unissued units in the Scheme during or since the end of the financial year; or

6

Level 10, 12 Creek St Brisbane QLD 4000 GPO Box 457 Brisbane QLD 4001 Australia

Tel: +61 7 3237 5999 Fax: +61 7 3221 9227 www.bdo.com.au

BDO Audit Pty Ltd ABN 33 134 022 870 is a member of a national association of independent entities which are all members of BDO Australia Ltd ABN 77 050 110 275, an Australian company limited by guarantee. BDO Audit Pty Ltd and BDO Australia Ltd are members of BDO International Ltd, a UK company limited by guarantee, and form part of the international BDO network of independent member firms. Liability limited by a scheme approved under Professional Standards Legislation, other than for the acts or omissions of financial services licensees.

DECLARATION OF INDEPENDENCE BY P A GALLAGHER TO THE DIRECTORS OF TRILOGY FUNDS MANAGEMENT LIMITED AS RESPONSIBLE ENTITY FOR PACIFIC FIRST MORTGAGE FUND

As lead auditor of Pacific First Mortgage Fund for the year ended 30 June 2016, I declare that, to the best of my knowledge and belief, there have been:

1. No contraventions of the auditor independence requirements of the Corporations Act 2001 inrelation to the audit; and

2. No contraventions of any applicable code of professional conduct in relation to the audit.

P A Gallagher Director

BDO Audit Pty Ltd

Brisbane, 30 August 2016

7

Pacific First Mortgage Fund Auditor's Independence Declaration30 June 2016

Note 2016 2015$ $

Revenue and other income - 5,127,066

580,042 122,726 13,500,000 - 14,080,042 5,249,792

Expenses4 (46,690) (69,376)

• Trade and other receivables 6 - (4,092,813)• Mortgage loans 7 2,910 (655,205)

(3,139,039) (3,660,497)11(c) (365,480) (756,245)

(3,548,299) (9,234,136)

Profit/(loss) for the year before finance costs 10,531,743 (3,984,344)

• Interest expense - -

Profit/(loss) for the year attributable to unitholders 10,531,743 (3,984,344)

Other comprehensive incomeOther comprehensive income - -

10,531,743 (3,984,344)

For the year ended 30 June 2016

Total comprehensive income for the year attributable to unitholders

Pacific First Mortgage FundStatement of profit or loss and other comprehensive income

Interest revenue - mortgage loansInterest revenue - cash and cash equivalents

Auditor's remunerationImpairment gains/(losses):

Other expensesResponsible Entity management fees

Finance costs:

Litigation settlement proceeds

The statement of profit or loss and other comprehensive income should be read in conjunction with the accompanying notes 8

Note 2016 2015$ $

AssetsCash and cash equivalents 5 15,788,538 54,839,444 Trade and other receivables 6 3,500 48,951 Mortgage loans 7 - - Total assets 15,792,038 54,888,395

LiabilitiesTrade and other payables 8 1,848,847 1,443,897

1,848,847 1,443,897 9 13,943,191 53,444,498

15,792,038 54,888,395

Pacific First Mortgage FundStatement of financial positionAs at 30 June 2016

Total liabilities

Total liabilities (excluding liabilities attributable to unitholders)Net assets attributable to unitholders

The statement of financial position should be read in conjunction with the accompanying notes 9

Note 2016 2015$ $

Cash flows from operating activities - 789,732

580,042 119,924 Litigation settlement proceeds received 13,500,000 -

(740,919) (1,232,689) (2,913,079) (3,071,138)

Net cash provided by/(used in) operating activities 10 10,426,044 (3,394,171)

Cash flows from investing activities (112,991) (5,027,403) 115,901 71,255,045

Net cash provided by investing activities 2,910 66,227,642

Cash flows from financing activities (49,479,860) (12,343,864)

Net cash used in financing activities (49,479,860) (12,343,864)

Net (decrease)/increase in cash and cash equivalents (39,050,906) 50,489,607 Cash at beginning of the reporting period 54,839,444 4,349,837 Cash and cash equivalents at end of financial year 5 15,788,538 54,839,444

Mortgage loan funds advancedMortgage loan funds repaid

Payments for return of capital to unitholders

Pacific First Mortgage FundStatement of cash flowsFor the year ended 30 June 2016

Interest received - mortgage loansInterest received - cash and cash equivalents

Responsible entity management fees and reimbursementsOther costs paid

The statement of cash flows should be read in conjunction with the accompanying notes 10

(a)

(b)

(c)

•

In adopting the wind-up basis of reporting, the assets are stated at their anticipated settlement amounts. Theestimated net residual value of the asset represents the Responsible Entity's best estimate of the recoverablevalue of assets, net of selling expenses. Given the uncertainties in valuing assets on a wind-up basis, it is likelythat the valuation of assets included in these financial statements may differ from actual values on realisation.

The financial statements were approved by the Board of Directors of Trilogy Funds Management Limited on 30August 2016.

These financial statements are presented in Australian dollars, which is the Scheme’s functional currency.

The preparation of financial statements requires management to make judgements, estimates and assumptionsthat affect the application of accounting policies and the reported amounts of assets, liabilities, income andexpenses. Actual results may differ from these estimates.

The accounting policies set out below have been applied consistently to all periods presented in these financialstatements. The Scheme has not early adopted any accounting standard.

Pacific First Mortgage FundNotes to the financial statements30 June 2016

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimatesare recognised in the period in which the estimate is revised and in any future period affected.

In particular, information about significant areas of estimation uncertainty and critical judgements in applyingaccounting policies that have the most significant effect on the amounts recognised are disclosed in:

Pacific First Mortgage Fund (Scheme) is a registered managed investment scheme under the Corporations Act2001 (Act). The financial statements of the Scheme are for the year ended 30 June 2016, and have beenprepared on a wind-up basis rather than on a going concern basis. Under the wind-up basis of reporting, assetsand liabilities are presented in decreasing order of liquidity and are not distinguished between current and non-current. The Scheme is a for-profit entity.

The financial statements are a general purpose financial report which has been prepared in accordance withAustralian Accounting Standards including Australian Accounting Interpretations adopted by the AustralianAccounting Standards Board and the Act. The financial statements of the Scheme comply with InternationalFinancial Reporting Standards and interpretations in their entirety.

Reporting entityNote 1

Note 2 Basis of preparation

Statement of compliance

The Scheme was constituted on 23 June 1998 and will terminate on 23 June 2078, unless terminated inaccordance with the Scheme's Constitution. At this time, the Scheme is to realise all assets and satisfy allliabilities, with surplus funds being distributed to unitholders.

The remaining mortgage loans held by the Scheme were realised during the financial year ended 30 June 2015.As a result, it is the intention of Trilogy Funds Management Limited (Responsible Entity) to wind-up the Schemefollowing the completion of all litigation involving the Scheme (refer Note 14).

Functional and presentation currency

Key assumptions and sources of estimation

Note 12(a): Financial risk management (credit risk)

Note 3 Significant accounting policies

11

(a)

(ii) RecognitionThe Scheme recognises financial assets and financial liabilities on the date it becomes a party to the contractualprovisions of the instrument.

(iii) Measurement

(iv) Impairments

(i) ClassificationInvestments and financial assets in the scope of AASB 139 Financial Instruments: Recognition andMeasurement are categorised as either financial assets at fair value through profit or loss, loans andreceivables, held-to-maturity investments, or available-for-sale financial assets. The classification depends onthe purpose for which the investments were acquired or originated. Designation is re-evaluated at eachreporting date, but there are restrictions on reclassifying to other categories.

Note 3 Significant accounting policies (continued)

Financial instruments

Pacific First Mortgage Fund

30 June 2016Notes to the financial statements

Financial assets, other than those at fair value through profit or loss, are assessed for indicators of impairmentat the end of each reporting period. Financial assets are considered to be impaired when there is objectiveevidence that, as a result of one or more events that occurred after the initial recognition of the financial asset,the estimated future cash flows of the investment have been affected.

Financial instruments are measured initially at fair value plus transaction costs. Transaction costs on financialassets and financial liabilities are amortised over the life of the asset or liability using the effective interestmethod.

A financial liability is derecognised when the obligation specified in the contract is discharged, cancelled orexpires.

The Scheme uses the weighted average method to determine realised gains and losses on derecognition offinancial assets.

Financial assets are recognised using trade date accounting. From this date any gains and losses arising fromchanges in fair value of the financial assets or financial liabilities are recorded.

Loans and receivables are financial assets with fixed or determinable payments that are not quoted in an activemarket. Such assets are recognised initially at fair value plus any directly attributable transaction costs.Financial assets classified as loans and receivables subsequently are carried at amortised cost using theeffective interest rate method, less impairment losses, if any.

Financial liabilities, other than those at fair value through profit or loss, are measured at amortised cost usingthe effective interest rate.

(vi) Specific instruments - cash and cash equivalentsCash comprises current deposits with banks. Cash equivalents are short-term highly liquid investments that arereadily convertible to known amounts of cash, are subject to an insignificant risk of changes in value, and areheld for the purpose of meeting short-term cash commitments rather than for investment or other purposes.

An impairment loss in respect of a receivable carried at amortised cost is reversed if the subsequent increase inrecoverable amount can be related objectively to an event occurring after the impairment loss was recognised.

(v) DerecognitionThe Scheme derecognises a financial asset when the contractual rights to the cash flows from the financialasset expire or it transfers the financial asset and the transfer qualifies for derecognition in accordance withAASB 139 Financial instruments: Recognition and Measurement .

12

(b)

(c)

(d)

(e)

(f)

Under current legislation the Scheme is not subject to income tax as its taxable income including assessablerealised capital gains is distributed in full to the unitholders. The Scheme fully distributes its distributableincome, calculated in accordance with the Scheme’s constitution and applicable taxation legislation, to theunitholders who are presently entitled to the income under the constitution.

Financial instruments held at fair value may include unrealised capital gains. Should such a gain be realised that portion of the gain that is subject to capital gains tax will be distributed so that the Scheme is not subject tocapital gains tax.

Taxation

All expenses, including management fees, are recognised in the statement of profit or loss and othercomprehensive income on an accruals basis.

Revenue is recognised and measured at the fair value of the consideration received or receivable to the extentit is probable that the economic benefits will flow to the Scheme and the revenue can be reliably measured. Thefollowing specific recognition criteria must also be met before income is recognised.

Revenue is recognised as the interest accrues (using the effective interest rate method) to the net carryingamount of the financial asset. All revenue is stated net of the amount of goods and services tax (GST).

Revenue and income recognition

Expenses

30 June 2016

Pacific First Mortgage FundNotes to the financial statements

Terms and conditions of units on issue

- receive income and capital distributions; - attend and vote at meetings of unitholders; and - participate in the termination and winding up of the Scheme.

The Scheme is not required to complete a statement of changes in equity as all unitholder funds have beenclassified as a financial liability.

(i) Interest revenue - mortgage loans and interest revenue

(ii) Changes in the fair value of investmentsNet gains or losses on investments held for trading or designated as at fair value through profit or loss arecalculated as the difference between the fair value at sale, or at year end, and the fair value at the previousvaluation point. This includes both realised and unrealised gains and losses, but does not include interest ordividend revenue.

Each unit confers upon the unitholder an equal interest in the Scheme and is of equal value. A unit does notconfer an interest in any particular asset or investment of the Scheme. Unitholders have various rights underthe Constitution and the Corporations Act 2001, including the right to:

- have their units redeemed;

Realised capital losses are not distributed to unitholders but are retained in the Scheme to be offset against anyfuture realised capital gains. If realised capital gains exceeds realised capital losses the excess is distributed tothe unitholders.

The unit price is based on unit price accounting outlined in the Scheme's Constitution and Product DisclosureStatement (PDS).

Unit prices

Note 3 Significant accounting policies (continued)

13

(g)

(h)

(i)

(j)

(k)

(l)

Rental income, management fees, custody fees and other expenses are recognised net of the amount of GSTrecoverable from the Australian Taxation Office (ATO) as a reduced input tax credit (RITC).

Receivables are recorded at amortised cost less impairment and may include amounts for distributions andinterest. Distributions are accrued when the right to receive payment is established. Interest is accrued at thereporting date from the time of last payment. Amounts are generally received within 30 days of being recordedas receivables.

Units issued to unitholders represent a right to an individual share in the Scheme and does not extend to a rightto the underlying assets of the Scheme.

Litigation recovery right (LRR)The LRR is a separate and transferrable entitlement that has been created to ensure all unitholders retain theright to their pro rata share of any net proceeds resulting from successful litigation undertaken.

Note 3 Significant accounting policies (continued)

Trade and other receivables

Goods and services tax

Increase/decrease in net assets attributable to unitholders

Issued units

Borrowing costs

Payables are stated with the amount of GST included.

Ordinary units

30 June 2016

Non-distributable income is transferred directly to net assets attributable to unitholders. This balancerepresents unrealised gains and losses due to the change in the fair value of investments. These gains andlosses have been recognised in the statement of profit or loss and other comprehensive income in either thecurrent or a previous period, and have not been distributed to unitholders.

Pacific First Mortgage FundNotes to the financial statements

Once the gains and losses have been realised, these items are distributed to unitholders. Income recognitiondifferences consist of accrued income not yet assessable, expenses provided or accrued which are not yetdeductible, net capital losses and tax free or tax deferred income.

The GST recoverable from the ATO is included in trade and other receivables, while GST payable to the ATO isincluded in trade and other payables, both of which are presented in the statement of financial position.

Cash flows are included in the statement of cash flows on a gross basis.

Borrowing costs directly attributable to the acquisition, construction or production of assets that necessarily takea substantial period of time to prepare for their intended use or sale, are added to the cost of those assets, untilsuch time as the assets are substantially ready for their intended use or sale.

All other borrowing costs are recognised in the profit or loss in the period in which they are incurred.

Trade and other payables represent the liability outstanding at the end of the reporting period for goods andservices received by the Scheme during the reporting period, which remains unpaid. The balance is recognisedas a current liability with the amounts normally paid within 30 days of recognition of the liability.

Trade and other payables

14

(m)

(n)

(o)

(i) AASB 9 Financial Instruments (Dec 2014)

30 June 2016Notes to the financial statementsPacific First Mortgage Fund

Impact to the Scheme

Nature of change

The Standard contains a single model that applies to contracts with customers and twoapproaches to recognising revenue: at a point in time or over time. The model features acontract-based five-step analysis of transactions to determine whether, how much and whenrevenue is recognised.

Application date 30 June 2018Impact to the Scheme

The Scheme has not yet assessed the full impact of this Standard.

Impairment of assetsAt the end of each reporting period, the Responsible Entity assesses whether there is any indication that anasset may be impaired. The assessment will include considering external and internal sources of information. Ifsuch an indication exists, an impairment test is carried out on the asset by comparing the recoverable amount ofthe asset to its carrying value. Any excess of the asset’s carrying value over its recoverable amount isexpensed to the statement of profit or loss and other comprehensive income.

When required by Accounting Standards, comparative figures have been adjusted to conform to changes inpresentation for the current year.

Certain new Accounting Standards and Interpretations have been published that are not mandatory for 30 June2016 reporting periods and have not been early adopted by the Scheme. The Scheme’s assessment of theimpact of these new Standards and Interpretations is set out below.

Note 3 Significant accounting policies (continued)

Where it is not possible to estimate the recoverable amount of an individual asset, the Responsible Entityestimates the recoverable amount of the cash-generating unit to which the asset belongs.

Comparative figures

New standards and interpretations not yet adopted

(ii) AASB 15 Revenue from Contracts with Customers

The AASB has issued the complete AASB 9. The new Standard includes revised guidance onthe classification and measurement of financial assets, including a new expected credit lossmodel for calculating impairment, and supplements the new general hedge accountingrequirements previously published. This supersedes AASB 9 (issued in December 2009-asamended) and AASB 9 (issued in December 2010). 30 June 2019AASB 9 may have a potential increase in the Scheme’s loans and advances provisioning.However, the Scheme has not yet fully assessed the impact of AASB 9 as this Standard doesnot apply mandatorily before 1 January 2018.

Nature of change

Application date

15

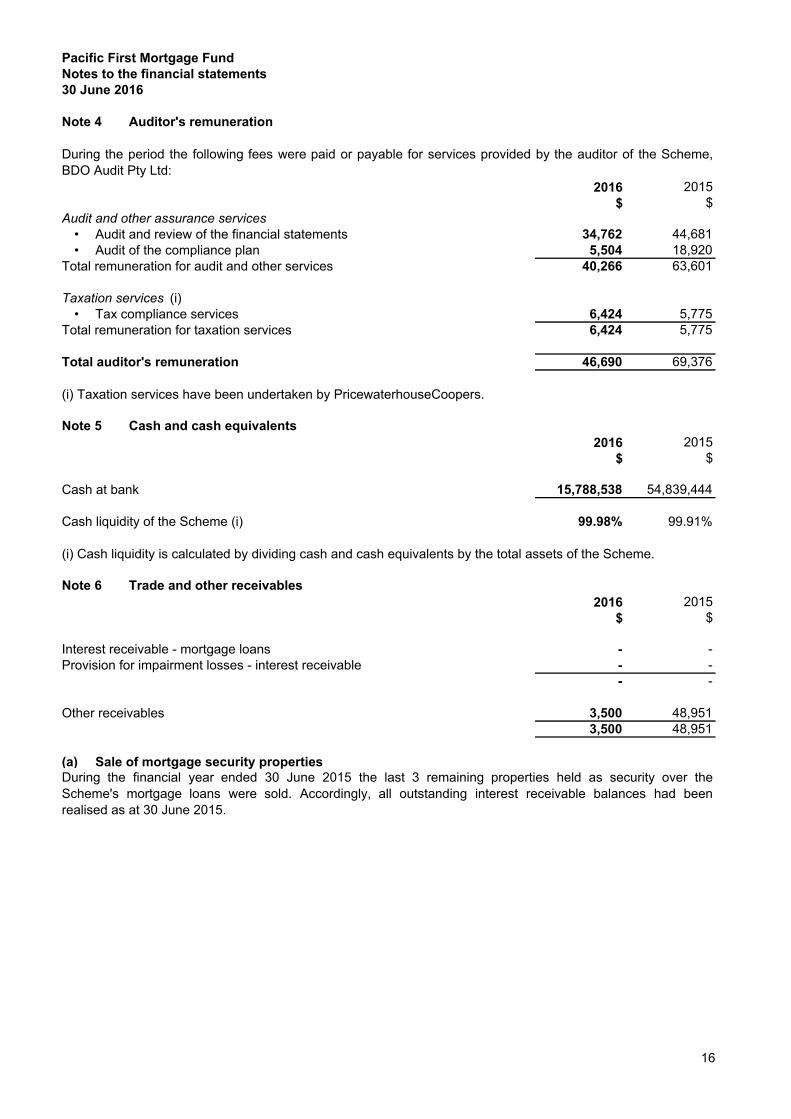

2016 2015$ $

• 34,762 44,681 • 5,504 18,920

40,266 63,601

• 6,424 5,775 6,424 5,775

46,690 69,376

2016 2015$ $

15,788,538 54,839,444

99.98% 99.91%

2016 2015$ $

- - - - - -

3,500 48,951 3,500 48,951

(a)

Audit of the compliance planAudit and review of the financial statements

Cash liquidity of the Scheme (i)

(i) Cash liquidity is calculated by dividing cash and cash equivalents by the total assets of the Scheme.

Other receivables

Tax compliance services

Note 5 Cash and cash equivalents

Taxation services (i)

Total remuneration for audit and other services

Notes to the financial statements

Audit and other assurance services

Note 4 Auditor's remuneration

Pacific First Mortgage Fund

During the period the following fees were paid or payable for services provided by the auditor of the Scheme,BDO Audit Pty Ltd:

30 June 2016

Cash at bank

Total remuneration for taxation services

Total auditor's remuneration

(i) Taxation services have been undertaken by PricewaterhouseCoopers.

Note 6 Trade and other receivables

Sale of mortgage security properties

Interest receivable - mortgage loansProvision for impairment losses - interest receivable

During the financial year ended 30 June 2015 the last 3 remaining properties held as security over theScheme's mortgage loans were sold. Accordingly, all outstanding interest receivable balances had beenrealised as at 30 June 2015.

16

(b)

2016 2015$ $

- 2,214,684 Realised (gains)/losses from sale of mortgage security properties - 1,878,129

- 4,092,813

Opening Charge for Amounts Closing balance the year written off (i) balance

$ $ $ $

- - - -

70,901,679 2,214,684 (73,116,363) -

2016 2015$ $

- - - - - -

(a)

(b)

2016 2015$ $

- 4,546,202 (2,910) (3,890,997) (2,910) 655,205

Provision for impairment losses - mortgage loansMortgage loans

During the financial year ended 30 June 2015 the last 3 remaining properties held as security over theScheme's mortgage loans were sold. Accordingly, all outstanding mortgage loan balances had been realised asat 30 June 2015.

Note 7 Mortgage loans

Sale of mortgage security properties

Impairments

Pacific First Mortgage FundNotes to the financial statements30 June 2016

Note 6 Trade and other receivables (continued)

Provision for impairment following balance date reviews

Impairment charges

Impairments

Movement in the provision for impairment loss on interest receivable is as follows:

Impairment charges recognised in the statement of profit or loss and other comprehensive income arereconciled as follows:

Provision for impairment losses - interest receivable

2016Interest receivable - mortgage loans

2015Interest receivable - mortgage loans

(i) Amounts written off represents the balance of provision for impairment losses cleared from the statement offinancial position for mortgage loans whose underlying security property was sold during the prior year.

Provision for impairment following balance date reviews

Held directly

Realised (gains)/losses from sale of mortgage security properties

Impairment chargesImpairment charges recognised in the statement of profit or loss and other comprehensive income arereconciled as follows:

17

(b)

Opening Charge for Amounts Closing balance the year written off (i) balance

$ $ $ $

- - - -

231,871,036 4,546,202 (236,417,238) -

2016 2015$ $

423,431 560,022 Unpaid return of capital (i) 1,391,370 838,180

24,046 35,695 10,000 10,000 1,848,847 1,443,897

Note 9

Accumulated Ordinary Contributed Accumulatedprofits units capital profits

$ No $ $53,444,498 879,122,759 798,621,273 70,615,683

- - - - - - - -

(50,033,050) - (13,186,841) (13,186,841)10,531,743 - - (3,984,344)13,943,191 879,122,759 785,434,432 53,444,498

2016 20150.02 0.06

Accrued audit and taxation fees

(i) Return of capital monies remain outstanding for a number of unitholders due to necessary banking detailsbeing unavailable at the time of processing, thus preventing the payments from being made. The ResponsibleEntity will continue to process sporadic payments as updated banking details are obtained.

Trade payables

Other payables

- -

Net assets attributable to unitholders

(50,033,050)

Net asset value per unitCents per unit as at 30 June

20152016

- - -

-

Balance - 1 Jul

Return of capital

879,122,759

30 June 2016

879,122,759 Balance - 30 June

Interest receivable - mortgage loans

2015

Pacific First Mortgage Fund

Trade and other payables

735,401,382

Ordinaryunits

No

Contributedcapital

$

Units issuedUnits redeemed

-

Units in the Scheme entitle the unitholder to participate in distributions and proceeds on the winding up of theScheme in proportion to the number of units held.

On a show of hands each unitholder present at a meeting in person or by proxy is entitled to one vote, and on apoll each member has one vote for each dollar of the value of the total units they have in the Scheme.

TCI* for the year

* TCI = Total comprehensive income

Note 8

785,434,432

Provision for impairment losses - mortgage loansMovement in the provision for impairment loss on mortgage loans is as follows:

2016

Note 7 Mortgage loans (continued)

Impairments (continued)

Interest receivable - mortgage loans

(i) Amounts written off represents the balance of provision for impairment losses cleared from the statement offinancial position for mortgage loans whose underlying security property was sold during the prior year.

Notes to the financial statements

18

Note 9

2016 2015$ $

10,531,743 (3,984,344)

(2,910) 4,748,018 - (4,337,334)

45,451 755,209 (148,240) (559,679)

- (16,041) 10,426,044 (3,394,171)

(a)

(b)

Note 10 Reconciliation of cash flows from operating activities

Net assets attributable to unitholders (continued)

The Responsible Entity of the Pacific First Mortgage Fund is Trilogy Funds Management Limited ABN 59 080383 679. City Pacific Limited ceased to act as Responsible Entity of the Scheme on 7 July 2009.

Notes to the financial statements30 June 2016

Adjustments for:Decrease in trade and other payables

No compensation is paid to the Directors of the Responsible Entity or to the key personnel of the ResponsibleEntity by the Scheme.

The Scheme does not employ personnel in its own right. However it is required to have an incorporatedResponsible Entity to manage the activities of the Scheme. The Executive Directors of the Responsible Entityare key personnel of that entity and their names are Rodger I Bacon, John C Barry, Philip A Ryan. Peter JArnold is transitioning from an Executive Director to a Non-Executive Director position. The Responsible Entityalso has two Non-Executive Directors being Robert M Willcocks and Rohan C Butcher.

The Responsible Entity is entitled to a management fee which is calculated as a proportion of total gross assetsof the Scheme.

Key management personnel

Profit/(loss) for the year attributable to unitholders

Pacific First Mortgage Fund

Related party transactions

Responsible Entity

Note 11

Litigation recovery right (LRR)All unitholders were issued a LRR, for nil value, for each ordinary unit held in the Scheme on 15 March 2011.The LRR is a separate and transferrable entitlement that has been created to ensure all unitholders retain theright to their pro rata share of any net proceeds resulting from successful litigation undertaken. The Schemehad on issue 887,040,412 LRR units as at 30 June 2016 (2015: 887,040,412), and no further LRR units wereissued during the year (2015: nil), nor were any redeemed (2015: nil).

Adjustments for:Net loss on fair value adjustmentsInterest revenue - mortgage loans

Changes in operating assets and liabilities:Decrease in trade and other receivablesDecrease in trade and other payables

Net cash provided by/(used in) operating activities

19

(c)

i.

2016 2015$ $

382,280 986,834 (16,800) (230,589) 365,480 756,245 481,575 457,561 847,055 1,213,806

ii.

2016 2015$ $

51,248 98,123

(d)

(e)

(f)

Trade and other payables (i)(ii)(iii)

Balances recorded in the statement of financial position

Pacific First Mortgage FundNotes to the financial statements30 June 2016

Transactions with related parties

(i) The Responsible Entity is entitled to a management fee of 1.50% p.a. (plus GST less RITC) calculated on themonthly gross asset value of the Scheme.

Transactions recorded in the statement of profit or loss and other comprehensive income

Note 11 Related party transactions (continued)

Transactions between related parties are on normal commercial terms and conditions no more favourable thanthose available to other parties unless otherwise stated.

The following transactions occurred with related parties:

ExpensesResponsible Entity management fees - gross (i)

The Scheme has not made, guaranteed or secured, directly or indirectly, any loans to the key managementpersonnel or their personally related entities at any time during the reporting period.

Apart from those details disclosed in this note, no Director has entered into a material contract with the Schemefrom inception to the end of the financial year and there were no material contracts involving Directors' interestssubsisting at year end.

(ii) The Responsible Entity has only brought to account a reduced management fee in accordance with itscommitment to firstly return $0.04 per unit to unitholders in April 2011, and a further $0.04 per unit in October2011. At both of those times a reduced payment of only $0.01 per unit was paid to unitholders. Accordingly, theResponsible Entity has excluded the unpaid portion of the scheduled capital repayments from the gross assetvalue of the Scheme for purposes of calculating the management fee. Following the return of capital paymentsprocessed during the year the adjustment will no longer be required in future financial years.(iii) The Responsible Entity incurs costs on behalf of the Scheme for which it is reimbursed in accordance withthe Constitution.

The Scheme has no investment in the Responsible Entity or its associates (2015: nil).

Expenses reimbursed (iii)

Responsible Entity management fees - reduction (ii)

Related party investments held by the Scheme

Key management personnel loan disclosures

Other transactions within the Scheme

20

(a)

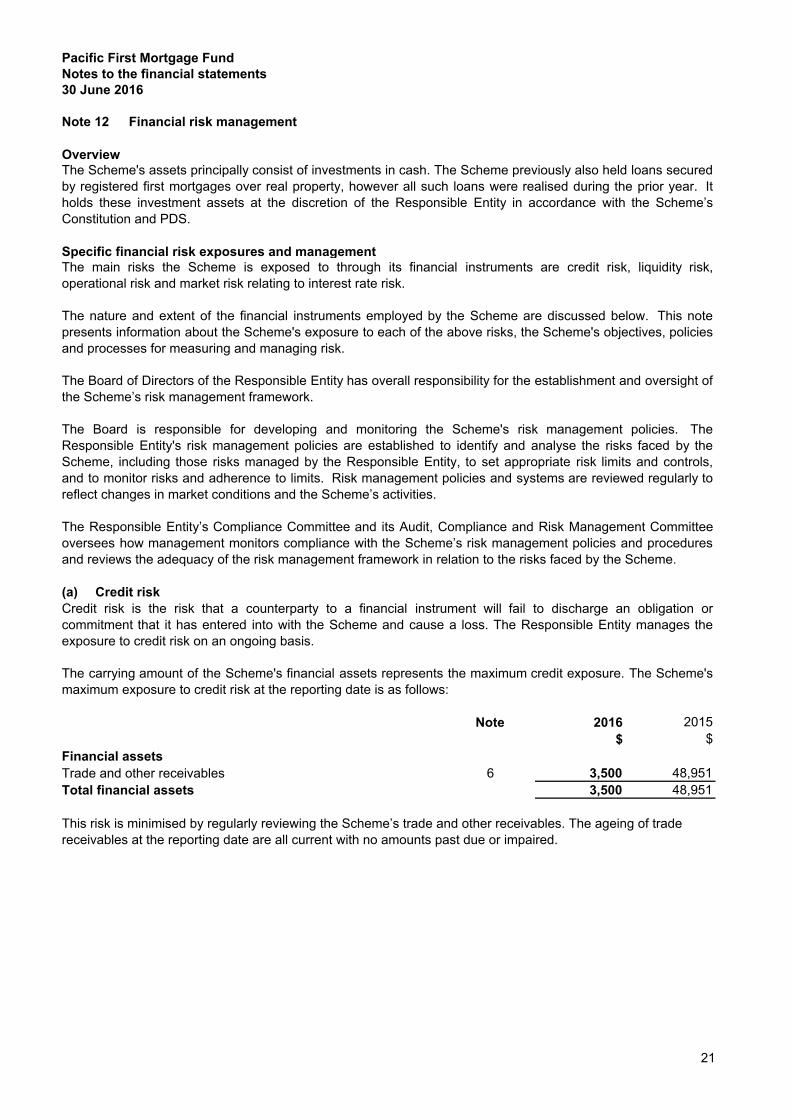

Note 2016 2015$ $

6 3,500 48,951 3,500 48,951

The carrying amount of the Scheme's financial assets represents the maximum credit exposure. The Scheme'smaximum exposure to credit risk at the reporting date is as follows:

This risk is minimised by regularly reviewing the Scheme’s trade and other receivables. The ageing of trade receivables at the reporting date are all current with no amounts past due or impaired.

The Board is responsible for developing and monitoring the Scheme's risk management policies. TheResponsible Entity's risk management policies are established to identify and analyse the risks faced by theScheme, including those risks managed by the Responsible Entity, to set appropriate risk limits and controls,and to monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly toreflect changes in market conditions and the Scheme’s activities.

The Responsible Entity’s Compliance Committee and its Audit, Compliance and Risk Management Committeeoversees how management monitors compliance with the Scheme’s risk management policies and proceduresand reviews the adequacy of the risk management framework in relation to the risks faced by the Scheme.

Credit risk is the risk that a counterparty to a financial instrument will fail to discharge an obligation orcommitment that it has entered into with the Scheme and cause a loss. The Responsible Entity manages theexposure to credit risk on an ongoing basis.

The Scheme's assets principally consist of investments in cash. The Scheme previously also held loans securedby registered first mortgages over real property, however all such loans were realised during the prior year. Itholds these investment assets at the discretion of the Responsible Entity in accordance with the Scheme’sConstitution and PDS.

Specific financial risk exposures and managementThe main risks the Scheme is exposed to through its financial instruments are credit risk, liquidity risk,operational risk and market risk relating to interest rate risk.

The nature and extent of the financial instruments employed by the Scheme are discussed below. This notepresents information about the Scheme's exposure to each of the above risks, the Scheme's objectives, policiesand processes for measuring and managing risk.

Pacific First Mortgage Fund

Trade and other receivablesTotal financial assets

Financial assets

Notes to the financial statements30 June 2016

Overview

The Board of Directors of the Responsible Entity has overall responsibility for the establishment and oversight ofthe Scheme’s risk management framework.

Note 12 Financial risk management

Credit risk

21

(b)

Contractualcash flows < 3 months 3-6 months 6-12 months

$ $ $ $

Financial liabilities 13,943,191 - - 13,943,191 1,848,847 1,848,847 - - 15,792,038 1,848,847 - 13,943,191

Financial liabilities 53,444,498 - - 53,444,498 1,443,897 1,443,897 - - 54,888,395 1,443,897 - 53,444,498

(c)

•

•

(d)

i.

Financial risk management (continued)

13,943,191 1,848,847 15,792,038

Note 12

Liquidity risk

The Scheme's capital management objectives aim to:

Capital management

ensure that the Scheme complies with capital and distribution requirements of its Constitution and PDS; and

The Scheme’s objective was designed to provide investors with regular income from a pool of high yieldingmortgage loans secured by registered first and second mortgages over real property and in certaincircumstances collateral security. However given, amongst other things, the default by developers, the reductionin the market values and the inability to sell assets at reasonable prices, the Scheme was forced to suspenddistributions to investors and subsequently commence liquidation of all Scheme assets in order to return capitalto unitholders.

Interest rate risk

ensure sufficient capital resources to support the Scheme's operational requirements.

$2016

The tables below reflect an undiscounted contractual maturity analysis for financial liabilities.

Carryingamount

53,444,498

Unitholder fundsTrade and other payables

Unitholder funds

Market risk is the risk that changes in market prices, such as interest rates, will affect the Scheme’s income orthe value of its holdings of financial instruments. Market risk embodies the potential for both loss and gains.The objective of market risk management is to manage and control market risk exposures within acceptableparameters, while optimising the return on risk.

The Scheme has no financial liabilities as at 30 June 2016 (2015: nil) and therefore has no exposure to interestrate risk.

The Scheme's capital management strategy seeks to maximise the return of capital to unitholders throughoptimising the level and use of capital resources and the mix of debt funding.

2015

Pacific First Mortgage FundNotes to the financial statements30 June 2016

Trade and other payables 1,443,897 54,888,395

Market risk

22

(d)

Profit / Unitholder(loss) funds

$ $

353,140 353,140 (353,140) (353,140)

629,575 629,575 (629,575) (629,575)

ii.

(e)

The Responsible Entity is pursuing a claim against former credit committee members and directors of City Pacific Limited (Former Responsible Entity), the former Responsible Entity of the Scheme.

2015Financial assets*

Market risk (continued)

Note 14 Litigation and contingent liabilities

Interest rate sensitivity analysis

The relationship between the custodian and Responsible Entity is set out in the Custodial Agreement.

Claim against former directors and officers of City Pacific Limited

The fair values of financial assets and liabilities approximate their carrying value. No financial assets orliabilities are readily traded on organised markets in standardised form.

The Scheme’s custodian is The Trust Company (Australia) Limited. The custodian holds title to the assets ofthe Scheme in its name on behalf of the Scheme. The total value of assets held by the custodian at cost as at30 June 2016 totals $15,792,038 (2015: $54,888,395).

The Scheme's remaining mortgage loans, secured by registered first and second mortgages over real propertyin Australia, were all realised during the prior year. Prior to the realisation, the majority of the Scheme's financialassets were subject to property value risk in the prevailing levels of market property values.

The Scheme's financial assets are subject to variable interest rates. The following table indicates the impact onhow profit and equity values reported at the end of the financial year would have been affected by a 1.00%increase/decrease in interest rates during the year.

2016Financial assets*+1.00% in interest rates

The custodian is entitled to an annual administration fee of $15,000 (plus GST) (2015: $15,000 (plus GST)),which is paid by the Scheme.

-1.00% in interest rates

Pacific First Mortgage FundNotes to the financial statements30 June 2016

Note 12 Financial risk management (continued)

The aggregate fair values and carrying amounts of financial assets and liabilities are disclosed in the statementof financial position and in the notes to the financial statements.

Fair value estimation

Note 13 Custodian of the Scheme

+1.00% in interest rates-1.00% in interest rates

* Includes cash and cash equivalents and mortgage loans (net of impairment losses).

Property value risk

23

Principal

Dailyaccruing

interestTotal interest

accrued Total payable$ $ $ $

62,947,487 13,759 1,637,321 64,584,808 62,947,487 13,759 1,637,321 64,584,808 10,565,043 2,309 274,771 10,839,814 10,565,043 2,309 274,771 10,839,814

The initial phase of the matter commenced on 10 March 2014 and was conducted over an 8-day period (InitialHearing) before his Honour Justice Wigney in the Federal Court in Sydney. The Initial Hearing dealt withmatters relating to lending decisions made by former directors and officers of the Former Responsible Entity inregard to the Scheme’s loan to AGA. 890 documents, comprising over 9,300 pages, were tendered to the courtin the Initial Hearing. The issues addressed in the Initial Hearing included the conduct of former directors andofficers at the time of approving increases in the AGA facility and the decision process undertaken by them.

Subsequent hearings of the trial took place before Justice Wigney over two three-day periods, commencing 15April 2014 and 2 June 2014, with closing oral submissions being heard on 16, 17 and 18 July 2014.

The total compensation owing, plus accrued interest as at 30 June 2016 is set out as follows:

Litigation and contingent liabilities (continued)

Further to the above, the Former Directors of City Pacific Limited are to required pay $144,000 by way ofsecurity for the Responsible Entity's costs for the appeal as part of the security of costs. The Former Directors ofCity Pacific Limited also filed and served an Amended Notice of Appeal on 17 June 2016 incorporating anapplication to adduce further evidence.

Mr Phil Sullivan (1)Mr Steve McCormick (1)Mr Ian Donaldson (2)Mr Thomas Swan (2)

Judgement debtor

(1) Mr Sullivan and McCormick are jointly and severally liable for $64.58 million in damages plus interest;

On 18 December 2015, Justice Wigney awarded judgement in favour of the Scheme. Former Directors of CityPacific Limited; Mr Phil Sullivan, Mr Steve McCormick, Mr Ian Donaldson and Mr Thomas Swan were all foundto have breached section 601FD of the Corporations Act.

Note 14

Claim against former directors and officers of City Pacific Limited (continued)

Notes to the financial statements30 June 2016

Class action law firm Maurice Blackburn has been retained by the Responsible Entity to act for the Scheme.The original $60 million claim was filed on 27 April 2012 in the Federal Court in Sydney. The claim allegedbreaches by the former directors and officers of their statutory duties under the Corporations Act 2001. At thecentre of the original claim were loans provided by the Former Responsible Entity to borrowing entities BullishBear Holdings Pty Ltd (Receiver and Manager Appointed) (In Liquidation) (Bullish Bear) and Atkinson GoreAgricultural Pty Ltd (Receiver and Manager Appointed) (AGA) between 2006 and 2009, which culminated insubstantial losses to the Scheme.

On 22 May 2013 the Responsible Entity narrowed its original claim by removing the $16.9 million (plus interest)claim in respect of the Bullish Bear loan facility to focus on the core claims arising from loan advances made toAGA, which amount to $37.1 million (plus interest). The Responsible Entity was able to resist an applicationlodged by the defendants on 15 May 2013 to transfer the action to the Supreme Court of Queensland, where aseparate action is pursued by the Responsible Entity against the guarantors of the Bullish Bear loan facility.

Pacific First Mortgage Fund

(2) Mr Donaldson and Mr Swan are jointly and severally liable for $10.84 million in damages plus interest.

On 16 March 2016 the Former Directors of City Pacific Limited lodged a Notice of Appeal. Additionally, thejudgement from the final orders was stayed, pending the hearing and determination of the appeal and certainconditions being met. It is understood that orders have been made for preparation of the appeal hearing, whichis likely to be heard in November 2016.

24

At the date of this report, the outcome of all litigation involving the Former Directors of City Pacific Limited isunable to be determined, nor is it possible to determine the recoverability of the compensation if the originaljudgement stands.

A claim against KPMG was filed in the Federal Court relating to their role as compliance plan auditor of theScheme. To ensure any potential action could be pursued and not time barred following KPMG’s 2008compliance plan audit, it was considered in the best interests of the Scheme to file the claim. This matter hasbeen set down for mediation in Sydney on 31 August 2016.

During the year a claim was served on the Scheme by King Tide Company Pty Ltd and Arawak Holdings Pty Ltd(plaintiff), a former borrower of the Scheme seeking damages of $5.23 million (plus interest and costs) on thebasis of non-performance by City Pacific Limited in relation to its role as lender for a transaction undertaken in2007. The Responsible Entity has retained Maurice Blackburn to defend the claim who have obtained an orderfor security for costs from the plaintiff. Maurice Blackburn have sought orders that security be in the form ofcash or bank guarantee. A cross claim has been filed for the Responsible Entity seeking $20.2 million from theplaintiff for the outstanding principal owing on the loan transaction. At the date of this report the security forcosts had not yet been paid.

Court proceedings against KPMG

Claim against the Scheme by King Tide Company Pty Ltd and Arawak Holdings Pty Ltd

Pacific First Mortgage FundNotes to the financial statements30 June 2016

Note 14 Litigation and contingent liabilities (continued)

Claim against former directors and officers of City Pacific Limited (continued)

Other than the matters described in Note 14 Litigation and contingent liabilities, there has not arisen in theinterval between the end of the financial year and the date of this report any item, transaction or event of amaterial and unusual nature likely, in the opinion of the Responsible Entity, to affect significantly the operationsof the Scheme, the results of those operations, or the state of affairs of the Scheme, in future financial years.

Note 15 Events subsequent to reporting date

25

(a)

(i)

(ii)

(b)

(c)

Managing Director Executive Deputy Chairman

Brisbane Brisbane30 August 2016 30 August 2016

Philip A Ryan Rodger I Bacon

Pacific First Mortgage FundDirectors' declaration

In the opinion of the Directors of Trilogy Funds Management Limited (Responsible Entity), the ResponsibleEntity of Pacific First Mortgage Fund (Scheme):

The financial statements and notes, as set out on pages 8 to 25 are in accordance with theCorporations Act 2001, including:

giving a true and fair view of the Scheme's financial position as at 30 June 2016 and of itsperformance, for the financial year ended on that date; and

complying with Australian Accounting Standards (including the Australian AccountingInterpretations) and the Corporations Regulations 2001;

the financial report also complies with International Financial Reporting Standards as disclosed in Note2; and

There are reasonable grounds to believe that the Scheme will be able to pay its debts as and when theybecome due and payable.

Signed in accordance with a resolution of the Board of Directors of the Responsible Entity.

26

Level 10, 12 Creek St Brisbane QLD 4000 GPO Box 457 Brisbane QLD 4001 Australia

Tel: +61 7 3237 5999 Fax: +61 7 3221 9227 www.bdo.com.au

BDO Audit Pty Ltd ABN 33 134 022 870 is a member of a national association of independent entities which are all members of BDO Australia Ltd ABN 77 050 110 275, an Australian company limited by guarantee. BDO Audit Pty Ltd and BDO Australia Ltd are members of BDO International Ltd, a UK company limited by guarantee, and form part of the international BDO network of independent member firms. Liability limited by a scheme approved under Professional Standards Legislation, other than for the acts or omissions of financial services licensees.

INDEPENDENT AUDITOR’S REPORT

To the unitholders of Pacific First Mortgage Fund

Report on the Financial Report

We have audited the accompanying financial report of Pacific First Mortgage Fund, which comprises the statement of financial position as at 30 June 2016, the statement of profit or loss and other comprehensive income and statement of cash flows for the year then ended, notes comprising a summary of significant accounting policies and other explanatory information, and the directors’ declaration.

Directors’ of the Responsible Entity’s Responsibility for the Financial Report

The directors of the responsible entity are responsible for the preparation of the financial report that gives a true and fair view in accordance with Australian Accounting Standards and the Corporations Act 2001 and for such internal control as the directors of the responsible entity determine is necessary to enable the preparation of the financial report that gives a true and fair view and is free from material misstatement, whether due to fraud or error. In Note 2, the directors also state, in accordance with Accounting Standard AASB 101 Presentation of Financial Statements, that the financial statements comply with International Financial Reporting Standards.

Auditor’s Responsibility

Our responsibility is to express an opinion on the financial report based on our audit. We conducted our audit in accordance with Australian Auditing Standards. Those standards require that we comply with relevant ethical requirements relating to audit engagements and plan and perform the audit to obtain reasonable assurance about whether the financial report is free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial report. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial report, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the scheme’s preparation of the financial report that gives a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the scheme’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the directors of the responsible entity, as well as evaluating the overall presentation of the financial report.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

27

BDO Audit Pty Ltd ABN 33 134 022 870 is a member of a national association of independent entities which are all members of BDO Australia Ltd ABN 77 050 110 275, an Australian company limited by guarantee. BDO Audit Pty Ltd and BDO Australia Ltd are members of BDO International Ltd, a UK company limited by guarantee, and form part of the international BDO network of independent member firms. Liability limited by a scheme approved under Professional Standards Legislation, other than for the acts or omissions of financial services licensees.

Independence

In conducting our audit, we have complied with the independence requirements of the Corporations Act 2001. We confirm that the independence declaration required by the Corporations Act 2001, which has been given to the directors of the responsible entity, would be in the same terms if given to the directors of the responsible entity as at the time of this auditor’s report.

Opinion

In our opinion:

(a) the financial report of Pacific First Mortgage Fund is in accordance with the Corporations Act 2001, including:

(i) giving a true and fair view of the scheme’s financial position as at 30 June 2016 and of its performance for the year ended on that date; and

(ii) complying with Australian Accounting Standards and the Corporations Regulations 2001; and

(b) the financial report also complies with International Financial Reporting Standards as disclosed in Note 2.

Emphasis of Matter

Without modifying our opinion, we draw attention to the matter set out in Note 1 noting the directors’ of the responsible entity’s intent to cease operations and wind up the scheme. As it is unlikely that the scheme will continue in operation for the foreseeable future, the financial report has been prepared on a wind up basis.

BDO Audit Pty Ltd

P A Gallagher Director

Brisbane, 30 August 2016

28

This page is intentionally blank

BTI 5510 Annual Report 2016.indd 3 6/09/2016 10:20 AM

www.balmaintrilogy.com.au

Trilogy Funds Management Pty Limited ABN 59 080 383 679Responsible Entity of the Pacific First Mortgage FundLevel 23, 10 Eagle Street Brisbane QLD 4000Tel: 1800 194 500 Fax: 1800 194 516

BTI 5567

BTI 5510 Annual Report 2016.indd 4 6/09/2016 10:20 AM