Embed Size (px)

Citation preview

Personal Finance

There are differences and similarities between a high school diploma and a college degree, and there are advantages and disadvantages to both. While it is generally believed a college degree would increase your career chances, there are good job opportunities for those without a degree.

High School Diploma or College Degree

Both high school diplomas and college degrees require students to take basic courses in subjects such as English composition, biology, math and physical education. And both types are considered vital for young people to succeed.

DifferencesUnlike the high school diploma, you can choose what career field you plan to major in throughout your years in college. And also unlike the diploma, there are various types of college degrees to pursue in order to advance in your career. They are the associate's, bachelor's, master's and doctoral degrees.

Similarities

Advantages and Disadvantages of High School DiplomasThe advantage of having a high school diploma is that you have the basic skills needed to enter the workforce. The disadvantage is that not all careers will allow you to advance without a college degree.

Advantages and Disadvantages of College DegreesThe advantages of having a college degree is that you have wider access to more advanced careers and you get better salaries in some careers. The disadvantage is that if you took out huge student loans, it may take you longer to repay them if you don't find a high-paying career.

SignificanceThe significance is that whether you have only a high school diploma or a college degree, no type of education is better than the other. The main priority for all students is that they utilize their skills to create better futures for themselves.

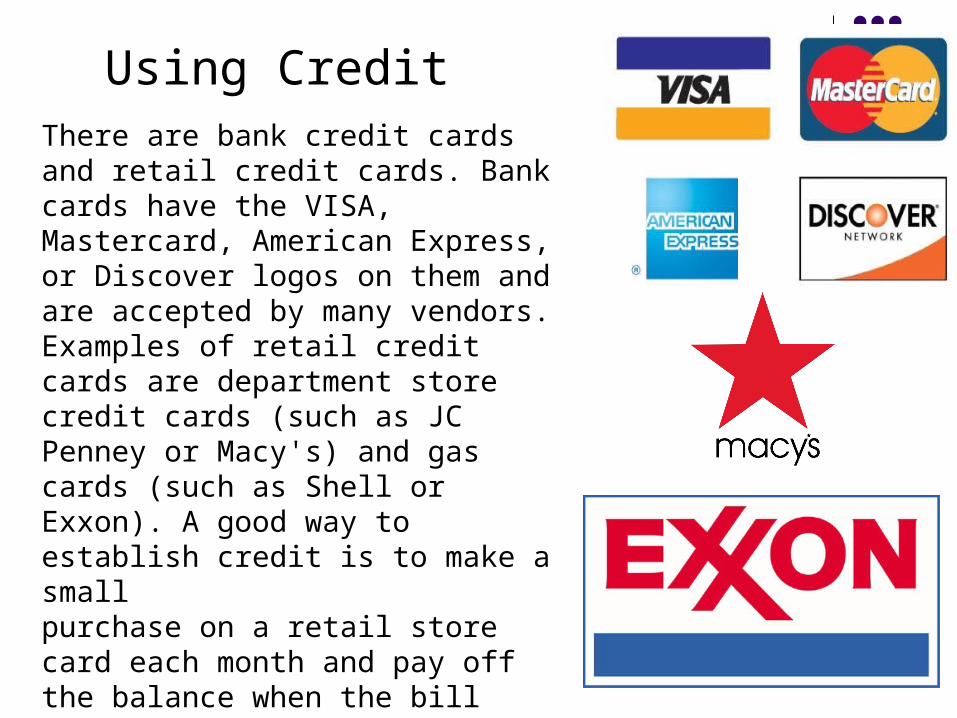

There are bank credit cards and retail credit cards. Bank cards have the VISA, Mastercard, American Express, or Discover logos on them and are accepted by many vendors. Examples of retail credit cards are department store credit cards (such as JC Penney or Macy's) and gas cards (such as Shell or Exxon). A good way to establish credit is to make a small purchase on a retail store card each month and pay off the balance when the bill comes. This shows creditors you aren't spending beyond your means and can handle the repayment obligations.

Using Credit

Using a bank card may get you into more debt than you can handle because you can use it almost anywhere. You might consider having a major credit card only for emergencies and don't keep the card in your wallet or you may be tempted to use it for other purchases.

Using Credit

Every time you use a credit card, you actually are borrowing money that is made available to you by a bank or other financial institution. The institution pays the debt to the vendor and, in turn, you pay the money back to the institution. By signing up for a credit card, you agree to pay back the money that you borrowed, in addition to any interest drawn on the amount you borrowed.

Issued by your bank, debit cards take funds directly from the money that you have in your bank account - acting much like a check, just faster. With a debit card, you don't have to carry cash or checks, and it is very convenient to shop at a variety of places including gas stations, grocery stores, restaurants and retail stores. They provide instant access to your money and are accepted worldwide.

What advantages do you have with a debit card over a credit card?

Debit Cards

Debit cards are used much like credit cards, meaning that the store where you are shopping 'swipes' them and you are normally given the option of signing your receipt instead of using a required PIN number (you can enter your PIN number if you prefer). You also typically do not have to show a picture ID.

The biggest advantage to a prepaid debit card is that it provides a way for you to limit your ability to spend money. A specific amount of money is loaded on to the card, and when you spend the money, further transactions are denied until the card is reloaded with funds. You can get access to account details, so that you can see where you are spending your money.

Prepaid Debit Cards

Is it possible o be overdrawn on your account debit card?

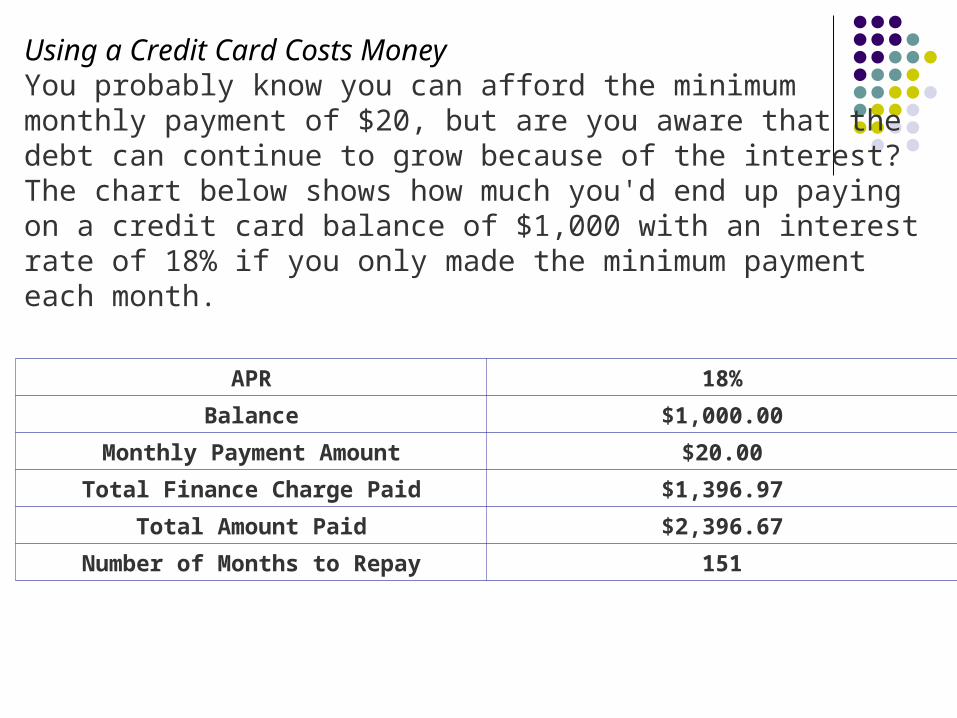

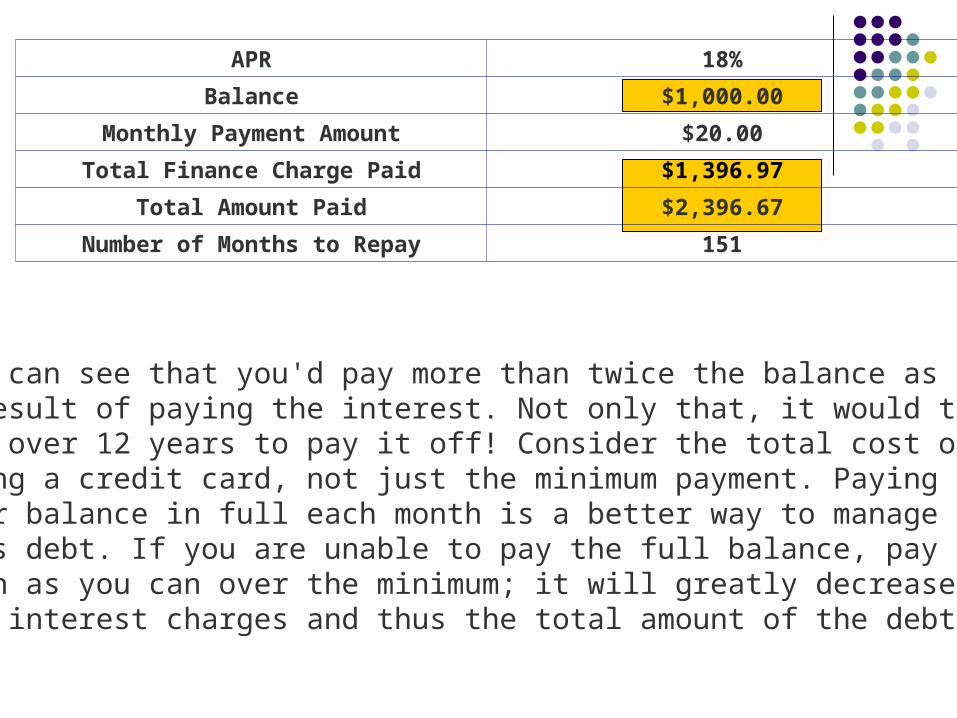

Using a Credit Card Costs MoneyYou probably know you can afford the minimum monthly payment of $20, but are you aware that the debt can continue to grow because of the interest? The chart below shows how much you'd end up paying on a credit card balance of $1,000 with an interest rate of 18% if you only made the minimum payment each month.

APR 18%

Balance $1,000.00

Monthly Payment Amount $20.00

Total Finance Charge Paid $1,396.97

Total Amount Paid $2,396.67

Number of Months to Repay 151

You can see that you'd pay more than twice the balance as a result of paying the interest. Not only that, it would take you over 12 years to pay it off! Consider the total cost of using a credit card, not just the minimum payment. Paying your balance in full each month is a better way to manage this debt. If you are unable to pay the full balance, pay is much as you can over the minimum; it will greatly decrease the interest charges and thus the total amount of the debt

APR 18%

Balance $1,000.00

Monthly Payment Amount $20.00

Total Finance Charge Paid $1,396.97

Total Amount Paid $2,396.67

Number of Months to Repay 151

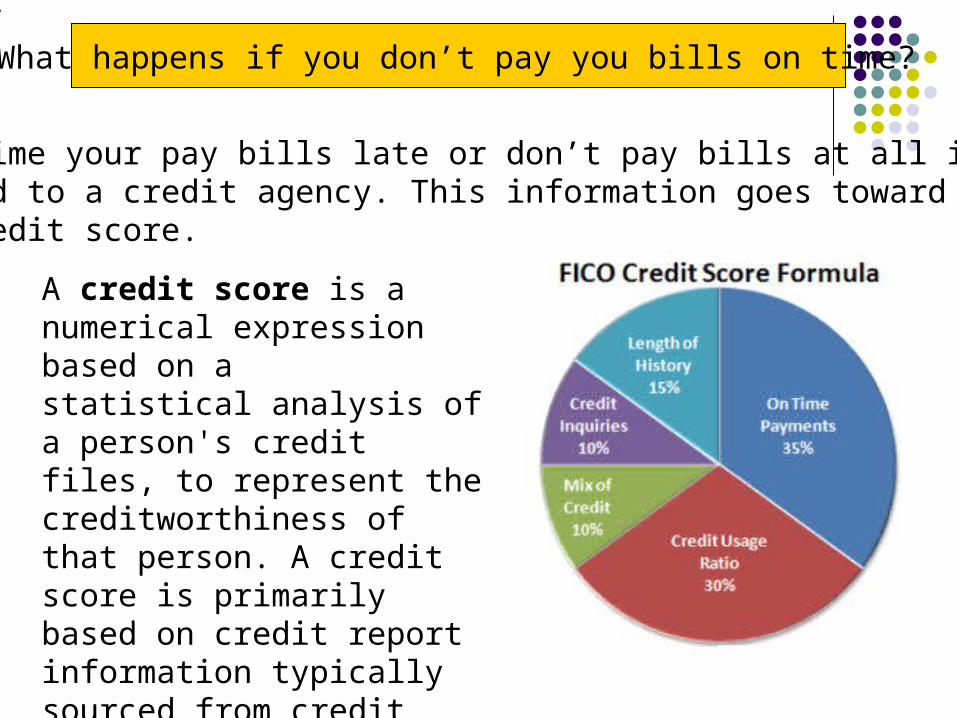

What happens if you don’t pay you bills on time?

• • • •

Every time your pay bills late or don’t pay bills at all it is reported to a credit agency. This information goes toward your credit score.

A credit score is a numerical expression based on a statistical analysis of a person's credit files, to represent the creditworthiness of that person. A credit score is primarily based on credit report information typically sourced from credit bureaus.

Free Credit ReportsThe amended Fair Credit Reporting Act permits consumers to request a free copy of their credit report once every 12 months from each of the three major credit reporting agencies The big three are Equifax, Experian, Trans Union).

Ever wonder how a lender decides whether to grant you credit? For years, creditors have been using credit scoring systems to determine if you’d be a good risk for credit cards, auto loans, and mortgages. These days, many more types of businesses — including insurance companies and phone companies — are using credit scores to decide whether to approve you for a loan or service and on what terms.

Auto and homeowners insurance companies are among the businesses that are using credit scores to help decide if you’d be a good risk for insurance. A higher credit score means you are likely less of a risk, and in turn, means you will be more likely to get credit or insurance — or pay less for it.

www.fdic.gov/consumers/consumer/ccc/reporting.html

The following website will lead you to the place you can get your yearly free credit score.

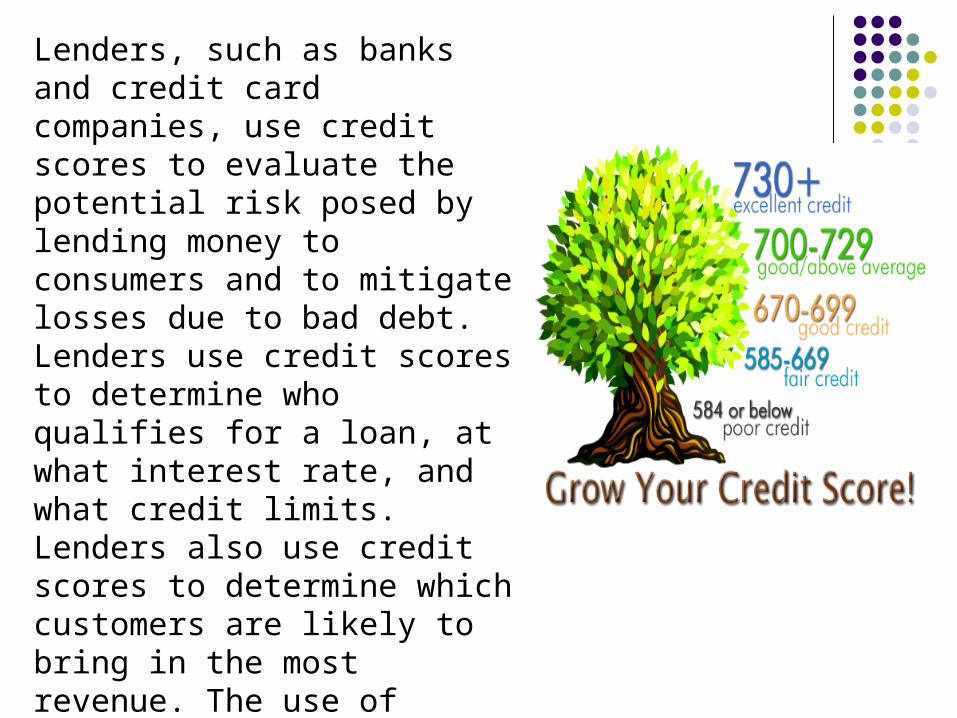

Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses due to bad debt. Lenders use credit scores to determine who qualifies for a loan, at what interest rate, and what credit limits. Lenders also use credit scores to determine which customers are likely to bring in the most revenue. The use of credit or identity scoring prior to authorizing access or granting credit is an implementation of a trusted system.

Credit scoring is not limited to banks. Other organizations, such as mobile phone companies, insurance companies, landlords, and government departments employ the same technique.

It makes good sense that lenders would want a good idea of how likely it would be for a borrower to default on a loan.

There's someone else who might be checking up on your credit history — your employer!

Your credit score tells potential creditors how risky of a borrower you are by gauging how responsible you've been with handing credit and managing debt.

Your employment history is not part of your credit score, but your credit score could be factored into your chances of getting a job. A good credit score will give you access to the best interest rates and it could also give you an edge if a potential employer runs a credit check for applicants. Just as lenders may see you as a risky borrower if you have a poor credit score, employers may also view you ask a risky employee.

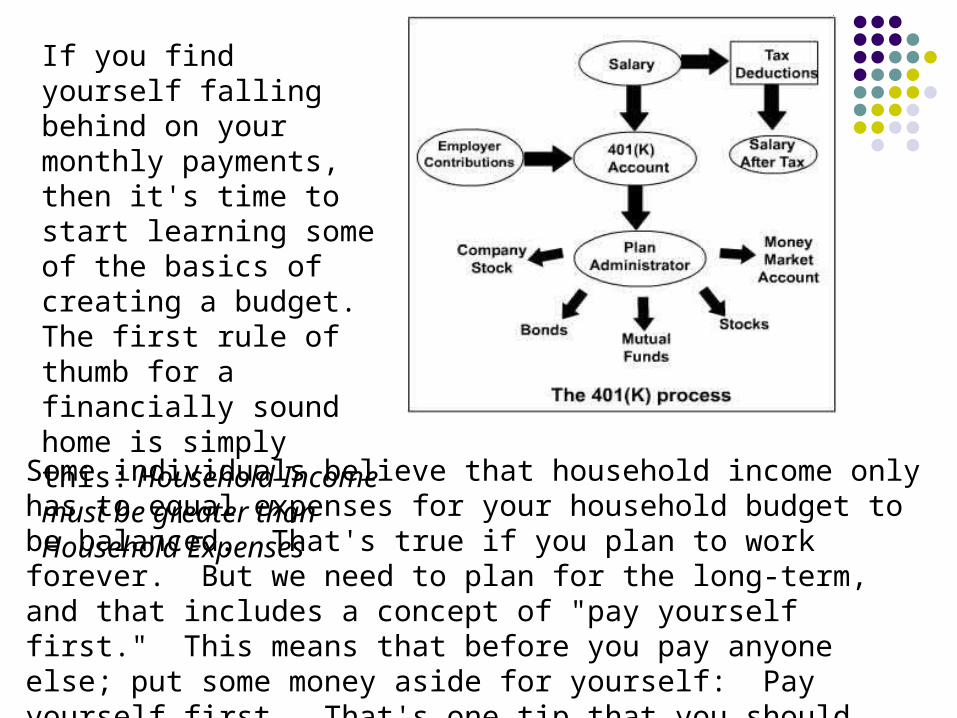

If you find yourself falling behind on your monthly payments, then it's time to start learning some of the basics of creating a budget. The first rule of thumb for a financially sound home is simply this: Household Income must be greater than Household Expenses

Some individuals believe that household income only has to equal expenses for your household budget to be balanced. That's true if you plan to work forever. But we need to plan for the long-term, and that includes a concept of "pay yourself first." This means that before you pay anyone else; put some money aside for yourself: Pay yourself first. That's one tip that you should strongly consider as part of your retirement plan and household budgeting process.

Everyone knows where their money comes from; it's where it goes that's hard to track. The income portion of your household budget accounts for all of the sources of income that you have coming into the home. This can include paychecks, interest income, tax refunds, stock dividends, bonus payments, and gifts of money.

Any reliable source of money flowing into your household each month should be included in the income section of your budget.

You can think of mandatory expenses as those monthly bills that are "must pay." Here you would include items such as a mortgage payment, car loans or lease payments, and property taxes. You'd also want to include expenses such as energy bills and other utilities. You should also include life insurance, health care costs, childcare, commuting expenses, groceries, and other expenses that help you get to work and provide you with a healthy life. Mandatory expenses are the absolute last costs you'd give up, expenses that you'd consider a requirement of running your household and daily living.

Don't forget to put some money away for the future - that's mandatory too. It's one of the fundamental rules for a sound financial planning strategy.

Discretionary Expenses

When you reach the discretionary expenses portion of your budget, this is where decisions start to get difficult. That's because this is the place where you really need to do some soul-searching to figure out if you need to spend money on these items.

Examples of discretionary expenses include going out to the movies, dining out at restaurants, extravagant vacations, expensive clothing, and other luxury items. You'll recognize this type of expense when you see one, and that brings up a good point.

The best place to examine your spending patterns is right on your monthly credit card statement. If you haven't been saving them, then you can probably download past statements from your credit card's online website. Take a close look at several credit card statements; you might be surprised at what you see.

Household Savings

Once you've identified your sources of income each month, and put together all of your expenses, it's time to see if your budget is balancing. At the very least, you want a balanced budget. At the other two extremes you might be running a budget deficit or a surplus. The formula is a simplified calculation of household savings:

Household Income - Household Expenses = Household SavingsIf the value for household savings is negative, then you have a budget deficit. If that value is zero, then your budget is balanced. If household savings is positive, then you're running a budget surplus, which is the sign of a "good" budget.

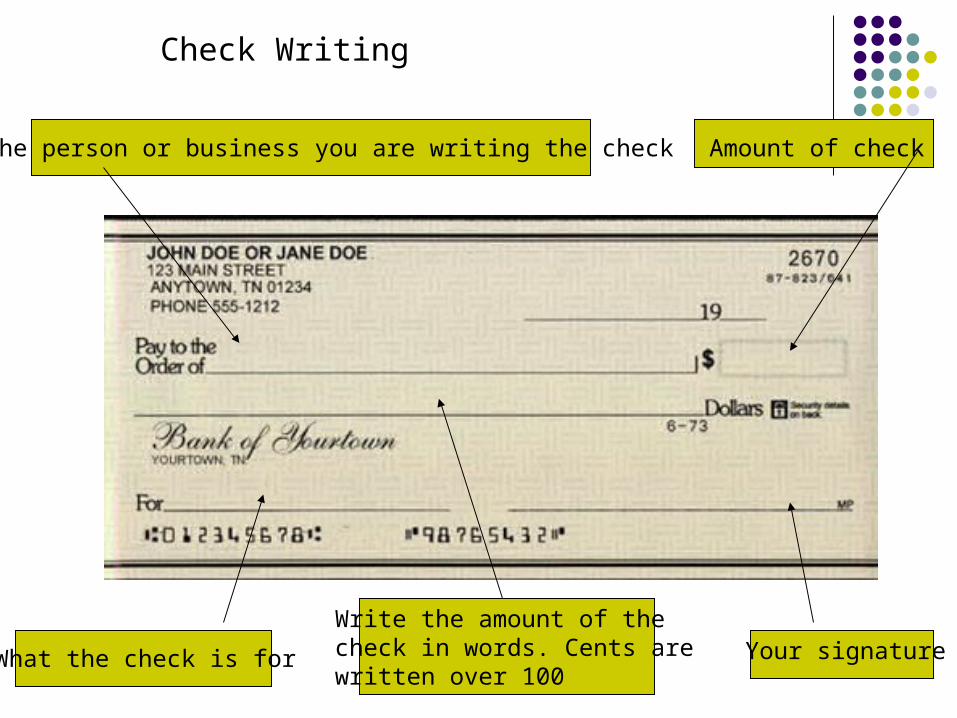

Check Writing

To the person or business you are writing the check Amount of check

Your signatureWhat the check is for

Write the amount of thecheck in words. Cents arewritten over 100

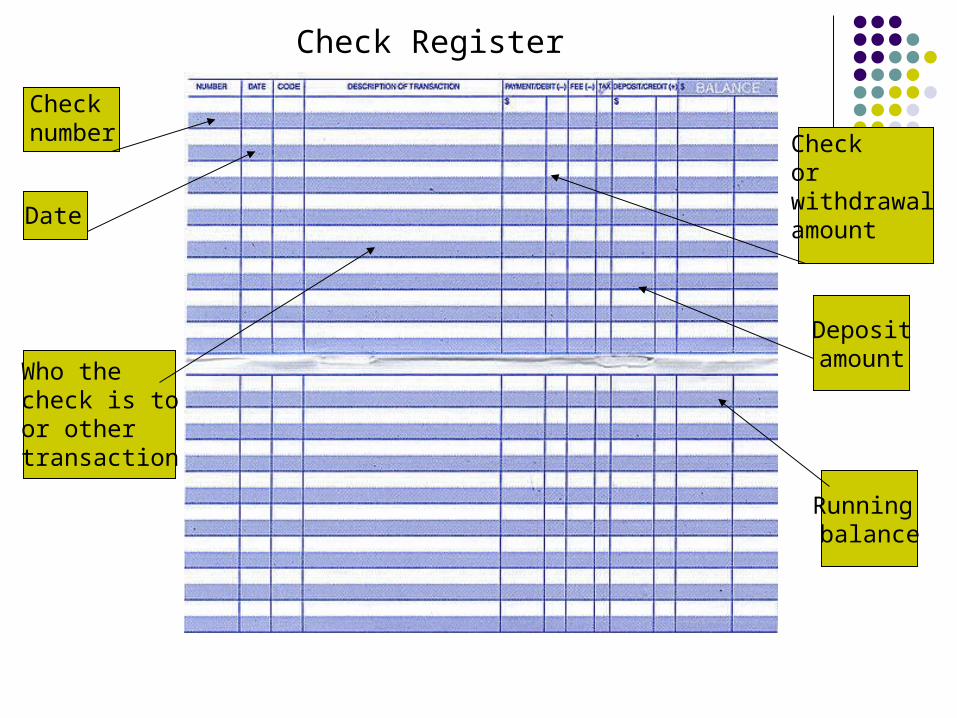

Check Register

Checknumber

Date

Who thecheck is toor othertransaction

Check or withdrawalamount

Depositamount

Running balance

As a consumer you have rights that protect you from producers that may want to take advantage of you.

You also have responsibilities to help protect yourself

The categories include:Safety, information, choice, to be heard, redress, education, a healthy environment, and to have basic needs met.

The table on the next slide explains each category as your right and responsibility.

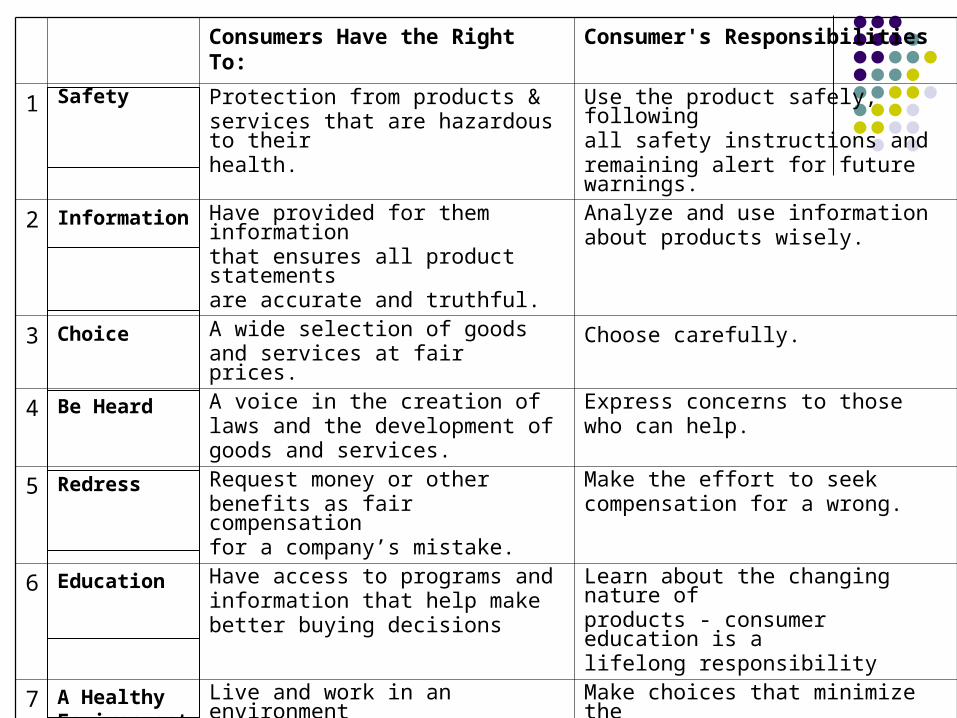

Consumers Have the Right To: Consumer's Responsibilities

1 Safety Protection from products & services that are hazardous to their health.

Use the product safely, following all safety instructions and remaining alert for future warnings.

2 Information Have provided for them information that ensures all product statements are accurate and truthful.

Analyze and use informationabout products wisely.

3 Choice A wide selection of goodsand services at fair prices.

Choose carefully.

4 Be Heard A voice in the creation oflaws and the development ofgoods and services.

Express concerns to thosewho can help.

5 Redress Request money or otherbenefits as fair compensationfor a company’s mistake.

Make the effort to seekcompensation for a wrong.

6 Education Have access to programs andinformation that help makebetter buying decisions

Learn about the changing nature of products - consumer education is alifelong responsibility

7 A Healthy Environment

Live and work in an environment that does not damage their health.

Make choices that minimize the environmental impact of your purchase on others.

8 Have Basic Needs Met

Fundamental right of accessto food, water and shelter.

Consume sustainably, so as not to prevent others from meeting their own needs.