Embed Size (px)

DESCRIPTION

Propety

Citation preview

HENRY BUTCHER MALAYSIA PENANG International Asset Consultants

PENANG REAL ESTATE MARKET Research Report H1 2013 (For internal circulation only)

TIME TO BUY, HOLD OR SELL? WHAT’S AHEAD?

Malaysian GDP growth at 4.1%

Malaysian economy is still on sturdy track with GDP growth at 4.1% in Q1 2013 ~ Department of Statistics. Construction and services sectors were the major catalysts that spearheading the country’s economy with 14.7% and 5.9% growth respectively.

The impressive growth of construction sector was mainly contributed by civil engineering subsector reinforced by infrastructure projects.

Residential subsector, hike up to 9.8% , largely attributed by housing development projects in Klang Valley and Penang.

On the other hand, manufacturing sector registered a mild growth of 0.3% only during Q1, 2013, largely due to the decline in the sub-sector of petroleum, chemical, rubber & plastic products and the lacklustre momentum in other sub-sectors.

Real estate is always a crucial link in global capital markets and risk management.

While the emerging economies of Malaysia go through its metamorphosis, the real estate industry is also developing rapidly with demand for sustainable developments, social amenities, physical infrastructure as well as the exponential increase of residential and commercial properties.

For the past few years, the Penang property market has been unprecedentedly extraordinary, exciting and challenging. This means that there is an inherent need for information and knowledge to improve decision making, whether it is among public institutions, commercial and financial entities, developers and investors.

This brief report is part of an ongoing effort to facilitate a better understanding of the market.

Against this backdrop, Henry Butcher

Malaysia, Penang, is pleased to present its current views on the Penang property market.

This report is intended for discussion and should not be relied upon as professional advice.

While every reasonable effort has been made to ensure the accuracy of the contents, no warranty is made with regard to that content.

Research Report H1 2013

Source: World Bank Databank, Department of Statistics Malaysia, IMF World Economic Outlook, October 2012.

Notes: E= Estimated; F=Forecasted

Chart 1: World, Malaysia and Penang’s GDP Growth, 2001 - 2013

upon global demand, was more vulnerable to the ex-ternal economic climate compared with the country as a whole (Chart 1).

Penang State, also commonly known as Pulau Pinang, Pearl of Orient, Prince of Wales Island, and Silicon Island of the World, encompasses an island and mainland (Seberang Perai), with a total land area of 293 km2and 738 km2 respectively.

The State, with mix of beachfront, city heritage, and hillside residential living, has been one of the excellence choices to live, work, raise the family and retire. The population in Penang was approximately 1.645 million (2012) against 1.611 million (2011), with an average annual growth rate of 2.11%.

GDP Growth of Penang

Penang is the country’s top three most developed and industrialized State despite being the second smallest State in Malaysia.

The manufacturing and tourism industries are the two key engines of economic growth and have generated substantial employment opportunities for the State.

The State, with it’s open and export based economy activities, which is highly dependent

Manufacturing and Approved Manufacturing Projects

The manufacturing sector, predominantly led by electronics and electrical clusters, is one of the key engines for the growth of Penang’s economy. During the first quarter of 2013, Penang ranked third, among the counterparts, in terms of the total proposed in-vestment in the approved manufacturing projects.

The proposed capital investment in Penang accounted for about 7.2% of the total proposed investment of the country. Domestic investment plays a significant role, accounted for almost 87% of the approved projects in Penang (Table 1 overleaf).

Penang continues to be one of the key choices for manufacturers. Apart from the halt of Bosch Solar Energy proposed crystalline photovoltaic (PV) plant, others major plants, such as Boon Siew Honda Sdn Bhd, VAT Manufacturing Malaysia Sdn Bhd, Bose Systems Malaysia Sdn Bhd, and Malaysian

Research Report H1 2013

The unemployment rate remained fairly stable at 3.3% in March 2013.

Inflation or Consumer Price Index (CPI) for the first five months of 2013, increased marginally by 1.6% to 106.2 compared to figure recorded (104.5) at the same period last year.

Penang, from a sleepy tropical… to a Silicon Island

Automotive Lighting Sdn Bhd are expected to start their operation at the Batu Kawan Industrial Park in 2013, which are also expected to generate additional 2,500 employment opportunities. Source : InvestPenang

Tourism

Tourism industry is the second engine of economic growth for Penang. Penang was in the top three with approximately 11% of the total registered hotel guests of the country.The number of hotel registered guests in Penang (2012) was 6.093 million, or 1.2% higher than the preceding year. (Table 2). Foreign and domestic guests recorded for nearly 51% and 49% respectively in Penang.

Table 1: Approved Manufacturing Projects, January – March 2013

Source: Malaysian Industrial Development Authority (www.mida.gov.my)

State

January - March 2013

No

Domestic In-

vestment

Foreign Invest-

ment

Total Proposed Capital Invest-

ment

(RM mil) (RM mil) (RM mil)

Penang 21 0.739 0.111 0.850

Other States 123 2.615 8.274 10.889

TOTAL 144 3.354 8.385 11.739

Table 2: Registered Hotel Guests, 2011 and 2012

Source: Research Division, Tourism Malaysia (www.tourism.gov.my)

The average hotel occupancy rate in Penang was recorded higher than the country, with 63.5% and 64% recorded in 2011 and 2012 respectively. (Table 3).

Today, tourism industry is fairy vibrant in Penang, particularly around George Town Unesco World Heritage Site. Various programmes and events have been arranged throughout the year with encouraging participation from both domestic and international tourists.

George Town Festival, Unesco George Town Heritage walking and cycling tours, streets art, clan jetties tour, etc, are among the niche tourism products that have drawn substantial interest of tourists to Penang.

Domestic Foreigner TOTAL

2011 2012 2011 2012 2011 2012

(in mil) (in mil) (in mil) (in mil) (in mil) (in mil)

Penang 2.956 2.996 3.063 3.097 6.019 6.093

Malaysia 27.737 29.901 26.019 26.171 53.756 56.072

Research Report H1 2013

“21,000 foreigners

have been approved

under Malaysia My

Second Home

(MM2H)

programme as at

March 2013”

Table 3: Average Occupancy Rate of Hotels, 2011 and 2012

Source: Research Division, Tourism Malaysia (www.tourism.gov.my)

On the other hand, the Malaysia My Second Home (MM2H) programme has generated a lot of interest and to-date (March 2013), more than 21,000 foreigners have been approved under this programme ~ Source : Tourism Malaysia.

Penang, with mix of beachfront, city heritage, and hillside residential living, has been one of the excellence choices to stay / retire for foreigners under the MM2H programme.

2011 2012

Penang 63.5 64.0

Malaysia 60.6 62.4

Table 4: Penang - Employment Structure, 2011 Q2 - 2012 Q1

Industry 2011 (Q2)

2011 (Q3)

2011 (Q4)

2012 (Q1)

Agriculture, Forestry and Fishing 2.1 2.0 2.2 2.4

Mining and quarrying - -

- 0.1

Manufacturing 32.7 34.3 32.4 32.2

Electricity, gas, steam and air conditioning supply

0.1

0.2

0.3 0.2

Water supply, sewarage, waste manage-ment and remediation activities

1.0 0.3 0.2 0.6

Research Report H1 2013

Employment and unemployment rate

Penang almost experienced a full employment situation. The latest unemployment figure yet to be out at the point of writing, but in average, the unemployment rate of the State was less than 3 per cent.

According to the latest Labour Force Survey conducted by the Department of Statistics, the manufacturing sector in Penang provided almost one-third of the total employment opportunities in the State, followed by whole sales and retail trades. (Table 4)

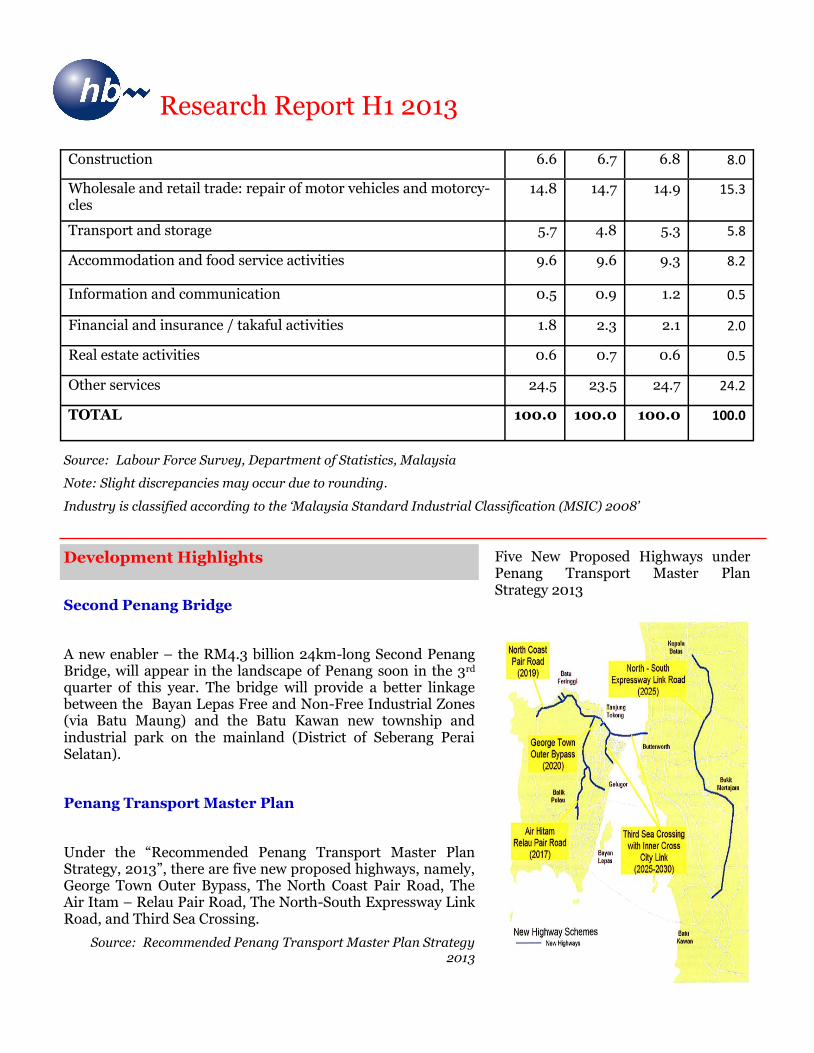

Second Penang Bridge

A new enabler – the RM4.3 billion 24km-long Second Penang Bridge, will appear in the landscape of Penang soon in the 3rd quarter of this year. The bridge will provide a better linkage between the Bayan Lepas Free and Non-Free Industrial Zones (via Batu Maung) and the Batu Kawan new township and industrial park on the mainland (District of Seberang Perai Selatan).

Penang Transport Master Plan

Under the “Recommended Penang Transport Master Plan Strategy, 2013”, there are five new proposed highways, namely, George Town Outer Bypass, The North Coast Pair Road, The Air Itam – Relau Pair Road, The North-South Expressway Link Road, and Third Sea Crossing.

Source: Recommended Penang Transport Master Plan Strategy 2013

Five New Proposed Highways under Penang Transport Master Plan Strategy 2013

Development Highlights

Research Report H1 2013

Source: Labour Force Survey, Department of Statistics, Malaysia

Note: Slight discrepancies may occur due to rounding.

Industry is classified according to the ‘Malaysia Standard Industrial Classification (MSIC) 2008’

Construction 6.6 6.7 6.8 8.0

Wholesale and retail trade: repair of motor vehicles and motorcy-cles

14.8 14.7 14.9 15.3

Transport and storage 5.7 4.8 5.3 5.8

Accommodation and food service activities 9.6 9.6 9.3 8.2

Information and communication 0.5 0.9 1.2 0.5

Financial and insurance / takaful activities 1.8 2.3 2.1 2.0

Real estate activities 0.6 0.7 0.6 0.5

Other services 24.5 23.5 24.7 24.2

TOTAL 100.0 100.0 100.0 100.0

Penang’s property market performance softened in the first quarter of 2013. (Table 5).The total number of properties transacted in Penang during the 1stquarter of 2013was recorded at 5,756 transactions, a significant drop of 18 per cent compared to the figure recorded at 7,007 transactions at the same period last year.

Despite the drop, the residential sector still remained its dominant share of 75% from the total number of properties transacted (Chart 2).

The number of commercial lots transacted, fell sharply in 1stquarter of 2013 compared to the same period last year. Nevertheless, despite the drop in number of transactions, the total transacted value of residential properties increased by 3.5% in the 1stquarter of 2013, due to the relatively strong demand from home purchasers as well as property investors coupled with the limited supply of residential stock in the market. Table 5 indicates the performance of Penang’s property market.

With the aims to protect the interest of the local property buyers and to curb the property speculation activities by foreign purchasers, the Penang State Government imposed a guideline on the minimum purchase price of property for foreign purchaser with effect from 1 July 2012.

On Penang Island, the minimum purchase price for strata-titled and landed properties are capped at RM1 million and RM2 million respectively. Nevertheless, for permanent residents, the existing limit of RM500,000 is retained.

For the approved applicants under the Malaysia My Second Home Program (MM2H), the minimum purchase price remains at RM500,000 with the limit to purchase up to 2 units only.

Research Report H1 2013

Sentiments of Penang real estate on

an upward trend...

Table 5: Performance of Penang Property Market, Q1, 2013

Source: Valuation and Property Services Department, Penang.

No. of Transaction Value of Transaction (RM mil)

Q1 2012 Q1 2013 % Change Q1 2012 Q1 2013 % Change

Residential 4981 4200 -15.7 1494.98 1546.62 +3.5

Commercial 776 465 -40.1 402.36 307.54 -23.5

Industrial 153 119 -22.2 198.83 132.46 -33.4

Agriculture 530 451 -14.9 139.11 136.63 -1.8

Development Land

563 518 -8.0 396.52 574.16 +44.8

Source: Property Stock Report, Q1, 2013,

Research Report H1 2013

Source: Property Stock Report, Q1, 2013, JPPH

Foreign transactions, of the total properties transacted in Penang, accounted for a small portion of 2.98% (or 774 transactions) and 2.26% (or 890 transactions) in 2010 and 2011 respectively.

Below are some snapshots of current development of several key developers in Penang:

Ivory Properties Group Berhad (IPGB) will kick off its Penang Times Square Phase Three, Forth and Fifth developments with a total of 1.5mil sq. ft. in gross floor area by end of 2013. The three phases, upon completion, consist of exclusive Small-Office-Home-Office (SOHO) units, a luxury shopping mall, a five-star hotel with 300 en-suite rooms, exclusive suites and a stand-alone Cineplex. The mall will be solely owned by IPGB and target to lure in more international retailers to fill up approximately 500,000 sq. ft. of the mall for a class of its own.

IJM targeted to spend about RM100 million for road infrastructure of The Light Waterfront Project. The 152-acre development on reclaimed land will have about 1,000 residential units. Of this 152 acres, 102 acres will comprise of commercial offices and retail outlets, several hotels, malls, a convention centre and a waterfront dining and entertainment district. Commercial projects for The Light are in the final stages of design at the moment. Land reclamation has just been completed and physical construction work is expected to commence in 2014. The residential portion, known as The Light Collection IV, comprising 78 condominium units and 19 units of sea-front luxurious bungalows, will be launched next year.

SP Setia Berhad will launch two new projects, namely Tower B of Setia V Residences on Persi-aran Gurney and Setia Sky Vista in Relau on Penang Island in the coming months. The sizes of condominium for Tower B of Setia V Residences are ranging from 1,300 to 1,800 sq. ft. and will be priced at approximately RM1,200 to RM1,300 per sq. ft. The units are slightly smaller and cheaper compared with neighbouring Tower A in the same parcel. The Tower B project (106 units) will be launched in September or October 2013 and would be its new development in the famed Persiaran Gurney strip for the next three years. Meanwhile, the Sky Vista (426 units) – a high-rise residential development in a green area at Relau, will be launched in November 2013.

Gurney Paragon, one of the premier projects of Penang-based developer Hunza Properties Bhd, is scheduled to be opened on 23 July 2013. It will provide a consistent stream income to the group with the option to set up a real estate investment trusts (REITs) vehicle, possibly in 2016 or 2017. Hunza has some 40 acres of land in Bayan Baru and the developer plans to build an iconic project when it is launch in mid-2015 or so. Initial estimate of the project will have a gross development value (GDV) of at least RM6 billion.

Eastern & Oriental Berhad (E&O) aims to start reclamation work next year for the 740 acres of land in Tanjung Tokong in the north-east coast of Penang for its RM12 billion Seri Tanjung Pinang Phase Two (STP2) development. It should take two years from the start of the land reclamation before the first project launch can be embarked upon. Phase Two, at three times the size of Phase One, will be a mixed integrated development comprising two islands of approximately 740 acres in size, and is projected to generate a GDV of RM12 billion.

Southbay, The Loft and Ferringhi Residences are among the current key projects of Mah Sing Group in Penang. The company is still looking for lands that can generate of a minimum yield of RM1 billion, and Penang is one of the prime areas for their land banks search. The group also plans to redesign its housing concepts to include more township projects featuring many affordable units. They are looking at building homes that will be priced below RM1 million and that will comprise mainly the types of homes that they are planning to build in the future.

Penang Master Builders’ and Building Materials Dealers Association highlighted that Penang’s construction and renovation industry would be booming with RM6 billion worth of jobs expected over the next 8 years. IJM Land (RM5.4 billion GDV), Mah Sing Group Berhad (RM248 million), Sunway Berhad (RM120 million), Ideal Property Development Sdn Bhd (RM2 billion), SP Setia (RM945 million), Eastern & Oriental Berhad (RM500 million) and Ivory Properties Group Berhad (RM520 million) are among the developers with plans for new residential and commercial schemes on the island in 2013.

Research Report H1 2013

PURPOSE BUILT OFFICE

The total supply of purpose built office space in Penang State was fairly stable with 1.068million sq m in Q1 2013, a slight increase of 0.6% from the preceding quarter (Q4, 2012). A slight improvement (0.8%) is observed in terms of demand with a take-up space of 0.863 million sq m in Q1, 2013, compared to 0.856 million sq m in the last quarter, 2012. The occupancy rate was registered at 80.9%.

Of the total supply of purpose built office space, 76% were located on the island. On Penang Island, the demand or total space occupied has registered a marginal increase of 0.4% to 0.651 million sq. m. from the previous quarter. The occupancy rate of the office space was about 80% in Q1, 2013.

Source : HBMPR/JPPH

The incoming supply of purpose built office in Penang State (all located on the mainland) is estimated to be 0.027 sq. m. As at Q1, 2013, about 0.148 million sq. m. of planned supply (on the island) was submitted for approval.

In brief, George Town prevails in the supply of office space, whilst there are more purpose built office buildings being planned in the Bayan Baru / Sungai

Nibong / Gelugor areas.

The market prices and rentals were generally healthy and stable. The market prices of prime office space ranged from RM180 to RM500 per sq. ft., whilst the market rentals ranged between RM1.50 to RM3 per sq. ft. on the island, depending on the location, grade of building, size and facilities provided.

Overall, the purpose built office sector is expected to remain stable in both selling and rental markets.

RETAIL SECTOR

In Q1, 2013, the total existing supply of shopping complex / retail space in Penang State was 1.422 million sq m. (15.3 million sq ft), an increase of 1.1% from the preceding quarter. The overall occupancy rate was recorded at about 69%.

Penang Island accounted for about 63% of the total retail space with an average occupancy rate of 75% recorded in Q1, 2013. On the mainland, the occupancy rate of the retail space was about 59%.

Research Report H1 2013

Source : HBMPR/JPPH

Gurney Paragon, a new shopping mall with a net lettable area of about 0.7 million sq. ft., is scheduled to commence its retail business in July 2013.

Apart from George Town, the South-West Dis-trict could be another potential growth area for retail sector, especially in the Bayan Baru / Sungai Nibong / Bayan Lepas areas with a current population of more than 140,000. The population is expected to grow in large numbers in the near future, given the fast pace of dynamic development of the new and upcoming property projects around the area. Moreover, the Bayan Lepas industrial area houses more than 300 factories, comprising MNCs, major local industrial players and small and medium manufacturing establishments. These factories are estimated engaging more than 50,000 of strong spending working professionals, engineers and manufacturing specialists.

Furthermore, the on-going Subterranean Penang International Convention and Exhibition Center (sPICE) with an Aquatic Centre, a four-star hotel and a retail podium, is expected to draw substantial number of domestics and foreign visitors and participants for meeting/incentive/convention/exhibition (MICE), which could potentially spur the retail / commercial activities of the Bayan Baru / Bayan Lepas vicinity.

HOTEL SECTOR

As at February 2013, there were a total of 150 hotels with 14,649 rooms in Penang, accounted for about 5.7% of the total hotels and 7.8% of the total rooms in Malaysia (Table 6).

The hotels in Penang, in general, registered a higher average occupancy rate of nearly 56.9% in Q1, 2013, compared to their counterparts in Malaysia (Table 7).

Penang Malaysia

No. of Hotel

Total Rooms

No. of Hotel

Total Rooms

5-Star 9 3,180 93 35,012

4-Star 13 4,122 117 30,190

3-Star 10 1,619 209 37,365

2-Star 11 1,047 191 14,386

1-Star 3 126 115 5,484

3-Orchid 3 247 120 4,362

2-Orchid 4 145 203 5,877

1-Orchid 10 200 166 3,943

Unrated 87 3,963 1,420 50,252

TOTAL 150 14,649 2634 186,871

Table 6: Malaysia and Penang: Existing Hotels and Total Rooms, as at February 2013

Source: Property Stock Report, Q1 2013

Average Hotel Occupancy Rate (%)

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Penang 65.6 65.9 57.3 52.3 56.9

Malaysia 55.6 54.8 50.5 53.4 51.6

Table 7: Penang: Average Hotel Occupancy Rate (1-5 star)

Source: Property Stock Report, Q1 2013

Most of the smaller budget and boutique hotels, that used to cater for local and international guests, are predominantly located in the historical city of George Town. The promotional rates of boutique hotels are between RM350 to RM500 per rooms per night.

Research Report H1 2013

Novotel, a proposed RM100 million hotel with 250 rooms, would be developed by Ideal Group at Bayan Lepas. This RM100 million hotel would be located at Bayan Lepas and is expected to be commenced for business in 2014.

Other upcoming hotels such as Rice Miller Hotel & Residence, Mansion One Hotel, Jazz Hotel, Royal Bintang Hotel, G Hotel (extension), St Giles Hotel and Cititel Express, are scheduled to be completed in 2013/2014.

RESIDENTIAL SECTOR

As at Q1, 2013, the existing supply of landed and stratified residential properties in Penang State was 132,070 units and 234,195 units respectively.(Chart 6).

Chart 6: Existing Supply of Residential Units in Penang State, as at Q1, 2013

Source: HBMPR/JPPH

Of the total landed properties, 75% were located at Seberang Perai, with nearly half of them were situated at the District of Seberang Perai Tengah. On the other hand, 70% of the stratified residential properties were built on the island, with more than fourth-fifth were located on the North-East District.

In terms of future supply of residential property (Chart 7), about 51% are stratified property whilst 49% will be landed property. Of the stratified residential property, 63% will be located on the island.

On the flip side, nearly 90% of the future supply of landed residential property will be constructed on the mainland.

Chart 7: Future Supply of Residential Properties in Penang State, Q1, 2013

Several new luxurious condominiums located at the prime areas such as Gurney Drive and Pulau Tikus on Penang Island were transacted at approximately RM1,000 per sq. ft. Generally, the prices of condominiums at North-East District are in the range of RM400-RM700 per sq. ft.

Research Report H1 2013

Source : HBMPR/JPPH

Apart from building cost hike, the trend towards lifestyle concept and better quality of building specifications - to certain extent due to relatively strong demand derived from the home purchasers, have attributed to the higher selling prices of new residential projects for both landed properties as well as high-rise condominiums.

Rental yields of landed residential properties, in general, fetch lower yield of 2% -3% , whilst apartments and condominiums could fetch slightly higher yields that hovering around 4%-5%.

Major KL-based property developers, who are confidence with Penang’s real estate future, have made their present felt in Penang. Nevertheless, land scarcity, particularly on the island, remains a key challenge.

Selected major upcoming / under-constructions residential projects are as follows:

Southbay, Batu Maung

Summerton @ Bayan Indah

Penang World City

Vertiq, Metro East

The Light Waterfront

Nadayu 290, Jalan Bukit Gambier

Olive Tree Residences, Hotels and Commercial terrace, Bayan Baru

Arena Residence, Bayan Baru

Elite Height @ Bayan City, Bayan Baru

Promenade, Bayan Baru

Setia Greens, Sungai Ara

Setia V Residences, Gurney Drive

Pearl Villas @ Setia Pearl Island

Scott Residence, Jalan Macalister

Icon Residence, Pykett Avenue

Rice Miller City Residences, Weld Quay

The Shorefront, Farquhar Street

The Latitude, Mount Erskine

Permai Village and Permai Garden, Tanjung Bungah

Andaman Series @ Seri Tanjung Pinang

Marinox, Tanjung Tokong

Ferringhi Residences, Batu Ferringhi

PRE-WAR PROPERTIES

George Town, under the UNESCO World Heritage site, has been apportioned into core and buffer zones. The Core Zone covers an area of about 109 hectares bounded by the Straits of Malacca on the north-eastern cape of Penang Island, Love Lane to the north-west and Gat Lebuh Melayu and Jalan Dr. Lim Chwee Leong to the south-west corner. The Buffer Zone (150 hectares) is protecting Core Zone, bounded by stretch of sea area around the harbour, Jalan Prangin to the south-west corner and Jalan Transfer to the north-west corner.

There are a total of 4,665 buildings, with 50.2 per cent and 49.8 per cent located at Core and Buffer zones respectively. (Table 8):

Table 8: Total No. of Buildings within the Core and Buffer Zones of George Town

Source: Draft Special Area Plan – George Town, Historic Cities of the Straits of Malacca

Site Number of Buildings

Core Zone

Buffer Zone Total

George Town 2,344 2,321 4,665

Research Report H1 2013

It is observed that pre-war heritage property is in hot demand with immense poten-tial capital appreciation. Rare and unique good listings are limited.

The average price psf of pre-war heritage properties in George Town started to soar after 1999. (Chart 9). The CAGR (1999-2012) of pre-war properties average prices psf was 13.4%.

The demand for the pre-war heritage properties seems pretty resilient despite global economic uncertainty.

Chart 9: Average Price PerSq Ft of Penang’s Pre-war Properties (1980 – 2012)

Source : HBMPR/JPPH

Source : HBMPR/JPPH

Research Report H1 2013

On average, the current market price of pre-war properties at the George Town world heritage site ranging from RM800 per sq. ft. – RM1500 per sq. ft., depending on the location and condition of the said property.

INDUSTRIAL SECTOR

The industrial sector of Penang State has recorded a minor increase (0.14%) of industrial units supply and contracted growth (-22.2%) of transacted units in Q1, 2013. Global economy uncertainties and internal political risk have posed substantial challenges to the investment climate during the first quarter of 2013. As a result, investment / expansion decisions have been on hold and industrial market was softened.

In terms of supply (Chart 10 and Chart 11), more than 80% of the existing industrial units were located on the mainland as at Q1, 2013. Of these, more than two-third were situated on Seberang Perai Tengah.

In term of future / incoming supply of Industrial units for the State (Chart 12 and Chart 13), more than 75% would be constructed on the island (majority of them would be placed at South West district).

The mainland will accommodate the balance of about 25% of the future / incoming supply of industrial units for the State. Of these, more than 80% of them would be constructed at Seberang Perai Tengah. There would be no incoming supply of industrial unit at the Seberang Perai Selatan.

Source : HBMPR/JPPH

Research Report H1 2013

Source : HBMPR/JPPH

The political risk is softened after the general election which was held in early May 2013. According to the World Investment Report 2013 released by the United Nations Conference on Trade and Development (Unctad), Malaysia is ranked 16th top prospective host economy for 2013–2015, as well as maintained its ranking as the third largest recipient of FDI in Asean.

With the continuous concerted promotional effort by Invest Penang, the State continues to be a location of choice for foreign and domestic investors. The demand for industrial sites and factories is foreseen to remain relatively resilient. Nonetheless, due to the scarcity of land suitable for industrial development on the island as well as with the new linkage to Seberang Perai via the Second Penang Bridge, the future request for industrial sites and factories are projected to shift towards mainland, particularly to the Bukit Minyak and Batu Kawan areas.

Market prices and rentals of ready built factories, in general, are expected to remain at current levels as a result of oversupply of unoccupied factories in certain unpopular and non-strategic locations in Seberang Perai.

The dust of 13th General Election starts to subside. The property investors begin to revive or resume their investment interests that have been put on hold for the past one and a half year due to some political uncertainties. The astute investors, equipped with their conventional wisdom, are of the opinion that buying properties in choice locations in Penang are the preferred mode of wealth creation. Consumer confidence of both local and international investors on Penang’s properties remains buoyant. Therefore, Penang’s property market is foreseen to be filled up with more excitement soon. Nevertheless, global economy uncertainty, natural disaster and local political development are among the downside risks that should be observed.

Source : HBMPR/JPPH Source : HBMPR/JPPH

MARKET OUTLOOK 2013

Research Report H1 2013

142-M, JALAN BURMA ,

10050 PENANG MALAYSIA

Tel. No. +604 229 8999

Fax No. +604 229 8666

Email :

PROPERTY

CONSULTANCY

SERVICES

Property Investment

Estate Agency

Leasing & Lettings

Property Management

Building Surveying

Asset Valuation

Research & Consultancy

Tenders/Auction Sale

Project Consultancy

Marketing Consultancy

Urban Planning

HOTLINE

Sales & Marketing

+6016 412 5582

Asset Valuation

+6019 558 6199

+6012 513 6942

RESEARCH TEAM

Lim Wei Seong

Yeoh Peng Hong

David Lim

Advisor : Shawn Ong

COPYRIGHT

No part of this publication

including images & charts may

be reproduced or copied in

any form without written per-

mission from Henry Butcher

Malaysia Penang.

DISCLAIMER

N o r ep r e s e nt a t i o n o r

warranty, either expressed or

implied is made as to the

accuracy, reliability of the

contents in this newsletter.

You are advised to seek inde-

pendent opinion.

A ONE-STOP CENTRE FOR ALL YOUR REAL ESTATE NEEDS

MARKET OUTLOOK 2013—con’t

The opportunities could arise both on the island as well as the mainland. Investors perhaps could look into and analyse the future potential opportunities of the land banks around the intersection of the North-South Highway and the Second Penang Bridge. These could be the potential hot locations for the property market in the near future.

Sentiments are anticipated to remain cautiously optimistic whilst the general propensity for property investments is still strong for residential homes not only in the traditionally preferred locations but also for homes of high quality specifications, finishes, good security features and facilities.

On the other hand, Malaysia’s household-debt-to-Gross Domestic Product (GDP) ratio is a high 83%. It is the highest in emerging Asia. Bank Negara Malaysia (BNM) or the central bank of Malaysia, therefore, has recently on 5 July 2013 announced stricter lending guidelines with the aim to reduce household debt in the country. Three measures the central bank announced were (1) a maximum tenure of 10 years for personal loans, (2) a maximum tenure of 35 years for property loans, and (3) a ban on pre-approved personal financing products. Nonetheless, the new limits will not affect loan applications made before the announcement.

Under these new measures, property buyers will no longer have the option to take loans for longer than 35 years. Before the new caps, property buyers could take loans for up to 45 years. Moreover, new borrowers, especially those with lower incomes, can only take on debt amounting to 60% of their monthly take home pay.

The latest caps would mainly affect the younger generation, but may have a limited impact on the majority of older generation of Malaysian who could afford for higher monthly repayments. In today’s property prices in Penang (especially for freehold properties on the island), the level of affordability for the younger generation would be lower. However, these new measures are a positive pre-emptive move to reduce / curb household debt and excessive speculation, as well as to foster a better and healthier market and economy.

For more property articles, news and properties for sale/rent, please login

to our website www.henrybutcherpenang.com

HENRY BUTCHER MALAYSIA PENANG