Embed Size (px)

Citation preview

1

Pearson’s Federal Taxation 2018 Edition

Tax Legislative Update for The Tax Cut and Jobs Act of 2017 (TCJA)

Corporations, Partnerships, Estates & Trusts, Chapters C:1-C:16

Introduction

On December 22, 2017, President Trump signed the Tax Cuts and Jobs Act of 2017 (TCJA) into law. This legislation represents a major reform of the federal income tax system, with changes that affect many areas of the tax law. Among the changes are reduced rates for individuals and corporations, modifications to many of the itemized deductions that individual taxpayers traditionally included on their returns, elimination of the personal and dependency exemptions for individuals, an increased standard deduction, and a new deduction for qualified business income from pass-through entities. Most of the provisions apply to tax years beginning in 2018 and will be incorporated into the 2019 edition of Pearson’s Federal Taxation series. However, given the scope of these changes, many instructors will want to address the reform in their current classes. To aid instructors in this process, we offer the following summary of the tax reform legislation as these changes correspond to the existing chapter material.

Summary of Important New Legislation from

the Tax Cuts and Jobs Act of 2017 Chapter C:1: Tax Research No specific changes related to TCJA. Chapter C:2: Corporate Formations and Capital Structure Under Sec. 118(a) of the IRC, contributions to the capital of a corporation are not included in the corporation’s gross income. Under pre-TCJA tax law, tax-free contributions to capital did not included so called contributions in aid of construction or contributions by customers or potential customer. TCJA expands the list of contributions not qualifying for tax-free treatment to include contributions by governmental entities and civic groups. Generally, the new rules apply to contributions made after December 22, 2017. Chapter C:3: The Corporate Income Tax Corporate Alternative Minimum Tax: TCJA repeals the corporate AMT for tax years beginning after December 31, 2017. In years beginning in 2018 through 2020, any minimum tax

2

credit carryover from prior AMT years will be allowed to the extent of the regular tax liability plus 50% of the excess of the MTC over the amount credited against the regular tax. This 50% excess is treated as a refundable tax credit. In years beginning in 2021, 100% of the excess will be allowed as a refundable credit. Accounting Methods: TCJA increases the gross receipts test threshold for allowing a C corporation to use the cash method rather than the accrual method. The increase is from $5 million to $25 million. Moreover, the test no long has to be applied for all prior tax years after December 31, 1985. Instead, the corporation applies the test for a current year by looking just at the average gross receipts for the three years immediately preceding the current year (or shorter period if the corporation was not in existence for the entire three-year period). For taxable years beginning after December 31, 2018, the threshold will be adjusted for inflation. The increased threshold applies to tax years beginning after December 31, 2017.

For tax year beginning after December 31, 2017, a taxpayer meeting the $25 million gross receipts test described above, may treat inventory (1) as non-incidental materials and supplies or (2) in a manner that conforms to the taxpayer’s method of accounting used for financial statement purposes. Such taxpayers also are exempted from the uniform capitalization (UNICAP) rules. Limitation on Net Business Interest: TCJA limits the deductibility of business interest in a given year to the sum of the following amounts:

1. Business interest income. 2. 30% of adjusted taxable income (but not less than zero). 3. Floor plan financing interest.

Any amount disallowed because of the above limitation carries over to the next year. The carryover period is indefinite. Taxpayers meeting the $25 million gross receipts test for small businesses are exempt from this limitation. Business interest is that which is allocable to a trade or business and does not include investment interest. Business income it that which is allocable to a trade or business and does not include investment income. Adjusted taxable income means taxable income computed without regard to:

1. Income, gain, deduction, or loss not allocable to a trade or business. 2. Business interest or business interest income. 3. Any NOL deduction. 4. The qualified business income deduction. 5. For years beginning before January 1, 2022, any deduction allowable for

depreciation, amortization, or depletion. 6. Any other adjustments provided by the Treasury Department.

Regarding items 1 and 4, a regular C corporation is usually deemed to be a trade or business, and the qualified business deduction does not apply to regular C corporations. The term trade or business does not include performing services as an employee, an electing real property trade or business, an electing farming business, or certain regulated utilities. Application to partnerships and S corporations will be summarized in Chapters C:9 and C:11. The limit on business interest applies to tax years beginning after December 31, 2017. Business Expenses: TCJA disallows deductions for any activities involving entertainment, amusement, or recreation, including expenses related to a facility used in connection with these

3

activities. With some exceptions, this disallowance applies even if the expenses are related to the taxpayer’s trade or business. This change is effective for amounts incurred or paid after December 31, 2017.

In addition to bribes and penalties, and with some exceptions, TCJA disallows a deduction for amounts paid to a governmental entity in relation to the violation of any law or the investigation by a governmental entity into a potential violation of a law. This change is effective for amounts incurred or paid after December 22, 2017.

Section 162(m) limits the deduction for compensation to a “covered” employee to $1 million. Under TCJA, a covered employee includes the principal executive officer and principal financial officer plus the three highest compensated officers (other than the executive or financial officers) if the compensation of such other officers is required by the Securities Exchange Act of 1934 to be reported to shareholder. In addition, TCJA removes the exception to the $1 million limitation for performance-based compensation. This change is effective for tax years beginning after December 31, 2017, with exceptions for some pre-existing binding contracts. U.S. (Domestic) Production Activities Deduction: TCJA repeals this deduction for years beginning after December 31, 2017. Dividends-Received Deduction: TCJA reduces the DRD percentage from 70% to 50% for less-than-20% owned corporations and to 65% for 20% or more owned corporations. The 100% DRD remains intact for members of affiliated corporations. The revised DRD percentages apply to tax years beginning after December 31, 2017. Net operating loss deduction: TCJA repeals the carryback of NOL deductions (although the two-year carryback is retained for farming business losses). Moreover, the NOL carryover is extended indefinitely rather than just for 20 years. The revised NOL rules apply to NOLs arising in tax years ending after December 31, 2017. NOLs arising before the effective date still will be subject to the two-year carryback and 20-year carryover rules.

In addition, under the new rules, the deduction for an NOL carryover will be limited to 80% of taxable income before the NOL deduction in the carryover year. Thus, the NOL deduction is the lesser of the aggregate carryovers or 80% of taxable income computed without regard to the NOL deduction. Any amount of NOL carryover deduction disallowed because of the 80% limit carries over indefinitely. The 80% limitation rules apply to NOLs arising in tax years beginning after December 31, 2017. NOLs arising before the effective date will not be subject to the 80% limitation. Corporate Income Tax Rates: TCJA revises the corporate tax rates from a graduated rate structure with rates ranging from 15% to 35% to a flat rate of 21%. The reduced rate applies to regular C corporations and to personal service corporations. The revised corporate rate structure applies to tax years beginning after December 31, 2017. Controlled Groups: The definitions of controlled groups remains intact. However, because TCJA establishes a flat corporate tax rate (21%) and repeals the AMT, controlled group status is no longer relevant to graduated tax rates and the AMT exemption. Controlled groups status still remains relevant, however, to other provisions such as the Sec. 179 expense limitation, the

4

general business tax credit limitation, the minimum accumulated earning tax credit, the Sec. 167 loss and accrued expense limitations, and various other related party situations. Financial Statement Implications: Because of the reduction in the corporate tax rate, the various aspects of deferred taxes and effective tax rates will be measured using the 21% flat tax rate. Chapter C:4: Corporate Nonliquidating Distributions No specific changes related to TCJA. However, changes to the individual and corporate tax rates may alter how taxpayers plan and implement transactions. Also, the expansion of expensing under the new depreciation rules will likely magnify adjustments necessary to arrive at earnings and profits (E&P). Also because TCJA repealed the U.S. (domestic) production activities deduction, that item will no longer be an adjustment for the calculation of E&P. Finally, the changes to the corporate tax rates, dividend-received percentages, NOL deduction limits, and other disallowances will alter the magnitude of E&P adjustments. Chapter C:5: Other Corporate Tax Levies Corporate Alternative Minimum Tax: TCJA repeals the corporate AMT for tax years beginning after December 31, 2017. In years beginning in 2018 through 2020, any minimum tax credit carryover from prior AMT years will be allowed to the extent of the regular tax liability plus 50% of the excess of the MTC over the amount credited against the regular tax. This 50% excess is treated as a refundable tax credit. In years beginning in 2021, 100% of the excess will be allowed as a refundable credit. Chapter C:6: Corporate Liquidating Distributions No specific changes related to TCJA. However, changes to the individual and corporate tax rates may alter how taxpayers plan and implement transactions. Chapter C:7: Corporate Acquisitions and Reorganizations No specific changes related to TCJA. However, changes to the individual and corporate tax rates may alter how taxpayers plan and implement transactions. Chapter C:8: Consolidated Tax Returns Changes described for Chapter C:3 also will apply to affiliated groups filing consolidated tax returns.

5

Chapter C:9: Partnership Formation and Operation Qualified Business Income Deduction: TCJA adds a new deduction for qualified business income (sometimes referred to as the “pass through deduction”). The deduction reduces taxable income (instead of adjusted gross income), but taxpayers can take the deduction regardless of whether they claim the standard deduction or itemized deductions. The deduction is 20% of the taxpayer’s qualified business income from a partnership, S corporation, or sole proprietorship. The purpose of the deduction is to bring the tax rates on these types of businesses more in line with the reduced rates for corporations that Congress provided with the new tax law.

In general, the deduction is limited to the lesser of: (1) the combined qualified business income (combined QBI) of the taxpayer or (2) 20% of the excess of taxable income over any net capital gain. Qualified business income (QBI) is defined as the net amount of items of income, gain, deduction, and loss for the trade or business. Excluded from this definition are investment-related items such as capital gains and losses, dividends, and interest income as well as any employee compensation and guaranteed payments that the taxpayer receives from the entity.

Generally, QBI includes only income from a U.S. trade or business. In addition, taxpayers in service-related businesses (e.g., law, accounting, healthcare and consulting) are only eligible for the deduction if their taxable income is less than a threshold amount ($157,500 for single and $315,000 for married filing jointly). Beyond this guidance, the TCJA doesn’t provide a great deal of detail about what constitutes a qualifying trade or business that will be eligible for this deduction (for example, how does rental property fit under the framework of this new law?), so additional guidance will be necessary.

The new law also provides limitations based on W-2 wages. Here, combined QBI is defined as the lesser of:

(1) 20% of qualified business income, or (2) The greater of the following:

a. 50% of W-2 wages allocable to the taxpayer by the business, or b. 25% of allocable W-2 wages plus 2.5% of the allocable share of the

unadjusted basis of qualified property immediately after it has been acquired. The W-2 limitations, however, do not apply to those businesses that meet the same taxable income thresholds as those for service-related businesses covered in the previous paragraph (that is, $157,500 for single and $315,000 for married filing jointly).

For partnerships and S corporations, the deduction is applied at the partner or shareholder level. Accordingly, each partner or shareholder takes into account his or her share of entity levels of items. The business income deduction applies to tax years beginning after December 31, 2017. Loss Limitation: A partner’s distributive share of partnership losses is limited to the extent of the partner’s basis in his or her partnership interest (outside basis). For partnership tax years beginning after December 31, 2017, TCJA adds that, in determining any loss under this limitation, the parties must take into consideration a partner’s share of charitable contributions and foreign taxes paid or accrued. Thus, these two items reduce outside basis for purposes of the loss limitation and, apparently, are limited by outside basis as well, although the ordering of applying losses to the limitation is not entirely clear.

6

Accounting Methods: The provisions concerning the cash method and gross receipts test discussed in the Chapter C:3 summary apply as well to a partnership having a C corporation as a partner. The change regarding inventories discussed in this same summary also applies to partnerships. Limitation on Net Business Interest: The limitation on net business interest discussed in the Chapter C:3 summary applies to partnerships at the partnership level and is taken into account in computing partnership ordinary (non-separately stated) income or loss.

At the partner level, a partner’s adjusted taxable income for computing the interest limitation for interest incurred outside the partnership does not include pass-through items from the partnership but the partner’s adjusted taxable income is increased by his or her share of the partnership’s “excess taxable income.” Excess taxable income arises when the interest limitation at the partnership level exceeds the partnership’s net interest and is a mechanism for increasing a partner’s adjusted taxable income to take advantage of the unused limitation at the partnership level.

If net interest is limited at the partnership level, the excess interest does not carryover at the partnership level. Instead, each partner is allocated a share of the excess interest as a pass-through item to be carried to the partner’s succeeding tax year in which the partner is allocated excess taxable income. Limitation on Excess Business Losses: For tax years beginning after December 31, 2017 and before January 1, 2026, TCJA imposes a limitation on excess business losses, applicable to noncorporate taxpayers. The new law (Sec. 461(l)) defines an excess business loss as the excess of:

(1) The aggregate deductions, for the year attributable to trades and businesses, over (2) The sum of aggregate gross income or gain attributable to such trades or business, plus

$250,000 ($500,000 for married filing jointly). The $250,000 ($500,000) is will be adjusted for inflation in tax years beginning after December 31, 2018. Any disallowed excess loss carries over as a net operating loss.

For partnerships and S corporations, the limitation is applied at the partner or shareholder level., with each partner or shareholder taking into account his or her share of entity level items of income, gain, deduction, or loss. However, the new limitation applies after the application of the Sec. 469 passive activity loss limitation. Chapter C:10: Special Partnership Issues Technical Termination Rule Repealed: Under Pre-TCJA law, a partnership terminated if (1) no partner continued to operate any business of the partnership through the same or another partnership or (2) a sale of at least a 50% interest of the partnership occurs within a 12-month period. TCJA repeals the second, so-called technical termination condition, effective for partnership tax years beginning after December 31, 2017. Mandatory basis reduction: TCJA adds a second condition for requiring a mandatory basis reduction upon the sale or transfer of a partnership interest. For transfers occurring after

7

December 31, 2017, Sec. 743(d) now defines a substantial built-in loss as existing when either (1) the partnership’s adjusted basis in its property exceeds the property’s FMV by more than $250,000 or (2) the transferee partner would be allocated loss of more than $250,000 if the partnership were to sell its assets for their FMV immediately after the transfer. Chapter C:11: S Corporations Qualified Business Income Deduction: See the discussion in the Chapter C:9 summary. Limitation on Net Business Interest: Rules similar to those described in the Chapter C:9 summary apply to S corporations. Limitation on Excess Business Losses: See the discussion in the Chapter C:9 summary. Revocation of S election: TCJA adds a provision that, if an eligible terminated S corporation revokes it S election to become a C corporation, any Sec. 481 adjustment attributable to a required change from the cash to accrual method is taken into account ratably over the six-year period beginning with the year of change. An eligible terminated S corporation is a C corporation that (1) was an S corporation on the day before the enactment of TJCA (December 21, 2017), (2) during the two-year period beginning on the date of enactment (December 22, 2017) revokes its S election, and (3) on the revocation date has the same owners in the same proportion as on December 22, 2017. The new provision also prescribes how an eligible terminated S corporation allocates any cash distributions to the accumulated adjustments account and earnings and profits account in a prorated manner. Electing Small Business Trusts: Effective January 1, 2018, TCJA allows a nonresident alien to be a beneficiary of an ESBT. Also, for years beginning after December 31, 2017, ESBTs are subject to the same charitable contributions limitations as are individuals, that is, based on an AGI amount, rather than under previous trust rules based on gross income. Chapter C:12: The Gift Tax Estate Tax Basis Exclusion Amount: See the discussion in the Chapter C:13 summary. Chapter C:13: The Estate Tax Estate Tax Basis Exclusion Amount: TCJA doubled the estate tax basic exclusion amount, so fewer estates would be subject to taxation. The basic exclusion amount provided by the Tax Relief Act of 2010 was $5 million, so the new tax law doubles that to $10 million. This amount then is indexed for inflation from 2011 to the current year. The indexed amount was scheduled to be $5.6 million for 2018, so the assumption is that the new exclusion amount will be $11.2 million. (See Analysis of the Tax Cuts and Jobs Act by RIA Checkpoint—Paragraph 2801.) However, it should be noted that some commentators have suggested that the new indexing

8

method prescribed by TCJA will result in an amount slightly less—for example, $11.18 million. (See article by Lang and Nason in The National Law Review, December 28, 2017.) The increased basic exclusion amount applies to gifts made and estates of decedents dying after December 31, 2017 and before January 1, 2026. Chapter C:14: Income Taxation of Trusts and Estates Estate and Trusts Income Tax Rates: In addition to the rate reduction for individuals and corporations, TCJA also reduces the income tax rates for estates and trusts, with a sunset provision that makes these reduced rates effective for tax years that beginning after December 31, 2017 and before January 1, 2026. The new rate structure contains four brackets that range from 10% to 37%. The tax rates for 2018 are shown below. Estates and Trusts: If taxable income is: The tax is: Not over $2,550 10% of taxable income Over $2,550 but not over $9,150 $255.00, plus 24% of the excess over $2,550 Over $9,150 but not over $12,500 $1,839.00, plus 35% of the excess over $9,150 Over $12,500 $3,011.50, plus 37% of the excess over $12,500 Chapter C:15: Administrative Procedures Fines and Penalties: In general, fines and penalties are not deductible for tax purposes (Sec. 162(f)(1)). However, TCJA provides an exception when the amounts are paid for restitution, remediation, or amounts required to come into compliance with any law that was violated (Sec. 162(f)(2)). Government agencies must report to the IRS and to the taxpayer the amount of any settlement agreement or order when the amount involved exceeds $600, and separately identify any amounts that are for restitution or remediation of property, or for correction of non-compliance.

TCJA expands the Sec. 6695 penalty to apply failure to comply with due diligence requirements for determining the eligibility to file as a head of household and claim the child tax credit, the Hope and Lifetime Learning credit, and the earned income tax credit. The penalty is $500 for each failure.

For taxpayers claiming the new business income deduction, substantial underpayment of taxes for purposes of Sec. 6662(d) occurs when the underpayment exceeds 5% of the tax shown on the return (as opposed to 10% for other underpayments).

TCJA imposes other new penalties. However, these are beyond the scope of this textbook. Chapter C:16: U.S. Taxation of Foreign-Related Transactions Participation Exemption System: TCJA has instituted a participation exemption system for taxing foreign income. This system is designed to encourage the U.S. repatriation of foreign earnings that otherwise would be retained in C corporations operating abroad. Operationally, it

9

does so through a new Sec. 245A dividend-received deduction for the foreign-source portion of dividends received by a U.S. shareholder of a foreign corporation. To be eligible for the deduction, the U.S. shareholder must be a domestic corporation that owns at least 10 % of the stock in the foreign corporation. The amount of the foreign-source dividend portion, relative to the total Sec. 245A dividend amount, is based on the ratio of the foreign corporation’s undistributed foreign E&P to its total undistributed E&P as of the close of the foreign corporation’s tax year. No foreign tax credit or deduction is available to the U.S. shareholder with respect to a Sec. 245A dividend. For purposes of determining loss, but not gain, upon a subsequent sale or exchange of the foreign corporation stock, the U.S. shareholder must reduce its foreign corporation stock basis to the extent of its Sec. 245A dividends-received deduction. Deferred Foreign Income: Under new Sec. 965, a U.S. corporate shareholder who owns at least 10% of the stock in, or value of, a foreign corporation must include in its gross income (in 2018) the U.S. shareholder’s pro rata share of the foreign corporation’s post-1986 E&P, to the extent this amount has not been previously taxed in the United States. This pro rata share is net of the U.S. shareholder’s pro rata share of any E&P deficit generated by the foreign corporation. The effect of the inclusion is a one-time U.S. charge on the U.S. shareholder’s proportionate share of the foreign corporation’s pre-2018 undistributed foreign earnings. Of this share, an amount corresponding to the U.S. shareholder’s equity claim to cash and cash equivalents is taxable at an effective rate of 15.5%. An amount corresponding to the U.S. shareholder’s equity claim to non-liquid assets is taxable at an effective rate of 8%. Any foreign taxes paid on the includible amount are creditable against the shareholder’s U.S. tax liability. GILTI and FDII Income: As a result of TCJA, U.S. multinationals must include in gross income their pro rata share of foreign source passive and mobile income. Such income is of two types: (1) global intangible low-taxed income (GILTI) and (2) foreign-derived intangible income (FDII). The tax treatment of GILTI and FDII is similar to that of Subpart F income except GILTI and FDII are taxed at lower effective rates. The tax calculation is based on a complex formula that incorporates numerous variables, including a GILTI and FDII inclusion, a deduction based on a percentage of GILTI plus a percentage of FDII, limitations on taxable GILTI and FDII, the taxpayer’s U.S. corporate tax rate, and the applicable rate of foreign tax, if any. Base Erosion Payments: To address the situation where a U.S. multinational deducts payments to a related foreign party so as to reduce its U.S. taxable income, TCJA levies an “excise tax” on such payments. For purposes of this tax, the term “related party” is much broader than the definition of a controlled foreign corporation (CFC). It includes any 25% owner of the taxpayer or any person related to the taxpayer within the meaning of Secs. 267 and 482. The constructive ownership rules of Sec. 318 are applied to determine “ownership,” except the 10% threshold is substituted for the 50% threshold in ownership attribution from corporations to their shareholders. The tax is equal to the base erosion minimum amount for the tax year in question. This amount is equal to the excess of 10% of the taxpayer’s modified taxable income over its regular tax liability, adjusted for a portion of tax credits. Modified taxable income is regular taxable income calculated without regard to any deduction for a base erosion payment.

10

Provisions Modified: In addition, TCJA has modified the following international tax provisions:

Sec. 904 by adding a foreign tax credit limitation “basket” for foreign branch income. Sec. 863(b) concerning income sourcing from sales of inventory. Sec. 958 relating to constructive ownership attribution from a foreign corporation to a

U.S. shareholder. Sec. 951(b) redefining a U.S. shareholder’s ownership of CFC stock in terms of both

voting power and value. Sec. 951(a)(1), eliminating the 30-day holding period of CFC stock as a condition of the

U.S. shareholder’s taxability under Subpart F. Provisions Repealed: TCJA has repealed the following international tax provisions:

Sec. 902, allowing for a deemed paid foreign tax credit Sec. 954(a), which includes in Subpart F income foreign base company oil-related

income Sec. 955, which includes in Subpart F income foreign base company shipping income Sec. 956, which subjects to taxation the increase in CFC earnings invested in U.S.

property The new international tax provisions are effective for tax years beginning after December 31, 2017.

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

C:1-1C:1-2C:1-3C:1-4C:1-5C:1-6C:1-7C:1-8C:1-9

C:1-10C:1-11C:1-12C:1-13C:1-14C:1-15C:1-16C:1-17C:1-18C:1-19C:1-20C:1-21C:1-22C:1-23C:1-24C:1-25C:1-26C:1-27C:1-28C:1-29C:1-30C:1-31C:1-32

C:1-33C:1-34C:1-35C:1-36C:1-37C:1-38C:1-39

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

Chapter C:1

Discussion Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-1

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:1-40C:1-41C:1-42C:1-43C:1-44C:1-45C:1-46C:1-47C:1-48C:1-49C:1-50C:1-51C:1-52C:1-53C:1-54C:1-55C:1-56C:1-57C:1-58C:1-59

C:1-60

C:1-61

C:1-62

C:1-63C:1-64C:1-65C:1-66C:1-67

C:2-1C:2-2C:2-3C:2-4C:2-5C:2-6

Case Study Problem:

Tax Research Problems:

Chapter C:2

Comprehensive Problem:

Tax Strategy Problem:

Discussion Questions:

Copyright © 2018 Pearson Education, Inc.

C:SQR-2

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:2-7C:2-8C:2-9

C:2-10C:2-11C:2-12C:2-13C:2-14C:2-15C:2-16C:2-17C:2-18C:2-19C:2-20C:2-21C:2-22C:2-23C:2-24

C:2-25C:2-26C:2-27

C:2-28C:2-29C:2-30C:2-31C:2-32C:2-33C:2-34C:2-35C:2-36C:2-37C:2-38C:2-39C:2-40C:2-41C:2-42C:2-43C:2-44C:2-45C:2-46

Issue Identification Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-3

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:2-47 X

Nontaxable contributed capital to a corporation no longer includes (1) contributions made by current or potential customers (2) any contribution by any governmental entity or civic group (other than a current shareholder). In the current problem, Ace Corporation would recognize income.

C:2-48 X

New restrictions apply to the deductibility of interest if the taxpayer's average gross receipts exceed $25 million for the previous three years.

C:2-49C:2-50C:2-51C:2-52C:2-53

C:2-54C:2-55

C:2-56C:2-57C:2-58

C:2-59C:2-60

C:2-61C:2-62C:2-63C:2-64C:2-65C:2-66

Comprehensive Problems:

Case Study Problems:

Tax Strategy Problems:

Tax Research Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-4

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

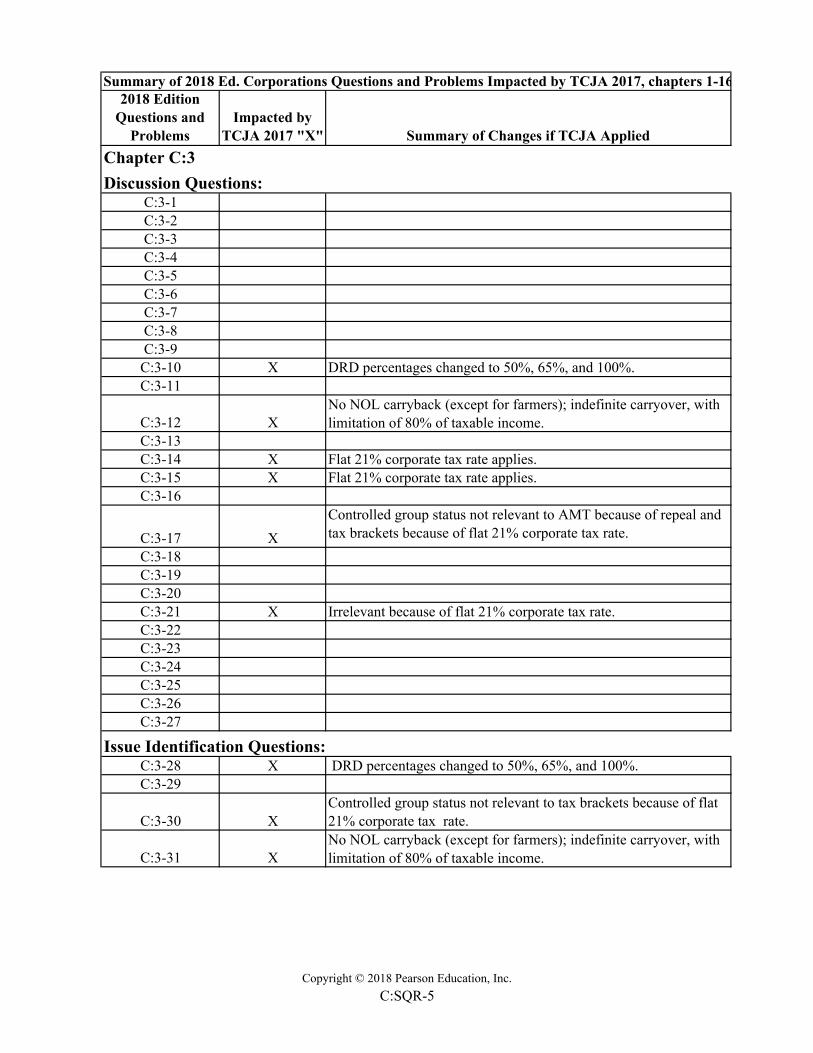

C:3-1C:3-2C:3-3C:3-4C:3-5C:3-6C:3-7C:3-8C:3-9

C:3-10 X DRD percentages changed to 50%, 65%, and 100%.C:3-11

C:3-12 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:3-13C:3-14 X Flat 21% corporate tax rate applies.C:3-15 X Flat 21% corporate tax rate applies.C:3-16

C:3-17 X

Controlled group status not relevant to AMT because of repeal and tax brackets because of flat 21% corporate tax rate.

C:3-18C:3-19C:3-20C:3-21 X Irrelevant because of flat 21% corporate tax rate.C:3-22C:3-23C:3-24C:3-25C:3-26C:3-27

C:3-28 X DRD percentages changed to 50%, 65%, and 100%.C:3-29

C:3-30 XControlled group status not relevant to tax brackets because of flat 21% corporate tax rate.

C:3-31 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

Issue Identification Questions:

Discussion Questions:

Chapter C:3

Copyright © 2018 Pearson Education, Inc.

C:SQR-5

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:3-32C:3-33C:3-34C:3-35C:3-36C:3-37C:3-38 X DRD percentage is 50%; USPAD repealed.C:3-39 X DRD percentages are 50% and 65%; USPAD repealed.C:3-40

C:3-41 XInterest deduction limited to interest income plus 30% of adjusted taxable income.

C:3-42 X

DRD percentage is 50%; no NOL carryback; flat 21% corporate tax rate.

C:3-43 X DRD percentage is 50%; no NOL carryback; USPAD repealed.C:3-44C:3-45C:3-46 X USPAD repealed; flat 21% corporate tax rate.C:3-47 X USPAD repealed; flat 21% corporate tax rate.C:3-48 X Flat 21% corporate tax rate.C:3-49 X Flat 21% corporate tax rate.

C:3-50 X

DRD percentage is 65%; USPAD repealed; flat 21% corporate tax rate.

C:3-51 X

DRD percentage is 65%; USPAD repealed; flat 21% corporate tax rate.

C:3-52C:3-53 X Irrelevant with flat 21% corporate tax rate.C:3-54 X Flat 21% corporate tax rate for corporations; revised individual tax raC:3-55C:3-56 X Flat 21% corporate tax rate.C:3-57 X Flat 21% corporate tax rate.

C:3-58 X

USPAD repealed; flat 21% corporate tax rate; DRD percentage is 65%.

C:3-59 XUSPAD repealed; flat 21% corporate tax rate; DRD percentage is 65%.

C:3-60

C:3-61 X

Flat 21% corporate tax rate; temporary differences valued at 21%; USPAD repealed; interest deduction limited to interest income plus 30% of adjusted taxable income.

C:3-62 XFlat 21% corporate tax rate; temporary differences and valuation allowance valued at 21%.

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-6

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:3-63 XFlat 21% corporate tax rate; temporary differences and unrecogized tax benefits valued at 21%.

C:3-64 XChange to Sec. 179 limits; DRD percentage is 50%; USPAD repealed; flat 21% tax rate.

C:3-65 X

Standard deduction increased; personal and dependency exemptions suspended; possible child credit; revised individual tax

t

C:3-66 -- 2017 tax forms will be subject to pre-TCJA tax law.C:3-67 -- 2017 tax forms will be subject to pre-TCJA tax law.

C:3-68 X Flat 21% corporate tax rate.C:3-69C:3-70

C:3-71C:3-72 X Gross receipts test increased to $25 million.C:3-73C:3-74 X Irrelevant with repeal of USPAD.

C:4-1C:4-2C:4-3C:4-4C:4-5C:4-6C:4-7C:4-8C:4-9

C:4-10C:4-11C:4-12C:4-13C:4-14C:4-15C:4-16C:4-17C:4-18

Discussion Questions:

Comprehensive Problem:

Tax Strategy Problem:

Tax Research Problems:

Tax Form/Return Preparation Problems:

Case Study Problems:

Chapter C:4

Copyright © 2018 Pearson Education, Inc.

C:SQR-7

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:4-19C:4-20C:4-21

C:4-22C:4-23C:4-24C:4-25

C:4-26C:4-27 X DRD percentages changed to 50%, 65%, and 100%; USPAD C:4-28 X repealed.C:4-29C:4-30C:4-31C:4-32C:4-33 X Corporate tax rate changed to flat 21%.C:4-34 X Corporate tax rate changed to flat 21%.C:4-35 X Corporate tax rate changed to flat 21%.C:4-36 X Corporate tax rate changed to flat 21%.C:4-37C:4-38 X Corporate tax rate is 21%; individual tax rate is 37%.C:4-39C:4-40C:4-41C:4-42C:4-43C:4-44C:4-45C:4-46C:4-47C:4-48 X Estate tax exemption amount has doubled.C:4-49C:4-50C:4-51 X Corporate tax rate changed to flat 21%.C:4-52C:4-53C:4-54C:4-55C:4-56C:4-57

Issue Identification Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-8

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:4-58 X Flat 21% corporate tax rate; individual tax rates revised.

C:4-59

C:4-60C:4-61

C:4-62C:4-63C:4-64C:4-65C:4-66

C:5-1 X Irrelevant because AMT repealed.C:5-2 X Irrelevant because AMT repealed.C:5-3 X Irrelevant because AMT repealed.C:5-4 X Irrelevant because AMT repealed.C:5-5 X Irrelevant because AMT repealed.C:5-6 X Irrelevant because AMT repealed.C:5-7 X Irrelevant because AMT repealed.C:5-8 X Irrelevant because AMT repealed.C:5-9 X Irrelevant because AMT repealed.

C:5-10 X Irrelevant because AMT repealed.C:5-11 X Irrelevant because AMT repealed.C:5-12 X Irrelevant because AMT repealed.C:5-13 X Irrelevant because AMT repealed.C:5-14 X Irrelevant because AMT repealed.C:5-15C:5-16C:5-17C:5-18C:5-19C:5-20C:5-21C:5-22C:5-23C:5-24C:5-25

Tax Research Problems:

Chapter C:5

Discussion Questions:

Case Study Problems:

Tax Strategy Problem:

Comprehensive Problem:

Copyright © 2018 Pearson Education, Inc.

C:SQR-9

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:5-26 X AMT repealed, but PHC and accumulsted earnings taxes not C:5-27C:5-28C:5-29C:5-30C:5-31

C:5-32 X Irrelevant because AMT repealed.C:5-33C:5-34

C:5-35 X Irrelevant because AMT repealed.C:5-36 X Irrelevant because AMT repealed.C:5-37 X Irrelevant because AMT repealed.C:5-38 X Irrelevant because AMT repealed.C:5-39 X Irrelevant because AMT repealed.C:5-40 X Irrelevant because AMT repealed.C:5-41 X Irrelevant because AMT repealed.C:5-42 X Irrelevant because AMT repealed.C:5-43 X Irrelevant because AMT repealed.C:5-44 X Irrelevant because AMT repealed.C:5-45 X Irrelevant because AMT repealed.C:5-46 X Irrelevant because AMT repealed.C:5-47 X Irrelevant because AMT repealed.C:5-48 X Irrelevant because AMT repealed.C:5-49 X Irrelevant because AMT repealed.C:5-50 X Irrelevant because AMT repealed.C:5-51 X Irrelevant because AMT repealed.C:5-52 X Irrelevant because AMT repealed.C:5-53 X Irrelevant because AMT repealed.C:5-54 X Irrelevant because AMT repealed.C:5-55 X Irrelevant because AMT repealed.C:5-56 X Irrelevant because AMT repealed.C:5-57C:5-58C:5-59

C:5-60 XDRD percentages changed to 50%, 65%, and 100%; flat 21% regular corporate tax rate applies.

C:5-61 XDRD percentages changed to 50%, 65%, and 100%; flat 21% regular corporate tax rate applies.

C:5-62 XDRD percentages changed to 50%, 65%, and 100%; flat 21% regular corporate tax rate applies.

C:5-63

Issue Identification Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-10

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:5-64C:5-65

C:5-66 XDRD percentages changed to 50%, 65%, and 100%; flat 21% regular corporate tax rate applies.

C:5-67 XDRD percentages changed to 50%, 65%, and 100%; flat 21% regular corporate tax rate applies.

C:5-68 X Irrelevant because AMT repealed.

C:5-69 XDRD percentages changed to 50%, 65%, and 100%; flat 21% regular corporate tax rate applies.

C:5-70C:5-71 X Flat 21% regular corporate tax rate applies.

C:5-72 X Irrelevant because AMT repealed.

C:5-73 X Flat 21% regular corporate tax rate applies.C:5-74

C:5-75 X Irrelevant because AMT repealed.C:5-76C:5-77

C:6-1C:6-2 X LLC may be eligible for the qualified business income deduction.C:6-3C:6-4C:6-5C:6-6C:6-7C:6-8C:6-9

C:6-10C:6-11C:6-12C:6-13C:6-14C:6-15

Tax Form/Return Preparation Problem:

Comprehensive Problem:

Tax Strategy Problems:

Case Study Problems:

Tax Research Problems:

Discussion Questions:

Chapter C:6

Copyright © 2018 Pearson Education, Inc.

C:SQR-11

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:6-16C:6-17C:6-18C:6-19C:6-20C:6-21C:6-22C:6-23C:6-24C:6-25 X NOL carryovers subject to 80% of taxable income limitation.C:6-26C:6-27C:6-28

C:6-29 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:6-30C:6-31

C:6-32C:6-33C:6-34C:6-35C:6-36C:6-37C:6-38C:6-39C:6-40C:6-41C:6-42C:6-43C:6-44C:6-45C:6-46 X Flat 21% corporate tax rate applies.C:6-47C:6-48 X Flat 21% corporate tax rate applies.C:6-49C:6-50C:6-51C:6-52C:6-53

Issue Identification Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-12

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:6-54 X

USPAD repealed; flat 21% corporate tax rate; DRD percentage is 50%; no NOL carryback (except for farmers); indefinite carryover NOL with limitation of 80% of taxable income.

C:6-55 XFlat 21% corporate tax rate applies; sole proprietorship may be eligible for qualified business income deduction.

C:6-56 X

Flat 21% corporate tax rate applies; sole proprietorship or S corporation may be eligible for qualified business income deduction.

C:6-57 XFlat 21% corporate tax rate applies; S corporation may be eligible for qualified business income deduction.

C:6-58 XFlat 21% corporate tax rate applies; Partnership may be eligible for qualified business income deduction.

C:6-59C:6-60

X

Flat 21% corporate tax rate applies; LLC or S corporation may be eligible for qualified business income deduction; revised individual tax rates apply.

C:7-1C:7-2C:7-3C:7-4C:7-5C:7-6C:7-7C:7-8C:7-9 X DRD percentages changed to 50%, 65%, and 100%.C:7-10C:7-11C:7-12C:7-13C:7-14C:7-15C:7-16

What Would You Do In This Situation?:

Comprehensive Problem:

Tax Research Problems:

Discussion Questions:

Chapter C:7

Tax Strategy Problems:

Case Study Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-13

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

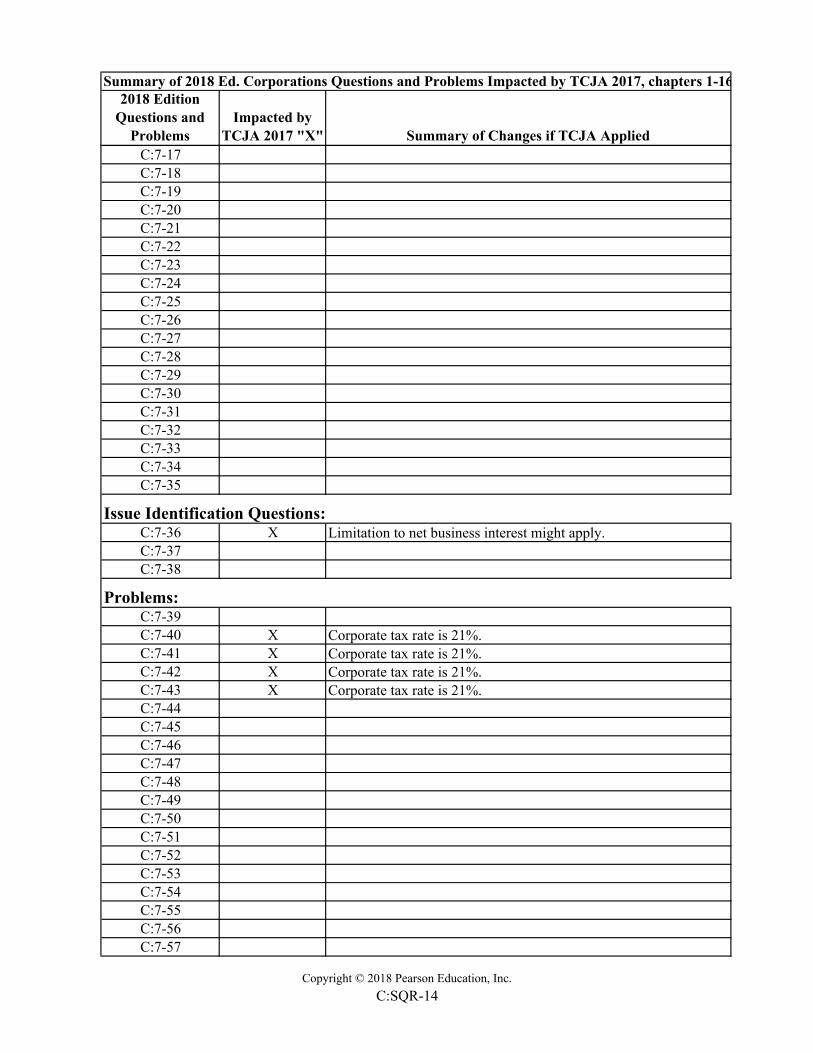

C:7-17C:7-18C:7-19C:7-20C:7-21C:7-22C:7-23C:7-24C:7-25C:7-26C:7-27C:7-28C:7-29C:7-30C:7-31C:7-32C:7-33C:7-34C:7-35

C:7-36 X Limitation to net business interest might apply.C:7-37C:7-38

C:7-39C:7-40 X Corporate tax rate is 21%.C:7-41 X Corporate tax rate is 21%.C:7-42 X Corporate tax rate is 21%.C:7-43 X Corporate tax rate is 21%.C:7-44C:7-45C:7-46C:7-47C:7-48C:7-49C:7-50C:7-51C:7-52C:7-53C:7-54C:7-55C:7-56C:7-57

Issue Identification Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-14

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:7-58C:7-59C:7-60C:7-61C:7-62C:7-63C:7-64C:7-65C:7-66C:7-67C:7-68C:7-69C:7-70 X NOL carryovers also subject to 80% of taxable income limitation.C:7-71 X NOL carryovers also subject to 80% of taxable income limitation.

C:7-72 XCorporate tax rate is 21%; 80% limit on NOL deduction might apply.

C:7-73 X Corporate tax rate is 21%.

C:7-74C:7-75C:7-76 X DRD percentage is 65%.

C:7-77 X Corporate tax rate is 21%.C:7-78

C:7-79C:7-80C:7-81

C:8-1C:8-2C:8-3C:8-4C:8-5C:8-6C:8-7C:8-8C:8-9

Comprehensive Problem:

Tax Strategy Problems:

Case Study Problems:

Tax Research Problems:

Chapter C:8

Discussion Questions:

Copyright © 2018 Pearson Education, Inc.

C:SQR-15

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:8-10C:8-11C:8-12C:8-13C:8-14C:8-15C:8-16 X DRD percentages changed to 50%, 65%, and 100%.

C:8-17 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-18 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-19 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-20C:8-21

C:8-22 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-23 X AMT repealed.C:8-24C:8-25

C:8-26 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-27

C:8-28 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-29C:8-30C:8-31C:8-32C:8-33C:8-34C:8-35C:8-36C:8-37C:8-38C:8-39C:8-40C:8-41C:8-42C:8-43C:8-44

Problems:

Issue Identification Questions:

Copyright © 2018 Pearson Education, Inc.

C:SQR-16

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:8-45C:8-46C:8-47

C:8-48 XDRD percentages changed to 50%, 65%, and 100%; flat 21% corporate rate applies.

C:8-49C:8-50

C:8-51 XDRD percentages changed to 50%, 65%, and 100%; 100% DRD for dividends from certain foreign corporations.

C:8-52 XControlled group status not relevant because of flat 21% corporate tax rate.

C:8-53 X Irrelevant because AMT repealed.C:8-54 X Tentative minimum tax and AMT are zero.

C:8-55 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-56 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-57 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-58 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-59 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-60 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-61 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-62 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

C:8-63 X Flat 21% corporate tax rate applies.C:8-64 X Flat 21% corporate tax rate applies.C:8-65 X Flat 21% corporate tax rate applies.C:8-66 X Flat 21% corporate tax rate applies.

C:8-67 XDRD percentages changed to 50%, 65%, and 100%; flat 21% corporate tax rate applies

C:8-68 -- 2017 tax forms will be subject to pre-TCJA tax law.

C:8-69 XNo NOL carryback (except for farmers); indefinite carryover, with limitation of 80% of taxable income.

Comprehensive Problems:

Tax Strategy Problem:

Copyright © 2018 Pearson Education, Inc.

C:SQR-17

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:8-70 -- 2017 tax forms will be subject to pre-TCJA tax law.

C:8-71

C:8-72C:8-73C:8-74

C:9-1 XReduced corporate tax rate; revised individual tax rates; business income deduction.

C:9-2 XReduced corporate tax rate; revised individual tax rates; business income deduction.

C:9-3C:9-4C:9-5C:9-6C:9-7C:9-8C:9-9

C:9-10C:9-11C:9-12 X Limitation on excess business losses.C:9-13 X Limitation on excess business losses.

C:9-14 XReduced corporate tax rate; revised individual tax rates; business income deduction.

C:9-15C:9-16C:9-17

C:9-18C:9-19C:9-20C:9-21C:9-22 X Limitation on excess business losses.C:9-23

C:9-24C:9-25

Tax Form/Return Preparation Problem:

Case Study Problem:

Tax Research Problems:

Chapter C:9

Discussion Questions:

Issue Identification Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-18

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:9-26C:9-27C:9-28C:9-29C:9-30C:9-31

C:9-32 XLimitation on net business interest; deduction disallowed for entertainment expenses.

C:9-33 XLimitation on net business interest; deduction disallowed for entertainment expenses.

C:9-34C:9-35C:9-36C:9-37C:9-38C:9-39C:9-40

C:9-41 XGiven the existence of debt, ordinary income may include interest expense subject to limitation on net business interest.

C:9-42 X Limitation on excess business losses.C:9-43 X Limitation on excess business losses.C:9-44 X Limitation on excess business losses.C:9-45 X Limitation on excess business losses.C:9-46C:9-47C:9-48C:9-49C:9-50C:9-51C:9-52C:9-53

C:9-54 X Limitation on excess business losses.

C:9-55 XLimitation on net business interest; may treat inventory as non-incidental materials and supplies.

C:9-56 X

Flat 21% tax rate for corporations; revised individual tax rates; increased standard deduction; personal exemptions suspended; limtation on net business interest.

C:9-57 X 2017 tax forms will be subject to pre-TCJA tax law.

C:9-58 X 2017 tax forms will be subject to pre-TCJA tax law.

Tax Strategy Problem:

Tax Form/Return Preparation Problems:

Comprehensive Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-19

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:9-59 X Limitation on excess business losses.C:9-60

C:9-61 X Revised rules on Sec. 179 expensing and bonus depreciation.C:9-62C:9-63C:9-64

C:10-1C:10-2C:10-3C:10-4C:10-5C:10-6C:10-7C:10-8C:10-9

C:10-10 X Technical termination rule repealed.C:10-11C:10-12 X Technical termination rule repealed.C:10-13C:10-14C:10-15

C:10-16C:10-17C:10-18C:10-19 X Technical termination rule repealed.C:10-20C:10-21

C:10-22 XFlat 21% corporate tax rate; revised individual tax rates; qualified business income deduction.

C:10-23 X Flat 21% corporate tax rate.

C:10-24C:10-25C:10-26C:10-27C:10-28C:10-29

Case Study Problems:

Tax Research Problems:

Chapter C:10

Discussion Questions:

Issue Identification Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-20

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:10-30C:10-31C:10-32C:10-33C:10-34C:10-35C:10-36C:10-37C:10-38 X Technical termination rule repealed.C:10-39C:10-40C:10-41C:10-42C:10-43C:10-44C:10-45 X Technical termination rule repealed.C:10-46C:10-47C:10-48 X Technical termination rule repealed.C:10-49 X Technical termination rule repealed.C:10-50C:10-51C:10-52 X Expansion of definition of substantial built-in loss.C:10-53C:10-54C:10-55

C:10-56 X Limitation on net business interest.C:10-57 X Technical termination rule repealed.

C:10-58

C:10-59 X Revised individual tax rates; technical termination rule repealed.

Tax Research Problems:C:10-60C:10-61C:10-62 X Technical termination rule repealed.C:10-63

Case Study Problem:

Comprehensive Problems:

Tax Strategy Problem:

Copyright © 2018 Pearson Education, Inc.

C:SQR-21

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:11-1 X

Flat 21% tax rate for corporations; revised individual tax rates; increased standard deduction; personal exemptions suspended; business income deduction.

C:11-2 X

Flat 21% tax rate for corporations; revised individual tax rates; increased standard deduction; personal exemptions suspended; business income deduction. Eligible terminated S corporation rules for cash to accrual changes.

C:11-3 X

Flat 21% tax rate for corporations; revised individual tax rates; increased standard deduction; personal exemptions suspended; business income deduction.

C:11-4C:11-5C:11-6C:11-7

C:11-8 XEligible terminated S corporation rules for cash to accrual changes may apply.

C:11-9C:11-10C:11-11C:11-12C:11-13 X Limitation on excess business losses.C:11-14 X Limitation on excess business losses.

C:11-15 XEligible terminated S corporation rules for cash to accrual changes may apply.

C:11-16C:11-17C:11-18C:11-19

C:11-20 X

Business income deduction may applied to S corporation shareholders. Revised corporate and individual tax rates. Dividends-received deduction percentages changed to 50%, 65%, and 100%. Individual charitable contribution deduction limitation increased to 60% of AGI.

C:11-21C:11-22C:11-23

C:11-24C:11-25

Chapter C:11

Discussion Questions:

Issue Identification Questions:

Copyright © 2018 Pearson Education, Inc.

C:SQR-22

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:11-26 X Limitation on excess business losses may apply.C:11-27 X Business income deduction may apply.

C:11-28 XFlat 21% tax rate for corporations; revised individual tax rates; increased standard deduction; personal exemptions suspended.

C:11-29C:11-30

C:11-31 XEligible terminated S corporation rules for cash to accrual changes may apply.

C:11-32C:11-33C:11-34C:11-35C:11-36 X Deduction disallowed for entertainment expenses.C:11-37C:11-38C:11-39C:11-40 X Flat 21% tax rate for corporations.

C:11-41 XRevised individual tax rates; kiddie tax applied using estate and trust income tax rates.

C:11-42 X Limitation on excess business losses may apply.C:11-43 X Limitation on excess business losses may apply.C:11-44 X Limitation on excess business losses may apply.C:11-45 X Limitation on excess business losses may apply.C:11-46 X Limitation on excess business losses may apply.

C:11-47 X

Limitation on excess business losses may apply. Eligible terminated S corporation rules for cash to accrual changes may apply.

C:11-48 X

Limitation on excess business losses may apply. No NOL carryback; indefinite carryover, with limitation of 80% of taxable income.

C:11-49C:11-50C:11-51C:11-52C:11-53C:11-54 X Limitation on excess business losses may apply.C:11-55 X Limitation on excess business losses may apply.

C:11-56 X Revised depreciation rules.

C:11-57 XDividends-received percentage 65%; USPAD repealed; flat 21% corporate tax rate.

C:11-58 X Flat 21% corporate tax rate.

Problems:

Comprehensive Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-23

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:11-59 X

Flat 21% corporate tax rate; revised individual tax rates; increased standard deduction; personal and dependency exemptions suspended. Limitation on excess business losses may apply.

C:11-60 X Flat 21% corporate tax rate; revised individual tax rates.C:11-61 X Flat 21% corporate tax rate; revised individual tax rates.C:11-62 X Flat 21% corporate tax rate; revised individual tax rates.

C:11-63 X 2017 tax forms will be subject to pre-TCJA tax law.C:11-64 X 2017 tax forms will be subject to pre-TCJA tax law.

C:11-65 XFlat 21% corporate tax rate; revised individual tax rates. Gross receipts test threshold increased to $25 million.

C:11-66 XNonresident alien can be a beneficiary of an electing small business trust.

C:11-67 X Limitation on excess business losses may apply.C:11-68 X Limitation on excess business losses may apply.

Note Includes changes due to higher annual exclusion of $15,000 in 2018.

C:12-1 XThe unified credit increases in 2018 to the amount of tax on approximately $11.2 million.

C:12-2C:12-3C:12-4C:12-5C:12-6C:12-7C:12-8C:12-9

C:12-10C:12-11C:12-12C:12-13C:12-14C:12-15C:12-16C:12-17C:12-18

Chapter C:12

Discussion Questions:

Tax Strategy Problems:

Tax Form/Return Preparation Problems:

Case Study Problem:

Tax Research Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-24

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

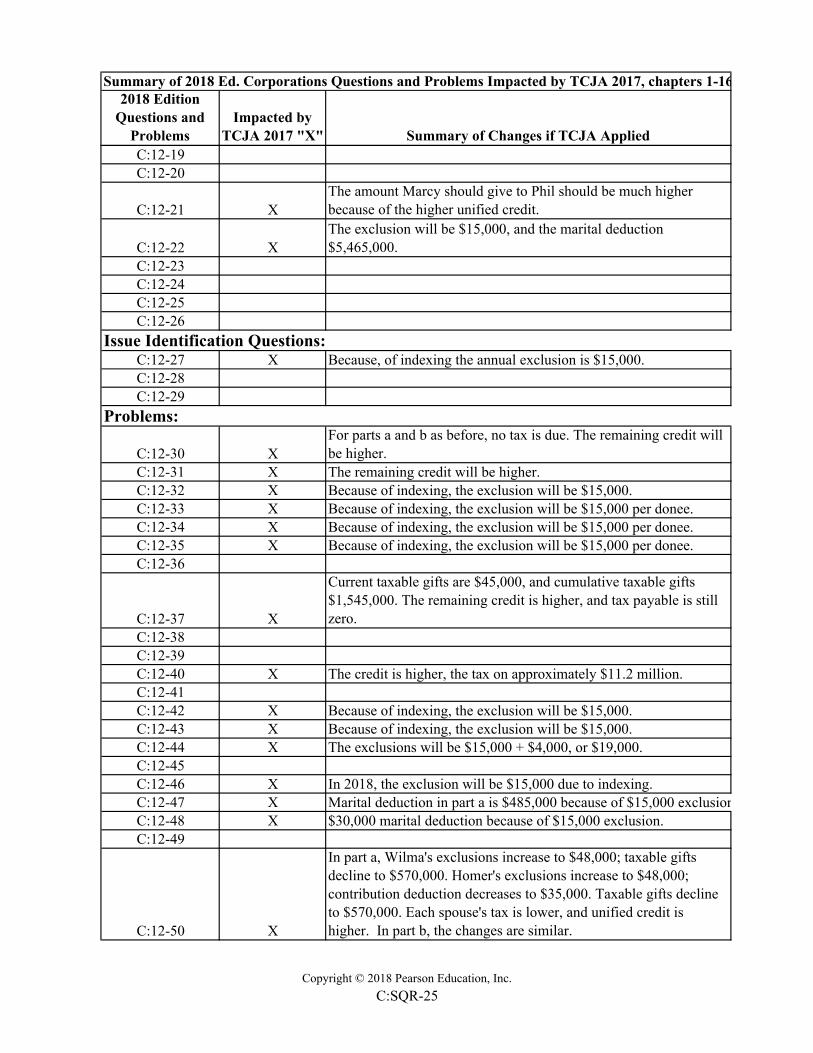

C:12-19C:12-20

C:12-21 XThe amount Marcy should give to Phil should be much higher because of the higher unified credit.

C:12-22 XThe exclusion will be $15,000, and the marital deduction $5,465,000.

C:12-23C:12-24C:12-25C:12-26

C:12-27 X Because, of indexing the annual exclusion is $15,000.C:12-28C:12-29

C:12-30 XFor parts a and b as before, no tax is due. The remaining credit will be higher.

C:12-31 X The remaining credit will be higher.C:12-32 X Because of indexing, the exclusion will be $15,000.C:12-33 X Because of indexing, the exclusion will be $15,000 per donee.C:12-34 X Because of indexing, the exclusion will be $15,000 per donee.C:12-35 X Because of indexing, the exclusion will be $15,000 per donee.C:12-36

C:12-37 X

Current taxable gifts are $45,000, and cumulative taxable gifts $1,545,000. The remaining credit is higher, and tax payable is still zero.

C:12-38C:12-39C:12-40 X The credit is higher, the tax on approximately $11.2 million.C:12-41C:12-42 X Because of indexing, the exclusion will be $15,000.C:12-43 X Because of indexing, the exclusion will be $15,000.C:12-44 X The exclusions will be $15,000 + $4,000, or $19,000.C:12-45C:12-46 X In 2018, the exclusion will be $15,000 due to indexing.C:12-47 X Marital deduction in part a is $485,000 because of $15,000 exclusionC:12-48 X $30,000 marital deduction because of $15,000 exclusion.C:12-49

C:12-50 X

In part a, Wilma's exclusions increase to $48,000; taxable gifts decline to $570,000. Homer's exclusions increase to $48,000; contribution deduction decreases to $35,000. Taxable gifts decline to $570,000. Each spouse's tax is lower, and unified credit is higher. In part b, the changes are similar.

Issue Identification Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-25

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:12-51 XThe exclusions total $45,000, and the marital deduction $35,000. Taxable gifts are $60,000. The remaining credit is higher.

C:12-52C:12-53C:12-54 X The annual exclusion is $15,000 because of indexing.

C:12-55 X

The annual exclusion is $15,000 for three gifts; the charitable contribuion deduction is $45,626, and marital deduction is $285,000. Taxable gifts are $40,000. The unified credit is higher.

C:12-56 XBecause of the very large unified credit, each tax liability is zero regardless of whether they elect gift splitting.

C:12-57 XIn each situation, the taxable gift is $1,000 lower because of the $15,000 exclusion.

C:12-58 X 2017 tax forms will be subject to pre-TCJA tax law.C:12-59 X 2017 tax forms will be subject to pre-TCJA tax law.

C:12-60 XThe annual exclusion is $15,000 per donee, and the unified credit is substantially higher. Karen should still pay the tuition directly.

C:12-61

C:12-62C:12-63C:12-64C:12-65C:12-66C:12-67C:12-68

C:13-1C:13-2C:13-3C:13-4C:13-5C:13-6C:13-7C:13-8

Comprehensive Problem:

Discussion Questions:

Tax Strategy Problems:

Tax Form/Return Preparation Problems:

Case Study Problems:

Tax Research Problems:

Chapter C:13

Copyright © 2018 Pearson Education, Inc.

C:SQR-26

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:13-9C:13-10C:13-11C:13-12C:13-13C:13-14C:13-15C:13-16C:13-17C:13-18

C:13-19 XIn 2018, the top income tax rate is 37% plus the extra 3.8% on net investment income.

C:13-20

C:13-21 X

The unified credit is higher, equal to the tax on approximately $11.2 million. The credit available for gift tax purposes likewise is higher.

C:13-22C:13-23C:13-24C:13-25

C:13-26 XThe basic exclusion amount is approximately $11.2 million in 2018.

C:13-27

C:13-28 X

GSTT will not be owed because the gift to the grandchild does not exceed the basic exclusion amount of approximately $11.2 million.

C:13-29 X

The couple's total wealth is approximately $11.3 million; they can have total wealth of approximately $22.4 million without owing tax. Dave need not disclaim.

C:13-30 XAs in problem C:13-29, the couple will not owe estate taxes because their total wealth does not exceed $22.4 million.

C:13-31 XNo estate tax will be owed, so deduct administration expenses on the income tax return.

C:13-32 X

Estate tax owed is zero due to higher unified credit. Because the estate tax (zero) will not be lower, alternate valuation cannot be elected.

C:13-33C:13-34C:13-35C:13-36C:13-37

Issue Identification Questions:

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-27

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

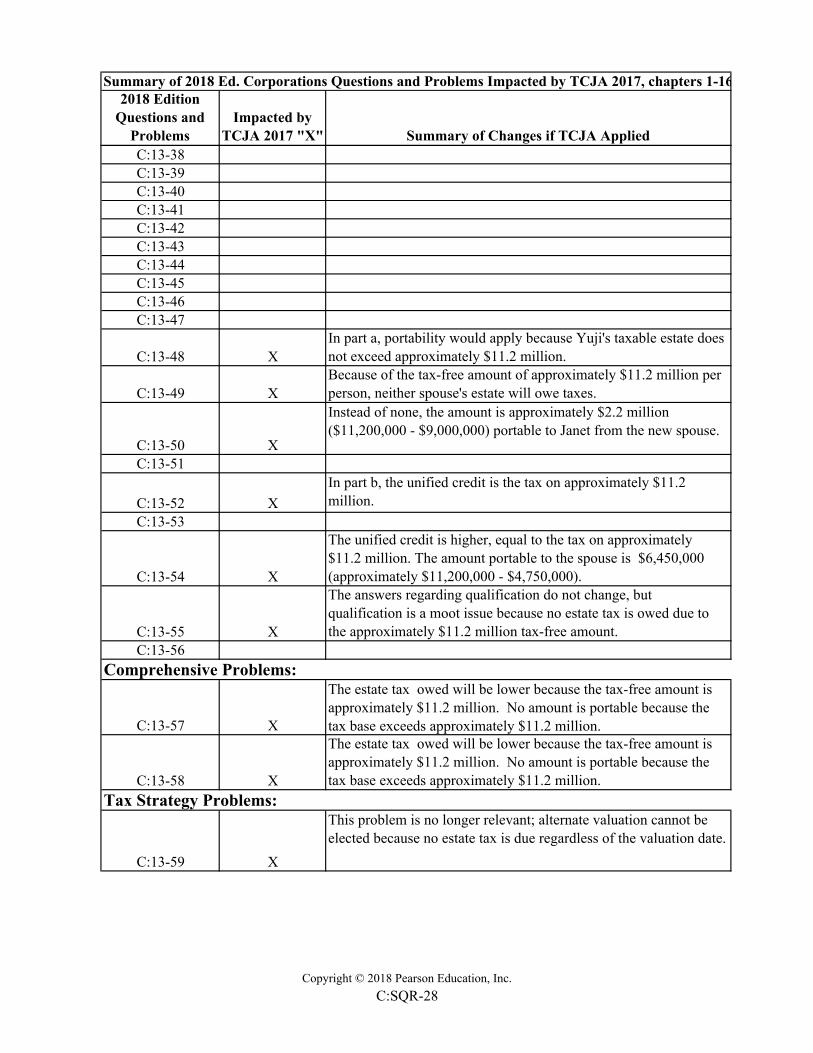

C:13-38C:13-39C:13-40C:13-41C:13-42C:13-43C:13-44C:13-45C:13-46C:13-47

C:13-48 XIn part a, portability would apply because Yuji's taxable estate does not exceed approximately $11.2 million.

C:13-49 XBecause of the tax-free amount of approximately $11.2 million per person, neither spouse's estate will owe taxes.

C:13-50 X

Instead of none, the amount is approximately $2.2 million ($11,200,000 - $9,000,000) portable to Janet from the new spouse.

C:13-51

C:13-52 X

In part b, the unified credit is the tax on approximately $11.2 million.

C:13-53

C:13-54 X

The unified credit is higher, equal to the tax on approximately $11.2 million. The amount portable to the spouse is $6,450,000 (approximately $11,200,000 - $4,750,000).

C:13-55 X

The answers regarding qualification do not change, but qualification is a moot issue because no estate tax is owed due to the approximately $11.2 million tax-free amount.

C:13-56

C:13-57 X

The estate tax owed will be lower because the tax-free amount is approximately $11.2 million. No amount is portable because the tax base exceeds approximately $11.2 million.

C:13-58 X

The estate tax owed will be lower because the tax-free amount is approximately $11.2 million. No amount is portable because the tax base exceeds approximately $11.2 million.

C:13-59 X

This problem is no longer relevant; alternate valuation cannot be elected because no estate tax is due regardless of the valuation date.

Comprehensive Problems:

Tax Strategy Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-28

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:13-60 X

With passing on at death, some tax is owed even with the higher unified credit. With giving now, no gift tax would be owed, and there would be no gross up. However, estate taxes would be owed because the tax base would exceed the tax-free amount of approximately $11.2 million.

C:13-61 X

If Nancy disclaims, the amount portable to her is $6.7 million ($11,200,000 - $4,500,000). Her estate tax liability will be zero. If she does not disclaim, $11.2 million will be portable to her. This amount exceeds her tax base, so her estate tax liability will be zero.

C:13-62 X 2017 tax forms will be subject to pre-TCJA tax law.C:13-63 X 2017 tax forms will be subject to pre-TCJA tax law.

C:13-64 X

GSTT will not be owed because the gift to the grandchild Halbert, Jr. does not exceed the basic exclusion amount of approximately $11.2 million.

C:13-65 XThis problem is no longer relevant; the estate will not owe taxes unless the appraisal is understated by at least about $5 million.

C:13-66

C:13-67 X

The research conclusion does not change. However, the result is somewhat of a moot issue because the surviving spouse's estate tax will be zero regardless due to the substantial increase in the unified credit.

C:13-68 X

The research conclusion does not change. However, the denial of a marital deduction is a moot issue because Sam's federal estate tax will be zero due to the substantial increase in the unified credit.

C:13-69C:13-70C:13-71C:13-72

Tax Form/Return Preparation Problems:

Case Study Problems:

Tax Research Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-29

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

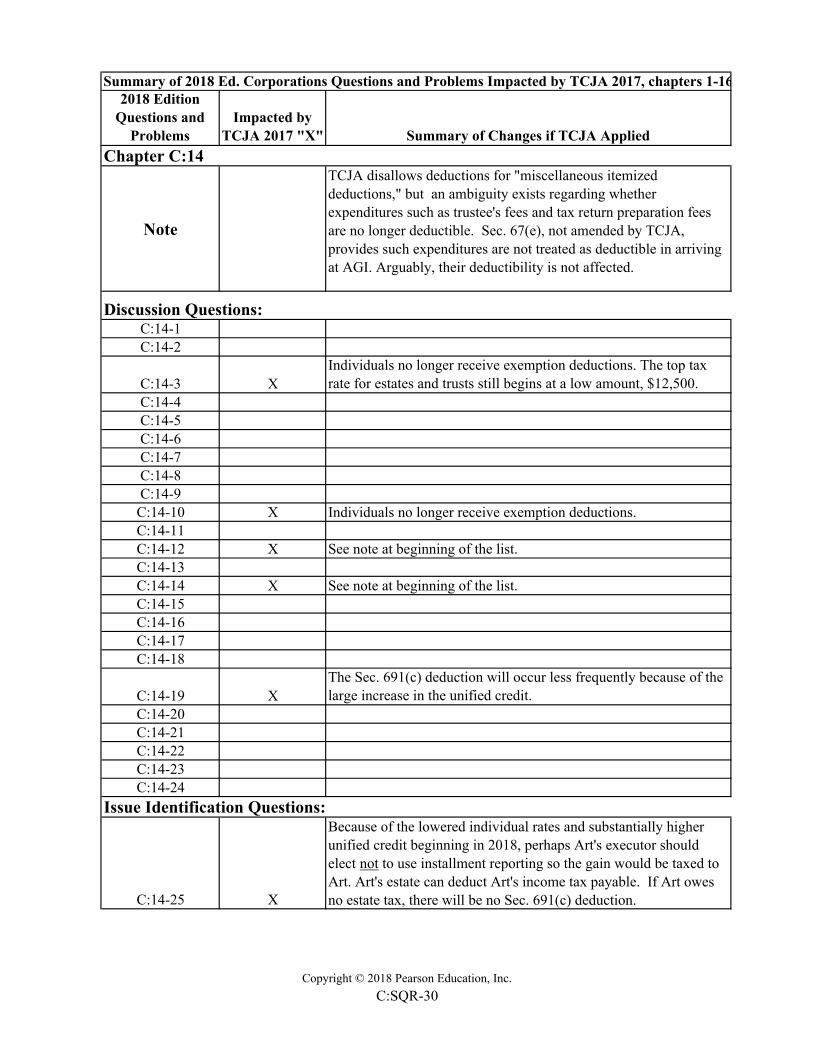

Note

TCJA disallows deductions for "miscellaneous itemized deductions," but an ambiguity exists regarding whether expenditures such as trustee's fees and tax return preparation fees are no longer deductible. Sec. 67(e), not amended by TCJA, provides such expenditures are not treated as deductible in arriving at AGI. Arguably, their deductibility is not affected.

C:14-1C:14-2

C:14-3 XIndividuals no longer receive exemption deductions. The top tax rate for estates and trusts still begins at a low amount, $12,500.

C:14-4C:14-5C:14-6C:14-7C:14-8C:14-9

C:14-10 X Individuals no longer receive exemption deductions. C:14-11C:14-12 X See note at beginning of the list.C:14-13C:14-14 X See note at beginning of the list.C:14-15C:14-16C:14-17C:14-18

C:14-19 XThe Sec. 691(c) deduction will occur less frequently because of the large increase in the unified credit.

C:14-20C:14-21C:14-22C:14-23C:14-24

C:14-25 X

Because of the lowered individual rates and substantially higher unified credit beginning in 2018, perhaps Art's executor should elect not to use installment reporting so the gain would be taxed to Art. Art's estate can deduct Art's income tax payable. If Art owes no estate tax, there will be no Sec. 691(c) deduction.

Issue Identification Questions:

Chapter C:14

Discussion Questions:

Copyright © 2018 Pearson Education, Inc.

C:SQR-30

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:14-26 X

Because the NOL arose before 2017, it is not affected by the 80% of taxable income limitation of TCJA. Joe will receive a larger standard deduction but no personal exemption.

C:14-27

C:14-28 X

The trust's tax on taxable income and net investment income will decline slightly. The individual will not receive a personal exemption but will have a higher standard deduction.

C:14-29 X The taxes decline for both taxpayers.C:14-30 X See note at beginning of the list regarding trustee's fees.C:14-31 X See note at beginning of the list regarding trustee's fees.

C:14-32 XSee note at beginning of the list regarding trustee's fees. The tax will differ slightly.

C:14-33 X See note at beginning of the list regarding trustee's fees.C:14-34 X See note at beginning of the list regarding trustee's fees.C:14-35C:14-36C:14-37C:14-38C:14-39 X See note at beginning of the list regarding trustee's fees.C:14-40 X See note at beginning of the list regarding trustee's fees.C:14-41 X See note at beginning of the list regarding trustee's fees.C:14-42C:14-43C:14-44C:14-45C:14-46C:14-47C:14-48C:14-49C:14-50

C:14-51 X

See note at beginning of the list regarding trustee's fees. The facts of the problem state Dana dies in 2016. If she died in 2018 instead, her estate would not be large enough to owe estate taxes. In parts c, d, and e there would be no Sec. 691(c) deduction. In part f the tax rate on income above $12,500 would be 37%.

C:14-52 X

At the trust level in both scenarios, the tax rate will be lower. Gordon's deductible loss will be limited to 80% of taxable income. His standard deduction will be $12,000; a personal exemption is no

Problems:

Comprehensive Problem:

Tax Strategy Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-31

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:14-53 XThe trust tax rates will be lower. Marshall's tax also will be lower because of the lower top rate.

C:14-54 X

The note at the beginning applies to administration expenses. The top rate for individuals is 37%; thus, their tax savings will be lower. The trust's tax will be slightly lower.

C:14-55 X 2017 tax forms will be subject to pre-TCJA tax law.C:14-56 X 2017 tax forms will be subject to pre-TCJA tax law.C:14-57 X 2017 tax forms will be subject to pre-TCJA tax law.

C:14-58 XIn part g the portion of the income taxed under the kiddie tax rules will be taxed at the fiduciary rates.

C:14-59

C:14-60 XSee note at the beginning of the list regarding trustee's fees. That point is relevant here also.

C:14-61C:14-62C:14-63C:14-64

C:15-1C:15-2C:15-3C:15-4C:15-5C:15-6C:15-7C:15-8C:15-9

C:15-10C:15-11C:15-12C:15-13C:15-14C:15-15C:15-16C:15-17C:15-18C:15-19C:15-20

Tax Form/Return Preparation Problems:

Case Study Problems:

Tax Research Problems:

Chapter C:15

Discussion Questions:

Copyright © 2018 Pearson Education, Inc.

C:SQR-32

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:15-21C:15-22C:15-23C:15-24C:15-25C:15-26C:15-27C:15-28C:15-29C:15-30

C:15-31 XNew penalty for failure to properly determine Head of Household and the Child Tax Credit and Hope Tax Credit ($500/failure).

C:15-32C:15-33

C:15-34C:15-35C:15-36

C:15-37C:15-38C:15-39C:15-40C:15-41C:15-42C:15-43C:15-44C:15-45C:15-46C:15-47C:15-48C:15-49C:15-50C:15-51C:15-52C:15-53C:15-54C:15-55C:15-56C:15-57C:15-58C:15-59C:15-60

Problems:

Issue Identification Questions:

Copyright © 2018 Pearson Education, Inc.

C:SQR-33

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:15-61C:15-62

C:15-63

C:15-64

C:15-65

C:15-66C:15-67C:15-68C:15-69C:15-70C:15-71

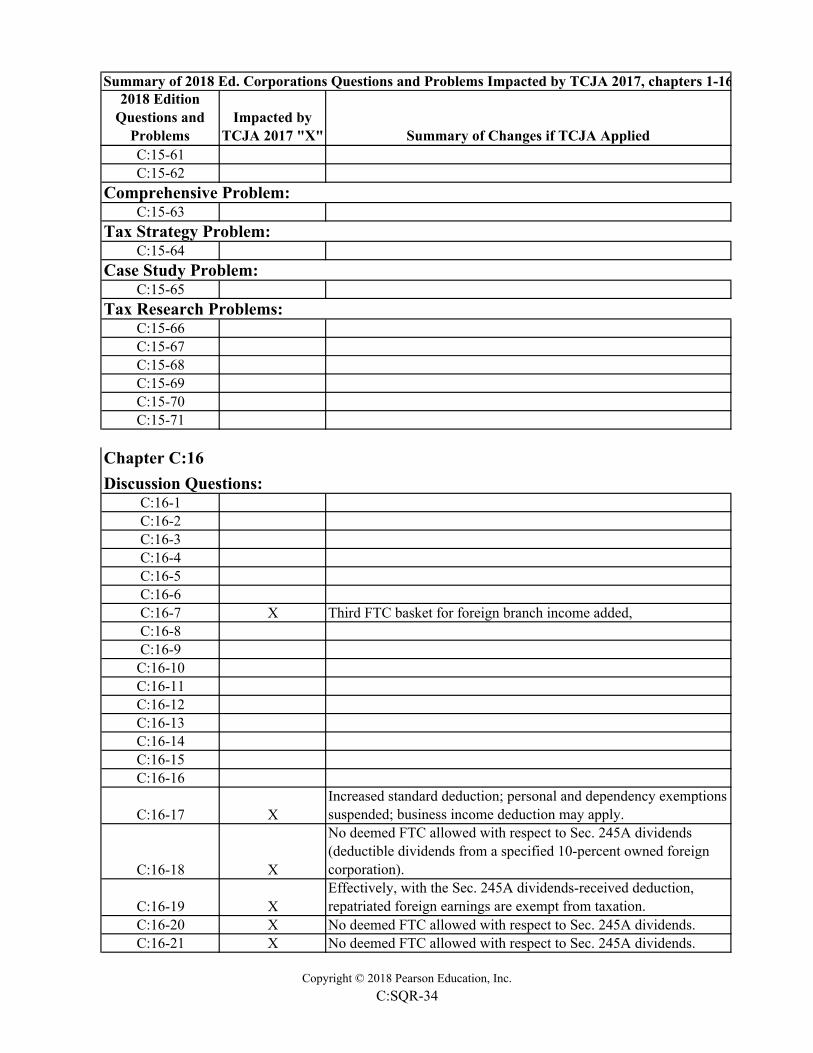

C:16-1C:16-2C:16-3C:16-4C:16-5C:16-6C:16-7 X Third FTC basket for foreign branch income added,C:16-8C:16-9

C:16-10C:16-11C:16-12C:16-13C:16-14C:16-15C:16-16

C:16-17 XIncreased standard deduction; personal and dependency exemptions suspended; business income deduction may apply.

C:16-18 X

No deemed FTC allowed with respect to Sec. 245A dividends (deductible dividends from a specified 10-percent owned foreign corporation).

C:16-19 XEffectively, with the Sec. 245A dividends-received deduction, repatriated foreign earnings are exempt from taxation.

C:16-20 X No deemed FTC allowed with respect to Sec. 245A dividends.C:16-21 X No deemed FTC allowed with respect to Sec. 245A dividends.

Comprehensive Problem:

Tax Strategy Problem:

Case Study Problem:

Tax Research Problems:

Chapter C:16

Discussion Questions:

Copyright © 2018 Pearson Education, Inc.

C:SQR-34

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:16-22 XU.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction.

C:16-23 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. Increase in CFC earnings invested in U.S. property no longer taxable.

C:16-24 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. Increase in CFC earnings invested in U.S. property no longer taxable. U.S. shareholder in CFC may own 10% or more of stock voting power or value.

C:16-25

C:16-26 XEffectively, with the Sec. 245A dividends-received deduction, repatriated foreign earnings are exempt from taxation.

C:16-27 XIncrease in CFC earnings invested in U.S. property no longer taxable.

C:16-28 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. Increase in CFC earnings invested in U.S. property no longer taxable.

C:16-29 X

U.S. corporate shareholder may deduct foreign source dividend portion of Sec. 1248 gain under Sec. 245A. No deemed FTC allowed with respect to Sec. 245A dividends.

C:16-30

C:16-31 XSec. 245A dividends-received deduction makes inversions less attractive.

C:16-32 X

Effectively, with the Sec. 245A dividends-received deduction, repatriated earnings are exempt from taxation. No deemed FTC allowed with respect to Sec. 245A dividends. Tax liability should be based on flat 21% corporate rate.

C:16-33 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. No deemed FTC allowed with respect to Sec. 245A dividends.

C:16-34

C:16-35 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. No deemed FTC allowed with respect to Sec. 245A dividends. Third FTC basket for foreign branch income added. No expenses allocable to numerator in FTC formula.

C:16-36 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. Increase in CFC earnings invested in U.S. property no longer taxable.

Issue Identification Questions:

Copyright © 2018 Pearson Education, Inc.

C:SQR-35

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:16-37

C:16-38 XTax liability should be based on flat 21% corporate rate. Numerator in FTC formula should be reduced by Sec. 245A dividends.

C:16-39 XTax liability should be based on flat 21% corporate rate. Numerator in FTC formula should be reduced by Sec. 245A dividends.

C:16-40C:16-41

C:16-42 XItemized deduction for employee-related expenses no longer allowed.

C:16-43 X

Itemized deduction for employee-related expenses no longer allowed. Increased standard deduction; personal and dependency exemptions suspended. Revised individual tax rates.

C:16-44 X Personal and dependency exemptions suspended.C:16-45 X Personal and dependency exemptions suspended.

C:16-46 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. No deemed FTC allowed with respect to Sec. 245A dividends. Tax liability should be based on flat 21% corporate rate.

C:16-47 X

US corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. No deemed FTC allowed with respect to Sec. 245A dividends. Tax liability should be based on flat 21% corporate rate.

C:16-48 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. No deemed FTC allowed with respect to Sec. 245A dividends. Tax liability should be based on flat 21% corporate rate.

C:16-49 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. No deemed FTC allowed with respect to Sec. 245A dividends. Tax liability should be based on flat 21% corporate rate.

C:16-50 X Tax liability should be based on flat 21% corporate rate.

C:16-51 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. No deemed FTC allowed with respect to Sec. 245A dividends. Tax liability should be based on flat 21% corporate rate. Numerator in FTC formula should be reduced by Sec. 245A dividends.

C:16-52C:16-53C:16-54

Problems:

Copyright © 2018 Pearson Education, Inc.

C:SQR-36

2018 Edition Questions and

ProblemsImpacted by

TCJA 2017 "X" Summary of Changes if TCJA Applied

Summary of 2018 Ed. Corporations Questions and Problems Impacted by TCJA 2017, chapters 1-16

C:16-55 X Tax liability should be based on flat 21% corporate rate.

C:16-56 XU.S. corporate shareholder may deduct foreign source dividend portion of Sec. 1248 gain under Sec. 245A

C:16-57 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. No deemed FTC allowed with respect to Sec. 245A dividends.

C:16-58 X

U.S. corporate shareholder of 10% corporation entitled to Sec. 245A dividends-received deduction. No deemed FTC allowed with respect to Sec. 245A dividends. Tax liability should be based on flat 21% corporate rate. U.S. corporate shareholder may deduct foreign source dividend portion of Sec. 1248 gain under Sec. 245A.

C:16-59 X 2017 tax forms will be subject to pre-TCJA tax law.C:16-60 X 2017 tax forms will be subject to pre-TCJA tax law.

C:16-61 XItemized deduction for employee-related expenses no longer allowed.