Embed Size (px)

Citation preview

August 30, 2016By James Ray

PE, PP & PS Market Update

www.icis.com 2

Over 9,200 price assessments in 1,200reports covering 180 commodities

More than 30 years of industry insight and data

Over 100,000 industry customers

Customers include virtually every major chemical company

Weekly contact with thousands of market participants

17,000+ annual news stories

700+ global employees

ICIS - Global Presence, Local Insight

www.icis.com 3www.icis.com 3

2015 Recap

Feedstocks

Polymer Markets

Supply & Demand

Price trends

Agenda

Copyright 2016 ICIS

www.icis.com 4

2015 Recap

www.icis.com 5

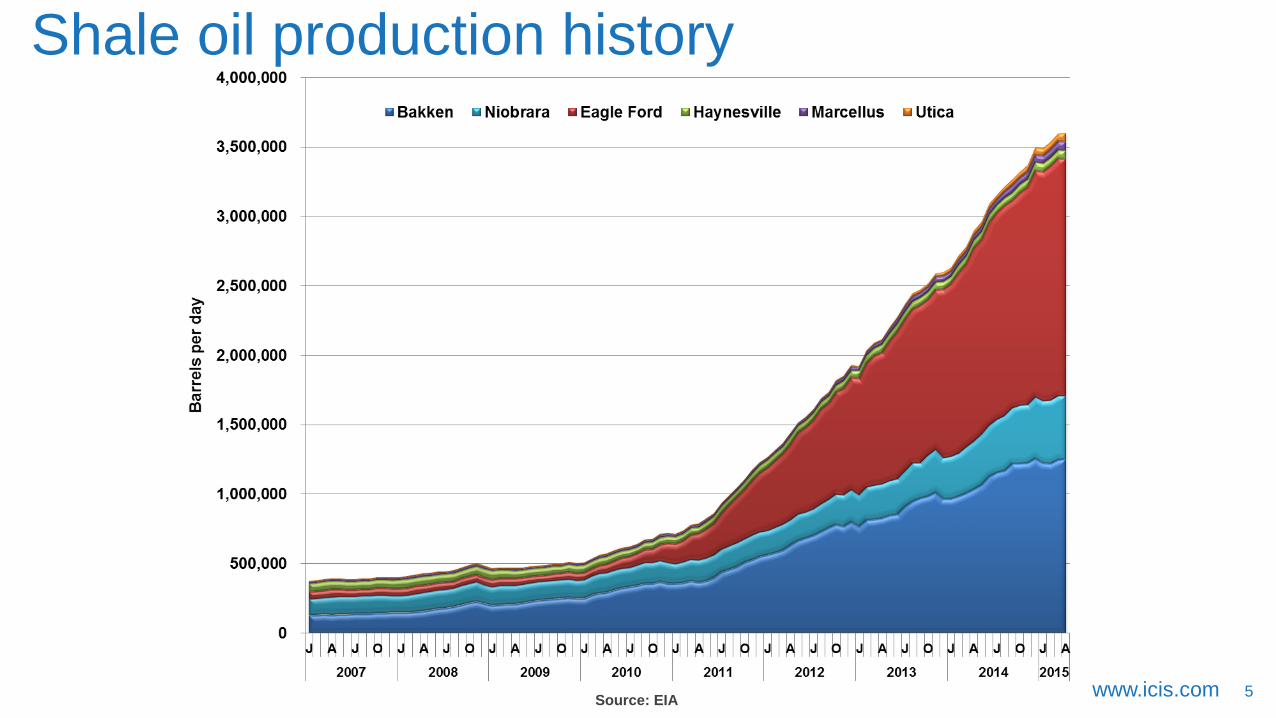

Shale oil production history

Source: EIA

www.icis.com 6

Production - 2010 vs. 2014

1.6 million bpd from most large producers, except...

With US added – difference is now 5.85 million bpd

Not 1.7% increase, but 6.3%!

This is what led to the low prices in 2015.

Source: EIA, ICIS Consulting

www.icis.com 7

• Gas cracking is solely focussed on the production of ethylene

• Heavier feedstocks produce significantly more co-products

Naphtha to Ethane:•95% reduction in propylene•96% reduction in butadiene•98% reduction in raffinate-1•98% reduction in pygas

Cracker yield patterns vary greatly across feedstock slates

Typical Yield Patterns of Different Steam Cracker

Feedstocks

0.0

0.5

1.0

1.5

2.0

2.5

3.0

ETHANE LPG NAPHTHA

Cum

ulai

ve y

ield

of p

rodu

cts,

tonn

e Ethylene Propylene Butadiene

Raffinate-1 Pygas Fuel oil

Source: ICIS Consulting

www.icis.com 8

Over supply crashes crude prices

www.icis.com 9

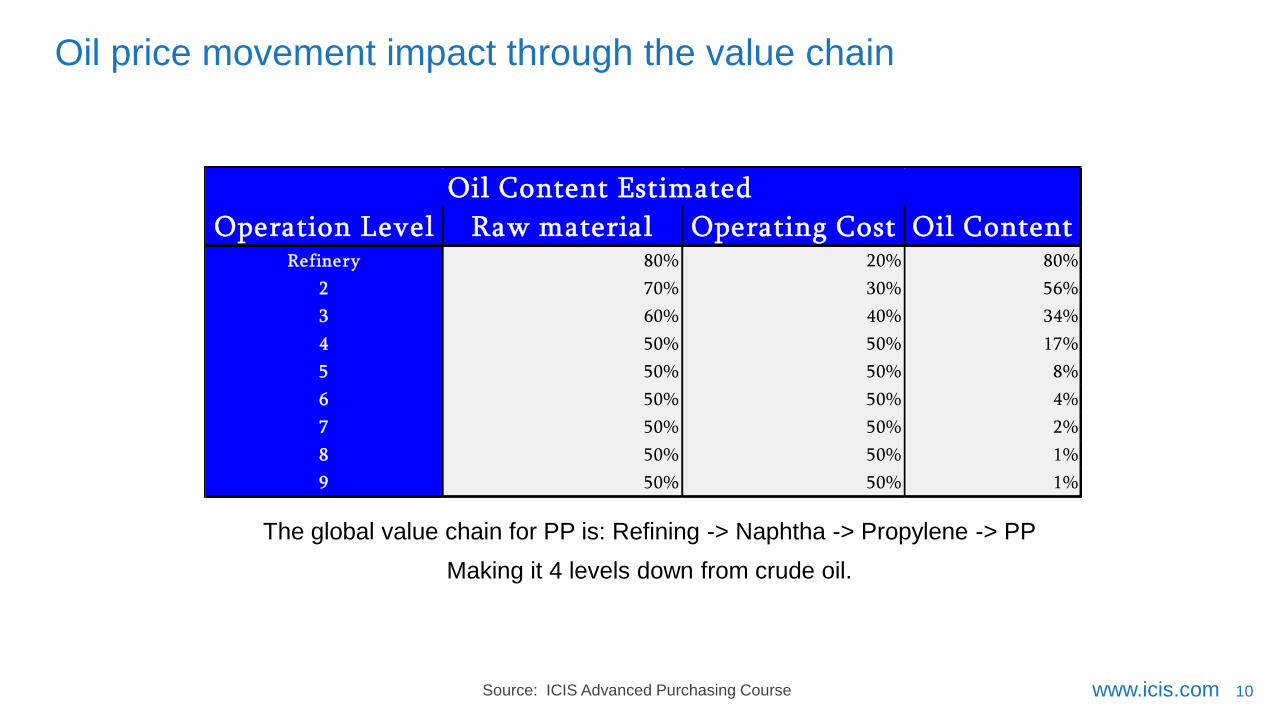

Oil price movement impact through the value chain

The Question at this point, is “Why doesn’t oil have more impact than this?”

The reason, is that the further down the value chain you travel, the more overhead, transportation, labor and profit there is.

Oil Content Theory

Operation Level Raw material Operating Cost Oil ContentRefinery 50% 50% 50%

2 50% 50% 25%

3 50% 50% 13%

4 50% 50% 6%

5 50% 50% 3%

6 50% 50% 2%

7 50% 50% 1%

8 50% 50% 0%

9 50% 50% 0%

Source: ICIS Advanced Purchasing Course

www.icis.com 10

Oil Content Estimated

Operation Level Raw material Operating Cost Oil ContentRefinery 80% 20% 80%

2 70% 30% 56%

3 60% 40% 34%

4 50% 50% 17%

5 50% 50% 8%

6 50% 50% 4%

7 50% 50% 2%

8 50% 50% 1%

9 50% 50% 1%

Oil price movement impact through the value chain

The global value chain for PP is: Refining -> Naphtha -> Propylene -> PP

Making it 4 levels down from crude oil.

Source: ICIS Advanced Purchasing Course

www.icis.com 11

PP Market – ICIS PP Sentiment Index Survey

US PP Market Price 2015 US PP Market Price 2016

The range of PP prices being paid is much wider today

www.icis.com 12

Polypropylene vs PGP

Producer margins peaked in Q3

before low cost Imports temporarily brought prices down.

www.icis.com 13

Update

www.icis.com 14

Tight Market Question

QUESTION:

Prices are increasing because the ethylene market is tight; how long is this condition expected to last?

ANSWER:

The US ethylene market is NOT tight.

In fact, the US is the second largest exporter in the world.

And the export prices are far below domestic prices to relieve the domestic over supply.

Source: ICIS Purchasing Advisory

www.icis.com 15

Tight Market Question

Knowing your product trade flow is essential for international trading.

To do so otherwise, can cost much more on a single shipment than the market intelligence costs!

Source: ICIS Purchasing Advisory

www.icis.com 16

Ethylene exports are up

Source: ICIS Dashboard - Copyright 2016 ICIS

Ethylene exports are up and will continue to rise

www.icis.com 17

HDPE vs ethylene

PE producer margins have remained high

www.icis.com 18

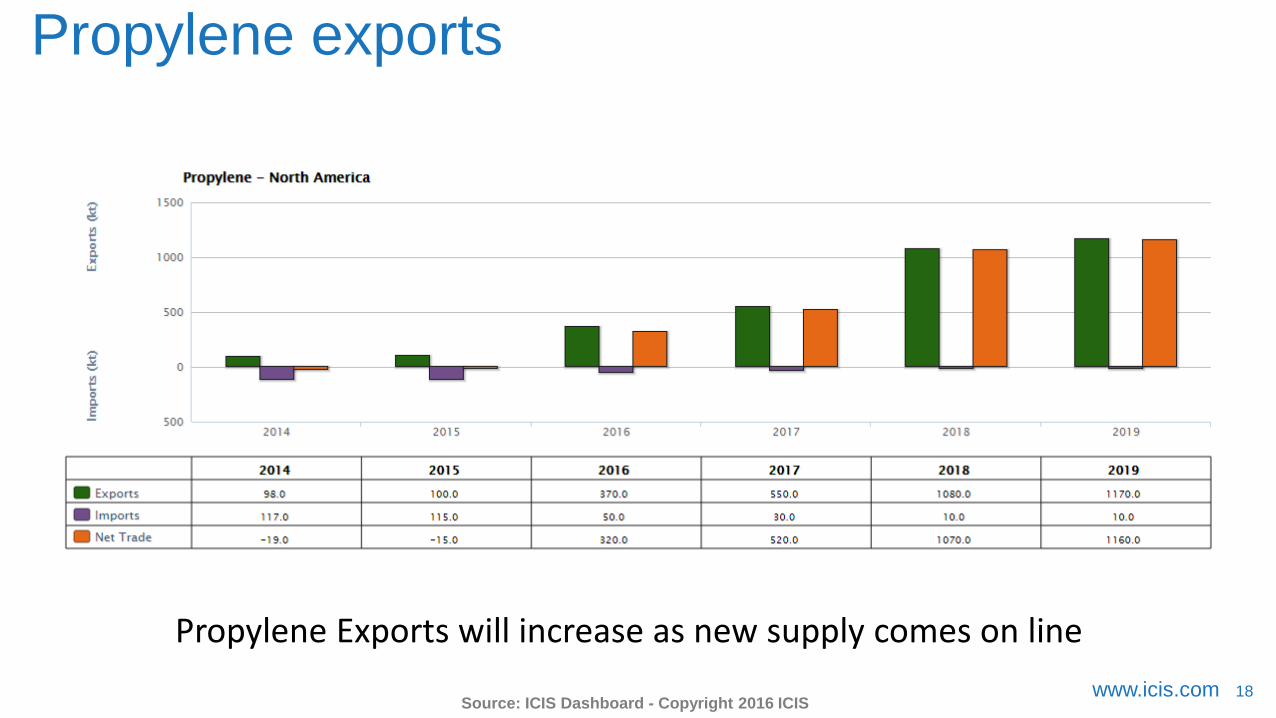

Propylene exports

Source: ICIS Dashboard - Copyright 2016 ICIS

Propylene Exports will increase as new supply comes on line

www.icis.com 19

PP vs propylene

Producer margins have remained stable

www.icis.com 20

Unexplained market price increases

QUESTION:

Why is one of my raw materials going up while oil is still low?

ANSWER:

The candid truth is that it is because most US buyers of this product lack market intelligence and strategic alternatives, so sellers can charge more without losing business volume.

I would encourage you to read the World Class Purchasing Vision in the 8/15/2016 edition of the ICIS Chemical Business Magazine.

Source: ICIS Purchasing Advisory

www.icis.com 21

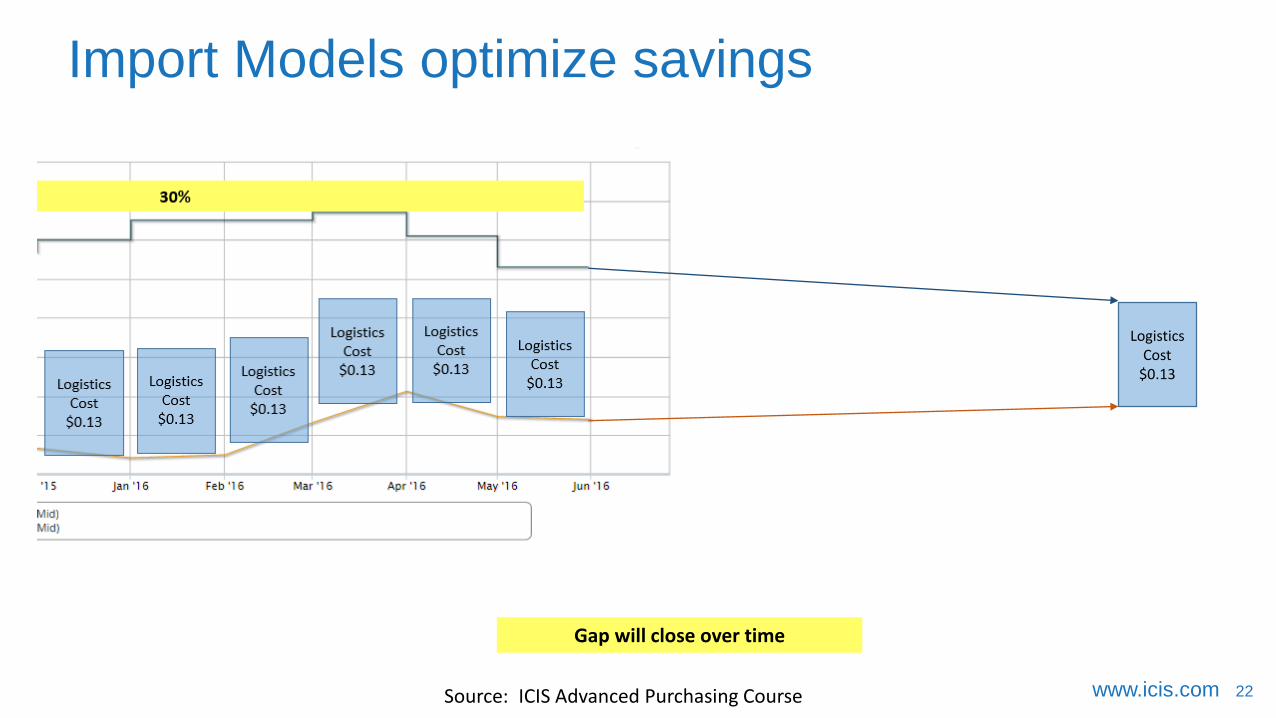

Import Models optimize savings

LogisticsCost

$0.13

10% 30%

20%

Import % of Monthly Purchase Volume

LogisticsCost

$0.13

LogisticsCost

$0.13

LogisticsCost

$0.13

LogisticsCost

$0.13

LogisticsCost

$0.13

LogisticsCost

$0.13

LogisticsCost

$0.13

LogisticsCost

$0.13 LogisticsCost

$0.13Logistics

Cost$0.13

LogisticsCost

$0.13

Source: ICIS Advanced Purchasing Course

www.icis.com 22

Import Models optimize savings

Gap will close over time

Source: ICIS Advanced Purchasing Course

LogisticsCost

$0.13

www.icis.com 23

Import Models optimize savings

Closing Gap with higher oil prices

Source: ICIS Advanced Purchasing Course

LogisticsCost

$0.13

www.icis.com 24

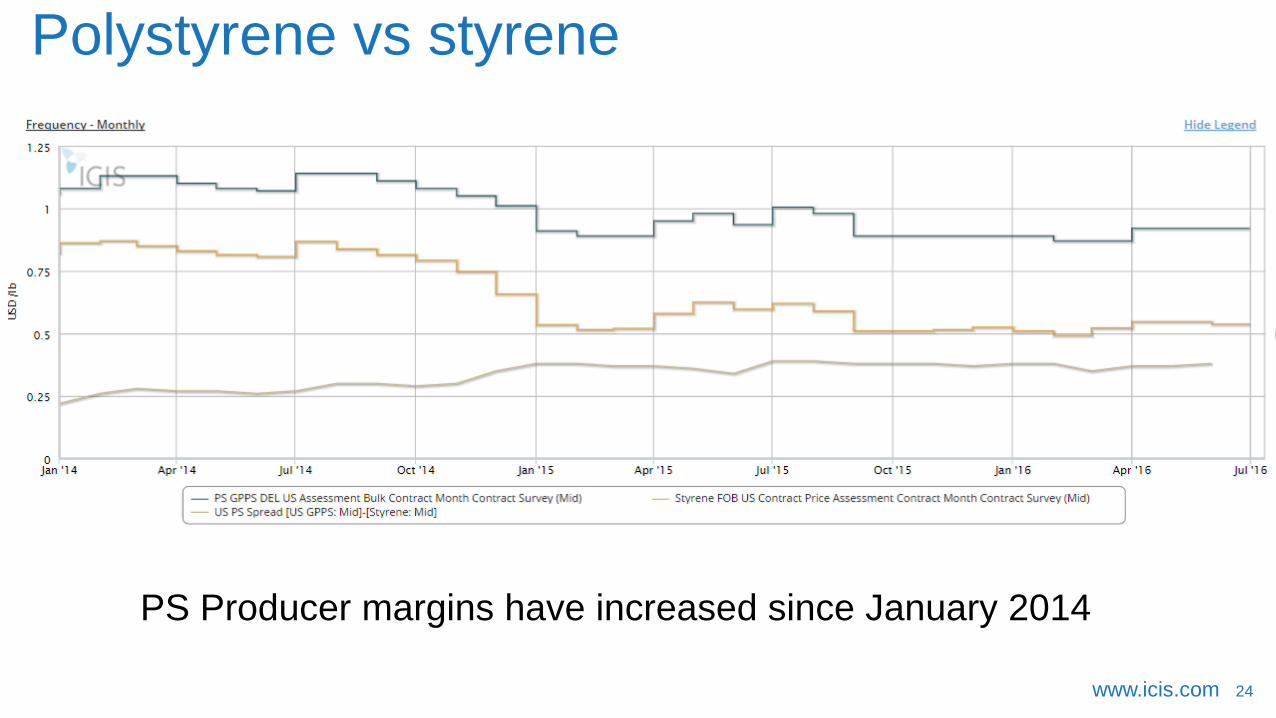

Polystyrene vs styrene

PS Producer margins have increased since January 2014

www.icis.com 25

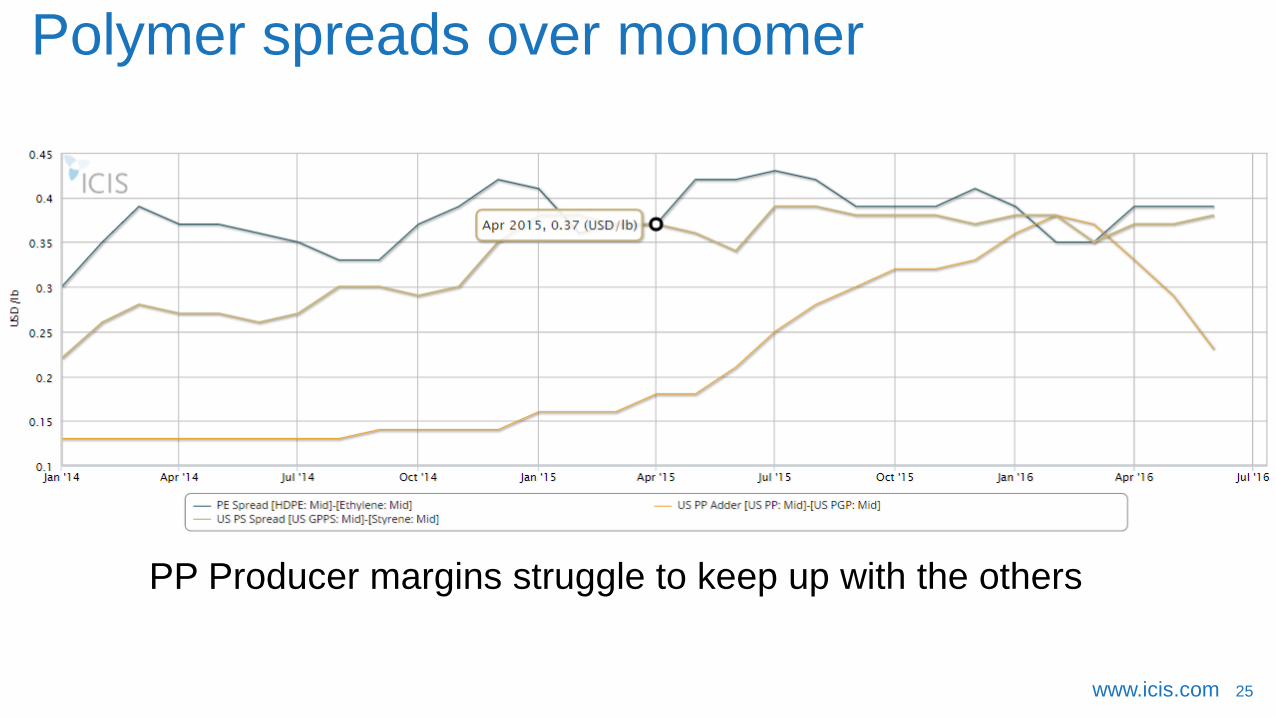

Polymer spreads over monomer

PP Producer margins struggle to keep up with the others

www.icis.com 26

Forecast

www.icis.com 27

Supply & Demand drives crude prices

www.icis.com 28

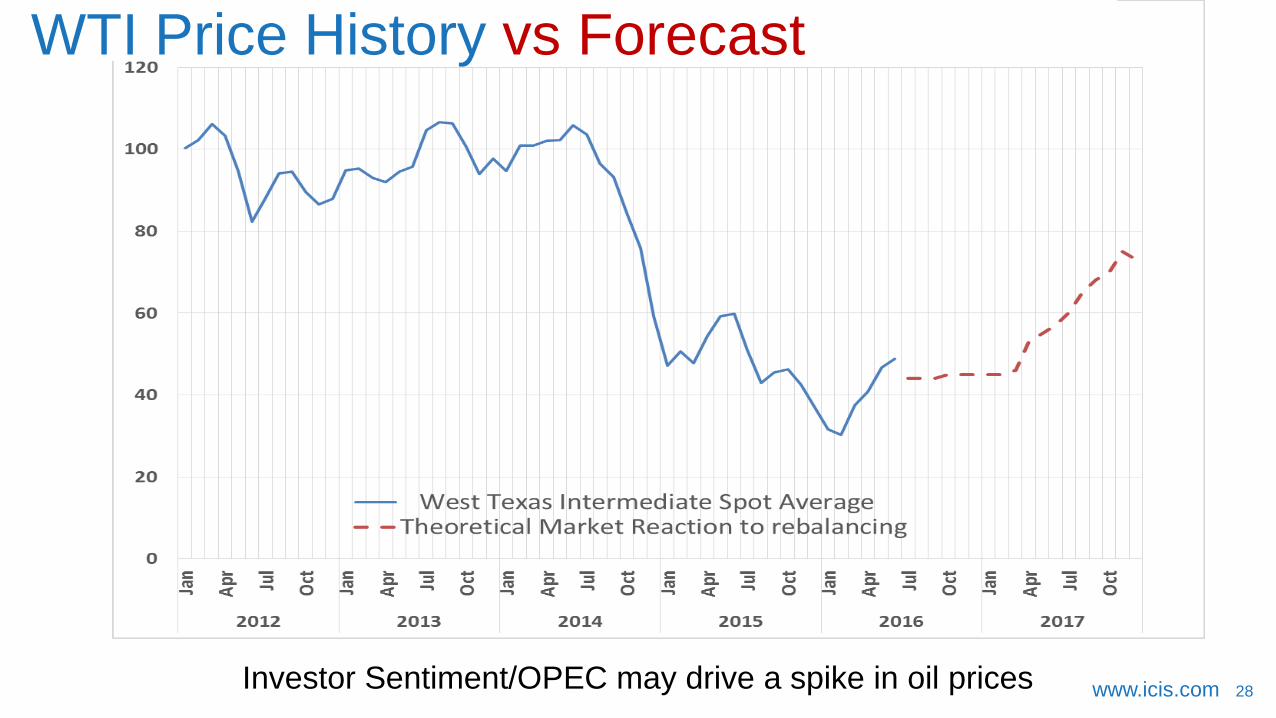

WTI Price History vs Forecast

Investor Sentiment/OPEC may drive a spike in oil prices

www.icis.com 29

Strategic Sourcing to insure a reliable supply at the lowest cost

TIGHTLONG

BALANCED

MARKET

3 - 10 year cycle

TIGHTLONG

PE Market

PP Market

Market Cycle Right now, PP is tight and growing tighter with no new capacity until probably 2020

Most markets go through a cycle of:

1. tight,2. balanced and 3. long supply

over years which affects your purchasing strategy

BALANCED

Source: ICIS Advanced Purchasing Course

PE on the other hand is slightly long and growing longer

www.icis.com 30

Strategic Sourcing to insure the lowest cost

SellersMarket

BuyersMarket

www.icis.com 31

Polyethylene supply is long

Source: ICIS Dashboard -Copyright 2016 ICIS

PE Supply is long and will remain so for several years despite growing export

www.icis.com 32

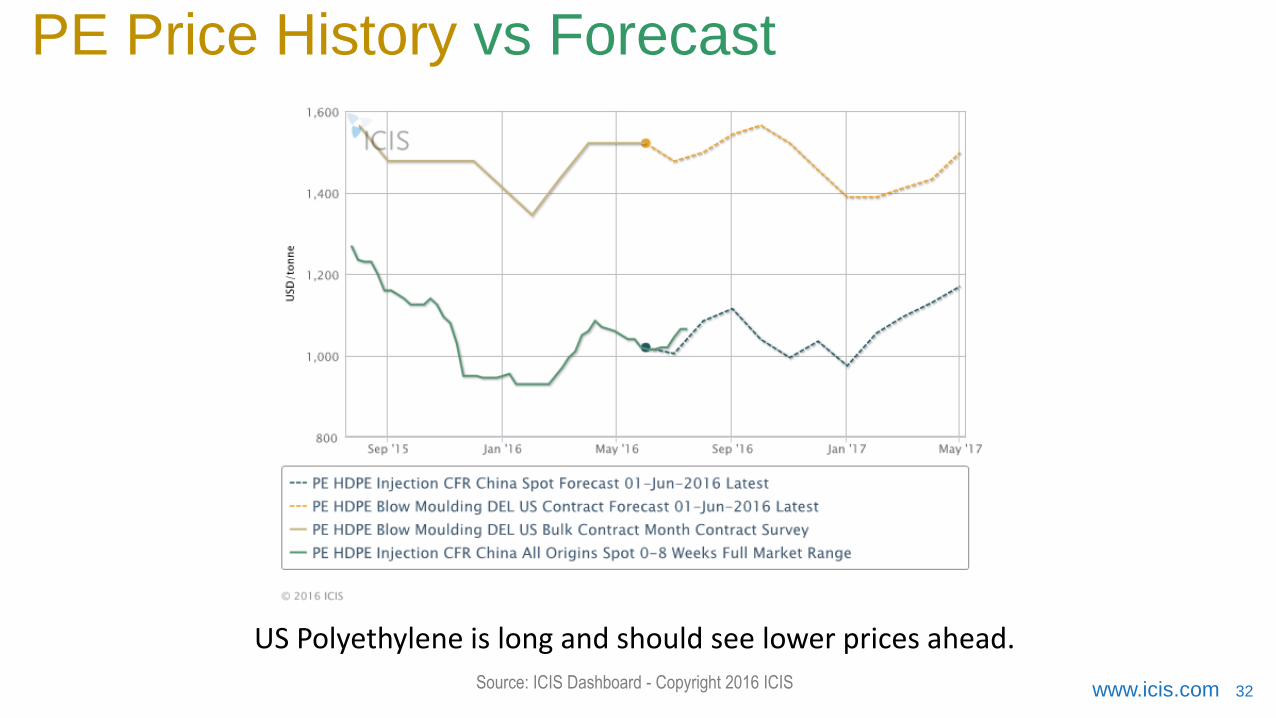

US Polyethylene is long and should see lower prices ahead.

Source: ICIS Dashboard - Copyright 2016 ICIS

PE Price History vs Forecast

www.icis.com 33

Polypropylene supply

Source: ICIS Dashboard - Copyright 2016 ICIS

PP supply is tight and utilization is headed even higher

www.icis.com 34

PP Price History vs Forecast

PP prices are expected to be stable until late 2017

www.icis.com 35

Strategic PP Sourcing to insure the lowest cost

www.icis.com 36

PS Price History vs Forecast

PS prices are expected to be lower until late 2017

www.icis.com 37

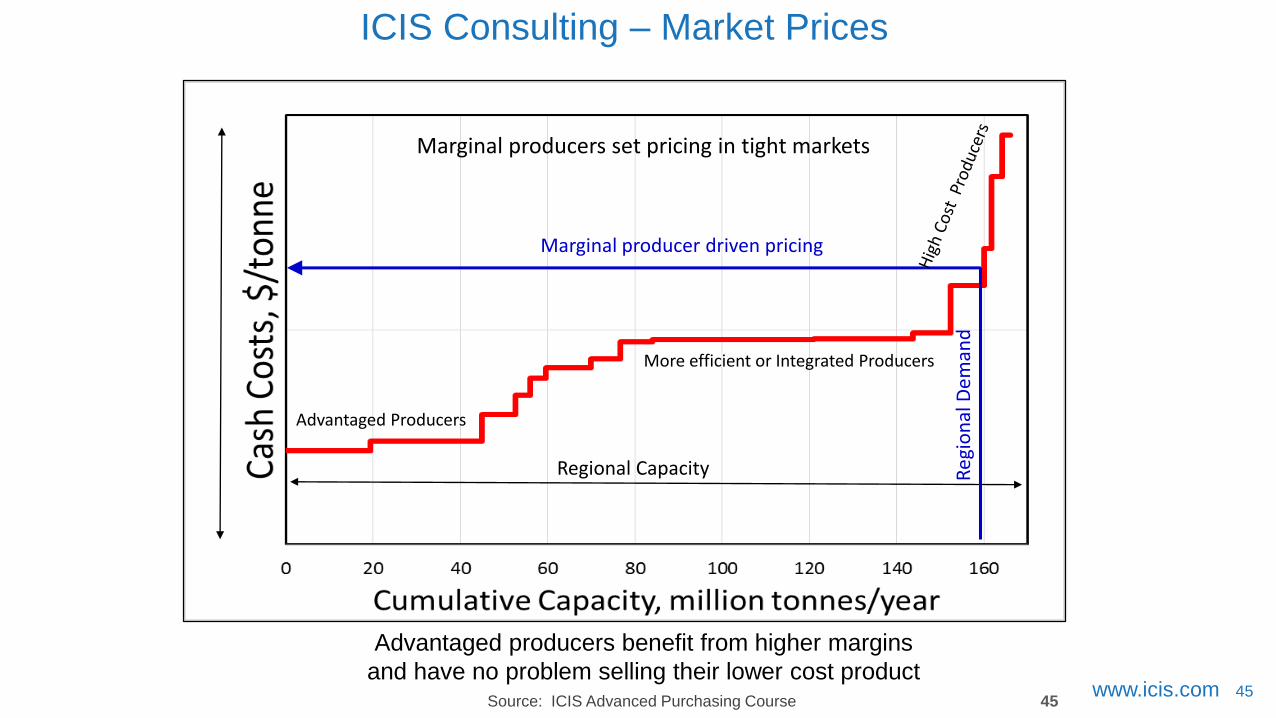

ICIS Consulting – Market Prices

Marginal producers set pricing in tight markets

More efficient or Integrated Producers

Regional Capacity

Marginal producer driven pricing

Reg

ion

al D

eman

d

37

Advantaged Producers

Advantaged producers benefit from higher margins

and have no problem selling their lower cost product

www.icis.com 38

Summary1. Higher PP Prices/Margins were realized last year as predicted.

2. Short term, prices will be stable, but changing Supply & Demand pictures will affect Purchasing Strategies.

3. PP prices will be lower short term before seeing 30+ cent adders.

4. PE Prices will be lower long term.

5. PS Prices will remain high and go even higher as 3 US producers now control over 80% of the capacity.

6. Oil Prices are generally predicted to increase slowly, but when Supply & Demand rebalances and inventory is reduced, expect investors to drive prices higher. Followed by an OPEC announcement to cut production and $100/bbl is possible.

7. Beyond that, the marginal oil producers will set the floor market price.

8. Crude oil will drive most prices higher in late 2017 and 2018.

Copyright 2016 ICIS

James Ray

Senior Consultant

ICIS Consulting, Americas

Direct: +1 713-525-2633

Cell: 1 903 245 [email protected]

http://www.linkedin.com/company/30337?trk=tyah&trkInfo=tas%3AICIS%20%2Cidx%3A3-1-5

www.linkedin.com/pub/james-ray/5/356/20b

Thank you

www.icis.com 40www.icis.com 40

APPENDIX

www.icis.com 41

Market Price Dynamics

www.icis.com 42

Ethylene Economic Model Ethylene yield model from

Linde Engineering and pricing data from ICIS pricing

Simple cost and margin measures are highly representative of typical manufacturing facilities

Models Europe, US, NEA and SEA crackers

Models naphtha and LPG feedstocks (Europe and Asia) and ethane and light naphtha feedstocks (US)

Methodology/guide:

www.icis.com/marginsFor a full methodology, click here

www.icis.com 43

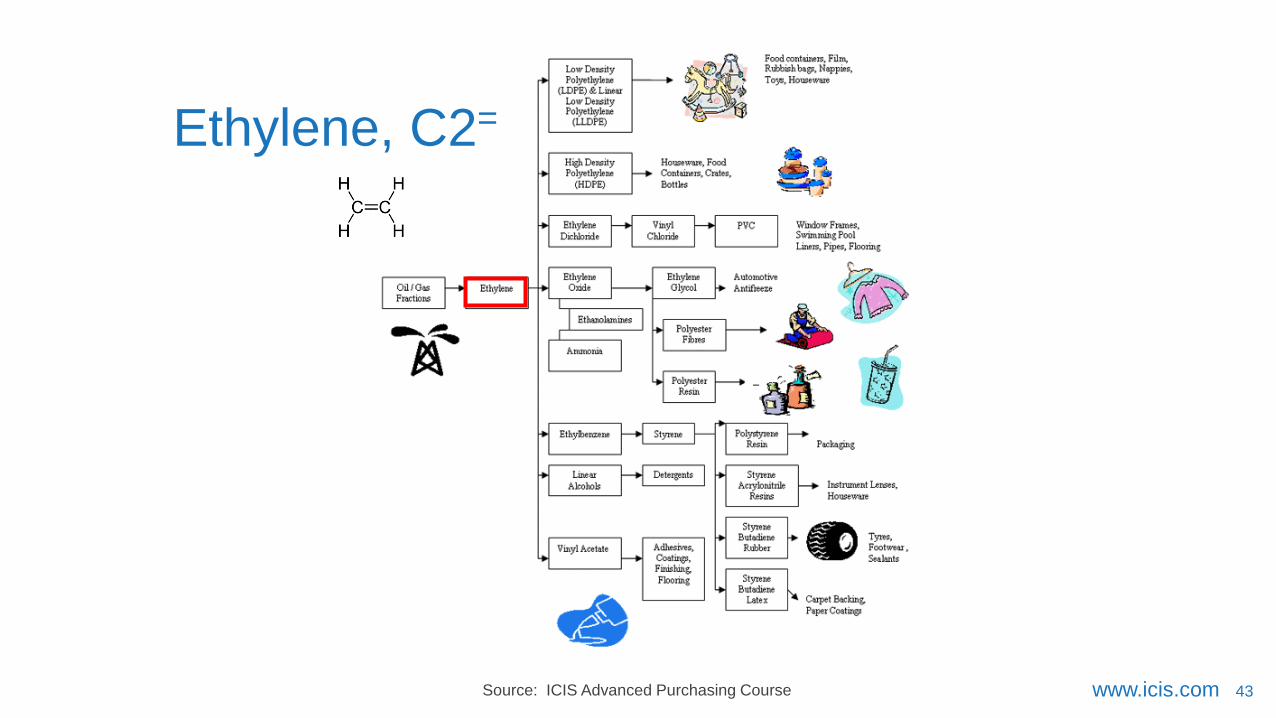

Ethylene, C2=

Source: ICIS Advanced Purchasing Course

www.icis.com 44

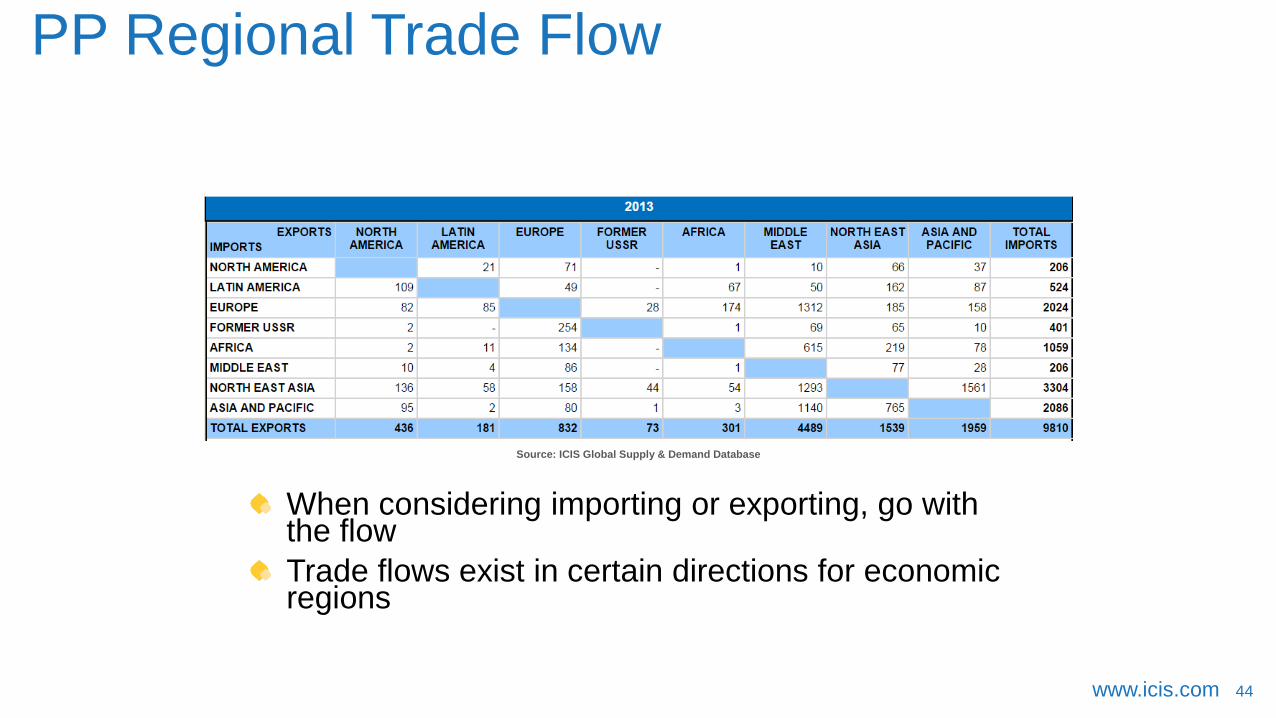

PP Regional Trade Flow

When considering importing or exporting, go with the flow

Trade flows exist in certain directions for economic regions

Source: ICIS Global Supply & Demand Database

www.icis.com 45

ICIS Consulting – Market Prices

Marginal producers set pricing in tight markets

More efficient or Integrated Producers

Regional Capacity

Marginal producer driven pricing

Reg

ion

al D

eman

d

45

Advantaged Producers

Advantaged producers benefit from higher margins

and have no problem selling their lower cost productSource: ICIS Advanced Purchasing Course

www.icis.com 46

PRICE COST MARGIN= +

Prices Consist of Cost and Margin

Margin will typically represent 15 to 60% of your market price

A function of feedstocks, variable and fixed costs

A function of Competition, i.e. supply & demand.

46Source: ICIS Advanced Purchasing Course

www.icis.com 47

Costs Correlates to Crude, but Margin does not

Margins correlate more to supply & demand

0

200

400

600

800

1000

1200

1400

1600

0 10 20 30 40 50 60 70 80

US

Do

llars

/ t

on

Crude Oil US$ per Bbl

Ethylene Variable Cost vs. Crude Oil

(Historical US$/Ton)

0

200

400

600

800

1000

1200

1400

1600

0 10 20 30 40 50 60 70 80

US

Do

llars

/ t

on

Crude Oil US$ per Bbl

Ethylene Variable Margins vs. Crude Oil

(Historical US$/Ton)

47Source: ICIS Advanced Purchasing Course

www.icis.com 48

Aromatic Derivatives

48Source: ICIS Advanced Purchasing Course

www.icis.com 49

Ethylene supply

Source: ICIS Dashboard - Copyright 2016 ICIS

Ethylene supply is up and utilization is headed downward

www.icis.com 50

Using High and Low Risk

50Source: ICIS Advanced Purchasing Course

www.icis.com 51

Ethylene margins via ethane cracking

Ethane cracking margins are very attractive investments because of

low cost ethane feedstocks

Source: ICIS Pricing

www.icis.com 52

Ethylene margins via naphtha cracking

Naphtha based ethylene is much less attractive and is the marginal

producer that sets the market price

Source: ICIS Pricing

www.icis.com 53

LDPE margins on February 27, 2015

1. Sell LDPE at: 80.00 cpp2. Purchase Ethylene at: -35.25 cpp3. Operating cost is:-9.59 cpp

===========Margin is:35.16 cpp

Source: ICIS Advanced Purchasing Course

www.icis.com 54

LDPE Margins on February 12, 2016

1. Sell LDPE at: 73.00 cpp2. Purchase Ethylene at: -24.75 cpp3. Operating cost is:

-10.02 cpp===========

Margin is:38.23 cpp

Source: ICIS Advanced Purchasing Course

www.icis.com 55

Oil price movement impact through the value chain

Using some analysis tools from the ICIS Advanced Purchasing Class, we compare the actual EO price against a theoretical one, which suggests there are savings opportunities that have been missed.

Good market intelligence like this helps buyers and sellers realize the full potential that they can capitalize on.

Source: ICIS Advanced Purchasing Course

www.icis.com 56

Sample Value Chain (detailed)

www.icis.com 57Source: ICIS Advanced Purchasing Course

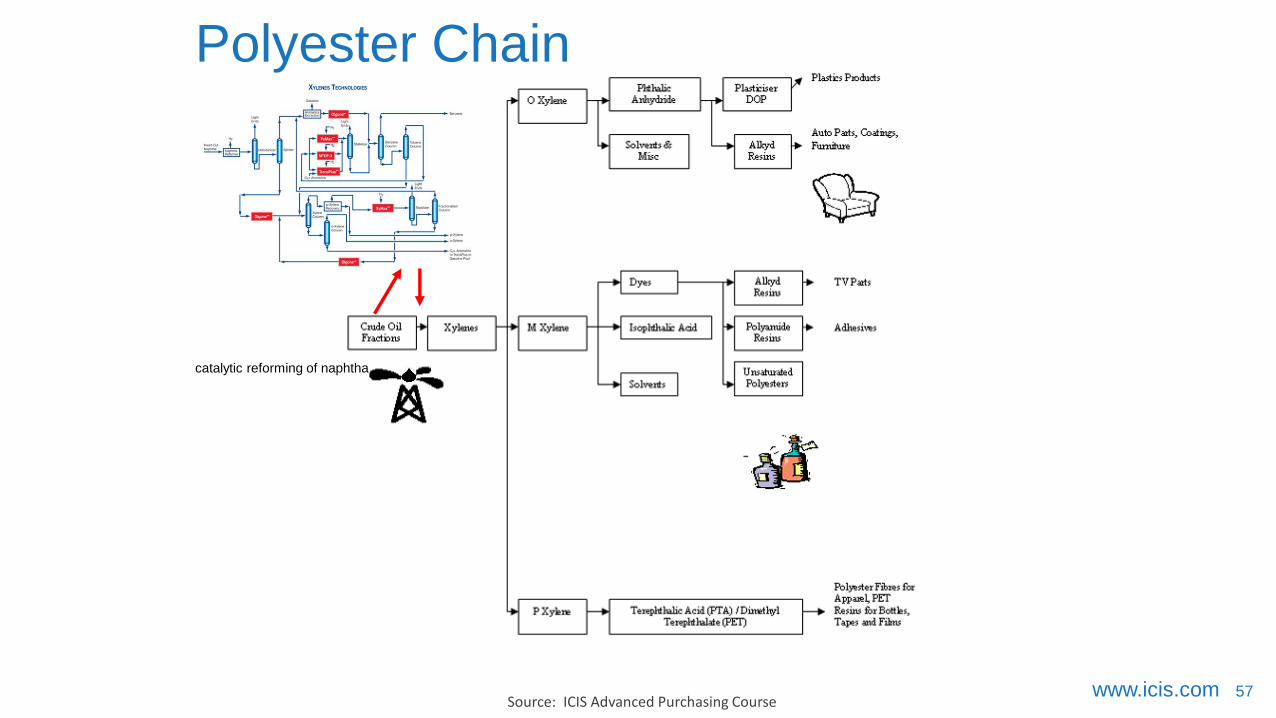

Polyester Chain

catalytic reforming of naphtha

www.icis.com 58

Polyester Chain

Source: ICIS Advanced Purchasing Course

www.icis.com 59

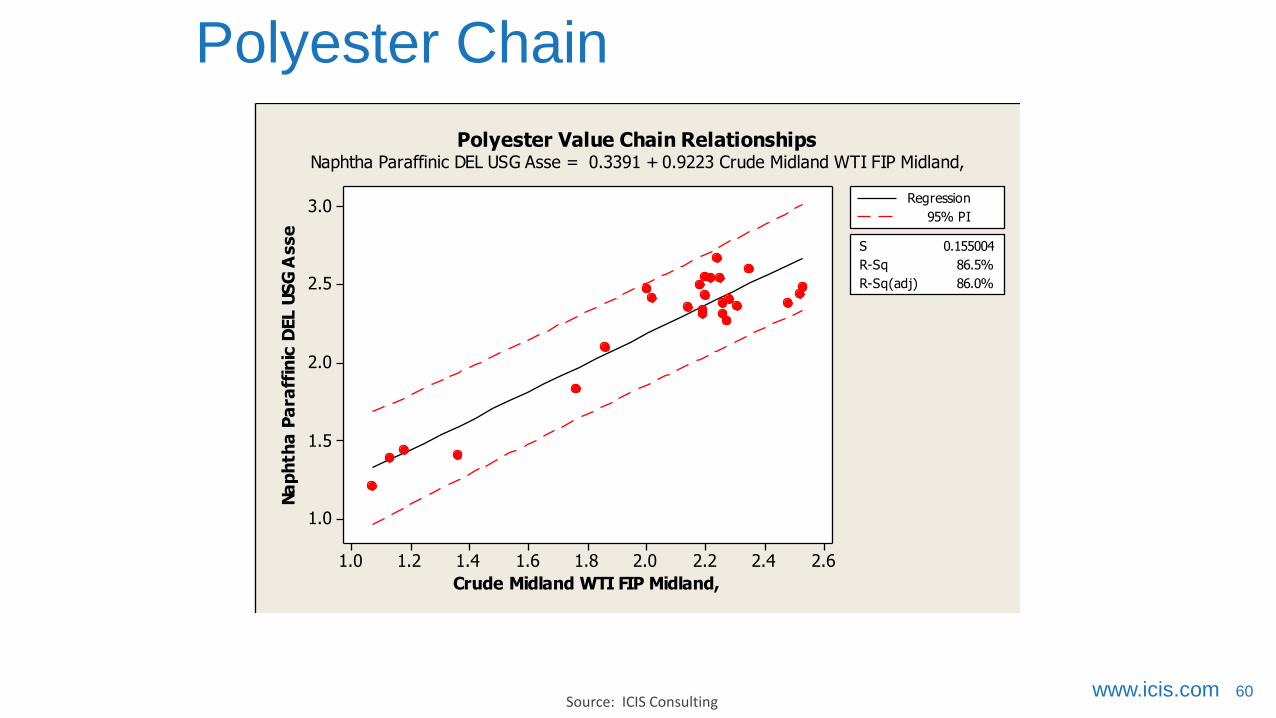

Polyester Chain

Source: ExxonMobil Chemical

www.icis.com 60

Polyester Chain

Source: ICIS Consulting

2.62.42.22.01.81.61.41.21.0

3.0

2.5

2.0

1.5

1.0

Crude Midland WTI FIP Midland,

Na

ph

tha

Pa

raff

inic

DEL U

SG

Asse

S 0.155004

R-Sq 86.5%

R-Sq(adj) 86.0%

Regression

95% PI

Polyester Value Chain RelationshipsNaphtha Paraffinic DEL USG Asse = 0.3391 + 0.9223 Crude Midland WTI FIP Midland,

www.icis.com 61

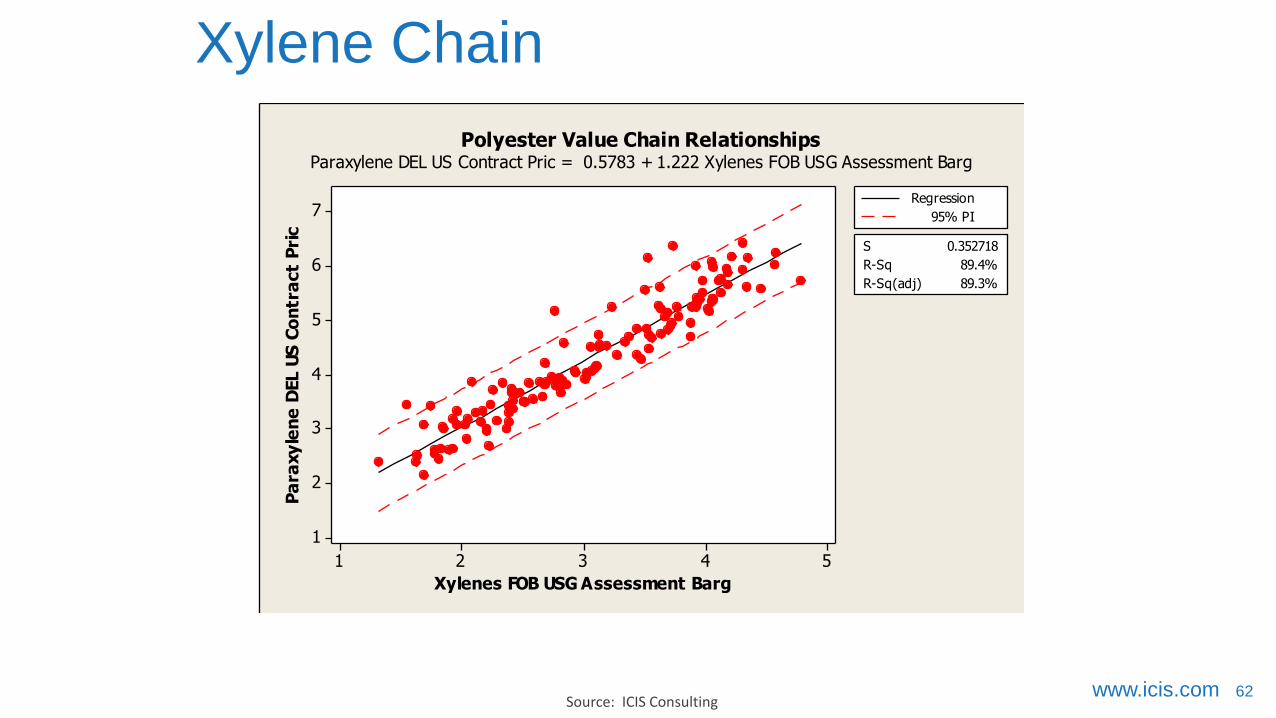

Xylene Chain

Source: ICIS Consulting

2.82.62.42.22.01.81.61.41.21.0

5

4

3

2

1

Naphtha Paraffinic DEL USG Asse

Xy

len

es F

OB

US

G A

sse

ssm

en

t B

arg

S 0.259449

R-Sq 85.8%

R-Sq(adj) 85.3%

Regression

95% PI

Polyester Value Chain RelationshipsXylenes FOB USG Assessment Barg = 0.1913 + 1.512 Naphtha Paraffinic DEL USG Asse

www.icis.com 62

54321

7

6

5

4

3

2

1

Xylenes FOB USG Assessment Barg

Pa

raxy

len

e D

EL U

S C

on

tra

ct

Pri

c

S 0.352718

R-Sq 89.4%

R-Sq(adj) 89.3%

Regression

95% PI

Polyester Value Chain RelationshipsParaxylene DEL US Contract Pric = 0.5783 + 1.222 Xylenes FOB USG Assessment Barg

Xylene Chain

Source: ICIS Consulting

www.icis.com 63

Xylene Chain

Source: ICIS Consulting

4.54.03.53.02.52.0

6.5

6.0

5.5

5.0

4.5

4.0

3.5

3.0

Xylenes FOB USG Assessment Barg

PTA

DEL U

S C

on

tra

ct

Pri

ce

Asse

s

S 0.128722

R-Sq 96.4%

R-Sq(adj) 96.3%

Regression

95% PI

Polyester Value Chain RelationshipsPTA DEL US Contract Price Asses = 1.522 + 0.9673 Xylenes FOB USG Assessment Barg

www.icis.com 64

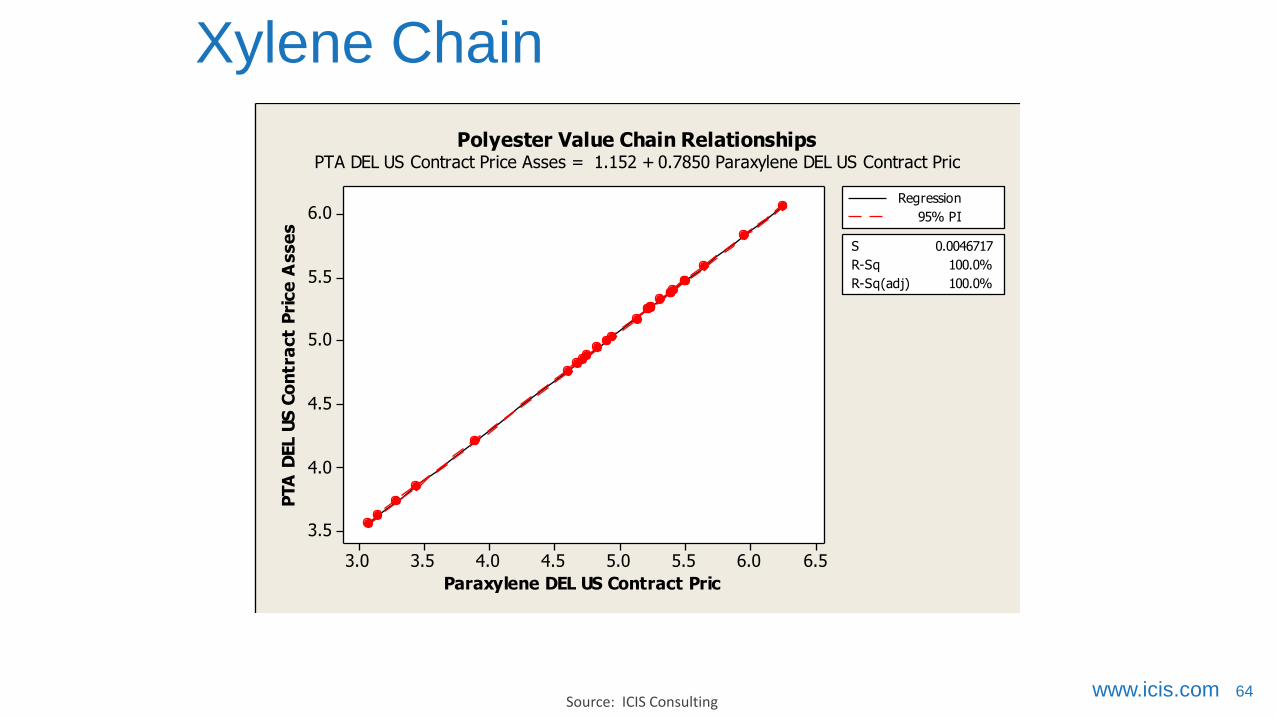

Xylene Chain

Source: ICIS Consulting

6.56.05.55.04.54.03.53.0

6.0

5.5

5.0

4.5

4.0

3.5

Paraxylene DEL US Contract Pric

PTA

DEL U

S C

on

tra

ct

Pri

ce

Asse

s

S 0.0046717

R-Sq 100.0%

R-Sq(adj) 100.0%

Regression

95% PI

Polyester Value Chain RelationshipsPTA DEL US Contract Price Asses = 1.152 + 0.7850 Paraxylene DEL US Contract Pric

Thank youJames Ray

Senior Consultant

ICIS Consulting, Americas

Direct: +1 713-525-2633

Cell: 1 903 245 [email protected]

http://www.linkedin.com/company/30337?trk=tyah&trkInfo=tas%3AICIS%20%2Cidx%3A3-1-5

www.linkedin.com/pub/james-ray/5/356/20b

www.icis.com 66

ICIS Advanced Purchasing Class

1. Understand cost structures and price drivers in petrochemicals

markets

2. Improve your comprehension of costs, margins and the value

chain

3. Learn how to effectively measure your performance

4. Explore contract mechanisms and how to improve supplier

relationships

5. Gain expert insights into strategy planning and risk

management

6. Develop your own cost model, to reduce exposure and

maximize margins

• http://www.icis.com/training/specialist-training-courses1/advanced-purchasing-skills-training-course/

ICIS PP Forecast Report

www.icis.com 68

www.icis.com 69

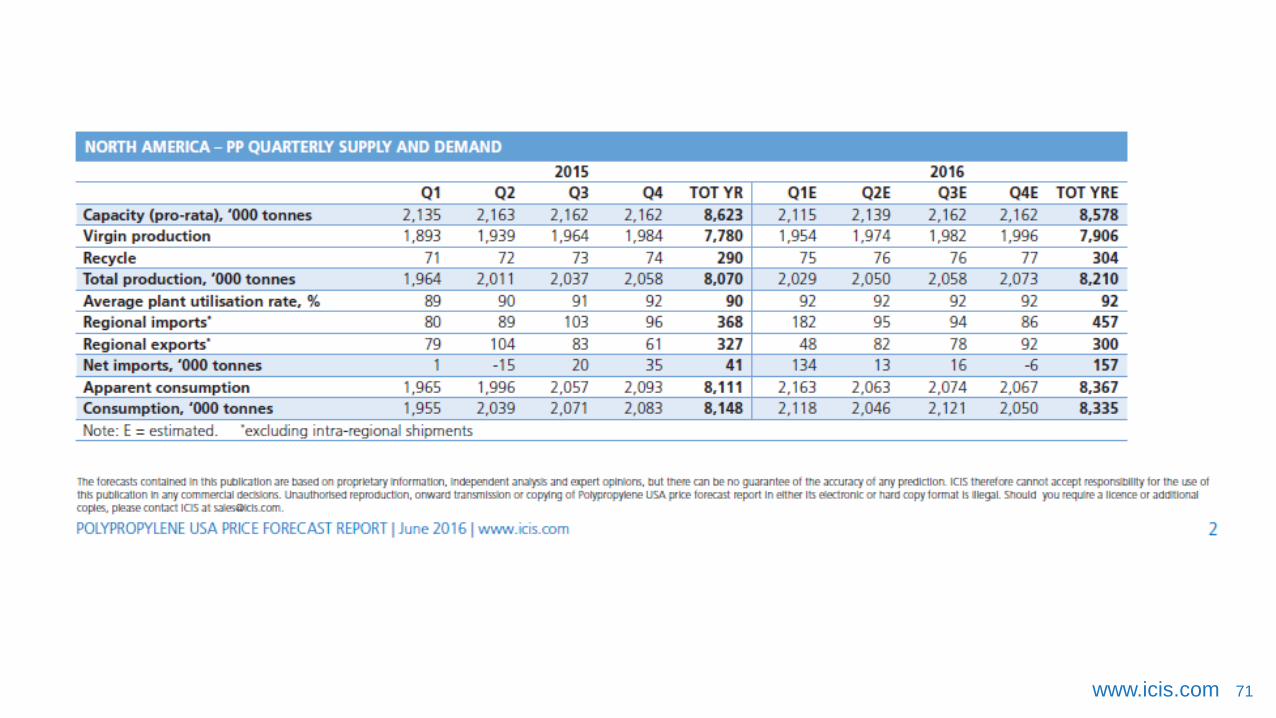

www.icis.com 70

www.icis.com 71

www.icis.com 72

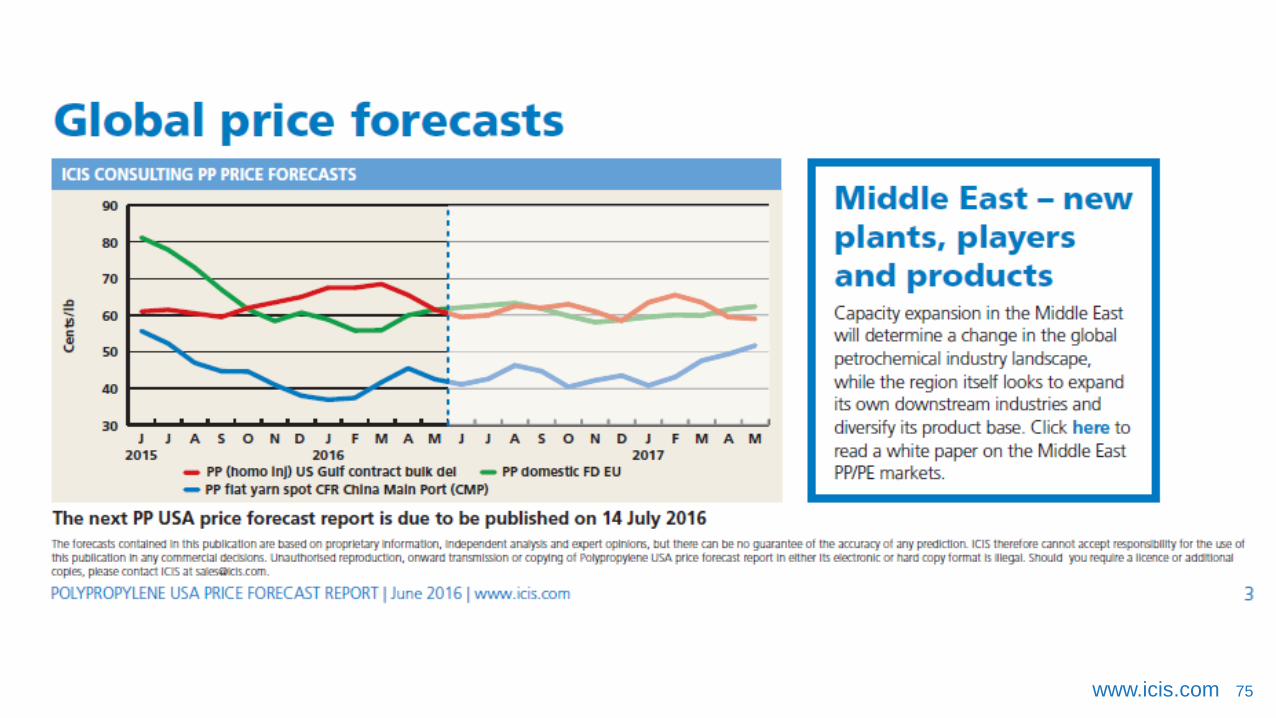

www.icis.com 73

The ICIS Sentiment Index is sent to hundreds of market participants. If you would like to participate and get a free report register here:

http://forms.icis.com/icis-sentiment-index

www.icis.com 74

www.icis.com 75

www.icis.com 76

www.icis.com 77

ICIS Consulting

Your partner for research and analysis, providing an alternative view of

chemical, fertilizer and energy markets

Access to powerful tools, data and industry experts providing:

• Insight on the global energy and crude markets, oil refining, petrochemicals,

fertilizers, specialty polymers and fine chemicals

• China specific insight into the domestics iron and steel, non-ferrous metals

and paper and pulp markets

• Analysis of current and future market prices, margins and supply and

demand trends that could affect your business

www.icis.com 78

ICIS, providing an alternative view of the global chemical and energy markets

Clients considering multi-

million dollar co-located

investment

An ICIS market study revealed

previously unseen issues for

both buyers & sellers and

offered client alternatives for

saving over $70,000,000

Will the site and

proposed formula

pricing be competitive

for 20 - 30 years?

www.icis.com 79

Clients planning a new chemical

plant need take-off agreements

Prior to public announcement,

clients need product sales outlets to

arrange financing for new operations

Through our vast network of contacts, ICIS was able to

arrange introductions to high level contacts within interested

companies resulting in several sales outlets for the client

ICIS, providing an alternative view of the global chemical and energy markets

www.icis.com 80

ICIS, providing an alternative view of the global chemical and energy markets

Growing converter clients

purchasing $500,000,000 of raw

material in a tight market

struggled with price and supply

issues

Through weekly consultations, ICIS guided clients through regional

short term raw material contract negotiations, cost reduction team

activities, and presented long term take-off opportunities.

Developing a global strategy along with working smarter, client was

able to reduce commodity raw material costs by approximately 2%

in a tight market

How do we insure a reliable

supply without over

paying?

www.icis.com 81

Multi-national clients seeking JV for a

multi-billion dollar investment

How sustainable is the shale

advantage?

Several feasibility studies were conducted by ICIS

Consulting for olefins/derivatives and refinery

feedstock complexes with the outcome pending

ICIS, providing an alternative view of the global chemical and energy markets

www.icis.com 82

How should we manage the business to

exploit increasingly global markets?

Calling on our wealth of global market and

industry information and combining that

with an insight of your business, we can

identify and outline opportunities and

scenarios.

ICIS Consulting recently carried

out a review of the Asian

propylene, paraxylene and

benzene markets for an Indian

petrochemical producer who was

keen to understand opportunities

ahead of its plant start up.

How could we grow our business

through organic growth and

acquisitions?

We can provide merger and acquisitions,

diversification and restructuring support to

help you make decisions about acquisition

investments and which organic developments

would deliver the greatest opportunities. ICIS

can carry out all the required research, from

initial screenings through to due diligence or

launch, including a full service capability for

the Chinese market.

ICIS, providing an alternative view of the global chemical and energy markets

www.icis.com 83

How can we be more profitable?

Using our price and margin models, as well

as our detailed supply and demand data,

we can provide in depth price and

profitability forecasting, providing your

business with reasoned analysis to support

future business and environment scenarios.

A market review and commercial

due diligence were performed for

a PTA producer ahead of their

annual PX term purchase

negotiations.

How should we manage future risks

to our business?

Future price and supply and demand

scenarios enable you to carry out

market and product developments

analysis to better understand where

you are heading in your markets.

ICIS, providing an alternative view of the global chemical and energy markets

www.icis.com 84

How can we be more competitive?

Our comprehensive company structure

and ownership information supports

customized competitive analysis work

allowing you to benchmark your

business and discover opportunities for

competitive advantage..

A feasibility study was conducted

by ICIS Consulting for a new

market entrant to explore product

options for an olefins/derivatives

and refinery feedstock complex.

Could we diversify to take

advantage of projected

margins?

Market entry studies and feasibility

analysis projects can support your

assessment of how attractive other

markets would be and drive your

development strategies. We also

conduct technology assessments,

helping you to focus and select the

right features for business success.

ICIS, providing an alternative view of the global chemical and energy markets

www.icis.com 85

How will projected supply and

demand trends affect my business?

Up to 50 years of historical information and

insight and al comprehensive view on the

short and long term supply and demand

landscape provide you with an outlook for your

products and markets.

ICIS recently provided an

expert opinion case review

to support a ship owner’s

case against an alleged

contamination claim.

What independent information and

expertise can I call on to help me

resolve disputes?

We can provide independent, expert

services for disputes and arbitration to

support the resolution of difficult

commercial issues when they occur.

ICIS, providing an alternative view of the global chemical and energy markets

www.icis.com 86

Contact us

Alan Holm

Head of Consulting and [email protected]

James Ray

Senior Consultant, [email protected]

Mike Perkins

Vice President, [email protected]

Ee Foong Ewe

Vice President, [email protected]

Purchasing Advisory Services available for feedstock and take-off agreements as well as market studies.