Embed Size (px)

Citation preview

Basics of Securitization Accounting

2004 ELA Lease Accountants Conference

2

2

What are Securitizations?

• Securitizations are a form of structured finance—cash flows are gathered and repackaged for the benefit of investors

• Securitizations are also known as asset backed securities (ABS)

− Borrowers lower their cost of financing− Investors get a credit enhanced product

• Securitization can either be on-balance sheet (secured financing) or off-balance sheet (sale of assets)

3

3

Elements of Securitization

• Servicing of assets− Collection of cash− Payment of cash to investors− Collection decisions (repossession vs. workout)− Originator/seller generally serves as servicer

• Limited recourse to originator/seller− Consistent with “true sale”− Originator/seller frequently retains subordinated classes that

provide credit enhancement to investors

4

4

Advantages to the Issuer

Real Advantages• Reduced cost of funds—every issuer can finance at AAA

rates• Structuring is Flexible—cash flows can be allocated in many

different ways− Credit ratings− Prepayments

Perceived Advantages with Sale Accounting• Improved ratios—leverage declines• Ability to recognize gains on sale of assets

5

5

FAS 140

Accounting for Transfers and Servicing of

Financial Assets and Extinguishments of

Liabilities

6

6

What Is The Conceptual Basis For A Sale Of Financial Assets Under FAS 140?

• The Transferor has SURRENDERED CONTROL of the assets. It should account for its interests in the assets

7

7

Are Leases Covered by FAS 140?

• FAS 140 relates to sale of financial assets− Equipment is not a financial asset− Operating leases are not financial assets− Capital leases can be financial assets

8

8

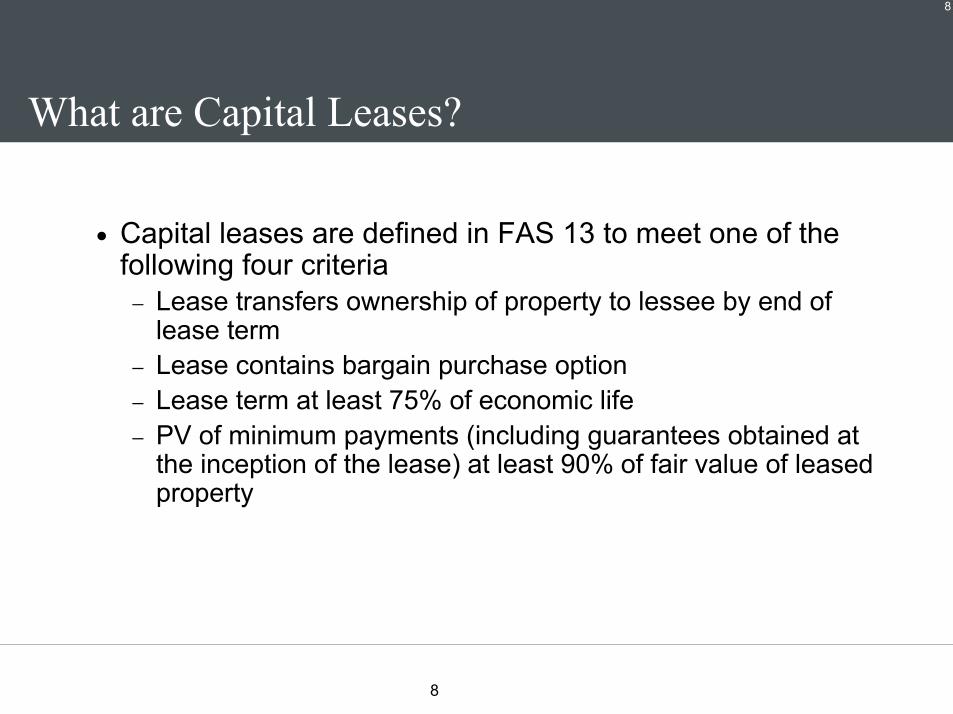

What are Capital Leases?

• Capital leases are defined in FAS 13 to meet one of the following four criteria

− Lease transfers ownership of property to lessee by end of lease term

− Lease contains bargain purchase option− Lease term at least 75% of economic life− PV of minimum payments (including guarantees obtained at

the inception of the lease) at least 90% of fair value of leasedproperty

9

9

Securitization of Capital Leases

• Capital Leases can be sold in a securitization transaction using a QSPE

• QSPE cannot own non-financial assets—including the residuals—a securitization of capital leases will strip out the residual

• Many operating lease securitization transactions have been structured to be on-balance sheet

− Automobile lease transactions are largest segment− Large residual makes lease operating lease without residual

guarantee

10

10

A Sale Of Financial Assets Must MeetALL Three Conditions

• Legal isolation from transferor

• Transferee must be able to pledge or exchange assets(If transferee is a QSPE, the beneficial interest holders must be able to pledge or exchange their beneficial interests)

• Transferor surrenders control of assets

11

11

What Is Involved In Legal Isolation?

• True sale− Have I sold the assets or have I simply raised money through a

secured borrowing?

• Non-consolidation− Is the buyer of the assets going to be consolidated with the

seller in the event of bankruptcy?

• Two step sale− Sale or contribution to bankruptcy-remote SPE

• True Sale− Transfer to securitization issuer

• Either a true sale or a first perfected security interest

12

12

Why Is a QSPE Important in Securitization?

• If transferee is not a QSPE, it must be able to pledge or exchange the assets for the transfer to be a sale

• FAS 140 REQUIRES that transferor DOES NOT consolidate a QSPE

• FIN 46R extends non-consolidation to most other parties− Cannot have unilateral right to cause the QSPE to liquidate

13

13

What Conditions Must a QSPE Meet?

• “Demonstrably distinct” from the transferor

• Limits on permitted activities

• Limits on assets

• Limits on sales of assets

14

14

What Does “Demonstrably Distinct” Mean?

The SPE cannot be unilaterally dissolved by the transferor, itsaffiliates or agents AND either:

• 10% of the fair value of the interests are held by independent third parties; or

• It is a guaranteed mortgage securitization

15

15

What Limitations Does A QSPE FaceOn Its Activities?

All of the activities must be:

• Significantly limited

• Entirely specified upfront in the legal agreements

• May be changed only with the approval of a majority of the independent investors

16

16

What Assets May A QSPE Hold?

• Passive financial assets transferred to it

• Passive derivatives

• Guarantees

• Servicing rights

• Temporarily non-financial assets obtained through foreclosure

• Cash and other temporary investments

17

17

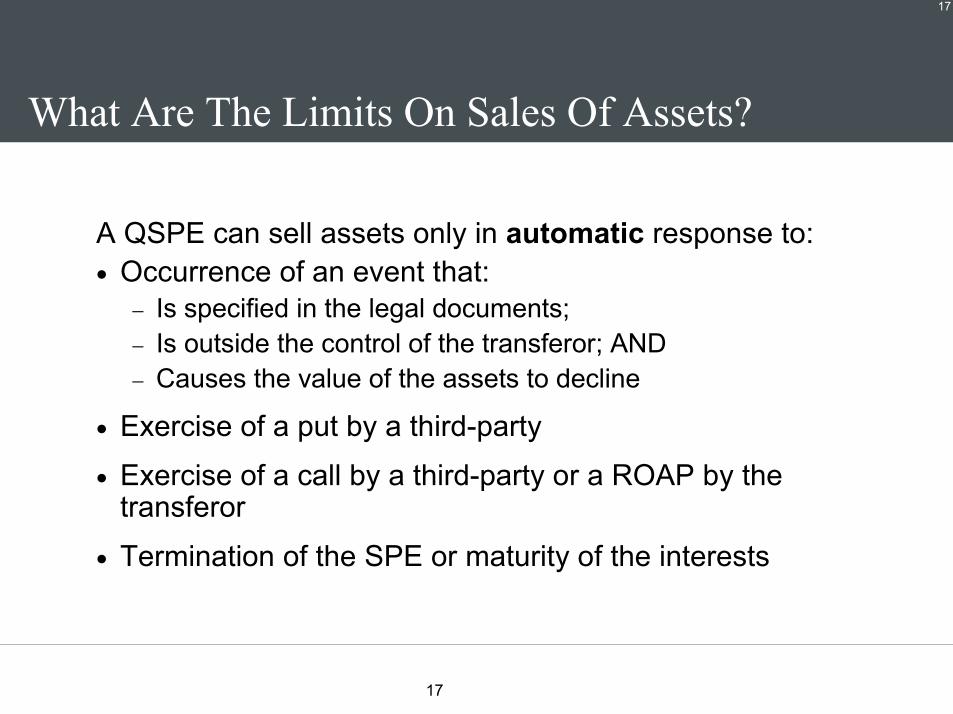

What Are The Limits On Sales Of Assets?

A QSPE can sell assets only in automatic response to:• Occurrence of an event that:

− Is specified in the legal documents;− Is outside the control of the transferor; AND− Causes the value of the assets to decline

• Exercise of a put by a third-party

• Exercise of a call by a third-party or a ROAP by the transferor

• Termination of the SPE or maturity of the interests

18

18

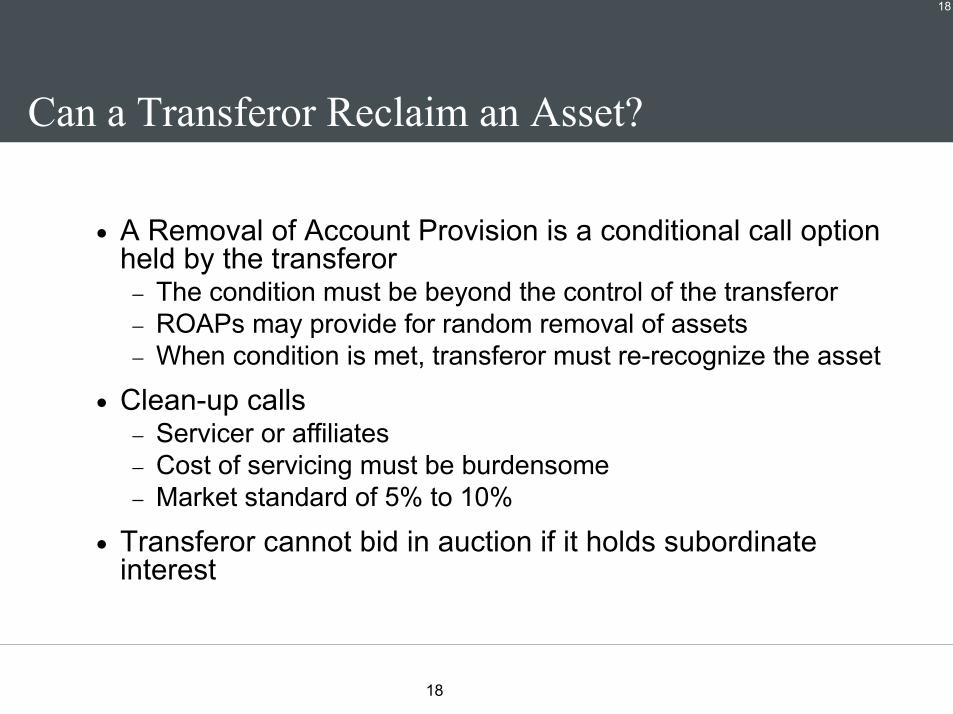

Can a Transferor Reclaim an Asset?

• A Removal of Account Provision is a conditional call option held by the transferor

− The condition must be beyond the control of the transferor− ROAPs may provide for random removal of assets− When condition is met, transferor must re-recognize the asset

• Clean-up calls− Servicer or affiliates− Cost of servicing must be burdensome− Market standard of 5% to 10%

• Transferor cannot bid in auction if it holds subordinate interest

19

19

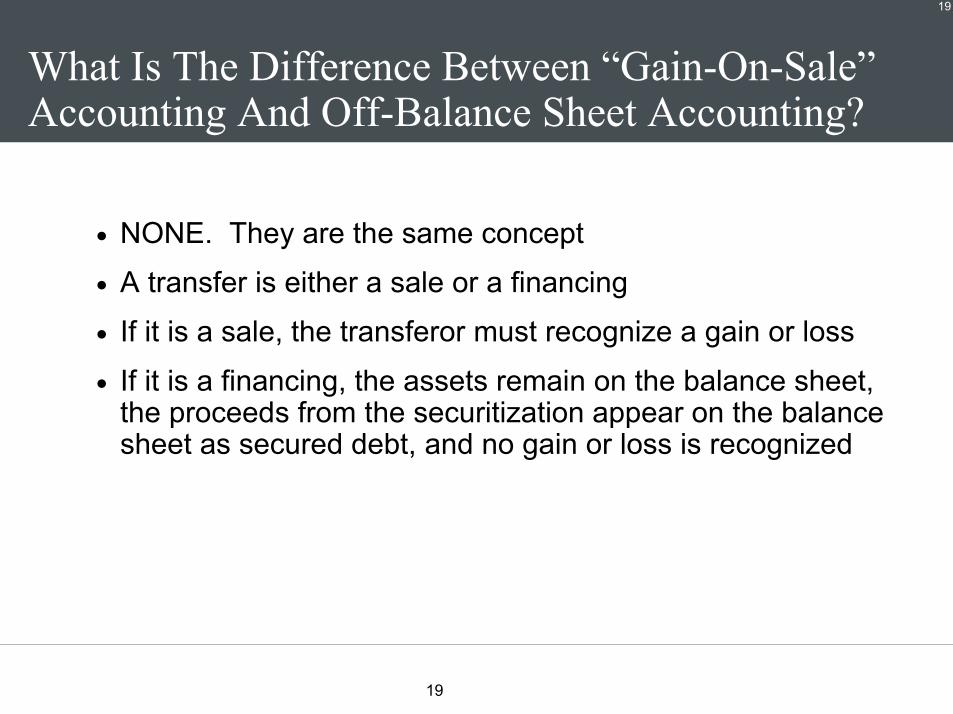

What Is The Difference Between “Gain-On-Sale” Accounting And Off-Balance Sheet Accounting?

• NONE. They are the same concept

• A transfer is either a sale or a financing

• If it is a sale, the transferor must recognize a gain or loss

• If it is a financing, the assets remain on the balance sheet, the proceeds from the securitization appear on the balance sheet as secured debt, and no gain or loss is recognized

20

20

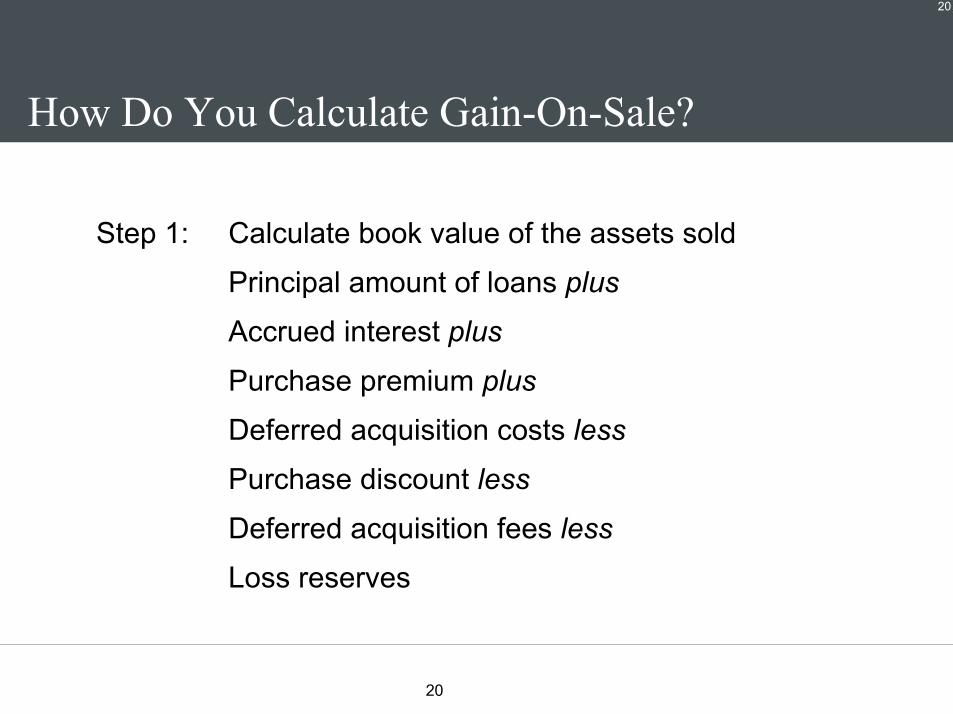

Step 1: Calculate book value of the assets sold

Principal amount of loans plusAccrued interest plus

Purchase premium plusDeferred acquisition costs lessPurchase discount less

Deferred acquisition fees lessLoss reserves

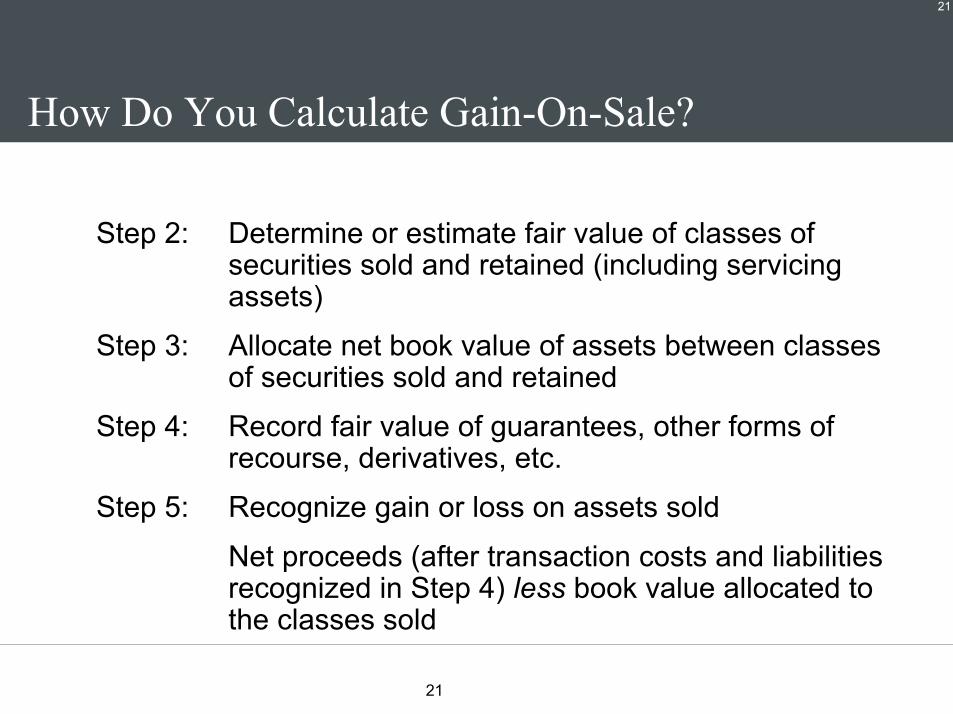

How Do You Calculate Gain-On-Sale?

21

21

Step 2: Determine or estimate fair value of classes of securities sold and retained (including servicing assets)

Step 3: Allocate net book value of assets between classes of securities sold and retained

Step 4: Record fair value of guarantees, other forms of recourse, derivatives, etc.

Step 5: Recognize gain or loss on assets sold

Net proceeds (after transaction costs and liabilities recognized in Step 4) less book value allocated to the classes sold

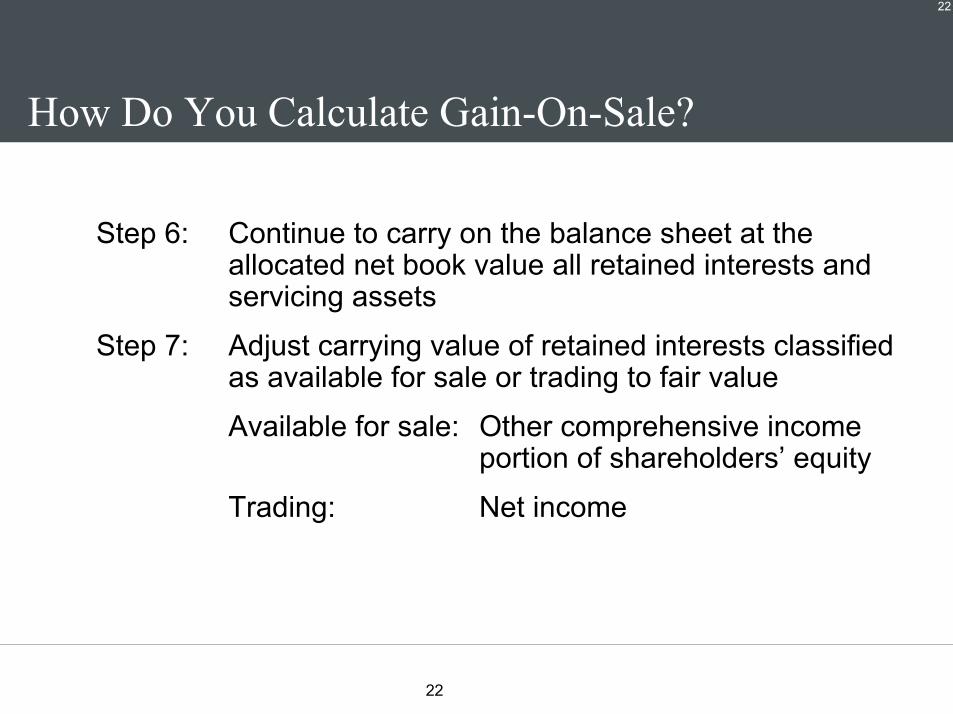

How Do You Calculate Gain-On-Sale?

22

22

Step 6: Continue to carry on the balance sheet at the allocated net book value all retained interests and servicing assets

Step 7: Adjust carrying value of retained interests classified as available for sale or trading to fair value

Available for sale: Other comprehensive income portion of shareholders’ equity

Trading: Net income

How Do You Calculate Gain-On-Sale?

23

23

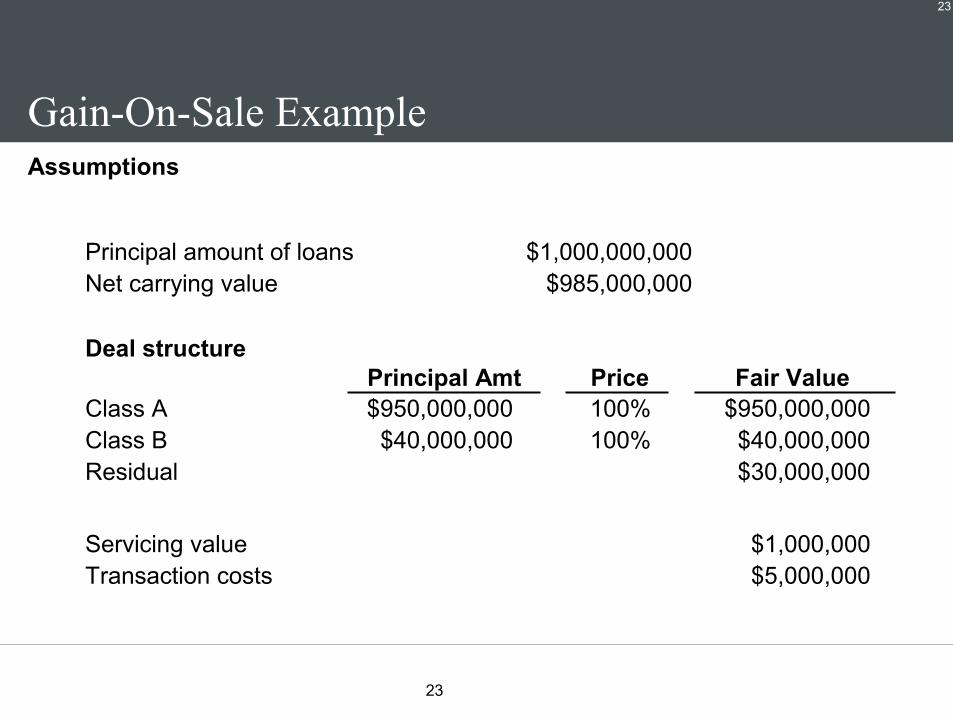

Gain-On-Sale Example

Principal amount of loansNet carrying value

Deal structure

Class AClass BResidual

Servicing valueTransaction costs

Principal Amt Price Fair Value$950,000,000

$40,000,000100%100%

$950,000,000$40,000,000$30,000,000

$1,000,000$5,000,000

$1,000,000,000$985,000,000

Assumptions

24

24

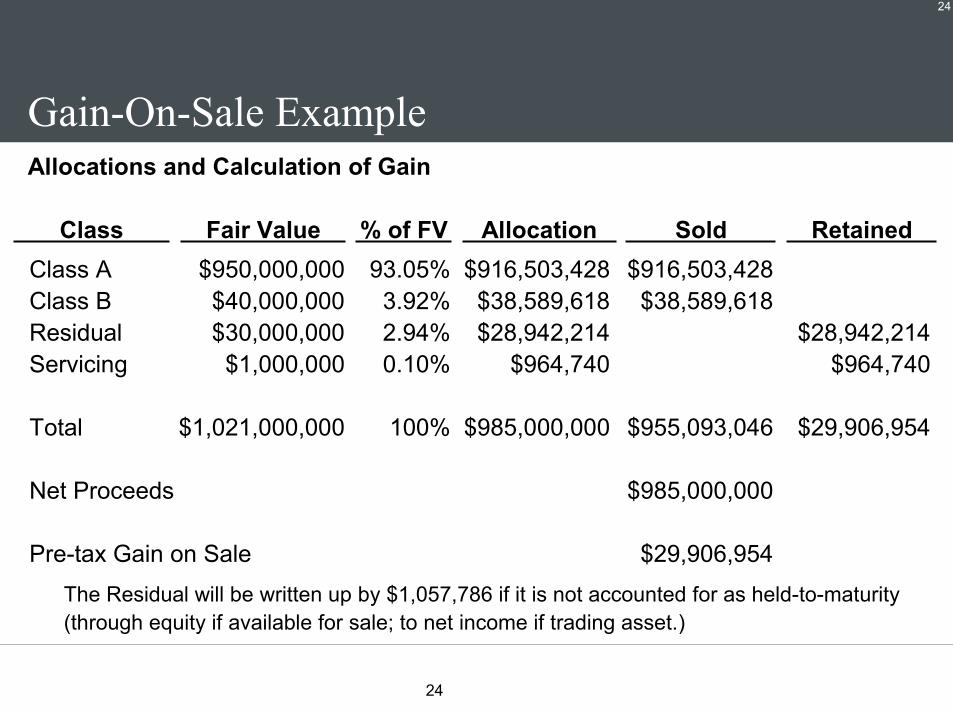

Gain-On-Sale Example

Class AClass BResidualServicing

Total

Net Proceeds

Pre-tax Gain on Sale

Class Fair Value % of FV Allocation Sold Retained$950,000,000$40,000,000$30,000,000

$1,000,000

$1,021,000,000

93.05%3.92%2.94%0.10%

100%

$916,503,428$38,589,618$28,942,214

$964,740

$985,000,000

$916,503,428$38,589,618

$955,093,046

$985,000,000

$29,906,954

$28,942,214$964,740

$29,906,954

The Residual will be written up by $1,057,786 if it is not accounted for as held-to-maturity (through equity if available for sale; to net income if trading asset.)

Allocations and Calculation of Gain

25

25

How Does A Transferor Value Residual Interests And Servicing Contracts?

• Underlying assumptions about interest rates, default rates, prepayment rates should reflect market assumptions

• Estimates of future cash flows should be based on reasonable and supportable assumptions and estimates

• All evidence should be considered

• Range of estimates should be considered (directly through expected cash flows or indirectly through risk adjusted discount rate)

26

26

FIN 46R

Consolidation of Variable Interest Entities

27

27

What Is The Conceptual Basis For FIN 46R?

• The party that has a majority of the RISKS AND REWARDS from an entity controls that entity and should be required to consolidate it

28

28

History of FIN 46R

• FIN 46 was issued in January 2003− Widely criticized as vague and difficult to apply

• FIN 46R was issued in December 2003− More than half of the paragraphs in the original statement were

changed− Some significant changes − Additional guidance provided in some areas− However, it provided no new guidance on how to apply the test

29

29

Summary of FIN 46R

• Primary Beneficiary refers to the party that has a controlling financial interest in a and must consolidate

• Variable Interests are the means through which financial support is provided to an entity and the providers gain or lose

• Qualifying SPEs under FAS 140 are not subject to the Interpretation—both for the transferor and other parties

30

30

What is a Variable Interest Entity?

• A Variable Interest Entity meets one of the following conditions:− Total equity at risk is not sufficient to permit the entity to finance its

activities without additional subordinated support• Presumed minimum of 10% can be overcome by several methods,

including equity greater than expected losses of the entity− Equity investors as a group lack one of the following characteristics:

• Direct or indirect ability to make decisions that affect the entity’s activities through voting rights (with voting rights proportional to obligation to absorb losses and/or right to receive upside)

• Obligation to absorb the expected losses of the entity if they occur• Right to receive expected residual returns of the entity if they occur

31

31

Who Is The Primary BeneficiaryAnd Consolidates?

• Primary Beneficiary holds Variable Interests that will absorb a majority of the VIE’s Expected Losses (the downside) and/or receive a majority of the VIE’s Expected Residual Returns (the upside)

• If one party has a majority of the downside and another has a majority of the upside, the party with the downside will be required to consolidate

• The ability to make decisions that significantly affect the results of the VIE is a “strong indication” of control

32

32

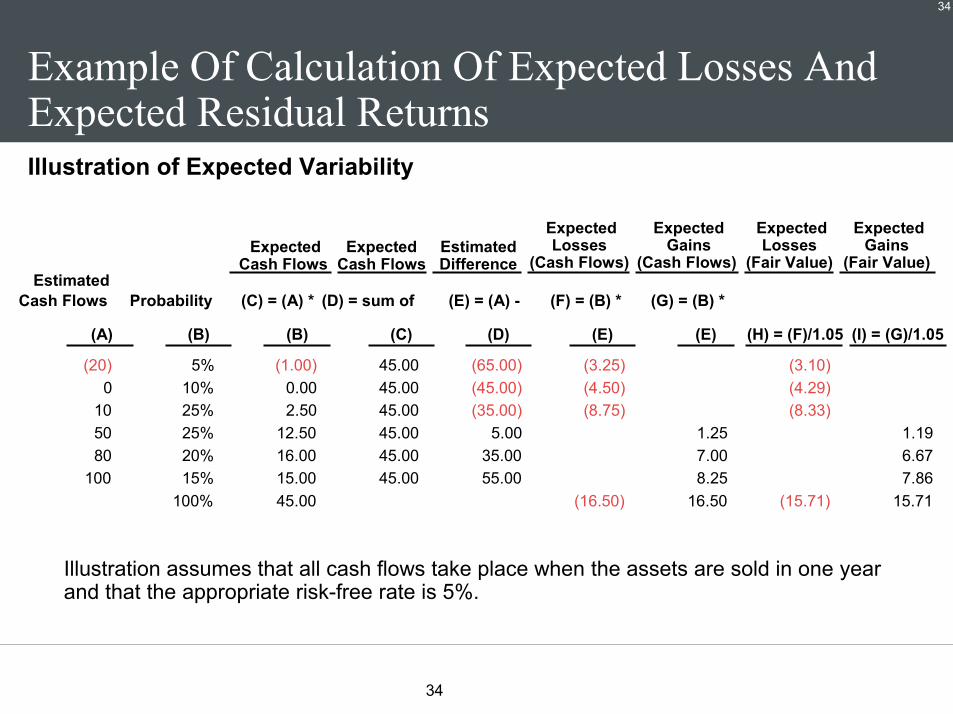

What Are “Expected Losses” And “Expected Residual Returns”?

• Expected Losses is the negative variability in the fair value of the net assets exclusive of variable interests

• Expected Residual Returns is the positive variability in the fair value of the net assets exclusive of variable interests

• Variability in fair value or cash flow?

• How do you allocate expected losses and expected residual returns among different holders of variable interests?

33

33

When Is The Primary Beneficiary Determined?

• Party determines whether it must consolidate a VIE at the time it first becomes involved with the VIE

• Must reconsider on few occasions− Significant change in contractual agreements− Primary Beneficiary sells some or all of its Variable Interests or

another party purchases additional interests− VIE issues new variable interests− Poor performance does not cause reconsideration

34

34

Example Of Calculation Of Expected Losses And Expected Residual Returns

ExpectedCash Flows

ExpectedCash Flows

EstimatedDifference

Estimated Cash Flows Probability (C) = (A) * (D) = sum of (E) = (A) - (F) = (B) * (G) = (B) *

(A) (B) (B) (C) (D) (E) (E) (H) = (F)/1.05 (I) = (G)/1.05

(20) 5% (1.00) 45.00 (65.00) (3.25) (3.10)0 10% 0.00 45.00 (45.00) (4.50) (4.29)

10 25% 2.50 45.00 (35.00) (8.75) (8.33)50 25% 12.50 45.00 5.00 1.25 1.19 80 20% 16.00 45.00 35.00 7.00 6.67

100 15% 15.00 45.00 55.00 8.25 7.86 100% 45.00 (16.50) 16.50 (15.71) 15.71

ExpectedGains

(Cash Flows)

ExpectedLosses

(Cash Flows)

ExpectedLosses

(Fair Value)

ExpectedGains

(Fair Value)

Illustration assumes that all cash flows take place when the assets are sold in one year and that the appropriate risk-free rate is 5%.

Illustration of Expected Variability

35

35

What Are “Silos” In FIN 46?

• A “silo” is a portion of a VIE in which ALL of the liabilities of the “silo” are asset specific—they all rely on specific assets as the only source of payment. A silo will be considered as a separate VIE and will be excluded the analysis of the VIE that owns the specific assets

Silos are expected to rarely exist due to the narrow definition.

E&Y has concluded that a total return swap may result in a silo. Other firms conclude that general recourse debt will eliminate a silo.

36

36

Variable Interests in Specified Assets

• Variable interests may relate only to specific assets and not the VIE as a whole (e.g., a guarantee of a loan; a subordinate interest in a pool of leases held by a VIE)

• Not considered to be variable interests in the VIE if− Specific assets are less than 50% by fair value− Holder has no other significant variable interests in the VIE as

a whole

• Variability from the specific assets is eliminated from the analysis used to identify the primary beneficiary

37

37

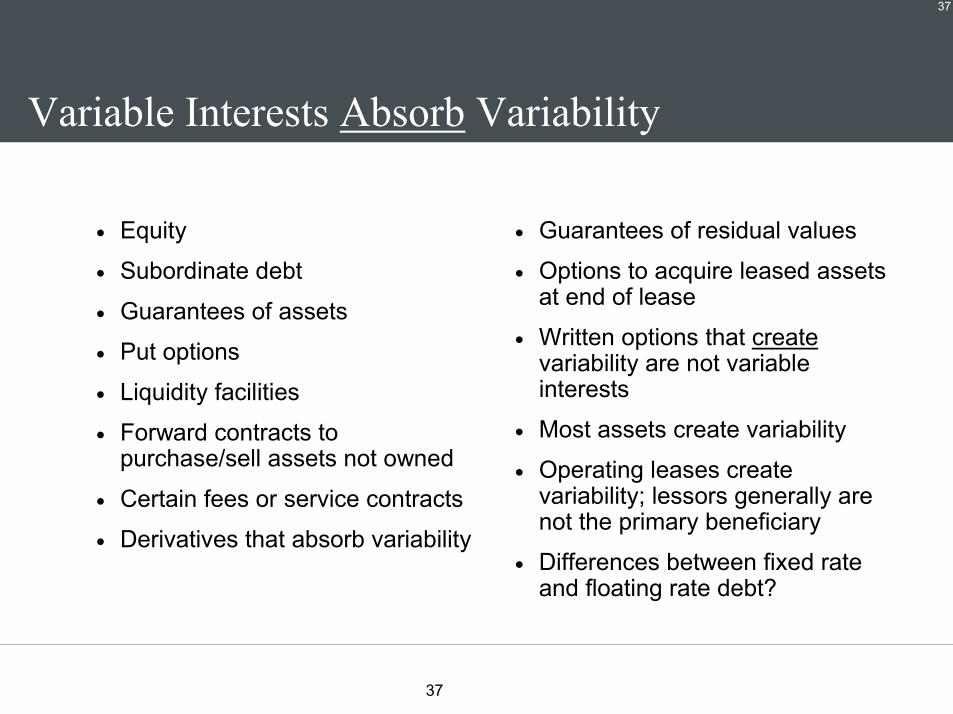

Variable Interests Absorb Variability

• Equity

• Subordinate debt

• Guarantees of assets

• Put options

• Liquidity facilities

• Forward contracts to purchase/sell assets not owned

• Certain fees or service contracts

• Derivatives that absorb variability

• Guarantees of residual values

• Options to acquire leased assets at end of lease

• Written options that createvariability are not variable interests

• Most assets create variability

• Operating leases create variability; lessors generally are not the primary beneficiary

• Differences between fixed rate and floating rate debt?

Current Issues inSecuritization Accounting 2004 ELA Lease Accountants Conference

2

FAS 140

Accounting for Transfers and Servicing of

Financial Assets and Extinguishments of

Liabilities

3

What Is The Conceptual Basis For A Sale Of Financial Assets Under FAS 140?

• The Transferor has SURRENDERED CONTROL of the assets. It should account for its interests in the assets

4

A Sale Of Financial Assets Must MeetALL Three Conditions

• Legal isolation from transferor

• Transferee must be able to pledge or exchange assets(If transferee is a QSPE, the beneficial interest holders must be able to pledge or exchange their beneficial interests)

• Transferor surrenders control of assets

5

Why Is a QSPE Important in Securitization?

• If transferee is not a QSPE, it must be able to pledge or exchange the assets for the transfer to be a sale

• FAS 140 REQUIRES that transferor DOES NOT consolidate a QSPE

• FIN 46 extends non-consolidation to most other parties

6

What Conditions Must a QSPE Meet?

• “Demonstrably distinct” from the transferor

• Limits on permitted activities

• Limits on assets

• Limits on sales of assets

7

FIN 46R

Consolidation of Variable Interest Entities

8

What Is The Conceptual Basis For FIN 46R?

• The party that has a majority of the RISKS AND REWARDS from an entity controls that entity and should be required to consolidate it

9

Summary of FIN 46R

• Primary Beneficiary refers to the party that has a controlling financial interest in a VIE and must consolidate

• Variable Interests are the means through which financial support is provided to an entity and the providers gain or lose

• Qualifying SPEs under FAS 140 are not subject to the Interpretation—both for the transferor and other parties

• Interpretation will affect multi-seller ABCP conduits and CDOs

10

What is a Variable Interest Entity?

• A Variable Interest Entity meets one of the following conditions:− Total equity at risk is not sufficient to permit the entity to finance its

activities without additional subordinated support• Presumed minimum of 10% can be overcome by several methods,

including equity greater than expected losses of the entity− Equity investors as a group lack one of the following characteristics:

• Direct or indirect ability to make decisions that affect the entity’s activities through voting rights (with voting rights proportional to obligation to absorb losses and/or right to receive upside)

• Obligation to absorb the expected losses of the entity if they occur• Right to receive expected residual returns of the entity if they occur

11

Who Is The Primary BeneficiaryAnd Consolidates?

• Primary Beneficiary holds Variable Interests that will absorb a majority of the VIE’s expected losses (the downside) and/or receive a majority of the VIE’s Expected residual returns (the upside)

• If one party has a majority of the downside and another has a majority of the upside, the party with the downside will be required to consolidate

• The ability to make decisions that significantly affect the results of the VIE is a “strong indication” of control

12

Proposed Amendment to

FAS 140

13

FAS 140 Amendment—History

• Emerging Issues Task Force had been considering an issue (Issue No. 02-12) whether a QSPE could have the discretion to set the terms of beneficial interests issued after the inception of the QSPE or whether all terms must be specified in the governingdocuments

• Issue could have affected master trusts and ABCP

• FASB took over project in January− Discretion of QSPE to set the terms of interests issued after inception− Ability of transferor to provide credit enhancement and/or liquidity to

QSPE− Equitable right of redemption issue

14

FAS 140 Amendment—History

• Exposure draft issued in June 2003− Legal isolation from transferor and affiliates− Two-step transfer must involve a QSPE if beneficial interests

are issued− Prohibition on transferor support− Prohibition on transferor derivatives− Limits on QSPEs that reissue beneficial interests− No equity securities

• Exposure draft widely criticized as inconsistent with control basis of FAS 140

• FASB has made decisions that have overturned some of these proposals

15

Subsequent FASB Decisions

• Decisions− Legal isolation from transferor and affiliates− Two-step transfer must involve a QSPE if beneficial interests

are issued− No prohibition on transferor support or transferor derivatives—

as long as consistent with legal isolation− Limits on QSPEs that rollover beneficial interests softened

from prohibition• “Not more than trivial incremental benefit” test (discretion to set

terms; provide credit support; provide liquidity support)− No equity

• Current proposed amendment is far more consistent with the control model of FAS 140 than earlier proposal

16

Subsequent FASB Deliberations

• Additions to project− Fair value accounting of servicing rights− Accounting for beneficial interests

• Retained interests initially measured at fair value not cost• Embedded derivatives will require further guidance

• FASB has been focused on issues relating to legal isolation− Participations− Set-off rights− Expect requirements consistent with legal “true sale”

• Revised exposure draft expected in 1Q 2005 with effectiveness in second half of 2005

17

EITF

Issue No. 03-1

18

EITF Issue No. 03-1

• Not limited to securitization transactions

• FAS 115 provides that changes in market value of AFS securities flow directly to equity (and not net income) unless impairment is other than temporary

− Other than temporary impairments expensed through net income

− Reversal of impairment does not flow through net income

19

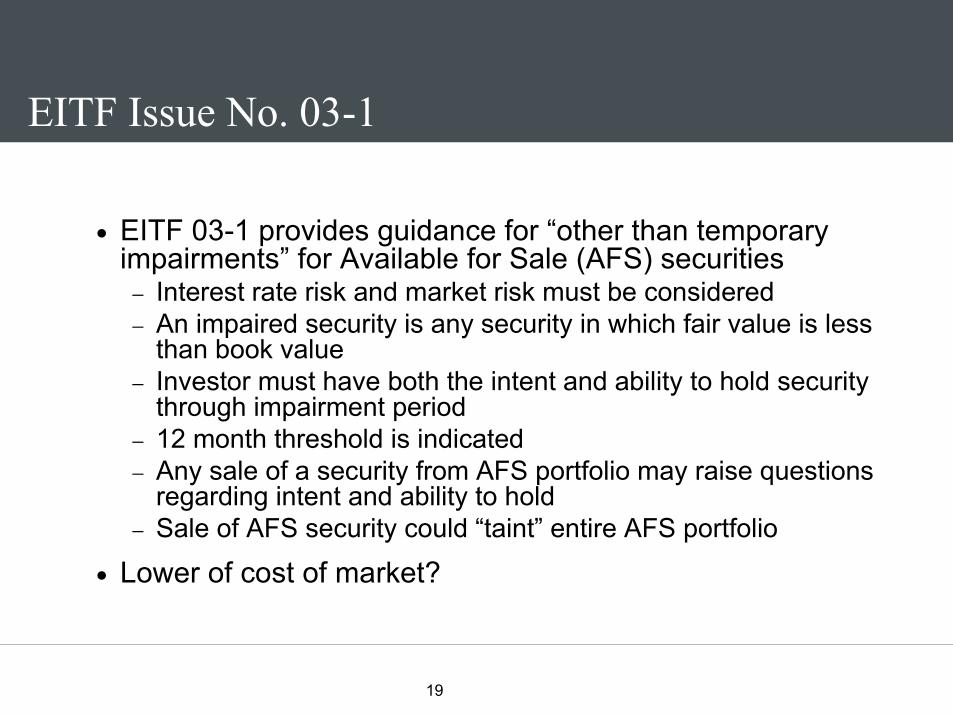

EITF Issue No. 03-1

• EITF 03-1 provides guidance for “other than temporary impairments” for Available for Sale (AFS) securities

− Interest rate risk and market risk must be considered− An impaired security is any security in which fair value is less

than book value− Investor must have both the intent and ability to hold security

through impairment period− 12 month threshold is indicated− Any sale of a security from AFS portfolio may raise questions

regarding intent and ability to hold− Sale of AFS security could “taint” entire AFS portfolio

• Lower of cost of market?

20

EITF

Issue No. 04-7

21

When is a Derivative a Variable Interest?

• FAS 46R indicates that variable interests absorb variability• Is a plain vanilla interest rate swap a variable interest? Does it

absorb or create variability?• Four views presented

− Fair value variability (View A)− Cash flow variability (View B)− Total variability (View C)− Design of the VIE (View D)

• Industry groups have presented other alternative views− Comprehensive economic analysis concludes that plain vanilla

derivatives both create and absorb variability and are not variable interests

22

Current Status

• Initial discussion in June 2004 was inconclusive

• Conclusion that plain vanilla derivatives are not variable interests will enhance ability to implement FIN 46R consistently

23

FIN 46R

GuidanceConsiderations

24

FIN 46R Continuing Issues

• What is a variable interest?− EITF 04-7 will provide guidance on derivatives

• How do you allocate expected losses and expected residual returns among different investors?

• Do general recourse liabilities used to finance assets eliminate silos?

• Many other implementation issues remain.

25

Expected Loss Notes

• Asset-backed commercial paper conduits have issued “expected loss notes” that do not require sponsor to consolidate conduit

− Sized at amount of expected losses, typically less than 0.10% of the assets of the conduit due to high quality of assets

− Yield on ELN is approximately 15% to 20%, but adds little incremental cost due to size

− ELN investor bears losses on assets owned by conduit

• Issues remain− Does exposure of ELN to loss end when asset is removed?− Modeling issues− SEC is discussing structure with at least two banks

• Solution most applicable to VIEs with high quality assets and low losses

26

“Joint Venture” VIE

• “Joint venture” solution relies on narrow definition for “silos”

• Multiple sellers sell assets to VIE− No seller sells 50% or more of the total assets− Assets should be comparable to improve marketability− VIE issues senior notes that are backed by all of the assets− Each seller receives a subordinate interest issued by the VIE that is

backed by only the assets that seller has sold− No seller takes on risk associated with other sellers’ assets− Each seller has a variable interest in only the assets it sold and does

not have a variable interest in the VIE as a whole

• Structure requires partners with similar assets and objectives− Increases complexity