Embed Size (px)

Citation preview

CASH MANAGEMENT CASH MANAGEMENT MODULEMODULEP d bP d bPrepared by:

Finance Division27th May 2010

Prepared by: Finance Division

27th May 201027th May 201027th May 2010

Presentation Contents

• IIUM Financial Policy No. 5: Cash ManagementOverviewO e eCash Management at KCD level

• IIUM Financial Policy No. 9: Treasury MattersOverviewProcedure for Receivables ActivityProcedure for Receivables ActivityFlow Chart for Recording of Collection via ORS Flow Chart for Banking In of CollectionFlow Chart for Banking In of Collection

Presentation Contents

• IIUM Financial Policy No. 4: Petty Cash Management

Petty Cash DisbursementPetty Cash RecoveryPetty Cash RecoveryPetty Cash Procedure (Operating)Petty Cash Procedure (Student)Issues on Petty Cash ManagementIssues on Petty Cash ManagementFlow Chart for Petty Cash Operating

Presentation Contents

• Financial Guideline to Organize Local and International Seminars/Conferences/

Prior to commencement of seminar/conferenceDuring the seminar/conferenceDuring the seminar/conferenceAfter the seminar/conferenceGuideline for Proposal Paper to Organize International Seminar/ConferenceInternational Seminar/Conference

• IIUM Financial Policy: Procedure to Solicit Funds f P blifrom Public

IIUM FINANCIAL POLICY NO. 5: CASH MANAGEMENT

Authority & Empowerment

The Finance Division has decentralized theauthority to collect & deposit cash & otherauthority to collect & deposit cash & othercollections on behalf of the University to the KCDs.

The Finance Division is responsible to record andThe Finance Division is responsible to record andallocate tax exemption, official & temporaryreceipts to the relevant KCDs.

The KCDs need to secure approval from theFinance Director for authority to collect cash &appointment of specific personnel who areappointment of specific personnel who areentrusted to handle cash. (Letter of Authority)

Receipt ManagementCollections will be recorded by receipts issued byFinance Division and kept in custody at the Centre.

Features of manual receipt:1. Printed in sequence number1. Printed in sequence number2. Contain payee’s name and if student, to include

matric number3 Carbon copy/stub clearly written3. Carbon copy/stub clearly written4. Certified by authorized personnel5. Damaged receipts to be retained for verification

The Assistant Director/College Principal/finance staffis responsible for the safekeeping of unused manualis responsible for the safekeeping of unused manualreceipts.

Receipt Management

Any blank manual receipt which is no longer in used must be crossed as “cancelled” with theused must be crossed as cancelled with the original copy and carbon copy properly attached in the receipt book.

The lost of receipts must be reported in writing to the Finance Director.

Cancelled receipts and damaged receipts must be kept for audit trail purposes.p p p

The retention period of financial documents is 7 yearsyears.

Custody & Deposit of Cash CollectionCollection

Amounts less than RM1 000 or one (1) weekAmounts less than RM1,000 or one (1) week collection, whichever is less, are to be banked in into the bank.

Amounts in cash collected less than RM1,000Amounts in cash collected less than RM1,000 and not yet banked in are to be kept in a safe with at least two persons in direct control of the amountsamounts.

Custody & Deposit of Cash Collection

General Rule: Any cash collected at CollectionCentre cannot be used or expended for anyypurpose. (i.e. purchase of stationery items,refreshment, etc.)

Nevertheless, for sponsorships received forapproved KCDs programs the amount receivedapproved KCDs programs, the amount receivedcan be used to finance the program expenditureprovided the collection is banked in first into theb k Th ll ti i t b d d i thbank. The collection is to be recorded in thetrust account of the respective KCDs.

IIUM FINANCIAL POLICY NO. 9: TREASURY MATTERS

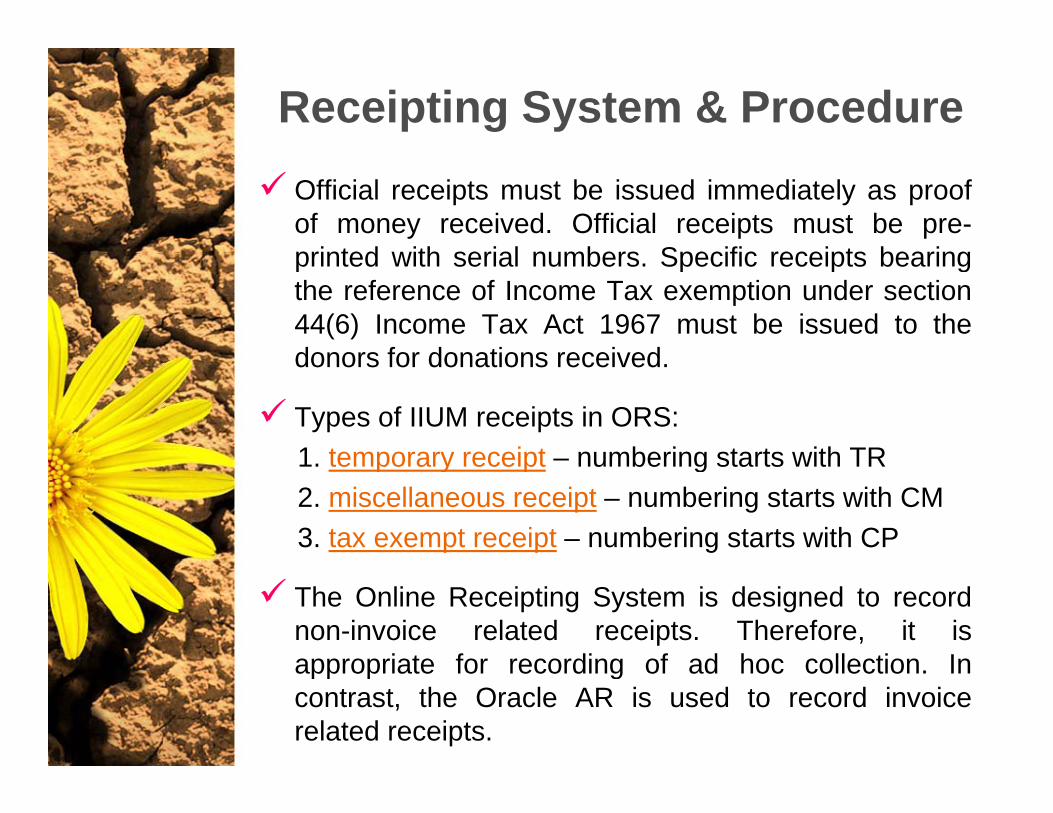

Receipting System & ProcedureOfficial receipts must be issued immediately as proofof money received. Official receipts must be pre-printed with serial numbers Specific receipts bearingprinted with serial numbers. Specific receipts bearingthe reference of Income Tax exemption under section44(6) Income Tax Act 1967 must be issued to thedonors for donations receiveddonors for donations received.

Types of IIUM receipts in ORS:1 temporary receipt numbering starts with TR1. temporary receipt – numbering starts with TR2. miscellaneous receipt – numbering starts with CM3. tax exempt receipt – numbering starts with CP

The Online Receipting System is designed to recordnon-invoice related receipts. Therefore, it isappropriate for recording of ad hoc collection Inappropriate for recording of ad hoc collection. Incontrast, the Oracle AR is used to record invoicerelated receipts.

Receipting System & ProcedureTh t i t (TR) t d i O liThe temporary receipt (TR) created via OnlineReceipting System (ORS) is issued for cash collectionamount less than RM50. The TR will be aggregated

d t d i t i ll i t (CM) t thand converted into miscellaneous receipt (CM) at theend of the day.

The miscellaneous receipt (CM) is used to record forThe miscellaneous receipt (CM) is used to record forany amount of collection.

The tax exempt receipt (CP) is issued to donors fordonations received for approved University programs.

The use of manual receipts are permitted in certaincircumstances as follows:circumstances as follows:a) After office hour collection (office closure) or;b) Collection for programs organized at locations where

accessibility to ORS is unavailable. (i.e. sportactivities at field area)

Receipting System & Procedure

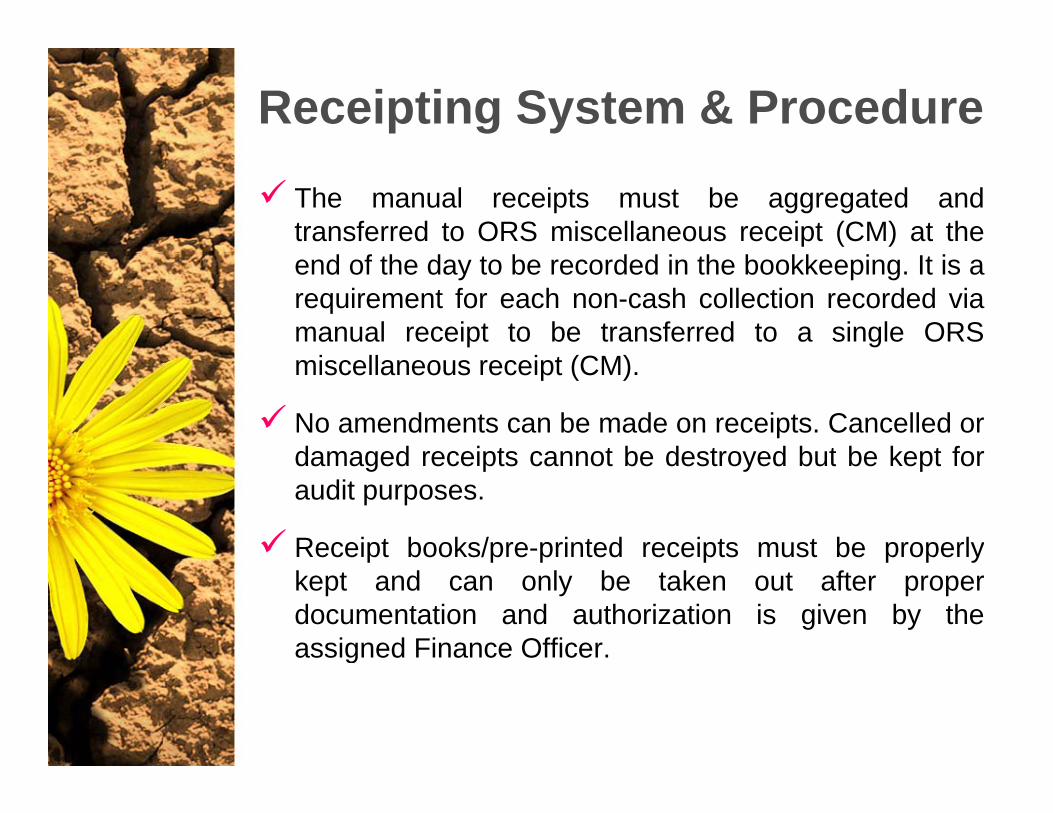

The manual receipts must be aggregated andtransferred to ORS miscellaneous receipt (CM) at theend of the day to be recorded in the bookkeeping. It is arequirement for each non-cash collection recorded viamanual receipt to be transferred to a single ORS

i ll i (CM)miscellaneous receipt (CM).

No amendments can be made on receipts. Cancelled ordamaged receipts cannot be destroyed but be kept fordamaged receipts cannot be destroyed but be kept foraudit purposes.

Receipt books/pre-printed receipts must be properlyp p p p p p ykept and can only be taken out after properdocumentation and authorization is given by theassigned Finance Officer.g

Receipting System & Procedure

Receipts must be signed by the Finance Director orany other authorized officer but not by the officer whoany other authorized officer, but not by the officer whois preparing the receipts.

The Treasury Instruction No. 70(a)(i) provides anexemption to the above policy in the event the officialreceipts are issued by using an electronic receiptingsystem. [TI 70(a)(i)]

A register detailing the recipient’s name, amount anddate received and cheque / document number mustdate received and cheque / document number mustbe recorded and the total amount must be reconciledwith collections at the end of the day.(Receipt Total Collection Report) (ORS Receipt Excel) (ORS Manual pg 3 9)(Receipt Total Collection Report) (ORS Receipt -Excel) (ORS Manual pg 3-9)

Banking In Procedure

All cash collections for the day must be credited tothe bank within three (3) working days if the( ) g ycollections have reached RM1,000.

All receipts through cheques (non-cash collection)must be credited to the bank within a week from thedate of their receipts.

Bank in slips must be retained and checked againstbank account number, bank stamping and cashbook.

There is a requirement to segregate the bank inslips for cash collection and non-cash collection.

Banking In ProcedureThe standard clearance period for bankers draft &telegraphic transfer in foreign currency are asf llfollows:

a) Bankers draft: 5 - 7 weeks. Similar to normalh b t i diff t tcheque but in different monetary currency.

b) Telegraphic transfer: 1-2 weeks. Require anintercept bank in Malaysia such as Citibank,Maybank, etc.

All cheques must be crossed upon receipt. Receiptsf f f ffor foreign currency received in the form of bankersdraft/ cheque/ telegraphic transfer can only bereflected in the system upon clearance by localbank and the exact amount in Malaysian Ringgit(MYR) is known.

Safekeeping of Collection

Cash collections below RM1,000 should bestored at the safe/strong room. Keys and lockg ycombination number must be known only byauthorized officers.

Any monies received that have yet to be sent tothe bank cannot be used for any purposes andy p pno officer/staff is allowed to borrow, advanceor change the money received on behalf of theUniversityUniversity.

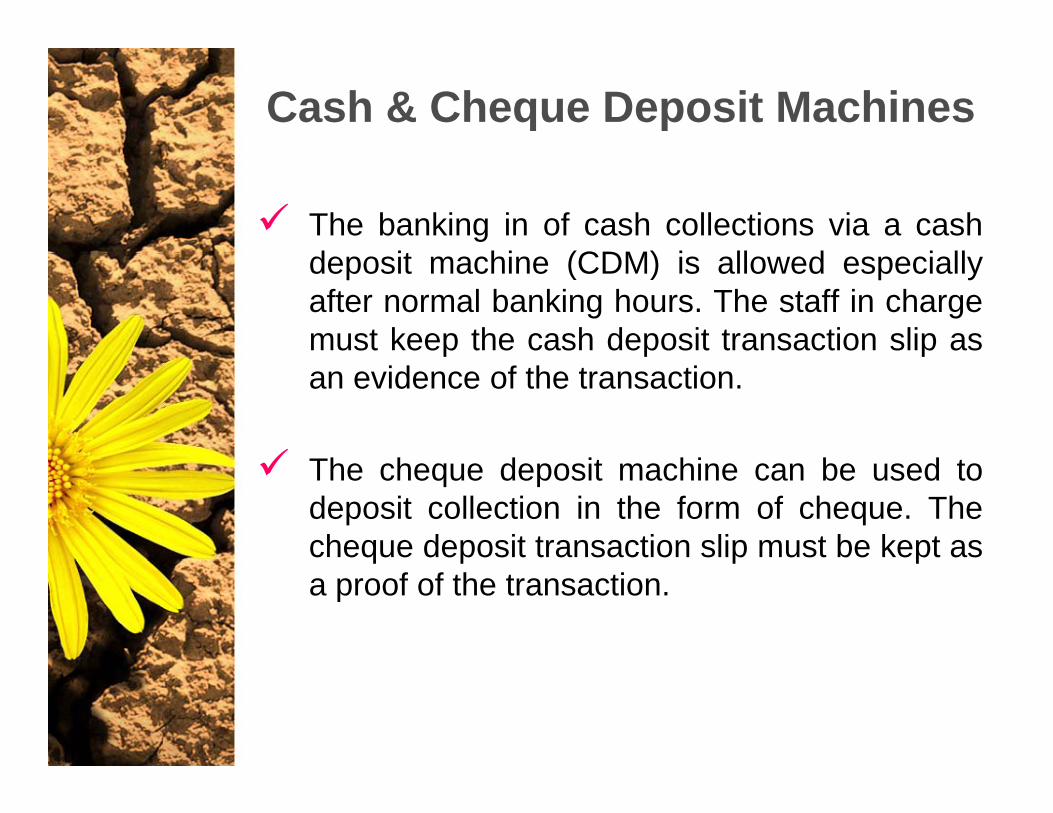

Cash & Cheque Deposit Machines

The banking in of cash collections via a cashd it hi (CDM) i ll d i lldeposit machine (CDM) is allowed especiallyafter normal banking hours. The staff in chargemust keep the cash deposit transaction slip asp p pan evidence of the transaction.

Th h d i hi b dThe cheque deposit machine can be used todeposit collection in the form of cheque. Thecheque deposit transaction slip must be kept asq p p pa proof of the transaction.

Others

All receipts must be properly recorded to theAll receipts must be properly recorded to theappropriate account codes.

Any receipts in the form of assets must obtainclearance from the Rector.

FLOW CHART FOR RECORDING OF COLLECTION VIA ONLINEOF COLLECTION VIA ONLINE RECEIPTING SYSTEM (ORS)

Flowchart for ORS Temporary Receipt Collection pdfCollection.pdf

Flowchart for ORS Misc Collection.pdf

Procedures for Banking In of Collectionof Collection

USE ONE BANK IN SLIPFOR ONE RECEIPT

Especially for non-cashcollectionFOR ONE RECEIPT collection

As for cash collection, multiple receipts can

be incorporatedin one bank in slip

Write at reverse side of chequethe KCD’s name

p

Banking in of collections into the bank

Procedures for Banking In of Collectionof Collection

Print the Receipt Total Collection Report (Misc. [CM] &

Tax Exempt [CP]) via ORS

The authorized officer needs to check and verify the printed

report on a daily basis to ensure data accuracy and

adherence to policy

Submit the report to Finance Division

bi kl b ion a bi-weekly basis

IIUM FINANCIAL POLICY NO 4: PETTY CASHNO. 4: PETTY CASH

MANAGEMENT

Petty Cash DisbursementPetty Cash DisbursementPetty Cash Limits:1) Operating expenses - cash reimbursement

up to RM500.00(minimum petty cash float is RM1 000)(minimum petty cash float is RM1,000)

2) Student expenses - cash reimbursement upto RM500.00(student petty cash float is RM2,000)

Payments are made for valid official usePayments are made for valid official use,employees making petty cash expendituresshall obtain sales receipt whenever possible.Th H d f D t t h ld if thThe Head of Department should verify thereceipt prior to disbursement.

Petty Cash DisbursementItems not receipted will be accounted for viacompletion of a “Petty Cash Voucher/Form”,signed by the employee receiving the money assigned by the employee receiving the money asreimbursement. In addition, the staff member isalso required to obtain a written verification fromH d f D t t th i dHead of Department or an authorizedrepresentative on the claim.

Th P tt C h I t F d (fl t) i t tThe Petty Cash Imprests Fund (float) is set up tocontrol cash disbursement.

Whenever cash is withdrawn the cash receipt orWhenever cash is withdrawn, the cash receipt orthe voucher must be placed in the fund.

The Authority for on Petty Cash Imprest is theThe Authority for on Petty Cash Imprest is theFinance Director.

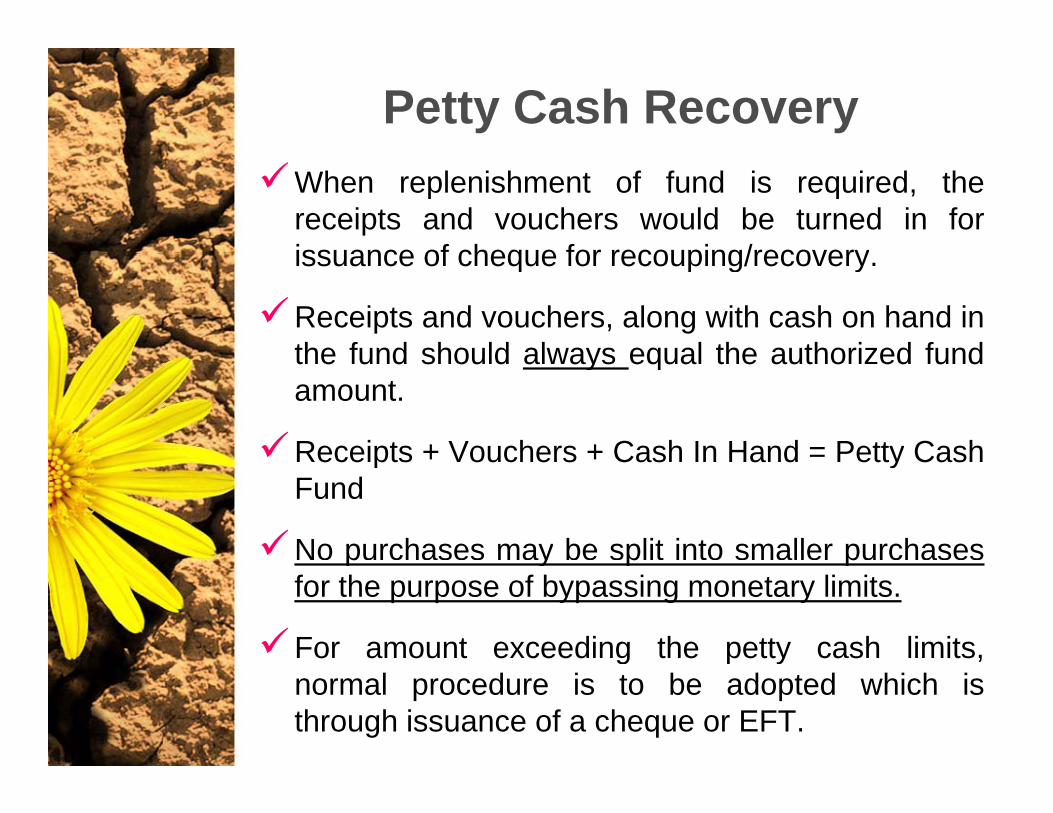

Petty Cash RecoveryWhen replenishment of fund is required, thereceipts and vouchers would be turned in forissuance of cheque for recouping/recoveryissuance of cheque for recouping/recovery.

Receipts and vouchers, along with cash on hand inthe fund should always equal the authorized fundthe fund should always equal the authorized fundamount.

Receipts + Vouchers + Cash In Hand = Petty CashReceipts + Vouchers + Cash In Hand Petty CashFund

No purchases may be split into smaller purchasesp y p pfor the purpose of bypassing monetary limits.

For amount exceeding the petty cash limits,g p ynormal procedure is to be adopted which isthrough issuance of a cheque or EFT.

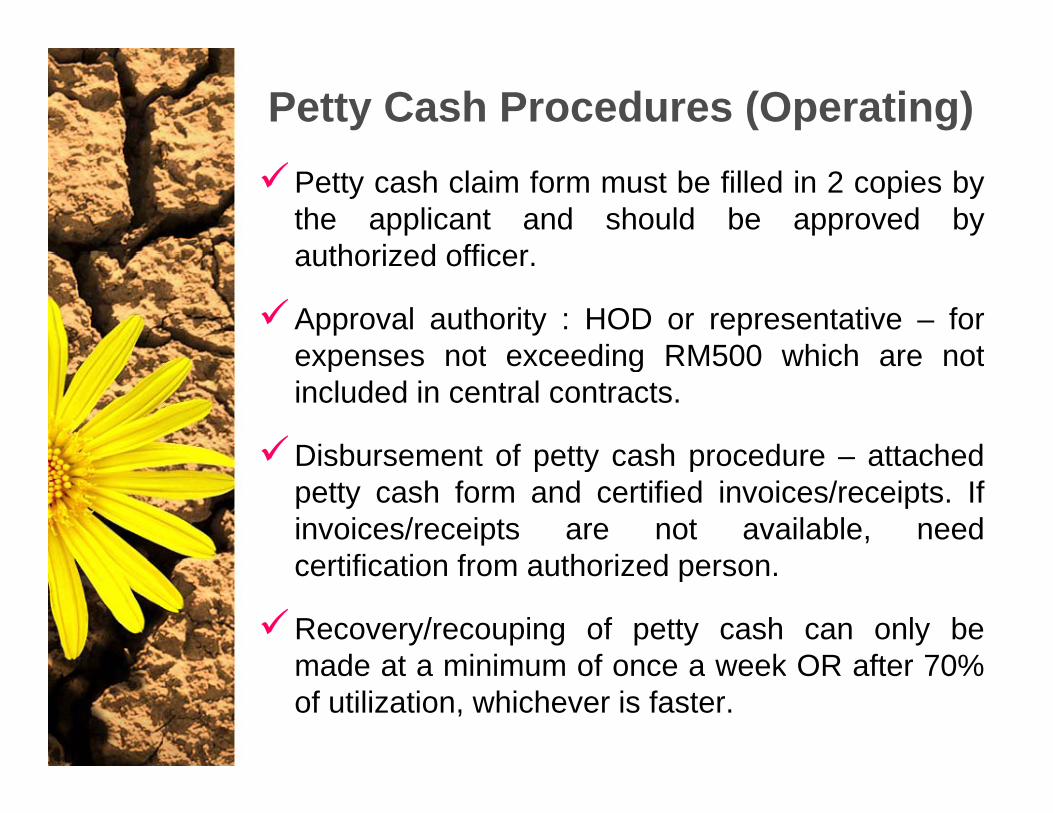

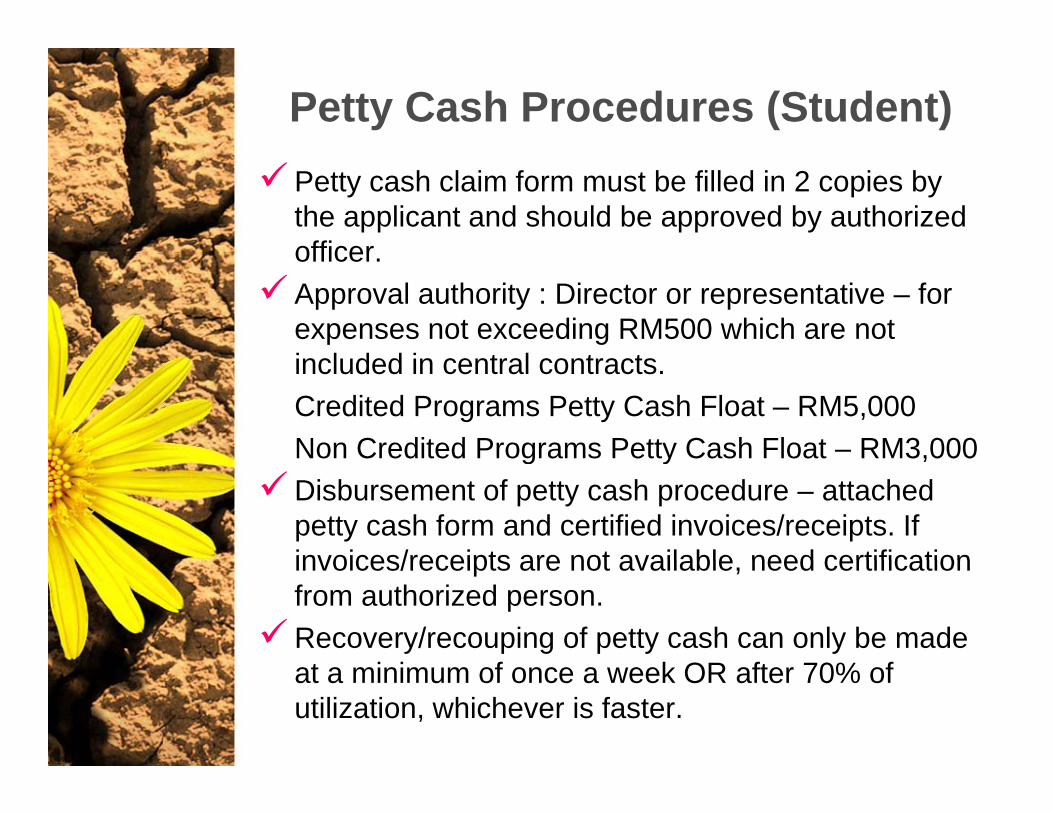

Petty Cash Procedures (Operating)Petty cash claim form must be filled in 2 copies bythe applicant and should be approved byauthorized officerauthorized officer.

Approval authority : HOD or representative – forexpenses not exceeding RM500 which are notexpenses not exceeding RM500 which are notincluded in central contracts.

Disbursement of petty cash procedure – attachedDisbursement of petty cash procedure – attachedpetty cash form and certified invoices/receipts. Ifinvoices/receipts are not available, needcertification from authorized personcertification from authorized person.

Recovery/recouping of petty cash can only bemade at a minimum of once a week OR after 70%made at a minimum of once a week OR after 70%of utilization, whichever is faster.

Petty Cash Procedures (Student)Petty cash claim form must be filled in 2 copies by the applicant and should be approved by authorized officerofficer.Approval authority : Director or representative – for expenses not exceeding RM500 which are not i l d d i t l t tincluded in central contracts.Credited Programs Petty Cash Float – RM5,000Non Credited Programs Petty Cash Float – RM3,000Non Credited Programs Petty Cash Float RM3,000Disbursement of petty cash procedure – attached petty cash form and certified invoices/receipts. If invoices/receipts are not available need certificationinvoices/receipts are not available, need certification from authorized person.Recovery/recouping of petty cash can only be made t i i f k OR ft 70% fat a minimum of once a week OR after 70% of

utilization, whichever is faster.

Petty Cash Management IssuesTHE USE OF PETTY CASH FUND FOR DISAPPROVED TYPES OF DISBURSEMENT

A d t f t dAs an advancement for programs to speedup purchasing activitiesPotential problems arising from suchp gpractice:

The available total petty cash fund will nottally with the petty cash fund balance intally with the petty cash fund balance inbookkeeping until reinstatement of fund ismade upon clearance of advancementhcheque.

A minimum or no movement of petty cashfund is recorded for the period.p

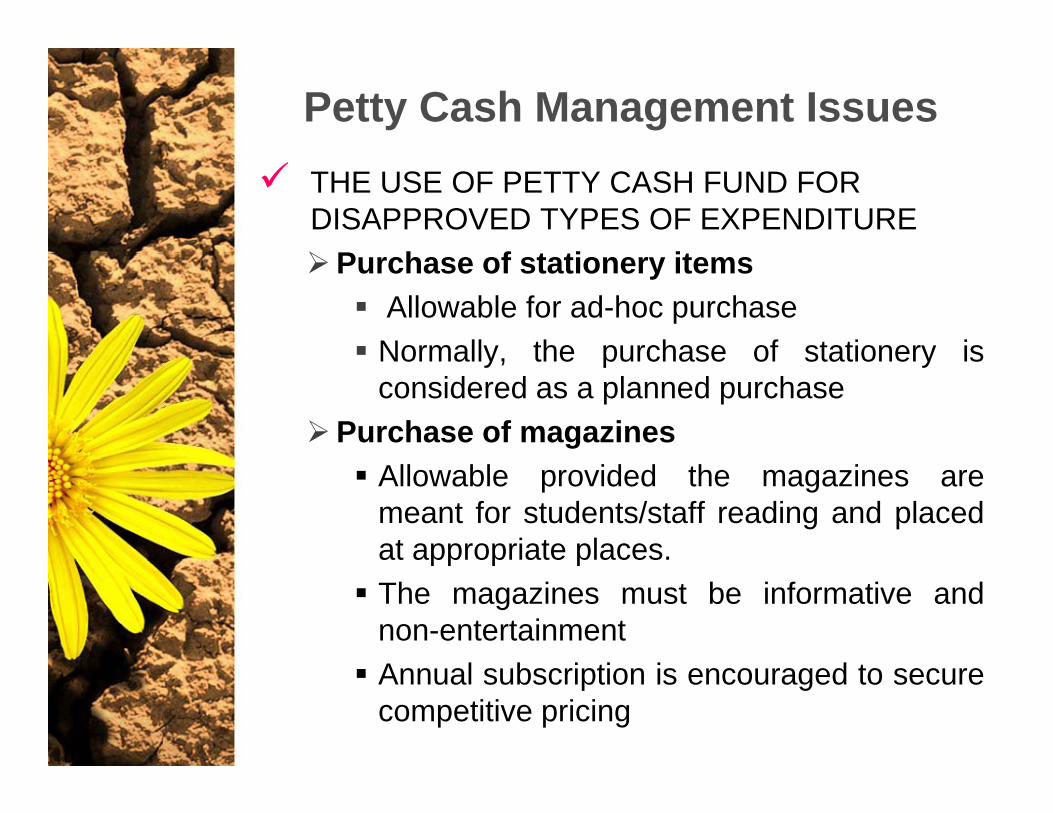

Petty Cash Management IssuesTHE USE OF PETTY CASH FUND FOR DISAPPROVED TYPES OF EXPENDITURE

P h f t ti itPurchase of stationery itemsAllowable for ad-hoc purchaseNormally the purchase of stationery isNormally, the purchase of stationery isconsidered as a planned purchase

Purchase of magazinesAllowable provided the magazines aremeant for students/staff reading and placedat appropriate places.pp p pThe magazines must be informative andnon-entertainmentA l b i i i dAnnual subscription is encouraged to securecompetitive pricing

FLOW CHART FOR OPERATING PETTY CASH

Vi i O P tt C h 1 3 dfVisio-Op_Petty_Cash_1-3.pdfVisio-Op_Petty_Cash_2-3.pdfVisio-Op_Petty_Cash_3-3.pdf

Petty Cash Report pdfPetty Cash Report.pdf

FINANCIAL GUIDELINE TOFINANCIAL GUIDELINE TO ORGANIZE LOCAL AND

INTERNATIONALINTERNATIONAL SEMINARS/CONFERENCES

GUIDELINE:GUIDELINE:TO ORGANIZE LOCAL AND

INTERNATIONALINTERNATIONAL SEMINARS/CONFERENCES

FLOW CHART:PROCEDURE TO ORGANIZE LOCALPROCEDURE TO ORGANIZE LOCAL

AND INTERNATIONAL SEMINARS/CONFERENCESSEMINARS/CONFERENCES

GUIDELINE FOR PROPOSAL PAPER TOGUIDELINE FOR PROPOSAL PAPER TO ORGANIZE INTERNATIONAL

SEMINAR/CONFERENCE/SEMINAR/CONFERENCE/WORKSHOP/FORUM FOR APPROVAL OF

MINISTER OF HIGHER EDUCATION

PEKELILING PERBENDAHARAANPEKELILING PERBENDAHARAAN BIL. 3 TAHUN 2003:

BAYARAN SAGUHATI PERSIDANGANBAYARAN SAGUHATI PERSIDANGAN

IIUM FINANCIAL POLICY: PROCEDURE TO SOLICITPROCEDURE TO SOLICIT

FUNDS FROM PUBLIC

Solicit of Funds From PublicPOLICY STATEMENT

It is always the intention of the University tod fi d ti itiencourage and finance programs and activities

organized by staff and students regardless whetherthey are conducted internally or externally providedth ti iti h d l f ththese activities have secured approval from therelevant University’s authorities prior to theirimplementation.

Some of the programs and activities would requirean additional fund in addition to the fund allocated byth U i it U d l i t ththe University. Under normal circumstances, theadditional fund is obtainable in the form of monetaryand in kind from outside parties such as individuals,

i t d bli t d th i tiprivate and public sectors and other organizations.

Solicit of Funds From Public

Nevertheless, the soliciting of fund andseeking of sponsorship activities from theg p ppublic have certain underlying procedures thatneed to be strictly adhered to prior to theirexecution to prevent any intention of obtainingexecution to prevent any intention of obtaining“personal“personal gain”gain” from the activities.

The solicitation letters of funds andsponsorships for different approved programsand activities must be authorized by theand activities must be authorized by thefollowing signatories:

Solicit of Funds From Public

No. Program Organizer Solicitation Letter’s Signatories

1. University Deputy Rectors & Rector

2. Faculty/Department/Division

Dean/DirectorDivision

3. Student Societies-under Deputy Rector (Student STAD Office Affairs) & respective

Directors

4 Student Societies under Dean/Director4. Student Societies-under Faculty/Department

Dean/Director

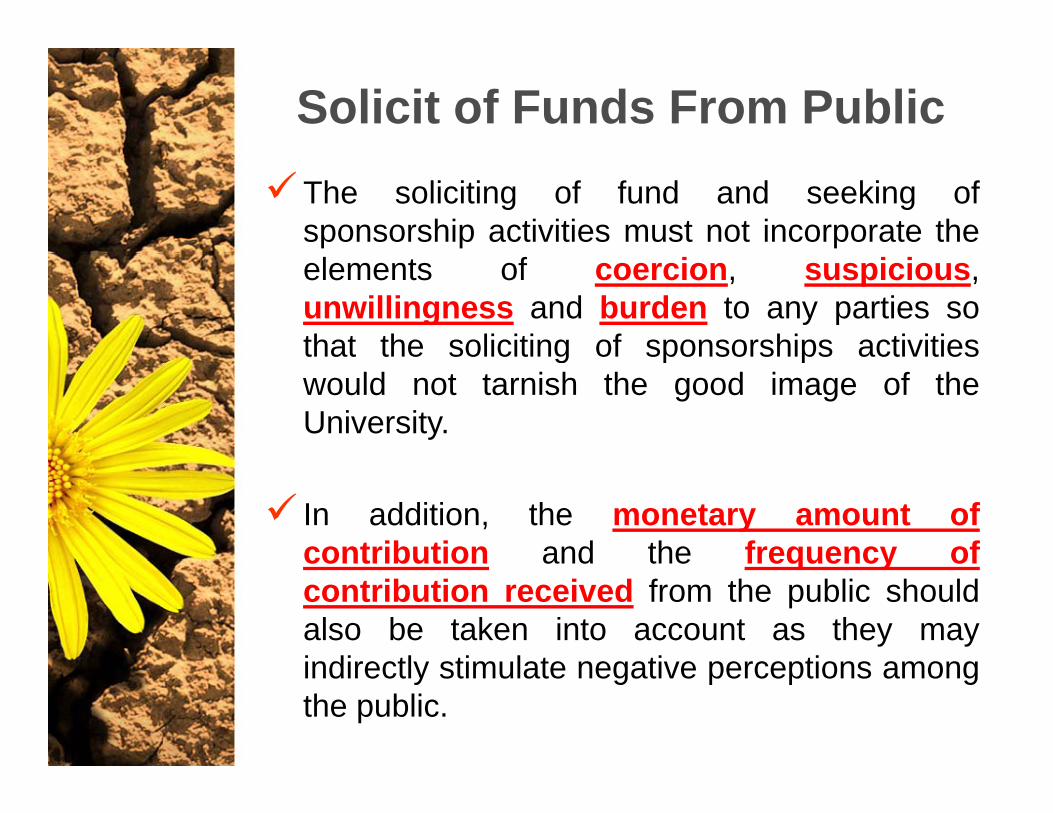

Solicit of Funds From PublicThe soliciting of fund and seeking ofsponsorship activities must not incorporate theelements of coercion, suspicious,unwillingness and burden to any parties sothat the soliciting of sponsorships activitiesthat the soliciting of sponsorships activitieswould not tarnish the good image of theUniversity.

In addition, the monetary amount ofcontribution and the frequency ofcontribution and the frequency ofcontribution received from the public shouldalso be taken into account as they mayindirectly stimulate negative perceptions amongindirectly stimulate negative perceptions amongthe public.

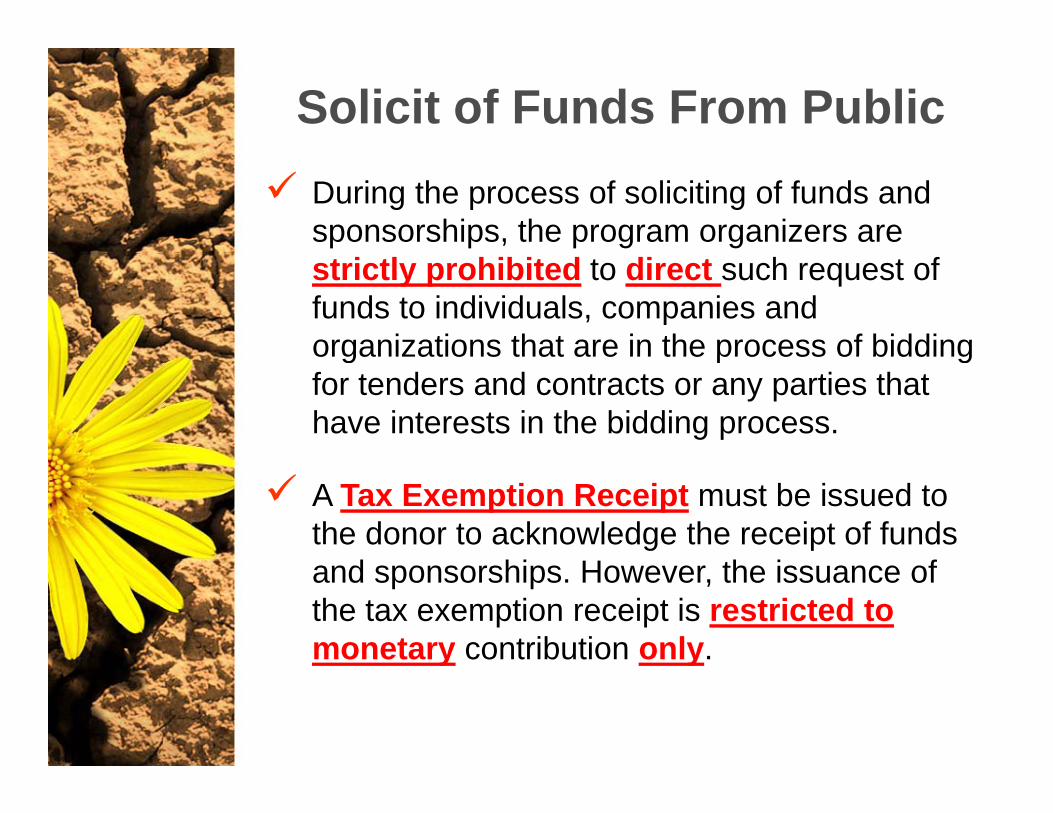

Solicit of Funds From PublicDuring the process of soliciting of funds and sponsorships, the program organizers are strictly prohibited to direct such request of funds to individuals, companies and organizations that are in the process of biddingorganizations that are in the process of bidding for tenders and contracts or any parties that have interests in the bidding process.

A Tax Exemption Receipt must be issued to the donor to acknowledge the receipt of funds

d hi H th i fand sponsorships. However, the issuance of the tax exemption receipt is restricted to monetary contribution only. y y

Solicit of Funds From Public

All donations and sponsorships forUniversity’s approved programs andUniversity s approved programs andactivities must be in the form of crossedcheque/banker’s draft/postal order/moneyorder made payable to “Finance DirectorInternational Islamic University Malaysia”in which thereafter will be deposited into thein which thereafter will be deposited into theUniversity’s bank account. The amountreceived will be recorded in the cost centrestrust accounts.

Solicit of Funds From PublicThe donations and sponsorships received mustbe utilized solelysolely for the approved programs andactivities and it is the responsibility of theactivities and it is the responsibility of therespective cost centres to prepare a properbookkeeping for the purpose of keeping track ofcash inflow and cash outflow of the trustcash inflow and cash outflow of the trustaccounts.

In order to secure the good “Islamic” image of theUniversity, the soliciting of fund and seeking ofsponsorship activities mustmust notnot be channeled top pcontroversial companies and organizations suchas those that are involved in forbidden activitiessuch as gambling and liquor industries.such as gambling and liquor industries.

Further Interpretations of PolicyThe policy extraction: “During the process ofsoliciting of funds and sponsorships, theprogram organizers are strictly prohibited toprogram organizers are strictly prohibited todirect such request of funds to individuals,companies and organizations that are in the

f fprocess of bidding for tenders and contractsor any parties that have interests in the biddingprocess”

The policy did not mention specifically if thecompany is bidding in a quotation exercisecompany is bidding in a quotation exercise.Nevertheless, the interpretation of the policycovers overall acquisition bidding process ofthe University.

Further Interpretations of PolicyIn the event that the request of fund has beenforwarded to the company earlier prior to itsinvolvement in the bidding process at the KCDs;involvement in the bidding process at the KCDs;

AND the person who is requesting for theAND the person who is requesting for thesponsorship is one of the members of technicalteam of tender/contract/quotation evaluation;

THEREFORE, the person must be cognizant ofthe fact that he or she should willinglyWITHDRAW from the evaluation team.

Any Questions ?

![Fax Reference Guide - Xeroxdownload.support.xerox.com/pub/docs/WCM24/userdocs/... · Fax Reference Guide ... Enter recipient’s Fax No. Memory :100% [ Fax No. ] Transmitting documents](https://img.pdfslide.us/doc/110x75/5e832a3407bd17145979ab9c/fax-reference-guide-fax-reference-guide-enter-recipientas-fax-no-memory.jpg)