Embed Size (px)

Citation preview

PAXIS JOINT WORKSHOP - Salamanca, June 2005

The attitude and thepotentiality of VC in Italian small firms: a comparison of a traditional anda new sector

Ugo FratesiPolitecnico di Milano and University of Pavia

andVittorio ModenaThe University of Pavia

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

Objectives of the workTo compare a new and a traditional

sector on: Knowledge and attitudes towards VC

investment Potentiality of VC to induce growth

Case study: ItalySmall and medium enterprises

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

Traditional sector: automotiveCapital intensityMass customization and “Lean

production” method Production is pulled by demand (just in time) Production is a continuous flow Production localised close to the final markets

Economies of scale at network levelShrinking but long life-cycle of products

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

Traditional sector: automotive (2)

Outsourcing and global sourcingFirst tier manufacturers (OEM) are also

multinationalsStricter ties with suppliers Importance of co-locationHigh costs of R&DSMEs tend to be low tier suppliers

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

New sector: softwareClassified as servicesNot all software is sold in the market Immaterial imputs and outputs “Experience good”Role of knowledge (external and internal)Role of R&D “craft” activity

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

New sector: software (2) Reproducible products 2 types of firms:

1. Software producersHigh fixed costs, low marginal costs

2. Software servicesLower fixed costs, higher marginal

costs

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

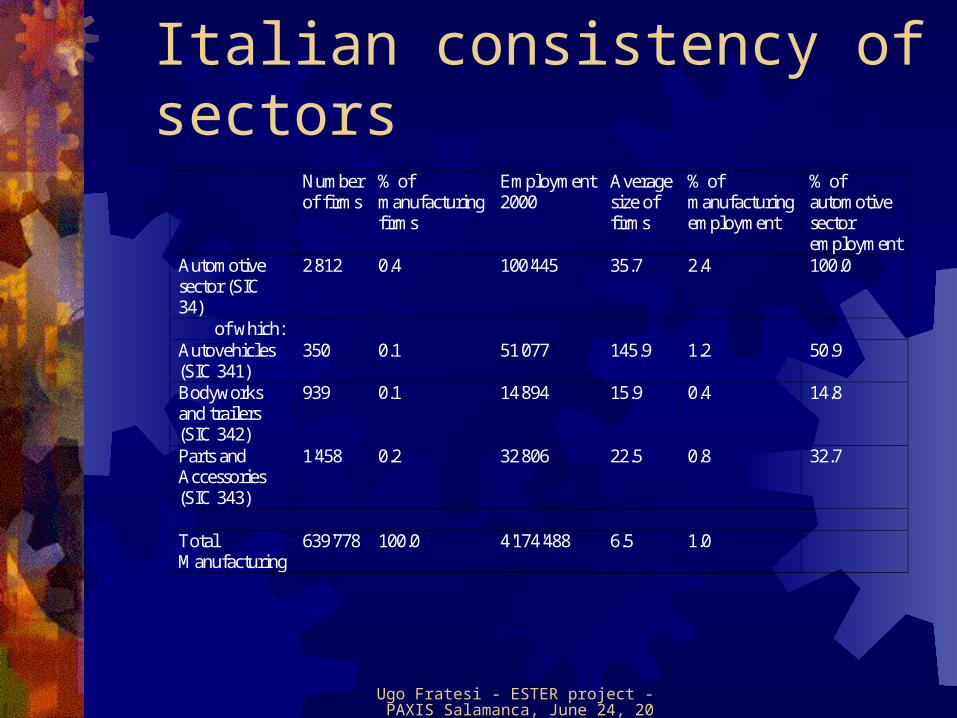

Italian consistency of sectors Number

of firms % of manufacturing firms

Employment 2000

Average size of firms

% of manufacturing employment

% of automotive sector employment

Automotive sector (SIC 34)

2'812 0.4 100'445 35.7 2.4 100.0

of which: Autovehicles (SIC 341)

350 0.1 51'077 145.9 1.2 50.9

Bodyworks and trailers (SIC 342)

939 0.1 14'894 15.9 0.4 14.8

Parts and Accessories (SIC 343)

1'458 0.2 32'806 22.5 0.8 32.7

Total Manufacturing

639'778 100.0 4'174'488 6.5 1.0

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

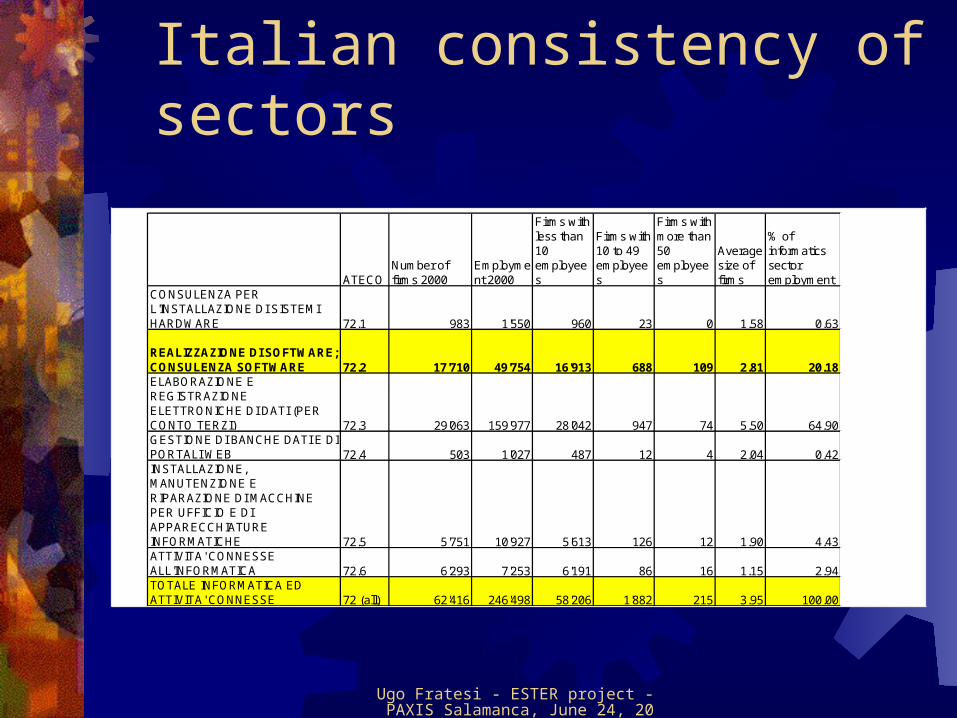

Italian consistency of sectors

ATECONumber of firms 2000

Employment 2000

Firms with less than 10 employees

Firms with 10 to 49 employees

Firms with more than 50 employees

Average size of firms

% of informatics sector employment

CONSULENZA PER L'INSTALLAZIONE DI SISTEMI HARDWARE 72.1 983 1'550 960 23 0 1.58 0.63

REALIZZAZIONE DI SOFTWARE; CONSULENZA SOFTWARE 72.2 17'710 49'754 16'913 688 109 2.81 20.18ELABORAZIONE E REGISTRAZIONE ELETTRONICHE DI DATI (PER CONTO TERZI) 72.3 29'063 159'977 28'042 947 74 5.50 64.90GESTIONE DI BANCHE DATI E DI PORTALI WEB 72.4 503 1'027 487 12 4 2.04 0.42INSTALLAZIONE, MANUTENZIONE E RIPARAZIONE DI MACCHINE PER UFFICIO E DI APPARECCHIATURE INFORMATICHE 72.5 5'751 10'927 5'613 126 12 1.90 4.43ATTIVITA' CONNESSE ALL'INFORMATICA 72.6 6'293 7'253 6'191 86 16 1.15 2.94TOTALE INFORMATICA ED ATTIVITA' CONNESSE 72 (all) 62'416 246'498 58'206 1'882 215 3.95 100.00

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

Geographic location (automotive)

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

Geographic location (software)

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

MethodologyFace to face interviews:

Semi-structured questionnaire involving 6 topics: General data, economic activity, growth,

innovativeness, financial aspects, attitude towards VC

Interviews with informed persons

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

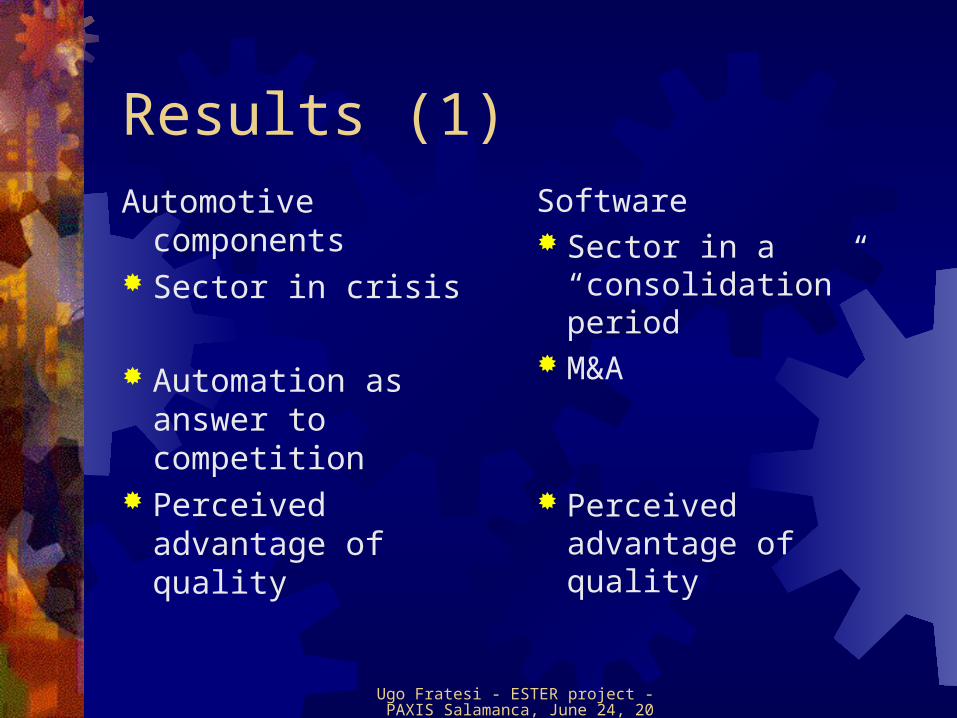

Results (1)

Automotive components

Sector in crisis

Automation as answer to competition

Perceived advantage of quality

Software Sector in a

“consolidation” period M&A

Perceived advantage of quality

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

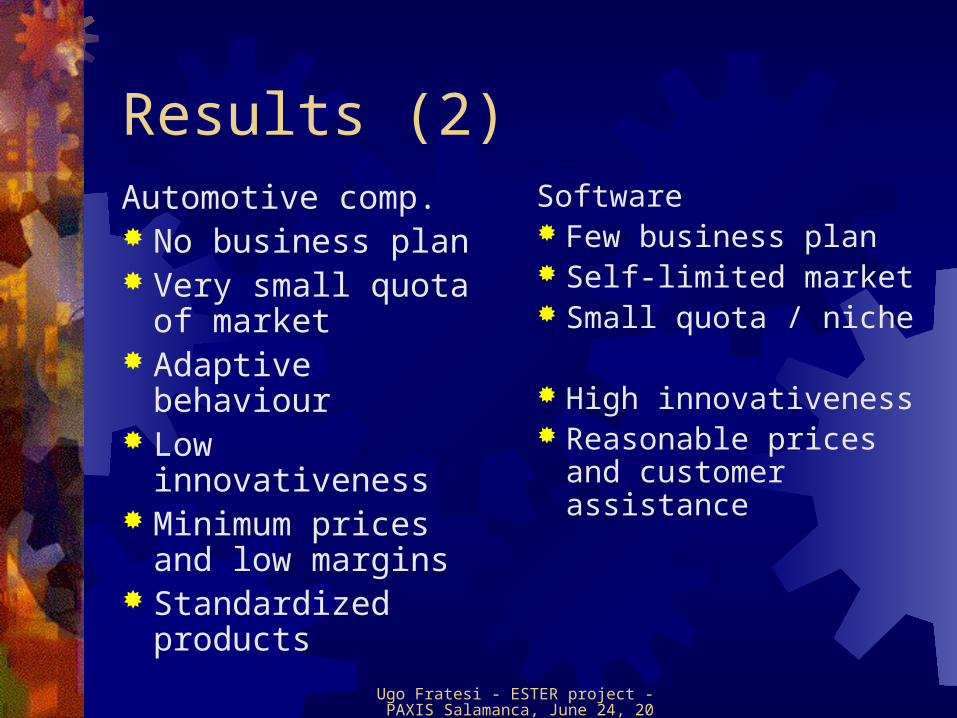

Results (2)Automotive comp. No business plan Very small quota of

market Adaptive behaviour Low innovativeness Minimum prices and

low margins Standardized

products

Software Few business plan Self-limited market Small quota / niche

High innovativeness Reasonable prices

and customer assistance

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

Results (3) Financing

Automotive comp. Negative attitude

towards banks Self-financing Incremental

investment

Software Negative attitude

towards banks Self-financing Low initial invesment Higher needed

investment above a ceiling

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

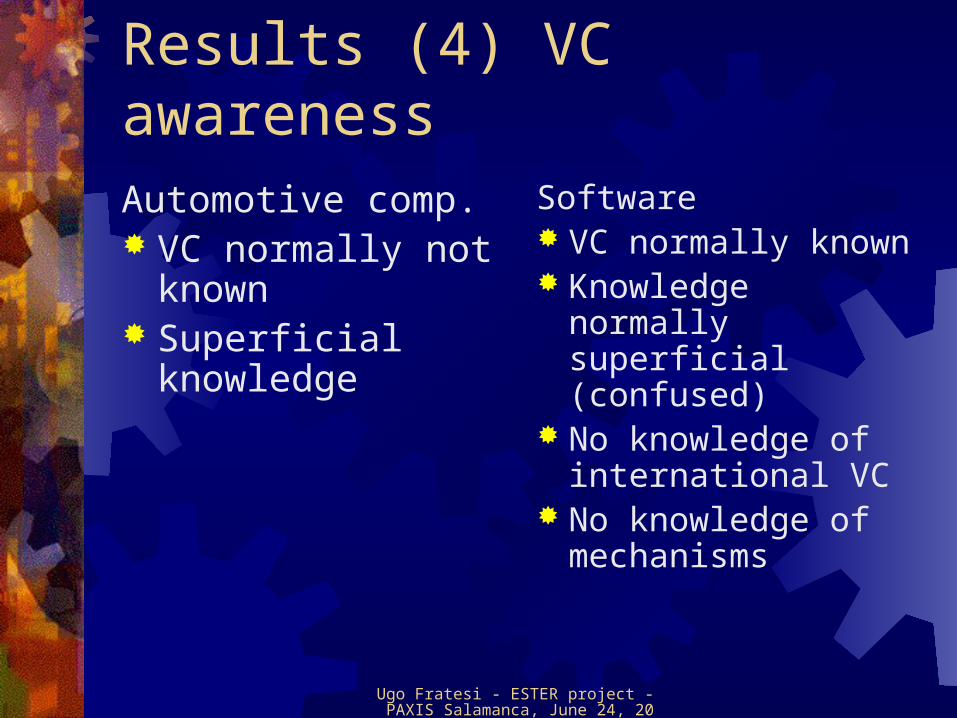

Results (4) VC awarenessAutomotive comp. VC normally not

known Superficial

knowledge

Software VC normally known Knowledge normally

superficial (confused)

No knowledge of international VC

No knowledge of mechanisms

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

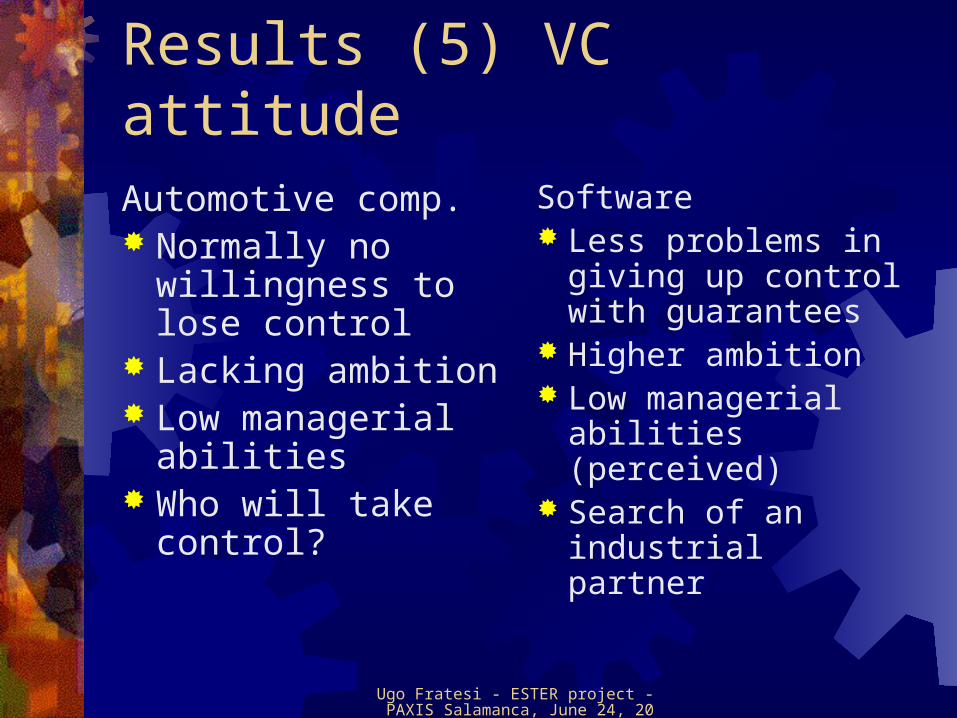

Results (5) VC attitudeAutomotive comp. Normally no

willingness to lose control

Lacking ambition Low managerial

abilities Who will take

control?

Software Less problems in

giving up control with guarantees

Higher ambition Low managerial

abilities (perceived) Search of an

industrial partner

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

Results (6) VC potentiality

Automotive comp.

LOW Market is

conservative Price concurrence

already very high Difficult for SMEs to

introduce innovations

Sotware

MEDIUM Market is (less)

conservative Quality difficult to

detect Difficult to reach the

markets even with new and better products

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

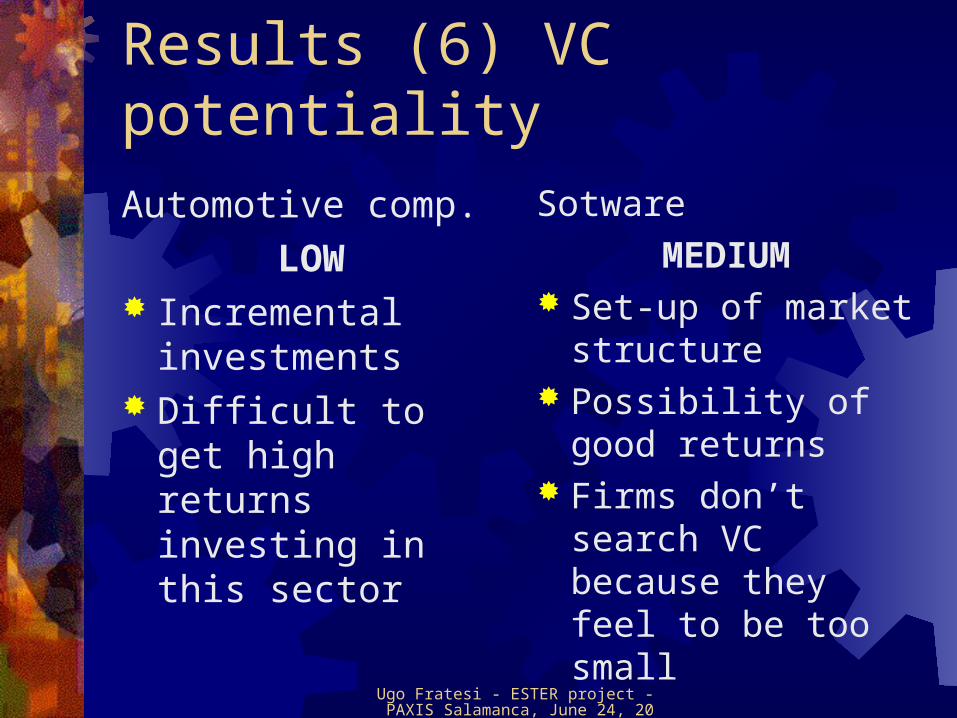

Results (6) VC potentiality

Automotive comp.

LOW Incremental

investments Difficult to get high

returns investing in this sector

Sotware

MEDIUM Set-up of market

structure Possibility of good

returns Firms don’t search

VC because they feel to be too small

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

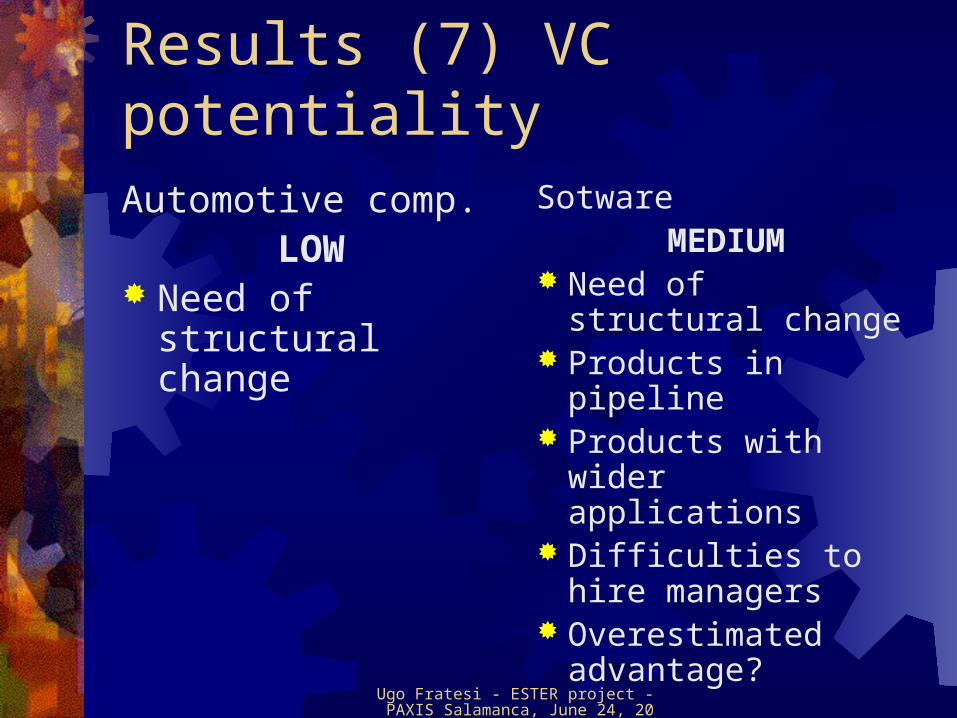

Results (7) VC potentialityAutomotive comp.

LOW Need of structural

change

SotwareMEDIUM

Need of structural change

Products in pipeline Products with wider

applications Difficulties to hire

managers Overestimated

advantage?

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

ConclusionsMore and better information is needed

both in traditional and new sectorsNeed of “learning” mechanisms?Lack of investments in the range

200,000 to 800,000 EuroVC alone not enough: need to assist

firms/entrepreneurs with managerial expertise

Ugo Fratesi - ESTER project - PAXIS Salamanca, June 24, 2005

Thank you !Ugo Fratesi

Università degli Studi di Pavia and

Politecnico di Milano

P.zza Leonardo da Vinci, 32, I-20133

Tel. +39-02-2399-3966

http://www.unipv.it/ester/index.html