Embed Size (px)

Citation preview

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 1

Lecture 4

UNDERSTANDING

INTEREST RATES (2)

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 2

The behavior of interest rates

• What determines the quantity demanded of an asset?– Wealth (total resources owned) – Expected return of one asset relative to

alternative assets– Risk (the degree of uncertainty associated

with the return)– Liquidity (the ease and speed with which

an asset can be turned into cash)

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 3

The demand for bonds

• We consider a one-year discount bond, paying the owner the face value of €1,000 in one year.

• If the holding period is one year, the return on the bond is equal the interest rate i.

• It means: i = r = (F-P)/P

• If the bond price is €950, r = 5.3%

• We assume a quantity demanded at that price of €100 billion.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 4

The demand for bonds

• If the price falls, say to €900, the interest rate increases (to 11.1%).

• Because the return on the bond is higher, the demand for the asset will rise, say to €200 billion, etc.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 5

The demand for bonds

950

900

850

800

750

5.3

11.1

17.6

25.0

33.0

Interest rate (%)Price of bond (€)

100 500400300200

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 6

The supply for bonds

950

900

850

800

750

5.3

11.1

17.6

25.0

33.0

Interest rate (%)Price of bond (€)

100 500400300200

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 7

Market equilibrium (asset market approach)

950

900

850

800

750

5.3

11.1

17.6

25.0

33.0

Interest rate (%)Price of bond (€)

100 500400300200

CP* i*

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 8

Market equilibrium

• Equilibrium occurs at point C, where demand and supply curves intersect.

• P* is the market-clearing price, and i* is the market-clearing interest rate.

• If the P P*, there is “excess supply” or “excess demand” of bonds.

• The supply and demand curves can be brought into a more conventional form:

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 9

A reinterpretation of the bond market

Interest rate (%)

33.0

25.0

17.6

11.1

5.3

100 500400300200

Demand for bonds, Bd =Supply of loanable funds, Ls

Supply of bonds, Bs =Demand for loanable funds, Ld

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 10

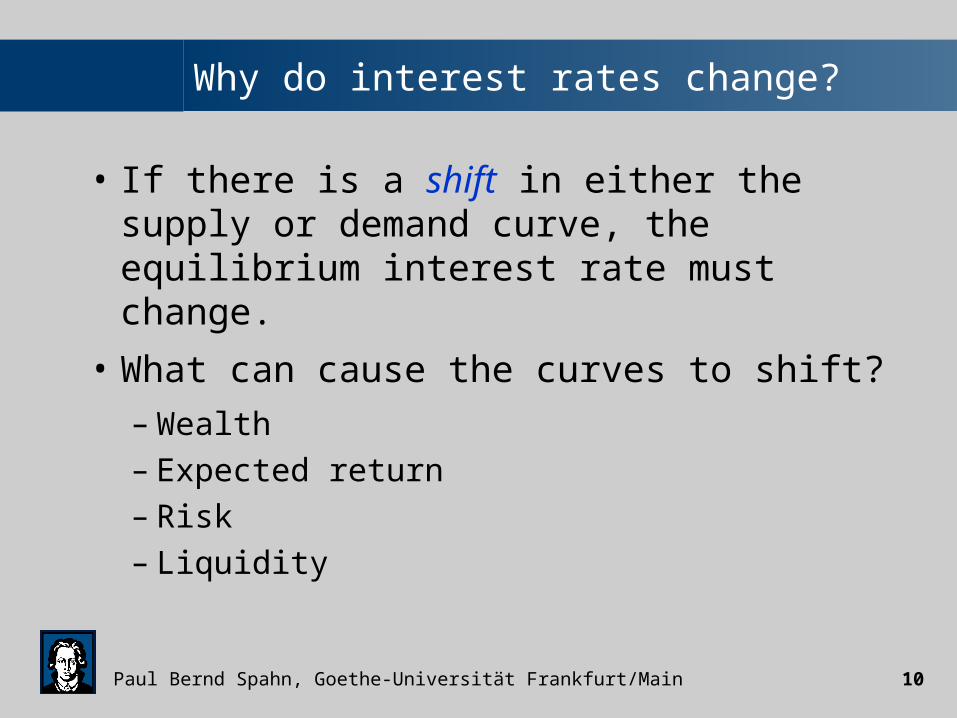

Why do interest rates change?

• If there is a shift in either the supply or demand curve, the equilibrium interest rate must change.

• What can cause the curves to shift?

– Wealth– Expected return– Risk– Liquidity

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 11

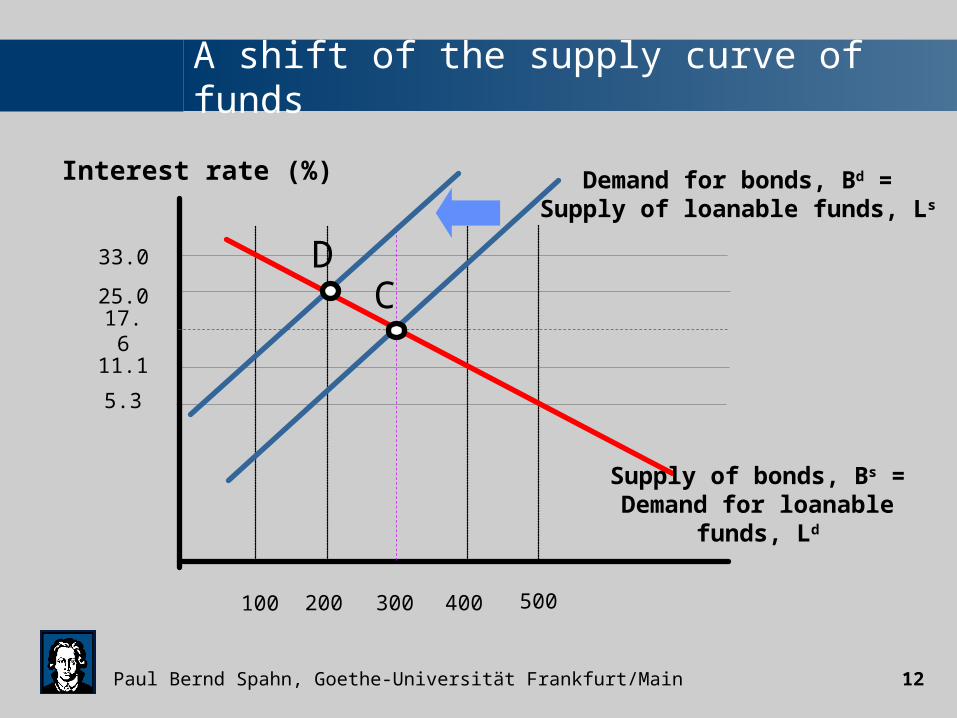

Example: Increase in risk, and demand for bonds

• If the risk of a bond increases, the demand for bonds will fall for any level of interest rates.

• It means that the supply of loanable funds is reduced.

• It is equivalent to a leftward shift of the supply curve.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 12

A shift of the supply curve of funds

Interest rate (%)

33.0

25.0

17.6

11.1

5.3

100 500400300200

Demand for bonds, Bd =Supply of loanable funds, Ls

Supply of bonds, Bs =Demand for loanable funds, Ld

CD

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 13

Effects on the supply of funds for bonds

Wealth right

Expected interest

left

Expected inflation

left

Risk left

Liquidity right

Change invariable

Change inquantity

Change ininterest rate

Shift in supply curve

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 14

The supply of bonds

• Some factors can cause the supply curve for bonds to shift, among them

– The expected profitability of investment opportunities

– Expected inflation– Government activities

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 15

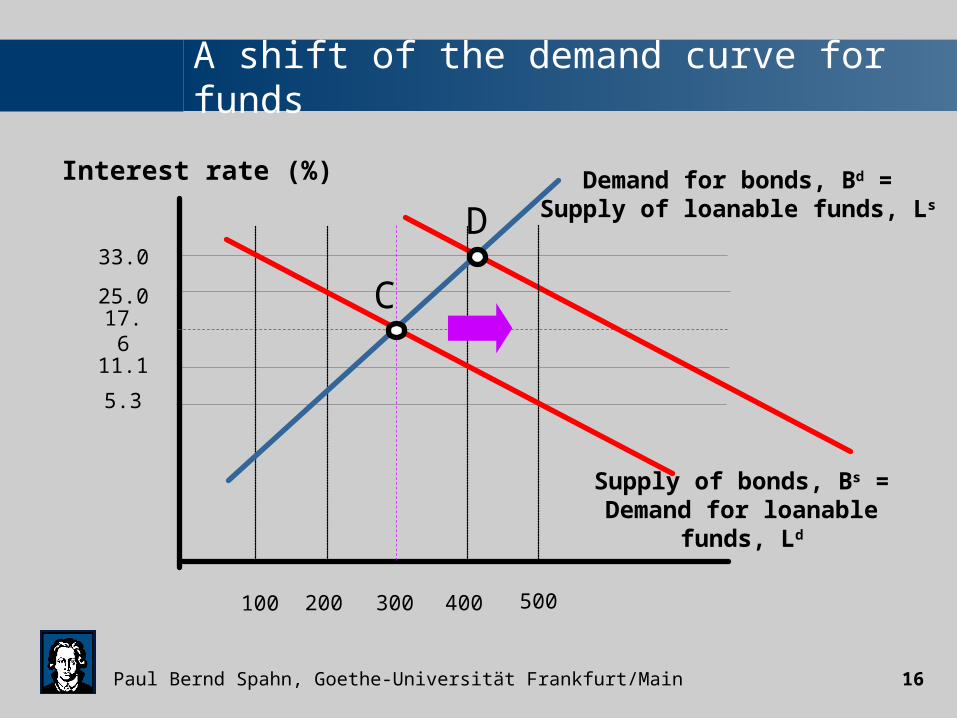

Example: Higher profitability and supply of bonds

• If the profitability of a firm increases, the supply for corporate bonds will increase for any level of interest rates.

• It means that the demand of loanable funds increases.

• It is equivalent to a rightward shift of the demand curve.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 16

A shift of the demand curve for funds

Interest rate (%)

33.0

25.0

17.6

11.1

5.3

100 500400300200

Demand for bonds, Bd =Supply of loanable funds, Ls

Supply of bonds, Bs =Demand for loanable funds, Ld

C

D

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 17

Effects on the demand of funds for bonds

Profitability right

Expected inflation

right

Governmentactivities

right

Change invariable

Change inquantity

Change ininterest rate

Shift in demand

curve

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 18

Expected inflation: The “Fisher effect”

• If expected inflation increases, both curves are affected:

– The supply of bonds (demand for funds) shifts to the right

– The demand for bonds (supply of funds for bonds) shifts to the left

• When expected inflation increases, the interest rate will rise (“Fisher effect”).

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 19

The “Fisher effect”

Interest rate (%)

33.0

25.0

17.6

11.1

5.3

100 500400300200

Demand for bonds, Bd =Supply of loanable funds, Ls

Supply of bonds, Bs =Demand for loanable funds, Ld

C

D

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 20

Government activities

• If government expands its debt (level of assets), this is tantamount to increasing its demand for loanable funds.

• It will increase the interest rate.

• In order to contain this effect, the EU member states have introduced the “Maastricht budget criteria”: – Level of government debt < 60% of GDP– Annual budget deficit < 3% of GDP

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 21

Maastricht budget criteria: Comparison

Zur Anzeige wird der QuickTime™ Dekompressor „TIFF (LZW)“

benötigt.

Zur Anzeige wird der QuickTime™ Dekompressor „TIFF (LZW)“

benötigt.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 22

France and Germany

Zur Anzeige wird der QuickTime™ Dekompressor „TIFF (LZW)“

benötigt.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 23

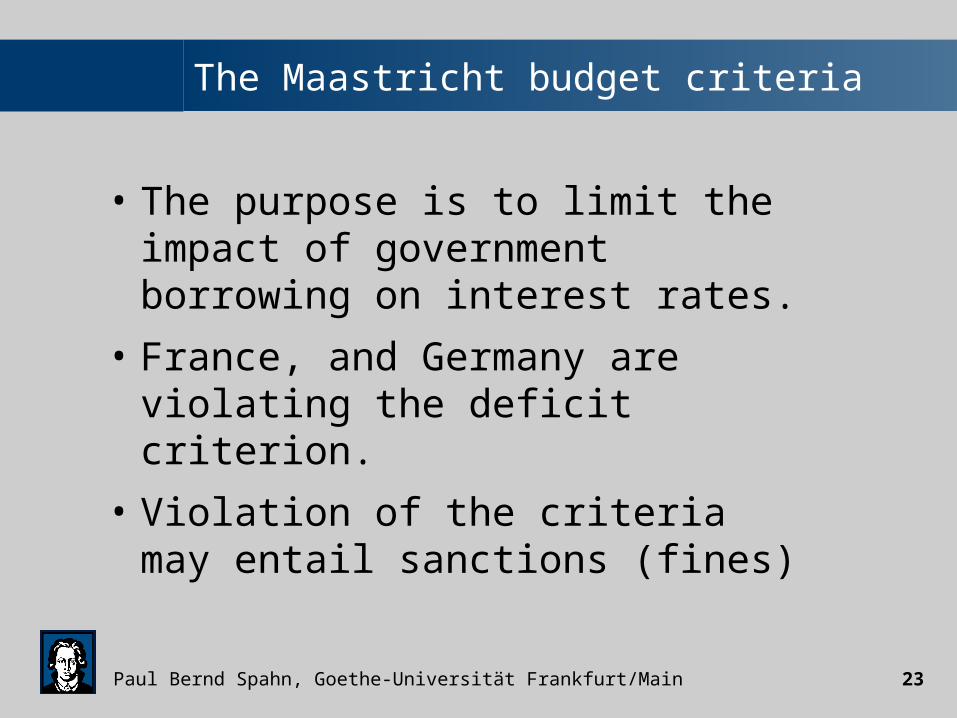

The Maastricht budget criteria

• The purpose is to limit the impact of government borrowing on interest rates.

• France, and Germany are violating the deficit criterion.

• Violation of the criteria may entail sanctions (fines)

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 24

The market for EMU government bonds (1997)

Zur Anzeige wird der QuickTime™ Dekompressor „TIFF (LZW)“ benötigt.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 25

Supply and demand for money

• An alternative model to the loanable funds theory is the model developed by J.M. Keynes: the liquidity preference theory.

• It determines the equilibrium rate of interest in terms of supply and demand for money.

John Maynard Keynes

(1883-1946)

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 26

Starting point of liquidity preference

• There are only two assets that people use to store wealth: money and bonds.

• It implies that Wealth = B + M , orBs + Ms = Bd + Md , orBs - Bd = Md - Ms

• If the money market is in equilibrium, the bond market is also in equilibrium.

• Keynes assumes that money earns no interest.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 27

Opportunity costs of money

• The amount of interest (expected return) sacrificed by not holding the alternative asset (here: bond) represents the opportunity costs of holding money.

• As interest rate rise (ceteris paribus), the expected return on money falls relative to the expected return on bonds.

• As these cost of holding money increase,the demand for money falls.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 28

Equilibrium in the market for money

Interest rate (%)

33.0

25.0

17.6

11.1

5.3

100 500400300200

Supply of money, Ms

Demand for money, Md

C

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 29

Shifts in the demand for money curve

• Keynes considers two reasons why the demand for money curve could shift:– income;– and the price level

• As income rises– wealth increases and people want to hold

more money as a store of value– people want to carry out more transactions

using money.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 30

Income and price-level effect

• A higher level of income causes the demand for money to increase and the demand curve to shift to the right.

• Changes in the price level: Keynes took the view that people care about the real value of money.

• If the price level increases, the real value of money falls:

• People want to hold a greater amount of money to restore their holdings in real terms.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 31

Response to a change in income

Interest rate (%)

33.0

25.0

17.6

11.1

5.3

100 500400300200

Supply of money, Ms

Demand for money, Md

C

D

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 32

Response to a change in the money supply

• It is assumed that the central bank controls the total amount of money available.

• The supply of money is “totally inelastic”.

• However the central bank can gear the money supply by political intervention.

• If the money supply increases, the interest rate will fall (liquidity effect).

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 33

Response to a change in money supply

Interest rate (%)

33.0

25.0

17.6

11.1

5.3

100 500400300200

Supply of money, Ms

Demand for money, Md

C D

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 34

Secondary effects of increased money supply

• If the money supply increases this has a secondary effect on money demand

• As we have seen:– it has an expansionary effect on the economy and raises

income and wealth. -> interest rates increase (income effect).

– it causes the overall price level to increase-> interest rates increase (price effect).

– it affects the expected inflation rate-> interest rates increase (Fisher-effect).

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 35

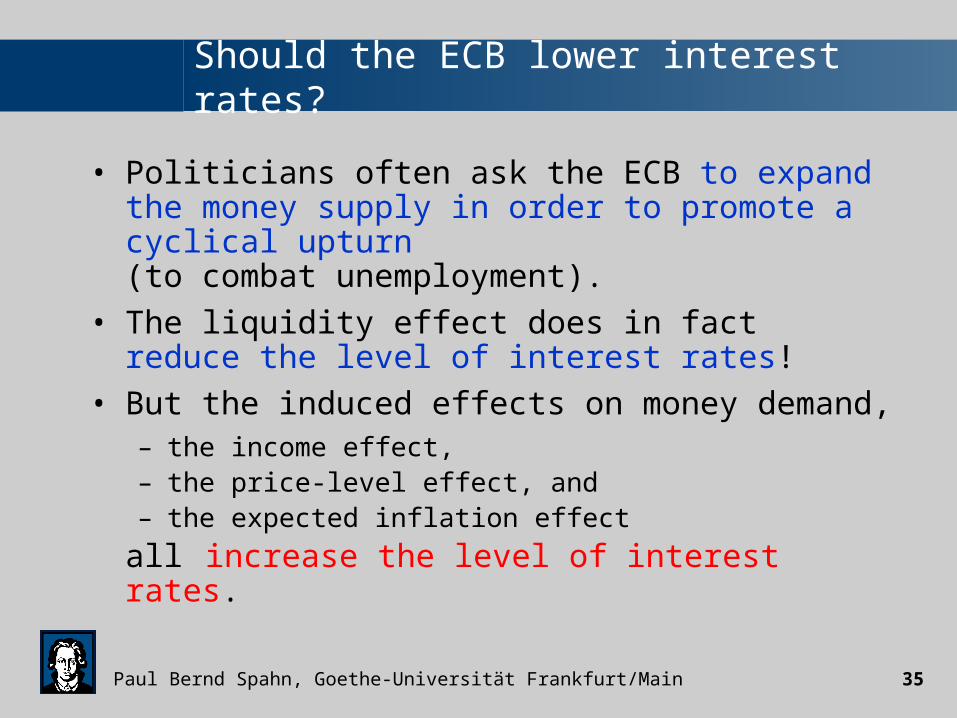

Should the ECB lower interest rates?

• Politicians often ask the ECB to expand the money supply in order to promote a cyclical upturn (to combat unemployment).

• The liquidity effect does in fact reduce the level of interest rates!

• But the induced effects on money demand,– the income effect,– the price-level effect, and– the expected inflation effect

all increase the level of interest rates.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 36

Increase of money supply plus demand shift

33.0

25.0

17.6

11.1

5.3

100 500400300200

Supply of money, Ms

Demand for money, Md

C D

Interest rate (%)

E

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 37

Growth of money (M3)

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 38

Short-term interest rates

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 39

Longer-term interest rates

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 40

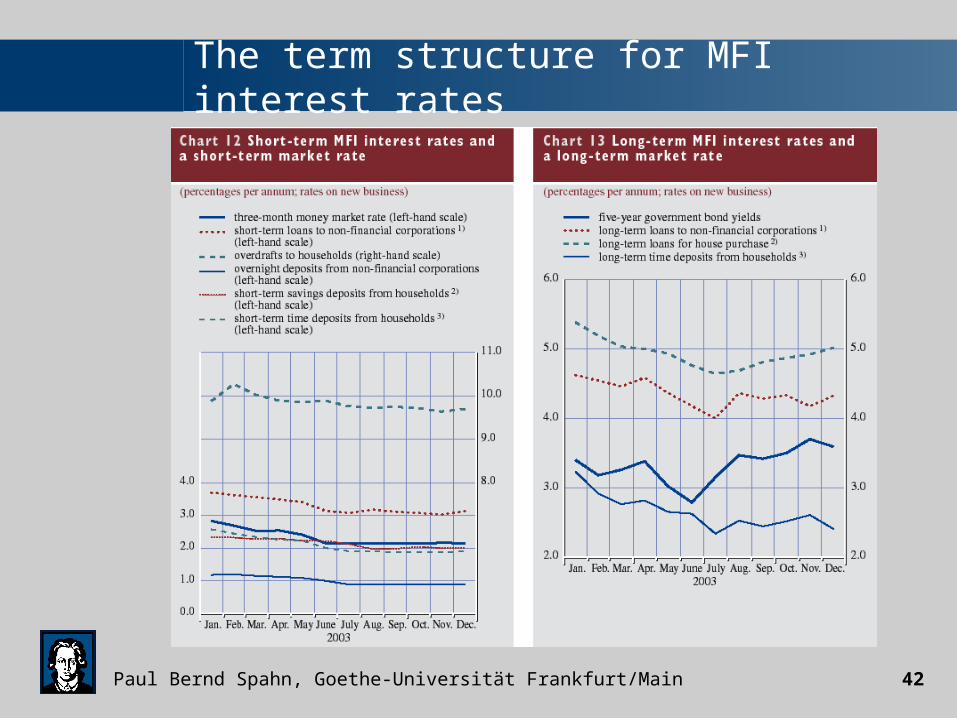

Interest rate spreads

• “The” interest rate is an abstraction. In the real world there are many interest rates.

• Interest rates differ notably with respect to the maturity of the underlying loan.

• Long-term interest rates are less affected by short-term monetary policy.

• They typically attract a higher return than short-term lending.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 41

The term structure of interest rates (USA)

Zur Anzeige wird der QuickTime™ Dekompressor „TIFF (LZW)“ benötigt.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 42

The term structure for MFI interest rates