Embed Size (px)

Citation preview

Partnership with Petro ietnam

2012

This Publication is prepared in the consultation with PricewaterhouseCoopers (Vietnam) Ltd and is intended to provide a high level overview of PVN’s investment projects. The Publication does not constitute an offer or invitation or a solicitation of any offer or invitation for the sale or purchase of any of the assets, business or shares described herein. The information in this Publication does not purport to be comprehensive. No representation or warranty, express or implied is or will be given by PVN, PwC or their respective directors, offi cers, employees or advisers or any other persons as to the accuracy and completeness of this Publication. No responsibility or liability is accepted for the accuracy or suffi ciency thereof, or for any errors, omissions or misstatement, negligent or otherwise relating thereto.

This Publication is all right reserved by Petrovietnam (PVN).

4 Message from the President and CEO 6 Chapter 1: Vietnam – An Accessible Growth Market7 Vietnam – One of the Most Dynamic Economies in Southeast Asia 11 Promising Energy Market from both the Supply and the Demand Side 13 An Attractive Destination for FDI in the Region 15 Country Snapshot16 Chapter 2: PVN as the partner of choice 17 Historical Milestones17 Major business activities and strategy 18 PVN as the partner of choice21 Chapter 3: Partnership by Sector22 1. Upstream Industry 25 Song Hong Basin 30 Phu Khanh Basin32 Onshore Mekong Delta (DBSCL)34 Nam Con Son Basin 36 Phu Quoc Basin 40 Malay – Tho Chu - Phu Quoc Basin42 2. Mid and Downstream Industry45 Nam Con Son No.2 Pipeline46 Ca Mau Gas Processing Plant47 Dung Quat Refi nery 48 Long Son Refi nery49 Ca Mau Fertilizer Plant50 Petrovietnam Gas Corporation (PVGas)51 Petrovietnam Petrochemical & Textile Fiber Joint Stock Company (PVTex)52 3. Power Industry56 Song Hau 1 Coal-fi red Power Plant57 Hoa Thang 1 Wind Power Project58 Thai Binh 2 Coal-fi red Power Plant 59 Vung Ang 1 Coal-fi red Power Plant 60 Quang Trach 1 Coal-fi red Power Plant61 Long Phu 1 Coal-Fired Power Plant62 DakDrinh Hydro Power Plant63 Hua Na Hydro Power Plant64 Nhon Trach 1 Thermal Power Plant 65 4. Services 69 Phuoc An Port Project (PAP)71 Dung Quat Shipyard (DQS)74 Petrovietnam Construction Joint Stock Corporation (PVC)75 Petrovietnam Tower 77 Petrovietnam Finance Corporation (PVFC) 78 Petrovietnam Transportation Corporation (PVTrans)79 Petrovietnam Oil Stockpile Company Limited (PVOS)80 Appendix 1 - List of Selected Key Legal Documents85 Appendix 2 - Abbreviations

Table of Contents

Message from the President and CEO

On behalf of Vietnam Oil and Gas Group (Petrovietnam), I would like to extend our warmest greetings and sincere gratitude to you.

Vietnam is forecast to be the fastest growing economy in Southeast Asia over the next few years. The country is not only rich in oil and gas resources but also has a rapidly growing industrial sector and 87 million aspiring consumers which together drive demand for energy products. Due to its promising economic development potential and open investment regime the country has attracted a large number of foreign investors and will continue to be a preferred investment destination in the future.

Petrovietnam is proud to play a pivotal role in the development of Vietnam’s economy. We have been the fl agship energy group of the country since our establishment in 1975. Over the past 3 decades, we have expanded from oil and gas exploration and production into refi ning and petrochemicals and related sectors such as power generation, support services, ship building, infrastructure and others. Our presence has expanded to cover 14 countries and will continue to explore new opportunities overseas.

In 2011, Petrovietnam generated total revenues of USD 35 billion, accounting for a signifi cant part of Vietnam’s GDP and was a major contributor to the State Budget. Between 2006 and 2010, the group achieved an average annual revenue growth rate of 28% and is recognized as the economic locomotive of the country.

We are currently operating 20 oil and gas fi elds in the Country, along with 5 abroad and we operate the fi rst oil refi nery in Vietnam. In the power sector, we are the second largest power producer in the Country and will continue to maintain this position. In the midstream sector, we operate 5 gas pipelines with a total capacity of 14 billion m3 per day.

Successful collaboration with foreign partners has contributed an important part to our success. We are confi dent of continuing our highly successful growth path and invite you to join us in making profi table investments in Vietnam’s fast growing economy. This project summary gives an overview of 29 investment opportunities in 4 areas namely Upstream, Mid and Downstream, Power and Services.

We enclose summaries of these investment opportunities in the following sections. Further detailed information can be obtained via direct discussions with Petrovietnam’s executives.

We look forward to cooperating with you in the near future.

Dr. Do Van Hau

Partnership with Petrovietnam 20126

Chapter 1: Vietnam - an AccessibleGrowth Market

7Chapter 1: Vietnam – An Accessible Growth Market

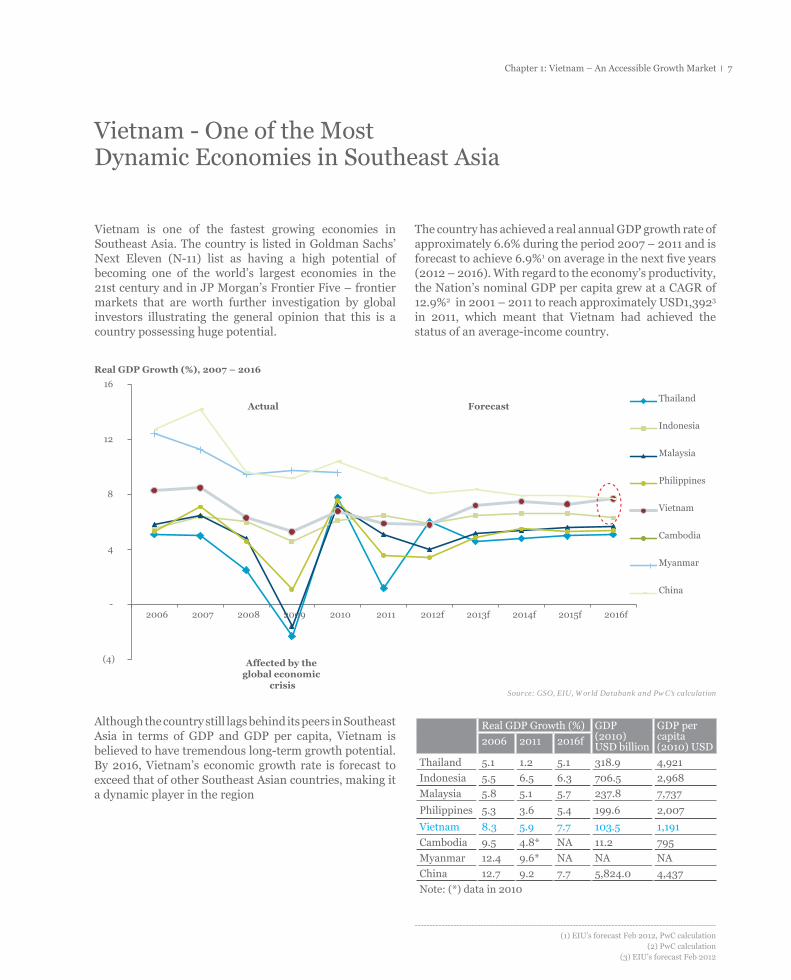

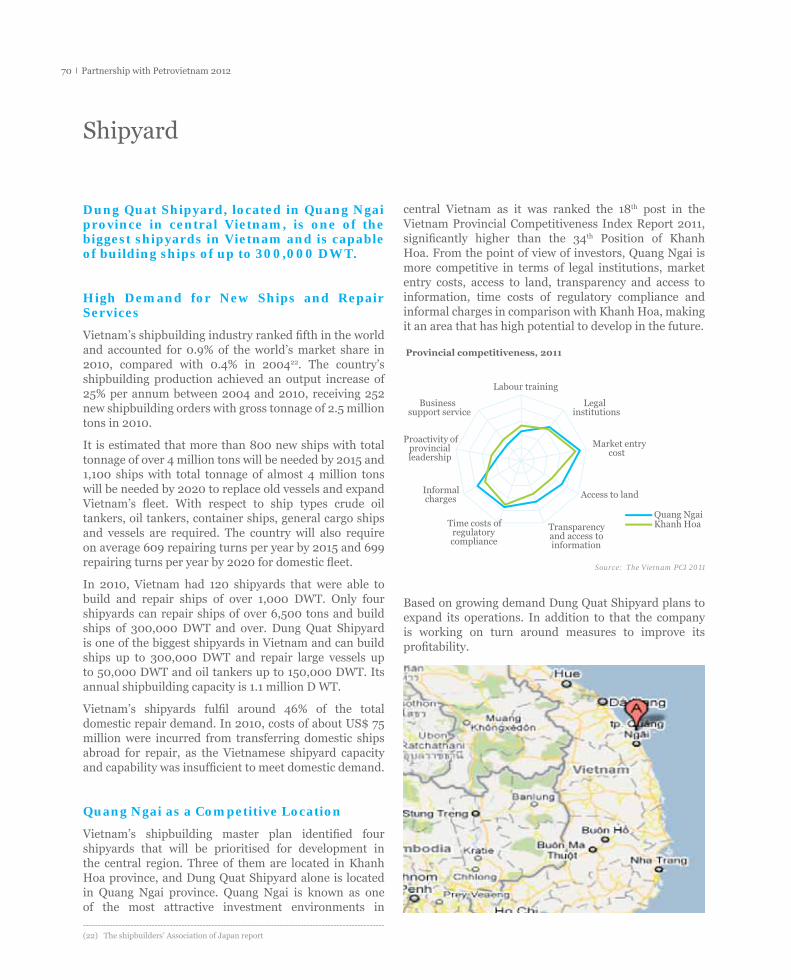

Vietnam is one of the fastest growing economies in Southeast Asia. The country is listed in Goldman Sachs’ Next Eleven (N-11) list as having a high potential of becoming one of the world’s largest economies in the 21st century and in JP Morgan’s Frontier Five – frontier markets that are worth further investigation by global investors illustrating the general opinion that this is a country possessing huge potential.

The country has achieved a real annual GDP growth rate of approximately 6.6% during the period 2007 – 2011 and is forecast to achieve 6.9%1 on average in the next fi ve years (2012 – 2016). With regard to the economy’s productivity, the Nation’s nominal GDP per capita grew at a CAGR of 12.9%2 in 2001 – 2011 to reach approximately USD1,3923 in 2011, which meant that Vietnam had achieved the status of an average-income country.

Although the country still lags behind its peers in Southeast Asia in terms of GDP and GDP per capita, Vietnam is believed to have tremendous long-term growth potential. By 2016, Vietnam’s economic growth rate is forecast to exceed that of other Southeast Asian countries, making it a dynamic player in the region

Real GDP Growth (%) GDP (2010)USD billion

GDP per capita (2010) USD2006 2011 2016f

Thailand 5.1 1.2 5.1 318.9 4,921

Indonesia 5.5 6.5 6.3 706.5 2,968

Malaysia 5.8 5.1 5.7 237.8 7,737

Philippines 5.3 3.6 5.4 199.6 2,007

Vietnam 8.3 5.9 7.7 103.5 1,191

Cambodia 9.5 4.8* NA 11.2 795

Myanmar 12.4 9.6* NA NA NA

China 12.7 9.2 7.7 5,824.0 4,437

Note: (*) data in 2010

Vietnam - One of the Most Dynamic Economies in Southeast Asia

Source: GSO, EIU, World Databank and PwC’s calculation

(4)

-

4

8

12

16

2006 2007 2008 2009 2010 2011 2012f 2013f 2014f 2015f 2016f

Real GDP Growth (%), 2007 – 2016

Thailand

Indonesia

Malaysia

Philippines

Vietnam

Cambodia

Myanmar

China

Affected by the global economic

crisis

ForecastActual

-----------------------------------------------------------------------------------------------------(1) EIU’s forecast Feb 2012, PwC calculation

(2) PwC calculation(3) EIU’s forecast Feb 2012

Partnership with Petrovietnam 20128

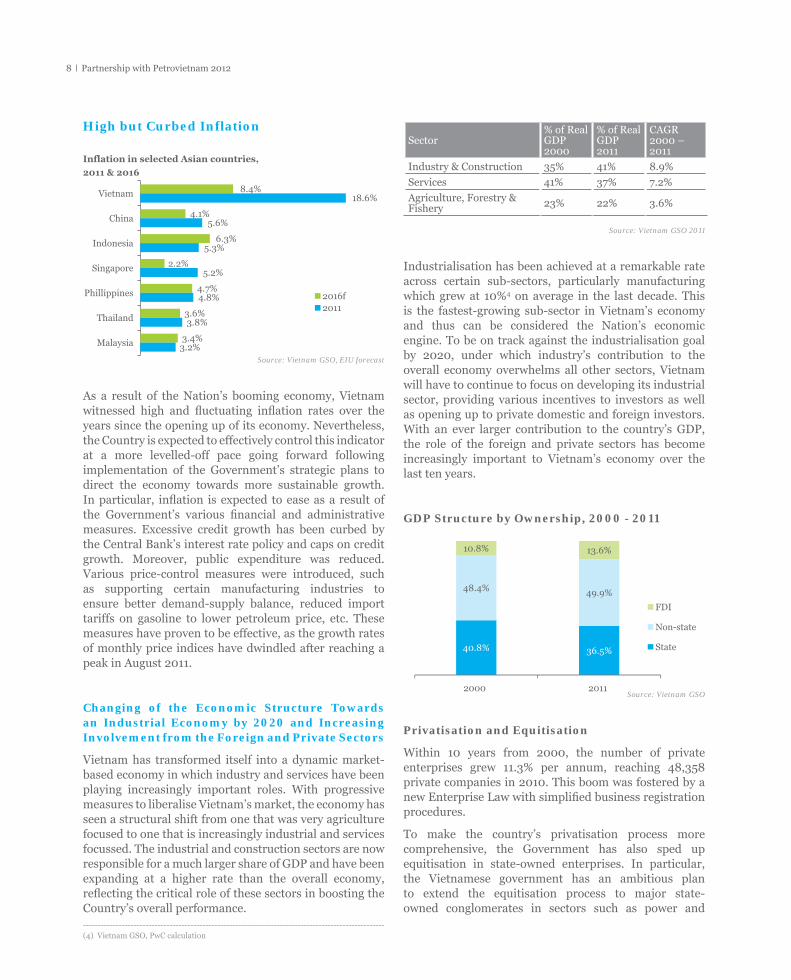

High but Curbed Inflation

3.2%

3.8%

4.8%

5.2%

5.3%

5.6%

18.6%

3.4%

3.6%

4.7%

2.2%

6.3%

4.1%

8.4%

Malaysia

Thailand

Phillippines

Singapore

Indonesia

China

Vietnam

Inflation in selected Asian countries,

2011 & 2016

2016f2011

Source: Vietnam GSO, EIU forecast

As a result of the Nation’s booming economy, Vietnam witnessed high and fl uctuating infl ation rates over the years since the opening up of its economy. Nevertheless, the Country is expected to effectively control this indicator at a more levelled-off pace going forward following implementation of the Government’s strategic plans to direct the economy towards more sustainable growth. In particular, infl ation is expected to ease as a result of the Government’s various fi nancial and administrative measures. Excessive credit growth has been curbed by the Central Bank’s interest rate policy and caps on credit growth. Moreover, public expenditure was reduced. Various price-control measures were introduced, such as supporting certain manufacturing industries to ensure better demand-supply balance, reduced import tariffs on gasoline to lower petroleum price, etc. These measures have proven to be effective, as the growth rates of monthly price indices have dwindled after reaching a peak in August 2011.

Changing of the Economic Structure Towards an Industrial Economy by 2020 and Increasing Involvement from the Foreign and Private Sectors

Vietnam has transformed itself into a dynamic market-based economy in which industry and services have been playing increasingly important roles. With progressive measures to liberalise Vietnam’s market, the economy has seen a structural shift from one that was very agriculture focused to one that is increasingly industrial and services focussed. The industrial and construction sectors are now responsible for a much larger share of GDP and have been expanding at a higher rate than the overall economy, refl ecting the critical role of these sectors in boosting the Country’s overall performance.

Sector% of Real GDP 2000

% of Real GDP 2011

CAGR2000 – 2011

Industry & Construction 35% 41% 8.9%

Services 41% 37% 7.2%

Agriculture, Forestry & Fishery 23% 22% 3.6%

Source: Vietnam GSO 2011

Industrialisation has been achieved at a remarkable rate across certain sub-sectors, particularly manufacturing which grew at 10%4 on average in the last decade. This is the fastest-growing sub-sector in Vietnam’s economy and thus can be considered the Nation’s economic engine. To be on track against the industrialisation goal by 2020, under which industry’s contribution to the overall economy overwhelms all other sectors, Vietnam will have to continue to focus on developing its industrial sector, providing various incentives to investors as well as opening up to private domestic and foreign investors. With an ever larger contribution to the country’s GDP, the role of the foreign and private sectors has become increasingly important to Vietnam’s economy over the last ten years.

GDP Structure by Ownership, 2000 - 2011

40.8% 36.5%

48.4% 49.9%

10.8% 13.6%

2000 2011

FDI

Non-state

State

Source: Vietnam GSO

Privatisation and Equitisation

Within 10 years from 2000, the number of private enterprises grew 11.3% per annum, reaching 48,358 private companies in 2010. This boom was fostered by a new Enterprise Law with simplifi ed business registration procedures.

To make the country’s privatisation process more comprehensive, the Government has also sped up equitisation in state-owned enterprises. In particular, the Vietnamese government has an ambitious plan to extend the equitisation process to major state-owned conglomerates in sectors such as power and

-----------------------------------------------------------------------------------------------------(4) Vietnam GSO, PwC calculation

9Chapter 1: Vietnam – An Accessible Growth Market

telecommunications. By 2014, the Government aims to replace the current monopoly and subsidised power situation with a competitive power generation market. In seaport construction, the PPP form of investment is encouraged and is becoming increasingly popular.

Doors are also widened for foreign players. Foreign investors now can acquire shares in domestic corporations, in some industries being able to take a majority stake if desired. Further liberalisation and growing foreign involvement is expected in the electricity sector.

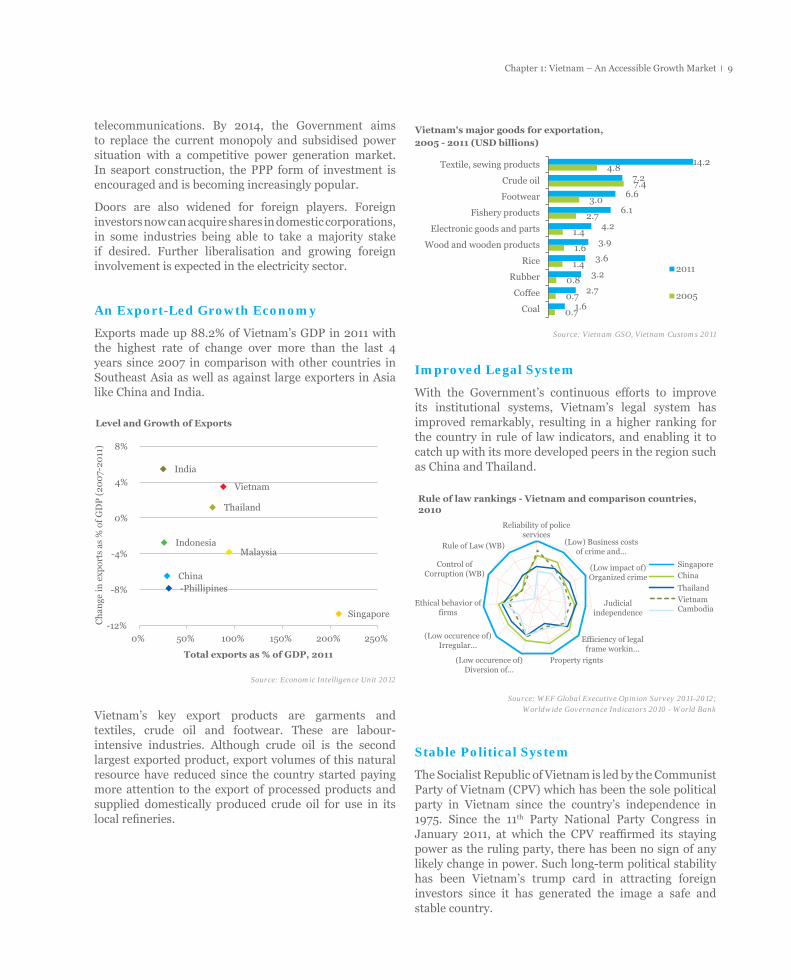

An Export-Led Growth Economy

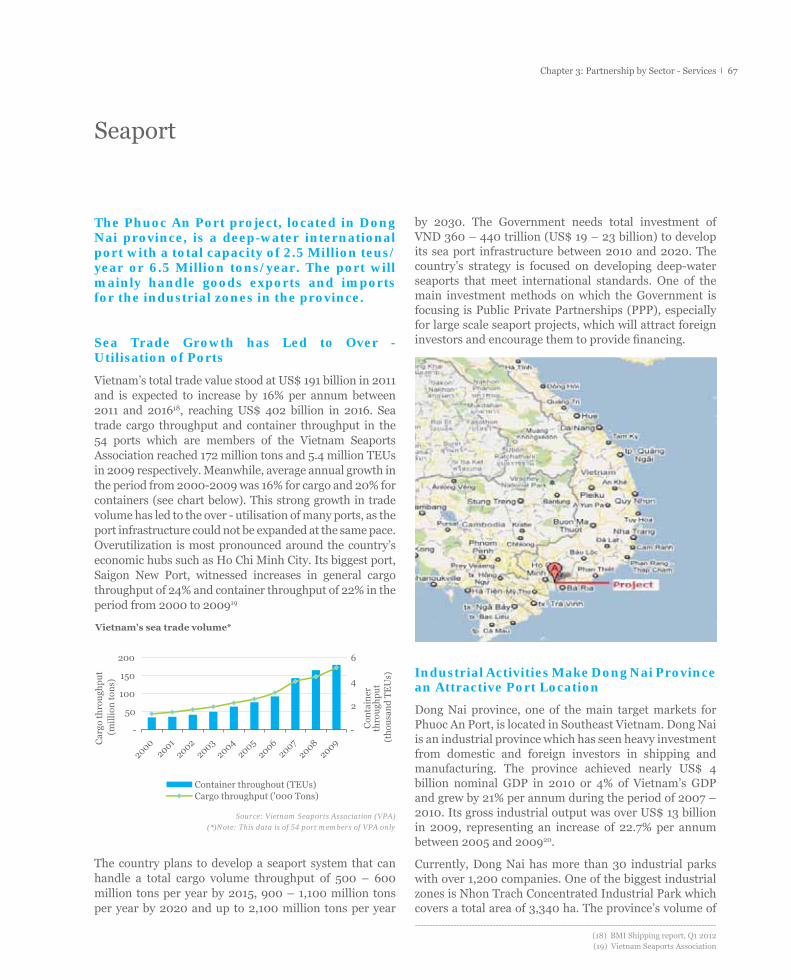

Exports made up 88.2% of Vietnam’s GDP in 2011 with the highest rate of change over more than the last 4 years since 2007 in comparison with other countries in Southeast Asia as well as against large exporters in Asia like China and India.

IndonesiaMalaysia

-Phillipines

Thailand

Vietnam

Singapore

China

India

-12%

-8%

-4%

0%

4%

8%

0% 50% 100% 150% 200% 250%

Ch

ange

in e

xpor

ts a

s %

of

GD

P (

200

7-20

11)

Total exports as % of GDP, 2011

Level and Growth of Exports

Source: Economic Intelligence Unit 2012

Vietnam’s key export products are garments and textiles, crude oil and footwear. These are labour-intensive industries. Although crude oil is the second largest exported product, export volumes of this natural resource have reduced since the country started paying more attention to the export of processed products and supplied domestically produced crude oil for use in its local refi neries.

14.2

7.2

6.6

6.1

4.2

3.9

3.6

3.2

2.7

1.6

4.8

7.4

3.0

2.7

1.4

1.6

1.4

0.8

0.7

0.7

Textile, sewing products

Crude oil

Footwear

Fishery products

Electronic goods and parts

Wood and wooden products

Rice

Rubber

Coffee

Coal

Vietnam's major goods for exportation, 2005 - 2011 (USD billions)

2011

2005

Source: Vietnam GSO, Vietnam Customs 2011

Improved Legal System

With the Government’s continuous efforts to improve its institutional systems, Vietnam’s legal system has improved remarkably, resulting in a higher ranking for the country in rule of law indicators, and enabling it to catch up with its more developed peers in the region such as China and Thailand.

Rule of law rankings - Vietnam and comparison countries,2010

Reliability of policeservices

(Low) Business costsof crime and...

(Low impact of)Organized crime

Judicialindependence

SingaporeChina

Thailand

VietnamCambodia

Efficiency of legalframe workin...

Property rignts(Low occurence of)Diversion of...

(Low occurence of)Irregular...

Ethical behavior offirms

Control ofCorruption (WB)

Rule of Law (WB)

Source: WEF Global Executive Opinion Survey 2011-2012; Worldwide Governance Indicators 2010 - World Bank

Stable Political System

The Socialist Republic of Vietnam is led by the Communist Party of Vietnam (CPV) which has been the sole political party in Vietnam since the country’s independence in 1975. Since the 11th Party National Party Congress in January 2011, at which the CPV reaffi rmed its staying power as the ruling party, there has been no sign of any likely change in power. Such long-term political stability has been Vietnam’s trump card in attracting foreign investors since it has generated the image a safe and stable country.

Partnership with Petrovietnam 201210

By virtue of such consistency as a one-party State, together with the clear mechanisms for leadership transition and the likelihood that policies will not change drastically in the medium term, Vietnam is well-known for its political stability. According to the 2010 Foreign Invested Enterprises Survey5, political stability ranks among the top three determinants encouraging FDI fl ows into Vietnam.

Prospects of a Better Administrative Environment

Though various measurements have been taken to improve the administrative environment, this remains an issue that has diluted foreign investors’ interest in Vietnam’s business environment. However, the Government is determined to change the situation through several major reform initiatives such as Project 30 (Vietnam’s Master Plan of Administrative Procedure Simplification in the field of state management for the period 2007 – 2010). The project has brought significant changes in Vietnam’s business environment such as in the customs area with the widespread introduction of e-customs and implementation of one-stop shop customs procedures which have allowed businesses to cut costs. According to the Organization of Economic Cooperation and Development, Vietnam’s success in Project 30 will provide useful lessons for other emerging nations which are also in the process of administration reforms.

A Large Pool of Well-Educated Workers at a Relatively Low Cost

Growth ’06 – ’10

1.2%

3.6%

0.5%

2.7%

1.6%11 11 12 12 1235 36 37 38 3938 39 39 40 3944 45 46 47 51

112 114 116 119 118

-

50

100

150

200

250

2006 2007 2008 2009 2010

Labor force (million people), 2005-2010

Indonesia

Vietnam

Thailand

Philippines

Malaysia

Source: World Bank

Abundant labour supply is one of the Country’s main attractions for foreign investors as well as it being a solid base for sustainable economic growth. In the 2005 - 2010 period, the employed population grew at a CAGR of 2%. Vietnam’s workforce growth is comparable with other fast-developing Southeast Asian countries like Indonesia,

Malaysia and the Philippines. By 2020, nearly 70% of the population, or about 70 million people, will be of working age. Labour quality is in line with the region, with the same adult literacy rate (93%6) as China, Malaysia and Thailand. In addition, there have been an increasing number of Vietnamese students studying overseas with an estimated 25,0007 foreign-educated students graduating each year. This is a positive complement to the country’s skilled workforce.

The labour quality has also improved as a result of the Government’s attention to education related investment as well. According to the World Bank, Vietnam’s public spending on education is higher than that of most of its neighbouring countries in Southeast Asia (5.2% of GDP in 2009 in comparison with Malaysia’s less than 5%, Thailand’s 4%, and Indonesia’s 3.5%). This bodes well for the long term future of the country.

Average wage, 2010 (Minimum annual salary per worker, USD)

Vietnam 1,002

Indonesia 1,027

China 1,500

Philippines 2,053

Thailand 2,293

Malaysia 4,735

Owing to its maintenance of a relatively low average labour cost base, Vietnam has become increasingly competitive compared to its neighbouring countries in the region and to the world’s favourite labour markets, such as China. The country’s competitive labour costs, its high quality, hard working and abundant workforce have specifi cally encouraged global producers and manufacturers (e.g. Canon, Intel, Samsung, Honda, etc.) to relocate their production hubs to Vietnam. In 2010, Intel – the world’s largest chip maker – opened its biggest chip factory in the world in Vietnam. Intel said it was attracted to Vietnam by its skilled, vibrant workforce, as well as the support and incentives Intel received from the Vietnam Government, the Saigon Hi-tech Park and suppliers. Other big names that have chosen Vietnam as a manufacturing base include Nokia, which is building a USD 300 million mobile phone plant, Danish-owned ScanCom International - one of the world’s leading exporters of wooden outdoor furniture, XP Power - the UK-listed electronic components manufacturer, etc.

-----------------------------------------------------------------------------------------------------(5) USAID, VNCI. The survey was conducted with 1,155 Foreign-Invested Enterprises (FIEs) from 47 different countries throughout Vietnam’s 63 provinces(6) World Databank(7) British Council

11Chapter 1: Vietnam – An Accessible Growth Market

Rich natural mineral resources, strong oil & gas demand and fast-growing refining capacity have helped vietnam stand out as an attractive upstream and downstream market for exporters, investors and manufacturers in the asia pacific region

Oil Demand and Supply

Vietnam will have strong demand for oil for the foreseeable future in line with the Country’s economic growth. The Nation’s consumption rate (see chart) is expected to grow at a much higher rate than those of other benchmarked countries in the Asia Pacifi c region, including the fastest-growing economy, China.

Philippin

es

Vietnam

China

Thailan

d

Mala

ysia

Australi

a

-

2

4

6

8

10

12

14

16

Ba

rre

ls/y

ea

r

Oil consumption per capita, 2010-2015

2010

2015f

4.2%

(0.8) %

2%

3.2%

1.4% 4.6%

CAGR ’10 – ’15

Source: BMI Vietnam Oil and Gas Report Q4 2011

Vietnam’s oil reserves in 2010 were the fourth largest in the Asia Pacifi c region after China, India and Malaysia while its gas reserves ranked seventh. The country’s oil reserves accounted for 10% of the region’s total and increased by an annual average rate of 8.5% from 2000 – 2010. Thanks to an oil reserves-to-production ratio (RPR) that is the region’s highest, Vietnam holds fourth place in Asia Pacifi c, behind Australia, the Philippines and India, in BMI’s Upstream Business Environment rating

3.6

17.519.9

11.8

32.6

22.2

30.0

9.9 11.3

0

5

10

15

20

25

30

35

-

5

10

15

20

Ye

ars

Bil

lio

n b

arr

els

Asia-Pacific Oil Reserves and RPR, 2010

Oil reserve

Thaila

nd

Brunei

Austral

ia

Indones

ia

Vietnam

Mal

aysia

India

China

Other

Asia

...

RPR

Source: BP’s World Energy Report 2011

Gas Demand and Supply

-

400

800

1,200

1,600

Cu

bic

me

tre

s

Gas consumption per capita, 2010 – 2015

2010 2015f

Philippin

es

China

Vietnam

Thailan

d

Mala

ysia

Australi

a

3.4%13.5%

3.4%

8.1%

4.6%1.3%

CAGR ’10 – ’15

Source: BMI Vietnam Oil and Gas Report Q4 2011

Promising Energy Market from both the Supply and the Demand Side

Partnership with Petrovietnam 201212

Vietnam’s gas consumption per capita is only 8% of the level in more developed countries like Malaysia. Given the country’s high gas consumption growth rates, it is likely to become a notable potential market.

The country’s gas reserves made up 4% of the region’s total and increased by an annual average rate of 13.8% in 2000 – 2010. New gas sources discovered off the South-wwestern coast of Vietnam have encouraged construction of pipelines to transport gas onshore and have thus boosted gas production. The country has the prospect of achieving high gas output levels in the near term, with a signifi cant forecast growth of 22%8 between 2011 and 2015.

-

2,000

4,000

6,000

8,000

10,000

-

100

200

300

400

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

2010

2011

Mil

lio

n m

3

Mil

lio

n t

on

s

Gas production in Vietnam, 2000 - 2011

LPG Dry Gas

Source: BMI Vietnam Power Report Q3 2011

In view of the signifi cant growth in national gas consumption, Vietnam is expected to become a net importer of LNG in order to meet the increasing domestic demand from 2015.

Refi nery Demand and Supply

Currently, Vietnam’s refi ning capacity covers approximately 30% of domestic petroleum demand. This fi gure is forecast to reach 60% by 2015 when Nghi Son Refi nery will enter into commercial operation. The six benchmarked countries account for nearly 50% of the region’s refi ning capacity, with China being the biggest producer. Although Vietnam accounts for the smallest portion of the region’s total output, the country’s growth in this industry is impressive. Vietnam has been on track in playing catch-up with the region with the aim of becoming self-reliant in refi ned products in the future.

Philippin

es

Mala

ysia

Vietnam

Australi

a

Thailan

d

China

-

2,000

4,000

6,000

8,000

10,000

12,000 '0

00

ba

rre

ls/d

ay

Oil refining capacity, 2010 – 2015

2010 2015f

CAGR ’10 – ’15

11.9% 0% 31% 0%0%

3.4%

Source: BMI Vietnam Oil and Gas Report Q4 2011

Hungry for electricity to support the country’s industrialisation process, Vietnam is an attractive destination for investments in power infrastructure projects

Philippin

es

Vietnam

Thailan

d

China

Mala

ysia

Australi

a

-

5

10

15

MW

h

Electricity consumption per capita, 2010 – 2015

2010 2015f

CAGR ’10 – ’15

3.8%8.5%

4.0%5.8% 4.2%

(0.2)%

Source: BMI Vietnam Power Report Q3 2011

Vietnam’s current consumption remains low compared with developed countries, but the country’s per-capita power consumption growth rate is expected to hit an impressive 8.5% vs. China’s 5.8% in the period 2010 – 2015. Rapid economic growth has created a huge demand for electricity and hence for new power plants. Electricity demand has consistently exceeded supply over recent years.

To support Vietnam’s transition to a market economy, the Government has implemented a 3 stage scheme to develop a competitive power market. As part of this effort, a gradual adjustment to the tariff has been implemented with the aim for the tariff to be on full commercial basis.

-----------------------------------------------------------------------------------------------------(8) BP’s World Energy Report 2011, PwC calculation

13Chapter 1: Vietnam – An Accessible Growth Market

Vietnam is a key destination for FDI in the region as a result of the Country’s open economic policies and moves to ease regulatory restrictions on investments as part of its accession to the WTO in 2007 and in accordance with several bilateral agreements that are in place. For example, Enterprise Law issued in 2005 has provided a common legal framework for all enterprises of different sectors (i.e. FDI, domestic private and SOEs). The Law has created a more equal regulatory environment for both domestic and foreign entities with almost no discrimination. In some cases, especially at the provincial level, FDI enterprises receive even more privileges and incentives than local private enterprises, such as lower tax rates or access to land.

In addition, due to its political stability, many foreign investors have considered Vietnam an investment hub alternative to China. Since 2007, FDI in Vietnam has increased signifi cantly. The FDI sector has reported impressive average growth of 23% per annum9 in terms of contribution to nominal GDP over the last decade, refl ecting the sector’s increasingly signifi cant role within Vietnam’s economy.

Foreign Investment

Vietnam has introduced various measures to encourage foreign investment into Vietnam. Investment in certain sectors, for example, infrastructure, high- and bio-technology, development of the petrochemicals industry is highly encouraged. Similarly, investment in certain geographical areas of Vietnam can be encouraged. Overall, investment or business sectors in Vietnam can be divided or categorised into four areas: those in which foreign investment is ‘specially encouraged’; those in which foreign investment in ‘encouraged’; those in which foreign investment is ‘conditional’ upon satisfying additional conditions; and fi nally those in which foreign investment is ‘prohibited’.

Under Viet Nam legal system, investment projects in the ‘specially encouraged’ and ‘encouraged’ sectors can be entitled to land incentives and tax incentives. The extent of the tax incentives has been however been reduced over the past few years so that only a few of these encouraged sectors are now entitled to them.

Industry sectors in which investment is encouraged/specially encouraged to support the country’s sustainable economic growth include amongst others:

• Production of light construction, composite, sound-proof of or other types of new materials;

• Construction of establishments using new energy, such as solar or wind power or bio gas;

• Application of high, new and bio-technology;• Treatment of pollution, protection of environment

and collection of waste;• Developing the petrochemicals industry ;• Investing in building power plants, power distribution

and transmission networks;

Corporate Structure

Vietnam now allows companies to be transformed into joint-stock companies in order to attract more capital from foreign investors, diversify investment forms, and improve the investment environment. In addition, listed companies have been able to increase the proportion of shares held by foreign investors from 30% to 49% since 2005. The Investment Law was introduced and applicable to all types of enterprise, providing equal treatment for enterprises of all nationalities without any discrimination between domestic and foreign investors. Following WTO commitments, signifi cant changes are expected across various sectors, including to the ownership structure in the services sector. From 2011 foreign investors will be allowed to establish a 100%-foreign-owned company in petroleum exploitation support services.

Incentives for Foreign Investment

Since 2009, tax incentives have been available for some of sectors that are special encouraged or encouraged by the Government. These sectors include scientifi c research and technological development, infrastructure development, projects in high-tech industries or high-tech zones, software development, training and health care, culture, sports and environmental activities. Accordingly, taxpayers may be eligible for preferential tax rates, tax holidays and reductions. An enterprise can be exempted from Corporate Income Tax (CIT) for a certain period beginning immediately after it fi rst makes profi ts, followed by a period where tax is charged at 50% of the applicable rate;

An Attractive Destination for FDIin the Region

-----------------------------------------------------------------------------------------------------(9) Vietnam GSO, PwC calculation

Partnership with Petrovietnam 201214

Import duty exemptions are also available for the import of machinery and equipment to form fi xed assets of encouraged projects and for use in the oil and gas sector;

Value-added tax (VAT) is exempted for certain categories of purchases: imported leased drilling rigs and ships that cannot be produced in Vietnam; equipment, machinery, spare parts, specialised means of transportation.

Multi & Bilateral Trade Agreements

The Vietnamese Government has been pursuing an open economic policy in favour of foreign trade, rapid liberalisation and integration into the global economy. In order to improve the foreign trade environment, various actions have been taken by the Government. In terms of external relationships, the Country has increased its presence in the international arena to boost its market openness and to liberalise foreign investment activities. Vietnam has been a WTO member since 2006. Since then, the Country has gradually improved its regulatory environment in accordance with its WTO commitments.

Apart from the WTO, Vietnam is also a member of a growing network of Free Trade Agreements (FTAs), both individually and as a member of ASEAN. Particularly, in 2011 – 2012, Vietnam has begun negotiating a Free Trade Agreement with the EU. Vietnam has become a negotiating member of the Trans-Pacifi c Strategic Economic Partnership (TPP) on Financial Services and Investment Agreements. Accordingly, trade barriers will be lowered further and agreement between the EU and the TPP is expected to be concluded in 2013 – 2015.

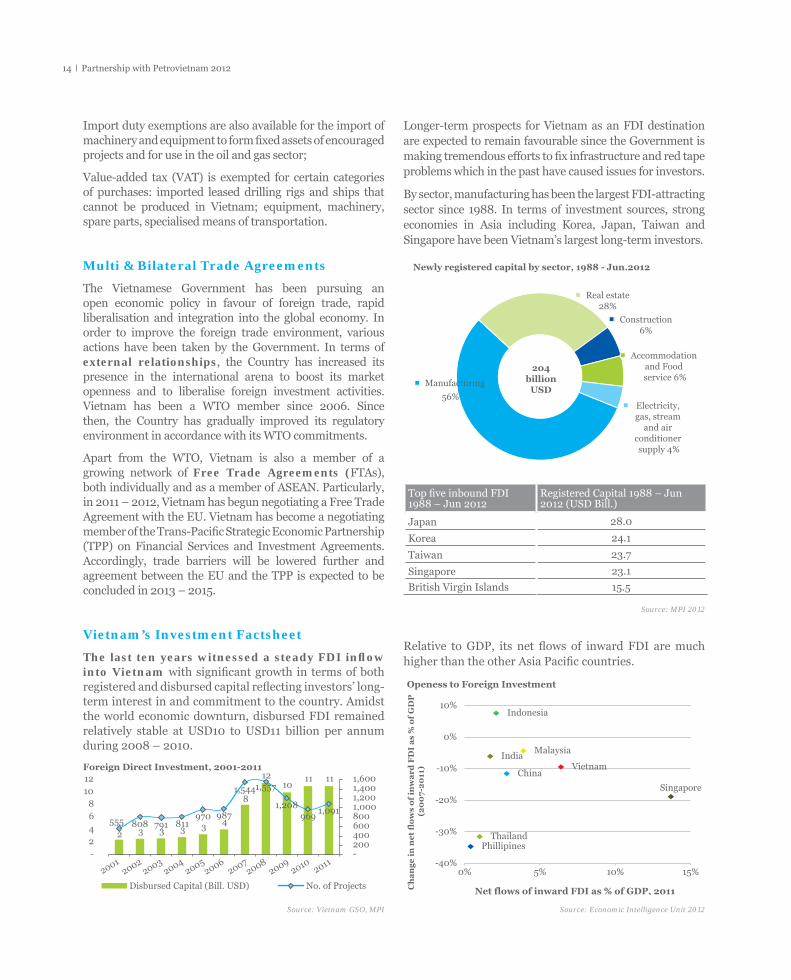

Vietnam’s Investment Factsheet

The last ten years witnessed a steady FDI infl ow into Vietnam with signifi cant growth in terms of both registered and disbursed capital refl ecting investors’ long-term interest in and commitment to the country. Amidst the world economic downturn, disbursed FDI remained relatively stable at USD10 to USD11 billion per annum during 2008 – 2010.

20012002

20032004

20052006

20072008

20092010

2011

2 3 3 3 3 4

8

12 10

11 11

555 808 791 811 970 987

1,544 1,557

1,208 969

1,091

-200 400 600 800 1,000 1,200 1,400 1,600

- 2 4 6 8

10 12 Foreign Direct Investment, 2001-2011

Disbursed Capital (Bill. USD) No. of Projects

Source: Vietnam GSO, MPI

Longer-term prospects for Vietnam as an FDI destination are expected to remain favourable since the Government is making tremendous efforts to fi x infrastructure and red tape problems which in the past have caused issues for investors.

By sector, manufacturing has been the largest FDI-attracting sector since 1988. In terms of investment sources, strong economies in Asia including Korea, Japan, Taiwan and Singapore have been Vietnam’s largest long-term investors.

Manufacturing

56%

Real estate28%

Construction6%

Accommodation and Food service 6%

Electricity, gas, stream

and air conditioner supply 4%

Newly registered capital by sector, 1988 - Jun.2012

204billion

USD

Top fi ve inbound FDI1988 – Jun 2012

Registered Capital 1988 – Jun 2012 (USD Bill.)

Japan 28.0

Korea 24.1

Taiwan 23.7

Singapore 23.1

British Virgin Islands 15.5

Source: MPI 2012

Relative to GDP, its net fl ows of inward FDI are much higher than the other Asia Pacifi c countries.

Indonesia

Malaysia

Phillipines Thailand

Vietnam

Singapore

China

India

-40%

-30%

-20%

-10%

0%

10%

0% 5% 10% 15%

Ch

an

ge

in

ne

t fl

ow

s o

f in

wa

rd F

DI

as

% o

f G

DP

(2

00

7-2

011

)

Net flows of inward FDI as % of GDP, 2011

Openess to Foreign Investment

Source: Economic Intelligence Unit 2012

15Chapter 1: Vietnam – An Accessible Growth Market

Area 330,957.6 sq km Currency Vietnamese Dong (VND)

Population • 87.84 million • 31.7% in urban areas

Exchange rate (2011) USD 1 = VND 20,649

Key Cities• Capital: Hanoi City• Largest city: Ho Chi Minh City

(Population: 7.5 million) Labour force 51.4 million

Administrative Units

64 provinces and cities directly under the Central Government Exports

USD 53.1 billion (fi rst half of 2012)Major commodities: textiles, crude oil, footwear, fi shery products, electronic goods, computers and partsMajor trading partners: US, EU, ASEAN, Japan, China,

GDP Nominal – USD 122.8 billion Per capita – USD 1,375Growth – 5.89%

Imports

USD 53.8 billion (fi rst half of 2012)Major commodities: Machinery, instruments, refi ned petroleum oil, iron, steel, textile fabrics, electronic goods, computers & partsMajor trading partners: China, ASEAN, Japan, Korea, EU

GDP composition

Agriculture: 22%Industry: 41%Services: 37%

Foreign Direct Investment

USD 203 billion (1988 – Jun. 2012)Major investors: Japan, Korea, Taiwan, Singapore, British Virgin Islands

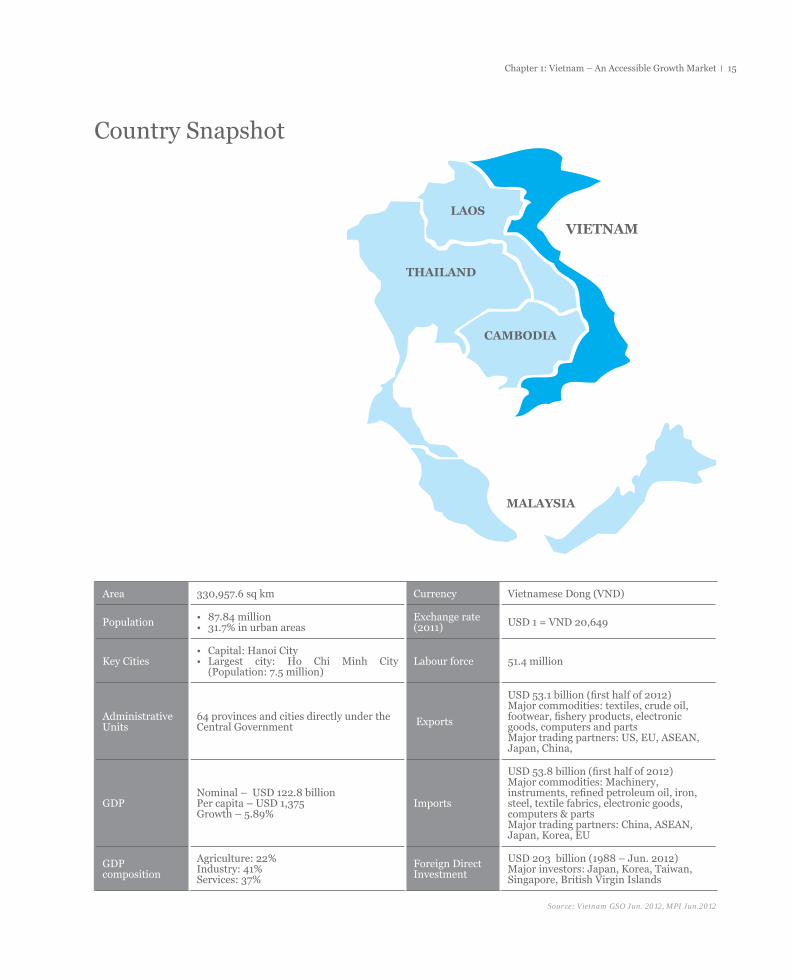

Country Snapshot

VIETNAM

MALAYSIA

THAILAND

LAOS

CAMBODIA

Source: Vietnam GSO Jun. 2012, MPI Jun.2012

Partnership with Petrovietnam 201216

Chapter 2: PVN as the Partner of Choice

17Chapter 2: PVN as the Partner of Choice

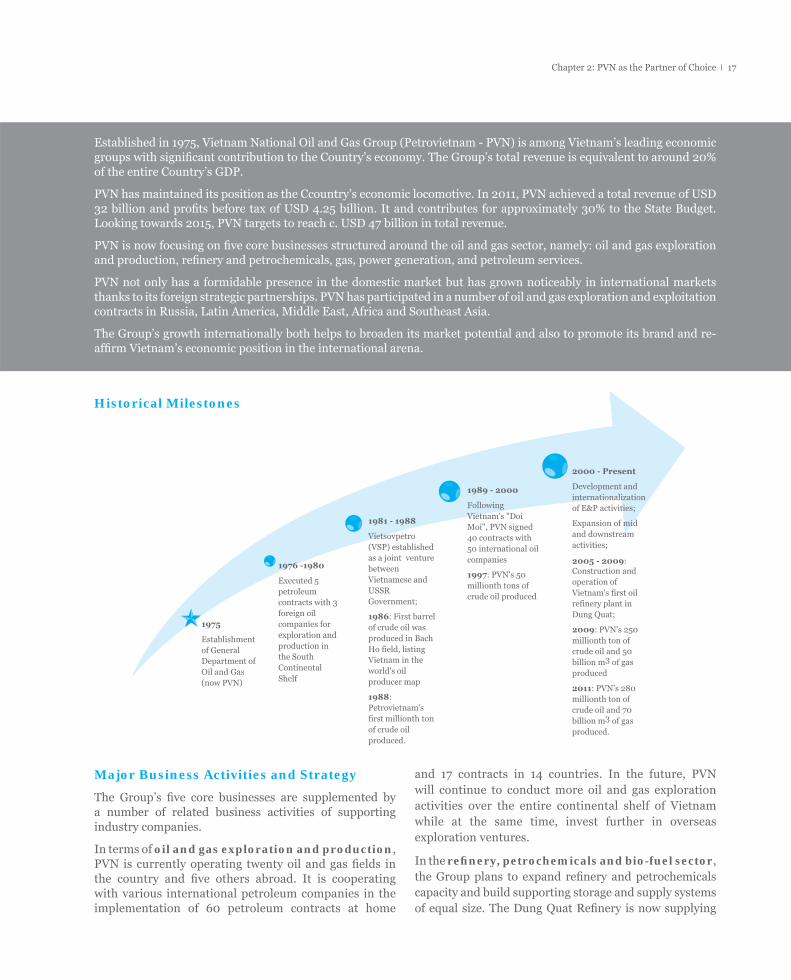

Established in 1975, Vietnam National Oil and Gas Group (Petrovietnam - PVN) is among Vietnam’s leading economic groups with signifi cant contribution to the Country’s economy. The Group’s total revenue is equivalent to around 20% of the entire Country’s GDP.

PVN has maintained its position as the Ccountry’s economic locomotive. In 2011, PVN achieved a total revenue of USD 32 billion and profi ts before tax of USD 4.25 billion. It and contributes for approximately 30% to the State Budget. Looking towards 2015, PVN targets to reach c. USD 47 billion in total revenue.

PVN is now focusing on fi ve core businesses structured around the oil and gas sector, namely: oil and gas exploration and production, refi nery and petrochemicals, gas, power generation, and petroleum services.

PVN not only has a formidable presence in the domestic market but has grown noticeably in international markets thanks to its foreign strategic partnerships. PVN has participated in a number of oil and gas exploration and exploitation contracts in Russia, Latin America, Middle East, Africa and Southeast Asia.

The Group’s growth internationally both helps to broaden its market potential and also to promote its brand and re-affi rm Vietnam’s economic position in the international arena.

Major Business Activities and Strategy

The Group’s fi ve core businesses are supplemented by a number of related business activities of supporting industry companies.

In terms of oil and gas exploration and production, PVN is currently operating twenty oil and gas fi elds in the country and fi ve others abroad. It is cooperating with various international petroleum companies in the implementation of 60 petroleum contracts at home

and 17 contracts in 14 countries. In the future, PVN will continue to conduct more oil and gas exploration activities over the entire continental shelf of Vietnam while at the same time, invest further in overseas exploration ventures.

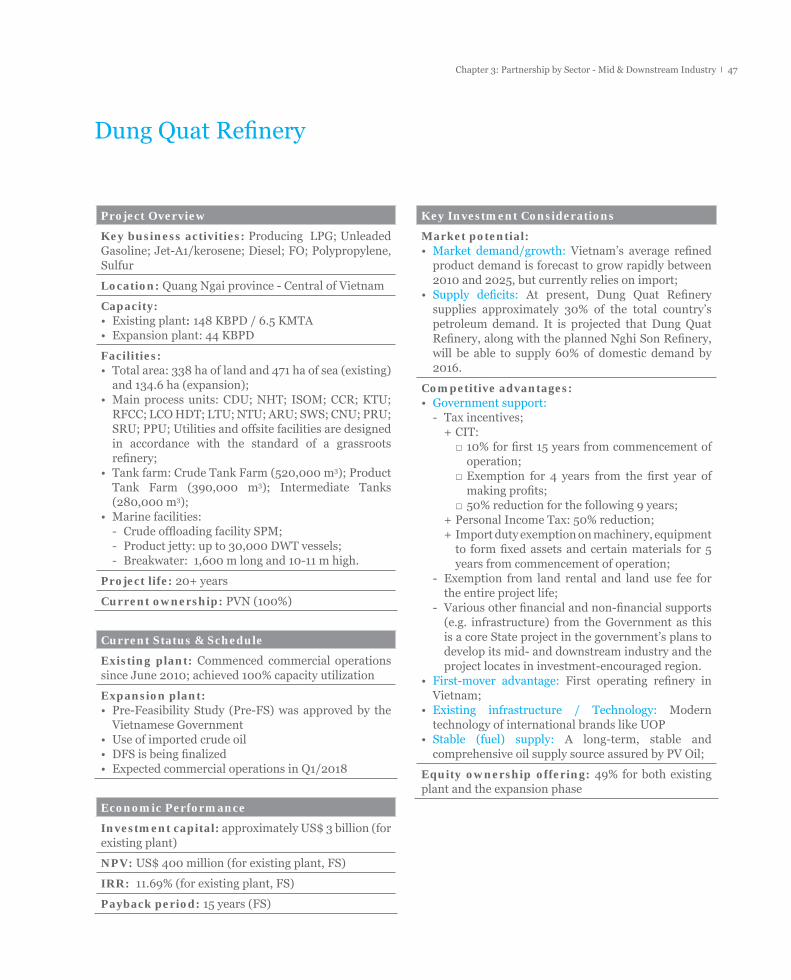

In the refi nery, petrochemicals and bio-fuel sector, the Group plans to expand refi nery and petrochemicals capacity and build supporting storage and supply systems of equal size. The Dung Quat Refi nery is now supplying

Historical Milestones

1975

Establishment of General Department of Oil and Gas (now PVN)

1976 -1980

Executed 5 petroleum contracts with 3 foreign oil companies for exploration and production in the South Continental Shelf

1981 - 1988

Vietsovpetro (VSP) established as a joint venture between Vietnamese and USSR Government;

1986: First barrel of crude oil was produced in Bach Ho field, listing Vietnam in the world's oil producer map

1988:Petrovietnam's first millionth ton of crude oil produced.

1989 - 2000

Following Vietnam's "Doi Moi", PVN signed 40 contracts with 50 international oil companies

1997: PVN's 50 millionth tons of crude oil produced

2000 - Present

Development and internationalization of E&P activities;

and downstream activities;

2005 - 2009:Construction and operation of Vietnam's first oil refinery plant in Dung Quat;

2009: PVN's 250millionth ton of crude oil and 50billion m3 of gas produced

2011: PVN’s 280millionth ton of crude oil and 70 billion m3 of gas produced.

Expansion of mid

Partnership with Petrovietnam 201218

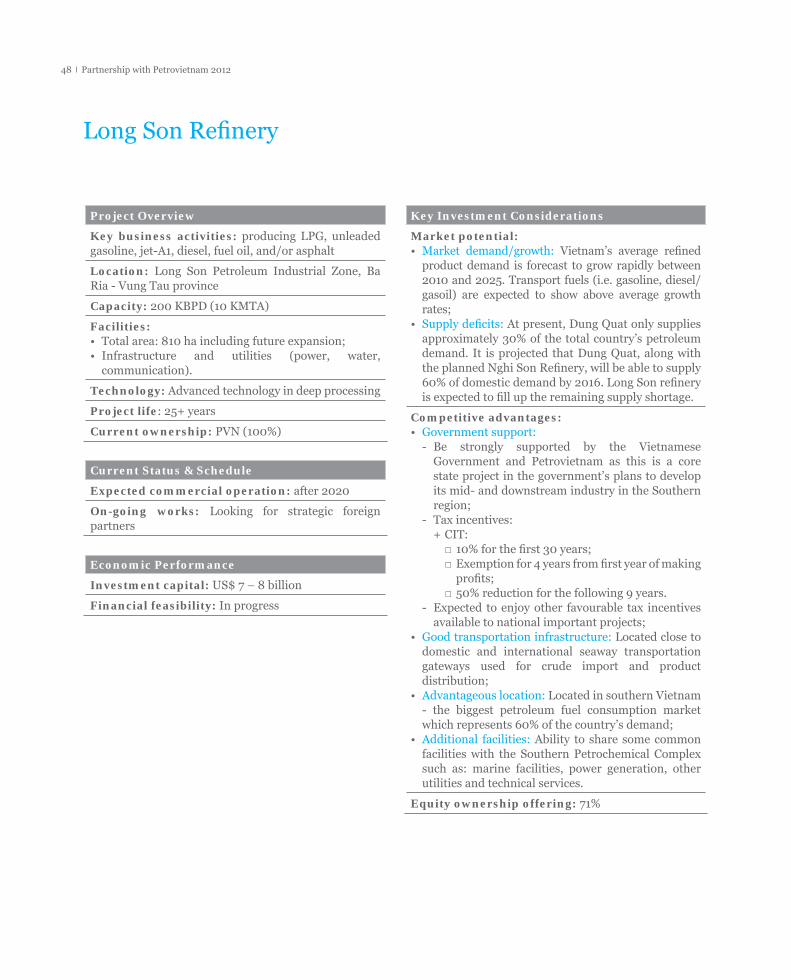

30% of domestic demand. In the coming years, PVN will make more investments in expanding the Dung Quat Refi nery and in constructing the Nghi Son and Long Son Refi nery and Petrochemical Complex (the Long Son Petrochemical Plant) to raise the total refi ning capacity to 16-17 million tons per year by 2015 and 30 million tons per year by 2025.

As for the gas industry, PVN will develop an integrated industry with a focus on the development of the national gas industry infrastructure. The completion of the gas industry infrastructure in the South and the formation of the infrastructure for the gas industry in the North and Central regions will ensure suffi cient gas supply to industry and for public consumption. PVN’s objective is to produce 17-21 billion m3 of gas a year by 2015, 22-29

billion m3 of gas and 3-4 million tons of LPG by 2025.

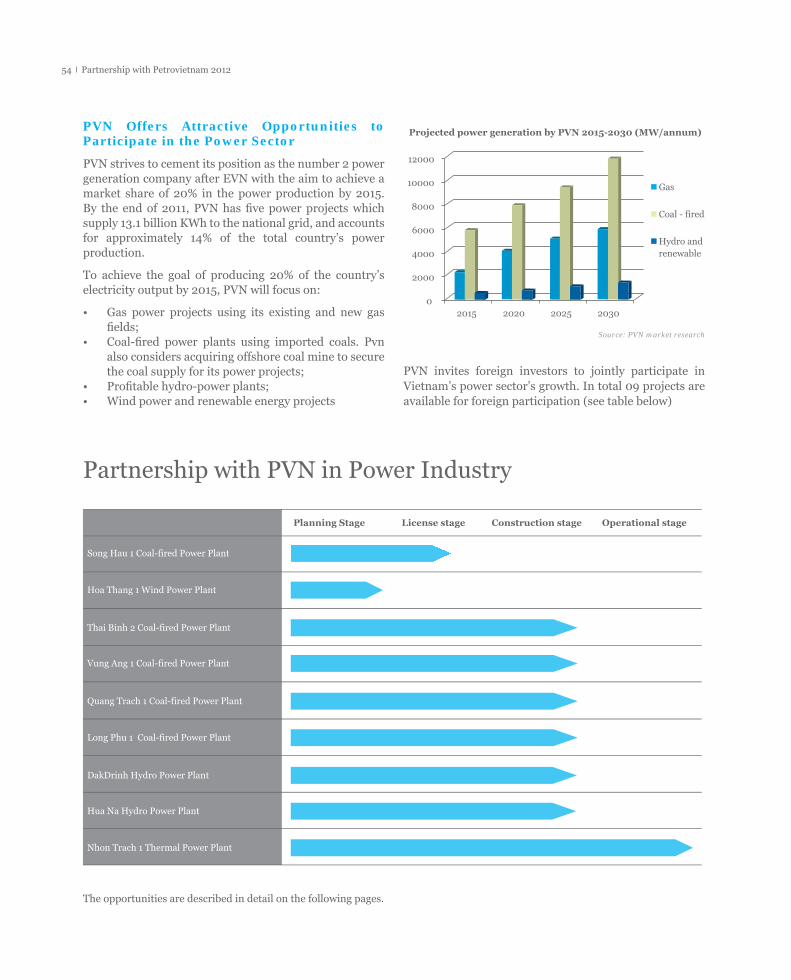

In the power generation sector, the Group will continue to participate in power generation and be the second largest power producer after EVN. Its focus will be gas- and coal-fi red power generation in parallel with the gas industry development programme mentioned earlier so that by 2015 the total power generation capacity of all PVN’s power plants will be over 9,250 MW and 13,000 MW by 2020 accounting for approximately 20% of total Country’s power production.

With regards to petroleum technical services, PVN will continue to develop its capability to better address the domestic petroleum services demand while making fi rm steps towards the regional and international markets by 2020.

Vision Toward 2025 “To Be The Flagship Petroleum Group In The Region By 2025 – A Pride Of Vietnam”

PVN and the Government

PVN is a leading state-owned economic Group with revenue accounting a signifi cant partfor 20% of the Nation’s GDP and contributing a signifi cant part to the State Budget. PVN is one of the government bodies used to realize national macroeconomic objectives. On the one hand, the Government reserves total control over the corporation’s organisation and operations. On the other hand, PVN acts as the Country’s economic locomotive not only in the oil and gas sector but also in energy-related industries. PVN is considered the government vehicle for implementing and realising national strategic energy plans as well as other macroeconomic plans to support the country’s growth.In the Government’s future energy plan to boost the Country’s energy sector as well as strengthen its global competitiveness, PVN is placed at the core. In other words, the Group is backed by the Government and receives support in terms of both fi nance and policy-related matters.

In the power sector PVN also has a pivotal role in realizing the Country’s energy development plan. PVN has been assigned by the Government to develop a number of important national power projects. PVN is the second largest power producer in the country, only after EVN. PVN also represents the Country in promoting energy cooperation between Vietnam and other countries through various cooperation agreements signed between the corporation and foreign National Oil Corporation (NOCs).

PVN is the fl agship of Vietnam’s state-owned enterprises (SOEs). Vietnam has ambitious plans to speed up the

renovating and modernizing the Country’s large SOEs, transforming them into international competitors that are more market-oriented and effi cient. PVN takes a lead role in this plan.

PVN as the Partner of Choice

PVN is the preferred partner for foreign companies who wish to participate in the country’s energy market. The Group has impressive track records in developing projects on its own and together with foreign partners. The following successful stories provide an overview of what PVN and its partners have achieved together:

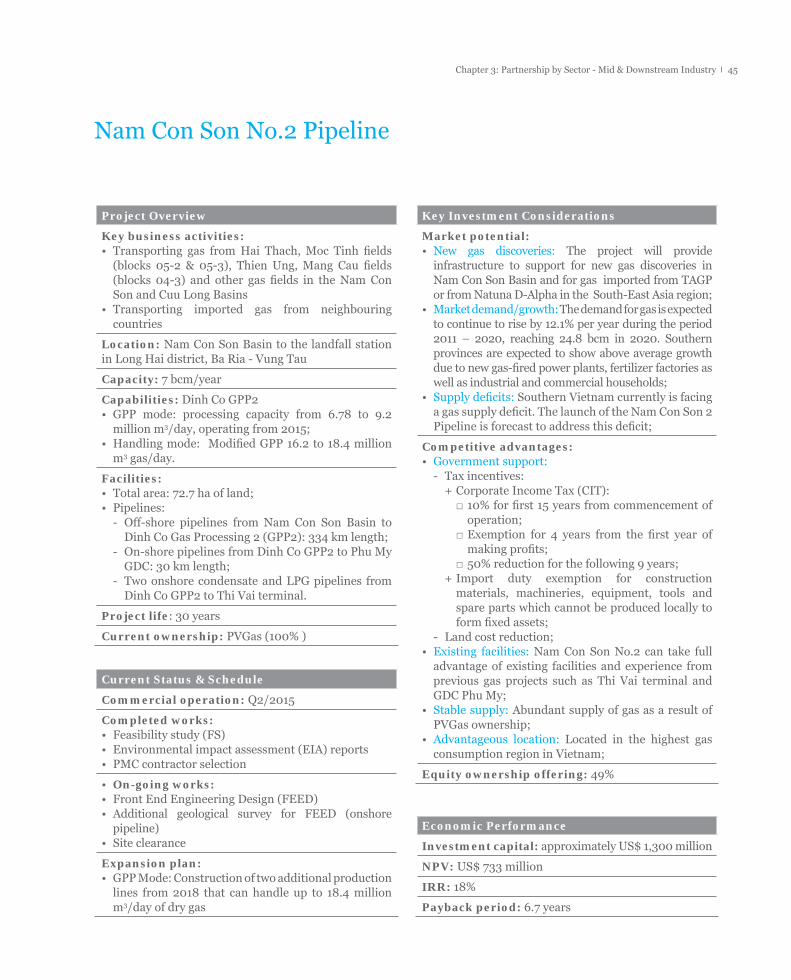

Nam Con Son Pipeline 1

The Nam Con Son Pipeline is the fi rst and longest pipeline of Vietnam. It was developed jointly by PVN (51%), BP (32.67%) and ConocoPhillips (16.33%) in the form of a BCC.

The pipeline has a capacity of 7 billion m3 per annum and came into commercial operation in 2003. It supplies natural gas to the Phu My Power Complex, Phu My Fertilizer and other petrochemical factories in the surrounding area. The pipeline currently operates at full capacity. The revenue from transportation of gas in 2010 reached USD 220 million.

The success of Nam Con Son pipeline 1 encouraged PVN to expand the project to Phase 2, which expects to enter commercial operation by 2018.

19Chapter 2: PVN as the Partner of Choice

Block B – Omon Gas Pipeline Project

The project Block B – Omon Gas Pipeline is a key project in Vietnam’s oil and gas industry. Construction of the pipeline system started in November 2009 and is planned for commercial operation in Q2/2014. Once put into operation, the system will transfer natural gas from Block B, 48/95 and 52/97 (B & 52) in the southwest sea of Vietnam to provide gas for power plants in Omon and Tra Noc – Can Tho Province (capacity: 3,000 MW), to 2 Ca Mau power plants and to households in the southwestern region of the country.

With a total length of 400 km, of which the offshore length is 246 km and the onshore length is 154 km, cutting across Can Tho City and 4 provinces (Hau Giang, Kien Giang, Bac Lieu, Ca Mau), the project can deliver 18.3 millions m3/day-night (6.4 billion m3/year).

Total investment capital of the project is USD 1 billion in which PVN holds a 51% ownership, Chevron 29%, MOECO 15% and PTTEP 5%. The cooperation for this project marked a milestone in Vietnam’s long-term partnership with foreign counterparts in constructing gas pipelines. The project will act to encourage foreign investors to participate in implementing gas projects in Vietnam in the future.

Vietsovpetro Joint Venture

This is the fi rst joint venture with foreign partners of Vietnam in the oil and gas sector and is one of the most successful foreign partnerships. Three of their oilfi elds are currently under production of which Bach Ho is the largest oilfi eld in Vietnam and the 3rd largest in the Northwest Pacifi c Region (Japan, China and ASEAN). OAO Zarubejneft holds a 49% interest in the joint venture. The remaining 51% is held by PVN.

In 2011, the total revenue from sale of crude oil reached USD 5.61 billion. The Russian partner’s share of the profi ts reached over USD 580 million, a USD 121 million higher than previous year.

Nghi Son Petrochemical and Refinery Complex

Nghi Son is Vietnam’s second planned refi nery after the Dung Quat Refi nery. Once operations commence in 2016 (targeted), the plant will have a capacity (Phase 1) of 10 million tons of crude oil per year (200 thousand BPD), using crude oil from the Middle East. Nghi Son’s main products will include A92, and A95 petroleum, diesel, jet fuel, etc. Nghi Son and Dung Quat’s outputs are suffi cient to meet about 60% of domestic demand for petroleum products.

The project is being jointly developed by Kuwait Petroleum International (KPI) 35.1%, Idemitsu Kosan (IKC) 35.1%; Petrovietnam 25.1% and Mitsui Chemicals (MCI) 4.7%. With the involvement of foreign partners, Nghi Son Refi nery will become a refi nery of international standards with modern technology. The joint venture also gives the refi nery a stable and long-term crude oil supply that helps it to maintain sustainable growth and competitiveness in terms of operations and effi ciency and the establishment of high quality human resources.

PVN – Gazprom Gas Exploitation Joint Venture

The Joint Venture Agreement (JVA) with Gazprom - Russia’s top gas producer - is PVN’s most recent partnership. The two corporations signed a JVA in April 2012. Under this agreement, Gazprom holds a 49% share in the joint venture, the key business activity of which is to exploit gas in Block No. 05.2 and 05.3 along Vietnam’s continental shelf. Two gas condensate fi elds Moc Tinh and Hai Thach as well as the Kim Cuong Tay oil fi eld were discovered in these two blocks. Gas reserves in these fi elds are estimated at 55.6 billion m3, together with 25.1 million tons of gas condensate. Gazprom and PVN have plans to launch the construction of 16 production wells at depths of 2,000 to 4,600 meters in order to develop the fi elds.

PVI’s Partnerships with Oman, Talanx and Sun Life

PVI is one of the leading insurance companies of Vietnam. In 2011, PVI generated a gross premium of US$202 million. Total revenue growth was 25% year-on-year. 2011 was the second year PVI was rated Financial Strength Rating of B+ (Good) by A.M Best and acknowledged as the honourably prized Insurance Company of the Year, Vietnam by World Finance. PVI Reinsurance - a subsidiary of PVI, was also rated Financial Strength Rating of B+ (Good) by A.M Best in 2011.

After signing the partnership agreement with Oman Investment Fund, PVI has entered into a strategic investment agreement with Talanx Insurance Investment (Germany). Recently, PVI and Sun Life Financial have signed an agreement to form a life insurance joint venture - PVI Sun Life. This establishment will help PVI to become the second insurance company in Vietnam providing both life and non-life insurance products.

Partnership with Petrovietnam 201220

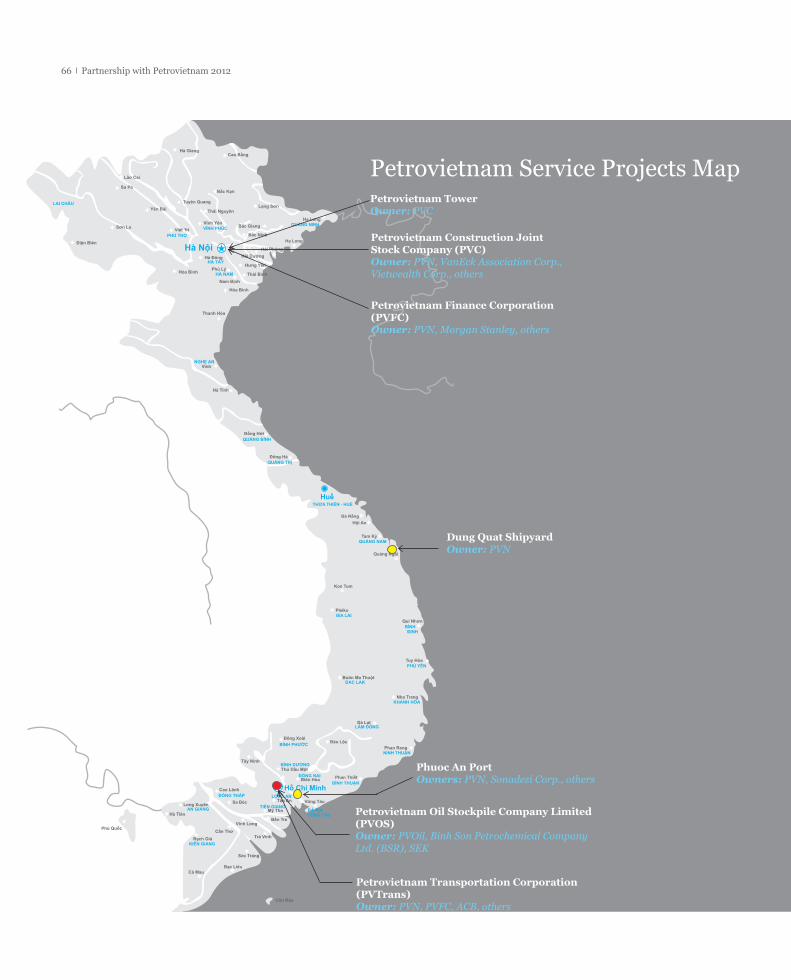

Overview of Non E&P Projects

No. Project Name Owner Location

Total Investment Capital (million USD)

Total Assets 31/12/2011 (million USD)

Equity Ownership Offering

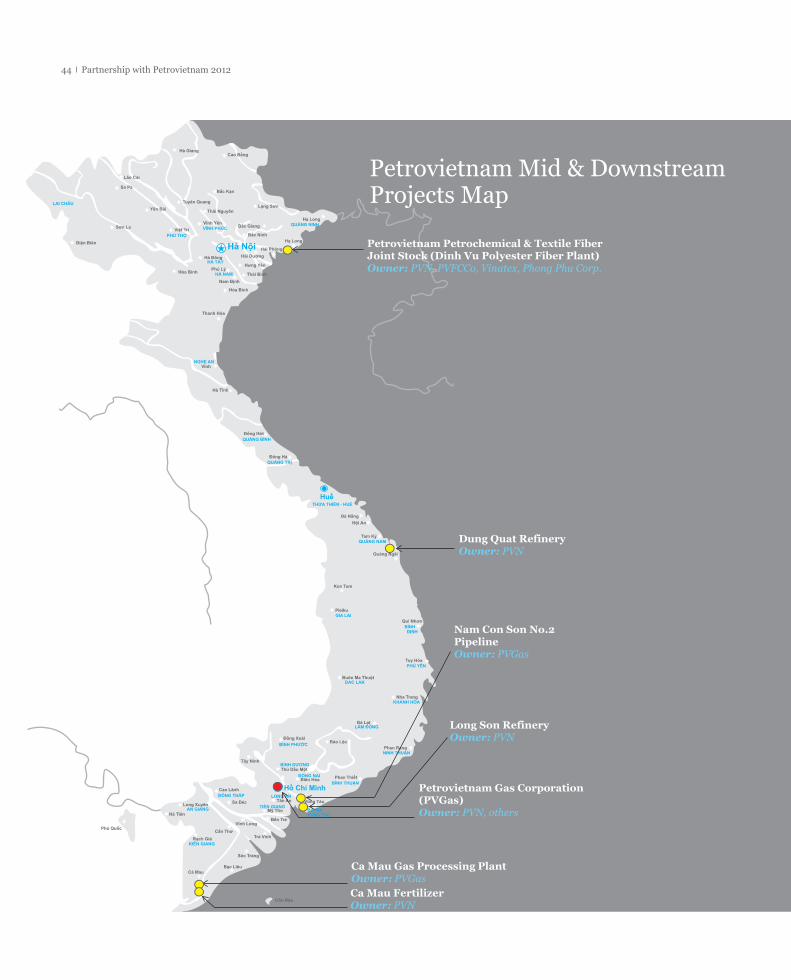

I Mid-and-Downstream 7 projects

I-1 Nam Con Son No.2 Pipelines PVGas Ba Ria - Vung Tau Province 1,300 49%

I-2 Ca Mau Gas Processing Plant PVGas Ca Mau Province 700 49%

I-3 Dung Quat Refi nery (Existing) PVN Quang Ngai Province 3,000 49%

I-4 Dung Quat Refi nery (Expansion) PVN Quang Ngai Province 1,212 49%

I-5 Long Son Refi nery PVN Ba Ria - Vung Tau Province

7,000-8,000 71%

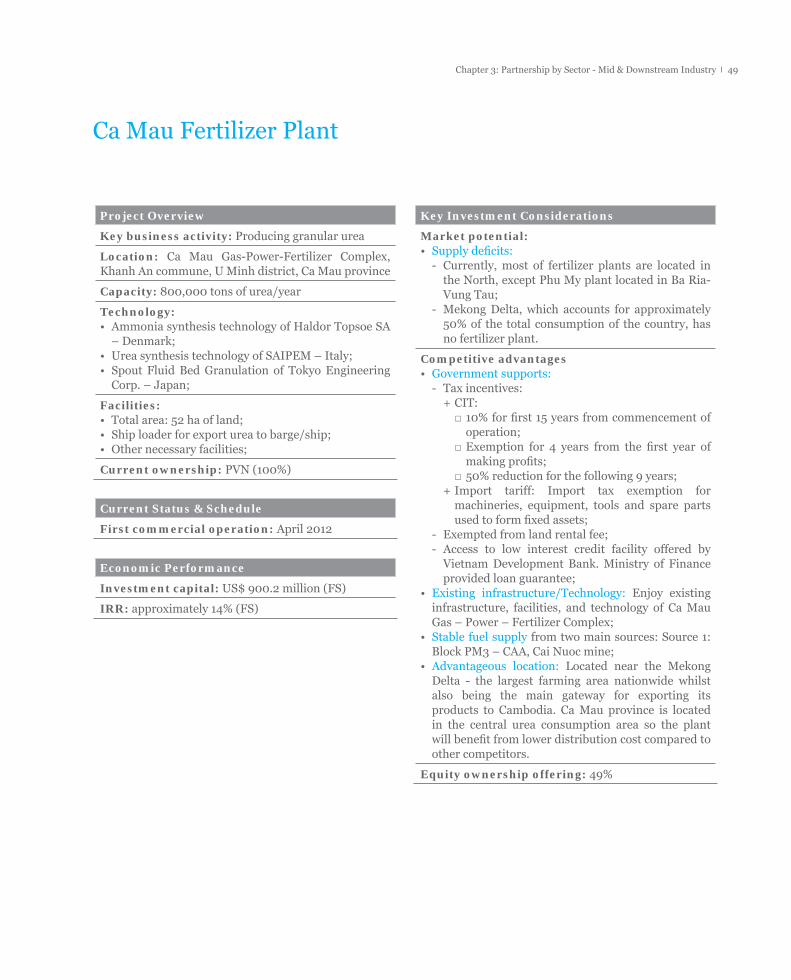

I-6 Ca Mau Fertilizer Plant PVN Ca Mau Province 900.2 49%

I-7 Petrovietnam Gas Corporation (PVGas) PVN, other investors Ho Chi Minh City 2,209 21.7%

I-8Petrovietnam Petrochemical & Textile Fiber Joint Stock Company (PVTex)

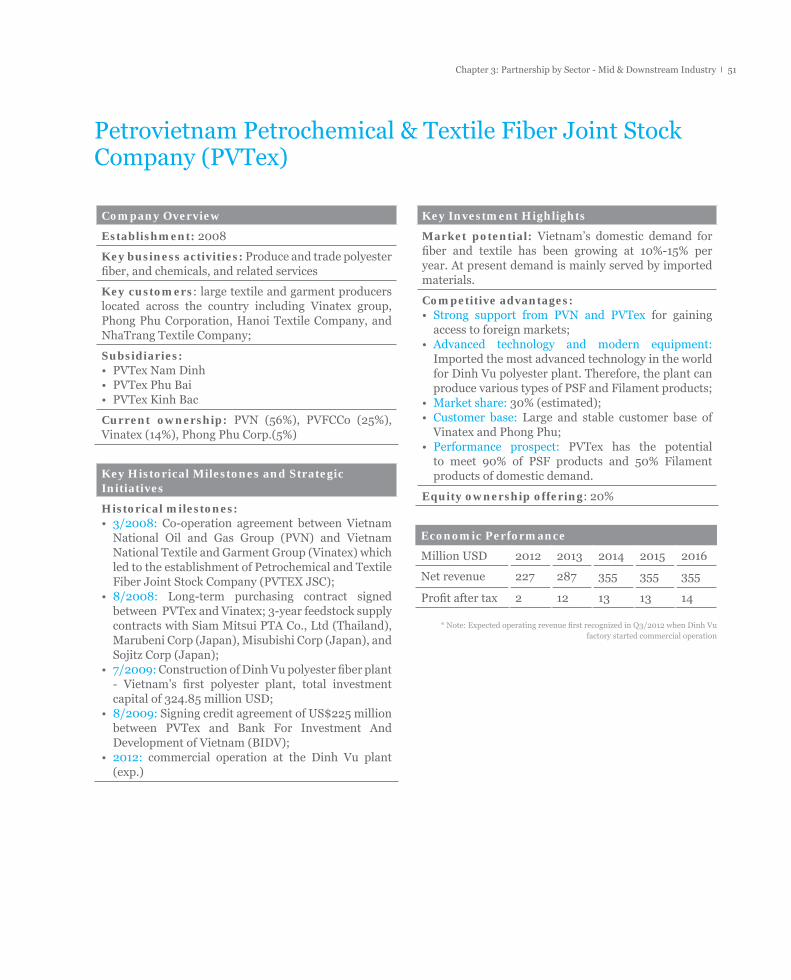

PVN, PVFCCo, Vinatex, Phong Phu Corp. Hai Phong City 324.85 20%

II Power 9 projects

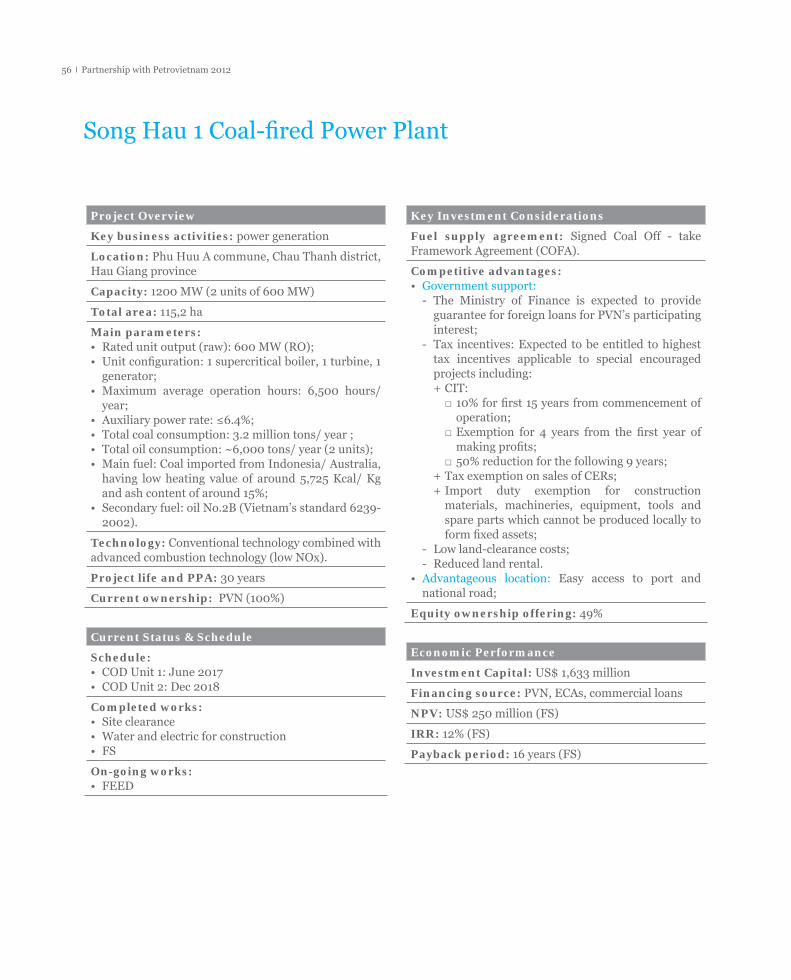

II-1 Song Hau 1 Coal-fi red Power Plant PVN Hau Giang Province 1,633 49%

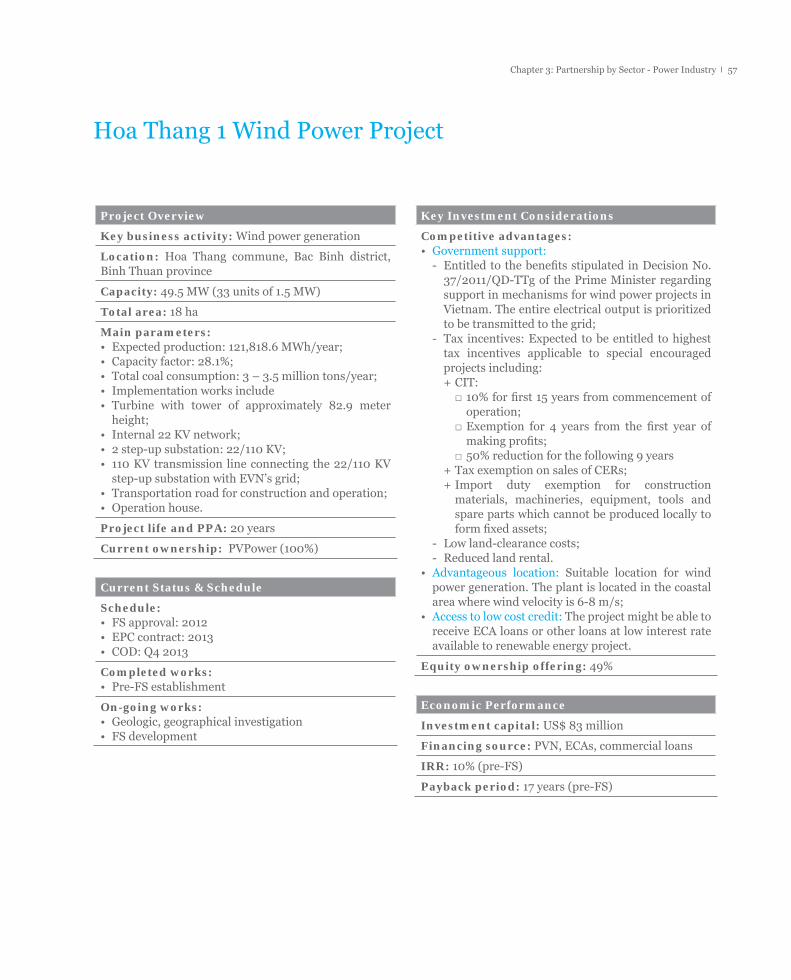

II-2 Hoa Thang 1 Wind Power Plant PVPower Binh Thuan Province 83 49%

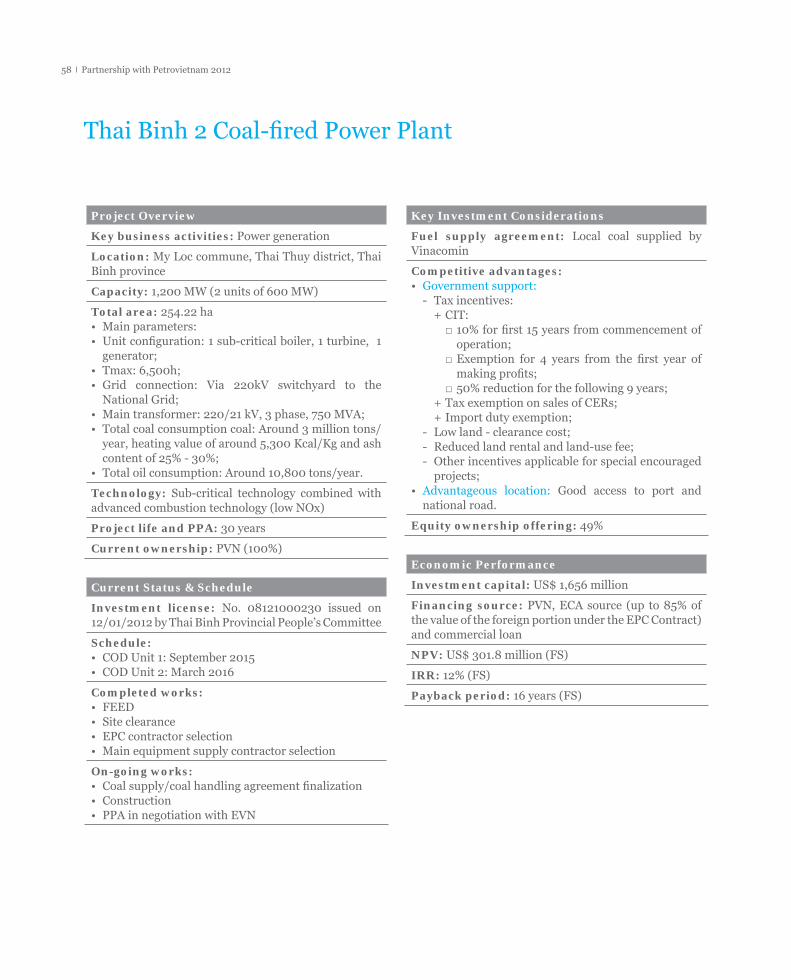

II-3 Thai Binh 2 Coal-fi red Power Plant PVN Thai Binh Province 1,656 49%

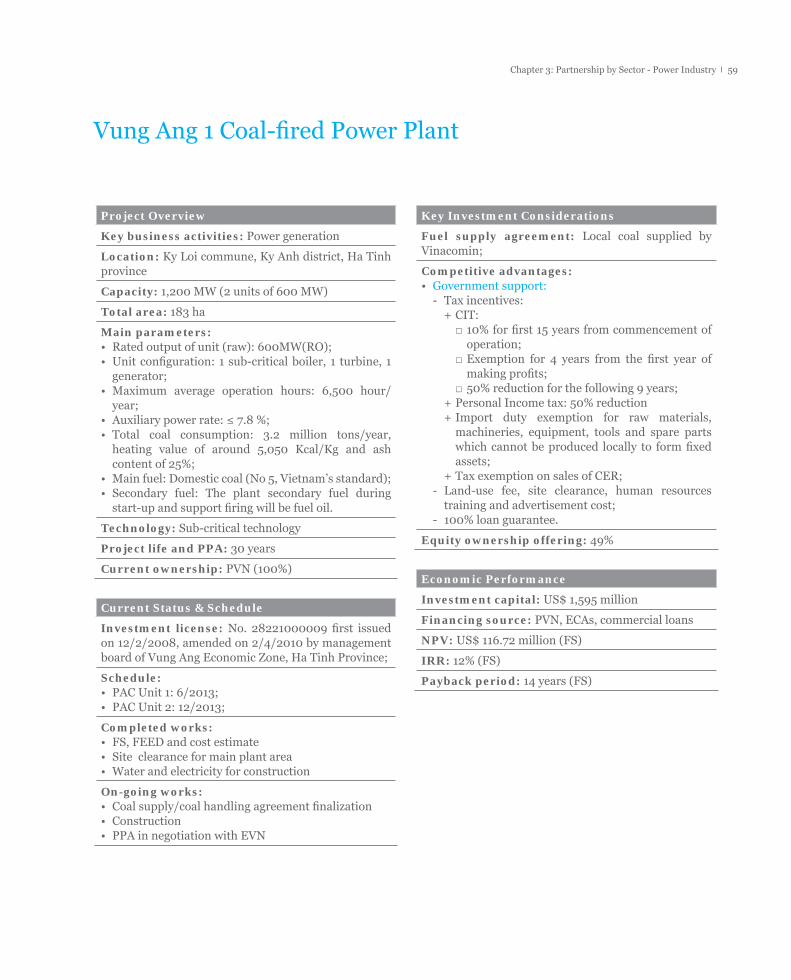

II-4 Vung Ang 1 Coal-fi red Power Plant PVN Ha Tinh Province 1,595 49%

II-5 Quang Trach 1 Coal-fi red Power Plant PVN Quang Binh Province 1,778 49%

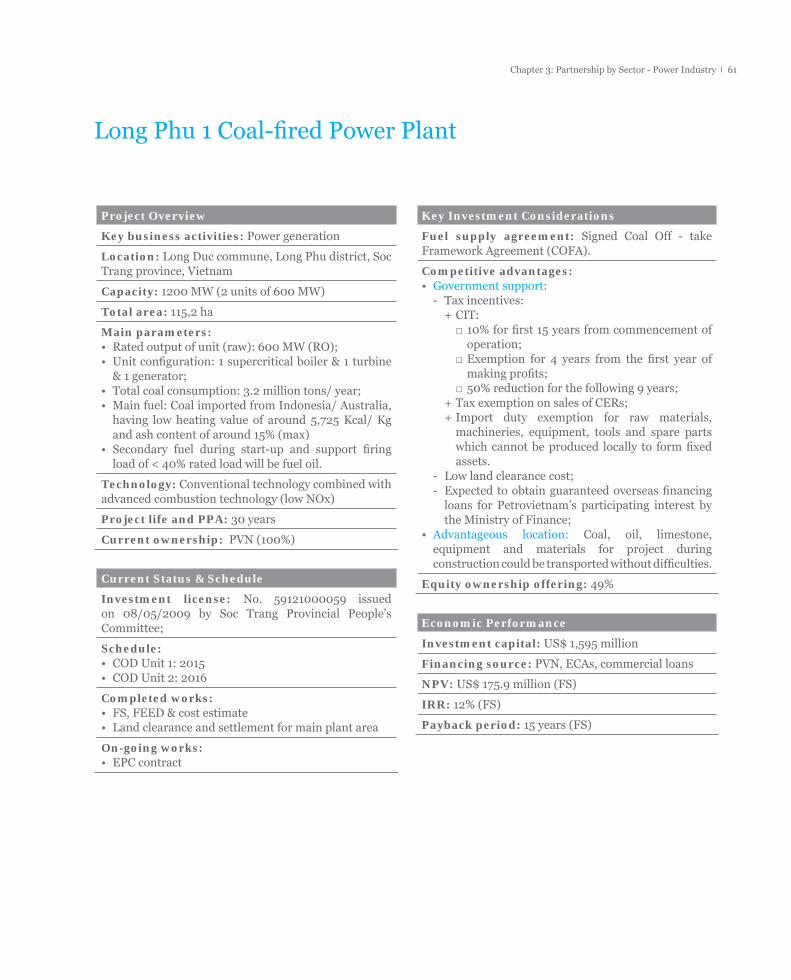

II-6 Long Phu 1 Coal-fi red Power Plant PVN Soc Trang Province 1,595 49%

II-7 DakDrinh Hydro Power PlantPV Power, BIDV, Licogi, SongDa Group, DHC’s employees

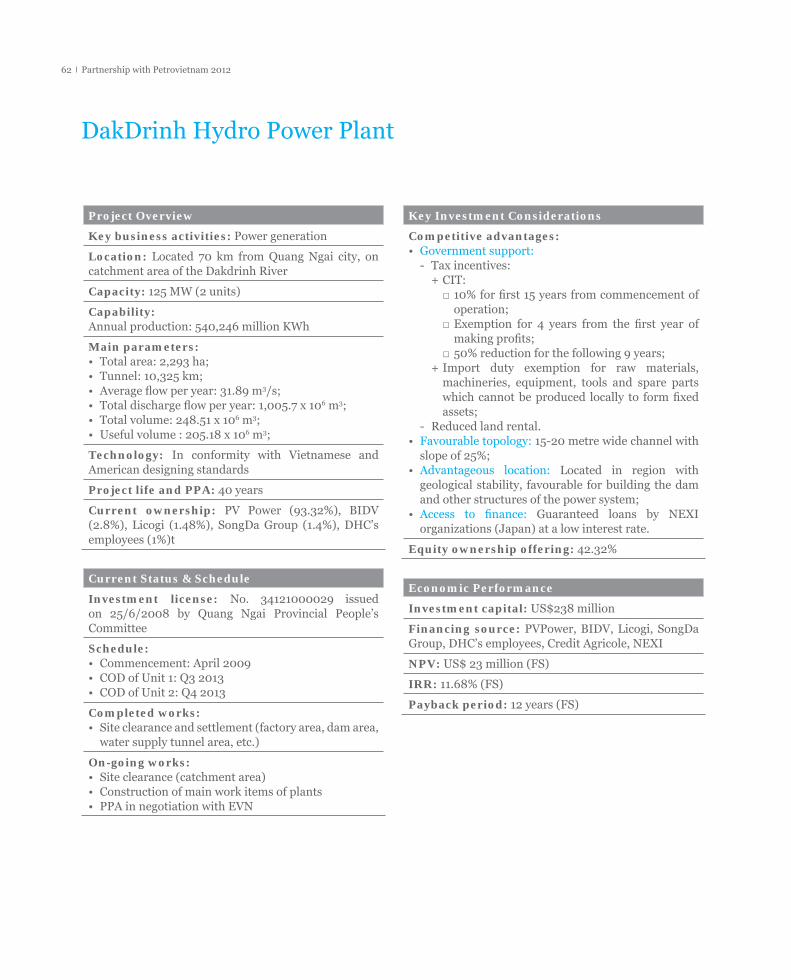

Quang Ngai Province 238 42.32%

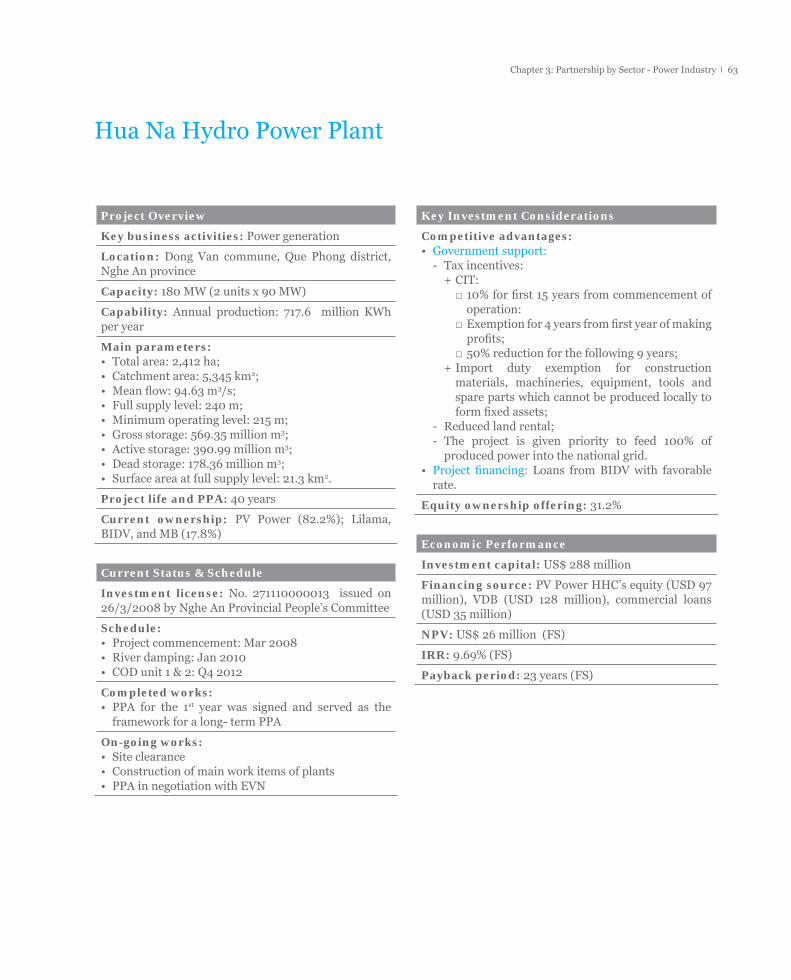

II-8 Hua Na Hydro Power Plant PV Power; Lilama, BIDV, MB Nghe An Province 288 31.2%

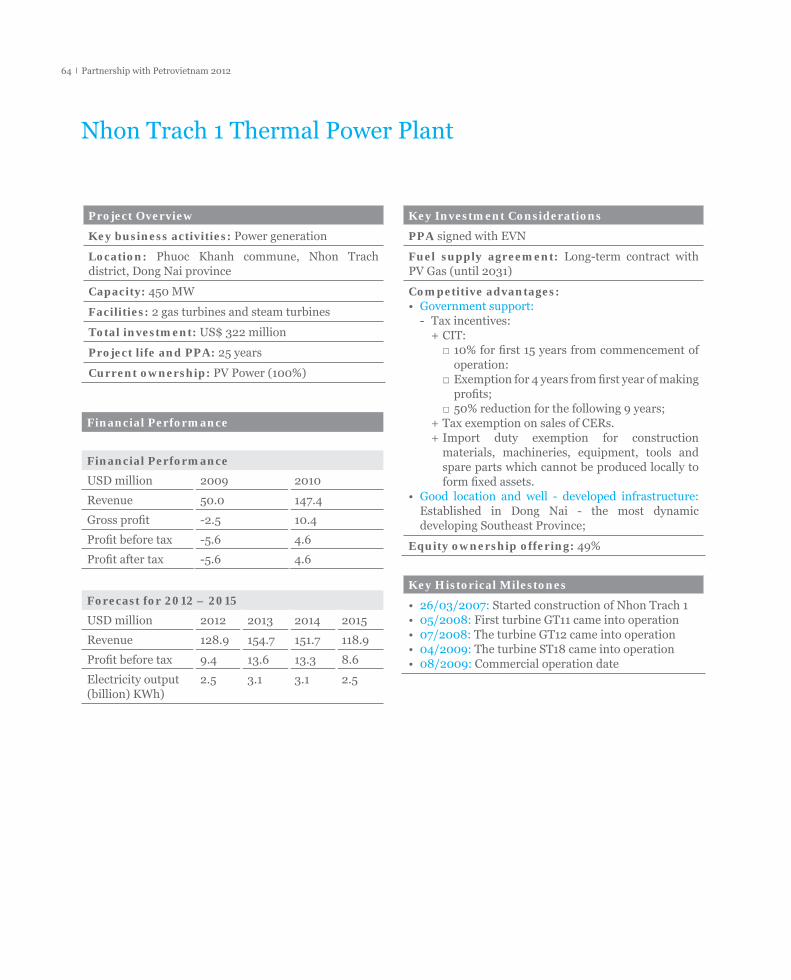

II-9 Nhon Trach 1 Thermal Power Plant PVPower Dong Nai Province 322 49%

III Services 7 projects

III-1 Phuoc An Port PVN, Sonadezi Corp Dong Nai Province 979 49%

III-2 Dung Quat Shipyard PVN Quang Ngai Province 749 49%

III-3 Petrovietnam Construction Joint Stock Company (PVC)

PVN, VanEck Association Corp., Vietwealth Corp, Others

Hanoi City 817 17%

III-4 Petrovietnam Tower PVC Hanoi City 571 49%

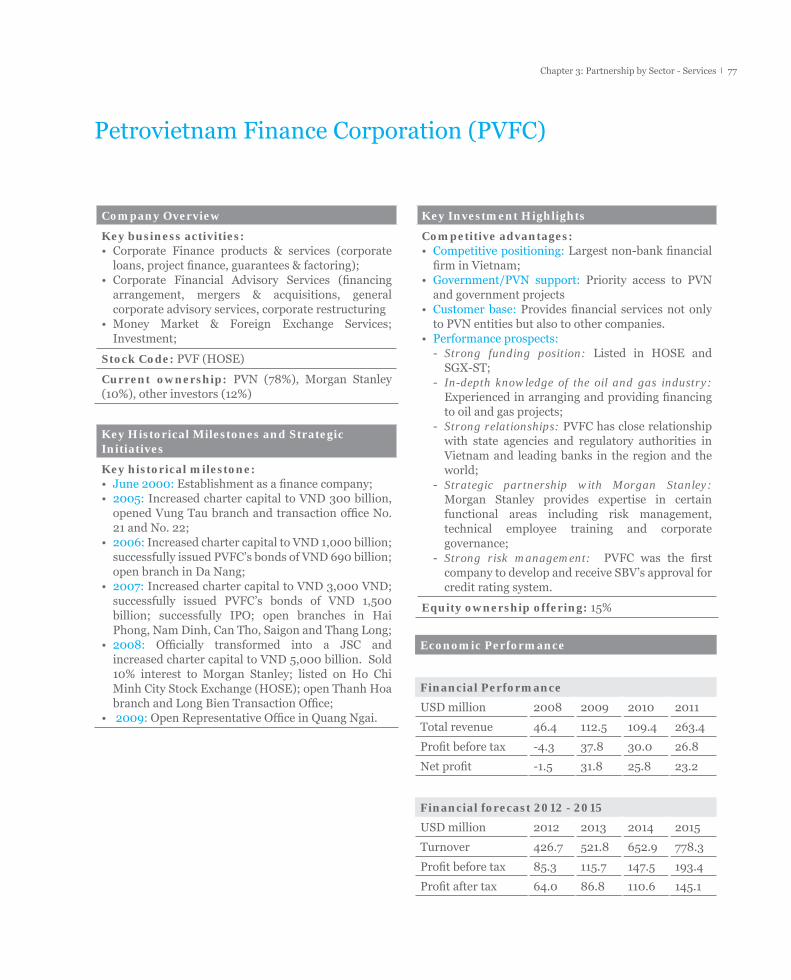

III-5 Petrovietnam Finance Corporation (PVFC)

PVN, Morgan Stanley, Others Hanoi City 4,300 15%

III-6 Petrovietnam Transportation Corporation (PVTrans)

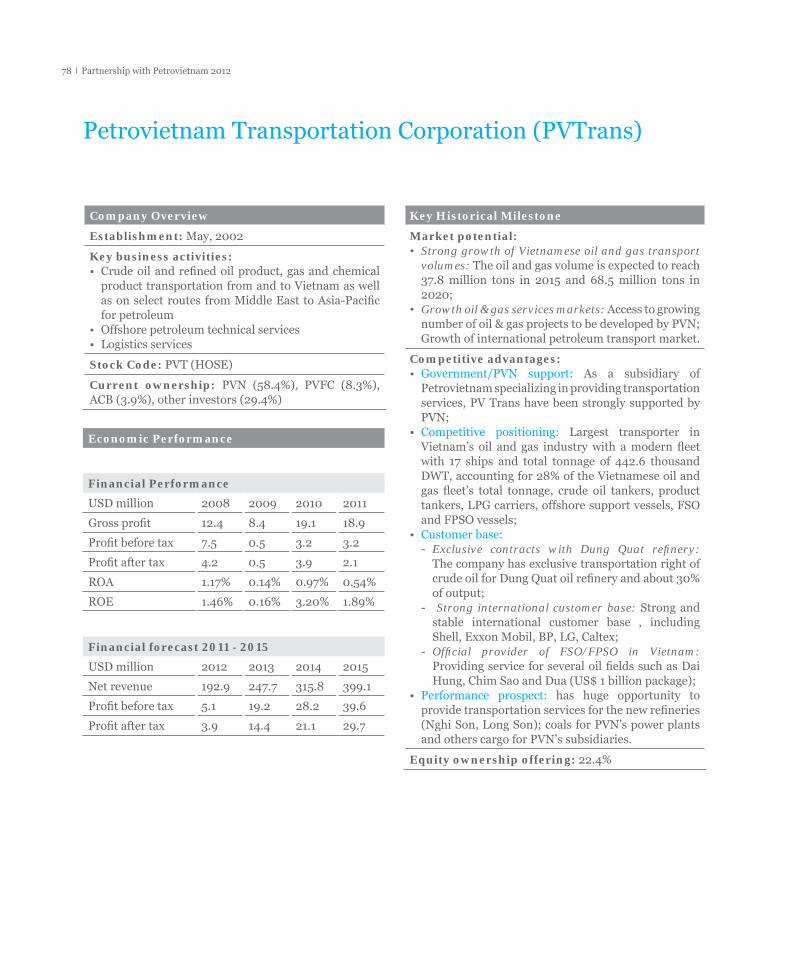

PVN, PVFC, ACB, Others Ho Chi Minh City 388 22.4%

III-7 Petrovietnam Oil Stockpile Company Limited (PVOS)

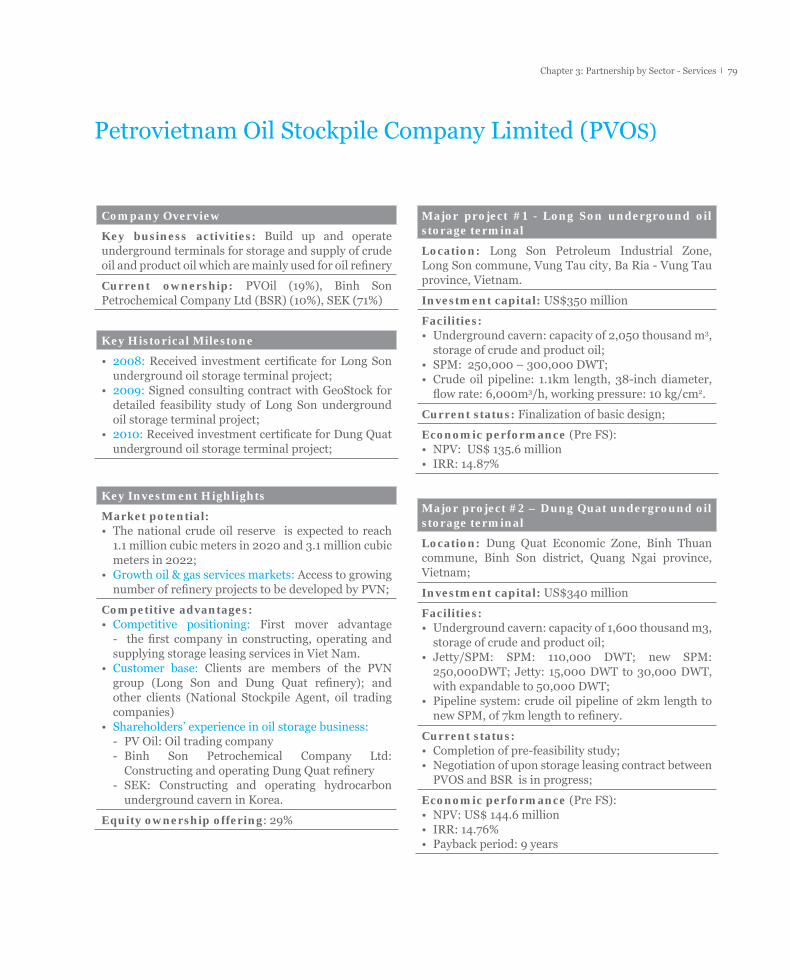

PV Oil, Binh Son Petrochemical Company Ltd (BSR) SEK

Ho Chi Minh City 2.610 29%

-----------------------------------------------------------------------------------------------------(10) Newly set-up company

21Chapter 3: Partnership by Sector

Chapter 3: Partnership by Sector

1. Upstream Industry

2. Mid & Downstream Industry

3. Power Industry

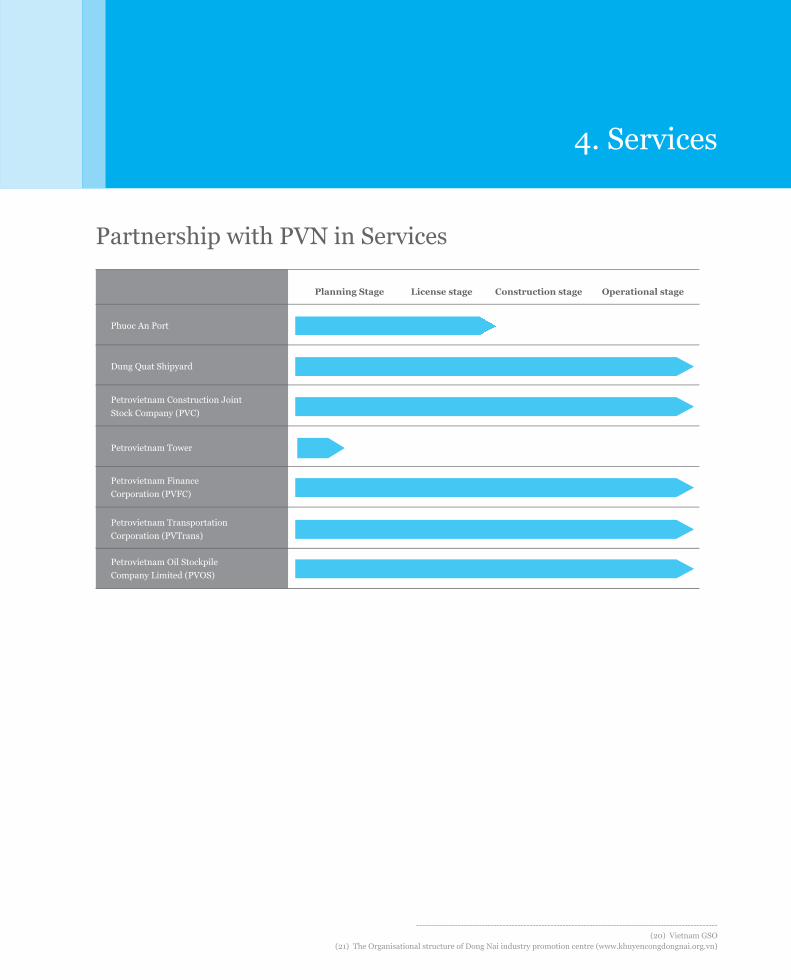

4. Services

Partnership with Petrovietnam 201222

Upstream Industry Overview

1. Upstream Industry

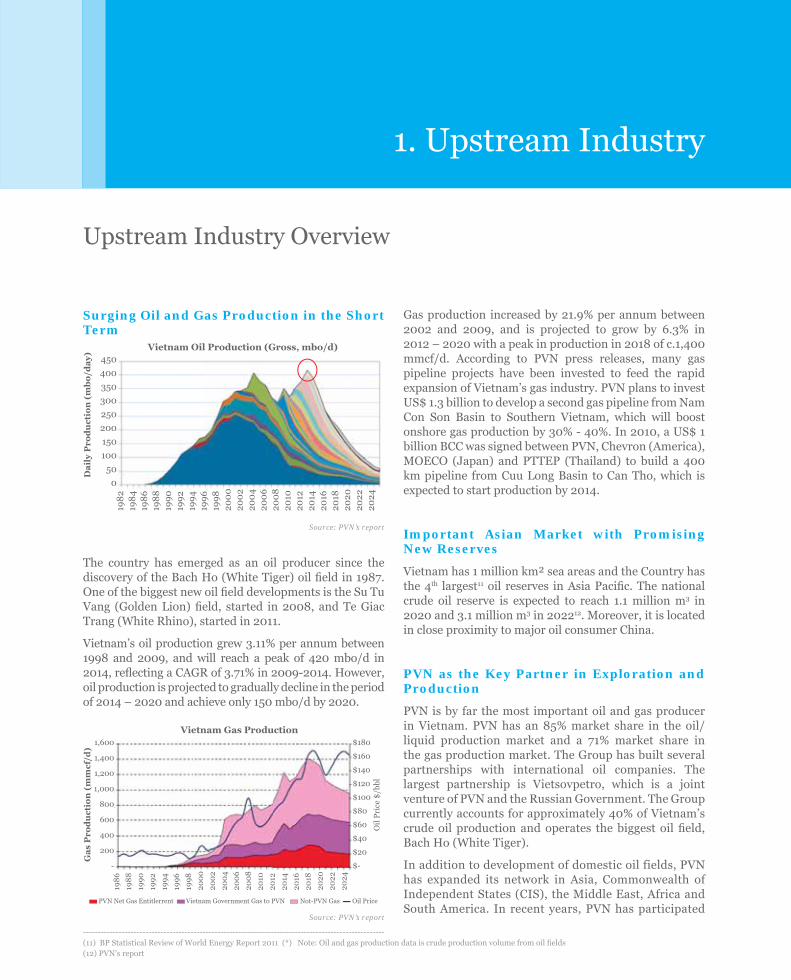

Surging Oil and Gas Production in the Short Term

Vietnam Oil Production (Gross, mbo/d)

198

219

84

198

619

88

199

019

92

199

419

96

199

820

00

200

220

04

200

620

08

2010

2012

2014

2016

2018

2020

2022

2024

450

400

350

300

250

200

150

100

50

0

Da

ily

Pro

du

ctio

n (

mb

o/d

ay)

Source: PVN’s report

The country has emerged as an oil producer since the discovery of the Bach Ho (White Tiger) oil fi eld in 1987. One of the biggest new oil fi eld developments is the Su Tu Vang (Golden Lion) fi eld, started in 2008, and Te Giac Trang (White Rhino), started in 2011.

Vietnam’s oil production grew 3.11% per annum between 1998 and 2009, and will reach a peak of 420 mbo/d in 2014, refl ecting a CAGR of 3.71% in 2009-2014. However, oil production is projected to gradually decline in the period of 2014 – 2020 and achieve only 150 mbo/d by 2020.

Vietnam Gas Production

Ga

s P

rod

uct

ion

(m

mcf

/d)

1,600

1,400

1,200

1,000

800

600

400

200

-

$180

$160

$140

$120

$100

$80

$60

$40

$20

$-

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

2010

2012

2014

2016

2018

2020

2022

2024

Oil

Pri

ce $

/bbl

PVN Net Gas Entitlerrent Vietnam Government Gas to PVN Not-PVN Gas Oil Price

Source: PVN’s report

Gas production increased by 21.9% per annum between 2002 and 2009, and is projected to grow by 6.3% in 2012 – 2020 with a peak in production in 2018 of c.1,400 mmcf/d. According to PVN press releases, many gas pipeline projects have been invested to feed the rapid expansion of Vietnam’s gas industry. PVN plans to invest US$ 1.3 billion to develop a second gas pipeline from Nam Con Son Basin to Southern Vietnam, which will boost onshore gas production by 30% - 40%. In 2010, a US$ 1 billion BCC was signed between PVN, Chevron (America), MOECO (Japan) and PTTEP (Thailand) to build a 400 km pipeline from Cuu Long Basin to Can Tho, which is expected to start production by 2014.

Important Asian Market with Promising New Reserves

Vietnam has 1 million km² sea areas and the Country has the 4th largest11 oil reserves in Asia Pacifi c. The national crude oil reserve is expected to reach 1.1 million m3 in 2020 and 3.1 million m3 in 202212. Moreover, it is located in close proximity to major oil consumer China.

PVN as the Key Partner in Exploration and Production

PVN is by far the most important oil and gas producer in Vietnam. PVN has an 85% market share in the oil/liquid production market and a 71% market share in the gas production market. The Group has built several partnerships with international oil companies. The largest partnership is Vietsovpetro, which is a joint venture of PVN and the Russian Government. The Group currently accounts for approximately 40% of Vietnam’s crude oil production and operates the biggest oil fi eld, Bach Ho (White Tiger).

In addition to development of domestic oil fields, PVN has expanded its network in Asia, Commonwealth of Independent States (CIS), the Middle East, Africa and South America. In recent years, PVN has participated

-----------------------------------------------------------------------------------------------------(11) BP Statistical Review of World Energy Report 2011 (*) Note: Oil and gas production data is crude production volume from oil fi elds(12) PVN’s report

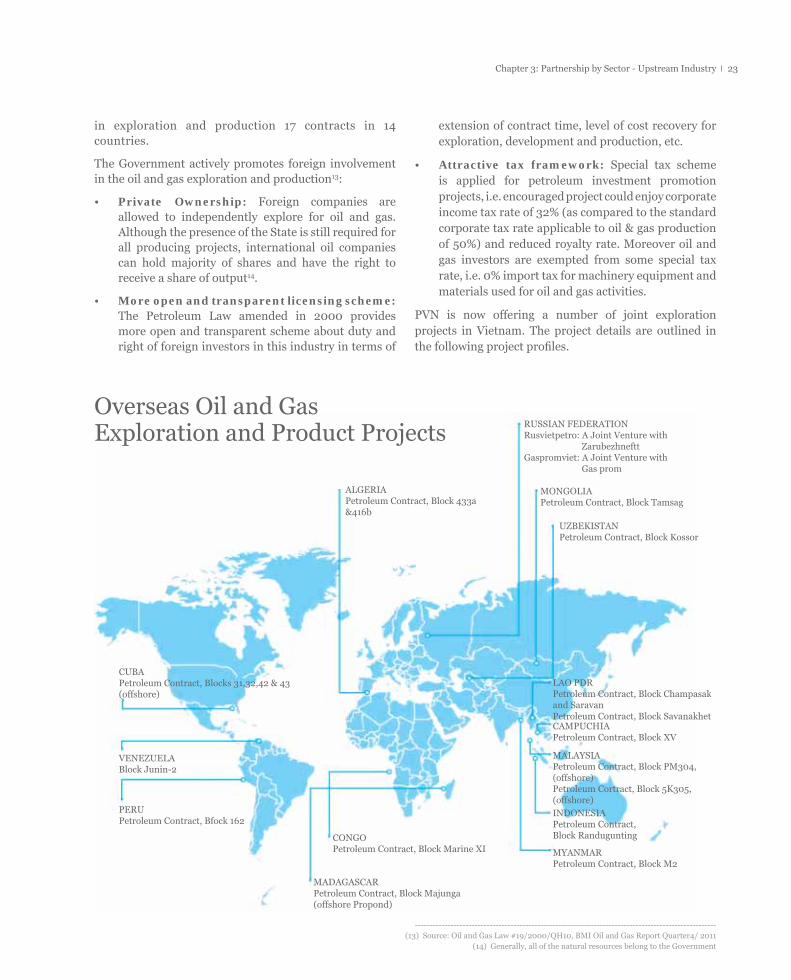

23Chapter 3: Partnership by Sector - Upstream Industry

in exploration and production 17 contracts in 14 countries.

The Government actively promotes foreign involvement in the oil and gas exploration and production13:

• Private Ownership: Foreign companies are allowed to independently explore for oil and gas. Although the presence of the State is still required for all producing projects, international oil companies can hold majority of shares and have the right to receive a share of output14.

• More open and transparent licensing scheme: The Petroleum Law amended in 2000 provides more open and transparent scheme about duty and right of foreign investors in this industry in terms of

extension of contract time, level of cost recovery for exploration, development and production, etc.

• Attractive tax framework: Special tax scheme is applied for petroleum investment promotion projects, i.e. encouraged project could enjoy corporate income tax rate of 32% (as compared to the standard corporate tax rate applicable to oil & gas production of 50%) and reduced royalty rate. Moreover oil and gas investors are exempted from some special tax rate, i.e. 0% import tax for machinery equipment and materials used for oil and gas activities.

PVN is now offering a number of joint exploration projects in Vietnam. The project details are outlined in the following project profi les.

ALGERIAPetroleum Contract, Block 433a&416b

CONGOPetroleum Contract, Block Marine XI

MADAGASCARPetroleum Contract, Block Majunga(offshore Propond)

CUBAPetroleum Contract, Blocks 31,32,42 & 43(offshore)

VENEZUELABlock Junin-2

PERUPetroleum Contract, Bfock 162

RUSSIAN FEDERATIONRusvietpetro: A Joint Venture with ZarubezhnefttGaspromviet: A Joint Venture with Gas prom

MONGOLIAPetroleum Contract, Block Tamsag

UZBEKISTANPetroleum Contract, Block Kossor

LAO PDRPetroleum Contract, Block Champasakand SaravanPetroleum Contract, Block SavanakhetCAMPUCHIAPetroleum Contract, Block XV

MALAYSIAPetroleum Contract, Block PM304,(offshore)Petroleum Cortract, Block 5K305,(offshore)INDONESIAPetroleum Contract,Block Randugunting

MYANMARPetroleum Contract, Block M2

Overseas Oil and Gas Exploration and Product Projects

-----------------------------------------------------------------------------------------------------(13) Source: Oil and Gas Law #19/2000/QH10, BMI Oil and Gas Report Quarter4/ 2011

(14) Generally, all of the natural resources belong to the Government

Partnership with Petrovietnam 201224

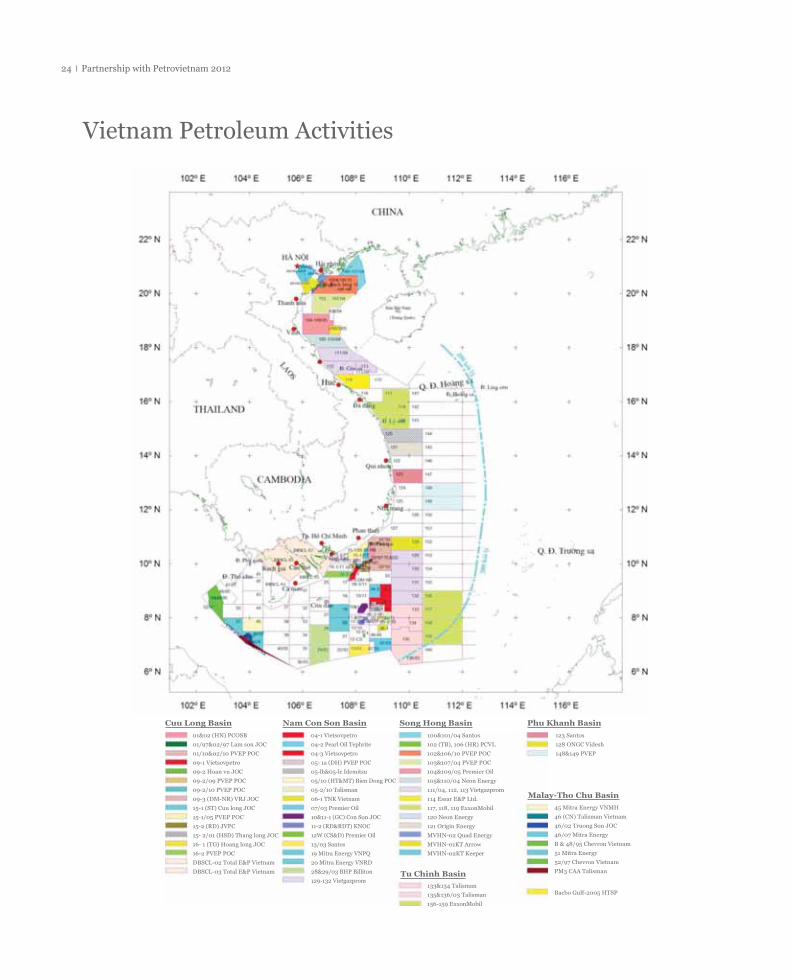

Cuu Long Basin Nam Con Son Basin Song Hong Basin Phu Khanh Basin

Malay-Tho Chu Basin

Tu Chinh Basin

01&02 (HN) PCOSB

01/97&02/97 Lam son JOC

01/10&02/10 PVEP POC

09-1 Vietsovpetro

09-2 Hoan vu JOC

09-2/09 PVEP POC

09-2/10 PVEP POC

09-3 (DM-NR) VRJ JOC

15-1 (ST) Cuu long JOC

15-1/05 PVEP POC

15-2 (RD) JVPC

15- 2/01 (HSD) Thang long JOC

16- 1 (TG) Hoang long JOC

16-2 PVEP POC

DBSCL-02 Total E&P Vietnam

DBSCL-03 Total E&P Vietnam

100&101/04 Santos

102 (TB), 106 (HR) PCVL

102&106/10 PVEP POC

103&107/04 PVEP POC

104&109/05 Premier Oil

105&110/04 Neon Energy

111/04, 112, 113 Vietgazprom

114 Essar E&P Ltd.

117, 118, 119 ExxonMobil

120 Neon Energy

121 Origin Energy

MVHN-02 Quad Energy

MVHN-01KT Arrow

MVHN-02KT Keeper

123 Santos

128 ONGC Videsh

148&149 PVEP

45 Mitra Energy VNMH

46 (CN) Talisman Vietnam

46/02 Truong Son JOC

46/07 Mitra Energy

B & 48/95 Chevron Vietnam

51 Mitra Energy

52/97 Chevron Vietnam

PM3 CAA Talisman

Bacbo Gulf-2005 HTSP133&134 Talisman

135&136/03 Talisman

156-159 ExxonMobil

04-1 Vietsovpetro

04-2 Pearl Oil Tephrite

04-3 Vietsovpetro

05- 1a (DH) PVEP POC

05-lb&05-lc Idemitsu

05/10 (HT&MT) Bien Dong POC

05-2/10 Talisman

06-1 TNK Vietnam

07/03 Premier Oil

10&11-1 (GC) Con Son JOC

11-2 (RD&RDT) KNOC

12W (CS&D) Premier Oil

13/03 Santos

19 Mitra Energy VNPQ

20 Mitra Energy VNRD

28&29/03 BHP Billiton

129-132 Vietgazprom

Vietnam Petroleum Activities

25Chapter 3: Partnership by Sector - Upstream Industry

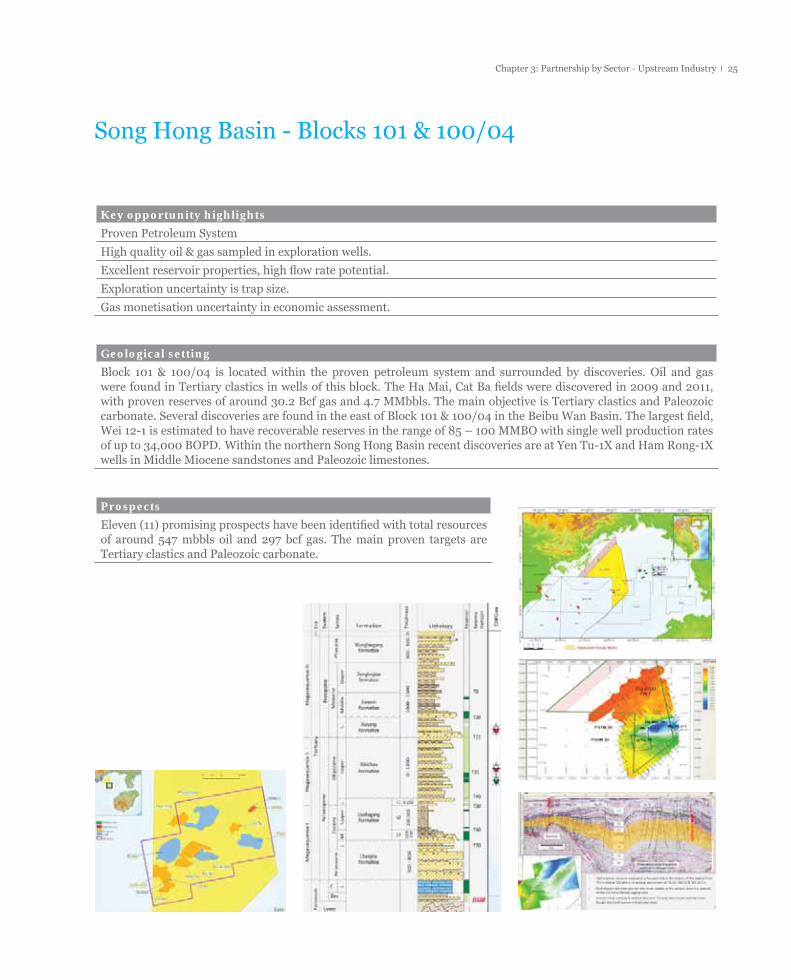

Song Hong Basin - Blocks 101 & 100/04

Key opportunity highlights

Proven Petroleum System

High quality oil & gas sampled in exploration wells.

Excellent reservoir properties, high fl ow rate potential.

Exploration uncertainty is trap size.

Gas monetisation uncertainty in economic assessment.

Geological setting

Block 101 & 100/04 is located within the proven petroleum system and surrounded by discoveries. Oil and gas were found in Tertiary clastics in wells of this block. The Ha Mai, Cat Ba fi elds were discovered in 2009 and 2011, with proven reserves of around 30.2 Bcf gas and 4.7 MMbbls. The main objective is Tertiary clastics and Paleozoic carbonate. Several discoveries are found in the east of Block 101 & 100/04 in the Beibu Wan Basin. The largest fi eld, Wei 12-1 is estimated to have recoverable reserves in the range of 85 – 100 MMBO with single well production rates of up to 34,000 BOPD. Within the northern Song Hong Basin recent discoveries are at Yen Tu-1X and Ham Rong-1X wells in Middle Miocene sandstones and Paleozoic limestones.

Prospects

Eleven (11) promising prospects have been identifi ed with total resources of around 547 mbbls oil and 297 bcf gas. The main proven targets are Tertiary clastics and Paleozoic carbonate.

Partnership with Petrovietnam 201226

Song Hong Basin - Blocks 108/04, 116

Geological setting

The Tertiary sedimentary Song Hong Basin is made up of different structural units with different hydrocarbon potential.

Block 108/04 lies in the Central Trough of the Song Hong Basin, which is fi lled up with a sediment package accumulated in tectonically stable conditions.

Block 116 lies in the Quang Ngai graben where Tertiary sediment comprised of Eocene to present day sediment with a thickness of appx. 9,000 m. Quang Ngai graben is a relatively simple geological structure (a narrow deep sag) dominated by Miocene submarine sand bodies of high reservoir quality. This graben is one of the major kitchens in the Southern part of Song Hong Basin.

Petroleum systemsProven petroleum basin containing oil discoveries (10 oil and gas discovery wells)

Source rock

Oil and gas-prone Paleogen-Lower Miocene lacustrine shales in Quang Ngai graben and the centre of Song Hong Basin. Probably Middle Miocene marine mudstone in the center of the Song Hong Basin.

ReservoirMiocene clastic turbidite fans; Lower Miocene sandstone; Pre-Tertiary basement.

SealLocal seal in Lower Miocene shales; Regional seal in Miocene-Pliocene shales.

Trap

Major prospects for low magnitude four way dip closure on the Dong Son uplift in the block 108/04 related to gas accumulation.

Pre-Tertiary basement highs, drape over basement, stratigraphic traps (block 116).

27Chapter 3: Partnership by Sector - Upstream Industry

Song Hong Basin - Blocks 108/04, 116

Block 108/04

Area: 1,210 km2

Location: Offshore North Vietnam

Sea level: 20-50 m

Seismic: 460 line-km 2D

Well: No well

Block 108/04 is thought to have commercial hydrocarbon potential. There are many oil and gas discoveries found in adjacent areas such as Ham Rong, Yen Tu, Hac Long and Dong Fang

Block 116

Area: 5,033 km2

Location: Offshore North Vietnam

Sea level: 20-110 m

Seismic: 3619.3 line-km 2D

Well: No well

Block 116 is thought to have hydrocarbon potential. Oil and gas discoveries are found in neighbouring blocks 114, 115, 117 and 118.

Partnership with Petrovietnam 201228

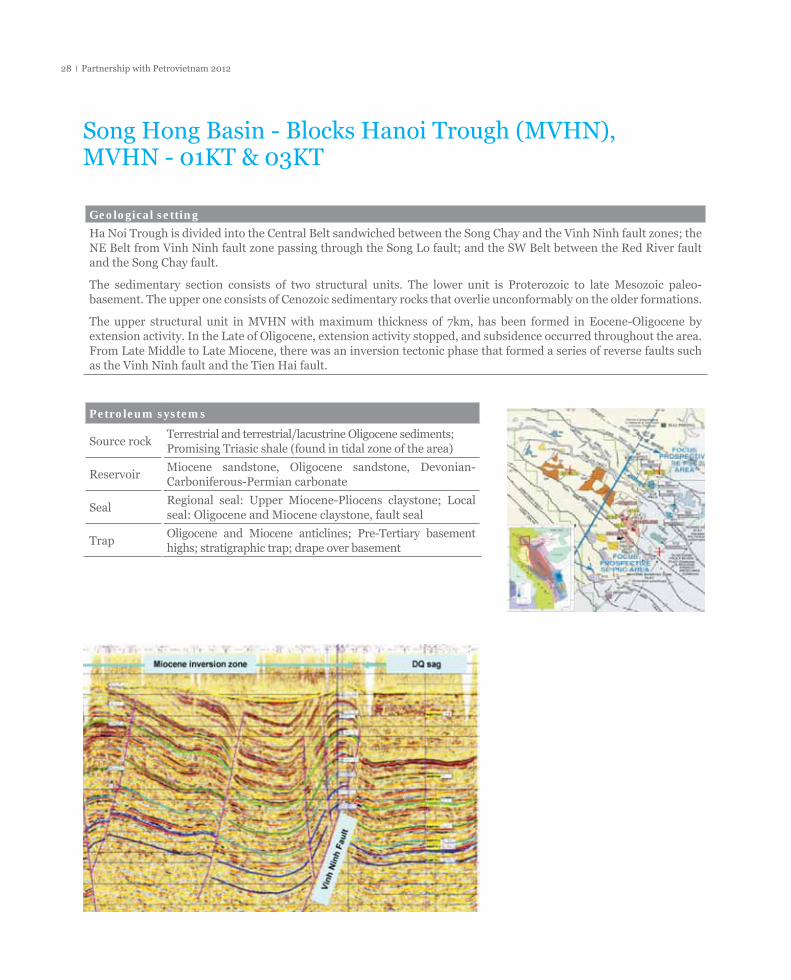

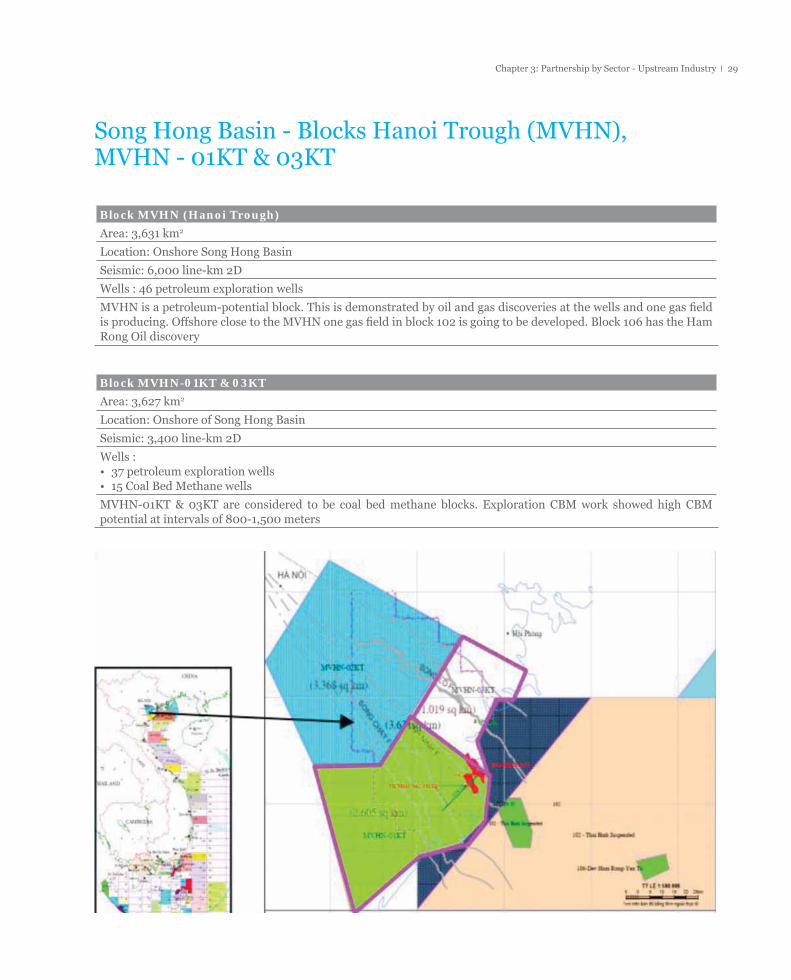

Song Hong Basin - Blocks Hanoi Trough (MVHN), MVHN - 01KT & 03KT

Geological setting

Ha Noi Trough is divided into the Central Belt sandwiched between the Song Chay and the Vinh Ninh fault zones; the NE Belt from Vinh Ninh fault zone passing through the Song Lo fault; and the SW Belt between the Red River fault and the Song Chay fault.

The sedimentary section consists of two structural units. The lower unit is Proterozoic to late Mesozoic paleo-basement. The upper one consists of Cenozoic sedimentary rocks that overlie unconformably on the older formations.

The upper structural unit in MVHN with maximum thickness of 7km, has been formed in Eocene-Oligocene by extension activity. In the Late of Oligocene, extension activity stopped, and subsidence occurred throughout the area. From Late Middle to Late Miocene, there was an inversion tectonic phase that formed a series of reverse faults such as the Vinh Ninh fault and the Tien Hai fault.

Petroleum systems

Source rockTerrestrial and terrestrial/lacustrine Oligocene sediments; Promising Triasic shale (found in tidal zone of the area)

ReservoirMiocene sandstone, Oligocene sandstone, Devonian-Carboniferous-Permian carbonate

SealRegional seal: Upper Miocene-Pliocens claystone; Local seal: Oligocene and Miocene claystone, fault seal

TrapOligocene and Miocene anticlines; Pre-Tertiary basement highs; stratigraphic trap; drape over basement

29Chapter 3: Partnership by Sector - Upstream Industry

Song Hong Basin - Blocks Hanoi Trough (MVHN), MVHN - 01KT & 03KT

Block MVHN (Hanoi Trough)

Area: 3,631 km2

Location: Onshore Song Hong Basin

Seismic: 6,000 line-km 2D

Wells : 46 petroleum exploration wells

MVHN is a petroleum-potential block. This is demonstrated by oil and gas discoveries at the wells and one gas fi eld is producing. Offshore close to the MVHN one gas fi eld in block 102 is going to be developed. Block 106 has the Ham Rong Oil discovery

Block MVHN-01KT & 03KT

Area: 3,627 km2

Location: Onshore of Song Hong Basin

Seismic: 3,400 line-km 2D

Wells : • 37 petroleum exploration wells • 15 Coal Bed Methane wells

MVHN-01KT & 03KT are considered to be coal bed methane blocks. Exploration CBM work showed high CBM potential at intervals of 800-1,500 meters

Partnership with Petrovietnam 201230

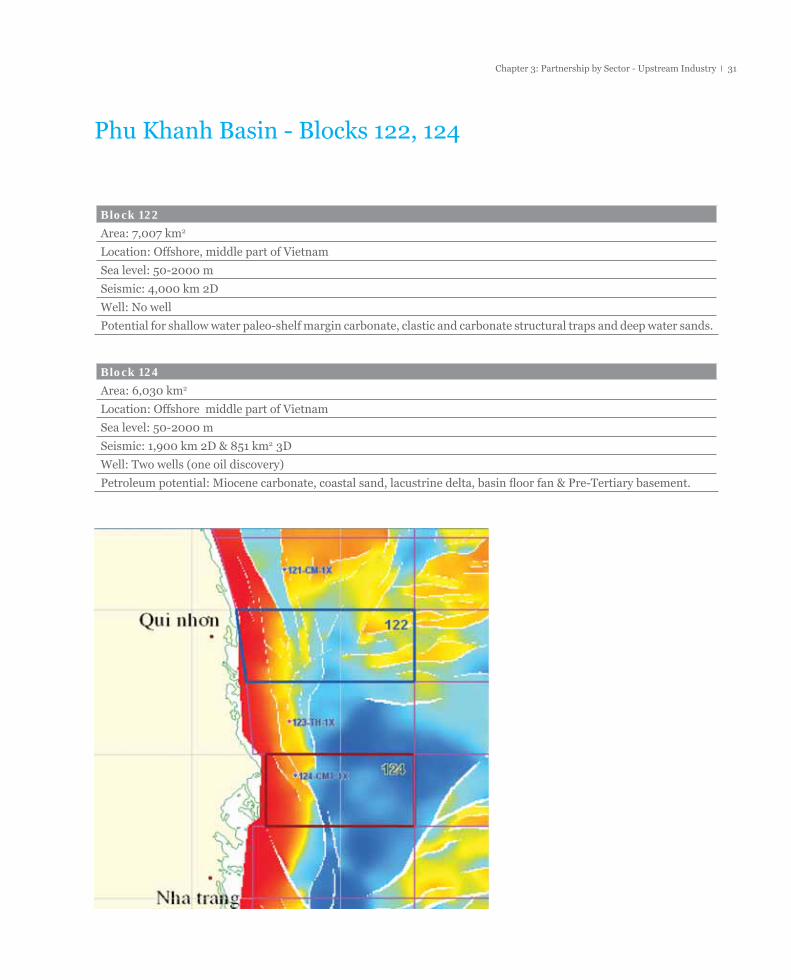

Phu Khanh Basin - Blocks 122, 124

Geological setting

The Tertiary sedimentary Phu Khanh Basin is related to the development of the Bien Dong Sea, extrusion of Indochina (L. Eocene – E. Oligocene), and associated with sea fl oor spreading (Top Oligocene), end of rifting and sea fl oor spreading (Top Middle Miocene) and thermal subsidence.

Petroleum systemsProven petroleum basin containing oil discoveries

Source rockLacustrine sediments deposited in graben and half-graben lakes during the main rifting phase.

ReservoirPaleogene fl uvial sandstones; Neogene turbidite-, shelf-, lowstand delta- and coastal sandstones; Early Miocene platform and reef carbonates; Pre-Tertiary basement.

SealLocal seal: interbedded shales;Regional seal: Late Miocene & Pliocene shales.

TrapFaulted basement highs; drape clastics on basement high/ tilted fault blocks; fl ower structures; carbonate platform.

Hydrocarbon Occurrence

Oil discovery and gas shows in two exploration wells and one oil seepage in Dam Thi Nai area.

31Chapter 3: Partnership by Sector - Upstream Industry

Phu Khanh Basin - Blocks 122, 124

Block 122

Area: 7,007 km2

Location: Offshore, middle part of Vietnam

Sea level: 50-2000 m

Seismic: 4,000 km 2D

Well: No well

Potential for shallow water paleo-shelf margin carbonate, clastic and carbonate structural traps and deep water sands.

Block 124

Area: 6,030 km2

Location: Offshore middle part of Vietnam

Sea level: 50-2000 m

Seismic: 1,900 km 2D & 851 km2 3D

Well: Two wells (one oil discovery)

Petroleum potential: Miocene carbonate, coastal sand, lacustrine delta, basin fl oor fan & Pre-Tertiary basement.

Partnership with Petrovietnam 201232

Onshore Mekong Delta (DBSCL) - Blocks DBSCL-01,02,03&04

Geological setting

Mekong delta comprises a Permian and Triassic Basin in the Northwest and Tertiary sedimentary basin in the Southeast and is related to the two rifting phases in Permian and Early Oligocene.

An extension and drifting phase until the end of the Permian period, with consequent compressive phenomena affecting the Khorat Basin in Thailand.

Shrinking and/or Collision phase between early Triassic to Jurassic, at fi rst in the northeast with the South-China block along Song Ma suture line; then to the west along the Nan Uttaradit and Bengtong Raub suture lines.

Petroleum systems in the Mekong delta are referred to adjacent basins

Khorat Basin:

Source rockPermian/Triassic fl uvial-lacustrine shale; Main gas potential

ReservoirWeathering granites basement, fractured dolomites/limestone Permian; fl uvial sandstone Triassic/Jurassic

Seal Interbeded Permian, Triassic and early Jurassic shales

TrapClastics drape on paleo highs, titled fault blocks, carbonate platform, inversion folding

Cuu Long Basin:

Source rock Lacustrine Oligocene shale

Reservoir Oligo-Miocene clastics, fractured granites basement

Seal Olio-Miocene Interbeded shales

Trap Faulted basement highs, drape clastics, titled fault blocks

33Chapter 3: Partnership by Sector - Upstream Industry

Onshore Mekong Delta (DBSCL) - Blocks DBSCL-01,02,03&04

DBSCL02 and 03 are close to the Khorat Basin which has prolifi c hydrocarbon potential in Pre-tertiary fractured carbonate reservoirs

DBSCL01 is close to the Cuu Long basin, which has prolifi c hydrocarbon potential in Tertiary clastics and basement reservoirs

DBSCL01, 02, 03 & 04 are potential but frontier and regarded as attractive areas for exploration

Block DBSCL-01,02,03&04

Area: 54,500 km2

Location: Onshore Mekong Delta, South of Vietnam

Seismic: 1,317 km (2D) • DBSCL-01: 717 km seismic 2D• DBSCL-02: 300km seismic 2D• DBSCL-03: 300 km seismic 2D• DBSCL-04: No seismic data

Well: six wells

Partnership with Petrovietnam 201234

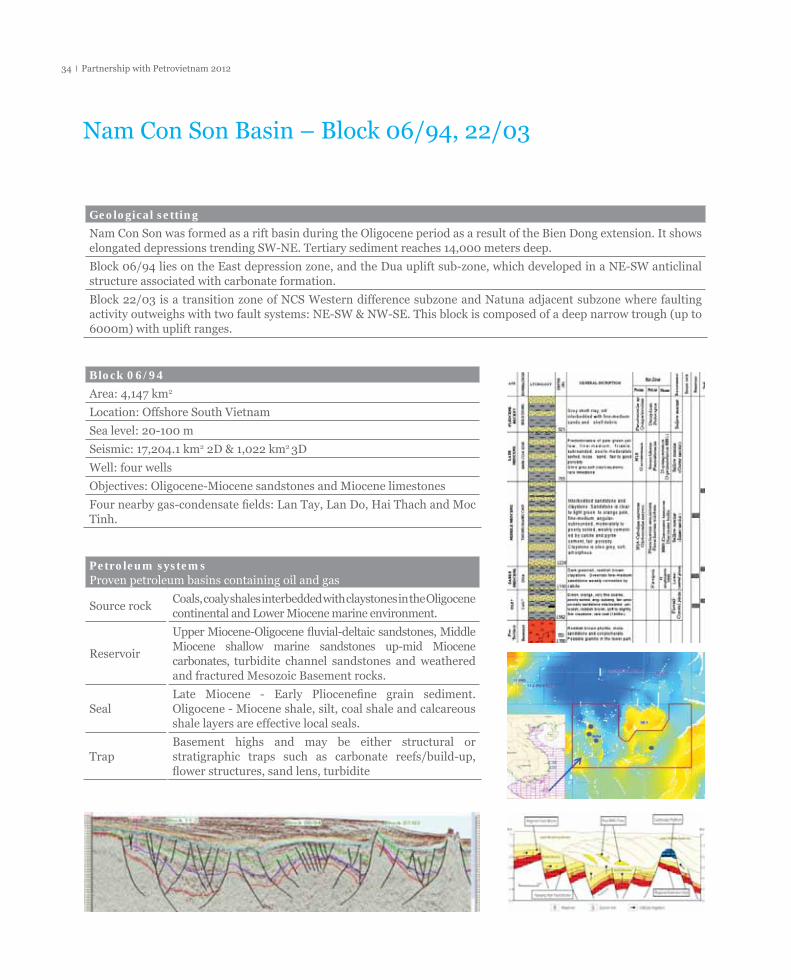

Nam Con Son Basin – Block 06/94, 22/03

Geological setting

Nam Con Son was formed as a rift basin during the Oligocene period as a result of the Bien Dong extension. It shows elongated depressions trending SW-NE. Tertiary sediment reaches 14,000 meters deep.

Block 06/94 lies on the East depression zone, and the Dua uplift sub-zone, which developed in a NE-SW anticlinal structure associated with carbonate formation.

Block 22/03 is a transition zone of NCS Western difference subzone and Natuna adjacent subzone where faulting activity outweighs with two fault systems: NE-SW & NW-SE. This block is composed of a deep narrow trough (up to 6000m) with uplift ranges.

Block 06/94

Area: 4,147 km2

Location: Offshore South Vietnam

Sea level: 20-100 m

Seismic: 17,204.1 km2 2D & 1,022 km2 3D

Well: four wells

Objectives: Oligocene-Miocene sandstones and Miocene limestones

Four nearby gas-condensate fi elds: Lan Tay, Lan Do, Hai Thach and Moc Tinh.

Petroleum systemsProven petroleum basins containing oil and gas

Source rockCoals, coaly shales interbedded with claystones in the Oligocene continental and Lower Miocene marine environment.

Reservoir

Upper Miocene-Oligocene fl uvial-deltaic sandstones, Middle Miocene shallow marine sandstones up-mid Miocene carbonates, turbidite channel sandstones and weathered and fractured Mesozoic Basement rocks.

SealLate Miocene - Early Pliocenefi ne grain sediment. Oligocene - Miocene shale, silt, coal shale and calcareous shale layers are effective local seals.

TrapBasement highs and may be either structural or stratigraphic traps such as carbonate reefs/build-up, fl ower structures, sand lens, turbidite

35Chapter 3: Partnership by Sector - Upstream Industry

Nam Con Son Basin – Block 06/94, 22/03

Block 22/03

Area: 4,753 km2

Location: Offshore Southern part of Vietnam

Sea level: 20-100 m

Seismic: 3,000 km 2D

Well: One well (oil show and good seal)

Prospects & leads: Five

Objectives: Pre-Tertiary fractured basement and Miocene sandstone

Estimated HC Reserve: 2.2 BCFS

Petroleum systemsProven petroleum basins containing oil and gas

Source rock Oligocene shale and coaly shale

ReservoirOligocene and Miocene sandstones; fractured granite basement

SealLower Miocene – Pliocene shale: good regional seal; Late Oligocene claystone: local seal

Trap Basement high, tittled fault block and combination types

Partnership with Petrovietnam 201236

Phu Quoc Basin - Blocks 31, 32, 33, 34, 35 & 36/03

Geological setting

Phu Quoc–Kampot Som Basin is a Late Jurassic to Early Cretaceous foreland basin developed in response to the build-up of the paleo-Pacifi c magmatic arc. It forms an elongated, more than 500 km long sediment-filled depression extending from south-western Cambodia in the north to the central southern part of the Gulf of Thailand. This basin is up to 150 km wide with its axis along the approximate latitudes of 1030–1040.

Petroleum systems

Source rock Oligocene shales

Reservoir Oligocene – Miocene sandstones

Seal Oligocene – Miocene interbeded shales

Trap Tilted fault blocks

Hydrocarbon Occurrence

Oil fi elds in adjacent Cuu Long basin.

Block 31 32 33 34 35 36/03Area (km

2) 5,036 4,440 4,630 4,700 4,630 2,950

Sea level (m) 20 20 - 30 30 - 40 50 50 50 Seismic 2D (km) 1,294 685 431 477 380 593 Well 1 - - - - -

HC Potential Cenozoic Basin

Cenozoic Basin

Cenozoic Basin

Cenozoic Basin

Cenozoic Basin

Cenozoic Basin

37Chapter 3: Partnership by Sector - Upstream Industry

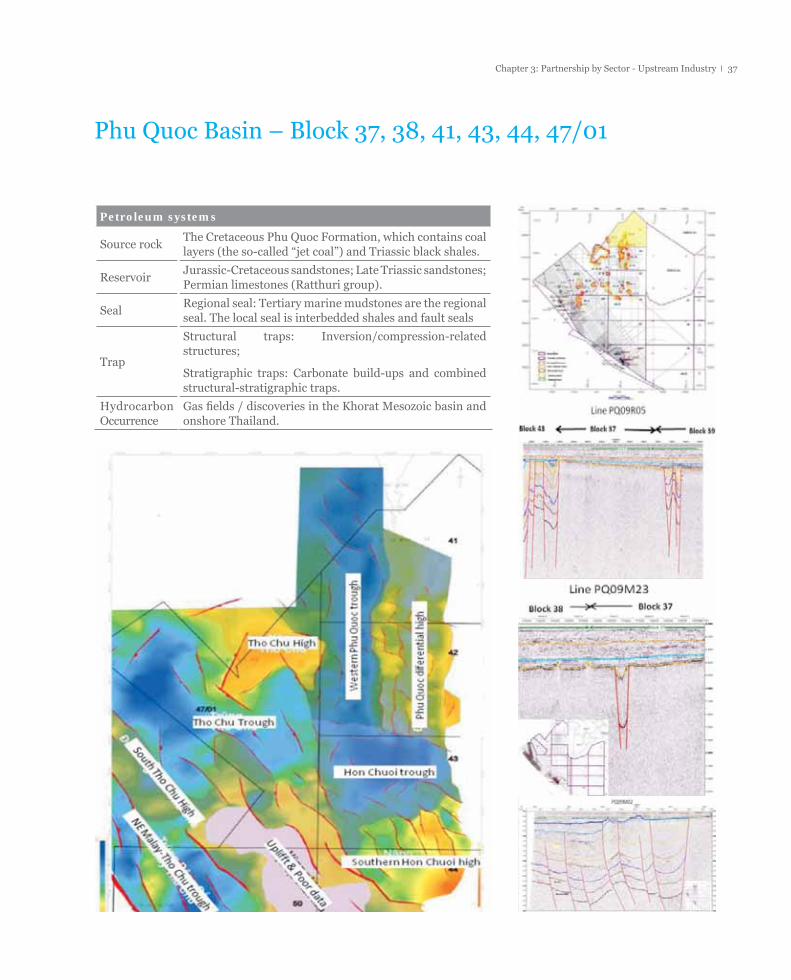

Phu Quoc Basin – Block 37, 38, 41, 43, 44, 47/01

Petroleum systems

Source rockThe Cretaceous Phu Quoc Formation, which contains coal layers (the so-called “jet coal”) and Triassic black shales.

ReservoirJurassic-Cretaceous sandstones; Late Triassic sandstones; Permian limestones (Ratthuri group).

SealRegional seal: Tertiary marine mudstones are the regional seal. The local seal is interbedded shales and fault seals

Trap

Structural traps: Inversion/compression-related structures;

Stratigraphic traps: Carbonate build-ups and combined structural-stratigraphic traps.

Hydrocarbon Occurrence

Gas fi elds / discoveries in the Khorat Mesozoic basin and onshore Thailand.

Partnership with Petrovietnam 201238

Block 37

Area: 5,020 km2

Location: Southwest Offshore Vietnam

Sea level: 20-30 m

Seismic: 775 km 2D

Well: No well

HC Potential in Mesozoic basin

Block 38

Area: 6,060 km2

Location: Southwest Offshore Vietnam

Sea level: 30-40 m

Seismic: 800 km 2D seismic

Well: No well

HC Potential in Mesozoic basin

Block 41

Area: 5,020 km2

Location: Southwest Offshore Vietnam

Sea level: 20 m

Seismic: 1,145 km 2D

Well: No well

Prospects & Leads: 4

HC Potential in Mesozoic basin

Block 43

Area: 4,850 km2

Location: Southwest Offshore Vietnam

Sea level: 20 m

Seismic: 2461 km 2D seismic

Well: No well

Prospects & Leads: 4

HC Potential in Mesozoic basin

39Chapter 3: Partnership by Sector - Upstream Industry

Block 44

Area: 4,760 km2

Location: Southwest offshore Vietnam

Sea level: 20 m

Seismic: 1109 km 2D seismic

Well: No well

Prospects & Leads: 2

Potential in Mesozoic basin

Block 47/01

Area: 5,850 km2

Location: Southwest Offshore Vietnam

Sea level: 20-50 m

Seismic: 1457 km 2D seismic

Well: No well

Prospects & Leads: 5 MZ

Potential in Mesozoic basin

Partnership with Petrovietnam 201240

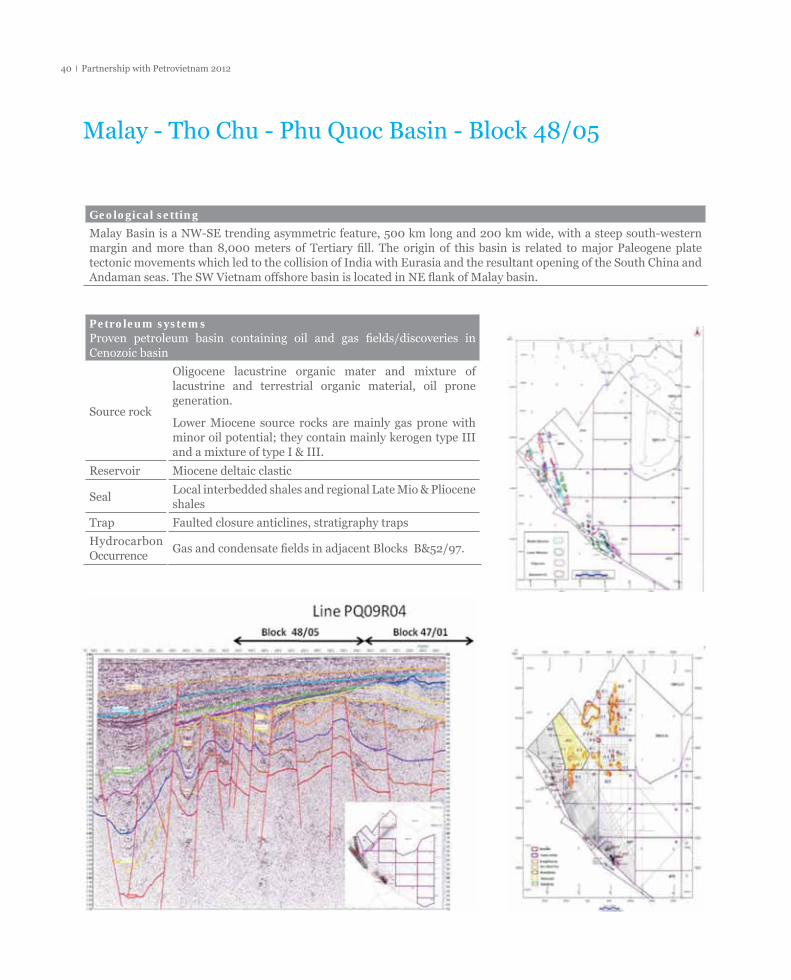

Malay - Tho Chu - Phu Quoc Basin - Block 48/05

Geological setting

Malay Basin is a NW-SE trending asymmetric feature, 500 km long and 200 km wide, with a steep south-western margin and more than 8,000 meters of Tertiary fi ll. The origin of this basin is related to major Paleogene plate tectonic movements which led to the collision of India with Eurasia and the resultant opening of the South China and Andaman seas. The SW Vietnam offshore basin is located in NE fl ank of Malay basin.

Petroleum systemsProven petroleum basin containing oil and gas fi elds/discoveries in Cenozoic basin

Source rock

Oligocene lacustrine organic mater and mixture of lacustrine and terrestrial organic material, oil prone generation.

Lower Miocene source rocks are mainly gas prone with minor oil potential; they contain mainly kerogen type III and a mixture of type I & III.

Reservoir Miocene deltaic clastic

SealLocal interbedded shales and regional Late Mio & Pliocene shales

Trap Faulted closure anticlines, stratigraphy traps

Hydrocarbon Occurrence

Gas and condensate fi elds in adjacent Blocks B&52/97.

41Chapter 3: Partnership by Sector - Upstream Industry

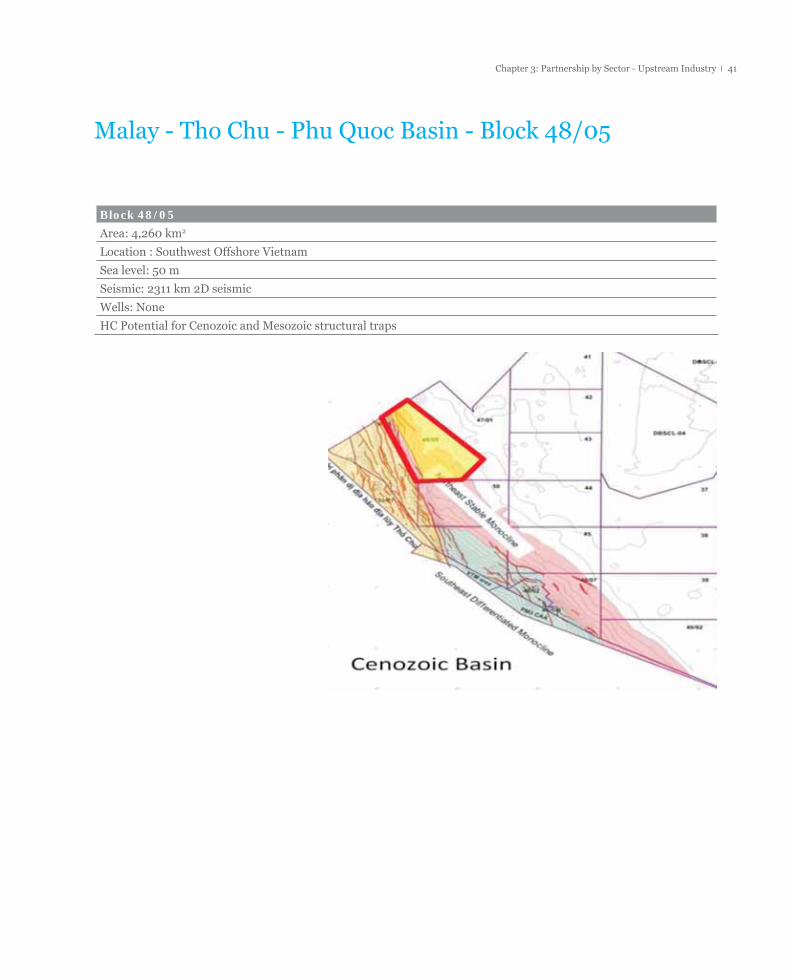

Malay - Tho Chu - Phu Quoc Basin - Block 48/05

Block 48/05

Area: 4,260 km2

Location : Southwest Offshore Vietnam

Sea level: 50 m

Seismic: 2311 km 2D seismic

Wells: None

HC Potential for Cenozoic and Mesozoic structural traps

Partnership with Petrovietnam 201242

2. Mid and Downstream Industry

Mid And Downstream Industry Overview

Vietnam’s oil and gas market is expanding quickly on the back of the country’s strong overall economic growth. To meet rising demand the country is embarking on an ambitious plan to build its domestic mid and downstream industry. The following chapter explains the development of the market and the participation opportunities which PVN is offering to foreign investors.

Rapidly Growing Oil and Gas Demand

The Vietnamese economy has been growing at an average annual rate of c. 7% historically and is forecast to continue its impressive growth in the future. Vietnamese oil consumption increased by 4.7% per annum during the 2008 - 2011 period and is forecast to grow by 6.2% per year from 326 KBPD in 2011 to 554 KBPD in 2020.

-

100

200

300

400

500

600

Vietnam's Oil consumption ('000 b/d)

2008200920102011

2012f

2013f

2014f

2015f

20l6f

2017f

20l8f

2019f

2020f

Source: BMI Vietnam Oil and Gas Report Q4 2011