Embed Size (px)

Citation preview

Examiner’s use only

Team Leader’s use only

Surname Initial(s)

Signature

Centre No.

Candidate No.

Turn over

Question Leave Number Blank

1

2

3

4

5

6

7

TotalThis publication may be reproduced only in accordance with Pearson Education Ltd copyright policy. ©2013 Pearson Education Ltd.

Printer’s Log. No.

P42221AW850/6001/57570 1/1/1/1/1/e2

*P42221A0136*

Paper Reference(s)

6001/01London Examinations GCEAccounting (Modular Syllabus)Advanced SubsidiaryUnit 1: The Accounting System and

CostingTuesday 8 January 2013 – AfternoonTime: 3 hours

Materials required for examination Items included with question papersNil Source booklet

Instructions to CandidatesIn the boxes above, write your centre number, candidate number, your surname, initial(s) and signature. Check that you have the correct question paper.Answer FIVE questions, choosing TWO from Section A and THREE from Section B.Indicate which question you are answering by marking the box ( ).If you change your mind, put a line through the box ( ) and then indicate your new question with a cross ( ).All calculations must be shown.Write your answers in the spaces provided in this question paper.Do not return the insert with the question paper.

Information for CandidatesThe marks for individual questions and the parts of questions are shown in round brackets: e.g. (2).There are 7 questions in this question paper. The total mark for this paper is 200. There are 36 pages in this question paper. Any blank pages are indicated.Calculators may be used.The source material for use with questions 1 to 7 is in the enclosed source booklet.

Advice to CandidatesWrite your answers neatly and in good English.

Paper Reference

6 0 0 1 0 1

Leave blank

2

*P42221A0236*

SECTION A

Answer TWO questions from this section.

If you answer question 1, put a cross in this box ( ).

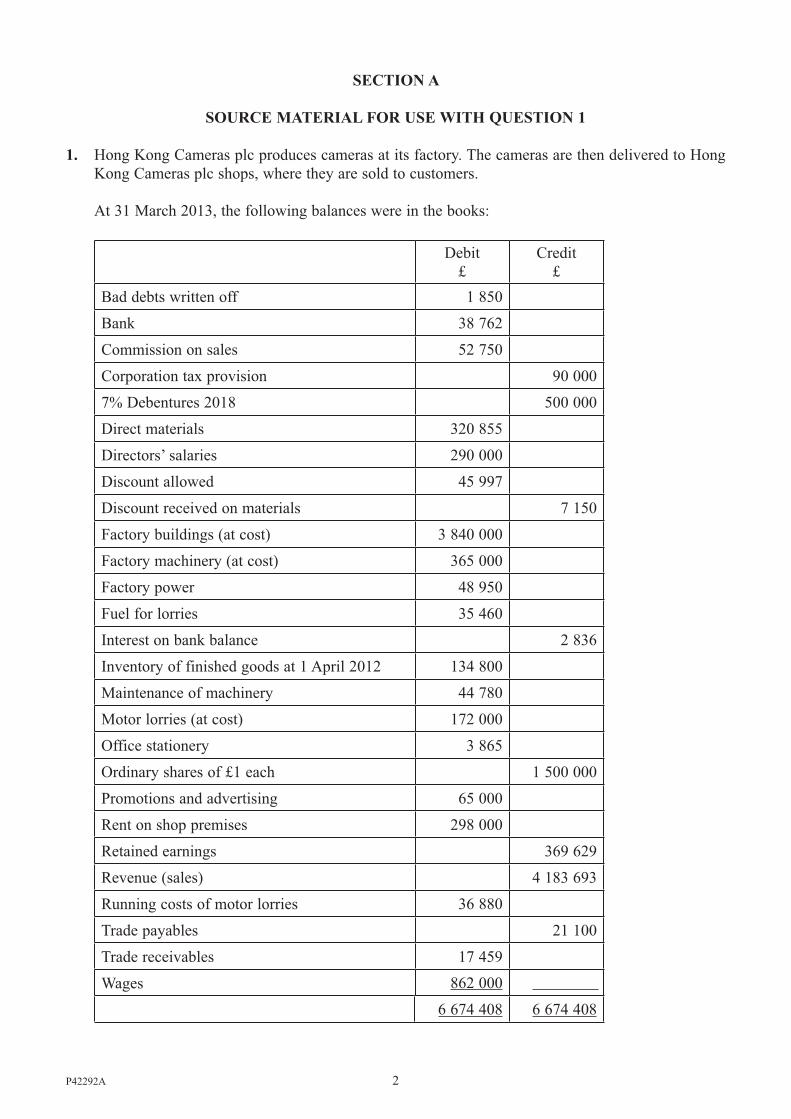

Source material for question 1 is on pages 2 and 3 of the source booklet.

1. (a) Prepare the:

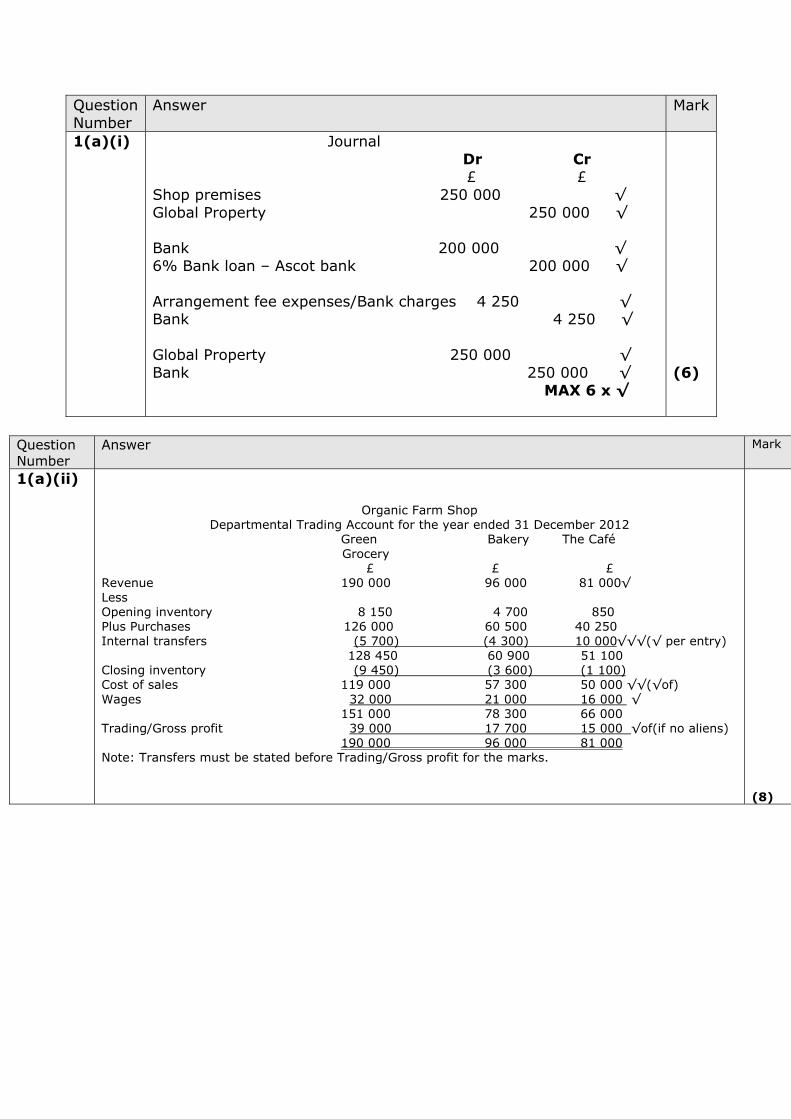

(i) Journal entries to record the purchase of the shop premises in 5. above. Narratives are not required

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(6)

Leave blank

3

*P42221A0336* Turn over

(ii) Departmental Trading Account of Organic Farm Shop showing the profit/loss of each department for the year ended 31 December 2012

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(8)

Leave blank

4

*P42221A0436*

(iii) Statement of Comprehensive Income for the business as a whole for the year ended 31 December 2012

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(16)

Leave blank

5

*P42221A0536* Turn over

(iv) Statement of Financial Position at 31 December 2012.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

Leave blank

6

*P42221A0636*

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(14)

Leave blank

7

*P42221A0736* Turn over

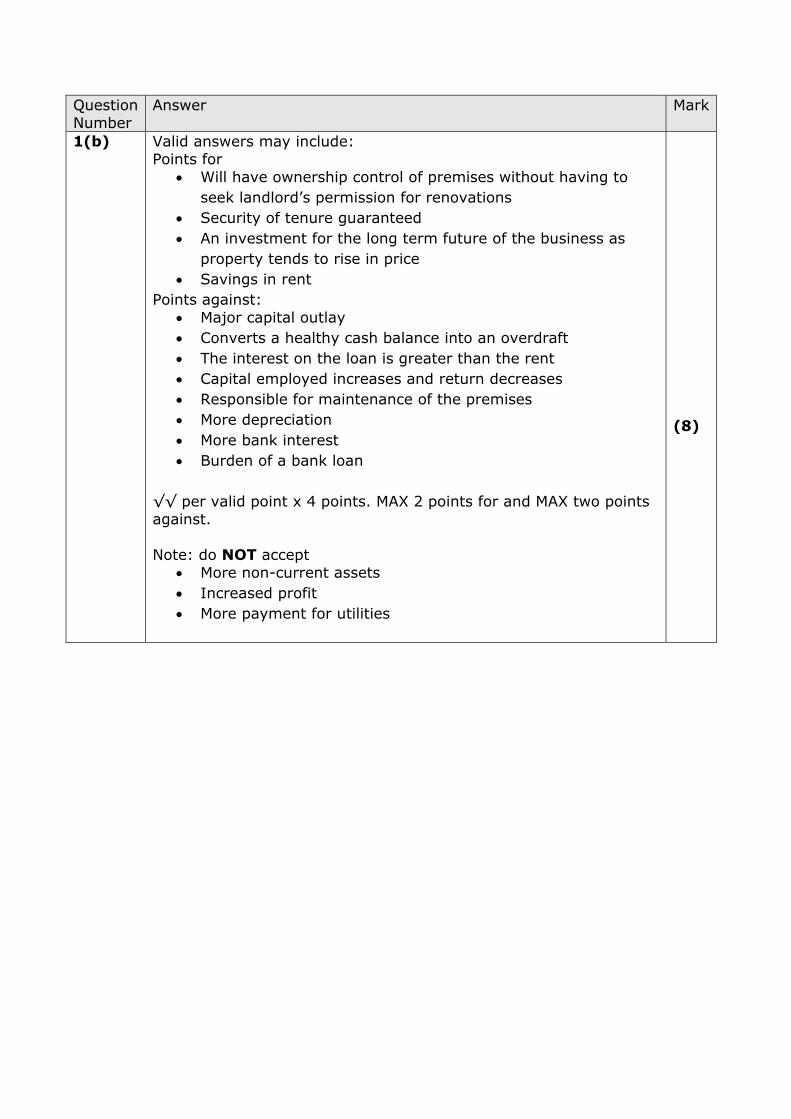

(b) Evaluate the owner’s decision to purchase the shop premises as an alternative to renting.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(8) Q1

(Total 52 marks)

Leave blank

8

*P42221A0836*

If you answer question 2, put a cross in this box ( ).

Source material for question 2 is on pages 4 and 5 of the source booklet.

2. (a) Explain the meaning of the debit balance on the Rent receivable account on 1 January 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(4)

Leave blank

9

*P42221A0936* Turn over

(b) Prepare the following accounts for the year ended 31 December 2012, including the appropriate transfer to the financial statements:

(i) Sundry expenses account

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(4)

Leave blank

10

*P42221A01036*

(ii) Premises repairs account

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(4)

(iii) Rent receivable account.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(4)

Leave blank

11

*P42221A01136* Turn over

(c) State one accounting concept which:

(i) supports the change of depreciation method proposed by Arpan

(ii) does not support the change of depreciation method proposed by Arpan.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(4)

Leave blank

12

*P42221A01236*

(d) Distinguish between capital expenditure and revenue expenditure.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(4)

Leave blank

13

*P42221A01336* Turn over

(e) State, giving your reasons, whether each of the following is capital expenditure or revenue expenditure:

� � �� ���������� ����� � �� ��� ��������������

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(4)

Leave blank

14

*P42221A01436*

(f) Calculate, showing clearly all workings, the:

(i) adjustment required to the provision for depreciation on the machines to 31 December 2011 to account for the change in depreciation method

(ii) depreciation charge on all the machines for the year ended 31 December 2012.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(8)

Leave blank

15

*P42221A01536* Turn over

(g) Prepare, for the year ended 31 December 2012, the:

� � ���� ��������������

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(3)

� � ����� ����������������������������������������

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(5)

Leave blank

16

*P42221A01636*

(h) Evaluate Arpan’s decision to change the basis of charging depreciation on machines from the straight line method to reducing balance method.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(8) Q2

(Total 52 marks)

Leave blank

17

*P42221A01736* Turn over

If you answer question 3, put a cross in this box ( ).

Source material for question 3 is on pages 6 and 7 of the source booklet.

3. (a) Explain the following accounting concepts. For each concept give one example from the draft Statement of Comprehensive Income prepared by Xevena and from the additional information given, where the concept has not been correctly applied:

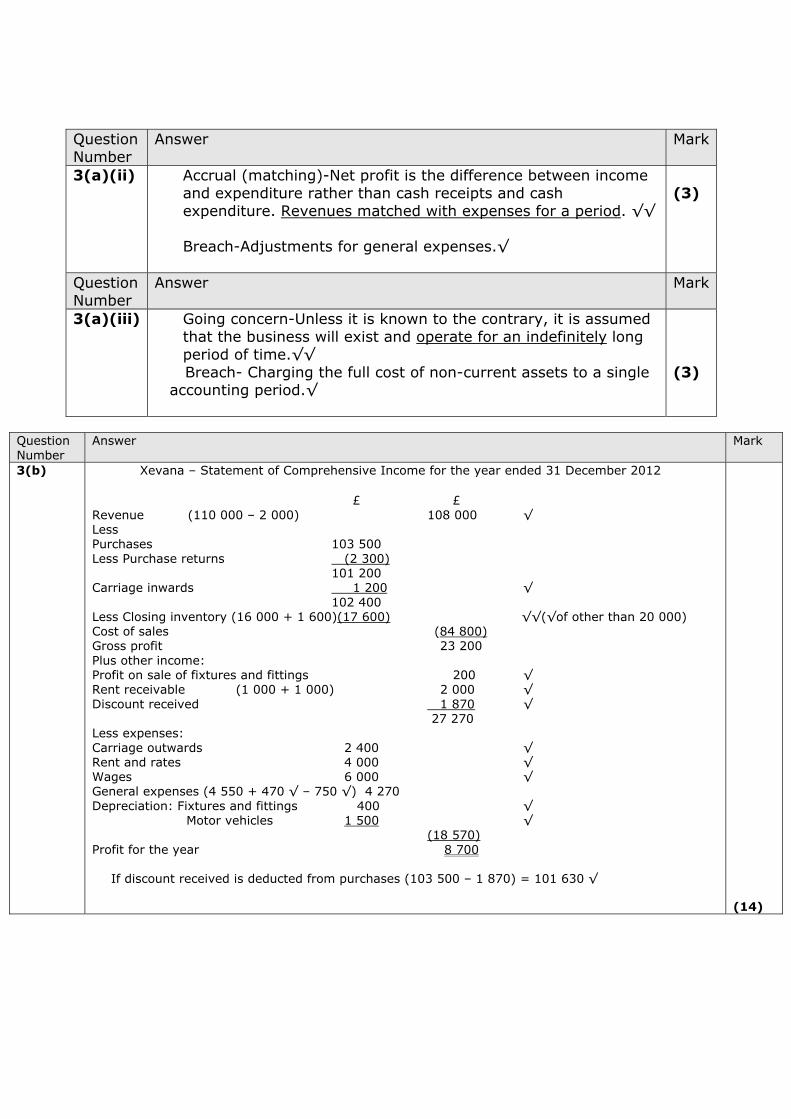

(i) Realisation

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(3)

(ii) Accrual (matching)

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(3)

(iii) Going concern.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(3)

Leave blank

18

*P42221A01836*

(b) Redraft the corrected Statement of Comprehensive Income after taking into account the additional information given for the year ended 31 December 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

Leave blank

19

*P42221A01936* Turn over

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(14)

(c) Prepare the Purchases Ledger Control Account, calculating the trade payables balance at 31 December 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(6)

Leave blank

20

*P42221A02036*

(d) Prepare the Statement of Financial Position at 31 December 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(15)

Leave blank

21

*P42221A02136* Turn over

(e) Evaluate the use of accounting concepts when preparing financial statements.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

....................................................................................................................................... (8)

TOTAL FOR SECTION A: 104 MARKS

Q3

(Total 52 marks)

Leave blank

22

*P42221A02236*

SECTION B

Answer THREE questions from this section.

If you answer question 4, put a cross in this box ( ).

Source material for question 4 is on page 8 of the source booklet.

4. (a) Explain the term profitability.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(4)

Leave blank

23

*P42221A02336* Turn over

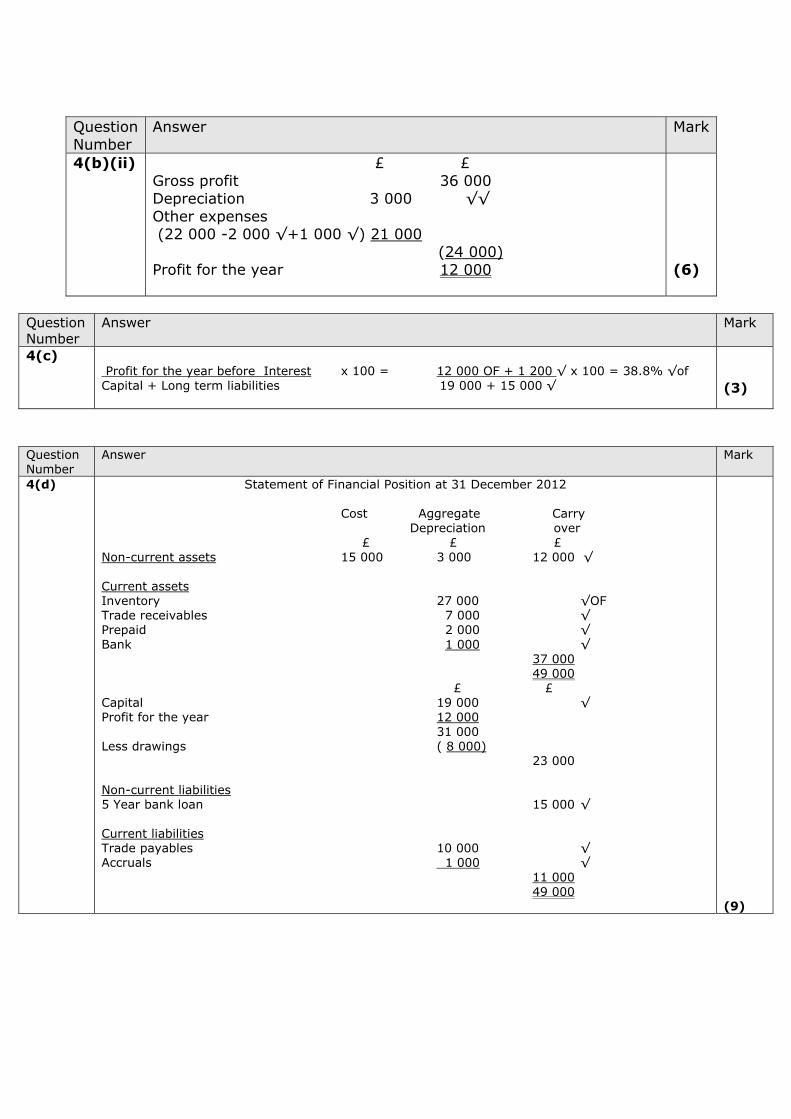

(b) Prepare the Statement of Comprehensive Income for the year ended 31 December 2012, showing clearly the:

(i) value of the inventory at 31 December 2012

(ii) profit for the year.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................(6)

(c) Calculate the percentage return on capital employed for the year.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................ (3)

Leave blank

24

*P42221A02436*

(d) Prepare the Statement of Financial Position at 31 December 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................(9)

Leave blank

25

*P42221A02536* Turn over

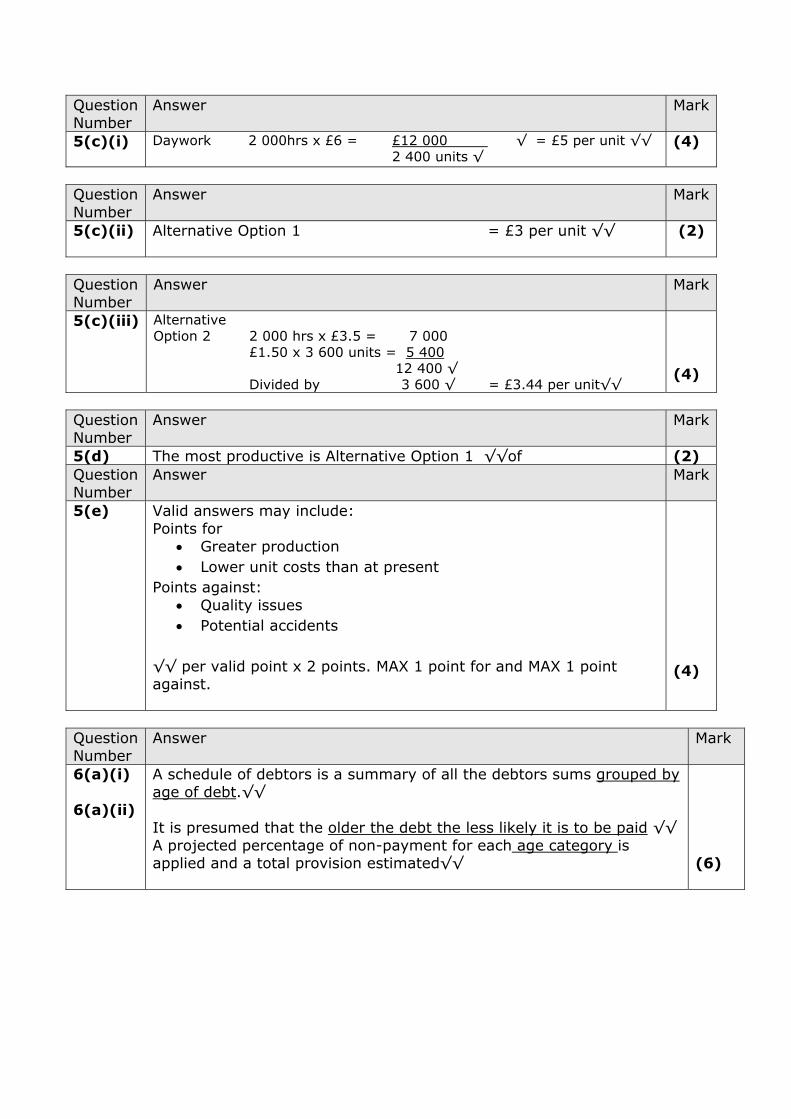

(e) Calculate the:

(i) current ratio

................................................................................................................................ ................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................