Embed Size (px)

Citation preview

Pantea AlirezazadehU N I V ER S ITY O F C O N N EC TIC U T

Communicating the Value of Intangibles: The Role of Capitalization and Patent in the

Software Industry

Research Objective

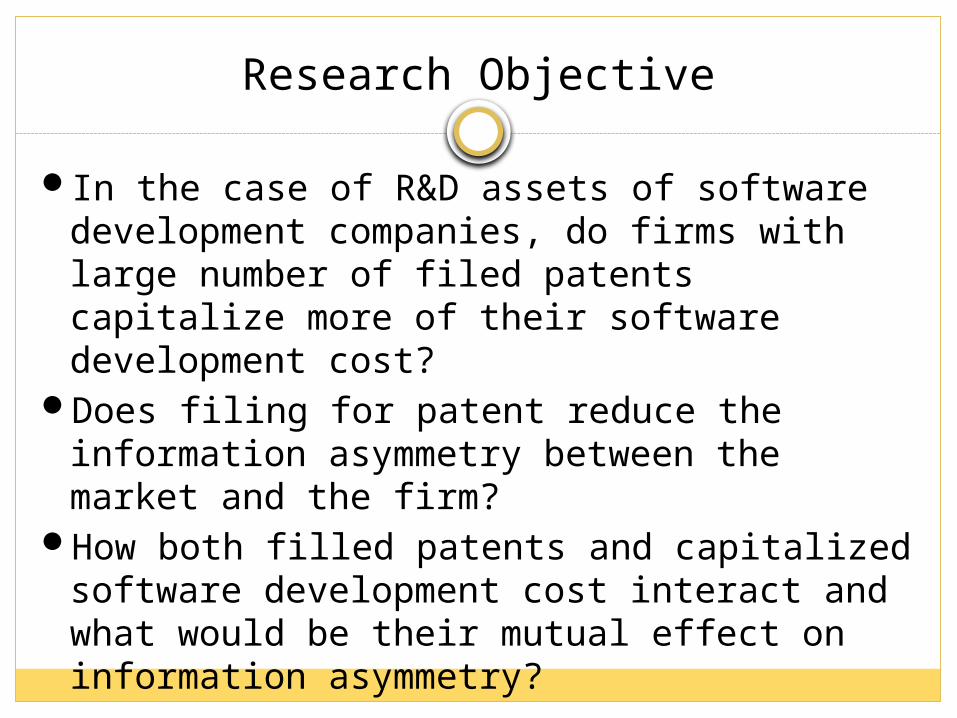

In the case of R&D assets of software development companies, do firms with large number of filed patents capitalize more of their software development cost?

Does filing for patent reduce the information asymmetry between the market and the firm?

How both filled patents and capitalized software development cost interact and what would be their mutual effect on information asymmetry?

Outline

IntangiblesAccounting Rules for Capitalization of R&D AssetsFilling for PatentPrior researchHypothesis DataResult

IntangiblesAccounting rules define an asset intangible if it owns the

following characteristics:

Lack of physical substanceNon-financial natureInitial useful life extends beyond a single financial

reporting period

Patents

Trademark

R&DBrand

Computer Software

How it measure Intangibles?

Market Capitalization

Return on Invested Capital

Score Cards

Direct Measure of Intellectual Capital

Brand Valuation

Research and Development

The Standard of Financial Accounting Standards(SAFS) No. 2 requires the immediate expensing of all R&D activities.

SFAS No. 86 indicate that software capitalization, the only exception in the United States to the full expensing rule of R&D (SFAS No. 2), can be capitalized under certain conditions

SFAS No. 86 Requirements

InitiationStage

Technical Feasibility Ready to be Sold

Software Sale

Expense Capitalize Capitalize Expense

Capitalized Software Development Costs

Income Statement

Operating Expenses: Depreciation/Amortization R&D

Balance Sheet

Assets: Property, Plant, Equipment Capitalized Development Cost

Prior Literature: Capitalize or Expense!?

Capitalizing software developments costs leads to higher earnings variability which is positively correlated with forecast errors (Shi 2002).

Analysts concerned with the size of their earnings forecast errors view capitalization negatively (Aboody and Lev 1998).

The greater the uncertainty of future economic benefits from R&D expenditures, the weaker would be the case in favor of capitalization (Kothari and et. al 2002).

Prior Literature: Capitalize or Expense!?

Capitalized values of R&D are significantly associated with stock prices. (Lev and Sougiannis 1996)

Capitalization-related variables in the financial statement are significantly associated with capital market variables and future earnings. (Aboody and Lev 1998)

The expensing of R&D by firms with increasing investment rate in R&D is associated with a decline in the informativeness of reported earnings. (Lev and Zarowin 1999)

Capitalization of intangibles is associated with higher analyst following and lower absolute earnings forecast errors. (Matolcsy and Wyatt 2006)

Allowing managers to credibly signal their superior information by either capitalizing successful R&D investment or expensing unsuccessful R&D investments reduces information asymmetry. (Ahmed and Falk 2006).

Patents: A Popular Choice of Innovation Proxy

Patentable

Patentable Subject Matter

Industrial Application

New

Non-Obvious

Prior Literature: Patenting and Market Value

Patent citation has a noticeable effect on market value (Hall and et. al. 2005).

Patents have a significant impact on firm-level productivity and market value (Bloom and Reenen 2002).

There is positive relation between the future operating performance and productivity of a firms’ innovation efforts (Pandit et. al. 2009 ).

Hypothesis

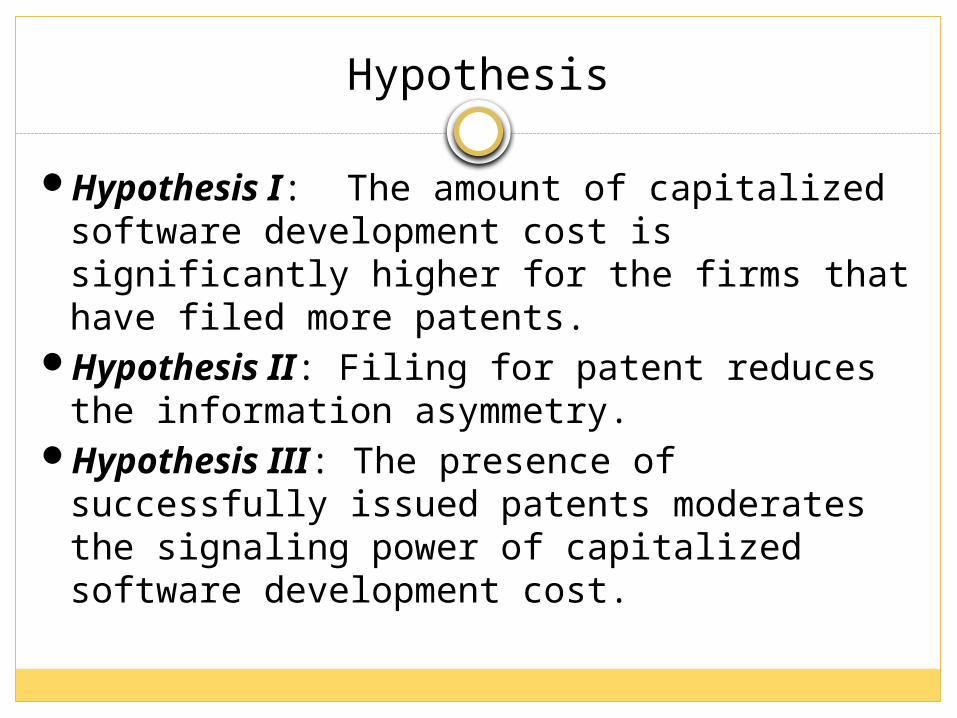

Hypothesis I: The amount of capitalized software development cost is significantly higher for the firms that have filed more patents.

Hypothesis II: Filing for patent reduces the information asymmetry.

Hypothesis III: The presence of successfully issued patents moderates the signaling power of capitalized software development cost.

Variable DescriptionCapValue Capitalized software development cost divided by market value

MarketValue Market value of the firm three months after the fiscal year

DevelopmentIntensity Annual software development costs to sales

Profitability Net income plus software amortization minus the annually capitalized software divided by sales.

Leverage Long-term debt divided by book value of equity

Patent The number of patents applied by the end of the fiscal year

Spread Annual average of the logarithm daily relative bid-ask spread, defined as absolute value of the bid-ask spread divided by their average

Volatility Logarithm standard deviation of daily stock return

Capitalization The amount of capitalized software development cost

Patent Dummy 1 if the firm has filed any patent that year and 0 otherwise

Turnover Annual average of logarithm trading volume in shares divided by number of shares outstanding

Price Annual average of the logarithm of daily stock price

Analyst Number of analysts supplying one-year ahead earning forecast

Data

COMPUSTAT, CRSP, I/B/E/S

SEC Filings,

DirectEdgar

USPTO,

NBER

260 firms for years 2000 to 2008 Computer programming and

prepackaged companies: SIC 7370-7372

Data Collection:

Capitalization of the software development cost and amortization of software asset

Financial data Patent Data

Hypothesis I

itititit

itY

ititYit

ntLogLagPateeLogLeveragyofitabilitLog

itymentIntensLogDevelopalueLogMarketVYReLogCapValu

1643

2008

2000210

Pr

Variable Coefficient t-value

LogMarketValue -.0079 -5.75***

LogDevelopmentIntensity .0063 2.88***LogProfitability .0076 4.2***LogLeverage .0035 4.64***LogLagPatent .0030 2.75***

***Denote significance at a probability level below 0.01**Denote significance at a probability level below 0.1

Heckman Model

itititit

itY

ititYit

ntLogLagPateeLogLeveragyofitabilitLog

itymentIntensLogDevelopalueLogMarketVYReLogCapValu

1643

2008

2000210

Pr

Variable Coefficient t-value

LogMarketValue -.0079 -5.40***

LogDevelopmentIntensity .0063 2.88***LogProfitability .0076 4.2***LogLeverage .0035 4.64***LogLagPatent .0030 2.75***

***Denote significance at a probability level below 0.01**Denote significance at a probability level below 0.1

Hypothesis II

variable Coefficient t-value

LogMarketValue -0.19 -13.75 ***

Volatility 0.37 11.00 ***

Turnover -0.42 -31.76 ***

Price -0.31 -17.08 ***

Analyst -0.002 -1.53

Patent -0.02 -1.81**

ititit

itititY

ititYit

iedPatentApplAnalyst

iceTurnoverVolatilityetValueLogLogMarkYRSpread

76

43

2008

2000210 Pr

***Denote significance at a probability level below 0.01**Denote significance at a probability level below 0.1

Hypothesis III

Variable Coefficient t-Value

LogMarketValue -0.20 -15.92***Volatility 0.39 11.53***Turnover -0.41 -33.08***Price -0.3 -17.86***Analyst -0.002 -1.61PatentDummy -0.06 -3.3 ***Capitalization -0.008 -0.93PatentDummy*Capitalization 0.10 4.05***

itititit

ititY

itititYit

ationyCapitalizPatentDummtionCapitalizayPatentDummAnalyst

iceTurnoverVolatilityalueLogMarketVYRSpread

8765

4

2008

20003210 Pr

***Denote significance at a probability level below 0.01

Hypothesis III

Variable Coefficient t-Value

SharOut 0.12 3.73***Analyst 0.0035 9.72***PatentDummy 0.34 6.01***Capitalization 0.01 0.37PatentDummy*Capitalization -0.08 -1.84**

***Denote significance at a probability level below 0.01**Denote significance at a probability level below 0.1

itit

itititY

ititYit

ationyCapitalizPatentDummtionCapitaliza

yPatentDummAnalystSharOutSharOutYRTurnover

65

432

2008

200010

Conclusion

Both filing for patent and capitalizing the software development costs both reduce the information asymmetry between firm and the market.

Firms that file for more patents have a higher rate of capitalization.

Filing for patent reduces the effect of capitalization on information asymmetry.