Embed Size (px)

Citation preview

IUSS Pavia - Institute for Advanced Study

Master in Cooperation and Development

Palestinian foreign trade:

Current situation and future prospects

Laura Panza

Supervisor: Prof. Marco Missaglia

Academic Year 2006/2007

1

IUS

S -

Pavia

Laura Panza

Palestinian foreign trade: Current situation and future prospects

An Individual Study Submitted in Partial Fulfilment of the Requirements for the Master degree in

Cooperation and Development

Supervisor: Prof. Marco Missaglia

Pavia, January 28-29 January 2008

2

IUS

S -

Pavia

Contents

1. Introduction 3

2. The effects of the asymmetric integration: a non-viable economy 4

3. Macroeconomic overview 7

4. The structure of trade 14

5. Trade agreements 23

6. Indirect taxes 25

7. Export of labor 33

8. The rise of the informal sector 35

9. Export promotion 37

10. Conclusion 45

References 47

3

IUS

S -

Pavia

1.Introduction

The aim of this paper is to investigate whether trade can be a vehicle for growth and development

for the Palestinian economy, taking into consideration its nature of war-torn, occupied territory.

The first two chapters (2-3) of the following analysis aim to depict the current economic

performance of the Occupied Territories: starting from a wide framework, which identifies the roots

of the non-viability of the Palestinian economy, they further give an overall glance to its

macroeconomic structure. Chapter 4 goes in deeper details, analyzing the changes in the trade

structure and trade policies caused by the second intifada and the consequent distortions derived by

the political instability, which deepened the asymmetric forced integration with the Israeli

economy: the rise in the share of both imports and exports from and to Israel during the last decade

represents in fact the clearest sign of the absence of the necessary means to conduct an independent,

non-biased trade policy, thus leading to a process of inward orientation of the Palestinian economy.

Chapter 5 and 6 focus on the trade agreements and the indirect taxation system currently

implemented, which embody the institutional legitimation of the WBGS forced dependency on

Israeli market.

The paper further describes another factor hindering the process of development, the export of labor

(chapter 7), outlining how the flow of workers employed in the Israeli market constituted one of the

major obstacles to the possibility of structural change and increasing productive capacities for the

Palestinian economy. The strengthening of the policy of closures, concretely materialized with the

impossibility of accessing the Israeli labor market, as well as with the absence of expanding the

supply side of the domestic economy, brought, as direct consequence, to the widening of the

informal sector (chapter 8).

At the light of the above mentioned considerations, that helped drawing a clearer picture of WBGS

current economic status, chapter 9 outlines some trade policies that could be implemented as

recovery strategy, focusing on export promotion; the methodology used to validate the proposed

suggestions was based on the computation of Palestinian revealed comparative advantage, using the

Balassa index. Considering the scarcity of natural factor endowments, marble and stone constitute

the only Palestinian competitive commodities: an effective export policy should therefore focus on

supplying high value added goods and services and on finding new niche markets.

Finally, the conclusive chapter outlines the necessity of establishing freedom of movement and

access as preliminary condition for the achievement of economic viability: finding a political

solution constitutes therefore the first step that can lead to economic growth.

4

IUS

S -

Pavia

2. The effects of the asymmetric integration: a non-viable economy

Thirteen years after the beginning of the Oslo peace process and signing of the Economic Protocol

between Israel and the Palestinians, we find that the issue of the economic viability1 of the

Palestinian state is still unresolved. In fact it is difficult to talk about economic viability,

considering that there is no workable definition of what is a Palestinian economy: it is generally

agreed that the Palestinian economy covers the regions of the West Bank and Gaza Strip (WBGS),

but the territories and the borders delineating these areas are not well defined.

In order to understand why today the economic situation of the West Bank and Gaza Strip is non-

viable, it’s necessary to analyze how it evolved during 40 years of Israeli military occupation, the

main responsible for the fragmentation of its economic space. The Palestinian economy maintains

the typical features of an underdeveloped economy and it’s still organized around the same structure

of 1967, when agriculture was the dominant sector and the industrial sector (which composed less

than 10% of the GDP) was organized around micro-enterprises producing for the local market.

The repercussions of forty years of military occupation are visible in the economic anomaly that

WBGS is facing: on one side the forced integration in the Israeli economy led to a dramatic rise of

per capita incomes, which are higher than those of the Arab neighboring countries; on the other side

the Palestinian economic structure remained unchanged, with agriculture playing an extremely

relevant role and with an industrial share of GDP of a bare 14%.

The trend that the Occupied Palestinian Territories (OPT) are experiencing stands out in contrast

with the recent economic developments of other Mediterranean countries2, that, in the last decade

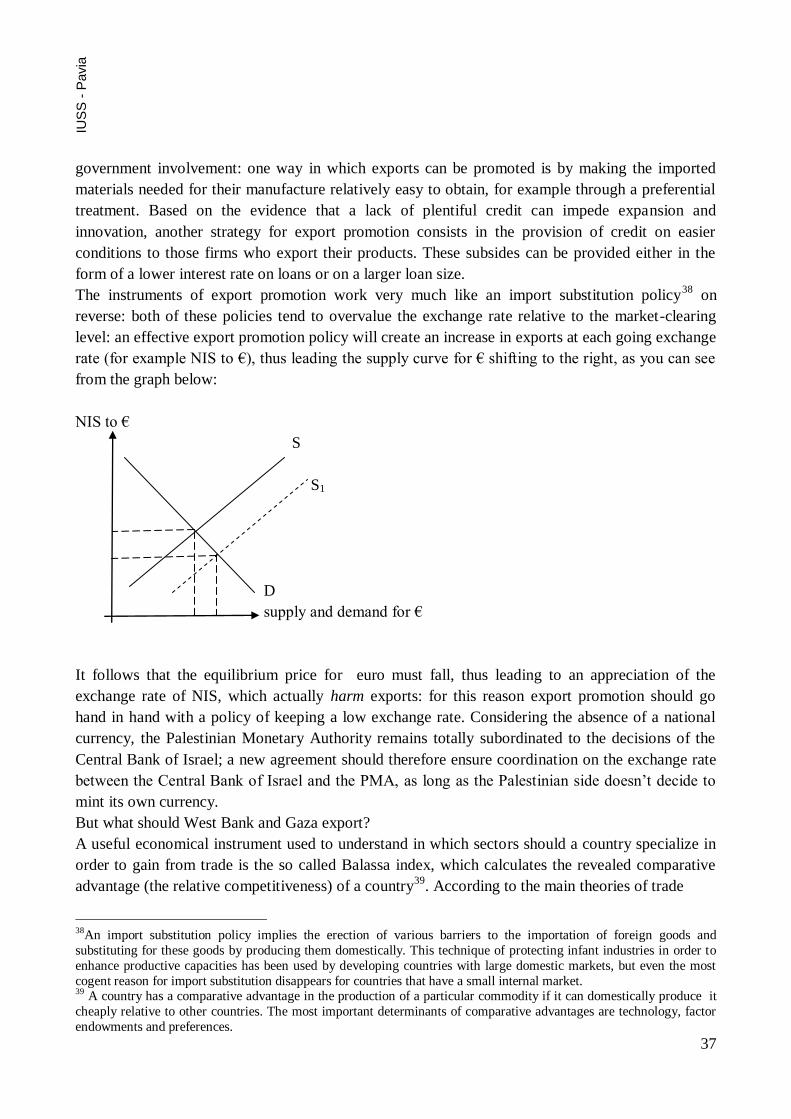

saw a decrease in the share of agriculture in GDP (less than 3% in Jordan) and an increase of the

industrial sector (30% of GDP in Jordan, more than 20% in Egypt). The process of structural

change can be identified as the key lever of the good economic performance of MED countries,

most of which kept on growing at a good pace, as it’s shown by figure 1.

On the contrary, the Palestinian productive sectors have stagnated: services, trade and construction,

driven by the higher incomes (pushed up by the remittances of Palestinian workers employed in

Israel), have thrived leaving a heavily distorted economy in a state of arrested development. Thus,

the unidirectional economic ―integration‖ regulated by the Israeli government, hindered the

improvement of Palestinian productive capacities, the possibility of access to market information, as

well as the promotion of Palestinian business in new markets.

1 It is generally understood that an economy is viable if it’s able to use its human, financial and physical resources to grow, sustain itself and increase the welfare of the inhabitants living within its area. 2 The term Mediterranean countries (MED countries) refers to the countries participating in the Euro-Mediterranean

Partnership. These are Algeria, Egypt, Israel, Jordan, Lebanon, Morocco, the OPT, Syria and Tunisia.

5

IUS

S -

Pavia

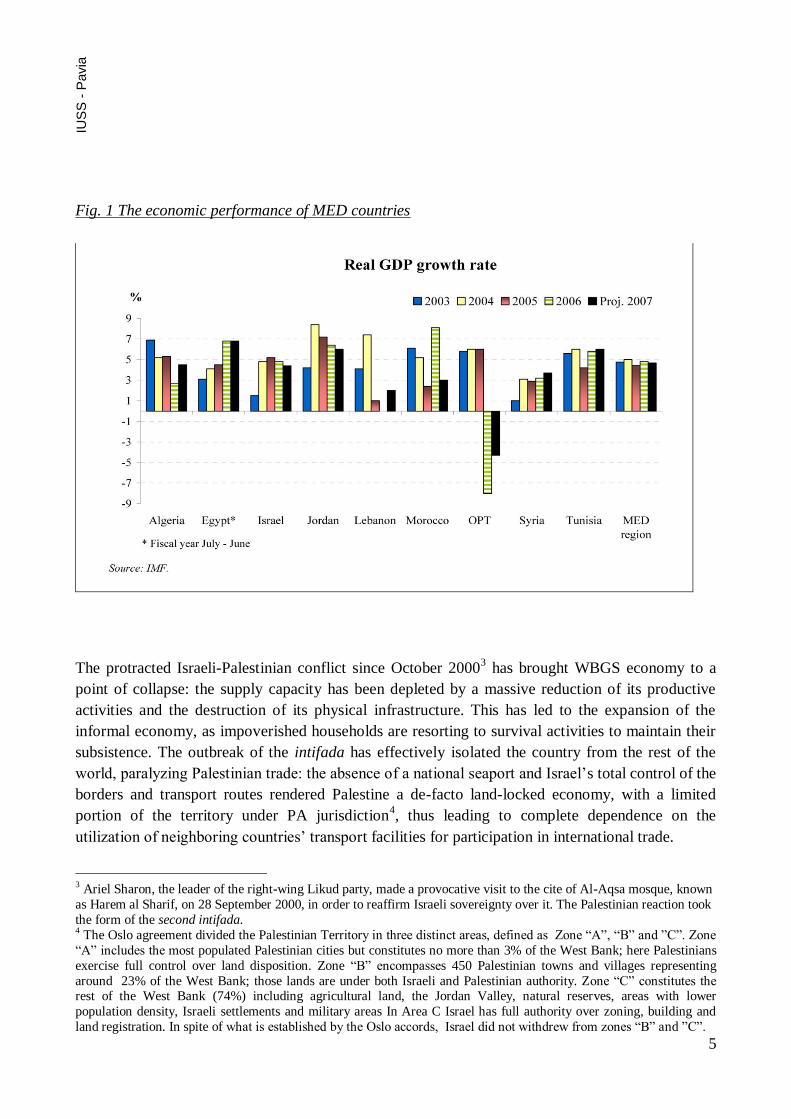

Fig. 1 The economic performance of MED countries

The protracted Israeli-Palestinian conflict since October 20003 has brought WBGS economy to a

point of collapse: the supply capacity has been depleted by a massive reduction of its productive

activities and the destruction of its physical infrastructure. This has led to the expansion of the

informal economy, as impoverished households are resorting to survival activities to maintain their

subsistence. The outbreak of the intifada has effectively isolated the country from the rest of the

world, paralyzing Palestinian trade: the absence of a national seaport and Israel’s total control of the

borders and transport routes rendered Palestine a de-facto land-locked economy, with a limited

portion of the territory under PA jurisdiction4, thus leading to complete dependence on the

utilization of neighboring countries’ transport facilities for participation in international trade.

3 Ariel Sharon, the leader of the right-wing Likud party, made a provocative visit to the cite of Al-Aqsa mosque, known

as Harem al Sharif, on 28 September 2000, in order to reaffirm Israeli sovereignty over it. The Palestinian reaction took

the form of the second intifada. 4 The Oslo agreement divided the Palestinian Territory in three distinct areas, defined as Zone ―A‖, ―B‖ and ‖C‖. Zone

―A‖ includes the most populated Palestinian cities but constitutes no more than 3% of the West Bank; here Palestinians

exercise full control over land disposition. Zone ―B‖ encompasses 450 Palestinian towns and villages representing

around 23% of the West Bank; those lands are under both Israeli and Palestinian authority. Zone ―C‖ constitutes the rest of the West Bank (74%) including agricultural land, the Jordan Valley, natural reserves, areas with lower

population density, Israeli settlements and military areas In Area C Israel has full authority over zoning, building and

land registration. In spite of what is established by the Oslo accords, Israel did not withdrew from zones ―B‖ and ‖C‖.

6

IUS

S -

Pavia

The significant difference in size and level of economic development constitutes the biggest

obstacle for a possible symmetric economic integration between the two countries: WBGS Gross

National Income (GNI) per capita was only 7% of that of Israel in 2004; even more significant are

the differences captured by Palestinian GDP, which represented a mere 3% of Israeli’s GDP in

2005. The major asymmetries in respective economic weights are reflected in the relative

importance of respective markets: WBGS markets covered 6% of total Israeli exports, as compared

with Israeli markets, accounting for 88% of Palestinian exports in 2005: similarly, Palestinian goods

represented only 0,8% of total Israeli imports, while the corresponding rate in case of WBGS was

74%.

7

IUS

S -

Pavia

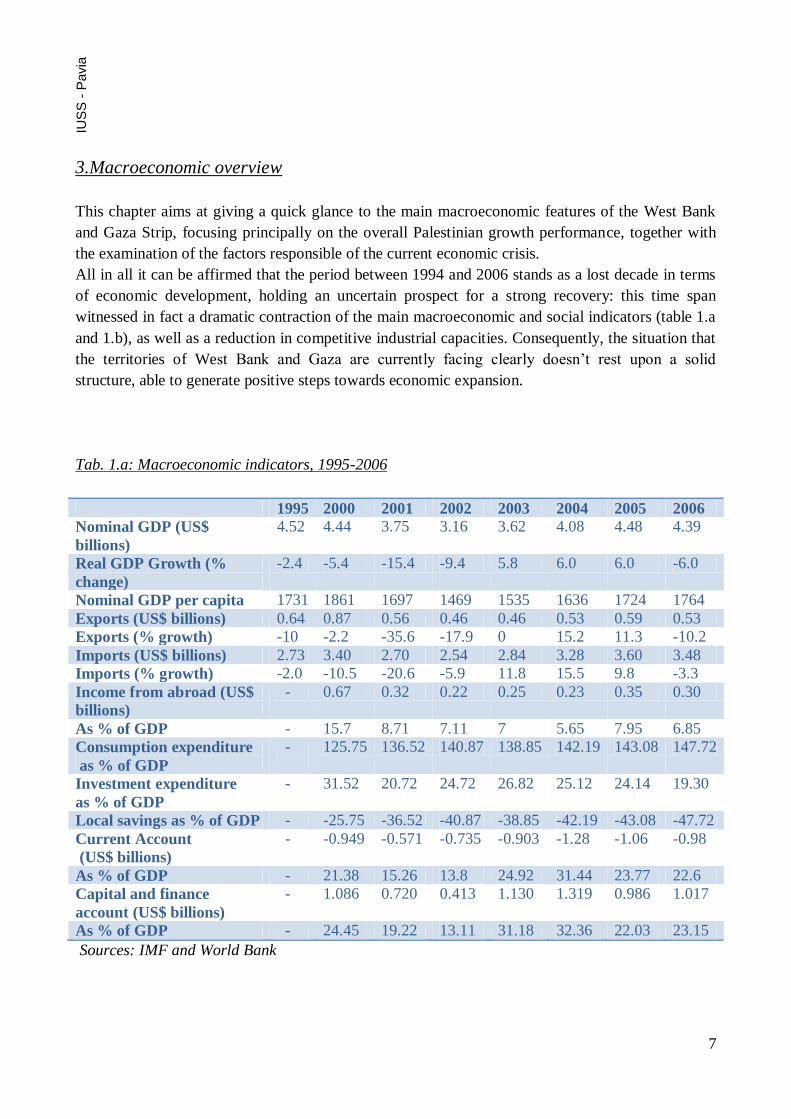

3.Macroeconomic overview

This chapter aims at giving a quick glance to the main macroeconomic features of the West Bank

and Gaza Strip, focusing principally on the overall Palestinian growth performance, together with

the examination of the factors responsible of the current economic crisis.

All in all it can be affirmed that the period between 1994 and 2006 stands as a lost decade in terms

of economic development, holding an uncertain prospect for a strong recovery: this time span

witnessed in fact a dramatic contraction of the main macroeconomic and social indicators (table 1.a

and 1.b), as well as a reduction in competitive industrial capacities. Consequently, the situation that

the territories of West Bank and Gaza are currently facing clearly doesn’t rest upon a solid

structure, able to generate positive steps towards economic expansion.

Tab. 1.a: Macroeconomic indicators, 1995-2006

1995 2000 2001 2002 2003 2004 2005 2006

Nominal GDP (US$

billions)

4.52 4.44 3.75 3.16 3.62 4.08 4.48 4.39

Real GDP Growth (%

change)

-2.4 -5.4 -15.4 -9.4 5.8 6.0 6.0 -6.0

Nominal GDP per capita 1731 1861 1697 1469 1535 1636 1724 1764

Exports (US$ billions) 0.64 0.87 0.56 0.46 0.46 0.53 0.59 0.53

Exports (% growth) -10 -2.2 -35.6 -17.9 0 15.2 11.3 -10.2

Imports (US$ billions) 2.73 3.40 2.70 2.54 2.84 3.28 3.60 3.48

Imports (% growth) -2.0 -10.5 -20.6 -5.9 11.8 15.5 9.8 -3.3

Income from abroad (US$

billions)

- 0.67 0.32 0.22 0.25 0.23 0.35 0.30

As % of GDP - 15.7 8.71 7.11 7 5.65 7.95 6.85

Consumption expenditure

as % of GDP

-

125.75 136.52 140.87 138.85 142.19 143.08 147.72

Investment expenditure

as % of GDP

- 31.52 20.72 24.72 26.82 25.12 24.14 19.30

Local savings as % of GDP - -25.75 -36.52 -40.87 -38.85 -42.19 -43.08 -47.72

Current Account

(US$ billions)

- -0.949 -0.571 -0.735 -0.903 -1.28 -1.06 -0.98

As % of GDP - 21.38 15.26 13.8 24.92 31.44 23.77 22.6

Capital and finance

account (US$ billions)

- 1.086 0.720 0.413 1.130 1.319 0.986 1.017

As % of GDP - 24.45 19.22 13.11 31.18 32.36 22.03 23.15

Sources: IMF and World Bank

8

IUS

S -

Pavia

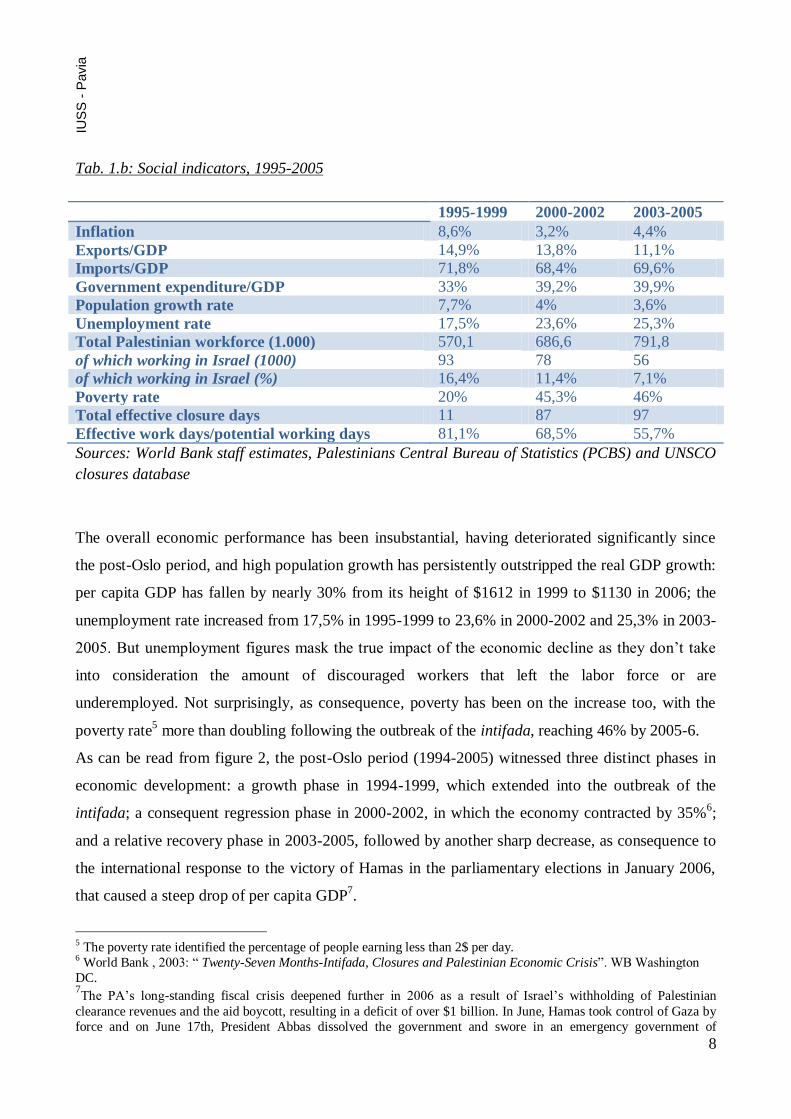

Tab. 1.b: Social indicators, 1995-2005

1995-1999 2000-2002 2003-2005

Inflation 8,6% 3,2% 4,4%

Exports/GDP 14,9% 13,8% 11,1%

Imports/GDP 71,8% 68,4% 69,6%

Government expenditure/GDP 33% 39,2% 39,9%

Population growth rate 7,7% 4% 3,6%

Unemployment rate 17,5% 23,6% 25,3%

Total Palestinian workforce (1.000) 570,1 686,6 791,8

of which working in Israel (1000) 93 78 56

of which working in Israel (%) 16,4% 11,4% 7,1%

Poverty rate 20% 45,3% 46%

Total effective closure days 11 87 97

Effective work days/potential working days 81,1% 68,5% 55,7%

Sources: World Bank staff estimates, Palestinians Central Bureau of Statistics (PCBS) and UNSCO

closures database

The overall economic performance has been insubstantial, having deteriorated significantly since

the post-Oslo period, and high population growth has persistently outstripped the real GDP growth:

per capita GDP has fallen by nearly 30% from its height of $1612 in 1999 to $1130 in 2006; the

unemployment rate increased from 17,5% in 1995-1999 to 23,6% in 2000-2002 and 25,3% in 2003-

2005. But unemployment figures mask the true impact of the economic decline as they don’t take

into consideration the amount of discouraged workers that left the labor force or are

underemployed. Not surprisingly, as consequence, poverty has been on the increase too, with the

poverty rate5 more than doubling following the outbreak of the intifada, reaching 46% by 2005-6.

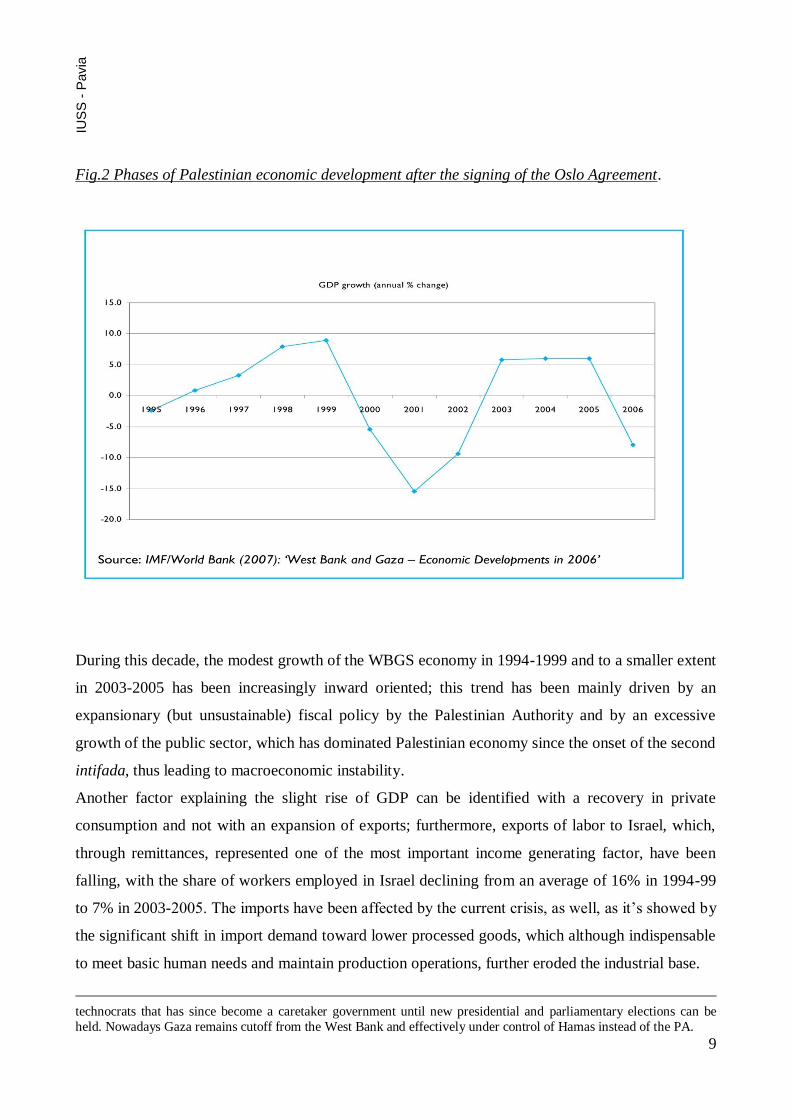

As can be read from figure 2, the post-Oslo period (1994-2005) witnessed three distinct phases in

economic development: a growth phase in 1994-1999, which extended into the outbreak of the

intifada; a consequent regression phase in 2000-2002, in which the economy contracted by 35%6;

and a relative recovery phase in 2003-2005, followed by another sharp decrease, as consequence to

the international response to the victory of Hamas in the parliamentary elections in January 2006,

that caused a steep drop of per capita GDP7.

5 The poverty rate identified the percentage of people earning less than 2$ per day. 6 World Bank , 2003: ― Twenty-Seven Months-Intifada, Closures and Palestinian Economic Crisis‖. WB Washington

DC. 7The PA’s long-standing fiscal crisis deepened further in 2006 as a result of Israel’s withholding of Palestinian

clearance revenues and the aid boycott, resulting in a deficit of over $1 billion. In June, Hamas took control of Gaza by

force and on June 17th, President Abbas dissolved the government and swore in an emergency government of

9

IUS

S -

Pavia

Fig.2 Phases of Palestinian economic development after the signing of the Oslo Agreement.

During this decade, the modest growth of the WBGS economy in 1994-1999 and to a smaller extent

in 2003-2005 has been increasingly inward oriented; this trend has been mainly driven by an

expansionary (but unsustainable) fiscal policy by the Palestinian Authority and by an excessive

growth of the public sector, which has dominated Palestinian economy since the onset of the second

intifada, thus leading to macroeconomic instability.

Another factor explaining the slight rise of GDP can be identified with a recovery in private

consumption and not with an expansion of exports; furthermore, exports of labor to Israel, which,

through remittances, represented one of the most important income generating factor, have been

falling, with the share of workers employed in Israel declining from an average of 16% in 1994-99

to 7% in 2003-2005. The imports have been affected by the current crisis, as well, as it’s showed by

the significant shift in import demand toward lower processed goods, which although indispensable

to meet basic human needs and maintain production operations, further eroded the industrial base.

technocrats that has since become a caretaker government until new presidential and parliamentary elections can be

held. Nowadays Gaza remains cutoff from the West Bank and effectively under control of Hamas instead of the PA.

10

IUS

S -

Pavia

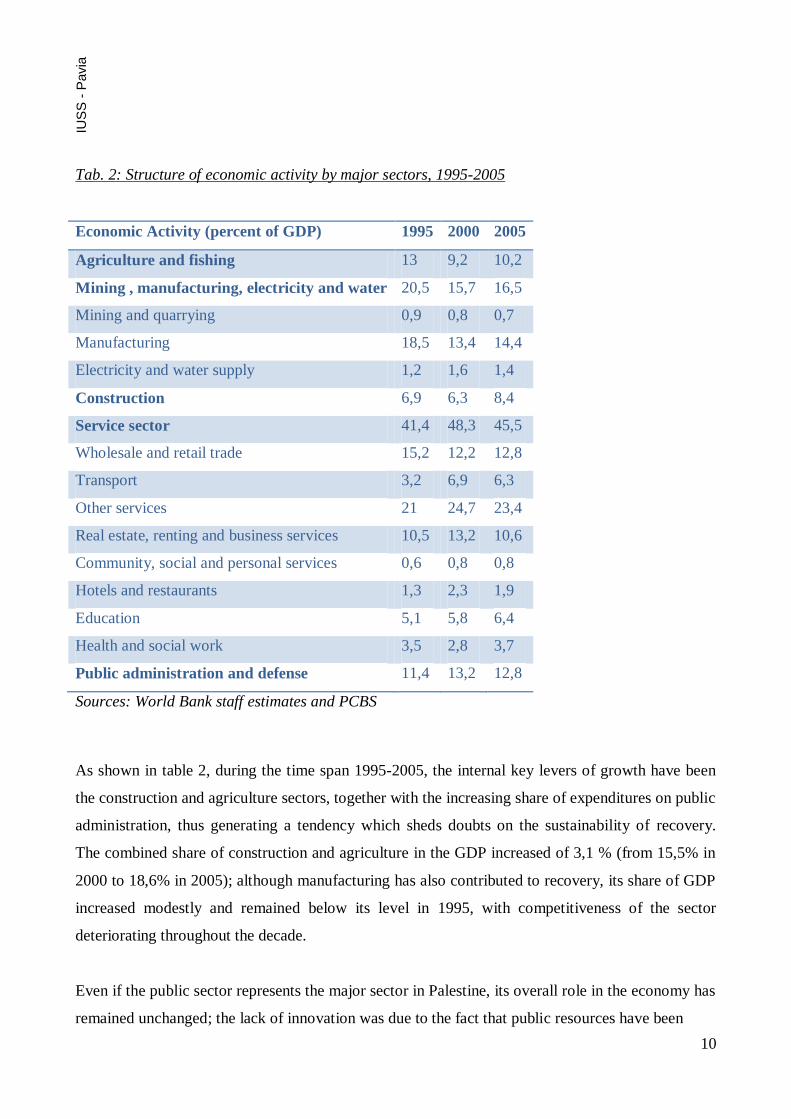

Tab. 2: Structure of economic activity by major sectors, 1995-2005

Economic Activity (percent of GDP) 1995 2000 2005

Agriculture and fishing 13 9,2 10,2

Mining , manufacturing, electricity and water 20,5 15,7 16,5

Mining and quarrying 0,9 0,8 0,7

Manufacturing 18,5 13,4 14,4

Electricity and water supply 1,2 1,6 1,4

Construction 6,9 6,3 8,4

Service sector 41,4 48,3 45,5

Wholesale and retail trade 15,2 12,2 12,8

Transport 3,2 6,9 6,3

Other services 21 24,7 23,4

Real estate, renting and business services 10,5 13,2 10,6

Community, social and personal services 0,6 0,8 0,8

Hotels and restaurants 1,3 2,3 1,9

Education 5,1 5,8 6,4

Health and social work 3,5 2,8 3,7

Public administration and defense 11,4 13,2 12,8

Sources: World Bank staff estimates and PCBS

As shown in table 2, during the time span 1995-2005, the internal key levers of growth have been

the construction and agriculture sectors, together with the increasing share of expenditures on public

administration, thus generating a tendency which sheds doubts on the sustainability of recovery.

The combined share of construction and agriculture in the GDP increased of 3,1 % (from 15,5% in

2000 to 18,6% in 2005); although manufacturing has also contributed to recovery, its share of GDP

increased modestly and remained below its level in 1995, with competitiveness of the sector

deteriorating throughout the decade.

Even if the public sector represents the major sector in Palestine, its overall role in the economy has

remained unchanged; the lack of innovation was due to the fact that public resources have been

11

IUS

S -

Pavia

increasingly allocated to wages, currently accounting for 95% of total expenditure. The period

2003-2005 witnessed two larges salary hikes8, despite the PA’s revenue fall, following the outbreak

of the intifada and the international boycott of the Hamas government, thus provoking a 20% rise in

the average wage rate in 2004 and a further 20% during the last quarter of 2005. The increase in the

wage bill appears to have acted countercyclical and helped to protect household incomes in times of

economic crisis; however, in particular during 2002-2003, the wage expenditure was quite far above

trend and in excess of what the cyclical downturn of the economy would have suggested;

expenditure in this sector may have contributed to social stability, but they did not contribute to

growth. Overall, continued rise of the expenditures during the intifada resulted in a rapid expansion

in the expenditure/GDP ratio, which was more than doubled during 1999-2005, reaching 49%, one

of the highest ratios in the world.

Palestinian economy is highly sensitive to external stimuli, as it’s confirmed by the fact that the

main indicators of the limited growth process in WBGS don’t generate from internal dynamics, but

are driven by external assistance and workers’ remittances from Israel, rather than increased local

productive capacities for tradable goods and productivity growth. This phenomenon of diverging

productivity between WBGS and Israel, is well documented by the economist S. Dessus,9 attesting

that the benefits of the integration of Palestinian economy with a much more highly developed

partner (Israel) have not materialized. The conditions necessary to allow a process of deeper

integration were not in place even before the intifada: the formal agreement that ruled the economic

relationship between Israel and WBGS (the so called Paris Protocol), signed in 1994 during the

Oslo peace process did not allow the development of the Palestinian economy; on the contrary, it

increased its level of dependency on the Jewish state, because of the establishment of a quasi-

custom union, characterized by the absence of internal borders and by the use of Israeli domestic

currency in the Occupied Territories. This form of integration has not generated economies-of-scale

effects and although WBG has remained under a single customs ―envelop‖, its economy has never

8 The first salary hike occurred in late 2003 as part of the wage increase envisaged when the Civil Service Law was implemented. The second round of salary increases benefited security service staff in particular relevant to civil

servants. 9 Sebastien Dessus, ―A Palestinian Growth History, 1968-2000‖ (Journal of Economic Integration, Vol. 19, N° 3, 2004)

12

IUS

S -

Pavia

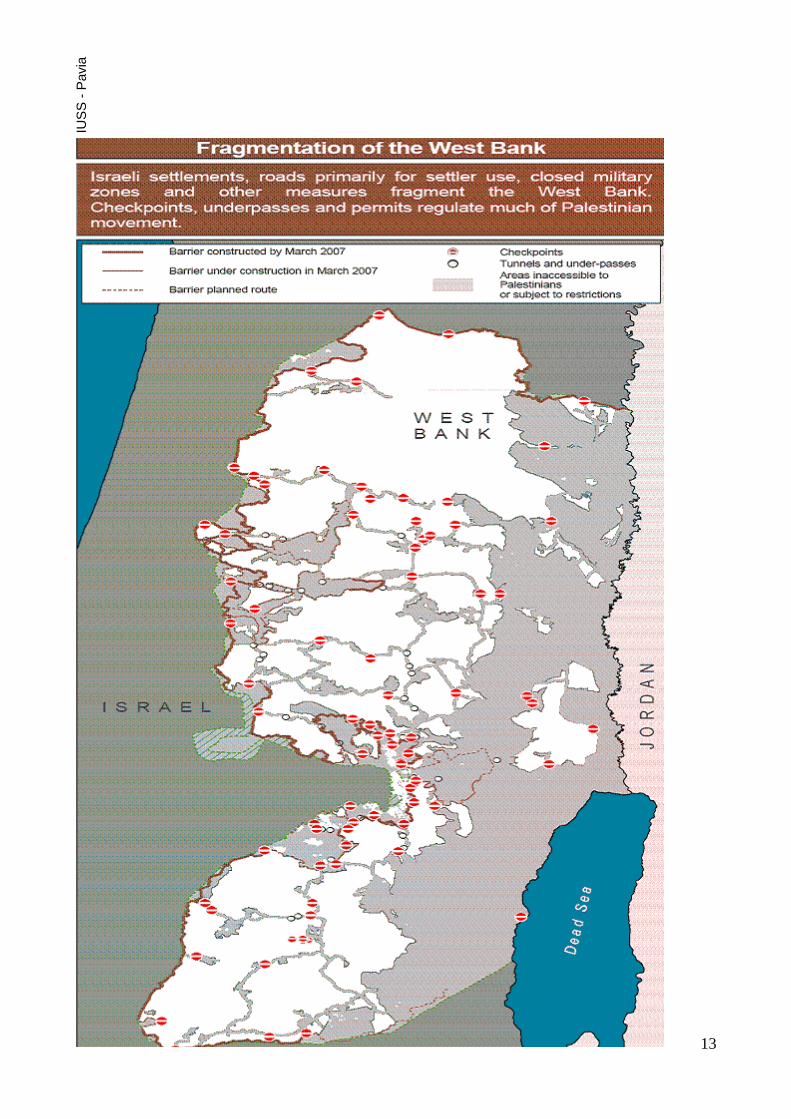

been a single economic space10

(the map on p. 12 clearly shows West Bank’s territorial

fragmentation).

The economy is effectively undergoing a process of ―de-development‖, connected with the

emerging of an autarchic economic structure, marked by the weakening of the economic

relationship both between Israel and WBG and inside of the Territories themselves. A de-developed

economy is characterized by a lack of productive capacities able to lead to structural change and

reforms: according to the economist Sara Roy11

, this phenomenon had been caused by a precise

Israeli strategy aiming at hindering the achievement of the economical and institutional changing,

necessary to originate a process of capital and investment accumulation in WBG: these policies,

defined ―integration and externalization‖ were based on the appropriation of Palestinian resources

and on the employment of cheap unskilled Palestinian labor in Israel; the long term effect of this

trend was the impossibility of building a solid industrial base and of an efficient infrastructure; in

addition to that, a process of enclavisation12

originated as result of the decrease of the economic

activities following the Al-Aqsa intifada, thus hindering the creation of a viable Palestinian

economy.

10 Since borders’ controls have been in place not only between Israel and WBG , but also inside of the Occupied

Territories, the WBG has been de facto a two layered, if not multiple layered economy, because of the presence of

multiple checkpoints within its territory. 11 Roy Sara, 2001: ―Palestinian society and economy: the continued denial of a possibility” Journal of Palestine Studies XXX n°4 p. 5-20. 12 The term enclavisation describes a process of internal withdrawal and divarication of the economy, of detachment

from international commercial relationships and the return to traditional activities and modes of production.

13

IUS

S -

Pavia

14

IUS

S -

Pavia

4.The structure of trade

“The trade regime in the Paris Protocol was designed solely to serve passing political purposes;

while the political design was obscure, the Protocol exhibited the same characteristics in the

economic arrangements. This created uncertainty of nature and an extent that would make it

impossible for any economic system to function properly”.

Nu’man Kanafani13

The Palestinian Territories are characterized by a high degree of openness to international trade.

According to the PCBS data, during the last decade imports of final goods, services, equipment and

intermediate inputs used in domestic production represented approximately 70% of GDP, while

exports of goods and services represented between 15 and 20% of GDP. Such large degree of

openness, considering that Israel constitutes the most important source of Palestinian imports and

the largest market for its exports, leaves West Bank and Gaza vulnerable to the economic policies

and strategies of the occupying government. Israeli restrictions on the movement of both labor and

goods have affected the regular flow of Palestinian exports and imports, resulting in massive

distortions in the economy, including the loss of external markets, shrinkage and fragmentation of

internal markets between major cities, increased transaction costs, risk, uncertainties, and so on. In

fact, even if in 1995 the PNA replaced the Israeli Civil Administration in ruling economic activities

in WBG, the Palestinian economy remains totally contained by Israel14

; estimates from the World

Bank Report 2006 indicate that total restricted areas represent more than the 50% of the West Bank.

The lack of territorial contiguity within the West Bank is the most evident sign of a fragmented

economy: besides the physical impediments, that are clear manifestations of the policy of closures,

the Israeli government set up a series of more complex restrictions, rooted in military orders

associated with the occupation, based on a set of administrative practices and permit policies which

limit the freedom of movement, of obtaining a job, of investing capital; they are used to bar

Palestinians from accessing large segments of the West Bank including all areas within the

13 N. Kanafani: ―Economic Aspects of the Israeli-Palestinian Conflict‖. The Economic Journal, 111. June 2001 14 The Paris Protocol on Economic Relations between the Government of Israel and the PLO Representing the Palestinian People, signed in Paris the 28/04/1994, outlines the Palestinian autonomous sphere of competences and the

rules regulating economic relationships with Israel. The main issues of the protocol deal with trade, labour market and

fiscal system.

15

IUS

S -

Pavia

municipal boundary of the settlements, the Jordan Valley, East Jerusalem, restricted roads and other

military ―closed‖ areas.

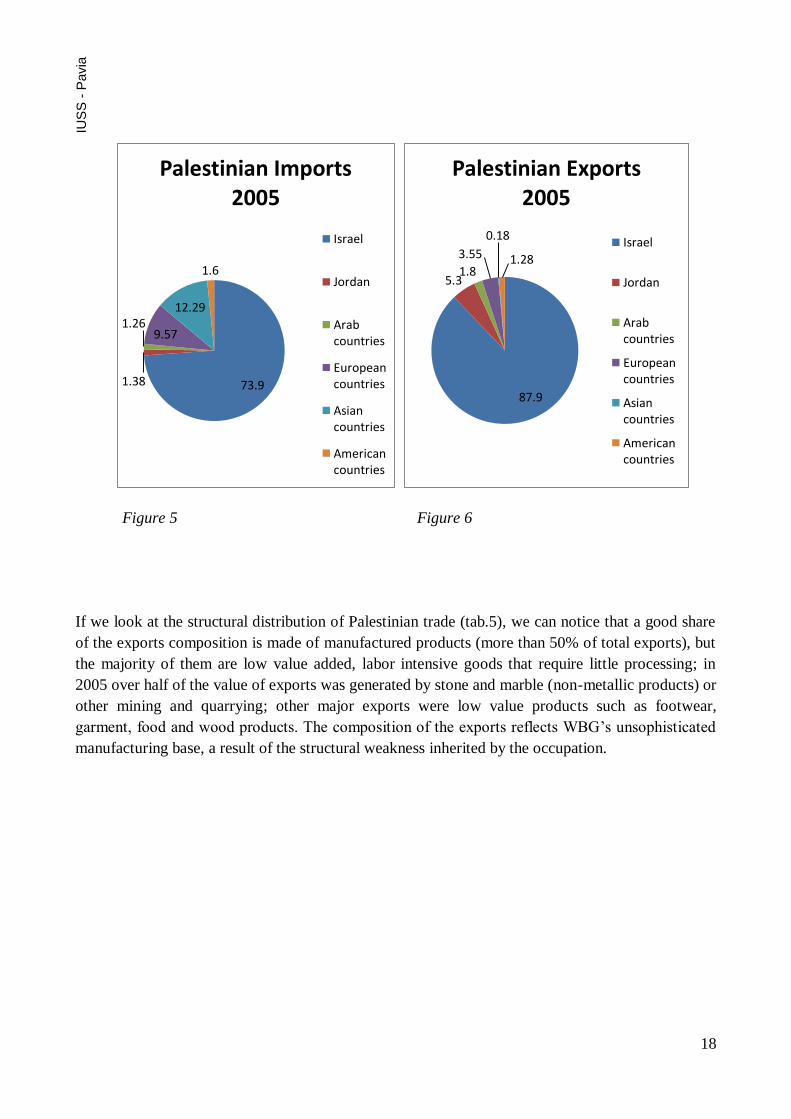

As indicated by table 3 and in figures 3 and 4, in 1999 Israel accounted for 71% of total Palestinian

imports and 97% of total exports. By comparison Jordan, the second most important trade partner,

had a meager share of 2,3%, while other markets accounted for insignificant shares: Palestinian

exports to Arab countries constituted less than 1% of total exports, showing a sharp decrease in

comparison with the 80s, when they accounted for more than 30% of the total export. On the

regional level, Europe was the most important source of non-Israeli imports, with more than 15% of

the total value of Palestinian imports in 1999. This strong level of dependence on the Israeli

economy became deeper and deeper in the following years, thus further slowing down the

capability of autonomous trade policy decision of the PA.

Tab. 3: Trade partners of the Palestinian Territory by value of trade, 1999

Region Imports Exports Total Trade

Millions of US$ % Millions of US$ % Millions of US$ %

Israel 1.853,6 70,5 360,4 96,9 2.214,1 73,8

Jordan 59,8 2,3 8,4 2,3 68,3 2,3

Total Arab countries 73,9 2,8 9,6 2,6 83,5 2,8

European countries 405,9 15,4 1,5 0,4 407,4 13,6

Asian countries 193,9 7,4 0 0 194 6,5

American countries 56, 5 2,1 0,4 0,1 56,9 1,9

Total Trade 2.629 100 372,1 100 3.001,1 100

Source: PCBS, ―Statistical Abstract of Palestine N. 2‖ November 2001

16

IUS

S -

Pavia

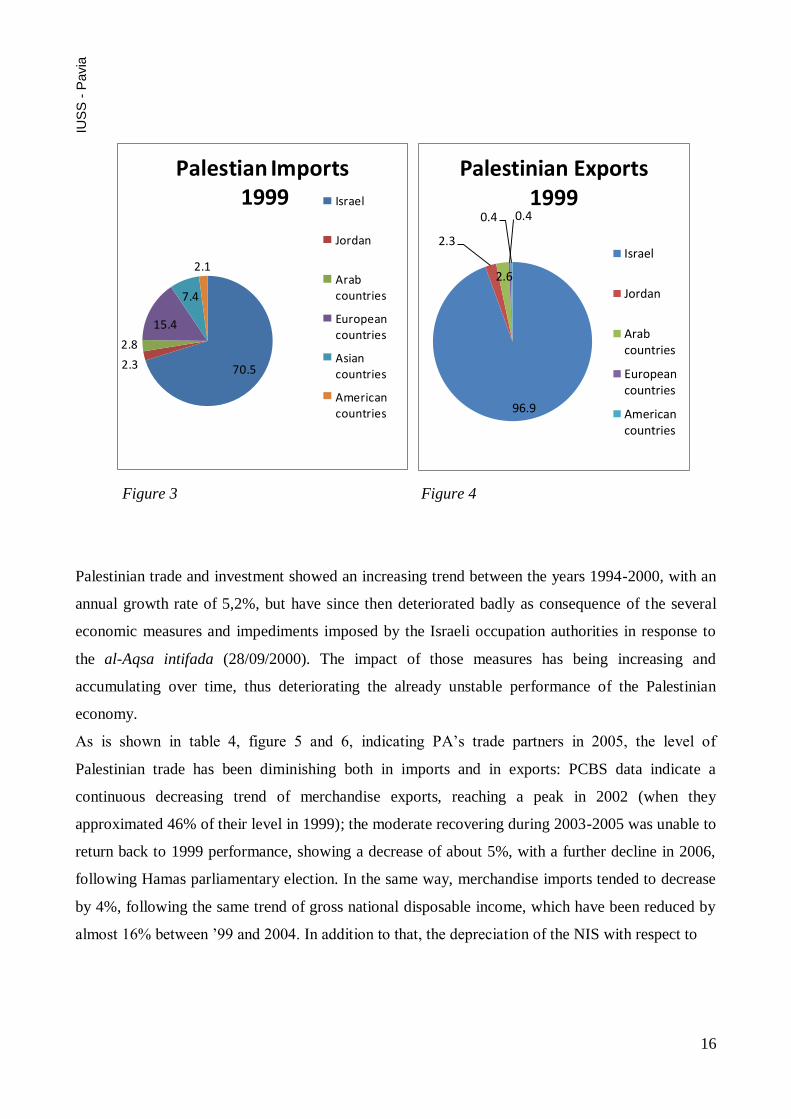

70.52.3

2.8

15.4

7.4

2.1

Palestian Imports1999 Israel

Jordan

Arab countries

European countries

Asian countries

American countries 96.9

2.3

2.6

0.40.4

Palestinian Exports 1999

Israel

Jordan

Arab countries

European countries

American countries

Figure 3 Figure 4

Palestinian trade and investment showed an increasing trend between the years 1994-2000, with an

annual growth rate of 5,2%, but have since then deteriorated badly as consequence of the several

economic measures and impediments imposed by the Israeli occupation authorities in response to

the al-Aqsa intifada (28/09/2000). The impact of those measures has being increasing and

accumulating over time, thus deteriorating the already unstable performance of the Palestinian

economy.

As is shown in table 4, figure 5 and 6, indicating PA’s trade partners in 2005, the level of

Palestinian trade has been diminishing both in imports and in exports: PCBS data indicate a

continuous decreasing trend of merchandise exports, reaching a peak in 2002 (when they

approximated 46% of their level in 1999); the moderate recovering during 2003-2005 was unable to

return back to 1999 performance, showing a decrease of about 5%, with a further decline in 2006,

following Hamas parliamentary election. In the same way, merchandise imports tended to decrease

by 4%, following the same trend of gross national disposable income, which have been reduced by

almost 16% between ’99 and 2004. In addition to that, the depreciation of the NIS with respect to

17

IUS

S -

Pavia

the US$ and the Euro has resulted in a cut of imports from both Europe (-37%) and the United

States (-23,8%)15

.

Furthermore, the increased dependency of Palestinian economy on Israel can be attested by two

indicators:

the proportion of Palestinian direct imports from Israel: total imports rose from 70% to

almost 74%;

the trade deficit: it has widened over time, due to the percentages of reduction in exports

which have been greater than those in imports.

Tab. 4: Trade partners of the Palestinian Territory by value of trade, 2005

Region Imports Exports Total trade

Millions of US$ % Millions of US$ % Millions of US$ %

Israel 1.872,8 73,9 290,55 87,9 2163,35 75,7

Jordan 35,12 1,38 17,46 5,3 52,58 1,83

Total Arab Countries 32,12 1,26 5,8 1,8 37,92 1,32

European Countries 242,35 9,57 11,73 3.55 254,08 8,8

Asian Countries 311,25 12,29 0,6 0,18 311,85 10,8

American countries 38,22 1,6 4,2 1,28 42,42 1,48

Total trade 2531,86 100 330.34 100 2862,2 100

Sources: PCBS ― Total Value of Exports from Remaining West Bank*16

and Gaza Strip by Country

of Destination and SITC. Total Value of Imports for Remaining West Bank* and Gaza Strip by

Country of Origin and SITC‖. 3 Divisions in 2005.

15 PCBS, Palestinian Foreign Trade Statistic, various issues, 1996-2004. 16

* Remaining west Bank refers to all West Bank excluding those parts of Jerusalem which were annexed by Israel in 1967.

18

IUS

S -

Pavia

73.91.38

1.269.57

12.29

1.6

Palestinian Imports 2005

Israel

Jordan

Arab countries

European countries

Asian countries

American countries

87.9

5.31.8

3.55

0.18

1.28

Palestinian Exports 2005

Israel

Jordan

Arab countries

European countries

Asian countries

American countries

Figure 5 Figure 6

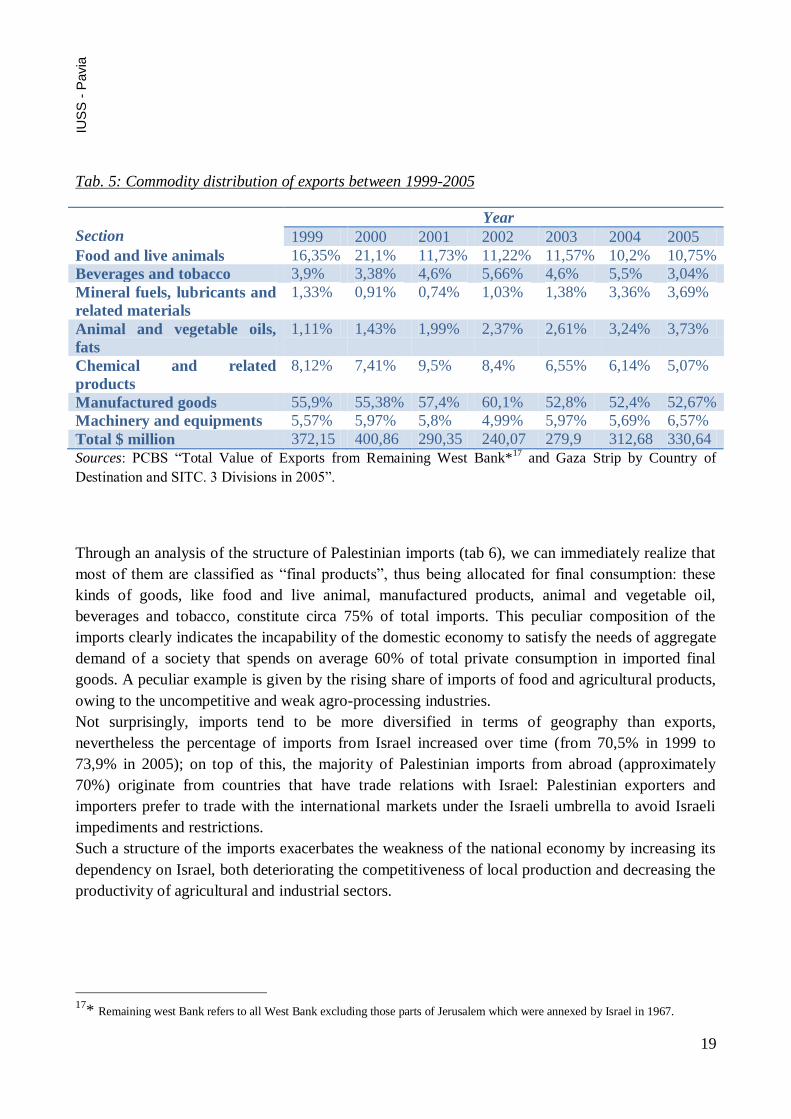

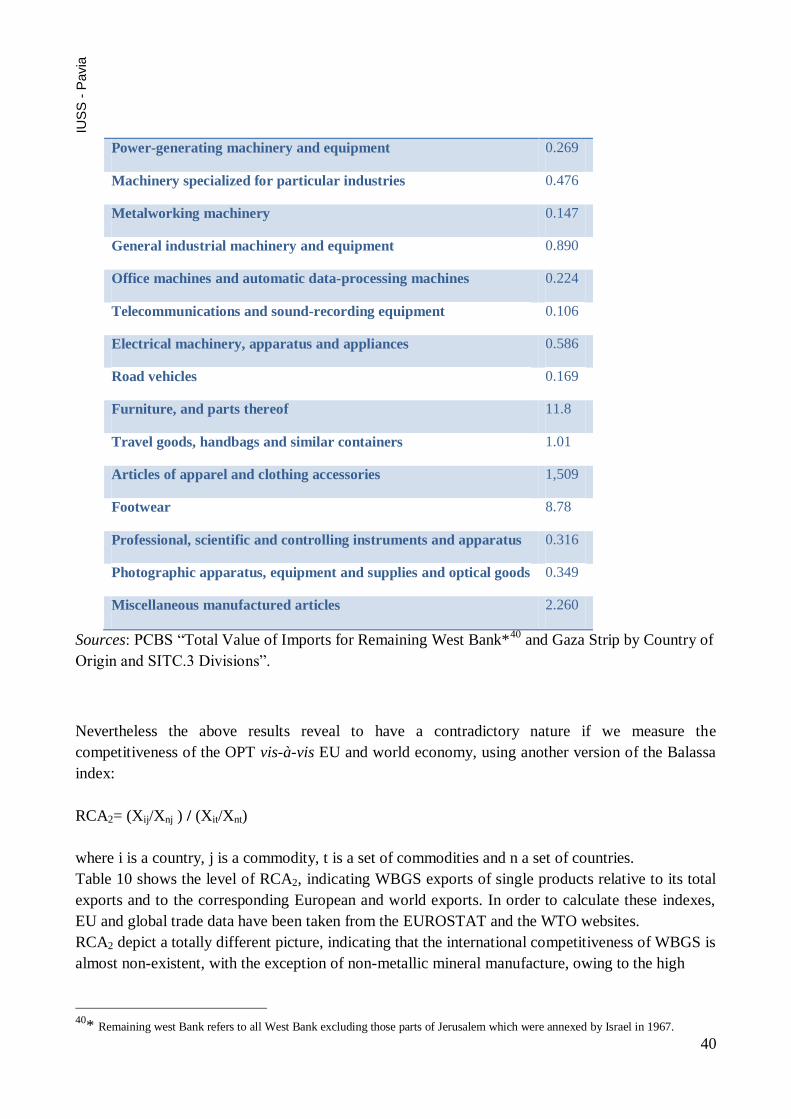

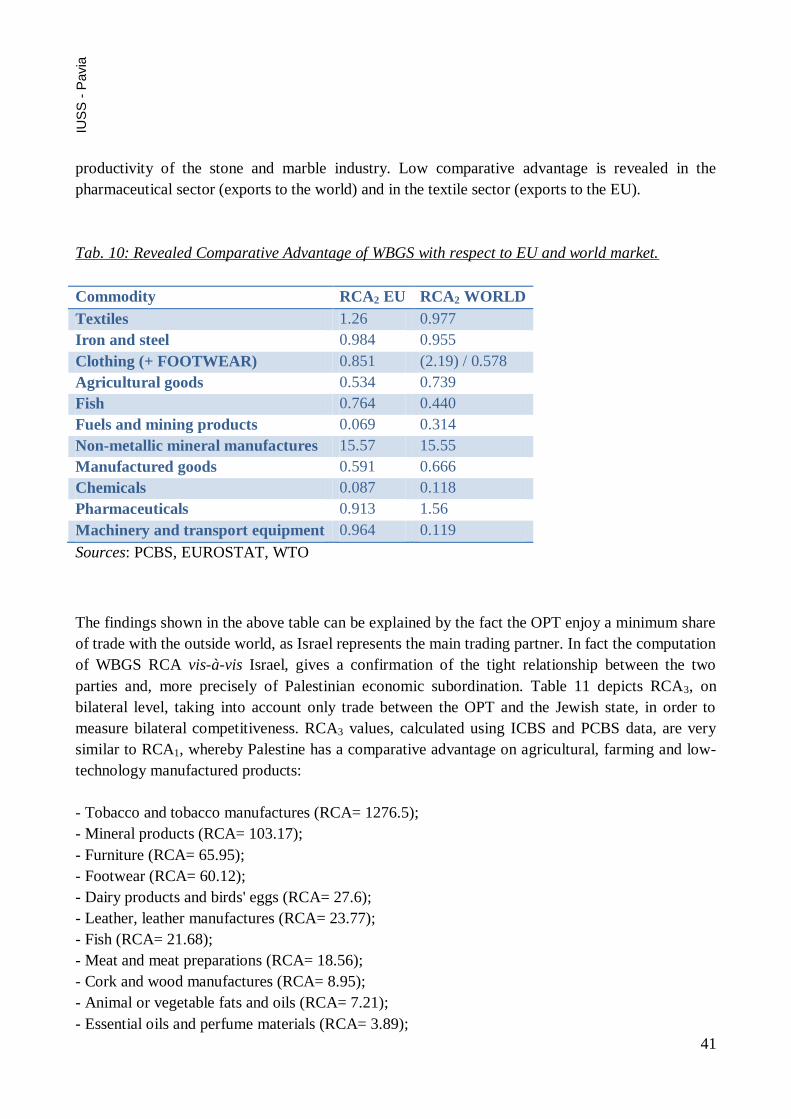

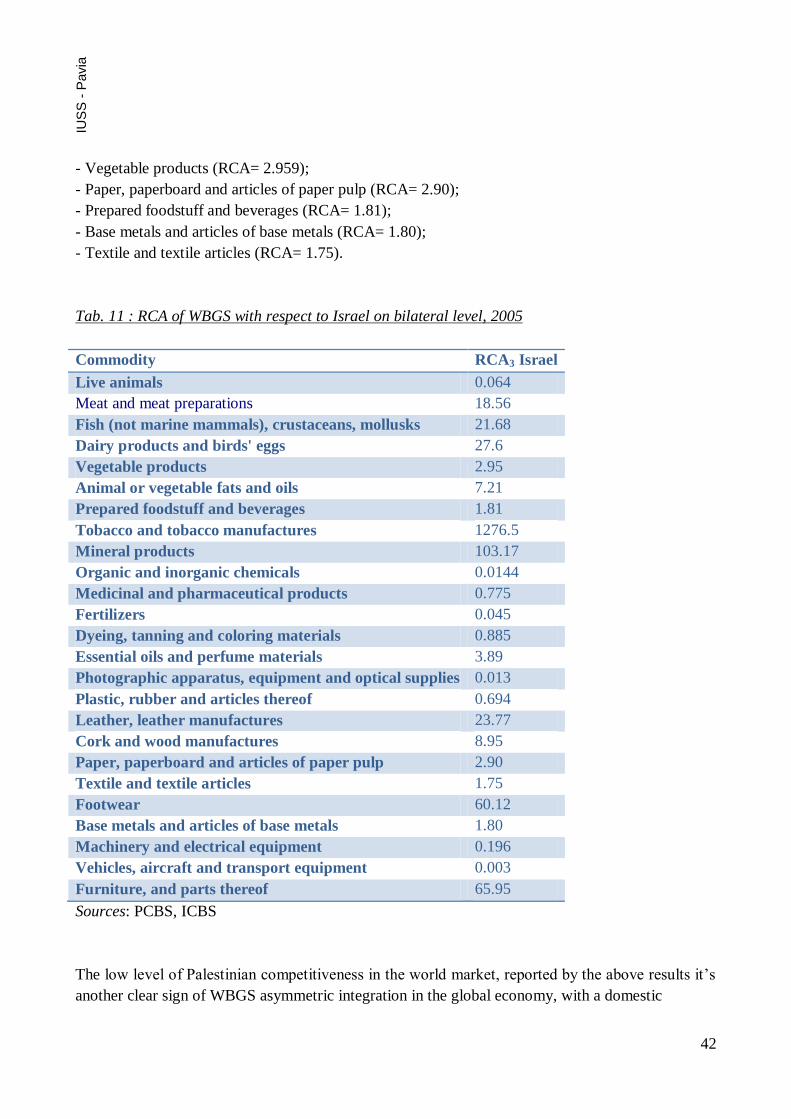

If we look at the structural distribution of Palestinian trade (tab.5), we can notice that a good share

of the exports composition is made of manufactured products (more than 50% of total exports), but

the majority of them are low value added, labor intensive goods that require little processing; in

2005 over half of the value of exports was generated by stone and marble (non-metallic products) or

other mining and quarrying; other major exports were low value products such as footwear,

garment, food and wood products. The composition of the exports reflects WBG’s unsophisticated

manufacturing base, a result of the structural weakness inherited by the occupation.

19

IUS

S -

Pavia

Tab. 5: Commodity distribution of exports between 1999-2005

Section

Year

1999 2000 2001 2002 2003 2004 2005

Food and live animals 16,35% 21,1% 11,73% 11,22% 11,57% 10,2% 10,75%

Beverages and tobacco 3,9% 3,38% 4,6% 5,66% 4,6% 5,5% 3,04%

Mineral fuels, lubricants and

related materials

1,33% 0,91% 0,74% 1,03% 1,38% 3,36% 3,69%

Animal and vegetable oils,

fats

1,11% 1,43% 1,99% 2,37% 2,61% 3,24% 3,73%

Chemical and related

products

8,12% 7,41% 9,5% 8,4% 6,55% 6,14% 5,07%

Manufactured goods 55,9% 55,38% 57,4% 60,1% 52,8% 52,4% 52,67%

Machinery and equipments 5,57% 5,97% 5,8% 4,99% 5,97% 5,69% 6,57%

Total $ million 372,15 400,86 290,35 240,07 279,9 312,68 330,64

Sources: PCBS ―Total Value of Exports from Remaining West Bank*17

and Gaza Strip by Country of

Destination and SITC. 3 Divisions in 2005‖.

Through an analysis of the structure of Palestinian imports (tab 6), we can immediately realize that

most of them are classified as ―final products‖, thus being allocated for final consumption: these

kinds of goods, like food and live animal, manufactured products, animal and vegetable oil,

beverages and tobacco, constitute circa 75% of total imports. This peculiar composition of the

imports clearly indicates the incapability of the domestic economy to satisfy the needs of aggregate

demand of a society that spends on average 60% of total private consumption in imported final

goods. A peculiar example is given by the rising share of imports of food and agricultural products,

owing to the uncompetitive and weak agro-processing industries.

Not surprisingly, imports tend to be more diversified in terms of geography than exports,

nevertheless the percentage of imports from Israel increased over time (from 70,5% in 1999 to

73,9% in 2005); on top of this, the majority of Palestinian imports from abroad (approximately

70%) originate from countries that have trade relations with Israel: Palestinian exporters and

importers prefer to trade with the international markets under the Israeli umbrella to avoid Israeli

impediments and restrictions.

Such a structure of the imports exacerbates the weakness of the national economy by increasing its

dependency on Israel, both deteriorating the competitiveness of local production and decreasing the

productivity of agricultural and industrial sectors.

17

* Remaining west Bank refers to all West Bank excluding those parts of Jerusalem which were annexed by Israel in 1967.

20

IUS

S -

Pavia

Tab. 6: Commodity distribution merchandise imports between 1999 – 2005

Section

Year

1999 2000 2001 2002 2003 2004 2005

Food and live animals 23,6% 18,12% 20,1% 19,65% 18,8% 16,2% 15,56%

Beverages and tobacco 3,11% 4,27% 4,77% 5% 5,03% 4,58% 4,04%

Mineral fuels, lubricant and

related materials

14,79% 19,12% 18,6% 23,8% 16,1% 19,7% 21,6%

Chemical and related

products

5,53% 8,75% 6,4% 6,1% 5,5% 4,9% 5,53%

Manufactured goods 20,65% 21,91% 24,5% 19,13% 27,3% 26,2% 31,2%

Machinery and transport

equipment

18,05% 14,8% 12,2% 11,9% 10,3% 10,15% 10,55%

Total $ million 2629 2382,8 2033,7 1515,6 1800,27 2373,24 2531,86

Sources: PCBS ―Total Value of Imports for Remaining West Bank*18

and Gaza Strip by Country of

Origin and SITC.3 Divisions‖.

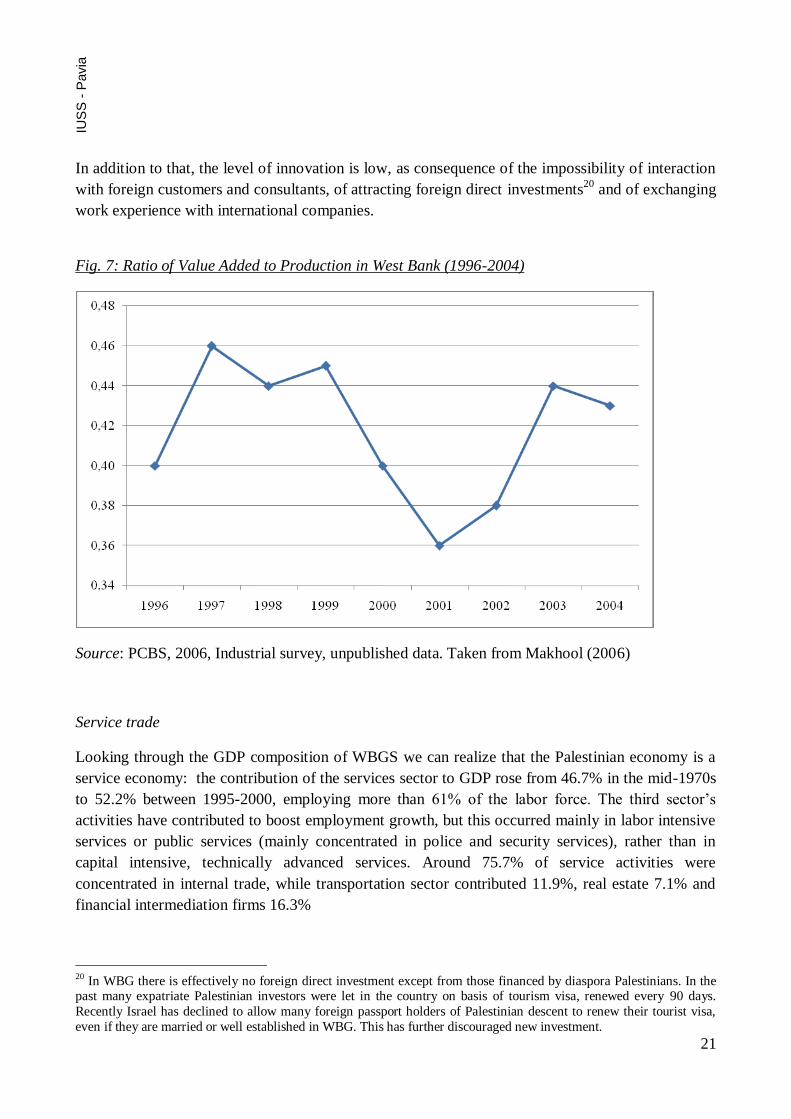

The most used indicator to measure the efficiency of a sector of the economy is given by the ratio of

value added to output; as shown in figure 7, in the industrial sector this indicator declined from

around 40 in 1996 to 37 in 2001; the slight recover in 2004 was not enough to guarantee a good

degree of competitiveness in the world market.

Competitiveness is calculated as the ratio of value added to wages: it measures the value added

obtained by one dollar in wages. In the West Bank and Gaza there was a sharp decline in 2000-2002

followed by a slight recovery in 2003-2004, clearly showing the lack of competitiveness of

Palestinian goods, particularly in labor intensive products: for example average wage productivity

in Palestinian industry is only 57% of Egypt’s and 85% of Israel’s. The level of Palestinian wages,

which is higher than those of the neighboring countries, owing to the influence of the Israeli market,

constitutes one of the main impediments to competitiveness, with particular distortive effects in

those sectors that could have comparative advantages.

Furthermore, one of the most important explanations for the low productivity of Palestinian

enterprises is due to their small size, that doesn’t allow them to attain economies of scale; the

economy has a fragmented industrial base, with 90% of the establishments employing fewer than 5

employees, mainly involved in producing labor intensive manufactured goods. As a result, the trade

sector entails an expending deficit and an excessive leakage19

of economic resources to Israel.

18

* Remaining west Bank refers to all West Bank excluding those parts of Jerusalem which were annexed by Israel in 1967. 19 The term leakage reflects the degree to which economic resources are channeled out of the economy to the rest of the world through the persistence of the current account deficit. The larger the deficit, the higher the degree of leakage and

the higher the degree of dependence on imports to satisfy domestic demand. The important issue in case of Palestine is

that a substantial portion of this leakage is concentrated with Israel.

21

IUS

S -

Pavia

In addition to that, the level of innovation is low, as consequence of the impossibility of interaction

with foreign customers and consultants, of attracting foreign direct investments20

and of exchanging

work experience with international companies.

Fig. 7: Ratio of Value Added to Production in West Bank (1996-2004)

Source: PCBS, 2006, Industrial survey, unpublished data. Taken from Makhool (2006)

Service trade

Looking through the GDP composition of WBGS we can realize that the Palestinian economy is a

service economy: the contribution of the services sector to GDP rose from 46.7% in the mid-1970s

to 52.2% between 1995-2000, employing more than 61% of the labor force. The third sector’s

activities have contributed to boost employment growth, but this occurred mainly in labor intensive

services or public services (mainly concentrated in police and security services), rather than in

capital intensive, technically advanced services. Around 75.7% of service activities were

concentrated in internal trade, while transportation sector contributed 11.9%, real estate 7.1% and

financial intermediation firms 16.3%

20 In WBG there is effectively no foreign direct investment except from those financed by diaspora Palestinians. In the past many expatriate Palestinian investors were let in the country on basis of tourism visa, renewed every 90 days.

Recently Israel has declined to allow many foreign passport holders of Palestinian descent to renew their tourist visa,

even if they are married or well established in WBG. This has further discouraged new investment.

22

IUS

S -

Pavia

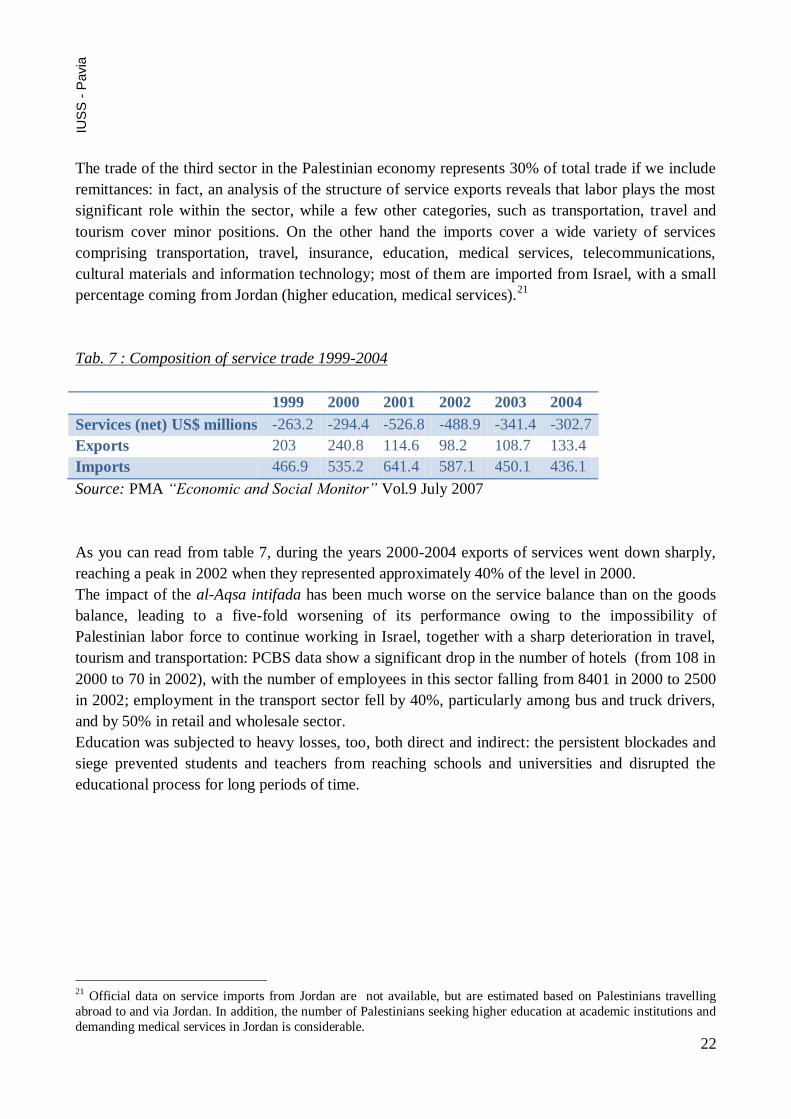

The trade of the third sector in the Palestinian economy represents 30% of total trade if we include

remittances: in fact, an analysis of the structure of service exports reveals that labor plays the most

significant role within the sector, while a few other categories, such as transportation, travel and

tourism cover minor positions. On the other hand the imports cover a wide variety of services

comprising transportation, travel, insurance, education, medical services, telecommunications,

cultural materials and information technology; most of them are imported from Israel, with a small

percentage coming from Jordan (higher education, medical services).21

Tab. 7 : Composition of service trade 1999-2004

1999 2000 2001 2002 2003 2004

Services (net) US$ millions -263.2 -294.4 -526.8 -488.9 -341.4 -302.7

Exports 203 240.8 114.6 98.2 108.7 133.4

Imports 466.9 535.2 641.4 587.1 450.1 436.1

Source: PMA “Economic and Social Monitor” Vol.9 July 2007

As you can read from table 7, during the years 2000-2004 exports of services went down sharply,

reaching a peak in 2002 when they represented approximately 40% of the level in 2000.

The impact of the al-Aqsa intifada has been much worse on the service balance than on the goods

balance, leading to a five-fold worsening of its performance owing to the impossibility of

Palestinian labor force to continue working in Israel, together with a sharp deterioration in travel,

tourism and transportation: PCBS data show a significant drop in the number of hotels (from 108 in

2000 to 70 in 2002), with the number of employees in this sector falling from 8401 in 2000 to 2500

in 2002; employment in the transport sector fell by 40%, particularly among bus and truck drivers,

and by 50% in retail and wholesale sector.

Education was subjected to heavy losses, too, both direct and indirect: the persistent blockades and

siege prevented students and teachers from reaching schools and universities and disrupted the

educational process for long periods of time.

21 Official data on service imports from Jordan are not available, but are estimated based on Palestinians travelling

abroad to and via Jordan. In addition, the number of Palestinians seeking higher education at academic institutions and

demanding medical services in Jordan is considerable.

23

IUS

S -

Pavia

5. Trade agreements

The viability of the Palestinian economy will continue to depend on the nature of its trade relations

with the outside world: the central question that needs to be answered is what is the optimal trade

arrangement that can exist between the WBGS and Israel as well as between the WBGS and the rest

of the world, keeping in mind that Israel remains today the biggest market for Palestinian imports

and exports: in fact the application of the Paris Protocol, creating a quasi-custom union between

WBGS and Israel, prevented Palestinian products from enjoying the benefits of the agreements

signed between the PNA and other countries.

The Paris protocol

The current Palestinian trade regime is dominated by the ―Paris Protocol on Economic Relations

between the Government of Israel and the PLO Representing the Palestinian People”, established

in 1994 within the broader framework of the Oslo Agreement to govern the economic relationship

between Israel and the Occupied Territories. It establishes a quasi-custom union between the two

economies by identifying three lists of goods in order to let the two parties implement different

import-export policies, without fixing any commercial border between them. Nevertheless the

volume of merchandise that could be autonomously administered by the PA has been subjected to a

series of restrictions, as the types of importable goods have been subdivided in three different

categories:

- A1: foodstuff and agricultural products, with the exclusion of fresh fruit and vegetable can be

imported from Arab or Islamic countries in a maximum quantity of 50% of the domestic demand;

fertilizers, household machinery and construction industry machinery can be imported exclusively

from Jordan and Egypt for a maximum quantity of 30% of the domestic market.

- A2 : follows same rules of A1 but covers some imports from all over the word.

- B: capital goods for economic development, like machinery for industry and agriculture, are not

subjected to restrictions in quantity or in origin, but they have to conform to Israeli standard.

Furthermore, the Protocol establishes that the export of Palestinian goods must follow the

environmental, health and security standards in force in Israel. With the exception of some

merchandise such as vegetables, poultry, milk and eggs (subjected to quotas22

) the agreement

guarantees free movement of both agricultural and industrial products from both parts, without

applying any import tax.

The implementation of the guidelines of the Paris Protocol (PP) provoked an increase in the prices

of essential inputs of production, as well as Palestinian production that relied on imported inputs,

thus weakening the comparative advantage of the Palestinian products internally and abroad. A

further distortion caused by the quasi-custom union manifested itself when Israel liberalized its

trade in particular areas as part of fulfilling its promises to the World Trade Organization without

coordination with the Palestinian side.

22 Quotas are intended to protect Israeli goods from Palestinian competition. This measure is based on a unilateral

asymmetric decision, which doesn’t foresee the same treatment for Palestinian agricultural products.

24

IUS

S -

Pavia

Considering the status quo and the de facto trade regime, the PP appears outdated and inapplicable,

principally because of the absence of the main principle on which it was built: the freedom of

movements of people and goods between the OPT and Israel. The various policies implemented on

local basis that have rendered the PP inoperable can be so summarized:

the creation of additional barriers between the two markets, due to the expansion of the

settlements and to the roads leading to them, dividing the West Bank in cantons or

bantustan23

.

the restriction of entering the Jordan Valley for most Palestinian, dramatically limiting the

possibility of investing and of benefiting from this important agricultural region.

the ongoing economic boycott of the Gaza Strip, implemented through the de facto closure

of Karni/al Montar and Rafah Border Crossings, completely isolating it from any relation

with the outside world.

the unilateral creation of de facto non-agreed economic borders through the continued

separation of East Jerusalem from the West Bank, the complex system of areas and subareas

created by the separation wall and the checkpoints, exasperating the fragmentation of the

West Bank, depriving it from substantial sources of trade and commerce.

Trade and transport agreements between Egypt, Jordan and the PA

In addition to the Paris Protocol the PA has currently other bilateral agreements with Jordan and

Egypt; following the access on the Arab Free Trade Area (AFTA) in 2002, Palestine is also putting

efforts in fostering regional trade integration24

.

Palestinian trade with Jordan is regulated by two agreements:

o Preferential trade agreement, signed in 1995: it establishes a framework for cooperation in

the areas of trade, investment and transportation, providing for the elimination of non-tariff

trade barriers, optimizing transport and trade procedures25

.

o Transport agreement, signed in 2000: it exempts Palestinian and Jordanian trucks from

administrative fees. The two sides also signed a custom cooperation agreement in 2001

which fosters the exchange of administrative and technical expertise and the harmonization

of custom procedures.

The preferential trade agreement with Egypt, signed in 1998, establishes a coordination of national

custom procedures, including the exchange of customs information and technical expertise, in

addition to facilitating transit operation.

23 In the WBGS case the term bantustan indicates a limited area, from which Palestinians can go out only through a

permit granted by the Israeli authorities. 24 The League of Arab States decided to apply a special and differential treatment to Palestine, exempting its exports from custom tariffs and taxes with similar effect. However, those efforts were rendered invalid by existing non-tariff

barriers , poor transportation and trade infrastructure services. 25 The Protocol calls for mutual recognition of National standards for vehicles transporting goods in transit

25

IUS

S -

Pavia

The potential beneficial effects of these agreements, aimed at lowering the level of dependence of

the Palestinian trade from Israel, were nevertheless not set in motion for several reasons, the most

important of which can be identified by Israeli security measures at Palestinian borders; first of all,

all the exports and imports exit and entering the OPT need first to pass through the inspections of

Israeli crossing points. In the case of Gaza and West Bank exports travelling to or through Jordan,

after inspection at Israeli crossing points26

, they are escorted in convoys of 5-15 trucks by Israeli

security patrols up to the commercial crossing with Jordan. Trucks are then subjected to ―back to

back‖ procedures27

(see table below) for further inspection and then reloaded onto Jordanian trucks

before reaching their final destination.

The imports coming from Egypt or Jordan follow the same ―back to back‖ procedure and are

subjected to strict quota: the number of trucks crossing Allenby is limited to 50 a day, while those

from Egypt is limited to 25.

Other agreements have been signed by the PNA, but most of them don’t find a real application

unless the Israeli government has stipulated analogous accords: it is in fact impossible to import or

export to countries that don’t have a trade agreement with the occupier.

Trade with Saudi Arabia

Palestinian traders can export all types of products to Saudi Arabia, and in the mean time, the

government of Saudi Arabia grants duty free treatment to the following Palestinian products:

26 There are different border crossing points and re-export points between the Palestinian Territory and its neighboring

states: Rafah Border Crossing between Gaza and Egypt; Karni/Almontar Border Crossing connecting Gaza with the

West Bank and Israel; King Husseyn Bridge and Damya Bridge, between West Bank and Jordan‖; most of exports and imports flow through Eretz crossing, between Gaza and Israel. 27 During the back to back procedures goods are unloaded from Palestinian trucks, placed on the ground for inspection

and reloaded in Jordanian trucks.

“Back to Back” vs “Door to Door” A ―back-to-back‖ cargo movement is generally understood as the transfer of loose goods from

one truck to another, positioning two trucks with their backs to one another. Primitive variants

involve labor-intensive handling and placement of cargo on the ground during the transfer, thus

originating serious time delays and damages to cargo. Even if a modern ―back-to-back‖ system

which is less damaging than primitive one has been developed, thanks to the adoption of a

coordinated transfer across a level platform using mechanized equipment, it is not currently

used.

The concept of ―door to door‖, as envisioned by the Palestinian Authority, refers to the

movement of a cargo, intact and in a single vehicle, from the cargo’s point of origin to its

destination. Under this definition, door to door describes the movement of the vehicle and its

cargo, not simply the cargo—and is akin to what is seen in international agreements as a right of

transit.

26

IUS

S -

Pavia

agricultural products, livestock, metallic and non-metallic raw materials. At the same time imports

from Saudi Arabia is limited to items listed in A1 and A2.

In order to benefit from the preferential arrangement an official certificate of origin is required,

stamped accordingly by the Saudi Embassy in Jordan or Egypt , together with the official invoice.

The name of the producer, country of citizenship and the rule of origin should be clearly indicated

on the product.

Declaration of Free Trade between WBGS and the USA

Under the Palestinian-US Free Trade Agreement, duty free treatment is granted to all Palestinian

products entering the US and vice versa. In order to benefit from the duty free treatment, a

certificate of origin must accompany the goods.

Free Trade Arrangement between the Palestine Liberation Organization and Canada

According to the arrangement signed between the parties, tariffs were eliminated on industrial

products. For agricultural products and processed food, tariffs were reduced or eliminated in

accordance with quotas.

Interim Association Agreement on Trade and Cooperation between the European Union and the

Palestine Liberation Organization.

The interim association agreement on Trade and Cooperation grants reciprocal duty free treatment

on industrial products complying with the rule of origin. Concerning agricultural items, the

European Union grants duty free or reduced tariff treatment on the products exported to the EU

within quotas. The same applies on agricultural imports from the EU to the WBGS.

Interim Agreement between the EFTA States and the Palestine Liberation Organization

The following EFTA countries signed an interim agreement with the PLO: Iceland, Liechtenstein,

Norway and Switzerland. The Agreement provides duty free treatment to most Palestinian and

EFTA industrial products. Moreover, duty free is granted to some Palestinian and EFTA processed

agricultural products, while the majority of processed agricultural products are granted at a reduced

tariff. A duty free treatment is also granted to fish and other marine products. The PLO has signed

separate protocols with the four EFTA countries to identify the agricultural duty free products, as

EFTA countries do not share a common agricultural policy.

Agreement on Commercial Cooperation between the Palestine Liberation Organization and Russia

Both parties extend to one another the status of the Most Favored Nation in regard to trade.

Imports and exports between the two parties are duty free for the following goods:

Instruments and items specified for montage and repair.

Equipment and instruments specified for undertaking experiments and scientific research.

Articles for demonstration during fairs and exhibitions.

Containers and similar packages utilized in international trade on a return basis.

27

IUS

S -

Pavia

6. Indirect taxes28

―The imports and exports of Palestinians through the points of exit and entry in Israel will be given

equal trade and economic treatment”

Art. III (13) Paris Protocol

The territories of the West Bank and Gaza Strip live under the same custom envelop of Israel: for

this reason it’s impossible to speak about Palestinian trade policy, as it remains totally bound the

occupier’s trade strategy: Israeli tax rates, both direct and indirect, constitute the governing

guidelines, as are Israeli standards and import regulations.

According to the Paris Protocol, the PA should impose the same indirect taxes of Israel, including

the VAT, purchase taxes and custom duties on both domestic and imported goods. Furthermore,

under the Revenue Clearance System set in place through the Protocol, the Israeli government is

required to transfer to the PA all import duties on products destined to the Palestinian Territories: in

fact, only Israeli firms are licensed as clearing agents at the commercial borders with Jordan, Egypt

and Israel29

. Even if the accord establishes that the PA is responsible for the implementation of

clearance procedures at the main crossing points with Jordan and Egypt (though the situation

changed after the second intifada)30

, the largest portion of PA’s revenues is from imports coming

through Israel (80% of the goods are imported through the port of Ashod). These revenues are

collected by the Israeli authorities and then transferred to the PA on the basis of the import

document, which testifies the final destination of the products. Owing to the impossibility of setting

Palestinian clearing agencies to work on the borders, the Israeli government deducts from the

revenues a 3% administrative cost, to remunerate their work on behalf of the PA.

As outlined in the previous chapter, the PA is given the possibility of setting its own custom rates

only for the goods nominated in the lists A1 and A2, where, within defined quota, the approval of

the Israeli authorities is not required (according to this regulation, at present no customs are applied

to a series of imports, like cattle, dried yogurt and wheat). Another exception established by the

agreement concerns the purchase tax on cars, whereby the Israeli apply a 95% rate, while the

Palestinian 75%.

28 Most of the information provided by this chapter have been written thanks to the collaboration of Hatem Yousef,

Director General of Custom and Excise in the West Bank and Reuven Melzer, Senior Chief Coordinator of the

department of Customs and VAT in Israel. 29

The custom clearance procedure applied in the Occupied Territories is derived from the Israeli custom law, as the PA

doesn’t have a custom law of its own: it’s a combination of Israel regulations and bylaws, code no. 11 issued in 1929

and its amendments which apply in the Gaza Strip, the Jordanian Customs and Excise Act no.1 issued in 1962 and its

amendments that applied in the West Bank. 30 Article 14 of the Paris Protocol reads as follows: ― In the entry points of the Jordan river and the Gaza Strip (….) the

Palestinian Authority will have full responsibility and powers in the Palestinian custom point (freight area) for the

implementation of the agreed upon customs and importation policy as specified in this protocol, including the

inspection and the collection of taxes and other charges, when due. (…) The Palestinian custom official will be responsible for the handling of the customs procedures including the inspection and the collection of due taxes.‖ Since

September 2000 all entry points into the Palestinian Territories have been exclusively controlled by Israeli authorities,

making the above quoted provisions dead letter.

28

IUS

S -

Pavia

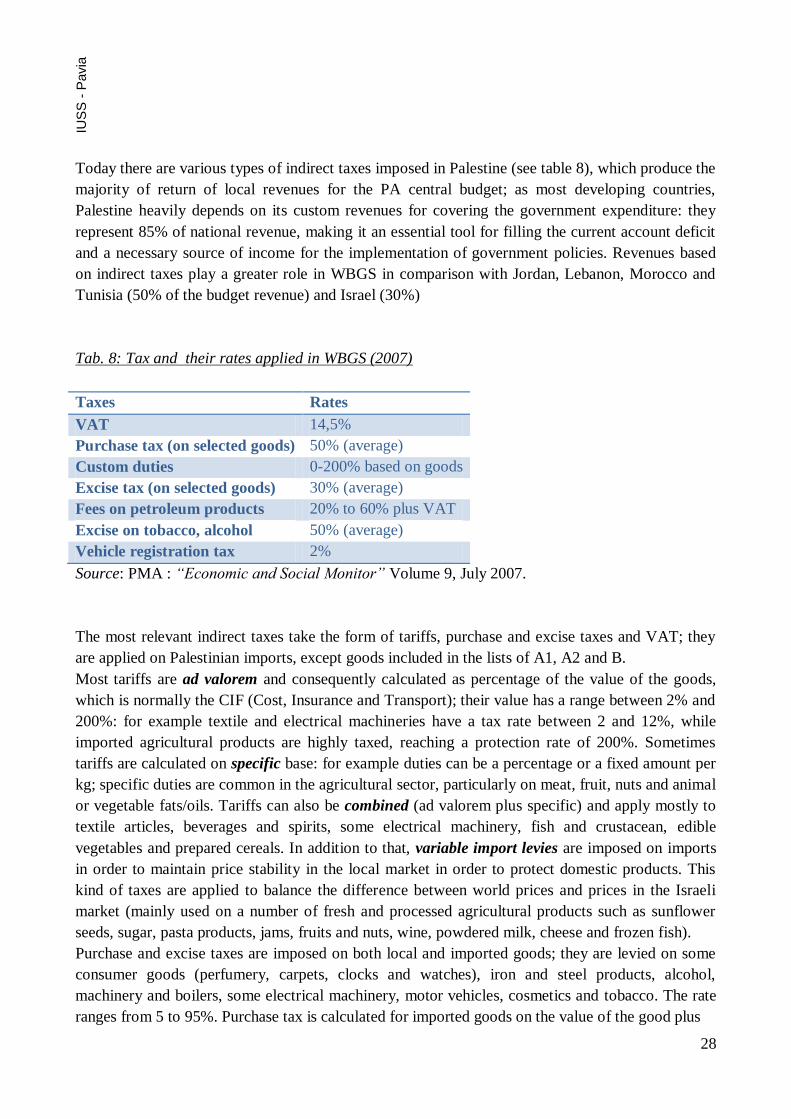

Today there are various types of indirect taxes imposed in Palestine (see table 8), which produce the

majority of return of local revenues for the PA central budget; as most developing countries,

Palestine heavily depends on its custom revenues for covering the government expenditure: they

represent 85% of national revenue, making it an essential tool for filling the current account deficit

and a necessary source of income for the implementation of government policies. Revenues based

on indirect taxes play a greater role in WBGS in comparison with Jordan, Lebanon, Morocco and

Tunisia (50% of the budget revenue) and Israel (30%)

Tab. 8: Tax and their rates applied in WBGS (2007)

Taxes Rates

VAT 14,5%

Purchase tax (on selected goods) 50% (average)

Custom duties 0-200% based on goods

Excise tax (on selected goods) 30% (average)

Fees on petroleum products 20% to 60% plus VAT

Excise on tobacco, alcohol 50% (average)

Vehicle registration tax 2%

Source: PMA : “Economic and Social Monitor” Volume 9, July 2007.

The most relevant indirect taxes take the form of tariffs, purchase and excise taxes and VAT; they

are applied on Palestinian imports, except goods included in the lists of A1, A2 and B.

Most tariffs are ad valorem and consequently calculated as percentage of the value of the goods,

which is normally the CIF (Cost, Insurance and Transport); their value has a range between 2% and

200%: for example textile and electrical machineries have a tax rate between 2 and 12%, while

imported agricultural products are highly taxed, reaching a protection rate of 200%. Sometimes

tariffs are calculated on specific base: for example duties can be a percentage or a fixed amount per

kg; specific duties are common in the agricultural sector, particularly on meat, fruit, nuts and animal

or vegetable fats/oils. Tariffs can also be combined (ad valorem plus specific) and apply mostly to

textile articles, beverages and spirits, some electrical machinery, fish and crustacean, edible

vegetables and prepared cereals. In addition to that, variable import levies are imposed on imports

in order to maintain price stability in the local market in order to protect domestic products. This

kind of taxes are applied to balance the difference between world prices and prices in the Israeli

market (mainly used on a number of fresh and processed agricultural products such as sunflower

seeds, sugar, pasta products, jams, fruits and nuts, wine, powdered milk, cheese and frozen fish).

Purchase and excise taxes are imposed on both local and imported goods; they are levied on some

consumer goods (perfumery, carpets, clocks and watches), iron and steel products, alcohol,

machinery and boilers, some electrical machinery, motor vehicles, cosmetics and tobacco. The rate

ranges from 5 to 95%. Purchase tax is calculated for imported goods on the value of the good plus

29

IUS

S -

Pavia

the amount of custom duty, applying the Tama System, which is called ―import increment rate‖:

Tama is the Hebrew acronym for import rate uplift and is a mark-up applied before calculating the

purchase tax31

.

The Value Added Tax is an indirect form of taxation on both locally produced and imported goods:

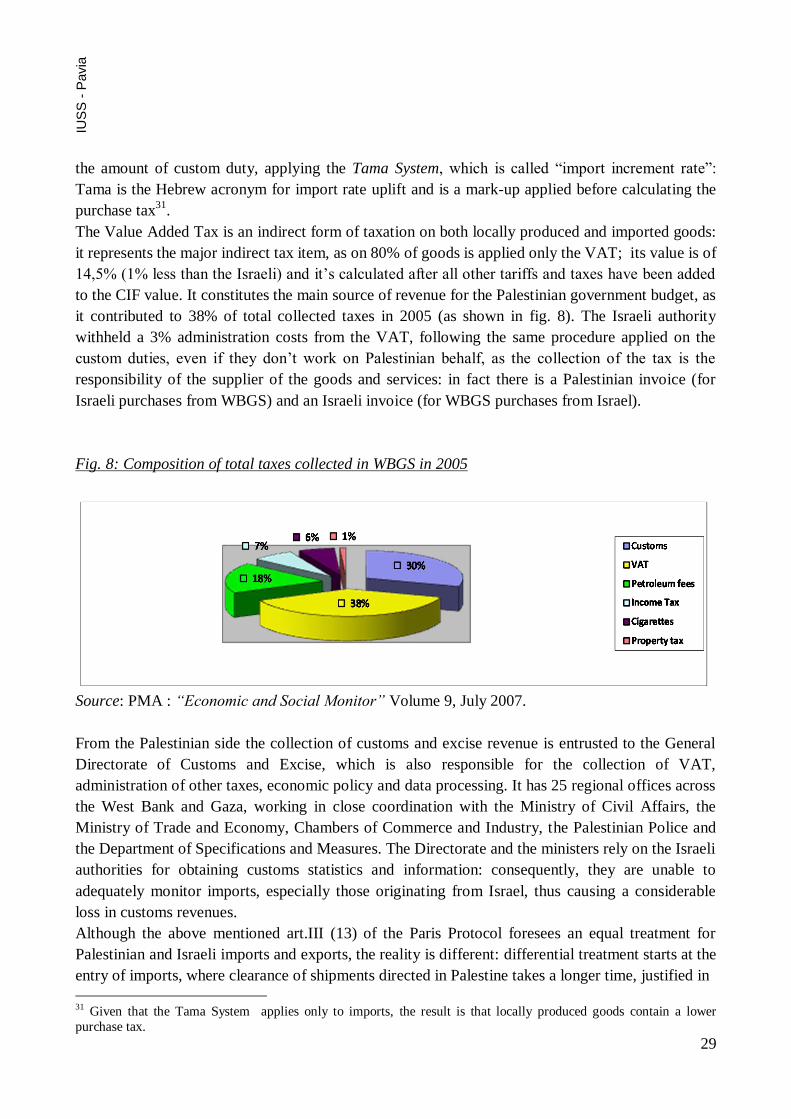

it represents the major indirect tax item, as on 80% of goods is applied only the VAT; its value is of

14,5% (1% less than the Israeli) and it’s calculated after all other tariffs and taxes have been added

to the CIF value. It constitutes the main source of revenue for the Palestinian government budget, as

it contributed to 38% of total collected taxes in 2005 (as shown in fig. 8). The Israeli authority

withheld a 3% administration costs from the VAT, following the same procedure applied on the

custom duties, even if they don’t work on Palestinian behalf, as the collection of the tax is the

responsibility of the supplier of the goods and services: in fact there is a Palestinian invoice (for

Israeli purchases from WBGS) and an Israeli invoice (for WBGS purchases from Israel).

Fig. 8: Composition of total taxes collected in WBGS in 2005

Source: PMA : “Economic and Social Monitor” Volume 9, July 2007.

From the Palestinian side the collection of customs and excise revenue is entrusted to the General

Directorate of Customs and Excise, which is also responsible for the collection of VAT,

administration of other taxes, economic policy and data processing. It has 25 regional offices across

the West Bank and Gaza, working in close coordination with the Ministry of Civil Affairs, the

Ministry of Trade and Economy, Chambers of Commerce and Industry, the Palestinian Police and

the Department of Specifications and Measures. The Directorate and the ministers rely on the Israeli

authorities for obtaining customs statistics and information: consequently, they are unable to

adequately monitor imports, especially those originating from Israel, thus causing a considerable

loss in customs revenues.

Although the above mentioned art.III (13) of the Paris Protocol foresees an equal treatment for

Palestinian and Israeli imports and exports, the reality is different: differential treatment starts at the

entry of imports, where clearance of shipments directed in Palestine takes a longer time, justified in

31 Given that the Tama System applies only to imports, the result is that locally produced goods contain a lower

purchase tax.

30

IUS

S -

Pavia

terms of security. A study of the World Bank32

certifies that Israeli imports face a risk of security

check of 15-20% (80-90% of Israeli imports are checked only through a computerized system),

whereas WBG importers face the certainty of security checks. Another study by the Confederation

of Palestinian Chamber of Commerce, Palestinian companies exporting through Haifa faced higher

costs (18%) and longer delays (20%) than comparable Israeli companies. As a result, in order to

avoid paying extra costs, because of border security measures, many companies directly purchase

goods imported into Israel by Israeli firms (following a subcontracting mechanism).

On top of this, importers and exporters from the West Bank are compelled to use Israeli transport

companies when goods are destined for WBGS or leaving WBGS through Israel. ―Back to back‖

system (see box pag.20) provokes additional transition costs, not only because of extra unloading

and loading operations but also because of extra time and possible losses in quality as a result of

rough handling.

According to the current structure of the taxing system three main issues can be raised, which

outline the necessity of modifying the current custom union agreement:

The absence of a Palestinian custom clearing authority gives the Israeli government the

possibility of exerting political pressure before handing over the collected funds to the PA

treasury: this situation took place in 2001-2002 and in 2006, where the occupier withheld

the tax revenues, motivating the decision with political reason. Considering that in WBGS

tax productivity is very high (three times higher than the average among Arab states) and

that tax revenue normally constitute about 20% of the total Palestinian GDP (compared to

8% of other Arab states), the Israeli decision of withholding tax revenues provoked a serious

unbalance in the government budget. At the moment most of those withheld funds have

been given back to the PA, even if some of the amount has been deducted to refund the

Israeli victims of the conflict33

.

Owing to the so called quasi-custom union system, the PA is experiencing relevant losses in

VAT revenues for the goods imported to Israel and then re-exported to Palestine, as the

VAT collected remains within the Israeli state; this practice is implemented owing to a

distortion of the original accord, which states that taxes should be collected according to

final destination of the goods; the Israeli authorities substituted the word destination with

the term declaration, thus withholding large amounts of money. According to World Bank

estimates, the lost revenues reach a sum of 174 million dollars per year.

The PA has lost custom duties, excise taxes and VAT on purchases which are not

documented by invoices. The fiscal leakage is estimated to be between 3 and 4.2% of GDP.

On this basis it is necessary to reconsider the structure of the Paris Protocol and to identify

alternative trade regimes which could generate better Palestinian economic outcomes than the

32 World Bank, 2006: ―West Bank and Gaza Country Economic Memorandum. Growth in the West Bank and Gaza:

Opportunities and Constraints”. Vol. 1 33 No parallel treatment has been offered to Palestinian victims.

31

IUS

S -

Pavia

existing custom union. The recent academicals debate concerning a revision of the current

agreement between Israel and the PNA sets on the ground different options:

a) an upgrading of the existing Paris Protocol, eliminating the above mentioned distortions;

b) a custom union within two independent states, effectively providing for free exchange of

goods between two independent states;

c) an agreement with the Most Favored Nation principle, which would give the WBGS the

same opportunity to reform its trade relation with both Israel and third parties under a

uniform approach;

d) a Free Trade Agreement, which would unable the OPT to amend their trade policy only

vis-à-vis third parties; it would require checking the origin of goods flowing between

WBGS and Israel to determine whether they are produced within the FTA (and as such

eligible if tax exemptions) or whether they are re-exports originating from third parties.

e) An Asymmetric Free Trade Area, which recognizes the existence of initial different

conditions and of asymmetrical relationships between countries: these factors are taken

into account and modify a pure form of FTA, fixing some commercial clauses. In the

Israeli-Palestinian case it could imply: fixing temporary favorable prices for WBGS,

independently from the FTA, stipulating independent trade agreements with third

partners and the implementation of protection mechanisms for infant industries.

32

IUS

S -

Pavia

7. Export of labor

The level of dependence of the Palestinian trade from the Israeli market grows much higher if we

take into account the role of remittances: since 1967 exports of labor from West Bank and Gaza

have been more important than exports of goods, as you can read from fig. 9, contributing to

finance a large trade deficit.

Fig. 9 Exports of Palestinian goods and services to Israel

The combination of large exports of labor, together with the limited investment in the industrial

sector and the absence of technology transfer, has undermined the competitiveness of WBGS

industrial sector (a phenomenon identified in economics with the term of Dutch disease) and limited

the potential for growth in the domestic labor productivity: in fact the possibility of a daily

commute to work in Israel increased the wage bill beyond the productivity growth. Even during the

phases of growth, the increase of Palestinian GDP was not export led, but rather driven by a rise in

consumption thanks to higher incomes deriving from remittances. The increase in number of jobs

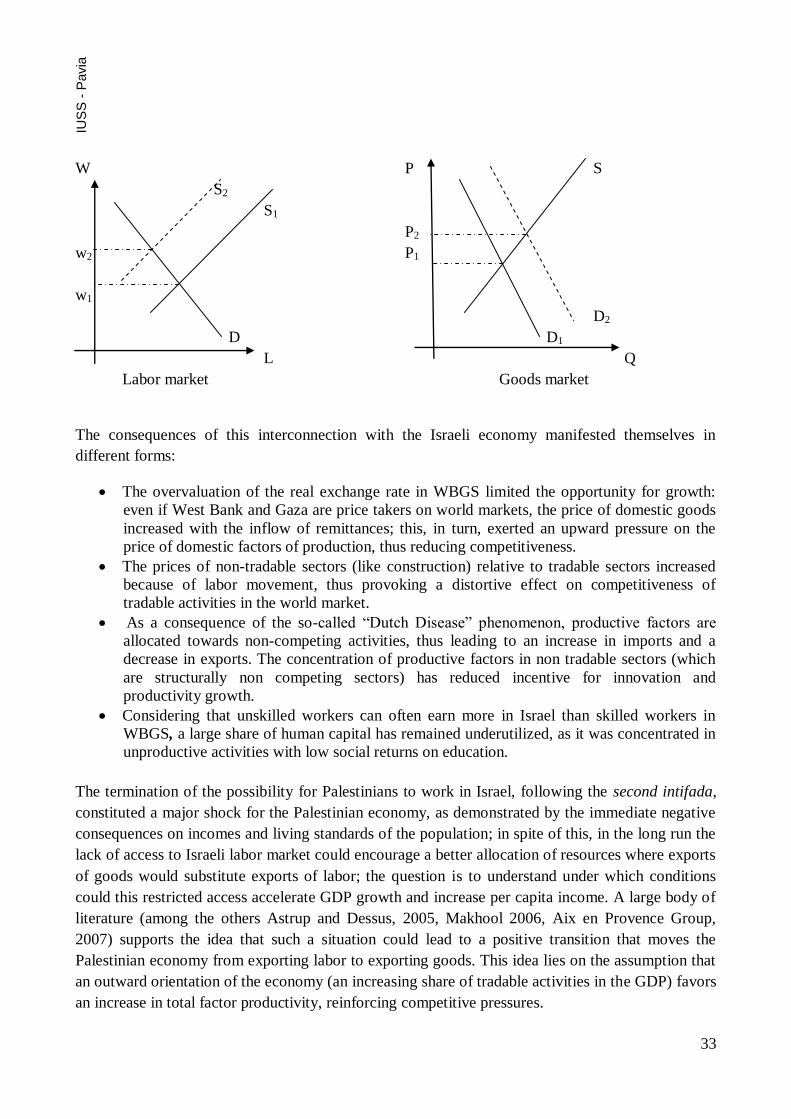

available for the Palestinian workers in Israel led to a larger decrease in the labor supply of the

Palestinian labor market (the supply curve shifts to the right) thus enhancing the wage bill and to a

greater demand for domestic products (the demand curve moves to the left), thus increasing

domestic prices, as shown in the graph below.

33

IUS

S -

Pavia

W P S

S2

S1

P2

w2 P1

w1

D2

D D1

L Q

Labor market Goods market

The consequences of this interconnection with the Israeli economy manifested themselves in

different forms:

The overvaluation of the real exchange rate in WBGS limited the opportunity for growth:

even if West Bank and Gaza are price takers on world markets, the price of domestic goods

increased with the inflow of remittances; this, in turn, exerted an upward pressure on the

price of domestic factors of production, thus reducing competitiveness.

The prices of non-tradable sectors (like construction) relative to tradable sectors increased

because of labor movement, thus provoking a distortive effect on competitiveness of

tradable activities in the world market.

As a consequence of the so-called ―Dutch Disease‖ phenomenon, productive factors are

allocated towards non-competing activities, thus leading to an increase in imports and a

decrease in exports. The concentration of productive factors in non tradable sectors (which

are structurally non competing sectors) has reduced incentive for innovation and

productivity growth.

Considering that unskilled workers can often earn more in Israel than skilled workers in

WBGS, a large share of human capital has remained underutilized, as it was concentrated in

unproductive activities with low social returns on education.

The termination of the possibility for Palestinians to work in Israel, following the second intifada,

constituted a major shock for the Palestinian economy, as demonstrated by the immediate negative

consequences on incomes and living standards of the population; in spite of this, in the long run the

lack of access to Israeli labor market could encourage a better allocation of resources where exports

of goods would substitute exports of labor; the question is to understand under which conditions

could this restricted access accelerate GDP growth and increase per capita income. A large body of

literature (among the others Astrup and Dessus, 2005, Makhool 2006, Aix en Provence Group,

2007) supports the idea that such a situation could lead to a positive transition that moves the

Palestinian economy from exporting labor to exporting goods. This idea lies on the assumption that

an outward orientation of the economy (an increasing share of tradable activities in the GDP) favors

an increase in total factor productivity, reinforcing competitive pressures.

34

IUS

S -

Pavia

8. The rise of the informal sector

As depicted from the previous chapters, the fluctuations in the political and economical

environment, particularly in the absence of political and economical stability, which have

continuously characterized the Palestinian context since the compulsory expulsion in 1948, led to

the creation to an extremely fragile and unstable economy. The natural response to this precarious

economic structure was the rise of the informal sector, whose main characteristic is the high level of

flexibility and the ability to adjust rapidly to changes. This sector expanded itself overtime,

providing a principle income for the families and acting as an important device for poverty

alleviation. In contrast with the widespread mistrust for governmental institutions, informal

enterprises are approved socially, as they provide financial profit for many poor families and are

considered preferable to the very basic assistance offered by the Minister of Social Affairs. It

became apparent that most operators in domestic commerce and service activities in the informal

sector set up their projects during the second intifada, but many informal enterprises’ projects

started before the creation of the PNA, thus outlining the continuous structural role of informality

form the early phases of the Palestinian economy.

A study from the Palestinian Economic Policy Research Institute (MAS)34

shows that the major role

covered by the informal enterprises was to provide work opportunities for family members new to

the labor market, for those who lost their jobs in the Israeli market, or for returnees. Other

enterprises were started in response to a change in health of a family member or the ageing of the

head of the household by establishing a home-base shop. Another research by MAS35

shows that

the biggest percentage of operators in the informal economy are involved in service activities

(32.4%), followed by the construction sector (29.7%), commercial activities (28%) and industrial

and handicraft activities (9.9%)

The most efficient competitive mechanism used in marketing the products and services of the

informal enterprises is achieved through the cut of production costs: the high level of flexibility,

being a major feature of this sector, is actually put in motion by the poor working conditions of the

workers, who work for long hours, without time off, without respect of any norm for the workers’

protection. The economic efficiency of the sector is testified by its total value added, which, in

2003, amounted to nearly US$ 115 million (approximately 67% of the total production), thus

showing a better performance if compared with the formal sector (look at fig. 7 page 13). The main

reason of this phenomenon can be explained by the fact that the average wage in this sector was

around US$ 800 annually per worker, much lower than the national average, (4040 US$ per capita

per year).

In Palestine informal sector enterprises are family based: the family as such provides the supply of

an inexpensive workforce, in addition to the use of family members as backup when needed,

especially women, children and elderly: the availability of flexible workforce constitutes a vital tool

34 Majdi Malki: “The Informal sector Enterprises in the West Bank and Gaza Strip: Case Studies”. MAS, December

2000. 35 MAS: ―Social and economic characteristics of the informal sector in the West Bank and Gaza Strip‖, 2004.

35

IUS

S -

Pavia

for the success of the informal enterprises as it gives them the ability to respond to changes in

demand for their products and services at low production costs. Moreover, these enterprises have a

low degree of risk, as they cover an existing demand: having good information of the market needs,

they direct their products to specific geographic areas in the district where they are located, in

neighboring villages or refugee camps.

Another crucial feature that renders this sector so effective is the low capital required to start the