Embed Size (px)

Citation preview

Asia’s Private Equity News Source avcj.com April 11 2017 Volume 30 Number 14

FOCUS ANALYSIS

Piece of the puzzleCorporate, family investors find ways to target Indonesia venture capital Page 8

Time for a raw dealInvestors keep focus on resources sector Page 10

Where giants tread1Q analysis: Major players lead the way Page 12

Indonesia Infrastructure Fund’s Harold Tjiptadjaja

Page 15

INDUSTRY Q&A

Indonesia’s GP talent pool remains shallow

Page 14

FOCUS

Venture capital goes mainstream in Indonesia

Page 3

Adamantem, Banyan, Capital Square, Eight Roads, FountainVest, Hillhouse, J-Star, KKR, L Catterton, Multiples, Tokio Marine, True North, Warburg Pincus

Page 5

EDITOR’S VIEWPOINT

NEWS

years

Both same font

PRE-CONFERENCE ISSUE AVCJ PRIVATE EQUITY AND VENTURE CAPITAL FORUM INDONESIA 2017

AVCJ WILL SKIP AN ISSUE NEXT WEEK FOR THE SUMMER HOLIDAYS. WE RETURN ON APRIL 25

Unlocking liquidity for private equity investors

www.collercapital.com London, New York, Hong Kong

Anything is possible if you work with the right partner

Number 14 | Volume 30 | April 11 2017 | avcj.com 3

EDITOR’S VIEWPOINTallen.lee@@avcj.com

IT WASN’T UNTIL A FEW YEARS THAT venture capital became an important part of the Southeast Asian investment landscape. Sure, there were a few deals here and there in Singapore, and maybe Kuala Lumpur or Jakarta as well, but nothing more than a blip compared to the interest in buyouts and growth capital in the private equity space. It is a very different story today, with venture capital taking off in Southeast Asia in a big way. New VC firms and start-ups are proliferating.

For most readers, the emergence of VC comes as no surprise. Southeast Asia’s demographics – 600 million people, rising incomes, growth in mobile adaption – are attractive enough that even Chinese investors are now looking for deals. Importantly, Southeast Asia is now home to a handful of formidable technology companies, from Garena in gaming and e-commerce to Go-Jek in ride hailing and delivery. They have proved not only that ASEAN can be a hotbed for new technologies, but also that it is possible to nurture a generation of entrepreneurs with the creativity to adapt business models to local markets.

As the major metropolitan hub in Southeast Asia’s largest market, Jakarta is arguably the beating heart of this new ecosystem. Start-ups, particularly in e-commerce and online-to-offline services, require high frequency of use and ease of delivery as they scale up. Densely populated urban centers are logical target markets, and Jakarta can serve as a platform for addressing other Indonesian cities. The society is also entrepreneurial by nature and land and labor is relatively cheap, which can help slow burn rates.

This sea change in venture capital has been reflected in the evolution of the program for the AVCJ Indonesia Forum over the years. The 2017 event, which takes place in Jakarta on April 27, represents quite a departure from our first, in 2012. Back then, the only technology-relevant content was a panel on the country’s mobile consumer market (at the time, Indonesia was

BlackBerry’s second largest market globally); actual VC investing was not listed in the program discussion points, although it may well have been raised during some sessions.

This year’s event not only features multiple technology-focused panel discussions and addresses, but it is also sponsored and supported by some of the leading venture capital investment firms in Southeast Asia. There are numerous reasons for this, but it is worth noting that – across Asia – larger private equity investors are becoming more important as a source of financing and exits for venture capital firms.

The AVCJ Indonesia Forum has grown with the market and brings together investors (LPs as well as GPs) from different disciplines and of different sizes to look at the key factors driving or holding back the country’s development as a market for private investments. While Indonesia has been always been, and will likely remain, a difficult place for the uninitiated to do deals, continued communication involving all stakeholders gives the market a better chance of fulfilling its potential – for venture capital and private equity.

Allen LeePublishing DirectorAsian Venture Capital Journal

Venture rising Managing Editor

Tim Burroughs (852) 2158 9661

Associate Editor

Winnie Liu (852) 2158 9663

Staff Writer

Holden Mann (852) 2158 9646

Justin Niessner (852) 2158 9678

Design

Edith Leung, Mansfield Hor

Rana Tang

Events

George Sengulovski,

Jessie Chan, Jonathon Cohen,

Sarah Doyle,

Amelie Poon, Fiona Keung,

Jovial Chung,

Marketing

Agrina Sandri,

Priscilla Chu,

Research

Helen Lee,

Herbert Yum,

Kaho Mak, Tim Wong

Sales

Anil Nathani,

Darryl Mag, Debbie Koo,

Samuel Lau,

Gavin Lam, Pauline Chen

Subscriptions

Karina Ting

Sally Yip

Publishing Director

Allen Lee

The Publisher reserves all rights herein. Reproduction in whole or

in part is permitted only with the written consent of AVCJ Group Limited.

ISSN 1817-1648 Copyright © 2017

A Mergermarket Group company

Hong Kong Headquarter Suite 1602-6

Grand Millennium Plaza181 Queen’s RoadCentral Hong KongT. (852) 2158 9700F. (852) 2158 9701

E. [email protected]. avcj.com

Beijing Representative OfficeRoom 77, Level 26,

Fortune Financial Center No. 5, Dong San Huan Zhong Road Chaoyang District,

Beijing, 100020 ChinaT. (86) 10 5869 6203F. (86) 10 5869 6205 E. [email protected]

R E G I S T R A T I O N N O W O P E N

» 7TH ANNUAL INSTITUTIONAL INVESTORS-ONLY SUMMIT 15 MAY 2017 | THE RITZ-CARLTON, WASHINGTON, D.C.

» EMPEA MEMBERS-ONLY RECEPTION 15 MAY 2017 | FAIRMONT HOTEL, WASHINGTON, D.C.

» IFC’S 19TH ANNUAL GLOBAL PRIVATE EQUITY CONFERENCE IN ASSOCIATION WITH EMPEA

16-17 MAY 2017 | THE RITZ-CARLTON, WASHINGTON, D.C.

» EMPEA FUNDRAISING MASTERCLASS 18 MAY 2017 | THE RITZ-CARLTON, WASHINGTON, D.C.

www.globalpeconference.com

Number 14 | Volume 30 | April 11 2017 | avcj.com 5

ASIA PACIFIC

Pay rises level off in Asian private equityOnly about one third of the 210 private capital professionals in Heidrick & Struggles’ 2016-2017 Asia Pacific Private Capital Compensation Survey reported a jump in base salary in 2016 over the previous year. About half reported a rise in their 2015 base salary in the previous year’s survey. The downward trend in compensation is believed to reflect the weaker deal flow seen in 2016.

AUSTRALASIA

Adamantem buys NZ’s Heritage LifecareAdamantem Capital has acquired New Zealand aged-care and retirement village operator Heritage Lifecare for an enterprise valuation of NZ$115 million ($80 million). The GP plans to support Heritage’s expansion plans through consolidation plays in Australia and New Zealand’s highly fragmented aged care sector.

PE-owned Seafolly makes South America bolt-onL Catterton Asia has purchased Colombian beachwear brand Maaji in a bolt-on acquisition for its Australian swimwear brand Seafolly. Media reports put the size of the investment at about A$50 million ($38 million). L Catterton plans to combine Seafolly and Maaji into a leading global beach lifestyle brand.

Sequoia India leads Series C for HealthEngineSequoia Capital India has made its debut investment in an Australia-based start-up, leading a A$26.7 million ($20.2 million) Series C round for online healthcare marketplace HealthEngine. Australian PE firm Alium Capital also invested along with several family offices. Sequoia will join cornerstone investors Telstra Ventures and Seven West Media on the HealthEngine board.

GREATER CHINA

Volkswagen invests $180m in MobvoiVolkswagen’s China unit has agreed to invest $180 million in Mobvoi, a start-up developing

artificial intelligence (AI) technology for the automotive sector. The investment will support a joint venture to use AI-related applications in smart transportation innovations. Mobvoi’s other backers include Google, Sequoia Capital China, Zhenfund and Susquehanna Investment.

Hillhouse, FountainVest agree Zhaopin take-privateHillhouse Capital and FountainVest Partners, along with Australia’s Seek International, have agreed to buy US-listed Chinese recruitment website Zhaopin in a deal that values the company at $1.01 billion. Seek will remain the majority shareholder following the acquisition.

The buyers won out over bidders including CDH Investments, Shanghai Goliath Investment Management and Sequoia Capital.

Car trading site Souche gets $180m Series DWarburg Pincus has led a $180 million Series D round for Chinese online second-hand car trading platform Souche. Hong Kong-based VMS Investment Group, ClearVue Partners, Zuoyu Capital, Haitong International, CreditEase and Morningside Venture Capital also participated. The round comes less than five months after the company’s $100 million Series C led by Ant Financial.

VCs back Series C for mother-and-baby playerEight Roads Ventures has led a Series C round of undisclosed size for Mama+, a social networking and e-commerce platform focused on China’s mother-and-baby market. Other investors include GSR Ventures, Core Capital, Lightspeed China Partners, GWC and Steamboat Ventures. The capital will be used to expand the company’s service capacity and enter China’s third-tier cities.

Banyan raises $725m across US dollar, renminbi fundsBanyan Capital has raised more than RMB5 billion ($725 million) for its latest US dollar-denominated and renminbi-denominated venture capital funds. The US dollar fund comprises a $350 million main corpus and a $50 million side vehicle, while the renminbi fund closed at RMB2.5 billion. Both funds will focus on early and growth-stage TMT investments.

FountainVest, CMC fully exit IMAX ChinaFountainVest Partners and CMC Capital Partners have completed their exit from IMAX China, selling their 5.9% stake to an unnamed investment bank for an estimated HK$836 million ($108 million). The two firms paid $80 million for a 20% stake in 2014, and have realized a likely HK$2.5 billion across several partial exits since.

ACP joins $166m round for Chinese solar playerAsia Climate Partners (ACP) has participated in a $166.7 million investment in Chinese solar power plant developer United Photovoltaics Group (United PV). Orix Corp and China Merchants New Energy Group also participated. The investment is

KKR secures $5.8b first close on third Asian fundKKR has reached a first close of just under $5.8 billion on its third pan-Asian fund, which has an institutional hard cap of $8.5 billion. A further $700 million in commitments are expected from the firm’s balance sheet and management team. The first close took place on March 31, according to sources familiar with the situation.

The LP roster for KKR Asian Fund III includes Minnesota State Board of Investment, which approved a commitment of up to $150 million, its first commitment to a KKR Asian fund, and to any

vehicle dedicated to the region. Louisiana State Employees’ Retirement System is said to have agreed to invest $50 million in the fund.

KKR closed its second fund at $6 billion in mid-2013. According to the firm’s most recent annual report, the fund had generated a net IRR of 21.9% and a multiple of 1.6x as of December 2016. The IRR and multiple for Fund I, which closed at $4 billion in 2007, were 13.6% and 2.2x. For the firm’s $1 billion China growth fund – raised in 2010 – they were 7.8% and 1.4x.

The second fund remains the largest pool of PE capital ever raised for Asia, but several other managers have seen a substantial step up in fund size on their previous vintages.

NEWS

R E G I S T R A T I O N N O W O P E N

» 7TH ANNUAL INSTITUTIONAL INVESTORS-ONLY SUMMIT 15 MAY 2017 | THE RITZ-CARLTON, WASHINGTON, D.C.

» EMPEA MEMBERS-ONLY RECEPTION 15 MAY 2017 | FAIRMONT HOTEL, WASHINGTON, D.C.

» IFC’S 19TH ANNUAL GLOBAL PRIVATE EQUITY CONFERENCE IN ASSOCIATION WITH EMPEA

16-17 MAY 2017 | THE RITZ-CARLTON, WASHINGTON, D.C.

» EMPEA FUNDRAISING MASTERCLASS 18 MAY 2017 | THE RITZ-CARLTON, WASHINGTON, D.C.

www.globalpeconference.com

avcj.com | April 11 2017 | Volume 30 | Number 146

intended to improve United PV’s capital structure and provide support for further expansion.

Credit assessment platform Wecash gets $80mChinese financial technology company Wecash has completed an $80 million Series C round led by China Merchants Venture Capital, Forebright Capital and SIG Asia. Beijing Dongfang Hongdao Asset Management and Lingfeng Capital also took part. The company will use the capital to scale up its domestic and global business.

DCL launches debut US dollar fundDCL Investments, a China-focused distressed debt and special situations manager, is targeting around $300 million for its first US dollar-denominated fund. The GP wants to raise RMB5 billion ($724 million) across the US dollar fund and its second renminbi fund, which recently reached a first close of RMB1.5 billion. DCL closed its debut renminbi fund last October with more than RMB3 billion in commitments.

VCs back female-focused finance start-upShanghai Mime Financial, a consumer finance platform targeting young females in China, has raised a Series C round amounting to hundreds of millions of renminbi led by Haier Capital, Xiyu Capital and Panda Capital. The company provides lifestyle-related loans through arrangements with merchants and financial institutions.

NORTH ASIA

J-Star acquires Japan pet services companyJ-Star has bought Japanese veterinarian services company Fuji Field for an undisclosed sum. The transaction is a bolt-on to portfolio company JVCC, which was established to organize Japan’s fragmented veterinarian industry. J-Star acquired Fuji Field through its third buyout fund, which is targeting $300 million.

SOUTH ASIA

True North leads $162m insurance buyoutA consortium led by True North Managers and including Faering Capital will buy an 80% stake in

India’s Religare Health Insurance (RHI) for INR10.4 billion ($162 million). RHI’s parent, Religare Enterprises, is seeking to divest its holdings in noncore businesses and has made several sales to PE firms in the past 12 months.

Warburg Pincus invests $77m in jewelerWarburg Pincus has committed INR5 billion ($77 million) to Indian jewelry retailer Kalyan Jewellers, raising the GP’s commitment to the company to INR17 billion. Kalyan will use the new capital to

extend its network within India and in the Middle East and Asia. The company sells gold, silver, platinum and diamond jewelry.

Mahindra leads $21m round for MedwellMahindra Partners has led a $21 million Series B round for Indian home healthcare start-up Medwell Ventures, operator of Nightingales Home Health Services. Existing investors Eight Roads Ventures and F-Prime also participated.

Multiples acquires India’s PeopleStrongIndian GP Multiples Alternative Asset Management has acquired domestic human resource (HR) services and technology company PeopleStrong through a combination of primary and secondary investments. PeopleStrong’s other investors include Lumis Partners, AAA Ventures and The HR Fund.

Capital Square agrees Essar BPO carve-outSingapore-based Capital Square Partners has agreed to acquire business process outsourcing (BPO) service provider Aegis from Indian conglomerate Essar Group at a reported valuation of around $300 million. It serves clients in a range of industries, including telecom, technology, media, financial services and retail.

SOUTHEAST ASIA

Dragon sets up Myanmar microfinance business Vietnam-based GP Dragon Capital has joined Myanmar conglomerate Loi Hein to seed a Yangon-based microfinance services business. The pair will commit $5 million to the project, known as Ruby Hill Microfinance, with Loi Hein taking a 51% stake. Ruby Hill will target the more than 30 million people in Myanmar believed to lack access to financial services.

Jafco invests $12m in adtech firm AdAsiaJafco Asia has invested $12 million in Series A funding for Singapore-based advertising technology company AdAsia Holdings, which aims to improve the performance of marketers, advertisers and publishers. The capital will be used for product development and expanding the operational footprint.

Japan’s Tokio Marine closes Fund V at $466mTokio Marine Capital has reached a final close of JPY51.7 billion ($466 million) on its fifth Japan mid-market fund on the back of strong support from domestic LPs, notably regional banks.

TMCAP2016 was established in October of last year with a target of JPY50 billion. The first investment from the vehicle was completed in December with the acquisition of Ropia, a manufacturer of chilled desserts.

Tokio Marine had considered marketing the fund to overseas investors as well, with a view to

diversifying the LP base. However, demand from domestic institutional players was strong enough that there was no space for offshore capital.

Of the 34 LPs, 17 are regional banks and account for just under one third of the total corpus, according to a source familiar with the situation. Other commitments came from pension funds, city banks, trust banks, insurance companies, fund-of-funds and corporates. More than 80% of LPs in Tokio Marine’s previous fund re-upped in the new vehicle.

The private equity firm raised JPY23.3 billion – from 18 LPs – for its previous fund, which closed in 2013. The GP seeks control positions in middle market private companies in Japan, typically working with existing management teams of established businesses that have steady growth and a strong or niche market position.

NEWS

Number 14 | Volume 30 | April 11 2017 | avcj.com 7

Lexington Partners is a leader in the global secondary market. Since

1990, we have completed over 400 secondary transactions, acquiring

more than 2,700 interests managed by over 650 sponsors with a total

value in excess of $36 billion. For over 25 years, we have excelled at

providing customized alternative investment solutions to banks,

�nancial institutions, pension funds, sovereign wealth funds,

endowments, family of�ces, and other �duciaries seeking to

reposition their private investment portfolios. Our unparalleled global

sponsor relationships, capital resources, and reputation as a reliable

counterparty are widely recognized, and we have skilled professionals

to work with you in six locations. To make an inquiry, please call us or

send an email to [email protected].

First Order of Business: Secondaries

Innovative Directions in Alternative Investing

www.lexingtonpartners.com

New York • Boston • Menlo Park • London • Hong Kong • Santiago

LP FirstOrder Ad AVCJ-Wky Web DR012417.pdf 1 1/24/17 10:40 AM

avcj.com | April 11 2017 | Volume 30 | Number 148

COVER [email protected]

NOT LONG AFTER KEJORA VENTURES launched its debut fund in 2013, co-founders Sebastian Togelang and Andy Zain were approached by the CEO of Indosat Ooredoo, one of Indonesia’s leading telecom providers: He wanted to create an incubator to support domestic start-ups. Indosat would put up the money; would Kejora be willing to run it in return for shares in the portfolio companies?

Four years on, the incubator – known as Ideabox – has backed 16 businesses, each of which received up to $500,000 and was taken

through a 120-day accelerator program. Ideabox represents a successful partnership between a VC firm and a local corporate, but it isn’t the only one to emerge under the Kejora banner.

Barito Pacific Group, a conglomerate with interests in petrochemicals, timber and palm oil, was one of four family-owned business groups that together committed $12 million to Fund I. It has re-upped for Kejora’s second fund, which has an overall target of $80 million. The number of family office and corporate LPs is growing in tandem with the fund size, but as much for strategic as economic reasons.

“These families have established connections to key decision-makers and people in government over many years. It is good to have them as partners, particularly when they already have media or retail assets and can offer some strategic value,” says Togelang. “These partnerships are one of the ways we want to

help start-ups grow faster in Southeast Asia, but at the same time we wanted to be independent. Fortunately we have several families Investors to maintain this neutrality.

These groups – acting through family offices as well as through the companies they own – have become a significant presence in Indonesian venture capital, making commitments to funds, establishing VC units, and making balance sheet investments in start-ups. Rather than squeezing out independent GPs, they are seen as a complementary force in a nascent ecosystem, but

it is imperative that structures maintain a balance between different interests.

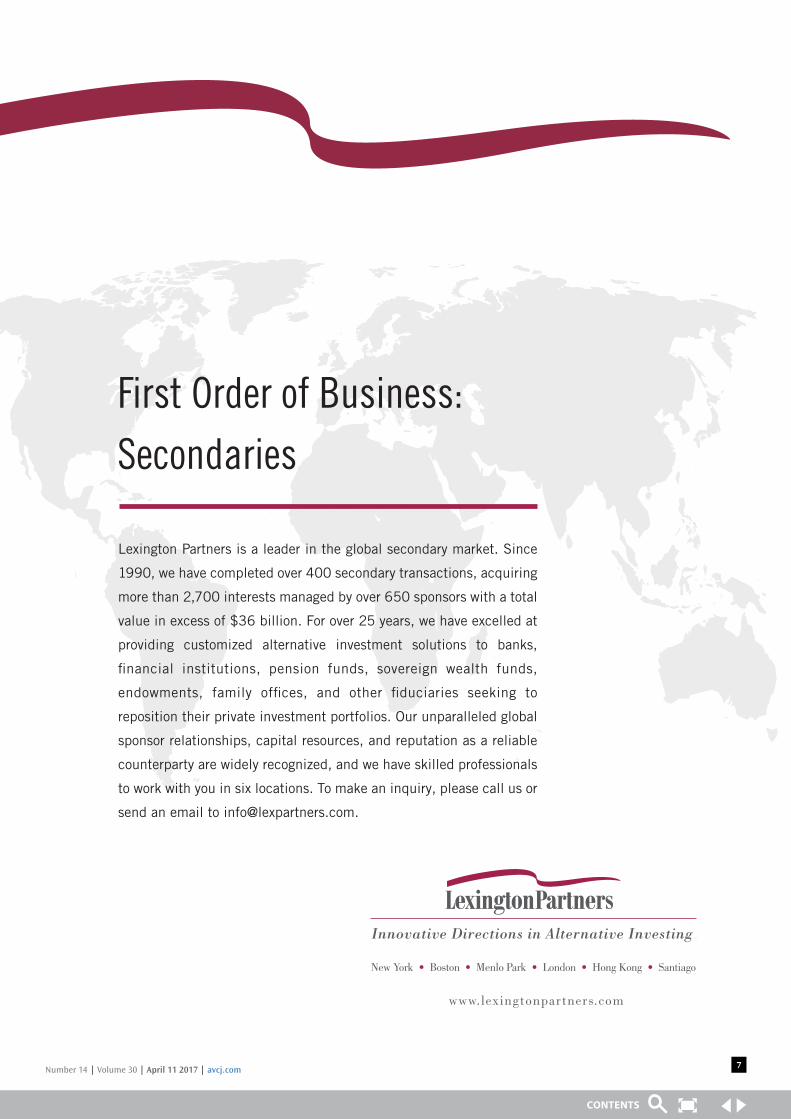

Zero to heroVenture capital has gone from zero profile to high profile in the space of six years: there were barely a dozen investments of negligible aggregate size – in most cases the dollar value was not disclosed – in 2011; in each of the last two years, the deal count has surpassed 50, with an unprecedented $781 million committed in 2016, most of it to ride hailing and delivery player Go-Jek.

The seeds of domestic corporate VC were sown at the start of this period. Djarum Group is regarded as the pioneer, having established domestic incubator Merah Putih and early-stage investor GDP Venture – which is led by Martin Hartono, son of Djarum Group’s head – in 2010. GDP’s acquisitions include social networking site Kaskus and e-commerce platform Blibli.

Over the next few years, others followed suit. For example, the Widjaja family’s Sinar Mas Group established Sinar Mas Digital Ventures (SMDV), while the Riady family’s Lippo Group set up Lippo Digital Ventures (LDV) and launched its own e-commerce business, MatahariMall. LDV subsequently transitioned from a family-owned into a family-sponsored GP – Venturra Partners – that is backed by Lippo but raises third-party capital as well.

Among the telecom and media specialists, Indosat Ooredoo formed an investment unit around the time it launched the incubator with Kejora. Telkom Indonesia has a similar setup, with captive VC unit MDI and incubator Indigo, and Emtek Group has established itself as an aggressive balance sheet investor. Several banks, including Bank Mandiri and Bank Central Asia, have also set up captive investment divisions.

Activity now stretches well beyond Indonesia’s largest companies. Mark Thornton, managing director of Indonesia Private Equity Consultants and also Jakarta-based CIO of a non-Indonesian family office, notes that he often comes across groups looking to enter the space, with little thought to strategy. The classic example would be an overseas-educated third-generation family member who has no interest in the family business and is allocated capital for investment.

“He comes back and sets up a venture business and runs some family money. It doesn’t work very well and it doesn’t really matter. Other groups recognize they need to hire people to do it professionally,” Thornton says. “But the people who do these roles tend not to last very long, especially if they want a mixed portfolio of listed and private investments. As soon as the listed investments struggle they are out of the door. Family offices often don’t have the patience to see things through and the stomach for risk.”

Although there is no shortage of family scions in venture capital, it doesn’t follow that they are necessarily part of unsophisticated setups. As Khailee Ng, managing partner at 500 Startups, puts it: “You rarely see one family member running around with a check book. They build these businesses for learning and success, and this involves hiring outside professionals.”

Venturra is a widely cited example of this. John Riady is the grandson of Lippo founder

Corporate kingpinsThe corporates and family groups that dominate Indonesia’s economy are becoming increasingly active in the VC space. To independent GPs, they are more friend than foe, but agendas and approaches vary

Indonesia PE investment by type

Source: AVCJ Research

2,500

2,000

1,500

1,000

500

0

60

50

40

30

20

10

US$

mill

ion

Dea

ls

No. of VC deals2011 2012 2013 2014 2015 2016

Venture capitalGrowth capital Buyout

Number 14 | Volume 30 | April 11 2017 | avcj.com 9

Mochtar Riady and said to be a competent technology investor in his own right. But he brought in Rudy Ramawy, formerly a director at Google Indonesia, to serve as managing partner of LDV; the pair were joined at Venturra by Rocket Internet alumnus Stefan Jung. Skystar Capital is also said to be run by a combination of professionals and members of its family affiliate, which also owns Kompas Gramedia Group.

Strategic rationaleFor Kompas Gramedia, a media conglomerate with interests spanning newspapers and magazines, book publishing, multimedia and hospitality, the motivation for participating in venture capital is clear: the company wants to get the inside track on technological developments that will redefine its core businesses and if possible use its existing assets to monetize them. The same can be said of telecom providers and financial institutions.

“The sector is changing and the bank recognized it could lose market share to financial technology companies. It wanted to stop losing customers, so the bank decided to establish a corporate VC to invest in these potentially disruptive areas,” says Eddi Danusaputro, CIO of Mandiri Capital, which was established by Bank Mandiri last year. In addition to capital, portfolio companies get access to the bank’s financial expertise and can test their products on a large network of merchants and customers.

Opinion is divided on whether the activities of investment units under the diversified family groups is more opportunistic than strategic. The launch of MatahariMall by Lippo would appear to fall into the latter category: the company saw how e-commerce was cannibalizing traditional retail, where it has a significant presence, and positioned MatahariMall to capture some of this business by offering an online-to-offline consumer experience.

“Many of these groups are investing in businesses that will become big in the future, and e-commerce is definitely an area in which they see disruption of their core businesses,” says Adrian Li, co-founder of Convergence Ventures. “I don’t think it is opportunistic and only happening because e-commerce is the flavor of the month. Look at any market in the world and e-commerce has taken market share from traditional retail, so these are defensive measures.”

In other situations, it is harder to trace motivations back to a fear of disruption. Many of the leading conglomerates have substantial property businesses and a healthy start-up ecosystem is seen as a way to attract young professionals and expatriates to a new township, making apartments easier to sell. Any investment in an incubator or co-working space could

therefore be considered a small marketing cost tied to a much larger project.

With this in mind, if there is likely to be any confusion over a captive investment unit’s ultimate agenda, it is important that the group makes its position clear. “Especially in the early stages, they might need to make explain that they are operating as financial rather than strategic investors says Kejora’s Togelang. “This means clarifying how some entrepreneurs or other minority investors can exit in the future and how they can work with other groups to scale further.”

While some family groups insist on control, which is likely to be a deal-breaker for many entrepreneurs, the primary concern when bringing a corporate VC unit into a funding round as a minority investor are the strings attached. Is the investor insisting on exclusivity, which would prevent its peers from participating

in future funding rounds? And would alignment with this group rule out partnerships with others? Danusaputro says these issues have led to Mandiri Capital missing out on deals.

Beyond that, an entrepreneur might be resistant towards particular groups. “People used to say, ‘Don’t you just want to own us?’ and it took a while for them to understand that we are a minority investor along the lines of a Western VC firm,” Roderick Purwana, managing director at SMDV, told AVCJ earlier this year. “Even now, start-ups that are familiar with us have a very positive or negative view.”

Pick your partnerFor similar reasons, VC firms are wary of being perceived as too close to an individual family group. After closing their first fund at $150 million in 2015, the Venturra founders stressed that Lippo has no more influence over investment decisions than any other LP. Like Kejora, Convergence was careful to cast itself as a fully independent player, even though the majority of the capital in its $30 million debut vehicle comes from corporate and family office-type LPs.

Rather, the reliance on these investors is seen as characteristic of a market that has yet to deliver sufficient exits to attract fund-of-funds and endowments. Venture capital firms think about family groups in terms what works for each fund – the number and diversity of the participants, and how they can add value to the portfolio.

“Corporates have become more and more open to taking on LP positions in funds. What they’ve found is that by doing this they are able

to get capital managed in a professional and independent vehicle and also get some of the insights into the industry offered by professional GPs,” says Convergence’s Li. “If you looked a few years back that wouldn’t happen.”

Indeed, feedback on the major corporate or family-backed venture capital investors is generally positive. Their enthusiasm is seen as beneficial to the ecosystem – it helps to have established local players expressing confidence in local start-ups – and they are useful source of co-investment capital when portfolio companies require follow-on funding. If their strategic resources can help these businesses scale faster as well, all the better.

Needless to say, not every group fits this profile. According to one industry participant with a more jaundiced view, many Indonesian families have accumulated wealth rapidly on

the back of government contracts, concessions and cheap land deals. This hampers their ability to make long-term strategic plans. The danger is they see venture capital in the same way: a source of quick returns on investments that require minimal hands-on management.

More groups are expected to participate in the asset class, and their approaches will evolve over time, whether that means going direct or through LP commitments to funds. The large conglomerates in particular – given their significance to the Indonesian economy – will play a significant role in the development of the ecosystem, as VC-style investors in start-ups and as strategic buyers who facilitate exits for VCs.

Both Kejora’s Togelang and Ng of 500 Startups talk about progress being dependent on a change in mindset, but with different objectives. Asked whether corporates and families could fill the country’s Series B funding gap, Togelang says more will take part, but it will take time for them to get comfortable with the business models and the notion of minority ownership at lofty valuations. Ng, meanwhile, envisions venture capital as an agent of longer-term reform.

“If some of these families look at it with a longer horizon, say 30-50 years, any one of them could create a big shift in the way Indonesia will be,” he explains. “What makes technology so exciting is the entrepreneurs have a bold vision. If the families come in with the same kind of boldness – as well as their resources, networks and access to talent – that could be very exciting. But it means approaching the sector with more deliberation and vision.”

COVER [email protected]

“You rarely see one family member running around with a check book” – Khailee Ng

avcj.com | April 11 2017 | Volume 30 | Number 1410

WHEN SINGAPORE’S PIERFRONT CAPITAL committed $25 million to Indonesian miner Merdeka Copper Gold last September, it demonstrated the resilience of the domestic resources sector’s appeal – even in the face of severe challenges to investor sentiment. The show of confidence, however, belies a consistent wariness for what is arguably private equity’s toughest theater of operation.

At the company level, the investment was notable for confirming Merkeda’s full reputational recovery after a two-year dispute at its flagship Tujuh Bukit mine that ended in 2014. At that time, Saratoga Capital and Provident Capital helped broker a rescue buyout by Kendall Court, effectively smothering an all-too common spot fire in negotiating Indonesian ownership rights.

Merdeka also received its latest backing – in the form of a term loan facility – during the most confidence-rattling Indonesian mining controversy in recent memory. As of January this year, a rising tide of resource nationalism has hardened long-developing government moves to seize control of Freeport-McMoran’s gigantic Grasberg copper-gold mine in the province of Papua, triggering emotional public demonstrations and economically important operational disruptions.

“Investors, especially foreign investors are assessing the Freeport situation at this time to see if the agreements that have been agreed to in the past will be honored by all stakeholders,” says Kay Mock, a founding partner at Saratoga. “It’s a tricky situation because changes in regulations do happen. The rules introduced by the government indicate that they would like to see local parties own the majority of significant concessions – and I think this is probably something that is going to continue.”

Unpredictable beastThe notion that Indonesia is a more difficult and bureaucratically cumbersome investment environment than otherwise similar developing economies is based on impressions of the market’s unpredictability. This factor has been evident in the counterintuitive timing of the country’s latest attempt to rewrite foreign ownership rules for commodities projects.

Most emerging resource markets began pressing nationalistic agendas as the

commodities boom crested a series of price highs from 2011 to 2013. Indonesia, by contrast, didn’t fire up efforts to wrest control of resources from foreign operators until 2014 when commodity values had already begun to sink.

The narrative suggests that the country’s resource politics are comparatively less connected to economic cycles in the sector. Since the election of President Joko Widodo in mid-2014, a number of regulatory changes have eroded investor sentiment despite the administration’s pro-business reputation. It is claimed that Widodo’s lack of resources experience has emboldened the government’s old power brokers in the sector to push policies

that are not necessarily in line with national interests.

A steady string of disputes at Grasberg during the past few years has given this backdrop some of its most dramatic flashpoints. Most recently, the government has sought to take 51% control of the operation within two years under revised foreign ownership rules. At the same time, export rights have been curtailed with new requirements for on-site processing and local investor participation. Freeport has responded by reducing Grasberg output to as low as 10% of capacity and laying off some 2,100 workers.

The overall effect has been a reduced footprint of Western-headquartered conglomerates. In the past year, BHP Billiton and Newmont Mining have been pressured to sell minerals projects to local buyers. In energy, Chevron has decided to pull out of the country in several years, and Total has been refused a gas contract extension despite its Japanese partner being allowed to continue operating. Interestingly, Japan and Korea-based companies are rarely targeted by government-linked takeovers.

For regional private equity players, the implied

opportunity lies in picking up the best assets that strategics are leaving behind. EMR Capital, for example, entered Indonesia in 2015 with a consortium of co-investors including Farallon Capital Management by purchasing the Martabe gold mine from Hong Kong and Australia-based G-Resources in a deal worth $775 million.

“We expect that some of the headline items in the press should be contained to those situations rather than seen as a proxy for what’s happening in general,” says Jason Chang, managing director and CEO at EMR. “We continue to be attracted to Indonesia, not just for the quality of the projects, but also because we expect the government will continue to be open to foreign investment. In

terms of consistency, there may be rule changes, but these are generally well foreshadowed and applied prospectively.”

The government’s tendency to revise resource sector rules has nevertheless become a common concern among interested players. The export ban on unprocessed ores legislated in early 2014 is the highest profile of these changes. It requires base metal exporters to build smelters that can cost in excess of $1 billion and guzzle enough electricity to necessitate an additional on-site power plant.

National copper output fell 24.5% year-on-year during 2014 to 366,000 metric tons as nickel production dropped 55% to 215,000 tons. Earlier this year, the government reacted by softening the ban’s enforcement parameters but ultimately aggravating a general sense that regulations are subject to constant revision. Companies with exposure to commodities outside the purview of the ban – such as Martabe and Merdeka – have fared relatively well.

“Pierfront invested in Merdeka Copper Gold with a degree of confidence that the domestic upgrading regulations would not impact a gold-focused operation that produces gold and silver

Storms and blue skyIndonesia’s resources sector has proven a socially and politically tumultuous investment environment in recent years. GPs are monitoring the headline issues and maintaining long-term confidence

“You can’t pull the trigger on spending billions of dollars if you don’t know within the next 5-10 years if you’re going to end up losing control of the project” – Mark Thornton

Number 14 | Volume 30 | April 11 2017 | avcj.com 11

dore bars on site,” says Andrew Starkey, director for Pierfront. “As such, a detailed assessment of the circumstances surrounding the export ban was not required.”

Merdeka has remained unscathed simply because its copper resources are deposited at deeper levels than the gold – a commodity that is not impacted by the ban. Operations are expected to begin exploiting copper reserves in about five years. “It’s something we would need to deal with, but we still have some time to figure it out,” explains Saratoga’s Mock.

In addition to gold, coal has performed relatively well in the past year due to increased demand from China and firmer pricing. The challenge for regional private equity players looking to benefit from the momentum is entering an environment already dominated by domestic capital. But even outside of coal, the chances of identifying acquisition targets suitable to private equity and private credit investors remain limited to a thin field of viable options.

“Within the coal industry, there is a wide range of investment opportunities. However, in the precious and non-precious metal sector, there are only a small number of assets of a suitable quality and scale that are either in production or could be in production over the short to medium time horizon,” adds Pierfront’s Starkey.

Cost considerationsPrivate investment opportunities in the oil and gas space may also come under pressure as a result of regulatory changes that are expected to make it harder to develop more speculative deep-water blocks. Earlier this year, the government signaled an overhaul one of the cost recovery regime for oil and gas production sharing contracts (PSC) – transitioning the industry to a system based on gross split production sharing contracts, whereby the required capital and risk is to be fully borne by the contractor.

“The feedback we have received is that for blocks that will require high capital expenditure, the new gross split regime is unlikely to be attractive relative to the previous regime,” says Ben McQuhae, a partner at Jones Day, specializing in energy and natural resources. “In some cases, the new fiscal terms may simply be a deal breaker for would-be investors. But the uncertainty created may well add value to some companies that hold an old-form PSC license with full cost recovery benefits.”

Theoretically, the change represents a streamlined approvals system, but it will result in new costs being eligible for tax deduction, which could in turn result in offsetting delays. The increased risk burden on operators, meanwhile,

means that technically difficult early-stage projects are likely to suffer from underinvestment as existing licenses expire and fall under the terms of the new regime.

According to Wood Mackenzie, Indonesia’s expiring PSCs were worth about $10 billion as of November last year but are predominantly composed of mature or late-life tenements. This scenario implies an expanded role for state oil company Pertamina, which has already been muscling in on properties held by the likes of Chevron.

“For the big oil and gas majors in Indonesia, the one thing that keeps them up at night is the fact that the rules keep changing,” says Mark Thornton, managing director of Indonesia Private Equity Consultants. “You can’t pull the trigger on spending billions of dollars if you don’t know within the next 5-10 years if you’re going to end up losing control of the project.”

Regulatory uncertainties are further intensified by decentralization of government oversight. Since the constitutional reforms of the early 2000s, Indonesian decision-making authority has gradually evolved from a top-down Jakarta-centered system to a more complicated power hierarchy involving multiple layers of local stakeholders, typically with incompatible interests. Although such bureaucracy is far from unexpected in developing markets, its comparatively recent arrival in Indonesia has created new problems for industries with particularly long timeframes such as resources.

In a political sense, regional empowerment has been a successful initiative since it preserved the integrity of a fragmented archipelago nation as it transitioned out of the centralized military leadership of the three-decade Suharto era.

However, it has also resulted in an inexperienced provincial authority structure with unrealistic expectations for foreign resource players and a susceptibility to conflicts of interest.

Political capitalWith the arrival of the Widodo government, a clear vision of economic expansion has been put in place, but it is not yet evident that it can be consistently executed or sustained past the political cycle. The overarching concern is that the struggle to effectively combine policy vision, execution and sustainability has created an environment that is now less accommodating to foreign resources investors than previous administrations. Indeed, consultancies serving foreign investors in the country have charted a distinct decline in resources related activity.

“Wherever investors are looking is where we tend to operate, and from the perspective of our client profile, it’s not an extractives market anymore – it’s a consumer and infrastructure market,” says Dane Chamorro, a senior partner at Control Risk in Singapore. “This is not a place you want to be for extractives at the moment. That might change, but right now, Indonesia just doesn’t have the policy elements that foreign investors need to be successful in that sector.”

The natural counterpoint to this view is that growth in one area doesn’t necessarily mean that other areas are shrinking. The explosion of interest in consumer plays based on domestic demographics has changed the ratios in Indonesia’s economic pie chart, but it hasn’t nullified the intrinsic value of the export-oriented resources sector.

PE investors pursuing resource strategies with a higher risk-return are expected to continue finding opportunities in locally-connected companies. This opening may be especially inviting to distress specialists, given the fact that many of the Indonesian companies that formed in the heat of the latest commodities boom have taken on more debt than they can handle. Much of this debt is in US dollar terms, which could ripen the M&A market if US interest rates go up.

“A challenging market does not mean that it is closed for foreign investors, although they certainly have to manage risks carefully to operate in Indonesia’s resources sector,” says Adimas Nurahmatsyah, senior associate for investigations and disputes in Kroll’s Indonesian team. “The challenge does not necessarily come from public scrutiny or local civil society, but from facing political and business actors who, on occasion, exploit local sentiment for their own gain. Therefore the most important thing for foreign companies to do is to understand who they are dealing with, who are their counterparts, and what are their expectations.”

Mature projects with upsideEnhanced oil recoveryLate-lifeDiscovered resource opportunities

Indonesia’s expiring oil and gas production sharing contracts (PSC)

Source: Wood Mackenzie

avcj.com | April 11 2017 | Volume 30 | Number 1412

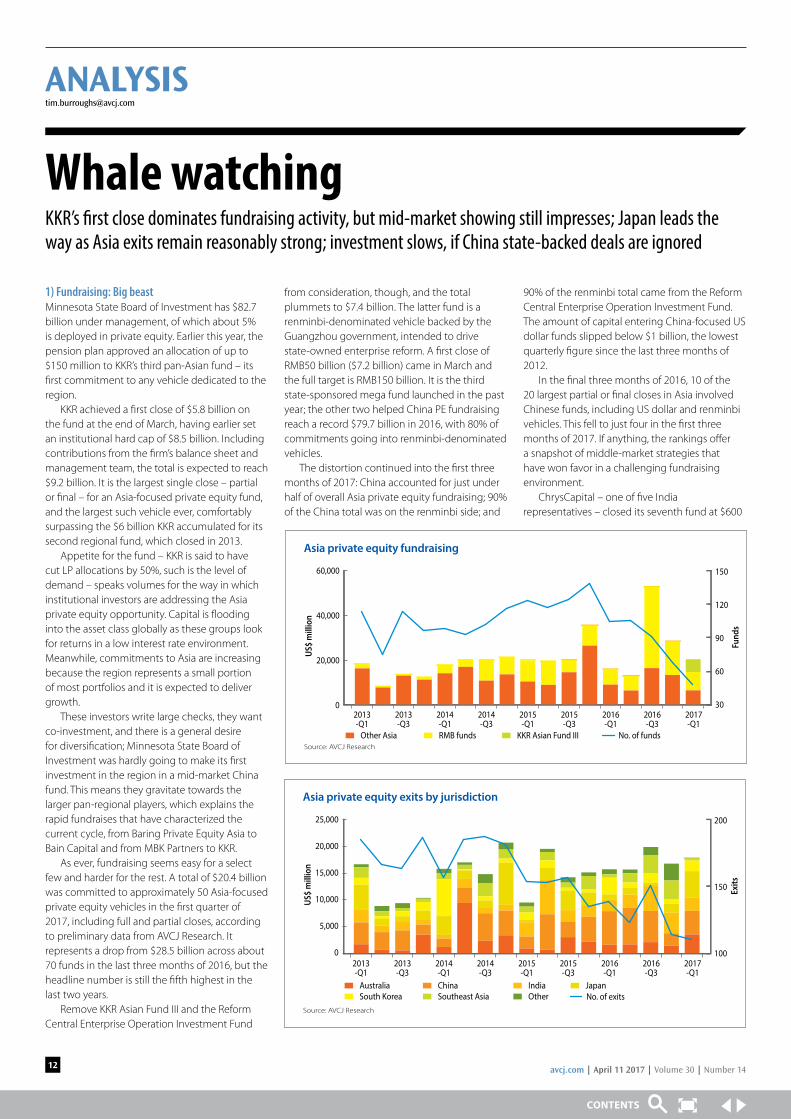

1) Fundraising: Big beastMinnesota State Board of Investment has $82.7 billion under management, of which about 5% is deployed in private equity. Earlier this year, the pension plan approved an allocation of up to $150 million to KKR’s third pan-Asian fund – its first commitment to any vehicle dedicated to the region.

KKR achieved a first close of $5.8 billion on the fund at the end of March, having earlier set an institutional hard cap of $8.5 billion. Including contributions from the firm’s balance sheet and management team, the total is expected to reach $9.2 billion. It is the largest single close – partial or final – for an Asia-focused private equity fund, and the largest such vehicle ever, comfortably surpassing the $6 billion KKR accumulated for its second regional fund, which closed in 2013.

Appetite for the fund – KKR is said to have cut LP allocations by 50%, such is the level of demand – speaks volumes for the way in which institutional investors are addressing the Asia private equity opportunity. Capital is flooding into the asset class globally as these groups look for returns in a low interest rate environment. Meanwhile, commitments to Asia are increasing because the region represents a small portion of most portfolios and it is expected to deliver growth.

These investors write large checks, they want co-investment, and there is a general desire for diversification; Minnesota State Board of Investment was hardly going to make its first investment in the region in a mid-market China fund. This means they gravitate towards the larger pan-regional players, which explains the rapid fundraises that have characterized the current cycle, from Baring Private Equity Asia to Bain Capital and from MBK Partners to KKR.

As ever, fundraising seems easy for a select few and harder for the rest. A total of $20.4 billion was committed to approximately 50 Asia-focused private equity vehicles in the first quarter of 2017, including full and partial closes, according to preliminary data from AVCJ Research. It represents a drop from $28.5 billion across about 70 funds in the last three months of 2016, but the headline number is still the fifth highest in the last two years.

Remove KKR Asian Fund III and the Reform Central Enterprise Operation Investment Fund

from consideration, though, and the total plummets to $7.4 billion. The latter fund is a renminbi-denominated vehicle backed by the Guangzhou government, intended to drive state-owned enterprise reform. A first close of RMB50 billion ($7.2 billion) came in March and the full target is RMB150 billion. It is the third state-sponsored mega fund launched in the past year; the other two helped China PE fundraising reach a record $79.7 billion in 2016, with 80% of commitments going into renminbi-denominated vehicles.

The distortion continued into the first three months of 2017: China accounted for just under half of overall Asia private equity fundraising; 90% of the China total was on the renminbi side; and

90% of the renminbi total came from the Reform Central Enterprise Operation Investment Fund. The amount of capital entering China-focused US dollar funds slipped below $1 billion, the lowest quarterly figure since the last three months of 2012.

In the final three months of 2016, 10 of the 20 largest partial or final closes in Asia involved Chinese funds, including US dollar and renminbi vehicles. This fell to just four in the first three months of 2017. If anything, the rankings offer a snapshot of middle-market strategies that have won favor in a challenging fundraising environment.

ChrysCapital – one of five India representatives – closed its seventh fund at $600

Whale watchingKKR’s first close dominates fundraising activity, but mid-market showing still impresses; Japan leads the way as Asia exits remain reasonably strong; investment slows, if China state-backed deals are ignored

Asia private equity exits by jurisdiction

Source: AVCJ Research

25,000

20,000

15,000

10,000

5,000

0

200

150

100

US$

mill

ion

Exits

No. of exits

2013-Q1

2013-Q3

2014-Q1

2014-Q3

2015-Q1

2015-Q3

2016-Q1

2016-Q3

2017-Q1

JapanIndiaAustralia ChinaSouth Korea Southeast Asia Other

Asia private equity fundraising

Source: AVCJ Research

60,000

40,000

20,000

0

150

120

90

60

30

US$

mill

ion

Fund

sNo. of funds

2013-Q1

2013-Q3

2014-Q1

2014-Q3

2015-Q1

2015-Q3

2016-Q1

2016-Q3

2017-Q1

Other Asia RMB funds KKR Asian Fund III

Number 14 | Volume 30 | April 11 2017 | avcj.com 13

million, in part due to a steady track record: more than $4.2 billion realized across 55 complete exits, representing all of the capital from its first four funds and over 100% of committed capital from its fifth. Meanwhile, South Korea’s VIG Partners hit the hard cap of $600 million, making a meaningful breakthrough with foreign LPs who were convinced by the strategy on the back of the performance of Fund II.

There were also the first signs of what is expected to be an uptick in Japan fundraising this year, with Tokio Marine Capital and CITIC Capital Partners announcing final closes on their latest vehicles of JPY51.7 billion ($466 million) and JPY30 billion. In addition, The Longreach Group reached a first close of around $200 million on its third North Asia-focused fund, which has a particular focus on Japan.

Although there is foreign LP interest in Japan’s mid-market space – CITIC and Longreach both attracted offshore money – Tokio Marine’s investor base is purely domestic. This reflects the growing interest in private equity among Japanese institutional players. Of the 34 LPs in the fund, 17 are regional banks and they account for one third of the total corpus.

2) Exits: Japan shows its strengthUniversal Studios Japan (USJ) has been a fun ride for PE. MBK Partners, which privatized the business in 2009 with existing backer Goldman Sachs and Owl Creek Asset Management, was on course for a 4.95x return at the end of 2015 based on the sale of a 51% interest to Comcast NBCUniversal earlier that year plus distributions already made and the value of the unrealized stake. In February, Comcast completed the acquisition, paying JPY254.8 billion ($2.3 billion) in a deal that valued USJ at JPY840 billion, including debt. PAG Asia Capital, which invested in 2013, also exited.

Infrequent big ticket trade sales tend to skew the exit numbers in Japan. With proceeds of $5 billion, the first three months of 2017 represented the country’s best quarterly showing since Permira sold Arysta LifeSciences in 2014. However, USJ was not the only contributor. Japan accounted for six of the 15 largest exits across the region as Bain Capital made partial exits from Macromill and Skylark, Cerberus Capital pared its holding in Seibu, and a PE consortium sold Peach Aviation.

Australia, China and South Korea also posted quarter-on-quarter gains in aggregate exit value. While activity in China was reasonably widespread, Australia and Korea – like Japan – relied on a single stand-out transaction: TPG Capital’s $3 billion sale of Alinta Energy Group to Hong Kong’s Chow Tai Fook; and the $1.74 billion exit of Daesung Industrial Gases by a Goldman

Sachs-led consortium to MBK Partners.These deals helped drive overall Asia private

equity exits to $17.1 billion in the first quarter, up from $16.5 billion in the last three months of 2016. It represents the fifth-highest quarterly total in five years, even though the actual number of exits, at just over 100, was well below the average. Trade sale activity continues to be strong, with proceeds of $12.5 billion ensuring that Asia cleared $10 billion for the fifth quarter in a row. The average for the 20 quarters preceding this period is $6.5 billion. Sales to other financial sponsors were also relatively robust, coming in at $2.4 billion.

On the other hand, public market exits continued to disappoint. After $1.4 billion was realized in the last three months of 2016 – the

second-lowest quarterly total since 2011 – the first three months of 2017 delivered only a modest improvement. GPs came away with $1.9 billion from about 25 deals, a showing that would no doubt be blamed on market volatility.

The recent rebound in private equity-backed IPO activity also appears to be short-lived. A total of 59 offerings generated proceeds of $5.8 billion, down from $11.9 billion from 114 offerings in the last three months of 2016 and $12.8 billion from 67 in the quarter before that. However, the IPO markets are very much a China-driven phenomenon and Chinese New Year shortens the window of opportunity for new offerings.

3) Investment: Unigroup the outlier Tsinghua Unigroup has risen to prominence as China’s agent-of-choice for establishing a meaningful market share in global semiconductor manufacturing. Spreadtrum Communication and H3C Technologies are among its international M&A scalps, while Western Digital, ChipMOS Technologies and Silicon Precision Industries are high-profile failures. More recently Unigroup, which is controlled by an investment arm of Tsinghua

University, has turned its attention to greenfield projects at home.

Last month, Unigroup received more fuel for its ambitions as China Development Bank and Sino IC Capital – manager of the state-backed China Integrated Circuit Industry Investment Fund – committed RMB150 billion ($22 billion) in funding. As a result, private equity investment in China hit a record $36.6 billion in the first three months of the year, but the Unigroup deal cannot be seen as representative of purely commercially driven activity. Exclude it, and the China total falls to $14.6 billion, largely in keeping with previous quarters.

Continued robust deal flow in China flies in the face of mounting concerns about private

market valuations – although early-stage investment came to just $2 billion, the lowest quarterly total since early 2015, suggesting that reality might be starting to bite in certain segments of the market.

Areas of interest remain largely the same: consumer and technology. Notably, The Carlyle Group teamed up with CITIC Group’s Hong Kong-listed unit and CITIC Capital Partners to buy the McDonald’s China and Hong Kong business for $2 billion, while internet start-ups such as Alibaba Group’s local services platform Koubei, chauffeured car service Ucar, online used car auction business Uxin Group, and bicycle-sharing player Ofo raised sizeable growth equity rounds.

Asia-wide PE investment came to $50.1 billion across approximately 700 transactions, falling to $28 billion if Unigroup is ignored. This compares to $43.6 billion, from the same number of deals, in the last three months of 2016. Australia and Japan both saw substantial drops in capital committed – a result of one unusually large deal in each market during October-December. Investment in South Korea and India rose, the latter rebounding from a weak previous quarter to continue its recent strong showing.

Top 10 private equity investments, 1Q 2017Investee (country)

Amount (US$m) Investors

Tsinghua Unigroup (China) 21,786 China Development Bank; Sino IC Capital

McDonald's - China and Hong Kong (China) 2,080 CITIC Capital Partners; CITIC; Carlyle

Daesung Industrial Gases (Korea) 1,740 MBK Partners

Grab (Singapore) 1,500 SoftBank

China Three Gorges South Asia Investment (China)

1,392 China Development Bank; IFC; Silk Road Fund; Export-Import Bank of China

Hitachi Koki (Japan) 1,266 KKR

Koubei (China) 1,100 CDH Investments; Primavera; Silver Lake; Yunfeng Capital

Bharti Infratel (India) 947 CPPIB; KKR

Ucar (China) 670 China UnionPay; CICC; Shanghai Pudong Development Bank

Yingde Gases (China) 616 PAG Asia Capital

Source: AVCJ Research

avcj.com | April 11 2017 | Volume 30 | Number 1414

AVCJ RESEARCH HAS RECORDS OF TWO dozen private equity investments of $75 million or more in Indonesia between 2008 and 2014. Only seven of these were by brand-name global or pan-regional players, and four were split between CVC Capital Partners and TPG Capital. There have been 11 more deals in this size bracket since then. Seven featured the likes of KKR, Warburg Pincus, General Atlantic, and Capital Group, as well as TPG and CVC.

Progress may be relatively slow, but a growing number of big ticket investors appear to be making their mark on Indonesia. The same cannot be said of domestic GPs. In 2011, there were four established PE firms in the country: Northstar Group, Saratoga Capital, Quvat Management, and Ancora Capital. Today the number remains the same: Northstar and Saratoga remain, while the other two have been replaced by Falcon House Partners and Capsquare Asia Partners.

“In terms of raising capital in an institutionalized manner, the number one problem is the talent pool isn’t that deep. You don’t find many Indonesians in consulting firms and investment banks, which is where a lot of PE talent originates,” says Patrick Walujo, co-founder and managing partner at Northstar. “Second, it isn’t clear whether the market needs additional funds at this moment. Even without more Indonesian GPs the market is still robust, we see a lot of regional GPs becoming more active.”

Other industry participants agree wholeheartedly with the observation about talent. Indonesians who could feasibly make a pitch to foreign institutional investors generally require some level of overseas education and work experience. Many who meet these criteria come from wealthy families and end up working in the family business. The exceptions aren’t necessarily drawn to mid-market private equity.

“There is a shortage of talented people who are well connected, and most of them get snapped up by the big guys and the established local players as their on-the-ground talent in Indonesia,” says David East, partner and head of transaction services as KPMG Indonesia.

Limiting factorsHowever, human resources is not the only limitation. Whenever attention is drawn to how

small private equity is as a proportion of GDP in Indonesia compared to China and India as well as developed markets, it is usually followed by observations about the distinctive nature of the country’s economy. Specifically, the way in which power is concentrated in the hands of family-owned conglomerates.

Mark Thornton, managing director of Indonesia Private Equity Consultants, believes these family groups make their own PE-style investments, distorting the market and hindering independent GPs. The GPs say this is overplayed. Walujo notes that Northstar has never lost out to one of these groups in a competitive situation, while Brian Doyle, founding partner at Falcon House, says mid-market firms like his see plenty of deal flow from first or second generation entrepreneurs who are looking for professional growth capital and institutional value-add.

Falcon House and Capsquare emerged during the fervor of 2011 when close to a dozen private equity firms were trying to raise debut Indonesia funds. Both proved they have staying power.

Falcon House closed its first fund at $212 million in 2013 and then hit the hard cap of $400 million on its second vehicle last year. Capsquare raised around $80 million for its first fund and is said to be in the process of raising a new pool of capital.

“Today’s fundraising environment is more challenging compared to 2011 and 2012,” says Doyle. “Specifically, the macro story might be perceived as less compelling to some investors, many LPs are also waiting for exits that demonstrate the market’s return potential, and the overall pool of capital available for first time and younger funds is shrinking. However, the expected impact of the success of tax amnesty and far reaching economic reforms over the past years is likely to change this equation.”

While the government’s policy agenda has helped spur confidence, it is not shared by all LPs, who weigh the positives out of Indonesia against the merits of historically more reliable markets in the region.

“I don’t think there is the same level of interest

in Indonesia as other major Asian markets – whether that’s a holdover from the bad old days of the Asian financial crisis or more recent disappointments. Even these one-off mega hits like Matahari Department Store [a CVC investment from 2010] are not enough to get people excited about a country fund, so many just put their money with one of the pan-regional guys,” says Doug Coulter, a partner at LGT Capital Partners.

He adds that most LPs spend little time in Indonesia, particularly given the opaqueness and complexity of the market. It doesn’t get a lot of mind space relative to other jurisdictions, and as such, the generally lower allocations should not come as a surprise.

Silver lining?Nevertheless, Indonesia remains an attractive proposition in terms of demographics – more than half the population is under 30 years of age – rising urbanization, and the proportion of disposable income that is channeled into

consumer spending. There is certainly no shortage of activity at the apex of consumer and technology, with a handful of independent or captive GPs established in the last few years and now operating in the Series A space.

Northstar’s Walujo admits that expectations for the economy were very high in 2011 and these haven’t been met, with Indonesia enduring a torrid 2014-2015 as a combination of wweaker commodities prices and instability in the broader global economy took their toll. But he suggests that the consumer sector in particular is worth reconsidering.

“Interest in consumer businesses has fallen in recent years because growth has slowed, but the reality is the macro has stayed intact in this and other sectors. It is a good time to invest in areas when people are not looking at them. The challenge for us is to make sure we understand the drivers behind the development of a sector and analyze the areas we want to invest in,” Walujo says.

Slim pickingsWhile the number of GPs active in Indonesian venture capital has mushroomed in recent years, there has been no change on the private equity side. The market suffers from talent and perception issues

“The number one problem is the talent pool isn’t that deep” – Patrick Walujo

Number 14 | Volume 30 | April 11 2017 | avcj.com 15

Q: The Widodo administration has made infrastructure improvement central to its domestic agenda. How do you expect the political climate to affect opportunities for private investors?

A: Since 2014 the Indonesian government has been pushing a lot on infrastructure both through the state budget as well as through state-owned enterprises. But they also realized they need the private sector to join in, so right now there’s an opportunity for private investors to enter the market. After 10 years there is always a changing of the guard, but if you believe this administration will continue after the next election then it is likely we will have stability for the next seven years. I always tell investors and developers that now is the right time to start developing your project. Developing an infrastructure project can take years, so if you start now you have time to finish before the next administration takes over.

Q: What are the biggest challenges facing private investors that want to participate in the sector?

A: The developers in the market right now are all medium-sized companies, because the private infrastructure sector has just emerged in the last 10 years. So the central question is how you can build enough capacity and size to go for a successful exit. For example, in the power sector there is a rule of thumb that you need at least 1,000 megawatts of capacity to have a decent IPO. It might be lower for renewables, because the market appreciates renewable and clean energy

more than traditional power plants. But the fact remains that you cannot remain small and find an exit. Building a platform by combining energy assets is one way to attain scale and eventually attract investors to take your stake.

Q: Do you see opportunities for investment beyond the infrastructure projects themselves?

A: There are other attractive opportunities around infrastructure, mostly around supply chains and supporting industries. In the case of a solar power plant, the plant itself might not be your thing, because the tariff is fixed and there’s very little upside. But if you look at the whole value chain, they need the panels and all the electrical instruments to construct that solar power plant. In hydro power, where the government is targeting 14,000 MW of capacity, plants require turbines that are either produced locally or imported from overseas, so you can invest in manufacturers or importers. It’s a market that has yet to be explored.

Q: Have you seen any investments recently that target these areas?

A: In the last year there was an investment by Asia Climate Partners in a US battery company – Fluidic Energy – that also has operations in Indonesia. These batteries are meant to be used as a backup for solar power, wind power, or any other renewable energy source. There’s an opportunity to use them not just in the domestic energy industry, but to make Indonesia a base to build and export to

other Southeast Asian countries as well.

Q: Where do infrastructure projects most often run into problems?

A: One of the worst enemies of infrastructure in Indonesia is delay. It’s not a question of whether the project will be done, but by how much it will be delayed. You need to make sure you’ve taken account of that possibility in your business plan. Otherwise you might become frustrated at having not reached the size you’d planned for earlier, and if it goes on long enough you may even have to

sell it down at a valuation you wouldn’t like.

Q: What causes these delays?A: When you are setting up a power

plant, you may need hundreds of permits before you can even start construction. And if you have four or five projects you must repeat the process four or five times. It’s not like some areas of consumer investment, where if you get a license to operate a cinema you can build five in one city. If you are building a fiber optic network for multiple cities you have to go through the process over and over again. And sometimes when you are in the middle of the process suddenly the person in charge changes, and then you have to start from zero again. So this is the kind of patience you need. You might have thought that you could build 1,000 MW in five years, but in reality it’s only 500 MW. This means that your IPO target, which was in three years, might have to be extended to seven years.

Q: What investment strategies are best suited to the sector?

A: In consumer you just have your own market, but in infrastructure you have to deal with many government institutions as well as specific sector challenges. So if you’re investing in infrastructure you have to pick just one sector where you know you are strong, where you know the ins and outs, and then try to add value based on your knowledge and experience. If you’re in toll roads, then you have to go in toll roads all the way – the same for power and ports. Otherwise, if you try and combine multiple kinds of assets, I think it will be difficult for you to see a profit.

HAROLD TJIPTADJAJA | INDUSTRY Q&A [email protected]

The long haulHarold Tjiptadjaja, managing director at government-backed non-bank financial institution Indonesia Infrastructure Finance, discusses the qualities foreign investors need to navigate the sector

“You have to pick just one sector where you know you are strong, where you know the ins and outs, and then try to add value based on your knowledge and experience”

Amit AnandFounding PartnerJUNGLE VENTURES

Dayu Dara PermataCo-FounderGO-LIFE

Julianto SidartoSpecial AdvisorALPHA JWC VENTURES

Sandhya DevanathanCountry Head - SingaporeFACEBOOK

Florian HolmCo-CEO, IndonesiaLAZADA GROUP

Jonathan SudhartaCEO & Co-FounderHALODOC

Forum key statistics

27 April 2017 • Mandarin Oriental, Jakarta

6th Annual Private Equity & Venture Forum

GLOBAL PERSPECTIVE, LOCAL OPPORTUNITY

avcjindonesia.com

Enquiry

Registration and sponsorship enquiries:

Anil Nathani T: +852 2158 9636 E: [email protected]

For the latest programme and speaker line-up, visit avcjindonesia.com

Indonesia 2017

8interactivesessions

35+speakers

200+Participants

40+Limited Partners

9countries represented

5premium networking opportunities

Join your peers#avcjindonesia

China 2017

Keynotes

Capturing the next wave of private market opportunities

Confirmed speakers include:

Co-SponsorsAsia Series Sponsor

REGISTER NOW!

Noni PurnomoPresident DirectorBLUE BIRD GROUP HOLDING

Sandiaga S. UnoFounding PartnerSARATOGA CAPITAL