Embed Size (px)

Citation preview

Page 1 of3 ®

Dear Saxena/Dheeraj,

ClI comments on CP N032/2011-12.For=n.a pis

Regards,

Deepak<=div>

---------- Forwarded message -=-------From: Rajesh Menon <=a href-vmailto.rajesh.menonrgtcii.in" target="_blank">rajesh.menon@ciLi=> Date: Wed, Feb 15,2012 at 3:35 PM Subject: RE: CP-No.32/2011-12- Determ=nation of Tariff for aeronautical services in respect oflOI Airport, New =elhi - Stakeholder Consultation Reg To: cv.dccga[<.({?;aera.Q.ov.in, cvdeepCcI)grnail.com Cc: Babu Khan <bah=.khan((j)cii.in>

Dear Mr. Deepak,

I am p=eased to enclose Gil comments on AERA Consultation Paper rega=ding DIAL Proposal for Revision of Tariff.

regards

Rajesh Menon

Deputy Director General

Confederation of Indian Industry

From: cV,decpal<@acra.9.=..'!l Q [mailto:Sent: '.l'ucsdav, January 24, 2=12 6:0J PM To: khoslaa(?!}jata.org; !1gQya1((lhctairwav=.com; vi=inksJ13rmq(q),airindia.in; inchargc.3asl(il)airindia.in; [email protected]; [email protected]; jennif=:r.packianui1i ntcrgl0 be.com; rahul.bhatiau.f1inlerglobe.com; waoind iaCa)gmail.co=; kv.d:;:modaran(q)apaoindia. com; khoslaa(Q)iata.org; chairman@)fl :kingfishcr.com; =raheja({l;aai .aero; snayar({ij,3gaoinc1 ia.=001 ; n3vi.n=wig[(l

(.

)dcccanair.com;. !Iii \vaU<.dcy (if),g;n ~lil . com ; pravccl1. gupt=~@2goill(li go . in; [email protected]; tan j::::m((!!.iata .org; asivanandan=:i ctaitwavs.com; I11trchan(q)jctairways.com; kamal.hingoraniC(11spiccjeLcom; coo(d),consumer-vo=cc.org; gmf]n=1'((I)airi ndia.in; viiay.pau]({11airindiaoin; kd.ro~~l~airindi a .in<a>; apaoindia({(1gma:l.com; ma :vcndra.dcswa1(e/),cii.in; babu.kban((l;cii .in; rdm ~11cll ts.org; cut=(d)cLLts.org; khmmadhe=raj(({)rcdiffl11 aU .com;

mhtml:http://sg3.attach.mail.ymail.com/in.fl922.mail.yahoo.com/ya/se... 05-03-2012

Confederation of Indian Industry

Comments on AERA Consultation Paper regarding DIAL Proposal for Revision of Tariff

According to estimates India aviation sector has a potential to become the third largest aviation market in the world , next only to USA and China.

Airport sector, which is the foundation of aviation sector, is estimated to require an investment of Rs. 67,500 crores; a lion share of which, as high as Rs. 50,000 crore, is expect to be contributed by private sector.

In order to facilitate private investment of such magnitude, India needs a progressive, forward looking , investor friendly & fair policy and regulatory framework.

The consultative approach adopted by AERA is progressive, forward looking and a step in the right direction.

CII is pleased to submit the following comments on AERA Consultation Paper regarding DIAL Proposal for Revision of Tariff, for the kind consideration of AERA :

A. Return on Equity

In regards to the Return on equity, the Regulator has proposed a ROE of 16% as against 24% filed by the Concessionaire, DIAL.

CII supports the aproach of Capital Asset Pricing Model (CAPM) adopted by AERA in determining the cost of equity, However, CAPM model provides different results as per the different set of assumptions taken in determining the components of the model.

CII would urge the Regulator to study the approach followed by airport regulators around the world to adopt the best practices prevalent, of calculating the cost of equity from the CAPM model. This would ensure a fair outcome and could be used in all the future determination by the authority.

CAPM formula for calculating cost of Equity is as under

Cost of Equity =Risk Free Rate + Beta * Market Risk Premium

Asset beta

Best practice AERA Best AERA approach practice approach

Asset betas Mix of Book Market of companies Asset value value of operating in betas of of equity either companies equity taken developed or operating taken based on developing In both an economies developed analyst' taken and report depending developing on the economies country taken under consideration

The following graphic compares the global best practice followed with the approach followed by AERA in determining the inputs which go into the CAPM model

X+

AERABest AERA Best practice

approachpractice approach

Return of Return of yields Current Historical

benchmark benchmark on Govt.

average index of the index of a

bonds yields on

country In mature taken

Govt. consideration economy

which is bonds

(US)taken a better

takentaken and then

measure adjusted of to India forward sovereign looking risk risk free rate

On the basis of the above arguments, we make the following submission which represents the Industry Association's view on the determination of the inputs in calculating the Cost of Equity

Our Recommendation Risk free rate Parameter AERA Proposed

Risk free rate should be forward looking, hence current rate should be considered

Beta

Historical risk free rate taken

Beta of mature markets of developed Should account for the developing nature economies taken of the economy, nascent nature of the

airport sector in India and the additional risks associated with this sector

Market risk Mature market (US) benchmark Benchmark index from India should be premium index considered and then adjusted taken

- - - - J2.rl ndJ9 sovereign risk - - - --.. . _- - ---_.

Further, CII believes that a fair return should compensate for the commensurate risk taken. CII would specifically like to highlight the following two points :

B. Risk profile of the airport operations business vis-it-vis other infrastructure sectors

Although Indian airports operate under regulatory conditions similar to other capital intensive and long gestation infrastructure assets such as power, roads, ports, the risk profile is not comparable with the other infrastructure assets. Aviation sector is cyclical in nature and the degree of severity or volatility in cash flows is higher. Given the economic downturn in the global and domestic economy, there is expected to the significant volatility in traffic which is a key

business driver for both aero and non-aero revenues. This further increases the risk profile of the airport operations business.

An independent study conducted by KPMG puts Airport risks to be the highest among the infrastructure sectors.

Multi Sector Revenue 3 M(2)

Revenue Collection 3 M(2)

Regulatory Risk 3 L(1) M(2)

Self-Performance 2 M(2)

Performance of other 1 stakeholders

Capital Cycle Risk 3

Political Risk 2

• For the purposes of the above analysis, roads under toll are considered as an infrastructure asset. In the case of airports , hybrid till +rate of return model is considered.

• High - H (3), Medium - M(2), Low - L(1)

Given the risks, lenders are cautious when issuing long term debt to airport operators. Also, Indian airport financing is highly leveraged leading to fixed cash outflows in the form of interests and repayments. This translates into a longer gestation period to the equity investors. Finally, there are significant political risks as well in the airport.

Given below are examples of Return on Equity allowed by the Regulator from other infrastructure sectors in India

• Ports - Return on Capital Employed (equivalent of WACC) of 18% compared to 10.33% WACC allowed by AERA

• Power - Return on Equity of 16% allowed where regulated asset base is not adjusted for depreciation every year and where terminal value of the assets accrue to the operator, whereas for Delhi airport, the RoE of 16% is allowed

on depreciated asset base with the airport asset to be handed over to AAI at the end of the concession period.

• B. Terminal value

An important issue which the Regulator should consider is the terminal value of the asset under consideration.

In case of DIAL assets built by the JVC would be returned back to AAI at the end of the concession period. In return, the JVC would be provided with no appreciation on the assets. It may be noted that in other infrastructure sectors like Power, at the end of the concession period, the asset is retained by the JVC.

Considering the residual value of this project is zero, the fair rate of return may be considered on the upper side.

In light of the above facts, we urge the Regulator to revisit the proposed 16% RoE and revise the same upwards to make the returns commensurate to the risks taken.

C. Treatment of Non-transfer asset as Quasi-equity

In regards to the cost of refundable security deposit, the Regulator has determined that the concessionaire would not be provided with any return on the same as the cost of acquiring it is zero.

The SSA provides the Regulator to observe the principle:

"Commercial: In setting up the price cap, AERA will have regard to the need for the JVC to generate sufficient revenue to cover efficient operating costs, obtain the return of capital over its economic life and achieve a reasonable return on investment commensurate with the risk involved. II

The SSA mandates the Regulator to provide a reasonable return on any investment made in the project by the concessionaire. The refundable security deposits are treated in the books of the concessionaire and are in its custody. The utilization of the same would also be dependent on the decision taken by the concessionaire. If the concessionaire has chosen to invest the same in this project, such amount should earn a reasonable return on investment.

Considering the above argument, the Regulator should provide at least the cost of debt in rupee terms for this investment made by the Concessionaire.

Providing any return less than the cost of debt in rupee terms would be against the spirit and principles laid down by the SSA.

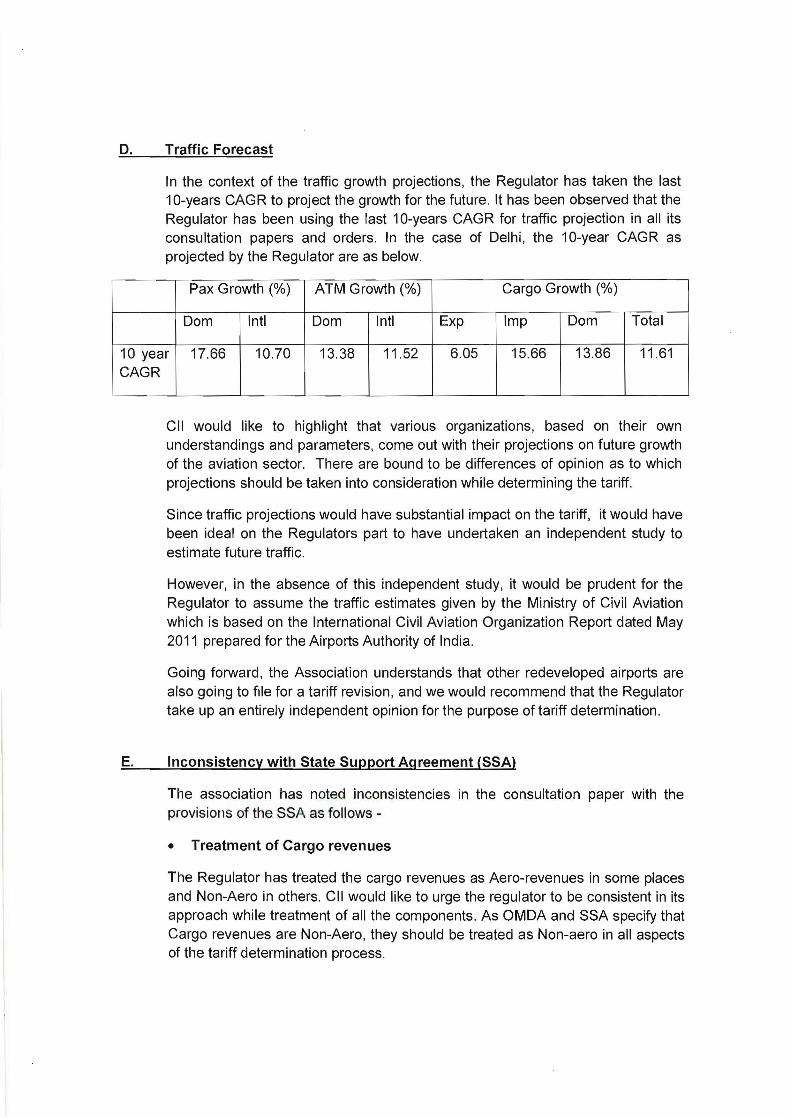

D. Traffic Forecast

In the context of the traffic growth projections, the Regulator has taken the last 10-years CAGR to project the growth for the future. It has been observed that the Regulator has been using the last 10-years CAGR for traffic projection in all its consultation papers and orders. In the case of Delhi, the 10-year CAGR as projected by the Regulator are as below.

Pax Growth (%) ATM Growth (%) Cargo Growth (%)

Dom Inti Dom Inti Exp Imp Dom Total

10 year CAGR

17.66 10.70 13.38 11.52 6.05 15.66 13.86 11.61

CII would like to highlight that various organizations , based on their own understandings and parameters, come out with their projections on future growth of the aviation sector. There are bound to be differences of opinion as to which projections should be taken into consideration while determining the tariff.

Since traffic projections would have substant ial impact on the tariff, it would have been ideal on the Regulators part to have undertaken an independent study to estimate future traffic.

However, in the absence of this independent study, it would be prudent for the Regulator to assume the traffic estimates given by the Ministry of Civil Aviation which is based on the International Civil Aviation Organization Report dated May 2011 prepared for the Airports Authority of India.

Going forward, the Association understands that other redeveloped airports are also going to file for a tariff revision, and we would recommend that the Regulator take up an entirely independent opinion for the purpose of tariff determination.

E. Inconsistency with State Support Agreement (SSA)

The association has noted inconsistencies in the consultation paper with the provisions of the SSA as follows

• Treatment of Cargo revenues

The Regulator has treated the cargo revenues as Aero-revenues in some places and Non-Aero in others. CII would like to urge the regulator to be consistent in its approach while treatment of all the components. As OMDA and SSA specify that Cargo revenues are Non-Aero, they should be treated as Non-aero in all aspects of the tariff determination process.

• CPI minus X

CII has observed that the Regulator has adjusted the operating expenses and the non-aero revenues for CPI. Over and above this, it has reduced the X-factor by considering CPI in the calculation of the X-factor.

CPI is a year on year phenomenon. Hence, the model created as per the base year numbers would be devoid of any inflationary growth for the coming years, provided that the growth projections taken for each component of the target aero revenue determination is based on real growth. The X-factor determined from such a process would result in the calculation of real tariff required to achieve the target aero revenues. Adjusting for inflation after this process would enable the concessionaire to meet its target aero revenues in real terms. The SSA also provides for a similar approach in determining the X-factor.

CII would like the Regulator to follow similar guidelines, as also iterated in the SSA, in adjustment for CPI in the X-factor calculation.

• Service Quality Parameters

In relation to the compliance of service quality levels by the airport operator, the Regulator has stated that the Regulator would be providing rebate to the users in case of under-achievement by the airport operator on the stated service levels. The Regulator has also recognized that the argument of double penalization would surface.

CII is of the view that while the Regulator clearly specifies that penalization by AAI is a contractual arrangement and penalizing by AERA is a statutory arrangement , it must be noted that no such caution/clause was provided by either OMDA or the SSA to the Airport Operator during the signing of the agreements. This is unfair on the investor who had based its cost estimate on the compliance requirements with prescribed quality standards.

Considering all the above stated arguments, the industry associations would like the Regulator to reconsider their current decision on the partial honouring of the OMDA and SSA. Had the participants of the bid been cautioned earlier regarding such clause change, the benefits in terms of revenue share provided to AAI could have considerably been lower.

• Non-aero estimates for the control period

We have noted that the Regulator has estimated the non-aero revenues for the control period 2009-2014 taking the year 2008-09 as the base. We also understand that the projections have been made using the passenger traffic growth rates plus an assumed increase in penetration of non-aero spends.

The accuracy of these projections is a concern as we already have witnessed a significant difference in the actual non aero revenues for FY10 and FY11 as

compared to the estimates made for these years. This also leads us to conjecture that the estimates for the next 2 years could also be significantly off the mark.

We believe that it is advisable to take actual data for the years for which it is available and then project it from that year onwards based on the decided assumptions.

This, in our view, would lead to the actual figures for the coming years to be more in line with what has been projected thus arriving at a more realistic scenario with respect to subsidization of aero activities.

F. Viability

DIAL has been reporting losses in the last five years. With the revision in tariff proposed as per the consultation paper, DIAL will continue to face losses. Therefore, tariff revision should be revisited to allow for healthy cash flows so as to maintain a healthy debt-service ratio within the industry norms.

Caution should be taken that any changes in regulation should not induce financial sickness. It should be noted here that a sick airport will have repercussions on the airlines as well as on the economy as a whole.

F. Discounts on domestic landing charges and collection charges on DF

DIAL had filed for a discount on timely payment of domestic landing charges and levy of collection charges for OF. CII believes that such discounts and collection charges are always healthy for the growth of the industry as a whole and should be considered by the Regulator.

G. Conclusion

CII would like to congratulate DIAL for building world-class airport infrastructure with such exquisite facilities. The service levels at the Delhi airport are among the top-5 airports in the world. The facilities provided at the airport including the connectivity to-and-from the airport, the upcoming Aero-city, transit hotel and retail spread at the terminal are adding/going to add substantial benefit to the users of the airport and the economy at large.

*********

![Sent - AERAaera.gov.in/documents/pdf/4 Indian Oil pb 05-14-15.pdfFrom: Airport Manager COK [mailto:AirportIVlanagerCOK@etihad,ae] Sent: Friday, March 28, 2014 11:49 AM To: Moorthy,](https://img.pdfslide.us/doc/110x75/5acd25e67f8b9aad468d952b/sent-indian-oil-pb-05-14-15pdffrom-airport-manager-cok-mailtoairportivlanagercoketihadae.jpg)