Embed Size (px)

Citation preview

Pacific Ethanol, Inc.Pacific Ethanol, Inc.Pacific Ethanol, Inc.Pacific Ethanol, Inc.

November 16, 2016

(Nasdaq: PEIX)

Investor Presentation

Statements and information contained in this communication that refer to or include Pacific Ethanol’s estimated or anticipated future results or other non-historical expressions of fact are forward-looking statements that reflect Pacific Ethanol’s current perspective of existing trends and information as of the date of the communication. Forward looking statements generally will be accompanied by words such as “anticipate,” “believe,” “plan,” “could,” “should,” “estimate,” “expect,” “forecast,” “outlook,” “guidance,” “intend,” “may,” “might,” “will,” “possible,” “potential,” “predict,” “project,” or other similar words, phrases or expressions. Such forward-looking statements include, but are not limited to, market conditions, including the supply of and domestic and international demand for ethanol and co-products, growth for these products, as well as margins, commodity prices and export conditions; expectations regarding improvements in production assets and the carbon intensity of ethanol produced; expected gains from hedged positions; production levels of cellulosic ethanol and premiums and enhanced profitability from cellulosic ethanol; the timing, effectiveness, and costs and energy savings, of technologies implemented at Pacific Ethanol’s plants; the ability of Pacific Ethanol to timely and successfully execute on, and the effects of, its initiatives to optimize production, improve plant efficiencies and increase yields, reduce operating costs, and lower the carbon intensity of ethanol produced; the effects of Low-Carbon Fuel Standards in California and Oregon, and the premiums Pacific Ethanol may generate for its ethanol as a result of those programs; the expected adoption and growth of 15% ethanol blends; and Pacific Ethanol’s other plans, objectives, expectations and intentions. It is important to note that Pacific Ethanol’s plans, objectives, expectations and intentions are not predictions of actual performance. Actual results may differ materially from Pacific Ethanol’s current expectations depending upon a number of factors affecting Pacific Ethanol. These factors include, among others, adverse economic and market conditions, including for ethanol and its co-products; fluctuations in the prices of oil and gasoline; raw material costs, including ethanol production input costs; changes in governmental regulations and policies; insufficient capital resources; the inability to successfully execute on plant improvement initiatives or install new technologies, or both. These factors also include, among others, the inherent uncertainty associated with financial and other projections; the anticipated size of the markets and continued demand for Pacific Ethanol’s products; the impact of competitive products and pricing; the risks and uncertainties normally incident to the ethanol production and marketing industries; changes in generally accepted accounting principles; successful compliance with governmental regulations applicable to Pacific Ethanol’s facilities, products and/or businesses; changes in laws and regulations; the loss of key senior management or staff; and other events, factors and risks previously and from time to time disclosed in Pacific Ethanol’s filings with the Securities and Exchange Commission including, specifically, those factors set forth in the “Risk Factors” section contained in the Company’s Form 10-Q filed with the Securities and Exchange Commission on August 5, 2016.

2

Cautionary StatementsCautionary StatementsCautionary StatementsCautionary Statements

3

o 8 strategically located bio-refineries located in the U.S.

o Production capacity of 515M gallons/yr.

o Current run rate of 1 billion gallons/yr. of marketing volume

o Co-product production capacity of over 1.5M tons/yr. (dry matter basis)

o Positioned to access 48 states and export markets with ethanol production and

marketing

Mission: To be the leading producer and marketer of low-carbon renewable fuels

Feedstock procurementEthanol & co-

product productionMarketing, transportation

& logisticsDistribution & customer

services

Pacific Ethanol, Inc.

History: Founded in 2003, public in 2005 as the first pure-play ethanol company

Stock Profile a 11/09/16:

• Nasdaq: PEIX

• Trading at $6.45

• Market cap of $278.5M

o Octane, carbon and cost benefits of ethanol driving market growth

o Regulations support long-term increasing demand for renewable fuels

4

Leveraging strong operating platform to drive growth

o Strategically located biorefineries serve multiple markets

o Diversity of geography, technology, feedstocks, logistics and products

o Implementing plant improvements to increase efficiencies & yields

o Organic growth and acquisitions to increase market share

Continued long-term demand for ethanol

Strong financial foundation

o Q3’16 net sales of $417.8M

o Record total gallons sold of 243.7M

o Net loss $3.8M or $0.09 per share

o Adjusted EBITDA was $9.3M

Reasons to InvestReasons to InvestReasons to InvestReasons to Invest

$380.6 $376.8

$342.4

$422.9 $417.8

211.6 213.4 206.7233.2 243.7

0

50

100

150

200

250

300

350

400

450

Q3'15 Q4'15 Q1'16 Q2'16 Q3'16

Quarterly Revenue & Total Gallons Sold

Net Sales Total Gallons Sold

5

Fundamentals Support Continued Demand

Gasoline demand in the US market has hit record highs with lower fuel prices, an increase in large vehicle sales

and a strong summer driving season

Source: NYMEX, CBOT, EIA

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

WT

I [U

SD

/BB

L]

CO

RN

[U

SC

/BS

H]

Corn vs. Crude Oil

CBT CORN First Month [USC/BSH]

NYMEX Light Sweet Crude Oil (WTI) Futures Pit (Front Month) [USD/BBL]

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4

9.6

9.8

10.0

2-Jan 2-Feb 2-Mar 2-Apr 2-May 2-Jun 2-Jul 2-Aug 2-Sep 2-Oct 2-Nov 2-Dec

Mil

lio

ns

BB

ls p

er

Da

y

U.S. Motor Gasoline Demand

Based on 4-Wk Average

5-Year Range 2014 2015 2016

6

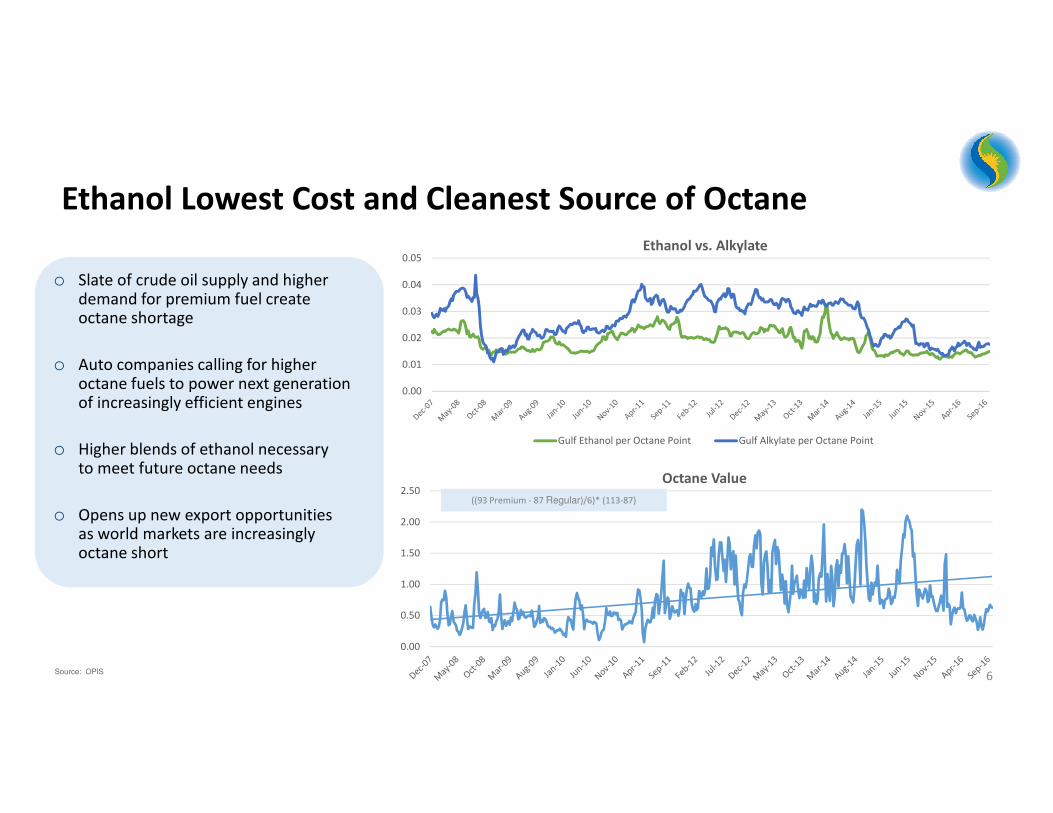

o Slate of crude oil supply and higher demand for premium fuel create octane shortage

o Auto companies calling for higher octane fuels to power next generation of increasingly efficient engines

o Higher blends of ethanol necessary to meet future octane needs

o Opens up new export opportunities as world markets are increasingly octane short

Ethanol Lowest Cost and Cleanest Source of Octane

Source: OPIS

0.00

0.50

1.00

1.50

2.00

2.50Octane Value

((93 Premium - 87 Regular)/6)* (113-87)

0.00

0.01

0.02

0.03

0.04

0.05Ethanol vs. Alkylate

Gulf Ethanol per Octane Point Gulf Alkylate per Octane Point

7

o Export levels are on track to exceed 2015 levels with expectations of nearly 1 billion gallons of exports in 2016

o Global demand is growing 2-3% annually as global markets incorporate environmental and performance benefits

o Approximately 30 countries have renewable fuel standards or targets

o US ethanol producers supply the world with low-cost ethanol while sugar prices surge

Source: EIA, Department of Commerce

Exports Create Growing Opportunity

99.6

(100.0)

(50.0)

-

50.0

100.0

150.0

200.0

Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

MM

Ga

llo

ns

U.S. Ethanol Export and Import

Import Export Net Export

8Source: EIA

Top Markets for U.S. Ethanol in 2015

Canada

249

(30%)

Mexico

34 (4%)

Brazil

116

(14%)

Oman

33 (4%)

Philippines

72

(9%)

Tunisia

26

(3%)

Rest of world 12%

Total 2015 Export 844 million gallons

India

47

(6%)

China 71

(8%)

S. Korea

60

(7%)

Netherlands

34

(4%)

9Source: Renewable Fuels Association.

o Breaching the blend wall

o Only Federal fuels policy to reduce greenhouse gas (GHG) emissions

o Need regulatory certainty to secure development of cellulosic ethanol projects

Renewable Fuel Standard

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Bil

lio

n G

all

on

s

RFS- Conventional Biofuel RFS - Advanced Biofuel Installed Capacity

Industry Production Total Demand Incl. Net Export blend ratio @ 10%

blend ratio @ 15% Domestic Ethanol Demand

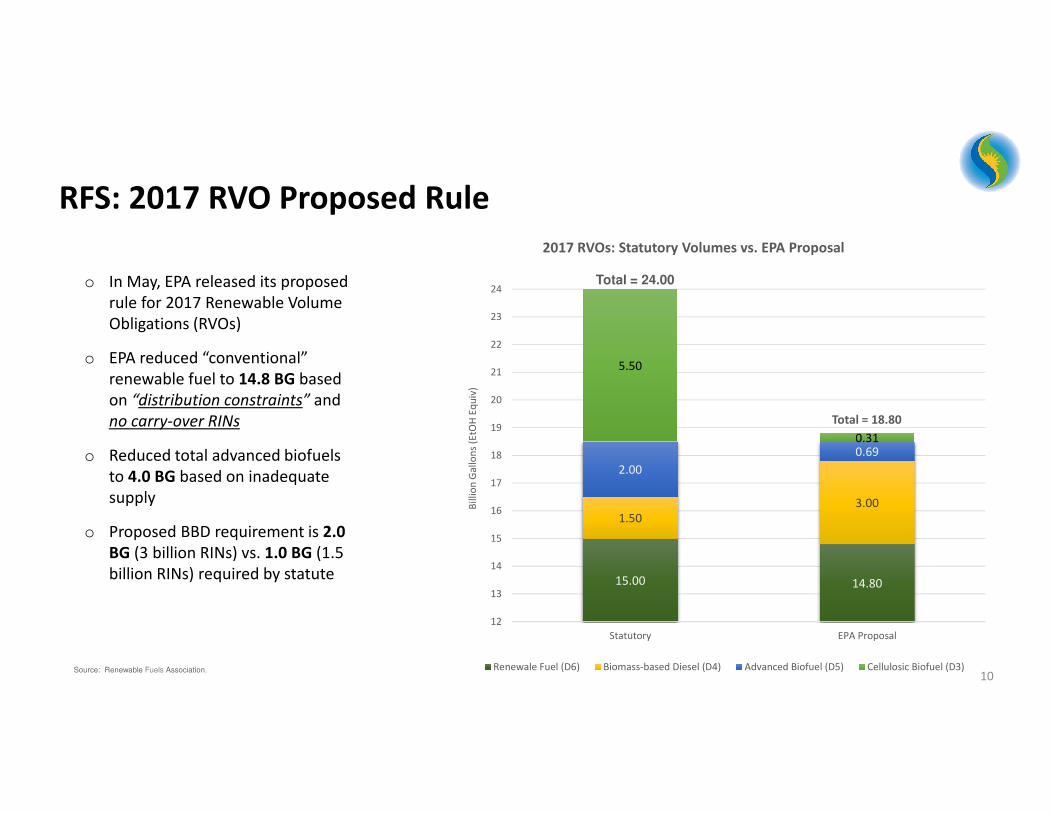

RFS: 2017 RVO Proposed Rule

15.00 14.80

1.50

3.00

2.00

0.69

5.50

0.31

12

13

14

15

16

17

18

19

20

21

22

23

24

Statutory EPA Proposal

Bil

lio

n G

all

on

s (E

tOH

Eq

uiv

)

2017 RVOs: Statutory Volumes vs. EPA Proposal

Renewale Fuel (D6) Biomass-based Diesel (D4) Advanced Biofuel (D5) Cellulosic Biofuel (D3)

o In May, EPA released its proposed

rule for 2017 Renewable Volume

Obligations (RVOs)

o EPA reduced “conventional”

renewable fuel to 14.8 BG based

on “distribution constraints” and

no carry-over RINs

o Reduced total advanced biofuels

to 4.0 BG based on inadequate

supply

o Proposed BBD requirement is 2.0

BG (3 billion RINs) vs. 1.0 BG (1.5

billion RINs) required by statute

Total = 18.80

Total = 24.00

10Source: Renewable Fuels Association.

11Source: OPIS

o The California Air Resources Board (CARB) re-adopted the LCFS with the revised program effective Jan. 2016

o Oregon LCFS initiated Jan. 2016 for a 10% reduction in carbon intensity by 2025

o RFS is successful carbon policy at the national level

Pacific Ethanol currently receives a $0.08 per gallon

premium over standard Midwest ethanol on each CA

production gallon sold into the CA market

Low-Carbon Fuel Standards

-

0.020

0.040

0.060

0.080

0.100

0.120

California Ethanol premium $/gal (CI 69.6)

1%2.0%

3.5%5.0%

7.5%

10.0%

20.0%??

0%

5%

10%

15%

20%

25%

2015 2016 2017 2018 2019 2020 2030 E

California LCFS Program

Reduction in Carbon Intensity

12

HQPacific Ethanol Plants

Marketing Partner PlantsTerminals

Pekin, IL

100mmgy

Wet Mill

Pekin, IL

60mmgy

Dry Mill

Aurora, NE

110mmgy

Dry Mill

Boardman, OR

40mmgy

Dry Mill

Burley, ID

60mmgy

Dry Mill

Stockton, CA

60mmgy

Dry Mill

Madera, CA

40mmgy

Dry Mill

Aurora, NE

45mmgy

Dry Mill

Serving Multiple MarketsServing Multiple MarketsServing Multiple MarketsServing Multiple Markets

o Leveraging leading market share

position on the West Coast to

expand throughout the country

o Expanding ethanol distribution

capabilities through transportation

arrangements such as recently

signed unit train agreement at

Pekin plant

Pacific Ethanol Pacific Ethanol Pacific Ethanol Pacific Ethanol

MarketingMarketingMarketingMarketing

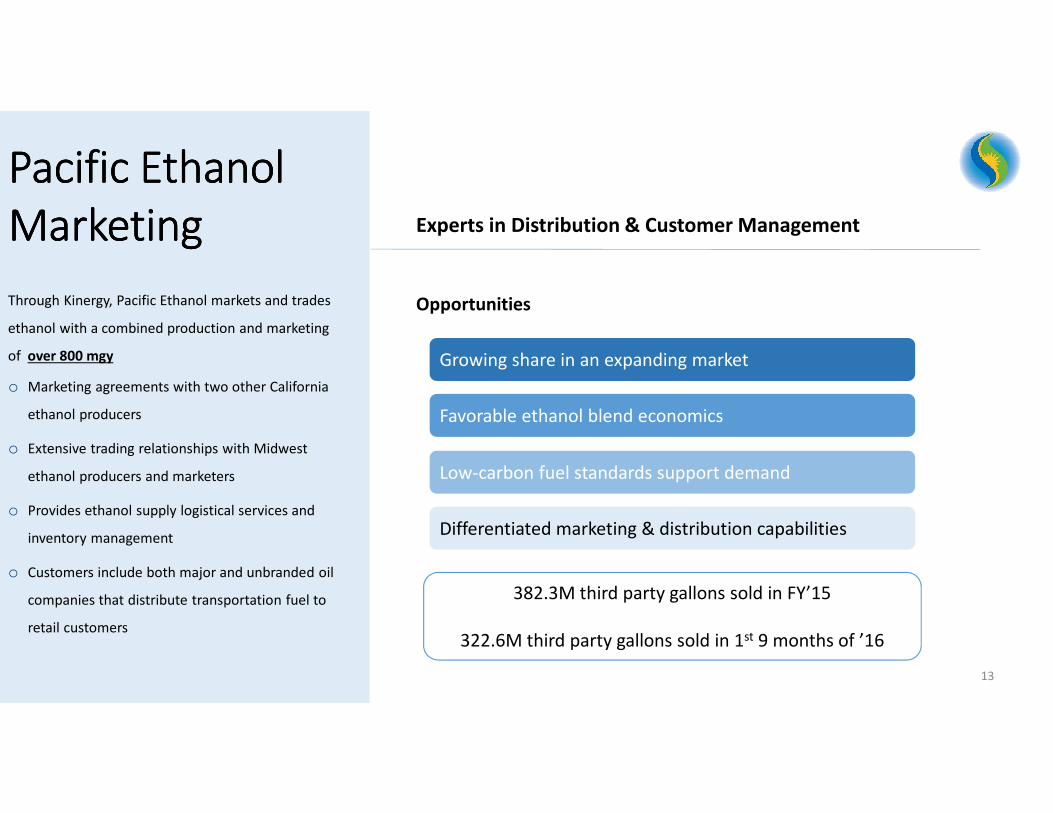

Through Kinergy, Pacific Ethanol markets and trades

ethanol with a combined production and marketing

of over 800 mgy

o Marketing agreements with two other California

ethanol producers

o Extensive trading relationships with Midwest

ethanol producers and marketers

o Provides ethanol supply logistical services and

inventory management

o Customers include both major and unbranded oil

companies that distribute transportation fuel to

retail customers

13

Opportunities

382.3M third party gallons sold in FY’15

322.6M third party gallons sold in 1st 9 months of ’16

Experts in Distribution & Customer Management

Growing share in an expanding market

Favorable ethanol blend economics

Low-carbon fuel standards support demand

Differentiated marketing & distribution capabilities

Madera, CAMadera, CAMadera, CAMadera, CA

Burley, IDBurley, IDBurley, IDBurley, IDStockton, CAStockton, CAStockton, CAStockton, CA

Date of Operation:Date of Operation:Date of Operation:Date of Operation:

September 2008

Annual Capacity:Annual Capacity:Annual Capacity:Annual Capacity:

60.0 mmgy

Technology:Technology:Technology:Technology:

Dry mill, WDG, corn oil,

cellulosic ethanol, terminal

Date of Operation:Date of Operation:Date of Operation:Date of Operation:

October 2006

Annual Capacity:Annual Capacity:Annual Capacity:Annual Capacity:

40.0 mmgy

Technology: Technology: Technology: Technology:

Dry mill, WDG, corn oil,

grain mill

Date of Operation:Date of Operation:Date of Operation:Date of Operation:

August 2007

Annual Capacity:Annual Capacity:Annual Capacity:Annual Capacity:

40.0 mmgy

Technology:Technology:Technology:Technology:

Dry mill, WDG, corn

oil, CO2

Date of Operation:Date of Operation:Date of Operation:Date of Operation:

April 2008

Annual Capacity:Annual Capacity:Annual Capacity:Annual Capacity:

60.0 mmgy

Technology:Technology:Technology:Technology:

Dry mill, WDG, corn oil

14

Western BiorefineriesWestern BiorefineriesWestern BiorefineriesWestern BiorefineriesStrategically located in the feed and fuel markets they serve

Boardman, ORBoardman, ORBoardman, ORBoardman, OR

Pekin, IL Pekin, IL Pekin, IL Pekin, IL –––– Dry MillDry MillDry MillDry Mill

Pekin, IL Pekin, IL Pekin, IL Pekin, IL –––– Wet Mill / YeastWet Mill / YeastWet Mill / YeastWet Mill / Yeast

15

Aurora, NEAurora, NEAurora, NEAurora, NE

Aurora, NEAurora, NEAurora, NEAurora, NE

Date of Operation:Date of Operation:Date of Operation:Date of Operation:

2012

Annual Capacity:Annual Capacity:Annual Capacity:Annual Capacity:

110.0 mmgy

Technology:Technology:Technology:Technology:

Dry mill, DDG/WDG,

corn oil

Date of Operation:Date of Operation:Date of Operation:Date of Operation:

1995

Annual Capacity:Annual Capacity:Annual Capacity:Annual Capacity:

45.0 mmgy

Technology:Technology:Technology:Technology:

Dry mill, DDG/WDG,

corn oil

Date of Operation:Date of Operation:Date of Operation:Date of Operation:

2007

Annual Capacity:Annual Capacity:Annual Capacity:Annual Capacity:

60.0 mmgy

Technology:Technology:Technology:Technology:

Dry mill, DDG, corn oil

Date of Operation:Date of Operation:Date of Operation:Date of Operation:

1981 / 1999

Annual Capacity:Annual Capacity:Annual Capacity:Annual Capacity:

100.0 mmgy / 55

mlbs/yr

Technology:Technology:Technology:Technology:

Wet mill, corn gluten

feed, corn germ & meal,

CO2, yeast

Yeast plantYeast plantYeast plantYeast plant

Midwest BiorefineriesMidwest BiorefineriesMidwest BiorefineriesMidwest BiorefineriesLocated near feedstock sources and directly linked to strong markets for ethanol and co-products

Distillers Grains with Solubles (DGS) & Wet Distillers Grains (WDG)

Production of over 1M tons per year (tpy) (dry matter) of DDG & WDG

• Pacific Ethanol plants are strategically located near dairies and feedlots and able to sell WDG directly to those users in the heart of the livestock industries of California, Oregon, Idaho and Nebraska

Distillers Corn Oil

Production of over 85M pounds of corn oil

• All Pacific Ethanol facilities produce corn oil, which is sold into feed markets as well as feedstock markets for biodiesel production

CO2

Production over 100K tons annually

• Pacific Ethanol sells raw CO2, another co-product of ethanol production, for processing into liquid CO2 and dry ice

16

Dry Mill CoDry Mill CoDry Mill CoDry Mill Co----Product PlatformProduct PlatformProduct PlatformProduct Platform

17

Corn Gluten Meal & Corn Gluten Feed

Production of 265k tpy of corn gluten feed and corn gluten meal annually

• Corn gluten meal is used primarily as a protein source and corn gluten

feed is used as fiber, starch and steep water source in poultry,

livestock rations, fish and pet foods

Corn Condensed Distillers Solubles (CCDS)

• CCDS is a palatable, free-flowing, energy and protein source for cattle

and fits into a large number of feeding programs

Corn Germ

Production of 70K tons of corn germ annually

• Through the wet milling process Aventine separates off the germ of

the corn kernel and sends it to third parties for further processing into

corn oil and corn germ meal.

Yeast

Production of over 50M pounds annually

• When extracted from the starch stream in the wet mill, yeast is

processed, dried, bagged and sold for animal, pet and human food

applications and is AIB food grade and also Kosher certified

Wet Mill CoWet Mill CoWet Mill CoWet Mill Co----Product PlatformProduct PlatformProduct PlatformProduct Platform

18

First of its kind registration from the Environmental Protection Agency (EPA)

o Production uses Edeniq Pathway and Cellunator technologies

o Achieving targeted yield increases of > 2%

o Expected to provide meaningful contribution to plant profitability

o Long-term goal to expand cellulosic production technology

to additional plants

Cellulosic Ethanol Production Generating ValueCellulosic Ethanol Production Generating ValueCellulosic Ethanol Production Generating ValueCellulosic Ethanol Production Generating Value

Now generating high-value Renewable Identification Numbers (RINs) at Stockton facility

Pacific Ethanol’s Stockton, CA ethanol facility

19

5 Megawatt solar photovoltaic (PV) power system at Madera plant

Reduces cost of operations

• Displaces approximately one-third of the grid electricity currently used

• Expected to cut annual utility operating costs by over $1 million,

not including tax credits

Improves carbon score

• Drives premium pricing on ethanol produced due to reductions in

carbon-intensity

• California’s Low Carbon Fuel Standard supports premium pricing for

ethanol produced with lower carbon scores

Source: SolarEnergyArena.com

Installing Solar PowerInstalling Solar PowerInstalling Solar PowerInstalling Solar Power

Expected to be fully operational

in early 2018 after

interconnection agreements

with local utility company

1st Ever Commercial Solar Electricity Project at a U.S. Ethanol Plant

Lower operating costs

Reduce energy demand

Increase yields

Low-cost operating platform

20

Additional Plant Additional Plant Additional Plant Additional Plant Investment InitiativesInvestment InitiativesInvestment InitiativesInvestment Initiatives

Initiated startup of industrial scale

membrane system at Madera plant

Expect to begin commercial

operations of cogeneration technology

at Stockton plant by December 2016

Expect a strong and supportive environment for ethanol into 2017

21

o Oil prices are forecasted to remain stable or move modestly higher

o Supply and Demand expected to remain well balanced

o Domestic demand set to strengthen as E15 expands, driven by new infrastructure and higher blending levels called for by the RFS

o Export forecasts remain robust as US ethanol remains the most competitively priced octane component in world markets

Encouraging Industry OutlookEncouraging Industry OutlookEncouraging Industry OutlookEncouraging Industry Outlook

3 Mos. 3 Mos. 3 Mos. 3 Mos.

9/30/169/30/169/30/169/30/16

3 Mos. 3 Mos. 3 Mos. 3 Mos.

9/30/159/30/159/30/159/30/15

9 Mos. 9 Mos. 9 Mos. 9 Mos.

9/30/169/30/169/30/169/30/16

9 Mos. 9 Mos. 9 Mos. 9 Mos.

9/30/159/30/159/30/159/30/15

Net sales $ 417,806 $ 380,622 $ 1,183,039 $ 814,419

Gross profit (loss) 6,364 (7,380) 25,137 (2,113)

SG&A 5,971 7,446 20,436 16,344

Operating income (loss) 393 (14,826) 4,701 (18,457)

Fair value adjustments (69) 1,202 (53) 1,413

Interest expense, net (3,874) (5,167) (16,643) (7,187)

Other income, net 32 203 92 16

Provision (benefit) for income taxes -- (3,925) (245) (6,095)

Consolidated net loss(3,518) (14,663) (11,658) (18,120)

Net loss available to common stockholders $ (3,837) $ (14,982) $ (12,607) $ (18,979)

Net loss per share, basic & diluted $ (0.09) $ (0.36) $ (0.30) $ (0.63)

Adjusted EBITDA(1)$ 9,282 $ 2,432 $ 31,319 $ 5,212

(1) A reconciling table for Adjusted EBITDA is available on slide 18 of the presentation

(Figures below in thousands, except per share amounts)

22

Consolidated Statement of OperationsConsolidated Statement of OperationsConsolidated Statement of OperationsConsolidated Statement of Operations

Net loss reflects the following

o Higher beginning inventory

valuation

o Lower margins in the ethanol

trading business resulting

from an intra-quarter drop in

ethanol prices

o Significant repair expense

o Non-cash mark-to-market

adjustments related to open

hedge positions

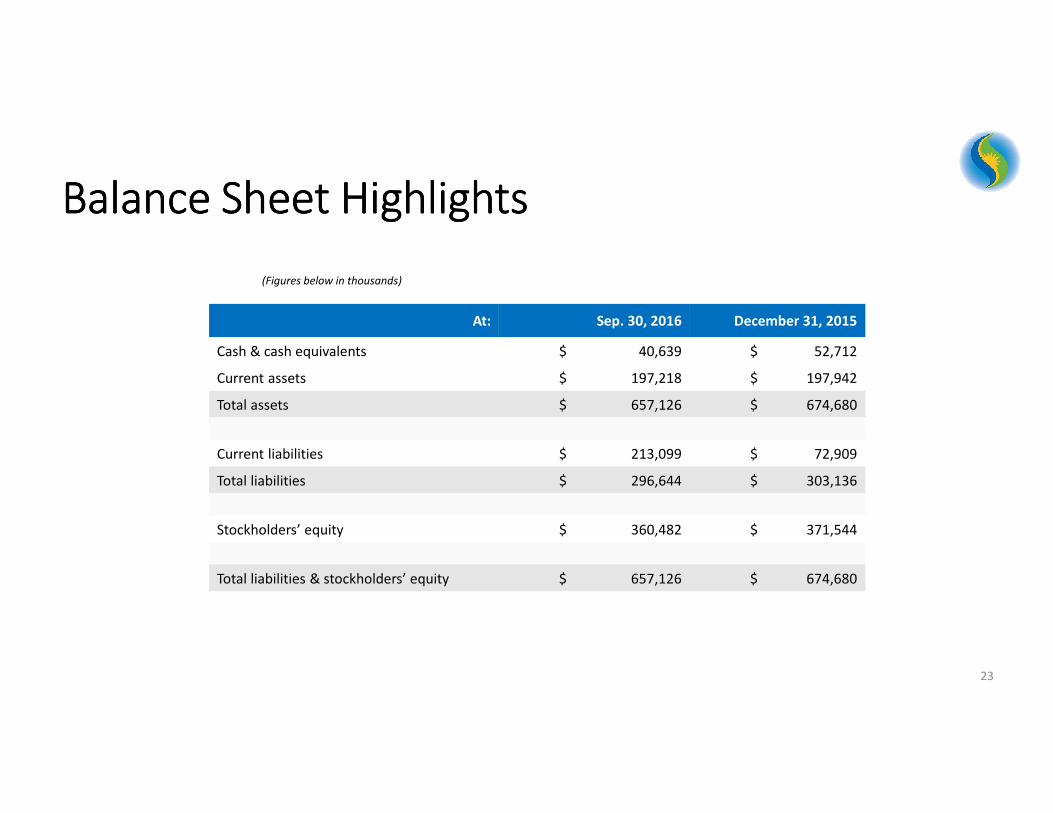

At: Sep. 30, 2016 December 31, 2015

Cash & cash equivalents $ 40,639 $ 52,712

Current assets $ 197,218 $ 197,942

Total assets $ 657,126 $ 674,680

Current liabilities $ 213,099 $ 72,909

Total liabilities $ 296,644 $ 303,136

Stockholders’ equity $ 360,482 $ 371,544

Total liabilities & stockholders’ equity $ 657,126 $ 674,680

(Figures below in thousands)

23

Balance Sheet HighlightsBalance Sheet HighlightsBalance Sheet HighlightsBalance Sheet Highlights

24

Strategy for GrowthStrategy for GrowthStrategy for GrowthStrategy for Growth

o Evaluating and investing in innovative technologies that optimize plant efficiencies,

improve our carbon score and ultimately enhance our profitability

o Reduce cost of capital by restructuring term debt

o Leverage diverse base of production and marketing assets to expand share of renewable

fuel and co-product markets

Lower carbon scoreStrengthen

balance sheet

Implement plant

improvements

Leverage diverse

assets

TTTTHANKHANKHANKHANK YYYYOUOUOUOU

25

26

AAAAPPENDIXPPENDIXPPENDIXPPENDIX

Management believes that certain financial measures not in accordance with generally accepted accounting principles (GAAP) are useful measures of operations.

The company defines Adjusted EBITDA as unaudited net income (loss) attributed to Pacific Ethanol before interest, provision (benefit) for income taxes, fair value adjustments,

purchase accounting adjustments and depreciation and amortization expense. A table is provided at the end of this presentation that provides a reconciliation of Adjusted

EBITDA to its most directly comparable GAAP measure. Management provides this non-GAAP measure so that investors will have the same financial information that

management uses, which may assist investors in properly assessing the company’s performance on a period-over-period basis. Adjusted EBITDA is not a measure of financial

performance under GAAP, and should not be considered an alternative to net income or any other measure of performance under GAAP, or to cash flows from operating,

investing or financing activities as an indicator of cash flows or as a measure of liquidity. Adjusted EBITDA has limitations as an analytical tool and you should not consider this

measures in isolation or as a substitute for analysis of the company’s results as reported under GAAP.

27

Use of NonUse of NonUse of NonUse of Non----GAAP Measures GAAP Measures GAAP Measures GAAP Measures

* Adjusted for non-controlling interests

3 Mos. 3 Mos. 3 Mos. 3 Mos.

9/30/169/30/169/30/169/30/16

3 Mos. 3 Mos. 3 Mos. 3 Mos.

9/30/159/30/159/30/159/30/15

9 Mos. 9 Mos. 9 Mos. 9 Mos.

9/30/169/30/169/30/169/30/16

9 Mos. 9 Mos. 9 Mos. 9 Mos.

9/30/159/30/159/30/159/30/15

Net loss attributed to Pacific Ethanol $ (3,518) $ (14,663) $ (11,658) $ (18,033)

Adjustments:

Interest expense* 3,874 5,167 16,643 7,134

Provision (benefit) for income taxes -- (3,925) (245) (6,095)

Purchase accounting adjustments -- 8,700 -- 8,700

Fair value adjustments 69 (1,202) 53 (1,413)

Depreciation and amortization expense* 8,857 8,355 26,526 14,919

Total adjustments 12,800 17,095 42,977 23,245

Adjusted EBITDA $ 9,282 $ 2,432 $ 31,319 $ 5,212

(Figures below in thousands)

28

Adjusted EBITDA ReconciliationAdjusted EBITDA ReconciliationAdjusted EBITDA ReconciliationAdjusted EBITDA Reconciliation

* Adjusted for noncontrolling interest.