Embed Size (px)

Citation preview

Overview of Commercial Banking

Overview of Commercial Banking

Ken CarsonSVP/Credit Administrator

Umpqua Bank

February 8, 2006

Ken CarsonSVP/Credit Administrator

Umpqua Bank

February 8, 2006

AgendaAgenda

•Marketing•Commercial Lending•Credit Assessment•Credit Policy•Pricing•Problem Loans•Careers in Commerical

Lending

•Marketing•Commercial Lending•Credit Assessment•Credit Policy•Pricing•Problem Loans•Careers in Commerical

Lending

Marketing Commercial Banking Products

Marketing Commercial Banking Products

Consumer Lead Product:– The checking account

Commercial Lead Product:– The loan

Consumer Lead Product:– The checking account

Commercial Lead Product:– The loan

Marketing Commercial Banking Products

Marketing Commercial Banking Products

Commercial Banking Products:– Loans– Depository– Cash Management Services– Merchant Visa– Internet & Electronic Banking– Investments– Leases

Commercial Banking Products:– Loans– Depository– Cash Management Services– Merchant Visa– Internet & Electronic Banking– Investments– Leases

Marketing Commercial Banking Products

Marketing Commercial Banking Products

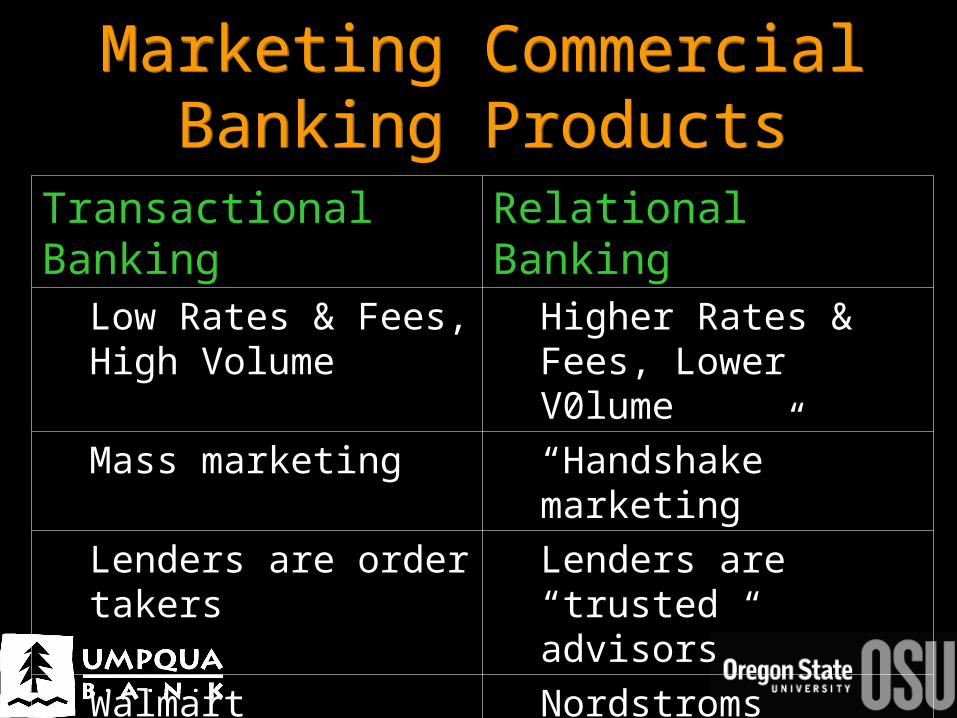

Transactional Banking

Relational Banking

Low Rates & Fees, High Volume

Higher Rates & Fees, Lower V0lume

Mass marketing “Handshake” marketing

Lenders are order takers

Lenders are “trusted advisors”

Walmart Nordstroms

Marketing Commercial Banking Products

Marketing Commercial Banking Products

Competition– Other Commercial Banks– Non-Bank Competition– Quasi-governmental agencies

Competition– Other Commercial Banks– Non-Bank Competition– Quasi-governmental agencies

Commercial LoansCommercial Loans

Types of Commercial Loans– Short Term Working Capital

Loans– Revolving Lines of Credit– Term Loans– Commercial Real Estate Loans

Types of Commercial Loans– Short Term Working Capital

Loans– Revolving Lines of Credit– Term Loans– Commercial Real Estate Loans

Commercial LoansCommercial Loans

Cash Flow vs. Asset BasedCash Flow vs. Asset BasedCash Flow Based Asset Based

Repayment: Profits Repayment: Liquidiation

Collateral: Unsecured

Collateral: Secured

Not margined Margined

Cash Flow Covenants Working Capital Covenants

Credit AssessmentCredit Assessment

The Five C’s– Character– Capacity

The Five C’s– Character– Capacity

Credit AssessmentCredit Assessment

CapacityCapacity

The Key Principle:The Key Principle:

Loans are repaid by cash, Loans are repaid by cash,

notnot by profits. by profits.

The Key Principle:The Key Principle:

Loans are repaid by cash, Loans are repaid by cash,

notnot by profits. by profits.

Credit AssessmentCredit Assessment

CapacityCapacity

Corollary to the Key PrincipleCorollary to the Key Principle

Your loan is repaid by cash, Your loan is repaid by cash,

notnot by ratios. by ratios.

Corollary to the Key PrincipleCorollary to the Key Principle

Your loan is repaid by cash, Your loan is repaid by cash,

notnot by ratios. by ratios.

Credit AssessmentCredit Assessment

The Five C’s– Character– Capacity

The Five C’s– Character– Capacity – Capital– Collateral– Conditions

– Capital– Collateral– Conditions

Credit Policies and Procedures

Credit Policies and Procedures

Internal Credit Procedures– Board of Directors– Chief Credit Officer– Credit Committee vs. One-over-one– House Limit & the Legal Lending Limit– Total Credit Exposure

Internal Credit Procedures– Board of Directors– Chief Credit Officer– Credit Committee vs. One-over-one– House Limit & the Legal Lending Limit– Total Credit Exposure

Credit Policies and Procedures

Credit Policies and Procedures

Monitoring Loans– Loan Covenants– Collateral Monitoring– Risk Ratings

Monitoring Loans– Loan Covenants– Collateral Monitoring– Risk Ratings

Credit Policies and Procedures

Credit Policies and Procedures

Lending Between Banks– Why?

•Reduce concentration risk•Manage overall portfolio•Manage the bank’s balance sheet

– Types of inter-bank lending•Syndications•Participations•Sale to the Secondary market

Lending Between Banks– Why?

•Reduce concentration risk•Manage overall portfolio•Manage the bank’s balance sheet

– Types of inter-bank lending•Syndications•Participations•Sale to the Secondary market

Pricing LoansPricing Loans

Pricing Structures– Variable Rate Loans– Fixed Rate Loans– Swaps, Collars & Other

Derivates– Loan Fees

Pricing Structures– Variable Rate Loans– Fixed Rate Loans– Swaps, Collars & Other

Derivates– Loan Fees

Pricing LoansPricing Loans

Pricing Considerations– Cost of Funds

•Actual Cost of Funds•Marginal Cost of Funds

Pricing Considerations– Cost of Funds

•Actual Cost of Funds•Marginal Cost of Funds

Interest Rate Yield Curve

Interest Rate Yield CurveInterest Rate Changes

Federal Home Loan Bank Rates

0.000

1.000

2.000

3.000

4.000

5.000

6.000

Jan-04

Mar-04

May-04

Jul-04

Sep-04

Nov-04

Jan-05

Mar-05

May-05

Jul-05

Sep-05

Nov-05

Jan-06

Month

Pe

rce

nt

CMA1-Year3-Year5-Year10-year

Interest Rate ChangesFederal Home Loan Bank Rates

0.000

1.000

2.000

3.000

4.000

5.000

6.000

Jan-04

Mar-04

May-04

Jul-04

Sep-04

Nov-04

Jan-05

Mar-05

May-05

Jul-05

Sep-05

Nov-05

Jan-06

Month

Pe

rce

nt

CMA1-Year3-Year5-Year10-year

Pricing LoansPricing Loans

Pricing Considerations– Cost of Funds

•Actual Cost of Funds•Marginal Cost of Funds

– Risk Factors– Market Factors– Relationship Factors

Pricing Considerations– Cost of Funds

•Actual Cost of Funds•Marginal Cost of Funds

– Risk Factors– Market Factors– Relationship Factors

Managing Problem Loans

Managing Problem Loans

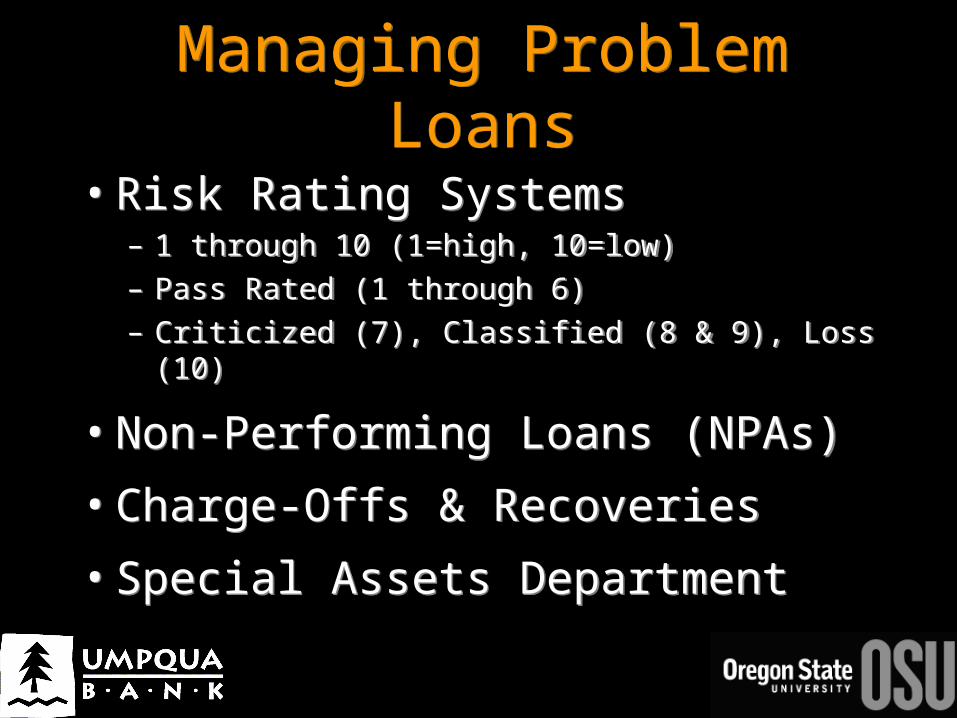

• Risk Rating Systems– 1 through 10 (1=high, 10=low)– Pass Rated (1 through 6)– Criticized (7), Classified (8 & 9), Loss (10)

• Non-Performing Loans (NPAs)

• Charge-Offs & Recoveries

• Special Assets Department

• Risk Rating Systems– 1 through 10 (1=high, 10=low)– Pass Rated (1 through 6)– Criticized (7), Classified (8 & 9), Loss (10)

• Non-Performing Loans (NPAs)

• Charge-Offs & Recoveries

• Special Assets Department

Loan Loss AllocationLoan Loss Allocation

Beginning Allocation 44.2

- Charge Offs -7.8

+ Recoveries +4.9

+ Loss Provision Exp. +2.5

= Ending Allocation =43.8

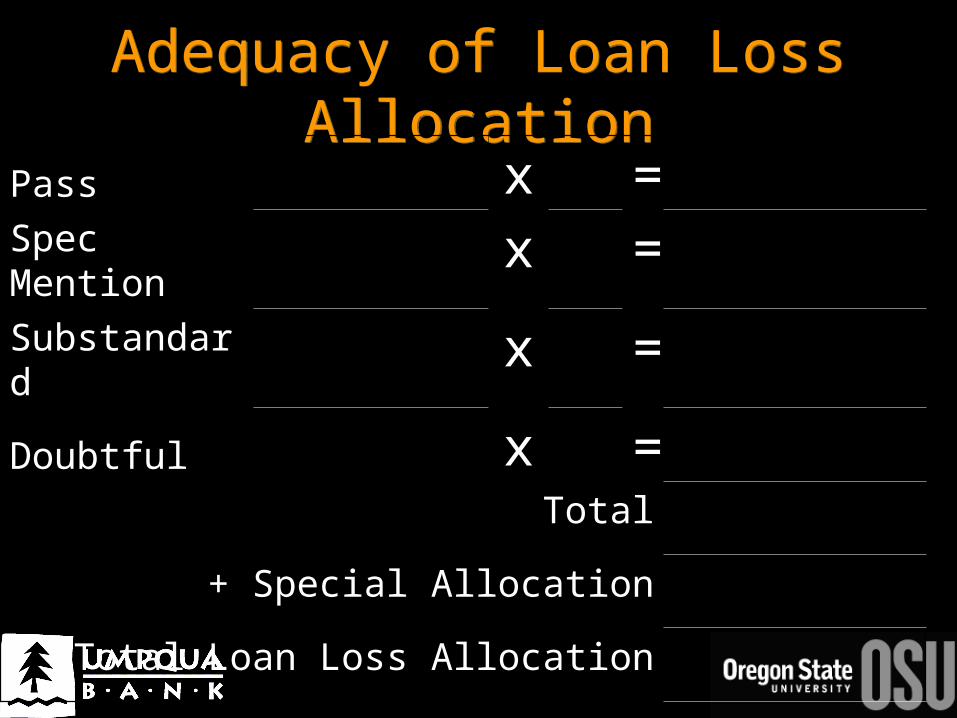

Adequacy of Loan Loss Allocation

Adequacy of Loan Loss Allocation

Pass x =Spec Mention

x =

Substandard

x =

Doubtful x =Total

+ Special Allocation

Total Loan Loss Allocation

Careers in BankingCareers in Banking

The Typical Career Path– Loan Assistant– Credit Analyst– Assistant Relationship Manager– Relationship Manager

The Typical Career Path– Loan Assistant– Credit Analyst– Assistant Relationship Manager– Relationship Manager

Careers in BankingCareers in Banking

Skills & Character Qualities– Non-negotiables

•You will be drug tested•No criminal records

Skills & Character Qualities– Non-negotiables

•You will be drug tested•No criminal records

Careers in BankingCareers in Banking

Skills & Character Qualities– Technical Skills

•Accounting•Computer Skills

Skills & Character Qualities– Technical Skills

•Accounting•Computer Skills

Careers in BankingCareers in Banking

Skills & Character Qualities– Character Qualities

•Work Ethic & Initiative•Professionalism•Teachable•Patience

Skills & Character Qualities– Character Qualities

•Work Ethic & Initiative•Professionalism•Teachable•Patience

![Umpqua bank san francisco [finno]](https://img.pdfslide.us/doc/110x75/54c92db44a7959f7238b45e9/umpqua-bank-san-francisco-finno.jpg)