Embed Size (px)

Citation preview

Overview of

Assurance Standards &

Documentation

LUNAWAT & CO.Chartered AccountantsLUNAWAT & CO.Chartered Accountants CA. PRAMOD JAIN

FCA, FCS, FCMA, LL.B, MIMA, DISA

CA. PRAMOD JAINFCA, FCS, FCMA, LL.B, MIMA, DISA17th September 201417th September 2014

Applicability

� Every CA performing assurance practice have to comply with Technical Standards

� Audit & Assurance Standards are also Technical Standards

�With effect from 1stApril 2008 Auditing and Assurance Standards (AAS) have been re-classified

� Gets a legal backing by Companies Act 2013

Lunawat & Co.

Companies Act 2013

� 2 (7) - “Auditing Standards” means the standards of auditing or any addendum thereto for companies or class of companies referred to in s. 143 (10)

� 132(1)(a) – NFRA to recommend to CG –◦ auditing policies and standards for adoption by companies or class of companies or their auditors, as the case may be.

◦ to monitor and enforce these standards

◦ oversee the quality of service of the professions associated with ensuring compliance with such standards

� 143(2)-Auditor to ensure compliance while issuing report

� 143(9) - Auditor to comply with the auditing standards

� 143(10) – CG to prescribe SAs – till notification ICAI

Lunawat & Co.

No. of Standards

Type of Standards Numerical Series

No. of Standard

Standards on Quality Control (SQC)

01-99 1

Standards on Auditing (SA) 100-999 37

Standards on Review Engagements (SRE)

2000-2699 2

Standards on Assurance Engagements (SAE)

3000-3699 2

Standards on Related Services (SRS)

4000-4699 2

Standards on Internal Audit (SIA)

18

Lunawat & Co.

Standards on Auditing

SA. No.

Sub-division No.

100-199 Introductory Matters 0

200-299 General Principles & Responsibilities 9

300-499 Risk Assessment and Response to Assessed Risks

6

500-599 Audit Evidence 11

600-699 Using Work of Others 3

700-799 Audit Conclusions and Reporting 5

800-899 Specialized Areas 3

Lunawat & Co.

General Principles & Responsibilities

SA. No.

Sub-division

200 Overall Objectives of the Independent Auditor and the Conduct of

an Audit in Accordance with Standards on Auditing

210 Agreeing the terms of Audit Engagement

220 Quality Control for an Audit of Financial Statements

230 Audit Documentation

240 The Auditor’s Responsibility to consider Fraud in an Audit of

Financial Statements

250 Consideration of Laws and regulations in an Audit of Financial

Statements

260 Communications with Those Charged with Governance

265 Communicating Deficiencies in Internal Control

299 Responsibility of Joint auditors

Lunawat & Co.

Risk Assessment & Response to Assessed Risks

SA. No.

Sub-division

300 Planning an Audit of Financial Statements

315 Identifying and assessing the Risks of Material

Misstatement through understanding the entity and its

Environment

320 Materiality in Planning and Performing an Audit

330 The Auditor’s Response to Assessed Risks

402 Audit consideration relating to entities using Service

Organisations

450 Evaluation of Misstatements identified during the

Audit

Lunawat & Co.

Audit Evidence

SA. No.

Sub-division

500 Audit Evidence

501 Audit Evidence – Specific Considerations for

Selected Items

505 External Confirmations

510 Initial Engagements – Opening Balances

520 Analytical Procedures

530 Audit Sampling

540 Auditing accounting estimates, including Fair

Value Accounting estimates, and related

disclosures

Lunawat & Co.

Audit Evidence

SA. No.

Sub-division

550 Related Parties

560 Subsequent Events

570 Going Concern

580 Written Representations

Lunawat & Co.

Using Work of Others

SA. No.

Sub-division

600 Using the Work of Another Auditor

610 Using the Work of Internal Auditors

620 Using the Work of an Auditor’s Expert

Lunawat & Co.

AUDIT CONCLUSIONS AND REPORTING

SA. No.

Sub-division

700 Forming an Opinion and Reporting on Financial

Statements

705 Modifications to the Opinion in the Independent

Auditor’s Report

706 Emphasis of Matter Paragraphs and Other Matter

Paragraphs in the Independent Auditor

710 Comparative Information—Corresponding Figures

and Comparative Financial Statements

720 The Auditor’s Responsibility in relation to other

information in Documents containing Audited

Financial Statements

Lunawat & Co.

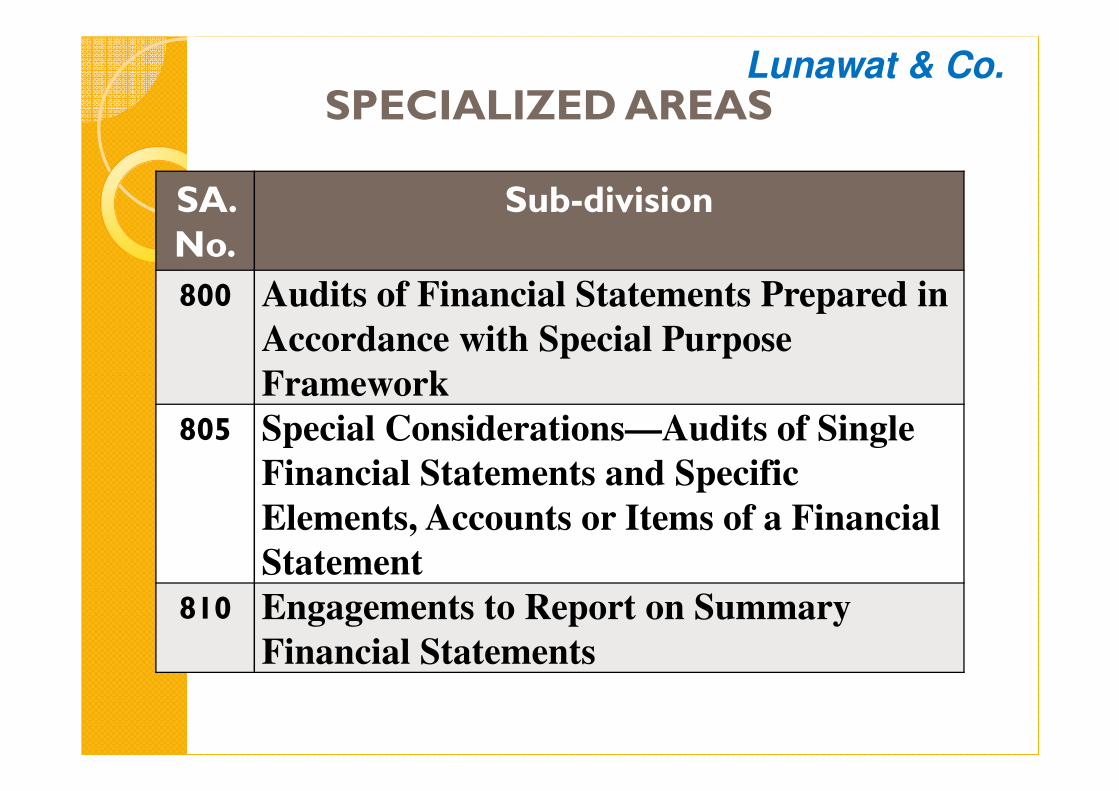

SPECIALIZED AREAS

SA. No.

Sub-division

800 Audits of Financial Statements Prepared in

Accordance with Special Purpose

Framework

805 Special Considerations—Audits of Single

Financial Statements and Specific

Elements, Accounts or Items of a Financial

Statement

810 Engagements to Report on Summary

Financial Statements

Lunawat & Co.

Standards on Review Engagements

SRE No.

Sub-division

2400 Engagements to Review Financial Statements

2410 Review of Interim Financial Information Performed by the Independent Auditor of the Entity

Lunawat & Co.

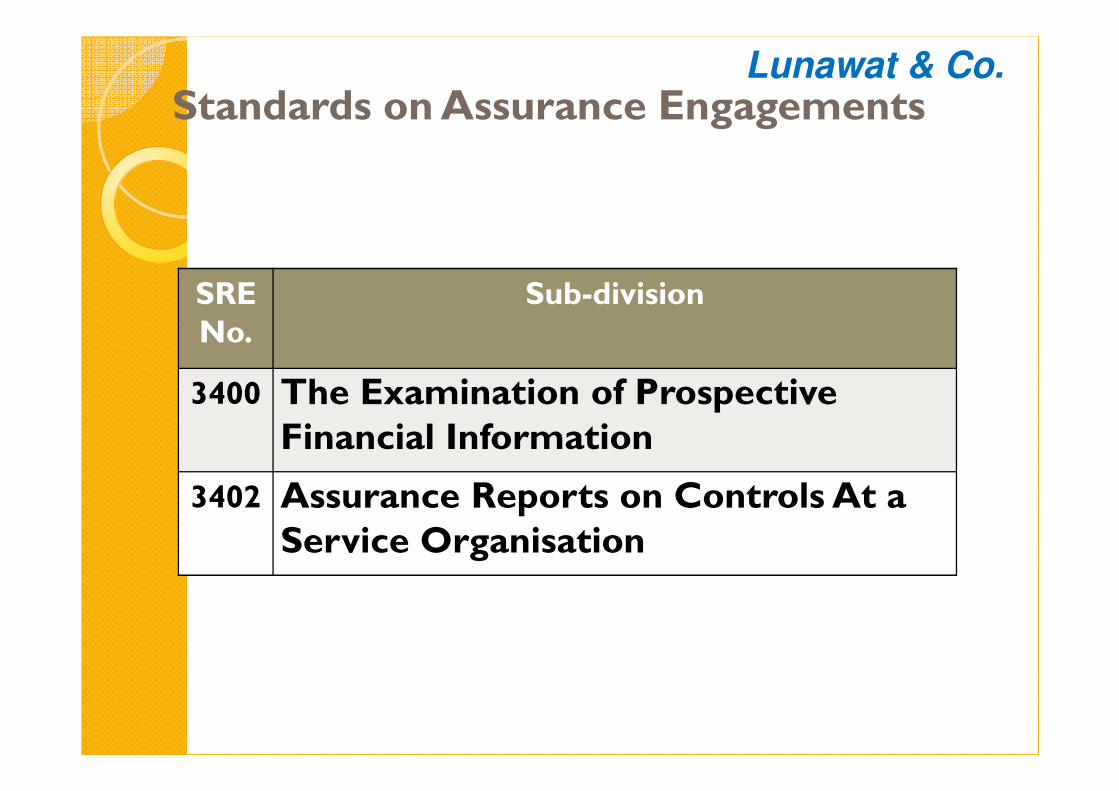

Standards on Assurance Engagements

SRE No.

Sub-division

3400 The Examination of Prospective Financial Information

3402 Assurance Reports on Controls At a Service Organisation

Lunawat & Co.

Standards on Related Services

SRE No.

Sub-division

4400 Engagements to Perform Agreed-upon Procedures regarding Financial Information

4410 Engagements to Compile Financial Information

Lunawat & Co.

Standards on Internal Audit

SIA No. Standard

1 Planning an Internal Audit

2 Basic Principles Governing Internal Audit

3 Documentation

4 Reporting

5 Sampling

6 Analytical Procedures

7 Quality Assurance in Internal Audit

8 Terms of Internal Audit Engagement

9 Communication with Management

Lunawat & Co.

Standards on Internal AuditS No. Standard

10 Internal Audit Evidence

11 Consideration of Fraud in an Internal Audit

12 Internal Control Evaluation

13 Enterprise Risk Management

14 Internal Audit in an Information Technology Environment

15 Knowledge of the Entity & its Environment

16 Using the Work of an Expert

17 Consideration of Laws and Regulations in an Internal Audit

18 Related Parties

Lunawat & Co.

SQC� Only 1 - Quality control for Firms that perform Audits and Reviews of Historical Financial Information, & Other Assurance and related Services Engagements

� Mandatory - For all engagements relating to accounting periods beginning on/after1.4.09

� Objective -To provide guidance regarding a firm’s responsibilities for its system of quality control for:◦ Audits of historical financial information ◦ Reviews of historical financial information◦ For other assurance◦ For related services engagements

� Peer Review after 1.4.2014

Lunawat & Co.

Lunawat & Co.

QC to Include Policies for

� Leadership responsibilities for quality within the firm

� Ethical requirements

� Acceptance and continuance of client relationship and specific engagements

� Human resources

� Engagement performance

� Monitoring

Lunawat & Co.

Code of Conduct

� Integrity

� Independency

� Objectivity

� Professional competence and due care

� Confidentiality

� Professional behaviour

Lunawat & Co.

SA-230 - Documentation

In today’s scenario, where the quality of audit and assurance work is getting increasingly questioned and auditors are being called to

justify their opinion,

adequate documentation

is the only way for an

auditor to substantiate that he was

not negligent

Lunawat & Co.

Maintenance of Professional Skills and Standards

� Staff Supervision and Development Policy

� Guidelines for Maintenance of Professional Skills and Standards

� Policy Regarding Considering of Skill and Competence Before Assignment of Attestation Engagement

Lunawat & Co.

Staff Supervision and Development

� Recruitment Policy

� Staff Appointment Letter

� Monthly Staff Performance Sheet

� Registers of Continuing Professional Education of firm’s Personnel.

� Register of In-house Continuing Professional Education.

Lunawat & Co.

Independence Policies and its Communication

� Policy of Independence

� Register of Disclosure of Interest by Partners and Staff in Professional Assignments Handled by the Firm

� Policy Regarding Acceptance of An Engagement

Lunawat & Co.

Outside Consultation

� Guidelines for Maintenance of Professional Skills and Standards.

� Procedure for Consultation

� Expert Consultants’ List

� Document whenever consultation is done as per the policy of the firm.

Lunawat & Co.

Review and Evaluation of System of Internal Controls

� Knowledge of Client’s Business.

� Authorization Matrix

� Audit Program.

� List of documents a firm should obtain during Attestation Service Engagement – internal control policies.

� Risk Assessment Checklist.

Lunawat & Co.

Substantive Tests

� Knowledge of Client’s Business.

� Audit Program.

� Materiality Planning

� Letter to be sent by Auditee to Bankers for External Confirmation Directly in Name of firm.

� Letter to be sent by Auditee to Parties for Balance Confirmation Directly in Name of firm.

� Letter to be sent by Auditee to Concerns with Whom Stocks of the Auditee are kept, and are to be confirmed.

Lunawat & Co.

Audit Record Administration� Appointment Letter

� Audit Engagement letter.

� Engagement Initiation Letter.

� List of Documents a firm should obtain during Attestation Service Engagement.

� Audit Program.

� CARO Requirement Checklist.

� Risk Assessment Checklist.

� AS Verification checklist.

� Ratio Analysis Sheet.

� Overall Certificates.

� Representation letters.

Lunawat & Co.

Financial Statements Presentation

� Compliance Overview of Accounting Standards for Corporate Enterprises by firm during Audit.

� Compliance Overview of Accounting Standards for Non-Corporate Enterprises by firm during Audit.

� List of documents a firm should obtain during Attestation Service Engagement.

� Overall Certificates

� Management representation letters

Lunawat & Co.

Audit Conclusions and Reporting

� AS verification checklists

� List of documents a firm should obtain during Attestation Service Engagement.

� Overall Certificates

� CARO Requirement Checklist.

� Management representation letters.

� Signed final trial balance.

� Signed financial statements.

Lunawat & Co.

Office Administration

� Code of Conduct

� Policies and Procedures for Recording and Monitoring of Incoming and Outgoing Documents.

� Policies for Attendance of Staff including Staff Going on Audits.

� Policies for Billing and Follow up.

� Policy of Retention of Client.

� Policies and Procedures for Disaster Recovery Plan (DRP) and Business Continuity Plan (BCP).

Lunawat & Co.

Documentation

� Have checklists, tell articles to cross verify

� Seniors to cross verify

� Take necessary certificates / representation from management

� External Confirmations

� Comply with SAs

�Work not documented is work not done.

Lunawat & Co.

Lunawat & Co.