Embed Size (px)

Citation preview

8/29/2018 1

Outlook/Visi Pengembangan Industri Kopi, Kakao serta Industri Pengolahannya Lainnya

Forum Diskusi Pengembangan Industri dan Rantai Nilai Global: Pelajaran dari Sektor Kopi dan Kakao

Jakarta , 28 August 2018

Adhi LukmanChairman of Indonesian Food and Beverage Industry Association

DEVELOPMENT OF FOOD INDUSTRYTowards GVC

The 4th largest population.

261.9 millions (June, 2017)

GDP 1.004 Trillions USD

(2017)*

GDP growth 5.27%

(YoY-Q2-2018)

Inflation 3.12 % (YoY

Q2-2018)

Expenditure/capita

-Food 50.62 %-Processed food 17.15 %

of GDP (2017)

GDP per capita 3,876 USD (2017)

Indonesia

The 2nd longest Coastline

99,000 KM

13,466 islands

Contribution to GDP by Island (Q2-2018)

Arah Pembangunan Industri Nasional

5.61 % 4.84 %4.43 %5.05 %

5.32% 6.14 %5.97 %5.61 %

9.49% 9.23 %8.33 %7.54 %

4.41 %

2014 2015 2016 2017 2018 Q2

All About Food Industry (Source: BPS – MoI)

Non-Oil Industry Sector growth

Contribution Food

Industry to Total GDP

Food Industry growth

8.67 %

F&B is the Biggest Contributor to Public Consumption

F&B Industry (Source: BPS)

Category

2014 2015 Growth

Medium - Large Small & Micro Medium - Large Small & Micro Medium - Large Small & Micro

Food 877,771 2,324,212 719,116 3,664,208 (18.07) 57.65

Beverages 52681 81,027 46,379 85,167 (11.96) 5.11

Total 930,452 2,405,239 765,495 3,749,375 (17.73) 55.88

% 27.89 72.11 16.95 83.05

Category

2014 2015 Growth

Medium - Large Small & Micro Medium - Large Small & Micro Medium - Large Small & Micro

Food 5,794 1,198,491 5,438 1,567,019 (6.14) 30.75

Beverages 374 44,694 310 47,130 (17.11) 5.45

Total 6,168 1,243,185 5,748 1,614,149 (6.81) 29.84

% 0.49 99.51 0.35 99.65

Workers Engaged

Number of Establishment Source : BPS

All About Food Industry: F&B Investment Realization

Source: BKPM

Investment in F&B industry sector 2017: ➢DDI grow around 20% ➢FDI grow minus 7%

INVESTMENT

2014 2015 2016 2017

P I P I P I P I

DDI 493 19,596.39 879 24,533.99 1,169 32,028.50 1,419 38,540.10

(Rp. Billions)

FDI 1,054 3,139.60 886 1,521.18 1,947 2,115.00 1,649 1,970.30

(USD million)

Total 1,547 1,765 3,116 3,068

FDI Food Industry 586.7 Million USD

8/29/2018 12

Ease Of Doing

Business Index 2018

# 72 of 190 (91 of 190) Countries

#6 in ASEAN

The Global Competitiveness Index

2017 – 2018

36 of 137(41 of 138)Countries

#4 in ASEAN

LogisticPerformance Index 201846 0f 167

(63 of 160)Countries

#5 in ASEAN

Labor Productivity per worker GDP 2012

#4 in ASEAN

Global Food Security

Index 2017

69 of 113 Countries

(71 of 113)#5 in

ASEAN

The Global Innovation Index 2017

87 of 127 Countries

#5 in ASEAN

INDONESIA in the World Rank

Trade Balance of Semi processed & Processed Food in 2014-2018 (April)In USD . Source: BPS/ Ministry of Trade

Export Import Balanced

2014 2015 2016 2017 2018 Apr 2014 2015 2016 2017 2018 Apr 2014 2015 2016 2017 2018 Apr

6.353.427.439 6.002.001.194 6.152.058.092 6.504.683.113 2.256.021.3667.304.062.157 6.278.094.256 7.063.688.813 7.807.647.063 2.418.132.060 -950.634.718 -276.093.062 -911.630.721 -1.302.963.950 -162.110.694

Export Import Balanced

Country 2014 2015 2016 2017 2018 Apr 2014 2015 2016 2017 2018 Apr 2014 2015 2016 2017 2018 Apr

MALAYSIA 813.305.570 785.566.583 735.289.971 704.925.394 225.357.729 392.852.447 331.810.997 386.036.415 489.775.664 179.240.439 420.453.123 453.755.586 349.253.556 215.149.730 46.117.290

PHILIPPINE 456.899.018 468.351.572 558.369.049 612.528.900 218.608.110 29.956.751 25.143.725 29.910.789 37.799.770 16.654.838 426.942.267 443.207.847 528.458.260 574.729.130 201.953.272

SINGAPORE 309.196.623 268.166.469 284.789.030 314.471.812 118.828.186 215.983.590 186.202.973 184.752.627 200.305.955 79.957.477 93.213.033 81.963.496 100.036.403 114.165.857 38.870.709

VIETNAM 223.762.918 231.197.147 295.497.627 291.108.463 74.929.255 24.189.870 49.755.636 37.885.175 57.933.920 27.556.694 199.573.048 181.441.511 257.612.452 233.174.543 47.372.561

CAMBODIA 307.079.757 271.217.783 284.468.926 287.720.284 83.603.973 18.170 22.817 404.570 375.905 3.518 307.061.587 271.194.966 284.064.356 287.344.379 83.600.455

THAILAND 187.767.449 186.750.794 203.284.548 203.982.509 77.184.143 870.044.570 856.477.952 1.134.814.892 1.361.172.913 456.101.626 -682.277.121 -669.727.158 -931.530.344 -1.157.190.404 -378.917.483

BRUNEI DARUSSALAM

13.244.236 13.901.646 14.187.345 12.240.986 4.107.817 0 0 0 1.110 200 13.244.236 13.901.646 14.187.345 12.239.876 4.107.617

MYANMAR 10.596.204 14.715.019 23.578.338 49.709.705 23.032.039 2.463.692 3.879.744 4.170.781 3.142.794 1.430.350 8.132.512 10.835.275 19.407.557 46.566.911 21.601.689

LAOS 123.094 152.381 184.638 352.296 12.066 50.617.818 741.902 54.885 463.261 0 -50.494.724 -589.521 129.753 -110.965 12.066

Indonesia – World

Indonesia – ASEAN

Indonesia – RECP plus

Indonesia -RCEP + Canada

Export Import Balanced

Country 2014 2015 2016 2017 2018 Apr 2014 2015 2016 2017 2018 Apr 2014 2015 2016 2017 2018 Apr

JAPAN 250,862,770 226,707,352 227,329,602 240,348,838 83,434,444 19,085,240 19,799,056 20,536,360 23,274,284 7,711,607 231,777,530 206,908,296 206,793,242 217,074,554 75,722,837

PR of CHINA 284,715,924 311,181,650 329,740,193 395,041,597 112,644,081 711,277,907 560,982,575 742,865,199 806,769,405 251,893,438 (426,561,983) (249,800,925) (413,125,006) (411,727,808) (139,249,357)

SOUTH KOREA 266,142,310 149,784,454 172,942,833 175,333,109 65,679,641 107,400,680 99,083,843 104,660,674 123,625,210 46,582,927 158,741,630 50,700,611 68,282,159 51,707,899 19,096,714

NEW ZEALAND 191,879,150 130,146,361 114,830,423 155,949,061 56,031,924 79,783,943 64,563,264 54,751,252 51,735,039 12,469,782 112,095,207 65,583,097 60,079,171 104,214,022 43,562,142

AUSTRALIA 156,792,692 171,938,542 152,890,834 165,231,710 65,408,877 534,128,428 511,516,419 525,902,863 420,569,925 64,325,050 (377,335,736) (339,577,877) (373,012,029) (255,338,215) 1,083,827

INDIA 73,159,685 80,753,824 89,522,434 90,066,304 39,358,441 177,847,853 90,199,505 80,040,579 93,853,422 41,968,885 (104,688,168) (9,445,681) 9,481,855 (3,787,118) (2,610,444)

CANADA 33,980,315 34,396,421 62,674,691 66,216,684 20,170,699 50,441,403 25,209,561 12,095,506 9,855,771 3,983,881 (16,461,088) 9,186,860 50,579,185 56,360,913 16,186,818

Trade Balance of Semi processed & Processed Food in 2014-2018 (April)In USD . Source: BPS/ Ministry of Trade

Huge Export Potential To Be Explored

(1,400,000,000)

(1,200,000,000)

(1,000,000,000)

(800,000,000)

(600,000,000)

(400,000,000)

(200,000,000)

0

200,000,000

400,000,000

600,000,000

800,000,000

USD

2014 2015 2016 2017 2018 Apr

Indonesia – ASEAN

(500,000,000)

(400,000,000)

(300,000,000)

(200,000,000)

(100,000,000)

0

100,000,000

200,000,000

300,000,000

JAPAN PR of CHINA SOUTH KOREA NEW ZEALAND AUSTRALIA INDIA TAIWAN CANADA

2014 2015 2016 2017 2018 Apr

Trade Balance of Semi processed & Processed Food in 2014-2018 (April)In USD . Source: BPS/ Ministry of Trade

Huge Export Potential To Be Explored

Indonesia – RECP ++

State of the Global Islamic Economy (GIE) Report 2017/2018(73 Countries) by Thomson Reuters

Challenges Along the Food Supply Chain

Competitiveness

TariffQuality

Nutrition

Healthier Choice

HALAL

Standard

Label

Regulation & Govt Policy

Logistic

Time delivery

Ethnic &

Habits.

Resources

Innovation

Disruptive Economic

Big Data

Food loss

Food waste

Profitability

Added Value

Cost related to raw material import, export , energy, logistic, etc.

Opportunity to Canada

The Three Stages of Export Preparation to Canada

Source: TPSA

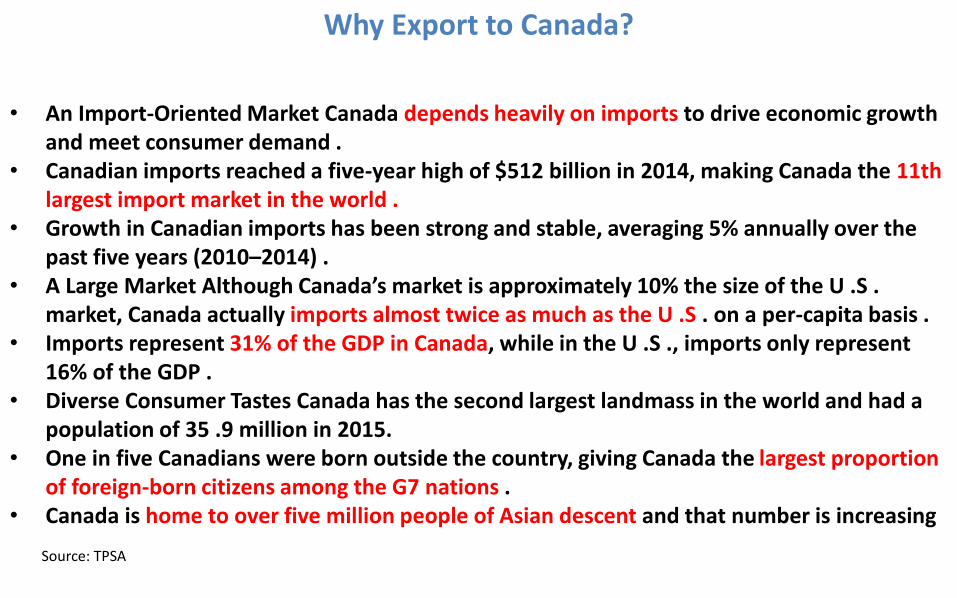

• An Import-Oriented Market Canada depends heavily on imports to drive economic growth and meet consumer demand .

• Canadian imports reached a five-year high of $512 billion in 2014, making Canada the 11th largest import market in the world .

• Growth in Canadian imports has been strong and stable, averaging 5% annually over the past five years (2010–2014) .

• A Large Market Although Canada’s market is approximately 10% the size of the U .S . market, Canada actually imports almost twice as much as the U .S . on a per-capita basis .

• Imports represent 31% of the GDP in Canada, while in the U .S ., imports only represent 16% of the GDP .

• Diverse Consumer Tastes Canada has the second largest landmass in the world and had a population of 35 .9 million in 2015.

• One in five Canadians were born outside the country, giving Canada the largest proportion of foreign-born citizens among the G7 nations .

• Canada is home to over five million people of Asian descent and that number is increasing

Why Export to Canada?

Source: TPSA

• Canada’s multiculturalism also influences mainstream consumer tastes . • A Strong Economy, grew by 2 .4% in 2014, and inflation rates have remained below 3% for

the past two decades . While Canada appeared to be entering a recession in mid-2015, the economy has remained stable and with a strong labour force .

• Increasing Exports from Southeast Asia to Canada. Exports from ASEAN countries to Canada have increased by 55% over the last 10 years . Canada’s overall imports only increased 35% in that same time period .

• A Strong Canada-Indonesia Partnership Indonesia and Canada have a long history of collaboration and cooperation .

Why Export to Canada?

Source: TPSA

Opportunities for Exporting to Canada (Agro-Food)

Source: TPSA *Normalized Revealed Comparative Advantage

Opportunities in Canada

Cocoa

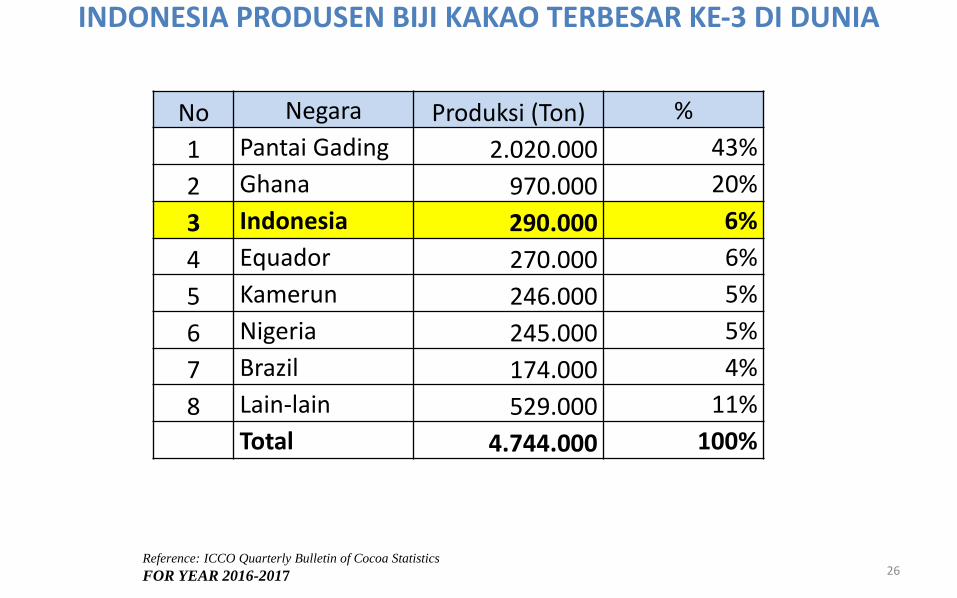

INDONESIA PRODUSEN BIJI KAKAO TERBESAR KE-3 DI DUNIA

Reference: ICCO Quarterly Bulletin of Cocoa Statistics

FOR YEAR 2016-2017

No Negara Produksi (Ton) %

1 Pantai Gading 2.020.000 43%

2 Ghana 970.000 20%

3 Indonesia 290.000 6%

4 Equador 270.000 6%

5 Kamerun 246.000 5%

6 Nigeria 245.000 5%

7 Brazil 174.000 4%

8 Lain-lain 529.000 11%

Total 4.744.000 100%

26

Proyeksi Demand & Supply Kakao Dunia

0

1

2

3

4

5

6

7

8

9

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

supply

demand

price

( U

SD

00

0 )

(Demand & Supply in million tones)27

28

KONSUMSI KAKAO DUNIA per negara (kg/capita)

World cocoa demand continues to increase 2-4% every year or about 80.000 tons-160.000 tons/year.

Source : ICCO 2010 edited

11.56

10.519.72 9.44

8.498.16

7.26

6.37 6.34 6.21

0.25 0.04 0.030

2

4

6

8

10

12

14

PRODUSEN KAKAO OLAHAN DUNIA

(OOO TONS)

Source : ICCO Ouarterly Bulletin of Cocoa Statistic. 29

No. Negara 2010 2011 2012 2013 2014 2015 2016

2017

1 Pantai Gading 411 431 471 535 519 558 510 577

2 Belanda 525 500 535 540 530 508 520 565

3 Indonesia 150 270 310 324 340 335370 455

4 Jerman 361 407 402 415 530 415 440 410

5 USA 382 387 413 418 446 400 410 390

6 Brasil 226 242 241 245 240 224 228 227

7 Ghana 212 212 225 228 234 234 210 250

8 Malaysia 298 297 293 260 259 195190 216

9 Singapura 80 80 80 80 80 80 80 80

10 Lain-lain 1,086 1,146 1,141 1,217 1,157 1,203

1,202 1,230

Total 3,731 3,972 4,111 4,262 4,335 4,152 4,160 4,400

KAPASITAS INDUSTRI KAKAO INDONESIA

Tahun

Kap.

Terpasang

( Ton )

Kap.

Terpakai

( Ton )

Tingkat

Utilisasi

(%)

2007 345,000 159,934 46%

2008 345,000 172,827 50%

2009 345,000 130,054 38%

2010 360,000 151,420 42%

2011 560,000 268,000 48%

2012 660,000 310,000 47%

2013 735,000 324,000 44%

2014 765,000 392,000 51%

2015 800,000 414,000 52%

2016 800,000 392,000 49%

2017 800,000 465,000 58%30

Industri kakao berkembang

pesat sejak diterapkan bea

keluar biji kakao tahun 2010.

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Source: AIKI

31

MAPPING OF INDONESIAN COCOA INDUSTRY

Tangerang-Banten

PT. Golden Harvest Cocoa PT. Danora Agro Prima PT. Bumi Tangerang PT. Kakao Mas Gemilang PT. Mas Ganda

Sulawesi Tenggara

PT. Kalla Kakao Industry

Sulawesi Selatan

PT. Mars Symbiosience

PT. Unicom Kakao Makmur

PT. Makassar Berkat Kakao

PT. Kopi Jaya Kakao

PT. Hope Indonesia

Pt.Transmar Cocoa

PT. Barry – Comextra

Jawa Barat

PT. Papandayan Cocoa

IndustryJawa Timur

PT. Teja Sekawan Cocoa Ind

PT. Budidaya Kakao Lestari

PT. Jebe Koko

PT.Cargill Indonesia

Medan, Sumatera Utara

PT. Cocoa Ventures Indonesia

Batam

PT. Asia Cocoa Indonesia

Ekspor – Impor Kakao Indonesia

32

CommodityExport Import Balanced

2017 2018 Jun 2017 2018 Jun 2017 Juni 2018

Cocoa 1,120,251,807 559,832,864 646,337,454 365,052,431 473,914,353 194,780,433 Sumber: Basis Data Ekspor Impor Komoditi Pertanian, Kementerian Pertanian, Agustus 2018 (USD)

Tahun Volume (ton) Nilai ( USD )

2007 19.655 39.221.399

2008 22.968 59.573.565

2009 24.286 76.312.425

2010 24.831 89.497.057

2011 19.100 62.881.032

2012 23.943 62.977.883

2013 30.766 77.422.094

2014 109.409 341.437.411

2015 53.372 169.734.659

2016 61.015 184.667.284

2017 226.613 486.544.060

Sumber : BPS

Sejak 2014 Indonesia telah menjadi pengimpor biji kakao.

Volume dan Nilai impor Biji Kakao Indonesia

Tahun Biji Kakao Kakao Olahan

2010 432,000 103,055

2011 210,000 178,951

2012 163,500 196,479

2013 188,320 196,333

2014 63,330 240,967

2015 39,622 287,193

2016 28,329 273,057

2017 25,098 303,880

EKSPOR BIJI KAKAO & OLAHANNYA (ton)

NILAI DEVISA KOMODITI KAKAO

Tahun

2011 2012 2013 2014 2015 2016 2017

Devisa(USDMilyar)

1,40 0,99 1,09 1,09 1,27 1,19 1,07

Kakao penghasil devisa terbesar ketiga setelah sawit dan karet dalam sektor perkebunan.

Coffee

110

119

108

129

120

129

123

133137

148152

149152

157 158

113116

120123

129

133 132

136139

143

149152

155 155157

105

115

125

135

145

155

2003 3004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 *)

Pruduction

Consumption

35

WORLD COFFEE PRODUCTION & CONSUMPTION

Volume (billion bag)

Sumber : ICO. Tahun 2017 *)

Estimated

REGION 2012/13 2013/14 2014/15 2015/16 CAGR

Africa 10 470 10 597 10 754 10 794 1.0 %

Asia & Oceania 29 445 30 701 32 550 33 611 4.5 %

Central America & Mexico

5 200 5 156 5235 5306 0.7 %

Europe 50 028 50 179 50 912 51 590 1.0 %

North America 26 778 27 706 27 359 28 931 2.6 %

South America 25 042 24 682 24 949 25 237 0.3 %

WORLD TOTAL 146 964(8 817 840 Ton)

149 022(8 941 320 Ton)

151 758 (9 105 480 Ton)

155 469(9 328 140 Ton)

1.9 %

WORLD COFFEE CONSUMPTION, 2012/2013 – 2015/2016

In Thousand 60 kg bags

Source: ICO

No. NEGARA KONSUMSI TOTAL 2015/16 PERTUMBUHAN/TH (%) KONSUMSI/KAPITA

1 European Union 42 604 0,7 6,5 kg/th

2 USA 25 336 2,9 4,3 kg/th

3 Japan 7 790 1,9 3,4 kg/th

6 Russian Federation 4 303 6,9 1,8 kg/th

5 Canada 3 595 0,8 6,5 kg/th

6 Algeria 2 282 2,4 3,4 kg/th

7 South Korea 2 161 7,3 2,5 kg/th

8 Australia 1 720 3,2 4,3 kg/th

9 Saudi Arabia 1 566 7,6 2,9 kg/th

10 Turkey 1 106 10,5 0,9 kg/th

INDONESIA 4 500 (270 000 Ton) 4,9 1,1 kg/th

KONSUMSI KOPI 10 NEGARA PENGIMPOR KOPI TERBESAR

Dalam ribuan kantong 60 kg

Composition of World Coffee Production and The Position of Indonesia

38

Produksi Kopi di Indonesia (000 Ton)

PRODUKSI KOPI Indonesia

ACEH6%

SUMUT8%

SUMBAR 4%

JAWA TIMUR

8%

SULSEL5%

SUMSEL22%

LAMPUNG21%

BENGKULU9%

LAINNYA17%

Produksi kopi thn 2017 *) : 637.539 ton

ACEH

SUMUT

SUMBAR

JAWA TIMUR

SULSEL

SUMSEL

LAMPUNG

BENGKULU

LAINNYA

Sumber : Statistik Perkebunan Indonesia 2016Keterangan: *) Angka Sementara

1. Brazil: US$4.6 billion (14.1% of total coffee exports)

2. Vietnam: $3.5 billion (10.7%)

3. Germany: $2.64 billion (8.1%)

4. Colombia: $2.58 billion (7.9%)

5. Switzerland: $2.2 billion (6.9%)

6. Italy: $1.6 billion (5%)

7. Indonesia: $1.19 billion (3.6%)

8. Honduras: $1.16 billion (3.6%)

9. France: $1.07 billion (3.3%)

10. Belgium: $940.3 million (2.9%)

11. Ethiopia: $938 million (2.9%)

12. United States: $873.1 million (2.7%)

13. Netherlands: $754.1 million (2.3%)

14. Guatemala: $748.6 million (2.3%)

15. Peru: $707.2 million (2.2%)http://www.worldstopexports.co

m/coffee-exports-country/

The 15 Countries that

Exported the Highest

Dollar Value Worth Of

Coffee in 2017

vs

Source: BPS

Perkembangan Berat dan Nilai Ekspor Kopi, 2009-2016

Perkembangan Berat dan Nilai Impor Kopi, 2009-2016

Export – Import Coffee Indonesia

GVCKadang dibutuhkan import coffee bean untuk memenuhi demand dari Consumers (blending)

Berat Ekspor Kopi menurut Deskripsi HS, 2016

• Sebagian besarekspor mentah

• Nilai tambahrendah

Source: BPS

Source: MARKET RESEARCH REPORT (TPSA Feb, 2017)

Peluang Meningkatkan Ekspor Kopi keKanada masih Cukup Besar

• Canadian imports of Indonesian coffee climbed to $44.3 million last year (2017), an increase of 28% since 2014.

• Indonesia ranks as the sixth-largest supplier of coffee to Canada

https://biv.com/article/2018/05/initiative-aims-increase-indonesian-coffee-imports

Towards GVC

Raw Material:

• Availability, continuity and sustainability

• Quality, Time Delivery, Price competitiveness

• Planning upstream –downstream

• Regulations and government policies must support sustainable raw materials and business friendly

• Innovation is a must

Added Value Products:

• Market more open & difficult to stop Global Sourcing

• Competition is tougher• Food Products must be

innovative with new products to meet consumer’s needs and lifestyle

• Anticipation of rapid changes in the global market

• Disruptive economicThe food industry is still dependent on imported raw materials (semi processed) → intermediate industry

The Global Value Chain (GVC) Challenges

47

• Trade is no longer dominated by products, but in tasks and components.

• According to UNCTAD, 60% of global trade is in intermediate goods and services.

› Share of Foreign Value-Added in global exports is 28% (22% for food products)

What is Indonesia’s involvement in GVCs?

Indonesia is not currently well integrated into GVCs as yet ......

48 |

CountryForeign value-added content of exports

Korea 44

Malaysia 42

Mexico 32

Thailand 30

China 30

Indonesia 9

Why are Global Value Chains (GVC) Important?

49 |

• Industrial organisation (and economic opportunities for participation) is increasingly shaped by the actor practices of globally coordinated lead firms

• “There is a positive correlation between participation in GVCs and growth rates of GDP per capita. GVCs have a direct economic impact on value added, jobs and income.”

• “They can also be an important avenue for developing countries to build productive capacity, including through technology dissemination and skill building, thus opening up opportunities for longer-term industrial upgrading.”

(UNCTAD 2013 World Investment Report on Global Value Chains)

50|

IFIC operations

Foundation

IFIC

International Collaborations

Research Institutes

Other Industry

Associations

Food Association

GAPPMI/ Industry

Stakeholders Academia CSIRO/BI

C

Accreditation Org.

Go

vern

ance

Fun

din

g

Universities

IFIC Programs & Projects

Governance & Management

Service Revenues

THE STAKEHOLDERS, THE PROPOSED SCOPE: PROJECTS & PROGRAMS

G o I & Agencies Representatives

❑ Development Projects❑ Capacity Development ❑ Promotion Programs

❑ Information Services❑ Intermediary Services❑ One-on-One Projects ❑ Consortium Projects

It’s time..!

8/29/2018 53

Natural

Resources

Gov. Policy & other

supporting

ADDED VALUE PRODUCT,

SAFE , Halal

COMPETITIVE

CONSUMERS

What industry need? →Creating a Competitive Product to GVC

•Technology•Disruptive economic•Innovation•Consumer’s preference•Marketing

purpose

548/29/2018

Compliance to Regulation

The market between Indonesia-Canada is

complimentary

F & B trade between Indonesia and

Canada is still small

Innovative for Added Value

Competitiveness Technical assistance

What to do ? → Key to Success

8/29/2018 55

Thank you

![kakao[Kakao Driver auto pay] [Kakao Money transfer] [Billing service] Kakao Bank [Installment Saving] [FX transfer] • Kakao Pay subscribers 16.8 million, total transaction volume](https://img.pdfslide.us/doc/110x75/60bbbb1bb6cd3d06fc70e674/kakao-driver-auto-pay-kakao-money-transfer-billing-service-kakao-bank-installment.jpg)