Embed Size (px)

Citation preview

Outlook for the World

Paper Grade Pulp Market

Kurt Schaefer, VP Fiber

November 2015

1 © Copyright 2015 RISI, Inc. | Proprietary Information

World Pulp & Recovered Paper

5-Year and 15-Year Forecasts

www.risi.com/forecasts

World Pulp Monthly

www.risi.com/wpm

This Forecast Presentation Is Based on Our Pulp and RCP Forecasts For more information:

New Edition:

The China Pulp Market in

Transition:

A Comprehensive Analysis

and Outlook

Announcing Our Updated China Pulp

Study---Available This Week.

© Copyright 2015 RISI, Inc. | Proprietary Information 3

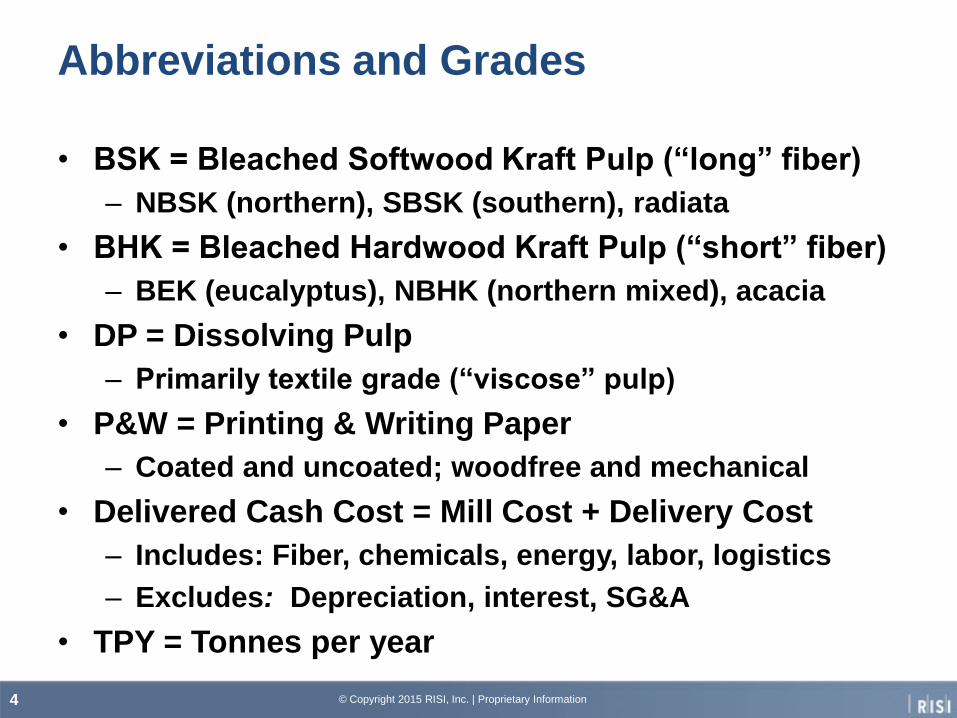

Abbreviations and Grades

• BSK = Bleached Softwood Kraft Pulp (“long” fiber)

– NBSK (northern), SBSK (southern), radiata

• BHK = Bleached Hardwood Kraft Pulp (“short” fiber)

– BEK (eucalyptus), NBHK (northern mixed), acacia

• DP = Dissolving Pulp

– Primarily textile grade (“viscose” pulp)

• P&W = Printing & Writing Paper

– Coated and uncoated; woodfree and mechanical

• Delivered Cash Cost = Mill Cost + Delivery Cost

– Includes: Fiber, chemicals, energy, labor, logistics

– Excludes: Depreciation, interest, SG&A

• TPY = Tonnes per year

4 © Copyright 2015 RISI, Inc. | Proprietary Information

Global Real GDP: Economic Growth

Rebalancing and Accelerating in 2016

5 © Copyright 2015 RISI, Inc. | Proprietary Information

-0.8

-0.3

0.9

1.6 1.8

2.2

1.5

2.4 2.7

3.0

7.7 7.7 7.3

6.9 6.6

3.4 3.3 3.3 3.1

3.7

-2

-1

0

1

2

3

4

5

6

7

8

9

12 13 14 15 16 12 13 14 15 16 12 13 14 15 16 12 13 14 15 16

Euro area United States China World

%

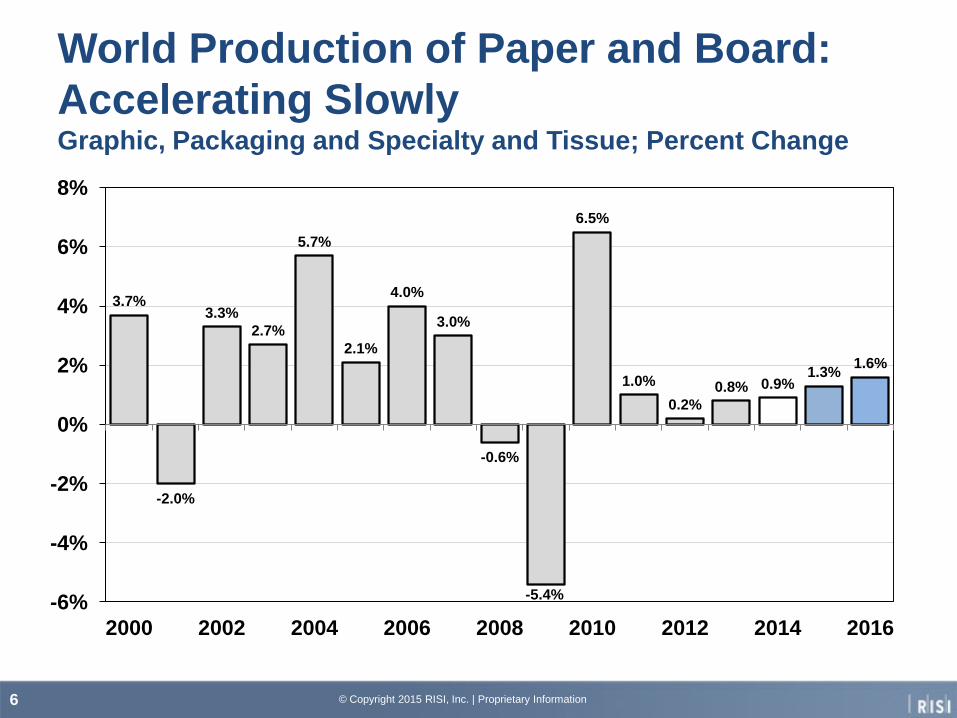

World Production of Paper and Board:

Accelerating Slowly Graphic, Packaging and Specialty and Tissue; Percent Change

6 © Copyright 2015 RISI, Inc. | Proprietary Information

3.7%

-2.0%

3.3%

2.7%

5.7%

2.1%

4.0%

3.0%

-0.6%

-5.4%

6.5%

1.0%

0.2%

0.8% 0.9% 1.3%

1.6%

-6%

-4%

-2%

0%

2%

4%

6%

8%

2000 2002 2004 2006 2008 2010 2012 2014 2016

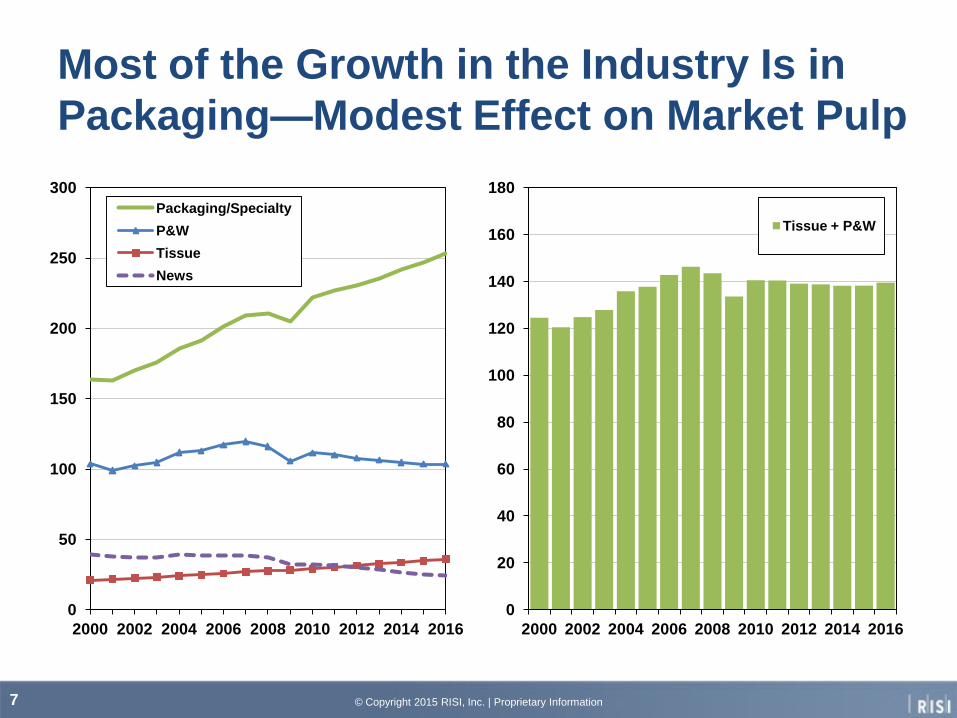

Most of the Growth in the Industry Is in

Packaging—Modest Effect on Market Pulp

© Copyright 2015 RISI, Inc. | Proprietary Information 7

0

50

100

150

200

250

300

2000 2002 2004 2006 2008 2010 2012 2014 2016

Packaging/Specialty

P&W

Tissue

News

0

20

40

60

80

100

120

140

160

180

2000 2002 2004 2006 2008 2010 2012 2014 2016

Tissue + P&W

The New Reality for World P&W Demand:

Peak Demand Has Already Happened

8 © Copyright 2015 RISI, Inc. All rights reserved.

0

20

40

60

80

100

120

140

160

180

80 85 90 95 00 05 10 15

Millio

n M

etr

ic T

on

s

P&W Production

2007 Forecast

In China, P&W Production Is Leveling

Off, While Tissue Continues to Grow

9 © Copyright 2015 RISI, Inc. | Proprietary Information

0

5

10

15

20

25

30

1990 1995 2000 2005 2010 2015

Millio

n T

on

nes p

er

Year

P&W

Tissue

P&W Consumption per Person,

1970 to 2014

10 © Copyright 2015 RISI, Inc. | Proprietary Information

0

20

40

60

80

100

120

140

0 5000 10000 15000 20000 25000 30000 35000

Japan

South Korea

China

kg/person

Per capita real GDP, US$

BHK Capacity in China on a Mill-by-Mill

Basis

11 © Copyright 2015 RISI, Inc. | Proprietary Information

0

1

2

3

4

5

6

7

8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Oji Nantong

Chenming Zhanjiang

Asia Symbol Rizhao

APP Hainan

Others

Even in a Weak Dollar Setting, China’s

Pulp Producers Have Competitiveness

Problems Related to Fiber Supply

• Lack of woodfiber

and available land

– Many plantations are

on marginal sites

with low yields

– Labor costs have

been rising quickly

– Importing woodfiber

is expensive

• Tighter enforcement

of pollution and water

use standards

© Copyright 2015 RISI, Inc. | Proprietary Information 12

Eucalyptus in southern China

What Are the Sources of Incremental

China’s Pulp Demand?

• Tissue production is rising by about 600,000 tpy

– Predominantly based on virgin fiber

• Policy closures of “backward” pulp and paper

capacity favors BHK consumption growth (at the

expense of local fiber, including nonwood).

• Rising demand for higher quality paper also raises

BHK demand

• Continuing move toward more BHK, less BSK, as

new paper machines are installed.

• BSK demand for absorbent applications is growing

• Conclusion: Net imports of BHK into China will

continue to show solid growth

13 © Copyright 2015 RISI, Inc. | Proprietary Information

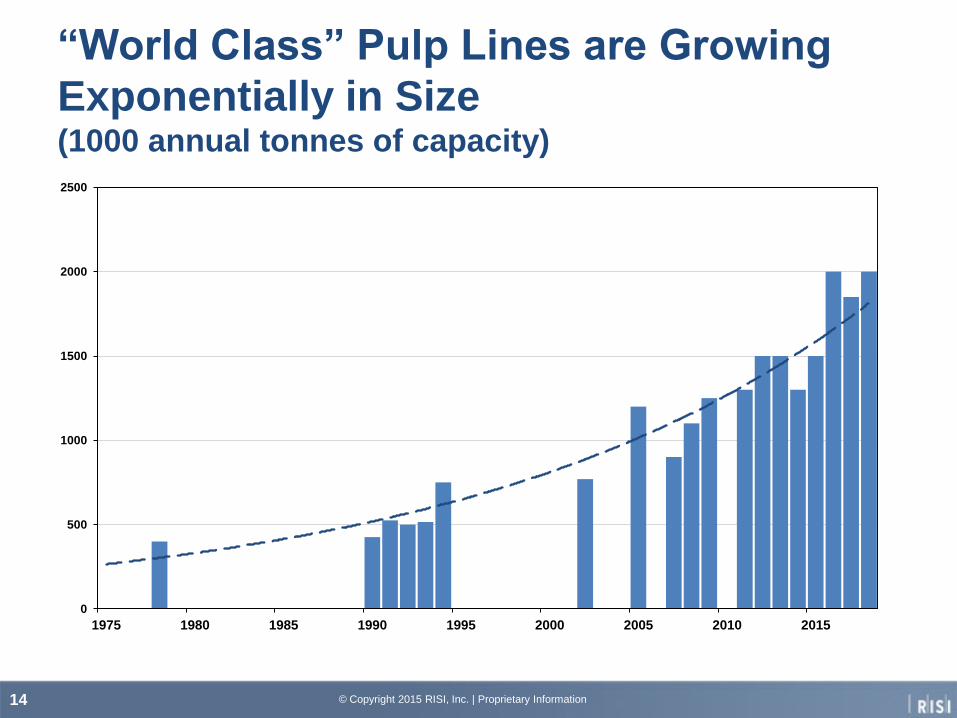

“World Class” Pulp Lines are Growing

Exponentially in Size (1000 annual tonnes of capacity)

14 © Copyright 2015 RISI, Inc. | Proprietary Information

0

500

1000

1500

2000

2500

1975 1980 1985 1990 1995 2000 2005 2010 2015

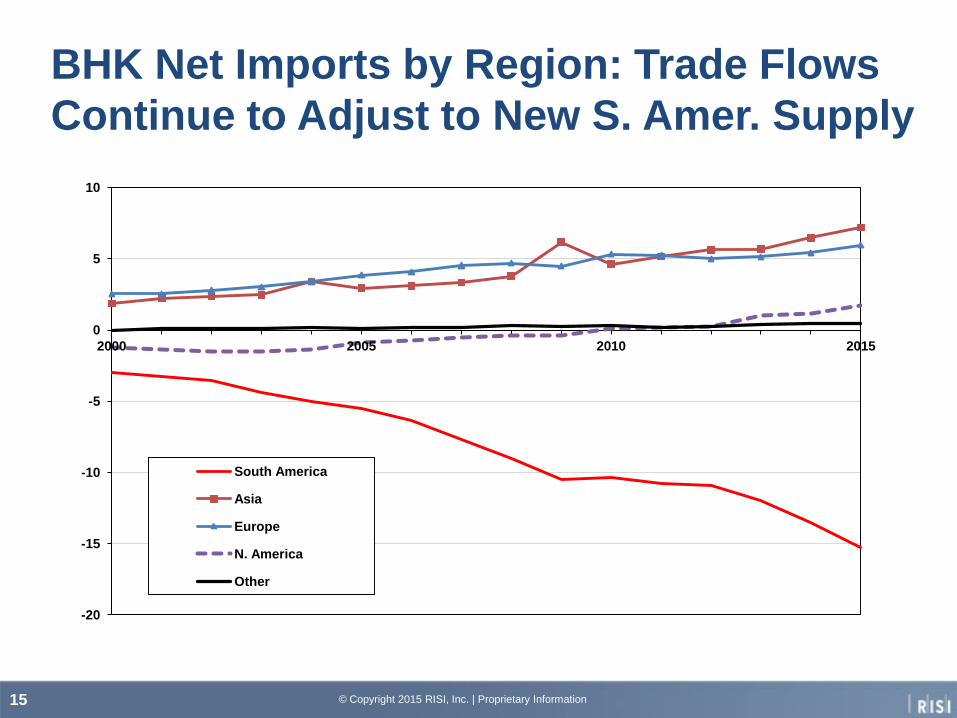

BHK Net Imports by Region: Trade Flows

Continue to Adjust to New S. Amer. Supply

15 © Copyright 2015 RISI, Inc. | Proprietary Information

-20

-15

-10

-5

0

5

10

2000 2005 2010 2015

South America

Asia

Europe

N. America

Other

In Indonesia, APP’s South Sumatra BHK

Project Will Open in 2016/Early 2017

• 2.0-2.8 million tonnes per year of BEK and BAK

• Acacia from plantations in South Sumatra

• May include paper machines eventually

© Copyright 2015 RISI, Inc. | Proprietary Information 16

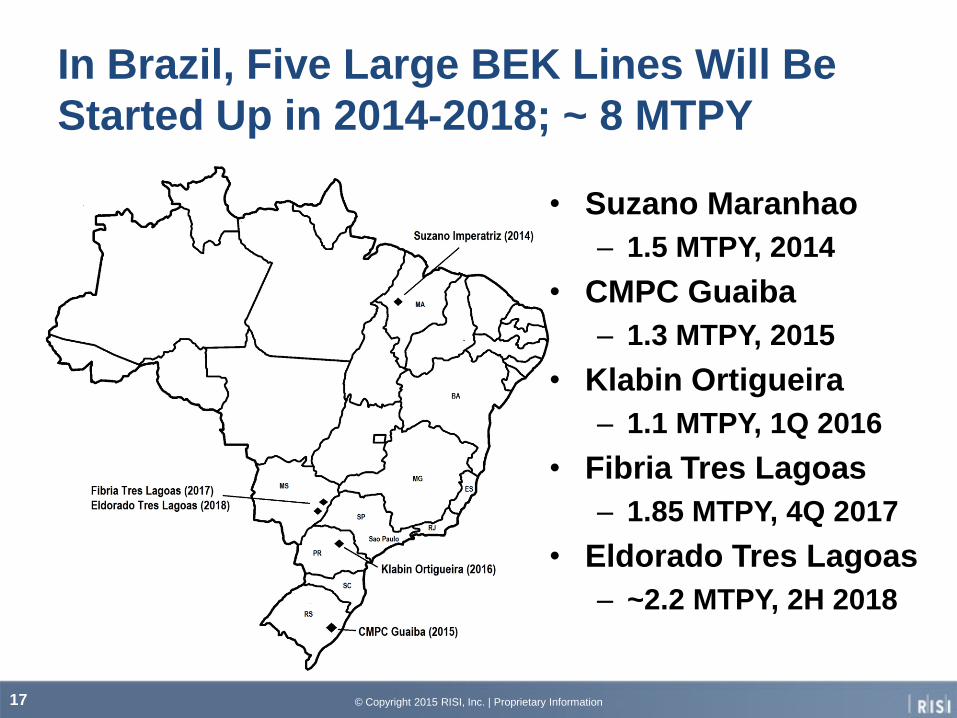

In Brazil, Five Large BEK Lines Will Be

Started Up in 2014-2018; ~ 8 MTPY

• Suzano Maranhao

– 1.5 MTPY, 2014

• CMPC Guaiba

– 1.3 MTPY, 2015

• Klabin Ortigueira

– 1.1 MTPY, 1Q 2016

• Fibria Tres Lagoas

– 1.85 MTPY, 4Q 2017

• Eldorado Tres Lagoas

– ~2.2 MTPY, 2H 2018

© Copyright 2015 RISI, Inc. | Proprietary Information 17

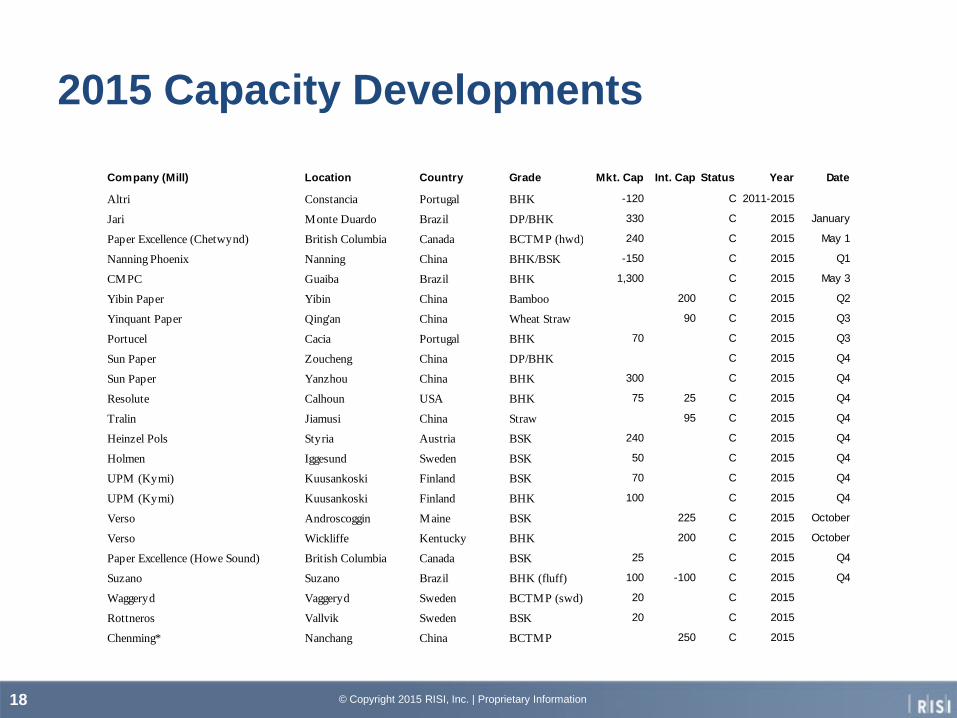

2015 Capacity Developments

18 © Copyright 2015 RISI, Inc. | Proprietary Information

Company (Mill) Location Country Grade Mkt. Cap Int. Cap Status Year Date

Altri Constancia Portugal BHK -120 C 2011-2015

Jari Monte Duardo Brazil DP/BHK 330 C 2015 January

Paper Excellence (Chetwynd) British Columbia Canada BCTMP (hwd) 240 C 2015 May 1

Nanning Phoenix Nanning China BHK/BSK -150 C 2015 Q1

CMPC Guaiba Brazil BHK 1,300 C 2015 May 3

Yibin Paper Yibin China Bamboo 200 C 2015 Q2

Yinquant Paper Qing'an China Wheat Straw 90 C 2015 Q3

Portucel Cacia Portugal BHK 70 C 2015 Q3

Sun Paper Zoucheng China DP/BHK C 2015 Q4

Sun Paper Yanzhou China BHK 300 C 2015 Q4

Resolute Calhoun USA BHK 75 25 C 2015 Q4

Tralin Jiamusi China Straw 95 C 2015 Q4

Heinzel Pols Styria Austria BSK 240 C 2015 Q4

Holmen Iggesund Sweden BSK 50 C 2015 Q4

UPM (Kymi) Kuusankoski Finland BSK 70 C 2015 Q4

UPM (Kymi) Kuusankoski Finland BHK 100 C 2015 Q4

Verso Androscoggin Maine BSK 225 C 2015 October

Verso Wickliffe Kentucky BHK 200 C 2015 October

Paper Excellence (Howe Sound) British Columbia Canada BSK 25 C 2015 Q4

Suzano Suzano Brazil BHK (fluff) 100 -100 C 2015 Q4

Waggeryd Vaggeryd Sweden BCTMP (swd) 20 C 2015

Rottneros Vallvik Sweden BSK 20 C 2015

Chenming* Nanchang China BCTMP 250 C 2015

2016 Capacity Developments

19 © Copyright 2015 RISI, Inc. | Proprietary Information

Company (Mill) Location Country Grade Mkt. Cap Int. Cap Status Year Date

ENCE Navia Spain BHK 40 C 2015-16 Q2-Q1

Catalyst Paper Maine USA BHK -130 P 2015-18

Expera Old Town USA BSK/BHK -180 C 2016 Q1

WestRock Evadale USA BSK -90 90 C 2016 Q1

Svetlogorsky Svetlogorsk Belarus BSK/BHK/DP 400 C 2016 Q1

Klabin Ortigueira Brazil BHK 1,100 C 2016 Q1

Klabin Ortigueira Brazil BSK 400 C 2016 Q1

SodraCell Morrum Sweden BSK 35 C 2016 Q1

IGIC (Woodland) Maine USA BHK -100 100 C 2016 Q1-Q2

International Paper (Riegelwood) North Carolina USA BSK 360 C 2016 Q2

PT OKI/APP Sumatra Indonesia BHK 2,800 C 2017 Q3

Double A Alizay France BHK 130 C 2016 Q3

ITC Bhadrachalam India BCTMP 105 C 2016 Q3

SodraCell Varo Sweden BSK 275 C 2016 Q3

Domtar (Ashdown) Arkansas USA BSK 230 -95 C 2016 Q3

Domtar (Ashdown) Arkansas USA BHK -135 C 2016 Q3

UPM Kaukas Finland BSK/BHK ? C 2016 End

Columbia Pulp Washington USA UKP (Straw) 125 P 2016

Yongfeng* Xuyong China Bamboo 200 C 2016

Irving New Brunswick Canada BSK 30 C 2016

Key BHK Capacity Developments

• Sun Paper Yanzhou switch to BHK, Q4: 250-300k?

• Old Town closures, Q4/Q1: ~180k BHK/BSK

• Klabin Ortigueira, Q1: 1.1 million BHK

• APP OKI, Q3/Q4: 2.0-2.8 million BHK

20 © Copyright 2015 RISI, Inc. | Proprietary Information

Key BSK Capacity Developments

• Svetlogorksy BSK/BHK/DP 1H2016: 400k

• Klabin Ortigueira 1Q16: 400k

• IP Riegelwood 2Q16: 360k

• Domtar Ashdown 3Q16: >300k

• Sodra Varo 3Q16: 275k

21 © Copyright 2015 RISI, Inc. | Proprietary Information

FX: Strong Dollar Continues in 2016

22 © Copyright 2015 RISI, Inc. | Proprietary Information

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

EUR USD

CAD USD

BRL USD

2016 Forecast Summary

• Continuing strong dollar, with upside risk in terms of

dollar strength with acceleration of the US economy

– Putting downward pressure on production costs

• Modest acceleration in growth of paper and board

demand, mostly b/c of packaging

• In the pulp market, supply-side changes remain

more prominent than usual

• For BHK, given the new assumed timing for the

South Sumatra project, profitability seems to be on a

downward trend through the end of 2016

• For BSK, 2nd half of 2016 could see capacity growth

> demand growth, esp. for SBSK/fluff

23 © Copyright 2015 RISI, Inc. | Proprietary Information

New Edition:

The China Pulp Market in

Transition:

A Comprehensive Analysis

and Outlook

Announcing Our Updated China Pulp

Study---Available Today.

© Copyright 2015 RISI, Inc. | Proprietary Information 24