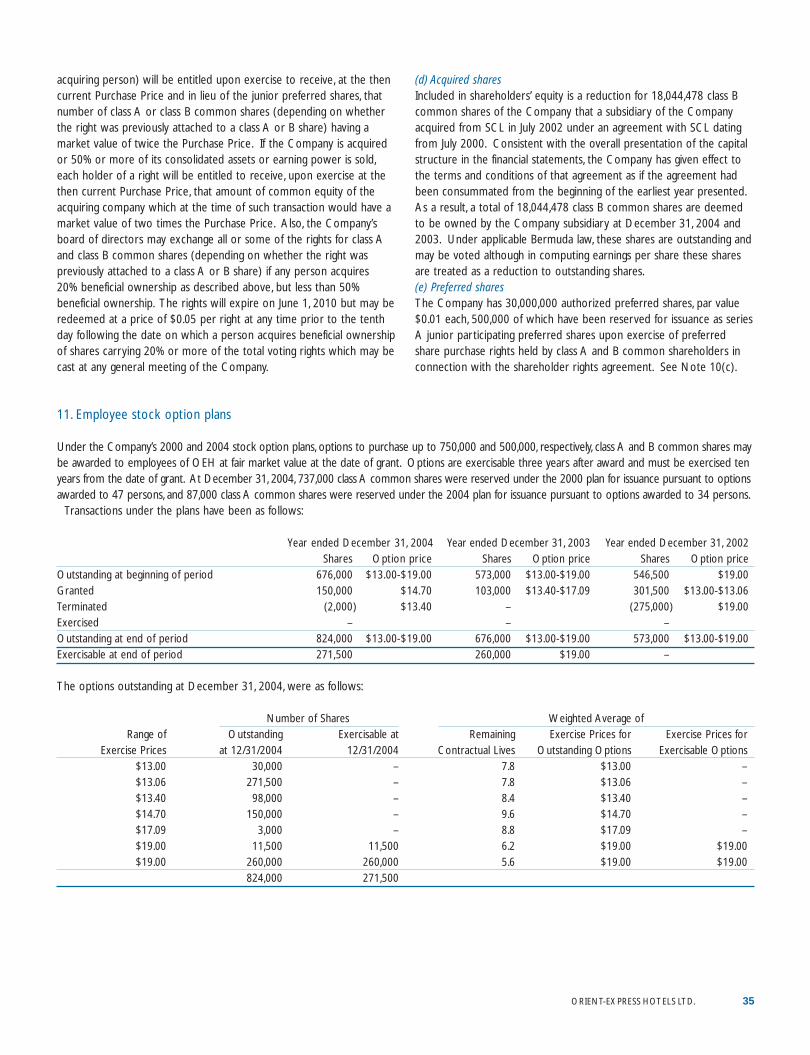

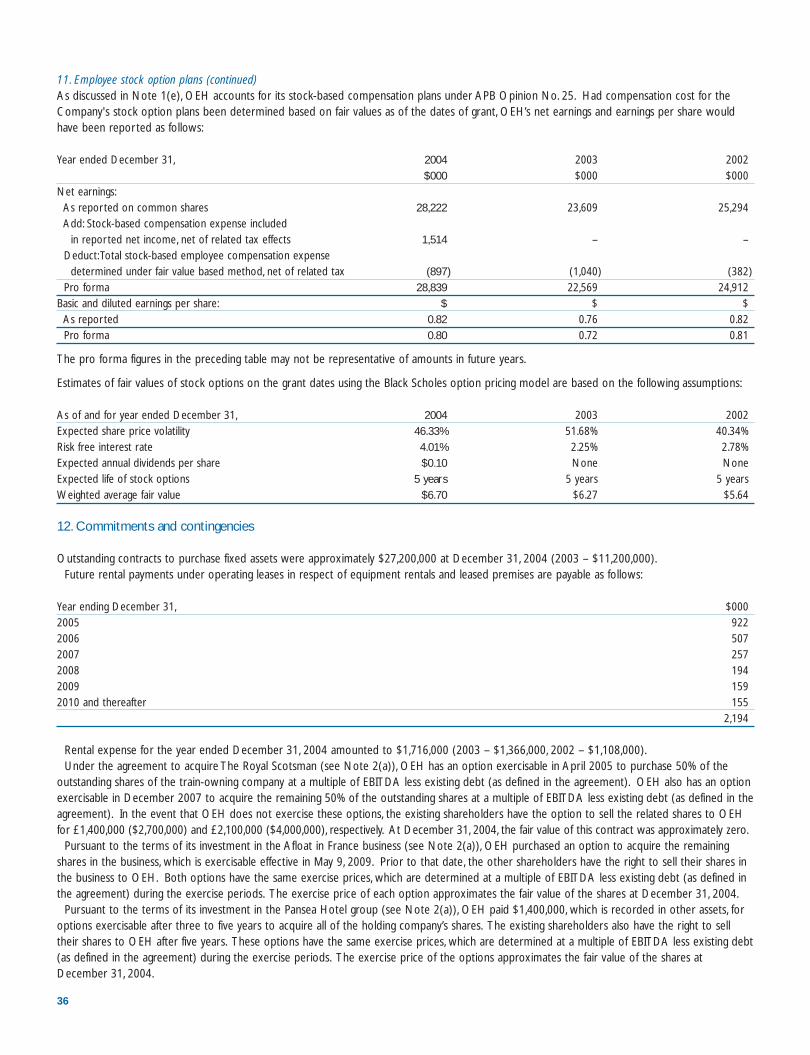

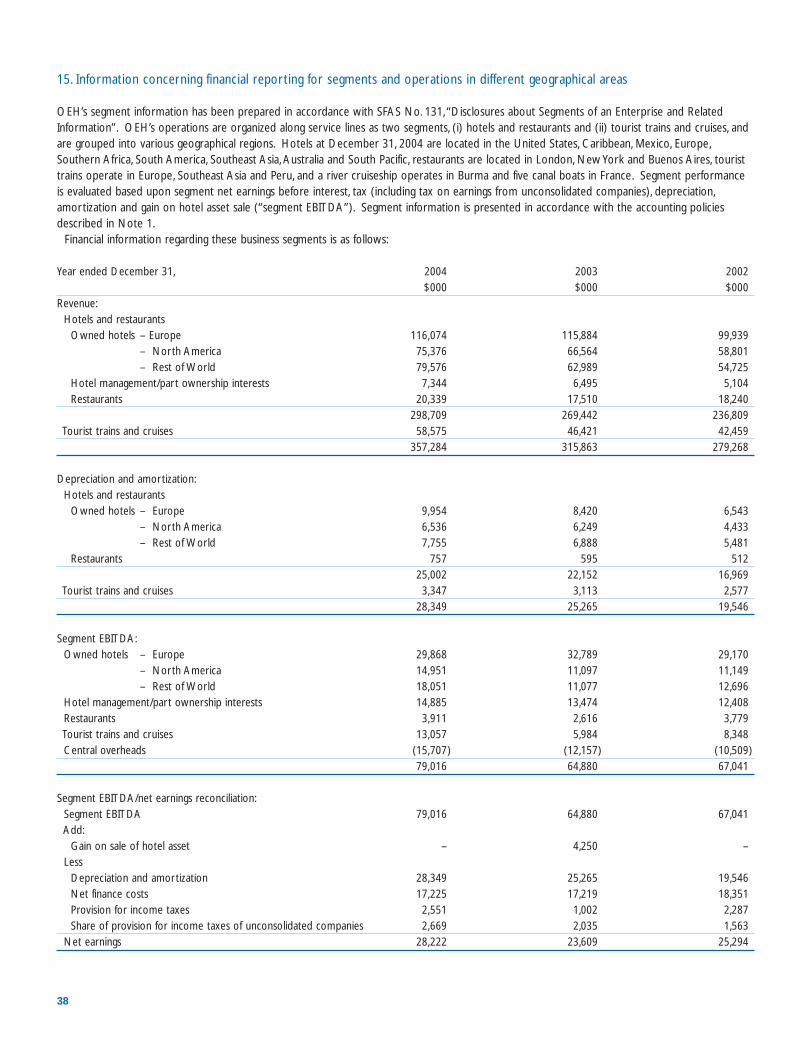

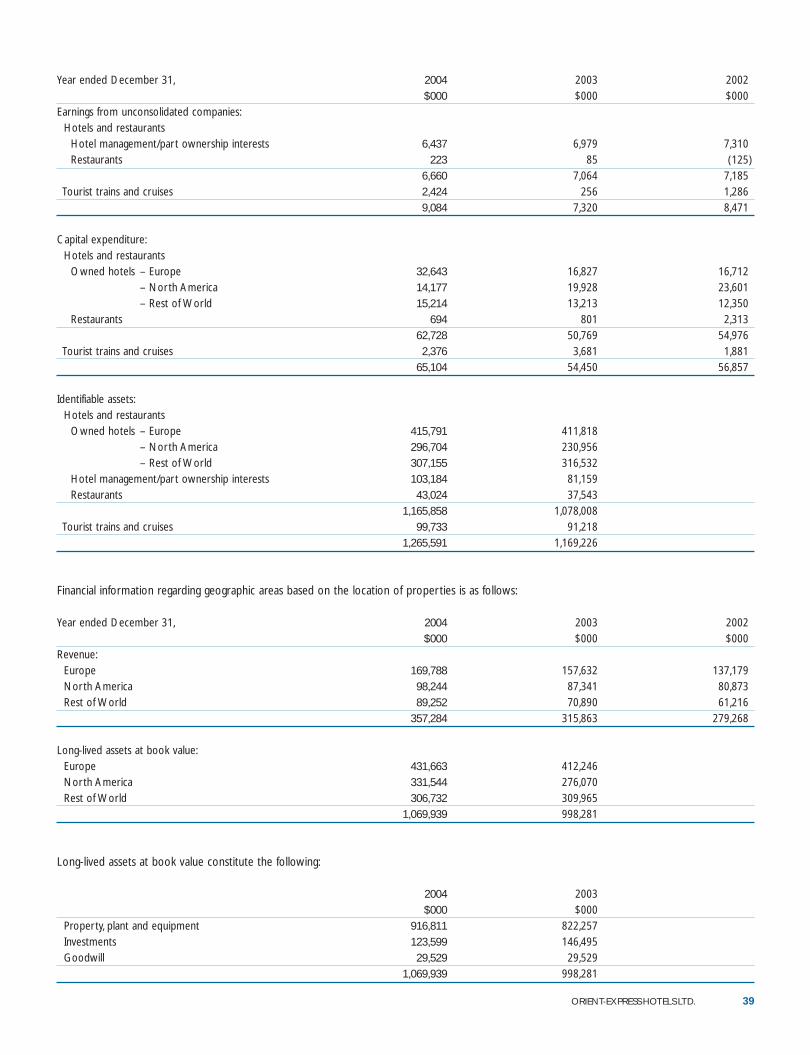

Embed Size (px)

Citation preview

3470-AR

-04

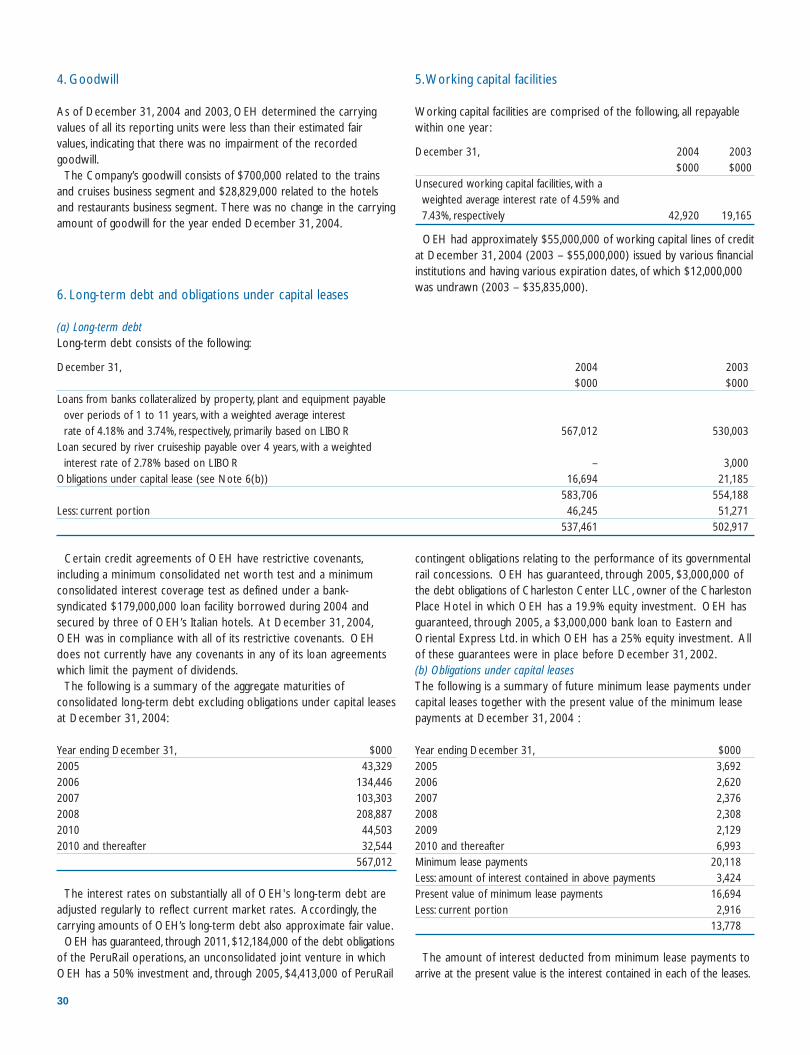

Orient-Express H

otels Ltd.A

nnual Report 2004

HOTEL CIPRIANI

Venice, ItalyPALAZZO VENDRAMIN

Venice, ItalyHOTEL SPLENDIDO

Portofino, Italy

HOTEL SPLENDIDO MARE

Portofino, ItalyVILLA SAN MICHELE

Florence, Italy CAPANNELLE

Tuscany, ItalyHOTEL CARUSO

Ravello, Italy HOTEL RITZ

Madrid, SpainLA RESIDENCIA

Deià, Mallorca, Spain

LAPA PALACE

Lisbon, PortugalREID'S PALACE HOTEL

Madeira, PortugalHÔTEL DE LA CITÉ

Carcassonne, FranceGRAND HOTEL EUROPE

St Petersburg, RussiaHARRY’S BAR

London, EnglandLE MANOIRAUX QUAT’SAISONS

Chef-Proprietor Raymond BlancOxfordshire, England

‘21’ CLUB

New York, New YorkINN AT PERRY CABIN

St Michaels, MarylandKESWICK HALL

Charlottesville,VirginiaWINDSOR COURT HOTEL

New Orleans, LouisianaCHARLESTON PLACE

Charleston, South CarolinaEL ENCANTO

Santa Barbara, California

MAROMA RESORT AND SPA

Riviera Maya, MexicoLA SAMANNA

St Martin, French West IndiesMOUNT NELSON HOTEL

Cape Town, South AfricaTHE WESTCLIFF

Johannesburg, South AfricaORIENT-EXPRESS SAFARIS

Eagle Island Camp, BotswanaORIENT-EXPRESS SAFARIS

Khwai River LodgeBotswana

ORIENT-EXPRESS SAFARIS

Savute Elephant CampBotswana

THE OBSERVATORY HOTEL

Sydney, AustraliaLILIANFELS BLUE MOUNTAINS

Katoomba, New South Wales,Australia

COPACABANA PALACE

Rio de Janeiro, BrazilLA CABAÑA

Buenos Aires, Argentina

MIRAFLORES PARK HOTEL

Lima, PeruHOTEL MONASTERIO

Cuzco, PeruMACHU PICCHU

SANCTUARY LODGE

Machu Picchu, Peru

BORA BORA LAGOON

RESORT & SPA

Bora Bora, French Polynesia

PERURAIL

Peru VENICE SIMPLON-ORIENT-EXPRESS

London, Paris,Venice

BRITISH PULLMAN

South of EnglandNORTHERN BELLE

North of EnglandTHE ROYAL SCOTSMAN

ScotlandEASTERN & ORIENTAL EXPRESS

Southeast AsiaROAD TO MANDALAY

Irrawaddy River, Burma(Myanmar)

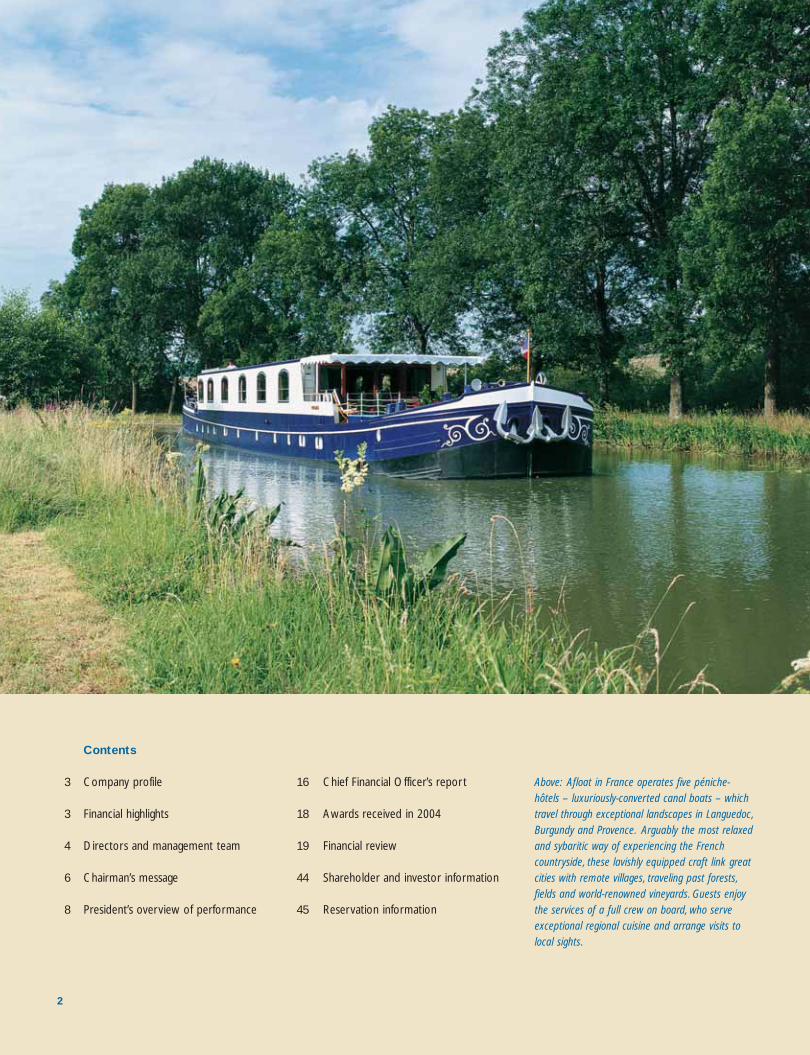

AFLOAT IN FRANCE

France

Orient-Express Hotels Ltd.

www.orient-express.com

PANSEA HOTELS & RESORTSSiem Reap, Bali, Koh Samui,

Luang Prabang,Yangon,Southeast Asia

Orient-Express Hotels Ltd. 2004 ANNUAL REPORT

48818_COVERS.rev 20/4/05 4:56 pm Page 1

2

Afloat in FranceBurgundy and Languedoc, FranceU.K. telephone: +44 20 7960 0500Fax: +44 20 7805 5908U.S. telephone: +1 401 351 7518Fax: +1 401 351 7220

Bora Bora Lagoon Resort & SpaTahiti, French PolynesiaTelephone: +689 60 40 00 Fax: +689 60 40 03

British PullmanSouth of EnglandU.K. telephone: +44 20 7960 0500Fax: +44 20 7805 5908U.S. telephone: +1 401 351 7518 Fax: +1 401 351 7220

Charleston PlaceCharleston, South CarolinaTelephone: +1 843 722 4900 Fax: +1 843 722 0728

Copacabana PalaceRio de Janeiro, BrazilTelephone: +55 21 2548 7070 Fax: +55 21 2235 7330

Eastern & Oriental ExpressSoutheast AsiaU.K. telephone: +44 20 7960 0500Fax: +44 20 7805 5908U.S. telephone: +1 401 351 7518 Fax: +1 401 351 7220

El Encanto Hotel & Garden VillasSanta Barbara, California Currently under development.

Grand Hotel EuropeSt Petersburg, RussiaTelephone: +7 812 329 6000 Fax: +7 812 329 6001

Harry’s BarLondon, England (A private club)

Hotel CarusoRavello, ItalyTelephone: +39 0185 267898 Fax: +39 0185 267899

Hotel Cipriani and Palazzo VendraminVenice, ItalyTelephone: +39 0 41 520 7744 Fax: +39 0 41 520 3930

Hôtel de la CitéCarcassonne, FranceTelephone: +33 468 71 98 71 Fax: +33 468 71 50 15

Hotel MonasterioCuzco, PeruTelephone: +51 84 24 1777 Fax: +51 84 24 6983

Hotel RitzMadrid, SpainTelephone: +34 91 701 67 67 Fax: +34 91 701 67 76

Hotel Splendido andSplendido MarePortofino, ItalyTelephone: +39 0185 267 800 Fax: +39 0185 267 804

Jimbaran Puri BaliBali, IndonesiaTelephone: +62 361 701 605 Fax: +62 361 701 320

Keswick HallCharlottesville,VirginiaTelephone: +1 434 979 3440 Fax: +1 434 977 4171

La CabañaBuenos Aires,ArgentinaTelephone and fax: +54 11 4814 0001

Lapa PalaceLisbon, PortugalTelephone: +351 21 394 9494 Fax: +351 21 395 0665

La Résidence d’AngkorSiem Reap, Cambodia Telephone: +855 63 963 390 Fax: +855 63 963 391

La Résidence Phou VaoLuang Prabang, LaosTelephone: +856 71 21 2194Fax: +856 71 21 2534

La ResidenciaDeià, Mallorca, SpainTelephone: +34 971 63 90 11 Fax: +34 971 63 93 70

La SamannaSt Martin, French West IndiesTelephone: +590 590 87 6400 Fax: +590 590 87 8786

Le Manoir aux Quat’SaisonsOxfordshire, EnglandTelephone: +44 1844 278881 Fax: +44 1844 278847

Lilianfels Blue MountainsKatoomba,Australia Telephone: +61 2 4780 1200 Fax: +61 2 4780 1300

Machu Picchu Sanctuary LodgeMachu Picchu, PeruTelephone: +51 84 21 1038 Fax: +51 84 21 1053

Maroma Resort and SpaRiviera Maya, MexicoTelephone: +52 998 872 8200 Fax: +52 998 872 8220

Miraflores Park HotelLima, PeruTelephone: +51 1 242 3000 Fax: +51 1 242 3393

Mount Nelson HotelCape Town, South Africa Telephone: +27 21 483 1000 Fax: +27 21 483 1782

NapasaiKoh Samui,ThailandTelephone: +66 77 42 92 00Fax: +66 77 42 92 01

Northern BelleU.K.U.K. telephone: +44 20 7690 0500Fax: +44 20 7805 5908U.S. telephone: +1 401 351 7518 Fax: +1 401 351 7220

Orient-Express SafarisEagle Island Camp, Khwai River Lodge,Savute Elephant Camp Botswana, Southern AfricaTelephone: +27 11 274 1800 Fax: +27 11 481 6065

PeruRailHiram Bingham train, Cuzco-Machu PicchuTelephone: +51 84 238 722 Fax: +51 84 221 114

Reid’s PalaceFunchal, Madeira, PortugalTelephone: +351 291 71 7171 Fax: +351 291 71 7177

Road To MandalayMandalay, MyanmarU.K. telephone: +44 20 7960 0500Fax: +44 20 7805 5908U.S. telephone: +1 401 351 7518 Fax: +1 401 351 7220

The Governor’s ResidenceYangon, Myanmar Telephone: +951 229 860Fax: +95 1 228 260

The Inn at Perry CabinSt Michaels, Maryland Telephone: +1 410 745 2200 Fax: +1 410 745 3348

The Observatory HotelSydney,Australia Telephone: +61 2 9256 2222 Fax: +61 2 9256 2233

The Orient-Express Gift CollectionLondon, EnglandTelephone: +44 20 7805 5019 Fax: +44 20 7805 5909

The Royal ScotsmanEdinburgh, ScotlandU.K. telephone: +44 131 555 1344Fax: +44 131 555 1345U.S. telephone: +1 800 922 8625

The WestcliffJohannesburg, South Africa Telephone: +27 11 646 2400 Fax: +27 11 646 3500

‘21’ ClubNew York, New YorkTelephone: +1 212 582 7200 Fax: +1 212 581 7138

Ubud Hanging GardensBali, IndonesiaTelephone: +62 361 701 605Fax: +62 361 701 320

Venice Simplon-Orient-ExpressLondon-Paris-VeniceU.K. telephone: +44 20 7960 0500Fax: +44 20 7805 5908U.S. telephone: +1 401 351 7518 Fax: +1 401 351 7220

Villa San MicheleFlorence, Italy Telephone: +39 0 55 567 8200 Fax: +39 0 55 567 8250

Windsor Court HotelNew Orleans, Louisiana Telephone: +1 504 523 6000 Fax: +1 504 596 4513

Reservation information

Contents

3 Company profile

3 Financial highlights

4 Directors and management team

6 Chairman’s message

8 President’s overview of performance

16 Chief Financial Officer’s report

18 Awards received in 2004

19 Financial review

44 Shareholder and investor information

45 Reservation information

Above: Afloat in France operates five péniche-hôtels – luxuriously-converted canal boats – whichtravel through exceptional landscapes in Languedoc,Burgundy and Provence. Arguably the most relaxedand sybaritic way of experiencing the Frenchcountryside, these lavishly equipped craft link greatcities with remote villages, traveling past forests,fields and world-renowned vineyards. Guests enjoythe services of a full crew on board, who serveexceptional regional cuisine and arrange visits tolocal sights.

45ORIENT-EXPRESS HOTELS LTD.www.orient-express.com

COVERS.rev 21/4/05 3:35 pm Page 2

3ORIENT-EXPRESS HOTELS LTD.

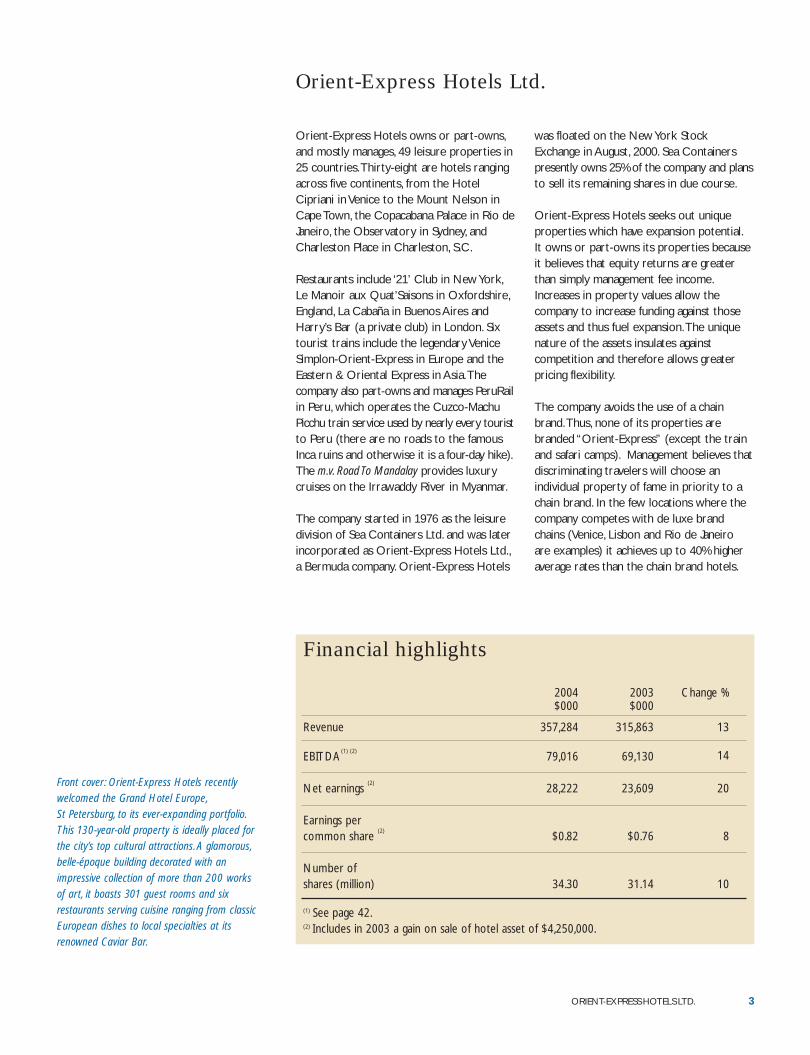

Orient-Express Hotels Ltd.

Orient-Express Hotels owns or part-owns,and mostly manages, 49 leisure properties in25 countries.Thirty-eight are hotels rangingacross five continents, from the HotelCipriani in Venice to the Mount Nelson inCape Town, the Copacabana Palace in Rio deJaneiro, the Observatory in Sydney, andCharleston Place in Charleston, S.C.

Restaurants include ‘21’ Club in New York,Le Manoir aux Quat’Saisons in Oxfordshire,England, La Cabaña in Buenos Aires andHarry’s Bar (a private club) in London. Sixtourist trains include the legendary VeniceSimplon-Orient-Express in Europe and theEastern & Oriental Express in Asia.Thecompany also part-owns and manages PeruRailin Peru, which operates the Cuzco-MachuPicchu train service used by nearly every touristto Peru (there are no roads to the famousInca ruins and otherwise it is a four-day hike).The m.v. Road To Mandalay provides luxurycruises on the Irrawaddy River in Myanmar.

The company started in 1976 as the leisuredivision of Sea Containers Ltd. and was laterincorporated as Orient-Express Hotels Ltd.,a Bermuda company. Orient-Express Hotels

was floated on the New York StockExchange in August, 2000. Sea Containerspresently owns 25% of the company and plansto sell its remaining shares in due course.

Orient-Express Hotels seeks out uniqueproperties which have expansion potential.It owns or part-owns its properties becauseit believes that equity returns are greaterthan simply management fee income.Increases in property values allow thecompany to increase funding against thoseassets and thus fuel expansion.The uniquenature of the assets insulates againstcompetition and therefore allows greaterpricing flexibility.

The company avoids the use of a chainbrand.Thus, none of its properties arebranded “Orient-Express” (except the trainand safari camps). Management believes thatdiscriminating travelers will choose anindividual property of fame in priority to achain brand. In the few locations where thecompany competes with de luxe brandchains (Venice, Lisbon and Rio de Janeiro are examples) it achieves up to 40% higheraverage rates than the chain brand hotels.

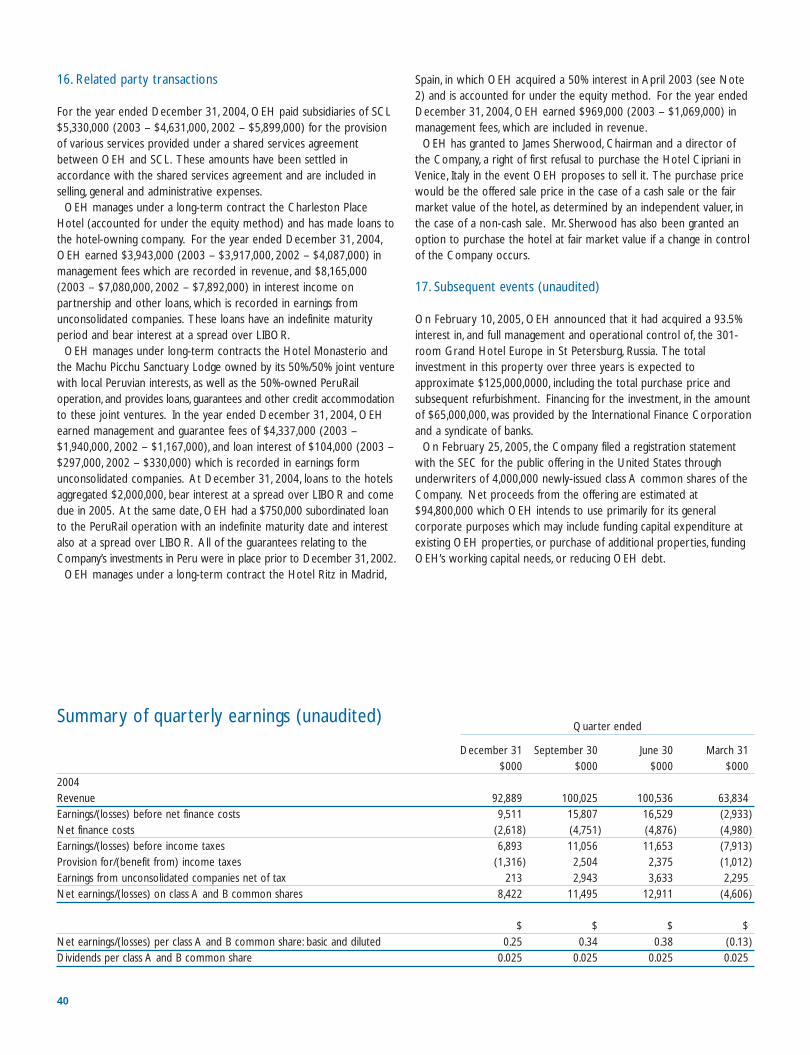

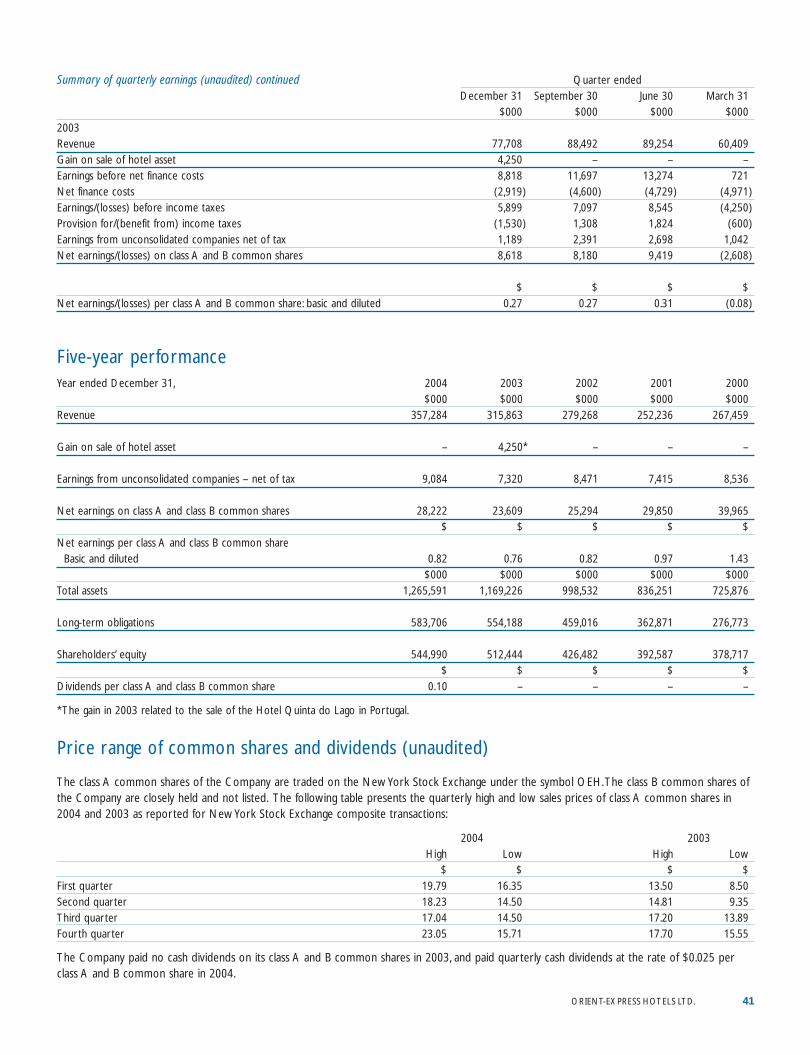

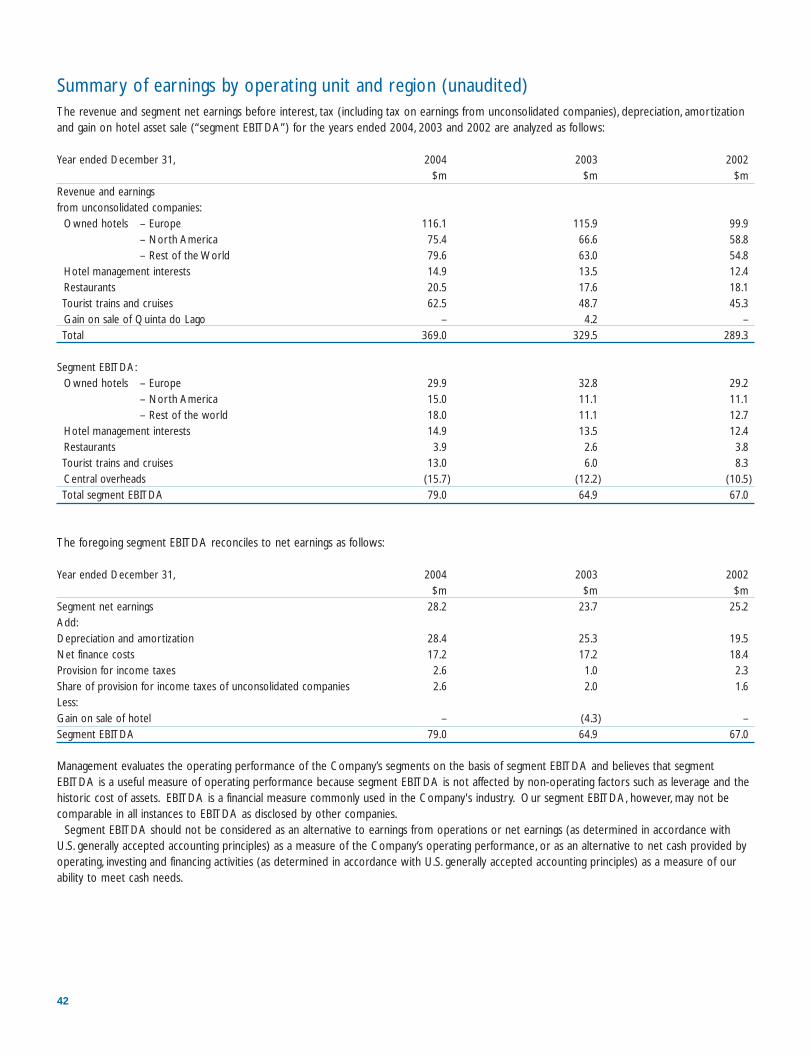

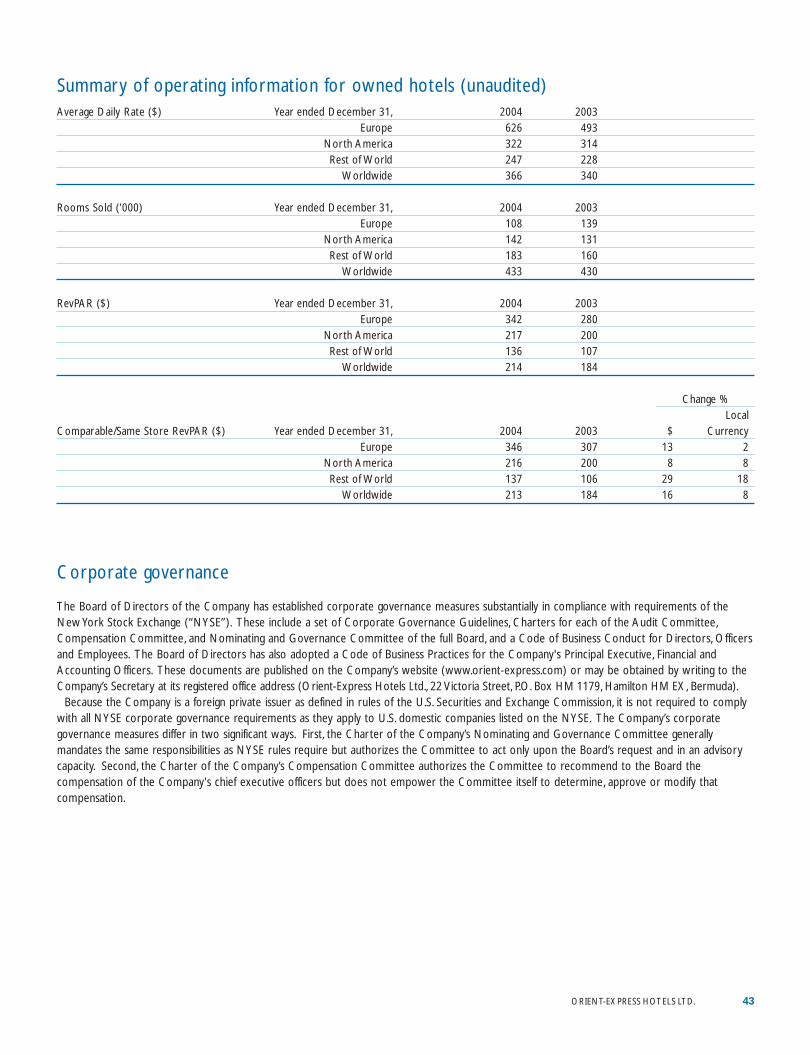

2004 2003 Change %$000 $000

Revenue 357,284 315,863 13

EBITDA(1) (2)

79,016 69,130 14

Net earnings (2)

28,222 23,609 20

Earnings per common share

(2)$0.82 $0.76 8

Number of shares (million) 34.30 31.14 10

(1) See page 42.(2) Includes in 2003 a gain on sale of hotel asset of $4,250,000.

Financial highlights

Front cover: Orient-Express Hotels recentlywelcomed the Grand Hotel Europe,St Petersburg, to its ever-expanding portfolio.This 130-year-old property is ideally placed forthe city’s top cultural attractions. A glamorous,belle-époque building decorated with animpressive collection of more than 200 worksof art, it boasts 301 guest rooms and sixrestaurants serving cuisine ranging from classicEuropean dishes to local specialties at itsrenowned Caviar Bar.

48818_p3_7.qxd.rev2 20/4/05 3:11 pm Page 3

4

Directors

From left to rightDaniel J. O’SullivanSenior Vice President – Finance andChief Financial Officer (retired) of Sea Containers Ltd.

John D. Campbell * Senior Counsel (retired) of ApplebySpurling Hunter (attorneys).Mr Campbell was a member of the firm until 1999, and is also aDirector of Sea Containers Ltd.

James B. SherwoodChairman of the company.Mr Sherwood is also a Director andPresident of Sea Containers Ltd.

Simon M.C. SherwoodPresident of the company.Previously Senior Vice President –Leisure of Sea Containers Ltd.(1997-2000) and was originallyappointed Vice President in 1991,prior to which he was Manager,Strategic Consulting of BostonConsulting Group (1986-1990).

Georg R. RafaelManaging Director of Rafael Group S.A.M.Previously Vice Chairman – ExecutiveCommittee of Mandarin OrientalHotels (2000-2002). ManagingDirector and founder of RafaelHotels (1986-2000) and JointManaging Director of RegentInternational Hotels (1972-1986).

J. Robert Lovejoy *Senior Managing Director ofRipplewood Holdings LLC (a privateequity investment firm).Prior to joining Ripplewood, MrLovejoy was Managing Director ofLazard Frères & Co. LLC and aGeneral Partner of the predecessorpartnership for over 15 years.

James B. Hurlock * Partner (retired) of White & Case LLP(attorneys).Mr Hurlock was Chairman of theManagement Committee of White &Case LLP (1980-2000), overseeing thefirm’s worldwide operations.

*Member of the Audit Committee

48818_p3_7.qxd.rev2 20/4/05 3:14 pm Page 4

5ORIENT-EXPRESS HOTELS LTD.

Management team

Back row from left to rightPaul White Vice President – Hotels, Africa,Australia and South America. Previously a managerof the company working on hotel financial andoperational matters, having joined from ForteHotels in 1991.

James G. Struthers Vice President – Finance andChief Financial Officer. Joined the company in2000. Previously Finance Director of Eurostar UKLtd. (1997-1999).Worked with Sea ContainersLtd. as Controller (1991-1996), having qualifiedas a chartered accountant with KPMG in 1986.

David C.Williams Vice President – Sales &Marketing. Joined the company in 1981 andserved as Commercial Director responsible forstrategic marketing developments and businessinitiatives in the Americas, Europe and Asia-Pacific. Previously with Carlson MarketingGroup.

Dean P. Andrews Vice President – Hotels,North America. Joined the company in 1997,having been previously with Omni Hotels

(1981-1997) working in new hotel developmentand financial and asset management.

Nicholas R.Varian Vice President – Trains andCruises. Joined Orient-Express Hotels in 1985from P&O Steam Navigation Company andbecame Vice President responsible for train and cruise activities in 1989.

Roger V. Collins Vice President – TechnicalServices. An engineer his entire career, he hasworked in the hotel industry since 1979 withGrand Metropolitan Hotels, Courage Inns andTaverns, and Trusthouse Forte Hotels, joiningOrient-Express Hotels in 1991.

Edwin S. Hetherington Secretary. Also VicePresident, General Counsel and Secretary of Sea Containers Ltd., having joined Orient-Express Hotels in 1980.

Front row seatedAdrian D. Constant Vice President – Hotels,Europe. Joined the company from Le MeridienHotels in 2001, where he had responsibility for

the development of its hotels in South America.He has also managed hotels in the Algarve,Malta, London and Madrid.

Pippa Isbell Vice President – Public Relations.Joined the company in 1998 after selling thepublic relations consultancy she founded in 1987, which had clients such as Inter-ContinentalHotels, Forte, Hilton International, Jarvis Hotels,and Millennium and Copthorne.

Natale Rusconi Vice President.Appointed ManagingDirector of Hotel Cipriani,Venice, in 1977 andresponsible for makingHotel Cipriani one of theworld’s top luxury hotels.Previously at the SavoyHotel and with CIGAHotels.

48818_p3_7.qxd.rev2 20/4/05 3:15 pm Page 5

Chairman’s message

April 1, 2005

Dear Shareholder

2004 was a year of excellent earnings growthfor your company. Excluding the gain on saleof a hotel in 2003, net earnings in 2004 were46% higher than in 2003, reaching $28.2million ($0.82 per common share) on revenueof $357.3 million. Revenue was up 13% fromthe prior year. This having been said, our netearnings still did not surpass the $40 millionof 2000, nor do they take into account thecapital investment made since 2000, so thereis considerable upside to come. As revenuerises through increased occupancy and higherrates, a greater proportion will fall to thebottom line. This is one of the reasons why a13% revenue gain translated into a 46% netearnings increase in 2004.

Our key financial indicators for 2004 were:a RevPAR of $213 vs. $184 in 2003, an increaseof 16%; EBITDA was $79 million vs. $65 million(excluding gain on sale of a hotel); long-termdebt (excluding the current portion) to equityratio was 1:1 with current assets equallingcurrent liabilities; year-end cash and undrawncredit facilities were $98 million comparedwith $149 million at the end of 2003.

The company made a number of newinvestments in 2004 plus the majorinvestment in the Grand Hotel Europe in St Petersburg, Russia in February, 2005. Inaddition, it invested $65 million in existingproperties. Because of the cash expended in

connection with these transactions, it wasdeemed prudent to enlarge the capital basein March, 2005 by selling 5.05 million class Acommon shares at $25.54 per share. Thisshould give the company the freedom tomake further attractive acquisitions and capitalimprovements in coming years, whilemaintaining balance in the company’s keyfinancial ratios.

In addition to the Grand Hotel Europeinvestment in early 2005, the company in2004 committed $8 million through aconvertible loan to the Pansea group inSoutheast Asia (EBITDA of Pansea doubled in 2004 over 2003 to $2.4 million), weacquired El Encanto in Santa Barbara,California in November, 2004 for $26 millionand we bought a 50% interest in Afloat inFrance in May, 2004 for $3 million (with anoption to acquire the other 50%). All theseacquisitions fit the company’s strategy of only investing in unique properties. The list of investments in existing properties is too long to recite here, but needless to say,we believe it will convert quickly intoincreased profitability.

Our diversity of investment by region andproduct (hotels, restaurants and tourist trains)has served us well. While European hotelearnings in 2004 were flat due to the strengthof the euro and British pound, earnings fromtourist trains soared and made Europe as awhole significantly more profitable in 2004than in 2003. All other regions outperformed2003 in 2004 but in making this comparison

Above:The Casanova Spa at Hotel Cipriani overlooksbeautiful gardens where vines named after thelegendary seducer are planted. Managed by Babor,the spa is an elegant retreat enhanced by locallymade features such as Murano glass chandeliers.

2003 2004

EBITDA Total $ millions

Owned hotels – Europe 29.9 32.8 (8.8)

North America 15.0 11.1 34.7

Rest of the World 18.1 11.1 63.0

Total owned hotels 63.0 55.0 14.4

Management and part-ownership interests 14.9 13.5 10.4

Restaurants 3.9 2.6 49.5

Total hotels and restaurants 81.8 71.1 14.9

Trains and cruises 13.0 6.0 118.2

Central overheads (15.8) (12.2) (29.2)

Gain on sale of Quinta do Lago – 4.3

Total EBITDA 79.0 69.1* 14.3

79.0

69.1

6

we need to take into account the SARSepidemic and the Iraq war in 2003 whichboth affected travel.

We are particularly pleased with ourinvestments in Latin America. Travel to Peru,Brazil, Argentina and Mexico where we haveproperties, has increased not only from theUS but from Europe and by nationals living inLatin America. We are currently looking atthree hotel acquisitions in Latin America but itis too early to say whether any will come tofruition. Our luxury tourist train, the HiramBingham, introduced in 2004 on the Cuzco-Machu Picchu route in Peru, has proven verypopular. Our plan to convert the LakeTiticaca steamer ss. Ollanta into an overnightcruise ship has been abandoned as the cost of conversion proved to be too high, so thevessel will be retained in its present state forday excursions. We own a property in theColca Canyon in Peru which is earmarked for development into a hotel when access

2004 2003 Change %

EBITDA ($ millions)

* Figures in 2003 include $4.25 million from gain on sale of the Hotel Quinta do Lago in November 2003.

48818_p3_7.qxd.rev2 20/4/05 3:13 pm Page 6

7ORIENT-EXPRESS HOTELS LTD.

Above: Planet at the Mount Nelson Hotel is Cape Town’s most elegant new bar. Guests sipchampagne at an onyx, underlit bar and relax on leather banquettes beneath a fiber optic MilkyWay and a mobile of the solar system.

problems can be resolved. This spectacularvalley is the home of the condor, the largestbird in the world.

In North America, the focus of ourattention is our residential village developmentat La Samanna in St Martin, addition of roomsat Maroma Resort and Spa on the RivieraMaya in Mexico, construction of an annex forconferences and banqueting at the WindsorCourt in New Orleans and renovation of El Encanto in Santa Barbara, California.

In Europe, the restoration of the HotelCaruso in Ravello, Italy is well advanced andthe hotel will reopen this summer. The GrandHotel Europe in St Petersburg is in excellentphysical condition but we will want toredecorate the property.

No significant investment is required in2005 in our South Pacific hotels followingcompletion of improvements to Bora BoraLagoon Resort & Spa and Lilianfels. In Asia,Pansea will be opening the Ubud HangingGardens Hotel in Bali in July and is currentlycompleting a renovation of its Jimbaran Puribeach hotel also in Bali.

We are acquiring a 50% interest in theRoyal Scotsman tourist train in April, 2005 for $2.7 million and have an option to acquirethe other 50%.

We continue to follow two policies thatdifferentiate us from many of ourcompetitors. We do not manage propertiesunless we hold an equity interest, usually 50%or more, in them. We do this for tworeasons. First, we want to realize the benefitof increasing property values and secondly wewant to decide on physical improvements.When management and ownership aredivorced the two interests are not always inalignment. Second, we do not brand ourproperties “Orient-Express” but insteadpromote them under their individual nameswhich we believe adds value throughexclusiveness and rate setting. We do,however, centrally market the propertiesthrough the Orient-Express Hotels,Trains &Cruises trade name.

Our largest shareholder, Sea ContainersLtd., has recently sold down part of its holdingin conjunction with our primary share issue,and now owns 25% of Orient-Express Hotels.Sea Containers has indicated that its intention is to exit entirely its investment inOrient-Express Hotels in due course.

Our results for 2004 were achievedthrough the hard work of our 5,500 staff in25 countries. In recognition of his formativerole in the company, Dr Natale Rusconi,

General Manager of the Hotel Cipriani inVenice (our first hotel) and the person whointroduced me to the hotel business, wasmade a Vice President in 2004. David CWilliams was promoted to Vice President –Sales and Marketing during the year.

Barring unforeseen events, 2005 and 2006appear to be very promising for your company.

Sincerely,

James B. SherwoodChairman & Founder

48818_p3_7.qxd.rev2 20/4/05 3:14 pm Page 7

8

President’s overview of performance

Hotels: EuropeSame store RevPAR in local currency was up2% allowing us no more than to hold groundagainst inflation. As a result EBITDA on asame store basis was flat at about $30 million(the 2003 results include over $3 million ofEBITDA from the Hotel Quinta do Lagogenerated during the year prior to its sale).Given the difficult trading conditions at manyof our hotels we are quite pleased with thisperformance. The strength of the euro, upanother 11% over the year, continues to be achallenge and has reduced the percentage ofU.S. guests to about 25%, well down fromhistoric levels. Our U.S. bookings showedsome growth in 2004 but there is unlikely tobe a major recovery with the dollar so weak.

Our most exciting development is that in February 2005 we acquired the majorityinterest in the Grand Hotel Europe, StPetersburg (301 keys) – the residual 6%continues to be owned by the City of St Petersburg. This is Russia’s most famoushotel and recently celebrated its 130thbirthday. It is located in the heart of the cityon Nevsky Prospekt attracting both touristsand business travelers. In 2004 it generatedEBITDA of about $17 million and ourinvestment was made at an EBITDA multipleof about six, so this investment willimmediately add to the company’s earnings.In addition it should help us build Russianoutbound business for our other properties.

ItalyWork is well advanced at the Hotel Carusoin Ravello and the property should open in a few months’ time for the high season. Thehotel really will be stunning with magnificentviews out over the Amalfi coast and aspectacular pool set in historic gardens. Thedesign includes a large number of suites, asthese are so popular (and profitable) at ourother Italian hotels. This project has takenmany years to complete due to the strictdevelopment regulations in the area. Theselimitations make it difficult for anybody to addnew hotels so over the next few years we areconfident our investment in the Caruso willgenerate very attractive returns.

At the Hotel Cipriani and PalazzoVendramin (104 keys) EBITDA increased

another $0.5 million in spite of the strongeuro acting as a deterrent to U.S. guests. Wecontinue to invest in improvements at thehotel. The new spa has been well receivedand this last winter we have enhanced manyrooms by adding balconies and we havecreated the Dogaressa suite with views overSt Mark’s Square.

The Hotel Splendido and Splendido Mare(81 keys) fully justified our investments of lastwinter with RevPAR up 15% in euros (26% indollars) and EBITDA growing by $1 million.

The Villa San Michele (45 keys) had atougher year and we had to show moreflexibility with rates than in the past but EBITDAheld at $2.9 million similar to the result in2003. With so much going on at the Carusoand Cipriani we are not planning any majorchanges this year at our other Italian hotels.

SpainThe Hotel Ritz (167 keys) showed goodprogress, increasing its market penetration andrevenue share in Madrid. However this wasmore than offset by a generally weak marketthat also suffered in the aftermath of theterrorist bomb attacks in the city. We havelifted service standards at the hotel and are

now starting to make physical improvements.The lobby and reception area have beenrefurbished and major works should start onthe rooms this summer.

Our new suites at La Residencia (59keys) in Mallorca have been a great successwith the hotel’s average room rate going up11% in euros (22% in dollars). This underlinesthe value of our permits to add up to 20additional suites. This winter we worked onthe central guest areas making improvementsto the lounges and adding a new elevator toimprove access to the main pool.

PortugalPortugal had another difficult year withoccupancy and EBITDA down at both our

Above: The newly designed Medieval Room atHôtel de la Cité embodies all the history andmagic of the ancient citadel of Carcassonne.With its rich wood paneling, hand-carved canopybed and crackling log fire, it takes visitors back tothe days when knights in armour rode through the fortress town. This spectacular guest room is just one of the hotel’s many memorableaccommodations, which include suites with privateterraces overlooking the French countryside.

48818_p8_19.rev2 20/4/05 3:21 pm Page 8

9

Reid’s Palace Hotel

Lapa Palace Hotel

La Residencia

Hôtel de la Cité

Hotel Splendido and Hotel Splendido Mare

Hotel Caruso

Villa San Michele

Hotel Cipriani andPalazzo Vendramin

Harry’s BarLe Manoir aux Quat’Saisons

Hotel Ritz

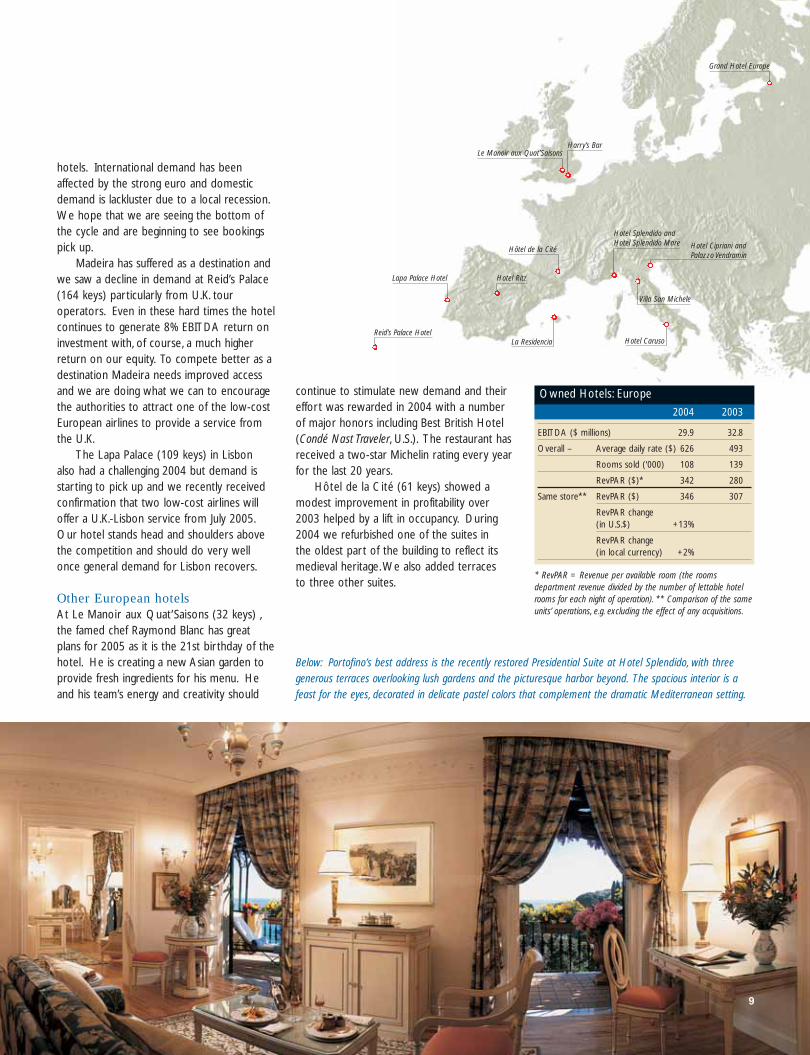

hotels. International demand has beenaffected by the strong euro and domesticdemand is lackluster due to a local recession.We hope that we are seeing the bottom ofthe cycle and are beginning to see bookingspick up.

Madeira has suffered as a destination andwe saw a decline in demand at Reid’s Palace(164 keys) particularly from U.K. touroperators. Even in these hard times the hotelcontinues to generate 8% EBITDA return oninvestment with, of course, a much higherreturn on our equity. To compete better as adestination Madeira needs improved accessand we are doing what we can to encouragethe authorities to attract one of the low-costEuropean airlines to provide a service fromthe U.K.

The Lapa Palace (109 keys) in Lisbon also had a challenging 2004 but demand isstarting to pick up and we recently receivedconfirmation that two low-cost airlines willoffer a U.K.-Lisbon service from July 2005.Our hotel stands head and shoulders abovethe competition and should do very wellonce general demand for Lisbon recovers.

Other European hotelsAt Le Manoir aux Quat’Saisons (32 keys) ,the famed chef Raymond Blanc has greatplans for 2005 as it is the 21st birthday of thehotel. He is creating a new Asian garden toprovide fresh ingredients for his menu. Heand his team’s energy and creativity should

continue to stimulate new demand and theireffort was rewarded in 2004 with a numberof major honors including Best British Hotel(Condé Nast Traveler, U.S.). The restaurant hasreceived a two-star Michelin rating every yearfor the last 20 years.

Hôtel de la Cité (61 keys) showed amodest improvement in profitability over2003 helped by a lift in occupancy. During2004 we refurbished one of the suites in the oldest part of the building to reflect itsmedieval heritage.We also added terraces to three other suites.

Owned Hotels: Europe

2004 2003

* RevPAR = Revenue per available room (the roomsdepartment revenue divided by the number of lettable hotelrooms for each night of operation). ** Comparison of the sameunits’ operations, e.g. excluding the effect of any acquisitions.

EBITDA ($ millions) 29.9 32.8

Overall – Average daily rate ($) 626 493

Rooms sold (‘000) 108 139

RevPAR ($)* 342 280

Same store** RevPAR ($) 346 307

RevPAR change (in U.S.$) +13%

RevPAR change (in local currency) +2%

Below: Portofino’s best address is the recently restored Presidential Suite at Hotel Splendido, with threegenerous terraces overlooking lush gardens and the picturesque harbor beyond. The spacious interior is afeast for the eyes, decorated in delicate pastel colors that complement the dramatic Mediterranean setting.

Grand Hotel Europe

48818_p8_19.rev2 20/4/05 3:22 pm Page 9

10

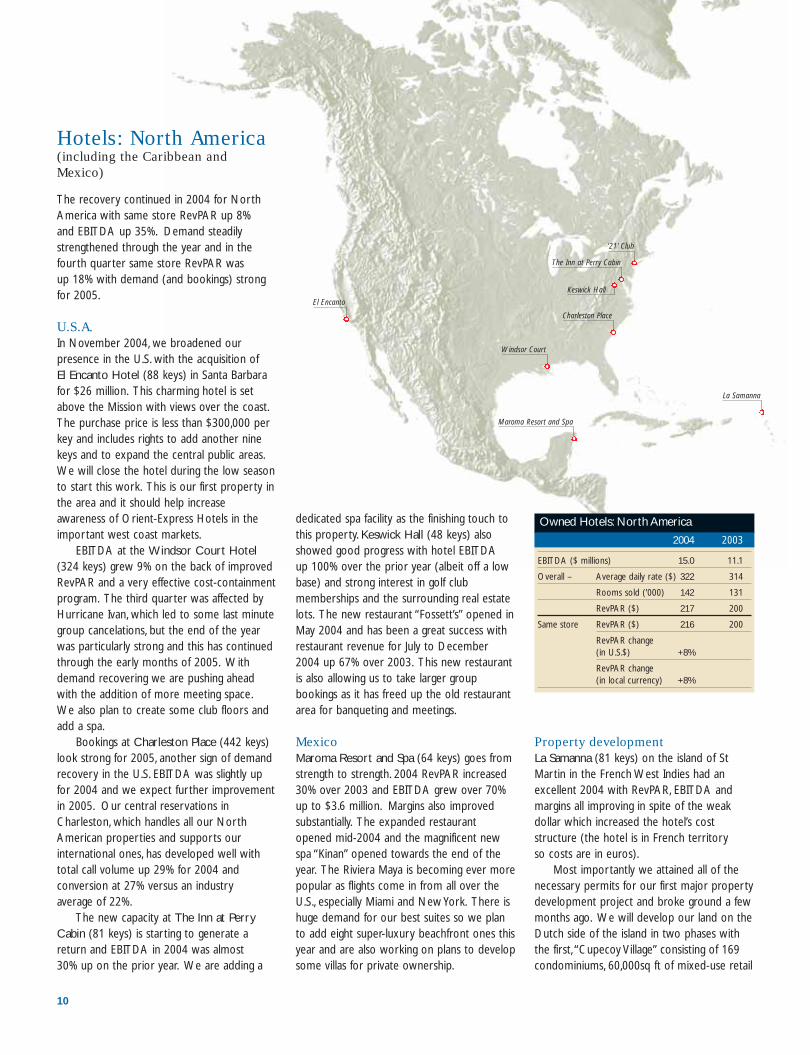

Hotels: North America(including the Caribbean andMexico)

The recovery continued in 2004 for NorthAmerica with same store RevPAR up 8% and EBITDA up 35%. Demand steadilystrengthened through the year and in thefourth quarter same store RevPAR was up 18% with demand (and bookings) strongfor 2005.

U.S.A.In November 2004, we broadened ourpresence in the U.S. with the acquisition of El Encanto Hotel (88 keys) in Santa Barbarafor $26 million. This charming hotel is setabove the Mission with views over the coast.The purchase price is less than $300,000 perkey and includes rights to add another ninekeys and to expand the central public areas.We will close the hotel during the low seasonto start this work. This is our first property inthe area and it should help increaseawareness of Orient-Express Hotels in theimportant west coast markets.

EBITDA at the Windsor Court Hotel(324 keys) grew 9% on the back of improvedRevPAR and a very effective cost-containmentprogram. The third quarter was affected byHurricane Ivan, which led to some last minutegroup cancelations, but the end of the yearwas particularly strong and this has continuedthrough the early months of 2005. Withdemand recovering we are pushing aheadwith the addition of more meeting space.We also plan to create some club floors andadd a spa.

Bookings at Charleston Place (442 keys)look strong for 2005, another sign of demandrecovery in the U.S. EBITDA was slightly upfor 2004 and we expect further improvementin 2005. Our central reservations inCharleston, which handles all our NorthAmerican properties and supports ourinternational ones, has developed well withtotal call volume up 29% for 2004 andconversion at 27% versus an industry average of 22%.

The new capacity at The Inn at PerryCabin (81 keys) is starting to generate areturn and EBITDA in 2004 was almost 30% up on the prior year. We are adding a

dedicated spa facility as the finishing touch tothis property. Keswick Hall (48 keys) alsoshowed good progress with hotel EBITDA up 100% over the prior year (albeit off a lowbase) and strong interest in golf clubmemberships and the surrounding real estatelots. The new restaurant “Fossett’s” opened inMay 2004 and has been a great success withrestaurant revenue for July to December2004 up 67% over 2003. This new restaurantis also allowing us to take larger groupbookings as it has freed up the old restaurantarea for banqueting and meetings.

MexicoMaroma Resort and Spa (64 keys) goes fromstrength to strength. 2004 RevPAR increased30% over 2003 and EBITDA grew over 70%up to $3.6 million. Margins also improvedsubstantially. The expanded restaurantopened mid-2004 and the magnificent newspa “Kinan” opened towards the end of theyear. The Riviera Maya is becoming ever morepopular as flights come in from all over theU.S., especially Miami and New York. There ishuge demand for our best suites so we planto add eight super-luxury beachfront ones thisyear and are also working on plans to developsome villas for private ownership.

Property developmentLa Samanna (81 keys) on the island of StMartin in the French West Indies had anexcellent 2004 with RevPAR, EBITDA andmargins all improving in spite of the weakdollar which increased the hotel’s coststructure (the hotel is in French territory so costs are in euros).

Most importantly we attained all of thenecessary permits for our first major propertydevelopment project and broke ground a fewmonths ago. We will develop our land on theDutch side of the island in two phases withthe first, “Cupecoy Village” consisting of 169condominiums, 60,000sq ft of mixed-use retail

Windsor Court

Maroma Resort and Spa

Charleston Place

‘21’ Club

The Inn at Perry Cabin

Keswick Hall

La Samanna

Owned Hotels: North America

2004 2003

EBITDA ($ millions) 15.0 11.1

Overall – Average daily rate ($) 322 314

Rooms sold (’000) 142 131

RevPAR ($) 217 200

Same store RevPAR ($) 216 200

RevPAR change (in U.S.$) +8%

RevPAR change (in local currency) +8%

El Encanto

48818_p8_19.rev2 20/4/05 3:21 pm Page 10

11ORIENT-EXPRESS HOTELS LTD.

Above: Positioned on the Californian coast at Santa Barbara, El Encanto Hotel & Garden Villashas long been an exclusive retreat for Hollywoodcelebrities and other guests in search of peace and serenity. This elegant property comprisesclusters of cottages set in gardens planted withrare trees. Orient-Express Hotels is working withthe National Trust for Historic Preservation torestore the hotel, and to add five more cottages,a spa and a fitness center.

and a marina with seven mega-yacht berths.This development will be spread over severalyears and could generate about $50 millioncumulatively in profit on sale of condominiumsas well as an ongoing earning stream of about$5 million per annum. It will use just over twothirds of our land parcel on the Dutch side.

On the French side we have also brokenground and are building 10 luxury cliff-frontvillas. This project should be complete in thenext two years and generate profit on sale of over $10 million. It uses only a small part of our French-side land and we are alreadyworking on designs for a further 20 villas on other parcels. In addition to the profit

on sale, there will be ongoing earnings frommaintenance/service charges and revenuefrom renting out the villas when not used bythe owners.

We look on property development as agrowing business for us as it fits well with ourcompany’s image and can make good use ofthe land bank we have built up over the years.In addition to our projects at La Samanna andKeswick we are working to roll out ourdevelopment arm at Maroma,The Inn at PerryCabin and Bora Bora Lagoon Resort & Spa.

48818_p8_19.rev2 20/4/05 3:20 pm Page 11

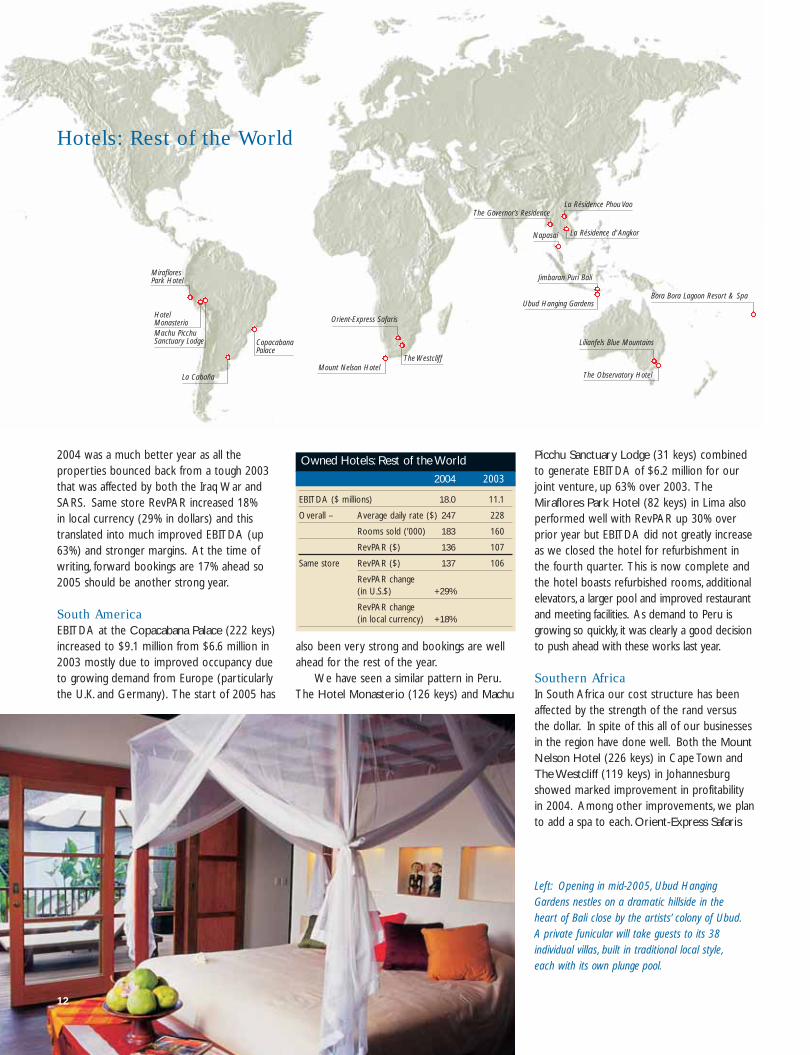

2004 was a much better year as all theproperties bounced back from a tough 2003that was affected by both the Iraq War andSARS. Same store RevPAR increased 18% in local currency (29% in dollars) and thistranslated into much improved EBITDA (up63%) and stronger margins. At the time ofwriting, forward bookings are 17% ahead so2005 should be another strong year.

South AmericaEBITDA at the Copacabana Palace (222 keys)increased to $9.1 million from $6.6 million in2003 mostly due to improved occupancy dueto growing demand from Europe (particularlythe U.K. and Germany). The start of 2005 has

also been very strong and bookings are wellahead for the rest of the year.

We have seen a similar pattern in Peru.The Hotel Monasterio (126 keys) and Machu

Picchu Sanctuary Lodge (31 keys) combinedto generate EBITDA of $6.2 million for ourjoint venture, up 63% over 2003. TheMiraflores Park Hotel (82 keys) in Lima alsoperformed well with RevPAR up 30% overprior year but EBITDA did not greatly increaseas we closed the hotel for refurbishment inthe fourth quarter. This is now complete andthe hotel boasts refurbished rooms, additionalelevators, a larger pool and improved restaurantand meeting facilities. As demand to Peru isgrowing so quickly, it was clearly a good decisionto push ahead with these works last year.

Southern AfricaIn South Africa our cost structure has beenaffected by the strength of the rand versusthe dollar. In spite of this all of our businessesin the region have done well. Both the MountNelson Hotel (226 keys) in Cape Town andThe Westcliff (119 keys) in Johannesburgshowed marked improvement in profitabilityin 2004. Among other improvements, we planto add a spa to each. Orient-Express Safaris

MirafloresPark Hotel

HotelMonasterioMachu PicchuSanctuary Lodge

La Cabaña

CopacabanaPalace

Mount Nelson HotelThe Westcliff

Orient-Express Safaris

The Observatory Hotel

Lilianfels Blue Mountains

Bora Bora Lagoon Resort & SpaUbud Hanging Gardens

Jimbaran Puri Bali

Napasai

The Governor’s Residence

La Résidence d’ Angkor

La Résidence Phou Vao

Hotels: Rest of the World

Left: Opening in mid-2005, Ubud HangingGardens nestles on a dramatic hillside in the heart of Bali close by the artists’ colony of Ubud.A private funicular will take guests to its 38individual villas, built in traditional local style,each with its own plunge pool.

Owned Hotels: Rest of the World

2004 2003

EBITDA ($ millions) 18.0 11.1

Overall – Average daily rate ($) 247 228

Rooms sold (’000) 183 160

RevPAR ($) 136 107

Same store RevPAR ($) 137 106

RevPAR change (in U.S.$) +29%

RevPAR change (in local currency) +18%

12

48818_p8_19.rev2 20/4/05 3:23 pm Page 12

13ORIENT-EXPRESS HOTELS LTD.

RestaurantsOur largest investment in stand-alone restaurantsis at ‘21’ Club in New York. 2004 was a muchstronger year with revenue up 14% and EBITDA$1.2 million ahead of the prior year. Thebusiness climate seems more positive as weenter 2005 and we are getting more demandfrom the investment banking sector that hasalways been a mainstay for the restaurant.

Our other restaurant investments aremuch smaller. At La Cabaña in Buenos Aires2004 was the first full year of operations andthe restaurant made a small loss but demand is steadily growing month on month so 2005should show improvement. Harry’s Bar ourjoint venture private dining club in Londoncontinues to do well.

Above: The new infinity swimming pool at BoraBora Lagoon Resort & Spa is the largest in thelagoon, and enjoys spectacular views of MotuToopua, a fragment of an ancient volcano. Alsonew for guests is the opportunity to combine a stay with a six-night cruise aboard a 30-berthyacht, visiting nearby islands.

(39 keys) generated EBITDA of $0.2 million in2004 after suffering a $0.5 million loss in2003. Bookings are well ahead (again) andwe are now offering an air service to thecamps from Johannesburg which should makeaccess much easier for our guests.

AustralasiaAll of our properties in Australasia showedmarked improvement as they recovered in2004 from the downturn in 2003 (primarilydue to SARS). At The Observatory Hotel(96 keys) occupancy recovered to 69% from56% in 2003 and EBITDA increased byalmost 70%.

At Lilianfels (85 keys) in the BlueMountains we finished our refurbishment,adding an outdoor pool and a spa. In thesecond half of the year the hotel returnedimmediately to pre-2000 operating levels and bookings are well ahead for 2005.

Bora Bora Lagoon Resort & Spa

(79 keys) was a major problem in 2003generating $1.2 million loss at the EBITDAlevel. The results have turned around in 2004with RevPAR up over 50% generatingEBITDA of $0.5 million for the year. 2005looks like another year of improvement butlonger term we still face challenges as severalnew hotels are under construction in the area.

AsiaOur Asian hotel collection is the Pansea groupof six properties and our investment duringFebruary 2004 looks to have been very welltimed as demand has picked up reflecting therecovery of tourism to Southeast Asia.

At Jimbaran Puri (41 keys) in Bali,occupancy grew back to 71% in 2004 versusonly 47% in 2003. As a result, revenue andEBITDA both increased to more than 2.5times the prior year level. In Bali we have underconstruction Ubud Hanging Gardens (38 keys)that will open mid-2005.This beautiful propertyis located in the mountains and each roomhas a private pool. Ubud has always been apopular destination and should be the perfectcomplement to our existing beachfront hotel.

The Napasai (55 keys) on Koh Samui,Thailand opened during 2004 so it is early daysto judge performance. Fortunately Koh Samuiisland is on the east side of Thailand so it was

unaffected by the tsunami or its aftermath.La Résidence d’Angkor (55 keys) in

Siem Reap, La Résidence Phou Vao (34 keys)in Luang Prabang, and The Governor’sResidence (49 keys) in Yangon have all seensubstantial gains and Pansea’s total EBITDAhas more than doubled over 2003. Ouragreement with Pansea includes a convertibleloan and the right to buy the company at afuture date so we are very encouraged to seethe business grow so well.

48818_p8_19.rev2 20/4/05 3:24 pm Page 13

14

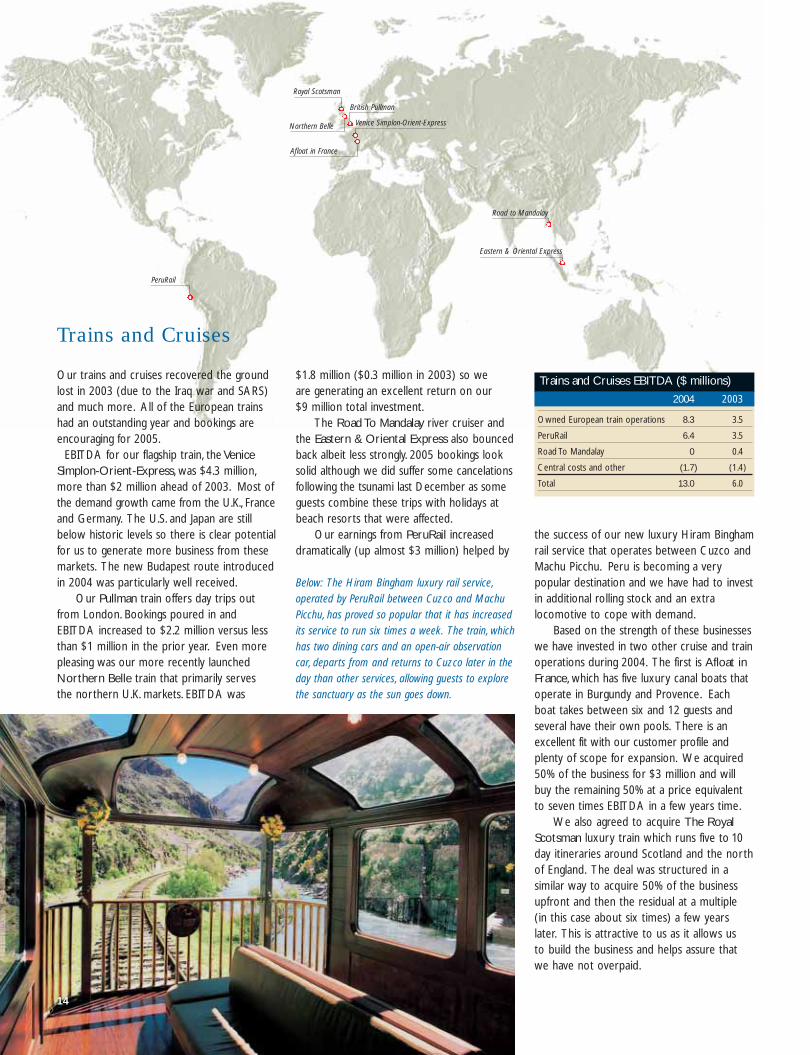

PeruRail

Eastern & Oriental Express

Road to Mandalay

Afloat in France

Royal Scotsman

Northern Belle

British Pullman

Venice Simplon-Orient-Express

Trains and Cruises

Our trains and cruises recovered the groundlost in 2003 (due to the Iraq war and SARS)and much more. All of the European trainshad an outstanding year and bookings areencouraging for 2005.

EBITDA for our flagship train, the VeniceSimplon-Orient-Express, was $4.3 million,more than $2 million ahead of 2003. Most ofthe demand growth came from the U.K., Franceand Germany. The U.S. and Japan are stillbelow historic levels so there is clear potentialfor us to generate more business from thesemarkets. The new Budapest route introducedin 2004 was particularly well received.

Our Pullman train offers day trips outfrom London. Bookings poured in andEBITDA increased to $2.2 million versus lessthan $1 million in the prior year. Even morepleasing was our more recently launchedNorthern Belle train that primarily serves the northern U.K. markets. EBITDA was

$1.8 million ($0.3 million in 2003) so we are generating an excellent return on our $9 million total investment.

The Road To Mandalay river cruiser andthe Eastern & Oriental Express also bouncedback albeit less strongly. 2005 bookings looksolid although we did suffer some cancelationsfollowing the tsunami last December as someguests combine these trips with holidays atbeach resorts that were affected.

Our earnings from PeruRail increaseddramatically (up almost $3 million) helped by

Below: The Hiram Bingham luxury rail service,operated by PeruRail between Cuzco and MachuPicchu, has proved so popular that it has increasedits service to run six times a week. The train, whichhas two dining cars and an open-air observationcar, departs from and returns to Cuzco later in theday than other services, allowing guests to explorethe sanctuary as the sun goes down.

Trains and Cruises EBITDA ($ millions)

2004 2003

Owned European train operations 8.3 3.5

PeruRail 6.4 3.5

Road To Mandalay 0 0.4

Central costs and other (1.7) (1.4)

Total 13.0 6.0

the success of our new luxury Hiram Binghamrail service that operates between Cuzco andMachu Picchu. Peru is becoming a verypopular destination and we have had to investin additional rolling stock and an extralocomotive to cope with demand.

Based on the strength of these businesseswe have invested in two other cruise and trainoperations during 2004. The first is Afloat inFrance, which has five luxury canal boats thatoperate in Burgundy and Provence. Eachboat takes between six and 12 guests andseveral have their own pools. There is anexcellent fit with our customer profile andplenty of scope for expansion. We acquired50% of the business for $3 million and willbuy the remaining 50% at a price equivalentto seven times EBITDA in a few years time.

We also agreed to acquire The RoyalScotsman luxury train which runs five to 10day itineraries around Scotland and the northof England. The deal was structured in asimilar way to acquire 50% of the businessupfront and then the residual at a multiple (in this case about six times) a few yearslater. This is attractive to us as it allows us to build the business and helps assure thatwe have not overpaid.

48818_p8_19.rev2 20/4/05 3:29 pm Page 14

15ORIENT-EXPRESS HOTELS LTD.

I look back with some satisfaction at theOutlook section of last year’s annual report.It was clear at that time we were likely to seea recovery with much stronger demand “fromthe second quarter onwards”. As weexpected, results have picked up particularlytowards the end of the year and 2004 fourthquarter RevPAR was up 12% in local currency(18% in dollars).

What we could not foresee was thesuccess we would have in finding exciting newacquisitions to add to our portfolio. TheGrand Hotel Europe is a very positive

The magic of the Scottish Highlands surroundsguests aboard The Royal Scotsman, as it travelsthrough wild countryside and along virgin stretchesof coast.The train stops at castles, whiskeydistilleries and other places of interest along theway, where guests enjoy special tours in thecompany of local experts – or even the laird of a private estate.

addition as it is a large investment at six timesEBITDA so it instantly adds to the bottomline. Our ability to locate and complete thissort of deal is a major strength of thecompany.

Another real positive is the speed withwhich we have attained the required permitsfor our first major property development,the villas and condominiums at La Samanna.I expect property developments around theworld to become a major generator of profitfor the company in the years to come.

We look forward to 2005 with high

expectations. At the time of writing business isgoing well, bookings are 7% ahead of last yearand we have the added upside from theforthcoming opening of the Caruso hotel inItaly and profits from our recent acquisitionselsewhere.

Simon M. C. Sherwood President

Outlook for 2005

48818_p8_19.rev2 20/4/05 3:25 pm Page 15

Chief Financial Officer’s report

EBITDA in 2004 was up 22% to $79 millionfrom $64.9 million (excluding the gain on sale of a hotel in 2003). Depreciationincreased by $3.1 million primarily due toacquisitions, capital expenditure and partly the weaker dollar.

We continue to enjoy the benefit of a low effective tax rate (16% in 2004) due inlarge part to the company being incorporated in Bermuda so the flow-through from EBITDA to bottom line earnings is particularlyefficient. Net earnings for the year increasedby 46% from $19.4 million in 2003 (excludingthe gain on sale of a hotel) to $28.2 million.Cash flow from operations improved 60%from $33 million to $53 million.

Above: Keswick Hall at Charlottesville,Virginia,has opened “Fossett’s”, a new 70-seat restaurantnamed for Thomas Jefferson’s cook at his nearbyhome of Monticello.This is a dining room with a view: floor-to-ceiling windows provide aspectacular panorama of the recently upgradedArnold Palmer championship golf course and the countryside beyond.

16

All owned hotels

2004 2003

Overall – Average daily rate ($) 366 340

Rooms sold (’000) 433 430

RevPAR ($) 214 184

Same store RevPAR ($) 213 184

RevPAR change (in U.S.$) 16%

RevPAR change (in local currency) 8%

During the year, the company invested$35 million in acquisitions, which included the purchase of El Encanto in Santa Barbara($26 million) and an investment in Afloat inFrance ($3 million). A further $65 million wasspent on capital expenditure to existingproperties (including approximately $15million of maintenance capital expenditure).The major works during the year were thecontinued renovation of the Hotel Caruso,the addition of rooms and new facilities atMaroma Resort and Spa, a new spa at theCipriani, completion of the refurbishment of Bora Bora Lagoon Resort & Spa and the addition of new rooms and improvedfacilities at La Residencia.

To fund this program, the company drewdown debt of $110 million versus principalrepayments of $55 million. After payingdividends of $3 million, net cash flow for the year was a surplus of $5 million, resultingin a cash balance of $86 million at 31December, 2004.

Total debt at year end was $584 millionof which $303 million was in euros, $218million in U.S. dollars and the balance in othercurrencies. All the debt is senior securedmortgage finance. We find that the uniqueproperties we have in our portfolio areattractive security to the banks allowing them

Left: Maroma Resort and Spa on the MexicanRiviera has recently added a new, dedicated spa“Kinan” that offers a number of specializedMexican treatments.

48818_p8_19.rev2 21/4/05 10:31 am Page 16

17ORIENT-EXPRESS HOTELS LTD.

have obtained attractive finance. The terms ofthis financing is such that the company willprovide its equity participation by way of theland and not cash. The loan will be repaid asstage payments are received from thepurchasers of condominiums and villas with aproportion of these proceeds going to thebank and the balance to the company. Thisshould further enhance the cash flow returnof the project.

With all of this activity in the last 12months (particularly the Grand Hotel Europe)and other acquisitions and investments thatwe have under consideration, we decided toraise additional funds through the sale ofequity. In March 2005 the company sold

5.05 million shares at $25.54 per share.Sea Containers (our largest shareholder) alsotook the opportunity to sell 4.5 million sharesreducing its shareholding from 42% down to25%. This has helped alleviate any perceivedoverhang related to its position and has alsogreatly increased the company’s free float(excluding Sea Containers’ shareholding) from20 million shares to 30 million shares.

James G. StruthersVice President – Finance and Chief FinancialOfficer

to offer us very competitive rates and terms.Our average cost of debt was 4.1% atDecember 31, 2004.

The company has been very active so farin 2005. On February 8 we added the Grand Hotel Europe in St Petersburg to ourcollection of hotels. This will result in a totalinvestment of around $125 million once ourprogram of refurbishment and investment iscomplete. $65 million of finance has beenprovided by a syndicate of banks led by theInternational Finance Corporation, a subsidiaryof the World Bank, which has extensivelending experience in Russia.

We have also made much progress withour property development on St Martin and

48818_p8_19.rev2 20/4/05 3:26 pm Page 17

18

A selection of awards received in 2004

Hotel Cipriani• Gold List Condé Nast Traveler (U.S.)• 6th Best City Hotel in Europe

Departures magazine (U.S.)• Best Hotel in Venice

Andrew Harper’s Hideaway Report (U.S.)• 5th Best European Hotel Condé Nast Traveller (U.K.)

Villa San Michele• Gold List Condé Nast Traveler (U.S.)• 11th Best International Resort Hideaway

Andrew Harper’s Hideaway Report (U.S.)• 25th Best European Hotel Condé Nast Traveller (U.K.)

Hotel Splendido • Gold List Condé Nast Traveler (U.S.)• 6th Best International Resort Hotel

Andrew Harper’s Hideaway Report (U.S.)• 7th Best European Hotel Condé Nast Traveller (U.K.)

Hôtel de la Cité • 500 Ultimate Guide – The Greatest Hotels in

The World Travel & Leisure (U.S.)• Gold List Condé Nast Traveler (U.S.)• Retained one Michelin Star for the third

consecutive year Michelin Guide

Lapa Palace• Top Restaurant in Lisbon – Ristorante Hotel

Cipriani Zagat Guide (U.S.)• Gold List Condé Nast Traveler (U.S.)• Top Hotel in Lisbon

Andrew Harper’s Hideaway Report (U.S.)• 18th Best European Hotel Condé Nast Traveller (U.K.)

Reid’s Palace• Gold List Condé Nast Traveler (U.S.)

Hotel Ritz, Madrid• Gold List Condé Nast Traveler (U.S.)• 16th Best City Hotel in Europe

Departures magazine (U.S.)• Best Hotel in Madrid Global Finance (U.S.)• Top Hotel in Madrid

Andrew Harper’s Hideaway Report (U.S.)• Spain’s Leading Hotel World Travel Awards

La Residencia• 11th Best Beach Hotel in Europe

Departures magazine (U.S.)

Windsor Court Hotel• 17th Best City Hotel in the U.S.A. & Canada

Departures magazine (U.S.)• 8th Best Hotel in the U.S.A. and Canada

Travel and Leisure (U.S.)• Top Hotel in New Orleans

Andrew Harper’s Hideaway Report (U.S.)

Miraflores Park Hotel• One of the World’s Best Business Hotels

Travel & Leisure (U.S.)• 6th Best South American Hotel

Condé Nast Traveller (U.K.)

Bora Bora Lagoon Resort & Spa• Gold List (scored 100% for location)

Condé Nast Traveler Gold (U.S.)• 9th Best Spa in Australia and the South Pacific –

Maru Spa Condé Nast Traveller (U.K.)• 9th Best Hotel in Australia, New Zealand & South

Pacific Departures magazine (U.S.)• 6th Best Australasia and South Pacific Leisure

Hotel Condé Nast Traveller (U.K.)• Maru Spa named as the “New Spa to Watch”

Travel & Leisure (U.S.)

Mount Nelson Hotel• Included in the 500 Ultimate Guide of the

Greatest Hotels in The World Travel & Leisure (U.S.)• Gold List Condé Nast Traveler (U.S.)• 12th Best Overseas Leisure Hotel in Africa,

Indian Ocean and Maldives Condé Nast Traveller (U.K.)

• Africa’s Leading Hotel World Travel Awards

The Westcliff• Gold List Condé Nast Traveler (U.S.)

Above: The Maru Spa at Bora Bora Lagoon Resortoffers guests a unique experience – traditionalPolynesian treatments high above the ground in thebranches of a massive banyan tree. This loftytreehouse spa is complemented by other treatmentrooms on the beachfront and beside the lagoon –all encircled by lush tropical gardens.

The Inn at Perry Cabin• Included in the 500 Ultimate Guide – The

Greatest Hotels in The World Travel & Leisure (U.S.)• Gold List Condé Nast Traveler (U.S.)• 18th Best U.S. Resort Hideaway

Andrew Harper’s Hideaway Report (U.S.)

Keswick Hall• Gold List Condé Nast Traveler (U.S.)• 23rd Best Boutique Hotel in U.S.A. & Canada

Departures magazine (U.S.)

Charleston Place • Gold List Condé Nast Traveler (U.S.)• 4th Top U.S. and Canada Destination

Travel and Leisure (U.S.)• Gold Key Award 2004 for Excellence in

Hospitality Design (U.S.)• Top City Hotel Spa in the U.S.A. and Canada –

The Spa at Charleston Place Travel & Leisure (U.S.)• One of the top 100 travel experiences in the

world – highest score ever in the 17-year history of the award Condé Nast Traveler (U.S.)

• Preferred Hotel PartnerDiners Club Magazine (Germany)

Maroma Resort and Spa• Gold List Condé Nast Traveler (U.S.)• Mexico’s Leading Spa Resort

World Travel Awards • 3rd Best Central American Hotel

Condé Nast Traveler (U.S.)

La Samanna• Included in the 500 Ultimate Guide to the

Greatest Hotels in The World Travel & Leisure (U.S.)• Top Hotel in the Atlantic & Caribbean

Departures magazine (U.S.)

Copacabana Palace• Gold List Condé Nast Traveler (U.S.)• 4th Best Hotel in Mexico, Central and South

America Departures magazine (U.S.)• South America’s Leading hotel

World Travel Awards • 18th Best Overseas Leisure Hotel – Americas

and Caribbean Condé Nast Traveler (U.S.)• 7th Best South American Hotel

Condé Nast Traveller (U.K.)

Hotel Monasterio• Gold List Condé Nast Traveler (U.S.)• 82nd Best Hotel in the World

Condé Nast Traveller (U.K.)• 4th Best Hotel in South America

Condé Nast Traveller (U.K.)• Peru’s Leading Hotel World Travel Awards

48818_p8_19.rev2 20/4/05 1:37 pm Page 18

19ORIENT-EXPRESS HOTELS LTD.

Khwai River Lodge• Gold List Condé Nast Traveler (U.S.)• 12th best safari camp Condé Nast Traveller (U.K.)

Savute Elephant Camp• 2nd Best Safari Camp in Botswana

Travel & Leisure (U.S.)

Le Manoir aux Quat’Saisons• Best British Hotel Condé Nast Traveler (U.S.)• Gold List Condé Nast Traveler (U.S.)• 2nd Best Country Hotel in Europe

Departures magazine (U.S.)• Gold Ribbon RAC (U.S.) • 3rd Best U.K. Leisure Hotel Condé Nast

Traveller (U.K.)• Retained two Michelin Stars for the 20th

consecutive year Michelin Guide

The Observatory Hotel• Gold List Condé Nast Traveler (U.S.)• Best Five Star Accommodation Hotel &

Accommodation Management magazine (Australia)• Best Overall Accommodation Property in Australia

Hotel & Accommodation Management magazine (Australia)

• Deluxe Hotel of the Year Australian Hotel Awards • 20th Best Australasia and South Pacific Overseas

Leisure Hotel Condé Nast Traveller (U.K.)• 11th Best Pacific Rim Hotel Condé Nast

Traveler (U.S.)• Australasia’s Leading Hotel World Travel Awards

Lilianfels Blue Mountains Resort & Spa• Best Boutique Hotel Hotel & Accommodation

Management magazine (Australia)• Best Regional Property Hotel & Accommodation

Management magazine (Australia)• Best Restaurant – Darley’s Australian Hotel Awards• 14th Best Overseas Leisure Hotel Australasia and

South Pacific Condé Nast Traveller (U.K.)• 14th Best Hotel in the Pacific Rim

Condé Nast Traveler (U.S.)

Corporate• Gold E Award of Excellence – James B.

Sherwood Entrée (U.S.) • Best Travel & Leisure Title – Orient-Express

Magazine APA Media Awards (U.K.)• James B. Sherwood awarded Hotel Design Award

(U.K.)• National Order of the Southern Cross –

James B. Sherwood Government of Brazil

Financial review

Contents

Report of independent registered public accounting firm 21

Consolidated balance sheets 22

Statements of consolidated operations 23

Statements of consolidated cash flows 24

Statements of consolidated shareholders’ equity 25

Notes to consolidated financial statements 26

Summary of quarterly earnings 40

Five-year performance 41

Price range of common shares 41

Summary of earnings by operating unit and region 42

Summary of operating information for owned hotels 43

Corporate governance 43

Shareholder and investor information 44

48818_p8_19.rev2 20/4/05 12:22 pm Page 19

20

This report contains, in addition to historical information, forward-looking statements that involve risks and uncertainties. These includestatements regarding earnings growth, investment plans and similarmatters that are not historical facts. These statements are based onmanagement’s current expectations and are subject to a number ofuncertainties and risks that could cause actual results to differmaterially from those described in the forward-looking statements.Factors that may cause a difference include, but are not limited to,those mentioned in the report, unknown effects on the travel andleisure markets of terrorist activity and any police or militaryresponse, varying customer demand and competitive considerations,realization of bookings and reservations as actual revenue, inability tosustain price increases or to reduce costs, fluctuations in interestrates and currency values, uncertainty of negotiating and completingproposed capital expenditures and acquisitions, adequate sources ofcapital and acceptability of finance terms, possible loss or amendmentof planning permits and delays in construction schedules forexpansion projects, shifting patterns of tourism and business traveland seasonality of demand, adverse local weather conditions,changing global and regional economic conditions, and legislative,regulatory and political developments. Further information regardingthese and other factors is included in the filings by the company andSea Containers Ltd. with the U.S. Securities and Exchange Commission.

48818_p20_44.qxd.rev2 19/4/05 3:10 pm Page 20

21ORIENT-EXPRESS HOTELS LTD.

Report of Independent Registered Public Accounting Firm

Board of Directors and Shareholders March 3, 2005Orient-Express Hotels Ltd.Hamilton, Bermuda

We have audited the accompanying consolidated balance sheets ofOrient-Express Hotels Ltd. and subsidiaries (the “Company”) as ofDecember 31, 2004 and 2003, and the related consolidated statementsof operations, shareholders’ equity, and cash flows for each of the threeyears in the period ended December 31, 2004. The consolidatedfinancial statements are the responsibility of the Company’smanagement. Our responsibility is to express an opinion on theseconsolidated financial statements based on our audits.

We conducted our audits in accordance with the standards of thePublic Company Accounting Oversight Board (United States). Thosestandards require that we plan and perform the audit to obtainreasonable assurance about whether the consolidated financialstatements are free of material misstatement. An audit includesexamining, on a test basis, evidence supporting the amounts anddisclosures in the consolidated financial statements. An audit alsoincludes assessing the accounting principles used and significantestimates made by management, as well as evaluating the overallfinancial statement presentation. We believe that our audits provide areasonable basis for our opinion.

In our opinion, such consolidated financial statements present fairly, inall material respects, the financial position of Orient-Express Hotels Ltd.

and subsidiaries as of December 31, 2004 and 2003, and the results oftheir operations and their cash flows for each of the three years in the period ended December 31, 2004, in conformity with accounting principles generally accepted in the United States of America.

We have also audited, in accordance with the standards of thePublic Company Accounting Oversight Board (United States), theeffectiveness of the Company’s internal control over financial reportingas of December 31, 2004, based on the criteria established in InternalControl – Integrated Framework issued by the Committee ofSponsoring Organizations of the Treadway Commission and our report(not presented herein) dated March 3, 2005 expressed an unqualifiedopinion on management’s assessment of the effectiveness of theCompany’s internal control over financial reporting and an unqualifiedopinion on the effectiveness of the Company’s internal control overfinancial reporting.

Deloitte & Touche LLPNew York, New York

48818_p20_44.qxd.rev2 20/4/05 10:22 am Page 21

22

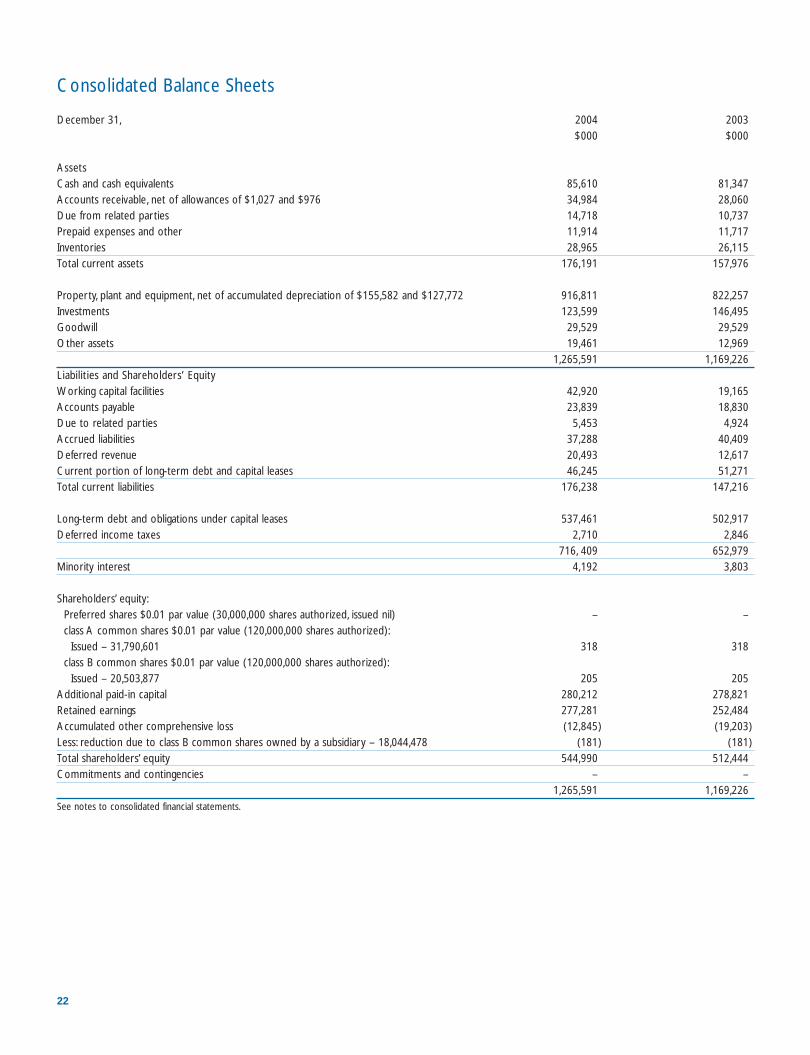

December 31,

AssetsCash and cash equivalentsAccounts receivable, net of allowances of $1,027 and $976Due from related partiesPrepaid expenses and otherInventoriesTotal current assets

Property, plant and equipment, net of accumulated depreciation of $155,582 and $127,772 InvestmentsGoodwillOther assets

Liabilities and Shareholders’ EquityWorking capital facilitiesAccounts payableDue to related parties Accrued liabilities Deferred revenueCurrent portion of long-term debt and capital leases Total current liabilities

Long-term debt and obligations under capital leasesDeferred income taxes

Minority interest

Shareholders’ equity:Preferred shares $0.01 par value (30,000,000 shares authorized, issued nil)class A common shares $0.01 par value (120,000,000 shares authorized):

Issued – 31,790,601class B common shares $0.01 par value (120,000,000 shares authorized):

Issued – 20,503,877Additional paid-in capitalRetained earningsAccumulated other comprehensive lossLess: reduction due to class B common shares owned by a subsidiary – 18,044,478Total shareholders’ equityCommitments and contingencies

See notes to consolidated financial statements.

2004$000

85,61034,98414,71811,91428,965

176,191

916,811123,59929,52919,461

1,265,591

42,92023,8395,453

37,28820,49346,245

176,238

537,4612,710

716, 4094,192

–

318

205280,212277,281(12,845)

(181)544,990

–1,265,591

2003$000

81,34728,06010,73711,71726,115

157,976

822,257146,49529,52912,969

1,169,226

19,16518,8304,924

40,40912,61751,271

147,216

502,9172,846

652,9793,803

–

318

205278,821252,484(19,203)

(181) 512,444

–1,169,226

Consolidated Balance Sheets

48818_OEX_FINANCIALS_p20.qxd 14/4/05 2:04 pm Page 22

23ORIENT-EXPRESS HOTELS LTD.

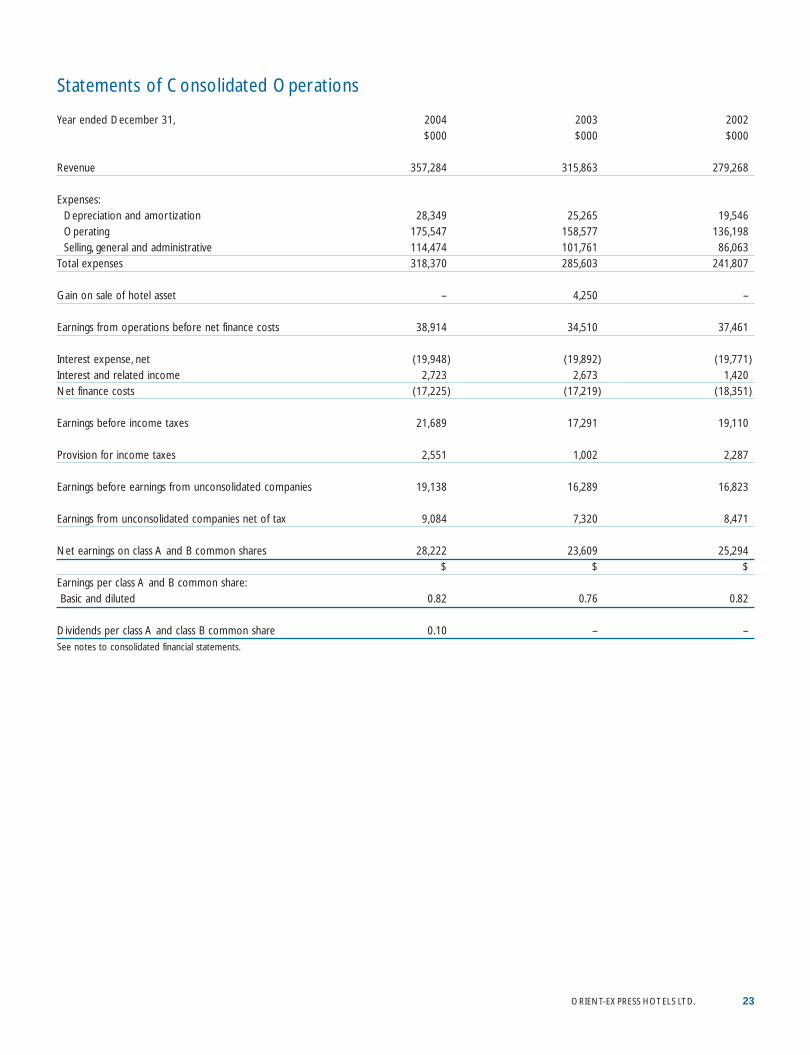

Year ended December 31,

Revenue

Expenses:Depreciation and amortizationOperatingSelling, general and administrative

Total expenses

Gain on sale of hotel asset

Earnings from operations before net finance costs

Interest expense, netInterest and related incomeNet finance costs

Earnings before income taxes

Provision for income taxes

Earnings before earnings from unconsolidated companies

Earnings from unconsolidated companies net of tax

Net earnings on class A and B common shares

Earnings per class A and B common share:Basic and diluted

Dividends per class A and class B common shareSee notes to consolidated financial statements.

2003$000

315,863

25,265158,577101,761285,603

4,250

34,510

(19,892)2,673

(17,219)

17,291

1,002

16,289

7,320

23,609$

0.76

–

2004$000

357,284

28,349175,547114,474318,370

–

38,914

(19,948)2,723

(17,225)

21,689

2,551

19,138

9,084

28,222$

0.82

0.10

2002$000

279,268

19,546136,19886,063

241,807

–

37,461

(19,771)1,420

(18,351)

19,110

2,287

16,823

8,471

25,294$

0.82

–

Statements of Consolidated Operations

48818_p20_44.qxd.rev2 20/4/05 10:23 am Page 23

24

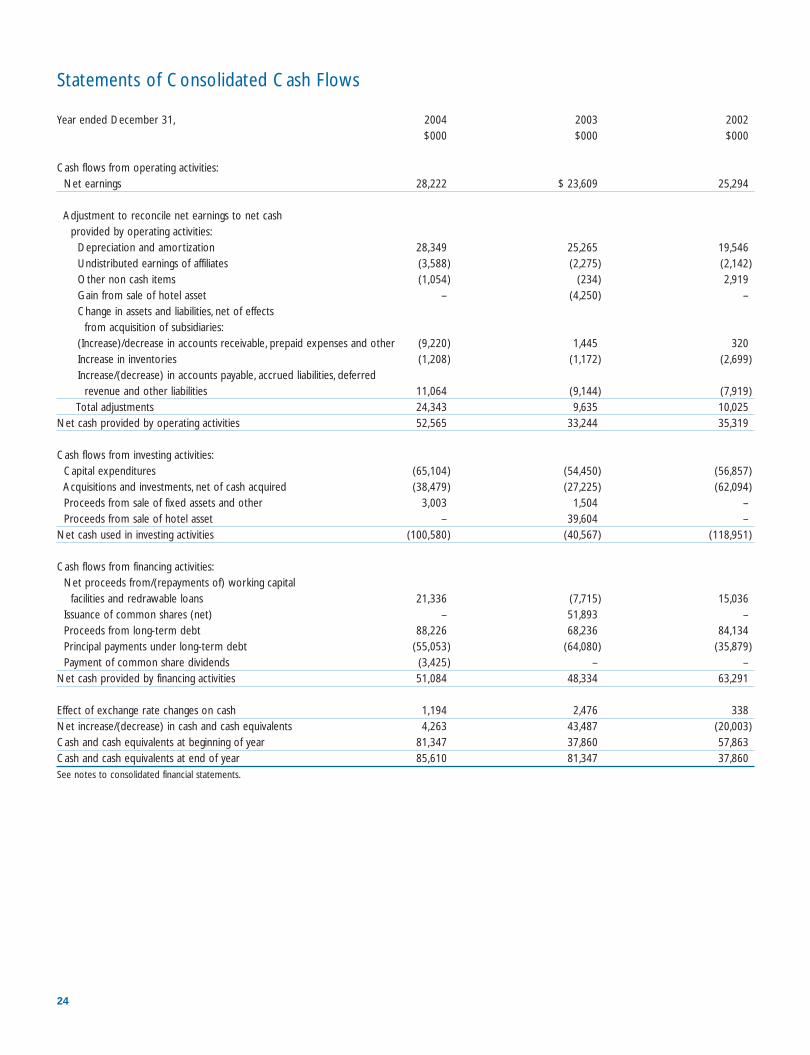

Year ended December 31,

Cash flows from operating activities:Net earnings

Adjustment to reconcile net earnings to net cash provided by operating activities:

Depreciation and amortizationUndistributed earnings of affiliatesOther non cash itemsGain from sale of hotel assetChange in assets and liabilities, net of effects

from acquisition of subsidiaries:(Increase)/decrease in accounts receivable, prepaid expenses and other Increase in inventories Increase/(decrease) in accounts payable, accrued liabilities, deferred

revenue and other liabilitiesTotal adjustments

Net cash provided by operating activities

Cash flows from investing activities:Capital expendituresAcquisitions and investments, net of cash acquiredProceeds from sale of fixed assets and otherProceeds from sale of hotel asset

Net cash used in investing activities

Cash flows from financing activities:Net proceeds from/(repayments of) working capital

facilities and redrawable loansIssuance of common shares (net)Proceeds from long-term debtPrincipal payments under long-term debtPayment of common share dividends

Net cash provided by financing activities

Effect of exchange rate changes on cashNet increase/(decrease) in cash and cash equivalentsCash and cash equivalents at beginning of yearCash and cash equivalents at end of yearSee notes to consolidated financial statements.

2003$000

$ 23,609

25,265(2,275)

(234)(4,250)

1,445 (1,172)

(9,144)9,635

33,244

(54,450)(27,225)

1,50439,604

(40,567)

(7,715)51,89368,236

(64,080)–

48,334

2,47643,48737,86081,347

2004$000

28,222

28,349(3,588)(1,054)

–

(9,220)(1,208)

11,06424,34352,565

(65,104)(38,479)

3,003–

(100,580)

21,336–

88,226(55,053)(3,425)51,084

1,1944,263

81,34785,610

2002$000

25,294

19,546(2,142)2,919

–

320(2,699)

(7,919) 10,02535,319

(56,857)(62,094)

––

(118,951)

15,036–

84,134(35,879)

–63,291

338(20,003)57,86337,860

Statements of Consolidated Cash Flows

48818_OEX_FINANCIALS_p20.qxd 14/4/05 2:05 pm Page 24

25ORIENT-EXPRESS HOTELS LTD.

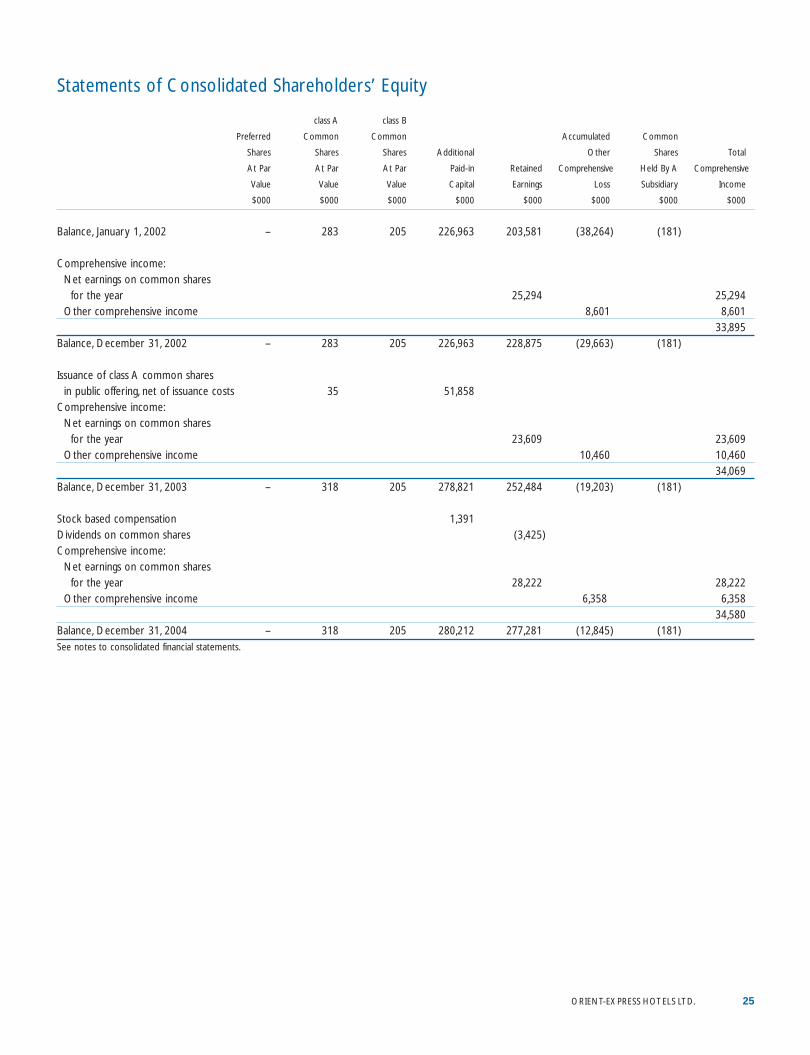

Balance, January 1, 2002

Comprehensive income:Net earnings on common shares

for the yearOther comprehensive income

Balance, December 31, 2002

Issuance of class A common shares in public offering, net of issuance costs

Comprehensive income:Net earnings on common shares

for the yearOther comprehensive income

Balance, December 31, 2003

Stock based compensationDividends on common sharesComprehensive income:

Net earnings on common shares for the year

Other comprehensive income

Balance, December 31, 2004See notes to consolidated financial statements.

Total

Comprehensive

Income

$000

25,294 8,601

33,895

23,60910,46034,069

28,222 6,358

34,580

Common

Shares

Held By A

Subsidiary

$000

(181)

(181)

(181)

(181)

Accumulated

Other

Comprehensive

Loss

$000

(38,264)

8,601

(29,663)

10,460

(19,203)

6,358

(12,845)

Retained

Earnings

$000

203,581

25,294

228,875

23,609

252,484

(3,425)

28,222

277,281

Additional

Paid-in

Capital

$000

226,963

226,963

51,858

278,821

1,391

280,212

class B

Common

Shares

At Par

Value

$000

205

205

205

205

class A

Common

Shares

At Par

Value

$000

283

283

35

318

318

Statements of Consolidated Shareholders’ Equity

Preferred

Shares

At Par

Value

$000

–

–

–

–

48818_p20_44.qxd.rev2 20/4/05 10:23 am Page 25

26

Notes to Consolidated Financial Statements

1. Summary of significant accounting policies and basis of presentation

(a) BusinessIn this report Orient-Express Hotels Ltd. is referred to as the“Company”, and the Company and its subsidiaries are referred tocollectively as “OEH”. At December 31, 2004, Sea Containers Ltd., aBermuda company (“SCL”), owned 42% of the equity shares in theCompany.

At December 31, 2004, OEH owned or invested in 37 de luxe hotelsand resorts located in the United States, Caribbean, Europe, southernAfrica, South America, Southeast Asia, Australia and South Pacific, threerestaurants in London, New York and Buenos Aires, six tourist trains inEurope, Southeast Asia and Peru, and a river cruiseship in Burma andfive canal boats in France. See Note 17 regarding the purchase of anadditional hotel in February 2005.(b) Basis of presentationThe accompanying consolidated financial statements reflect the resultsof operations, financial position and cash flows of the Company and allits majority-owned subsidiaries. The consolidated financial statementshave been prepared using the historical basis in the assets and liabilitiesand the historical results of operations directly attributable to OEH,and all intercompany accounts and transactions between the Companyand its subsidiaries have been eliminated. Unconsolidated companiesthat are 20% to 50% owned are accounted for on an equity basis.

Cash and cash equivalents include all cash balances and highly-liquidinvestments having original maturities of three months or less.

The consolidated financial statements include an allocation of certaingeneral corporate administrative expenses from SCL which are providedunder a shared services agreement with SCL. In the opinion ofmanagement, general corporate administrative expenses have beenallocated to OEH on a reasonable and consistent basis usingmanagement's estimate of services provided by SCL. However, suchallocations are not necessarily indicative of the level of expenses whichmight have been incurred had OEH not been operating under a sharedservices agreement during the periods presented. Therefore, the financialinformation included herein may not necessarily reflect the consolidatedresults of operations, financial position and cash flows of OEH hadOEH been a separate stand alone entity for the years presented.

Certain items in 2003 and 2002 have been reclassified to conform tothe current year's presentation.

“FASB” means Financial Accounting Standards Board and “APB”means Accounting Principles Board, the FASB’s predecessor. “SFAS”means Statement of Financial Accounting Standards of the FASB, and“FIN” means an accounting interpretation of the FASB.(c) Foreign currency translationThe functional currency for each of the Company’s foreign subsidiariesis the applicable local currency. Foreign subsidiary income andexpenses are translated into U.S. dollars, the reporting currency of theCompany, at the average rates of exchange prevailing during the year.The assets and liabilities are translated into U.S. dollars at the rates ofexchange on the balance sheet date and the related translationadjustments are included in accumulated other comprehensiveincome/(loss). No income taxes are provided on the translation

adjustments as management does not expect that such gains or losseswill be realized. Foreign currency transaction gains and losses arerecognized in operations as they occur.(d) EstimatesThe preparation of financial statements in conformity with accountingprinciples generally accepted in the United States of America requiresmanagement to make estimates and assumptions that affect thereported amounts of assets and liabilities and the disclosure ofcontingent assets and liabilities at the date of the financial statementsand the reported amounts of revenues and expenses during thereporting period. Estimates include, among others, the allowance fordoubtful accounts, depreciation and amortization, carrying value ofassets including intangible assets, employee benefits, taxes andcontingencies. Actual results may differ from those estimates.(e) Stock-based compensationSFAS No. 123, “Accounting for Stock Based Compensation”, asamended by SFAS No. 148, “Accounting for Stock-BasedCompensation – Transition and Disclosure – An Amendment of FASBStatement No. 123”, encourages but does not require companies torecord compensation cost for stock based employee compensationplans at fair value. The Company has chosen to account for stockbased compensation using the intrinsic value method prescribed in APBOpinion No. 25, “Accounting for Stock Issued to Employees”, asamended, and related interpretations.(f) Revenue recognitionHotel and restaurant revenues are recognized when the rooms areoccupied and the services are performed. Tourist train and cruiserevenues are recognized upon commencement of the journey.Deferred revenue consisting of deposits paid in advance is recognizedas revenue when the services are performed for hotels and restaurantsand upon commencement of tourist train and cruise journeys.Revenues under management contracts are recognized based upon theattainment of certain financial results, primarily revenue and operatingearnings, in each contract as defined.(g) Earnings from unconsolidated companiesEarnings from unconsolidated companies include OEH’s share of thenet earnings of its equity investments as well as interest income relatedto loans and advances to the equity investees amounting to $8,165,000in 2004 (2003 – $7,080,000, 2002 – $7,892,000).(h) Marketing costsMarketing costs are expensed as incurred and are reported in selling,general and administrative expenses. Marketing costs include costs ofadvertising and other marketing activities. These costs were$26,780,000 in 2004 (2003 – $24,783,000, 2002 – $20,091,000).(i) Interest expense, netOEH capitalizes interest during the construction of assets. Interestexpense, net excludes interest which has been capitalized in theamount of $1,708,000 in 2004 (2003 – $1,795,000, 2002 –$1,271,000).(j) Interest and related incomeInterest and related income consists entirely of foreign currencyexchange transaction gains of $2,723,000 in 2004 (2003 – $2,673,000,2002 – $1,420,000).(k) Income taxesDeferred income taxes result from temporary differences between thefinancial reporting and tax bases of assets and liabilities. Deferred taxesare recorded at enacted statutory rates and are adjusted as enacted

48818_p20_44.qxd.rev2 19/4/05 3:03 pm Page 26

27ORIENT-EXPRESS HOTELS LTD.

rates change. Classification of deferred tax assets and liabilitiescorresponds with the classification of the underlying assets and liabilitiesgiving rise to the temporary differences or the period of expectedreversal, as applicable. A valuation allowance is established, whennecessary, to reduce deferred tax assets to the amount that is morelikely than not to be realized based on available evidence.(l) Earnings per shareBasic earnings per share exclude dilution and are computed by dividingnet earnings available to common shareholders by the weightedaverage number of class A and B common shares outstanding for theperiod. The number of shares used in computing basic earnings pershare was 34,250,000 for the year ended December 31, 2004 (2003 –31,139,000, 2002 – 30,800,000). The number of shares used incomputing diluted earnings per share was 34,367,000 for the yearended December 31, 2004 (2003 – 31,152,000, 2002 – 30,858,000).

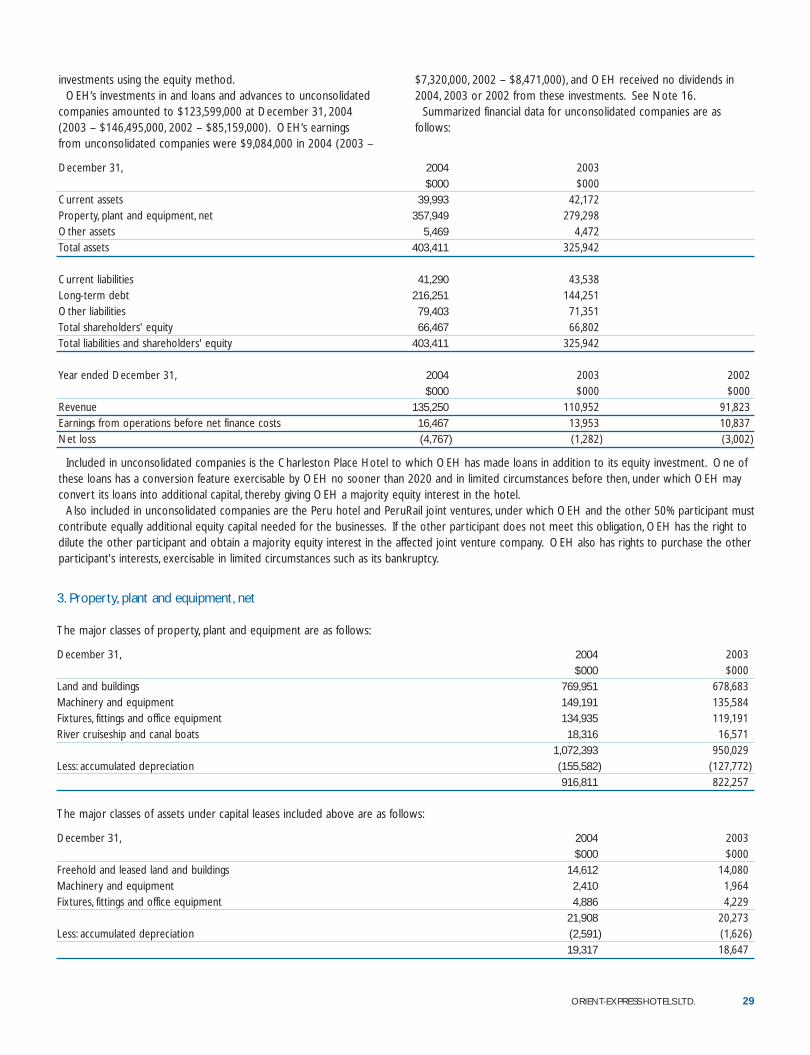

The following table is a reconciliation of the net earnings and pershare amounts used in the calculation of basic earnings per share anddiluted earnings per share: