Embed Size (px)

Citation preview

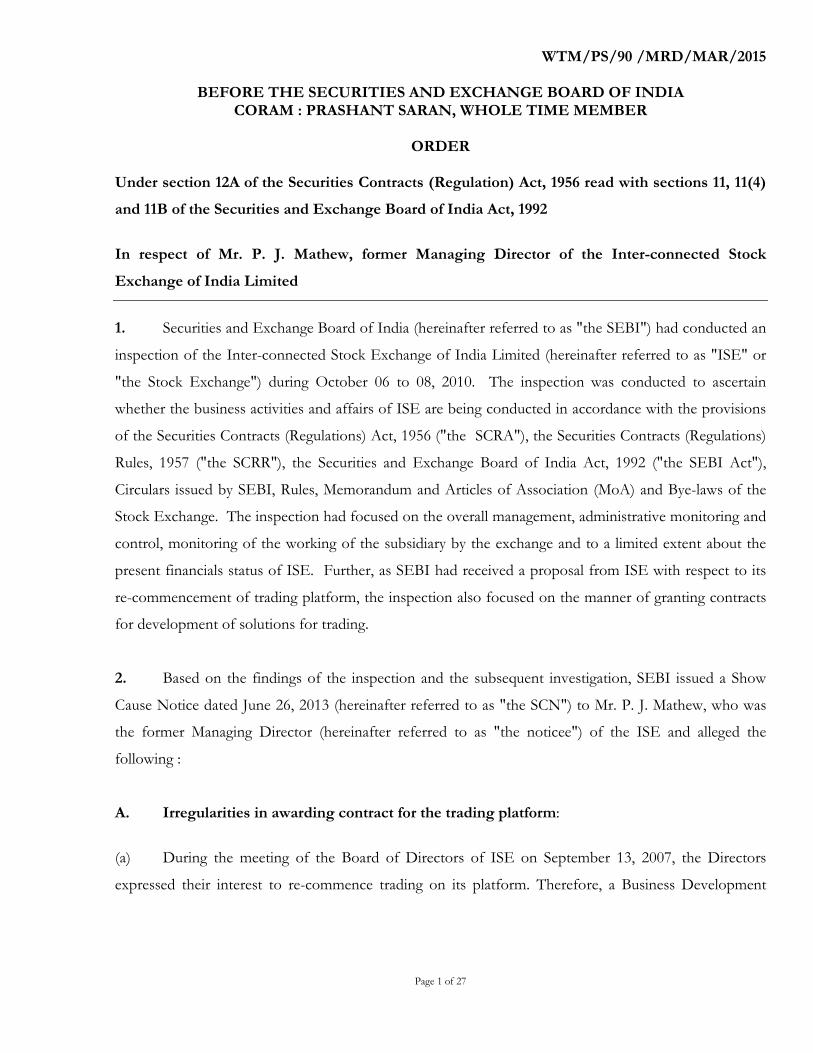

Page 1 of 27

WTM/PS/90 /MRD/MAR/2015

BEFORE THE SECURITIES AND EXCHANGE BOARD OF INDIA CORAM : PRASHANT SARAN, WHOLE TIME MEMBER

ORDER

Under section 12A of the Securities Contracts (Regulation) Act, 1956 read with sections 11, 11(4)

and 11B of the Securities and Exchange Board of India Act, 1992

In respect of Mr. P. J. Mathew, former Managing Director of the Inter-connected Stock

Exchange of India Limited

1. Securities and Exchange Board of India (hereinafter referred to as "the SEBI") had conducted an

inspection of the Inter-connected Stock Exchange of India Limited (hereinafter referred to as "ISE" or

"the Stock Exchange") during October 06 to 08, 2010. The inspection was conducted to ascertain

whether the business activities and affairs of ISE are being conducted in accordance with the provisions

of the Securities Contracts (Regulations) Act, 1956 ("the SCRA"), the Securities Contracts (Regulations)

Rules, 1957 ("the SCRR"), the Securities and Exchange Board of India Act, 1992 ("the SEBI Act"),

Circulars issued by SEBI, Rules, Memorandum and Articles of Association (MoA) and Bye-laws of the

Stock Exchange. The inspection had focused on the overall management, administrative monitoring and

control, monitoring of the working of the subsidiary by the exchange and to a limited extent about the

present financials status of ISE. Further, as SEBI had received a proposal from ISE with respect to its

re-commencement of trading platform, the inspection also focused on the manner of granting contracts

for development of solutions for trading.

2. Based on the findings of the inspection and the subsequent investigation, SEBI issued a Show

Cause Notice dated June 26, 2013 (hereinafter referred to as "the SCN") to Mr. P. J. Mathew, who was

the former Managing Director (hereinafter referred to as "the noticee") of the ISE and alleged the

following :

A. Irregularities in awarding contract for the trading platform:

(a) During the meeting of the Board of Directors of ISE on September 13, 2007, the Directors

expressed their interest to re-commence trading on its platform. Therefore, a Business Development

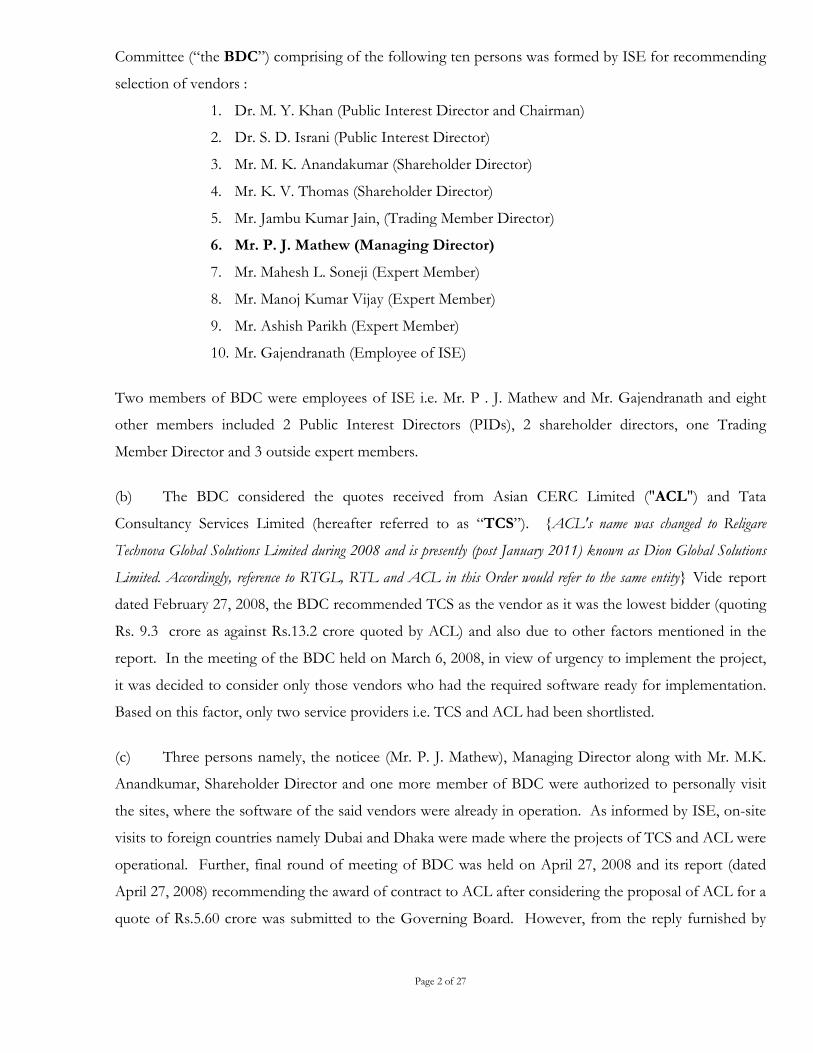

Page 2 of 27

Committee (“the BDC”) comprising of the following ten persons was formed by ISE for recommending

selection of vendors :

1. Dr. M. Y. Khan (Public Interest Director and Chairman)

2. Dr. S. D. Israni (Public Interest Director)

3. Mr. M. K. Anandakumar (Shareholder Director)

4. Mr. K. V. Thomas (Shareholder Director)

5. Mr. Jambu Kumar Jain, (Trading Member Director)

6. Mr. P. J. Mathew (Managing Director)

7. Mr. Mahesh L. Soneji (Expert Member)

8. Mr. Manoj Kumar Vijay (Expert Member)

9. Mr. Ashish Parikh (Expert Member)

10. Mr. Gajendranath (Employee of ISE)

Two members of BDC were employees of ISE i.e. Mr. P . J. Mathew and Mr. Gajendranath and eight

other members included 2 Public Interest Directors (PIDs), 2 shareholder directors, one Trading

Member Director and 3 outside expert members.

(b) The BDC considered the quotes received from Asian CERC Limited ("ACL") and Tata

Consultancy Services Limited (hereafter referred to as “TCS”). {ACL's name was changed to Religare

Technova Global Solutions Limited during 2008 and is presently (post January 2011) known as Dion Global Solutions

Limited. Accordingly, reference to RTGL, RTL and ACL in this Order would refer to the same entity} Vide report

dated February 27, 2008, the BDC recommended TCS as the vendor as it was the lowest bidder (quoting

Rs. 9.3 crore as against Rs.13.2 crore quoted by ACL) and also due to other factors mentioned in the

report. In the meeting of the BDC held on March 6, 2008, in view of urgency to implement the project,

it was decided to consider only those vendors who had the required software ready for implementation.

Based on this factor, only two service providers i.e. TCS and ACL had been shortlisted.

(c) Three persons namely, the noticee (Mr. P. J. Mathew), Managing Director along with Mr. M.K.

Anandkumar, Shareholder Director and one more member of BDC were authorized to personally visit

the sites, where the software of the said vendors were already in operation. As informed by ISE, on-site

visits to foreign countries namely Dubai and Dhaka were made where the projects of TCS and ACL were

operational. Further, final round of meeting of BDC was held on April 27, 2008 and its report (dated

April 27, 2008) recommending the award of contract to ACL after considering the proposal of ACL for a

quote of Rs.5.60 crore was submitted to the Governing Board. However, from the reply furnished by

Page 3 of 27

ISE (to the SCN issued to it) to SEBI, it was observed that ACL submitted a revised quote only on April

28, 2008 i.e. after the meeting of BDC recommending the name of ACL to the Governing Board. As

regards the revised quotes from TCS (the other bidder), the noticee informed SEBI that TCS was not

interested in revising of quote, though no documentary support to that effect had been furnished.

(d) Further it was noted that the BDC report was not signed by Dr. M. Y. Khan, a Public Interest

Director and Chairman of the Committee, as well as four other members namely Dr. S. D. Israni (Public

Interest Director), Mr. Mahesh L. Soneji (Expert Member), Mr. Manoj Kumar Vijay (Expert Member),

and Mr. Ashish Parikh (Expert Member), out of a total of eight members. Thus, a total of five out of

eight members, excluding Exchange employees, had not signed the report and there was no mention of

absence/dissent note in the report. The three members who signed the report are Shareholder Directors

and Trading Member Directors of ISE.

(e) In view of the same, it was alleged that the BDC report itself was questionable, irrespective of its

recommendations. It was alleged that the noticee, being the Managing Director of ISE and also a

member of the BDC committee and being part of the group which had visited Dubai and Dhaka to

ensure that the software of ACL and TCS are ready for use, had failed to ensure that a democratic/fair

approach of vendor selection was carried out.

(f) It was noticed that an agreement was signed between ISE and ACL known as Master Service

Agreement ('MSA'). The MSA between ISE and ACL mentions about "receipt of third party software

license agreement” by ISE from ACL. The third party software license agreement had been defined as

agreement between ACL and Cambridge Solutions Limited ("Cambridge"). On perusal of the MSA, it

was noted that ACL’s proprietary software was allegedly not enough for ISE’s trading platform but was

principally dependent on a software which ACL was to license/procure from Cambridge. This third

party software was an important part of product being slated to be delivered by ACL. This was a major

factor for determining the eligibility of ACL for award of contract. Owing to the fact that it was a third

party software, it is alleged that there is an added layer of interaction slowing down the whole process

because the ACL software architects would have to get in touch with Cambridge software architects for

the same. Contrary to the initial directions of BDC of awarding the contract to the entity which had the

required software ready for implementation, ISE had signed an agreement with ACL, knowing that ACL

did not have the software and was procuring the same from Cambridge.

Page 4 of 27

(g) It was therefore alleged that noticee was fully aware of the third party software license agreement

at the time of award of the contract to ACL and that it appeared to have been deliberately covered

up/ignored while listing out the relative strengths of the vendors by BDC/Board. It was also alleged that

the noticee failed to perceive that ACL was practically behaving as a re-seller of third party software

instead of a software provider.

(h) The SCN also stated that the vendor (ACL) selected by the BDC could not deliver and that

resulted in loss of money (i.e. payment to lawyers (to the tune of Rs. 17 lakhs) to recover Rs. 50 lakhs

from ACL) and loss of time. In addition, given the fact that Cambridge actually owned the software that

ACL bagged the order for, and also given the fact that the order was to be given to an entity with the

software ready for installation, and that ACL did not own the software ready for installation, it was

alleged that the BDC should not have placed the order with ACL at all. Further, Cambridge (from whom

ACL was buying the order) could have been given the opportunity to bid.

In view of the above, the SCN alleged that the noticee being the Managing Director (during the relevant

period) of ISE, a member of the BDC committee and being part of the group who visited Dubai and

Dhaka to ensure that the software of TCS and ACL are ready for use as directed by BDC, had failed to

ensure the fair manner of vendor selection, which resulted in the selection of wrong vendor and

substantial loss to ISE.

B. Failure to ensure compliance with the Securities Contracts (Regulation) (Manner of

Increasing and Maintaining Public Shareholding in Recognized Stock Exchanges) Regulations,

2006 ("the MIMPS Regulations"):

a. In order to ensure, amongst others, a greater transparency in dealings, accountability, market

discipline, to remove conflicts of interests, to have a balanced approach, to take into account the

interests of other players, to equip an exchange to face and withstand competition etc, which would

not otherwise be available in a mutualised stock exchange, SEBI vide Circular ref. no.

Cir.No.SMD/Policy/Cir-3/03 dated January 30, 2003, had introduced the scheme of

corporatization and demutualization for stock exchanges and fixed a time frame for switch over to

the said scheme.

b. In order to ensure that the stock exchanges demutualise themselves in true spirit and purpose,

SEBI had also prescribed the manner in which minimum public share holding should be increased

/ maintained in stock exchanges. The MIMPS Regulations were formulated by SEBI to provide for

Page 5 of 27

the manner in which stock exchanges would have to restructure their capital following a scheme of

corporatization and demutualization. Further regulation 11 of the said Regulations obligates the

Stock exchange to ensure that its shareholders comply with regulations 8 and 9 of the MIMPS

Regulations.

c. During the course of inspection, it was observed that in disregard of the aforesaid provisions, one

of the shareholders of the ISE, namely, Religare Technova Limited ("RTL") was holding more than

21% of the equity holding of the Exchange, directly and through persons acting in concert.

d. SEBI vide letter dated September 21, 2005 advised ISE that Public Interest Directors (hereafter

referred to as “PIDs”) would be selected by the Board of Directors of the Exchange from SEBI

constituted panel of PIDs and that the same shall be suitably incorporated in Articles, Rules of ISE.

Further, based on a clarification sought by ISE, SEBI vide letter no.

MRD/DSA/C&D/SL/143463/08 dated November 06, 2008 advised ISE to suitably amend clause

1.3.5 wherein the word ‘elected’ shall be replaced with the word ‘selected’.

e. In this regard, in the meeting of the Board of ISE held on November 20, 2009 it was decided to

call for polling by representatives of Religare Group and Chairman of the Board Mr. K. Rajendran

Nair accepted the same.

f. The decision to allow polling on the matter of appointment of PIDs wherein it was said that the

PIDs would be selected by the Board of directors of the Exchange from a panel constituted by

SEBI was in complete defiance to the above directives / letters of SEBI.

g. Further, on perusal of the minutes of EGM of the Exchange held on November 20, 2009 it was

observed that four individuals, namely, Mr. Kiran Vaidya, Mr. Ravi Batra and Mr. Kapil Sanghvi,

& Ms. Shruti Gupta had represented several corporate shareholders of the Exchange and had voted

in the meeting. Each of these individuals (except Ms. Shruti Gupta and Mr. Kapil Sanghvi who

represented one shareholder) had represented two or more of such shareholders simultaneously in

the said meeting. Details of the same is as follows:

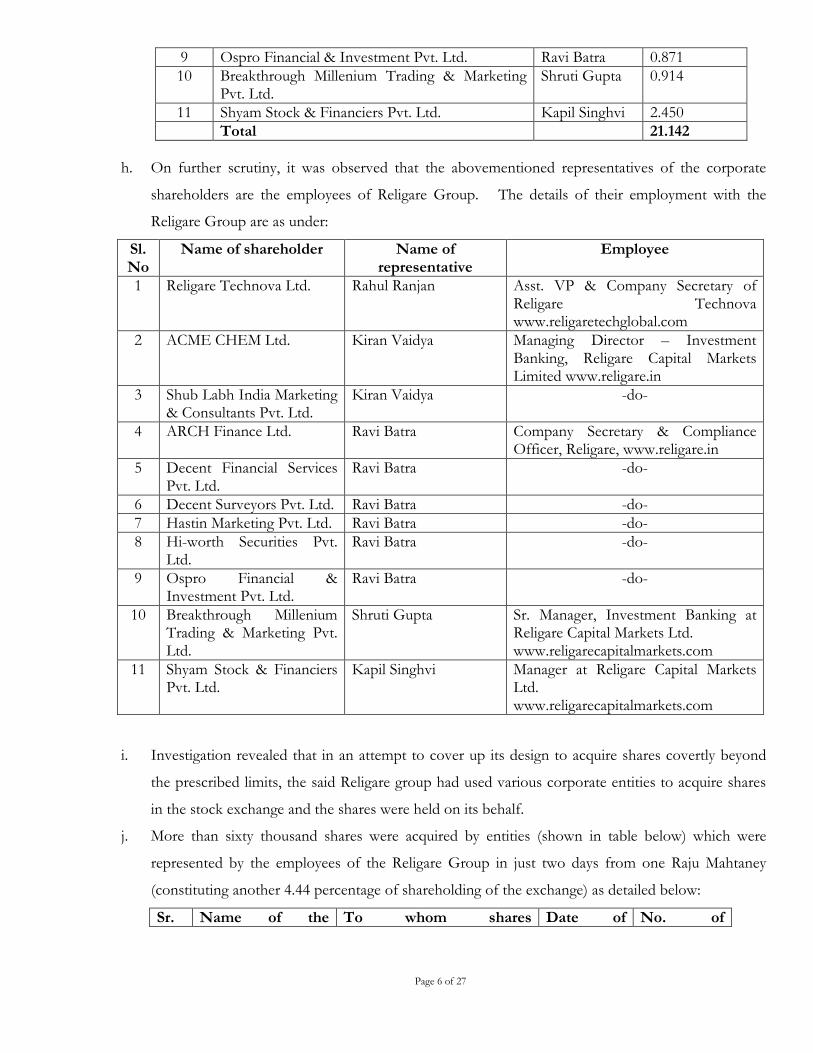

Sl.No. Name of shareholder Name of representative

Shareholding (%) in ISE

1 Religare Technova Ltd. Rahul Ranjan 4.440 2 ACME CHEM Ltd. Kiran Vaidya 4.458 3 Shub Labh India Marketing & Consultants Pvt.

Ltd. Kiran Vaidya 1.763

4 ARCH Finance Ltd. Ravi Batra 2.675 5 Decent Financial Services Pvt. Ltd. Ravi Batra 0.964 6 Decent Surveyors Pvt. Ltd. Ravi Batra 0.857 7 Hastin Marketing Pvt. Ltd. Ravi Batra 0.929 8 Hi-worth Securities Pvt. Ltd. Ravi Batra 0.821

Page 6 of 27

9 Ospro Financial & Investment Pvt. Ltd. Ravi Batra 0.871 10 Breakthrough Millenium Trading & Marketing

Pvt. Ltd. Shruti Gupta 0.914

11 Shyam Stock & Financiers Pvt. Ltd. Kapil Singhvi 2.450 Total 21.142

h. On further scrutiny, it was observed that the abovementioned representatives of the corporate

shareholders are the employees of Religare Group. The details of their employment with the

Religare Group are as under:

Sl. No

Name of shareholder Name of representative

Employee

1 Religare Technova Ltd. Rahul Ranjan Asst. VP & Company Secretary of Religare Technova www.religaretechglobal.com

2 ACME CHEM Ltd. Kiran Vaidya Managing Director – Investment Banking, Religare Capital Markets Limited www.religare.in

3 Shub Labh India Marketing & Consultants Pvt. Ltd.

Kiran Vaidya -do-

4 ARCH Finance Ltd. Ravi Batra

Company Secretary & Compliance Officer, Religare, www.religare.in

5 Decent Financial Services Pvt. Ltd.

Ravi Batra -do-

6 Decent Surveyors Pvt. Ltd. Ravi Batra -do- 7 Hastin Marketing Pvt. Ltd. Ravi Batra -do- 8 Hi-worth Securities Pvt.

Ltd. Ravi Batra -do-

9 Ospro Financial & Investment Pvt. Ltd.

Ravi Batra -do-

10 Breakthrough Millenium Trading & Marketing Pvt. Ltd.

Shruti Gupta Sr. Manager, Investment Banking at Religare Capital Markets Ltd. www.religarecapitalmarkets.com

11 Shyam Stock & Financiers Pvt. Ltd.

Kapil Singhvi Manager at Religare Capital Markets Ltd. www.religarecapitalmarkets.com

i. Investigation revealed that in an attempt to cover up its design to acquire shares covertly beyond

the prescribed limits, the said Religare group had used various corporate entities to acquire shares

in the stock exchange and the shares were held on its behalf.

j. More than sixty thousand shares were acquired by entities (shown in table below) which were

represented by the employees of the Religare Group in just two days from one Raju Mahtaney

(constituting another 4.44 percentage of shareholding of the exchange) as detailed below:

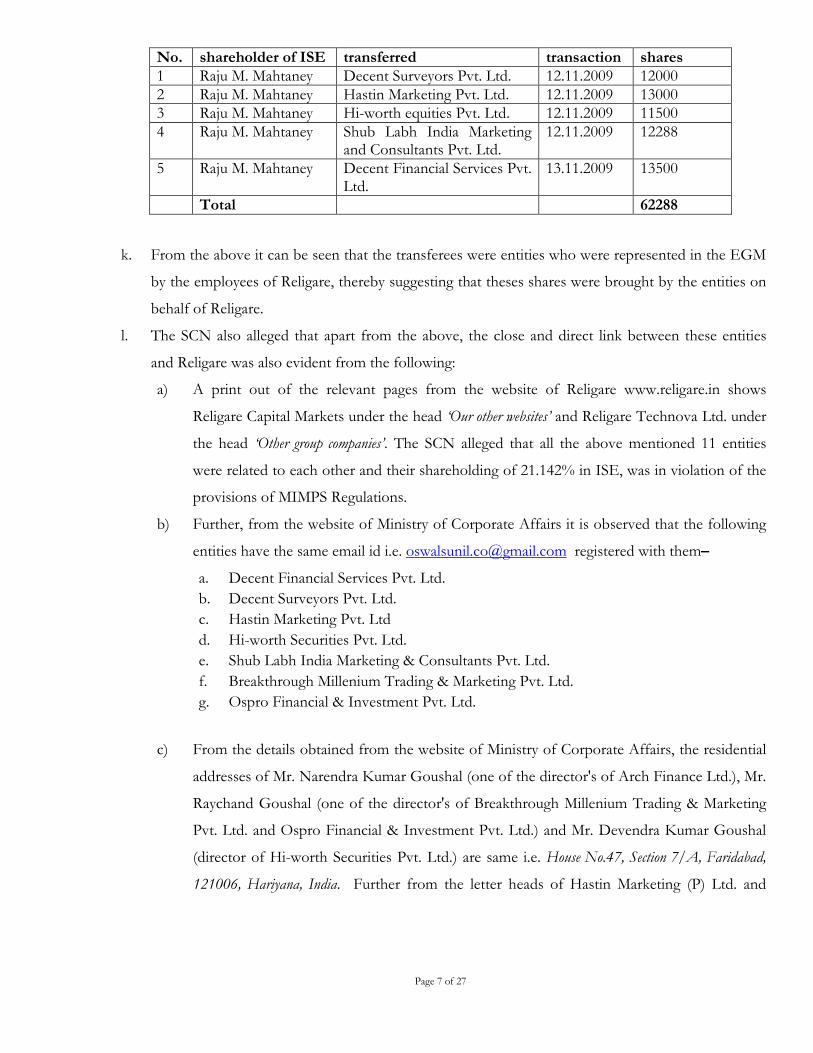

Sr. Name of the To whom shares Date of No. of

Page 7 of 27

No. shareholder of ISE transferred transaction shares 1 Raju M. Mahtaney Decent Surveyors Pvt. Ltd. 12.11.2009 12000 2 Raju M. Mahtaney Hastin Marketing Pvt. Ltd. 12.11.2009 13000 3 Raju M. Mahtaney Hi-worth equities Pvt. Ltd. 12.11.2009 11500 4 Raju M. Mahtaney Shub Labh India Marketing

and Consultants Pvt. Ltd. 12.11.2009 12288

5 Raju M. Mahtaney Decent Financial Services Pvt. Ltd.

13.11.2009 13500

Total 62288

k. From the above it can be seen that the transferees were entities who were represented in the EGM

by the employees of Religare, thereby suggesting that theses shares were brought by the entities on

behalf of Religare.

l. The SCN also alleged that apart from the above, the close and direct link between these entities

and Religare was also evident from the following:

a) A print out of the relevant pages from the website of Religare www.religare.in shows

Religare Capital Markets under the head ‘Our other websites’ and Religare Technova Ltd. under

the head ‘Other group companies’. The SCN alleged that all the above mentioned 11 entities

were related to each other and their shareholding of 21.142% in ISE, was in violation of the

provisions of MIMPS Regulations.

b) Further, from the website of Ministry of Corporate Affairs it is observed that the following

entities have the same email id i.e. [email protected] registered with them–

a. Decent Financial Services Pvt. Ltd.

b. Decent Surveyors Pvt. Ltd.

c. Hastin Marketing Pvt. Ltd

d. Hi-worth Securities Pvt. Ltd.

e. Shub Labh India Marketing & Consultants Pvt. Ltd.

f. Breakthrough Millenium Trading & Marketing Pvt. Ltd.

g. Ospro Financial & Investment Pvt. Ltd.

c) From the details obtained from the website of Ministry of Corporate Affairs, the residential

addresses of Mr. Narendra Kumar Goushal (one of the director's of Arch Finance Ltd.), Mr.

Raychand Goushal (one of the director's of Breakthrough Millenium Trading & Marketing

Pvt. Ltd. and Ospro Financial & Investment Pvt. Ltd.) and Mr. Devendra Kumar Goushal

(director of Hi-worth Securities Pvt. Ltd.) are same i.e. House No.47, Section 7/A, Faridabad,

121006, Hariyana, India. Further from the letter heads of Hastin Marketing (P) Ltd. and

Page 8 of 27

Decent Surveyors (P) Ltd., it was observed that they have offices at 81, Daryaganj, Second

Floor, New Delhi.

m. Regulation 11 of the MIMPS Regulations casts an obligation on the stock exchange to ensure that

its shareholding is in compliance with Regulations 8 and 9 of the Regulations which prescribe

ownership restrictions of 5 % on any entity read with regulation 52 of the SECC Regulations, 2012.

ISE was continuously filing undertakings (as required under Regulation 11 of the MIMPS regulations)

that it is in compliance with the prescribed norms. In view of the above, it was alleged that the

declarations filed in this regard are incorrect and have been falsely filed over a long period of time. As

the Religare group along with its PACs controls / holds a substantial shareholding (i.e. 21.142%) it

is alleged that the ISE did not ensure compliance with the MIMPS Regulations.

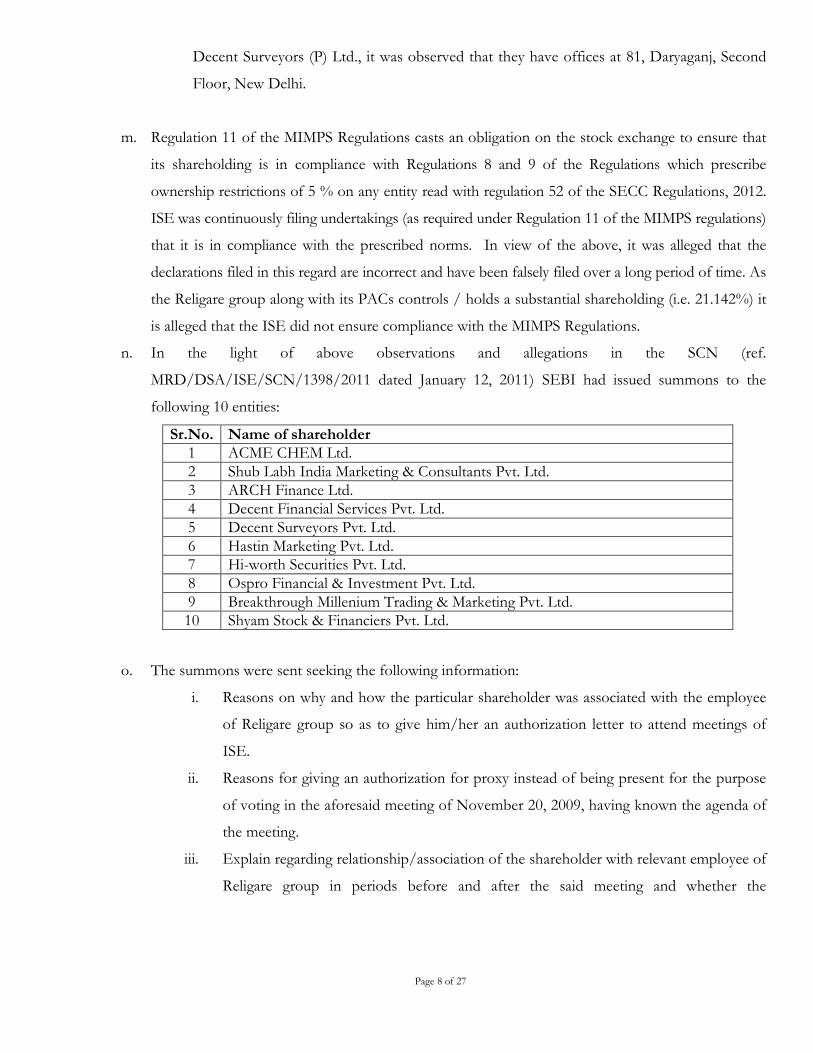

n. In the light of above observations and allegations in the SCN (ref.

MRD/DSA/ISE/SCN/1398/2011 dated January 12, 2011) SEBI had issued summons to the

following 10 entities:

Sr.No. Name of shareholder 1 ACME CHEM Ltd. 2 Shub Labh India Marketing & Consultants Pvt. Ltd. 3 ARCH Finance Ltd. 4 Decent Financial Services Pvt. Ltd. 5 Decent Surveyors Pvt. Ltd. 6 Hastin Marketing Pvt. Ltd. 7 Hi-worth Securities Pvt. Ltd. 8 Ospro Financial & Investment Pvt. Ltd. 9 Breakthrough Millenium Trading & Marketing Pvt. Ltd. 10 Shyam Stock & Financiers Pvt. Ltd.

o. The summons were sent seeking the following information:

i. Reasons on why and how the particular shareholder was associated with the employee

of Religare group so as to give him/her an authorization letter to attend meetings of

ISE.

ii. Reasons for giving an authorization for proxy instead of being present for the purpose

of voting in the aforesaid meeting of November 20, 2009, having known the agenda of

the meeting.

iii. Explain regarding relationship/association of the shareholder with relevant employee of

Religare group in periods before and after the said meeting and whether the

Page 9 of 27

shareholder had given clear indication about views in favour of or against the agenda in

the aforementioned meeting.

iv. Rationale for giving proxy to employee of Religare group, especially given the fact that

Religare Technova Ltd., a Religare group company held 4.44% of ISE at the time of the

aforementioned meeting.

p. Out of the aforementioned ten shareholders except for Hi-worth Securities Pvt. Ltd., all the other

nine shareholders made similar submissions, as below:

i. The shareholders were original allottees and had bought shares in ISE assuming that

the investment would generate significant value over a period of time.

ii. Arch Finance limited in its letter dated 15th October 2009 drew attention of other

shareholders to the state of affairs at ISE raising several issues including a) some queries

related to accounting and financials b) ISE is making operational losses c) advertising

and publicity costs are incurred while ISE makes losses d) managerial remuneration has

increased from FY 08 to FY 09 in the time of economic slowdown e) investments

made at huge losses f)advances given to subsidiary companies g) delay in paying service

tax dues.

iii. ACL wrote a letter dated December 3, 2009 to all shareholders intimating that

management of ISE was working with malafide intention and had no vision to develop

the exchange and agreed to lead the process for all the shareholders. In addition to

some issues related to financials, it had also raised other issues including a) no effort

had been made by existing management to develop a robust business model b) matters

related to interference of ISE, especially Mr. P J Mathew in the day to day affairs such

as HR, utilizing client funds, changing of client code etc. of the subsidiary company of

ISE i.e., ISE Securities Ltd. c) registering of ISE as an SME Exchange in the light of the

competition faced by ISE.

iv. The shareholders believed that initiatives of ACL will benefit the minority shareholders

and therefore they supported it.

v. The shareholders had given their clear views on the agenda items to be discussed on

20th November, 2009. From the agenda/notes provided by ISE it is noted that the only

agenda of the said meeting was to amend bye-laws in accordance with directives of

SEBI. However, it appears from the letter of ACL mentioned at pt 3 above, that the

agenda appears to be more than that and also that the Chairman might have made

misleading and coercive statements.

Page 10 of 27

q. From all of the above it was alleged that the management of ISE, especially the noticee and Board

of ISE were quite informed about the formation of a group of shareholders that were behaving like

persons acting in concert (PAC) and allegedly chose to ignore these activities. Therefore, it was

alleged that ISE management did not find it necessary to take cue of the connections among

various shareholders obviously available in public domain, which would have been checked as a

part of the monitoring mechanism. This overturns the concept of demutualization, as the

shareholders are acting in concert.

r. As regards the monitoring mechanism for detecting violations of MIMPS Regulations, investigation

had revealed that the monitoring mechanism of ISE mainly consisted of relying upon the

declarations of the shareholders at the time of buying shares of ISE and checking names of the

directors etc from the website of Ministry of Company Affairs. In case of original allottees at the

time of demutualization, a list of directors was provided by the shareholders (also known as original

allottees). In case of shareholders transferring their shares, the details of the transferee are provided

by the transferor and transferee, with an undertaking that they are complying with the provisions of

the MIMPS Regulation and are not acting in concert with any other shareholder of ISE. Generally,

ISE verifies details (mainly names) of the directors of its corporate shareholders with the details

available on the website of MCA (http://mca.gov.in). However, addresses of the shareholders as

appearing in the MCA website were not checked for PAC. Addresses of the directors as appearing

on the MCA website were also not checked. In case of corporate shareholder, if the management

of the corporate shareholder changed, a fresh undertaking was not taken as it was understood that

the undertaking given by the earlier management held good. In case of change of name of the

shareholders, MCA website was checked again for verifying common directors. ISE relies upon the

undertaking given by the shareholders with respect to whether they acted as PACs or not and

checks for common directors among various shareholders as per information available on the

MCA website. However, in case common directors were to be found and the aggregate holding of

those shareholders were more than 5% of the total paid up equity of the ISE, then ISE would

report to SEBI for taking appropriate action. Beyond this no other steps are taken by ISE.

s. With respect to the above said 11 entities, the SCN alleged that ISE did not carry out a proper

scrutiny, even after receiving the SCN {ref. no. MRD/DSA/ISE/SCN/1398/2011 dated January 12,

2011} from SEBI. The SCN (issued in the instant matter against Mr. P. J. Mathew) further alleged that

the above conduct of ISE was practically the same as having a 'check-list approach' to a serious

matter of preventing violations of MIMPS Regulations by ISE.

Page 11 of 27

t. As regards the meeting held on November 20, 2009, it was alleged that the same was one of its

kind, wherein a set of people associated with ACL (i.e. related to 10 out of 41 (as on 30.09.2010)

shareholders) tried to influence decision making at ISE’s general body meeting. This instance

should have prompted some action by ISE. However, it was alleged that ISE neither took any

action nor informed the same to SEBI. The SCN also alleged that with respect to a complaint filed

by one S.Ravi with SEBI, ISE had informed (vide reply dated December 7, 2009) SEBI that some

shareholders were forming a cartel. The letter also stated that “group of shareholders had issued

requisition dated July 14, 2009”, “new shareholders for whom Mr. Ravi is soliciting support are all acting in concert

with Religare.” and that “share holders who were part of the group companies of the Software Vendor and other

shareholders who were acting in concert”.

The SCN alleged that the same indicated that ISE/noticee was aware of the issues in the Stock

Exchange regarding shareholders acting in concert from a long time and that no corrective action

was taken. The SCN also alleged "You choose to mention about it only consequent to a complaint filed in

SEBI by one of the PIDs himself and has reported about PAC very incidentally".

u. Regulation 11 of the MIMPS Regulations read with Regulation 52 of the Securities Contracts

(Regulation) (Stock Exchanges and Clearing Corporations) Regulations, 2012 ("the SECC

Regulations, 2012) casts an obligation on the stock exchange to ensure that its shareholding is in

compliance with Regulations 8 and 9 of the Regulations which prescribe ownership restrictions of 5

% on any entity. The exchange had been continuously filing undertakings (as required under

Regulation 11 of the MIMPS regulations) that it was in compliance with the prescribed norms. As is

evident from the details mentioned above, the declarations filed in this regard by the exchange/MD

of the exchange were incorrect and had been falsely filed over a long period of time. As the Religare

group along with its PACs controls / holds a substantial shareholding (i.e. 21.142%) it becomes

evident that the Exchange had not ensured compliance with the MIMPS Regulations.

From all of the above it was alleged that the management of ISE, especially the noticee and the

Board of ISE were quite informed and aware about the formation of a group of shareholders that

were behaving like persons acting in concert (PAC) and still chose to ignore these activities. The

details as brought out above, also indicates that the person were acting in concert and you have

been continuously filing incorrect declarations in this regard with SEBI. It was alleged that the

noticee did not take any action and "remained non-responsive on this issue" and thereby defeated

the purpose of demutualization.

Page 12 of 27

C. Allegation of Proxy Voting by Mr. P.J. Mathew:

a. SEBI vide letter dated September 21, 2005 advised ISE that PIDs would be selected by the Board

of Directors of the Stock Exchange from SEBI constituted panel of PIDs and that the same shall

be suitably incorporated in Articles, Rules of ISE. Further, based on a clarification sought by ISE,

SEBI vide letter no. MRD/DSA/C&D/SL/143463/08 dated November 06, 2008 advised ISE to

suitably amend clause 1.3.5 wherein the word ‘elected’ shall be replaced with the word ‘selected’.

b. In this regard, in the meeting of the Board held on November 20, 2009 it was decided to call for

polling by representatives of Religare Group and Chairman of the Board Mr. K. Rajendran Nair

accepted the same. The SCN had alleged that the decision to allow polling on the matter of

appointment of PIDs, pursuant to SEBI directives, was in complete defiance to the above

directives / letters of SEBI.

c. As mentioned in the SCN (MRD/DSA/ISE/SCN/1398/2011 dated January 12, 2011), during the

course of inspection, it was observed that the noticee, while representing the governing board of

the Exchange as Ex-Officio member of the Exchange in the EGM/AGM, in total disregard of

provisions of corporatization and demutualization and the duties expected of a MD, had acted as a

proxy for certain individual share holders of the Exchange in the EGM of the Exchange for the

meeting held on 20th November 2009.

d. Details of the proxy votes cast by the noticee on behalf of certain persons are given below:

S No

Name of the Shareholder Name of the Representative

Shareholding (%) in ISE

1 Anand Mahendra Shah P. J. Mathew 0.900 2 Anand Vishnu Naik & Mohan Anand

Naik P. J. Mathew 1.000

3 Dileep Baid P. J. Mathew 1.000 4 Jay Mahendra Shah P. J. Mathew 0.100

e. It is pertinent to mention here that as per the provisions of Articles and bye-laws of ISE (Art.175

(ii)) which provides that in the absence of the Chairman, the Managing Director shall be vested

with the powers, rights duties and functions of the Chairman as provided in the Articles of

Association, Rules, Bye laws and Regulations of the Company. The articles of the exchange cast a

huge responsibility on the noticee (as MD) with respect to the functioning of the exchange.

f. Therefore, it was alleged that despite the specific duties entrusted upon the MD/CEO of a stock

exchange and also the unique position enjoyed by him by virtue of his appointment, the noticee

had undermined the role and duties expected of an MD of a Stock Exchange by acting on behalf of

Page 13 of 27

certain shareholders of the stock exchange and by casting proxy votes for individual shareholders

of the exchange, even though the noticee was representing the management of the Exchange.

g. The behavior corroborates the alleged pattern that the noticee had been working in sync with

shareholders instead of being neutral to the views of the shareholders and act in the well-being of

ISE.

h. The conduct of the noticee in indulging in proxy voting for an agenda of a meeting specifically held

to implement SEBI directives while representing the management was alleged to be a conflict of

interest.

i. The SCN had also alleged that by allegedly voting on behalf of shareholders, the noticee had

defeated the spirit of corporatization and demutualization scheme.

3. In view of the above, the SCN alleged that "59. ............................Mr. P J Mathew had violated

Regulation 11 read with Regulations 8 and 9 of the MIMPS Regulations read with Regulation 52 of SECC Regulations

2012, SEBI circular no. No.SMD/POLCIY/Cir-3/03 dated January 30, 2003, code of conduct/corporate governance

norms prescribed by SEBI vide its letter no.LKS/229/2001 dated May 18, 2001 & letter no

MRD/DSA/C&D/50049/05 dated September 21, 2005, code of conduct for the directors stipulated by SEBI vide

letter no.LKS/229/2001 dated May 18, 2001 and letter no MRD/DSA/C&D/50049/05 dated September 21,

2005 read with SEBI’s Circular No.SMD/POLCIY/Cir-3/03 dated January 30, 2003.......".

4. The SCN advised the noticee to show cause as to why appropriate directions as deemed fit and

proper under section 12A of the Securities Contracts (Regulation) Act, 1956 (hereinafter referred to as

"the SCRA") and sections, 11, 11(4) and 11B of the Securities and Exchange Board of India Act, 1992

(hereinafter referred to as "the SEBI Act"), should not be issued against him for the alleged violations.

The SCN also advised the noticee to file his reply and indicate whether he desired a personal hearing in

the matter.

5. The noticee filed his replies to the SCN vide letters dated July 12, 2013 and July 19, 2013. He was

afforded an opportunity of personal hearing on August 05, 2013, when the noticee along with Mr. S.D.

Israni, Advocate and Mr. Milind Nigam, Company Secretary of ISE, appeared and made submissions.

The noticee also tendered his written submissions dated August 05, 2013.

6. The following were inter alia the submissions made by the noticee in respect of the allegations:

Page 14 of 27

Submissions with respect to the allegation of irregularities in the award of contract for setting up

trading platform:

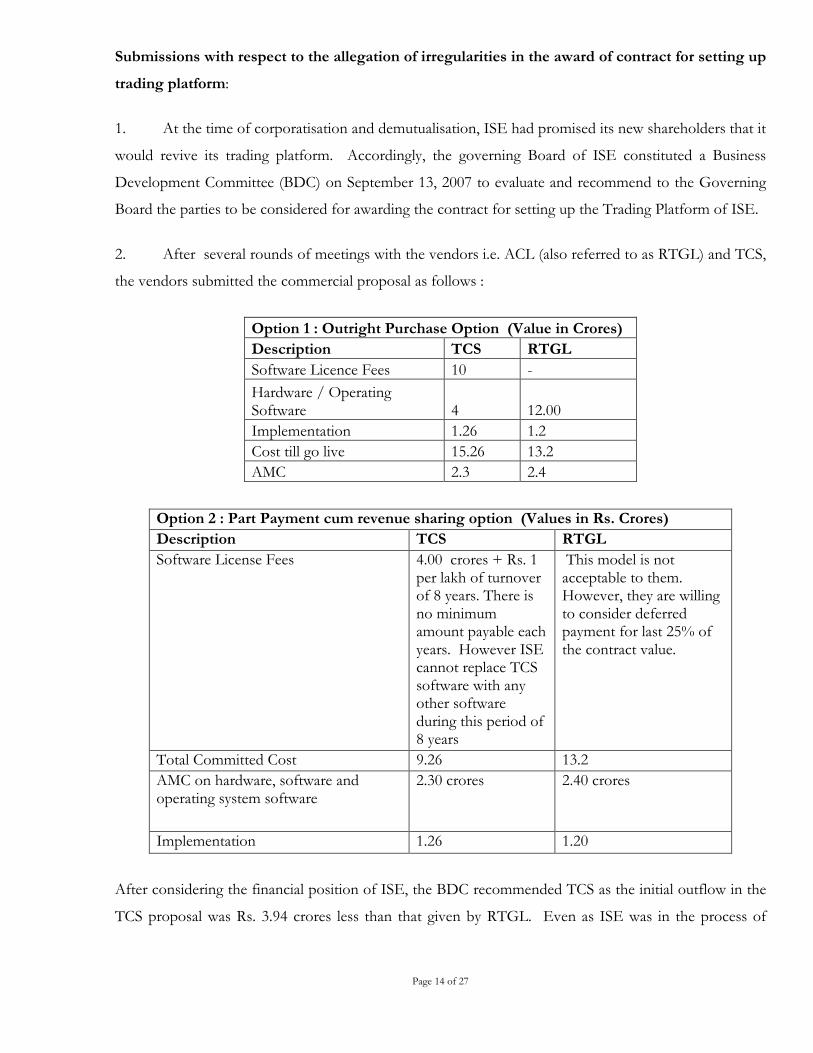

1. At the time of corporatisation and demutualisation, ISE had promised its new shareholders that it

would revive its trading platform. Accordingly, the governing Board of ISE constituted a Business

Development Committee (BDC) on September 13, 2007 to evaluate and recommend to the Governing

Board the parties to be considered for awarding the contract for setting up the Trading Platform of ISE.

2. After several rounds of meetings with the vendors i.e. ACL (also referred to as RTGL) and TCS,

the vendors submitted the commercial proposal as follows :

Option 1 : Outright Purchase Option (Value in Crores)

Description TCS RTGL

Software Licence Fees 10 -

Hardware / Operating Software 4 12.00

Implementation 1.26 1.2

Cost till go live 15.26 13.2

AMC 2.3 2.4

Option 2 : Part Payment cum revenue sharing option (Values in Rs. Crores)

Description TCS RTGL

Software License Fees 4.00 crores + Rs. 1 per lakh of turnover of 8 years. There is no minimum amount payable each years. However ISE cannot replace TCS software with any other software during this period of 8 years

This model is not acceptable to them. However, they are willing to consider deferred payment for last 25% of the contract value.

Total Committed Cost 9.26 13.2

AMC on hardware, software and operating system software

2.30 crores 2.40 crores

Implementation 1.26 1.20

After considering the financial position of ISE, the BDC recommended TCS as the initial outflow in the

TCS proposal was Rs. 3.94 crores less than that given by RTGL. Even as ISE was in the process of

Page 15 of 27

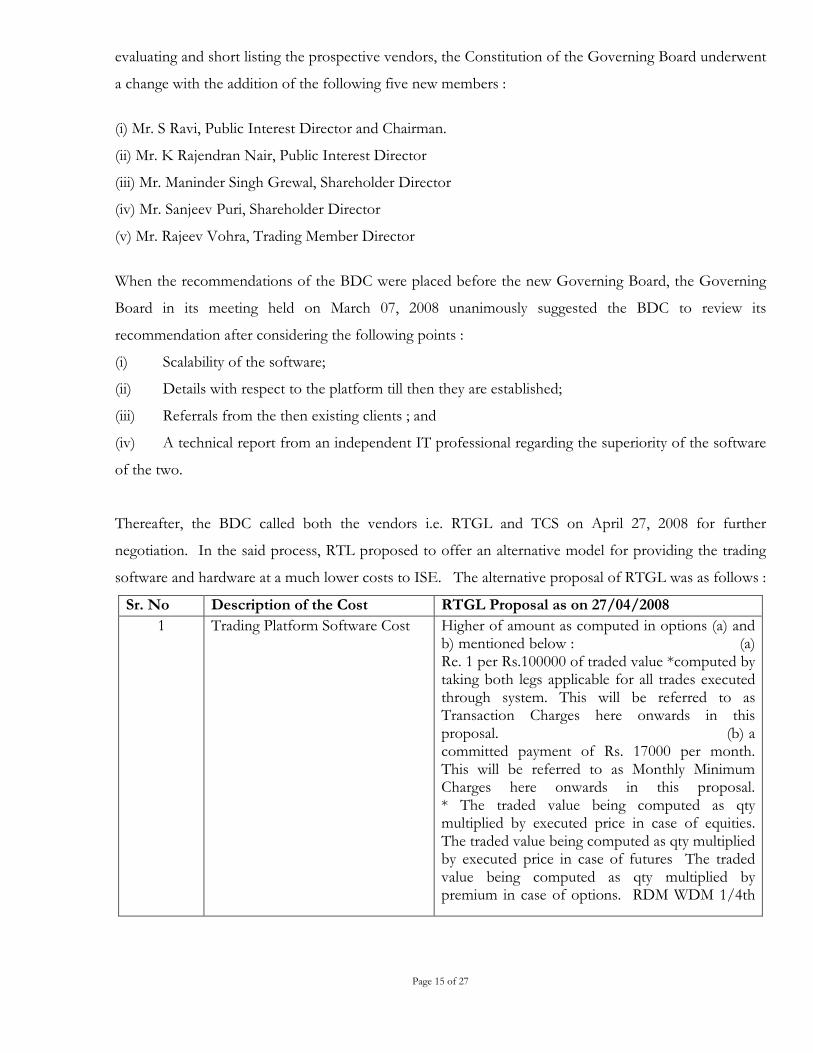

evaluating and short listing the prospective vendors, the Constitution of the Governing Board underwent

a change with the addition of the following five new members :

(i) Mr. S Ravi, Public Interest Director and Chairman.

(ii) Mr. K Rajendran Nair, Public Interest Director

(iii) Mr. Maninder Singh Grewal, Shareholder Director

(iv) Mr. Sanjeev Puri, Shareholder Director

(v) Mr. Rajeev Vohra, Trading Member Director

When the recommendations of the BDC were placed before the new Governing Board, the Governing

Board in its meeting held on March 07, 2008 unanimously suggested the BDC to review its

recommendation after considering the following points :

(i) Scalability of the software;

(ii) Details with respect to the platform till then they are established;

(iii) Referrals from the then existing clients ; and

(iv) A technical report from an independent IT professional regarding the superiority of the software

of the two.

Thereafter, the BDC called both the vendors i.e. RTGL and TCS on April 27, 2008 for further

negotiation. In the said process, RTL proposed to offer an alternative model for providing the trading

software and hardware at a much lower costs to ISE. The alternative proposal of RTGL was as follows :

Sr. No Description of the Cost RTGL Proposal as on 27/04/2008

1 Trading Platform Software Cost Higher of amount as computed in options (a) and b) mentioned below : (a) Re. 1 per Rs.100000 of traded value *computed by taking both legs applicable for all trades executed through system. This will be referred to as Transaction Charges here onwards in this proposal. (b) a committed payment of Rs. 17000 per month. This will be referred to as Monthly Minimum Charges here onwards in this proposal. * The traded value being computed as qty multiplied by executed price in case of equities. The traded value being computed as qty multiplied by executed price in case of futures The traded value being computed as qty multiplied by premium in case of options. RDM WDM 1/4th

Page 16 of 27

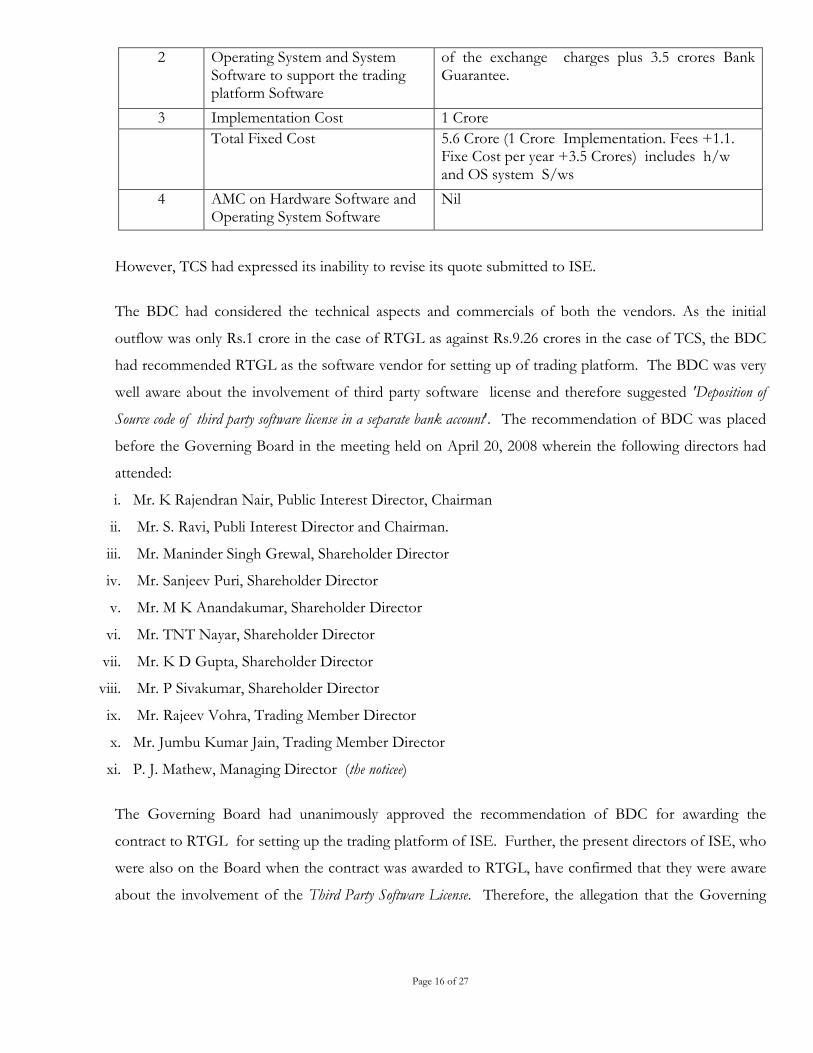

2 Operating System and System Software to support the trading platform Software

of the exchange charges plus 3.5 crores Bank Guarantee.

3 Implementation Cost 1 Crore

Total Fixed Cost 5.6 Crore (1 Crore Implementation. Fees +1.1. Fixe Cost per year +3.5 Crores) includes h/w and OS system S/ws

4 AMC on Hardware Software and Operating System Software

Nil

However, TCS had expressed its inability to revise its quote submitted to ISE.

The BDC had considered the technical aspects and commercials of both the vendors. As the initial

outflow was only Rs.1 crore in the case of RTGL as against Rs.9.26 crores in the case of TCS, the BDC

had recommended RTGL as the software vendor for setting up of trading platform. The BDC was very

well aware about the involvement of third party software license and therefore suggested 'Deposition of

Source code of third party software license in a separate bank account'. The recommendation of BDC was placed

before the Governing Board in the meeting held on April 20, 2008 wherein the following directors had

attended:

i. Mr. K Rajendran Nair, Public Interest Director, Chairman

ii. Mr. S. Ravi, Publi Interest Director and Chairman.

iii. Mr. Maninder Singh Grewal, Shareholder Director

iv. Mr. Sanjeev Puri, Shareholder Director

v. Mr. M K Anandakumar, Shareholder Director

vi. Mr. TNT Nayar, Shareholder Director

vii. Mr. K D Gupta, Shareholder Director

viii. Mr. P Sivakumar, Shareholder Director

ix. Mr. Rajeev Vohra, Trading Member Director

x. Mr. Jumbu Kumar Jain, Trading Member Director

xi. P. J. Mathew, Managing Director (the noticee)

The Governing Board had unanimously approved the recommendation of BDC for awarding the

contract to RTGL for setting up the trading platform of ISE. Further, the present directors of ISE, who

were also on the Board when the contract was awarded to RTGL, have confirmed that they were aware

about the involvement of the Third Party Software License. Therefore, the allegation that the Governing

Page 17 of 27

Board was not aware about the involvement of third party software license is factually incorrect as it is

contrary to facts.

It is a matter of record that TCS had also confirmed that they had attended the meeting for three

negotiations. Therefore, the allegation of not giving opportunity to TCS to renegotiate is factually

incorrect.

The Governing Board also confirmed in its meeting held on January 25, 2011 that "The Managing Director

has disclosed all the facts and details available to him and required to be known prior to awarding the contract. There was

no further information expected from him to consider the proposals, hence, it is factually incorrect to state that the Managing

Director failed to give his transparent opinion and acted in concert with the dominant shareholder. It is also factually

incorrect to say that there is a dominant shareholder. Please note that all actions of Mr. Mathew were in good faith and

only in the interest of the Exchange. He strongly refutes the allegation that he had sided with any shareholder, he would like

to reaffirm that at no stage he had sided with any shareholder, he has worked in the interest of ISE. Therefore, in the

circumstances we request you to kindly withdraw your said allegation".

As regards the allegation/observation in the SCN that "... In addition given the fact that Cambridge actually

owned the software RTGL bagged the order for, also given the fact that to be given to an entity with the software were ready

for installation and that RTGL did not own the software ready for installation and it is alleged that BDC should not have

order to RTGL further Cambridge from whom RTGL was buying the order should have been given the opportunity to

bid", the noticee submitted the following:

Both TCS and RTGL did not have readily usable software for the purpose of the trading platform. The

BDC and the Board of Directors, after considering the initial cash outflow, consciously took a decision

to give order to RTGL since initial cash outflow was only Rs. 1 crore but in the case of TCS it was 9.26

crore. The governing Board insisted to deposit the source code in an escrow account for the best

interest of the stock exchange. After terminating the contract with RTGL, ISE had awarded the

contract to TCS and TCS took more than one year. In case of TCS, there was no third party license

agreement and therefore the Governing Board did not insist on the deposit of source code in an escrow

account. The noticee again reiterated that the Governing Board of ISE was aware of third party licenses

agreement in the case of RTGL. As regards the observation that ISE did not provide an opportunity to

Cambridge for installing the software in ISE, the noticee submitted that when the contract was awarded

to TCS after terminating the RTGL contract, ISE had made an advertisement in the newspaper.

Page 18 of 27

However, Cambridge had neither shown any interest nor applied in the process. According to the

noticee, the allegation that ISE did not provide opportunity to bid by Cambridge was incorrect.

With respect to the allegation that "In the investigation, that the BDC report is not signed by Dr. M Y Khan,

PID, Chairman of the Committee and as well as other 4 members of the Committee namely Dr. Israni, Shri Mahesh L

soneji, Shri Manoj Kumar Vijaya and Shri Ashish Parekh, out of the total 8 members thus a total of 5 out of 8 members

excluding exchange employees had not signed the report and there is no mention of the absence or dissent note in the report.

Further the 3 remaining members who are shareholders directors and trading members of ISE. " the noticee submitted

the following :

"The BDC meeting held on April 27, 2008, 8 members were present in the meeting. After the meeting the reports were

prepared in the evening. the same has to be placed in the next day Board meeting. so the decision of BDC in the previous

day were signed by those BDC members who are also the members of the Governing Board who attended the Board meeting.

The decision of the BDC was unanimous. Please note that BDC role is only recommendatory. The Board is having

authority to approve or reject the recommendations of the committee. All Board Members unanimously approved the

recommendation. If I had an intention to do something wrong I would have been taken the signature from the other BDC

members after the Board meeting but I did not do the same. Please note that I have acted with total transparency and the

competent authority ie. The Governing Board unanimously approved to award the contract to RTGL So the above

mentioned allegations does not have any merits".

With respect to the allegation "It is alleged that you being MD of ISE, member of the BDC committee and being part

of the group who visited Dubai and Dhaka to ensure that the Software of Asian CERC and TCS as directed by BDC

has failed to ensure that vendor selection was carried out in a fair manner which resulted in selection of a wrong vendor and

substantial loss to ISE", the noticee submitted that "BDC and Governing Board has considered that initial outflow of

the company and also they were very much aware about the third party license agreement. For protecting the interest of the

company the board had decided to incorporate the clause in depositing the source code in an Escrow Account. Since RTGL

violated the MSA the company had terminated the contract and recovered the advance paid to them. In any commercial

transaction the amount paid to lawyer for recovering the advance amount paid to the vendor is a necessity. If I had been

helping RTGL I would not have taken steps to cancel the contract and would not have reported the lapses of RTGL to

Governing Board so the allegations is totally incorrect and I totally deny the allegations".

The noticee submitted that he had acted and implemented only the directions of the Governing Board of

ISE in the best interest of the company. His contention therefore was that the allegations against him

are factually incorrect. The noticee further stated that when the termination of contract of RTGL took

place, the representative of RTL, on the then Governing Board of ISE threatened that the noticee would

be a permanent enemy of Religare and that with all their connections in SEBI, they will try to destabilize

ISE.

Page 19 of 27

Submissions with respect to failure to comply with the MIMPS Regulations:

a. The noticee stated that the allegation that he had given wrong declaration with respect to

MIMPS Regulations to SEBI was wrong and was not borne out by facts.

b. As SEBI had not prescribed any policy or guidelines for monitoring the MIMPS Regulations, ISE

on its own had formulated a policy for monitoring the MIMPS Regulations. The same was also

submitted to SEBI.

c. Based on the criterion formulated by ISE for monitoring the MIMPS Regulations, ISE could not

conclude that any of its shareholders were acting in concert.

d. Nevertheless, ISE found that few shareholders were acting against the interest of ISE.

Therefore, ISE intimated to SEBI vide its letter dated December 07, 2009 about the action of

few shareholders such as voting against the resolution for amending the Articles of Association in

line with SEBI directions requisitioning the calling for EGM for derecognizing ISE. However,

no direction was received from SEBI.

e. On receipt of SEBI's show cause notice, ISE issued letters to those shareholders to confirm

whether they were acting in concert. Copies of confirmation received from those shareholders

that they were not acting in concert had already been submitted to SEBI.

f. Therefore, as per the available records, ISE was unable to conclude as to whether any of the

shareholders were acting in concert. Therefore the allegation that the noticee had given wrong

declaration with respect to MIMPS Regulations to SEBI is incorrect as they had tried their best to

ascertain the correct status.

In the AGM held on September 29, 2009, along with the normal AGM agenda items, SEBI mandated

amendments to the Articles were also placed. But a few shareholders defeated the SEBI mandated

amendments saying that those were against their fundamental rights. Subsequently ISE called an EGM

on November 20, 2009 only for passing SEBI mandated amendments. Few shareholders again defeated

the resolution. The outcomes of the EGM and AGM's i.e. minutes of the two meetings were

forwarded to SEBI on January 18, 2010.

With respect to ACME Ltd, which held more than 4% equity stake ISE verified whether the said

company was acting in concert with the Religare Group. After visiting their office and meeting their

Directors, it was gathered that they were not connected with Religare Group. In case of ACME Ltd

although they had given proxy to an employee of Religare for the voting at the EGM held on November

Page 20 of 27

20, 2009, they had authorised Mr. K. V. Thomas who was representing the Regional Stock Exchange at

the EGM held on November 12, 2010. Hence, according to the noticee, it would not be appropriate to

construe that ACME Ltd was acting in concert with Religare.

The noticee also contended that a person acting as a proxy for another would not mean that he is acting

in concert as credentials of all the entities who were named in the SCN were checked with the norms

formulated by ISE and also the confirmations received from such entities that they do not act as PACs.

Submissions with respect to Proxy Voting by the noticee:

a. ISE had called an AGM on September 29, 2009 to approve the routine agenda of the General

Meeting such as adoption of Annual Accounts, Declaration of Dividend,

Appointment/Reappointment of Directors and Appointment /Reappointment of Auditors.

b. Apart from the routine agenda, there was an agenda to amend the Articles of Association of ISE

in terms of SEBI letter no. MRD/DSA/C&D/50049/05 dated September 25, 2005 and Letter

no. MRD/DSA/C&D/SL/143463/08 dated November 6, 2008. The shareholders passed all the

other agenda items except the amendments to the articles which was required to be passed in

terms of the directives of SEBI. The alterations of the Articles required special resolution to be

passed by the members of ISE.

c. Subsequently, an EGM, was called on November 20, 2009 and the only agenda was for

amending the Articles of Association in terms of the above said SEBI letter. Some of the

shareholders had requested, in writing, the noticee to accept their proxy and to vote in favour of

the resolution required to be passed for amending the articles in terms of the SEBI directives.

d. The finding of inspection was made without considering the very fact that the directives of SEBI

if not implemented would call the very existence of ISE into question and would have exposed

the exchange to the charge of having disregarded and violated the SEBI directives.

e. It was the noticees belief that as per Article 195 of AoA of the Company, it was his duty to

implement the SEBI directives. He had no personal interest whatsoever other than implementing

the SEBI directives. It was also mentioned to SEBI officials many times that proxies was

accepted only to implement SEBI directives and not for any personal reasons.

f. Therefore, there was no question of any conflict of interest as the noticee was acting purely in his

professional capacity to discharge his duties and as such did not violate the code of conduct for

directors. According to him, even under the Companies Act, 1956, there was no bar against the

Managing Director from accepting a proxy. The noticee had accepted proxies only to implement

the SEBI directives as he felt that it was his prime duty to implement the SEBI directives. His

Page 21 of 27

conduct was in the best interest of the company to ensure that necessary resolution is passed by

the members.

g. From the foregoing, SEBI would observe that all his actions have been above board and done

purely to discharge his duties towards the exchange.

h. The noticee stated that he had been made a scapegoat through the design of some people

wanting to destabilise ISE and also harass him for not giving into their nefarious designs.

The proxies which were accepted by the noticees were with specific directions from the Shareholders to

implement the SEBI directive.

The noticee also made the following general submissions:

• The noticee was a law abiding professional and had an unblemished record of 24 years

association with the capital market. The noticee submitted that he was a General Manager

with Cochin Stock Exchange and was associated with it for 12 years. Pursuant to this,

he was an Executive Director of the Madras Stock Exchange for 5 years and thereafter

joined ISE w.e.f August 2007.

• The noticee submitted that during his association with the Capital Market and holding

responsible positions in the stock exchanges he was not served with any notice by SEBI

or by those stock exchanges.

• The noticee submitted that he has always discharged his duties strictly in accordance with

SEBI Regulations and had scrupulously followed the rules governing the functioning of

stock exchanges.

• The noticee submitted that ISE had received a show cause notice on January 12, 2011

and the allegations levelled against the Board of Directors were : (i) Lack of Transparency

in awarding the contract (ii)Casting of proxy vote by the MD (iii) Failure to ensure

compliance with MIMPS. ISE forwarded its reply and the personal hearing scheduled in

that matter was postponed. The noticee submitted that no hearing had been conducted in

respect of the said show cause notice. The noticee submitted that the new show cause

notice issued to him on June 26, 2013 containing more or less the same allegations as in

the earlier SCN i.e. (i) irregularities in awarding contract for the trading platform (ii)

Failure to ensure compliance with the MIMPS Regulations. (iii) Proxy voting by PJ

Mathew.

Page 22 of 27

• ISE was waiting for the last two and a half years for the outcome of the 1st show cause

notice. However, ISE did not receive any communication which meant that ISE had

satisfactorily explained all the allegations.

• The noticee submits that when ISE sent the proposal for his reappointment as Managing

Director which was followed with a reminder, he received the captioned SCN. The

noticee submits that the contents of both the show cause notices (the SCN issued to ISE

and the present SCN issued to him) are the same and has alleged that he is victimized by

some interested persons.

7. I have considered the SCN, the replies of the noticee, submissions and written submissions

tendered during the personal hearing and other material available on record. I proceed to consider the

allegations leveled against the noticee along with his submissions. The first charge against the noticee is

that he, as the Managing Director of the ISE had failed to ensure the fair manner of vendor selection,

which resulted in the selection of wrong vendor and substantial loss to ISE. In this regard, the noticee

had contended that the Board of Directors had confirmed that the Managing Director (i.e., noticee) had

given all the relevant information to the Board in respect of awarding the contract to RTGL. Further, as

per the meeting of the Governing Board held on July 16, 2013, the Board was satisfied that the available

records in ISE and also the confirmation made by the present directors (who were part of the Governing

Board when the contract was awarded to RTGL), showed that the Managing Director (i.e., the noticee)

had informed the then Governing Board about the involvement of the Third Party Software License at

the time of negotiations with RTGL before awarding the contract, which was also included in the MSA.

It was also submitted that this MSA was vetted by an external independent agency duly appointed by the

Governing Board of ISE. The noticee had also contended that the minutes of the Governing Board held

on July 25, 2008 showed that the Third Party License Agreement and Escrow Agreement was with the

knowledge and approval of the Governing Board. The minutes of BDC meeting held on July 9, 2008

also mentioned about the third party agreement approval. As per the noticee, these two documents

clearly showed that the Governing Board and the BDC were well aware of the Third Party License

agreement. The noticee also submitted that the 'MSA' was signed only on August 7, 2008 which was after

the aforesaid approval given by the Board. Accordingly, the MSA, executed between RTGL and ISE, had

a clause for depositing the source code of the Third Party Software License in a Bank. According to the

noticee, the present Governing Board also had taken note of the same. In view of the above

submissions, the noticee had contended that the allegation that he had 'covered up the Third Party

License Agreement' was factually incorrect.

Page 23 of 27

I have considered the above submissions of the noticee. The allegations are twofold. One is the

irregularity in awarding the contract for setting up trading platform in ISE and the second is that "noticee

was fully aware of the third party software license agreement at the time of award of the contract to ACL and that it

appeared to have been deliberately covered up/ignored while listing out the relative strengths of the vendors by BDC/Board".

The SCN had also stated "......... In view of the above, the noticee being the MD of ISE (during the relevant period), a

member of the BDC committee and being part of the group who visited Dubai and Dhaka to ensure that the software of

TCS and ACL are ready for use as directed by BDC, had failed to ensure the fair manner of vendor selection, which

resulted in the selection of wrong vendor and substantial loss to ISE".

I note that the noticee in his submissions had stated that the BDC had considered the technical aspects

and commercials of both the vendors. Further, the initial outflow was Rs.1 crore in the case of proposal

from RTGL, whereas the same was Rs.9.26 crores in the case of TCS. Therefore the BDC had

recommended RTGL as the software vendor for setting up of trading platform. The noticee had also

submitted that BDC was very well aware about the involvement of third party software licence and

therefore suggested 'Deposition of Source code of third party software license in a separate bank

account'. The recommendation of BDC was placed before the governing Board in the meeting held on

April 20, 2008. The Governing Board of ISE had also confirmed the same. The noticee had also

submitted that the 'MSA' was signed only on August 7, 2008 which is after the aforesaid approval given

by the Board. According to the noticee, the Board of Directors have confirmed that the Managing

Director had given all the relevant information to the Board in respect of awarding the contract to

RTGL. The Governing Board in its meeting held on July 16, 2013, satisfied that the available records in

ISE and also the confirmation made by the present directors who have been part of the Governing

Board when the contract was awarded to RTGL, showed that the Managing Director had informed the

then Governing Board about the involvement of the Third Party Software License at the time of

negotiations with RTGL before awarding the contract, which was also included in the MSA having been

vetted by an external independent agency duly appointed by the Governing Board of ISE. Accordingly,

the MSA executed between RTGL and ISE had a clause for depositing the source code of the Third

Party Software License in a Bank.

I have also perused the MSA (dated 07.08.2008), wherein in clause 4.1(ii), there is a mention of 'Third

Party Software Applications'. The MSA had also mandated that the service provider (ACL) shall ensure

that the Third Party Software License Agreement (inclusive of escrow arrangement) is executed within 30

Page 24 of 27

days and that failure to deliver a copy of such agreement is considered as a material breach. Article 7 of

the MSA deals with Source Code Escrow. As per these provisions, the service provider shall have right

to access the source code of the third party software and also the right to modify such software for

maintenance, enhancement and support of the software applications. In view of the same, it may not be

reasonable to hold the noticee liable for not informing the Board about the third party software

arrangement. Yet, it leaves a question open that if software of neither TCS nor ACL were readily

deployable, the very act of shortlisting them appears to be arbitrary. Further, the noticee's handling of the

entire process of vendor selection reeks of ineptitude, at the very best.

The noticee had also stated that the Governing Board of ISE had confirmed in its meeting held on

January 25, 2011 that the Managing Director (i.e., the noticee) had disclosed all facts and details available

to him and required to be known prior to awarding the contract.

In view of the submissions and confirmation regarding the selection of vendor for providing trading

software to ISE and the fact that the Governing Board was aware of the 'third party software

arrangement' and had suitably inserted a clause in the MSA for submission of the Third Party Software

License in a Bank, it may not be reasonable to find the noticee liable for the above allegations.

8. The second allegation against the noticee is that the noticee and the Board of ISE were aware of

the formation of a group of shareholders who were behaving like persons acting in concert (PAC) and

still chose to ignore these activities. The SCN had also alleged that there were instances of filing of

incorrect declarations in this regard with SEBI. I also note that the SCN had alleged that "........ in

disregard of the aforesaid provisions, one of the shareholders of the Exchange M/s Religare Technova was holding more

than 21% of the equity holding of the Exchange, directly and through persons acting in concert." The SCN had also

alleged the 11 entities were acting as PACs for Religare Technova and had mentioned certain alleged

connections amongst them. It was also alleged that the noticee did not take any action.

The noticee had contended that SEBI had not prescribed any policy or guideline for monitoring

compliance with the MIMPS Regulations and that based on the criteria fixed by the ISE, the stock

exchange could not conclude that any of its shareholders were acting in concert. The noticee had also

contended that when ISE found that a few shareholders were acting against the interest of the stock

exchange, it brought the same to the notice of SEBI vide its letter dated December 07, 2009. The

noticee had also submitted that after receipt of SCN (issued to ISE), the stock exchange had issued

Page 25 of 27

letters to the shareholders to confirm whether they were acting in concert and had relied upon the

confirmations received from those entities that they did not act as PACs.

The noticee submitted that ACME Limited, which held 4% in ISE, cannot be construed as a PAC. As

per the noticee, though this entity had requested for proxy voting from an employee of Religare, it had

requested 'Mr. K.V. Thomas who was representing the Regional Stock Exchange at the EGM held on

November 12, 2010' to vote as proxy. The noticee had also contended that a person acting as a proxy

for another need not be that entity's PAC.

As MD of a SEBI recognized Stock Exchange, it was the duty of the noticee to implement the

provisions of the MIMPS Regulations in letter and spirit. The fact that an employee of Religare was

approached to act as proxy for an alleged PAC gives an indication that they could be acting with a

common purpose. ISE should not have been satisfied with a routine query and accepted a bland denial.

They should have tried to further explore the relationship amongst the alleged PACs and in case of

doubt should have informed SEBI. The MD/stock exchange could have sought guidance from SEBI

with respect to compliance with the MIMPS Regulations. The noticee did not follow the prudent path

and simply kept quiet and therefore had not acted in the best interest of the securities market.

9. The third and last allegation against the noticee is that he had acted as a proxy for few

shareholders of the stock exchange in respect of a resolution to amend the Articles/rules as directed by

SEBI. In this regard, I note that SEBI vide letter dated September 21, 2005 advised ISE that PIDs

would be selected by the Board of Directors of the Stock Exchange from SEBI constituted panel of

PIDs and that the same shall be suitably incorporated in Articles, Rules of ISE. Further, based on a

clarification sought by ISE, SEBI vide letter no. MRD/DSA/C&D/SL/143463/08 dated November 06,

2008 advised ISE to suitably amend clause 1.3.5 of the Articles of Association wherein the word ‘elected’

shall be replaced with the word ‘selected’. The SCN mentioned that instead of amending the relevant

rules, the ISE had called for an AGM on September 29, 2009 and an EGM on November 20, 2009 for

the purposes of making such amendments and in the EGM and alleged that the noticee had accepted and

acted as a 'proxy' for a few shareholders. As per the SCN, the noticee had acted as proxy for the

following persons:

Page 26 of 27

Details of the proxy votes cast by the noticee on behalf of the following persons:

S No

Name of the Shareholder Name of the Representative

Shareholding (%) in ISE

1 Anand Mahendra Shah P. J. Mathew 0.900 2 Anand Vishnu Naik & Mohan Anand

Naik P. J. Mathew 1.000

3 Dileep Baid P. J. Mathew 1.000 4 Jay Mahendra Shah P. J. Mathew 0.100

The noticee had contended that he acted as their proxy only to ensure that the SEBI directed

amendments go through and are approved in the said EGM. The noticee had also submitted that a few

shareholders had defeated the resolution brought for making such SEBI directed amendments and that

the outcome of such shareholders' meeting were informed to SEBI vide letter dated January 18, 2010.

In this regard, I find that the above amendments had to be carried out in view of the aforesaid SEBI

letters with respect to selection of PIDs. If the SEBI mandated amendments were not incorporated and

complied with by passing of appropriate amendments, the shareholders themselves would have been

responsible for the consequences that might have followed, including the de-recognition of the stock

exchange. The management could and should have made the AGM aware of consequences of not

passing the amendments. Therefore, the MD was not at all justified in acting as a proxy himself and thus

obviously aligning himself with a section of shareholders. The MD was not doing a favour by acting as a

proxy for ensuring that SEBI mandated amendments were passed in the shareholders meeting. In view

of the above observations, I am not able to accept the submission of the noticee that he acted as a proxy

to help SEBI.

In view of such facts and circumstances, the conduct of the noticee was not at all justified and he is

accordingly found liable for this charge.

10. I also note that SEBI vide Order dated December 08, 2014 allowed ISE to 'exit' from the

business of a stock exchange. Certain directions and conditions have been issued vide the said Order. I

also note that SEBI did not extend the term of the noticee as a managing director of the said exchange

beyond August 02, 2013.

11. In view of the foregoing, I, in exercise of the powers conferred upon me under section 19 of the

Securities and Exchange Board of India Act, 1992 and sections 11, 11(4) and 11B thereof and section

Page 27 of 27

12A of the Securities Contracts (Regulation) Act, 1956, hereby restrain the noticee, Mr. P. J. Mathew

(former Managing Director of the erstwhile Inter-connected Stock Exchange of India Limited) from accepting any

position as Managing Director or Chief Executive Officer in any of the SEBI recognized Stock

Exchanges for a period of one year.

12. The SCN dated June 26, 2013 issued to the above noticee stands disposed off accordingly.

PRASHANT SARAN WHOLE TIME MEMBER

SECURITIES AND EXCHANGE BOARD OF INDIA Date : March 19th, 2015 Place : Mumbai