Embed Size (px)

Citation preview

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

Optoelectronics:Successfully penetrating many

new markets

Michael Lebby

Michael Lebby ([email protected])

Overviewn Optomism in the marketplace

ÿ Market evolution over the next decaden Optoelectronic Markets

ÿ OIDA global forecast– Displays, HBLEDs, Image Sensors, Medical Photonics,

Solar Cellsn International Roadmaps

ÿ Global snapshot across the industryn Summary

ÿ DARPA matching program

Optomism is back again!

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

Next decade inOptoelectronics

Michael Lebby ([email protected])

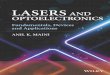

Next decade in optoelectronicsn Combined OE components and enabled products

ÿ 2004-16 CAGR 11%Global optoelectronics 10yr forecast for components and enabled

products

0

200

400

600

800

1000

1200

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$B

Components

Enabled

Is this a $T industry?

Michael Lebby ([email protected])

Global optoelectronics 10yr forecast for enabled and component segments

0

200

400

600

800

1000

1200

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$B

Storage Media

Passives, Solar Cells, Other

Display Modules

Fiber & Cable

Transceiver Modules

Sources & Detectors

Connectors and Hardware

Solar

LCD TVs

DVD Players/Videogames

Camera Phones & PDAs

FPD monitor systems

PDP TVs

Cameras/Scanners

Notebook PCs (display)

Optical Storage Drives

Fiber Network Eq.

Next decade optoelectronics segmentsn Strong consumer/entertainment drivers

Displays grow more slowly

Michael Lebby ([email protected])

Japanese future vision

Prospects of OE World Market (billion USD)

Source: http://www.oitda.or.jp/main/syourai04-j.html [ 1 USD=110 JPY ] AAGR: average annual growth rate

50.9 167.3

13.6

84.5

134.5

45.5

176.4

275.5

94.5

106.4

139.1

68.2

39.1

72.7

14.5

18.2

65.5

2.7

44.5

73.6

18.2

21.8

40.9

6.4

0

200

400

600

800

1000

2002 2010 2015

264

544

968

AAGR=10.9%

AAGR=12.1%

Medical Care / Welfare

Environment / Sensing

Optical (Solar) Energy

Processing

Input & Output

Display / Lighting

Optical Memory

Info-Communications

OITDA expects $1T OE business

Michael Lebby ([email protected])

Japanese Future with OIDA data

Prospects of OE World Market (billion USD)

[ 1 USD=110 JPY ]

50.9 167.384.5

134.5176.4

275.5

106.4

139.1

39.1

72.7

18.2

65.5

44.5

73.6

21.8

40.9

0

200

400

600

800

1000

2002 2010 2015

264

544

968

OE market growing well today

OIDA Market Data

304248

364

Source: http://www.oitda.or.jp/main/syourai04-j.html

2003 2004 2005

Michael Lebby ([email protected])

OIDA and OITDA next decade data

Prospects of OE World Market (billion USD)

[ 1 USD=110 JPY ]

50.9 167.384.5

134.5176.4

275.5

106.4

139.1

39.1

72.7

18.2

65.5

44.5

73.6

21.8

40.9

0

200

400

600

800

1000

2002 2010 2015

264

544

968

Maturing towards $1T business

OIDA Market Data

304248

364

Source: http://www.oitda.or.jp/main/syourai04-j.html

731

963

2011 2016

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

OptoelectronicsMarkets

Michael Lebby ([email protected])

Global OE markets for enabled products

n FPD displays big driver for enabled products ($364B)

Comparison of global optoelectronics market estimates for enabled products and optoelectronic components

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

2003 2004 2005

$B

Enabled Products

Components

Strong growth in OE enabled products

Sources: OIDA member companies, OIDA estimates, KMI, Infonetics, Ovum-RHK, TIA, IDC, CIR, Gartner, Dell’Oro, Aventis, Prudential Equity, Strategies Unlimited, CTIA, PIDA,OITDA, KAPID, Display Search, ISupply, MIC Japan

Michael Lebby ([email protected])

Global optoelectronics market growthn Consumer/Entertainment driving optoelectronics

ÿ Liquid crystal display becoming ubiquitous

Global Y/Y optoelectronics growth for market segment applications (2004 to 2005)

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Optical Comm ($23B to$26B)

Comp ($179B to $195B)

Cons/Ent ($100B to$144B)

No surprise !

Sources: OIDA member companies, Display Search, ISupply, OIDA estimates

Michael Lebby ([email protected])

Growth for OE enabled productsn Consumer products are jazzing the market in 2005

Revenue Growth Rates for Optoelectronics-Enabled Products for 2005

-10% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Fiber Network Eq.

Optical Storage Drives

Notebook PCs

Cameras/Scanners

PDP TVs

FPD monitor systems

Camera Phones & PDAs

DVD Players

LCD TVs

Y/Y Growth 16% -1% 9% 10% 45% 7% 41% 6% 79%

Fiber Network Eq.

Optical Storage Drives

Notebook PCs

Cameras/Scanners

PDP TVsFPD

monitor systems

Camera Phones &

PDAs

DVD Players

LCD TVs

Flat panel displays are everywhere

Sources: OIDA member companies, KMI, Infonetics, Ovum-RHK, TIA, IDC, CIR, Gartner, Dell’Oro, Aventis, Prudential Equity, OIDA estimates

Michael Lebby ([email protected])

Global OE components marketsn Displays dominate components

Global optoelectronics components revenues (2003 to 2005) including flat panel displays

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2003 2004 2005

$B

Storage Media

Passives, Solar Cells, Other

Display Modules

Fiber & Cable

Transceiver Modules

Sources & Detectors

Connectors and Hardware

Displays dwarf traditional OE components

Sources: OIDA member companies, KMI, Infonetics, Ovum-RHK, TIA, IDC, CIR, Gartner, Dell’Oro, Aventis, Prudential Equity, OIDA estimates

Michael Lebby ([email protected])

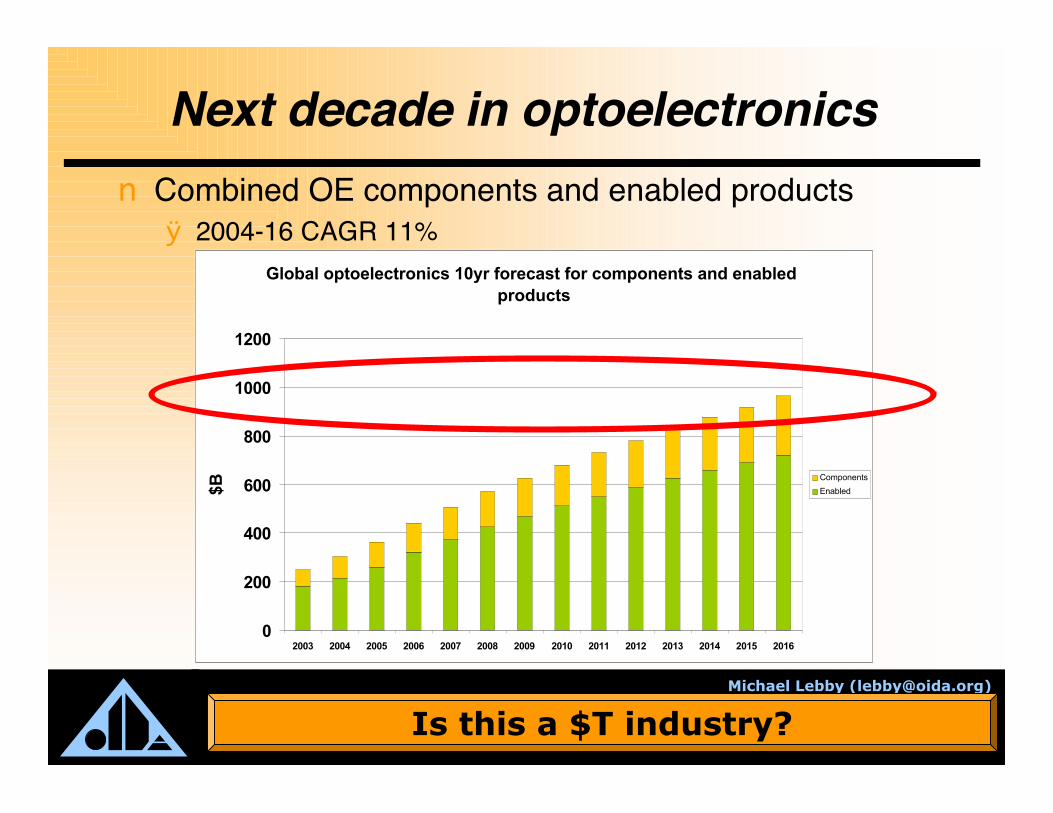

Global OE sources and detectorsn Image sensors strong growth due to camera phonesn HBLEDs now penetrating many consumer markets

Global optoelectronic sources and detectors component revenues (2003 to 2005)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2003 2004 2005

$B

Nondiode Lasers

Diode Lasers

Couplers

Image Sensors

LEDs

Growth driven by consumer markets

Sources: OIDA member companies, OIDA estimates, KMI, Infonetics, Ovum-RHK, TIA, IDC, CIR, Gartner, Dell’Oro, Aventis, Prudential Equity, Strategies Unlimited, CTIA, PIDA,OITDA, KAPID, Display Search, ISupply, MIC Japan

Michael Lebby ([email protected])

Growth in OE sources and detectorsn Image sensors driving the component growth in 2005

Global Y/Y optoelectronics sources and detectors component growth from 2004 to 2005

0% 5% 10% 15% 20% 25% 30%

LEDs

Image Sensors

Couplers

Diode Lasers

Nondiode Lasers

All segments showing strong growth

Sources: OIDA member companies, OIDA estimates, KMI, Infonetics, Ovum-RHK, TIA, IDC, CIR, Gartner, Dell’Oro, Aventis, Prudential Equity, Strategies Unlimited, CTIA, PIDA,OITDA, KAPID, Display Search, ISupply, MIC Japan

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

Display trends

Michael Lebby ([email protected])

Global display marketn a-Si TFT becoming the silicon (Vs GaAs) of displays

ÿ OLEDs expected to grow into huge opportunity

Display Forecast

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Rev

enu

e ($

Mil

lio

ns)

OLED

LTPS TFT LCD

PMLCD

a-Si TFT LCD

Other

Plasma

CRT

Watch OLEDs !

Sources: Display Search, ISupply, OIDA

Michael Lebby ([email protected])

OLEDs – emissive displaysn A flat radiating surface

ÿ New functional and design opportunities incomparison to point light sources. 150x150mm2 products available

n A wide viewing angleÿ Excellent readability from all perspectives

(e.g. self emitting logos)

n An integrated luminaireÿ The fusion of the lamp and luminaire world

Sources: EDM,Merck

Differentiation has to be strong…

Michael Lebby ([email protected])

Top 10 display applicationsn LCD TV 29% CAGR as key application

Top 10 mostly consumer/entertainment

Top 10 Display Applications

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007

Rev

enu

es

Others

PDA

Industrial

DVD

Game

Digtal Camera

Plasma TV

Notebook PC

Mobile Phone

LCD TV

Desktop Monitor

Sources: OIDA, Display Search, OIDA member companies

Michael Lebby ([email protected])

LCD “Glass” Size for Perspective

Source: DisplaySearch. LG.Philips LCD

Year: 2000Largest “Glass “ size = 3.5G

Optimized for Monitors and Notebook Screens

Year: 2004Largest “Glass “ size = 6GMonitors and Larger TVs

(and Digital Signage / Public Displays)

Year: 2006Largest “Glass “ size = 7G

Larger TVs and Digital Signage / Public Displays)

2000 2004 2006

6G & 7G technologies poised for ramp

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

HBLEDs become‘hot’

Michael Lebby ([email protected])

HB LED Forecast 2006-2012

0

2000

4000

6000

8000

10000

12000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Rev

enue

($M

illio

ns)

Historic

Other

Illumination

Signals

Automotive

Signs & Displays

Mobile Appliances

n Assumptionsn Maturing Mobile Appliance

Marketÿ Continuing ASP price erosionsÿ Offset by unit growthÿ OLEDs boost segment 2008

n Signs & Displays growthÿ Brighter, full color +

n Expanding deploymentAutomotive applicationsÿ Tail Light adoption 2006ÿ 2008 – Forward Lighting

n Illumination enters commercialgeneral lighting market slowlyÿ increasing momentum 2010

Sources: OIDA, Strategies Unlimited (historic data), iSupply, IoP, Yole Developpment, OITDA

The rise of the HBLED…

Opportunities are now outside comms

Michael Lebby ([email protected])

n Complex market segmentsÿ Mobile Appliance segment more matureÿ More growth still ahead for Signs & Displays, Automotive, & Illumination

– Illumination may get further kick from government initiatives

0.00

500.00

1000.00

1500.00

2000.00

2500.00

3000.00

Re

ve

nu

e (

$M

illi

on

s)

Mobile Apps. Signs/Displays Automotive Signals Illumination Other

HB LED Forecast by Market Segment: 2005-2012

2005

2006

2007

2008

2009

2010

2011

2012

Sources: OIDA, Strategies Unlimited (historic data), iSupply, IoP, Yole Developpment, OITDA

All segments with positive vectors

HBLEDs forecast to grow quickly

Michael Lebby ([email protected])

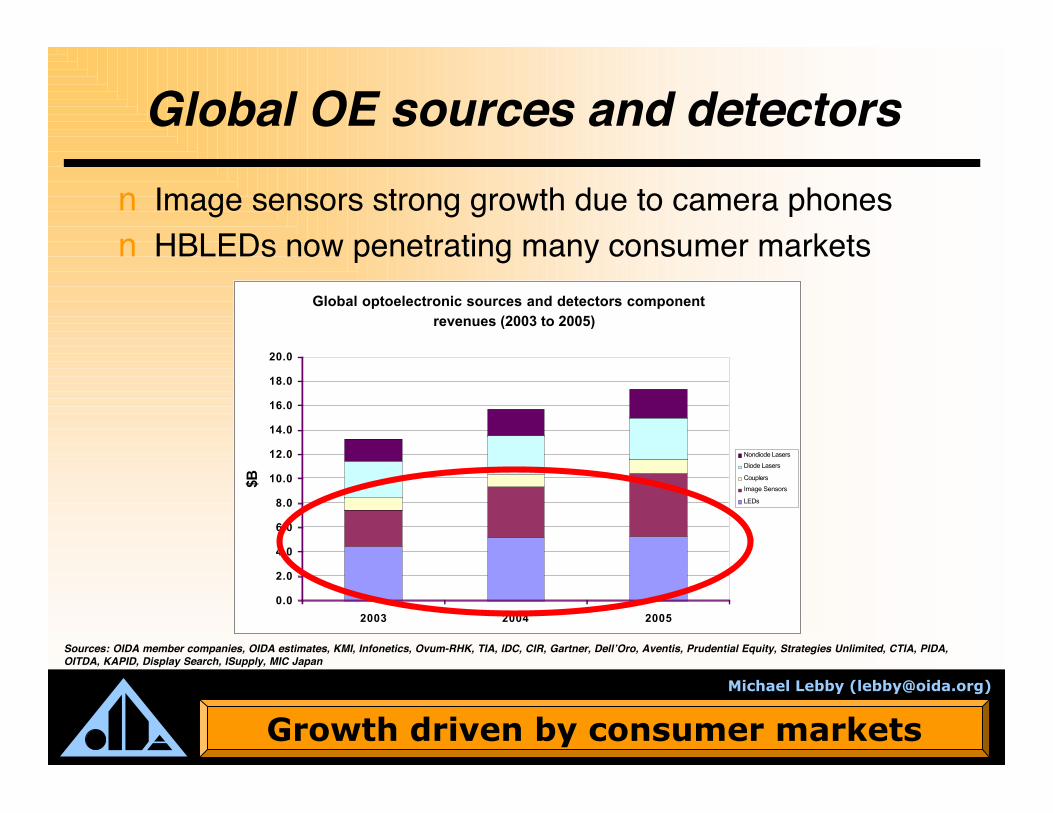

LED driving innovationsn 48 LEDs (sorted from 10K) – 18 red, 20 green, 10 bluen Folded light guide technology

Sources: DisplaySearch, NEC

Green LED performance low

2 Green LEDs to every 1 red and blue

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

Image sensors

Michael Lebby ([email protected])

Image sensor marketn Driven by camera phones

ÿ Security and automotive exciting areas to watch

Image Sensor Market Forecast

0.000

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

2005 2006 2007 2008 2009 2010

Rev

enu

e ($

Bill

ion

s)

Other (manufacturing, scanners,defense & aerospace)

Interactive Devices Inc. Toys

Automotive

Medical & Scientific

Security Devices

PC Cameras

Video Camcorders

Digital Still Cameras

Camera Phones

Sources: Strategies Unlimited, Micron, IC Insights, NE Asia, OIDA

New opportunities emerging

Michael Lebby ([email protected])

Image sensor technologyn CMOS is now dominant through consumer volume

applications

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Rev

enu

e (B

illi

on

s)

2004 2005 2006 2007 2008 2009 2010

Image Sensor Forecast

CMOS

CCD

Sources: Strategies Unlimited, Micron, IC Insights, NE Asia, OIDA

CMOS now cost effective

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

Photonic sensors

Michael Lebby ([email protected])

Photonic Chemical (Gas) Sensors

$3.0 Billion

$1.2 Billion

Fiber Optic Point & Distributive Sensors

Photonic Biomedical Sensors

$0.9 Billion

Photonic Sensor Market Potential (2009)

Strong opportunities in sensing

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

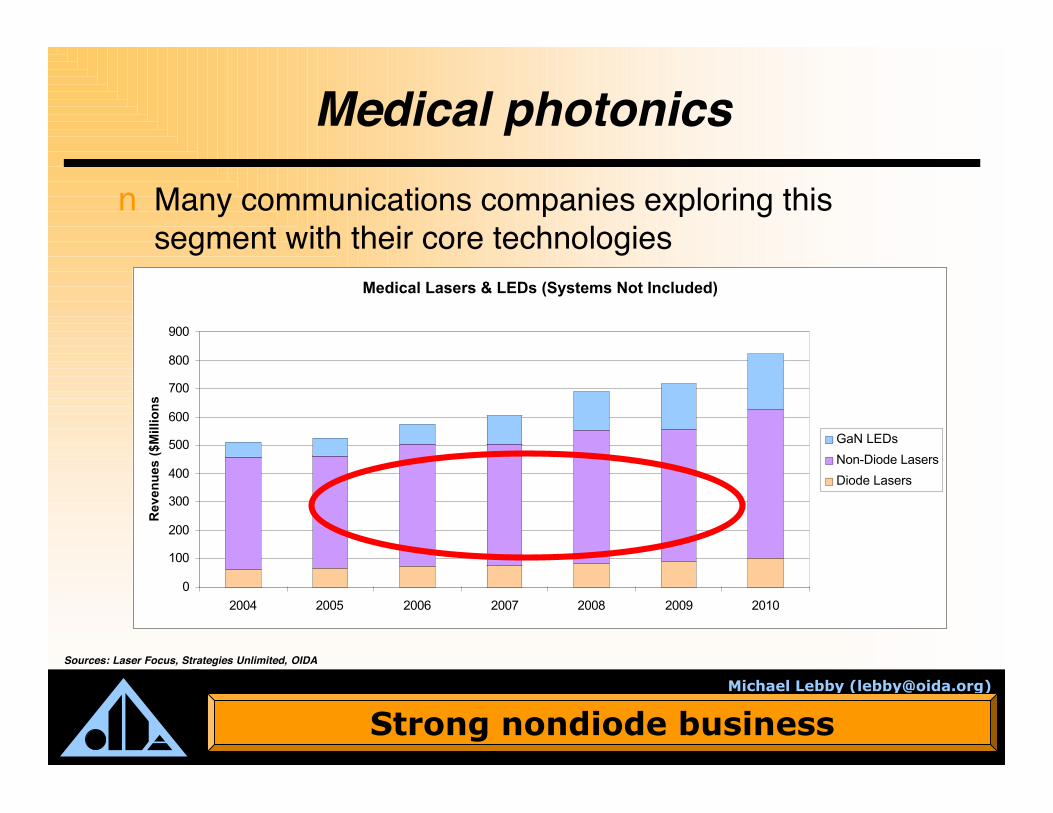

Medical photonics

Michael Lebby ([email protected])

Medical photonicsn Many communications companies exploring this

segment with their core technologiesMedical Lasers & LEDs (Systems Not Included)

0

100

200

300

400

500

600

700

800

900

2004 2005 2006 2007 2008 2009 2010

Rev

enu

es (

$Mill

ion

s

GaN LEDs

Non-Diode Lasers

Diode Lasers

Sources: Laser Focus, Strategies Unlimited, OIDA

Strong nondiode business

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

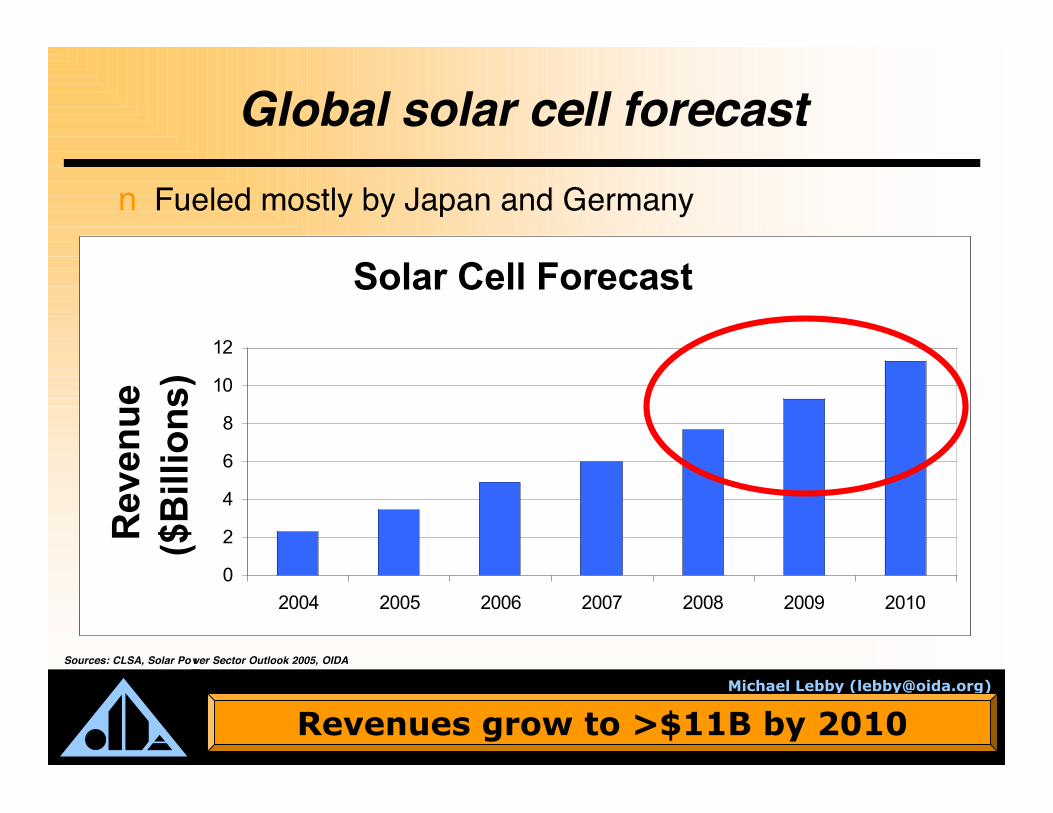

Solar

Michael Lebby ([email protected])

Global solar cell forecastn Fueled mostly by Japan and Germany

Solar Cell Forecast

0

2

4

6

8

10

12

2004 2005 2006 2007 2008 2009 2010

Rev

enu

e ($

Bill

ion

s)

Sources: CLSA, Solar Power Sector Outlook 2005, OIDA

Revenues grow to >$11B by 2010

Michael Lebby ([email protected])

Silicon based photovoltaic value chainn Improved cell efficiency means fewer modules are

needed for same power productionn Wafer costs could be reduced further with panels

Source: Ilan Gur – University of California, Berkeley

Innovative manf like displays is needed

Michael Lebby ([email protected])

Printing approaches to solar cellsn Organic carbon based inks technologyn Printing process allows continuous roll process

ÿ Lower capital investment (no clean room, vaccum, or silicon)

Source: Konarka

Capital investment in plant: big driver

Michael Lebby ([email protected])

Manufacturing focusedn CIGS (copper indium gallium diselenide) materials

Improved efficiencies ~20% today

Source: Thin Film Physics Group – ETH Zürich

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

80

60

40

20

0

Effi

cien

cy, h%

0 100 200 300 400 500Cost per Area $ / m2

$3.50/W

$1.00/W

$0.50/W$0.20/W$0.10/WThermodynamic Limit

∞ Junction Limit

5-6 Junction Limit

Single Junction Limit

SunPower h 21.5% cell

Legend

Shell h 14% cell

Sharp h 15% cell

Sanyo h 19% celln

n

BP Solar h 14.2% celln

n

2ND

Actual Data

Thin film today

Solar roadmap 2005

New DARPA program

3RD

OIDA Solar cell platform roadmap

Roadmapdevelopment

path

4TH

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

OIDA: comparingroadmaps…

Michael Lebby ([email protected])

European nanotechnology roadmap

Sources: BMBF, Optech-netMarket readiness0-5 years5-10 years10-15 years

Electronics/Infotechnology

Automotiveconstruction

Medicine / LifeScience

Energy/Environmenttechnology

Chemistry /Materials

Precision mechanics/optics / analysis

DiscoveryResearch

Technicalprototypes

ApplicationInnovation

DistributionDiffusion

Diode Laser

OLED

Anti-reflection coatings

Dye solar cells

White LEDs

X-ray optics

Quantum dot solar cells

NEMS

Trends towards advanced analysis

Michael Lebby ([email protected])

2005 2010 2011 20122009200820072006

Nano-Bio ChipBio-photonics Senser& analysi

s

Med-display

Field

Carbon Nano tube

Photon detector

Digital X-ray detector

Advanced X-ray/CT display

Fix(CO2)

H2 production

Surface treatment & Bonding

Photonics-Catalysis

Advanced ultrasonic display

Med- display (transfer)

Trends of advancing technologies

Source: KAPID (Korea)

Korean biophotonics roadmap

Michael Lebby ([email protected])

OIDA Bio-nano-photonics trends roadmap2005 2009 2013 2017

Technology level

Biocompatiblein-vivo

nanodevices

Nanodevicebiometricsensing

Nano biolabelingand diagnosis

Multianalyte DetectionBiorecognition MoleculesFluidicsIn-vivo sensorsChemical ID BiosensorsData processing, PatternRecognition, Automation

Michael Lebby OIDA (2006)

OIDA

Patterning biorecognition elementsCoupling biorecognition elementswith arrays of detectors and emittersImprint technologies for patterningReal time monitoringLong term stability testing

Functional biorecognitionelements with opto devices

Diagnosis reagents Drug delivery Implantable biosensing Biobatteries(nano spheres/capules)

(optically sensitive devices) Bioenergy cells

Nanodevice signal transport Nanobiosensors Neuro chips/devices

Nanosensor arrays Artificial retina/olfactory/taste

Nano biolabeling Nanoparticle biolabeling Nanoparticle biochips

Nanoparticle diagnosis reagent Biosafety

Trends towards advanced applications

Michael Lebby ([email protected])

OIDA Sensor Roadmap

Highway sensingSmart highways (tolls)Pollen sensingInformation sensingWeather, UV sensing

2005 2009 2013 2017

Health Care(medical,

welfare, health)

Data(highway, living,

society)

Environmental(industrial,

energy,agriculture)

Advancedtechnology

O2 monitoringGene therapyLaser therapyUV monitorsGlucose monitoringPulmonary monitoring

Michael Lebby OIDA (2006)

OIDA

Optical mammographyMicro chemistryMetabolism monitoringPartially automated diagnosisGlucose monitoringGene monitoring

Optical computedtomographyFully automated diagnosisWellness monitoringSickness forecasting

Advanced highway sensingLaser based cruise controlStress & fatigue sensingPollen sensingInformation sensingWeather, UV sensing

Auto network infrastructuremm-wave cruise controlLifestyle orientated networksOdor, taste sensing

NOx, Sox, DioxinForest, river ocean,atmosphere monitoring

Crisis mgt (tsunami, flood)Sensing networkEnergy storage sensing

Environmental networksFemtosecond photonprocessing

Industrial lasersNano-sensingPlastic decompositionAgricultural photonicsFemtosecond lasersSingle photon measuring

X-ray lasersTHz frequency sensingPlastic decompositionHigh harmonic sensingGlobal monitoring

Alto-second pulse sensingQuantum non-destructivemeasuring/monitoringGlobal environmentsimulator/modeling

Trends towards integrated sensing

Michael Lebby ([email protected])

Evolution of treatment: from single- tomulti-functional nanotech platforms

Content density device complexity

Tre

atm

ent

Eff

ecti

ven

ess

1) ‘Nano’ in-vitro sensorsEarlier diagnostics

2) Traditional therapy

1) ‘Nano’ in-vitro sensorsEarlier diagnostics

2) Localized nano-therapyMore effective treatment

Reduced site effects

1) Quantitative in-vivonano-sensors

Further improved diagnostics

2) Localized nano-therapyMore effective treatment

Reduced site effects

Source: NIH-NCI

Roadmap to more complex treatments

Research demonstrations

In-vitro – recognizesample from body

and interrogate

In-vivo – better selectivescreening and

recognizing biomarkers

OIDA Nano-photonics cancer platforms roadmap

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

DARPA/OIDA new R&Dmatching program

Michael Lebby ([email protected])

University Photonics Research (OE Centers)n DARPA/MTO funds 4 University Consortiums for photonics research

ÿ Novel materials, devices, system on a chipÿ In 2nd year of 4 year program

n DARPA would like UPR Centers to have industry collaboration toaccelerate specific programs for development

n DARPA is willing to match industry participationÿ Trending towards 50% DARPA, 50% Industry (post doc)ÿ Post doc will work on specific industry interest to accelerate project through

researchÿ Expectation

– 10 accelerating programs (DARPA total commitment $500k)– Per person: $100k (ie $50k match)– Type of match TBD

DARPA wants industry supporting R&D

Michael Lebby ([email protected])

Summaryn Optoelectronics market is now vibrant

ÿ Consumer/entertainment driving growth todayÿ OE penetration in many new markets, driven by displays

n Key trendsÿ Displays – the LCD gathers momentum; OLEDs grow quicklyÿ HBLEDs: solid state lighting and automotive excitingÿ Image sensing, fiber sensors, lasers and solar vibrantÿ Consumer products multiply with optoelectronics

n OIDA now very active…ÿ Bringing industry closer to academia…ÿ Helping DARPA match projects between industry/academia

OIDA is Optomistic J

OPTOELECTRONICS INDUSTRY DEVELOPMENT ASSOCIATION

End

Michael Lebby ([email protected])

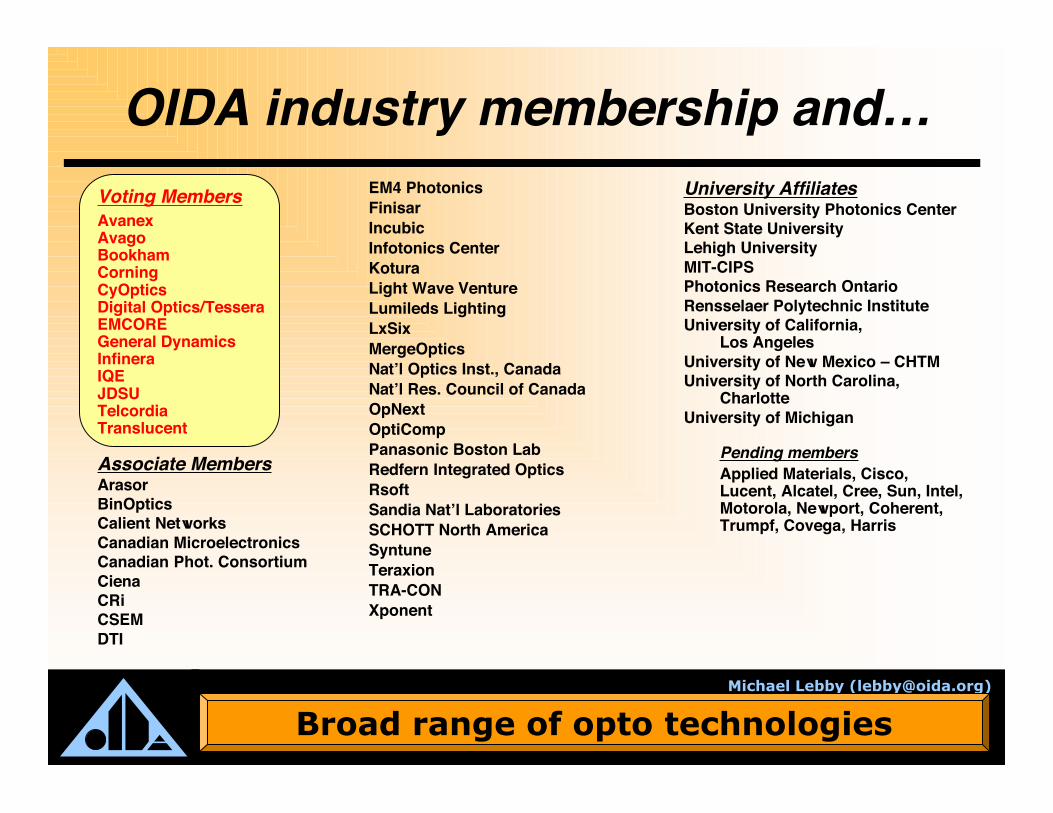

OIDA industry membership and…Voting MembersAvanexAvagoBookhamCorningCyOpticsDigital Optics/TesseraEMCOREGeneral DynamicsInfineraIQEJDSUTelcordiaTranslucent

Associate MembersArasorBinOpticsCalient NetworksCanadian MicroelectronicsCanadian Phot. ConsortiumCienaCRiCSEMDTI

EM4 PhotonicsFinisarIncubicInfotonics CenterKoturaLight Wave VentureLumileds LightingLxSixMergeOpticsNat’l Optics Inst., CanadaNat’l Res. Council of CanadaOpNextOptiCompPanasonic Boston LabRedfern Integrated OpticsRsoftSandia Nat’l LaboratoriesSCHOTT North AmericaSyntuneTeraxionTRA-CONXponent

University AffiliatesBoston University Photonics CenterKent State UniversityLehigh UniversityMIT-CIPSPhotonics Research OntarioRensselaer Polytechnic InstituteUniversity of California,

Los AngelesUniversity of New Mexico – CHTMUniversity of North Carolina,

CharlotteUniversity of Michigan

Pending membersApplied Materials, Cisco,Lucent, Alcatel, Cree, Sun, Intel,Motorola, Newport, Coherent,Trumpf, Covega, Harris

Broad range of opto technologies

Michael Lebby ([email protected])

OIDA – OSA Affiliate Members3M Company Electro-Optics Technology Inc Morgenthaler Ventures Promex Industries Inc

4D Technology Corporation Elliot Scientific Ltd MPB Communications, Inc Quantronix LasersAculight Corp ELS Elektronik Laser System GmbH New Focus Inc Quintessence Photonics Corporation

ADE Phase Shift EM4 Inc New Scale Technologies R Bradley & Assoc LTDAdvanced Glass Industries Engineering Synthesis Design Inc Newport Corporation Rainbow Research Optics, Inc.

Advanced Photonix, Inc. Essex Corporation nLight Photonics Corp Raydiance, IncAerodyne Research, Inc. Fiberguide Industries, Inc. Northrop Grumman Information Technology RED-C Optical Networking

Aerotech Inc Fiberxon, Inc. NP Photonics Inc Research Electro-Optics, IncAFL Telecommunications Fresnel Technologies Inc NSG America Rochester Precision Optics

Albert Einstein College of Medicine Gemfire Corp Nufern Rockwell Science Co LLCAlpine Research Optics Goodrich Corporation Ocean Optics Inc RPC Photonics Inc

Apogee Photonics Inc Greater Rochester Enterprise OFR Inc, Optics for Research RSoft Design GroupAPPLIED IMAGE Group Griot Group Inc OFS, Specialty Photonics Division S.I. Vavilov State Optical Institute

ARIA Technologies, Inc. G-S PLASTIC OPTICS Olympus Integrated Tech America Inc Santec CorporationASML Optics LLC Hamamatsu Corporation Omega Optical Inc Santur Corporation

Aurora Optical Hardin Optical Co. Ophir Optronics Inc Scintera NetworksAvo Photonics Harrick Plasma Opnext Inc Scottish Development International

Barr Associates Inc Headwall Photonics Inc Optical Air Data Systems SENKO Advanced Components IncBinOptics Corp Horiba Jobin Yvon Inc Optical Research Associates Siskiyou Corporation

Bioptigen Ibsen Photonics A/S Opticorp Inc Special Optics IncBreault Research Organization Inc IMRA America Inc Optics for Devices, SCHOTT North America Spectra-Mat Inc

Bright View Technologies InPhenix, Inc Optics Technology Inc Spiricon IncCalifornia Eastern Laboratories INRAD Inc OpticsProfessionals LLC Summers Optical

Cambridge Technology Inc Intel Corp Optigo Systems Sutter Instrument CoCambridge University Press Ionic Systems Optikos Corporation Sydor Optics Inc

CDM Optics Inc IPG Photonics Corp Optimax Systems Inc TeachSpin IncCentral Glass & Ceramics Res Inst JDS Uniphase Corp OptiPro Systems Technical Manufacturing Corporation

CEYX Technologies Inc JMAR Technologies, Inc. Optiwave Corporation Tempo Plastic CoChang Chun Bo Xin Photoelectric Co., Ltd. Kapteyn-Murnane Laboratories Optometrics Corporation TeraXion, Inc

Checkpoint Technologies, LLC KoSearch Inc OptoSigma Corporation The Institute of OpticsChristie Associates Kotura, Inc. Orbits Lightwave, Inc. Thorlabs Inc

Chroma Technology Corp LabNow, Inc. OZ Optics, Ltd Tinsley/SSG PrecisionCoherent Inc LaCroix Optical Co Pacific Biosciences, Inc. Toptica Photonics Inc

ColorChip, Ltd. Lambda Research Corporation Palomar Technologies Tower Optical CorpConoptics Inc Laser Focus World PD-LD Inc u2t Photonics AG

Corning Inc Lasertel Inc Pennsylvania State University Univ of Arizona Optical Sciences CenterCovega Corporation Light Brigade, Inc Pentax Corp University of Central Florida, CREOL

CRI Inc LINOS Photonics Inc PFG Optics US Conec LtdCrystal Fibre Louis Rudzinsky Associates Inc Photonics Industries International Inc Verrillon Inc

CVI Laser LLC Lumen Flow Corporation Photonics On-Fiber Devices Inc VPIsystemsDel Mar Photonics Inc Lumetrics Photonics Spectra Wafer World Inc

Delta F Corp Luna Technologies, Inc Photop Koncent, Inc Xponent Photonics IncDeposition Sciences, Inc. Lydall Inc. PI (Physik Instrumente) L.P. Zygo Corporation

Diamond USA Inc Market Tech, Inc. piezosystem jena GmbH piezosystem jena GmbHDigital Optics Corp Massachusetts Inst of Tech Lincoln Lab Polatis, Inc. Polatis, Inc.

Directed Energy Solutions Meadowlark Optics Polymicro Technologies Inc Polymicro Technologies IncDSS Melles Griot Inc Precision Photonics Corporation Precision Photonics Corporation

Edmund Optics Merck KGaA Princeton Lightwave, Inc. Princeton Lightwave, Inc.

~ 250 Companies Represented

192 companiesrepresented

HighlightedCompanies(10) are alsoFull OIDAMembers