Embed Size (px)

Citation preview

John Peace

Chairman

Positioning for next phase of growth

Leadership transition

Major infrastructure investment

Key retail initiatives

Completed evolution to fully public company

2005/06 Highlights

Rose Marie Bravo

Chief Executive

Revenue

£742.9

£499.2

£675.8

£593.6

£715.5

2005/20062001/2002 2002/2003 2003/2004 2004/2005

Retail Wholesale Licensing

Year Financial Highlights (millions)

EBIT

2001/2002(1) 2002/2003(1) 2003/2004(1) 2004/2005(2) 2005/2006(3)

Year Financial Highlights (millions)

£90.3

£116.7

£142.6

£161.3 £165.6

Margin 18.1% 19.7% 21.1% 22.5% 22.3% (1) Under UK GAAP, excluding goodwill amortisation and exceptional items(2) Under IFRS(3) Pre-Atlas costs

£154.5Pre-Atlas

Diluted EPS

12.1p

2001/2002(1) 2002/2003(1) 2003/2004(1) 2004/2005(2) 2005/2006(2)

(1) Under UK GAAP, excluding goodwill amortisation and exceptional items(2) Under IFRS

Year Financial Highlights

14.6p

19.1p

22.2p24.1p

22.3pPre-Atlas

Products Channels Regions Atlas

Revenue by Product Category

Womenswear34%

Menswear28%

Accessories25%

Licensing11%

Other*2%

* Includes childrenswear

Underlying Growth

1H 2H Y

Womenswear 1% 6% 3%

Menswear 4% 3% 4%

Accessories 2% (2)% 0%

2005/06

Strong editorial response

Attracting new client

Strong sell-throughs

New marketing thrust

Voted top 10 women’s collection (WWD Fall 06)

Prorsum Runway

SS06 Campaign

Merchandising cornerstone

Reinvigorating the classics

Strong Spring season for coats, trenches, quilts

Outerwear

Spring/Summer 06

Second half strength

Reflects product adjustments

Improved product flow

Womenswear

Spring/Summer 06

Consistent performance

Ongoing product efforts

Customisation

Menswear

Spring/Summer 06

New merchandise direction

Continued investment

Handbag reorientation

Accessories

Spring/Summer 06

Fragrance

Licensing

Strength in product licenses

Eyewear in transition

Watches on track

Kate Moss

Underlying Growth

1H 2H Y

Retail 9% 13% 11%

Wholesale (1)% (7)% (4)%

Licensing 3% 8% 6%

Channels

Wholesale46%

Retail43%

Licensing11%

2005/06

2005/06 ActivityRetail

20% total revenue growth

– 25% second half

8% underlying space growth

– excludes Taiwan and Spain conversion

New stores/ Refurbishments/Concessions Expansions

US San Antonio, TX Philadelphia, PA

San Diego, CA Boston, MA

Naples, FL Denver, CO

Palm Beach Garden, FL Washington, DC

Outlets (3) Westchester, NY

EU Zurich (R) Frankfurt

ECI conversion (72) Munich

Concessions (7)

Outlets (3)

Asia Taiwan acquisition HK Sogo

Concessions (2)

2006/07 PlansRetail

14 new stores and concessions

Minimum 10% underlying space expansion

New stores/ Major Refurbishments/Concessions Expansions

US Atlantic City, NJ

Kansas City, MO

Northbrook, IL

Riverside, NJ

Outlets (2)

EU Madrid Regent Street, London

Concessions (3)

Asia Sydney Ocean Centre, HK

Concessions (3) Concessions (6)

Spain ConcessionsRetail

ECI Diagonal, Barcelona

International Wholesale

Emerging Markets

Outstanding gains in 2005/06

Opened 9 stores

Five stores planned for 2006/07

Warsaw, Poland

Wholesale

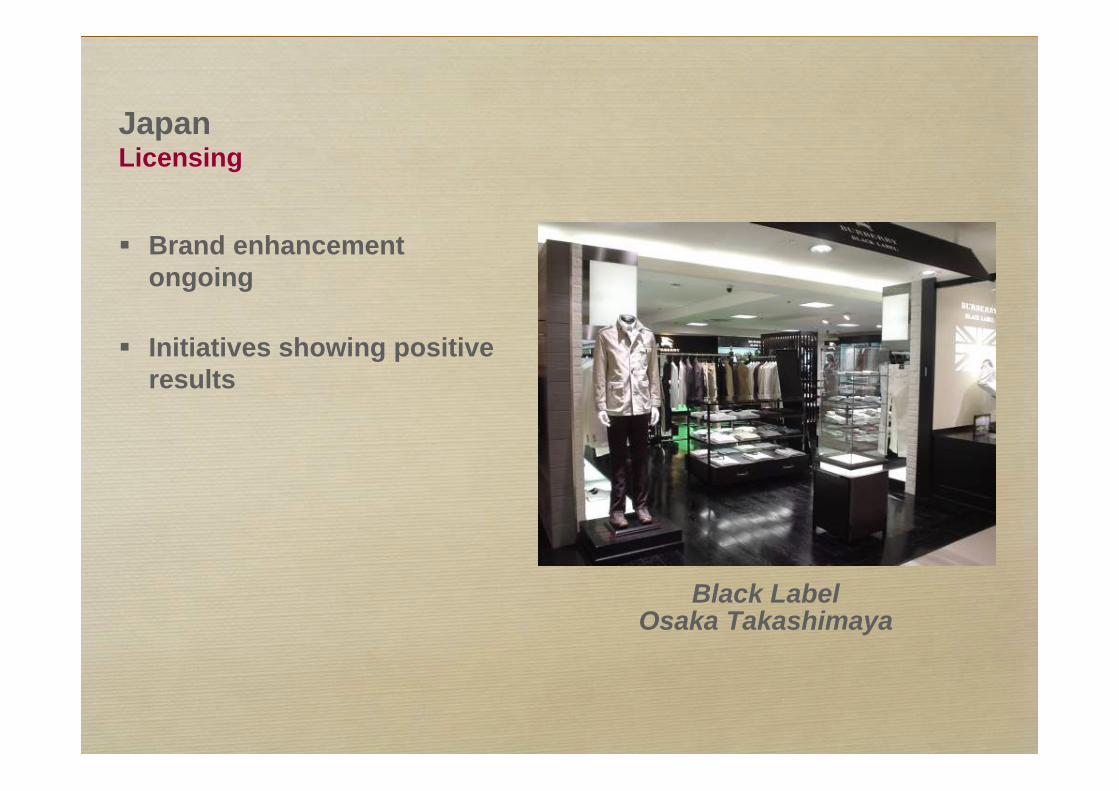

JapanLicensing

Brand enhancement ongoing

Initiatives showing positive results

Black LabelOsaka Takashimaya

JapanImports

AW06 import initiatives

– key categories

– leathergoods test

Prorsum concessions

Work in progress

Tokyo Subway Station

Stacey Cartwright

Chief Financial Officer

Financial Highlights(1)

(1) As reported under IFRS(2) Underlying figures are calculated at constant exchange rates, and exclude the effects from the Taiwan acquisition and Spain transitions

Year to 31 March

Turnover 715.5 742.9 4% 3%

Operating Profit before 161.3 165.6 3% 5%Atlas

Atlas cost - 11.1 - -

Diluted EPS before Atlas 22.2p 24.1p 9% -

Dividend per share 6.5p 8.0p 23% -

Dividend payout ratio 29% 33%

2004/05£m

2005/06£m

% GrowthReported Underlying (2)

Growth

– 5% reported

– 3% underlying

Turnover6 Months to 31 March

£367.5m£10.9

(£2.3) £384.3m

2004/05 2005/06Exchange rates

Underlying growth

Conversions

£8.2

Growth

– 24% reported

– 13% underlying

9% space increase

Retail Revenue6 Months to 31 March

2004/05 2005/06Exchange rates

Underlying growth

Conversions

£154.5m

£19.6 £6.6£11.5 £192.2m

Decline

– 13% reported

– 7% underlying

Key markets

– Spain

– US

Wholesale Revenue

2004/05 2005/06Exchange rates

Underlying growth

Conversions

£173.9m

6 Months to 31 March

(£11.8)(£13.8)£2.3

£150.6m

Growth

– 6% reported

– 8% underlying

Japan up high single digits

– royalty rate increase

Global licenses

– generally solid gains

Licensing Revenue6 Months to 31 March

2004/05 2005/06Exchange rates

Underlying growth

£39.1m£3.1 (£0.7) £41.5m

220bps gross margin expansion

Stronger collections

– AW05: lower mark downs

– SS06: good early response

Channel mix

Gross Profit Margin6 Months to 31 March

Second half2004/05

Second half2005/06

59.9% 62.1%

Operating Expenses before Atlas Costs6 Months to 31 March

Expanded retail network

– conversions

Investing in infrastructure

150th anniversary marketing

Exit GUS pension scheme

Second half2004/05

Second half2005/06

37.1%39.7%

Underlying growth

– H1 6%

– H2 5%

– FY 5%

EBIT before Atlas Costs6 Months to 31 March

£83.7m £3.8 £1.0 (£2.4)

2004/05 2005/06Exchange rates

Underlyinggrowth

Conversions

£86.1m

EBIT Margin

Pre Atlas costs

Retail and wholesale 14.8% 14.3% 14.5%

Licence 85.5% 85.4% 85.6%

Total 22.5% 22.2% 22.3%

Post Atlas costs

Total 22.5% 21.4% 20.8%

2004/05 First Half Year

Year to 31 March

2005/06

Cash Flow from Operations

EBIT (1) 161.3 165.6

Atlas costs – (11.1)

Depreciation and similar charges 24.4 24.9

Increase in stocks (12.9) (17.8)

(Increase)/Decrease in debtors (7.3) 2.2

Increase/(Decrease) in creditors 1.5 (21.2)

Other 8.4 5.8

Cash flow from operations 175.4 148.4

£ millions 2004/05 2005/06

(1) Before Atlas costs

Cash Flow

Cash flow from operations 175.4 148.4

Net interest 4.7 1.6

Capex (37.2) (30.7)

Property sales proceeds 3.1 3.6

Net acquisition related - (23.6)

Tax paid (49.5) (43.6)

Cash inflow before financing 96.5 55.7

£ millions 2004/05 2005/06

Year to 31 March

Capital Management

Cash neutral balance sheet

Completed £250 million repurchase programme

– £192 million repurchased in 2005/06

– £12.5 million net cash position at March 2006

Ongoing plans

– share repurchases consistent with capitalisation strategy

2005/06 ActivityAtlas

£50m programme over 3 years

P/L benefits in excess of £20m pa by 2007/08

Strong foundation

Moving from design to implementation

Firmly embedded in business

Expensed £11 million in 05/06Atlas

2006/07 PlansAtlas

Phase I Phase II Phase III

2006 2007

Treasury

Global Sales & Stock Analytics

UK/Europe & Corporate

US, Korea, HK & Taiwan

Post Implementation Support & other regions

2006/07 Outlook

Retail

– minimum 10% space expansion

– 14 new stores and concessions

Wholesale: H1 up low single digit underlying

Licensing: broadly flat underlying relative to 2005/06, with yennegative impact

Capital expenditures approximately £50 million

Atlas P/L benefits approximately £6mAtlas costs approximately £19m

Angela Ahrendts

Chief Executive Designate

Operational Excellence

Back end of the

business

Front end of the

business

Product: Multi-category Cross-Generational Appeal

Retail Led Growth

Invest in High Potential Growth Markets

Leveraging the Franchise

New York, 57th Street

Disclaimer

Certain statements made in this announcement are forward lookingstatements. Such statements are based on current expectations and are subject to a number of risks and uncertainties that could cause actual results to differ materially from any expected future results in forward looking statements.

This announcement does not constitute an invitation to underwrite, subscribe for or otherwise acquire or dispose of any Burberry Group plc shares. Past performance is not a guide to future performance and persons needing advice should consult an independent financial adviser.

![WEAPON STORES MANAGEMENT SYSTEM (SMS) · 2020-06-26 · stores management solutions enhanced stores management computer (e-smc)[2.3 [4.1 lbs.] stores control panel (scp) lbs.] gun](https://img.pdfslide.us/doc/110x75/5f33c89021254a014f59118c/weapon-stores-management-system-sms-2020-06-26-stores-management-solutions-enhanced.jpg)