Embed Size (px)

Citation preview

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 1/65

ONLINE TAX

MONITORING

SYSTEM AND

MANAGEMENT

1

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 2/65

A RESEARCH PROJECT SUBMITTED TO THE DEPARTMENT OF

COMPUTER SCIENCE

IN PARTAL FULFILMENT OF THE REQUIREMENT FOR THE

AWARD OF THE HIGHER NATIONAL DIPLOMA IN COMPUTER

SCIENCE.

NOVEMBER 2009

2

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 3/65

CERTIFICATION

We hereby certify that this research project was carried out by

....................................................

for the award of NATIONAL DIPLOMA CERTIFICATE, in computer

science

__________________ ______________

DATE

Project supervisor

_________________ ________________

DATECentre co-ordinator

3

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 4/65

DEDICATION

This research project is dedicated to the Almighty God for

His ever enduring love, kindness, mercy and grace all

through the course of this programme. Father, I thank and

worship you and give You all the Glory and Honour.

4

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 5/65

ACKOWLEDGEMENT

To God be the glory for it’s not by my power nor my might but by His

grace that is superfluous and more than sufficient. I thank for Him

making this programme a reality.

I am also grateful to my supervisor Mr Emmanuel Nelson Bassey for

his painstaking and thoroughness in supervising this project.

I acknowledged the immense support I received from my family for

their encouragement during the period of the programme.

This acknowledgement will be incomplete without noting the

contribution of the following people to the success of the programme,

the registrar and her assistance in Warri Continuing Centre and other

friends who had contributed in one-way or the other to the successful

completion of the programme.

A special word of thanks go to all staff of C.A.C.T. Publishers in

typing the various draft of the manuscript.

I wish to conclude this acknowledgement by expressing my sincere

appreciation to all my colleagues for their friendly disposition towards

5

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 6/65

me during the period of the programme. MAY GOD BLESS YOU

ALL.

6

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 7/65

A B S T R A C T.

In this project, attempt was made to examine the online tax

monitoring system and management in Edo State and critically look

into the hindrances on tax in this regard.

The writer critically looked into the short comings of tax control

system and management, which lead to the establishment of the

objectives of the study which included; the establishment of existence

of tax avoidance and evasion in Edo State; exploring the causes,

assessment of the extent of revenue generated and adoption of the

online tax monitoring system ; and suggest possible ways of

improving the efficiency of the system.

In order to arrive at a conclusive decision on the above objectives the

writer carried out an empirical survey and library research from which

the various data were obtained. Based on the data, three hypothesis

formulated by the researcher was tested using Chi-square analysis to

arrive at a better conclusion. The hypothesis testing was based on

7

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 8/65

primary data while the secondary data were further analyzed to

portray the state of affairs at various periods.

After careful analysis, it was discovered that revenue generated over

the years represents over 60% of the internally generated revenue.

However, the study revealed that state has potentials to double the

present effort but for the high level of tax evasion and avoidance

prevalent in the society.

8

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 9/65

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 10/65

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 11/65

4.4 Methods -- - - - - - - - 43

4.5 Events -- - - - - - - - 43

CHAPTER FIVE IMPLEMENTATION, RECOMMENDATION

AND CONCLUSION.

5.1 Implementation - - - - - - - 45

5.2 System modification - - - - - - 46

5.3 System testing - - - - - - - 49

5.4 Change over technique - - - - - 49

5.5 Conclusion - - - - - - - - 50

5.6 Recommendation - - - - - - 51

11

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 12/65

CHAPTER ONE

INTRODUCTION

1.1 THE BACKGROUND OF THE STUDY:

State tax systems have generally not changed dramatically

over the last few decade, yet they are facing profound

challenges. Increased international trade, the advent of

electronic commerce, evolving federal-state relations, and

interstate competition are just some of the developments that

will have a powerful influence on how states collect revenue.

This research project addresses a wide variety of issues

concerning the major sources of state tax revenue and provides

insight into what has worked in the past and what will or will not

work in the future.

State tax systems are in trouble. Revenue collection methods

developed more than a half-century ago are facing the strain of

dealing with 21st century economies. Globalization and e-

commerce are changing the way people work and purchase

goods, devolution has steadily shifted responsibility from the

12

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 13/65

federal government to the states, and tax incentives have

become the weapon of choice in the battle to attract business

investment.

Local governments across the States (EDO STATE) are

struggling to raise revenue to pay for public services. Increased

demands by citizens for more and better services; the ever-

rising costs of providing services; and a plethora of legal and

political restrictions on raising tax revenue have left many local

governments in dire fiscal straits. The problem is that the fiscal

autonomy of local governments has been declining for several

decades. By ceding financial control to the states, localities

cede political control over their affairs. Paralleling this loss of

financial and political control, local governments are losing

control over the property tax, their most stable and reliable

source of revenue.

13

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 14/65

In this research work, the researcher will analyze these and

other critical challenges facing state governments. He will

identify the important issues, and examines possible solutions

in formulating and implementing state tax policy as information

technology is the order of the day.

With the advent and introduction of the computer equipment in

Nigeria in 1960s, the Nigeria economy which has passed

through porous and substandard accounting methods was

transformed into modern and international standard. Hence, the

adoption and application of modern equipment (online tax

monitoring system) in collecting of taxes will be of immense

important.

Not only is the effective and fair collection of taxes an essential

government function, but it also forms one of the primary points

of interaction between most citizens and the federal

government. Consequently, any improvement in this process

not only will increase the effectiveness of the government but

also will reduce the frustrations of taxpayers. Since the

14

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 15/65

proposed tax system is an information-intensive activity, it can,

in principle, benefit from modern information technology to

improve quality of service and efficiency simultaneously.

Government today has benefited from information technology in

many ways. The importance of understanding and influencing

citizens' acceptance of e-government services is critical, given

the investment in technology and the potential for cost saving.

Nothing the impact on the way taxes are administered and the

information technology revolution. This research work will adopt

the use information technology to improve taxpayer service,

compliance, and revenue performance.

Information technology will change the boundaries of tax

administration from isolated single tax administrative units, to

unified tax authorities that administer all taxes including the

functions of customs. Information sharing by the many areas of

tax administration is the key to reducing compliance costs

borne by taxpayers, as well as enhancing the levels of

voluntary compliance with tax laws.

15

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 16/65

Private sector service providers are becoming an integrated

part of the administration of taxes. The tax administration

system of the future is likely to operate much more like the

service oriented financial services sector of the present, than

the heavy handed, and too often corrupt, bureaucratic

institutions of the past.

This research work will provides some insight into what is being

done now, including a sobering discussion of the

implementation problems being faced, in order to bring the

possibilities of the information technology revolution into the

reality of tax administration.

1.2 OBJECTIVES OF THE STUDY:-

The objective of this study is to create an online tax monitoring

system for tax payers in Edo State. It strongly belief that filing

taxes online will be inexpensive, accurate, fast and easy. The

need for this online tax monitoring system for the state is that:

• The tax payer’s service will be improved.

16

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 17/65

• It will help to modernise the internal revenue service.

In this research work seeks to cover major aspect of tax

operations in the state and also design an online tax monitoring

system that will achieve the following:

• Provide/maintain a unique record for every tax payer(tax

payer’s personal data).

• Provide fast access, modification, updating and rerieval of

tax payer’s records and other information by the database

administrator.

• Security of information.

1.3 SCOPE OF THE STUDY

This research will give an overview of online tax monitoring

system as well as the description of various tax system

available.

Other areas of coverage will be the description of the system

design of the proposed prototype of an online tax system and

the implementation of the system.

17

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 18/65

1.4 SIGNIFICANCE OF THE STUDY:-

The research work will be significant to the following group of

people:

Members of the society (individual tax payer): This tool will not

only determine their eligibility, but can also determine their filing

status, and the number of qualifying children, and it can

estimate their credit amount.

To the government: more especially the Board of Internal

Revenue, Federal Board of Inland Revenue, Budget

Departments, Planning Departments and other government

decision makers, the study is useful as this will provide a

meaningful and well organised database.

The use of online tax tool to monitor and manage income to

government will reveal lapses and so many hindrances on tax

effectiveness which I have hope that if appropriate corrective

measures are taken, will go a long way in improving taxation

revenue which in turn will improve the provision of necessary

social and economic activities.

18

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 19/65

Finally, it will be of immense help to academicians and future

researchers in the field of taxation and computer science.

1.5 LIMITATION OF THE STUDY

The research is aimed at describing the online tax monitoring

system and management for Edo State.

The researcher is aware of a number of limitations of this study.

Actually, the problems encountered by the researcher includes:

difficulty in procuring materials for the project, time factor and

financial constraints.

1.5.1 Material Constraints

There were a lot of constraint as to means of getting materials

for this research work. The researcher’s visit to other higher

institution looking for materials necessary for the work and the

difficulty faced in extracting vital material for the work.

1.5.2 Financial constraints

19

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 20/65

The researcher would have carried out the research to cover

more than the defined scope but due to lack of money to pay

for café services and gathering of information within Benin city

and it environ.

1.5.2 Time Constraints

A lot of time was wasted as the researcher visited the

organizations, government offices, organized private sectors of

the economy to gather information for successful completion of

this research work.

1.6 RESEARCH METHODOLOGY

Information for this research study was gathered from various

angles as follows:

(1) The use of the Internet: Much of the materials were down-

loaded from the internet on online tax monitoring system and

the design of such system.

(2) The procedural manuals and past research

materials/projects on online tax were also used.

20

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 21/65

(3) Some of the information used were extracted from compact

disk that has related topic.

CHAPTER TWO

REVIEW OF RELATED LITERATURE

Nigeria is among other developing countries, transforming into

an information society where value is now based on the ability

to use, share and create knowledge and information. Obviously,

the success in the information society demands computer

literacy.

Online tax monitoring system is a web-based (computer-

based) program that allows all tax payers to pay their taxes

electronically. Tax payers can pay their taxes without writing a

cheque, or visiting tax office.

This web-based system (online tax monitoring system) will offer

many benefits over traditional paper-based filing:

21

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 22/65

o Fast. Because the system performs all the calculations,

filers only need to answer a few simple questions and

then either enter or upload their jurisdictional data.

o Accurate. The system uses the latest tax rates and

performs all calculations to ensure the accurate filing.

The system also includes verification steps during the

filing process to check for accuracy before returns are

filed.

o Convenient. The system is available via the Internet 24

hours a day, seven days a week. The system also offers

a "save" option, which stores partially completed return

which can be finished at a later time.

o Easy to Use. It will be very simple and easy to operate as

it will have Help command/menus available. For first time

users, a "demo" mode will be made available to

experience the filing process without actually filing a

return.

Secure. The system will maintain the confidentiality of

return information through the use of encryption, physical

22

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 23/65

access security and industry-standard SSL (secure

socket layer) communications protocol.

ONLINE TAX TECHNOLOGIES

1. Employer Tax Information Online

Employers can receive ready access to their tax account

information by registering for Employer Tax Information Online.

During the quick and simple registration process, you will create

your User ID and password that will be used each time you access

the online system. You can even grant your employees and

outside bookkeepers, payroll companies and service agents,

freedom to provide service to you via the ETIO while controlling and

monitoring the services performed by them.

2. AMT Assistant

The AMT Assistant helps taxpayers determine whether or not they

may be subject to the Alternative Minimum Tax by automating the

23

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 24/65

AMT Worksheet It is believe that most taxpayers can make entries

and get an answer in five to 10 minutes using the new application.

3. Earned Income Credit Assistant

Determine if you are eligible for the Earned Income Tax Credit.

Your eligibility is dependent on several factors such as your filing

status, income level, and the number of qualifying children you

have, if any. This tool will not only determine your eligibility, but can

also determine your filing status, and the number of your qualifying

children, and it can estimate your credit amount.

4. Withholding Calculator

The purpose of this calculator is to help employees to ensure that

they do not have too much or too little income tax withheld from

their pay.

5. Online EIN (Employer Identification Number)

24

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 25/65

An Employer Identification Number (EIN) is a nine-digit number that

is assigned to business entities. The government can use this

number to identify taxpayers that are required to file various

business tax returns. EINs are used by employers, sole proprietors,

corporations, partnerships, non-profit organizations, trusts and

estates, government.

Electronic Tax Return Filing System

A system for filing electronic returns therefore has to be

designed with two requirements in mind:

1. It must be as easy as possible for the tax department to

prove that the taxpayer filed a fraudulent return.

It must be as hard as possible for the taxpayer to repudiate (deny)

filing a fraudulent return.

Issues with Digital Signatures

Tax returns are normally signed with a handwritten signature.

Unfortunately, this isn't possible with computers, so it's necessary

to use a digital signature generated by the computer instead.

Digital signatures are a two-part affair, a private key (supposedly

25

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 26/65

under your control) which you use for signing, and a public key

(contained in a key certificate) known to others which is used to

verify your signature. Knowledge of the public key/certificate

doesn't reveal the private key, so your signature isn't

compromised by having the certificate known.

The use of digital signatures has some unusual requirements,

particularly where non-repudiation is required. This is brought

about by the fact that, unlike a handwritten signature which

requires conscious effort by the user, a digital signature is

never generated by the user but is generated for them by their

computer, and may be generated in a completely transparent

manner (that is, the user isn't even aware that they're having

something signed on their behalf). For example when you make

a connection to a web server running SSL, your computer may

be generating a digital signature for you, but you're never told

that this is happening - you could in theory be signing your life

away without even knowing it.

SECURITY ISSUES:

• Confidentiality keeps outsiders out

26

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 27/65

• Non-repudiation keeps insiders honest

In terms of providing confidentiality, the security measures in

online tax system will protect users - there really isn't much to worry

about for end users. The problem is the issue of non-repudiation,

that the system isn't well designed to provide evidence which will

stand up to being challenged in court.

DATA IN THE ONLINE SYSTEM

Data elements and fields available in the system are arranged in

the following categories:

A. Taxpayer

B. Employee

C. Audit Trail Information (including employee log-in info)

D. Others

The online tax system will receive and process electronically filed

individual tax returns

This includes taxpayer’s name and address. It also includes:

* data about the nature, source, and amount of taxpayer income

27

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 28/65

and income tax withholding,

* data to support deductions, exemptions, credits, and other tax

benefits taken on the return,

* bank data to support taxpayer request for electronic payment of

balance due or direct deposit of refund, and

* electronic signature data

Employee login is required to access data in the system. Login

information is maintained in an audit trail.

USER PROFICIENCY

Many people have difficulties with operating with new

technologies and in-fact majority of tax payers have no good

knowledge of computer. The introduction of tax machine online

in the paying process is actually a risk of complicating the

whole issue of efficiency and effectiveness in raising tax.

SYSTEM RELIABILITY

The question of reliability is based on the security measure

adopted to give confident to the tax payers. It is noticed that

28

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 29/65

complex technologies can have problem of break down, report

errors, and stall, it is belief that in this system, much will be

done to eliminate such effect.

NEW INFORMATION SYSTEM

This system is design to:

Increase revenue collection and reduce receivables through

integrated data mining and case management

Cut costs and increase reliability by consolidating solid, legacy

tax systems into a unified, upgradeable platform

Improve audit controls and taxpayer compliance through end-

to-end integration and control of tax processes and data

Improve taxpayer services by enabling online registration, tax-

return filing, payment, and access to account information

Increase productivity with built-in depth of functionality,

flexibility, data reliability, and workflow.

29

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 30/65

Protect taxpayer confidentiality and privacy with embedded and

proven security technologies.

CHAPTER THREE

SYSTEM ANALYSIS AND DESIGN

3.1 THE OVERVIEW OF SYSTEM ANALYSIS

Systems are created to solve problems. Many of the fundamental

considerations affecting the design of a system, stems often

unconsciously, from the systems approach to organisations. The

systems approach has many facets of which the following are the

most important:

• All systems are composed of inter-related parts or sub-systems

and the system can only be explained as a whole. This is

known as holism or synergy. The systems view is that the

whole is more than just the sum of the parts and that vital inter-

30

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 31/65

relationships will be ignored or misunderstood if the separate

part are studied in isolation.

• Systems are hierarchical in that the parts or sub-systems are

made up of other smaller parts. For example, the accounting

system of an organisation may be a sub-system of the

information system, which is itself a sub-system of the

organisation as a whole. Tax administration falls as part of

accounting process.

• The parts of a system constitute an indissoluble whole so that

no part can be altered without affecting other parts. Many

organisational problems stem from ignoring this principle. For

example, a departmental procedure or form might be changed

without considering the ripple effects on the other departments

affected, with dire consequences. Taxation or tax administration

is part of the state source of revenue which can not be ignored.

• The sub-systems should work towards the goals of their higher

systems and not pursue their own objectives independently..

31

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 32/65

System analysis is the stage in the software development

process whereby the existing system is analysed in order to

ascertain the problems in the existing system in order to proffer

solutions to the problems identified.

3.1.1 ANATOMY OF THE EXISTING TAX SYSTEM

The Nigerian tax system is basically structured as a tool for revenue collection. This is a legacy from the pre-independencegovernment.

Based on 1948 British tax laws and have been mainly static

since enactment.

The present system of taxation or tax administration in Edo

State is manual. The body responsible for the administration of

tax in the state is State Board of Internal Revenue.

At present the board is made up of the following departments:

Dept; of other Revenue

Dept; of Income Tax

Dept; of Audit and Investigation

32

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 33/65

Dept; of Tax Drive

Dept; of Finance and Administration

Dept; of PAYE

Dept; of Planning Research and Statistics.

Legal Department

Department of Information (Tax and Vehicle Administration)

The State Board is responsible for:

Ensuring the effectiveness and optimum collection of all taxes

and penalties due to the Government under the relevant laws;

Doing all such things as may be deemed necessary and

expedient for the assessment and collection of the tax and shall

account for all amounts so collected in a manner to be

prescribed by the commissioner making recommendations

where appropriate, to the Joint Tax Board on tax policy, tax

reform, tax legislation, tax treaties and exemption as may be

required from time to time generally controlling the

management of the state service on matters of policy, subject

to the provisions of the law setting up the service; and

appointing, promoting, transferring and discipline on employees

of the state service.

33

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 34/65

DAY TO DAY RUNNING OF THE STATE SERVICE: Since the state service is an arm of the State Government, it is

placed under the Commissioner for Finance for Supervision

The Chairman/Administrator - is saddled with the statutory

responsibility of ensuring the smooth operation of the Board

and the State Service

The Director of Income Taxes: He oversees the smooth running

of all the PAYE and Self Employed Tax Offices in addition to

overseeing the duties of Capital Gains Tax office, the

information section in the Head Office and the Monitoring Unit

in the Head Office

The Director of Other Revenue: He oversees the operations of

all the Motor Licensing Offices in the State through the State

Licensing Officer. He also supervises the Stamp Duties Office

and the Pools Betting Office

The Director of Administration and Finance: The DAF is in

34

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 35/65

charge of the smooth operation of the Administration

Department, the Accounts Sections and the stores

The Director of Planning, Research and Statistics: He is

responsible for Planning, Research and Statistics. Relevant

data regarding the operations of the service are in his custody

THE RESIDENT COORDINATORS: With effect from 1998, the

Board has created the offices of the Resident Coordinators for

close monitoring of revenue collections of Tax and Motor

Licensing Offices in the field.

3.1.2 PROBLEMS OF THE EXISTING SYSTEM

The Nigerian tax system, is characterised by:

• Low contribution of Tax Revenue to Gross Domestic

Product.

• Lack of precision in tax statutes.

• Inadequate level of quality personnel.

• Low technology utilisation.

35

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 36/65

• Pervasive tax evasion and non-compliance especially by

the informal private sector and the public sector.

3.1.2.1 THE NEED FOR AN ALTERNATIVE SYSTEM

Having seen the problems faced by the system as a result of

the manual approach used, the need to adopt an alternative

approach cannot be undermined.

Automating the online tax monitoring system will at the long

run make the system an effective and efficient one in the aspect

of ensuring that accuracy in the tax revenue is maintained and

the state tax board can be up to date in modern technology.

3.1.3 THE PROPOSED SYSTEM

The proposed system is an on-line system (internet-based).

The system will be designed using MS Front Page, the HTML

codes for the front and MS Access for the database design.

The online tax system will receive and process electronically

filed individual tax returns.

36

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 37/65

Form for individual tax payer (this include taxpayer name,

gender and address. )

Also……….

* data about the nature, source, and amount of taxpayer

income and income tax withholding,

* data to support deductions, exemptions, credits, and other tax

benefits taken on the return,

* bank data to support taxpayer request for electronic payment

of balance.

*electronic signature data

*the online tax return sites will check for common errors and

correct them.

*the submission requirements ensure no one else can enter your

tax information;

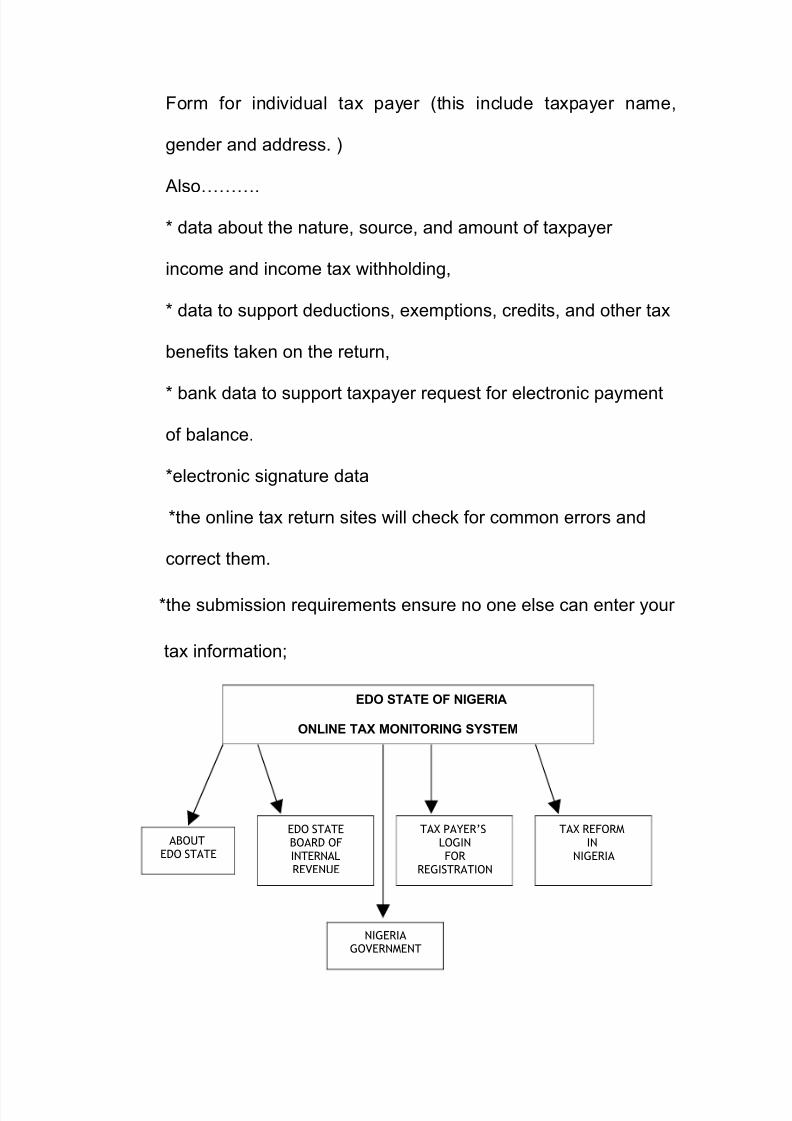

37

EDO STATE OF NIGERIA

ONLINE TAX MONITORING SYSTEM

ABOUTEDO STATE

EDO STATEBOARD OFINTERNALREVENUE

TAX PAYER’SLOGINFOR

REGISTRATION

TAX REFORMIN

NIGERIA

NIGERIAGOVERNMENT

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 38/65

3.2 SYSTEM DESIGN

It is a most crucial phase in the development of a system.

Normally, the design proceeds in two stages: (i) preliminary or

general design (ii) structure or detailed design.

1. Preliminary or general design

Designing an online system demands a great deal of creativity

and planning. It is also very costly and time consuming. In

system analysis, researcher has focused on what requirements

discovered in the analysis. In this design phase, the researcher

changes focus and concentrates on how a system can be

developed to meet the requirements. Several steps are useful

during this design phase:

• Review goals and objectives.

• Develop system model.

• Perform feasibility analysis

• a. Review goals and objectives. The objectives of

the new or revised system were identified during system

analysis and stated in the system analysis report. Before

38

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 39/65

the researcher can proceed with system design, these

objectives must be reviewed, since any system design

offered must conform to them. (convenient -- It is

available 24 hours per day, 7 days a week, It is easy -- ,

the online screens are designed to look like the return, It

is accurate -- the online system calculate the tax returns

accurately, It is free -- Paying by bank draft is free, It is

safe -- The web site and the taxpayer's data are secured,

It is acknowledged – the tax payers will receive an

acknowledgement from the Department that their returns

and payment have been received.

In order to maintain a broad approach and flexibility in the

system design phase, the analyst may restate users’

information requirements so that they reflect the needs of the

majority of users. For example, the finance department may

want a report of taxpayers who have been delinquent in

payments. Since this department may be only one subsystem

in a larger accounts-receivable system, the researcher may

restate this requirement more generally. It might more

39

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 40/65

appropriately be stated as (a) maintain an accurate and timely

record of the amounts owed by tax payer, (b) provide control

procedures that ensure detection of abnormal accounts and

report them on an exception basis, and (c) provide, in a timely

basis, information regarding accounts receivable to different

levels of management in the state board of internal revenue to

help achieve overall state government goals.

b. Develop system model. The researcher next attempts is to

represent symbolically the system’s major components is to

verify his understanding of the various components and their

interactions. The will may use flowcharts to help in the

development of a system model. In reviewing the models, the

analyst refers to system theory to discover any possible

omissions of important subsystems……

-are the major interactions among subsystems shown?

-are the inputs, processes, and outputs appropriately identified?

-does the model provide for appropriate feedback to each of the

subsystems?

-are too many functions included within one subsystem?

40

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 41/65

2. Structure or detailed design.

In the detailed design stage, computer oriented work begins in

earnest. At this stage, the design of the system becomes more

structured. Structure design is a blue print of a online system

solution to a given problem having the components and inter-

relationship among the same components as the original

problem. Input, output and processing specifications are drawn

up in detail. In the design stage, the programming language

and the platform in which the new system will run are also

decided.

There are several tools and techniques used for designing.

They are:

⇒ Flowchart

⇒ Data flow diagram

⇒ Data dictionary

⇒

Structured English

⇒ Decision tree.

41

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 42/65

New system is designed generally using logical models based on

the information derived from the previous stage. For the first time

physical aspects of the new system are included:

Type of system

⇒ Hardware specifications

Data organisation

⇒ Files/databases

Packages/programming

3.3 OUTPUT DESIGN:-

The output design shows how the report will actually look like.

The online tax monitoring system will generate the following

reports:

(i) Confirmation report: The report shows a confirmation

message telling the user(tax payer) that the information

submitted is successful.

(ii) Financial report: This report will show the total amount log

in by the tax pay and the balance if any.

3.4 INPUT DESIGN:-

42

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 43/65

This report shows a type of data entry and is user friendly. To

carry out this design, label and text box is needed.

3.5 FILE DESIGN

The system bas only one database file. This file is made up of

three tables. Each table of the database file is designed with

specific format for each field. Input is processed against the

files to produce the necessary output. Consideration involved in

the designing of these files are:

i). method of access

ii) record layout

Access mode for each of the files is random, that is records in a

file can be read or modified.

Record layout

This is the description of the structure of the records in each of

the file used. The record layout for all the two files used in the

online system are given below:

43

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 44/65

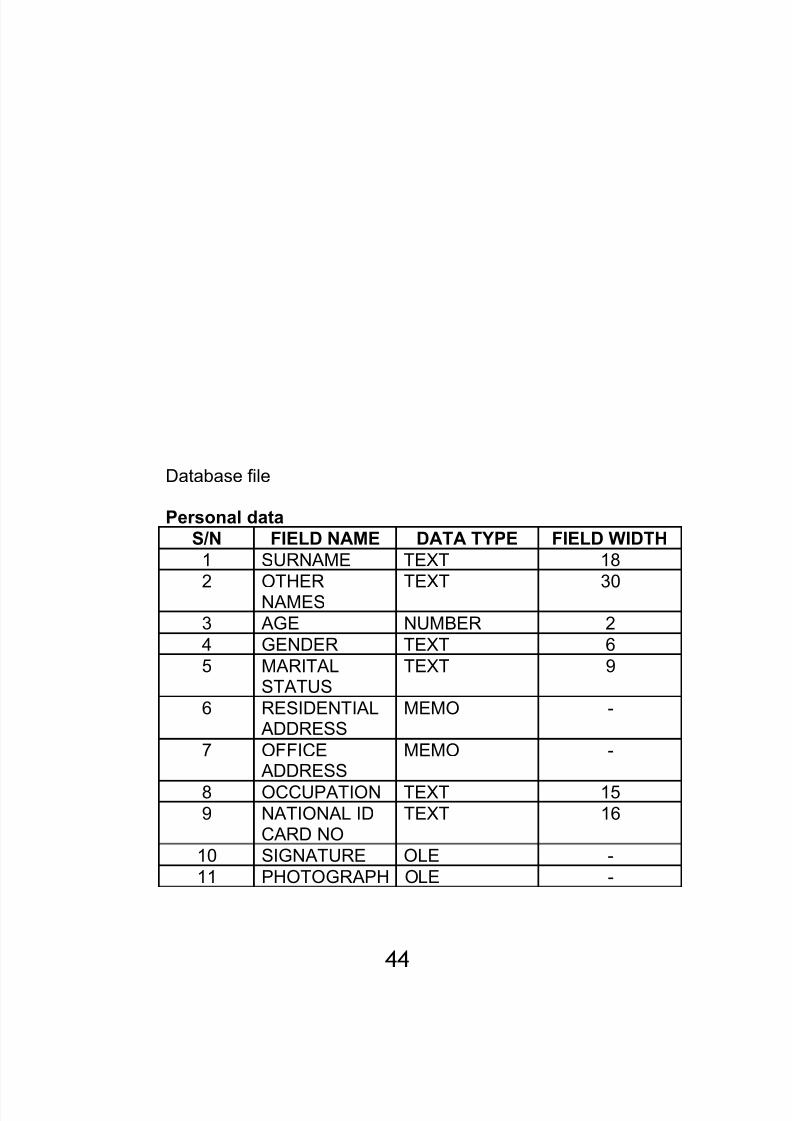

Database file

Personal data

S/N FIELD NAME DATA TYPE FIELD WIDTH

1 SURNAME TEXT 18

2 OTHERNAMES TEXT 30

3 AGE NUMBER 2

4 GENDER TEXT 6

5 MARITALSTATUS

TEXT 9

6 RESIDENTIALADDRESS

MEMO -

7 OFFICEADDRESS

MEMO -

8 OCCUPATION TEXT 159 NATIONAL ID

CARD NOTEXT 16

10 SIGNATURE OLE -

11 PHOTOGRAPH OLE -

44

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 45/65

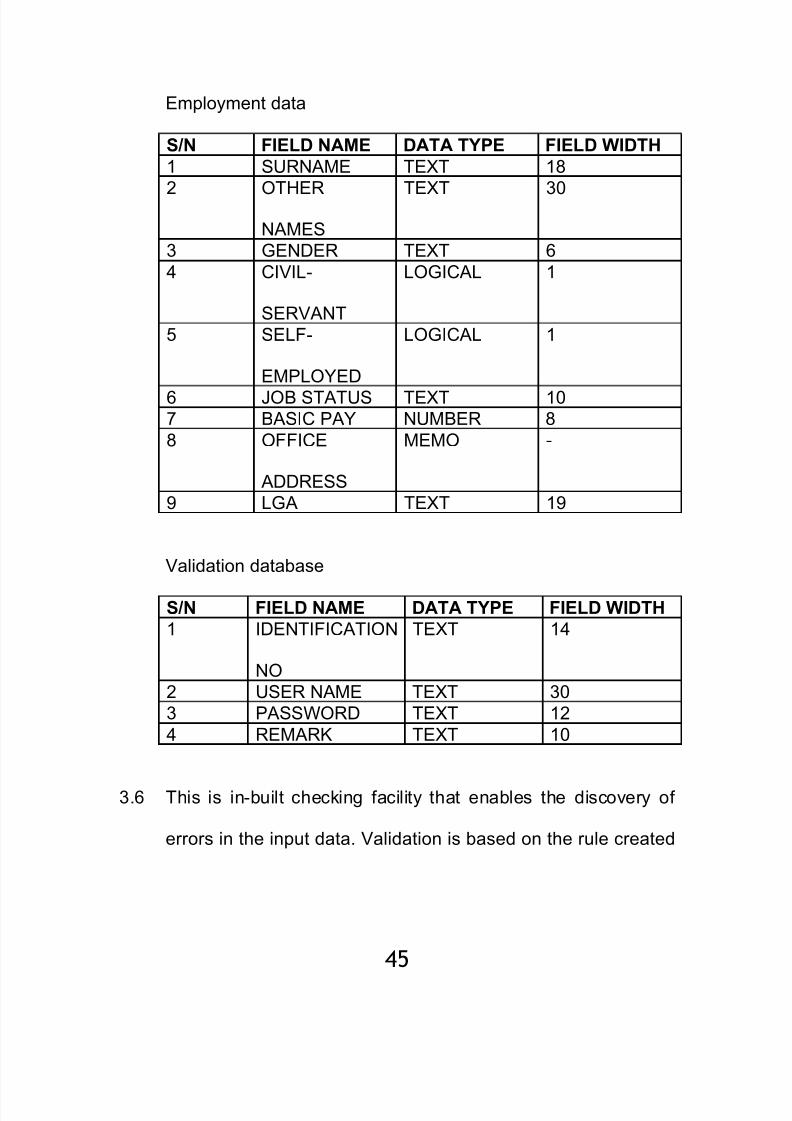

Employment data

S/N FIELD NAME DATA TYPE FIELD WIDTH

1 SURNAME TEXT 18

2 OTHER

NAMES

TEXT 30

3 GENDER TEXT 6

4 CIVIL-

SERVANT

LOGICAL 1

5 SELF-

EMPLOYED

LOGICAL 1

6 JOB STATUS TEXT 107 BASIC PAY NUMBER 8

8 OFFICE

ADDRESS

MEMO -

9 LGA TEXT 19

Validation database

S/N FIELD NAME DATA TYPE FIELD WIDTH

1 IDENTIFICATION

NO

TEXT 14

2 USER NAME TEXT 30

3 PASSWORD TEXT 12

4 REMARK TEXT 10

3.6 This is in-built checking facility that enables the discovery of

errors in the input data. Validation is based on the rule created

45

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 46/65

through expressions. When data fail validating, a message will

display informing the user of the error.

Example, if a field is meant for numeric value, the user

mistakenly inputted the alphabet, the system will prompt the

user with the message that there is an error in the input data. It

also provide the user the information on how to re-enter the

data correctly.

3.7 FILE SECURITY

Access to databases IS controlled by the use of passwords so

that only right user can gain access to the system . The security

is placed on the system through the use of a username and

password.

46

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 47/65

CHAPTER FOUR

DESIGN METHODOLOGY AND TECHNOLOGY

4.1 PROGRAMMING LANGUAGEThe design of the online system was accomplished due to the

application of many technologies. The web pages was

designed using ms front page and HPML (hypertext Markup

Language), the working program that enables the forms to

interface with the database files was designed in visual basic

programming language. The modular approach was used for

the program designs. That is, each module was designed and

developed separately and later linked together to form the

coherent system.

In software, a module is a part of a program. Programs are

composed of one or more independently developed modules

that are not combined until the program is linked. A single

47

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 48/65

module can contain one or several routines. Typical

characteristics of modular components include portability, which

allows them to be used in a variety of systems, and

interoperability, which allows them to function with the

components of other systems.

Modular programming is the concept that similar functions

should be contained within the same unit of programming code

and that separate functions should be developed as separate

units of code so that the code can easily be maintained and

reused by different programs. The source program listing is

attached in Appendix B. Various technologies applied will be

considered below:

(a) OVERVIEW OF HYPERTEXT MARKUP LANGUAGE

(HTML)

The Hypertext Markup Language (HTML) is a simple markup

language used to create hypertext documents that are platform

independent. HTML documents are SGML documents with

generic semantics that are appropriate for representing

information from a wide range of domains. HTML markup can

48

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 49/65

represent hypertext news, mail, documentation, and

hypermedia; menus of options; database query results; simple

structured documents with in-lined graphics; and hypertext

views of existing bodies of information.

HTML has been in use by the World Wide Web (WWW) global

information initiative since 1990.

HTML is an application of ISO Standard 8879:1986 Information

Processing Text and Office Systems; Standard Generalized

Markup Language (SGML).

HTML defines the structure and layout of a Web document by

using a variety of tags and attributes. The correct structure for

an HTML document starts with <HTML><HEAD>(enter here

what document is about)<BODY> and ends with

</BODY></HTML>. All the information you'd like to include in

your Web page fits in between the <BODY> and </BODY>

tags.

49

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 50/65

There are hundreds of other tags used to format and layout

the information in a Web page. Tags are also used to specify

hypertext links. These allow Web developers to direct users to

other Web pages with only a click of the mouse on either an

image or word(s).

HTML is a subset of a broader family of language called

standard generalised mark-up language (SGML) which is a

group of languages for encoding and formatting documents for

output to a computer screen but which are generally hidden

from the user. It is essentially a set of codes used to format the

appearance of web page and to create links.

Simply put, it is a way or means of formatting information to

make it suitable for display on the WWW.

b. VISUAL BASIC

Visual Basic, which is used for the form design and to interface

the data entry form to the database files is a programming

language suitable for all forms of computer applications-

50

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 51/65

numerical, scientific, graphical, database, commercial

programming. It is an object oriented programming (OOP)

language which has more advantages than its procedural

language counterpart. It is quite flexible and effective in

database manipulations, accessing and retrieval of information,

etc.

4.2 OBJECT ORIENTED PROGRAMMING

Object-oriented programming (OOP) is a programming language

model organized around "objects" rather than "actions" and data

rather than logic. Historically, a program has been viewed as a

logical procedure that takes input data, processes it, and produces

output data. The programming challenge was seen as how to write

the logic, not how to define the data. Object-oriented programming

takes the view that what we really care about are the objects we

want to manipulate rather than the logic required to manipulate

them. Examples of objects range from human beings (described by

name, address, and so forth) to buildings and floors (whose

properties can be described and managed) down to the little

51

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 52/65

widgets on your computer desktop (such as buttons and scroll

bars).

The first step in OOP is to identify all the objects you want to

manipulate and how they relate to each other, an exercise often

known as data modeling. Once you've identified an object, you

generalize it as a class of objects (think of Plato's concept of the

"ideal" chair that stands for all chairs) and define the kind of data it

contains and any logic sequences that can manipulate it. Each

distinct logic sequence is known as a method. A real instance of a

class is called (no surprise here) an "object" or, in some

environments, an "instance of a class." The object or class instance

is what you run in the computer. Its methods provide computer

instructions and the class object characteristics provide relevant

data. You communicate with objects - and they communicate with

each other - with well-defined interfaces called messages.

The concepts and rules used in object-oriented programming

provide these important benefits:

52

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 53/65

• The concept of a data class makes it possible to define

subclasses of data objects that share some or all of the main

class characteristics. Called inheritance, this property of

OOP forces a more thorough data analysis, reduces

development time, and ensures more accurate coding.

• Since a class defines only the data it needs to be concerned

with, when an instance of that class (an object) is run, the

code will not be able to accidentally access other program

data. This characteristic of data hiding provides greater system

security and avoids unintended data corruption.

• The definition of a class is reusable not only by the program

for which it is initially created but also by other object-oriented

programs (and, for this reason, can be more easily distributed

for use in networks).

• The concept of data classes allows a programmer to create

any new data type that is not already defined in the language

itself.

4.3 OBJECTS AND PROPERTIES

Your web page document is an object. Any table, form, button,

image, or link on your page is also an object. Each object has

53

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 54/65

certain properties (information about the object.) for example,

the background colour of the document is

written….document.bgcolor. you could change the color of your

page to red by writing the line: document.bgcolor=’’red”

The contents (or value) of a texbox named ‘password’ in a form

named ‘entry form is document.entryform. Passsword.Value.

4.4 METHODS

Most objects have a certain collection of things that they can

do. Different objects can do different things, just as a door can

open and close while a light a can turn on and off. A new

document is opened with the method document. Open () you

can write ‘Hello World’ into a document by typing document.

Write (Hello World’). Open () and write () are both methods of

the object: document.

4.5 EVENTS

Event are how we trigger our functions to run. The easiest

example is a button, whose definition includes the words on

click=’’run_my_function ()’’.

54

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 55/65

The onClick event, as its name implies, will run the function

when the user clicks on the button. Other events include. On

Mouse Over, OnMouseOut, OnFocus, OnBlur, Onload, and

OnUnload.

55

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 56/65

CHAPTER FIVE

IMPLEMENTATION ,RECOMMENDATION AND CONCLUSION.

5.1 IMPLEMENTATION

Implementation is the stage of a project during which theory is

turned into practice. During this phase, all the programs of the

system are loaded onto user’s computer. For effective

implementation to be carried out, the following will be required:

i) hardware and software requirement

ii) system modification

iii) system testing

iv) change over technique

Hardware and software requirement

Items needed here are as follows:

i). Pentium III computer or any one higher than this

ii). Not less than 128 Mega-Byte RAM (Random Access

Memory)

56

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 57/65

iii). Hard Disk of at least 10 Giga Byte

iv). Sound card and speakers

v). CD-ROM Drive

vi). Diskette Drive

vii). Un-interrupted Power Supply (UPS)

viii). Windows XP Operating system

ix). Internet Information Service

x). Visual Basic

xi). MS Access

xii). MS Front Page etc.

5.2 SYSTEM MODIFICATION

Pre-installation modification. User department personnel in

Board of Internal Revenue may request a modification to the

potential design of the system for a number of reasons. The

design may, for instance, create a number of previously

unforeseen problems or fail to resolve existing ones. This

situation may be discovered during prototyping, i.e. when

running a model of the system to assess if it will achieve

stipulated objectives. Such requests can be accepted after

57

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 58/65

discussions between management, operating department

(user) personnel and systems staff. This will necessitate a

modification to the relevant systems documentation to ensure it

accords to the system eventually implemented. A record of the

modification should be promulgated, i.e. committed to a formal

record indicating:

a. authority for the request;

b. date of request;

c. system or sub-system in question;

d. terms of reference indicating the reason for the

request;

e. agreed course of action

Post-implementation. This can be very costly, time-consuming

and disruptive. Inferior system design should be avoided at all

costs which is why defined checkpoints should be incorporated

at various stages of development. A system will need updating

due to technological and economic developments and the

passage of time.

58

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 59/65

File conversion and take-on of opening balances

Many computer-based systems are of an accounting nature

necessitating the conversion of files to magnetic media and the

transfer of opening balances to the computer files. The time it

takes to accomplish this task requires careful planning and

control. The Longer the transfer takes the more difficult it

becomes to catch up personnel attempt to run both the current

and the computer system on a disjointed basis. Catch-up must

be given priority while maintaining the current system in an up

to-date condition. Very often record are converted from ledger

cards on which transaction details are recorded by hand or

posting machine to magnetic media by suitable encoding

methods. Before conversion it is essential that the balances on

such record as tax record, payroll records of each tax payer are

reconciled to ensure only correct balances are transferred to

the new system. This creates a high volume activity and

suitable arrangements must be made sufficiently in advance to

avoid unnecessary take-on delay

59

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 60/65

5.3 SYSTEM TESTING

Prior to the installation of the computerised system test data

must be prepared for live testing. It is also necessary to

simulate the operation of the computer application before it is

installed, to detect any bugs. This is accomplished by desk

checking or dry running, which involves running through the

program coding, as the computer would do when processing

actual data.

In order to ensure that the web-site has been designed and

developed correctly ad that the system as a whole will work, the

website files were published to the server (IIS) and the site was

run in the server and all its component were working perfectly.

5.4 CHANGE OVER TECHNIQUE

The method of system changeover is outlined below to illustrate

the characteristics, which need to be taken into account during

the planning stage of installation.

60

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 61/65

(a)pilot scheme change over

Nature of a pilot scheme. This method of system changeover

adopts a cautious approach. Resources are not committed to a

state-wide implementation and the installation of a system is

restricted to one location only (i.e. state headquarters of Board

of Internal Revenue). The results obtained from running this

pilot scheme assist in determining the suitability of the system

for other locations (local government areas) in the state.

When to use a pilot scheme. A pilot scheme should be

adopted when the system under consideration has far-reaching

consequences on the efficient performance of key activities on

a wide scale throughout the “business”. In such case it is

prudent to limit the implementation to one office of the state tax

board to be used as a proving ground. This will then avoid

wide-scale disruption within the transaction environment.

5.5 CONCLUSION.

61

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 62/65

Web-based tax monitoring system, when properly examined

pose a great challenge to existing manual system with the

consideration of the following facts that……….

production of the desired information, at the right time, in the

right amount, with an acceptable level of accuracy and in the

form required at an economical cost;

incorporation of checks and controls which are capable of

detection and dealing with exceptional circumstances and

errors; effective safeguards for the prevention of fraud; efficient

security measures in order to avoid loss of data stored in

master file; efficient design of document and reports will make

the Edo State Government to achieve it goal in revenue

collection.

5.6 RECOMMENDATION

As soon as the online system becomes operational, it is

recommended that the following should be considered:

System monitoring. After the system has gone live and proved

to be performing satisfactory, it is still necessary to monitor the

system to ensure that no abnormalities occur and to remove the

62

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 63/65

cause if any arise. It may be found that, although the system is

achieving results as stipulated in the system specification, the

system design does not provide for certain requirements. This

situation will, of course, require system modification, which will

necessitate program recoding, recompiling and retesting.

System maintenance. Systems in their original form often

outlive their usefulness because of the need to change

business practices in accordance with changing economic

circumstances and the introduction of new legislation. In

addition, systems may be implemented initially on a stand-

alone functional basis and management may later consider it a

practical proposition to integrate related systems to avoid the

input of data several times to each of several systems for

different purposes.

Retraining personnel. When manual systems are superseded

by computerised applications there is a need to retrain existing

personnel or recruit personnel from external sources for the

new types of task which have been created. Before training can

63

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 64/65

commence, it is necessary to select suitable personnel with the

required aptitude and potential for specified tasks. The cost and

benefits will be compared to know if it has met its objectives.

64

8/14/2019 Online Tax Monetary System

http://slidepdf.com/reader/full/online-tax-monetary-system 65/65

REFERENCES

1. Emmanuel Nelson Bassey (2005) first edition. Contemporary

Issues on Management Information Systems.

2. College Training Kit …..Ms Front Page 2000. Unpublished

material College of Accountancy and Computer Technology-

Effurun.

3 KPMG-- The role of private sector initiatives in Nigerian tax

reforms (2006)

4.4. Seyi Bickersteth, National Senior Partner.Seyi Bickersteth, National Senior Partner.

KPMG Professional Services Lagos, Nigeria