Embed Size (px)

Citation preview

Step by step explanationsWritten by expertsCountdown listsChecklist

A practical guide for buying and selling your home

THEOn

THEMove®

AS

B B

ank

Lim

ited

PP

U31

378

ASB Bank Limited home loan criteria apply. A fee of up to $500, and a low equity fee may also apply.

Our Mobile Lending Managers are here to talk home loans at a time and place that’s convenient to you. So if you need assistance about a new home loan or re-fixing an existing loan, simply pick up the phone and arrange a time to talk to someone that has the experience and expertise to help. Our Mobile Lending Managers can even approve home loans on the spot, if you have all the necessary documentation. To find out more or to arrange a meeting, call Sean Brock, Emma Robinson or Ken Wimsett today.

Need to talk home loans? We’re here to help.

Sean Brock 027 444 8689

Emma Robinson027 241 0987

Ken Wimsett 027 446 9998

www.asb.co.nz

6143 4107 0110 MLM Wellington ad.indd 1 20/01/10 11:17 AM

A practical guide for buying and selling your home On THE Move®

First published in 1999 as Time Well Spent by NZ LAW Solutions Limited, a wholly owned subsidiary of NZ LAW Limited, PO Box 132, Napier.

Reprinted, 2000

Second edition, 2004

Third edition, 2006

Now updated and republished as On the Move, 2010

ISBN: 978-0-473-16375-4

© NZ LAW Limited, 2010

On the Move® is a registered trademark

Publisher: NZ LAW Limited

Text: Adroite Communications Ltd and NZ LAW Limited

Cover photograph: Alan Hay, NZ LAW Limited

Design/production: Mission Hall Creative, Wellington

Print: Milne Print Limited

All rights reserved. Material published in On the Move is true and accurate to the best knowledge of NZ LAW Limited. It should not be a substitute for legal advice. No liability is assumed by the publisher for any losses suffered by any person relying directly or indirectly on On the Move. No part of this book may be reproduced or used in any form or by any means; electronic or mechanical, including photocopying, recording or by any information storage and retrieval system, without permission in writing from the publisher and credit being given to the source.

NZ LAW Limited, PO Box 132, Napier Ph: 06-835 5299 Fax: 06-835 3741 Email: [email protected] Web: www.nzlaw.co.nz

Table of ContentsIntroduction 3

BuyingYourHome 5

First step: call us 5

Real estate agents 5

Making an offer 6• Applying for a loan 6

• Application fees 7

• Future plans 7

• Moving budget 7

The Sale Agreement 7• Conditional or unconditional offers 8

• Deposit 8

• Confirming finance 9

• Choosing a settlement date 9

• LIM Report 9

• Pre-purchase building inspection 10

• Final inspection before settlement 10

• Code Compliance Certificate 10

• Chattels 10

• Method of ownership 11

• Printed terms 11

• Other considerations 11

• Title to the property 12

Signing the Sale Agreement 12

• Presenting the offer to the seller 13

Your offer is accepted – what happens next? 13

Property tenure 14

Satisfaction of conditions 14

Settlement process 15

Settlement day 15

After completion 16

Delayed settlement 16

Countdown for home buying 17

ApplyingforaLoan 21

A lender’s security 21

Two stage process 21

Other considerations 22

1

SellingYourHome 23

LIM Report 23

Unit titles 24

Appointing a real estate agent 24

Auction, tender, fixed price or private sale? 25

Price 25

The Sale Agreement 25

Keys 26

Buying a new property 27

The settlement process 27

Electronic transactions 27

Countdown for home selling 29

MovingChecklist 33

OtherTypesofProperty 35

Apartments 35

Investment properties 36

Baches, cribs and holiday homes 37

Lifestyle blocks 37

Timeshares 38

Retirement villages 38

Overseas property investments 39

ProtectingYourInvestment 41

What to think about 41

Property (Relationships) Act 1976 41

Joint tenancy 42

Tenants in common 42

Joint Family Home 43

Family trust 43

Wills 43

Enduring Powers of Attorney 44

CostsfortheTransaction 45

WhatifitGoesWrong? 46

Glossary 48

Index 53

2

Introduction

Buying and selling a home can be an exciting time. There’s an opportunity to realise your hopes and dreams, and perhaps to begin a new part of your life.

However, the buying and selling process is not as easy as it looks, nor as straightforward as some people may tell you.

Inside this bookOn the Move® has been written not only to guide you through the legal aspects of the transaction, but also – more broadly – to give you comprehensive and practical advice on what to expect when you buy or sell your home.

We have provided separate sections for people buying and selling homes, as well as a discussion of the many other issues (legal or otherwise) you will need to consider during the process. There is also a chapter on different types of property – apartments, timeshares, holiday homes, retirement villages and buying for investment.

You will also find practical countdown lists, a moving checklist and a glossary of property transaction terms. Throughout the book you will find some lined pages to make notes.

Contact us earlyIf you are thinking of buying or selling property, please contact us early. Not only will we carry out the actual transaction for you, but we can also provide you with legal advice on how to structure your affairs.

Our contact details are on the back of this book. Alternatively, you can look on www.nzlaw.co.nz for your nearest NZ LAW Limited law firm.

Wehopeyoufindthisbookuseful.

Our firm is a member of NZ LAW Limited, an association of independent law practices with member firms located throughout New Zealand. There are more than 60 member firms practising in over 70 locations.

NZ LAW member firms have agreed to co-operate together to develop a national working relationship. Membership enables firms to access one another’s skills, information and ideas whilst maintaining client confidentiality.

3

Notes

4

Buying Your Home

When you are looking at buying a house, it’s easy to get excited about living in a new place and adding your own personal touches to it.

However, buying a home is probably one of the biggest investments you will ever make. It is sensible to obtain the best advice not only to ensure your purchase is smooth and trouble-free, but also to make sure the house is in good order, there are no issues with the property title, and that any future plans you may have for the house can be achieved.

Taking some time at the outset to read and follow the steps in this book may help save you time and money, and will give you the peace of mind that everything is well organised when you buy your home. A full countdown list for home buyers is on Pages 17–19.

First step: call usWe are here to help and guide you through the entire process from when you fi rst look at buying a new house to settlement day when you open the front door to your new home, and beyond.

Talking with us before you even start looking at houses will help you make the right decisions and ensure your property purchase is carried out effi ciently and cost-effectively.

We can give you some preliminary advice about the Agreement for Sale & Purchase and the buying process, and also talk with you about the best method to protect your investment. For example, if you do not already have a family trust, you may want to look into whether this is the best method to safeguard your newly purchased property. If so, you may want to consider establishing a family trust before you buy your new house, and you will need to set aside some time to do this.

Mostimportantly, do not sign an Agreement without talking with us fi rst.

Real estate agentsThe real estate agent dealing with the property you are thinking of buying has been engaged by the seller (or vendor) of the property and not by you. This means that the agent is acting for the seller and is acting in their best interests. Any advice the agent gives you, however well meaning, is secondary to the advice given to the seller.

If you want to receive independent advice that is tailored to your own interests, it is best you talk with us, rather than with the seller’s real estate agent.

5

Making an offerYou have found a house you want to buy and want to make an offer. Before you go ahead, there are a number of things you should think about before the offer documentation is completed.

You may wish to make some further checks before you go too much further. These may involve obtaining:

• Independent valuation by a registered valuer

• LIM Report

• Copy of the District Plan (in relation to the house being purchased)

• Building inspection by a building inspector, and/or an

• Engineer’s report by a registered engineer.

The latter two points are particularly important if you are worried about a leaky building. You should note that in a multi-unit development, the leaky building could involve all the owners, including yourself and not just the owner of the individual leaking unit.

As these reports will often involve extra costs to you, you may wish to make these part of the offer conditions.

In addition, you must take particular care to ensure that the financial side are things are water-tight, see more below.

ApplyingforaloanWhen you decide to put in an offer on a new home you will need to make sure you have sufficient funds available to pay a deposit and to service a loan. To calculate your ability to service a loan, your lender will usually give you a comprehensive work sheet asking you to list your assets and liabilities, income and expenditure, together with a monthly budget, to ensure you can meet the loan repayments.

If you want to do some preliminary calculations, most lenders provide calculation worksheets on their website.

Banks and other lenders place emphasis on different criteria for loans. There is a wide variety of lending products available, even within the same bank. It is well worth doing some research to ensure you have the best loan and one to suit your own circumstances.

You will need to talk with your proposed lender to make sure you will have all the funds necessary to ensure you can meet the obligations of your offer, on the terms that suit you.

Your lender will help you decide on the term (length) of the mortgage and on the mortgage product best suited for your circumstances. They may suggest a fixed or floating rate for your loan, or a combination of both. You may want a table, reducing or interest-only mortgage.

6

Some law firms provide a mortgage broking service or can recommend a mortgage broker. Using a broker may save you time having to shop around for the most appropriate arrangements to suit your own financial requirements. There is more information on this process in the chapter 'Applying for a Loan' on Pages 21–22.

ApplicationfeesLenders often charge an application fee for a mortgage (or it is added to the loan itself). Make sure that you have included this in your calculations.

Do be cautious if the seller’s real estate agent offers to arrange your finance. The agent is still acting for the seller and a conflict of interest may arise if they are acting for you and for the seller at the same time.

Our advice is to make arrangements with your lender yourself; alternatively, we are happy to act on your behalf.

FutureplansIf you plan to make alterations, additions or to sub-divide the property, talk with us about the viability of doing this. For instance, many house alterations require building consent, and subdivisions will require resource consent and may involve accounting for GST. This may have implications on the cost-effectiveness of your proposed projects.

MovingbudgetIn addition to the funds required to finance your new property, you should write a budget for the actual relocation cost.

Your budget should include the moving company’s fee, insurance to cover the transport of your possessions from one place to another, telecommunications, power or gas connection fees, burglar alarm check or installation of an alarm at your new property, boarding kennels for your pets if needed and so on. You should also ensure you have some contingency funds so you have the cash to pay for any unexpected expenses.

The Sale AgreementTo put in an offer for your new home, you will need to complete the Sale Agreement, formally called the ‘Agreement for Sale & Purchase’. We refer to it in this book as the ‘Agreement’.

In 2009 changes were made to the Agreement for Sale & Purchase. The Auckland District Law Society (ADLS) updated its existing Agreement form, and the Real Estate Institute of New Zealand (REINZ) introduced its own new Agreement. The real estate agent for the property you hope to buy will use either one of these forms. (See Page 25 under the Sale Agreement of this book for further commentary.)

7

It is vital that we check the Agreement BEFORE you finally sign it and present it to the seller. Faxing the Agreement, emailing a PDF or handing over a photocopy for us to check is fine.

DO NOT be tempted to make the Agreement simply ‘subject to lawyer’s approval’. This is not the time to cut corners and that simple phrase may not mean what you think it says.

ConditionalorunconditionaloffersYou must decide if your offer is to be made conditional on the sale of your existing home, obtaining finance or some other matter such as a builder’s or engineer’s report; or whether you can sign the Agreement unconditionally.

Making this decision will depend not only on your own circumstances but also on the strength of the property market at the time; there may be market pressure to make an unconditional offer.

It is fair to say that an unconditional offer, or an offer with only a small number of conditions, is likely to be viewed more positively by a seller than one that has many conditions. However, you should note our comments regarding LIM Reports (Page 9) and pre-purchase building inspection reports (Page 10) before deciding to make an unconditional offer.

DepositA deposit is paid to the seller as a sign of good faith that the property purchase will go ahead, and that any conditions in the Agreement will be fulfilled. The Agreement provides for this to be paid to the seller’s real estate agent’s trust account (or sometimes the seller’s lawyer), when you sign the Agreement. An alternative, which is becoming more common, is to make the deposit payable once the conditions are confirmed.

The deposit is usually 10% of the purchase price. However, this is negotiable and many sellers are happy with a lesser amount of, say, 5%.

As the deposit is a sign of good faith, your deposit (if paid before the agreement is unconditional) could be placed at risk, or forfeited, if you do not take all the necessary steps toward satisfying any conditions in the Agreement, or indeed if you confirm but do not settle.

8

Confirmingfinance

Although you may have discussed with your lender their agreement to the financial arrangements to buy your new home, you should always make your offer conditional on your finance being formally confirmed.

When finance is confirmed, your lender will probably instruct us to act for them as well as you the buyer. This saves doubling up on many expenses and we will make sure the lender’s conditions (which are often quite rigorous) are met.

ChoosingasettlementdateSettlement date is the day on which the property is paid for in full, and it is usually the day that you move into your new property.

It is usual to allow four to six weeks from signing the Agreement to settlement date. Many people name a Friday for settlement, however you may find it more convenient to choose another weekday. Moving companies are very busy late in the week, and you may find it easier to move on another day.

You should allow about 10 working days for finance to be formally approved. Another 10 working days should be allowed for the legal documents to be completed in time for settlement. Although these times can be shortened, you will find that plenty of time is needed to arrange your move.

LIMReportWe would strongly advise you to get a Land Information Memorandum (LIM) Report for your prospective property before making an offer. The LIM Report is provided by the local authority, for which you will need to pay a fee. Alternatively, the seller may have this available for prospective buyers to look over before making an offer; just check the LIM Report has been issued within the last few months.

The LIM Report gives information about plumbing, drainage and water reticulation plans, issued consents and permits, compliance schedules, licences, special site features, swimming pool fence regulations, unsatisfied requirements and a host of other details about the property.

The LIM Report may not give a complete picture if, for example, the seller or previous owner has done work without notifying the local authority. You should ask the seller specifically for details of any such work. It should be noted that gas installation certificates may not be covered in the LIM Report.

9

Pre-purchasebuildinginspectionA pre-purchase building inspection by a builder or building inspector can be included as a condition in the Agreement. An inspection will provide a comprehensive checklist against which a building is checked. It should include structural soundness, dampness or leaks, defects, repairs or alterations that may not have building permits.

When the inspection is being carried out, you may want to arrange to meet on site to ask any questions or to have some aspects of the inspection explained to you.

FinalinspectionbeforesettlementThe Agreement has a clause to allow a final inspection before settlement. We recommend that you instruct the real estate agent to arrange a time with the seller for you to make a final inspection of the property one or two days before settlement. It may pay for you to check all the chattels are in place, and that appliances are in the same condition as the time the Agreement was signed (in working order or not). The inspection may include turning on all the elements on the hob, switching on all the lights (it has been known for all the light bulbs to be removed), checking the garage door operates, the TV aerial is working, water and night store heaters don’t leak, and looking for any new damage.

If you find any problems with this pre-settlement inspection, you should get in touch with us urgently so we can contact the seller’s lawyer to rectify any problems before settlement

CodeComplianceCertificateFor a newly built house, and where the seller has done any work that requires a building consent, the standard Agreement requires the seller to supply a Code Compliance Certificate (CCC) from the local authority. This confirms the seller has carried out work on the house with a consent, and a CCC has been issued to confirm the work has been done within the consent conditions. The LIM Report will show whether CCCs have been issued for any previously approved work.

Some lenders may not provide finance, or release monies, on settlement day if a CCC has not been issued.

ChattelsChattels are usually included as part of the sale price and should be listed on the Agreement. (Remember, the Rating Valuation does not include chattels.)

Standard chattels listed are typically the stove, carpets, curtains, blinds and TV aerials. They may also include dishwashers and washing machines. If you are a rural dweller you may want to include items such as tunnel houses.

10

If you are buying the property as an investment, you will need to make a detailed chattels list and have the chattels valued for tax purposes A special clause will need to be added to the Agreement to cover this.

MethodofownershipAs mentioned earlier in this section under ‘First Step’ you should talk with us early on about the best type of ownership for your new property. Buying the house in your own name, or in your own and your spouse or partner’s name, may not be the most appropriate or useful method for your circumstances, particularly in light of the Property (Relationships) Act 1976.

The chapter ‘Protecting Your Investment’ on Page 41 discusses in more detail various methods of property ownership.

PrintedtermsThe printed terms in the standard Agreement are considered essential for both parties’ protection. Do not delete any of these printed terms unless we advise you to do so.

OtherconsiderationsLocationofthehouseontheproperty:In very old subdivisions occasionally houses are not located entirely on their own sections and encroach onto a neighbour’s land.

To make sure the house is properly located on the section, look on the LIM Report.

The Agreement provides that the seller is not bound to point out the boundaries so fence lines cannot necessarily be relied upon. However, it is still helpful to ask the seller where these are.

Limitationsonthetitle:Some titles are ’limited as to parcels’ which is a legal term indicating the size of the section is not guaranteed until a new survey is completed. This can often result in surprises for owners and their neighbours. We recommend that you obtain the site plan from the local authority before proceeding.

Access: All land must have legal access to it from the roadway. If the access involves a right- of-way, ie: access that is over someone else’s land or access is shared, you should check that there is a defined right to use the right-of-way. You should also check any maintenance provisions are fair and are properly understood by all the parties involved.

11

Restrictivecovenants: Restrictive covenants (such as height restrictions for buildings and trees, not allowing television aerials on houses nor allowing front fences, specifying minimum floor areas and prohibited building materials) may appear on the property’s title. We will check the implications of these restrictive covenants for you.

Buyingruralland: If you are buying rural land or a lifestyle block, you will need to check whether there is town water on the property, available water rights, whether you will need a septic tank, and the cost of getting services such as telephone, electricity and gas on to the property.

Whilst local authority rates on rural land are usually much less than on a town property, all the above services cost extra and you will need to allow for the provision of these in your budget.

You should get a copy of the Land Information Report (LIR) from the local authority. The LIR gives details relating to the physical and natural resources relevant to a property, lists what services are available and any restrictions there may be on the use or development of the land.

There is more discussion on lifestyle blocks in the chapter ‘Other Types of Property’ on Page 35.

TitletothepropertyThe Agreement has a provision for us to check the Certificate of Title to the property you propose buying.

In most cases, a title search obtained immediately after the Agreement has been signed will suffice. However, if you are concerned about whether there are special conditions which will apply to the property, for instance, in the case of bare land and new subdivisions where a title may not yet have been issued (where rights-of-way and building covenants will be important), we will arrange a title search before you make an offer.

Signing the Sale AgreementOnceyouarehappywiththeconditionsintheAgreement,itisreadyforyoutosign.The Agreement should be signed by all the parties who will be bound by it and whose names will be listed on the title. If, for example, your family trust is purchasing the property all trustees must sign the Agreement.

12

It should be noted that if you sign as a nominee, you are still personally bound by the Agreement.

PresentingtheoffertothesellerOnce you have signed the Agreement with an offer, the real estate agent will present it to the seller.

Your offer may be accepted straight away or the seller may come back to you with some additional conditions noted on the Agreement. These may include:

• ‘Cash out’ or ‘escape’ clause: This applies where your offer is conditional. It means that if the seller receives what they believe to be a better offer (where that offer is either unconditional where yours is conditional, or at a higher price, etc) before you make your offer unconditional (usually by selling your existing property or confirming finance), they must give you several working days to make the Agreement unconditional before they can cancel it. If you have to spend money on a valuation or building report, this type of clause may not suit you

• Back-up agreement: The seller may already have another offer, but is giving you the option to buy if the first offer does not become unconditional by a given date, or

• The seller may want to alter the price you have offered for the property, delete or change one of your conditions, change the proposed settlement day or alter some other detail.

These changes, or new conditions, become a ‘counter-offer’ and you are not bound to proceed unless you accept the seller’s new terms.

Each time a counter-offer is made, the Agreement and the changes are initialled by all parties (including trustees and/or nominees) and the real estate agent takes the Agreement back to the other party for written confirmation.

Your offer is accepted – what happens next?When your offer is accepted and both parties have signed the Agreement and initialled all the changes, you are both bound by its conditions. You will have to pay the deposit within the agreed timeframe; a late or unpaid deposit will attract interest. Failure to pay after three working days’ written notice demanding payment will allow the seller to cancel the contract.

Any deposit paid to a real estate agent’s trust account must be held for a minimum of 10 working days, unless agreed otherwise.

13

From the date the Agreement is signed and all alterations initialled by all parties, any time limits in the Agreement begin to run. Make sure you let us have the Agreement as quickly as possible so that we can ensure all the conditions are met on time.

Property tenureIn New Zealand there are various ways in which title to property is held. Some of these are:

• Feesimple: Fee simple is the most usual form of title available. It denotes a title on which there are no restrictions in the manner in which it can be held, kept or transferred, or passed on by Will.

‘Fee simple’ is not to be confused with ‘freehold’ which generally refers to a property that does not have a mortgage debt secured against it.

• UnitTitle: Special considerations arise if the property is held under a unit title, particularly in relation to the rules of the body corporate which govern the relationship between the various owners and the contributions to be made to the body corporate.

There may also be ‘local’ rules that apply in an ad hoc manner, such as booking arrangements for a shared tennis court.

• Cross-lease: The terms of a cross-lease need to be considered, for example, whether there are areas defined around the building for your sole use, ensuring the outline of the building on the plan correlates to the actual outline of the dwelling, and that details are given about the common areas and use of the driveway.

It can be an expensive exercise if additions have been made to the property, such as a conservatory built, without the legal documentation and survey completed to record those additions on the title.

• Leasehold: In some cases property may be leased for varying terms (usually 21 years for residential properties). There are several types of perpetually renewable leases. The exact provisions in relation to rent reviews and the basis of calculating rent should be discussed with us.

Satisfaction of conditionsThe Agreement states that a condition is not fulfilled until the party to be bound by it has received confirmation in writing.

If your Agreement has conditions, you should contact us well before the required confirmation dates. We will not confirm any conditions to the seller’s lawyer without your explicit instructions.

14

Remember that the time limits to fulfil any conditions apply strictly. The penalty could be that the Agreement could be cancelled by the seller, and you will miss out on buying your new property.

Settlement processHaving advised you on the best method of ownership for the property, see the chapter ‘Protecting your Investment’ on Page 41, we will prepare the transfer of the property into the appropriate names and complete the forms to ensure the local authorities get details of the transaction.

All law firms are now required to register land transactions electronically. Early on in the settlement process we will ask you to sign documents authorising electronic registration; we are also required to ask you for photographic government-issued proof of your identity (driving licence or passport).

The lender will forward their instructions shortly after the loan is approved and we will prepare the documents to be signed by you or your purchasing entity.

After checking the seller’s statement of the amount to settle the purchase, including apportionment of rates and other outgoings to the date of settlement, a complete statement of the amount required to settle will be sent to you. This statement takes into account the mortgages provided, your cash input and the deposit already paid.

After you have signed the lender’s documents we will ensure that their requirements are met and arrange for the funds to be available to you on settlement day.

Settlement dayOn settlement day, after receiving all the funds necessary to complete the purchase, we will arrange for the seller’s lawyer to be paid, clear title to be given to you and the keys made available. You will then be entitled to legal possession of your new property.

If settlement is delayed or takes place after the settlement date, you may be liable for late settlement interest on the unpaid purchase price.

15

After completionFollowing settlement, we will complete electronic registration of the transfer of the title into your name and the registration of any mortgages required by the lender.

With all titles now being stored electronically, after registration we

will send you a photocopy of the title showing the property registered in

your name, including the details of any registered mortgage.

Delayed settlementIf settlement of your prospective property is to be delayed, we may suggest a caveat be registered to protect your interests. A caveat is an official warning or caution registered on the title to a property that another party may have an interest or right over that property.

Registering a caveat will mean that any other prospective buyer of ‘your’ property will be warned of your interest or right over it.

16

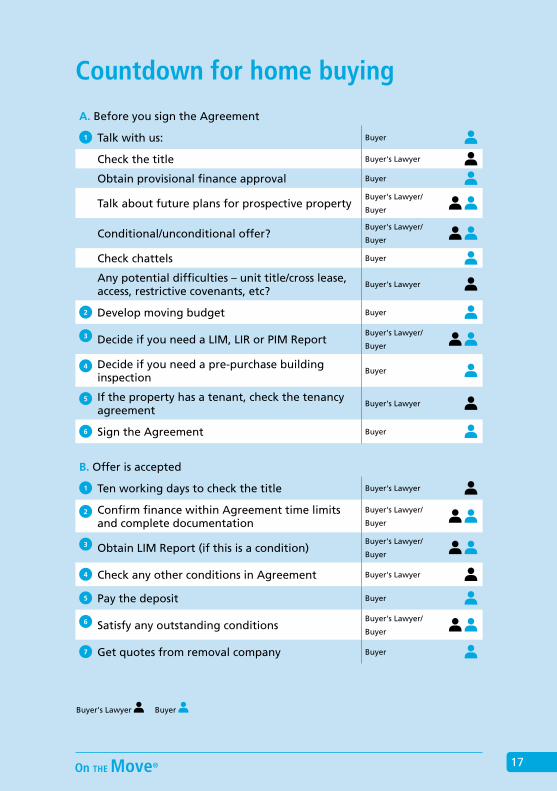

Countdown for home buying

A. Before you sign the Agreement

1 Talk with us: Buyer

Check the title Buyer's Lawyer

Obtain provisional finance approval Buyer

Talk about future plans for prospective propertyBuyer's Lawyer/

Buyer

Conditional/unconditional offer?Buyer's Lawyer/

Buyer

Check chattels Buyer

Any potential difficulties – unit title/cross lease, access, restrictive covenants, etc?

Buyer's Lawyer

2 Develop moving budget Buyer

3 Decide if you need a LIM, LIR or PIM ReportBuyer's Lawyer/

Buyer

4 Decide if you need a pre-purchase building inspection

Buyer

5 If the property has a tenant, check the tenancy agreement

Buyer's Lawyer

6 Sign the Agreement Buyer

B. Offer is accepted

1 Ten working days to check the title Buyer's Lawyer

2 Confirm finance within Agreement time limits and complete documentation

Buyer's Lawyer/

Buyer

3 Obtain LIM Report (if this is a condition)Buyer's Lawyer/

Buyer

4 Check any other conditions in Agreement Buyer's Lawyer

5 Pay the deposit Buyer

6 Satisfy any outstanding conditionsBuyer's Lawyer/

Buyer

7 Get quotes from removal company Buyer

Buyer's Lawyer Buyer

17

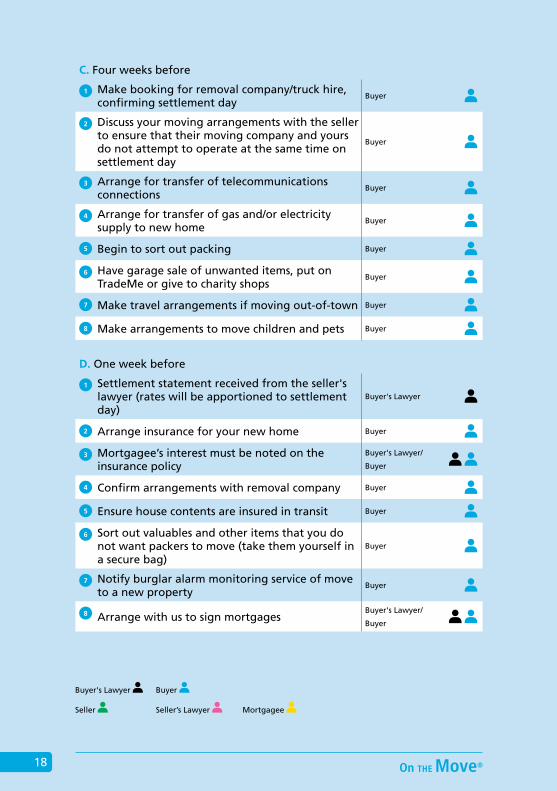

C. Four weeks before

1 Make booking for removal company/truck hire, confirming settlement day

Buyer

2 Discuss your moving arrangements with the seller to ensure that their moving company and yours do not attempt to operate at the same time on settlement day

Buyer

3 Arrange for transfer of telecommunications connections

Buyer

4 Arrange for transfer of gas and/or electricity supply to new home

Buyer

5 Begin to sort out packing Buyer

6 Have garage sale of unwanted items, put on TradeMe or give to charity shops

Buyer

7 Make travel arrangements if moving out-of-town Buyer

8 Make arrangements to move children and pets Buyer

D. One week before

1 Settlement statement received from the seller's lawyer (rates will be apportioned to settlement day)

Buyer's Lawyer

2 Arrange insurance for your new home Buyer

3 Mortgagee’s interest must be noted on the insurance policy

Buyer's Lawyer/

Buyer

4 Confirm arrangements with removal company Buyer

5 Ensure house contents are insured in transit Buyer

6 Sort out valuables and other items that you do not want packers to move (take them yourself in a secure bag)

Buyer

7 Notify burglar alarm monitoring service of move to a new property

Buyer

8 Arrange with us to sign mortgages Buyer's Lawyer/

Buyer

Buyer's Lawyer Buyer

Seller Seller’s Lawyer Mortgagee

18

E. Four days before

1 Do a final sort of items to be packed by removal company

Buyer

F. Three days before

1 Pre-settlement inspection (if required) Buyer

G. Two days before

1 Confirm arrangements for children and pets Buyer

H. On the day

1 Mortgage insurance arrangedBuyer's Lawyer/

Mortgagee/Buyer

2 Receive any cash contribution from the buyer Buyer's Lawyer

3 Moneys received from the lender Buyer's Lawyer

4 Keys handed over Buyer's Lawyer

5 Transfer (and mortgage) registered at LINZ Buyer's Lawyer

I. After settlement

1 Copy of new title to new owner Buyer's Lawyer

2 Copy of new title to lender Buyer's Lawyer

3 Local authorities notified Seller’s Lawyer

J. Transaction complete

19

Notes

20

Applying for a Loan

Most people need to apply for a home loan to help pay for their house purchase. There are a number of different lenders in the marketplace ranging from trading banks through to fi nance companies and private banks. When dealing with a lender, mortgage broker or any fi nancial advisor, we recommend you check they are compliant with the Financial Advisers Act 2009.

Each lender has a range of mortgage products available, all of which have different criteria, terms and conditions. Finding your way through this maze is not always easy. You should shop around and talk with lenders to get the most appropriate product for your particular circumstances.

Some people may prefer to use a mortgage broker to help them. Make sure that you get a broker who deals in the type of product that you want. For example, you may want a short notice loan so you need to ensure your broker deals in that type of product.

When considering using a broker fi nd out how you pay for their services. Most brokers are paid a commission by a lender, or others may charge you an extra fee. Check before you sign anything and talk with us if you would like advice.

A quick comparison of interest rates and products can be found on www.interest.co.nz

A lender’s securityWhen considering a loan application a lender will want to ensure:

• You have enough income to meet the loan repayments and other outgoings. This is sometimes known as ‘debt servicing’. A lender will usually ask for a monthly budget to ensure you can afford the mortgage repayments, and

• There is enough security in the property. Lenders sometimes refer to this as the ‘security ratio criteria’. It is the difference between the value of the property (which may be different from the price) and your personal contributions.

Two stage processThere is generally a two stage process to obtain housing fi nance.

StageOne:Looking for a new home

You should approach a lender before looking to buy a home to establish how much you can borrow. This will establish the price range of the property you can afford.

21

A lender will need to have evidence of your gross income/s (generally a lender will accept a pay slip as proof of income), a monthly household budget and a statement of position which lists your assets, any liabilities and so on.

To help you in your preliminary calculations to work out how much you can borrow and afford to repay, most lenders have mortgage calculators on their websites.

To make your offer as ‘clean’ as possible, ie: as few conditions as achievable, you may want to obtain some formal pre-approval from a lender to make your offer up to a particular sum. Talk with your lender about this.

StageTwo: Once the Agreement is signed

When the Agreement is signed you should immediately lodge a formal loan application with your chosen lender. At that stage, your lender will need a copy of the Agreement; some lenders may need a copy of the title for the property.

If the amount sought exceeds your lender’s security ratios, they may need a registered valuation of the property before confi rming a loan.

Other considerationsIt is important to note that even if a lender has indicated a loan will be approved before the Agreement is signed, the Agreement should still be made conditional on ‘obtaining fi nance satisfactory to the purchaser’, unless you have a formal written loan offer from a lender.

It would be unwise to simply rely on a verbal indication from your lender that a given sum will be lent.

Lenders have slightly different lending criteria. If one lender turns your application down, another may be able to help.

Even if your borrowing exceeds the security ratio, some lenders may still lend where mortgage guarantee insurance cover is arranged. This insurance is taken out at your cost to protect the lender.

It may also be possible to ‘massage’ your fi nancial debts by increasing your borrowing to repay short term credit card and hire purchase debt to bring you within the lender’s criteria. This may be investigated if the lender initially declines a loan.

22

Selling Your Home

If you are thinking of selling your home, do talk with us before contacting a real estate agent and placing your property on the market.

We will check that your property title is in good order and may advise you to fix any discrepancies or irregularities.

We can also talk with you about the pros and cons of selling through a real estate agency, or perhaps selling privately.

If you choose a real estate agency to handle the sale, we can discuss the currently accepted commission rate for real estate agents in the area. Commissions and advertising arrangements for properties are negotiable and may vary from agent to agent. As we deal with many property transactions, we are in a good position to ascertain trends in market expectations for commission, advertising arrangements and so on.

Before placing your property on the market, we recommend that you take care of some paperwork beforehand:

• Obtain your property’s Land Information Memorandum (LIM) Report (see the section below), and

• Unit title property owners should read the section Unit titles on Page 24 and ensure you have all the required documents available.

A full countdown list for home sellers is on Page 29-31.

LIM ReportWe recommend that you obtain your property’s Land Information (LIM) Report before placing your property on the market. The LIM Report is held by the local authority, to whom you will need to pay a fee.

The LIM Report gives information about plumbing, drainage and water reticulation plans, issued consents and permits, compliance schedules, licences, special site features, swimming pool fence regulations, unsatisfied requirements and many other details about your property.

The LIM Report will give a prospective buyer a lot of information about your property, and whether or not you (or earlier owners) have complied with the local authority’s requirements.

However, you need to consider what the LIM Report will disclose before placing your property on the market as there may be some problems of which you are unaware. If you wait for a potential purchaser to obtain the LIM Report and problems are discovered, you could be in for a nasty surprise.

23

Later on, when a prospective buyer is making an offer for your property they may wish to insert an extra clause into the Agreement making the purchase subject to their approval of the LIM Report.

Having a LIM Report available to any prospective buyers may circumvent having such a clause or speed up the decision time a buyer may need to make the purchase unconditional.

Unit titlesSpecial provisions apply if your property is a unit title. Before placing your unit title property on the market, you should have copies of all insurance policies or certificates effected by the body corporate, as well as a copy of the Section 36 certificate (a statement of the seller’s contributions and any liabilities) signed by the body corporate secretary. A prospective buyer may ask to see these before they put in an offer. When your property sells, this paperwork will have to be delivered to the buyer at least five working days before settlement.

If these documents are not provided, settlement (but not possession) may be deferred which may lead to serious complications if you are buying another property.

Appointing a real estate agentWe recommend that you shop around to find a real estate agent. Look around to see which agencies cover your area and which seem to have SOLD signs up quickly, look on the internet for properties for sale in your area and visit some open homes. This will help you get a feel for the market and for the real estate agencies operating in your area.

Get your shortlist of agencies down to two or three and ask them to look at your property. Each agency should be prepared to make a presentation to you on why they should be selected to act for you. They will give you an idea of price expectations and they should have prepared a preliminary marketing plan for your property. They should also let you know what costs will be incurred to help sell your property; this will include newspaper advertising, photographs, internet listings, signage and so on. All these costs will (usually) be additional to the commission you will be paying the agent.

Most importantly you also want to make sure that you and the real estate agent feel at ease with one another. Selling a property can be a very stressful and emotional time and the whole process is much easier if you and the agent can work comfortably together.

You will need to decide whether to appoint a sole agent, or to have a general listing with two or more real estate agents. There are pros and cons for both, and we can help you make this decision.

24

Once you have decided on a real estate agent to act for you, you need to sign an agency agreement. Read it over carefully before signing and do not hesitate to ask any questions if you are unclear on anything. Alternatively, we would be happy to review it for you.

Auction, tender, fixed price or private sale?There are a number of ways of selling a house:

• Fixed price

• Auction

• Tender, open or closed, or

• Private sale.

Your real estate agent will be able to tell you about the processes of each method of sale and what may be appropriate for your particular property and the area in which you live. We can also talk with you about the legal implications of whichever sale method you choose.

PriceYour real estate agent will guide you on the best asking price, the price guide or the auction reserve for your house. This will be based on the Rating Valuation and the recent sale prices of properties in your area. The price will also include some chattels such as carpets, curtains, blinds, stove and other items.

If your property has special features (such as garages on a road reserve or tunnel houses), or you simply do not agree with the figures supplied to you, it may be worthwhile getting a private valuation before agreeing to a sale price or range.

The Sale AgreementIn 2009 changes were made to the Agreement for Sale & Purchase. The Auckland District Law Society (ADLS) updated its existing Agreement form, and the Real Estate Institute of New Zealand (REINZ) introduced its own new Agreement.

However, there is now some discussion between ADLS and REINZ with a view to amalgamating the best aspects of each form into one new Agreement document.

We have our own views on both these forms, and believe it is imperative you discuss this with us, before you sign the Agreement, which of these two Agreement forms should be used for your property.

25

The Agreement form is designed for you and your real estate agent to ‘fill in the gaps’. However, a number of other clauses may need to be inserted or deleted.

You will also need to decide which chattels are to be sold with the house as these have to be listed individually in the Agreement.

Do talk with us if you have anything you would like clarified, or need some advice.

TheofferispresentedtoyouWhen an offer is presented to you by a prospective buyer, do talk with us BEFORE you sign the Sale Agreement. It should already be signed by the prospective buyers.

If there are too many conditions its effect could be simply to give the buyer an option to buy your property, rather than a firm sale, which could be disadvantageous to you.

An offer may be unconditional, or it may be conditional on the sale of the prospective buyer’s own home, or confirming finance, or it may contain other conditions.

All people who are listed on the title as owning the house will need to sign as sellers if the offer is counter-signed or the offer is accepted. This means that if your property is owned by a trust, all trustees must sign.

Please note that if one of the sellers is away or unable to sign, we will arrange for a Power of Attorney to be prepared which gives necessary authority to someone who can sign. Alternatively, arrangements can be made for signing by fax or a scan if the Agreement makes provision for signing in this manner.

Once the prospective buyer’s offer is accepted and both parties have signed the Agreement and initialled all the changes, you are both bound by its conditions. The deposit will be called for, and any conditions will need to be fulfilled within the agreed time limits so settlement can proceed.

KeysThe Agreement states that you will make available for the buyer all keys for exterior doors, electronic door openers and the alarm codes (unless the property is tenanted). These must all be available on settlement day.

If you have lent a key to anyone, you will need to get it back in time for settlement.

26

Buying a new propertyWhen you sell one property, you are usually buying another and will move into your new property on the day you leave your old house. It is probably best for both properties to be settled on the same day and for the respective conditions of both Agreements to operate contemporaneously.

The settlement processWe will prepare a settlement statement showing the buyer the amount to be paid on settlement day. A discharge of any mortgage or other debt shown against the title will be arranged and you can expect to have to sign a transfer authority about a week before settlement day.

From the proceeds of sale, and immediately after settlement, we will organise the repayment of any mortgages so that clear title is given to your buyer.

Rates and other outgoings such as body corporate payments will be apportioned to the settlement date. The buyer’s lawyer will probably require us to personally guarantee that the rates are paid, the water meter has been read at the settlement date and the water account paid. We will organise payment of these and account to you for the sale proceeds. Some lawyers will withhold a sum to cover these until the water account comes in a few days after settlement.

Electronic transactionsAll law firms now register land transactions electronically.

This is carried out by Land Information New Zealand (LINZ). Early on in the settlement process we will ask you to sign documents authorising electronic registration and we are required to see government-issued photographic proof of your identity. A current driver’s licence or a passport are the main options: if these are not available you will need to talk with us regarding alternative identification requirements (such as a firearms licence).

27

Notes

28

Countdown for home selling

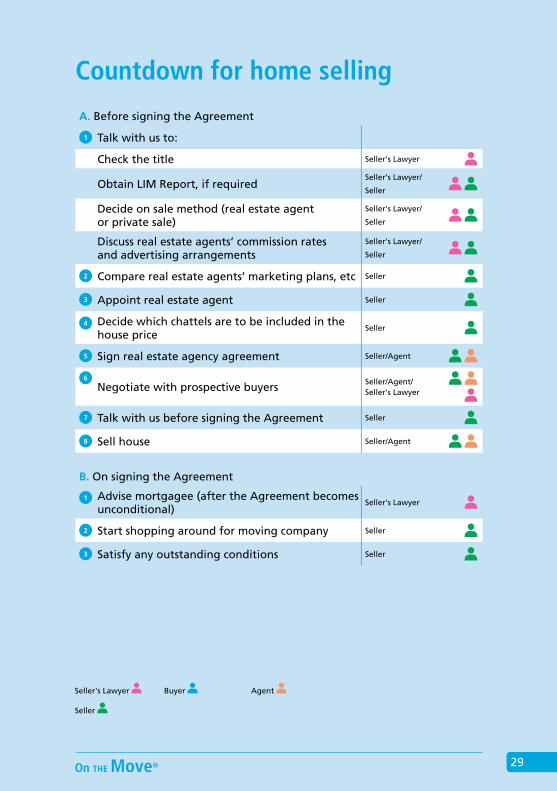

A. Before signing the Agreement

1 Talk with us to:

Check the title Seller's Lawyer

Obtain LIM Report, if requiredSeller's Lawyer/

Seller

Decide on sale method (real estate agent or private sale)

Seller's Lawyer/

Seller

Discuss real estate agents’ commission rates and advertising arrangements

Seller's Lawyer/

Seller

2 Compare real estate agents’ marketing plans, etc Seller

3 Appoint real estate agent Seller

4 Decide which chattels are to be included in the house price

Seller

5 Sign real estate agency agreement Seller/Agent

6

Negotiate with prospective buyersSeller/Agent/Seller's Lawyer

7 Talk with us before signing the Agreement Seller

8 Sell house Seller/Agent

B. On signing the Agreement

1 Advise mortgagee (after the Agreement becomes unconditional)

Seller's Lawyer

2 Start shopping around for moving company Seller

3 Satisfy any outstanding conditions Seller

Seller's Lawyer Buyer Agent

Seller

29

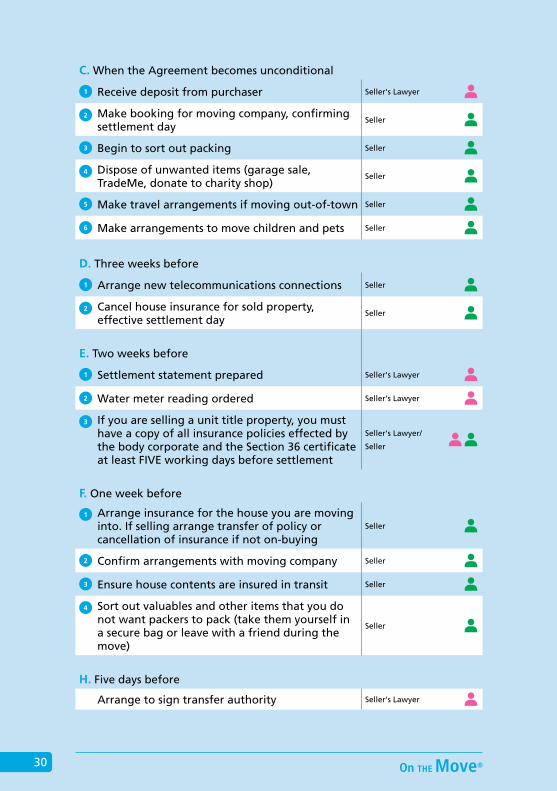

C. When the Agreement becomes unconditional

1 Receive deposit from purchaser Seller's Lawyer

2 Make booking for moving company, confirming settlement day

Seller

3 Begin to sort out packing Seller

4 Dispose of unwanted items (garage sale, TradeMe, donate to charity shop)

Seller

5 Make travel arrangements if moving out-of-town Seller

6 Make arrangements to move children and pets Seller

D. Three weeks before

1 Arrange new telecommunications connections Seller

2 Cancel house insurance for sold property, effective settlement day

Seller

E. Two weeks before

1 Settlement statement prepared Seller's Lawyer

2 Water meter reading ordered Seller's Lawyer

3 If you are selling a unit title property, you must have a copy of all insurance policies effected by the body corporate and the Section 36 certificate at least FIVE working days before settlement

Seller's Lawyer/

Seller

F. One week before

1 Arrange insurance for the house you are moving into. If selling arrange transfer of policy or cancellation of insurance if not on-buying

Seller

2 Confirm arrangements with moving company Seller

3 Ensure house contents are insured in transit Seller

4 Sort out valuables and other items that you do not want packers to pack (take them yourself in a secure bag or leave with a friend during the move)

Seller

H. Five days before

Arrange to sign transfer authority Seller's Lawyer

30

I. Four days before

Do final sorting of items to be packed by moving company

Seller

J. Three days before

1 Confirm arrangements for children and pets Seller

2 Pre-inspection by buyer, if requested Buyer/Seller

3 Ensure all chattels are in working order Seller

K. The day before

1 Make sure you have all the keys available to all exterior doors, window locks, garage door openers, plus burglar alarm instructions

Seller

L. On the day

1 Read meters and advise utility companies of readings

Seller

2 Moneys received from buyer’s lawyer Seller's Lawyer

3 Mortgage repaidSeller's Lawyer/

Lender

4 Keys handed over to new owner Seller's Lawyer

5 E-dealing released at LINZ Seller's Lawyer

M. After settlement

1 Payment of water and general rates Seller's Lawyer

2 Local authorities notified Seller's Lawyer

N. Transaction complete

Seller's Lawyer Buyer Agent

Seller Lender

31

Notes

32

Moving Checklist

Tick these tasks off as you go!

When the Agreement has been confi rmed, you can begin to let people know of your new address and the date on which you are moving. NZ Post provides some useful cards for this or use NZ Post’s website www.changemyaddress.co.nz. Some real estate companies also offer a similar service.

Family and friends (remember your Christmas card list)

Lender

Bank, if different from your lender

Insurance companies

Accountant

Inland Revenue Department

AA membership

School/kindergarten/child care

Babysitters

Motor vehicle registration

Credit card companies

Doctor and medical specialists

Dentist

Clubs

Local business accounts

Magazine subscriptions

Catalogue companies

Newspaper deliveries

Public library

Share Registers

Vet

You may also want to ask NZ Post to redirect all your mail. There is a small charge for this unless you are over 65 when it is free. You can choose the duration of the redirection.

Arrange with the alarm monitoring company to terminate monitoring in your old house, and install it in your new property on moving day. Remember to get the current codes from the seller, and then register your new alarm codes.

Organise a packing and removal company. This needs to be done well in advance. Get estimates from a couple of companies at least, together with copies of references and copies of their contracts. Make sure you organise insurance for your goods in transit. Do check your existing contents policy as sometimes moving contents is included – you don’t want to pay twice over.

33

If you are organising the move yourself, start to collect boxes and packing materials. Make sure your furniture is insured in transit, telling the insurance company you are packing yourself.

Start organising what you will take with you in the move and what should be disposed of. You may have things that are still in good order but you don’t want to take with you. These things could be given to a local charity, you could have a garage sale, sell them on TradeMe or recycle through www.freecycle.org.nz

Company directors must notify the Registrar of Companies of a change of address. If your home is the registered office of your company (or any other) you will also need to notify the Registrar of Companies. Time limits apply and special forms are needed. This can be done through www.companies.govt.nz or we can help arrange notification.

Ensure home and contents insurance is arranged for your new property.

Ensure the utility companies have connected their services to your new house. (Not all companies operate in every area.)

Telecommunications Electricity Gas

Change any direct debits for rates, electricity, gas, etc over to your new property.

Carry out a pre-settlement inspection of your new property, making sure that you arrange this with the seller’s permission. This means you can check to ensure any promised work has been completed. This also allows you to check that all the chattels you are buying with the house are operational and are left in the house on settlement day. It is very worthwhile testing every appliance, trying the garage door, ensuring the television works so the aerial is operating, etc.

Read the meter/s on moving day and phone through the readings to your gas/electricity suppliers.

Organise the actual move into your new home. Check with the sellers when they are moving out as they may leave before settlement day or on the day itself. You don’t want a clash of moving men!

Unless you have made prior arrangements for access, the moving company must wait until settlement has actually taken place and you have keys before they begin to unload your furniture.

Before moving into your new home, ask the seller to list the following:

Their forwarding address, email and telephone number

Neighbours’ names and phone numbers

Location of the mains and meters for water, gas and electricity

Burglar alarm instructions and operating manual. Check any alarm monitoring arrangements that may be in place

Rubbish and recycling collection details

Bus routes

Names of tradespeople who normally service the house, such as plumbers and electricians

Spare parts of any appliances, the guarantee cards and operating manuals, and

House plans, any wallpaper and paint samples.

Finally, make sure that you keep out your kettle, coffee and mugs or perhaps some cold drinks. There is nothing better than a hot cup of coffee or a glass of wine to enjoy when you have completed your move.

34

Other Types of Property

• Apartments

• Investment properties

• Baches, cribs and holiday homes

• Lifestyle blocks

• Timeshares

• Retirement villages

• Overseas property investments

ApartmentsUnittitle:The usual method of apartment ownership is a unit title.

Under a unit title scheme, all the owners comprise a body corporate which is responsible for maintaining the fabric and structure of the building and the grounds, as well as insurance. In addition to the usual outgoings for apartment living, you will also need to take into account any extra costs levied by the body corporate.

Depending on the size of the building, its construction and location, the body corporate levy could also include payment for garden maintenance, a building manager, a body corporate secretary and lift maintenance.

You should take particular note of the body corporate rules which set out the way in which it is run. Some rules are easily altered, others are not. There may be special rules relating to tennis courts, swimming pools, the barbeque area and any social clubs. Rules about pet ownership are usually particularly clear. For example, a budgie may be fine but a large dog may not be acceptable.

Apartments that are within a hotel complex have very particular rules and specific issues to consider.

The rules may set out how you live your life, and this may not suit your lifestyle.

If you are buying the apartment as an investment, you must ensure it can be let. Often specific rules apply to tenancies and it pays to check these before you decide to buy.

35

Buyingofftheplans: If the building is still only a set of plans, there are many issues (for example, taxation implications) to be taken into account before finally committing to a purchase. You should check whether any other buildings are being constructed nearby (or are on the drawing board) that may obstruct sunlight or views. Inner city apartments can be noisy from traffic, restaurants, late night revellers, railway lines, etc.

Special arrangements will need to apply to your deposit so it is not lost if the development does not proceed.

Flatowningcompanies: Whilst apartments are usually owned on a unit title, some ‘flat owning companies’ still exist. In this situation you buy shares in the company which owns the building. There are some issues with the saleability of an apartment which is held in this type of ownership. For example each purchaser must have the existing owners’ consent to be ‘let in’. This can sometimes reduce the pool of possible purchasers and, of course, the price.

Investment propertiesOwning an investment property can be a very worthwhile endeavour. The return on the investment may be greatly enhanced if the ownership structure is considered at the time of purchase. The property can, of course, be purchased personally. Alternatively you can buy the property through a Loss Attributable Qualifying Company (LAQC) or you may prefer to form a new family trust. Do talk with us early on so we can talk about the best ownership method for your particular situation.

During the purchase negotiations, careful thought should be given to the valuation of the chattels. The contract will need a special clause if depreciation is to be maximised.

You should also factor into your calculations the time taken to get new tenants and also the cost and time taken to fix any deferred maintenance.

Any investor in residential property should be familiar with the Residential Tenancies Act 1986 (currently under review), the scope and powers of the Tenancy Tribunal and tenants’ rights. Particular rules apply to bonds and tenancy agreements.

At the time of going to press, the government is debating a possible capital gains tax. Buyers should be aware of the implications that such a proposed tax may impose on an investment property purchase and/or existing property investments.

Sellinganinvestmentproperty: When selling you will need to take into account ‘recovered depreciation’ when setting your price, particularly for chattels. There could be serious tax consequences if this is not done correctly.

36

Tax: Specific tax issues need to be addressed when buying or selling investment properties. Your choice of buyer (ie: yourself, a company or trust) is just one of these. We can advise you on the most advantageous structure to adopt. It is extremely important to talk with us BEFORE signing the Agreement so any taxation advantages can be taken into account.

Baches, cribs and holiday homesSometimes baches, cribs and holiday homes are acquired for reasons other than their holiday value; holiday homes can play a specific role in retirement or investment planning.

The ownership structure for second homes should therefore be carefully considered. There may also be an opportunity to minimise tax; we can talk with you on specialist tax advice.

As the property is likely to be empty for much of the year, your insurance company must be notified of this. You may need to invest in a burglar alarm and/or special locks or shutters to help keep it secure.

Lifestyle blocksThere is more to this than deciding whether or not you may need a ride-on mower!

Bareblocks: You will need to ascertain if there is a suitable building platform for placing a house. Some titles have restrictions pointing out foundation difficulties, but others may not. Check with the local authority before you buy.

Water supply (for the house and possible irrigation requirements), drainage and septic tank requirements and regulations, as well as electricity supply and telephone lines should all be checked.

Access can be an issue on bare blocks. Many blocks have a lengthy right-of-way or shared road; some of these may not be formed at the time of purchase and could be expensive to construct.

Income-generatingblocks: Those life-stylers who want to make a living from the block will need to consider the economic viability of the land and soil tests may be needed. Talk with us if you would like some help with ascertaining the economic viability of your plans.

Buyers may want to consider obtaining a Land Information Report (LIR) from the local authority. The LIR gives details relating to the physical and natural resources of the property and may cover issues relating to flooding, contamination and water.

GST: Prospective buyers should be aware that there could be GST payable when buying a lifestyle block.

37

Non-residents:Please note that if you are not a New Zealand resident then any purchase of land over five hectares is subject to your obtaining approval with the Overseas Investment Office. As this can be a lengthy process you will need to contact us before signing any Agreement for Sale & Purchase to ensure this issue is properly covered. There is more about this on Page 39.

TimesharesThere has been a proliferation of timeshare apartments and resorts developed in New Zealand in the last 25 years or so. In most respects buying a timeshare is very similar to any other property purchase, however there are some differences.

Most timeshare properties in New Zealand have been set up using the body corporate structure accompanied by registered leases of every unit for each timeshare week. The registered proprietor of a timeshare title receives a share of the strata title and the lease of a unit for their timeshare week. You should obtain advice from the timeshare sellers and the body corporate or operator on pooling agreement administration where a timeshare is part of a holiday resort.

Retirement villagesThe physical security and wide range of activities offered by retirement villages are of major appeal to prospective residents. Retirement villages must operate within the Retirement Villages Act 2003 and its amendments, including the Code of Residents' Rights.

If you are considering living in a retirement village, do talk with us early on as we can advise on the unique nature of buying into this type of development. Issues to be considered before proceeding will depend on whether the village is already established, or merely a set of plans.

Before committing yourself to buy a unit, you should be aware of the nature of the occupation right offered in a retirement village. Most retirement villages do not offer readily transferable titles. The interest that is acquired by a buyer is generally a ‘licence to occupy’. This is similar to a lease that gives the resident the right to occupy a unit, but there are no rights over the land. In general, the occupation right is not able to be sold or otherwise disposed of other than through the retirement village proprietor.

Some villages have titles with a life interest, with a mortgage back to the buyer to secure the licence to occupy.

38

Most retirement villages require an up-to-date prospectus to be available to prospective buyers. Read it carefully and do hand it over to us for a close inspection so we can advise on the special nature of this type of purchase.

Of particular importance is the method of sale of the unit and reimbursement of capital when the time comes to sell your unit. Talk with the retirement village proprietor about this. The village will usually not pay you out until there is a buyer for your unit and there can be considerable delays in the reimbursement of capital. You should also investigate what is involved in moving from a unit into the hospital section of the retirement village (if there is one), and also the weekly or monthly service charges.

Moving into a retirement village can be of huge benefit to the elderly, and also to their families. Make sure you have done thorough research and remember to talk with us well before proceeding with a purchase.

Overseas property investmentsNewZealandersbuyingoverseas: If you are a New Zealander considering buying property offshore you will need to be very cautious about the type of property being offered . Do your research first, and then talk with us before taking the prospective purchase any further. Be wary of free trips ‘without obligation’ and high pressure sales people. Offers of ‘guaranteed returns’ should be viewed with caution. Remember, if it sounds too good to be true, it usually is.

Non-residentsbuyingNewZealandproperty: If you are neither a New Zealand citizen, nor ordinarily resident in New Zealand, you may need to apply to the Overseas Investment Office (OIO) for consent to buy:

• Non-urban land over five hectares, and/or

• ‘Sensitive land’ or land adjoining sensitive land such as beach or lakefront.

The Overseas Investment Act 2005 states how the rules apply. However, check with us first as to the application of the rules.

DONOT sign any documents until you have talked with us.

39

Notes

40

Protecting Your Investment

The need to protect a family’s investments has always been very important. For hundreds of years people have wanted to safeguard their family’s assets from any risks and claims.

You will also want to make sure your wishes regarding your property are carried out on your death.

This section gives an overview on a range of options to protect your assets.

What to think aboutIn order to protect your property investment you need think about a number of issues which range from the method by which your title is held to the possible establishment of a family trust.

You should think about:

• The nature of your employment and whether you are an employee, self-employed or an employer

• Exposure to creditors

• Your relationship: single, married, living in a de facto relationship, same sex relationship, or second and subsequent marriages

• Whether or not you have children, and

• Your hopes and aspirations.

In addition, the Property (Relationships) Act 1976 has had a major impact on all asset protection issues. It is a complex topic about which we need to talk with you face-to-face as one size does not fi t all. However, we provide a brief overview below.

Property (Relationships) Act 1976The Act came into force on 1 February 2002, replacing the Matrimonial Property Act 1976.

It applies automatically to all people who are married, and to people who are over 18 years old and who have lived in a de facto relationship for at least three years. In some circumstances the Act applies to de facto couples who have been living together for less than three years, for example, where there is a dependent child. The legislation also applies to same sex couples.

41

When a couple separates, all property acquired during that relationship is, as a general rule, shared equally between them. The reasons why the relationship ended are not relevant to this equal sharing rule.

The relationship home and other family chattels, including motor vehicles and boats, are also shared equally after three years, even if they were owned by only one of the parties before the relationship began.

Equal sharing applies whether the property is owned in joint or individual names.

Equal sharing also applies in the event of one partner dying during the relationship. The surviving partner then has a period of six months to decide whether to accept the provisions of the deceased person’s Will, or to make a claim for an equal share of the relationship property under the Act. Wills need to be carefully considered in the light of this legislation.

Whatarepossiblesolutions?It is possible to ‘contract out’ of the provisions of the Act if it does not suit your individual circumstances or will lead to a grossly unfair situation. Any agreement however must be fair to the other party. You are required to get independent legal advice and sign the contracting out agreement for it to have legal effect. Some agreements can be quite complex, but time spent now can prevent tears, frustration and litigation later.

Family trusts also give some protection from the legislation.

Joint tenancy‘Joint tenancy’ is a method of owning your home in conjunction with another person, whether or not that person is a partner or a spouse. On the death of one joint tenant, the property is automatically transferred to the survivor regardless of the provisions of the deceased’s Will.

Tenants in commonA property may be held as ‘tenants in common’. If one partner dies, their share does not pass automatically to the survivor (unlike a joint tenancy), but passes according to the deceased’s Will.

This ownership method is often recommended for partners or friends buying property together. It is also particularly important to think about this ownership structure when people want to reserve their share for their children (whether or not from another or prior relationship).

42

Joint Family HomeHaving your home registered as a Joint Family Home (JFH) is a comparatively inexpensive method to achieve limited protection against creditors’ claims. It is currently only available to married couples, and does not include couples who have a civil union. On registration as a JFH the property is owned by husband and wife as joint tenants. The registration is noted on the property’s title.

The main advantage of having a JFH is to provide protection for the home owners of up to, currently, $103,000 against ordinary creditors. It does not apply, however, against mortgagees.

The protection is granted immediately on settlement of the property as a JFH if the JFH application has been advertised (without any creditor lodging a caveat as an objection). If the application is not advertised, protection against creditors is deferred for two years from the settlement.

If your home is already registered as a JFH, when buying a new home it is possible to transfer the benefit from your current home to your new property immediately without having to advertise. Only one home can be registered as a JFH at any one time.

Family trustFamily trusts are the most commonly used method of asset protection and they are the best solution in many cases.

However, a family trust will only be recommended if it suits your individual circumstances. We can talk with you about your assets and liabilities so you can decide whether a trust is the best method to protect your property.

To know more about family trusts, please ask us for a copy of our handbook To Trust or Not to Trust.

WillsIf you are buying a home, it is essential you have a Will. You are the owner of a major asset and it is imperative that you leave instructions about what should happen to your property if you die.

Many people misunderstand what happens with the disposal of assets if someone dies without a Will (this is called intestate or intestacy). A Will ensures that your wishes are carried out subject to any possible claims that could be brought under the Family Protection Act 1955 and the Testamentary Promises Act 1949.

43

In addition, the Property (Relationships) Act 1976 has major implications for homeowners. It is essential that we talk about this while the property transaction is being prepared.

If you already have a Will, this is a good time to review it to ensure it is up-to-date and it still reflects your wishes.

Enduring Powers of AttorneyYou should also make sure you have Enduring Powers of Attorney (EPA) so that in the event of an accident or some incapacity, decisions can be made about your welfare and/or property, and keep your affairs in order. There are two forms of EPA.

PowerofAttorneyinrelationtopersonalcareandwelfare: This grants your attorney the power to act for you generally, although it may be restricted to defined specific matters such as a choice of rest home, medical care, etc. You can also place restrictions on your attorney, for example, ensuring that they consult with other family members before making final decisions.

There can be only one attorney (usually a spouse, partner or close relative) appointed in relation to your personal care and welfare. Provision can be made in the document for an alternative if the first appointee dies or becomes incapable.

PowerofAttorneyinrelationtoproperty: This allows the attorney to act in relation to all your property, or to specific property. More than one attorney may be appointed.

The witnessing provisions for EPAs are complex; we will make sure that each EPA is signed and witnessed correctly.

44

Costs for the Transaction

Knowing and understanding the costs involved is an important part of your property transaction. Not only do you have to factor in the legal costs, you will also need to budget for the real estate agent’s commission, any advertising costs, obtaining a LIM Report, any specialists’ reports such as a valuer or building inspector, the costs of a removal company, reconnection fees for utilities and telecommunications and so on.

We can give you a cost estimate for the legal transaction when you first talk to us about moving. This will include the fee for the time taken, the disbursements (such as the LIM Report, title searches, registration fees, etc) and GST. In accordance with the New Zealand Law Society’s Client Care Rules we will supply a cost estimate in an engagement letter or a terms of engagement communication.

Being responsible for the sale and/or purchase of a property is not simply a matter of filling in a few forms. There is a great deal of checking to do. On the average purchase with a mortgage there are about 40 separate steps to be taken and checks to be made. For a sale there are about 20 steps, and more if there is a mortgage to be repaid.

For us to give you an accurate estimate, you must tell us everything that is required so that you get as much value from the transaction as possible. For example, if you need a new Will, or require a property sharing agreement, let us know before we give you a cost estimate.

For other costs, make sure you give clear instructions of your requirements and get a written cost estimate.

45

What if it Goes Wrong?

Although you would have done everything possible to make sure you have a trouble-free move, sometimes things can go wrong and there is a dispute – however big or small. The Agreement for Sale & Purchase may still be relevant, so talk with us in the first instance.

Handling disputesIf the dispute is an issue you want to resolve yourself, we recommend you take the suggested steps below.

• Ensure you have got all the facts correct. This includes confirming the expectations that you believed you had, who said what and on what date