Embed Size (px)

Citation preview

Scatui. J. Mgmr, Vol. 9, No. I, pp. 61-76. 1993 Printed in Great Britain

02X1-75271Y3 $6.00 + 0.00 0 lYY3 Pergamon Prcas Ltd

ON THE CAUSALITY AND CO-MOVEMENTS OF SCANDINAVIAN STOCK MARKET RETURNS

MARKKU MALKAM.&KI,* TEPPO MARTIKAINEN,? JUKKA PERTTUNENt and

VESA PUTTONENt

*Bank of Finland and tSchoo1 of Business Studies, University of Vaasa

(First received October 1991; accepted in revised form February 1992)

Abstract - This paper reports some tests of Scandinavian stock market indices. Firstly, Granger causality tests of daily Swedish, Norwegian, Danish and Finnish stock returns are performed. Secondly, the effects of world-wide returns on these four Scandinavian markets are analysed. Some causality between Scandinavian markets is observed. The Swedish market is found to be the leading one of the four. while the other three appear to have no significant influence on other markets. Thus. the results do not indicate full integration of information between Scandinavian stock markets. The world-wide returns seem to have significant leading effects on Scandinavian market returns. This may be due to the growing international capital movements across countries and stock exchanges. The ongoing internationalization may well have significant effects on the returns behaviour of Scandinavian stock markets. in particular in Norway. Denmark and Finland.

Key words: Finance, stock markets, Scandinavia, causality

1. INTRODUCTION

International asset pricing and portfolio diversification have been the subjects of increasing attention in recent years. This is because the major national markets have been going through a period of rapid deregulation and integration. At the same time, the relative importance of non-U.S. capital markets has been growing rapidly. However, there are still some restrictions on the free international movement of capital. The main purpose of this study is to provide further evidence on the causality and co-movements of Scandinavian stock markets. Mathur and Subrahmanyam (1991) recently investigated the causality of Swedish, Norwegian, Danish and Finnish stock market returns, using monthly data for the period 19761985. They found that Swedish markets led the indices for Denmark, Finland and Norway, while Norway also influenced the Swedish and Danish markets. The Danish and Finnish markets did not show any significant influence on the other markets investigated.

The present paper differs from previous studies, and especially Mathur and Subrahmanyam (1991), on three counts. Firstly, it includes world-wide returns in investigating the lead-lag structures of the Scandinavian stock markets. This is important in the light of the higher level of capital movement between the world’s financial markets, and it can thus be assumed that global stock market behaviour influences Scandinavian market returns. Secondly, daily data from these markets are employed, The use of daily indices enables us to investigate the information flow between these

61

6X M. MALKAMAKI er cd

markets in greater detail. Thirdly, the period February 1988 to April 1990 is used in this study. Recent literature (see e.g. Nam Jeon and von Furstenberg, 1990 and Le. 1991) indicates that international co-movement in stock price indices has increased significantly since the October crash in 1987. In addition, the choice of such a late period is interesting because of the recent changes in structure and legislation in the Scandinavian markets, including the increase in trading volumes (see Korajczyk and Viallet (1989), where it was found that the behaviour of international asset-pricing models is significantly affected by changes in the regulatory environment in financial markets).

We hypothesize that world-wide returns lead Scandinavian market returns for two main reasons. Firstly, the world-wide index is heavily influenced by the U.S. market, which opens after the Scandinavian markets are already closed. The same kind of return spillover effect from New York to Tokyo has recently been reported by Hamao et al. (1990). Secondly, the non-syncroneity bias due to infrequent trading is much lower in the world index than in the indices of the Scandinavian markets. Thus, we can assume that the world index adjusts more rapidly to new information. This last aspect also leads us to hypothesize that the Swedish market, being clearly the largest market in Scandinavia, leads the returns of the other Scandinavian markets.

The remainder of the paper is organized as follows. In Section 2, a review of relevant literature is provided. In the third section, the data used in the study are described. Section 4 contains the empirical results of the study. Finally, in Section 5 conclusions are drawn.

2. LITERATURE REVIEW

Significant relationships between the returns of different stock markets have been reported in several studies. In an early paper, Makridakis and Wheelwright (1974) investigated the short-term stability of the relationships between 14 stock market indices and reported that the co-movements of international stock exchanges seem to be random. Similar conclusions were drawn by Hilliard (1979). However, the results of other more recent studies suggest a higher level of stability in international stock markets’ co-movements (see e.g. von Furstenberg and Nam Jeon, 1989; Grinold et al., 1989; Merit and Merit, 1989; Le, 1991 and Malkamaki, et al. 1991). A general trend seems to be that stock prices in different countries have been tending to move more similarly in the 1980s than before. Especially strong interrelationships have been reported since the October crash in 1987, and it appears that the co-movements have significantly changed since the crash period.

Nam Jeon and von Furstenberg (1990) investigated the interrelationships between stock prices in Tokyo, Frankfurt, London and New York for the period January 1986 to November 1988. Evidence of a remarkable structural change as regards the correlation structure and leadership was found in these four major markets since the crash in October 1987. International co-movements in stock price indices have increased significantly since the stock market crisis. The role of the immediately preceding market of stock prices in the determination of stock prices was also greatly enhanced. Le (1991) reported somewhat similar results to those of Nam Jeon and von Furstenberg (1990). A dramatic increase in correlation between U.S. and foreign market returns was found and

CAUSALITY AND CO-MOVEMENTS OF STOCK MARKET RETURNS 6’)

a significant impact was observed on international investors and for risk diversification, portfolio balancing and asset allocation.

Malkamaki et al. (1991) analysed the co-movements of stock returns in 24 countries in 1988. Certain types of risk categories for different stock markets were found, and three possible main reasons for these were suggested. Firstly, economic trade and currency areas seemed to affect the riskiness of different stock markets, with North American, European and Oceanic stock exchanges clearly generating their own distinct factors. Secondly, the level of institutional development of a given stock market also appeared to be a factor determining the level of international co-movements. Thin stock markets, including Finland, seemed to exhibit a price behaviour of their own. Thirdly, the combined effect of time zones and efficiency was also analysed.

There is some evidence to suggest that in terms of information the Scandinavian markets are not fully integrated with each other or with the main markets of the world. Hietala (1989) investigated the international betas for Finnish stocks by regressing the returns of Finnish stocks to the global market portfolio, estimated in terms of the return on the value-weighted world index. The results revealed very low correlations between the returns on Finnish stocks and those of the world market porfolio. Hietala saw the legal restrictions in force in Finland in the mid-1980s as being the main reason for this. Martikainen et al. (1991) looked at the level of dependence of the Finnish stock markets on the Swedish and U.S. stock markets, using an internationally extended market model for Finnish stocks, in which it was assumed that the return on a given Finnish asset was dependent on returns on the Finnish, Swedish and U.S. stock markets. The analysis revealed that several Finnish stocks contain significant Swedish risk components, while the interrelation between Finnish and U.S. markets was found to be much less strong. Yli-Olli et al. (1990) recently used the Arbitrage Pricing Model to investigate the common factors in Finnish and Swedish stock markets, and were able to identify two or three stable factors generating stock returns in these two neighbouring countries.

3. DATA DESCRIPTION

For the purpose of the analysis, daily stock market returns for February 1988 to April 1990 from four Scandinavian stock markets, i.e. Sweden, Norway, Denmark and Finland, are used in this article. Our research period thus begins after the October 1987 crash. Recent literature (e.g. Le, 1991; Hamao et al., 1990) indicates that the information flow between the world’s stock markets has significantly increased since the crash, and our data thus offer an interesting starting point compared with that of Mathur and Subrahmanyam (1991) where older data were used. In addition, the value-weighted worldwide market index is used. The chosen indices are the Financial Times Actuaries World Indices published daily by the Financial Times in co-operation with Goldman, Sachs & Co, and Wood MacKenzie Co. Country indices are calculated as weighted arithmetic means of stock prices, normalized to the same base period. The most important practical advantages of the FTA country indices used here are their representativeness and comparability. In general, a minimum of 70% of total market value is represented by the index.

In the country indices, weighting equates to relative market values. The stock prices are carefully adjusted for influences due to capital changes on a daily basis. In this study

70 M. MALKAMAKI el cd

returns are measured as first differences in the natural logarithms of price indices. The computation of price indices is based on middle market prices at the close of business. When there has been no trade, prices from the previous day have been used. The indices are given in dollars. Our preliminary analysis, not reported here, produced rather similar results regarding the correlation structure of market returns, regardless of whether local currencies or dollar values were used (see Malkamaki et al., 1991). This supports the work of Mathur and Subrahmanyam (1991), which found no significant influence on the empirical results in this respect.

During the research period there were some significant barriers that prevented the free flow of international capital between the Scandinavian and other stock markets. Since then most of these barriers have been abolished. For instance, foreign investors could not in principle own more than 20% of industrial companies in Sweden, Norway and Finland, and were not allowed to participate in the stock derivatives markets. Scandinavian investors also faced certain restrictions when buying overseas securities. Furthermore, the rather modest level of trading in unrestricted stocks and different tax rates between the markets both serve to reduce the integration of the Scandinavian markets. The illiquidity of the markets has been claimed as a major reason for the observed inefficiencies in the Scandinavian markets (see e.g. Jennergren and Korsvold, 1974; Berglund, 1986 and Claesson, 1987). Finally, restrictions on short selling have prevented investors from conducting efficient portfolio management in Scandinavian markets. Recently, the restriction on short selling has been partly abolished in the Swedish stock market.

The macroeconomic conditions in the Scandinavian countries are relatively similar. Similarly, high standards of living with fairly low rates of unemployment and a high standard of social services are typical of all four countries. Moreover, the economic co- operation between the countries is lively (for further analysis, see e.g. Mathur and Subrahmanyam, 1991).

4. EMPIRICAL RESULTS

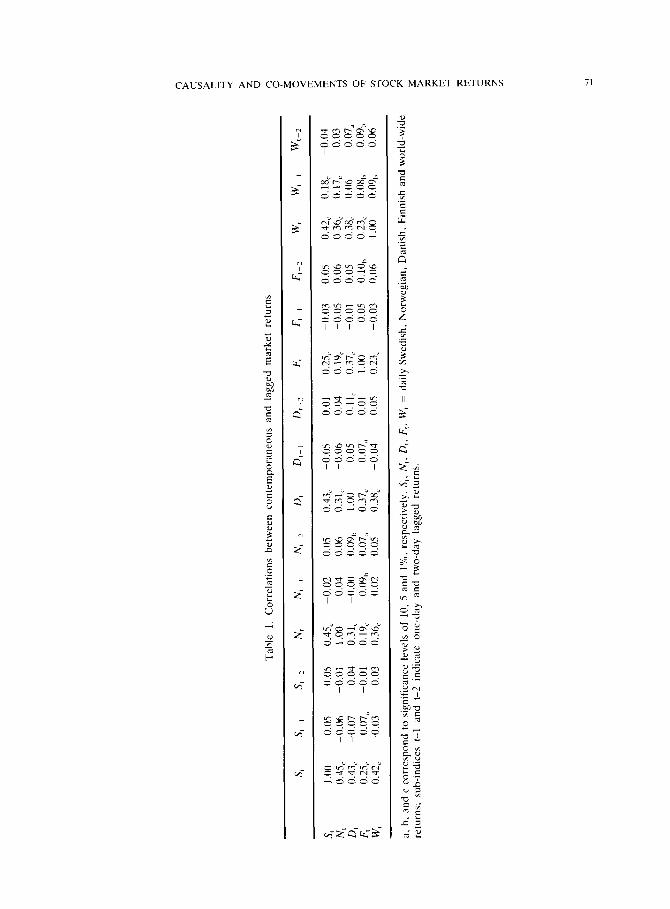

The main purpose of this paper is to investigate the question of whether various Scandinavian market returns lead one another. The same issue is also explored in the context of world-wide vs Scandinavian results. To this end, Granger causality tests are applied. Before examining the results of these tests, it could be useful to look first at the correlation coefficients between contemporaneous and lagged values of returns. These figures are presented in Table 1.

We can see here that contemporaneous returns on all markets, and the world index, are positively correlated. The lowest relation to other index returns is reported for the Finnish returns. There appear to be several reasons for the low level of global integration in the Finnish stock market. First of all, the thin trading in the Finnish stock market has obviously made transactions in Finnish stocks very difficult for foreign investors, and the relatively low number of non-restricted shares that can be bought by foreigners is a further disadvantage. In addition, Finnish firms are not very well known in global terms. Because of the complicated accounting system used in Finland, the foreign investors’ investment analysis is a complex affair and it is very difficult indeed to compare the status of Finnish firms with that of overseas companies. These explanations are naturally more

CAUSALITY AND CO-MOVEMENTS OF STOCK MARKET RETURNS 71

73 M. MALKAMAKI et ul

or less speculative, but they do probably help to account for the low level of integration between Finnish and other stock markets.

The results for the market returns on days t-l and t-2 are mainly consistent with the hypothesis that the stock markets do not possess significant ability for forecasting the future returns on other markets. The correlations are very low, and generally deviate insignificantly from zero. This is what we might expect to see on informationally efficient stock markets.

Although the cross-correlation coefficients provide valuable information concerning the relationship between the two time series, they do not test the direct causality. They do not answer the question of whether some market returns lead the returns on certain other markets or vice versa. A number of different causality tests have been proposed and used in the literature, and a view of these tests is provided in Geweke et al. (1983). The present study employs a regression technique in the Granger (1969) sense of causality.

A time series { Yt} is said according to Granger to cause another time series {Xt}, if the present X can be predicted better by using past values of y than by not doing so, with other relevant information including the past values of x being used in either case. The hypothesis that { Yt} causes {Xt} can be examined by regressing {Xt} on lagged {Xt} and lagged { Yt}, and testing the joint significance of the lagged values of { Yt}.

In order to test the null hypothesis that the Finnish returns (F) do not lead Swedish returns (S), the following steps are carried out. Firstly, the following regression is performed:

S, = u + b,S,_, + bzS,_2 + e,. (1)

Secondly, the regression added with lagged values of F is run

S, = a + b,S,_, + b2S,_z + b3Ftpl + b4Ftp2 + e,. (2)

Thirdly, in order to test the null hypothesis we compute the following F-statistic, which has the distribution F(k, - kc,, II - k, - 1):

F = [(n - k, - l)l(k, - k,)] [(R; - R,‘,)V - R,‘)], (3)

where rz = number of observations in the regression; k,, = the number of explanatory variables used in Equation (1); kr = the number of explanatory variables used in Equation (2); Ri = R* of the first regression; and Ri = R’ of the second regression.

A statistically significant F-value would indicate Granger causality from Finnish to Swedish markets. The causal relationship in the reverse direction is examined by substituting S, for F, and vice versa. If a causal relationship is also reported from the Swedish to the Finnish market, then there is feedback between these two markets. The same procedure is then repeated for each Scandinavian market investigated. The above procedure describes the standard Granger causality test procedure used in the literature. The standard Granger causality test includes only differenced series, i.e. in our case returns. However, it does not indicate whether the level series, i.e. in our cases logarithmic stock price indices, show any common trend. If the level series are co- integrated (see e.g. Cesar er al. (1990) for a clear presentation of co-integration theory), an error correction term should be included as an additional regressor to the causality

CAUSALITY AND CO-MOVEMENTS OF STOCK MAKKET RETURNS 73

tests (see Engle and Granger, 1987). This error-correction term is the residual term from the co-integration equation Pl, = ?J’2, + ht + E,, where Pl and p2 are level series. This is because the causality between markets may otherwise be underestimated, by ignoring the common trend in price series.

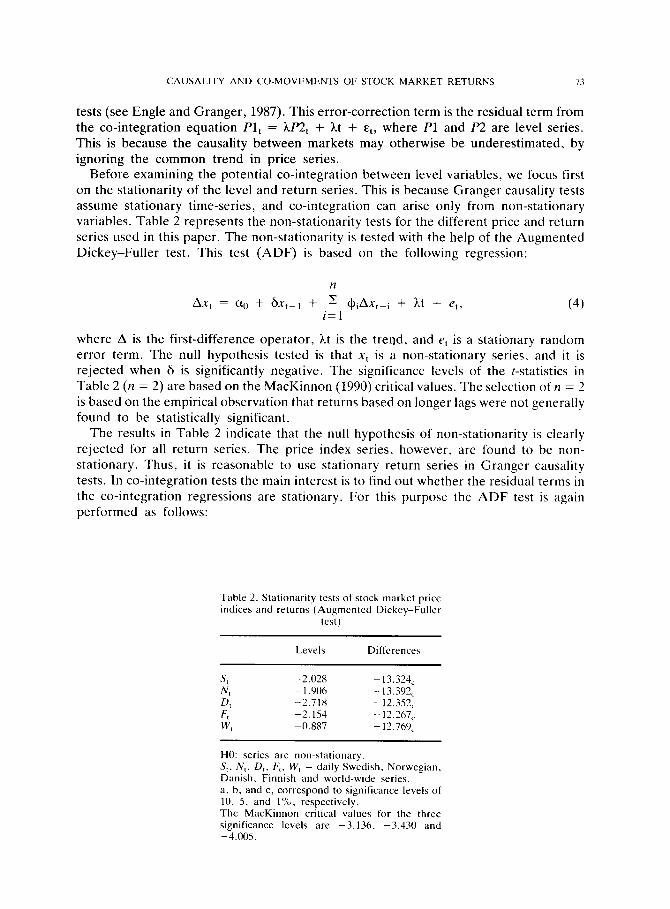

Before examining the potential co-integration between level variables, we focus first on the stationarity of the level and return series. This is because Granger causality tests assume stationary time-series, and co-integration can arise only from non-stationary variables. Table 2 represents the non-stationarity tests for the different price and return series used in this paper. The non-stationarity is tested with the help of the Augmented Dickey-Fuller test. This test (ADF) is based on the following regression:

n

AX, = at, + b-1 + ’ ~iAX,_i + ht + et, i=l

(4)

where A is the first-difference operator, ht is the trend, and e, is a stationary random error term. The null hypothesis tested is that x, is a non-stationary series, and it is rejected when 6 is significantly negative. The significance levels of the f-statistics in Table 2 (n = 2) are based on the MacKinnon (1990) critical values. The selection of n = 2 is based on the empirical observation that returns based on longer lags were not generally found to be statistically significant.

The results in Table 2 indicate that the null hypothesis of non-stationarity is clearly rejected for all return series. The price index series, however, are found to be non- stationary. Thus, it is reasonable to use stationary return series in Granger causality tests. In co-integration tests the main interest is to find out whether the residual terms in the co-integration regressions are stationary. For this purpose the ADF test is again performed as follows:

Table 2. Stationarity tests of stock market price indices and returns (Augmented Dickey-Fuller

test)

Levels Differences

St -2.028 ~ 13.324, N, -1.906 - 13.392, D, -2.71X - 12.352, F, -2.154 - 12.267, W -0.887 - 12.769,

HO: series are non-stationary. S,. N,. L),. F,, W, = daily Swedish. Norwegian, Danish, Finnish and world-wide series. a, h, and c, correspond to significance levels of IO. 5, and 1%. respectively. The MacKinnon critical values for the three significance levels are -3.136. -3.430 and -4.005.

74 M. MALKAMkKI et ul.

m

AE, = $F,_, + ’ Cpi AE,-i + vt, (5) i=l

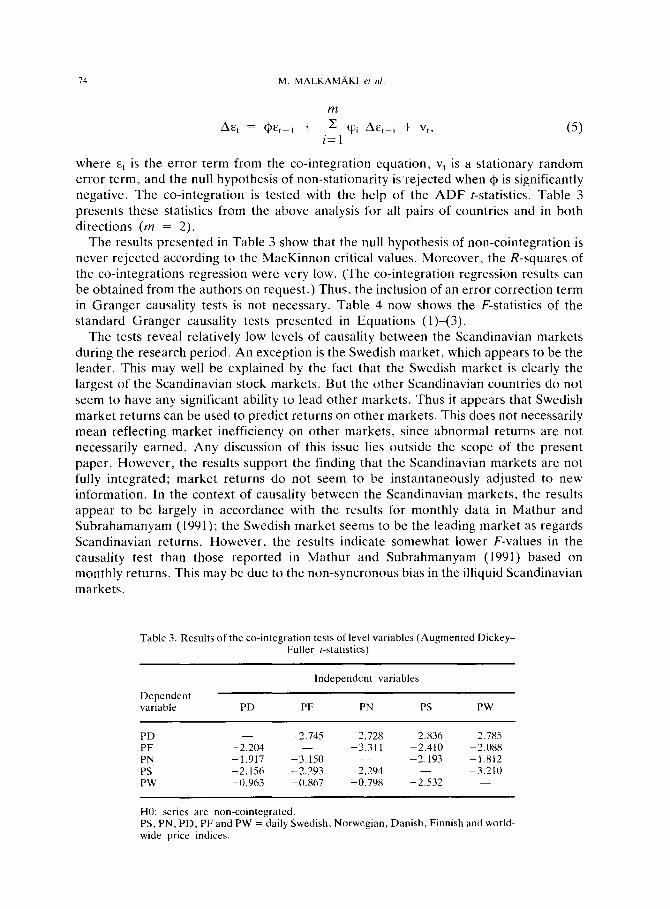

where E, is the error term from the co-integration equation, vt is a stationary random error term, and the null hypothesis of non-stationarity is’rejected when $ is significantly negative. The co-integration is tested with the help of the ADF t-statistics. Table 3 presents these statistics from the above analysis for all pairs of countries and in both directions (m = 2).

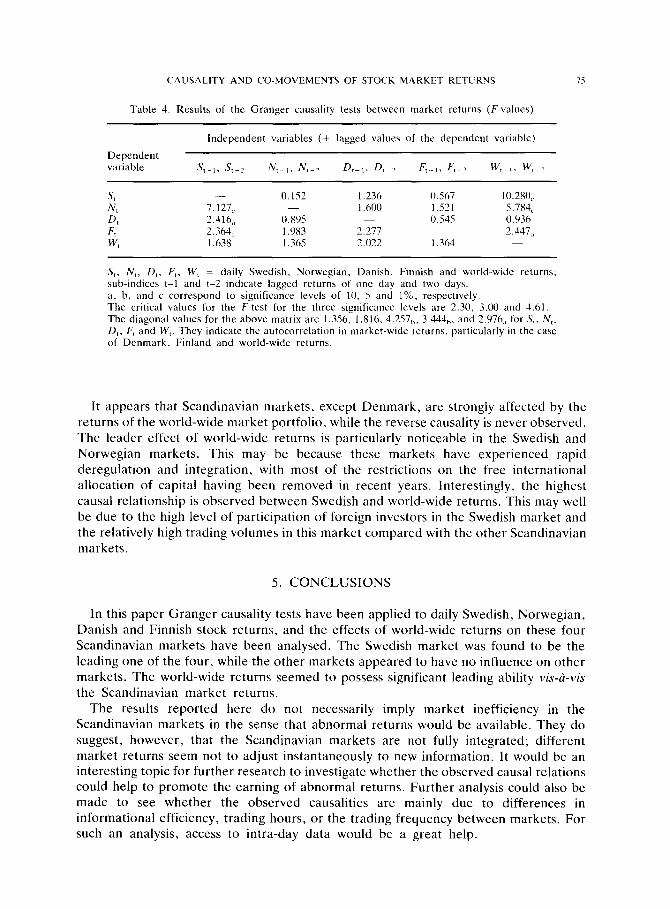

The results presented in Table 3 show that the null hypothesis of non-cointegration is never rejected according to the MacKinnon critical values. Moreover, the R-squares of the co-integrations regression were very low. (The co-integration regression results can be obtained from the authors on request.) Thus, the inclusion of an error correction term in Granger causality tests is not necessary. Table 4 now shows the F-statistics of the standard Granger causality tests presented in Equations (l)-(3).

The tests reveal relatively low levels of causality between the Scandinavian markets during the research period. An exception is the Swedish market, which appears to be the leader. This may well be explained by the fact that the Swedish market is clearly the largest of the Scandinavian stock markets. But the other Scandinavian countries do not seem to have any significant ability to lead other markets. Thus it appears that Swedish market returns can be used to predict returns on other markets. This does not necessarily mean reflecting market inefficiency on other markets, since abnormal returns are not necessarily earned. Any discussion of this issue lies outside the scope of the present paper. However, the results support the finding that the Scandinavian markets are not fully integrated; market returns do not seem to be instantaneously adjusted to new information. In the context of causality between the Scandinavian markets, the results appear to be largely in accordance with the results for monthly data in Mathur and Subrahamanyam (1991); the Swedish market seems to be the leading market as regards Scandinavian returns. However, the results indicate somewhat lower F-values in the causality test than those reported in Mathur and Subrahmanyam (1991) based on monthly returns. This may be due to the non-syncronous bias in the illiquid Scandinavian

markets.

Table 3. Results of the co-integration tests of level variables (Augmented Dickey- Fuller I-statistics)

Dependent variable PD

Independent variables

PF PN PS PW

PD - -2.745 -2.728 -2.836 -2.785 PF -2.204 -3.311 -2.410 -2.088 PN -1.917 -3.150 -2.193 -1.812 PS -2.156 -2.293 -2.294 -3.210 PW -0.963 -0.867 -0.798 -2.532

HO: series are non-cointegrated. PS, PN, PD, PF and PW = daily Swedish, Norwegian, Danish, Finnish and world- wide price indices.

CAUSALITY AND CO-MOVEMENTS OF STOCK MARKET RETURNS

Table 4. Results of the Granger causality tests between market returns (F-values)

75

Dependent variable

Independent variables (+ lagged values of the dependent variable)

.‘L,, St-2 N, ,, Nf-2 D,+,. D, 1 F, _I, Fr-2 W I. W 2

;, 9 0.152 7.127, I.236 1 ,600 0.567 1.521 10.2x0, 5.784, D, 2.416,, 0.X% 0.545 0.936 F, 2.364., I.983 2.277 2.447~, W 1.638 I .36S 2.022 1.364

S,. N,, D,. F,, W, = daily Swedish. Norwegian. Danish. Finnish and world-wide returns; sub-indices t-l and t-2 indicate lagged returns of one day and two days. a, b. and c correspond to significance levels of 10. 5 and 1%. respectively. The critical values for the F-test for the three significance levels are 2.30. 3.00 and 4.61. The diagonal values for the above matrix are 1.356, 1.816. 4.257,,, 3.444,. and 2.976,, for S,. N,. D,, F, and W,. They indicate the autocorrclation in market-wide returns, particularly in the case of Denmark, Finland and world-wide returns.

It appears that Scandinavian markets, except Denmark, are strongly affected by the returns of the world-wide market portfolio, while the reverse causality is never observed. The leader effect of world-wide returns is particularly noticeable in the Swedish and Norwegian markets. This may be because these markets have experienced rapid deregulation and integration, with most of the restrictions on the free international allocation of capital having been removed in recent years. Interestingly, the highest causal relationship is observed between Swedish and world-wide returns. This may well be due to the high level of participation of foreign investors in the Swedish market and the relatively high trading volumes in this market compared with the other Scandinavian markets.

5. CONCLUSIONS

In this paper Granger causality tests have been applied to daily Swedish, Norwegian, Danish and Finnish stock returns, and the effects of world-wide returns on these four Scandinavian markets have been analysed. The Swedish market was found to be the leading one of the four, while the other markets appeared to have no influence on other markets. The world-wide returns seemed to possess significant leading ability vis-d-vis the Scandinavian market returns.

The results reported here do not necessarily imply market inefficiency in the Scandinavian markets in the sense that abnormal returns would be available. They do suggest, however, that the Scandinavian markets are not fully integrated; different market returns seem not to adjust instantaneously to new information. It would be an interesting topic for further research to investigate whether the observed causal relations could help to promote the earning of abnormal returns. Further analysis could also be made to see whether the observed causalities are mainly due to differences in informational efficiency, trading hours, or the trading frequency between markets. For such an analysis, access to intra-day data would be a great help.

76 M. MALKAMAKI et ul

Acktn~w/edgrmen~s - We are grateful to the Editor. Antti Kanto, Martti Luoma, Juuso Vataja, Matti Viren. and anonymous Scandinavian Journul of Munugrmern referees for their useful comments on earlier versions of the paper.

REFERENCES

Berglund. T.. Anomalies in stock returns on a thin security market. Ph.D. Disserturion (II the Swedish School of Economics und Business Adminisnztion. Helsinki, Finland (1986).

Cesar, H.. De Haan. J. and Jacobs. J., Monetary targeting in The Netherlands: an application of co-integration tests, Applied Economics (19YO). pp. 1537-154X.

Claesson, K. (1987). Effektivitetcn pa Stockholms Fondbors, Ph.D. Dissernnion. Stockholm. Sweden. Engle. R. F. and Granger. C. W. J.. Co-integration and an error correction: representation. estimation and

testing. Economerricu (19X7), pp. 251-276. von Furstenberg, G. M. and Nam Jeon, B., International stock price movements: links and messages.

Brookings Pupers on Economic Acrivitv (19X9), No. I. DD. 125-l7Y. Geweke, Jy. Me&e, R. and Dent, W., Comparing alternative ;csts of causality in temporal systems. Analytic

results and experimental evidence. Journal of Economrrrics (1983). pp. 161-194. Granger. C. W., Investigating causal relations by economic models and cross-spectral methods. Economrmricu

(1969), pp. 423338. Grinold. R., Rudd, A. and Stefck. D., Global factors: fact or fiction. Journal of Portfolio Munugement (19X9).

Fall, pp. 79-88. Hamao..?.. Masulis, R. W. and Ng. V.. Correlations in price changes and volatility across international stock

markets. Review of Financial Srudies (1990). No. 2, mu. 2X1-307. Hictala, P. T., Asset-pricing in partially segmented mark&. Evidence from the Finnish markets. Journul of

Finance (1989). pp. 697-718. Hilliard. J. E., The relationship between equity indices on world exchanges. Journal of Finance (1979), No. I,

pp. 103-l 14. Jennergren, P. and Korsvold, P. E., Price formation in the Norwegian and Swedish stock markets. Some

random walk tests. Swedish Journul of Economics (1974). pp. 171-185. Korajczyk, R. A. and Viallet, C. J., An empirical investigation of international asset pricing. Reviru, of

Financial Sfudies (1989). No. 2, pp. 553-585. Le. S. V.. International investment diversification before and after the October IY. 1987 stock market crisis.

Journal of Business Research (1991). No. 4, pp. 305-310. MacKinnon, J., Critical values for cointegration tests. University of Culiforniu. San Diego. Working Paper

(1990). Makridakis, S. G. and Wheelwright, S. C., An analysis of the inter-relationships among the world stock

exchanges. Journal of Business Finance and Accounring (lY74), pp. 195-215. Malkamlki, M. J., Martikainen, T. and Perttunen, J.. On the riskiness of the world’s stock markets. Europeun

Journal of Operational Research (1991). No. 3, pp. 2X8-296. Martikainen, T.. Virtanen, I. and Yli-Olli. P., On the international co-movements of capital markets: evidence

from two Scandinavian stock markets. In: Khosrow Fatemi (Ed.), Infernutionul Trude und Finunce in rhe 1990’s. Proceedings of the lnternutionul Trude und Finunce Association, pp. 995-1009.

Mathur, I. and Subrahmanyam, V., An analysis of the Scandinavian stock indices. Journul of Inrermnionnl Finunciul Markets, Institutions and Money (1991). No. 1, pp. 01-l 14.

Merit, I. and Merit, G.. Potential gains from’international portfolio diversification and inter-temporal stability and seasonality in international stock market relationships. Journal of Banking und Finunce (1989). No. 4/5, pp. 627-640.

Nam Jcon. B. and von Furstenberg, G. M., Growing international co-movements in stock price indexes. Quurferly Review of Economics and Business (199(l), No. 3, pp. 15-30.

Yli-Olli. P., Virtanen. I. and Martikainen, T., Common factors in the Arbitrage Pricing Model in two Scandinavian countries. OMEGA lnrernarional Journal of Managemenr Science (1990). No. 6. pp. 615-624.