Embed Size (px)

Citation preview

Oil Market Outlook

NGA Market Forum, April 21 –Hartford, CT

Forward-Looking Statements

This presentation contains certain forward-looking statements that involve risks and uncertainties. Forward-looking statements are sometimes, but not always, identified by such phrases as “will”, “expects”, “is expected to”, “should”, “may”, “is likely to”, “intends” and “believes”. All statements other than statements of historical facts, including, among others, statements such as those regarding our future targeted financial position; return on capital employed; oil and gas production forecasts; reserve information; reserve recovery factors; plans for future development and operation of projects; estimates of capital expenditures and our expected exploration and development activities and plans; exploration expenditures; finding and development and production costs; expected start-up dates for projects; expected synergies resulting from the merger of Statoil ASA and the oil and gas assets of Norsk Hydro ASA; HSE goals and objectives of management for future operations are forward-looking statements. You should not place undue reliance on these forward-looking statements. Our actual results could differ materially from those anticipated in the forward-looking statements for many reasons, including the risks described in Item 3-Key Information in our Annual Report on Form 20-F/A filed with the US Securities and Exchange Commission, which can be found our website at www.Statoil.com.

These forward-looking statements reflect current views with respect to future events and are, by their nature, subject to significant risks and uncertainties because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements, including levels of industry product supply, demand and pricing; currency exchange rates; political and economic policies of Norway and other oil-producing countries; general economic conditions; political stability and economic growth in relevant areas of the world; global political events and actions, including war, terrorism and sanctions; the ability of Statoil to successfully integrate the oil and gas assets of Norsk Hydro ASA and the realization of expected synergies and cost savings from the merger; the timing of bringing new fields on stream; material differences from reserves estimates; inability to find and develop reserves; adverse changes in tax regimes; development and use of new technology; geological or technical difficulties; the actions of competitors; the actions of field partners; the actions of governments; relevant governmental approvals; industrial actions by workers; prolonged adverse weather conditions; natural disasters and other changes to business conditions; and other factors discussed in our Annual Report on Form 20-F/A.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot assure you that our future results, level of activity, performance or achievements will meet these expectations. Moreover, neither we nor any other person assumes responsibility for the accuracy and completeness of the forward-looking statements. Unless we are required by law to update these statements, we will not necessarily update any of these statements after the date of this presentation, either to conform them to actual results or to changes in our expectations.

Oil and Gas Reserves

Cautionary Note to U.S. Investors -- The United States Securities and Exchange Commission permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We use certain terms in this presentation, such as probable reserves, that the SEC's guidelines strictly prohibit us from including in filings with the SEC. U.S. Investors are urged to consider closely the disclosure in our Annual Report on Form 20-F/A, File No. 1-15200, available on our website at www.Statoil.com. You can also obtain this form from the SEC by calling 1-800-SEC-0330.

Disclaimer

2

Presentation Outline

• Who is Statoil?

• Current Global Market Fundamentals

• US Oil Production Growth Potential

3

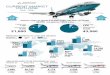

Statoil’s Business

International energy company with operations in

38 countries

More than 40 years of experience from oil and

gas production on the Norwegian continental

shelf

Headquartered in Stavanger,

Norway with approximately 22,000 employees

worldwide, and listed on the New York and

Oslo stock exchanges

Statoil’s strategy is centered around growth

and value enhancement through technology-

focused upstream strategy, strategic

midstream and downstream positioning, and

renewable energy and low-carbon

technologies

Eagle Ford Operator

Marcellus Operator

Bakken Operator

Eagle Ford

Alaska and Marcellus

Oil Sands, Canada

Deepwater Gulf of Mexico

Grand Banks, Canada

Oil trading, New York

2013

2012

2011

2010

2008

2007

2004

1996

1987

North American operations

Beaufort Sea

Kai Kos Dehseh

St. Johns

Marcellus

Eagle Ford Gulf of Mexico

Stamford

Washington D.C.

Grand Banks

Anchorage

Houston

Mexico City

South Riding Point Terminal Grand Bahamas

Calgary

Bakken

Austin

Williston

Chukchi Sea

Statoil Office

Statoil Asset

A reminder of the fundamentals of our industry

1970s │Big discoveries 2000s │Credit crunch and shale 1980s │The oil glut 1990s │Middle East

Volatility is the name of the game – predictions are uncertain

Brent price development

$/bbl

0

40

80

120

160

1970 1980 1990 2000 2010

Brent real Brent nominal

Sources: Thomson Reuters Datastream

6

7

Global oil demand growth mbd

Oil demand outlook – medium-term Average annual demand growth of 1.2 mbd

Source: IEA; Statoil

-0.5

0.0

0.5

1.0

1.5

2.0

2015 2016 2017 2018 2019 2020

Other non-OECD China

India OECD Americas

OECD Europe Other OECD

Total

• Demand growth driven by EM

• China and India continue delivering

healthy growth

• OECD resumes its downward

trend

• Rising prices towards the end of

the decade will impact demand

8

US oil production mbd

Oil supply outlook - medium-term US expected to deliver average annual growth of 0.5 mbd

Source: IEA; Statoil

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

0

2

4

6

8

10

12

14

16

2015 2016 2017 2018 2019 2020

Growth Production

0

2

4

6

8

10

12

14

16

2015 2016 2017 2018 2019 2020

Alaska GOM L-48 conventional NGL Shale

US oil production mbd

9

Non-Opec production ex US mbd, change yoy

Oil supply outlook – medium-term Non-Opec ex US in slight decline

Source: IEA; Statoil

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

2015 2016 2017 2018 2019 2020

Latin America Other non-OECD

OECD ex US Russia

• Reduced levels of investment in

the near term will bring less

production as the current project

portfolio runs out and natural

decline takes its toll

• Canada will add healthy growth

together with Brazil

• Russia heading for decline

10

Supply & Demand balance and

commercial oil stocks mbd

OECD commercial oil stocks mb, annual average

Global balance Tightening towards 2020

Source: IEA; Statoil

-0.6

0.0

0.6

1.2

1.8Change in oil stocks

94

96

98

100

102

2015 2016 2017 2018 2019 2020

Oil demand Oil supply

1800

1900

2000

2100

2200

2300

2400

2500

2600

2700

2015 2016 2017 2018 2019 2020

stocks change historical average

Today’s capex reductions risk tomorrow’s bbls

11

Project delays due to low price environment mbd

Sources: PIRA

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

By 2016 By 2018 After 2018

UK

Qatar

Kazakhstan

US-GOM

Saudi Arabia

Canada

Nigeria

Angola

Sources: IEA; Statoil

Supply & Demand balance (mbd)

94

95

96

97

98

99

100

101

102

2015 2016 2017 2018 2019 2020

Oil demand Oil supply

Can a more competitive shale bbl fill the gap?

12

US Tight Oil Price Supply Curve Shale Crude Oil Production @ $70/bbl mbd

Source: ARI Consulting

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2015 2020 20252015 2016

$-

$20

$40

$60

$80

$100

$120

$140

$160

$180

0 20 40 60 80 100

$/B

bl W

TI

Remaining Recoverable Resource (BBbls)

2013 2016

Where will the barrels come from?

13

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2014 2016 2018 2020 2022 2024 2026 2028 2030

Kbpd

Permian Eagleford Bakken Niobrara Woodford (SCOOP/STACK) Other

Cushing

~63% prod

closer to water

with sufficient

infrastructure

USGC

N.Dakota

Source: ARI ; Statoil

US Infrastructure beginning to catch up

14

NA Crude Differentials to Brent USD/bbl

-$40

-$35

-$30

-$25

-$20

-$15

-$10

-$5

$0

$5

WTI - Brent WCS - Brent Bakken - Brent

2013

2014

2015

2016

2017

2018

2019

2020

Source: Platts daily prices through Jan 2016.

NYMEX and Argus for 2016-2020 price outlook

15

Brent price short-term forecasts (USD/bbl)

30

50

70

90

110

130

2016 2022 2028 2034 2040

Brent price long-term forecasts (USD/bbl)

30

50

70

90

110

2015 2016 2017 2018

So, what can we expect in terms of pricing Large deviations, but all above futures prices from 2017 and onwards

Sources: Selected market outlook reports, Statoil * Lambert Energy’s medium-term Brent crude oil price

Presenter’s name: Matthew Partridge

Presenter’s title: Head of North American

Market Analysis

E-mail address: [email protected]

Tel: +203 905 7303 www.statoil.com

16