Embed Size (px)

Citation preview

Reporting2015

THE GLOBAL OIL AND GASINDUSTRY ASSOCIATIONFOR ENVIRONMENTALAND SOCIAL ISSUES

www.ipieca.org

Oil and gas industry guidance onvoluntary sustainability reportingA

LEGAL NOTE

This voluntary guidance document is designed to serve as a resource for interested companies; the indicatorsand information referenced in this work do not establish an industry standard as to the nature of a company’spublic reporting practice. The recommendations in this Guidance on how to report on a particular issue areaddressed to those companies who choose to include that issue in their voluntary sustainability reporting, andterms such as ’the reporting company should …’ are to be understood in this sense.

The terms and definitions used in this document are not necessarily the same as terms and definitions used invarious statutes, rules, codes or other authoritative legal documents. Users and readers of this document shouldrefer to relevant legal sources or consult their own legal counsel for explanations as to how the terms anddefinitions used in this document may differ from the legal terms and definitions (e.g. spills and hazardouswastes) used in their particular areas of operation. Anything in this document regarding voluntary reporting ofindicators is not intended to imply that any of the indicators are required to be reported under any national, localor other law. Furthermore, it is not intended to serve as a substitute for existing public reporting requirementsand regulations. Any company reporter that has a question as to whether or not reports that follow theinformation contained herein will meet any specific reporting requirements applicable to their particularoperations should consult with the reporter’s own legal counsel.

A CAUTIONARY NOTE REGARDING PERFORMANCE INDICATORS

Aggregated, company-level, non-financial performance data, developed using the indicators in this Guidance,can be informative for comparing relative performance among different companies, such as benchmarkingsafety incident statistics across the oil and gas industry. A company can use such comparisons to evaluate itsown performance relative to peers, and identify areas for potential improvement. However, limitations tocomparability exist due to various factors including the different methods companies may use to measure,normalize and report specific indicators. Although efforts have been made throughout the Guidance to improvecomparability, report users are advised to exercise caution when using data from sustainability reports tocompare performance. For example, comparing two companies that report greenhouse gas emissions on adifferent basis (e.g. equity share vs. operated, as described in Appendix A) could be misleading regarding actualperformance. Specific indicators from similar operations can sometimes be usefully compared to helpperformance management. However, the company-level, aggregate data typically reported in sustainabilityreports may not provide adequate comparability for some metrics. Where this Guidance mentions comparability,it is not intended to imply that data in sustainability reports, and therefore companies’ performance, are alwaysdirectly comparable.

Separate from company sustainability reporting, industry associations and others may choose to implementspecific performance benchmarking studies, which may build upon the indicators in this Guidance.

It is also recognized that it may take a number of years for companies to begin to report new or revisedindicators and/or reporting elements. This is particularly important for social and economic indicators that arestill evolving within company sustainability reports.

IOGP Report 437

© IPIECA/API/IOGP 2015 All rights reserved.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic,mechanical, photocopying, recording or otherwise, without the prior consent of IPIECA, API and IOGP.

Oil and gas industryguidance on voluntarysustainability reporting

5th Floor, 209–215 Blackfriars Road, London SE1 8NL, United Kingdom

Telephone: +44 (0)20 3763 9700

E-mail: [email protected] Internet: www.iogp.org

International Association of Oil & Gas Producers

5th Floor, 209–215 Blackfriars Road, London SE1 8NL, United Kingdom

Telephone: +44 (0)20 7633 2388

E-mail: [email protected] Internet: www.ipieca.org

The global oil and gas industry association for environmental and social issues

The American Petroleum Institute

1220 L Street NW, Washington DC, 20005-4070, USA

Telephone: +1 202 682 8000

Internet: www.api.org

3rd Edition, 2015

IPIECA • API • IOGP

ii

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 4 39Environmental issues and indicators

Environmental issues and indicators: an overview 40

l Climate change and energy 41

E1: Greenhouse gas (GHG) emissions 42

E2: Energy use 46

E3: Alternative energy sources 49

E4: Flared gas 51

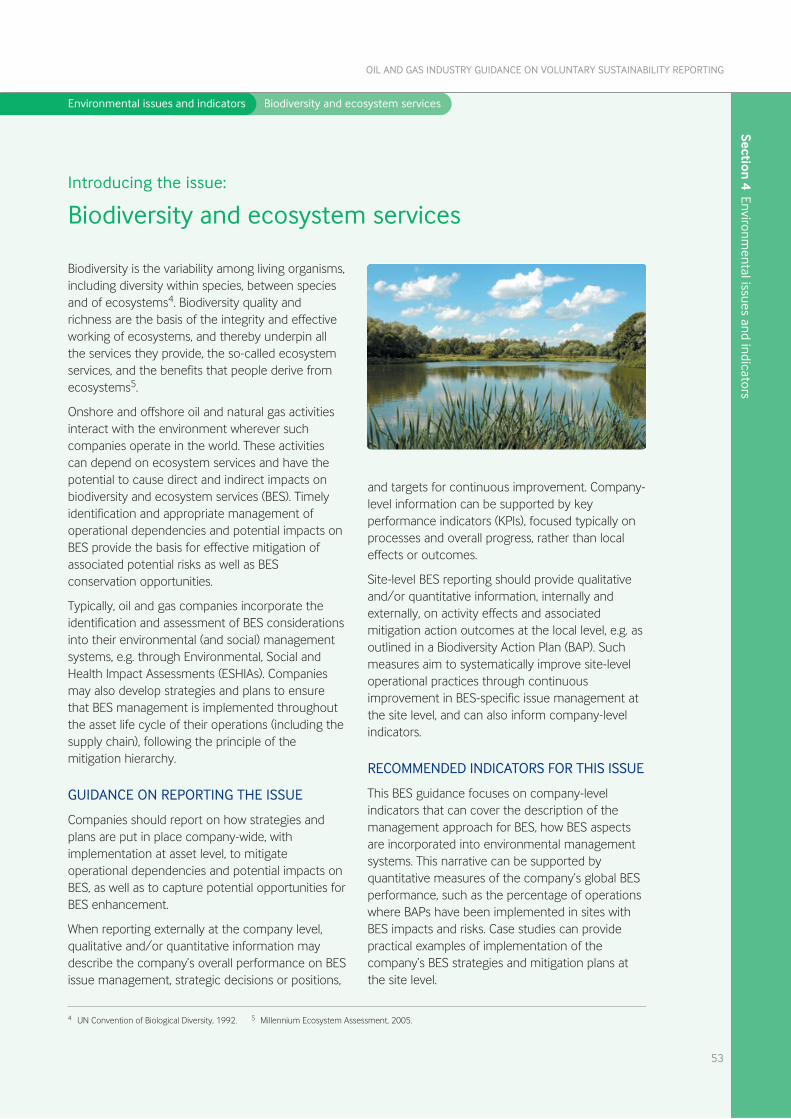

l Biodiversity and ecosystem services 53

E5: Biodiversity and ecosystem services 54

l Water 57

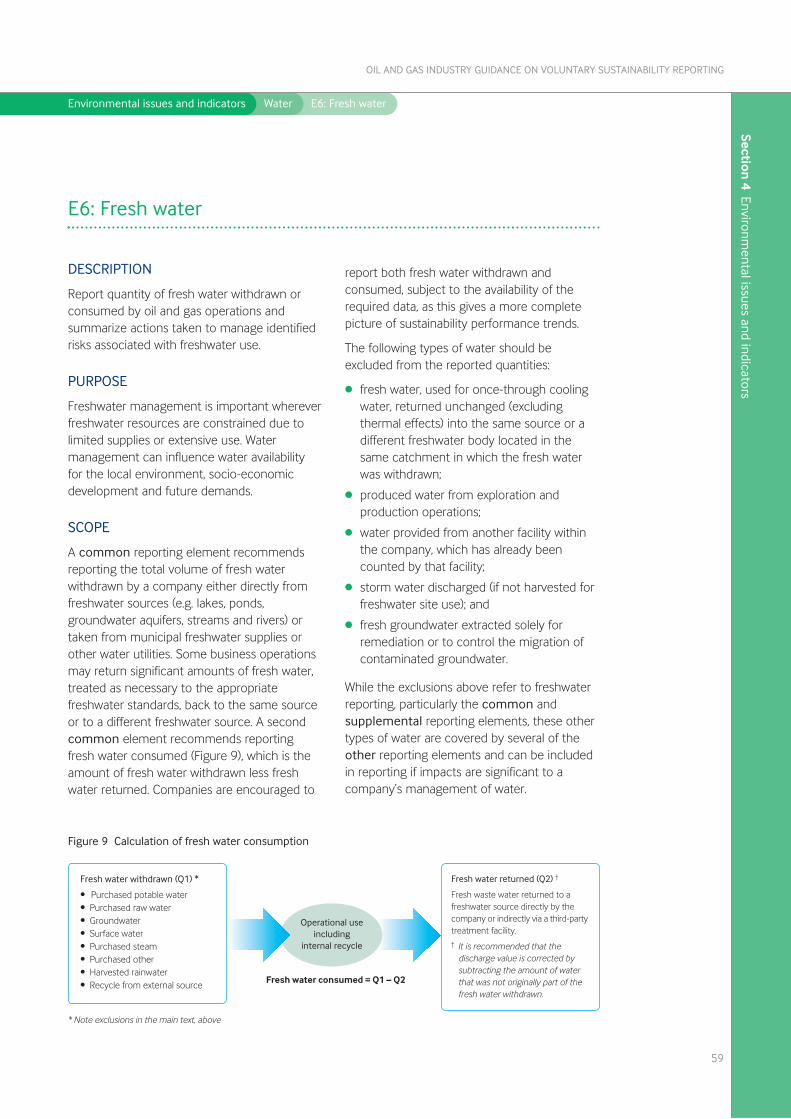

E6: Fresh water 59

E7: Discharges to water 63

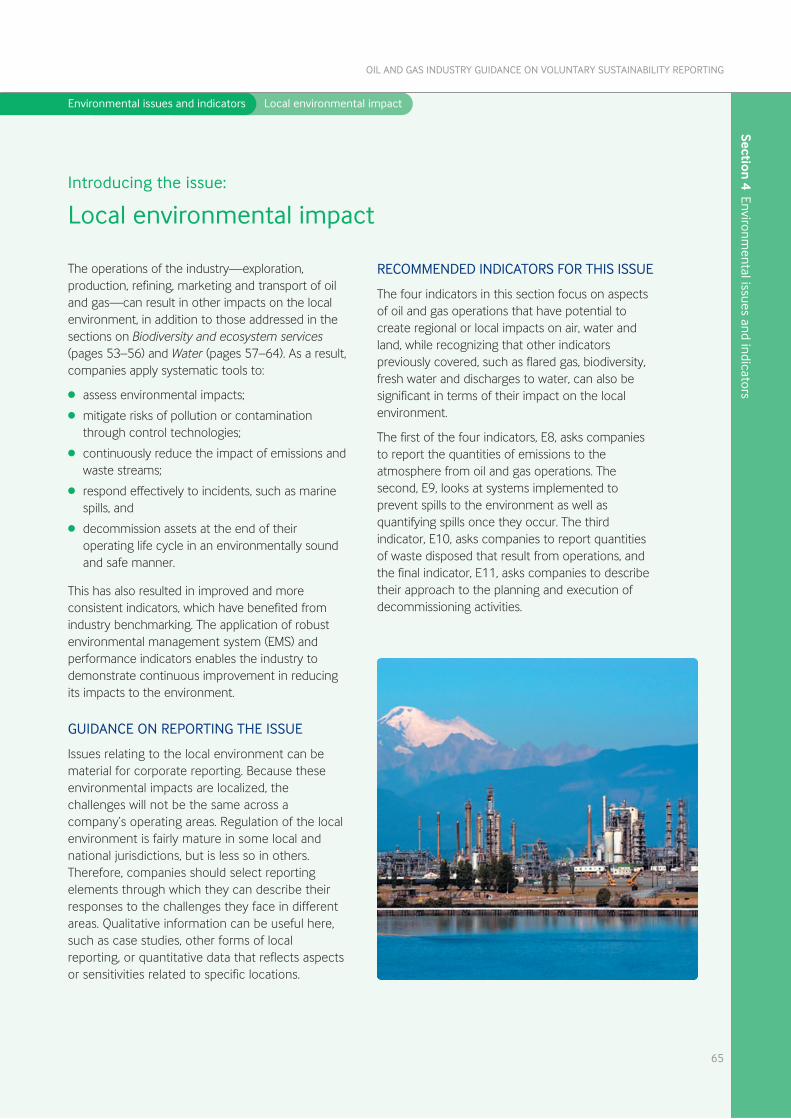

l Local environmental impact 65

E8: Other air emissions 66

E9: Spills to the environment 68

E10: Waste 71

E11: Decommissioning 74

Section 5 77Health and safety issues and indicators

Health and safety issues and indicators: 78an overview

l Workforce protection 79

HS1: Workforce participation 80

HS2: Workforce health 82

HS3: Occupational injury and illness incidents 84

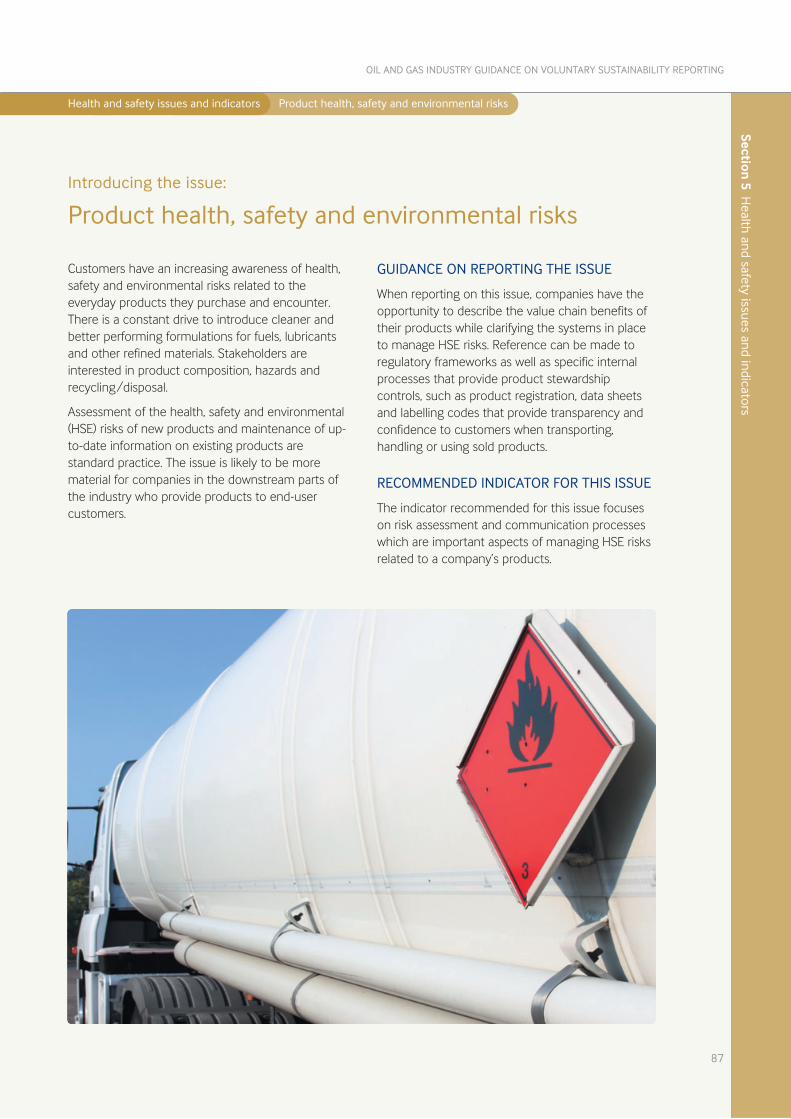

l Product health, safety and 87environmental risks

HS4: Product stewardship 88

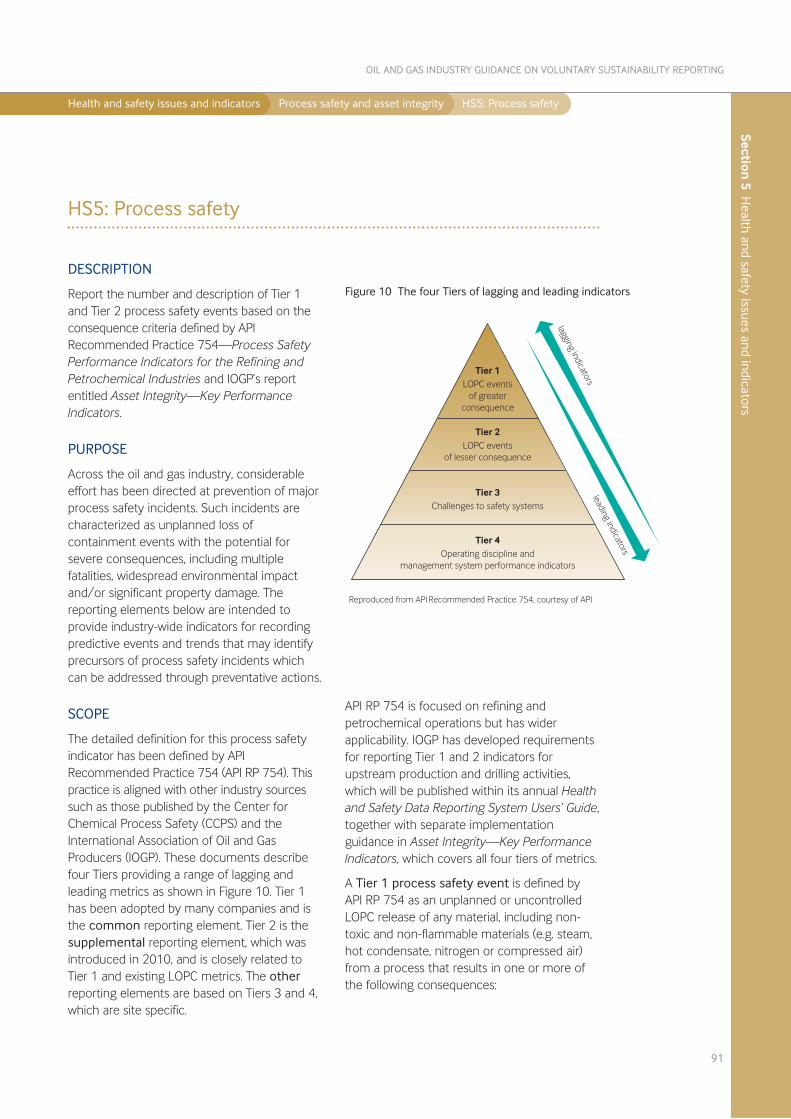

l Process safety and asset integrity 90

HS5: Process safety 91

Legal and cautionary notes Inside front cover

Improving our transparency: a foreword 2from the oil and gas industry associations

Joint statement of the independent 4Stakeholder Panel

Acknowledgements 6

Section 1 7Setting the context: why report?

Benefits of reporting 8

About the Guidance 9

Using the Guidance 9

Section 2 11The reporting process: how to report

General reporting principles 12

Process overview 12

Engaging stakeholders 13

Step 1: Articulate vision and strategy 15

Step 2: Describe governance and management systems 16

Step 3: Determine and prioritize material 18issues for reporting

Step 4 Select indicators and collect data 21

Step 5 Analyse data and incorporate into narrative 23

Step 6 Provide assurance 27

Section 3 29Issues and indicators: what to report

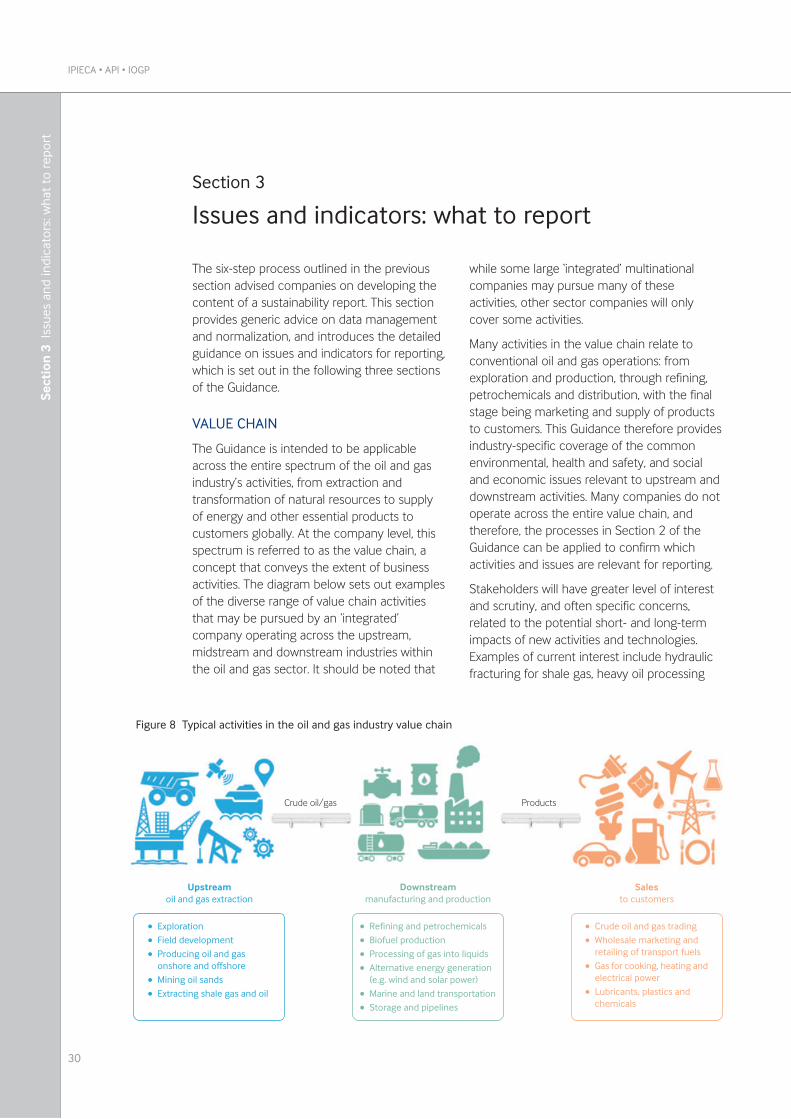

Value chain 30

Life-cycle considerations 31

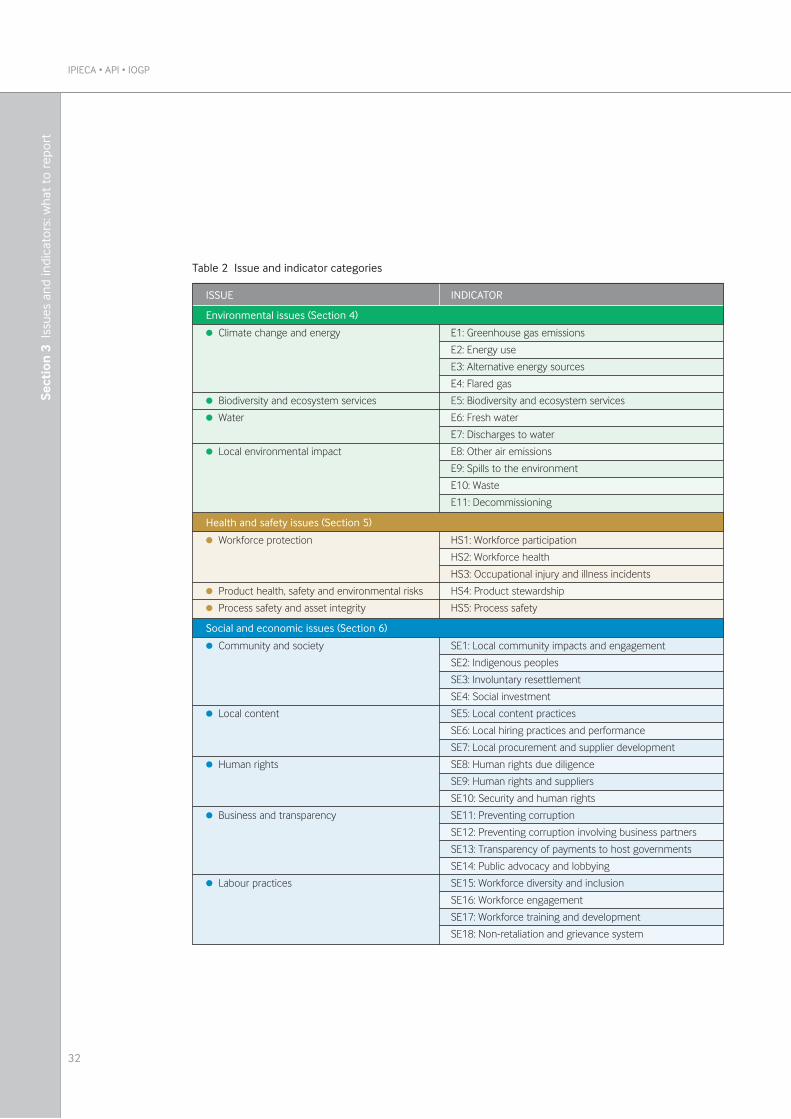

Overview of issues and indicators 31

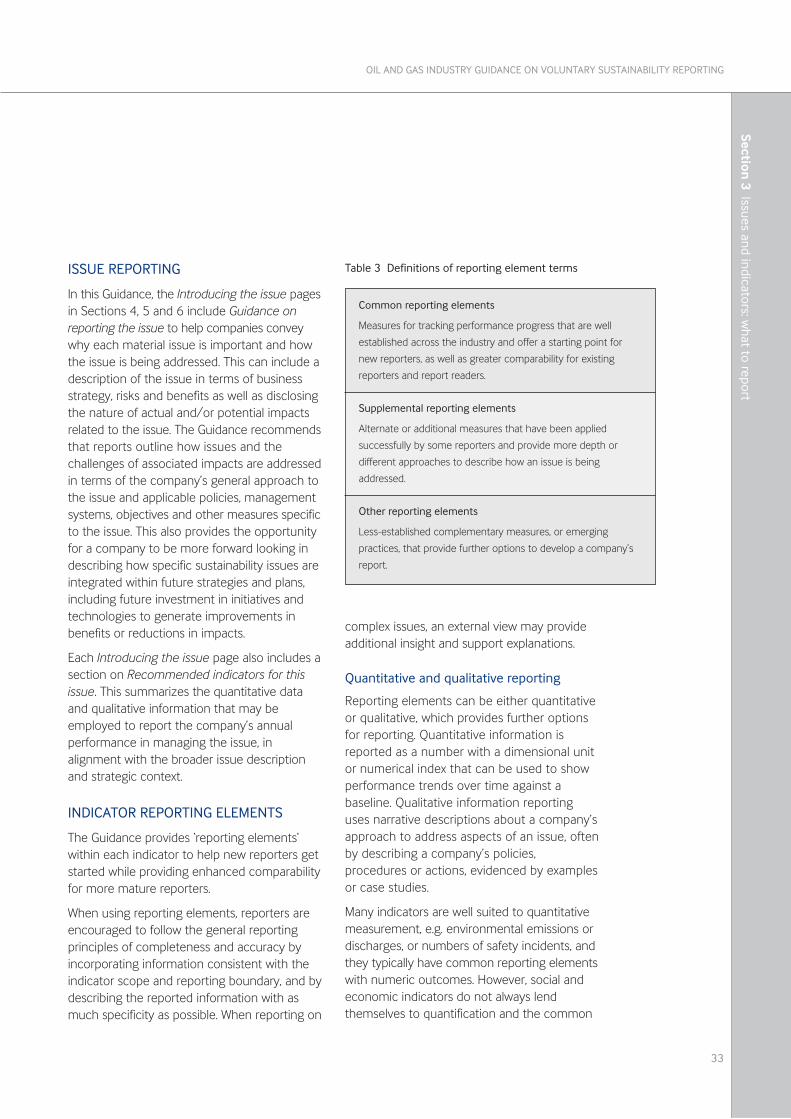

Issue reporting 33

Indicator reporting elements 33

Data management 35

Data normalization 36

Standard issue and indicator format 38

Contents

1

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 6 95Social and economic issues and indicators

Social and economic issues and indicators: an overview 96

l Community and society 97

SE1: Local community impacts and engagement 98

SE2: Indigenous peoples 100

SE3: Involuntary resettlement 102

SE4: Social investment 104

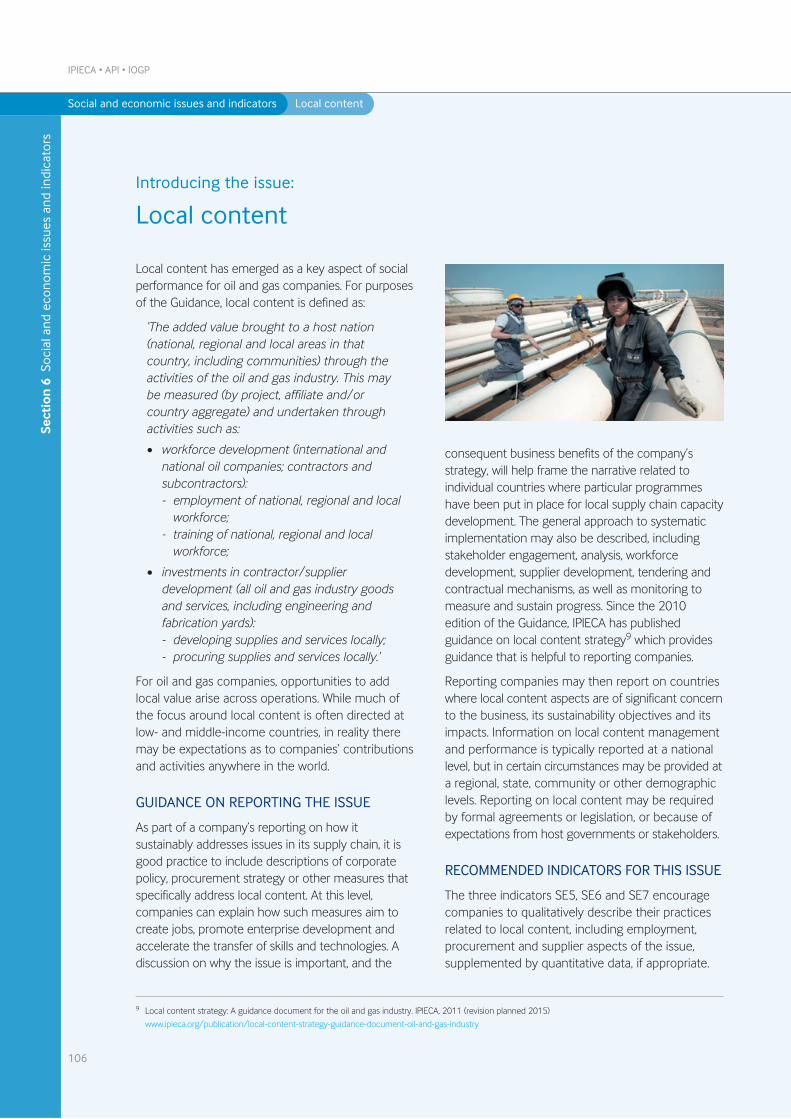

l Local content 106

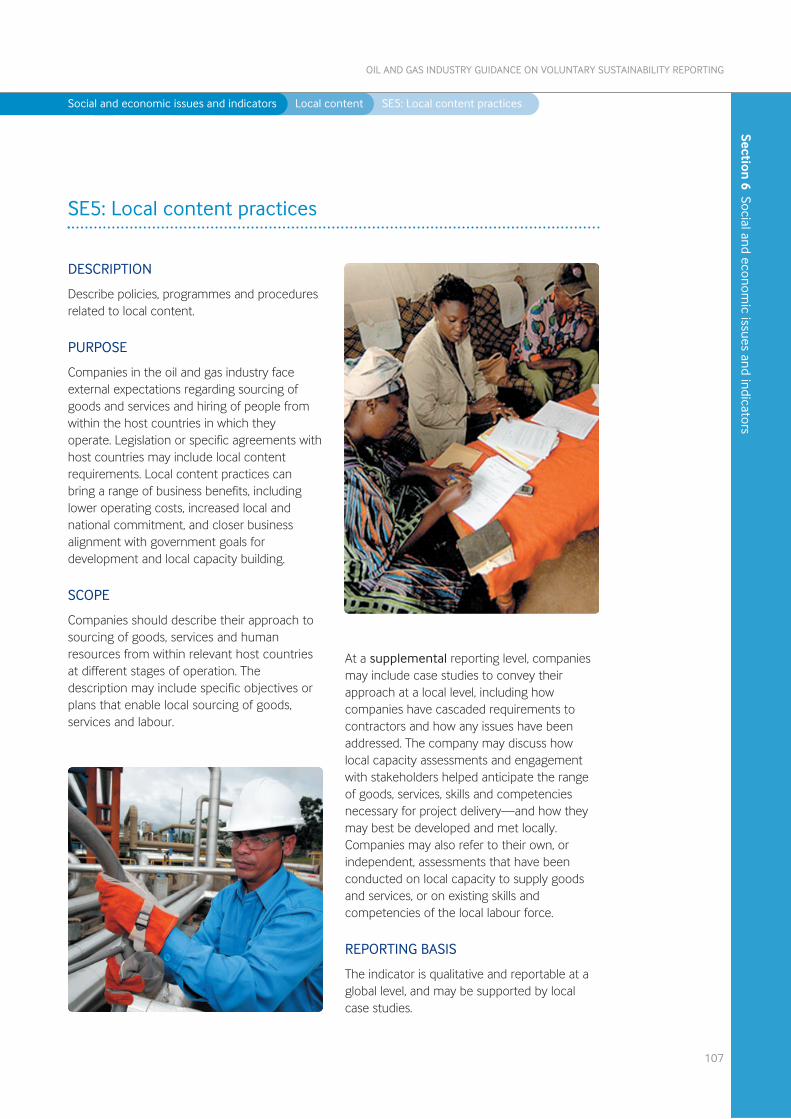

SE5: Local content practices 107

SE6: Local hiring practices 109

SE7: Local procurement and 110supplier development

l Human rights 112

SE8: Human rights due diligence 114

SE9: Human rights and suppliers 116

SE10: Security and human rights 117

l Business ethics and transparency 118

SE11: Preventing corruption 120

SE12: Preventing corruption involving 121business partners

SE13: Transparency of payments to 122host governments

SE14: Public advocacy and lobbying 124

l Labour practices 125

SE15: Workforce diversity and inclusion 127

SE16: Workforce engagement 128

SE17: Workforce training and development 129

SE18: Non-retaliation and workforce 130grievance system

Appendix A: Detailed guidance on 131developing a reporting boundary

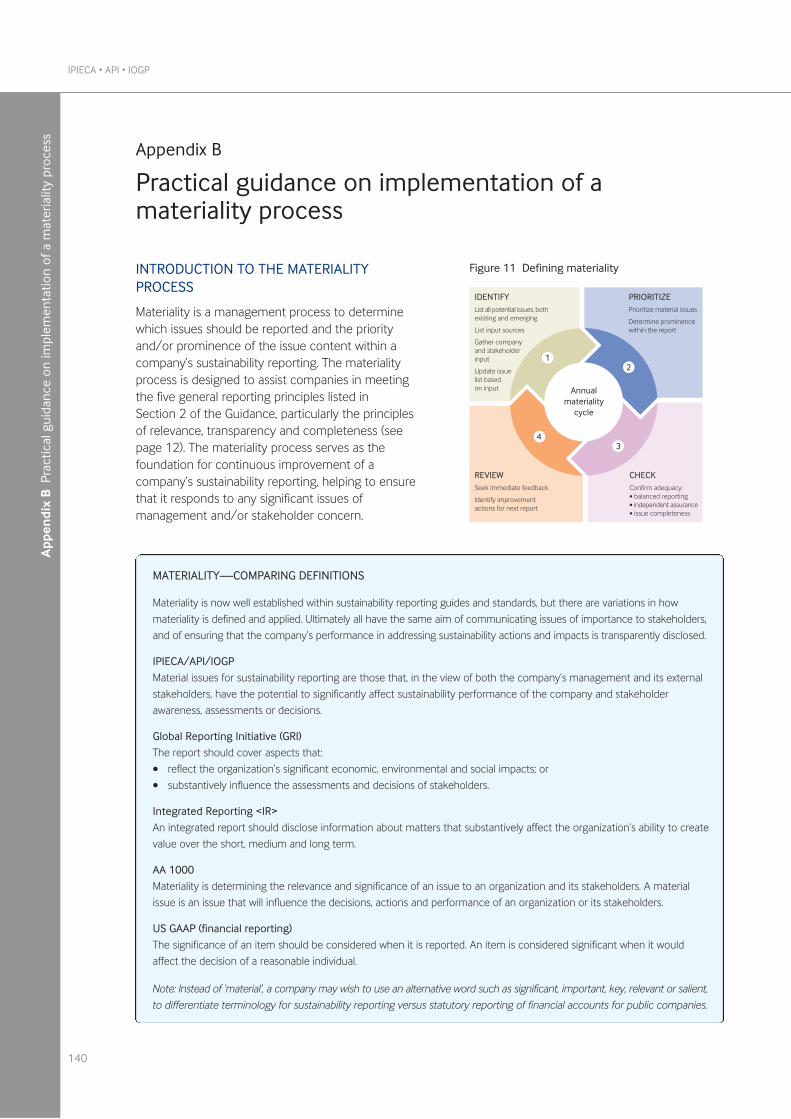

Appendix B: Practical guidance on 139implementation of a materiality process

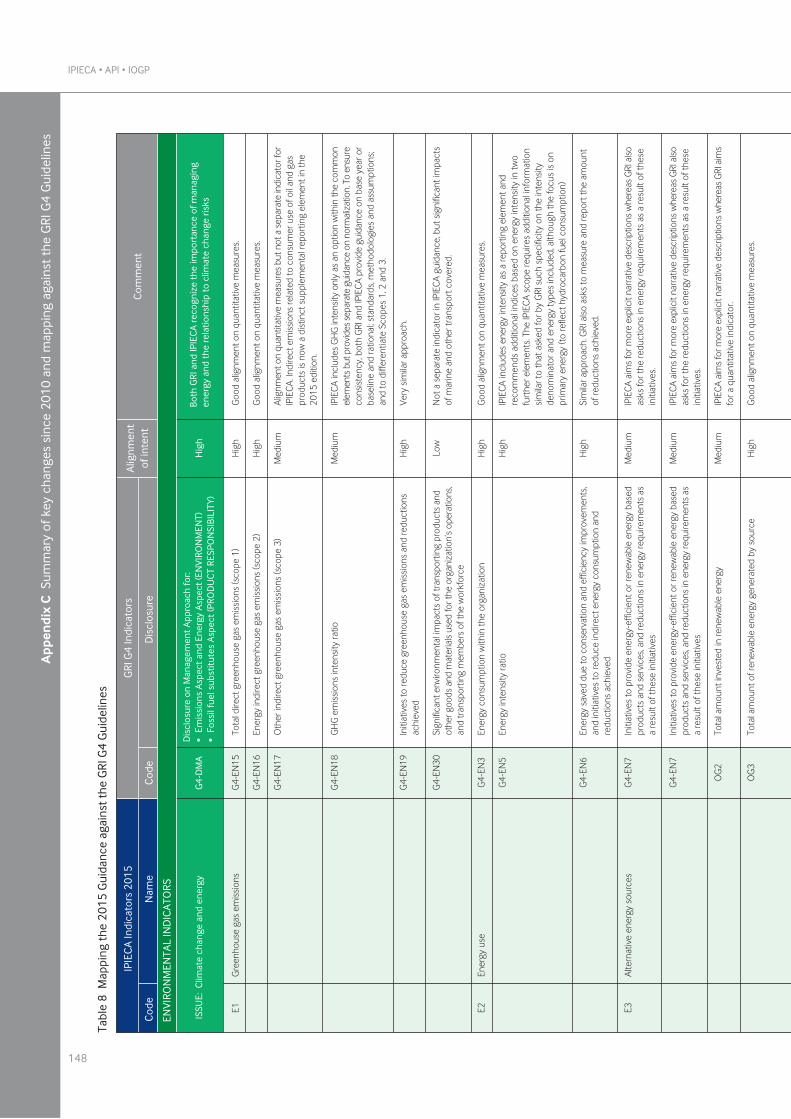

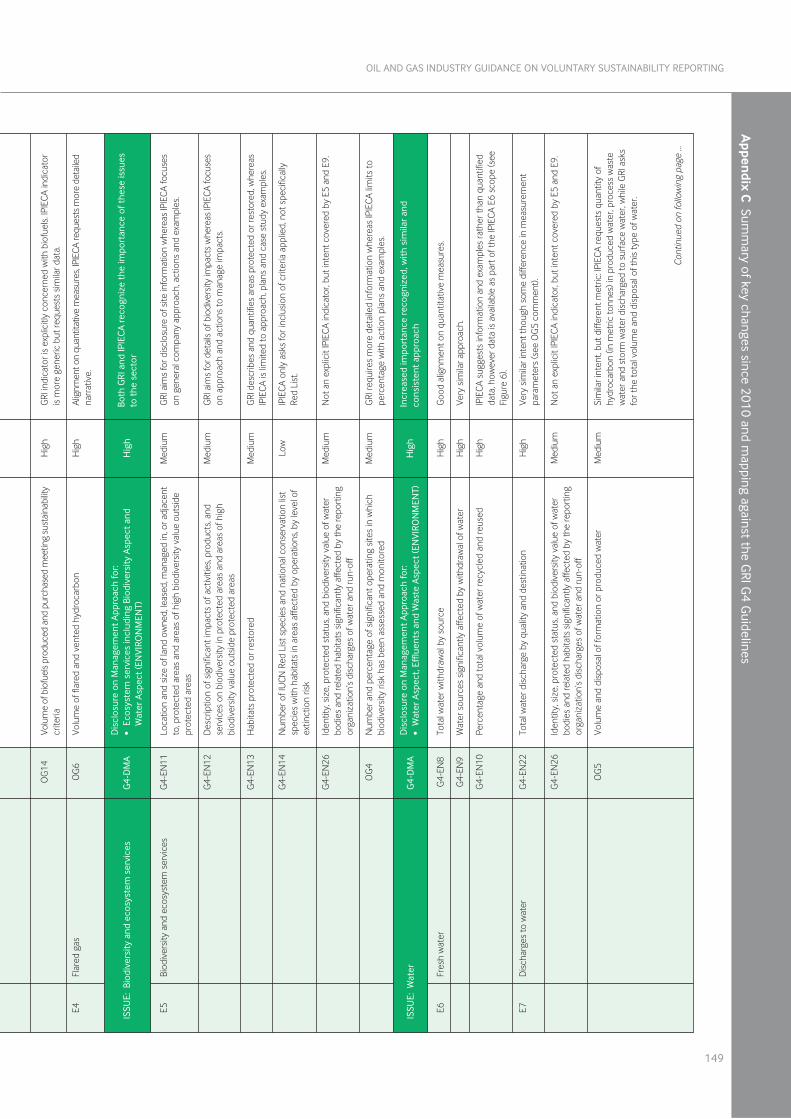

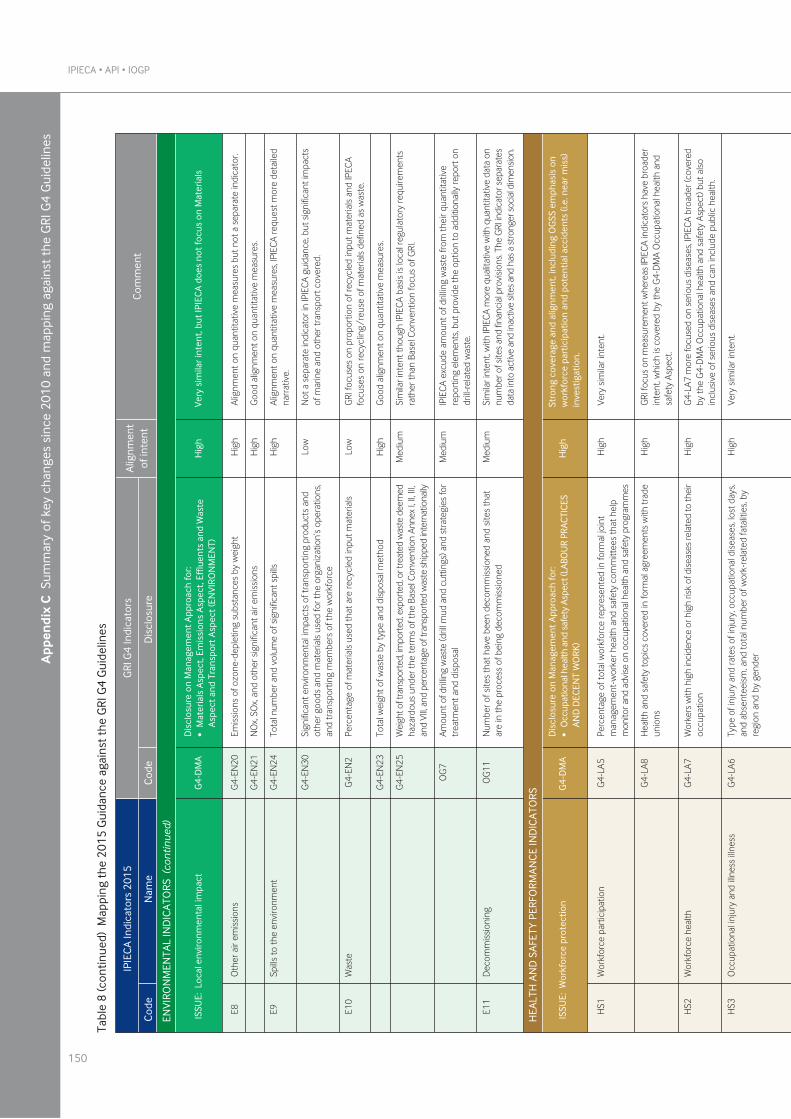

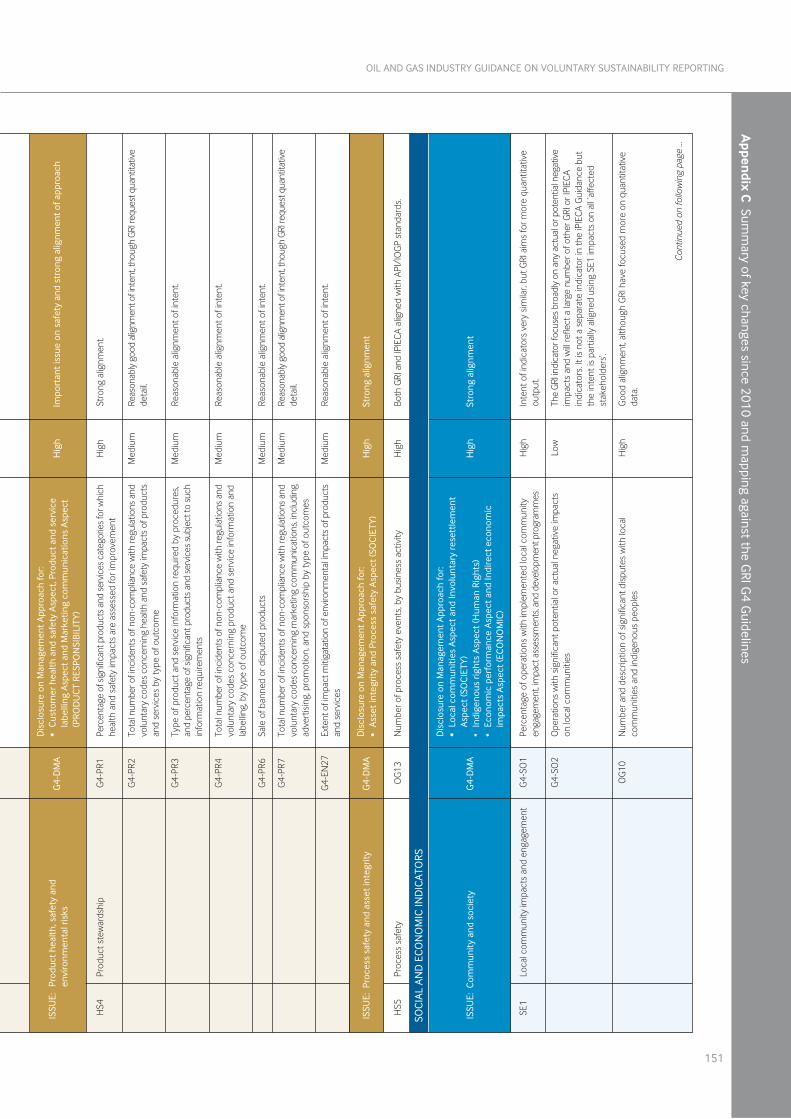

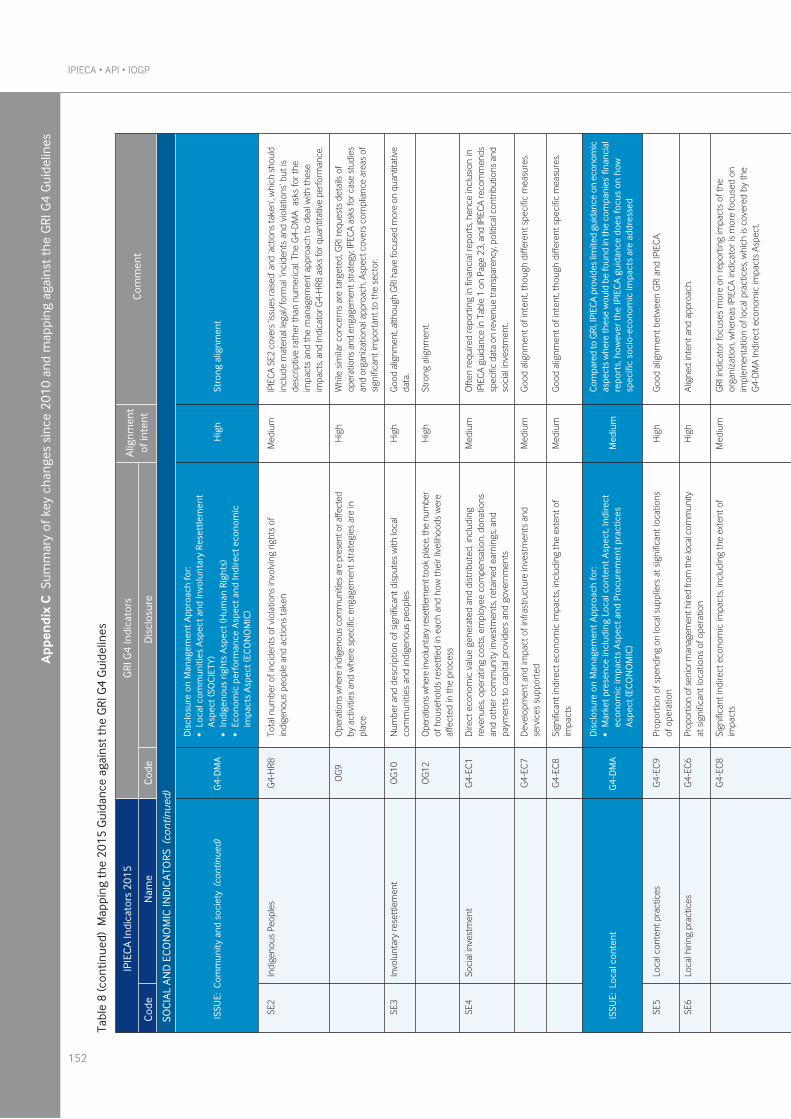

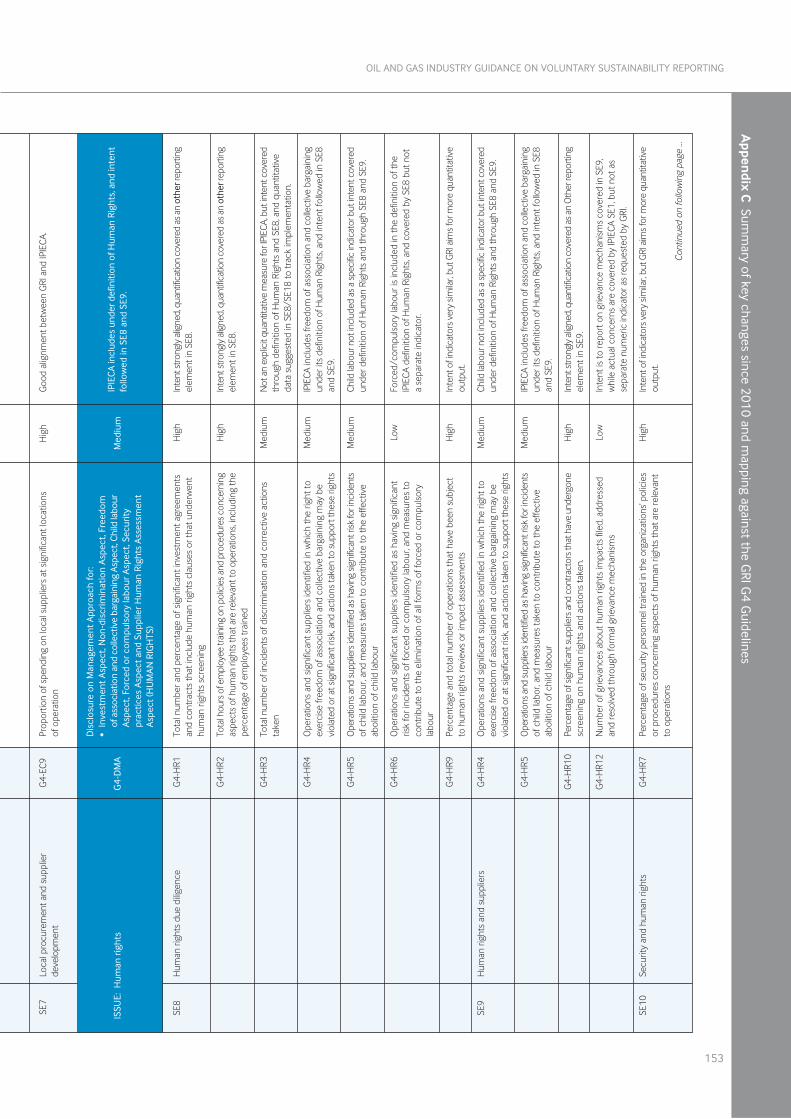

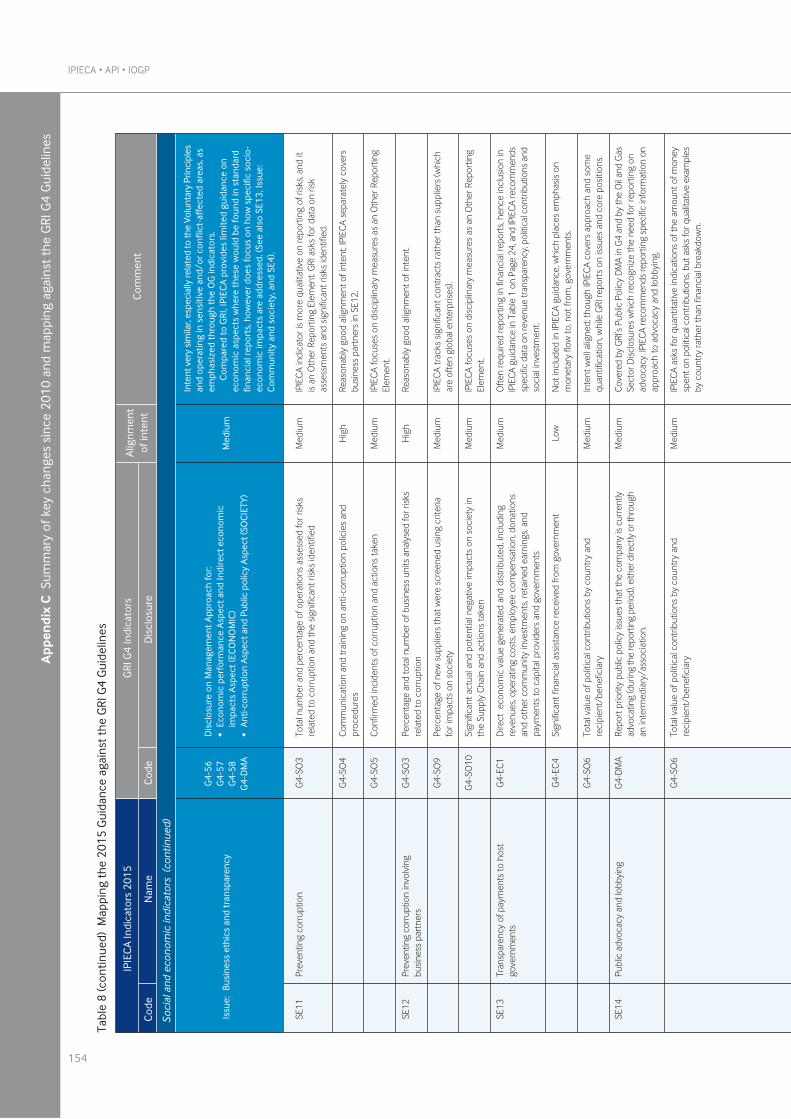

Appendix C: Summary of key changes 145since 2010 and mapping against theGRI G4 Guidelines

Appendix D: Measurement units and 157conversion factors (from IOGP)

Appendix E: References and 161source materials

Appendix F: Glossary 167

We are pleased to introduce the third edition of the Oiland Gas Industry Guidance on Voluntary SustainabilityReporting (hereinafter the ‘Guidance’).

IPIECA, the global oil and gas industry association forenvironmental and social issues, the AmericanPetroleum Institute (API) and the InternationalAssociation of Oil & Gas Producers (IOGP) have beenproviding sustainability reporting guidance for theindustry since 2005. This third edition marks over tenyears of sharing, assessing, debating and consensusbuilding for our three associations. The update wasundertaken recognizing that industry sustainabilityreporting is continuously progressing, with issue areasthat mature and develop at different paces. To maintaincontinuity, the revisions are not intended to effectextensive changes to the 2010 Guidance, but to addressfeedback received from subject matter experts, bothwithin and outside the industry, as well asimprovements in reporting practices.

IPIECA, API and IOGP believe that it is essential tocontinue providing this robust industry-developedframework to help companies shape the structure andcontent of their sustainability reporting, particularly fornew reporters. Recent years have been characterizedby an evolution in existing frameworks on voluntarysustainability reporting, the emergence of newvoluntary initiatives and mandatory sustainabilityreporting requirements in some countries. Thesevarying expectations and different definitions of how

and what companies should report have led tochallenges for many oil and gas companies.

The membership of our three associations includescompanies that are leaders in sustainability reporting, aswell as new reporters. This revision brings together theircollective wealth of technical expertise and reflects thereporting challenges that some companies continue toface. The industry’s commitment to this project isevidenced through the substantial participation in theupdate, as noted in the Acknowledgements on page 6.

EXPANDING ENGAGEMENT

The third edition reflects feedback and improvements inreporting practices from many sources within andoutside the industry. As in 2010, we engaged anexternal Stakeholder Panel of leading experts to adviseus on both the process and the content of theGuidance. We retained the same individuals andorganizations from the 2010 Panel where possible, andadded an additional member representing a humanrights perspective. We held a dialogue session in April2014 to provide the Panel with information on uptakeand feedback for the second edition, discuss drivers forthe update, share our future plans and ambitions, andreview improvement opportunities under consideration.We looked closely at materiality, how companies areidentifying and addressing the impacts of their businessand communicating the main sustainability issues theyface, and how this process could be improved.

IPIECA • API • IOGP

Improving our transparencyA foreword from the oil and gas industry associations

2

Brian Sullivan, IPIECAExecutive Director

Jack N. Gerard,API President and CEO

Michael Engell-Jensen,IOGP Executive Director

The Stakeholder Panel engagement for the 2015update resulted in comprehensive outcomes including:

l new guidance on strategic reporting for each of the12 sustainability issues; this is intended to helpcompanies report information on their managementapproach and strategies to address the sustainabilityissue and its related impacts—this extends reportingbeyond key performance indicators and numericalresponses, for example, in relation to climate changemitigation, adaptation and strategy;

l expanded guidance on materiality that aims to helpcompanies identify and prioritize impacts and issues,including a new appendix to provide practical guidanceon implementation of a materiality process; and

l new guidance on reporting across the value chainand life-cycle considerations to help ensure that allrelevant business activities are addressed whenreporting on material sustainability issues.

ENCOURAGING CONTINUOUS IMPROVEMENTTHROUGH THIS UPDATE

The oil and gas sector continues to provide essentialenergy for society’s development. Our membercompanies also recognize that managing sustainabilityimpacts associated with producing energy is an importantresponsibility, including addressing the challengesassociated with climate change risks, human rights andoperating in remote and sensitive areas of the world.

The Guidance continues to cover a range ofsustainability issues relevant to the oil and gas industry,based on industry consensus. It allows companies toselect from related indicators that offer a choice on thedepth and detail to be communicated. By providing

flexibility and consistency, the Guidance aims to serveboth new and experienced reporters while avoiding thepitfalls of formulaic reporting.

The Guidance remains voluntary and does not setminimum requirements or predetermine stakeholderrequests. Instead, we encourage a consistent ‘how-to’approach, with companies determining what to reportbased on a materiality process and stakeholderexpectations.

Key changes within the 2015 update include:

l a new issue area on water, with comprehensiveupdates to two water indicators;

l a new indicator covering planning and execution ofdecommissioning activities;

l alignment of the Social and economic section withthe United Nations Guiding Principles on Businessand Human Rights;

l upgrade of a range of reporting elements across thethree categories within each indicator, ‘common’,‘supplemental’ and ‘other’ reflecting improvedmaturity and consistency of reporting by companies;and

l additional or improved reporting elements for nine ofthe existing indicators.

For a more detailed list of changes see Appendix C.

LOOKING AHEAD

Our industry will continue to address multiplesustainability challenges as it seeks to provide theenergy essential for societal development. Throughoutthis journey, communication and engagement withstakeholders will be essential. It is our hope that theGuidance will continue to support the momentum wesee within our industry to publish sustainabilityinformation. Our aim is that the Guidance, as theprimary industry reporting framework, supportscompanies across the global oil and gas industry toimprove the quality and consistency of theirsustainability reporting.

IPIECA, API and IOGP will continue to encourage ourmembers and others in the industry to report on theirperformance in addressing sustainability issues. Ourassociations plan to continue supporting our membercompanies through sharing good practices, anddeveloping and maintaining our guidance onsustainability reporting as evidenced through this update.

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

3

ROGER HAMMOND (1956-2012)

We would like to recognize thecontribution of Roger Hammond, thefounder of Living Earth Foundation, intothe development of the second editionof the Guidance. In his role as a memberof the Stakeholder Panel, Rogerprovided key insights into sustainabilityissues which led to significantimprovements. We continue to valuethe inputs he provided, as well as the work he undertookwith the industry more broadly through Living Earth.

Roger Hammond,

Living Earth

IPIECA • API • IOGP

Joint statement of the Independent Stakeholder Panel

4

We are pleased to offer our comments on thisthird edition of IPIECA’s sustainability reportingguidance. Our role as a panel has been to offerour guidance to IPIECA as experts andstakeholders in relation to the industry’ssustainability impacts. Our purpose in doing thishas been two-fold: first, to help ensure that thenew edition of this sustainability reportingguidance adequately captures the sustainabilitylandscape, from impacts to risks andopportunities, relevant to the oil and gas sectorand its stakeholders; and second, to help ensurethat the guidance is designed to producetransparent, honest and informative reports thatadvance sustainability strategy and practice.

At a technical level, the updates to the guidancehave been thoughtful and highly competent,responsive both to stakeholders’recommendations and to wider trends insustainability practice and reporting. We areespecially pleased to see significant improvements

in particular to the sections on water, biodiversityand ecosystem services and human rights, all ofwhich help bring IPIECA’s guidance more closely inline with international best practice in reporting.

We also welcome the improvements to theguidance on how to describe sustainability issuesand impacts in reports beyond measurementprotocols and indicators. The new guidance ismore consistent and specific in terms of howreporters are asked to discuss the nature andsignificance of issues, how they relate to thecompany’s strategy, vision and future plans, andtheir general approach to managing the issues.We hope this improvement will result in reportsthat are clearer and more strategic, and thatenable greater accountability over time.

The guidance has also improved with respect tothe process of reporting. This includes identifyingand prioritizing reported content using theprinciple of materiality. While the materialityguidance is technically robust, it will not in itself

To improve external engagement as part of the Guidance revision process for both the second and thirdeditions, the IPIECA Reporting Working Group (RWG) convened a Panel made up of independentstakeholders with expertise in sustainability practices relating to the oil and gas industry. As knowledgeablemembers of the reporting community, the Panel represented views of typical report reader groups: businessand industry; environmental and community-oriented NGOs; investors; UN bodies; and multilateralinstitutions. At the onset of this engagement, the Panel was asked to assess the quality, credibility andeffectiveness of the revision process and to provide ideas for improvement. Through ongoingcommunications during the revision process, including a face-to-face dialogue in 2014, the Panel providedcandid, significant and challenging input on the RWG’s proposed updates to the second edition. For theRWG’s initial update proposals and the final draft, the Panel provided high-level feedback and detailedsuggestions, which were all reviewed and most were incorporated as improvements within this third edition.The following is the joint statement from the Independent Stakeholder Panel.

Tom Delfgaauw,

Independent

Matthias Beer, F&C

Asset Management

Margaret Jungk,

UN Working Group

on Business and

Human Rights

Judy Kuszewski,

Independent,

Panel Chair

Janet Ranganathan,

World Resources

Institute

Trevor Rees,

Living Earth

Robin Sandenburgh,

IFC

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

5

l Greater emphasis on targets: targets areessential for driving performance and creatinga basis for accountability and trust amongstakeholders. The 2015 Guidance does little toadvance the setting and reporting of targetsand progress against them compared with the2010 version.

l The absence of minimum reporting standards:the Guidance does not establish any basicrequirements for what would constitute anacceptable sustainability report for an IPIECAmember company. Today, as in 2010,members are free to choose whether or notthey will report at all. We encourage IPIECA todo more to encourage and measuremembers’ uptake of the Guidance, andprovide assurance that voluntary reporting ismaking a material difference. This includesensuring that members:

• produce public sustainability reports;

• use the IPIECA reporting Guidance as thebasis for their reports; and

• report all ‘common’ reporting elements at aminimum.

The time has come to move beyondsustainability reporting as a voluntary exercisedriven by idiosyncratic corporate circumstances,towards a sector that recognizes its responsibilityto account for its activities and performance, andto defend its strategies and instill confidence andtrust among stakeholders through robustreporting—to a minimum agreed level throughthis Guidance.

Ultimately, technical reporting challenges cannottake place in a vacuum without the clear supportof company leadership. We therefore encourageIPIECA to strengthen its role in driving changewithin the oil and gas sector by harnessing thevoice of CEOs and board level leaders to chart avision for the industry’s key sustainabilitychallenges. Now, more than ever, this leadershipvoice is required to enable the industry toreconcile the twin challenges of energy securityand climate change, while managing andmitigating a broad range of increasingly complexsustainability risks.

guarantee that companies will implement it asintended. We encourage companies to invest inhigh quality stakeholder engagement across themany aspects of their operations to ensure thatthe concerns of those most affected by thecompany’s operations are involved in reportingdecisions.

There are areas in which we would havepreferred the guidance to have gone further. Webelieve the future sustainability of the oil and gassector will be strongly influenced by threeinterconnected factors: 1) society’s need to limitglobal average atmospheric temperature rise totwo degrees above preindustrial levels; 2) rapidlyfalling prices for clean energy alternatives; and3) the transition to electric vehicles. As a result,‘stranded assets’ may pose a significant risk toboth the economic value and performance ofthe industry in the near future. While theguidance makes reference to this challenge, wefeel it could have advanced the state of reportingby strengthening recommendations on the riskmanagement approaches that companies areimplementing to anticipate this challenge.

Oil and gas companies face other risks to theirviability. Operating in regions that areinsufficiently democratically mature leads toconflict, social strife, bribery and corruption. Weexpect companies to acknowledge these risksand demonstrate how their operations fit intothat wider human perspective. We hope thatfuture editions of the guidance will inspirereporting in that direction.

We would prefer the guidance to give clearerinstruction to reporters on how their reportsmight be improved in the future, and what wouldconstitute a path of progress. The framework’semphasis on ‘common’, ‘supplemental’ and‘other’ reporting elements might drive a degreeof conformity, but may do so on the basis of thelowest common denominator rather thanencouraging leadership in reporting.

We regret that there are several significant areasin which the panel’s comments and suggestionsin 2010 have not been addressed. These remainimportant and should be addressed withurgency:

IPIECA • API • IOGP

6

ACKNOWLEDGEMENTS

The information contained in this document was developed jointly under the auspices of IPIECA,API and IOGP. It represents the work of a Reporting Working Group (RWG), composed of 80representatives from 28 companies and 4 trade associations.

The document benefitted significantly from the input and review of a Stakeholder Panel, whichmet formally with the RWG in April 2014 and also contributed throughout the process. IPIECA, APIand IOGP would also like to thank the organizations and individuals that responded during thepublic consultation period in December 2014. The comments received were of substantial valueto the revision. Particular thanks are given to Tamara Bergkamp, from the Global ReportingInitiative (GRI), for her contribution to the mapping document between the Guidance and GRI G4(pages 148–155).

In addition to input from many technical groups within IPIECA, API and IOGP, experts from thefollowing companies contributed substantial personal effort to the Guidance update:

For the 2015 edition, the IPIECA Secretariat project manager was Helen Murphy. Consultantsupport was provided by Bill Boyle (IPIECA senior associate) and Nigel Jones (design).

Anadarko

BG Group

BP

Chevron

ConocoPhillips

Eni

ExxonMobil

Hess

Husky Energy

Maersk Oil

Noble Energy

Petrobras

Repsol

Schlumberger

Shell

Statoil

Total

Photographs reproduced courtesy of the following: cover (upper left, lower left and lower right) and pages 11, 15, 29, 39, 58, 65, 66 (bottom), 70,77, 90, 95, 100, 102 and 104 (top): Shutterstock.com; pages 13, 16, 18, 23, 27, 49, 53, 54, 57, 63, 66 (top), 79, 84, 87, 89, 103, 114, 119, 125 and127: iStockphoto.com; cover (centre left) and page 106: BP; page 107 (bottom): Chevron; page 34: ©Larry Lee Photography/Corbis; cover (bottomcentre) and pages 25, 85, 97, 98, 104, 107 (top) and 112: ExxonMobil Corporation; pages 36, 80 and 110: Marathon Oil.

7

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 1

Setting the context:why report?

IPIECA • API • IOGP

8

Sect

ion

1 S

ettin

g th

e co

ntex

t: w

hy r

epor

t?

The oil and gas sector is a fundamental part oftoday’s world, providing essential energy and rawmaterials for global development. A dynamic andinnovative business, the industry constantly seeksto adapt to new situations and challenges. It investsnot only in the search for new oil and gas, but alsoin facilities, infrastructure, technology, localcommunities, health and safety, and theenvironment. The sector continually examinesopportunities to meet growing energy demandaround the world, while seeking to mitigate adverseimpacts of its activities as well as to address thepotential risks associated with climate change.

Not surprisingly, many people and organizationsworldwide want to understand the oil and gassector’s business and participate in dialogue withcompanies on the effects of their activities—theimpacts, benefits, risks and trade-offs. In addition toannual reports on financial performance and othercommunication initiatives, sustainability reporting—also known as corporate citizenship, corporateresponsibility or environmental, social andgovernance (ESG) reporting—is an important way forcompanies in the sector to engage with stakeholdersand help foster informed dialogue andunderstanding.

Oil and gas companies have been among thepioneers of sustainability reporting and haveprovided leading examples of good reportingpractices. This Guidance has been developed toshare good practice across the industry and toencourage companies, both current and newreporters, to keep their stakeholders informedabout their performance. The Guidance representsindustry consensus on the most prevalentsustainability issues and indicators, and aims tosupport continuous improvement of sustainabilityreporting and performance across the sector.

BENEFITS OF REPORTING

Reporting can bring companies recognizablebusiness benefits. Through communication on itsmost important sustainability issues, a company’sreport becomes a reliable source of information for

its stakeholders. By transparently describing itsbiggest challenges, reporting underpins stakeholderengagement and represents the company’s valuesin action.

For oil and gas companies, reporting provides arobust platform for describing how strategic globalissues—such as climate change and energy—arebeing addressed through long-term plans andcurrent initiatives. The report can also explain howthe company is managing the socio-economicimpacts and environmental, health and safety risksof operating in different locations. Once published,this information enables further communicationand engagement with stakeholders. The long-termbenefits of reporting include:

l enhanced business value as investorconfidence grows in response to evidence thatthe company is managing important risks andpositioning itself to take advantage of emergingopportunities;

l improved operations as employees develop adeeper understanding of a company’ssustainability values and performance indicatorsprovide insight to support continuousimprovement;

l strengthened relationships as local communityleaders, civil society representatives, governmentofficials and regulators, and other keystakeholders learn how the company responsiblymanages sustainability issues; and

l enhanced trust and credibility as customers,suppliers and the wider society understand thecompany’s brand, operations and products.

For many companies, sustainability reporting isonly one of the channels used to engagestakeholders. For example, a company may alsoproduce an annual report for its shareholders, ESGfilings for investment funds and research houses,an integrated report for providers of capital,statutory stock market filings in differentcountries, and regular publications for employees,customers or communities. Generating asustainability report using a consistent, robust

Section 1

Setting the context: why report?

9

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 1 Setting the context: w

hy report?

process also provides reliable, verifiableinformation and data that can underpin otherreports and communications.

ABOUT THE GUIDANCE

This third edition of the Guidance replaces thesecond edition published in December 2010. Thisrevision is based on industry experience, feedbackon the 2010 document, and significant insights andsuggestions from an independent panel ofstakeholders with expertise in the sector andsustainability reporting (see pages 4–5).

The Guidance aims to assist oil and gas companiesin developing and enhancing the quality andconsistency of their sustainability reporting. It isdesigned for use by any oil and gas companyoperating nationally, regionally or internationally.The Guidance deliberately provides choices, notonly for experienced reporters, but also to enablenew reporters or smaller companies to focus ontheir most important issues at a level appropriateto their business and stakeholders. It recognizesthat while some reporters are multinational publiccorporations, others may be state- or privately-owned companies, where local reporting tailoredto individual stakeholders may be more importantthan aggregated reporting at the global level.

The Guidance may also serve as a reference to helpreaders of company reports, including onlineinformation channels, to understand the basis forreporting in the oil and gas sector.

USING THE GUIDANCE

The Guidance is a reference tool aimed at helpingcompany sustainability managers, communicationsprofessionals and environmental, health and safetyor socio-economic specialists to develop corporate-level reporting for internal and external stakeholderaudiences. It can be used to report performance todifferent audiences in different ways—for activitiesin a single country, for large projects or for a singleoperation. The Guidance is designed to offerflexibility in support of new reporters, who may

initially focus on a limited number of keysustainability issues, geographical locations orspecific audiences, and then, over time, graduallyincrease coverage of their reporting.

This Guidance is voluntary. It does not setminimum requirements or predeterminestakeholder needs. Instead, it encouragescompanies to make informed choices on what isimportant for reporting by engaging with theirstakeholders and understanding their needs. Then,to support these choices, reporters can includerelevant data and information that benefit from theconsistency of industry consensus on the issues,indicators and reporting elements detailed in theGuidance. With effort focused primarily on thoseissues of significance to the individual companyand its stakeholders, reporting time and cost canbe better managed.

The Guidance provides two types of assistance byhelping companies decide:

l ‘how’ to report, by describing a process forreporting; and

l ‘what’ to report, by providing options fordeveloping the content of the report.

Process

In Section 2, companies are encouraged to employa stepwise process for reporting by:

l setting the context for the report by outlining thecompany’s high-level vision and strategy,together with governance and managementsystems;

l determining the issues to include by using amateriality process that identifies the completeset of issues of relevance to both the companyand its stakeholders; and

l selecting indicator data to be collected within thecompany’s reporting boundary and incorporatedinto the narrative.

IPIECA • API • IOGP

10

Sect

ion

1 S

ettin

g th

e co

ntex

t: w

hy r

epor

t?

The objective of each step is to build transparentand concise reporting as part of stakeholderengagement. The process helps the company toverify which issues and indicators are not materialand thus avoid unnecessary and time-consumingreporting which can obscure the relevant issues.

Content

Sections 3 to 6 provide direction on the content ofa typical oil and gas industry report. The Guidanceprovides a set of performance indicatorsappropriate to sustainability issues in the industry.Each indicator provides a choice of reportingelements depending on the depth or accuracyrequired (i.e. depending on the materiality of theissue for the company). The reporting elementsinclude measures that are ‘common’, being themost established and consistent across the industrytoday. Section 3 provides guidance (including onreporting boundaries and data normalization) that isbroadly applicable to the performance indicatorsprovided in Sections 4, 5 and 6, covering(respectively) environmental, health and safety, andsocial and economic issues.

The breadth and depth of the reporting content mayvary significantly between companies depending onthe extent of business activities and related impactsacross the value chain, as well as the materiality ofsustainability issues to the company and itsstakeholders. Listed below are several basiccomponents that are commonly included within anoil and gas sustainability report or website:

l CEO statement: this introductory statementfrom the company’s most senior executiveemphasizes the importance of reporting to thecompany, provides stakeholders with a strategicoverview and context for the sustainability issues,and highlights performance challenges andprogress for the reporting year.

l Addressing climate change risks: this issuecontinues to be regarded as the sector’s primarylong-term environmental issue, and companiestypically provide information on their position,strategy and actions related to the issue, as wellas disclosure of greenhouse gas (GHG) emissionsand other performance indicators.

l Managing risks of accidents: the oil and gasindustry has inherent hazards throughout thevalue chain that must be responsibly managedto prevent events that could potentially result inharm to people, damage to the environment,and socio-economic impacts. Companiestypically describe their systems to managesafety and related risks, and openly disclosetheir annual performance record including anysignificant incidents.

l Local impacts and benefits: oil and gascompanies often operate in places where theiractivities can have significant benefits, atcommunity or national level, but may also havelocal impacts which affect people or theenvironment. In addition to describing corporatepolicies and processes, reported content candraw attention to operations in developingcountries or sensitive environments, whereissues may include respect for human rights,transparency of payments to host governments,access to fresh water, or protection ofbiodiversity.

l Reporting process: companies generally explaintheir reporting process, including howstakeholders are engaged, how issues areprioritized for reporting, how information isprepared and validated, and whether any nationalor international reporting guidelines are used.

While the Guidance addresses many othercomponents of reporting content, the stakeholdersengaged during the development of this editionhave highlighted these five components as basicexpectations.

Referencing the Guidance

Companies who use the process and/or thecontent sections are encouraged to reference theGuidance, acknowledging IPIECA, API and IOGP,since doing so demonstrates a company’s efforts toreport consistently by applying oil and gas industrygood practice. Within their reports, companies maywish to include an index of the Guidance indicatorsused, which would signal that their reporting meetsthe intent of the indicator description and follows atleast one reporting element.

11

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 2

The reporting process:how to report

IPIECA • API • IOGP

12

Section 2

The reporting process: how to report

Sect

ion

2 T

he r

epor

ting

proc

ess:

how

to

repo

rt

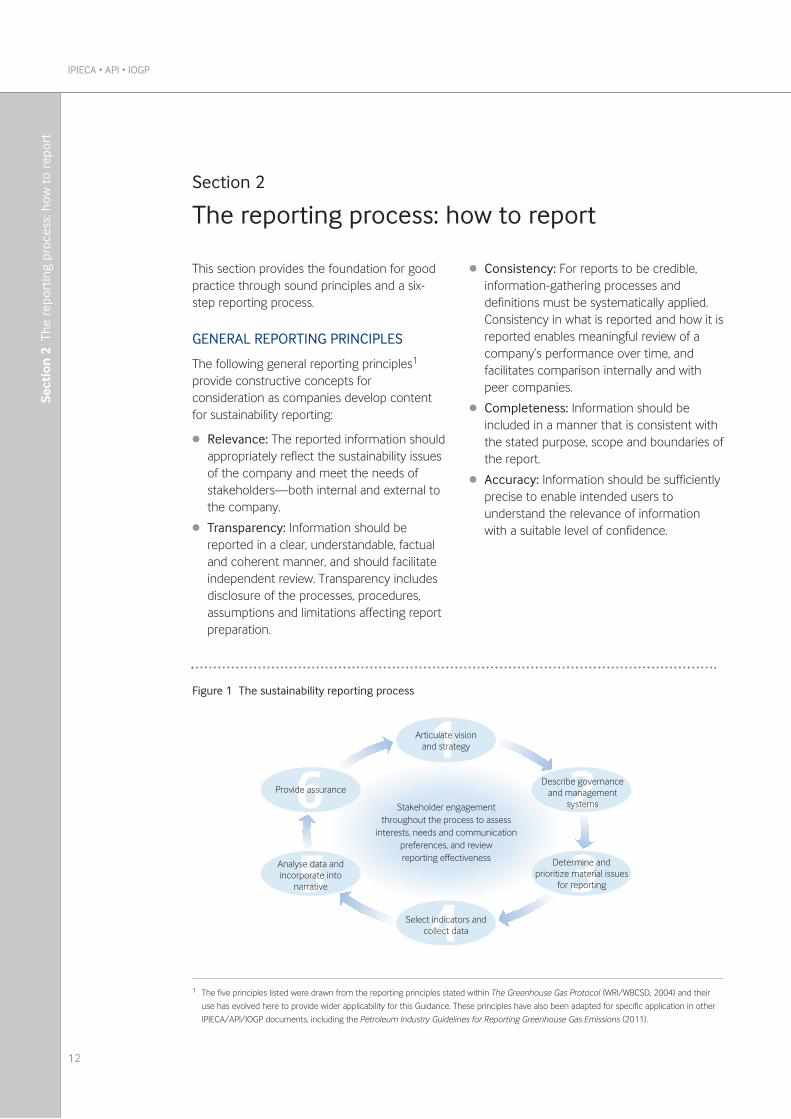

This section provides the foundation for goodpractice through sound principles and a six-step reporting process.

GENERAL REPORTING PRINCIPLES

The following general reporting principles1

provide constructive concepts forconsideration as companies develop contentfor sustainability reporting:

l Relevance: The reported information shouldappropriately reflect the sustainability issuesof the company and meet the needs ofstakeholders—both internal and external tothe company.

l Transparency: Information should bereported in a clear, understandable, factualand coherent manner, and should facilitateindependent review. Transparency includesdisclosure of the processes, procedures,assumptions and limitations affecting reportpreparation.

l Consistency: For reports to be credible,information-gathering processes anddefinitions must be systematically applied.Consistency in what is reported and how it isreported enables meaningful review of acompany’s performance over time, andfacilitates comparison internally and withpeer companies.

l Completeness: Information should beincluded in a manner that is consistent withthe stated purpose, scope and boundaries ofthe report.

l Accuracy: Information should be sufficientlyprecise to enable intended users tounderstand the relevance of informationwith a suitable level of confidence.

1 The five principles listed were drawn from the reporting principles stated within The Greenhouse Gas Protocol (WRI/WBCSD, 2004) and their

use has evolved here to provide wider applicability for this Guidance. These principles have also been adapted for specific application in other

IPIECA/API/IOGP documents, including the Petroleum Industry Guidelines for Reporting Greenhouse Gas Emissions (2011).

12

34

5

6����������� ������ �����

� ���������������������

� ��

�������������������������� �

������������

������������� ������������

���� ��������������������

������

������� ����

��������������������������������� ���� ���� � ���� ����������������

������ �������������������������

Figure 1 The sustainability reporting process

PROCESS OVERVIEW

The publication of a sustainability report, oronline content, is generally the result ofinternal corporate processes combined withexternal dialogue. Although each company willhave its own approach, Figure 1 illustrateshow stakeholder engagement underpins sixtypical process steps, which are discussed indetail in the rest of this section.

ENGAGING STAKEHOLDERS

Stakeholder engagement has an importantrole throughout the reporting process.Stakeholder viewpoints and dialogue can helpto ensure that the report is relevant,accessible and credible to external audiences.Feedback on the completed report canprovide valuable insight to improve futurereports and to initiate dialogue on issues.Thus, as an integral part of the reporting

process, companies could considerproactively soliciting stakeholder views atdifferent stages:

l Starting out: stakeholder opinion on thecompany’s vision and strategy, governance,management plans and approach, relevantissues and performance can be gathereddirectly through dialogue or indirectlythrough media articles, public reports andsurveys.

l During production: stakeholders can beinvited to comment on reportingexpectations or to review drafts. Stakeholderinput can also help to confirm the relevanceof the proposed content.

l Post-publication: stakeholders can be givenopportunities to review the completedreport, indicating how they might make useof it, and what they would like to see in thefuture.

13

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 2 The reporting process: how

to report

Many channels exist to further engagestakeholders on the report, including focusgroups, surveys, panels, web forums and socialnetworking. It is important to take care toensure consistency with the primary messagescontained in the report.

The process of reporting and relatedengagement is typically annual, providing aperiodic opportunity for stakeholders to assessprogress over time. Reported information may

be provided in different formats, from stand-alone printed reports to internet-accessibleformats that can allow a greater level of detail,timely updates and online feedback.

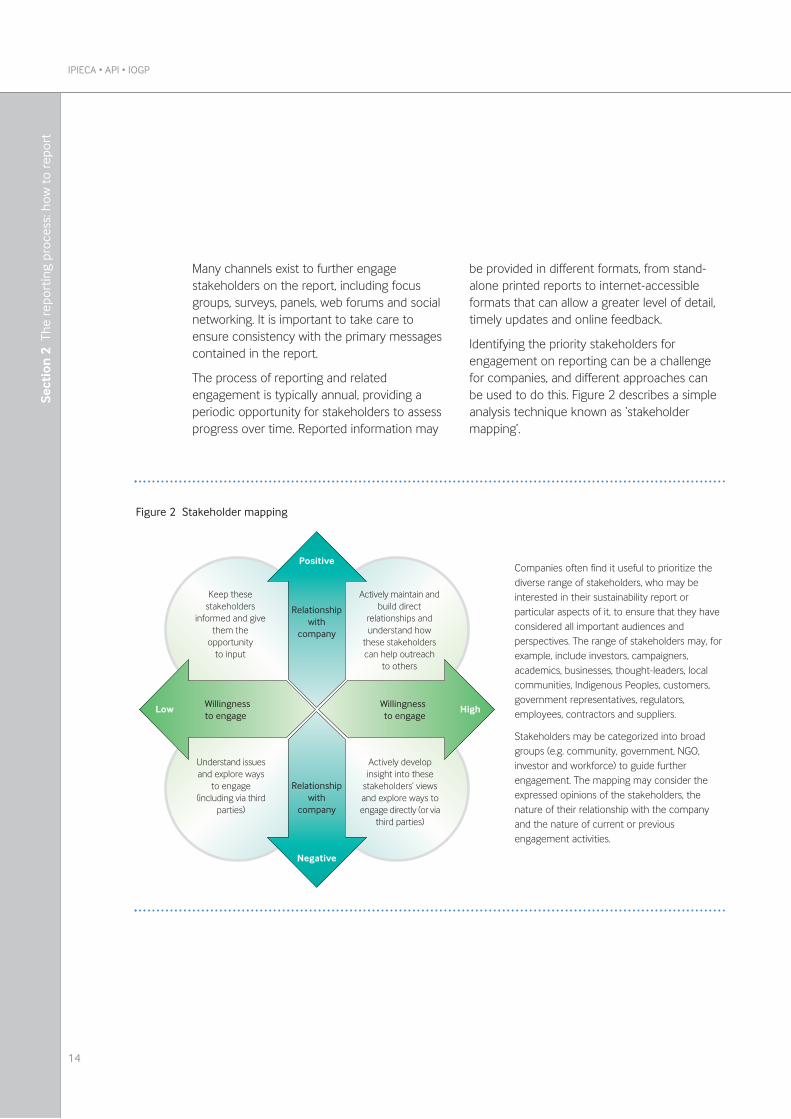

Identifying the priority stakeholders forengagement on reporting can be a challengefor companies, and different approaches canbe used to do this. Figure 2 describes a simpleanalysis technique known as ‘stakeholdermapping’.

IPIECA • API • IOGP

14

Sect

ion

2 T

he r

epor

ting

proc

ess:

how

to

repo

rt

��������

���������� ���

������

����� �������

���������������������������������������

����������������������������

������ ��� ������� ��������� � ������� �������������

�������

��� ����� � ���!�������

������"������������������

���� #

��������������� ������������ ������� $���� ���!������� ���������������"�����

���������� #

���������������

������

���������� ���

������

�� ��� ���������������

Figure 2 Stakeholder mapping

Companies often find it useful to prioritize thediverse range of stakeholders, who may beinterested in their sustainability report orparticular aspects of it, to ensure that they haveconsidered all important audiences andperspectives. The range of stakeholders may, forexample, include investors, campaigners,academics, businesses, thought-leaders, localcommunities, Indigenous Peoples, customers,government representatives, regulators,employees, contractors and suppliers.

Stakeholders may be categorized into broadgroups (e.g. community, government, NGO,investor and workforce) to guide furtherengagement. The mapping may consider theexpressed opinions of the stakeholders, thenature of their relationship with the companyand the nature of current or previousengagement activities.

A sustainability report should set out how acompany’s sustainability priorities are integratedinto its overall vision and business strategy.These priorities should cover both currentoperational issues, such as health and safety,environmental compliance, social/culturalrequirements and labour practices, as well aslonger-term considerations, such as climatechange risks or access to new energy resources.

DEFINE SUSTAINABILITY

Reports generally describe a company’sunderstanding of what ‘sustainability’, ‘corporateresponsibility’ or ‘corporate citizenship’ meansto their company, and indicate the mainimplications and opportunities for its core oiland gas businesses. For example, a companymay wish to discuss how its long-term successdepends on supplying necessary products andservices; but at the same time, how itrecognizes the need to respect and contributeto the communities where it operates and tosafeguard the environment and culturalheritage. Such a statement of intent helps toset the scene for describing the company’sforward vision and strategy.

REVEAL VISION

A company’s vision statement can look to thesustainability opportunities and challenges ofsupplying energy into the future. The vision willoften be presented in the context of existingcorporate values, principles and policycommitments with reference to:

l quality of products;

l safety and reliability of operations;

l care for the environment and communities;

l engaging stakeholders;

l respect for others and their rights; and

l innovation and pioneering solutions.

15

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 2 The reporting process: how

to report

Step 1: Articulate vision and strategy

EXPLAIN STRATEGY

A company can explain how its strategy andplans create value for its shareholders bymeans of its current performance and—in thatcontext—describe its principal sustainabilityissues and its approach to addressing them.The high-level vision and strategy are often setout in an executive management or chairman’sletter at the opening of the report. Thisintroduction to the report serves todemonstrate top-level personal commitment tosustainability and involvement in leading thebusiness to achieve the company’s vision andstrategy. The introduction is also anopportunity to show how management istaking responsibility for any difficult challenges,decisions or dilemmas faced by the company,and to set out how these will be addressed, forexample, through new investments, initiativesor goals. The description of the strategy can bedeveloped further throughout the reportcontent or on the company website with moredetail as appropriate.

Having articulated the vision and strategy, it isimportant for companies to report on the roleof the board and/or executives with regard tosustainability-related governance andmanagement systems.

OUTLINE BOARD GOVERNANCE

The report can describe how the boardfunctions, how often it meets and whetherspecific board members are associated withsustainability issues or are members of arelated subcommittee, which may includeindependent advisers. The report can alsodiscuss the role of the most senior executivesand how they manage the business, includingengaging with stakeholders and integratingsustainability considerations into decisionmaking. Because the details related togovernance and accountability do not typicallychange on an annual basis, companies may

provide such information on their website andhave the sustainability report refer the readerto the relevant web content. However, whenchanges occur related to governance, thecompany should consider whether these haveimplications relevant to the sustainabilityreport (Step 3) and the potential need toprovide prominent coverage of the effects ofthe changes.

DETAIL MANAGEMENT SYSTEMS

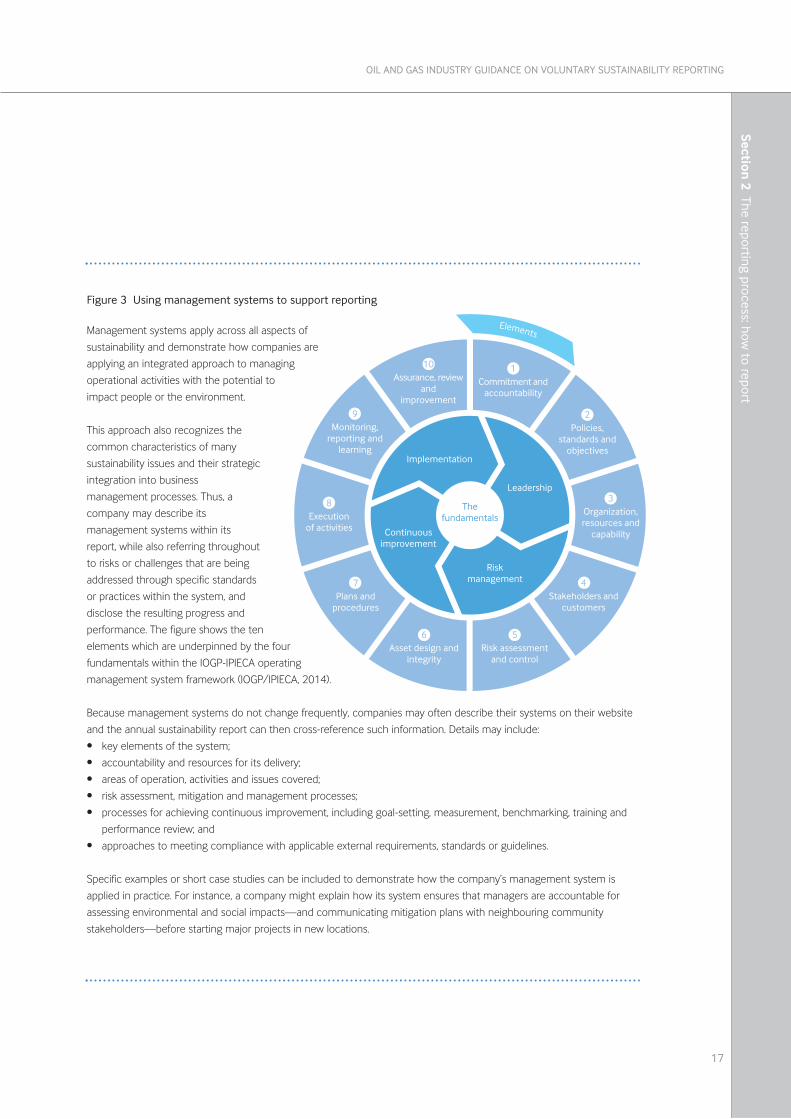

Robust management systems ensure that thecompany’s values, principles and policycommitments are consistently applied bymanagement across the company. The status,implementation and effectiveness of suchmanagement systems are usually addressed ina sustainability report. Companies typicallystate which systems are established, refer tomajor changes as appropriate in their printedsustainability report, and may provide moredetails about the systems on their website. Ifrelevant, companies should explain how theyhave applied, within their managementsystems, international standards or guidance,e.g. International Standards Organization (ISO)guidance such as the ISO 9000, ISO 14000 orISO 26000 series of documents, nationalpublications based on the Occupational Healthand Safety Advisory Services (OHSAS) 18001standard, or guidance from associations suchas IOGP or API. Such management systemsalso underpin the continuous improvementcycle of planning, execution, monitoring andreview. The monitoring step of this process isgenerally based on performance indicators,many of which can be included in thecompany’s sustainability report. Figure 3 showshow the use of management systeminformation provides a foundation thatcomplements and underpins the indicatorinformation in a report.

IPIECA • API • IOGP

16

Sect

ion

2 T

he r

epor

ting

proc

ess:

how

to

repo

rt

Step 2: Describe governance and management systems

17

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 2 The reporting process: how

to report

Management systems apply across all aspects of

sustainability and demonstrate how companies are

applying an integrated approach to managing

operational activities with the potential to

impact people or the environment.

This approach also recognizes the

common characteristics of many

sustainability issues and their strategic

integration into business

management processes. Thus, a

company may describe its

management systems within its

report, while also referring throughout

to risks or challenges that are being

addressed through specific standards

or practices within the system, and

disclose the resulting progress and

performance. The figure shows the ten

elements which are underpinned by the four

fundamentals within the IOGP-IPIECA operating

management system framework (IOGP/IPIECA, 2014).

Because management systems do not change frequently, companies may often describe their systems on their website

and the annual sustainability report can then cross-reference such information. Details may include:

• key elements of the system;

• accountability and resources for its delivery;

• areas of operation, activities and issues covered;

• risk assessment, mitigation and management processes;

• processes for achieving continuous improvement, including goal-setting, measurement, benchmarking, training and

performance review; and

• approaches to meeting compliance with applicable external requirements, standards or guidelines.

Specific examples or short case studies can be included to demonstrate how the company’s management system is

applied in practice. For instance, a company might explain how its system ensures that managers are accountable for

assessing environmental and social impacts—and communicating mitigation plans with neighbouring community

stakeholders—before starting major projects in new locations.

Figure 3 Using management systems to support reporting

�����������������

�����������

���������

������������

������

����������� ����������

����!�����

"#$����� ������

������������

%&�������

�����������������

"������������

�������!�����

'(������

����������!)������

*���������

���������

+$����������

��������

,(�����

���������

-�.������

�/����������

01�������������

�������

2��/��������

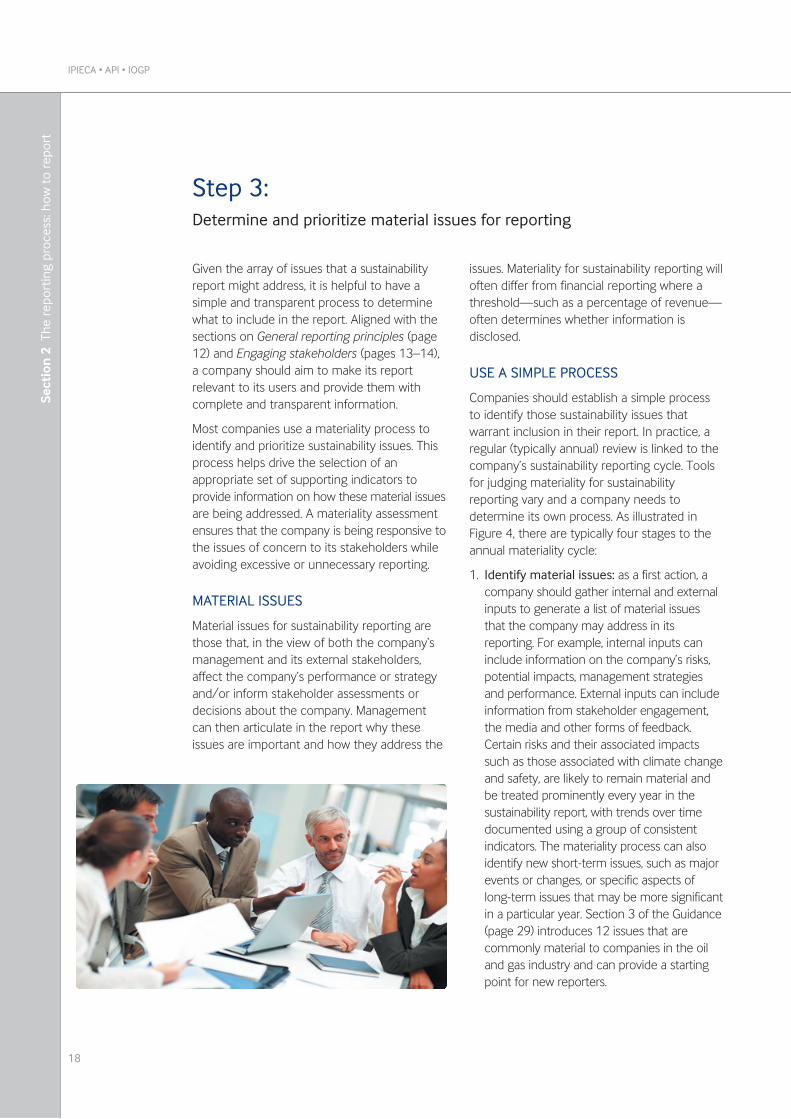

Given the array of issues that a sustainabilityreport might address, it is helpful to have asimple and transparent process to determinewhat to include in the report. Aligned with thesections on General reporting principles (page12) and Engaging stakeholders (pages 13–14),a company should aim to make its reportrelevant to its users and provide them withcomplete and transparent information.

Most companies use a materiality process toidentify and prioritize sustainability issues. Thisprocess helps drive the selection of anappropriate set of supporting indicators toprovide information on how these material issuesare being addressed. A materiality assessmentensures that the company is being responsive tothe issues of concern to its stakeholders whileavoiding excessive or unnecessary reporting.

MATERIAL ISSUES

Material issues for sustainability reporting arethose that, in the view of both the company‘smanagement and its external stakeholders,affect the company’s performance or strategyand/or inform stakeholder assessments ordecisions about the company. Managementcan then articulate in the report why theseissues are important and how they address the

issues. Materiality for sustainability reporting willoften differ from financial reporting where athreshold—such as a percentage of revenue—often determines whether information isdisclosed.

USE A SIMPLE PROCESS

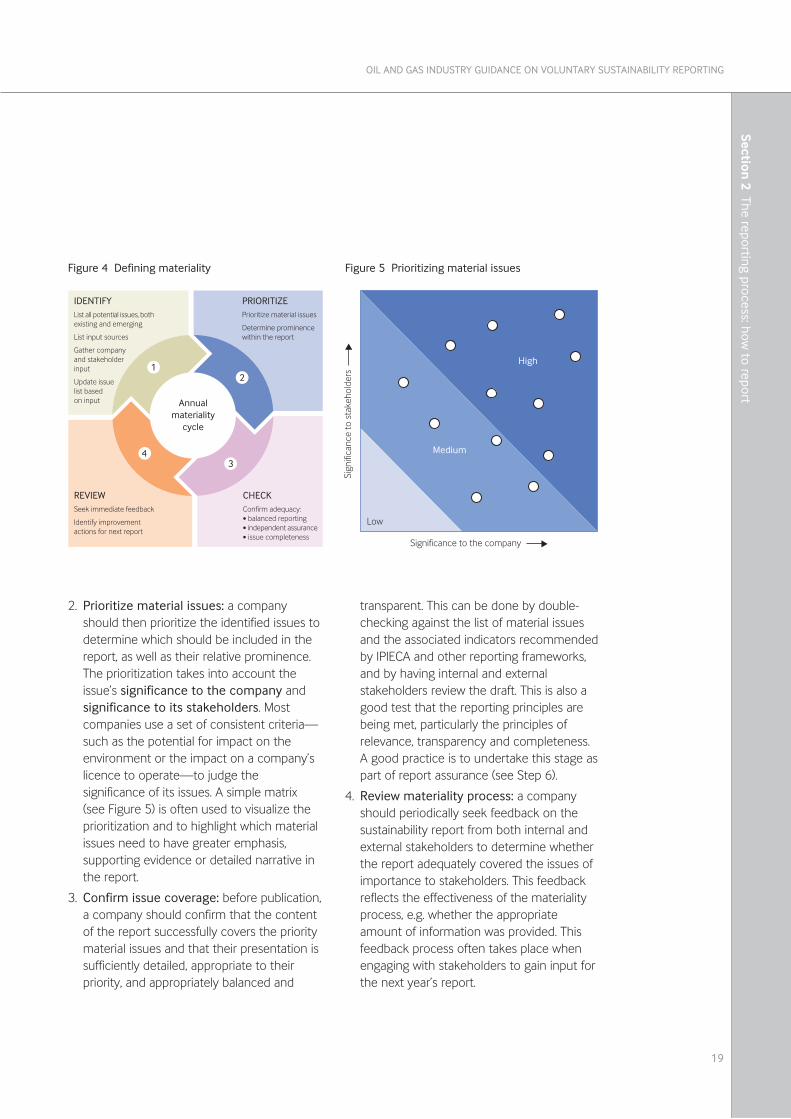

Companies should establish a simple processto identify those sustainability issues thatwarrant inclusion in their report. In practice, aregular (typically annual) review is linked to thecompany’s sustainability reporting cycle. Toolsfor judging materiality for sustainabilityreporting vary and a company needs todetermine its own process. As illustrated inFigure 4, there are typically four stages to theannual materiality cycle:

1. Identify material issues: as a first action, acompany should gather internal and externalinputs to generate a list of material issuesthat the company may address in itsreporting. For example, internal inputs caninclude information on the company’s risks,potential impacts, management strategiesand performance. External inputs can includeinformation from stakeholder engagement,the media and other forms of feedback.Certain risks and their associated impactssuch as those associated with climate changeand safety, are likely to remain material andbe treated prominently every year in thesustainability report, with trends over timedocumented using a group of consistentindicators. The materiality process can alsoidentify new short-term issues, such as majorevents or changes, or specific aspects oflong-term issues that may be more significantin a particular year. Section 3 of the Guidance(page 29) introduces 12 issues that arecommonly material to companies in the oiland gas industry and can provide a startingpoint for new reporters.

IPIECA • API • IOGP

18

Sect

ion

2 T

he r

epor

ting

proc

ess:

how

to

repo

rt

Step 3: Determine and prioritize material issues for reporting

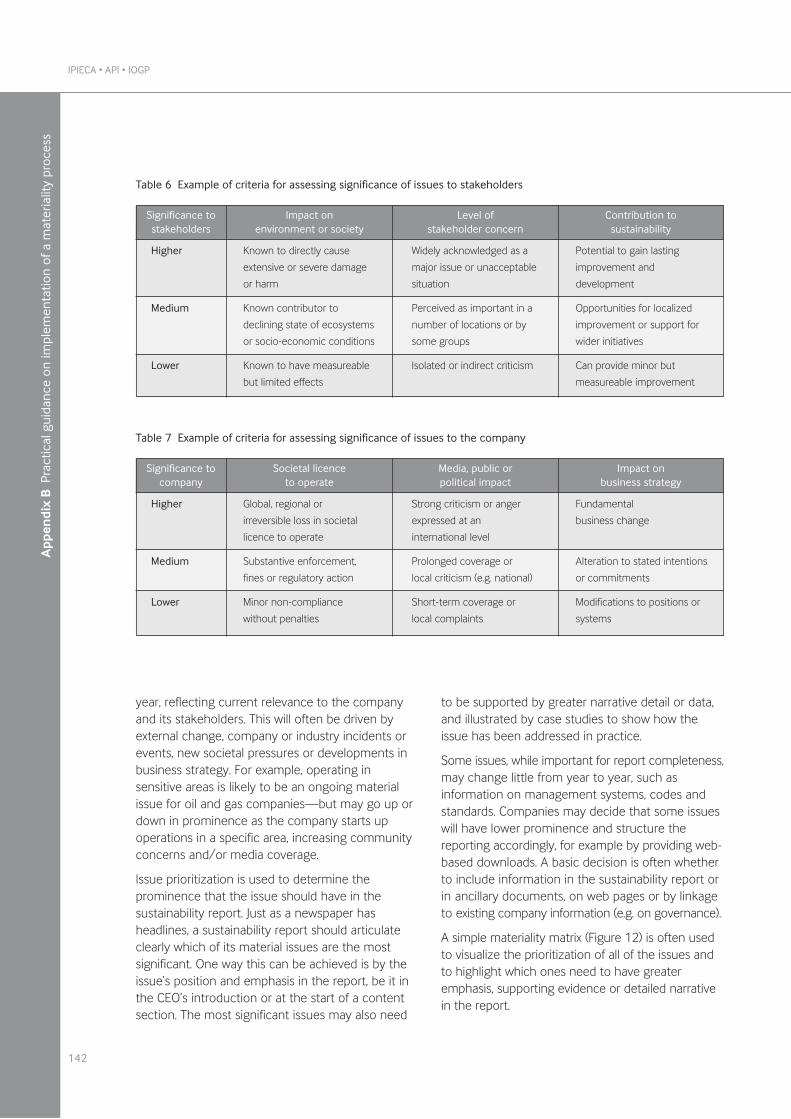

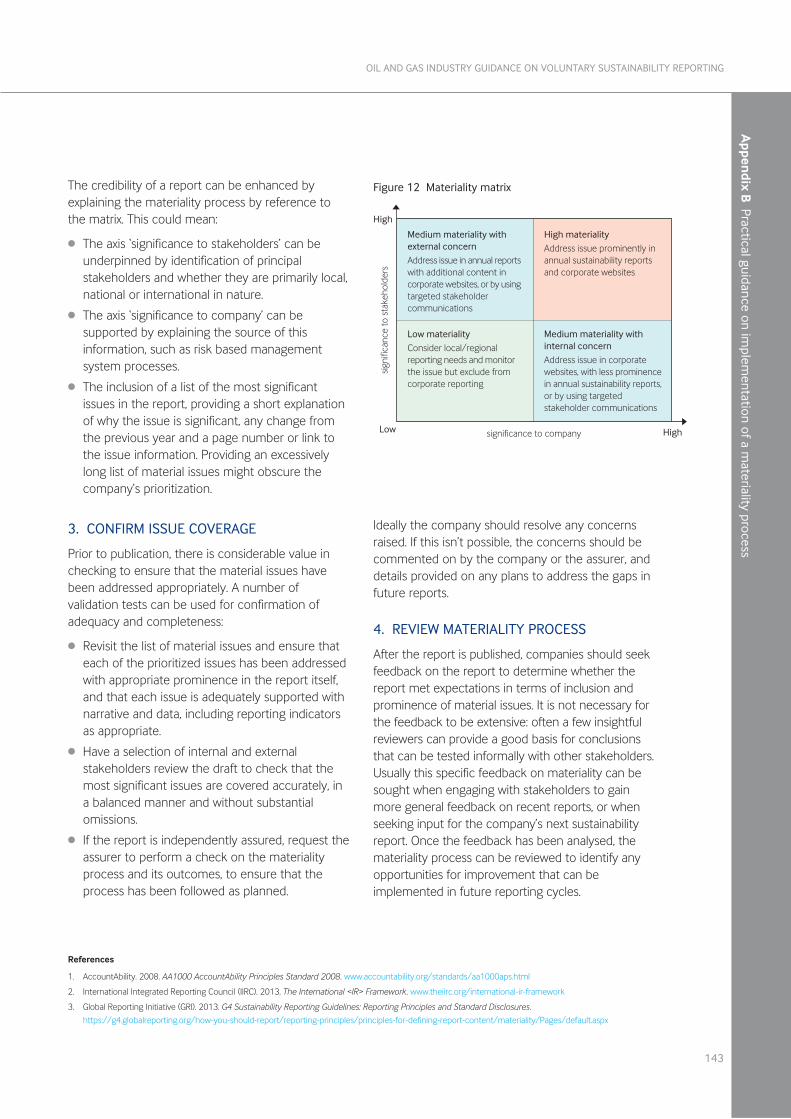

2. Prioritize material issues: a companyshould then prioritize the identified issues todetermine which should be included in thereport, as well as their relative prominence.The prioritization takes into account theissue’s significance to the company andsignificance to its stakeholders. Mostcompanies use a set of consistent criteria—such as the potential for impact on theenvironment or the impact on a company’slicence to operate—to judge thesignificance of its issues. A simple matrix(see Figure 5) is often used to visualize theprioritization and to highlight which materialissues need to have greater emphasis,supporting evidence or detailed narrative inthe report.

3. Confirm issue coverage: before publication,a company should confirm that the contentof the report successfully covers the prioritymaterial issues and that their presentation issufficiently detailed, appropriate to theirpriority, and appropriately balanced and

transparent. This can be done by double-checking against the list of material issuesand the associated indicators recommendedby IPIECA and other reporting frameworks,and by having internal and externalstakeholders review the draft. This is also agood test that the reporting principles arebeing met, particularly the principles ofrelevance, transparency and completeness.A good practice is to undertake this stage aspart of report assurance (see Step 6).

4. Review materiality process: a companyshould periodically seek feedback on thesustainability report from both internal andexternal stakeholders to determine whetherthe report adequately covered the issues ofimportance to stakeholders. This feedbackreflects the effectiveness of the materialityprocess, e.g. whether the appropriateamount of information was provided. Thisfeedback process often takes place whenengaging with stakeholders to gain input forthe next year’s report.

19

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 2 The reporting process: how

to report

Figure 4 Defining materiality

$��������������

�����

�3�42�56%� �������������� � ������!� ��������������

%� �������� ����

&������������� ������������

����� ��� ��� ���������

(�����2�7������������������ �

������������������������������

�8��9'��������(���)*���������������*���������� ����*�� ���������

��:������������������

+��������������������� ������!�������

"'

0�

Figure 5 Prioritizing material issues

&�����

8���

%��

�����������������������

�������������� �������

*���������� �����

�������������

� ���������

����,���������

����,�������

��,��������

���������

���������� ���� ���

*�� ����������� *�����������������������*������������ *���� �����

*������ ������������ ���*������������ *������������������*�������� ����� *�������� *���������������

*��-�� �����*�� ���� ��������*�������������������� *�� �������� ���� *���� �� ����� *������������*��������������������

*�������� *��������������*��������

*������ ���� *��� �*���� ��� ������*��������� ��������� � ��� ���� *���� ���� �������

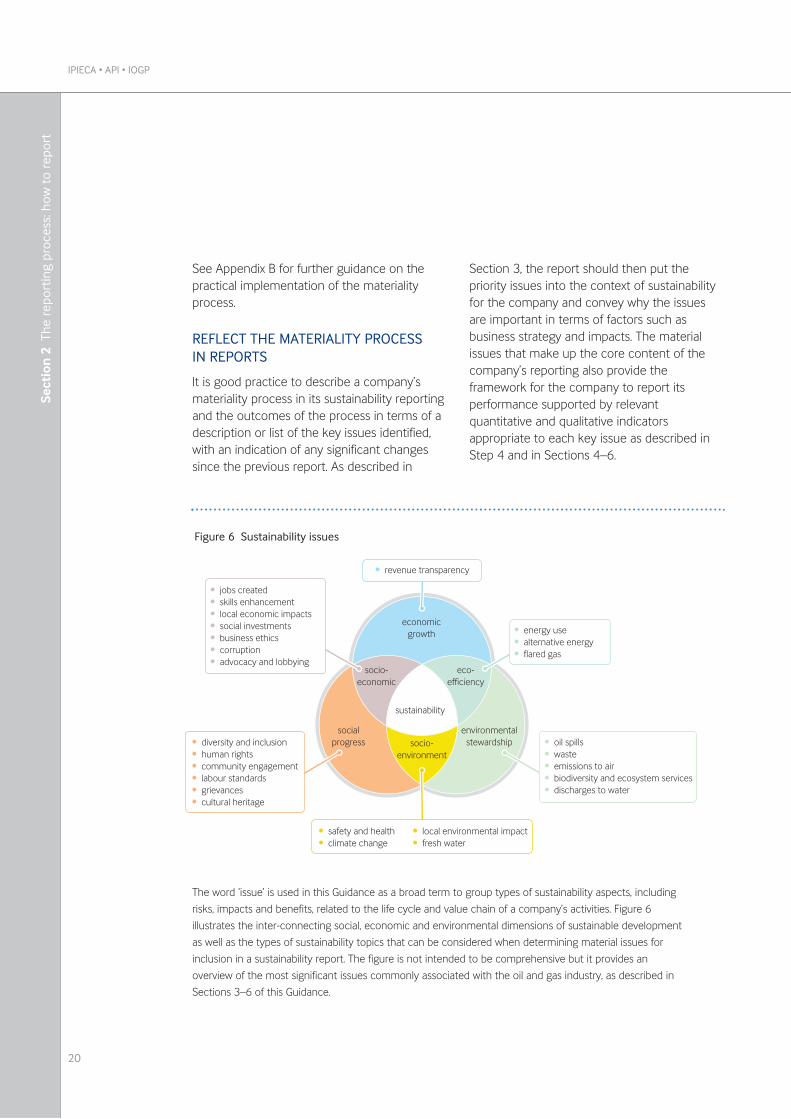

The word ‘issue’ is used in this Guidance as a broad term to group types of sustainability aspects, including

risks, impacts and benefits, related to the life cycle and value chain of a company’s activities. Figure 6

illustrates the inter-connecting social, economic and environmental dimensions of sustainable development

as well as the types of sustainability topics that can be considered when determining material issues for

inclusion in a sustainability report. The figure is not intended to be comprehensive but it provides an

overview of the most significant issues commonly associated with the oil and gas industry, as described in

Sections 3–6 of this Guidance.

Figure 6 Sustainability issues

See Appendix B for further guidance on thepractical implementation of the materialityprocess.

REFLECT THE MATERIALITY PROCESSIN REPORTS

It is good practice to describe a company’smateriality process in its sustainability reportingand the outcomes of the process in terms of adescription or list of the key issues identified,with an indication of any significant changessince the previous report. As described in

Section 3, the report should then put thepriority issues into the context of sustainabilityfor the company and convey why the issuesare important in terms of factors such asbusiness strategy and impacts. The materialissues that make up the core content of thecompany’s reporting also provide theframework for the company to report itsperformance supported by relevantquantitative and qualitative indicatorsappropriate to each key issue as described inStep 4 and in Sections 4–6.

IPIECA • API • IOGP

20

Sect

ion

2 T

he r

epor

ting

proc

ess:

how

to

repo

rt

21

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 2 The reporting process: how

to report

Step 4: Select indicators and collect data

INDICATOR SELECTION

Identification of a company’s material issuesfor reporting should inform the selection ofindicators. Section 3 of the Guidanceintroduces 12 ‘issue categories’ that are likelyto be relevant to many oil and gas companiesfor reporting, along with 34 ‘performanceindicators’ for use by companies, asappropriate, to demonstrate how the issuesare being addressed. While companies areencouraged to report in accordance withthese defined indicators, to enhancecomparability across the oil and gas sector,companies may also customize indicators ordevelop additional measures to improvereporting on key issues. Focused engagementwith internal and external stakeholders prior toreporting can provide useful early feedback onindicator selection.

Below are some factors to consider whenselecting indicators:

l Indicators for long-term issues need to bereported consistently every year, particularlyto track trends in performance againstcontinuous improvement objectives and toprovide comparability within and betweencompanies.

l Other issues may have emerged orincreased in importance over a short period.The company may decide to supplementpreviously used indicators with newmeasures to improve disclosures on itsassociated performance.

l In some instances, a significant or complexissue will relate to more than one of theissue categories, for instance with social,economic, health, safety and environmentaldimensions, and involve reporting against avariety of different indicators. Step 5provides two examples of reporting on thesetypes of issues—Research and technology,and Impacts on communities.

DATA COLLECTION

Having selected indicators, the next stage is todetermine what quantitative data andqualitative information will be collected withinthe company. The prominence that thecompany decides to give a material issue in itsreport will help to guide the depth and breadthof data or information collected. For eachindicator provided in Sections 4–6, a choice of‘reporting elements’ is provided that may beapplicable to the company’s operations, andwhich define the types of information or datathat can be collected:

l Common reporting elements provideperformance measures that are wellestablished across the industry and are agood starting point for new reporters or forthose seeking comparability.

l Supplemental reporting elements providealternate or additional choices of measuresthat provide more depth or differentapproaches.

l Other reporting elements provide furtherreporting options through less-establishedcomplementary measures, or emergingpractices.

Having defined and determined the quantitativedata and qualitative information to be collected,the company should request the data internally,supported by appropriate guidance anddefinitions. Requests for information should betimely: business and operational organizationsand functions need a reasonable opportunity tocollect data and verify its accuracy. Oncereceived, data can be consolidated on a

corporate basis and reviewed for completenesswithin the ‘reporting boundary’. (For detailedguidance on the reporting boundary and ondata management, such as establishingbaselines, see Section 3 and Appendix A.)

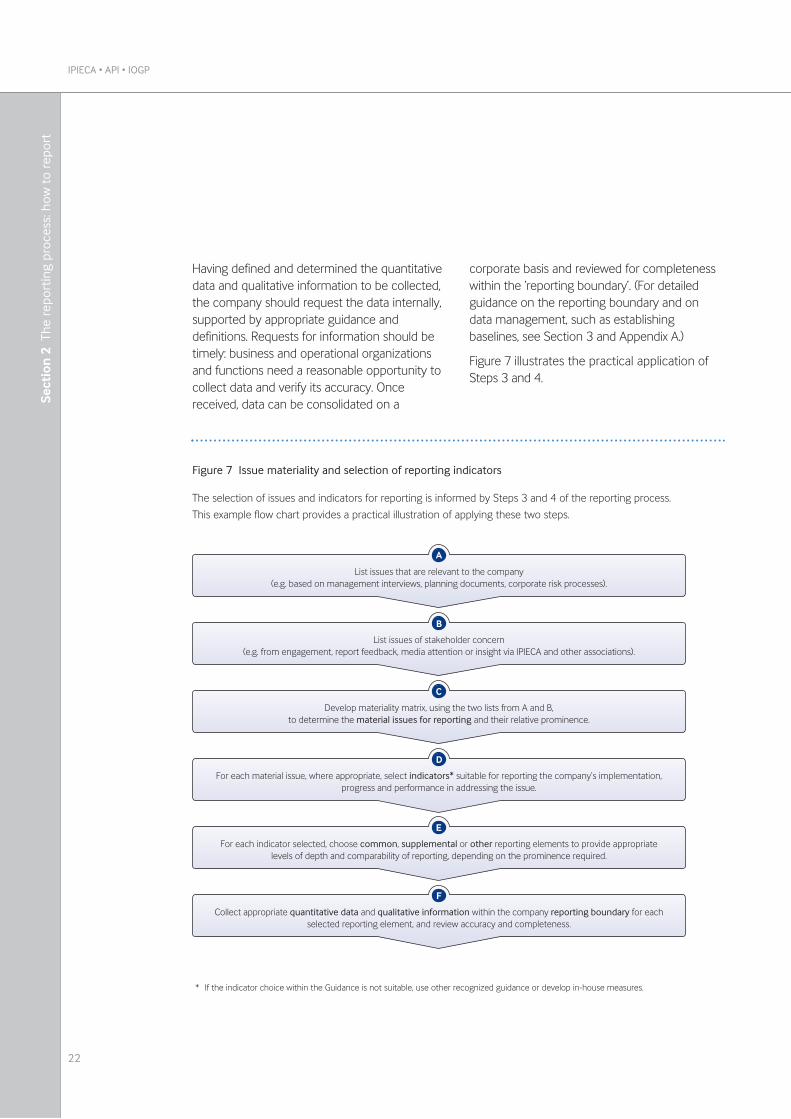

Figure 7 illustrates the practical application ofSteps 3 and 4.

�

�

�

�

�

�

%� ��� � �������������������������".�.�� ������������������� ����������������� ������������ ������ #.

%� ��� � ���� ��������������".�.�������������������������������������������� ��������+�+/'���������� ������� #.

�������������������!��� ������������� � �����������0���������������������������/����������������������������������.

1������������� ����������������� ������������;� ����������������������������$ ������������������ ������������������� �������� �.

1��������������� ���������� ����������������������������������������� ���������������������� �������������������������������������������������������������(����.

'���������������<�������������������<������������/����������������������������������!������������� ��������������������������������������������� .

The selection of issues and indicators for reporting is informed by Steps 3 and 4 of the reporting process.

This example flow chart provides a practical illustration of applying these two steps.

Figure 7 Issue materiality and selection of reporting indicators

* If the indicator choice within the Guidance is not suitable, use other recognized guidance or develop in-house measures.

IPIECA • API • IOGP

22

Sect

ion

2 T

he r

epor

ting

proc

ess:

how

to

repo

rt

23

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Step 5: Analyse data and incorporate into narrative

Section 2 The reporting process: how

to report

A sustainability report aims to demonstrate,through quantitative and qualitative evidence,that a company is systematically appraising andresponsibly managing its sustainabilityperformance. A major step in the reportingprocess is to analyse the indicator data andincorporate the results into a narrative thatdescribes performance progress within thecontext of the sustainability issues.

PUTTING RESULTS INTO CONTEXT

Providing context through narrative requires acompany to think strategically about how itcommunicates material issues and relevantindicator data. A report can help to explain thesignificance of a company’s performance byclarifying:

l how the results are relevant to thecompany’s operations;

l their significance in the context of historic orrecent trends and/or in relation to priorexpectations of performance, such ascontinuous improvement objectives;

l the nature of impacts on relevantstakeholders;

l the opinions of stakeholders or othercredible third parties on those impacts;

l the effect of existing strategy andmanagement on results;

l how the results may compare to relevantindustry benchmarks or averages; and

l strategic responses, goals or lessons learned.

The example on Research and technology, onpage 24, illustrates incorporation of indicatordata into narrative where it is important toprovide context for a strategic issue.

EXPLAIN PROGRESS AGAINST GOALS

Supported by the indicator information anddata, the narrative can plot progress againstthe company’s plans to achieve it’s goals,together with explanations for variations inrelated performance. Continuous improvementis a cornerstone of management systems andis generally based on a cycle of planning,implementing, measurement (using indicators)and assessment, which results in regularlyupdated improvement plans at the local level.Objectives, targets and other information canbe reported to demonstrate progress, forexample:

l quantitative targets based on outcomes,such as reduction of emissions or incidents;

l quantitative or qualitative objectives in termsof inputs, such as completion ofmanagement system initiatives by a planneddate;

l annual progress measured against acommitment to continuous improvement; or

l case studies providing evidence ofprogrammes planned across a specifiedperiod.

The oil and gas industry has a long history of innovation,

investing in research and development of new

technologies to produce, refine and manufacture energy

and other products for society. Within company reports, it

is important to look to the future in terms of how research

and technology can address sustainability challenges.

Describing a company’s strategy and current efforts to

provide advanced technical solutions helps to

demonstrate a company’s intent to reduce environmental

or other impacts while providing improved benefits that

enhance socio-economic development.

While many of the issues described in this Guidance can

benefit from innovative approaches, a high priority is

technological advances to address the risks of climate

change, often with related benefits for other issues, such

as air quality, access to fresh water and waste

minimization. Examples of advanced technology

approaches within the industry include:

• combining heat and power units to reduce energy

consumption;

• reformulating gasoline and diesel for increased fuel

efficiency and reduced emissions;

• investing in non-fossil fuel alternative energy supplies;

• improving energy efficiency within the value chain,

including measures that provide options to reduce

consumer fuel use and related emissions;

• reducing flaring through improved gas management;

• researching and piloting viable carbon capture and

storage processes, including sequestration in deep

geological aquifers;

• manufacturing advanced plastics and other materials

to make cars lighter, stronger and more efficient;

• partnering with vehicle manufacturers to develop fuel

cells and other energy sources; and

• developing sustainable biofuels, including researching

the feasibility of second-generation biofuels.

Other technologies may focus on a company’s footprint on

ecosystem services and marine or terrestrial biodiversity.

Examples include using more environmentally friendly

chemicals in field operations, drilling technology that requires

a smaller surface footprint, or brush cutters that leave

roots undisturbed. Innovation can also benefit the health,

safety and wellbeing of people, in the workforce or local

communities. This includes managing the risk of hazards

that could harm employees and contractors in the plant,

but also of transport safety, particularly for road vehicles.

EXAMPLE: RESEARCH AND TECHNOLOGY

IPIECA • API • IOGP

24

Sect

ion

2 T

he r

epor

ting

proc

ess:

how

to

repo

rt

BALANCED REPORTING

It is important to meet the principles oftransparency and completeness by disclosingany significant shortfalls, problems andincidents that have been faced by thecompany during the reporting period. Whilethere may be legal or other constraints interms of detailed disclosure, a report shouldnevertheless aim to present a balanced pictureof the company’s challenges as well asachievements. A report that tends to conveyonly ‘good news’ is unlikely to be seen ascredible, reasonable or sufficient in itscoverage. When reporting challenges, the

company should also take the opportunity tolook forward by demonstrating how it islearning and adapting to improve its futureperformance.

RECOGNIZE COMPLEX ISSUES

In some instances, a material issue may reflectseveral social, environmental or otherdimensions and involve reporting against avariety of different indicators. These multi-faceted topics are often associated withspecific events or activities, such as anexploration project in an environmentally andsocially vulnerable location. The example on

25

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 2 The reporting process: how

to report

Oil and gas company activities can be very large

undertakings in physical and economic terms. They may

bring many benefits for host communities. They may also

involve a range of impacts relating to health and safety,

economic, social and/or environmental concerns. Reporting

companies need to balance reporting at a corporate level

with attention to particular local situations. (See Working in

remote locations on page 26). A company’s materiality

appraisal (Step 3) will usually identify the specific

locations that warrant detailed coverage. Some aspects

that reporters may wish to consider include:

• corporate policies or programmes with respect to

communities, including specific objectives and

engagement activities (Section 6, SE1–SE4);

• descriptions of local context and particular impacts

regarding the local environment or cultural resources,

community health and safety, and local socio-

economic circumstances, supported by indicators

such as:

- Local hiring practices, and Local procurement

and supplier development (Section 6, SE6, SE7);

- Preventing corruption (Section 6, SE11);

- Human rights (Section 6, SE8–SE10);

- Biodiversity and ecosystem services (Section 4,

E5) and Fresh water (Section 4, E6); and

- Other air emissions, Spills to the environment,

Discharges to water and Waste (Section 4,

E7–E10);

• local engagement, concerns and expectations, and

strategies to address them; and

• independent reviews or lessons learned regarding

community impacts.

EXAMPLE: IMPACT ON COMMUNITIES

Impact on communities (below) illustrates thetypes of narrative and indicators that may bereported for such a complex issue.

EMPLOY CASE STUDIES

Case studies can be a particularly powerful wayto communicate how a company engages withstakeholders and approaches sustainabilitychallenges in the everyday conduct of itsbusiness. Putting indicator data in the contextof real-world operational challenges illustrateshow a company can work effectively tomanage and integrate sustainabilityperformance into its operations. The example

on Working in remote locations (page 26)shows how case studies can be built onspecific indicator information to link acompany’s global approach to addressingissues at the local level.

Table 1 Typical financial and operatinginformation data

INCORPORATING FINANCIAL DATA

Another useful approach is to incorporateselected financial and operating information toprovide business context when reporting onsustainability issues. Typically these data arealready publicly available and should be drawnfrom a company’s annual financial report toensure consistency. In a sustainability report,basic financial and operating information—seeTable 1 for suggested items—can appear ashighlights or in a summary data table. Althoughfinancial data are generally reported at theglobal level, it can help to report selectedinformation at a national or regional level.Companies should also consider reporting anylarge acquisitions or divestments in thereporting year if the changes materially affectthe size and scale of the company.

EXAMPLE: WORKING IN REMOTE LOCATIONS

The oil industry increasingly works in remote

locations, often in developing countries or in sensitive

environments. In such areas of the world,

sustainability issues can be particularly important

and care must be taken to respect ecosystem

services and the rights of local communities or

indigenous people. The materiality of issues in such

circumstances can be significant for stakeholders at

a local level. In such cases it is more appropriate to

develop narrative using a case study that

demonstrates how corporate strategy and values

are applied to the specific circumstances in the

remote location. For example, a case study to

describe activities in a location where there are risks

of impacting freshwater availability and affecting

community relationships might provide:

• the strategy behind the company’s activities and

an overview of the sustainability risks for the

remote location;

• the high-level corporate strategy for operating in

water-stressed regions, and company

approaches to managing community impacts

and engagement, supported by indicators

(Section 4, E6 and Section 6, SE1);

• an explanation of the local water-stress risks,

management plans and progress to minimize

the environmental impact of fresh water used by

the operations;

• a description of the successes, challenges and

outcomes of the local community engagement

(Section 6, SE1), stating any future

commitments made by the company; and

• stakeholder or expert third-party opinion and/or

data that provides additional perspective.

l Total revenues

l Operating expenses

l Total taxes paid

l Profit after tax

l Capital expenditure

l Number of employees

l Number of countries of operation

l Total production (upstream)

l Total throughput (downstream)

IPIECA • API • IOGP

26

Sect

ion

2 T

he r

epor

ting

proc

ess:

how

to

repo

rt

27

OIL AND GAS INDUSTRY GUIDANCE ON VOLUNTARY SUSTAINABILITY REPORTING

Section 2 The reporting process: how

to report

Inclusion of information to provide assuranceon the content of sustainability reports is acommon practice. Assurance processesprovide an opinion regarding the quality ofreported information and can emphasizeapplication of the General reporting principles(page 12). Companies generally have their owninternal assurance mechanisms, but externalassurance, in addition, can enhance theperceived credibility of a sustainability report.External assurance tends to take the form ofaudit-based verification or third-partycommentary. Both methods can coexist in asingle report, but they are distinct processes.

l Audit-based verification typically focuseson quantitative information, including datasystems and interpretation. These auditsare commonly undertaken by accountancyand consulting firms, and are typically seenas a ‘formal’ approach. Audit-basedverification may also seek to testmateriality processes or assess qualitativestatements or claims related tocommitments, vision and strategy, orgovernance and management systems.This approach may include assuranceagainst specific standards, such as:

• The International Standard on AssuranceEngagements (ISAE 3000, revised in2015), which is provided by theInternational Audit and AssuranceStandards Board (IAASB), part of theInternational Federation of Accountants(IFAC). This standard covers theprofessional procedures undertaken by anassurance provider and is binding on IFACmembers, including major accounting andconsulting firms. A choice of two levels ofassurance is provided—‘limited’ is a high-level review, while ‘reasonable’ is a morerigorous, in-depth process in which theauditors provide an opinion that the dataare reliable.