Embed Size (px)

Citation preview

OECD POLICY WORK ON GREEN INVESTMENTS

Nelly PetkovaOECD, Environment Directorate

Second international forum for sustainable business development 17 October 2013, Kiev, Ukraine

0

0.5

1

1.5

2

2.5

3

3.5

4

2

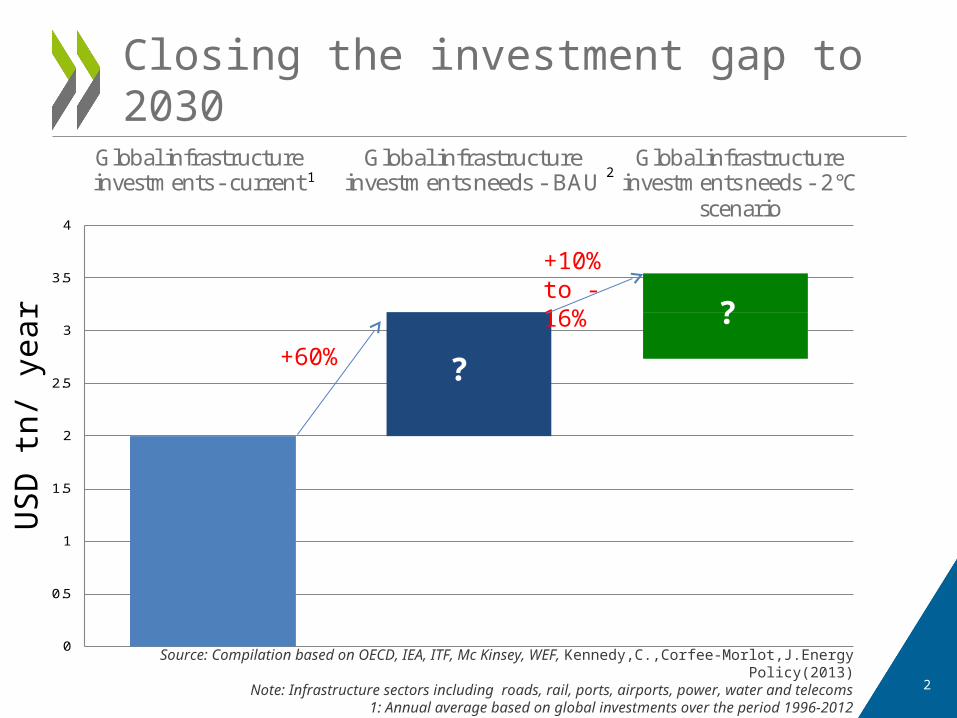

Closing the investment gap to 2030

Source: Compilation based on OECD, IEA, ITF, Mc Kinsey, WEF, Kennedy,C.,Corfee-Morlot,J.Energy Policy(2013)Note: Infrastructure sectors including roads, rail, ports, airports, power, water and telecoms

1: Annual average based on global investments over the period 1996-20122. Annual average needs for the period 2012-2030

US

D t

n/ y

ear

+60%

0

0.5

1

1.5

2

2.5

3

3.5

4

Global infrastructure investments - current

Global infrastructure investments needs - BAU

Global infrastructure investments needs - 2°C

scenario

0

0.5

1

1.5

2

2.5

3

3.5

4

Global infrastructure investments - current

Global infrastructure investments needs - BAU

Global infrastructure investments needs - 2°C

scenario

0

0.5

1

1.5

2

2.5

3

3.5

4

Global infrastructure investments - current

Global infrastructure investments needs - BAU

Global infrastructure investments needs - 2°C

scenario

1 2

?

+10% to -16%

?

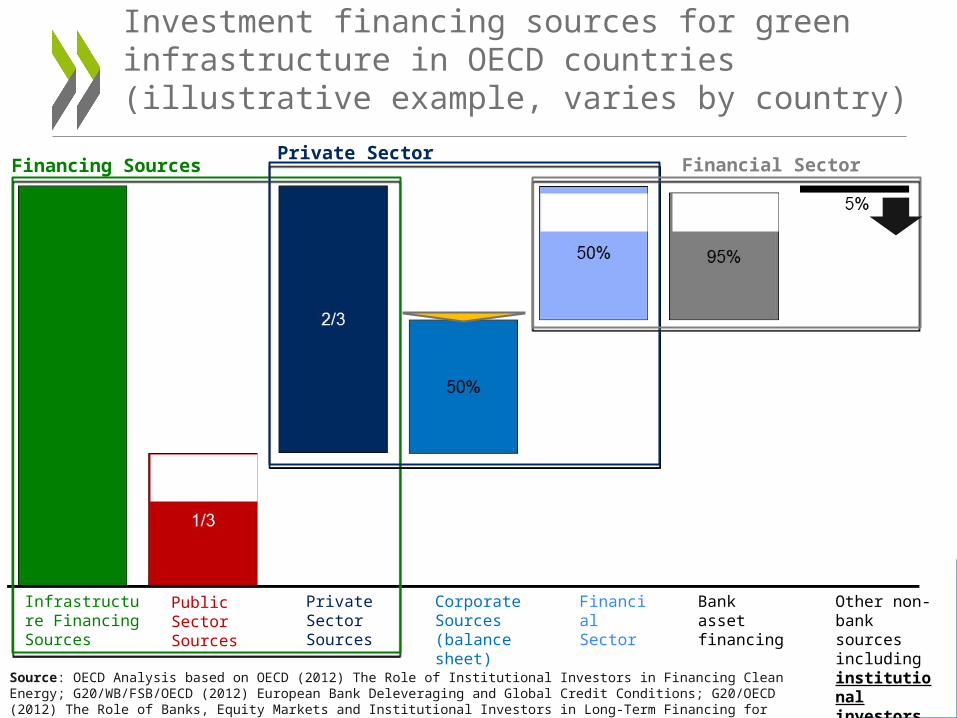

Investment financing sources for green infrastructure in OECD countries (illustrative example, varies by country)

Source: OECD Analysis based on OECD (2012) The Role of Institutional Investors in Financing Clean Energy; G20/WB/FSB/OECD (2012) European Bank Deleveraging and Global Credit Conditions; G20/OECD (2012) The Role of Banks, Equity Markets and Institutional Investors in Long-Term Financing for Growth and Development

Infrastructure Financing Sources

Private Sector Sources

Corporate Sources (balance sheet)

Financial Sector

Bank asset financing

Other non-bank sources including institutional investors

Public Sector Sources

Financing SourcesPrivate Sector

Financial Sector

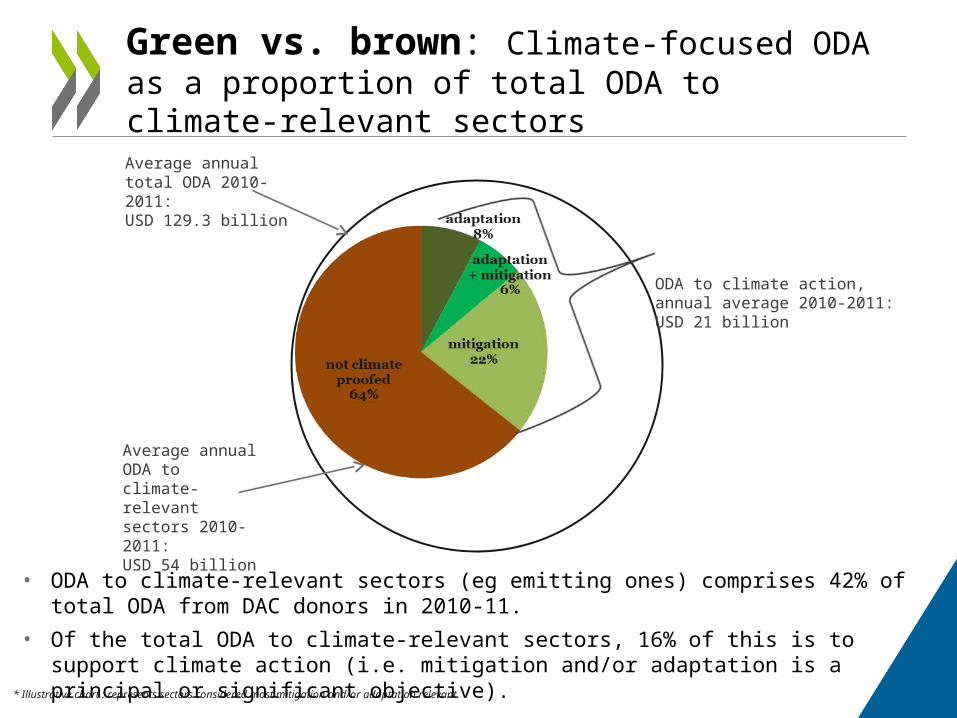

Average annual ODA to climate-relevant sectors 2010-2011: USD 54 billion

Average annual total ODA 2010-2011: USD 129.3 billion

• ODA to climate-relevant sectors (eg emitting ones) comprises 42% of total ODA from DAC donors in 2010-11.

• Of the total ODA to climate-relevant sectors, 16% of this is to support climate action (i.e. mitigation and/or adaptation is a principal or significant objective).

ODA to climate action, annual average 2010-2011: USD 21 billion

Green vs. brown: Climate-focused ODA as a proportion of total ODA to climate-relevant sectors

* Illustrative chart : represents sectors considered most mitigation and/or adaptation relevant.

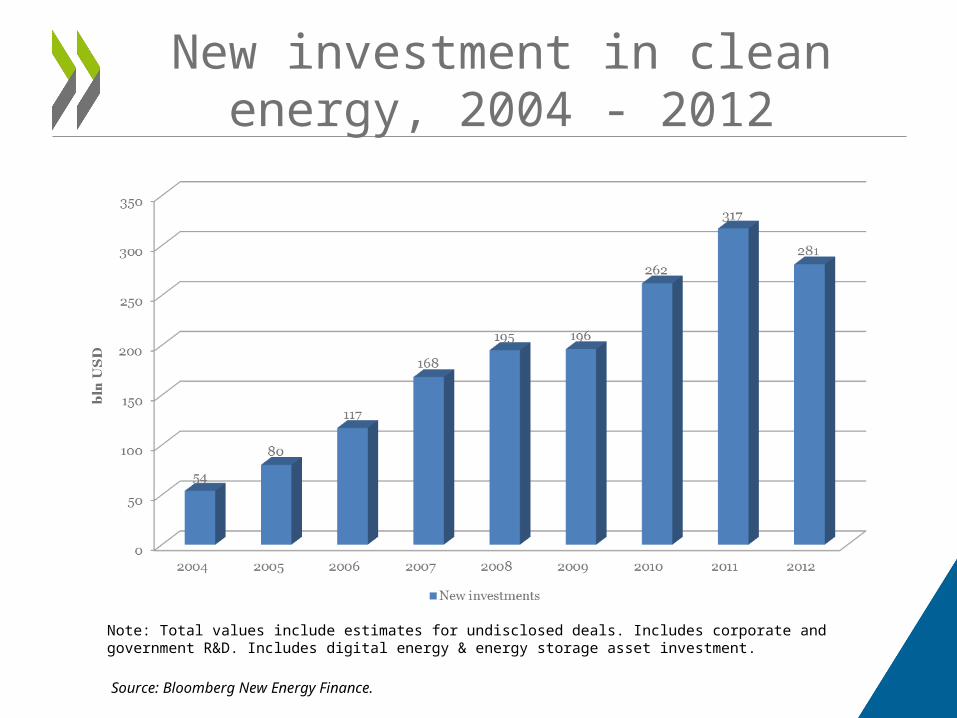

New investment in clean energy, 2004 - 2012

Source: Bloomberg New Energy Finance.

Note: Total values include estimates for undisclosed deals. Includes corporate and government R&D. Includes digital energy & energy storage asset investment.

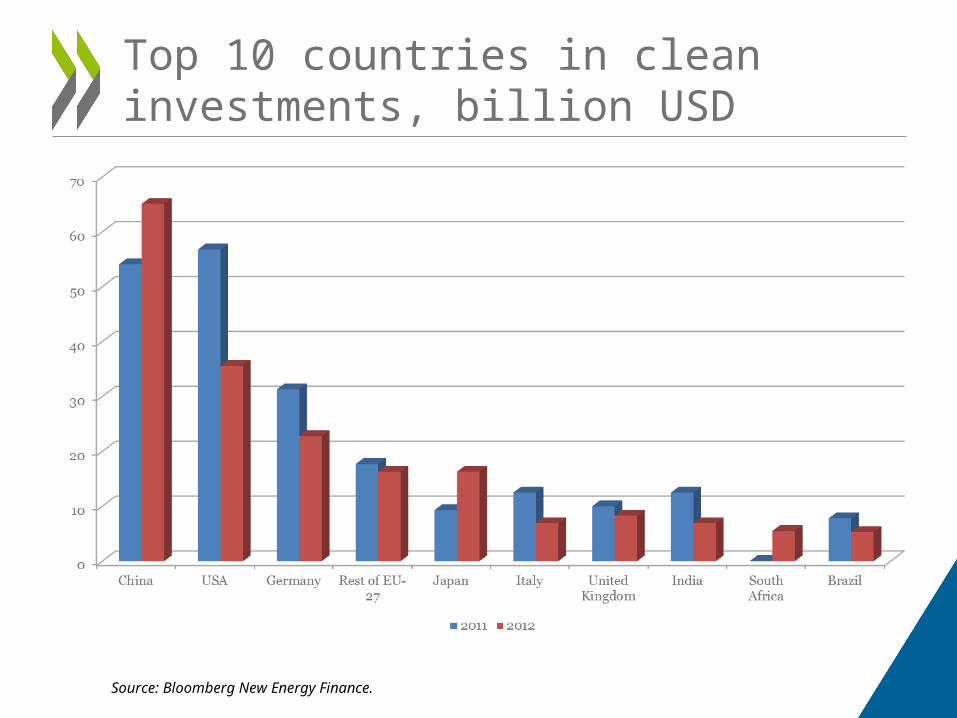

Top 10 countries in clean investments, billion USD

Source: Bloomberg New Energy Finance.

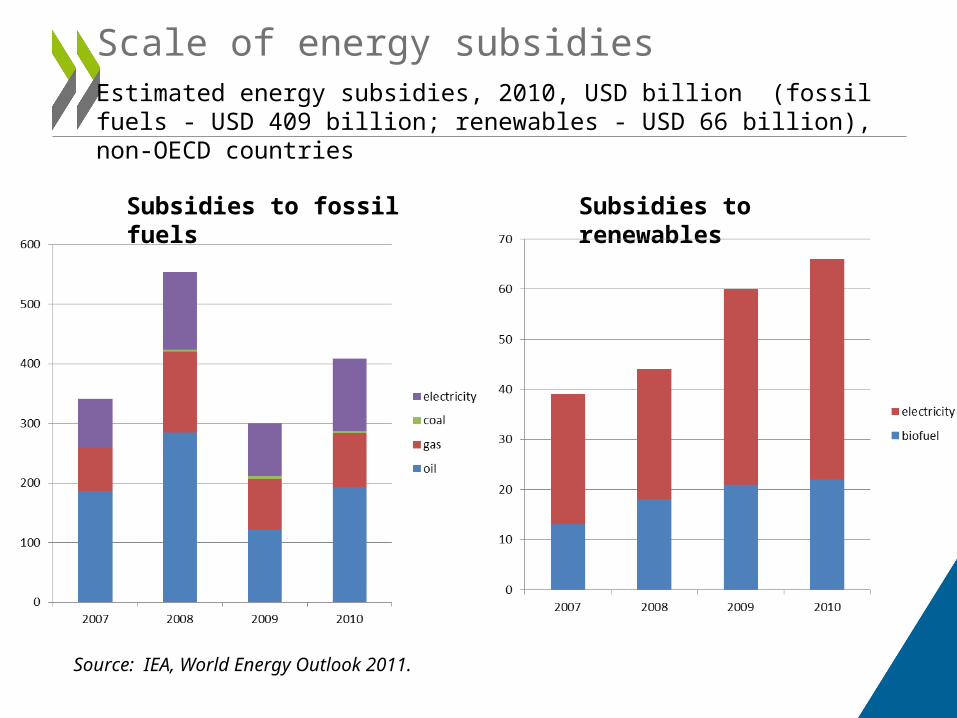

Scale of energy subsidiesEstimated energy subsidies, 2010, USD billion (fossil fuels - USD 409 billion; renewables - USD 66 billion), non-OECD countries

Source: IEA, World Energy Outlook 2011.

Subsidies to fossil fuels Subsidies to renewables

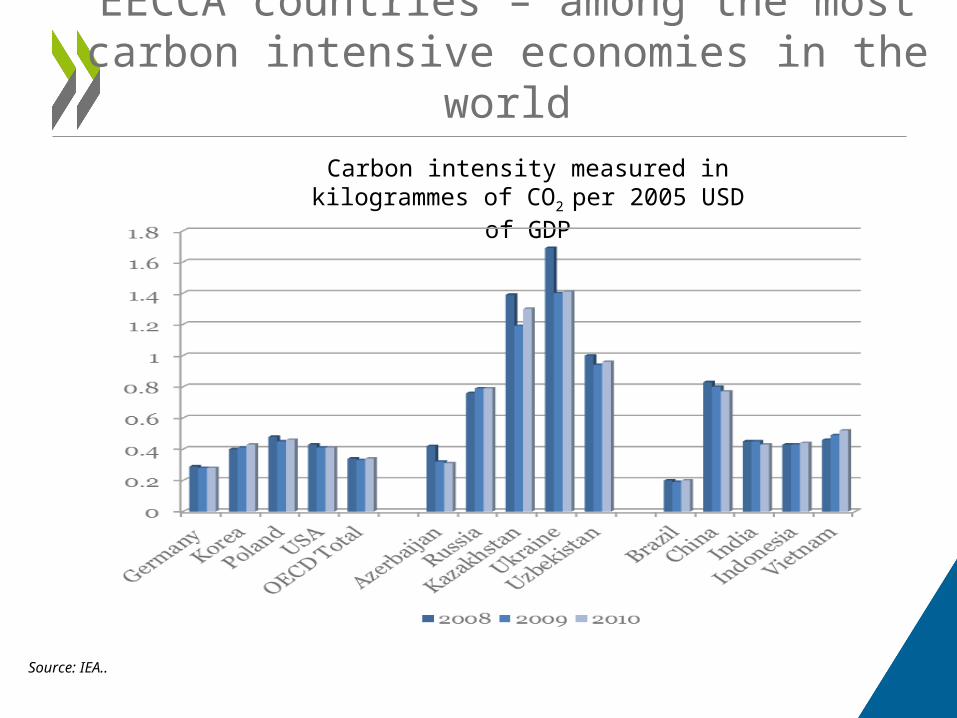

Carbon intensity measured in kilogrammes of CO2 per 2005 USD of GDP

EECCA countries – among the most carbon intensive economies in the world

Source: IEA..

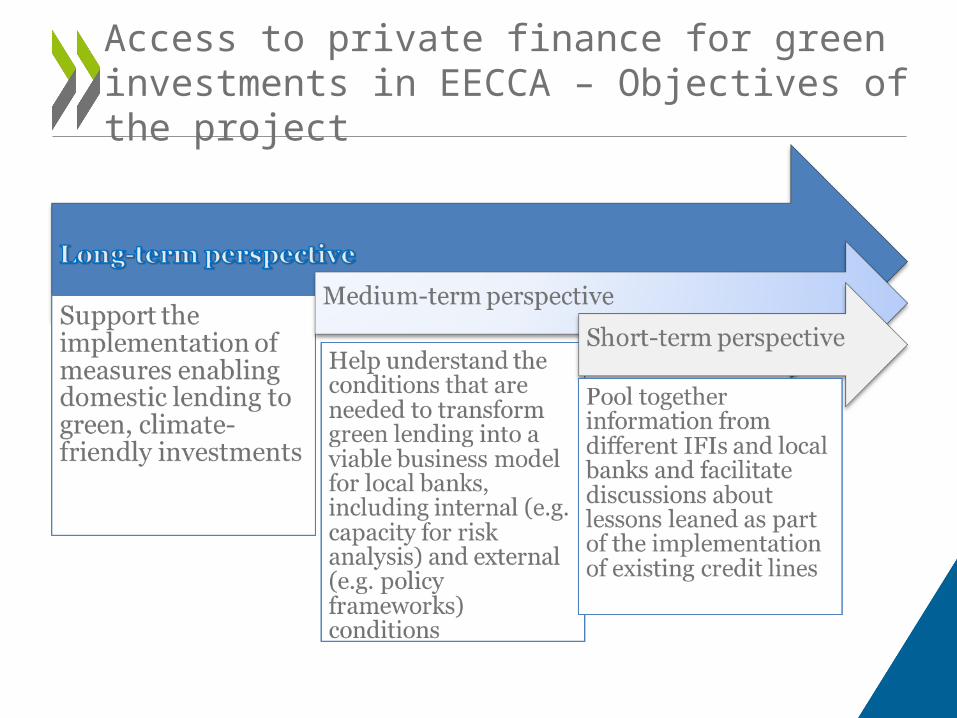

Access to private finance for green investments in EECCA – Objectives of the project

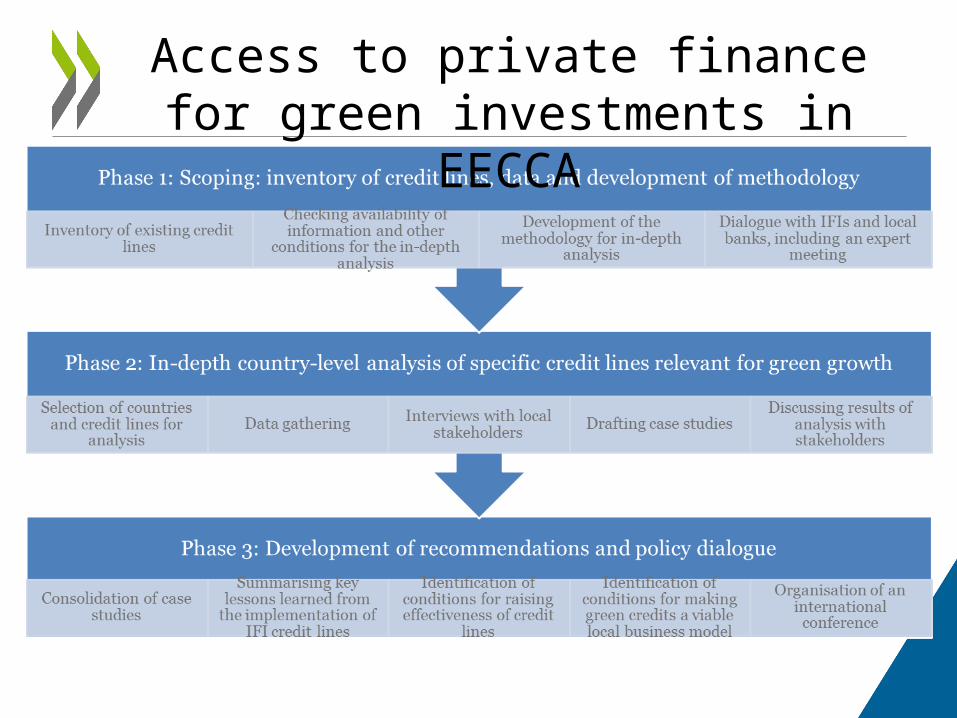

Access to private finance for green investments in EECCA

OECD-Ukraine Co-ordination Council

Agribusiness:Access to Finance

Machinery/Aircraft Manufacturing

Working Group 1 Working Group 3

Civil society and private sector representatives

Relevant ministries and government agencies

Chaired by First Deputy Prime Minister of Ukraine

OECD + donors(including relevant WG members)

The project Sector Competitiveness Strategy for Ukraine was launched in 2009The OECD Eurasia Competitiveness Programme

Energy-efficiency/ Renewable Energy

Working Group 4

Agribusiness:Human Capital

Working Group 2

Facilitate access to finance for SMEs

Improve investment policy and promotion

Strengthen the industry cluster

Ensure appropriate skills provision to the industry

Public-Private dialogue through Working Groups