Embed Size (px)

Citation preview

Ocado Group plc

FY19 Results11th February 2020

1

The Chairman’s OverviewLord Rose

©2020 Ocado Group plc. All rights reserved.

2

This presentation contains oral and written statements that are or may be “forward-looking statements” with respect to certain of Ocado’s plans and its current goals and

expectations relating to its future financial condition, performance and results. These forward-looking statements are usually identified by words such as ‘anticipate’, ‘target’,

‘expect’, ‘estimate’, ‘intend’, ‘plan’, ‘goal’, ‘believe’ or other words of similar meaning. By their nature, all forward-looking statements involve risk and uncertainty because they

are based on current expectations and assumptions but relate to future events and circumstances which may be beyond Ocado’s control. There are important factors that could

cause Ocado’s actual financial condition, performance and results to differ materially from those expressed or implied by these forward-looking statements, including, among

other things, UK domestic and global political, social, economic and business conditions, market-related risks such as fluctuations in interest rates and exchange rates, the policies

and actions of regulatory authorities, the impact of competition, the possible effects of inflation or deflation, variations in commodity prices and other costs, the ability of Ocado to

manage supply chain sources and its offering to customers, the effect of any acquisitions by Ocado, combinations within relevant industries and the impact of changes to tax and

other legislation in the jurisdictions in which Ocado and its affiliates operate. Further details of certain risks and uncertainties are set out in our Annual Report for 2019 which can

be found at www.ocadogroup.com. Ocado expressly disclaims any undertaking or obligation to update the forward-looking statements made in this presentation or any other

forward-looking statements we may make except as required by law. Persons receiving this presentation should not place undue reliance on forward-looking statements which

are current only as of the date on which such statements are made.

Forward-looking statementsDISCLAIMER

©2020 Ocado Group plc. All rights reserved.

3

Tim SteinerCEO

Introduction

©2020 Ocado Group plc. All rights reserved.

4

“We are pleased to report results which show strong momentum in the

business. Although statutory results reflected a combination of factors,

including the impact of the Andover fire, the underlying performance of Ocado

Retail and the successful growth of Ocado Solutions were very encouraging.

Our progress over the last twelve months, which includes signing our eighth

and ninth Solutions clients, Coles in Australia and Aeon in Japan, and

successfully maintaining strong growth post-Andover, has demonstrated many

of Ocado Group’s most important characteristics: resilience, innovation, focus

and execution. It is these qualities that will enable us to continue to develop

the Ocado Smart Platform to meet the evolving needs of our partners at the

cutting edge of online grocery retail.”

Tim Steiner, CEO

©2020 Ocado Group plc. All rights reserved.

5

10

Duncan Tatton-BrownCFO

Financial Review

©2020 Ocado Group plc. All rights reserved.

6

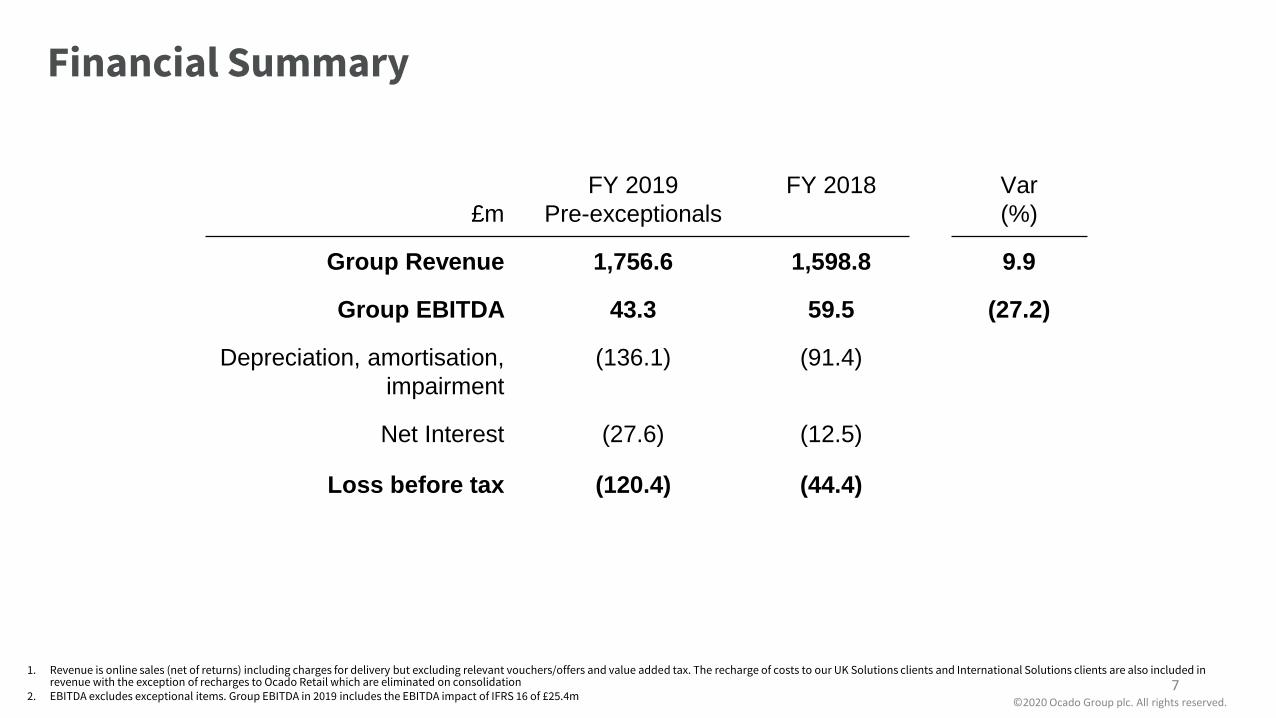

1. Revenue is online sales (net of returns) including charges for delivery but excluding relevant vouchers/offers and value added tax. The recharge of costs to our UK Solutions clients and International Solutions clients are also included in revenue with the exception of recharges to Ocado Retail which are eliminated on consolidation

2. EBITDA excludes exceptional items. Group EBITDA in 2019 includes the EBITDA impact of IFRS 16 of £25.4m

Financial Summary

£m

FY 2019

Pre-exceptionals

FY 2018 Var

(%)

Group Revenue 1,756.6 1,598.8 9.9

Group EBITDA 43.3 59.5 (27.2)

Depreciation, amortisation,

impairment

(136.1) (91.4)

Net Interest (27.6) (12.5)

Loss before tax (120.4) (44.4)

©2020 Ocado Group plc. All rights reserved.

7

Reviewing exceptionals impact

£m

Exceptionals

Impact

Loss before tax pre exceptionals FY 2019 (120.4)

Andover CFC (111.8)

Insurance reimbursement 23.8

Disposal of Fabled (1.1)

Joint Venture with M&S (3.4)

Litigation costs (1.3)

Other (0.3)

Loss before tax post exceptionals FY 2019 (214.5)

©2020 Ocado Group plc. All rights reserved.

● Write off of Andover CFC tangible assets, inventory and additional operating costs

● Insurance income recognised out of £74m received in the period

● proceedings against T0day and others for IP theft

8

Segmental Summary

1. Group totals include eliminations2. EBITDA excludes exceptional items and excludes the impact of IFRS 16

©2020 Ocado Group plc. All rights reserved.

Revenue1 EBITDA2

£m

FY 2019 FY 2018Var

%

FY 2019

Post

IFRS16

FY 2019

Pre

IFRS16

FY 2018 Var

%

Pre

IFRS16

Retail 1,617.5 1,466.6 10.3 35.0 20.2 30.1 (33.0)

UK Solutions &

Logistics

583.2 541.1 7.8 84.8 74.2 67.5 10.0

International Solutions 0.5 0.5 - (62.1) (62.1) (28.4) -

Other 9.8 9.2 6.5 (14.4) (14.4) (9.7) -

Total 1,756.6 1,598.8 9.9 43.3 17.9 59.5 (69.9)

9

Cash fees show progress building International Solutions

FY 2019 FY 2018Var

%

Revenue 0.5 0.5 -

EBITDA (62.1) (28.4) -

Fees invoiced 81.4 58.8 38.4

● Fees invoiced from international partners up significantly

● Immaterial revenue recognised under IFRS 15

● Cumulative unrecognised cash fees of around £140m of by end of 2019

● Significant growth in costs to support client requirements

©2020 Ocado Group plc. All rights reserved.

10

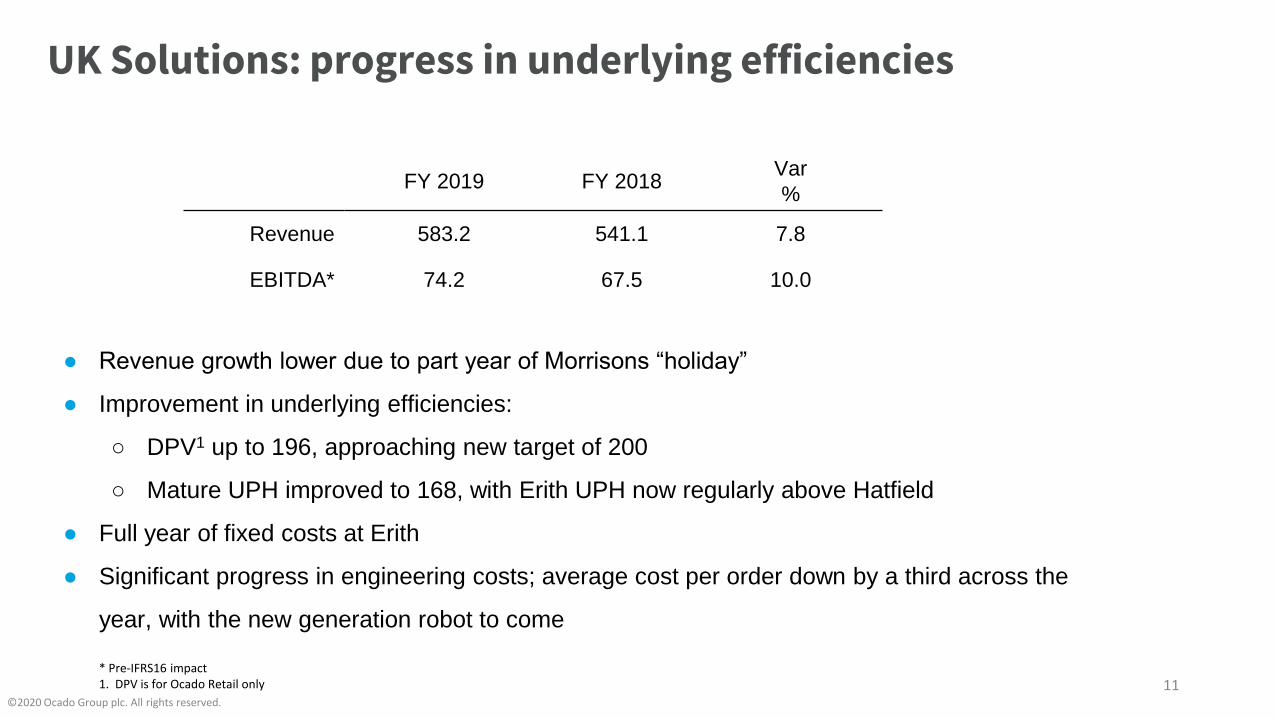

UK Solutions: progress in underlying efficiencies

©2020 Ocado Group plc. All rights reserved.

FY 2019 FY 2018Var

%

Revenue 583.2 541.1 7.8

EBITDA* 74.2 67.5 10.0

● Revenue growth lower due to part year of Morrisons “holiday”

● Improvement in underlying efficiencies:

○ DPV1 up to 196, approaching new target of 200

○ Mature UPH improved to 168, with Erith UPH now regularly above Hatfield

● Full year of fixed costs at Erith

● Significant progress in engineering costs; average cost per order down by a third across the

year, with the new generation robot to come

11* Pre-IFRS16 impact1. DPV is for Ocado Retail only

Ocado Retail: growth to bring improving efficiencies

©2020 Ocado Group plc. All rights reserved.12

10.3% growth in active

customers drives order volumes

With growth in orders coming

through new generation facilitiesWhich will drive material CFC

efficiency increases (UPH) at scale

+10.7%

growth in

big basket

order

volumes

Erith >70k OPW

Robotic

picking to

bring

efficiency

gains

beyond this

target

2018 2019 2018 2019 2019

Mature CFCs

Erith target

at maturity

721k

795k

294k

325k

Mature CFCs

Erith CFC

Andover CFC

168

200+

Note: Chart detailing order volumes growth is shown on a full year basis. The Andover fire occurred 6th February 2019. As a result, some of the capacity growth achieved in 2019 occurred before this date

Wastage: technology drives continuous operational improvement

©2020 Ocado Group plc. All rights reserved.

Industry

average range

2018

Ocado Retail

2019

Ocado Retail

2.0-3.0%

0.8%

0.4%

Wastage1 is a huge operational

challenge for the grocery industry

Hurdles

ForecastingInventory supply

Customer demand

Inventory

managementImperfect FIFO

Storage

Incorrect method

or extended time

OSP enables market

leading performance...

unprecedented accuracy,

efficiency and resilience

Scale

Better predictive capabilities

Perfect FIFO system

Strong visibility of customer

behaviour

...and is still improving

impact of:

Improved AI and ML

driven forecasting

1. Food items not sold as a % of sales Food that goes to landfill is only 0.02% of sales13

20191,2

(% Retail

Revenue)

20181,2

(% Retail

Revenue)

Var

(%)

Gross margin 32.9 33.0 (0.1)

Trunking and delivery costs (12.2) (12.4) 0.2

CFC costs (8.9) (8.4) (0.5)

Other operating costs (0.6) (0.7) (0.0)

Marketing costs (1.3) (0.9) (0.4)

Fees (5.1) (5.0) (0.1)

Operating contribution 4.8 5.6 (0.8)

Admin costs (3.5) (3.5) 0.0

EBITDA 1.3 2.1 (0.8)

1. Excluding exceptionals and pre-IFRS16.2. The costs of Ocado Retail’s operation in 2018, and in 2019 prior to the formation of the joint venture with M&S, have been allocated between the Retail Segment and UK & Logistics segment in order to be broadly comparable to the current contractual arrangements now in place

Ocado Retail performance

©2020 Ocado Group plc. All rights reserved.

14

Continued underlying progress,

fixed costs of Erith

Increased marketing costs following

Andover fire and with offline trial

Fees paid to Ocado Group for the

OSP and logistics solutions to

operate online offer

P&L20191,2

(% Retail Revenue) Consideration v. client P&L

Gross margin 32.9 Includes Waitrose sourcing fee and without scale advantages

Trunking and delivery costs (12.2)

CFC costs (8.9) Lower efficiency due to legacy assets

Other operating costs (0.6)

Marketing costs (1.3) Includes impact of Andover fire and without benefit of existing brand

Fees (5.1) Includes 3PL fees but lower OSP fee reflecting lower efficiency assets

Operating contribution 4.8

Admin costs (3.5) Higher admin fees due to set up and smaller scale

EBITDA 1.3

1. Excluding exceptionals2. The costs of Ocado Retail’s operation in 2019 prior to the formation of the joint venture with M&S, have been allocated between the Retail Segment and UK & Logistics segment in order to be broadly comparable to the current contractual arrangements now in place.

Ocado Retail: considerations versus other partners

©2020 Ocado Group plc. All rights reserved.

Client business with higher EBITDA margin at scale and low capital costs

15

16

Group net cash flow development

©2020 Ocado Group plc. All rights reserved.

16

411

751

43

50

74

(80)

(36)

558

60

(260)

(65)

FY18 Cash position

EBITDA

Working Capital

Insurance proceeds

GIP settlement

Finance costs + other

M&S deal proceeds

Share sales

Capex1

Other

FY19 Cash position

Proceeds from

M&S deal and

convertible

support strong

funding position

for future

growth

● proceeds received to date

● GIP cash settlement offset in

part by share sales

● Majority finance costs including

interest element of IFRS 16

● £600m convertible bond

issuance post year end1351

Capex split1

UK

CFCs

Int.

CFCs

Platform

Dev

Other

47

71

104

38

Strong operating

cash flow offset

by settlement

of GIP

(4)

Finance obligations

£m

1. Variance is the difference between accrued capital expenditure and cash capital expenditure

Outlook for 2020

● Revenue growth:

○ Retail 10‐15%

○ UK Solutions & Logistics below Retail reflecting full year impact of Morrisons’

“holiday” from Erith

○ International Solutions expected to be <£10m

■ International fees start to be recognised once operations commence

■ part year operations for Casino and Sobeys

● International Solutions fees invoiced > 40% growth

©2020 Ocado Group plc. All rights reserved.

17

Outlook for 2020 (continued)

● EBITDA:

○ Retail above revenue growth, reflecting improved operating margins as Erith scales

○ UK Solutions and Logistics to decline due to Morrisons’ “holiday” from Erith, with insurance

benefits recorded in exceptionals

○ International solutions to decline due to continued investment in build of the business and

increased support costs with launch of initial CFCs

● Continued insurance receipts

○ Partly funds UK CFCs

○ Both rebuild and business interruption recognised as exceptional income

● Capex forecast £600m

○ International CFCs - £225m

○ UK CFCs - £225m; Andover (c.40% of total) to be funded from insurance proceeds

○ Development and other - £150m

©2020 Ocado Group plc. All rights reserved.

18

10

Duncan Tatton-BrownCFO

Financial Review

©2020 Ocado Group plc. All rights reserved.

19

Tim SteinerCEO

©2020 Ocado Group plc. All rights reserved.

Building for tomorrow, at pace

Propose this picture as something

simulation related - visual way to remind

people of the importance of the software

element of the platform

Groupe Casino: Fleury-Mérogis, France

Sobeys: Vaughan, Ontario, Canada

20

Four key elements to the Ocado story in 2020

1. Developing the Ocado Smart Platform

2. Managing greater velocity in the business

3. Enhancing the customer experience at Ocado Retail

4. Creating the future, today: transformative innovation in the pipeline

©2019 Ocado Group plc. All rights reserved.

21

1 OSP: reliably providing the best customer outcomes...

©2030 Ocado Group plc. All rights reserved.

A market leading customer offer

Range

58,000 SKUs

8 products1 in

average basket

only at Ocado

Service

95% of orders

delivered on time

99% order accuracy

Ease of Use

Order through app,

website, and on

chosen device

Always improving

Price

Flexibility to price our

range so that we

offer the most value

for customers

221. Meaning any third party branded product that cannot be found elsewhere, including entire brands or different versions of a given product

1 ...while producing the best economics

©2030 Ocado Group plc. All rights reserved.

Centralised fulfilment has

fundamental characteristics

That drive economic

benefits

Typical micro

fulfilment centre

Leveraged in

our Zoom model

1. Large scale, centralised

operations

Margin benefit (long tail)

Improved

efficiencies

Inbound

Picking

Waste

2. Reduced supply chain Minimal supply chain cost

3. Use of own, purpose-built

technology and IP

Flexibility to pursue iterative

and step change innovation

Operating cost result Best in channel Materially higher Slightly higher

23

?

Operating click & collect is

not ‘free’ for a retailer3

● A store can service a limited amount of online sales

● Needs staff to operate; more required as scales

● We estimate click and collect could cost 3-4%

of sales to operate

Trunking is a small part

of delivery expense2

● The theoretical ‘gain’ to be made from closer start

location to customer

● Trunking costs 1.2% of sales for Ocado Retail

Scaled, centralised

planning drives benefits1

1 The last mile

©2030 Ocado Group plc. All rights reserved.

The benefit of proximity alone is minimal in the context of the operational benefits of the CFC model

24

● Strategic spoke network enables improved last mile

efficiency, including disbenefit of longer stem time

● We estimate that central planning brings an

operating benefit of around 0.5% of sales

Key Module Primary mission size(sq ft)

1Standard

CFCFull basket shop; large direct

and spoked catchment200k+

2MiniCFC

Full grocery shop; shorter lead times or to connect lower density areas to network

50-160k

3 MFC Immediacy 5-25k

4Store pick software

Best fulfilment in remote areas n/a

1 The OSP ecosystem

©2030 Ocado Group plc. All rights reserved.

OSP has the flexibility to develop bespoke networks to serve the unique needs of each market

12

3

4

An illustrative example

immediacy

same day

next day

Work underway to leverage the

ecosystem to reduce cost even further

2

25

1 Ocado Zoom: next steps in immediacy

©2020 Ocado Group plc. All rights reserved.

Working on plans for second site

FY19

The consumer trial

Future

Roll out with OSP

Validated real market opportunity in immediacy

Increased confidence we can deliver the best

offer and economics

Proving the model

Ongoing

Install our solution

Focus on operational efficiencies e.g. waste

Explore options to further optimise technology

Micro fulfilment solution to serve

immediacy missions in markets globally

Continue to evolve

26

1 Exploring the benefits of being a ‘member of the club’

©2030 Ocado Group plc. All rights reserved.

3. Global view

of consumer trends to keep

ahead of peers in local markets

1. Increased innovation

as Ocado Group scales,

with increased resources

and footprint

4. Future optionality

2. Share learnings

Quarterly meetings to discuss

build, launch and scaling in

home markets

A collaborative and future-focused network for forward-looking retailers

27

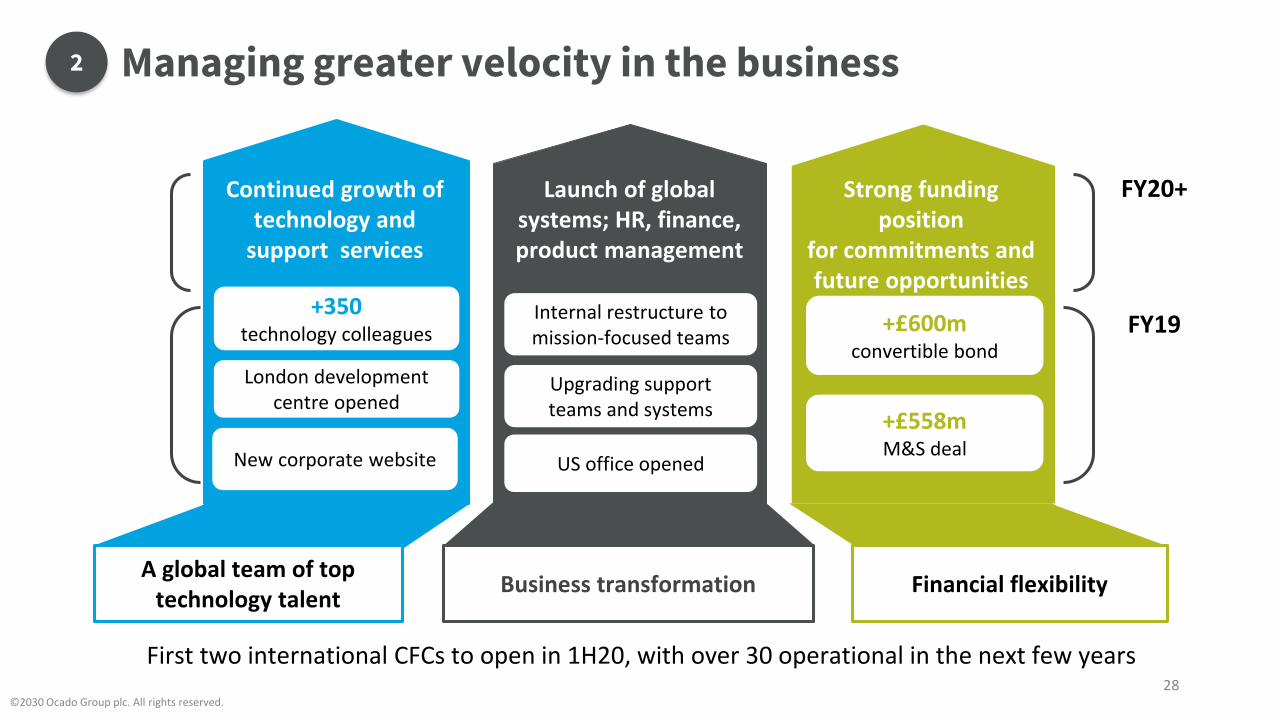

2 Managing greater velocity in the business

©2030 Ocado Group plc. All rights reserved.

First two international CFCs to open in 1H20, with over 30 operational in the next few years

A global team of top technology talent

Business transformation Financial flexibility

+£558mM&S deal

+£600mconvertible bond

US office opened

Upgrading support teams and systems

Internal restructure to mission-focused teams

Launch of global systems; HR, finance, product management

Strong funding position

for commitments and future opportunities

London development centre opened

+350technology colleagues

New corporate website

Continued growth of technology and

support services

FY19

FY20+

28

2 First CFCs opening - creating a template for execution

Enabling our partners to grow on their own terms, in and across markets

Pre-launchPreparation

responsibilities

Launch and GrowthGo-live and ramp according to

each partner’s strategic plan

Partner

SoftwareDevelopment and testing

HardwareInstallation and testing

PeopleRecruit and train

(PMs, engineers)

PeopleRecruit and train

(drivers, CFC staff)

Complete site

Roll out and drive propositionphasing, marketing, pricing, range

Project management Relationship management

assist on early execution share feedback, refine, grow

----------------------------

Support: online retail expertise, technical service24/7 on the ground and remote

Collaboration and innovationLeveraging shared learnings for all current and future sites

29

1.Develop

commercial and

marketing abilities

2.strengthening GM

1. Food innovation with

sourcing at scale

2. Working on

integrated CRM

1.Leading fulfilment operations with

continuous technology upgrades

2.New, profitable, immediacy and same

day models

3 Enhancing the customer experience at Ocado Retail

©2030 Ocado Group plc. All rights reserved.

Preparing for faster growth after near term capacity constraints ease

And together, we will improve

the customer offer even further

Creating new

opportunities

More data and

insights to act on

Unparalleled offer

More missions

served

To grow faster

Current

geographies

and missions

New geographies

New missions

We are well

placed to lead

Fastest growing

grocer in UK

Award-winning

proposition

30

4 Creating the future, today

©2030 Ocado Group plc. All rights reserved.

Parallel streams of innovation creating future value for the medium to long term

Pursuing constant

innovation

In the CoreFurther increasing the

competitive advantage that

OSP drives in grocery

VenturesA growing portfolio, leveraging

our technological know-how

and participating in innovation

in other adjacencies

Vertical farming

Automated

meal prep

3D printing

Robotic picking

● picking is c.50% of

CFC labour cost

● Aspire to equal

performance of

human for portion of

the range by FY20

31

Conclusions

©2020 Ocado Group plc. All rights reserved.

● OSP is a flexible model, with leading economics, that will help our partners

to win in online grocery across all missions and markets

● The model is always evolving and improving

● We are ready to work at even higher velocity

● Ocado Retail is poised for even faster growth in the UK

● We are innovating to drive future value, in grocery and beyond

32

Q&A

©2020 Ocado Group plc. All rights reserved.

33

Appendix

34

Cash Position

2019 (£m)

Cash and cash equivalents FY18 411

Net cash flow (218)

Proceeds from creation of JV with M&S 558

Cash and cash equivalents 751

Existing undrawn RCF 100

Total headroom 851

>£1.4bn in total headroom inclusive of £600m convertible bond issued after year end

©2020 Ocado Group plc. All rights reserved.

35

Capital expenditure1

FY 2019 (£m) FY 2018 (£m)

Mature CFCs 5 6

New CFCs 42 80

International CFCs 71 11

Delivery 17 22

Technology development 71 55

Fulfilment development 33 21

Other 21 18

Total 260 213

1. Capex excludes assets leased from MHE JV Co under finance lease arrangements

©2020 Ocado Group plc. All rights reserved.

36

Impact of IFRS 16 on FY19

©2020 Ocado Group plc. All rights reserved.

37

IFRS 16 Impact FY 2019 (£m)

Ocado Retail 14.8

UK Solutions & Logistics 10.6

International Solutions -

Other -

EBITDA 25.4

Depreciation, amortisation and impairment (19.8)

Net Finance Costs (14.9)

Total (9.3)