Embed Size (px)

Citation preview

Obour Land For Food Industries

Investor Presentation

August 2019

2

Table of Contents

I. Overview of the Market

II. Obour Land’s Strategy

III. 1H2019 Financial Performance

3

Disclaimer

This presentation and any materials distributed in connection with this presentation are not directed or intended for distribution to or use by, any person or entity that is a citizen or resident located

in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to the law or regulation of that jurisdiction or which would require any

registration or licensing within such jurisdiction. Persons who come into possession of any document or other information referred to herein should inform themselves about and observe any such

restrictions. Any failure to comply with these restrictions may constitute a violation of the securities laws of such jurisdictions.

This presentation includes forward-looking statements that reflect management’s current views with respect to future events and financial and operational performance. These statements contain

the words “anticipate”, “believe”, “intend”, “estimate”, “expect”, “may”, “plan”, “should”, “could”, “aim”, “target”, “might” and words of similar meaning. All statements other than statements of historical

facts included in this presentation, including, without limitation, those regarding the Company’s financial position, business strategy, plans and objectives of management for future operations are

forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or

achievements of the Company to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. The forward-looking statements

are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company will operate in the future. They speak only as at

the date of this presentation, and actual results or performance may differ materially from those expressed or implied from the forward-looking statements. In addition, the forward looking

statements are not intended to give any assurances as to future results and statements regarding past trends should not be taken as a representation that they will continue in the future. The

Company, the Banks and their respective advisers each expressly disclaim any obligation or undertaking to disseminate any updates or revisions to any forward looking statements contained

herein to reflect any change in the Company’s expectations or any change in the events, conditions or circumstances on which any such statement is based, unless otherwise required by law. The

Company does not undertake to review, confirm or release publicly or otherwise to investors or any other person any revisions to any forward-looking statements to reflect events occurring or

circumstances arising after the date of this presentation.

This presentation contains non-EAS measures (such as EBITDA). These measures have limitations as analytical tools and should not be consideration in isolation or as substitutes for analysis of

the Company’s results as reported under EAS.

This presentation, and any matter or dispute (whether contractual or non-contractual) arising out of it, shall be governed and construed in accordance with Egyptian law and the Courts of Cairo shall

have exclusive jurisdiction in relation to any such matter or dispute.

By attending this presentation and/or receiving this presentation document, you are agreeing to the terms and conditions set forth above.

I. Overview of the Market

5

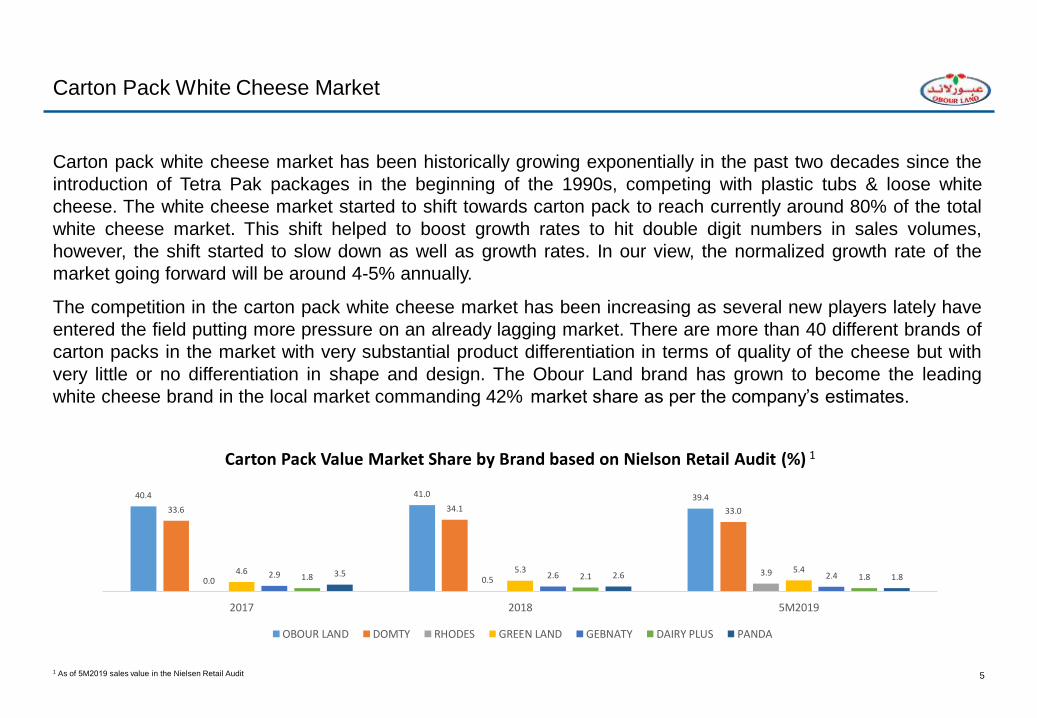

Carton Pack White Cheese Market

1 As of 5M2019 sales value in the Nielsen Retail Audit

Carton pack white cheese market has been historically growing exponentially in the past two decades since the

introduction of Tetra Pak packages in the beginning of the 1990s, competing with plastic tubs & loose white

cheese. The white cheese market started to shift towards carton pack to reach currently around 80% of the total

white cheese market. This shift helped to boost growth rates to hit double digit numbers in sales volumes,

however, the shift started to slow down as well as growth rates. In our view, the normalized growth rate of the

market going forward will be around 4-5% annually.

The competition in the carton pack white cheese market has been increasing as several new players lately have

entered the field putting more pressure on an already lagging market. There are more than 40 different brands of

carton packs in the market with very substantial product differentiation in terms of quality of the cheese but with

very little or no differentiation in shape and design. The Obour Land brand has grown to become the leading

white cheese brand in the local market commanding 42% market share as per the company’s estimates.

40.4 41.0 39.4

33.6 34.1 33.0

0.0 0.53.94.6 5.3 5.4

2.9 2.6 2.41.8 2.1 1.83.5 2.6 1.8

2017 2018 5M2019

Carton Pack Value Market Share by Brand based on Nielson Retail Audit (%) 1

OBOUR LAND DOMTY RHODES GREEN LAND GEBNATY DAIRY PLUS PANDA

6

Milk & Juice Markets

1 As of 5M2019 sales value in the Nielsen Retail Audit

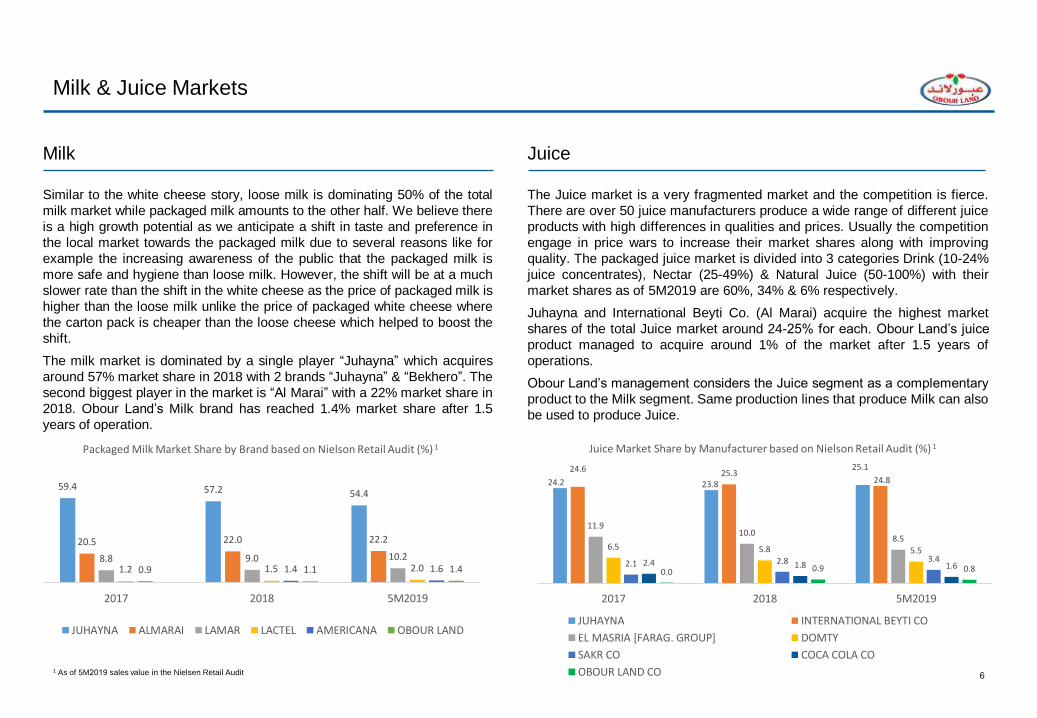

Milk

Similar to the white cheese story, loose milk is dominating 50% of the total

milk market while packaged milk amounts to the other half. We believe there

is a high growth potential as we anticipate a shift in taste and preference in

the local market towards the packaged milk due to several reasons like for

example the increasing awareness of the public that the packaged milk is

more safe and hygiene than loose milk. However, the shift will be at a much

slower rate than the shift in the white cheese as the price of packaged milk is

higher than the loose milk unlike the price of packaged white cheese where

the carton pack is cheaper than the loose cheese which helped to boost the

shift.

The milk market is dominated by a single player “Juhayna” which acquires

around 57% market share in 2018 with 2 brands “Juhayna” & “Bekhero”. The

second biggest player in the market is “Al Marai” with a 22% market share in

2018. Obour Land’s Milk brand has reached 1.4% market share after 1.5

years of operation.

Juice

The Juice market is a very fragmented market and the competition is fierce.

There are over 50 juice manufacturers produce a wide range of different juice

products with high differences in qualities and prices. Usually the competition

engage in price wars to increase their market shares along with improving

quality. The packaged juice market is divided into 3 categories Drink (10-24%

juice concentrates), Nectar (25-49%) & Natural Juice (50-100%) with their

market shares as of 5M2019 are 60%, 34% & 6% respectively.

Juhayna and International Beyti Co. (Al Marai) acquire the highest market

shares of the total Juice market around 24-25% for each. Obour Land’s juice

product managed to acquire around 1% of the market after 1.5 years of

operations.

Obour Land’s management considers the Juice segment as a complementary

product to the Milk segment. Same production lines that produce Milk can also

be used to produce Juice.

59.4 57.2 54.4

20.5 22.0 22.2

8.8 9.0 10.21.2 1.5 2.00.9 1.4 1.61.1 1.4

2017 2018 5M2019

Packaged Milk Market Share by Brand based on Nielson Retail Audit (%) 1

JUHAYNA ALMARAI LAMAR LACTEL AMERICANA OBOUR LAND

24.2 23.8

25.124.6 25.324.8

11.910.0

8.56.5 5.8 5.5

2.1 2.8 3.42.4 1.8 1.60.0 0.9 0.8

2017 2018 5M2019

Juice Market Share by Manufacturer based on Nielson Retail Audit (%) 1

JUHAYNA INTERNATIONAL BEYTI CO

EL MASRIA [FARAG. GROUP] DOMTY

SAKR CO COCA COLA CO

OBOUR LAND CO

II. Obour Land Strategy

8

White Cheese Strategy

Obour Land’s management is focusing on preserving the company’s leading place as the largest white cheese

producer in Egypt and to keep the gap between Obour Land and other competitors.

The company plans to keep developing its cheese products furthermore by investing in innovation and updating

its production lines to produce a more attractive product while improving the company’s cost efficiency. The

company is planning to replace old production lines with the latest advanced technologies in the white cheese

manufacturing industry to increase efficiency and productivity at lower costs as it will reduce the use of energy by

40%.

The new production lines’ output will have a new shape and design which will differentiate Obour Land’s brand

from all other brands in the market. The new production lines will be more environment-friendly as it will save

energy and produce more packs per hour while using less labor. The systematic improvement in reducing the

environmental impacts is a part of Obour Land’s efforts to improve its society and contributing towards a

sustainable development.

9

Milk & Juice Strategy

The company’s strategy in penetrating a new market is to achieve the utmost customer satisfaction by providing

a product with the highest quality levels consistently. Since commencing the production of Milk & juice, Obour

Land’s main focus is to achieve a premium quality product that can compete with top quality brands in the

market. The company launched its new products in December 2017 and starting testing the feedback of the

market in the first 3 months of operation to ensure that it will satisfy customers’ needs. The feedback was very

positive especially for the Milk product and the results were very promising.

Obour Land aims to acquire a decent market share based on customer preferences rather than discounted prices

therefore the company does not engage in price wars or offers big discounts as a way to penetrate a new market.

The management believes that this strategy will lead to having a more stable and long-term market share that

will be loyal to the brand similar to the company’s White Cheese success story and by using the same applied

sales policies.

The company’s cash payment policies for retails and wholesalers as well as other policies implemented in the

white cheese segment are factors that can slow the growth of Obour Land’s market share in Milk & Juice.

Wholesalers will not be tempted to purchase the new products in the beginning with the same policies applied in

the white cheese, where Obour Land is the market leader. However, the management believes that by reaching

out to small & large grocery shops directly by the company’s retail distribution vehicles and based on the

product’s premium quality, demand will be created in the market and wholesalers will eventually purchase the

new products while adhering to the company’s policies.

10

Processed Cheese

The company started the production of Processed Cheese in March 2018 and had

plans also to introduce a Mozzarella Cheese product. However, after monitoring and

testing both markets the management decided to cancel the Mozzarella product and

sell the production line to have more room in the factory to develop the Processed

Cheese products and to explore new ideas and innovations to expand the market

furthermore by introducing an innovative new product.

III. Financial Results 1H 2019

12

Financial Performance

Key Investment Highlights

High Quality Product Mix

Supply Chain and Sales Network

Revenues & COGS Build-Up

Financial Statements

1

2

3

4

5

13

High Quality Product Mix

Product Portfolio Synopsis

Brand

Product Family

Launch Date

SKUs

Production Capacity

(TPA)

1H2019 Utilization Rate

1H2019 Contribution to

Sales

1

Product Portfolio

Plastic

Tub2

Carton Pack180gm

Carton

Pack

2015

1

4,320

27%

1.2%

125gm

Carton

Pack

2011

4

23,625

61%

15.6%

250gm

Carton

Pack

2007

4

72,000

75%

54.5%

500gm

Carton

Pack

2007

7

54,000

45%

24.5%

Plastic

Tub

1999

24

4,130

55%

2.7%

80g Feta 125g Feta 125g Olive 125g

Istanbully

250g Olive250g Feta 250g

Istanbully

500g Olive 500g

Istanbully500g Feta

1kg Khazeen 1kg

Istanbully

1kg Feta

1kg

Double

Cream

1kg

Barameely1kg Istanbully

Vegetable

Fat

Natural

Fat

1kg

Talaga

Source: Company1Other Carton Pack SKUs include 1 Kg Istanbully, 1 Kg Olive, 1 Kg Chili, 500gm Feta slim, 500gm Olive slim, 500gm Chili slim, 500gm Istanbully slim, 250gm Chili slim, 125gmChili slim2 Other plastic tubs SKUs include 400gm Istanbully, 400gm Feta, 400gm Khazeen, 400gm Talaga, 400gm Istanbully Full Cream, 400gm Double Cream, 400gm Barameely, 1.5kg Feta Pepper, 11kg Feta and 12kg Low Salt3 Other Milk & Juice SKUs include 250ml Juice (Mango, Guava, Apple, Pineapple, Orange) 1litre Juice(Cocktail, Guava, Apple, Pineapple, Orange) and 500ml Milk

1 Kg

Carton

Pack

2017

4

36,000

4%

1.5%

1 Kg Feta

Milk & Juice3

Processed Cheese

1 Liter

Milk

&Juice

2018

3

42,000

18%

3.4%

250ml

Juice

2018

12

36,000

9%

1.3%

14

Sales Breakdown by Channel

Obour Land’s

distribution network is

helping the company to

control its products

prices while applying its

sales policies and

reducing SG&A

expenses.

The company is

planning to increase its

exports by focusing

more on exporting

Juice.

The Company grew its

fleet 22% CAGR in

2014-2018, however,

the number of fleet

decreased in 1H2019 to

reach 418 vehicles as

the company sold some

of the old vehicles to

replace with new

vehicles to reduce

running costs.

Source: Company

Supply Chain and Sales Network2

SharkiaMenoufia

Kafr El SheikhBeheira

Dakahlia

Qalyubia

Robust Distribution Platform

Indirect Distribution Wholesalers

North Sinai

Suez

Distribution Centers and Distribution Wholesalers

# Fleet

▲22%

Maximum Handling

Capacity (Tons/Day)

▲22%

60%66%

72%67% 70% 69%

37%29%

26%31% 27% 28%

3% 5% 2% 2% 3% 2%

0.14% 0.45% 0.18% 0.35%

2014 2015 2016 2017 2018 1H2019

Wholesalers Retailers Key Accounts Exports

191 201 201

345

423 418

90

14 0

19 0

24 0

29 0

34 0

39 0

44 0

2014 2015 2016 2017 2018 1H 2019

2014-2018 CAGR%

555 605

804

1018

1248 1233

25 0

45 0

65 0

85 0

10 50

12 50

14 50

2014 2015 2016 2017 2018 1H2019

15

Financial Performance

Net Revenues1 (EGP mn)

3

Gross Profit2, Margin (EGP mn, %) EBITDA, Margin (EGP mn, %)

Net Income, Margin (EGP mn, %) Net Cash3 (Net Debt) Cash Conversion Cycle (Days)

1 Net revenues are net of discounts2 Gross profit excludes depreciation expense included in the cost of sales3 Debt obligations include credit facilities, liabilities for the purchase of machinery and dividends payable

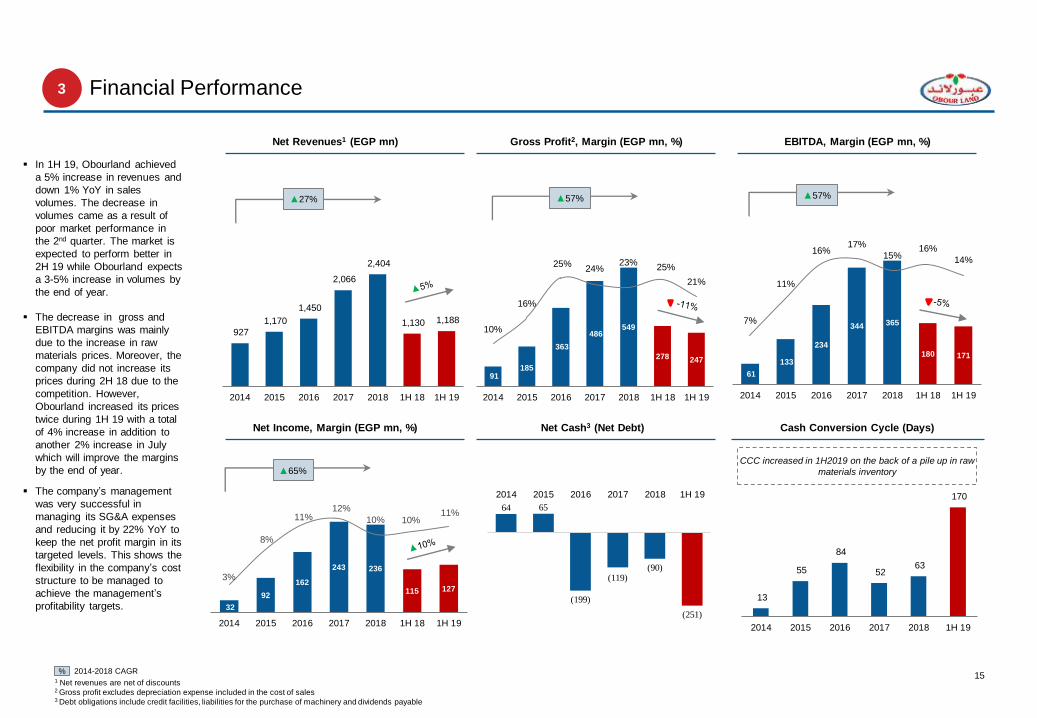

In 1H 19, Obourland achieved

a 5% increase in revenues and

down 1% YoY in sales

volumes. The decrease in

volumes came as a result of

poor market performance in

the 2nd quarter. The market is

expected to perform better in

2H 19 while Obourland expects

a 3-5% increase in volumes by

the end of year.

The decrease in gross and

EBITDA margins was mainly

due to the increase in raw

materials prices. Moreover, the

company did not increase its

prices during 2H 18 due to the

competition. However,

Obourland increased its prices

twice during 1H 19 with a total

of 4% increase in addition to

another 2% increase in July

which will improve the margins

by the end of year.

The company’s management

was very successful in

managing its SG&A expenses

and reducing it by 22% YoY to

keep the net profit margin in its

targeted levels. This shows the

flexibility in the company’s cost

structure to be managed to

achieve the management’s

profitability targets.

2014-2018 CAGR%

CCC increased in 1H2019 on the back of a pile up in raw

materials inventory

▲27% ▲57% ▲57%

▲65%

927

1,170

1,450

2,066

2,404

1,130 1,188

-

50 0

1, 000

1, 500

2, 000

2, 500

3, 000

2014 2015 2016 2017 2018 1H 18 1H 19

91 185

363

486 549

278 247

10%

16%

25%24%

23%25%

21%

0%

5%

10 %

15 %

20 %

25 %

30 %

-

10 0

20 0

30 0

40 0

50 0

60 0

2014 2015 2016 2017 2018 1H 18 1H 19

61

133

234

344 365

180 171

7%

11%

16%17%

15%16%

14%

0%

2%

4%

6%

8%

10 %

12 %

14 %

16 %

18 %

-

50

10 0

15 0

20 0

25 0

30 0

35 0

40 0

2014 2015 2016 2017 2018 1H 18 1H 19

32

92

162

243 236

115 127

3%

8%

11%12%

10% 10%11%

0%

2%

4%

6%

8%

10 %

12 %

14 %

0

50

10 0

15 0

20 0

25 0

30 0

2014 2015 2016 2017 2018 1H 18 1H 19

64 65

(199)

(119)(90)

(251)

2014 2015 2016 2017 2018 1H 19

13

55

84

52 63

170

-

20

40

60

80

10 0

12 0

14 0

16 0

18 0

2014 2015 2016 2017 2018 1H 19

16

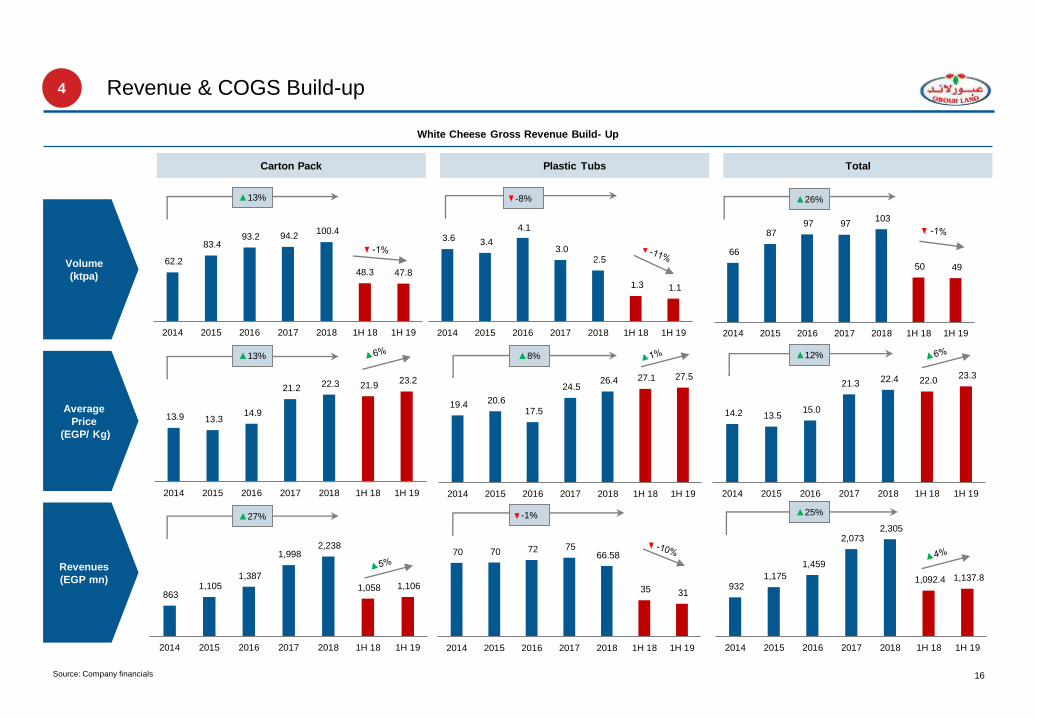

Revenue & COGS Build-up

White Cheese Gross Revenue Build- Up

Source: Company financials

Carton Pack Plastic Tubs Total

Volume

(ktpa)

Average

Price

(EGP/ Kg)

Revenues

(EGP mn)

▲13% -8% ▲26%

▲13% ▲8% ▲12%

▲27% -1% ▲25%

4

62.2

83.4 93.2 94.2

100.4

48.3 47.8

-

20 .0

40 .0

60 .0

80 .0

10 0.0

12 0.0

2014 2015 2016 2017 2018 1H 18 1H 19

3.6 3.4

4.1

3.0 2.5

1.3 1.1

2014 2015 2016 2017 2018 1H 18 1H 19

66

87 97 97

103

50 49

-

20

40

60

80

10 0

12 0

2014 2015 2016 2017 2018 1H 18 1H 19

13.9 13.3 14.9

21.2 22.3 21.9 23.2

-

5. 0

10 .0

15 .0

20 .0

25 .0

2014 2015 2016 2017 2018 1H 18 1H 19

19.4 20.6 17.5

24.5 26.4 27.1 27.5

-

5. 0

10 .0

15 .0

20 .0

25 .0

30 .0

2014 2015 2016 2017 2018 1H 18 1H 19

14.2 13.5 15.0

21.3 22.4 22.0

23.3

-

5. 0

10 .0

15 .0

20 .0

25 .0

2014 2015 2016 2017 2018 1H 18 1H 19

863 1,105

1,387

1,998 2,238

1,058 1,106

-

50 0

1, 000

1, 500

2, 000

2, 500

2014 2015 2016 2017 2018 1H 18 1H 19

70 70 72 75 66.58

35 31

-

10

20

30

40

50

60

70

80

2014 2015 2016 2017 2018 1H 18 1H 19

932 1,175

1,459

2,073 2,305

1,092.4 1,137.8

-

50 0

1, 000

1, 500

2, 000

2, 500

2014 2015 2016 2017 2018 1H 18 1H 19

17

Raw materials costs represent

the biggest portion of COGS,

contributing ~60% to sales in

1H 19 compared to 56% in 1H

18 due to the increase of raw

materials prices.

Others raw materials increased

significantly starting from 2018

due to the introduction of the

company’s new products Milk &

Juice. Others include raw milk,

juice concentrates, sugar &

other raw materials.

COGS Build-up

COGS Breakdown (EGP mn)

Gross Profit2, Margin (EGP mn, %)

Raw Materials Breakdown (EGP mn)Cost of Sales Breakdown (EGP mn)1

Source: Company financials1 Cost of sales excludes depreciation expense2 Gross profit excludes depreciation expense included in the cost of sales

91 185

363 486 549

278 247

10%

16%

25% 24%23%

25%21%

0%

5%

10 %

15 %

20 %

25 %

30 %

-

10 0

20 0

30 0

40 0

50 0

60 0

2014 2015 2016 2017 2018 1H 18 1H 19

716813 852

1211

1,400

636711

106

150168

295

352

162170

19

23 68

95

106

46

58

(5) (1) (0)(21)

(3)

8

2

2014 2015 2016 2017 2018 1H 18 1H 19

Raw Materials Packaging Industrial Expenses Change in Inventory

397 417 418 573568 266 298

80110 149

133

147 49 70

101 173 175336

329 132

151

30 29 36 50

72 32

38

107 85 74 119 283 158 154

2014 2015 2016 2017 2018 1H 18 1H 19

SMP & Milk Protein Concentrate Butter Oils GDL Others

18

Financial Statements – Income Statement

Source: Company Financial Statements1 Excludes depreciation expense2 The provisions for expected claims are related to the Company’s expected tax claims

5

EGP 2014 2015 2016 2017 2018 1H2018 1H2019

Revenues 926,979,665 1,169,837,613 1,450,122,574 2,065,516,703 2,403,541,039 1,129,578,266 1,187,567,544

Export Rebates - - - 558273

Cost of sales1 -835,651,737 -985,062,271 -1,087,501,189 -1,579,642,506 -1,854,824,403 -851,651,807 -940,371,584

Gross Profit 91,327,928 184,775,342 362,621,385 486,432,470 548,716,636 277,926,459 247,195,960

Gross Profit Margin 10% 16% 25% 24% 23% 24.6% 20.8%

Selling and marketing expense1 -26,702,550 -46,645,944 -117,932,531 -122,045,740 -156,462,756 -88,655,473 -62,853,571

General and administrative expense1 -3,945,846 -4,674,091 -10,847,153 -20,079,451 -27,607,376 -9,250,924 -13,089,457

EBITDA 60,679,532 133,455,307 233,841,701 344,307,279 364,646,504 180,020,062 171,252,932

EBITDA Margin 7% 11% 16% 17% 15% 15.9% 14.4%

Depreciation -8,042,793 -10,044,891 -13,301,946 -18,445,255 -37,802,074 -17,777,317 -21,599,818

EBIT 52,636,739 123,410,416 220,539,755 325,862,024 326,844,430 162,242,745 149,653,114

EBIT Margin 6% 11% 15% 16% 14% 14.4% 12.6%

Other income (loss) 201,794 2,522,059 2,109,459 579,535 3,830,747 2,018,664 1,077,841

Provision for expected claims2 -6,028,106 -5,730,770 -2,356,796

(Loss) gain from disposal of fixed assets 198,825 -51,050 287,206 5,101 1,549,569

Foreign exchange difference -178,319 913,605 -4,922,292 5,110,467 -830,775 -268,659 17,437,727

Net Interest Expense -733,459 -1,004,538 -5,973,933 -17,715,849 -24,374,339 -15,393,307 -4,778,207

EBT 46,097,474 120,059,722 209,683,399 313,836,177 305,470,063 148,604,544 164,940,044

Income tax -14,014,480 -28,208,203 -47,695,427 -70,639,403 -69,248,899 -33,422,558 -37,670,393

Net Profit 32,082,994 91,851,519 161,987,972 243,196,774 236,221,164 115,181,986 127,269,651

Net Profit Margin 3% 8% 11% 12% 10% 10.20% 10.72%

19

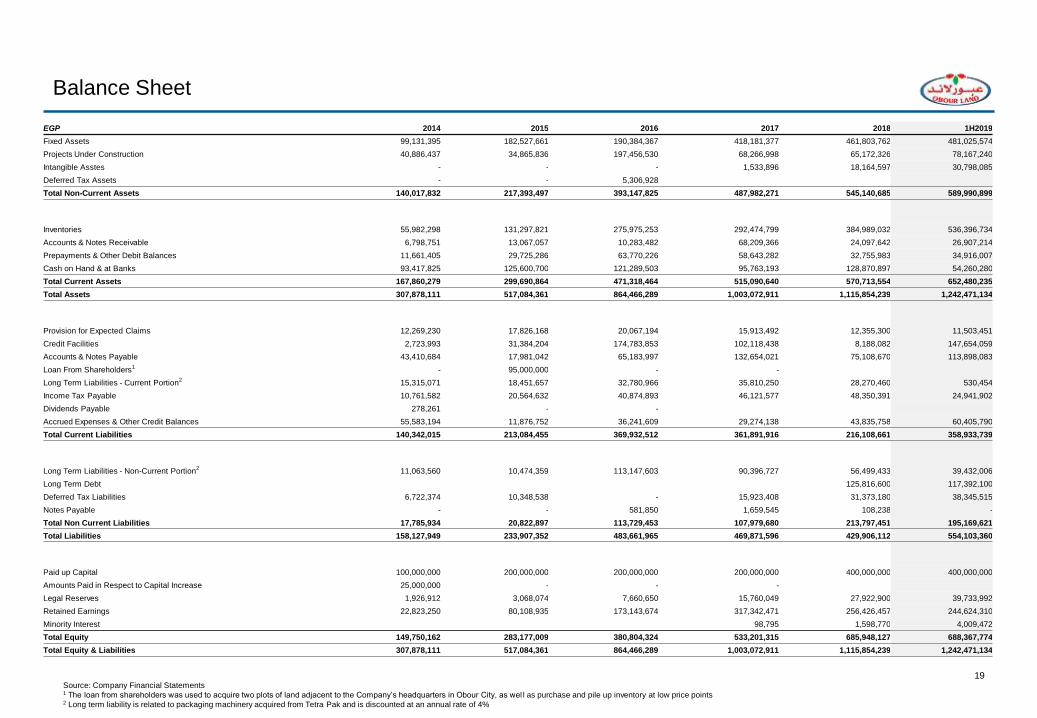

Balance Sheet

Source: Company Financial Statements1 The loan from shareholders was used to acquire two plots of land adjacent to the Company’s headquarters in Obour City, as wel l as purchase and pile up inventory at low price points2 Long term liability is related to packaging machinery acquired from Tetra Pak and is discounted at an annual rate of 4%

EGP 2014 2015 2016 2017 2018 1H2019

Fixed Assets 99,131,395 182,527,661 190,384,367 418,181,377 461,803,762 481,025,574

Projects Under Construction 40,886,437 34,865,836 197,456,530 68,266,998 65,172,326 78,167,240

Intangible Asstes - - - 1,533,896 18,164,597 30,798,085

Deferred Tax Assets - - 5,306,928

Total Non-Current Assets 140,017,832 217,393,497 393,147,825 487,982,271 545,140,685 589,990,899

Inventories 55,982,298 131,297,821 275,975,253 292,474,799 384,989,032 536,396,734

Accounts & Notes Receivable 6,798,751 13,067,057 10,283,482 68,209,366 24,097,642 26,907,214

Prepayments & Other Debit Balances 11,661,405 29,725,286 63,770,226 58,643,282 32,755,983 34,916,007

Cash on Hand & at Banks 93,417,825 125,600,700 121,289,503 95,763,193 128,870,897 54,260,280

Total Current Assets 167,860,279 299,690,864 471,318,464 515,090,640 570,713,554 652,480,235

Total Assets 307,878,111 517,084,361 864,466,289 1,003,072,911 1,115,854,239 1,242,471,134

Provision for Expected Claims 12,269,230 17,826,168 20,067,194 15,913,492 12,355,300 11,503,451

Credit Facilities 2,723,993 31,384,204 174,783,853 102,118,438 8,188,082 147,654,059

Accounts & Notes Payable 43,410,684 17,981,042 65,183,997 132,654,021 75,108,670 113,898,083

Loan From Shareholders1

- 95,000,000 - -

Long Term Liabilities - Current Portion2

15,315,071 18,451,657 32,780,966 35,810,250 28,270,460 530,454

Income Tax Payable 10,761,582 20,564,632 40,874,893 46,121,577 48,350,391 24,941,902

Dividends Payable 278,261 - -

Accrued Expenses & Other Credit Balances 55,583,194 11,876,752 36,241,609 29,274,138 43,835,758 60,405,790

Total Current Liabilities 140,342,015 213,084,455 369,932,512 361,891,916 216,108,661 358,933,739

Long Term Liabilities - Non-Current Portion2

11,063,560 10,474,359 113,147,603 90,396,727 56,499,433 39,432,006

Long Term Debt 125,816,600 117,392,100

Deferred Tax Liabilities 6,722,374 10,348,538 - 15,923,408 31,373,180 38,345,515

Notes Payable - - 581,850 1,659,545 108,238 -

Total Non Current Liabilities 17,785,934 20,822,897 113,729,453 107,979,680 213,797,451 195,169,621

Total Liabilities 158,127,949 233,907,352 483,661,965 469,871,596 429,906,112 554,103,360

Paid up Capital 100,000,000 200,000,000 200,000,000 200,000,000 400,000,000 400,000,000

Amounts Paid in Respect to Capital Increase 25,000,000 - - -

Legal Reserves 1,926,912 3,068,074 7,660,650 15,760,049 27,922,900 39,733,992

Retained Earnings 22,823,250 80,108,935 173,143,674 317,342,471 256,426,457 244,624,310

Minority Interest 98,795 1,598,770 4,009,472

Total Equity 149,750,162 283,177,009 380,804,324 533,201,315 685,948,127 688,367,774

Total Equity & Liabilities 307,878,111 517,084,361 864,466,289 1,003,072,911 1,115,854,239 1,242,471,134