Embed Size (px)

Citation preview

1

Nutricia: Michelangelo, a Strategy Tool

Introduction

June, 1994: Hans van der Wielen, C.E.O. of Nutricia NV, has come to the conclusion that his company has arrived at some kind of cross-roads. No longer merely a “Dutch” company, it has become a truly international one, facing an unending series of key decisions about acquisitions, product introductions, possible divestitures, shared production and R & D and the like, on the basis of the realities of the varied competition it faces in different regions, and of the cosmopolitan personnel which increasingly fill its ranks. Nyenrode University‟s MBA students have just pronounced their evaluation of and advice for van der Wielen‟s company. The occasion was a presentation marking the end of Nyenrode‟s annual “Integration Week,” during which students spend time studying the structures, aims, and policies of one specific company, interviewing both that company‟s officials and its stakeholders. It is precisely “structures, aims, and policies” that van der Wielen wants to have polished, perfected and most importantly supported enthusiastically by the international team from within Nutricia‟s increasingly-decentralized executive structure which he relies upon to steer the company forward. That Nutricia is successful is not in doubt; its soaring stock price (quadrupling within the past two years) is only the most publicly-evident sign of the company‟s prosperous condition. Its recent take-over of Milupa, a large German competitor, has marked a further success. But van der Wielen increasingly has the sense that that simple mission statement was no longer enough. Out of a discussion with Nyenrode‟s business policy professor, Fred Lachotzki, arises the Michelangelo Project, an intensive, company-wide consultative process designed to lay a

Professor Fred Lachotzki and research associates Michael A. Olson and Wendy Sjonger prepared this case as the basis for class discussion rather than to illustrate either effective or ineffective handling of an administrative situation. Copyright© 1998 by Nyenrode Universiteit Press, Breukelen, The Netherlands.

2

common philosophical ground among all Nutricia‟s divisions to ensure that they all act in accordance with a common corporate vision when grappling with the ever-greater number of problems demanding resolution in the competitive global market-place. And one result arising from out of that process is a company mission statement encapsulating Nutricia‟s desired self-definition: “To be the world-wide leader in specialized nutrition, primarily emanating from a dairy base.” Now, two-and-a-half years later at the beginning of 1997, an acquisition proposal resting on his desk, van der Wielen finds that very mission statement echoing through his head as he reflects upon the target in question. Vitamex is a Swedish company specializing in nutritional supplements (including vitamin preparations) called “neutriceuticals.” It is not a dairy-base company, but on the other hand it is definitely a strong player within a specialized segment. The take-over, if done, might be perceived as a change of a successful strategy, especially by the people who have been involved in the Michelangelo Project.

Company History1

At the beginning of this century, over 20% of the babies born in the Netherlands died before reaching the age of one. In most cases a digestive disorder was the cause of death, usually occurring when the babies could not be breast-fed and were given raw cow‟s milk as a substitute. However, in 1894 Prof. Alexander Backhaus had succeeded in reproducing breast milk in his laboratory and this meant that many new-born babies could now be saved. In 1896 Backhaus granted Martien van der Hagen an exclusive licence to manufacture and sell Backhaus Milk. The prospects for Backhaus Baby Milk were so good that Martien set up the Nutricia Limited Liability Company on March 4, 1901. Nutricia produced mainly speciality dairy products, such as condensed buttermilk for babies. In 1932 Chocomel was introduced and was an instant hit. After World War II the second generation Van der Hagen realised that new product development and new markets were the way to expand. In the Netherlands the first cans of Olvarit baby foods made their entrance in the shops in 1946, and export to Greece, Indonesia, and other overseas markets was resumed. After the sudden death of Jan van der Hagen in 1955, Mr H.H. van der Velden became the new C.E.O. On May 11, 1966 Nutricia ceased being a closed family concern and became a public company. Inasmuch as the company had originally come into existence because of a product invention, it was - like so many other companies - more product- and finance-oriented than market-led. Eighty percent of the turnover was realized in the Netherlands, the rest through export activities, mainly in Belgium and Greece. Research into new products in the 50‟s and 60‟s resulted mainly in extensions of existing product lines. In the 70‟s management took an important step in a new direction with ready-to-serve complete drip food for patients only able to digest liquid foods. In the 70‟s Nutricia proceeded gradually. There were no more product introductions with the same impact as Chocomel or Olvarit. Unable to come up with important product breakthroughs, the management mainly sought further growth through take-overs. Among the companies that Nutricia acquired were Remia (a manufacturer of oils, fats and margarine) and Luycks (a supplier of canned pickles and sauces). In 1975 Nutricia started to realize that its new activities were not nearly as profitable as its traditional ones.

1 Main source: Drs P.G. Hoefnagel. In Gebundeld verleden, p 103-122. Edited by: R. Grootveld and

B. Koopmans. Historisch Genootschap Oud-Soetermeer, Second edition (1993).

3

The economic recession started a cut-throat competition in commodity products without enough added value. Both Remia and Luycks suffered. Nutricia‟s profits dropped, and in 1979 Nutricia made a loss of 3.3 million, the first loss since 1901. In 1979 the third generation Van der Hagen stepped back in. Mr E.J. Van der Hagen adopted a new strategy which had two important aspects: internationalization and specialization. Non-related subsidiaries were divested. However, new acquisitions remained very much a part of the strategy. In 1981 Unigate handed over its subsidiary, Cow&Gate, for a 23.46% minority share in Nutricia. The acquisition doubled Nutricia‟s turnover in the infant food and clinical nutrition markets. This take-over was one of several ventures with various international partners. The idea was that Nutricia would contribute its know-how of specialized foods and production techniques, while its partners would provide Nutricia with the knowledge of the local market. In countries like the US and Indonesia Nutricia preferred joint venture structures so as to avoid immediate confrontations with powerful competitors such as Nestlé, Heinz and Unilever. Immediately after his appointment in 1979, Van der Hagen had set up a “Clinical Nutrition” working group to study the possibilities for “enteral clinical products.” It was decided that the clinical nutrition market was right for Nutricia and this led to an increase in R&D spending and eventually to new products. The Consumer Products Division also gained some profitable products, such as Chocomel Light, a successful relaunch of Fristi (a milk-based softdrink) and a completely new product range called Extran, a range of nutritional drinks for sportsmen and -women. Disposing of old subsidiaries and taking on new activities was combined with a complete reorganisation of both the holding company and the subsidiaries. To improve the bottom line further, Van der Hagen rationalized production. The 3.3 million loss in 1979 was followed by an almost 8 million guilder profit in 1980, despite a drop in turnover (from 543 million to 494 million).

Nutricia’s Markets

In January, 1992, Hans van der Wielen took over the helm from Van der Hagen as Nutricia‟s C.E.O. A chemical engineer by training out of Eindhoven University and a Nutricia veteran since 1980, he had been a production manager and then Director of Production in the Sales and Laboratories Divisions, and so a member of the Board of Managing Directors. The company he took over focused its activities, within a primarily European area of operations, on the development, manufacturing, and marketing of medically-sound nutrition products based upon scientific guidelines, as well as that of other specialized food products with high added value. Nutricia distinguished what it considered its core activities from other, more secondary activities (this is further elaborated in Appendix V; Appendices I through IV give fundamental organizational and financial information for the company). Its core activities at the time of van der Wielen‟s accession were the following product groups:

Infant Milk Formula (I.M.F.)

Enteral Clinical Nutrition (E.C.N.) - that is, special foods consumed via the gastro-intestinal tract, by either tube or peg, meant for hospital patients who cannot eat normally, will not eat normally, or do not eat enough

Meals, drinks, juices and cereals for babies and toddlers

Dietary/Health food

Skin- and throat care products

4

The other activities consisted mainly of consumer products emanating from a dairy basis, such as chocolate milk and yoghurt drinks. In Appendix VI Nutricia‟s turnover is specified per region. Further market details will only be given for I.M.F. and E.C.N., Nutricia‟s most important businesses, and briefly for the food and drinks division for babies and toddlers. Intensity of competition has varied per product group and also per geographic area, with a generally highly-competitive environment world-wide for baby food and E.C.N. and one slightly less so for I.M.F. The Milupa acquisition has strongly boosted Nutricia‟s market share (particularly for I.M.F.), not only in Milupa‟s former core markets in German-speaking Europe but also elsewhere, such as in South-East Europe.

Infant Milk Formula (I.M.F.)

Europe

The overall I.M.F. position of Nutricia in Europe is strong. Nutricia is the market leader in most European countries.

This premier position is also occupied in the newly-developed Eastern European countries: Poland 66%, Hungary 85% and The Czech and Slovak Republics 68%. Its main competitor in these markets is Nestlé, which holds respectively 13%, 11% and 15%. These markets are expected to grow, but they are also very price sensitive. Due to regulation by the World Health Organisation (W.H.O.) advertising products meant for consumption by children six months and younger is not allowed. This, of course, lays constraints on the marketing activities Nutricia can develop to gain market share.

In Central Europe Nutricia is again market leader, except for the Swiss region. There Nutricia possesses a market share of 27%, while Sandoz/Wander is market leader at 40%. In Germany, the Netherlands and Austria Nestlé is Nutricia‟s main competitor.

In Southern Europe Nutricia also holds either a first or second market-share position. Its main competitors are Nestlé, Sandoz/Wander and Danone. In Northern Europe Wyeth is the second player in the UK (39.1%) and in Ireland (32.3%) after Nutricia. In Denmark Nestlé is the market leader.

The overall European market share of Nutricia in 1996 was 40%. Nestlé was the second largest player at 19%, followed by Wyeth with 11%.

Asia Pacific

The main players in the Asia Pacific region are Wyeth and Nestlé. Nutricia is working on the making further progress in this market. In 1996 Nutricia expanded its activities in New Zealand and Australia through the acquisition of the I.M.F. activities of Douglas Pharmaceuticals. This company is the market leader in baby food in both New Zealand and Australia, with a market share of approximately 30%. Australia and New Zealand are also geographically interesting spots, as they serve as export bases for China and other countries in the region. China is an extremely important market for baby food and infant milk formula, given the high birthrates, rapid economic growth, westernization of tastes and a growing affluent class. Nestlé has already established joint ventures for these products. Heinz and Danone are also present in this market. Nutricia is currently working on establishing joint ventures in this area.

5

In general, it is accurate to say that several of Nutricia‟s competitors have a presence in various East Asian countries, but no company dominates the region yet.

Overseas

In Central America, South America and the Caribbean, Nutricia holds a market share of approximately 4%. The big players in this field are Nestlé (55%), Wyeth (16%), Ross Abbott (10%) and Mead Johnson (10%). Nutricia is not active in North America generally. In this part of the world Mead Johnson holds 52% market-share, Ross Abbott 35% and Nestlé approximately 7-8%.

Enteral Clinical Nutrition (E.C.N.)

E.C.N. concerns special foods which are given via the gastro-intestinal tract, by either tube or peg, as drinks or food. It is meant for patients who cannot eat, will not eat, are not allowed to eat or do not eat enough. E.C.N. is one of the fastest growing markets in the health care industry. In Europe the market had a total turnover of 437 million in 1991 and this is expected to grow to 730 million in 1997. There are a number of reasons which account for the positive outlook for E.C.N.:

An increase in clinical awareness of E.C.N. in Western and Eastern Europe, Latin America and in the Middle and Far East

An ageing population - this is mainly important for Western Europe and Eastern Europe

The substitution of T.P.N.2 by E.C.N.. This does not yet play a large role in Latin America, but it is also a potential issue there.

Growth in the Gross National Product. This is a very strong reason for the growth of the E.C.N. market, especially in Latin America and the Far East.

Cost containment of health care. In Western Europe this is a top issue, whereas in Eastern Europe, Latin America, the Middle East and the Far East it is an up-and-coming or potential topic.

In Western Europe Nutricia holds a key position in the E.C.N. market. It takes the leading position with a 32% share. The second place is taken by Fresenius with 21%, and the third by Sandoz with 12%. However, the most sophisticated market for E.C.N. is the United States, and Nutricia does not have a market presence there. Large players in this market are Abbott Laboratories, Ballard Medical, Baxter International, Coram health Care, McGaw, Mead Johnson Nutrition, Nestlé Clinical Nutrition, Ross Laboratories, Sherwood, Davis & Geck and Sandoz Nutrition. In contrast, although Nutricia is building a strong presence in E.C.N in Eastern Europe in a highly-competitive environment, the market is as yet still constrained by the low level of basic familiarity with (and therefore usage of) E.C.N. products generally. Similarly, the development of Nutricia‟s market-share in the potentially-gigantic China market has been impeded by the failure of a joint venture there in 1996 and the resulting need to search for new partners.

2 T.P.N. stands for Total Parental Nutrition. This method directly injects nutrition into the veins. E.C.N. is

usually preferred to T.P.N. because E.C.N. activates the normal digestive tract, it exposes the patient to minimal risks of infection, it is cheaper than T.P.N., and it enables medical professionals to target very specifically the nutritional needs of the patients.

6

Food and Drinks for Babies and Toddlers

In this segment Nutricia holds the leading market-share for Europe as a whole, as well as significant shares in markets in many other parts of the world (excluding North America). The company has branched out from an initial base in dairy foods to boost its turnover by offering a varied selection in wheat- and grain-based products as well, especially in the new Eastern European markets. In particular, phenomenal growth in the sales of these grain products in Poland in 1996 greatly strengthened Nutricia‟s financial results in that region.

Strategy Formulation “The Michelangelo Project”

“The marble not yet carved can hold the form of every thought the greatest artist has, and no conception can yet come to pass unless the hand obeys the intellect . . .” Michelangelo Nutricia was changing. That was clear, and this was the realization driving van der Wielen‟s search for a new vision for his company, a realization which had led him to seek some outside assistance (such as that which Lachotzki could provide) in the first place. In part, that change was deliberate and very much part of what van der Wielen wanted to do to make his mark on the company. What he had in mind was a more decentralised organisation structure, in which Central Europe (Van Hedel), Northern Europe (Roebuck), Southern Europe (Mannekens) and Overseas (Van Overbeek) were not only run with different management styles and cultures, but also by managers with entirely different personalities. And this strong focus on the individual business units had indeed lead to increased effectiveness and profits during the past few years. But what about the future? There was the danger, for example, that necessary co-operation between different divisions might end up taking place only if there was no alternative. How could the company gain a more co-operative, relaxed atmosphere - especially in executive board meetings where these autonomous, opinionated division-heads came together? Heretofore such meetings had had an atmosphere that was a bit tense, to say the least. That was the goal, then: Finding some common idea of the company and where it was going to function as a sort of “intellectual glue” to bind together the disparate, decentralized regional managers with a common “mindset.” Some sort of co-ordination was necessary for the company‟s future projects, even as all these managers had to deal with different problems unique to their assigned parts of the world. Van der Wielen and Lachotzki first decided upon a strategic session with the executive board to begin the search towards this common vision. In the invitation they issued to all participants, four key sections made clear to those invited what was to be involved:

7

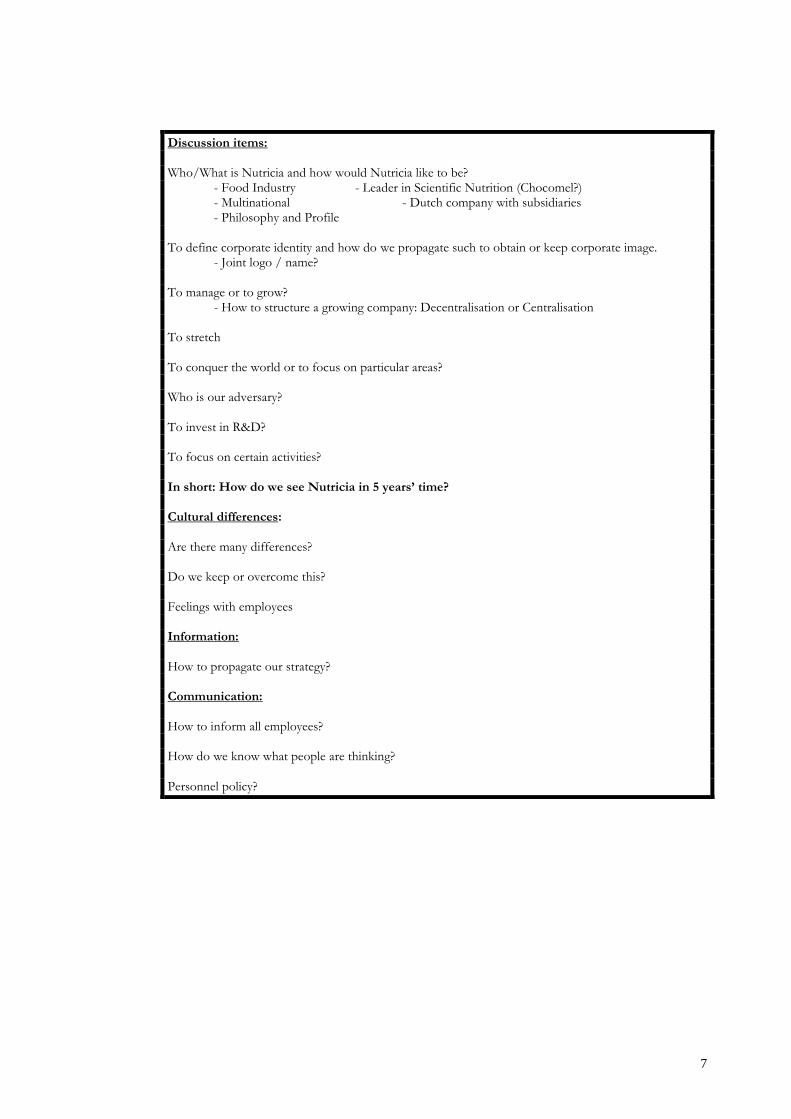

Discussion items: Who/What is Nutricia and how would Nutricia like to be? - Food Industry - Leader in Scientific Nutrition (Chocomel?) - Multinational - Dutch company with subsidiaries - Philosophy and Profile To define corporate identity and how do we propagate such to obtain or keep corporate image. - Joint logo / name? To manage or to grow? - How to structure a growing company: Decentralisation or Centralisation To stretch To conquer the world or to focus on particular areas? Who is our adversary? To invest in R&D? To focus on certain activities? In short: How do we see Nutricia in 5 years’ time? Cultural differences: Are there many differences? Do we keep or overcome this? Feelings with employees Information: How to propagate our strategy? Communication: How to inform all employees? How do we know what people are thinking? Personnel policy?

8

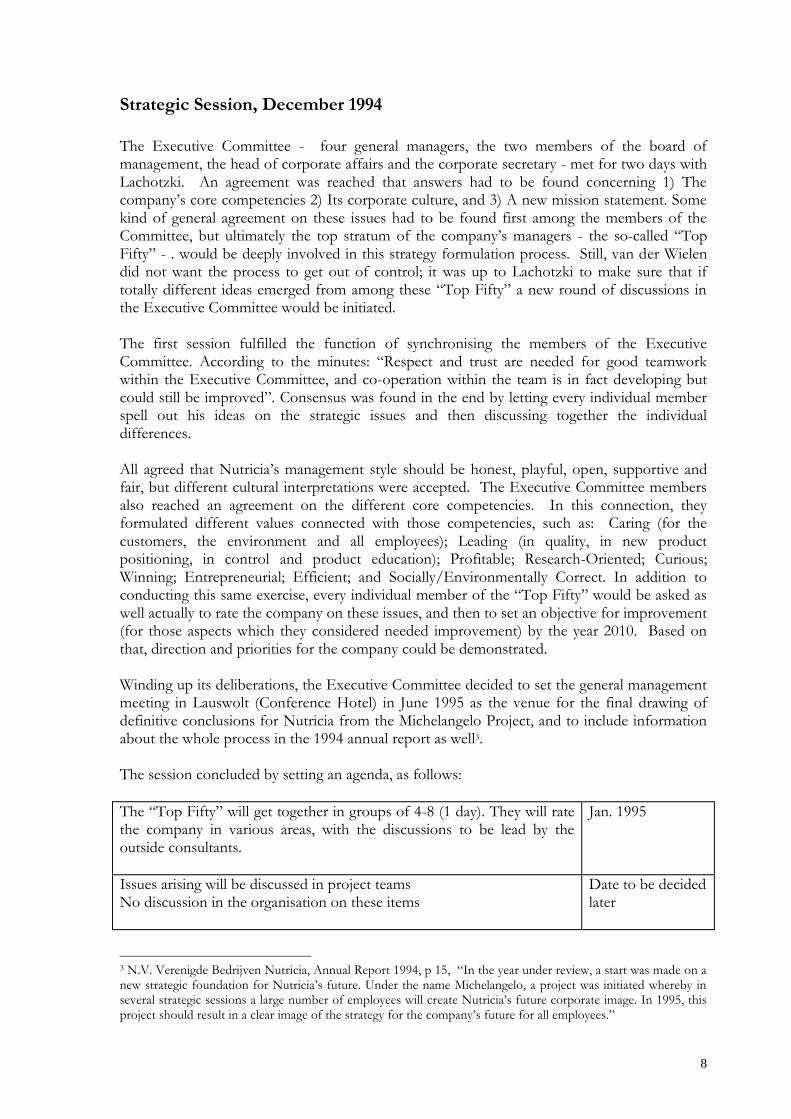

Strategic Session, December 1994

The Executive Committee - four general managers, the two members of the board of management, the head of corporate affairs and the corporate secretary - met for two days with Lachotzki. An agreement was reached that answers had to be found concerning 1) The company‟s core competencies 2) Its corporate culture, and 3) A new mission statement. Some kind of general agreement on these issues had to be found first among the members of the Committee, but ultimately the top stratum of the company‟s managers - the so-called “Top Fifty” - . would be deeply involved in this strategy formulation process. Still, van der Wielen did not want the process to get out of control; it was up to Lachotzki to make sure that if totally different ideas emerged from among these “Top Fifty” a new round of discussions in the Executive Committee would be initiated. The first session fulfilled the function of synchronising the members of the Executive Committee. According to the minutes: “Respect and trust are needed for good teamwork within the Executive Committee, and co-operation within the team is in fact developing but could still be improved”. Consensus was found in the end by letting every individual member spell out his ideas on the strategic issues and then discussing together the individual differences. All agreed that Nutricia‟s management style should be honest, playful, open, supportive and fair, but different cultural interpretations were accepted. The Executive Committee members also reached an agreement on the different core competencies. In this connection, they formulated different values connected with those competencies, such as: Caring (for the customers, the environment and all employees); Leading (in quality, in new product positioning, in control and product education); Profitable; Research-Oriented; Curious; Winning; Entrepreneurial; Efficient; and Socially/Environmentally Correct. In addition to conducting this same exercise, every individual member of the “Top Fifty” would be asked as well actually to rate the company on these issues, and then to set an objective for improvement (for those aspects which they considered needed improvement) by the year 2010. Based on that, direction and priorities for the company could be demonstrated. Winding up its deliberations, the Executive Committee decided to set the general management meeting in Lauswolt (Conference Hotel) in June 1995 as the venue for the final drawing of definitive conclusions for Nutricia from the Michelangelo Project, and to include information about the whole process in the 1994 annual report as well3. The session concluded by setting an agenda, as follows:

The “Top Fifty” will get together in groups of 4-8 (1 day). They will rate the company in various areas, with the discussions to be lead by the outside consultants.

Jan. 1995

Issues arising will be discussed in project teams No discussion in the organisation on these items

Date to be decided later

3 N.V. Verenigde Bedrijven Nutricia, Annual Report 1994, p 15, “In the year under review, a start was made on a new strategic foundation for Nutricia‟s future. Under the name Michelangelo, a project was initiated whereby in several strategic sessions a large number of employees will create Nutricia‟s future corporate image. In 1995, this project should result in a clear image of the strategy for the company‟s future for all employees.”

9

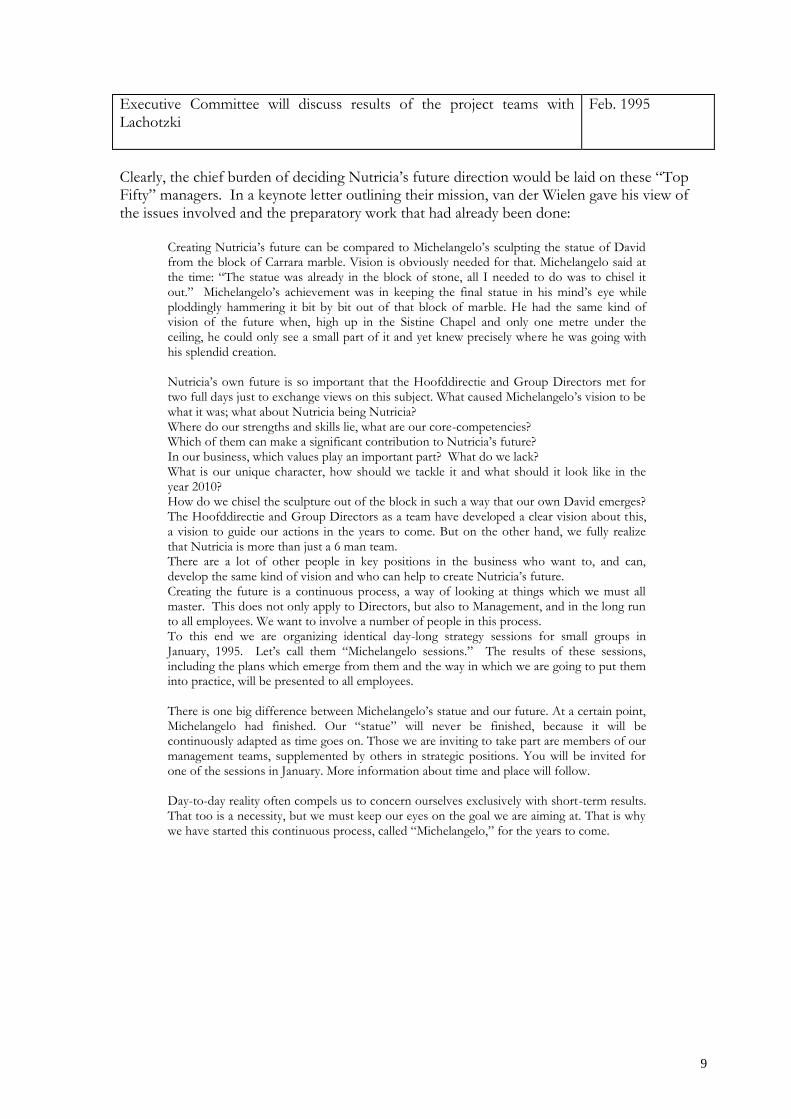

Executive Committee will discuss results of the project teams with Lachotzki

Feb. 1995

Clearly, the chief burden of deciding Nutricia‟s future direction would be laid on these “Top Fifty” managers. In a keynote letter outlining their mission, van der Wielen gave his view of the issues involved and the preparatory work that had already been done:

Creating Nutricia‟s future can be compared to Michelangelo‟s sculpting the statue of David from the block of Carrara marble. Vision is obviously needed for that. Michelangelo said at the time: “The statue was already in the block of stone, all I needed to do was to chisel it out.” Michelangelo‟s achievement was in keeping the final statue in his mind‟s eye while ploddingly hammering it bit by bit out of that block of marble. He had the same kind of vision of the future when, high up in the Sistine Chapel and only one metre under the ceiling, he could only see a small part of it and yet knew precisely where he was going with his splendid creation. Nutricia‟s own future is so important that the Hoofddirectie and Group Directors met for two full days just to exchange views on this subject. What caused Michelangelo‟s vision to be what it was; what about Nutricia being Nutricia? Where do our strengths and skills lie, what are our core-competencies? Which of them can make a significant contribution to Nutricia‟s future? In our business, which values play an important part? What do we lack? What is our unique character, how should we tackle it and what should it look like in the year 2010? How do we chisel the sculpture out of the block in such a way that our own David emerges? The Hoofddirectie and Group Directors as a team have developed a clear vision about this, a vision to guide our actions in the years to come. But on the other hand, we fully realize that Nutricia is more than just a 6 man team. There are a lot of other people in key positions in the business who want to, and can, develop the same kind of vision and who can help to create Nutricia‟s future. Creating the future is a continuous process, a way of looking at things which we must all master. This does not only apply to Directors, but also to Management, and in the long run to all employees. We want to involve a number of people in this process. To this end we are organizing identical day-long strategy sessions for small groups in January, 1995. Let‟s call them “Michelangelo sessions.” The results of these sessions, including the plans which emerge from them and the way in which we are going to put them into practice, will be presented to all employees. There is one big difference between Michelangelo‟s statue and our future. At a certain point, Michelangelo had finished. Our “statue” will never be finished, because it will be continuously adapted as time goes on. Those we are inviting to take part are members of our management teams, supplemented by others in strategic positions. You will be invited for one of the sessions in January. More information about time and place will follow. Day-to-day reality often compels us to concern ourselves exclusively with short-term results. That too is a necessity, but we must keep our eyes on the goal we are aiming at. That is why we have started this continuous process, called “Michelangelo,” for the years to come.

10

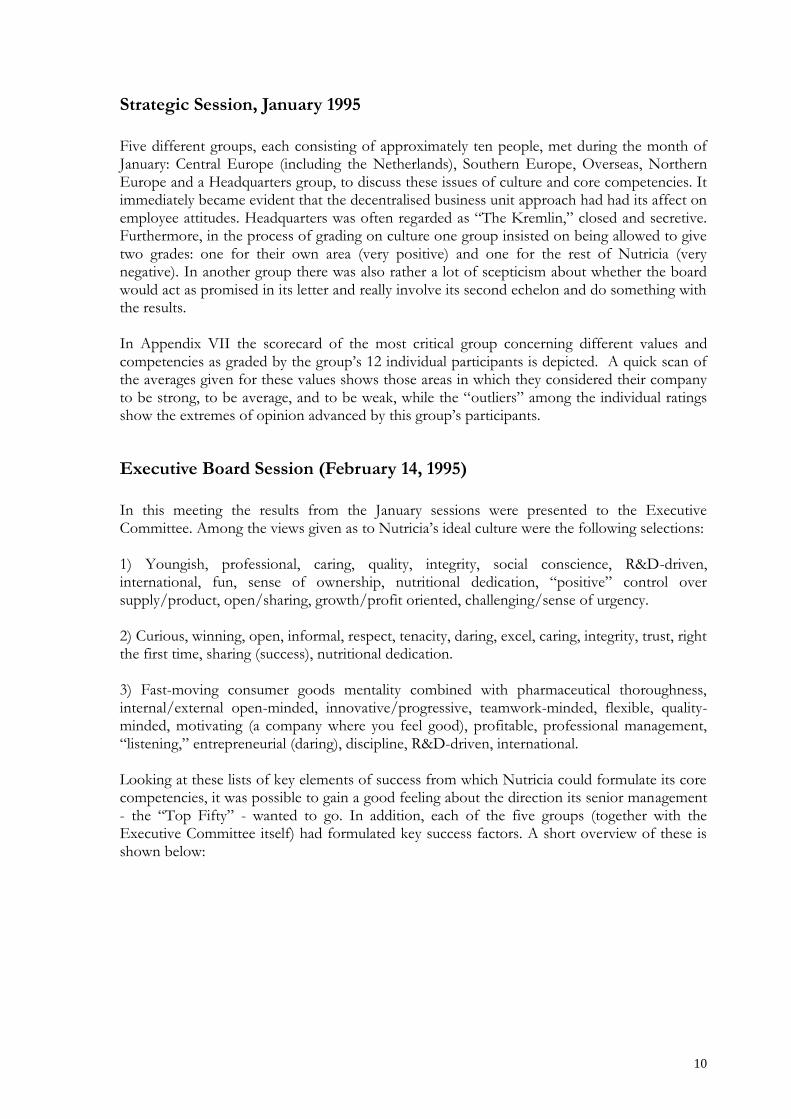

Strategic Session, January 1995

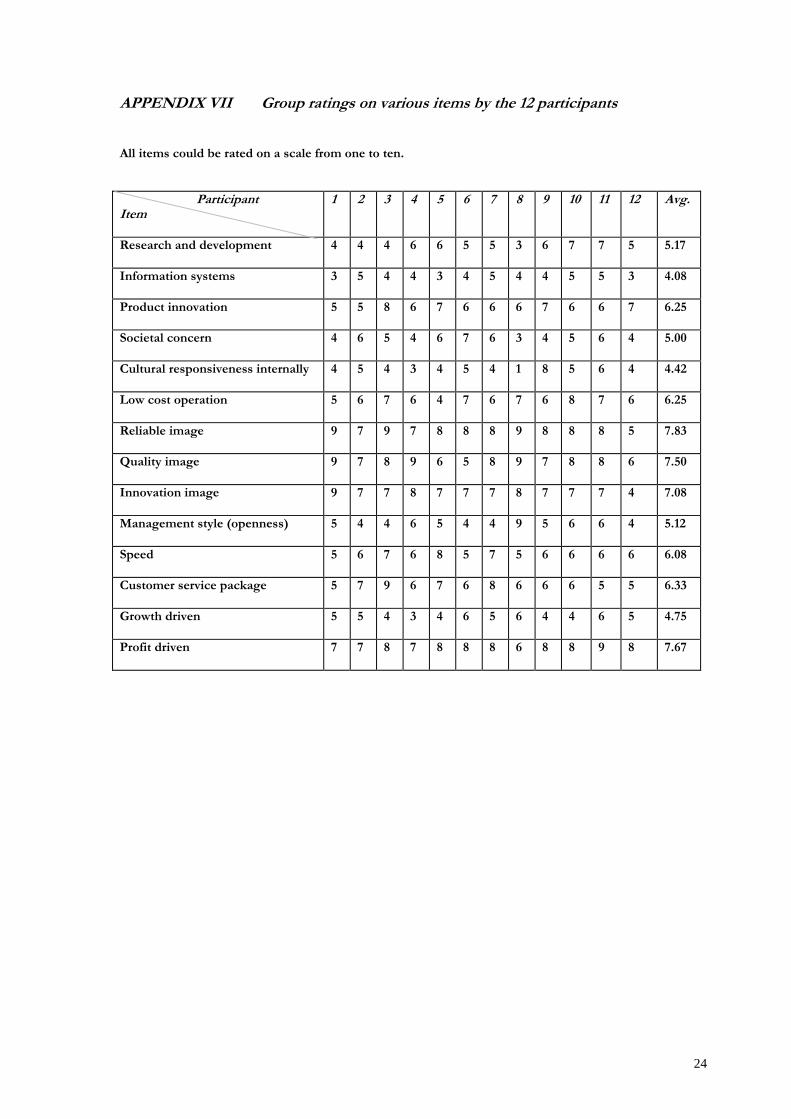

Five different groups, each consisting of approximately ten people, met during the month of January: Central Europe (including the Netherlands), Southern Europe, Overseas, Northern Europe and a Headquarters group, to discuss these issues of culture and core competencies. It immediately became evident that the decentralised business unit approach had had its affect on employee attitudes. Headquarters was often regarded as “The Kremlin,” closed and secretive. Furthermore, in the process of grading on culture one group insisted on being allowed to give two grades: one for their own area (very positive) and one for the rest of Nutricia (very negative). In another group there was also rather a lot of scepticism about whether the board would act as promised in its letter and really involve its second echelon and do something with the results. In Appendix VII the scorecard of the most critical group concerning different values and competencies as graded by the group‟s 12 individual participants is depicted. A quick scan of the averages given for these values shows those areas in which they considered their company to be strong, to be average, and to be weak, while the “outliers” among the individual ratings show the extremes of opinion advanced by this group‟s participants.

Executive Board Session (February 14, 1995)

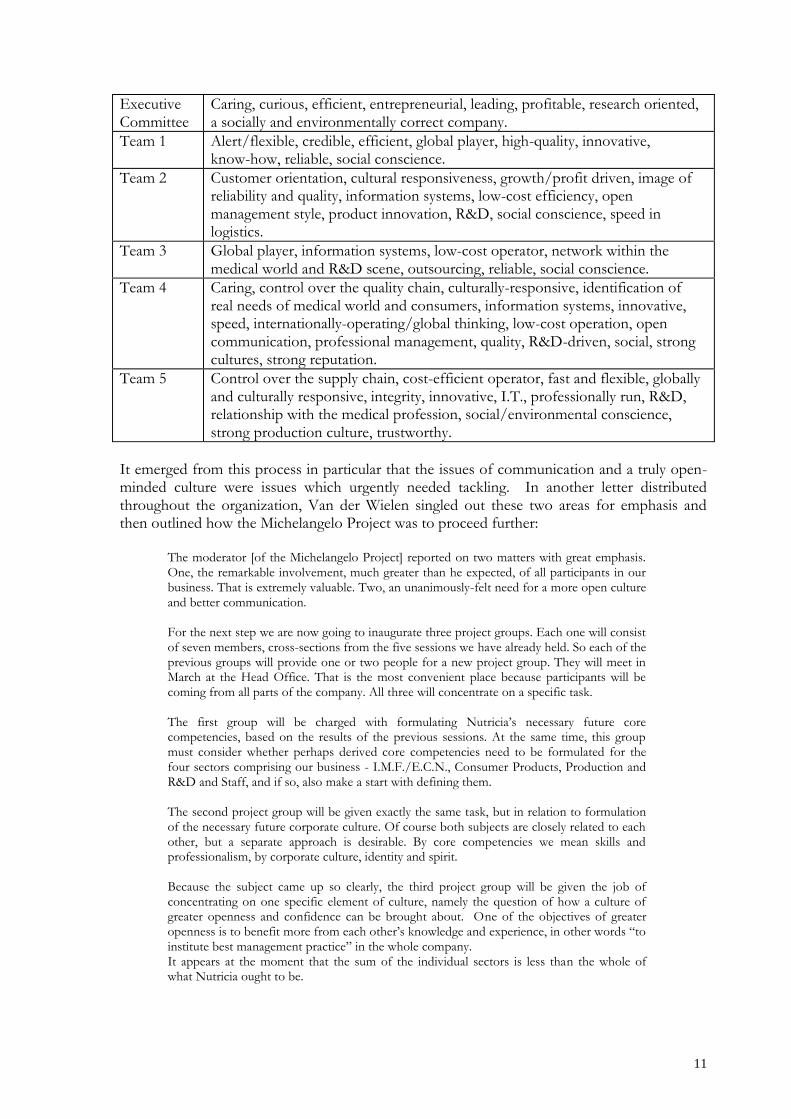

In this meeting the results from the January sessions were presented to the Executive Committee. Among the views given as to Nutricia‟s ideal culture were the following selections: 1) Youngish, professional, caring, quality, integrity, social conscience, R&D-driven, international, fun, sense of ownership, nutritional dedication, “positive” control over supply/product, open/sharing, growth/profit oriented, challenging/sense of urgency. 2) Curious, winning, open, informal, respect, tenacity, daring, excel, caring, integrity, trust, right the first time, sharing (success), nutritional dedication. 3) Fast-moving consumer goods mentality combined with pharmaceutical thoroughness, internal/external open-minded, innovative/progressive, teamwork-minded, flexible, quality-minded, motivating (a company where you feel good), profitable, professional management, “listening,” entrepreneurial (daring), discipline, R&D-driven, international. Looking at these lists of key elements of success from which Nutricia could formulate its core competencies, it was possible to gain a good feeling about the direction its senior management - the “Top Fifty” - wanted to go. In addition, each of the five groups (together with the Executive Committee itself) had formulated key success factors. A short overview of these is shown below:

11

Executive Committee

Caring, curious, efficient, entrepreneurial, leading, profitable, research oriented, a socially and environmentally correct company.

Team 1 Alert/flexible, credible, efficient, global player, high-quality, innovative, know-how, reliable, social conscience.

Team 2 Customer orientation, cultural responsiveness, growth/profit driven, image of reliability and quality, information systems, low-cost efficiency, open management style, product innovation, R&D, social conscience, speed in logistics.

Team 3 Global player, information systems, low-cost operator, network within the medical world and R&D scene, outsourcing, reliable, social conscience.

Team 4 Caring, control over the quality chain, culturally-responsive, identification of real needs of medical world and consumers, information systems, innovative, speed, internationally-operating/global thinking, low-cost operation, open communication, professional management, quality, R&D-driven, social, strong cultures, strong reputation.

Team 5 Control over the supply chain, cost-efficient operator, fast and flexible, globally and culturally responsive, integrity, innovative, I.T., professionally run, R&D, relationship with the medical profession, social/environmental conscience, strong production culture, trustworthy.

It emerged from this process in particular that the issues of communication and a truly open-minded culture were issues which urgently needed tackling. In another letter distributed throughout the organization, Van der Wielen singled out these two areas for emphasis and then outlined how the Michelangelo Project was to proceed further:

The moderator [of the Michelangelo Project] reported on two matters with great emphasis. One, the remarkable involvement, much greater than he expected, of all participants in our business. That is extremely valuable. Two, an unanimously-felt need for a more open culture and better communication. For the next step we are now going to inaugurate three project groups. Each one will consist of seven members, cross-sections from the five sessions we have already held. So each of the previous groups will provide one or two people for a new project group. They will meet in March at the Head Office. That is the most convenient place because participants will be coming from all parts of the company. All three will concentrate on a specific task. The first group will be charged with formulating Nutricia‟s necessary future core competencies, based on the results of the previous sessions. At the same time, this group must consider whether perhaps derived core competencies need to be formulated for the four sectors comprising our business - I.M.F./E.C.N., Consumer Products, Production and R&D and Staff, and if so, also make a start with defining them. The second project group will be given exactly the same task, but in relation to formulation of the necessary future corporate culture. Of course both subjects are closely related to each other, but a separate approach is desirable. By core competencies we mean skills and professionalism, by corporate culture, identity and spirit. Because the subject came up so clearly, the third project group will be given the job of concentrating on one specific element of culture, namely the question of how a culture of greater openness and confidence can be brought about. One of the objectives of greater openness is to benefit more from each other‟s knowledge and experience, in other words “to institute best management practice” in the whole company. It appears at the moment that the sum of the individual sectors is less than the whole of what Nutricia ought to be.

12

All three project groups will at the same time be asked to present outlined plans for implementation in the coming three years. For reasons of efficiency, the size of each group will be limited to 6 or 7 people. That means that about 20 out of 50 will be involved in the next stage. The 30 who are not, will of course be involved in the following stage, which will take place, if possible, before Lauswolt (the General Management Meeting). Of course I will keep you all informed of the outcome. After all, the future of our business will be shaped by us. To emphasise the importance that the Hoofddirectie and Group Directors attach to the Michelangelo Project, and thereby to immediately take the lead in moving towards a more open culture, I am asking you to let me know if there are any topics you think should be discussed in Lauswolt next June. Drop me a line.

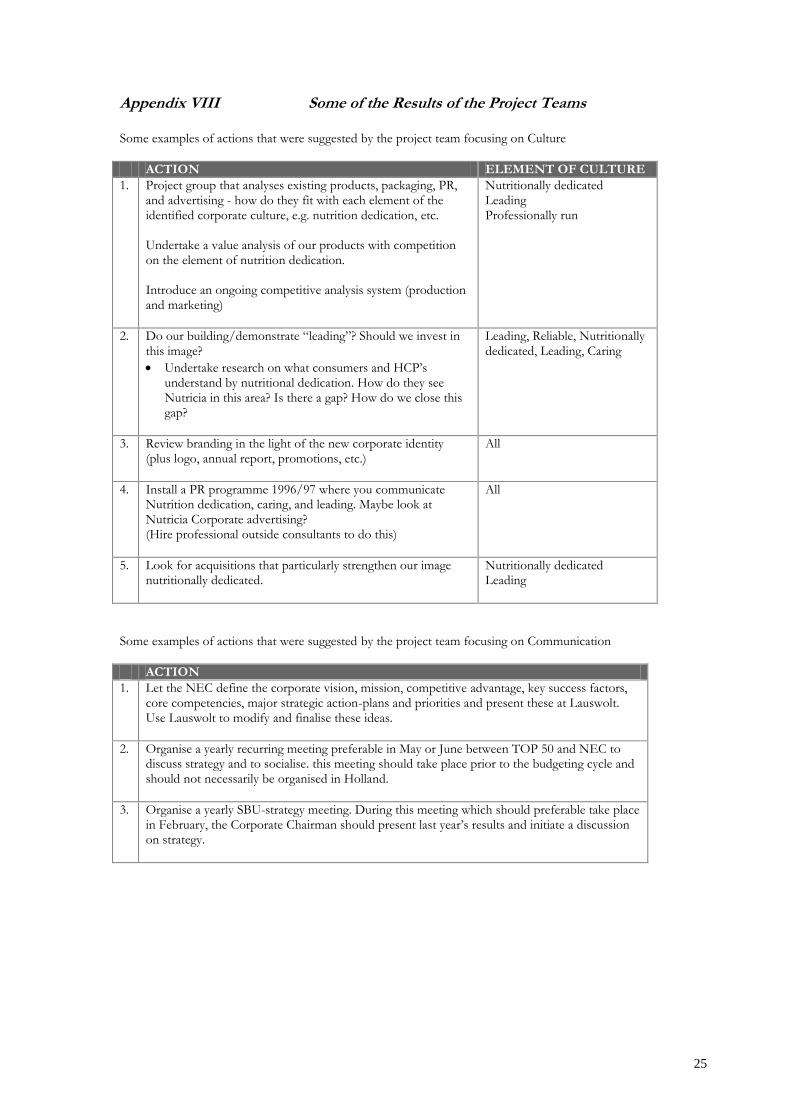

Project Team Discussions

The three project teams were set up after the executive board session had taken place. Their aim was to develop further insight into the problem areas which had been highlighted. They focused on generating suggestions to help Nutricia strengthen, achieve or improve its culture, internal communication and its core competencies. Each group consisted of one representative from the following units: Central Europe, Northern Europe, Southern Europe, Overseas and Corporate Staff. The results of each group are briefly described below. Group I Corporate Culture This group developed a view of the future corporate culture (roughly for the year 2010). They outlined how they would like Nutricia to be seen by all of its stakeholders, e.g. customers, staff, financial institutions, suppliers, competitors, media and potential recruits. This resulted in the following cultural statement of the corporate culture: “a profitable and growing, nutritionally-dedicated, caring, reliable and leading company, that is professionally run with a real sense of ownership.” This group also identified actions that would move Nutricia towards this goal. (See Appendix VIII). Group II Communication Based upon the discussions, the members of this group concluded that the causes of sub-optimal communication within Nutricia could be categorized into four general areas: 1. The perceived lack of clarity on strategic direction and corporate values and norms. 2. Certain aspects of Nutricia‟s organizational design. 3. Certain aspects of the Nutricia management style. 4. The lack of a clearly defined formal communication process. The group then presented steps for improvement in these areas. (See Appendix VIII) Group III Core Competencies This group searched for an answer to the question “Which skills and capabilities do we need to possess in order to achieve our strategic vision?” The consensus as to the current strategic vision of Nutricia emerged as follows: To be an international leader in specialised nutrition4. The participants of this group then defined which core competencies Nutricia needed to achieve this vision, and how to develop them. (See Appendix VIII). The results of these three project teams were presented in June 1995 during the general management meeting in Lauswolt.

4 “Specialized” refers to ECN, IMF and functional foods.

13

The Top Fifty managers were invited together with their spouses to a two-day general management meeting at Lauswolt. One day was spent socialising and one day doing business. Most of the business day was used to present the results of Michelangelo. Van der Wielen opened the meeting with the following statement:

I am excited about what has happened during this project. I am proud of the work and recommendations from all of you. Also this convinced me that together we have a great shared dream.

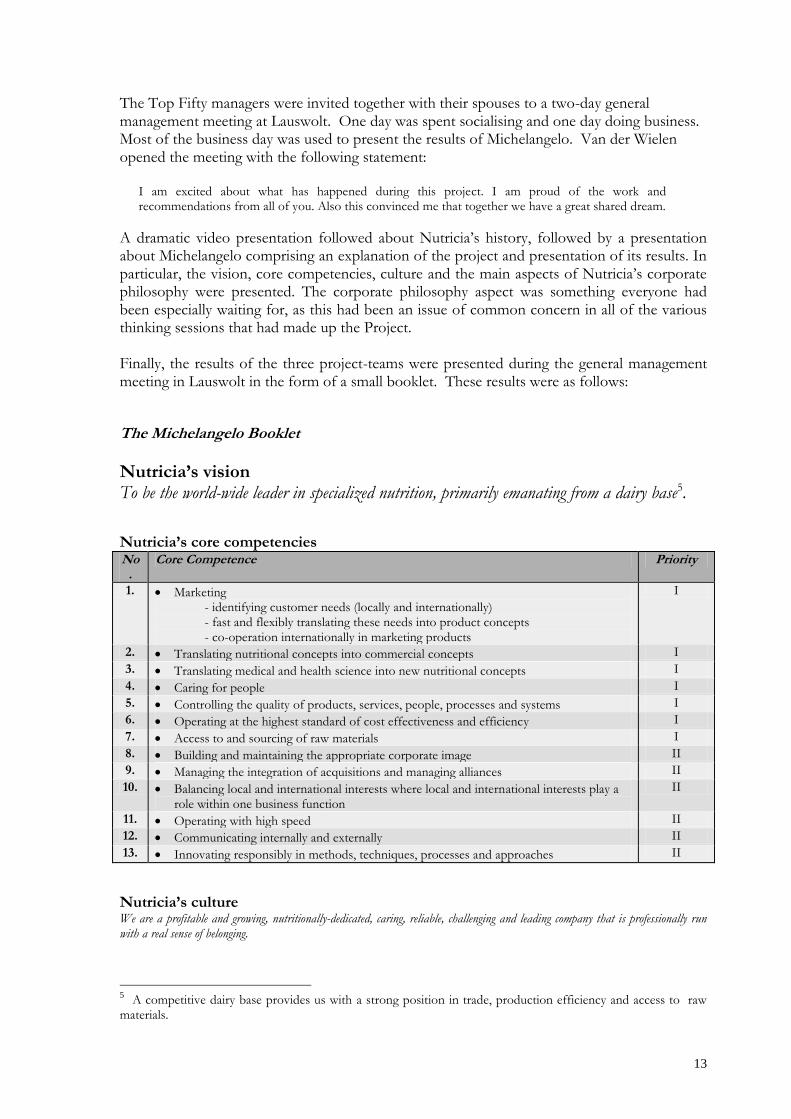

A dramatic video presentation followed about Nutricia‟s history, followed by a presentation about Michelangelo comprising an explanation of the project and presentation of its results. In particular, the vision, core competencies, culture and the main aspects of Nutricia‟s corporate philosophy were presented. The corporate philosophy aspect was something everyone had been especially waiting for, as this had been an issue of common concern in all of the various thinking sessions that had made up the Project. Finally, the results of the three project-teams were presented during the general management meeting in Lauswolt in the form of a small booklet. These results were as follows:

The Michelangelo Booklet

Nutricia’s vision To be the world-wide leader in specialized nutrition, primarily emanating from a dairy base5.

Nutricia’s core competencies No

. Core Competence Priority

1. Marketing - identifying customer needs (locally and internationally) - fast and flexibly translating these needs into product concepts - co-operation internationally in marketing products

I

2. Translating nutritional concepts into commercial concepts I

3. Translating medical and health science into new nutritional concepts I

4. Caring for people I

5. Controlling the quality of products, services, people, processes and systems I

6. Operating at the highest standard of cost effectiveness and efficiency I

7. Access to and sourcing of raw materials I

8. Building and maintaining the appropriate corporate image II

9. Managing the integration of acquisitions and managing alliances II

10. Balancing local and international interests where local and international interests play a role within one business function

II

11. Operating with high speed II

12. Communicating internally and externally II

13. Innovating responsibly in methods, techniques, processes and approaches II

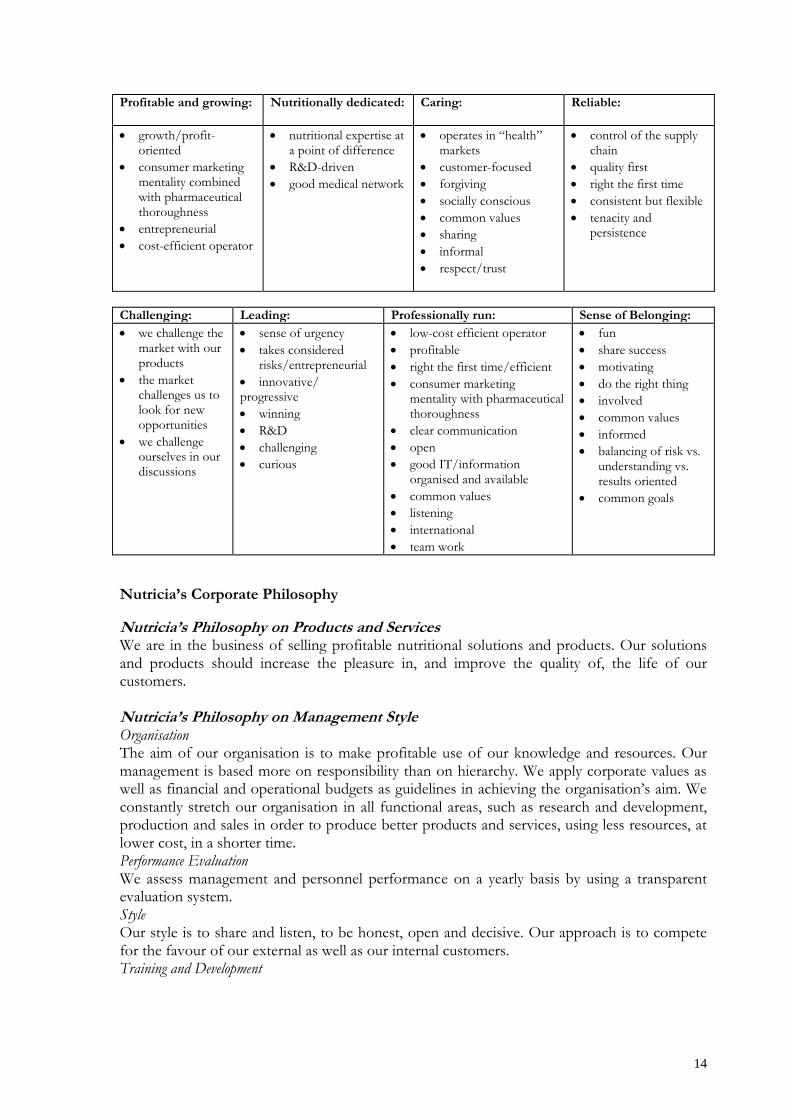

Nutricia’s culture We are a profitable and growing, nutritionally-dedicated, caring, reliable, challenging and leading company that is professionally run with a real sense of belonging.

5 A competitive dairy base provides us with a strong position in trade, production efficiency and access to raw

materials.

14

Profitable and growing: Nutritionally dedicated: Caring:

Reliable:

growth/profit-oriented

consumer marketing mentality combined with pharmaceutical thoroughness

entrepreneurial

cost-efficient operator

nutritional expertise at a point of difference

R&D-driven

good medical network

operates in “health” markets

customer-focused

forgiving

socially conscious

common values

sharing

informal

respect/trust

control of the supply chain

quality first

right the first time

consistent but flexible

tenacity and persistence

Challenging: Leading: Professionally run: Sense of Belonging:

we challenge the market with our products

the market challenges us to look for new opportunities

we challenge ourselves in our discussions

sense of urgency

takes considered risks/entrepreneurial

innovative/ progressive

winning

R&D

challenging

curious

low-cost efficient operator

profitable

right the first time/efficient

consumer marketing mentality with pharmaceutical thoroughness

clear communication

open

good IT/information organised and available

common values

listening

international

team work

fun

share success

motivating

do the right thing

involved

common values

informed

balancing of risk vs. understanding vs. results oriented

common goals

Nutricia’s Corporate Philosophy

Nutricia’s Philosophy on Products and Services We are in the business of selling profitable nutritional solutions and products. Our solutions and products should increase the pleasure in, and improve the quality of, the life of our customers. Nutricia’s Philosophy on Management Style Organisation The aim of our organisation is to make profitable use of our knowledge and resources. Our management is based more on responsibility than on hierarchy. We apply corporate values as well as financial and operational budgets as guidelines in achieving the organisation‟s aim. We constantly stretch our organisation in all functional areas, such as research and development, production and sales in order to produce better products and services, using less resources, at lower cost, in a shorter time. Performance Evaluation We assess management and personnel performance on a yearly basis by using a transparent evaluation system. Style Our style is to share and listen, to be honest, open and decisive. Our approach is to compete for the favour of our external as well as our internal customers. Training and Development

15

The company invests in the training of skills and the development of corporate values of all employees. We continually invest in a pool of top management by using job rotation and career development. Nutricia’s Philosophy on Research and Development We consider research and development to be the backbone of our leadership position. Research is centralized, development decentralized. Our research is in the forefront, speedy, and focused on being translated into profitable product implementations. We are open to using external research alliances. Nutricia’s Philosophy on Resources Our corporate priority is to guarantee permanent access to the raw materials we need. We strive for maximum control over our supply lines, thus taking full responsibility for all ingredients used in the products and services in the chain. Nutricia’s Philosophy on Society and Environment We take responsibility for the impact we have on the community, society and the environment. We do not accept or pursue activities that would seriously impede our capacity to realize our main task and vision. These, then, were Nutricia‟s own conclusions of the summer of 1995 about what sort of common strategic vision it needed to face the problems confronting it. But this represented only the internal point-of-view, the collective opinion of Nutricia‟s own top managers. It can usefully be compared to an earlier external judgment to see whether the output of the Michelangelo Project would also satisfy the requirements that a set of detached observers identify for the company‟s continued growth and success. One such external analysis was that conducted by the 1994 Nyenrode MBA class, the examination which initially spurred van der Wielen along the path the led to Michelangelo in the first place.

Nyenrode Universiteit Integration Week

The “Integration Week” at Nyenrode Universiteit is a yearly exercise which gives MBA students the opportunity to spend two weeks with the management and stakeholders of a specific company. They listen, question, talk, look at competitors and write one report with conclusions and recommendations. This report is presented to the company board. Nutricia opened its doors to this sort of examination in 1994. The MBA class examined Nutricia in its various aspects, and came to quite a few conclusions and recommendations, such as:

Nutricia‟s transition from a small Dutch multinational into a more globally-oriented company involves the introduction of new controls in conjunction with greater decentralisation of many functions company-wide. There must be greater integration of Nutricia‟s world-wide operations, while at the same time the focus of the company should shift from its present varied portfolio to a much more focused approach. By examining Nutricia‟s core competencies, the appropriate portfolio of businesses can be put together.

Nutricia must concentrate on high growth markets, product line extensions and related niche markets. However, there has been a lack of learning from past mistakes within the organization. Ventures which have failed offer an opportunity to understand the corporate culture and make the necessary fine-tuning, rather than continually repeating the mistake in another market.

16

Since Nutricia is a relatively small player in many markets, further expansion can only be achieved through a system of joint ventures and/or alliances with partners which have complementary capabilities. For example, with product lines such as E.C.N., Nutricia must locate appropriate partners which will enable the company to enter new high growth markets and tap into their research and specialised knowledge of local markets, not to mention their understanding of regulatory issues in the market concerned. This not only applies to the developing market, but also to the most sophisticated market for these products, namely the U.S.A.

Nutricia should react to cost and response time pressures by adopting Kaizen production philosophy and information management strategies.

The concentration of its sales and profits in the Benelux countries exposes the company to attacks from larger and financially more powerful competitors. As Nutricia globalizes, it will need to use more sophisticated financial instruments and to actively seek internationalization of management.

It was the students‟ opinion that Nutricia possesses the size and flexibility to make the changes outlined in their report. Once these recommendations were implemented, Nutricia would become a global player in scientific nutrition.

The Mixed Blessing of Success: Eat or Be Eaten

Van der Wielen‟s original realization that some new strategic vision was needed for his company stemmed from the paradoxical nature of the situation in which it found itself in the early 1990s. It was experiencing a growing internationalization, while at the same time going through a decentralization of authority, together with a renewed emphasis on core competencies, pushed through from its highest management levels. These developments had indeed contributed to the company‟s remarkable success - it had ever-growing profits, an up-to-date business structure and a fantastic stock price record6 - but this success had become a mixed blessing. Nutricia started to encounter what it meant to be a dominant player in the sensitive market for baby food; genetic modification issues and product recalls went hand in hand with becoming one of the stars of the Dutch stock exchange. More significantly, this success also meant that Nutricia was itself becoming an attractive acquisition target, so that its independence was potentially at risk. Rumors started that Nutricia was in play. When considering acquisitions in fast moving consumer goods industries, the multinationals operating in both food products and pharmaceuticals first look at the branded products which have a good margin and a strong market share in order to strengthen their portfolio. When one considers that Nutricia operates in specialized markets and has an extremely high market share in several countries as well, one can understand the attractiveness of Nutricia as a take-over candidate. The company‟s price/earnings multiple at the time when it first started to become a take-over candidate (for example, P/E = 18.7 in 19927) made it all the more attractive. Although there were protection mechanisms in place, “If someone offers twice the share price, the management will start to sweat”, declared Van Veen, Executive Vice-President.

6 See Appendix I, II, III and IV. 7 Source: Barclays de Zoete Wedd Nederland, 7 April 1994

17

Things got even more dangerous in 1993, when Unigate (UK), which controlled 29% of Nutricia‟s shares, informed Nutricia about its intention to sell off its interest. Unigate suggested the sale either in a share offer or to a strategic partner. “You can imagine the danger”, said Mr. van Veen. Nutricia tried to control the process. Unigate agreed to Nutricia‟s active role in negotiating with a strategic partner. Nutricia‟s strategy was to stay independent by finding a partner who would agree to stay in a minority position and would “swap” the 29% from Unigate. The idea was that the new partner would bring its specialised food division into Nutricia and that Nutricia would manage the bigger company. The strategic partner could be offered a Board seat. Talks started with Danone, Heinz, Sandoz and others which showed immediate interest. However, in the end they all wanted the option to control 100% of Nutricia someday, so ultimately no such deal was possible. All the while, however, Nutricia was gaining time and taking the opportunity to improve its profitability and boost its share price (which had grown from year-end price of 57.50 Dutch guilders in 1992 to 129.80 Dutch guilders in 1995). With such a price increase, Unigate preferred a share offer, so that in the end the shares were quietly placed with institutional shareholders. The threat of losing 29% of the shares in rival hands was over. However, Nutricia still remained an attractive target with market capitalisation of about 2.5 billion which could be worth 5 to 6 billion to an interested multinational. “We needed two things”, said van der Wielen, ”high profits and a high share price.” The increase in the share price was stimulated by all the rumors during the Unigate affair and the positive institutional bulletins predicting growing profitability in the future. At the same time, Nutricia was itself a suitor. With the goal in mind of fully focusing its product portfolio, Nutricia tried to exchange some of its activities with a division of Friesland Dairy Foods, a 4.5 billion turnover dairy co-operative. The idea was to hand over the fast moving consumer goods operation of Chocomel, Fristi and Nutroma in Belgium for all the I.M.F. activities of Friesland Dairy Foods. Unfortunately, in the end the parties announced that they could not reach an agreement. But there was another strong player in Europe - Milupa, with particularly strong positions in its home market in Germany and in France. Nutricia had repeatedly approached Milupa in the past with a view to running a joint operation. Despite this, when J.P. Morgan (Milupa‟s investment bank) called Mr. van Veen in mid-1995 it was merely to announce the auction of the German company, not to invite Nutricia to participate in the bid. Many U.S.-based corporations, particularly Heinz, had already demonstrated a strong interest in Milupa‟s shares. But Nutricia was interested, too; as van der Wielen stated in an interview at the time, “Milupa would be worth at least twice as much if managed the way Nutricia is.” Eventually it managed to enter the bidding process, if a bit late. Working under pressure, the company‟s executives quickly formulated their first bid, and then managed to receive the invitation to go further in the process with a “due diligence” investigation. In the end, the company outsmarted the competitors by winning Milupa for itself.

18

The acquisition of Milupa activities was successfully financed partly by the direct placement of depository receipts of shares of almost 10% with a limited number of institutional investors, as well as by the issue of a subordinated convertible debenture loan8. Its purchase price turned out to be approximately NLG 900 million, but the rapid integration of Milupa‟s assets and operations with Nutricia‟s contributed 46 million to operating profits even by the end of 1995. Total cost reductions from integrating Milupa amounted to 80 million in 1996; together with additional synergetic gains of 50 million in 1997 and 1998, this brought the total savings made possible by the acquisition to 130 million9. In light of the Milupa take-over and the continued impressive performance of the Nutricia group generally, many now consider that Nutricia is no longer in imminent danger of losing its own independence. Indeed, the company‟s share price has generally exceeded 200 Dutch guilders and even reached a record high of NLG 313 per share at the beginning of 1997. This means of course that any take-over would be very difficult and expensive, especially in view of the significant premium over the share price that is necessary in such cases to induce investors to deliver their shares. Still, competitors like Nestlé and Unilever might yet be interested in acquiring Nutricia. The other giant posing a potential threat is Novartis, newly-formed as the result of a merger between Ciba Geigy and Sandoz. This Novartis, together with Unilever, are corporate predators which potentially have plenty of cash to finance such an acquisition.

8 Nutricia Annual Report, 1995 9 ABN-Amro Hoare Govett, August 1996

19

Appendices

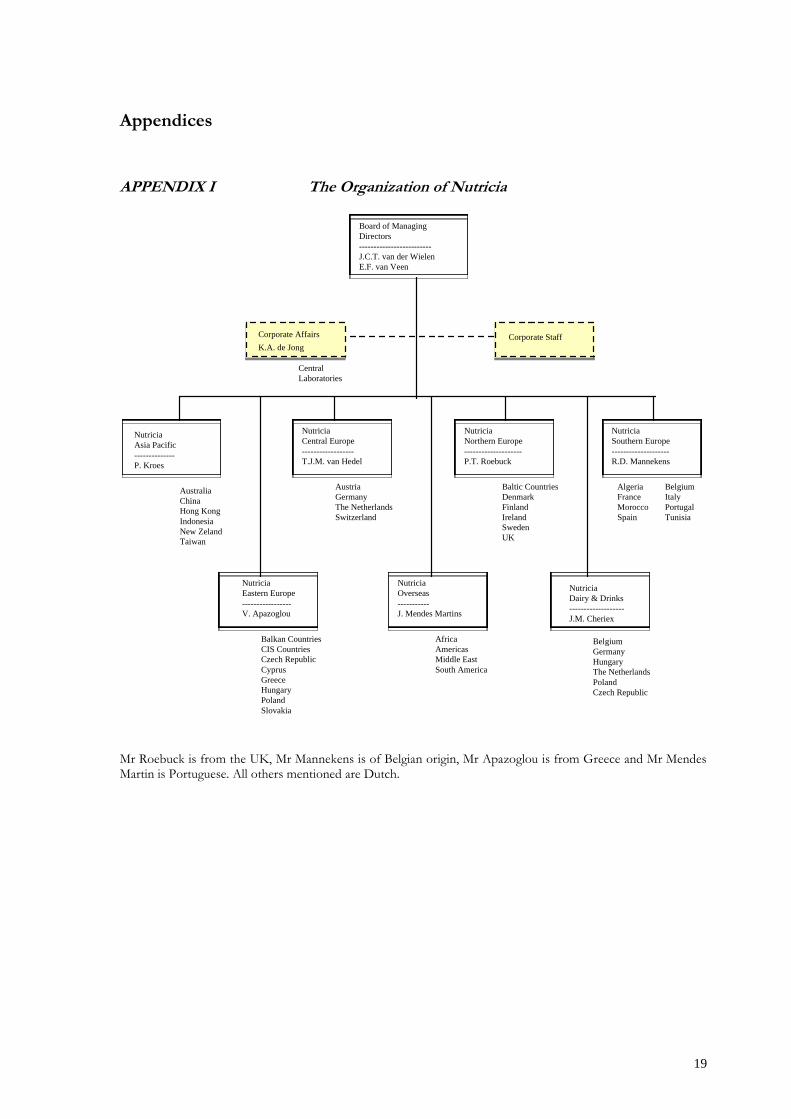

APPENDIX I The Organization of Nutricia

Mr Roebuck is from the UK, Mr Mannekens is of Belgian origin, Mr Apazoglou is from Greece and Mr Mendes Martin is Portuguese. All others mentioned are Dutch.

Nutricia

Southern Europe

--------------------

R.D. Mannekens

Nutricia

Northern Europe

--------------------

P.T. Roebuck

Nutricia

Asia Pacific

--------------

P. Kroes

Nutricia

Central Europe

------------------

T.J.M. van Hedel

Nutricia

Eastern Europe

-----------------

V. Apazoglou

Nutricia

Overseas

-----------

J. Mendes Martins

Nutricia

Dairy & Drinks

-------------------

J.M. Cheriex

Corporate Staff

Board of Managing

Directors

-------------------------

J.C.T. van der Wielen

E.F. van Veen

Central

Laboratories

Austria

Germany

The Netherlands

Switzerland

Baltic Countries

Denmark

Finland

Ireland

Sweden

UK

Algeria Belgium

France Italy

Morocco Portugal

Spain Tunisia

Australia

China

Hong Kong

Indonesia

New Zeland

Taiwan

Balkan Countries

CIS Countries

Czech Republic

Cyprus

Greece

Hungary

Poland

Slovakia

Africa

Americas

Middle East

South America

Belgium

Germany

Hungary

The Netherlands

Poland

Czech Republic

Corporate Affairs

K.A. de Jong

20

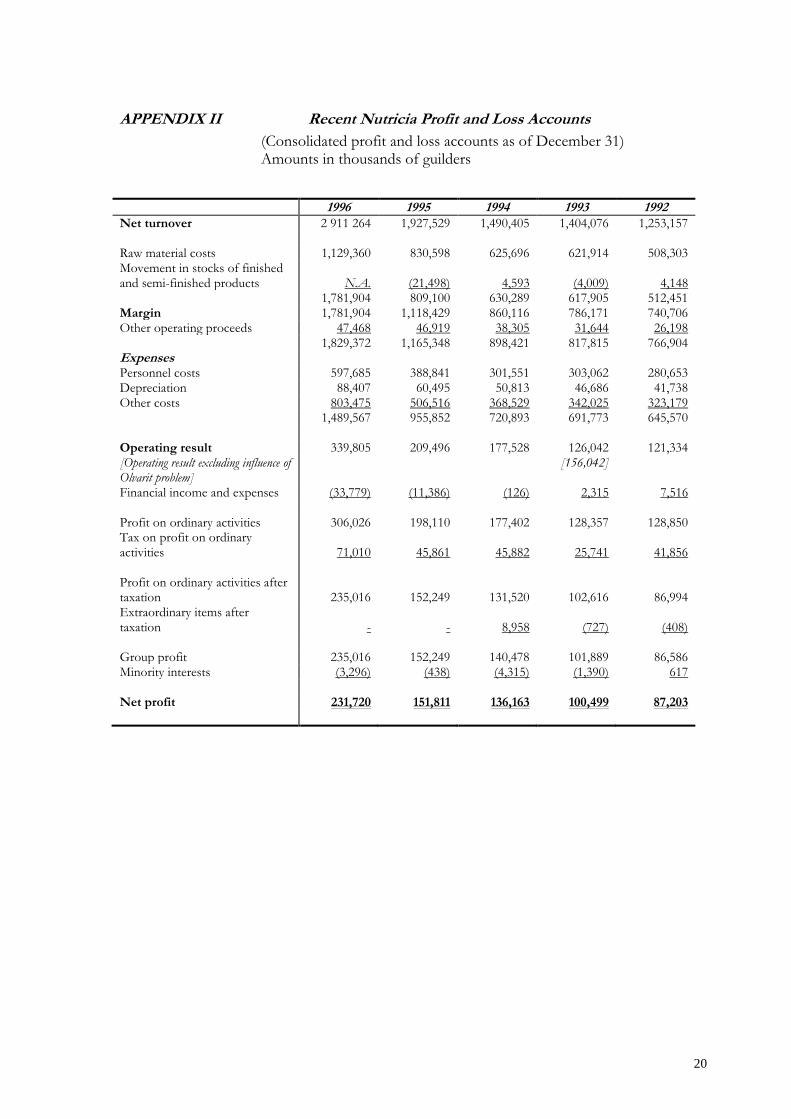

APPENDIX II Recent Nutricia Profit and Loss Accounts

(Consolidated profit and loss accounts as of December 31) Amounts in thousands of guilders

1996 1995 1994 1993 1992 Net turnover 2 911 264 1,927,529 1,490,405 1,404,076 1,253,157 Raw material costs 1,129,360 830,598 625,696 621,914 508,303 Movement in stocks of finished and semi-finished products

N.A.

(21,498)

4,593

(4,009)

4,148

1,781,904 809,100 630,289 617,905 512,451 Margin 1,781,904 1,118,429 860,116 786,171 740,706 Other operating proceeds 47,468 46,919 38,305 31,644 26,198 1,829,372 1,165,348 898,421 817,815 766,904 Expenses Personnel costs 597,685 388,841 301,551 303,062 280,653 Depreciation 88,407 60,495 50,813 46,686 41,738 Other costs 803,475 506,516 368,529 342,025 323,179 1,489,567 955,852 720,893 691,773 645,570 Operating result 339,805 209,496 177,528 126,042 121,334 [Operating result excluding influence of Olvarit problem]

[156,042]

Financial income and expenses (33,779) (11,386) (126) 2,315 7,516 Profit on ordinary activities 306,026 198,110 177,402 128,357 128,850 Tax on profit on ordinary activities

71,010

45,861

45,882

25,741

41,856

Profit on ordinary activities after taxation

235,016

152,249

131,520

102,616

86,994

Extraordinary items after taxation

-

-

8,958

(727)

(408)

Group profit 235,016 152,249 140,478 101,889 86,586 Minority interests (3,296) (438) (4,315) (1,390) 617 Net profit 231,720 151,811 136,163 100,499 87,203

21

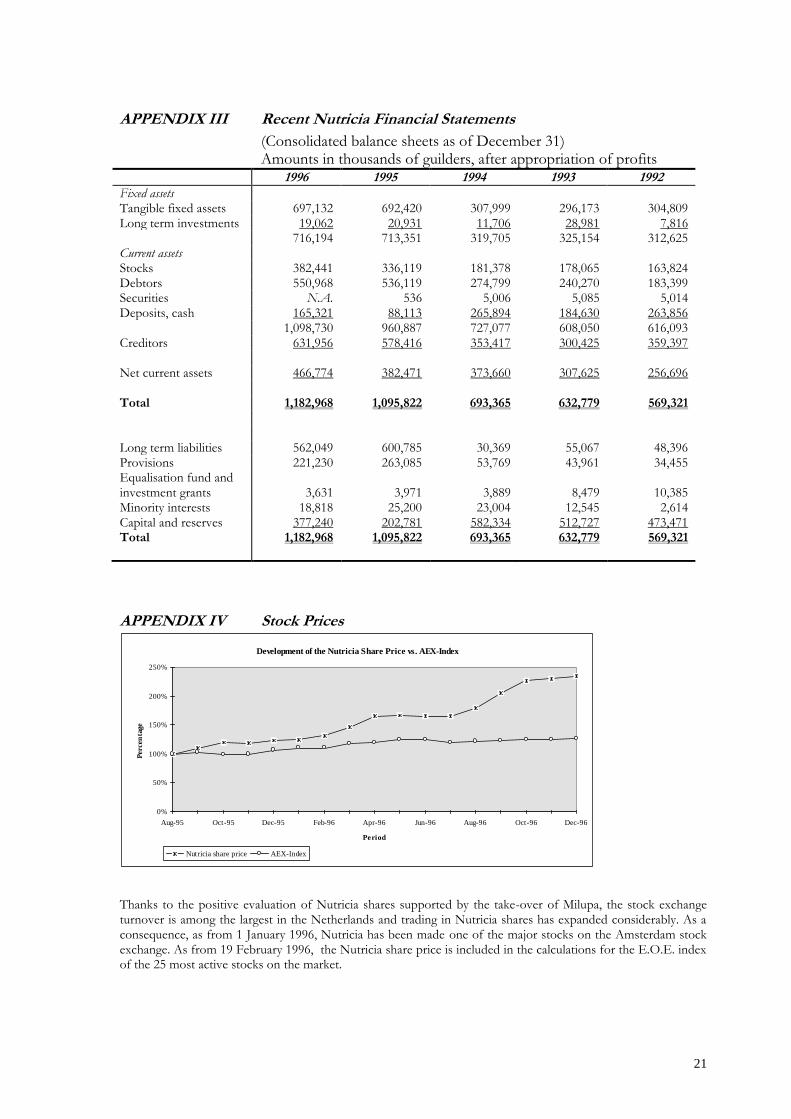

APPENDIX III Recent Nutricia Financial Statements

(Consolidated balance sheets as of December 31) Amounts in thousands of guilders, after appropriation of profits

1996 1995 1994 1993 1992 Fixed assets Tangible fixed assets 697,132 692,420 307,999 296,173 304,809 Long term investments 19,062 20,931 11,706 28,981 7,816 716,194 713,351 319,705 325,154 312,625 Current assets Stocks 382,441 336,119 181,378 178,065 163,824 Debtors 550,968 536,119 274,799 240,270 183,399 Securities N.A. 536 5,006 5,085 5,014 Deposits, cash 165,321 88,113 265,894 184,630 263,856 1,098,730 960,887 727,077 608,050 616,093 Creditors 631,956 578,416 353,417 300,425 359,397 Net current assets 466,774 382,471 373,660 307,625 256,696 Total 1,182,968 1,095,822 693,365 632,779 569,321 Long term liabilities 562,049 600,785 30,369 55,067 48,396 Provisions 221,230 263,085 53,769 43,961 34,455 Equalisation fund and investment grants

3,631

3,971

3,889

8,479

10,385

Minority interests 18,818 25,200 23,004 12,545 2,614 Capital and reserves 377,240 202,781 582,334 512,727 473,471 Total 1,182,968 1,095,822 693,365 632,779 569,321

APPENDIX IV Stock Prices

Thanks to the positive evaluation of Nutricia shares supported by the take-over of Milupa, the stock exchange turnover is among the largest in the Netherlands and trading in Nutricia shares has expanded considerably. As a consequence, as from 1 January 1996, Nutricia has been made one of the major stocks on the Amsterdam stock exchange. As from 19 February 1996, the Nutricia share price is included in the calculations for the E.O.E. index of the 25 most active stocks on the market.

Development of the Nutricia Share Price vs. AEX-Index

0%

50%

100%

150%

200%

250%

Aug-95 Oct-95 Dec-95 Feb-96 Apr-96 Jun-96 Aug-96 Oct-96 Dec-96

Period

Percen

tage

Nutricia share price AEX-Index

22

APPENDIX V Core and Other Activities

Product Groups 1996 x Dfl. 1,000

1995 x Dfl. 1,000

1994 x Dfl. 1,000

1993 x Dfl. 1,000

1992 x Dfl. 1,000

Infant milk formulae 1,095,426 640,396 484,950 514,898 405,904 Cereals 207,892 104,511 66,444 185,99210 202,127 Meals, drinks and juices 286,188 191,724 147,838 Enteral clinical nutrition and administrative systems

349,552

280,459

242,714

248,55911

222,628

Dietary products and health food

211,046

166,794

80,535

Skin (and throat) care products 58,407 35,255 24,967 26,849 30,891 Core activities 2,208,511 1,383,884 1,022,481 949,449 830,659 Milk-based drinks, sports drinks, coffee cream, etc.

479,966 379,933 381,154 384,910 378,723

Other products 222,787 128,457 61,803 42,868 12,884 Other activities 702,753 543,645 467,924 454,627 422,498 Total 2,911,264 1,927,529 1,490,405 1,404,076 1,253,157

for babies and toddlers

In the year 1996 Nutricia switched part of its product range from “Other activities” to the “Core activities”: skin care and throat care became a core activity. On the other hand the sports drinks became a non-core activity. In the years 1992, 1993, 1994 and 1995 the turnover of the sports drinks is included in the category “Dietary products and health food”.

Product Groups 1996 %

1995 %

1994 %

1993 %

1992 %

Infant milk formulae 37.6 33.2 32.5 36.7 32.4 Cereals 7.2 5.4 4.5 13.2 16.1 Meals, drinks and juices 9.8 9.9 9.9 Enteral clinical nutrition and administrative systems

12.0

14.6

16.3

17.7

17.8

Dietary products, sport and health food

7.3

8.7

5.4

Skin (and throat) care products 2.0 1.8 1.7 1.9 2.5 Core activities 75.9 73.6 70.3 69.5 68.8 Milk-based drinks, sports drinks, coffee cream, etc

16.4

19.7

25.6

27.4

30.2

Other products 7.7 6.7 4.1 3.1 1.0 Other activities 24.1 26.4 29.7 30.5 31.2 Total 100.0 100.0 100.0 100.0 100.0

for babies and toddler

The acquisitions of Milupa, S.H.S., Deva (a production plant in the Czech Republic) and Istra made important contributions to the rise in the percentage volume of the primary core activities.

10 Combines the total of „cereals‟ and „milk, drinks and juices‟. This also applies to 1992. 11 Combines the total of „Enteral Clinical nutrition and administrative systems‟ and „dietary products, sport and health food‟. This also applies to 1992.

23

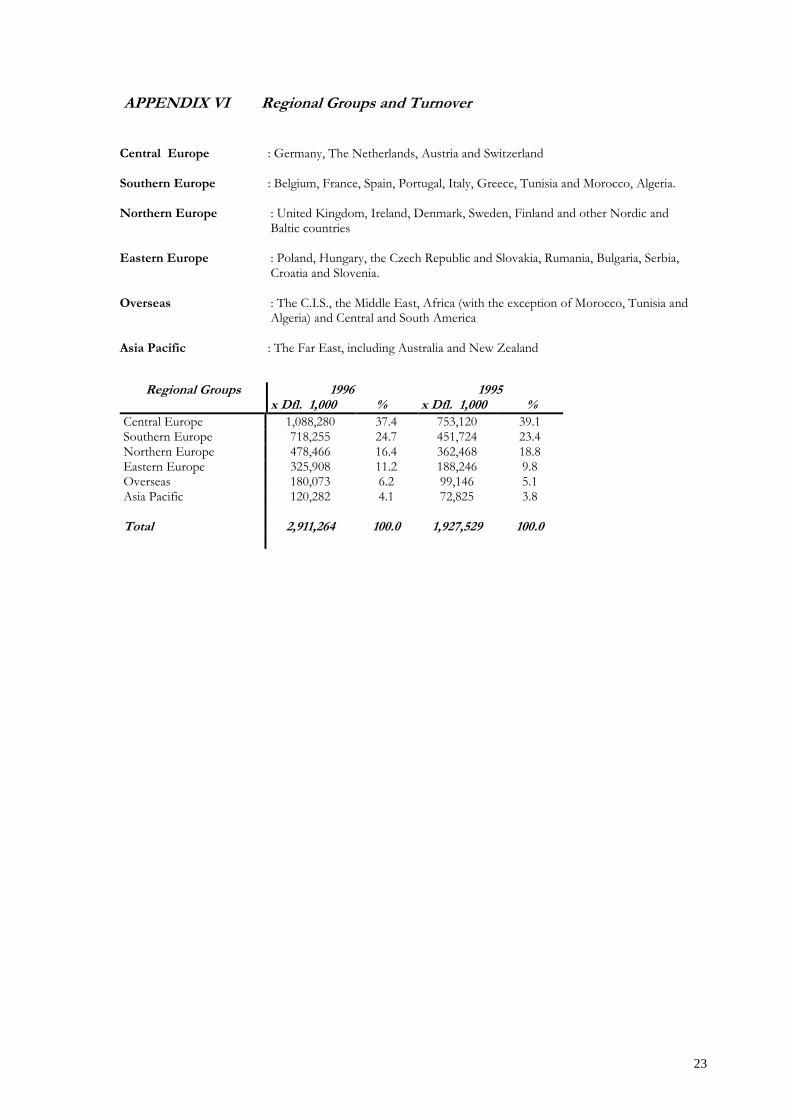

APPENDIX VI Regional Groups and Turnover

Central Europe : Germany, The Netherlands, Austria and Switzerland Southern Europe : Belgium, France, Spain, Portugal, Italy, Greece, Tunisia and Morocco, Algeria. Northern Europe : United Kingdom, Ireland, Denmark, Sweden, Finland and other Nordic and

Baltic countries Eastern Europe : Poland, Hungary, the Czech Republic and Slovakia, Rumania, Bulgaria, Serbia,

Croatia and Slovenia. Overseas : The C.I.S., the Middle East, Africa (with the exception of Morocco, Tunisia and

Algeria) and Central and South America Asia Pacific : The Far East, including Australia and New Zealand

Regional Groups 1996 x Dfl. 1,000 %

1995 x Dfl. 1,000 %

Central Europe 1,088,280 37.4 753,120 39.1 Southern Europe 718,255 24.7 451,724 23.4 Northern Europe 478,466 16.4 362,468 18.8 Eastern Europe 325,908 11.2 188,246 9.8 Overseas 180,073 6.2 99,146 5.1 Asia Pacific 120,282 4.1 72,825 3.8 Total 2,911,264 100.0 1,927,529 100.0

24

APPENDIX VII Group ratings on various items by the 12 participants

All items could be rated on a scale from one to ten.

Participant Item

1 2 3 4 5 6 7 8 9 10 11 12 Avg.

Research and development

4 4 4 6 6 5 5 3 6 7 7 5 5.17

Information systems

3 5 4 4 3 4 5 4 4 5 5 3 4.08

Product innovation

5 5 8 6 7 6 6 6 7 6 6 7 6.25

Societal concern

4 6 5 4 6 7 6 3 4 5 6 4 5.00

Cultural responsiveness internally

4 5 4 3 4 5 4 1 8 5 6 4 4.42

Low cost operation

5 6 7 6 4 7 6 7 6 8 7 6 6.25

Reliable image

9 7 9 7 8 8 8 9 8 8 8 5 7.83

Quality image

9 7 8 9 6 5 8 9 7 8 8 6 7.50

Innovation image

9 7 7 8 7 7 7 8 7 7 7 4 7.08

Management style (openness)

5 4 4 6 5 4 4 9 5 6 6 4 5.12

Speed

5 6 7 6 8 5 7 5 6 6 6 6 6.08

Customer service package

5 7 9 6 7 6 8 6 6 6 5 5 6.33

Growth driven

5 5 4 3 4 6 5 6 4 4 6 5 4.75

Profit driven

7 7 8 7 8 8 8 6 8 8 9 8 7.67

25

Appendix VIII Some of the Results of the Project Teams

Some examples of actions that were suggested by the project team focusing on Culture

ACTION ELEMENT OF CULTURE

1. Project group that analyses existing products, packaging, PR, and advertising - how do they fit with each element of the identified corporate culture, e.g. nutrition dedication, etc. Undertake a value analysis of our products with competition on the element of nutrition dedication. Introduce an ongoing competitive analysis system (production and marketing)

Nutritionally dedicated Leading Professionally run

2. Do our building/demonstrate “leading”? Should we invest in this image?

Undertake research on what consumers and HCP‟s understand by nutritional dedication. How do they see Nutricia in this area? Is there a gap? How do we close this gap?

Leading, Reliable, Nutritionally dedicated, Leading, Caring

3. Review branding in the light of the new corporate identity (plus logo, annual report, promotions, etc.)

All

4. Install a PR programme 1996/97 where you communicate Nutrition dedication, caring, and leading. Maybe look at Nutricia Corporate advertising? (Hire professional outside consultants to do this)

All

5. Look for acquisitions that particularly strengthen our image nutritionally dedicated.

Nutritionally dedicated Leading

Some examples of actions that were suggested by the project team focusing on Communication

ACTION

1. Let the NEC define the corporate vision, mission, competitive advantage, key success factors, core competencies, major strategic action-plans and priorities and present these at Lauswolt. Use Lauswolt to modify and finalise these ideas.

2. Organise a yearly recurring meeting preferable in May or June between TOP 50 and NEC to discuss strategy and to socialise. this meeting should take place prior to the budgeting cycle and should not necessarily be organised in Holland.

3. Organise a yearly SBU-strategy meeting. During this meeting which should preferable take place in February, the Corporate Chairman should present last year‟s results and initiate a discussion on strategy.

26

Some of the core competencies described by the project team focusing on Core Competencies

No.

Core Competence Priority

1. Marketing

identifying customer needs (locally and internationally)

fast and flexibly translating these needs into product concepts

co-operating internationally in marketing products

I

2. Caring for people

I

3. Translating medical and health sciences into new nutritional concepts

I

4. Translating nutritional concepts into commercial concepts

I

Some examples of actions that were suggested by the project team focusing on Core Competencies

ACTION

1. Accelerate the “construction” of networks with medical and health specialist who are working in areas of expertise which are relevant to Nutricia: ECN, IMF, Functional Foods.

2. Provide a clear statement of Vision, Objectives and Strategy to all levels of the organisation via the hierarchy.

3. File for ISO accreditation.

4. Stimulate awareness of the benefits of appropriate international co-operation at the highest level of the organisation.

5. Install a New Business Development Manager (NBDM) per region.

27

Appendix IX Letter of the C.E.O. concerning Milupa and Michelangelo

JF/EP 9319 18 September 1995 Dear ........................................, As holidays are over now, this is a good moment to refresh our thoughts of the General Management Meeting in Lauswolt. It was very inspiring to see how a great number of people with different backgrounds are daily busy to achieve our main objective: to become the world leader in specialised nutrition. To become a leader is not a static but a dynamic process that requires everyone‟s permanent attention. As you know, this year we started the Michelangelo-project. Michelangelo was the start of a long stretch in which we determine our future goals. Lauswolt was not the end of this project, just a break to make an inventory. What we say is important, but the only thing that counts is what we do. In Lauswolt, nearly 50 different points of action have been presented. As you will understand we cannot deal with all these subjects at the same time and must focus on priorities. We selected 6 items varying from Product Marketing Strategy to Management Development, from E-mail to Communication. A short list of these items is attached to this letter. CMT‟s special project teams will thoroughly look at these items to advise the Management of Nutricia. They will be responsible for implementation and communication of the various projects. The remaining points of action will be looked at at a later moment. Better communication is one of our priorities and to start with we enclose a videotape with presentations given in Lauswolt, directly linked to Michelangelo. You can use this videotape in your company as a tool to show your staff our ideas of Michelangelo. We also enclose an English translation of a Dutch document about the take-over of Milupa. This publication has been sent to all Nutricia employees in the Netherlands and might give you some ideas of how to communicate this take-over in your company. On the floppy you will find all figures belonging to the next. We will inform you about the progress of Michelangelo and the integration process of Milupa from time to time. With personal regards, Hans van der Wielen President

28

THE SIX ITEMS SELECTED FROM ALL ITEMS PRESENTED IN LAUSWOLT PRODUCT MARKETING STRATEGY 1. Realise that synergies between countries will increase as time continues 2. Actively manage the synergies by identifying and utilising them in order to increase profit and market power 3. Find the appropriate structure to accomplish this 4. Evaluate products (branding and packaging) in the light of the culture statement (professional, leading and

nutritionally dedicated) 5. Introduce an ongoing competitive analysis system (production and marketing) 6. Undertake a value analysis of our products with competition on the element of nutrition dedication 7. Publish a Nutrition Standard Book or use electronic highway to strengthen our image as nutritionally

dedicated 8. Design an annual score card for customer care-benchmarks (mainly logistics) Standardised for all Nutricia

companies Note that we should base these on customers‟ perceptions 9. Distribute product information booklet PUBLIC RELATIONS 1. Install a PR programme 1996/97 where you communicate Nutrition dedication, caring and leading. Look into

at Nutricia Corporate Advertising. 2. Re-institute a Corporate Newsletter MANAGEMENT DEVELOPMENT 1. Develop an approach which allows you to continuously invest in the development of your Top Management

and Young Potentials. 2. Design an international training program focusing on functional skills that allows you to communicate and

build culture, understanding of vision and mission, respect for key corporate values and norms. 3. Invest in the development of a strong and uniform esprit de corps among the top people. HELPDESK 1. Define a Helpdesk concept.

use a system whereby small countries (e.g. Hungary) can use larger centres to ask questions and then pass back the answer how to play a “leading” role even in emerging markets

E-MAIL/INTERNET 1. Install an international E-mail network and bring Nutricia on Internet STYLE&COMMUNICATION Organise a two-yearly recurring meeting preferably in May or June between TOP 50 and NEC12 to discuss strategy.

12Nutricia Executive Committee