Embed Size (px)

Citation preview

NSEL: A Scam or a Risk Management failure ?

Date – October 8, 2013 Prepared by – RMG Audit Team

1 of 27

INDEX

I. BACKGROUND - COMMODITY AND SPOT EXCHANGES 3

II. REGULATORY STRUCTURE & HISTORY 4

III. NSEL's INCEPTION 5

IV. VYAZ BADLA - THE SO CALLED RISK FREE PRODUCT 7

V. LEGAL VIOLATIONS 9

VI. THE BEGINNING OF THE FALL 10

VII. EXPOSURE TO BANKING INDUSTRY 12

VIII. FALSE CLAIMS BY NSEL & SUBSEQUENT DEVELOPMENTS 13

IX. CONCLUSION 15

ANNEXURE 1 – DETAILED DESCRIPTION OF EVENTS 17

ANNEXURE 2 – REFERENCES 27

2 of 27

I. BACKGROUND - COMMODITY & SPOT EXCHANGES

A commodity exchange is an exchange where various commodities and their derivative products are traded. Most commodity markets across the world trade in agricultural products and other raw materials (like wheat, barley, sugar, maize, cotton, cocoa, coffee, milk products, pork bellies, oil, metals, etc.) and contracts based on them. These contracts can be spot contracts, forwards, futures and options on futures. Other sophisticated products may include environmental instruments, swaps, or ocean freight contracts.

In this document, we shall focus on National Spot Exchange Ltd. (NSEL). NSEL & Multi Commodity Exchange (MCX) were promoted by Financial Technologies (FTIL). NSEL allowed trading in spot contracts in commodities (delivery based contracts) & MCX allows trading in commodity derivatives.

Set up in 2003, MCX was the first commodity derivative exchange in India. Besides NSEL & MCX, there are various other commodity exchanges recognized for allowing trading of various commodities. Following are some of the exchanges:

1. National Commodity and Derivatives Exchange, Mumbai and 2. National Multi Commodity Exchange, Ahmedabad, 3. Indian Commodity Exchange Ltd., Mumbai and 4. ACE Derivatives and Commodity Exchange.

Over ` 20 lakh crore of agricultural commodities are traded in India every year. Spot exchanges are electronic platforms similar to mandis where the buyer and seller exchange goods for money. All transportable commodities that can be stored in warehouses can be traded on commodity spot exchanges. Castor seeds, jeera, paddy and castor oil are among the most popular commodities on spot exchanges. Spot exchanges came into picture in 2007 by way of a government notification.

3 of 27

II. REGULATORY STRUCTURE & HISTORY

The Forward Markets Commission (FMC) is the regulator of forwards and futures markets in India. Post-independence, in the 1950s, India continued to struggle with feeding its population and the government increasingly restricting trading in food commodities. The government felt that derivative markets increased speculation which led to increased costs and price instabilities. In 1953, the Forward Contracts (Regulation) Act, 1952 (FCRA) finally prohibited options and futures trading altogether and FMC was designated as the regulator of commodity forwards and commodity futures markets.

On the basis of recommendations of the Khusro Committee (June 1980), government allowed futures trading in potatoes during the latter half of 1980. Futures trading was also resumed in castor seed, and gur (jaggery), and in 1992, extended to Hessian (Jute). In April 1999, futures trading was permitted in various edible oilseed complexes.

Department of Consumer Affairs appointed FMC as the designated regulator of spot exchanges in February 2012, but the FMC was only empowered to seek information and periodic submission of trading data by spot exchanges. Spot trading at the mandi is done under state laws and trading licenses are provided by State Agricultural Produce Market Committees (APMCs). It may be noted that SEBI doesn't have any role to play in regulating commodity exchanges.

After the NSEL crisis broke, FMC was shifted to Department of Economic Affairs, Ministry of Finance in September 2013.

4 of 27

III. NSEL's INCEPTION

NSEL was set up by Financial Technologies (India) Ltd (FTIL) – a company promoted Jignesh Shah . NSEL commenced “Live” trading in October 2008 and within months captured a bulk of the electronic spot market. When on 1st June 2007, the Department of Consumer Affairs (DCA) granted three entities - NSEL, NCDEX Spot and R-Next approval to set-up spot exchanges, it stipulated that they undertake only ‘ready contracts’.

As per FCRA, a ready delivery contract is a spot transaction with delivery of goods within 11 days & a forward contract is a contract which is not a ready delivery contract. In trade parlance, a ready delivery contract is called a T+10 contract. Spot exchanges are also allowed to offer 1 day forward contracts – that is, trading in warehouse receipts and intra-day netting of transactions – but since these are forward contracts and forward contracts are not permitted on spot exchanges (under FCRA), the exchanges have been given a specific exemption to allow 1 day forward contracts in 2007 by way of a Government Notification. Spot exchanges have to also adhere to the conditions that all outstanding positions will result in physical delivery and that the exchange will not allow any short selling on its platform. Although, spot exchanges had a set of rules to play by, no regulator was given the task to enforce these rules from 2007 to 2012.

When the NSEL commenced operations in October 2008, its objective was to help commodity producers find buyers. Spot exchanges normally offer T+2 contracts. If you purchased on the exchange, you paid your dues within two days and took delivery of whatever you had bought, whether castor seed or wool, the next day.

5 of 27

However, as that didn't bring volumes to the exchange, in 2010, NSEL introduced forward contracts that could be executed over 30 to 35 days. In other words, the settlement cycle was given another dimension. Now there were two settlement cycles: a 2-day cycle and a longer one that extended up to 35 days. As trades between two contracts go, arbitrageurs enter only when there is a huge difference between what they buy and what they sell. However, NSEL took it to another level i.e. there was a pattern to its price-discovery mechanism. The 30-35 days forward contract price, for instance, for all commodities was always higher than the 2-day forward contract price. As per Shankar Raman of Centrum Wealth Management: The prices were so funny that all the time there was about 15 % forward gap. There will always be a carrying cost, but a fixed 15-18 % is unheard off.

Commodity prices should fluctuate, but they didn't on the NSEL. If the spot price of a two-day contract was "x", the thirty-day contract price was one or two % more than "x". An investor simply bought the two-day spot contract and sold the thirty-day contract i.e. investor paid for the two-day contract and waited for the 30-day contract to sell the commodity at a higher price. That changed the fortunes of the NSEL. Monthly trading volumes on an average shot up from ` 1,000 crore in 2009-10 to ` 28,000 crore in May 2013. FTIL, the promoter, derived 57% of its profits from the exchange. The higher the trading turnover, the higher the revenues an exchange makes.

6 of 27

IV. VYAZ BADLA - THE SO CALLED RISK FREE PRODUCT

The transaction involves mill owners or planters, the spot exchange and brokers acting as financiers on behalf of their retail and HNI clients. In the first phase, a mill owner buys the produce on the NSEL or from mandis using cash or agri-finance largely from PSU banks. The stocks bought are stored at warehouses managed by NSEL / National Bulk Handling Corporation Ltd. (NBHC) - an FTIL Group Entity. Warehouse Receipts issued against the physical stocks are then traded on the NSEL.

Once this first step of the transaction is completed, the ‘vyaz badla’ cycle starts. In what is called a pair trade - the Mill owner sells the produce to the financier on the exchange platform under a T+3 or T+5 settlement cycle (Ready Contract). It means, warehouse receipt is delivered & money changes hands at T + 3/T + 5.

The mill owner simultaneously enters a long term higher price forward contract to buy the stock from the financier at the end of 25 days or 30 days or 35 days. At the end of the tenure these contracts are rolled over. The mill owner recovers his money, the financier get the difference between the two contract prices amounting to an approximately 14-16 % p.a. return. It appears to be a risk free return as the financier holds a warehouse receipt for the goods and NSEL stands counter-party guarantee to any transaction failure. It may be noted that NSEL was allowed to undertake only T+1 Forward Contracts but in realty NSEL allowed T + 25 / 30 / 35 forward contracts. This Vyaz Badla product and its many cousins survived on continuous rollovers or new money. Castor seed, castor oil, cotton wash oil, paddy, steel were the 5

7 of 27

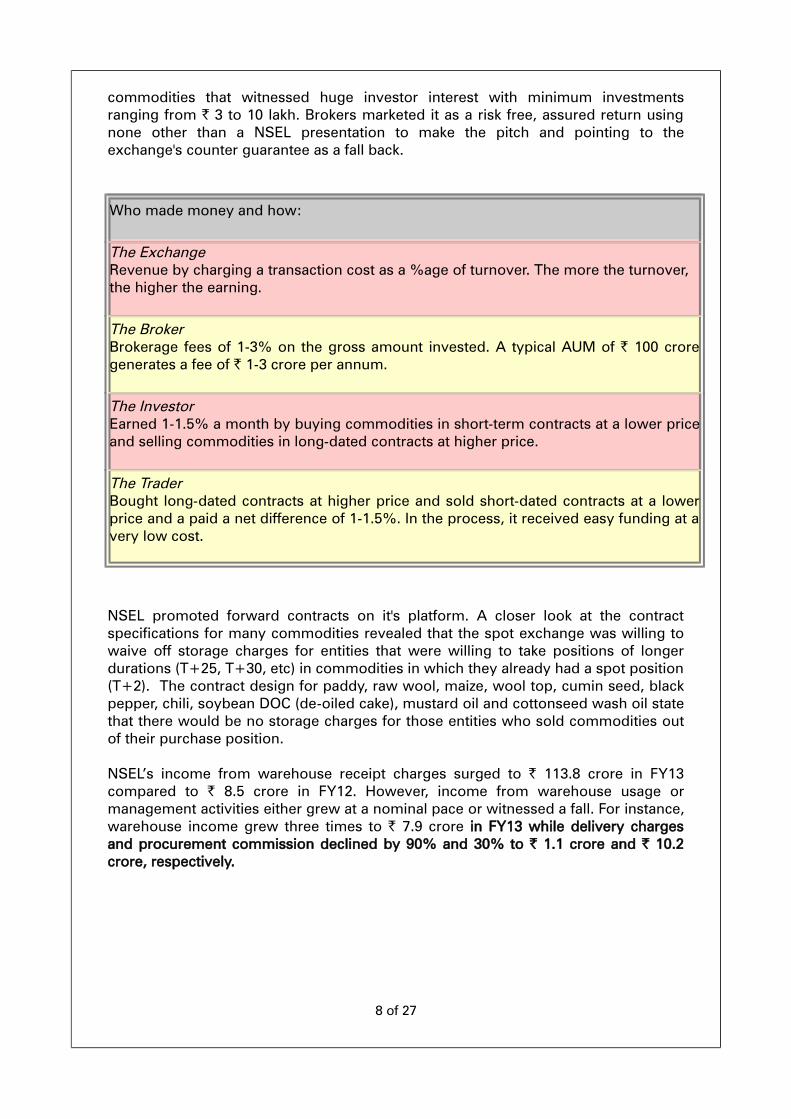

commodities that witnessed huge investor interest with minimum investments ranging from ` 3 to 10 lakh. Brokers marketed it as a risk free, assured return using none other than a NSEL presentation to make the pitch and pointing to the exchange's counter guarantee as a fall back.

Who made money and how:

The ExchangeRevenue by charging a transaction cost as a %age of turnover. The more the turnover, the higher the earning.

The BrokerBrokerage fees of 1-3% on the gross amount invested. A typical AUM of ` 100 crore generates a fee of ` 1-3 crore per annum.

The InvestorEarned 1-1.5% a month by buying commodities in short-term contracts at a lower price and selling commodities in long-dated contracts at higher price.

The TraderBought long-dated contracts at higher price and sold short-dated contracts at a lower price and a paid a net difference of 1-1.5%. In the process, it received easy funding at a very low cost.

NSEL promoted forward contracts on it's platform. A closer look at the contract specifications for many commodities revealed that the spot exchange was willing to waive off storage charges for entities that were willing to take positions of longer durations (T+25, T+30, etc) in commodities in which they already had a spot position (T+2). The contract design for paddy, raw wool, maize, wool top, cumin seed, black pepper, chili, soybean DOC (de-oiled cake), mustard oil and cottonseed wash oil state that there would be no storage charges for those entities who sold commodities out of their purchase position.

NSEL’s income from warehouse receipt charges surged to ` 113.8 crore in FY13 compared to ` 8.5 crore in FY12. However, income from warehouse usage or management activities either grew at a nominal pace or witnessed a fall. For instance, warehouse income grew three times to ` 7.9 crore in FY13 while delivery charges and procurement commission declined by 90% and 30% to ` 1.1 crore and ` 10.2 crore, respectively.

8 of 27

V. LEGAL VIOLATIONS

The VYAZ badla product may have been ingenious but it was also illegal. Because as mentioned earlier, spot exchanges can trade only in ready contracts and one day forward contracts. Under the FCRA the second part of the pair trade or the T+25, T+30 and T+36 contracts amounted to forward contracts – and spot exchanges are not allowed to conduct trade in these contracts.

On February 20, 2012, FMC asked NSEL to explain how 55 contracts on its platform had a settlement period of more than 11 days. FMC found that the Exchange allowed trading on the Exchange platform without verifying whether the seller had the stocks with him or not, thus in effect, allowing short sale by the members.

9 of 27

VI. THE BEGINNING OF THE FALL

The NSEL violations were first noticed by the Financial Stability and Development Council (FSDC) in May 2011. A sub-committee consisting of representatives from the Ministry of Consumer Affairs and the RBI was apprised of the lack of regulatory oversight on spot exchanges and its products.

Eight months later in February 2012, the DCA appointed FMC as the designated regulator of spot exchanges - but the Commission was only empowered to seek information and periodic submission of trading data by spot exchanges. Within days-Feb 21- FMC raised the first alarm (mentioned above).

In April, 2012 the DCA swung to action - also issuing a show cause notice to NSEL. The investigation continued for a year during which FMC submitted to the ministry a draft legislation to regulate spot exchanges. And then on July 13, 2013 the endgame began – the DCA ordered NSEL to settle all existing contracts by their due dates and not issue any further contracts.

But NSEL was stuck with products that either needed to be rolled over or refinanced. With a freeze on new contracts mill owners had no new source of funds and the threat of default loomed large. July 29 marked NSEL’s last successful payout. The July 30th and 31st payouts failed, forcing the Exchange to stop all trading and merge delivery and settlement of all contracts with 15 day deferment. On July 31, the NSEL suspended trade in all contracts except 'e-series'. An estimated 13,000 investors including 7,000 small investors were impacted.

The bourse blamed "loss of trading interest" and "abrupt structural changes in marketplace" for suspension of trade. From an average figure of about ` 1,000 crore daily, within three weeks it came down about ` 200 crore.

10 of 27

On 1st & 2nd August the share price of NSEL's promoter entity FTIL & MCX lost over 72% and 36% value, respectively.

Financial Technologies Share Price Chart during the default period

MCX Share Price Chart during the default period

11 of 27

VII. EXPOSURE TO BANKING INDUSTRY

1. Direct exposure to FT Group:Based on CNBC TV18 reports, fund-based exposure of the banks to FT Group stands at ` 960 crore, non-fund based exposure is at ` 1,930 crore, taking the total exposure to the FT Group to around ` 2900 crore. Although the figure looks large, their net outstanding to defaulting NSEL stands at miniscule ` 288 crore. Following are the exposures of some banks:

InstitutionFund & Non-fund based exposure

(in ` Crore)

HDFC Bank 690

Union Bank 520

Axis bank 352

Indusind Bank 314

Syndicate Bank 166

Kotak Mahindra Bank 137

NOTE: The above list is not an exhaustive list & the bank wise data on the net outstanding amount is not available

2. Exposures based on funding against Warehouse Receipts issued by NBHC (FT Group company):Some 42 banks, including major public and private banks, cooperative banks and regional rural banks, have loaned around `3,500 to 4,200 crore to farmers and traders against warehouse receipts issued by National Bulk Handling Corp. Ltd (NBHC). State Bank of India (SBI) has the maximum exposure of ` 700 crore to NBHC. The list of private sector banks with exposure to the warehousing arm includes ICICI Bank Ltd, HDFC Bank Ltd and Axis Bank Ltd. NBHC does not come under FMC’s regulatory mandate, said Ramesh Abhishek, chairman of the commission.

As far as banking exposure is concerned, NBHC plays the role of warehouse collateral manager and new customer referral agent. This is a case of conflict of interest as it tries to play multiple roles which are meant to be played by independent parties. One such instance, took place in Junagadh, Gujarat, in July when about ` 3 crore worth of jeera (cumin) stocks certified by NBHC were burnt allegedly by the holder to claim insurance. On inspection, the stock turned out to be groundnuts.

12 of 27

State-owned Dena Bank had lent money against the value of the stock based on the certification provided by NBHC. Typically, when customers approach banks for finance, the commodity is stored in a separate warehouse and inspection is done by another external agency.

Set up in 2005, NBHC conducts multiple businesses, including collateral management, leasing warehouses to manage clients’ stocks and procuring commodities from farmers against which bank loans are raised. As of 31 July, 2013, NBHC had over 1,500 warehouses and commodity management facilities under various commercial formats such as leased, franchisee and owned by the firm.

Banks typically give a specific commission to NBHC, say 1%, when the company refers clients. Under current norms, 40% of the loans of commercial banks need to be directed to agriculture, exports and other weaker sections. Lending against warehouse receipts issued against agricultural commodities qualifies as so-called priority sector lending as banks can categorize this as agriculture loans.

13 of 27

VIII. FALSE CLAIMS & SUBSEQUENT DEVELOPMENTS

Following the default, it was found that the exchange did not have adequate stocks to back it's overdue positions & Settlement Guarantee Fund was grossly overstated. The stocks were either missing, low in quantity or of inferior quality. Various government agencies such as FMC, Economic Offences Wing (EOW), Enforcement Directorate, Income Tax Department, the Institute of Chartered Accountants of India initiated the investigations. The FMC was shifted to Ministry of Finance from Ministry of Consumer Affairs & more powers were given to it. The NSEL repeatedly defaulted on it's scheduled payouts & couldn't even pay 15% of it's weekly obligations. Majority of the directors resigned & CEO took the blame on himself for mismanagement. Later, EOW found that 14 of 65 warehouses were non-existent & 30 warehouses did not have any stock. 1/3rd of the defaulting companies were found to be absent on the address registered with NSEL. The detailed description of each event is available in the Annexure 1 (Page 17) in a sequential way.

14 of 27

IX. CONCLUSION

NSEL turned out to be a sham operation, which was using a flimsy regulatory passport, and was running a para-banking operation without a system of securities and collaterals in place. To conclude, there were 6 main reasons for failure:

1. Distortion of meaning of spot transaction / allowing forward transactions: Definition of a ready delivery contract under FCRA is: 'a contract, which provides for the delivery of goods and the payment of a price therefore, either immediately or within such period not exceeding eleven days after the date of the contract'. In the absence of proper regulatory control, NSEL gave a new concept to the spot transactions by allowing delivery at T + 35. It can also be interpreted the other way, i.e. allowing forward contracts with settlement at T+35.

2. Regulatory vacuum: While NSEL is to be blamed for the current mess, this case also reflects the regulatory vacuum in context of the how a spot exchange needs to be run. There was no clarity on who should regulate spot exchange. It was not under the control of FMC as spot contracts are different from forward contracts. Also, since it is not a contract on financial assets, Securities and Exchange Board of India (SEBI) or Reserve Bank of India (RBI) couldn't have regulated it. NSEL knew this better than anybody and exploited the vacuum to float contracts, which created opportunities for transactions in commodities.

3. Ownership structure issues: It is pertinent to note that the ownership requirements for stock exchanges were notified by Government of India vide SCR (Manner of Increasing and Maintaining Public Shareholding) Regulations, 2006 (MIMPS). Even though NSEL is not a stock exchange strictly, should not there be a similar regulation of other exchanges as well. Promoters of NSEL are FTIL and National Agricultural Cooperative Marketing Federation of India Ltd. The ownership structure of spot exchange needs a change immediately to bring more transparency.

4. NBHC Conflict of Interest: Many warehouse receipts issued by NBHC were found to have been issued without adequate stocks. NBHC indulged in this activity as it was a promoted by FT (which is also a promoter of NSEL). NBHC had the incentive of boosting volumes as it's a group company of NSEL.

5. Spot exchange promoting speculation: There are reports, which suggest that the spot exchange became a place where 10% plus returns were guaranteed. While commodity holders deposited commodity in the warehouse to sell commodity, investors bought it and sold a longer settlement period. For example, if the depositor of the commodity sold it on T+2 basis and was bought by an investor, the investor further sold it for T+25 basis (always at a premium). This resulted in creation of repurchase contract, which is also known as repo contract. This was the beginning of speculative activity. Most of the transactions were driven by speculation and the greed to make quick money.

15 of 27

6. Poor transparency issues: Reports in the media suggest that NSEL claimed that it had ` 6,200 crores of stocks against the settlement exposure of around ` 5,400-5,500 crore. The Exchange also claimed that it had settlement guarantee fund of ` 839 crore which was later found to be ` 60 crore. The underlying stock positions were later found to be grossly inadequate & of inferior quality.

16 of 27

ANNEXURE 1 – DETAILED DESCRIPTION OF EVENTS

July 31 – Suspension of Trading affected 13,000 investors: Out of 13,000, 608 were small investors, who were to receive amounts of up to ` 2,00,000 & 6,380 investors who were due to receive amounts above ` 2,00,000 and up to `10,00,000.

August 1 - False claims about Settlement Guarantee Fund & Adequate Stocks: On August 1, the NSEL management claimed that the Exchange had stocks worth ` 6, 200 crore, enough to cover the outstanding obligations of ` 5,500 crore. It also declared that the settlement guarantee fund had ` 839 crore. The number was subsequently revised down to ` 65 crore. That same day NSEL worked out a settlement plan of 5% payments every week, for next 20 weeks.

August 3 - Meeting between Brokers, Millers & the Exchange: NSEL on 3rd August said that most of its trading members had proposed settling outstanding contracts over several months after the commodity exchange suspended trading in most forward contracts. Thirteen members would pay 5% of their outstanding obligations, a total of ` 31.07 billion, weekly, and eight members, with contracts amounting to ` 21.8 billion, would settle outright. NSEL said it had yet to reach an agreement with three of its members with outstanding obligations of ` 3.1 billion.

August 5 - FMC Direction: On 5th August, FMC asked the NSEL to create an escrow account to settle all claims after it emerged that the corpus of the bourse's Settlement Guarantee Fund was ` 65 crore, compared to its claims of over ` 839 crore.

August 6 – Suspension of e-series contracts: NSEL suspended trading of e-series contracts. NSEL offered e-series contracts in gold, silver, copper, zinc, lead, nickel and platinum. Under e-series contracts, retail investors can buy and sell commodities in demat form. E-series contributed about 40% of the NSEL's ` 18,315 crore total turnover in June. This is a unique market segment which functions like the cash segment in equities, but offers commodities in the demat form in smaller denominations. The Central Depository Services (CDSL) and National Securities Depository Services (NSDL) acted as the depository for e-series contracts of NSEL and issued depository certificates. The clearing and settlement, and pay-in and pay-out mechanism on these contracts were based on T+2 cycle. A key feature of the e-series was that there was no storage or holding cost for the stock and transaction cost of the exchange was ` 1,000 for every ` 1 crore turnover for delivery-based transactions. For intra-day transactions, the fee was ` 500 per ` 1 crore turnover.

17 of 27

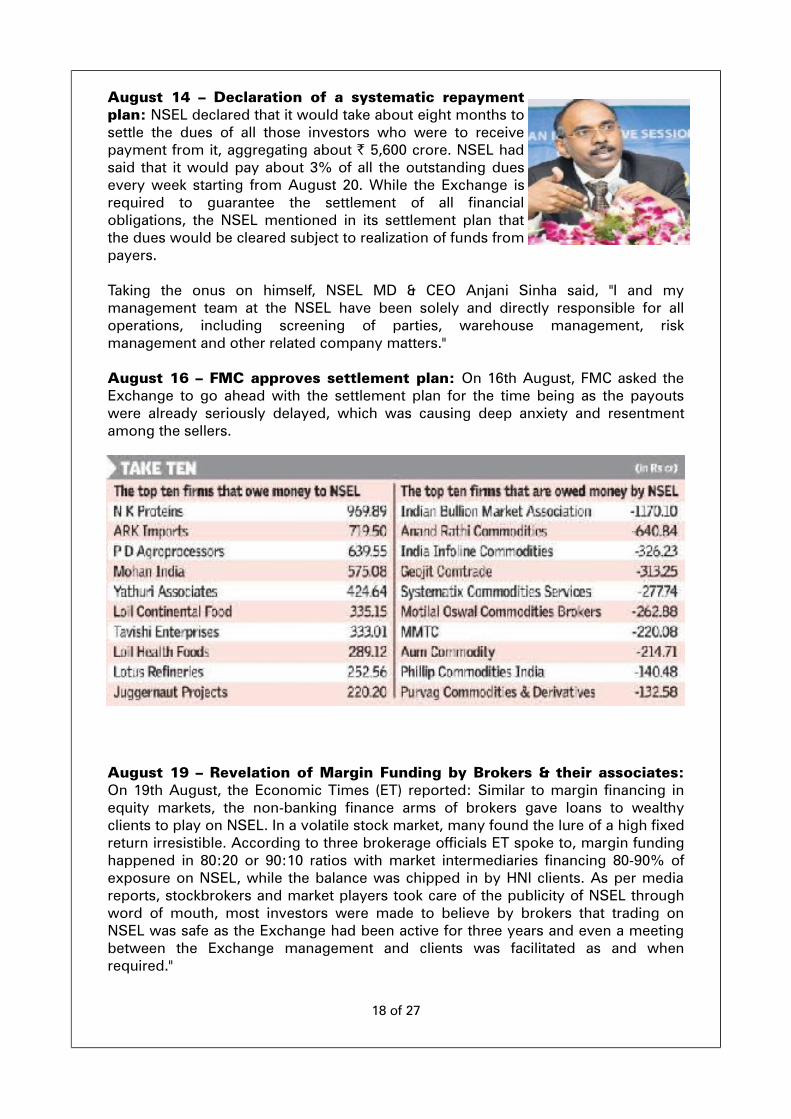

August 14 – Declaration of a systematic repayment plan: NSEL declared that it would take about eight months to settle the dues of all those investors who were to receive payment from it, aggregating about ` 5,600 crore. NSEL had said that it would pay about 3% of all the outstanding dues every week starting from August 20. While the Exchange is required to guarantee the settlement of all financial obligations, the NSEL mentioned in its settlement plan that the dues would be cleared subject to realization of funds from payers.

Taking the onus on himself, NSEL MD & CEO Anjani Sinha said, "I and my management team at the NSEL have been solely and directly responsible for all operations, including screening of parties, warehouse management, risk management and other related company matters."

August 16 – FMC approves settlement plan: On 16th August, FMC asked the Exchange to go ahead with the settlement plan for the time being as the payouts were already seriously delayed, which was causing deep anxiety and resentment among the sellers.

August 19 – Revelation of Margin Funding by Brokers & their associates: On 19th August, the Economic Times (ET) reported: Similar to margin financing in equity markets, the non-banking finance arms of brokers gave loans to wealthy clients to play on NSEL. In a volatile stock market, many found the lure of a high fixed return irresistible. According to three brokerage officials ET spoke to, margin funding happened in 80:20 or 90:10 ratios with market intermediaries financing 80-90% of exposure on NSEL, while the balance was chipped in by HNI clients. As per media reports, stockbrokers and market players took care of the publicity of NSEL through word of mouth, most investors were made to believe by brokers that trading on NSEL was safe as the Exchange had been active for three years and even a meeting between the Exchange management and clients was facilitated as and when required."

18 of 27

Even as brokers earned 10-12% on financing and 3-4 bps commission on trades, there was a 3-4% 'risk-free' spread for clients. Savvy stock and commodity traders and professional market analysts were the ones that availed margin financing to trade on NSEL. These were high-risk borrowers who saw risk-free returns. Eager for business, NBFCs funded them.

August 20 – NSEL defaults on first payout & demotion of it's MD & CEO: NSEL was able to pay only ` 92 crore on August 20, the first day for pay-out to investors, out of the scheduled ` 174.72 crore. NSEL demoted its Managing Director and CEO Anjani Sinha and six other top executives on a day it failed to meet the first scheduled repayment to investors. Hours after NSEL failed to meet its first payout, commodity market regulator FMC shot off a letter to the bourse's Board saying it risked losing its 'fit and proper person' status, and warned that in the event of such an 'eventuality' it could not continue to hold directorship or shareholding in MCX or any other recognized commodity futures exchange. FMC warned that non-settlement of the outstanding trade on NSEL seriously reflected on the Board's 'credibility' and 'reputation', key ingredients in meeting the fit and proper criterion for operating an exchange. FMC directed NSEL to declare members, who have failed in making payments, as defaulters and liquidate all their realizable assets. The regulator also asked NSEL to auction defaulters' commodities lying in the accredited warehouses as collateral.

August 21 – Member's cheques dishonored: ET reported that, cheques worth close to ` 550 crore submitted by borrowers on the NSEL had so far bounced, following which the FMC had directed the bourse to disclose copies of warehouse audit reports and even receipts of physical stocks underlying the e-series contracts that investors entered into to buy bullion in small lots. FMC is learnt to have sought details of all cheques received by the borrowers and their complete profile, including documents pertaining to know-your-customer formalities.

24thAugust 24 – FMC issues new rules on SGF: On 24th August, ET reported that, the FMC has ordered that all commodity exchanges will have to deposit 5% of the gross revenue earned in a previous year from FY15 onwards (April 1, 2014) in Settlement Guarantee Fund (SGF). As an initial contribution to SGF, exchanges will have to shell out a minimum of ` 10 crore or 5% of the sum total of gross revenues earned by them in the five financial years through FY13, or from the date they became operational. SGF will also comprise base minimum capital from member brokers and the interest earned by the exchange on the BMC, refundable deposits

19 of 27

made by members, excluding margins, settlement-related penalties charged from exchange from their members with effect from September 1, 2013. Interest amount and any other income accrued on the investment of funds of SGF shall also be credited to the fund. However, FMC has said that margin collected by an exchange from its members to trade should not be part of SGF

August 24 – IT Department discovers that underlying stock is inadequate:The crisis deepened with the Income-tax department confirming that transactions on the bourse were made against non-existent to inadequate stocks. In some cases there were no stocks, in others the quantity of the stocks was below than that claimed by some of the buyers. The survey results so far put a stamp of authenticity on speculation that many of the 24 buyers had borrowed money without having stocks in the NSEL

accredited warehouses. Income Tax (I-T) Department also commenced investigation on possible tax evasion by defaulters of the NSEL after discovering that stocks projected by most of them either don't exist or are over-reported. The I-T Department had conducted nationwide search on the business premises of about two dozen members of the NSEL on August 22. According to concerned officials most bill books, ledgers and accounts of these store houses have been found to be fictitious or under- reported which is a clear case of tax evasion. The department suspects the account books were fudged to dodge the tax net and present a fake picture of activities at these business entities.

August 27 & September 3 – NSEL defaults on 2nd & 3rd payout: NSEL could pay only ` 15.37 crore of ` 174.7 Crores, in its third consecutive failure to meet payment obligations. NSEL had defaulted in the first two pay-outs as it received only ` 92.73 crore from members in the first pay-out and ` 12.05 crore in the second pay-out, out of the scheduled ` 174.72 crore each. In other words, the exchange, till 3rd September, has disbursed only ` 120 crore against ` 524.16 crore.

On 27 August, NSEL said it had taken a loan of ` 177.23 crore from its promoter FTIL to pay investors who are owed up to ` 10 lakh each. The bourse had said it would fully pay the 608 investors to whom it owed up to ` 2 lakh each as on 31 July, and pay 50% of the dues upfront to 6,380 investors who are to receive between ` 2 lakh and ` 10 lakh each. The rest would be paid proportionately as per a settlement plan, it said.

September 2 - Preliminary Report by SGS (for Stock Audit): The report submitted by SGS, the Swiss firm hired by the exchange to audit stocks in the warehouses, found that the exchange had overstated the availability by 85%. In some of the other warehouses located within the premises of the borrowers, SGS officials were refused entry. SGS,

20 of 27

which provides inspection and verification services to the commodity trade, will file a final report after inspecting all the warehouses that dealt with the crisis-ridden spot exchange.

September 3 – NSEL declares 19 defaulters: As on 3rd September, NSEL declared 19 of its 24 members as defaulters and sent notices to 14 of them under section 13 of the Negotiable Instruments Act for bounced cheques that were provided towards settlement. It plans to recover money from the defaulters by selling their commodities lying in warehouses and other assets offered by them via personal resources.

Directors Resign: NSEL lost majority of it's directors after the scam broke. Mr. Shankarlal Guru (Chairman), Mr. Shreekant Javalgekar, Mr. Ramanathan Devarajan and Mr. B.D. Pawar resigned after news about the scam broke. The board had earlier sacked its managing director, Anjani Kumar Sinha. The board now had, Mr. Jignesh Shah and Mr. Joseph Massey.

September 4 – FMC direction to other exchanges for WDRA registration: For better regulation of warehouses, FMC has asked all national commodities

bourses to register their warehouses with the Warehousing Development & Regulatory Authority and obtain the accreditation certification before December 31. It has also asked the exchanges to accredit only those new warehouses at their end which have already been registered and accredited by WDRA.

September 4 - Report on NK Proteins: Business Standards reported that NK Proteins' has unsettled position of ` 969 crore at the NSEL vis-à-vis a net worth of `108 crore. ICRA recently downgraded its long-term rating to B- from BB+. NKPL is the biggest defaulter in the list of 24 members which collectively contributed to a default of ` 5,600 crore at NSEL.

September 6 – Sharp & Tannan Associates' report on precious metal stocks (e-series contracts): As per the report & NSEL press release, stocks backing the e-series contracts matched depository records and stock statements by the exchange and those lying with Brinks Arya India, provider of vaulting services. The amount of gold stock across Mumbai, Kolkata, New Delhi, Hyderabad, Ahmedabad and Jaipur are 910.65 kilos, silver stock is 46,167.7 kilos and platinum is 19 kilos. The verification did not reveal any discrepancy in the quantum of stock. It may be noted that Sharp & Tannan Associates was appointed by NSEL.

September 7 – I-T Department finds NSEL operated as a long-term financing platform: As per an Indian Express report, Income Tax Department

21 of 27

probe in NSEL has revealed that the bourse was used as a platform only to raise 'long-term finance' by entities that were not interested in the underlying commodities. Report also said that, I-T department is of the view that money was raised through the exchange platform to meet the working capital requirement and some entities have also channelized the money towards personal assets rather than business assets.

September 10 – NSEL Default's on 4th payout: NSEL defaulted for the fourth consecutive week as it could pay only ` 7.77 crore on Tuesday to investors out of scheduled ` 174.72 crore.

September 12 - Enforcement Directorate submits report to Finance Ministry: The report finds violation of Foreign Exchange Management Act (FEMA) and Prevention of Money Laundering Act (PMLA) by some borrowers on the exchange.

September 12 - SEBI conditionally renewed the license of MCX Stock Exchange: License was renewed for a period of 1 year w.e.f. September 16. MCX Stock Exchange was asked by SEBI to strengthen its governance structure to continue to remain as a recognized bourse.

September 12 - Mohan India (borrower) diverts ` 300 crore to other entities after July 31: According to NSEL records, Mohan India owes ` 605 crore towards its exposure to sugar stocks. Over the past few weeks, especially after August 1, money has been shifted out of group entities such as Mohan Built Developers, Yukati Builders, Meltreck Builders, Bharat Buildwell and Brinda Commodities. Some of these entities had received cash from Mohan India in the days before July 31, when NSEL was still functional, central agencies looking into the money trail said after examining the books and accounts of Mohan India. The records further showed several trading entities directly related to the group or its directors such as Anuj Traders, Neki Ram Vijay Kumar, Sandeep Kumar Anuj Kumar and Vishnu Trading had received several crores of rupees after August 1. Before July 31, about 70 % of Mohan India’s receipts were accounted for by NSEL trades. Group company Brinda Commodities and another entity, Whizkid Promoters, accounted for the rest.

September 13 – FMC shifted to Finance Ministry: The government brought the commodities market regulator, the FMC, under the purview of the Department of Economic Affairs in the Finance Ministry. Order issued by the Ministry of Finance said that all matters related to forward markets and FMC would henceforth be handled by DEA. Earlier FMC was covered by Ministry of Consumer Affairs.

September 15 – Revelations from Anjani Sinha's Affidavit (Former MD & CEO): The affidavit filed on September 11 with a local magistrate, revealed that:

1. By 2011-12, it was known that, if rollovers were not allowed, buyers would have defaulted by a huge amount & on the other hand, if rollovers continued, the exposure keeps on increasing every year by 20-25% due to impact of

22 of 27

rollover cost and exchange fee.

2. Due to the fear of widespread default, management allowed the exchange to function rather than stopping it boldly.

3. By end of December 2011, it was known that, exchange was not having stock to back the exposure. Still, management allowed him to continue because of the fear of widespread default if rollovers were stopped.

4. Lotus Refineries (Lotus) stopped repaying in 2011-12. Nonetheless, exchange officials requested Lotus to continue trading. The problem was if Lotus was declared as a defaulter, the entire system comes to a halt. Lotus stock was not in NSEL's possession and so, declaring him defaulter meant the entire edifice comes to a standstill.

5. Borrowers' factories were treated as warehouses and the exchange allowed them to borrow money and also keep stock.

September 18 - NSEL's former AVP reveals modus operandi: NSEL's former AVP disclosed that investors were misled by claiming that it could use stocks under the NBHC's management. NSEL officials misled investors by claiming it could use stocks under the management of NBHC to build positions on the exchange. This was revealed in a statement made by Jai Bahukhandi, former Assistant Vice-President (market operations), NSEL, before one of the several committees set up to probe the crisis. He also revealed that the trade was executed and the client offered these stocks through an offer letter, the CID (Commodity Inward Document) was generated in the eWDMS (Electronic Warehouse and Delivery Management System) at the head office of NSEL, though it did not have control on the stock. Simultaneously, quality certification and storage receipts were generated and marked for commodity pay-in, though the commodities were already under pledge to banks & managed by NBHC.

September 21 - Motilal Oswal group discloses details of it's exposure: The amount includes ` 195.24 crores owed by NSEL with respect to the positions taken by its clients through the broking platform offered by Motilal Oswal Group. ` 57.28 crores owed by NSEL with respect to the proprietary positions undertaken by Motilal Oswal Group and `

1.40 crores owed by NSEL with respect to the positions taken by its clients through the broking platform offered by Motilal Oswal Group and funded by the group.

September 25: FTIL Auditors Deloitte Haskins & Sells withdraw their report: The auditors of Financial Technologies informed BSE that the audit report on the standalone and consolidated financial statements for the year ended March 31, 2013, should no longer be relied upon.

23 of 27

September 25 - Margin Funding exposure of Geojit BNP Paribas Group is at ` 133 Crores: Business Standard reveals that Geojit Credits (P) Ltd, a non-banking financial company in which Geojit BNP Paribas has majority stake, has funding exposure of ` 133.2 crore to client trades on the scam-hit National Spot Exchange Ltd. The company funded this mostly through loans from group companies, according to a note it released on the exchange website. Geojit BNP Paribas had a consolidated net worth of ` 485.7 crore as of the end of June.

September 27 - ICAI initiates enquiry into issues involving NSEL auditors: Following a complaint, the NSEL matter was referred to the Disciplinary Committee. The audited accounts were withdrawn a day before FTIL's annual shareholder meeting on September 25. As per various media reports, NSEL's auditor Mukesh P Shah was a relative of FTIL Chairman and MD Jignesh Shah (the audit firm's key

proprietor is the husband of Jignesh Shah’s mother’s sister).

September 30 - FIR filed by EOW : EOW files FIR against Jigesh Shah, Joseph Massey (MD of MCX , another FTIL-promoted firm), other promoters, directors and defaulters charging them with cheating, forgery, breach of trust and criminal conspiracy, among others.

October 4 - MMTC Alleges: Jignesh Shah, NSEL conspired with defaulters: State-owned MMTC told the Attorney General of India (AG) that NSEL promoter Jignesh Shah, the board members of the exchange, its management, led by Anjani Sinha, and even the so-called defaulters had acted in collusion to dupe investors. MMTC which falls under the administrative control of the Ministry of Commerce and Industry has an exposure of ` 220 crore.

October 4 - Lookout notices issued for Shah, associates by EOW: The EOW of the Mumbai police stated that lookout notices have been issued against Shah and others along with an alert flashed to the immigration department to ensure that they do not leave the country. The police has already issued summons to all the accused asking them to present themselves at the EOW headquarters for questioning.

October 5 - Raw wool stock found to be inferior, worth a fraction during auction: Auction fetches best price of ` 21 per kg, whereas the last traded price on the bourse was ` 718 per kg . Two warehouses of ARK Imports in villages of Purba and Seerah were shown having raw wool stocks of 5,265 tonnes and 5,454 tonnes,

24 of 27

respectively. NSEL valued this stock at ` 377.53 crore and ` 391.10 crore, respectively. Thus, the exchange valued the total wool stock of 10,719 tonnes at ` 768.63 crore at an average price of ` 717 per kg. However, according to SGS audit, the Purba godown of ARK Imports had 1247.4 tonnes of raw wool, while the warehouse at Seerah village had slightly lesser quantity at 1216.8 tonnes.

October 6 - Ripple Effect - Cash segment, equity derivative turnover crashes at MCX-SX: As per latest data available with MCX-SX, its cash segment equity market turnover declined by 8.82 % to nearly ` 990 crore in September. MCX-SX's equity derivative segment turnover fell more sharply by 69.13 % in September to ` 7,133 crore, from ` 23,105 crore in August. A total of 2.57 lakh derivative contracts were traded on its platform in September compared to 8.61 lakh during August.

October 7 - EOW reveals that a total of 14 warehouses were found non-existent, while 30 warehouses were found to be empty.

October 8 - EOW wing discovers that 9 of the 27 companies that defaulted in making payments to the exchange never existed at the addresses they had furnished to NSEL. These nine companies account for half of the scam amount of ` 5,500 crore. The firms are:

1. Chandigarh-based LOIL Continental Foods Private Limited, 2. LOIL Health Foods Private Limited and 3. Whitewater Foods Private Limited; 4. Delhi-based Tavishi Enterprises Private Limited; 5. Yathuri Associates in Panchkula; 6. Ark Imports Private Limited, Ludhiana; 7. Aastha Minmet Private Limited, Bangalore, and 8. Swastik Overseas Corporation, Ahmedabad. &9. Namdhari Foods Private Limited

October 8 - The HC directed the FMC to monitor the settlement of e-series bullion contracts by the Bombay High Court : The interim order directed FMC to verify the genuineness of investors who want to en-cash their contracts or to re-materialise them (take physical delivery of gold/silver), in respect of aggrieved investors' petition that prayed for regulatory intervention for the settlement of the e-series contracts.

25 of 27

October 8 - Financial Express reports that, internal audit report red flagged NSEL financing activities in 2011: Minutes of board meetings reviewed by the FMC showed that an internal audit report submitted by Mukesh P Shah & Co had noted that NSEL was indulging in financing activities similar to a non-banking finance company (NBFC) without having the license to do so. The report was submitted to the board and recorded in the meeting minutes, even though no subsequent action was taken.

26 of 27

ANNEXURE 2 – REFERENCES

1. The FIRM Show – CNBC TV18

2. www.economictimes.com

3. www.firstpost.com

4. www.livemint.com

5. www.indianexpress.com

6. www.business-standard.com

7. www.moneycontrol.com

27 of 27