Embed Size (px)

Citation preview

World Bank Mineral Fiscal Regimes Presentation 1

A.1 INTRODUCTION AND BUILDING BLOCKS OF MINERAL FISCAL REGIMES

Recent developments Slides 1-12

John StrongmanExtractive Industries Expert

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 2

Introduction/Overview• This presentation is made primarily from the perspective of advising governments on the

design of a mineral fiscal regime• The focus is solely on mining i.e. non-fuel minerals and coal – not hydrocarbons.• It aims at giving an understanding,

• first, of the key characteristic of different mineral fiscal instruments • second, at how they interact together in terms of overall government revenues (tax

take) from the mineral sector in both a qualitative and quantitative manner and• Third, how a government can use a modelling approach to position its mineral fiscal

regime so that is has a tax take be in the lower part, the mid range or the higher part of the tax take for other mining countries

• It also touches on some related issues such as state equity in mining projects• It concludes with some mineral fiscal administration issues relating to protecting against

taxpayers seeking to minimize taxes in a host country by shifting taxable profits to another jurisdiction, since no matter now well designed a mineral regime is, it will not achieve expected results if it cannot be administered effectively

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 3

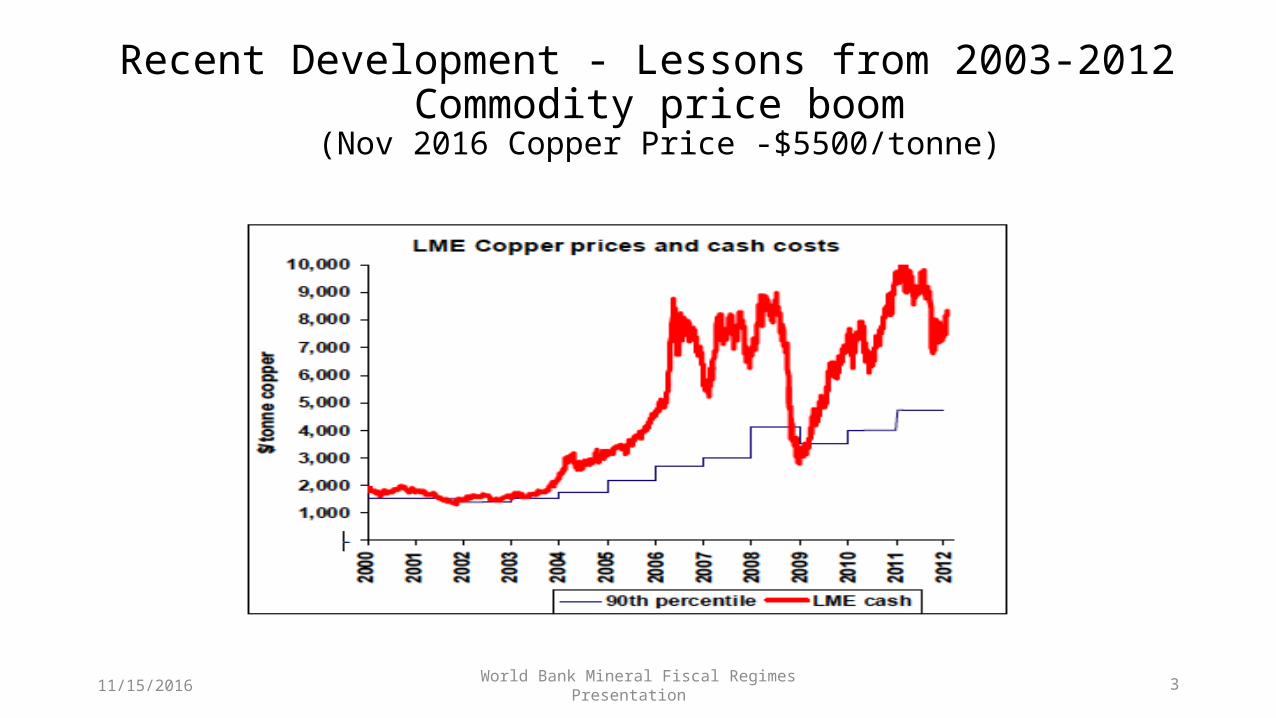

Recent Development - Lessons from 2003-2012 Commodity price boom

(Nov 2016 Copper Price -$5500/tonne)

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 4

Recent Development - Lessons from 2003-2011 Commodity price boom

Tax collections did not keep pace with profit growth Why? Inadequate Mineral Fiscal Regime design

• Countries had signed confidential contracts with overly “generous terms”• Countries lacked “progressive fiscal instruments”

• Inadequate Tax Administration Capacity – especially auditing• Countries lacked sufficient capacity to counteract profit shifting/tax

minimization behaviors especially those linked to “related party” transactions• Product transfer pricing audit capacity • Construction costs, operating costs audit capacity

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 5

Mineral/Economic RentMinerals can have a scarcity value that results

in Financial terms – in “excess profits” in Economic terms – in “mineral/economic rent” i.e. profits/returns over and above the minimum required for an investment to be

made Many minerals are sold at a world-wide market price – thus a high grade deposit can generate an economic rent (excess profit) as compared with a low grade or average project Economic rent can also be generated during commodity price booms when many projects can become extremely profitable while the price boom lasts Appropriate fiscal instruments are needed to enable governments to obtain a fair share of the economic rent/excess profitThese are generally referred to as “Progressive Fiscal Instruments”

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 6

Progressive Fiscal instruments

• Progressive Fiscal instruments • that take effect when a certain level of profitability is reached

• e.g. Resource Rent Tax; Excess Profits Tax• that have a base rate which increases when a certain “trigger” level of profitability is

reached • e.g. Variable Income Tax; Sliding-scale Royalty

Profit-based sliding-scale royalties introduced • South Africa 2008; • Chile 2010; • Peru 2011; • Australia MRRT 2012

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 7

Starting Point – the August 15, 2012 IMF paper "Fiscal Regimes for Extractive Industries: Design and Implementation”

IMF Paper Page 9 Revenue objectives are important for mineral fiscal regime design but involve complex trade-offs

Fiscal regimes vary greatly from country to country with a wide range of instruments being used

Fiscal regimes require tailoring to each country

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 8

Mineral Fiscal Regime Design – some key points

IMF Paper Comment

Mineral regimes need to be county-specificComplex trade offs will need to be addressed (page 6)

A Mineral Fiscal Policy can be used as the decision-making framework to address the complex trade offs

The central fiscal issue is ensuring a “reasonable” government share in extractive industries’ rents so that private investors have an adequate incentive to explore, develop, and produce; (page 9)

The target tax take can be positioned in relation to other countries

The Rate of CIT and Link to Additional Rent Taxation Section makes the point that it is the aggregate tax impact (tax take) that is of greatest importance to companies rather than the tax take from individual fiscal instruments (page 44)

The total tax take depends on all the fiscal instruments and how they interact – for example if the royalty is deductible for income taxes it reduces CIT payments

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 9

The Mineral Fiscal Regime - Main Instruments

The Mineral Fiscal Regime generally consists of Income and other taxes including dividend and other withholding taxesCustoms dutiesMineral royalties and fees Most jurisdictions use the term “non-taxes” to cover duties, royalties and fees The term “fiscal instruments” in this presentation is used to cover both tax and non-tax fiscal instruments.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 10

The Mineral Fiscal Regime - Institutional Responsibility and Authority

The Ministry of Finance - tax policy and legislation including applicable rates The Revenue Service - tax assessment, collection and auditsThe Customs Service - customs duties The Mining Ministry - mineral royalties and fees

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 11

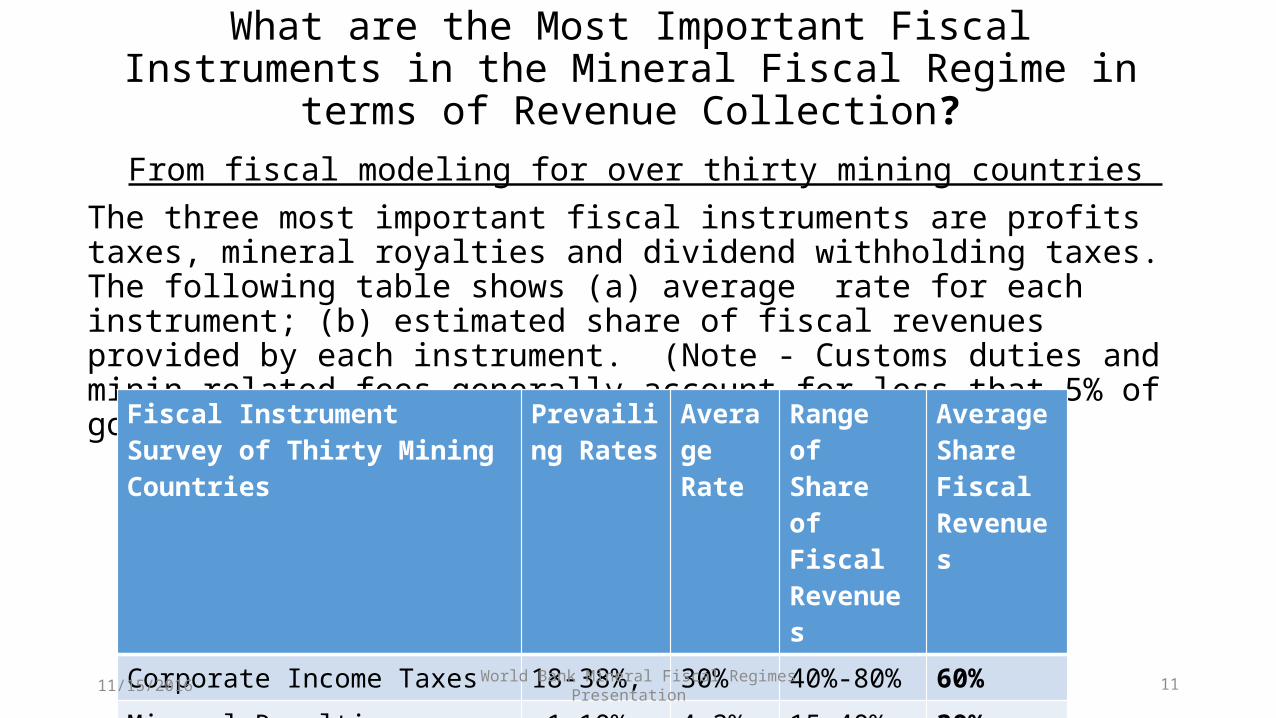

What are the Most Important Fiscal Instruments in the Mineral Fiscal Regime in terms of Revenue Collection?

From fiscal modeling for over thirty mining countries The three most important fiscal instruments are profits taxes, mineral royalties and dividend withholding taxes. The following table shows (a) average rate for each instrument; (b) estimated share of fiscal revenues provided by each instrument. (Note - Customs duties and minin-related fees generally account for less that 5% of government revenues over the life of a project).

Fiscal InstrumentSurvey of Thirty Mining Countries

Prevailing Rates

AverageRate

Range ofShare of Fiscal Revenues

Average ShareFiscal Revenues

Corporate Income Taxes 18-38%, 30% 40%-80% 60%Mineral Royalties (gold/copper) 1-10% 4.2% 15-40% 30%Dividend Withholding Taxes (DWT) 0%--20% 10% 0-20% 10%

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 12

Key Development

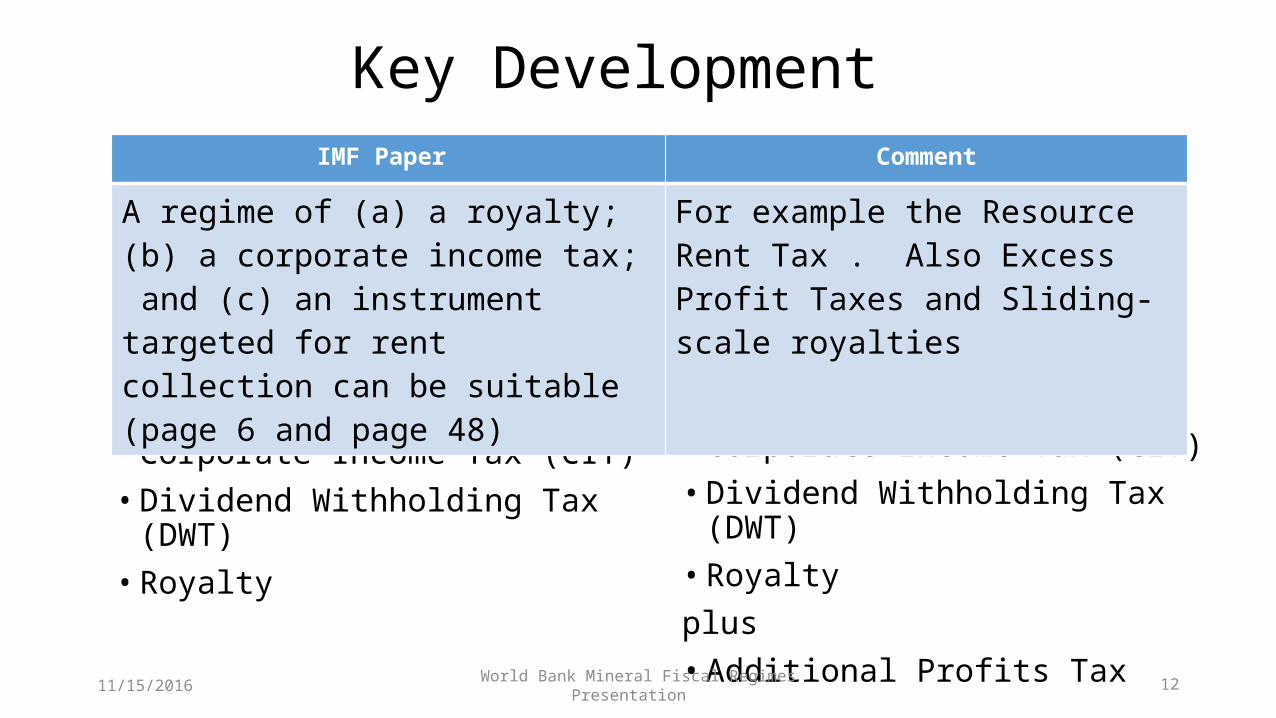

Previous Approach • Corporate Income Tax (CIT)• Dividend Withholding Tax (DWT)• Royalty

New Approach • Corporate Income Tax (CIT)• Dividend Withholding Tax (DWT)• Royalty plus• Additional Profits Tax

IMF Paper Comment

A regime of (a) a royalty; (b) a corporate income tax; and (c) an instrument targeted for rent collection can be suitable (page 6 and page 48)

For example the Resource Rent Tax . Also Excess Profit Taxes and Sliding-scale royalties

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 13

A.2 INTRODUCTION AND BUILDING BLOCKS OF MINERAL FISCAL REGIMES

Economy-wide, and Mineral Sector-specific Fiscal Instruments

Slides 13-24

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 14

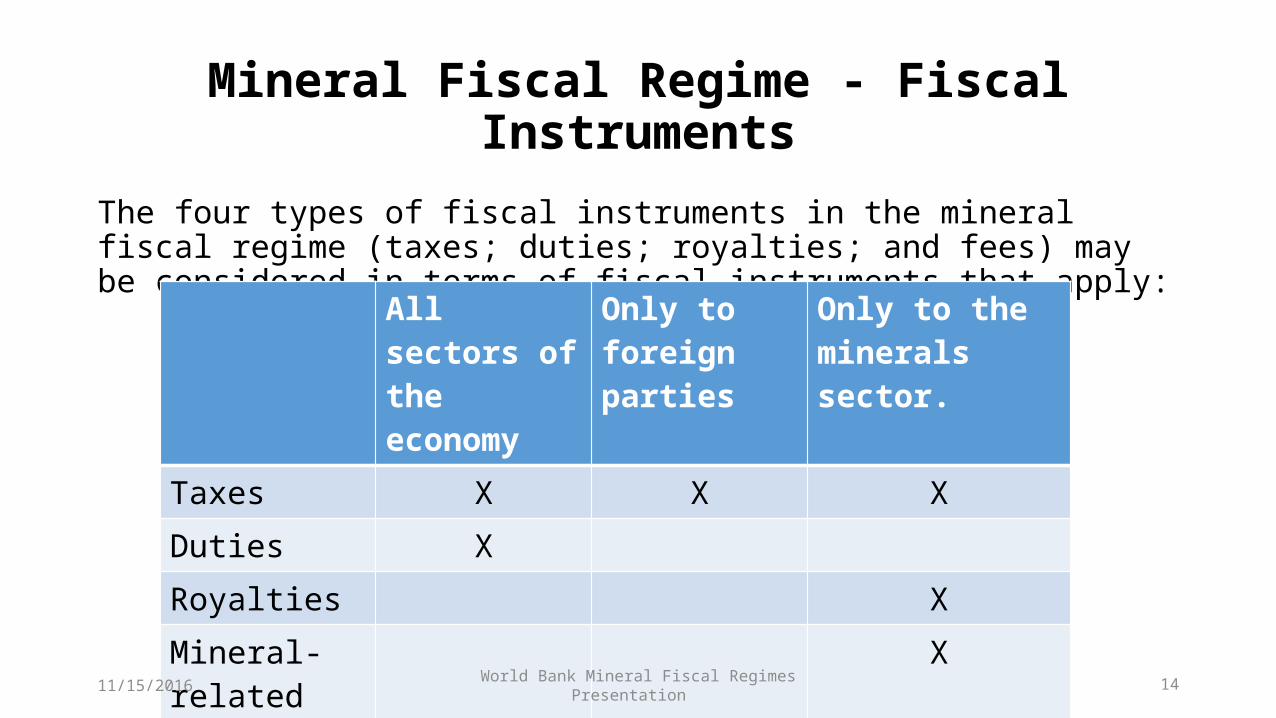

Mineral Fiscal Regime - Fiscal Instruments

The four types of fiscal instruments in the mineral fiscal regime (taxes; duties; royalties; and fees) may be considered in terms of fiscal instruments that apply:

All sectors of the economy

Only to foreign parties

Only to the minerals sector.

Taxes X X XDuties XRoyalties XMineral-related Fees

X

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 15

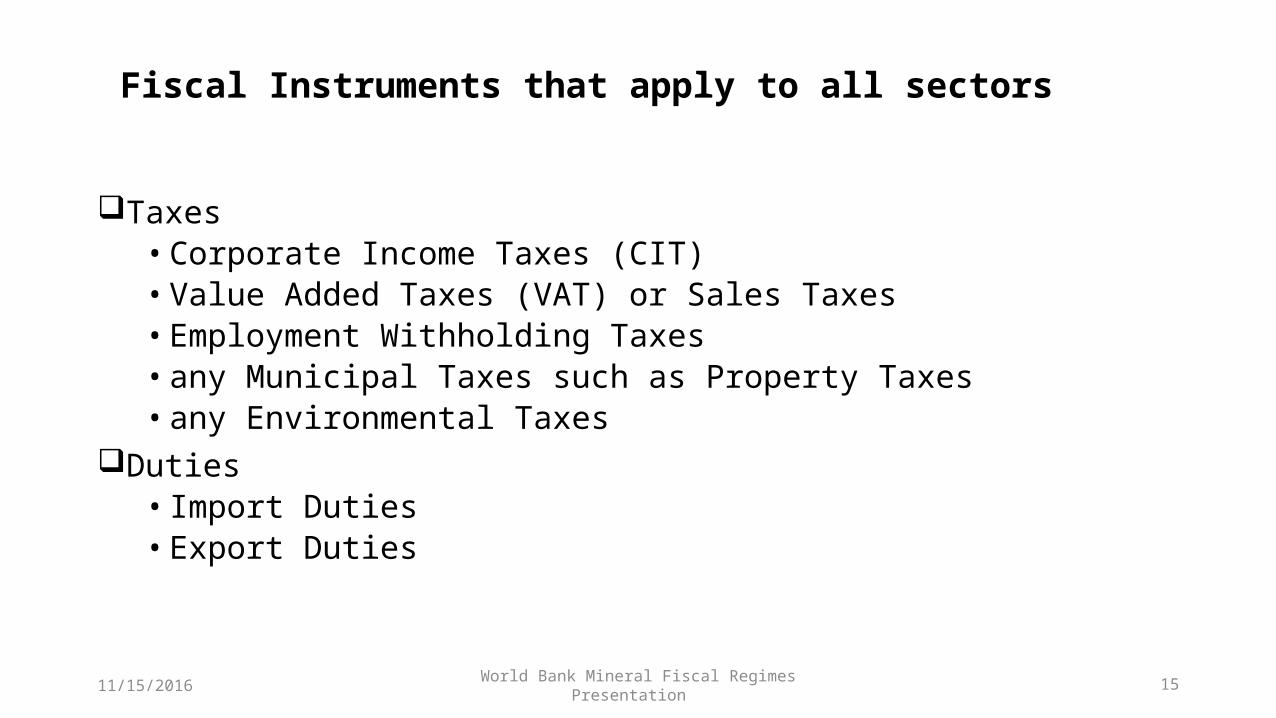

Fiscal Instruments that apply to all sectors

Taxes • Corporate Income Taxes (CIT)• Value Added Taxes (VAT) or Sales Taxes • Employment Withholding Taxes• any Municipal Taxes such as Property Taxes• any Environmental Taxes

Duties • Import Duties• Export Duties

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 16

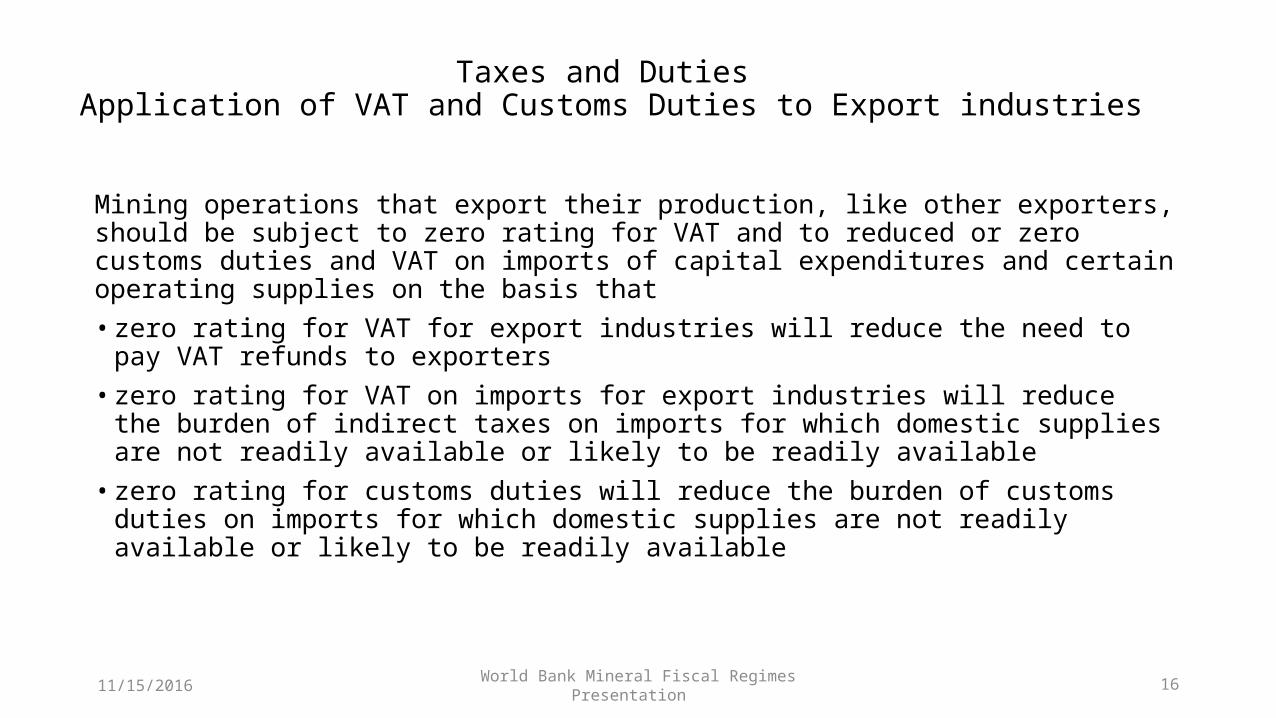

Taxes and Duties Application of VAT and Customs Duties to Export industries

Mining operations that export their production, like other exporters, should be subject to zero rating for VAT and to reduced or zero customs duties and VAT on imports of capital expenditures and certain operating supplies on the basis that • zero rating for VAT for export industries will reduce the need to pay VAT refunds to

exporters• zero rating for VAT on imports for export industries will reduce the burden of

indirect taxes on imports for which domestic supplies are not readily available or likely to be readily available

• zero rating for customs duties will reduce the burden of customs duties on imports for which domestic supplies are not readily available or likely to be readily available

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 17

Tax DepreciationMany countries use the following three depreciation categories for tax purposes

• exploration, • tangible assets (e.g. plant and equipment), and • other development costs (e.g. earth moving, shaft sinking) including

intangible assets (e.g. value of a license or management fees) • Accelerated depreciation can allow investors to recover their capital more

quickly – but reduces government revenues in the early years of project life• In the year that an asset comes into service, countries must also consider

whether to• allow depreciation for the whole year even if the asset has only been in

service for one or two months or • to only allow depreciation for the number of months that an asset has

been in service

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 18

Fiscal Instruments that Apply only to Foreign Parties

include Dividend Withholding Tax - InvestorsInterest Withholding Tax – Lenders Contractors Withholding Tax – Contractors

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 19

Fiscal Instruments that apply only to the Mining Sector

includeMineral Sector-related Fees• License Fees; Land access or use fees; • Municipal level mining-related feesMineral Royalties• Unit Royalties; Fixed Rate Ad Valorem Royalties; • Profits-based sliding scale royalties; Price-based sliding-scale royalties“Progressive” Taxes• Excess Profits Taxes; • Rate of Return type taxes

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 20

Payments associated with receipt of a mineral right and use of land – fees etc. Compensation for the removal of a non-renewable resource, generally owned by

the stateMineral royalties

• Unit mineral royalties • Ad valorem mineral royalties in the order of 2-3% of sales values

Capture of some of the mineral rent for the government Ad valorem mineral royalties in the order or 4% or above of sales value Sliding-scale mineral royalties Excess Profits Taxes; Rate of Return type taxes

Underlying Rationale for Fiscal Instruments that apply only to the Mining sector

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 21

Unit Mineral Royalty

• A fixed fee per unit e.g. ounce, pound or ton of material produced or sold. • Generally applied to low value minerals (such as construction materials)

produced for the domestic market with relatively stable prices. • Payments to government depend only on volume produced or sold and thus tend

to be fairly stable• Provides a base payment to government to compensate for the exploitation of a

non-renewable resource

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 22

Fixed Rate Ad Valorem Royalty

• A fixed percentage of the market value of minerals produced or sold. • Generally applied to higher-value minerals (such as metals) produced for the export

with world market prices that can go through large price cycles. • Payments to government depend on market price as well as quantity/quality and

thus payments have higher upside potential than for the unit royalty. • A 2-3% ? royalty may be considered to compensate for the exploitation of a non-

renewable resource • A higher royalty 4%+ may be considered to have a mineral rent component

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 23

Sliding-scale (Variable) Rate Ad Valorem Royalty

Sliding-scale (Variable) Rate Ad Valorem Royalty• Payments to government depend on a variable (not fixed) ad valorem royalty rate• Base rate (if 2-3%) may be considered to compensate for the exploitation of a non-

renewable resource Profit-Based• Royalty rate linked to profit of each taxpayer Price-Based – Mineral Specific • Sector wide royalty rate linked to the market price of a given mineralPrice-Based – Project Specific • Project-specific royalty rate set on a project by project basis

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 24

Excess Profits Tax and Rate of Return-type Tax

Step up Excess Profits Tax: • The Corporate Income Tax is stepped up to a higher rate above a certain profit

point Variable Excess Profits Tax• The Corporate Income Tax varies above a base level depending on a measure of

profitability Rate of Return-type Tax • Additional tax payments occur when the a pre-defined rate of return is exceeded

over time

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 25

B.1 INNOVATIONS IN DESIGNING MINERAL FISCAL REGIMES

Government Objectives/What Investors SeekSlides 25-36

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 26

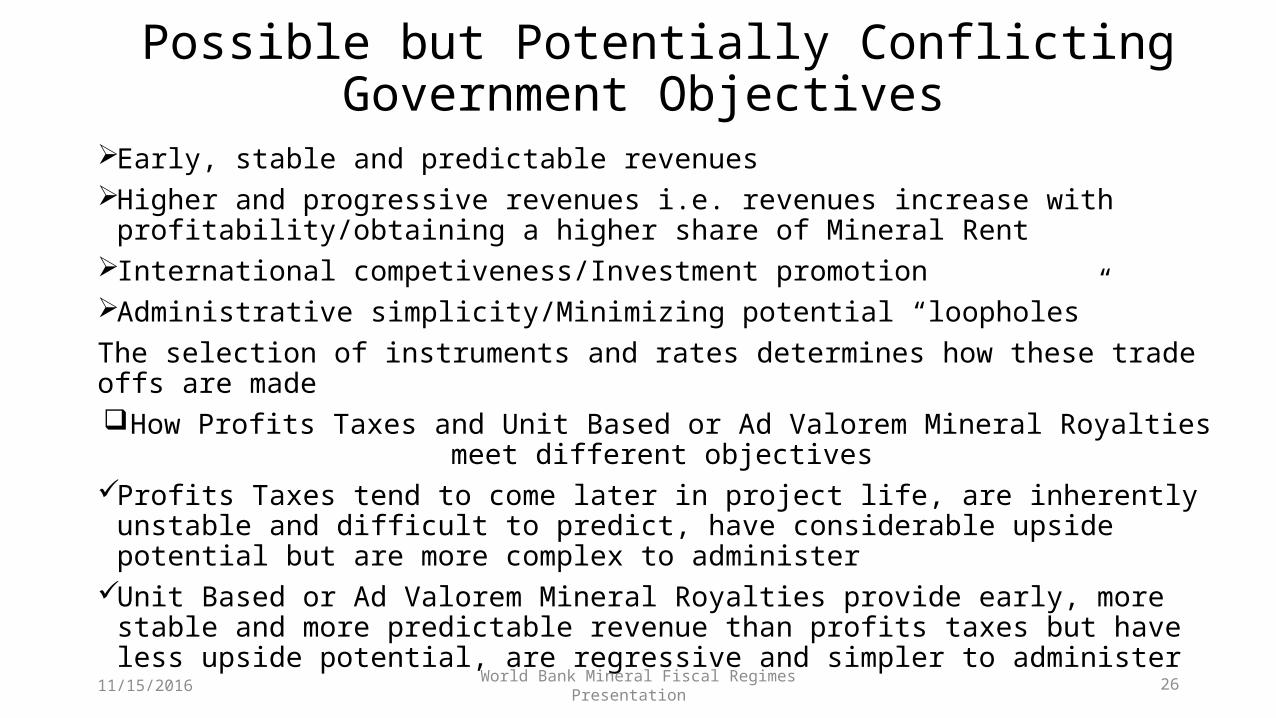

Possible but Potentially Conflicting Government Objectives

Early, stable and predictable revenuesHigher and progressive revenues i.e. revenues increase with profitability/obtaining a

higher share of Mineral Rent International competiveness/Investment promotionAdministrative simplicity/Minimizing potential “loopholes”The selection of instruments and rates determines how these trade offs are made

How Profits Taxes and Unit Based or Ad Valorem Mineral Royalties meet different objectives

Profits Taxes tend to come later in project life, are inherently unstable and difficult to predict, have considerable upside potential but are more complex to administer

Unit Based or Ad Valorem Mineral Royalties provide early, more stable and more predictable revenue than profits taxes but have less upside potential, are regressive and simpler to administer

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 27

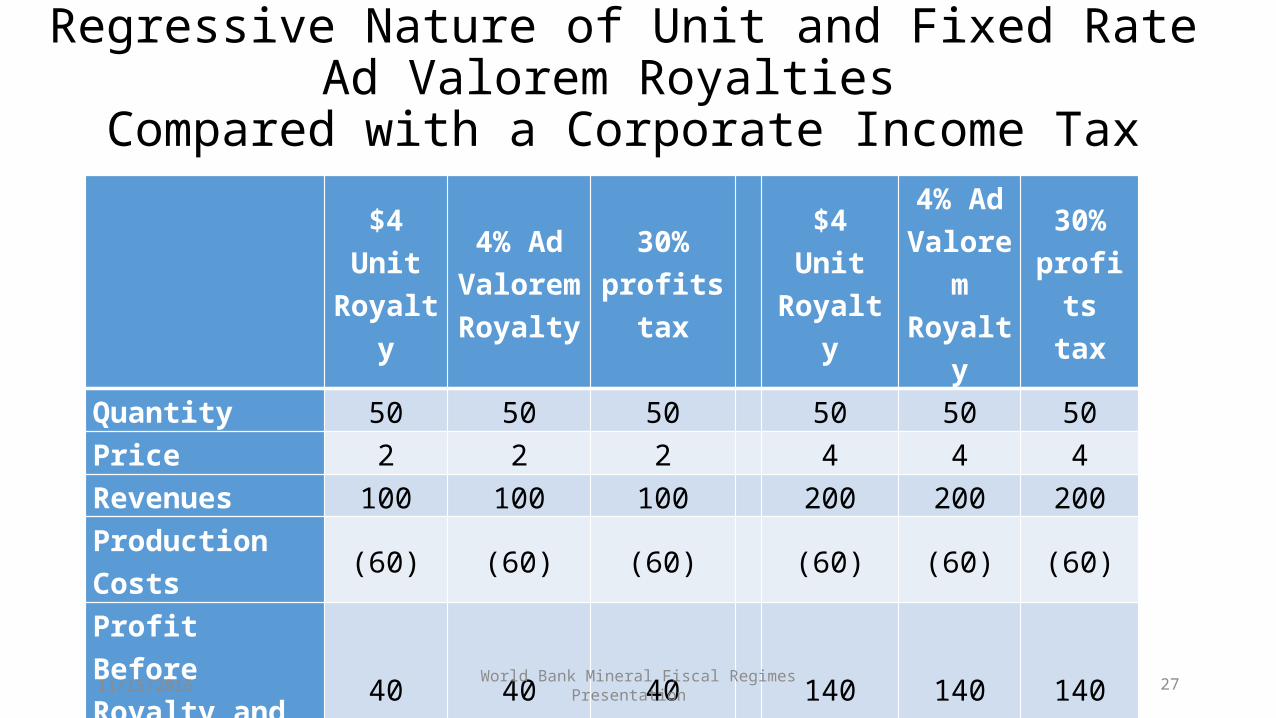

Regressive Nature of Unit and Fixed Rate Ad Valorem Royalties

Compared with a Corporate Income Tax $4 Unit

Royalty4% Ad

ValoremRoyalty

30% profits tax $4 Unit

Royalty4% Ad

ValoremRoyalty

30% profits

taxQuantity 50 50 50 50 50 50Price 2 2 2 4 4 4Revenues 100 100 100 200 200 200Production Costs (60) (60) (60) (60) (60) (60)Profit Before Royalty and Tax 40 40 40 140 140 140

Royalty 4 4 0 4 8 0Profits Tax 0 0 12 0 0 42Govt Revenues as % Profit

4/36=9%

4/36=9%

12/40=30% 3/137

=2.3%6/134=4.5%

42/140=30%

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 28

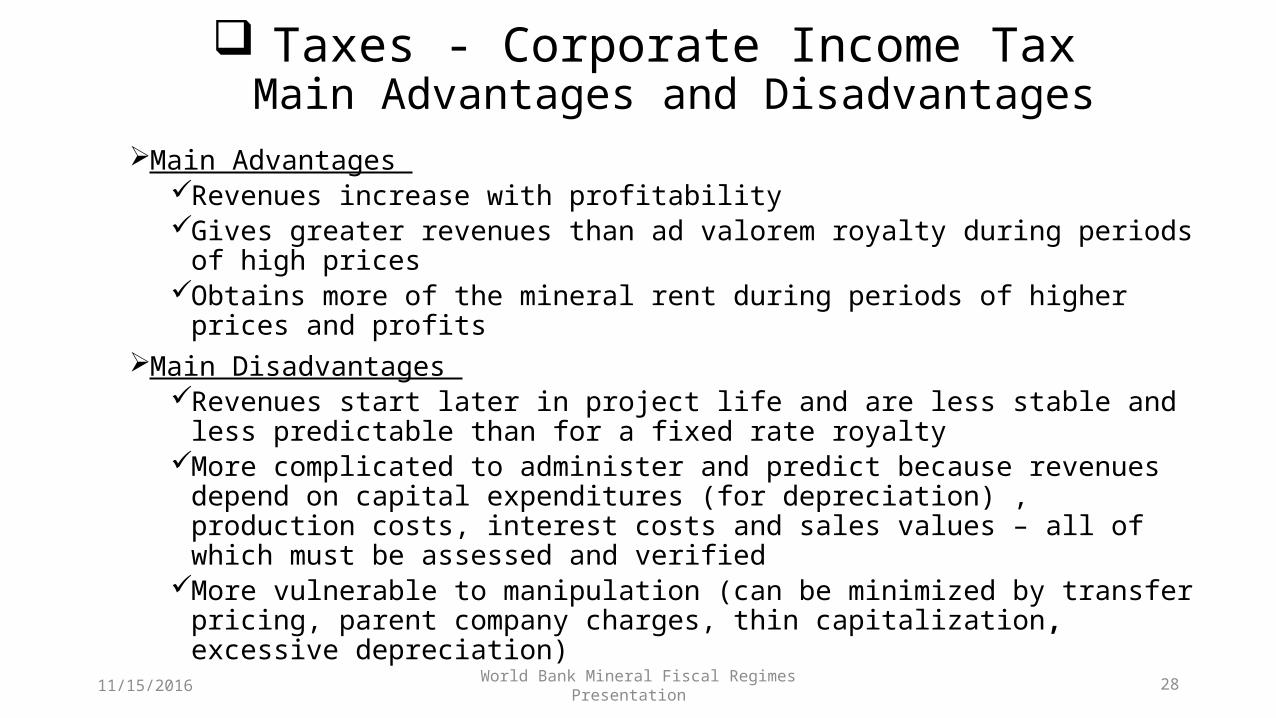

Taxes - Corporate Income TaxMain Advantages and Disadvantages

Main Advantages Revenues increase with profitabilityGives greater revenues than ad valorem royalty during periods of high prices Obtains more of the mineral rent during periods of higher prices and profits

Main Disadvantages Revenues start later in project life and are less stable and less predictable

than for a fixed rate royalty More complicated to administer and predict because revenues depend on

capital expenditures (for depreciation) , production costs, interest costs and sales values – all of which must be assessed and verified

More vulnerable to manipulation (can be minimized by transfer pricing, parent company charges, thin capitalization, excessive depreciation)

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 29

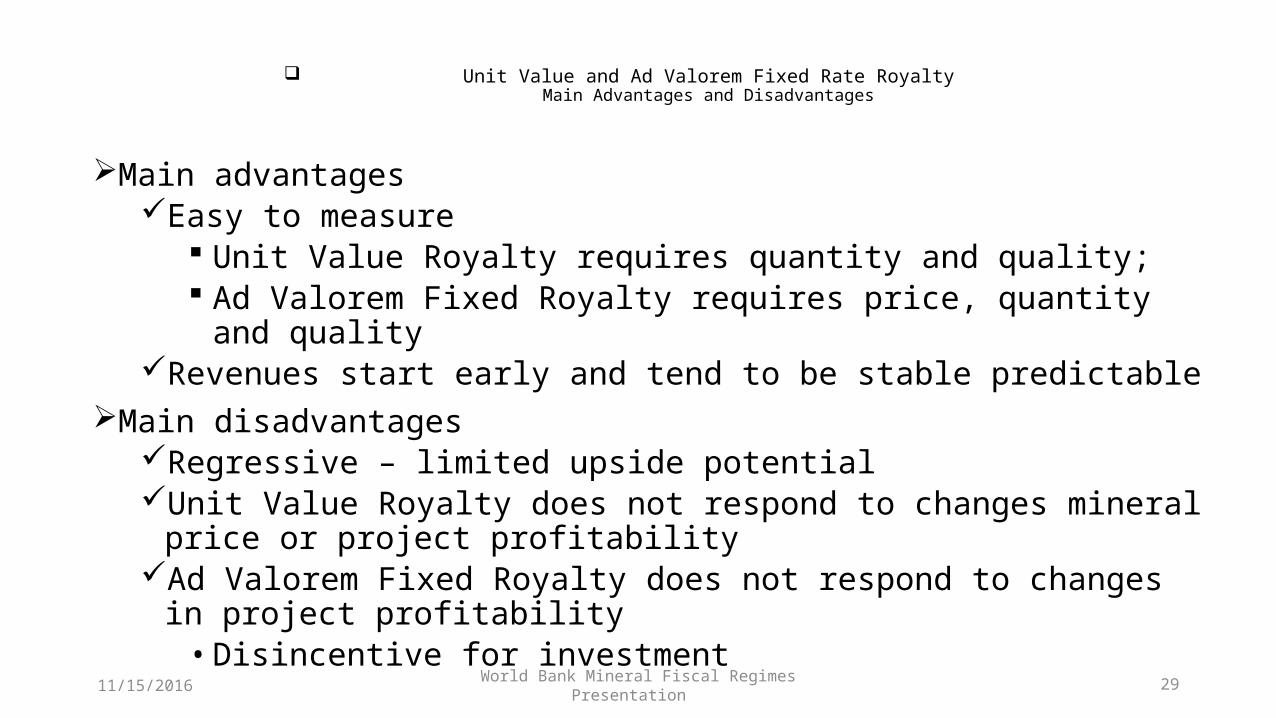

Unit Value and Ad Valorem Fixed Rate RoyaltyMain Advantages and Disadvantages

Main advantages Easy to measure

Unit Value Royalty requires quantity and quality; Ad Valorem Fixed Royalty requires price, quantity and quality

Revenues start early and tend to be stable predictable Main disadvantages

Regressive – limited upside potential Unit Value Royalty does not respond to changes mineral price or project

profitability Ad Valorem Fixed Royalty does not respond to changes in project profitability

• Disincentive for investment

11/15/2016

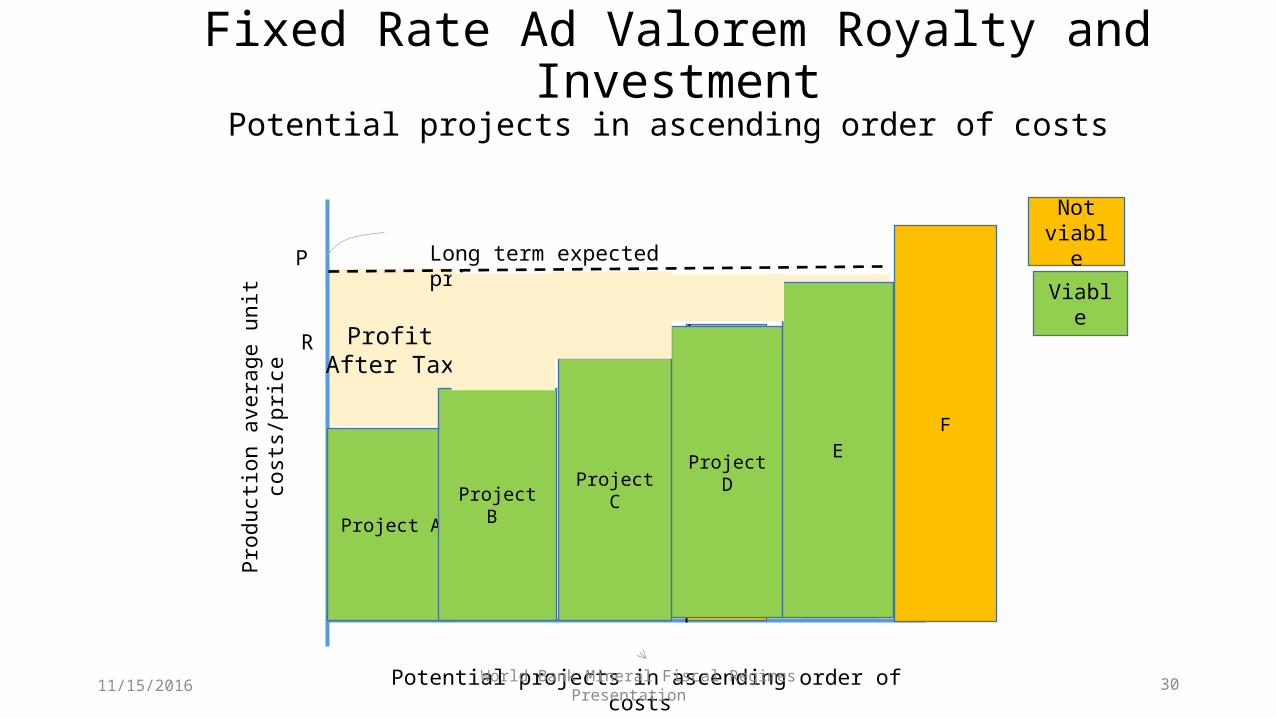

World Bank Mineral Fiscal Regimes Presentation 30

F

Pro

duct

ion

aver

age

unit

cost

s/pr

ice P

Potential projects in ascending order of costs

Fixed Rate Ad Valorem Royalty and Investment

Potential projects in ascending order of costs

Not viable

Viable

Long term expected price

Project CD

E

Project AProject B

R

Project DE

Profit After Tax

11/15/2016

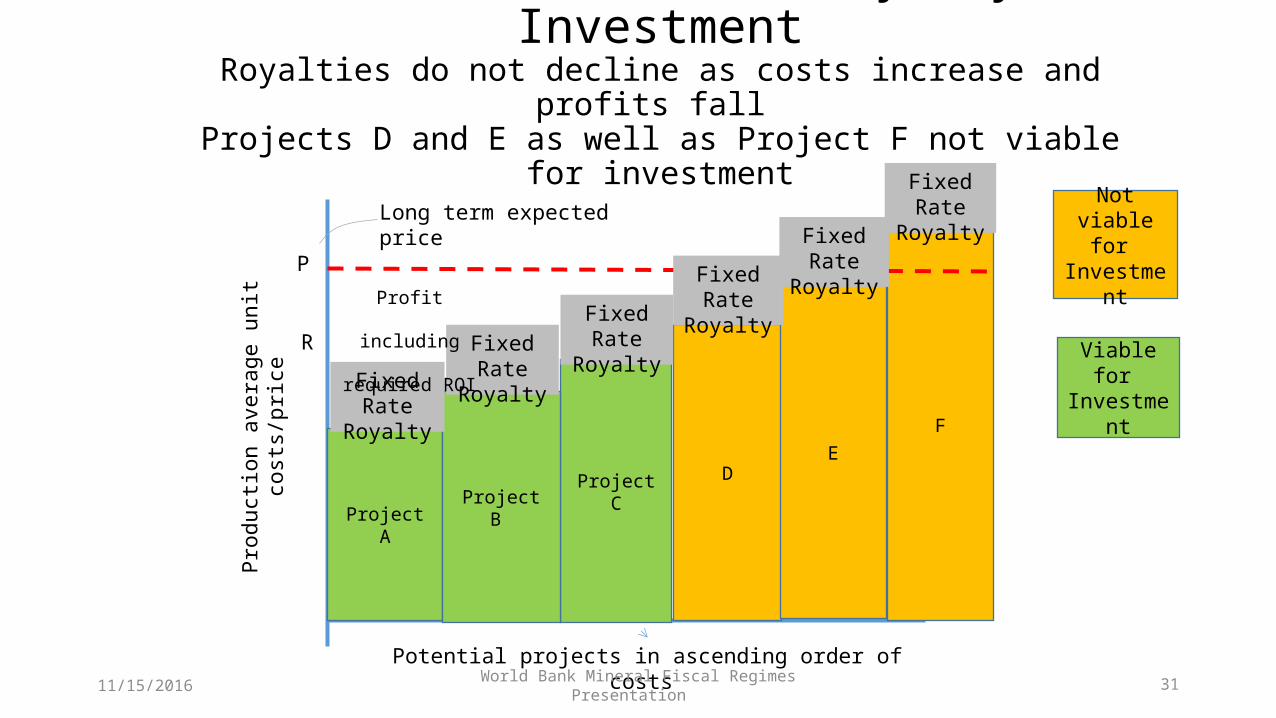

World Bank Mineral Fiscal Regimes Presentation 31

F

Pro

duct

ion

aver

age

unit

cost

s/pr

ice P

Potential projects in ascending order of costs

Fixed Rate Ad Valorem Royalty and Investment

Royalties do not decline as costs increase and profits fall Projects D and E as well as Project F not viable for

investmentLong term expected price

Project CD

E

Project AProject B

R

Fixed RateRoyalty

Fixed RateRoyalty

Fixed RateRoyalty

Fixed RateRoyalty

Fixed RateRoyalty

Fixed RateRoyalty

Profit including

required ROI

Not viablefor

Investment

Viablefor

Investment

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 32

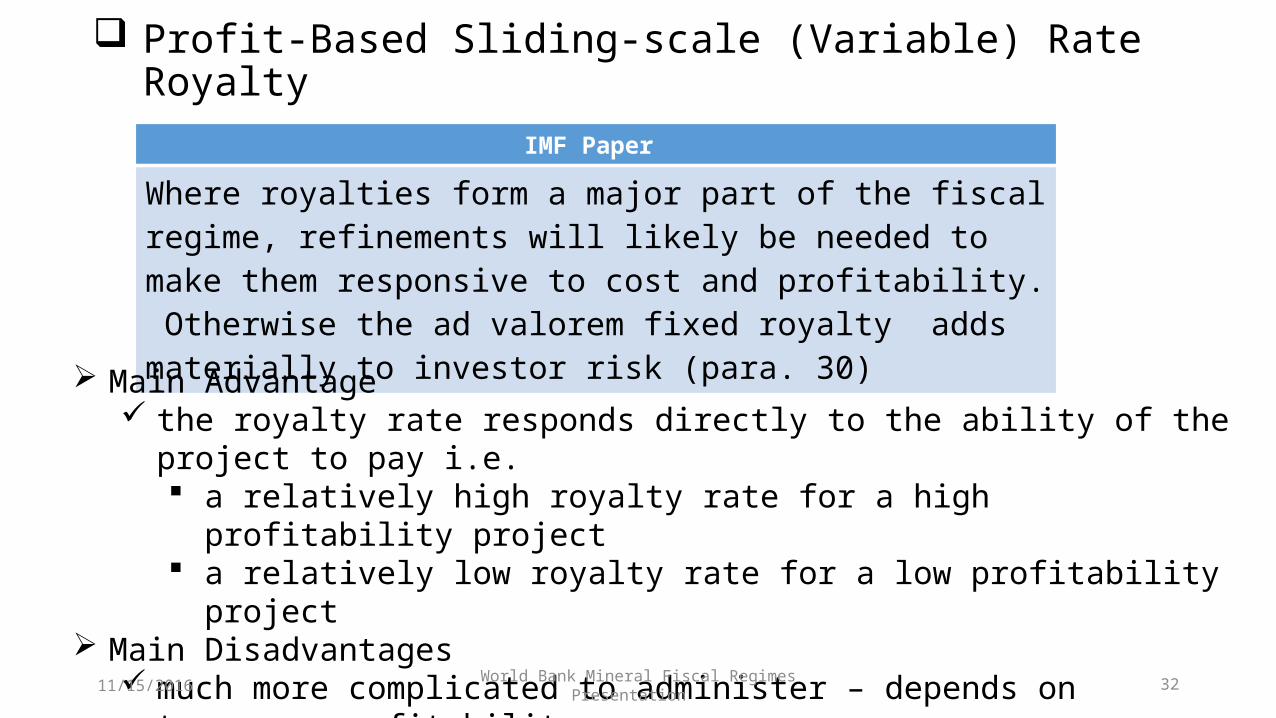

Profit-Based Sliding-scale (Variable) Rate RoyaltyIMF Paper

Where royalties form a major part of the fiscal regime, refinements will likely be needed to make them responsive to cost and profitability. Otherwise the ad valorem fixed royalty adds materially to investor risk (para. 30)

Main Advantage the royalty rate responds directly to the ability of the project to pay i.e.

a relatively high royalty rate for a high profitability project a relatively low royalty rate for a low profitability project

Main Disadvantages much more complicated to administer – depends on taxpayer profitability. Payments are much less stable than for the unit or fixed rate ad valorem royalties.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 33

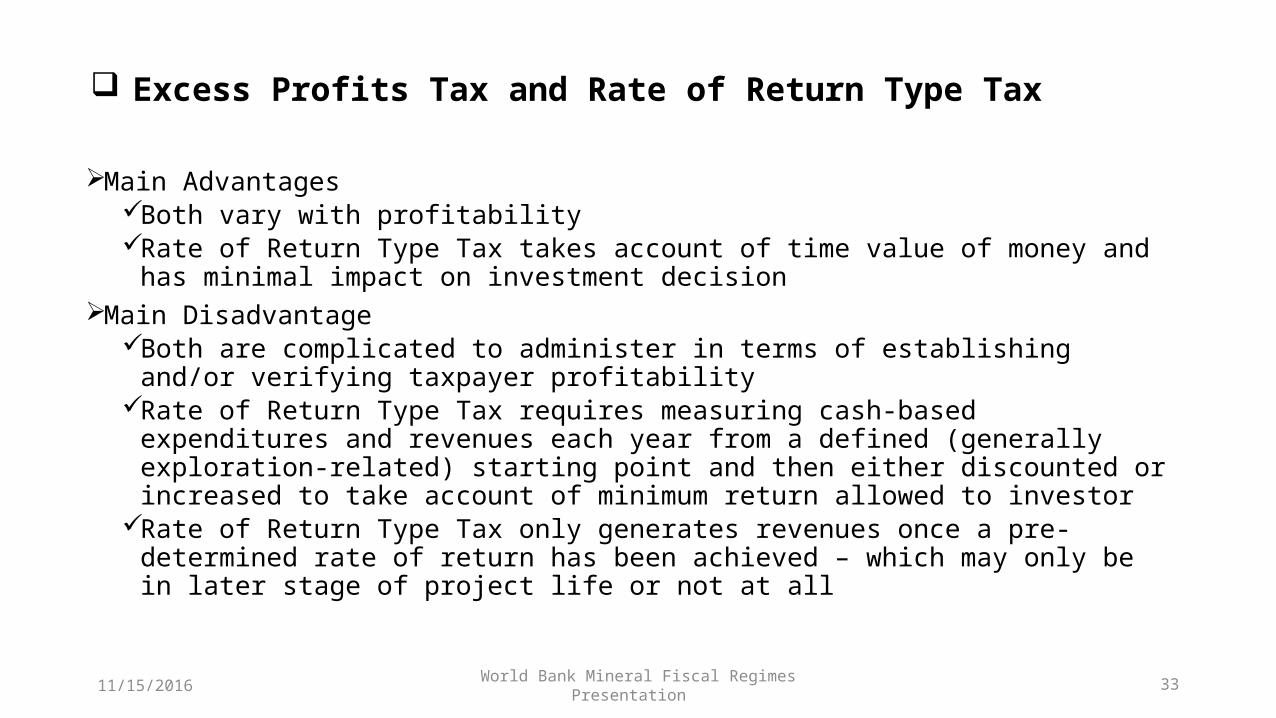

Excess Profits Tax and Rate of Return Type Tax

Main Advantages Both vary with profitabilityRate of Return Type Tax takes account of time value of money and has minimal impact

on investment decisionMain Disadvantage

Both are complicated to administer in terms of establishing and/or verifying taxpayer profitability

Rate of Return Type Tax requires measuring cash-based expenditures and revenues each year from a defined (generally exploration-related) starting point and then either discounted or increased to take account of minimum return allowed to investor

Rate of Return Type Tax only generates revenues once a pre-determined rate of return has been achieved – which may only be in later stage of project life or not at all

11/15/2016

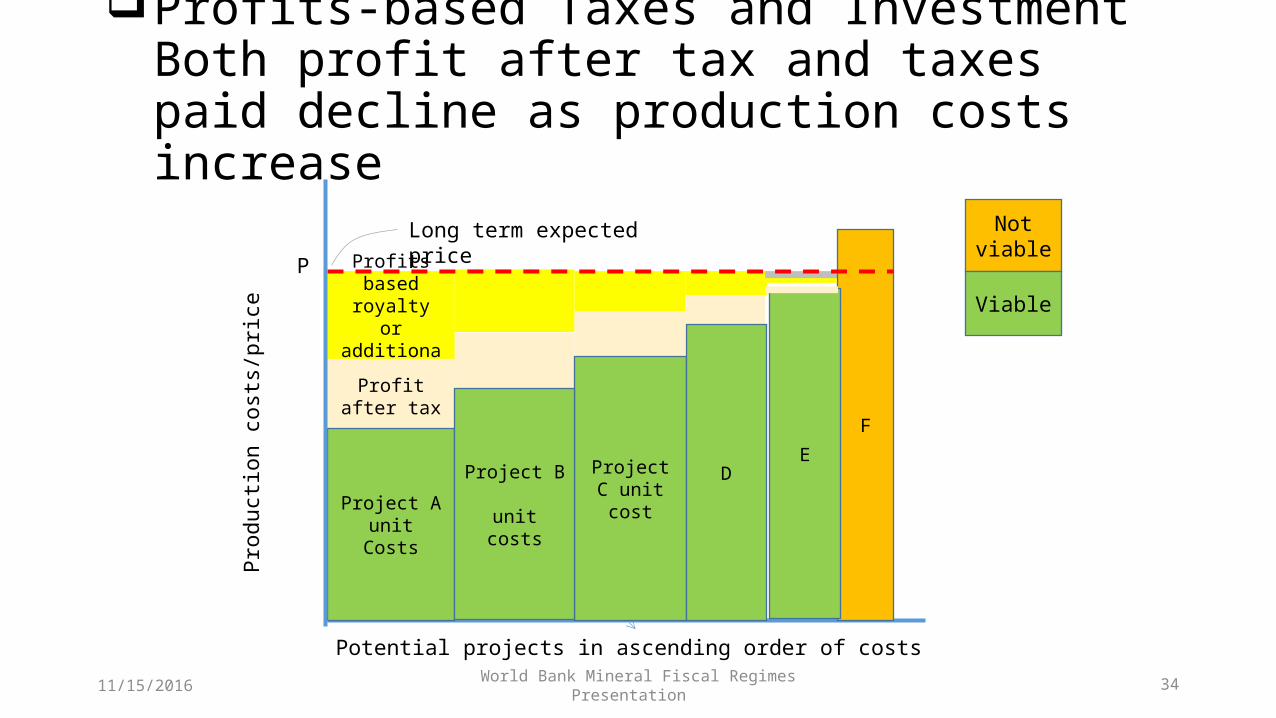

World Bank Mineral Fiscal Regimes Presentation 34

Profits based royalty or

additional tax

F

Pro

duct

ion

cost

s/pr

ice

P

Potential projects in ascending order of costs

Profits-based Taxes and InvestmentBoth profit after tax and taxes paid decline as production costs increase

Not viable

Viable

Long term expected price

Profit after tax

Project C unit cost

DE

Project Aunit Costs

Project B unit costs

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 35

What do Investors Seek in a Mineral Fiscal Regime?

The mineral sector requires large development expenditures including exploration and prefeasibility costs. Moreover, the initial exploration and construction phases are highly risky and offer no profits. A Modern Fiscal Regime can help attract good quality companies who are financially sound, technically competent and reliable and who will

• invest in potentially profitable (not loss-making) projects • not burden the government with excessive infrastructure costs • have the financial resources to withstand periods of low prices • follow the fiscal rules and not attempt to minimize taxes by profit-shifting or

cheating Considering these features, investors in the mining sector seek:• A fair sharing of taxable income – depends on total tax take . • Early recovery of initial capital – which is influenced by:

• the rate of depreciation for capital expenditures – high depreciation rates in the early years of operation will help bring forward capital recovery and

• the use of fixed rate royalties which will slow initial capital recovery11/15/2016

World Bank Mineral Fiscal Regimes Presentation 36

What do Investors Seek in a Mineral Fiscal Regime? (ii)• Investors look for minimum payments to government during loss-making periods,

through the introduction of legal provisions that allows for fixed rate payments (e.g. royalties) to be deferred during loss-making periods.

• Investors look for a longer loss carryover period (typically 8-10 years). Since mining projects can require large development expenditure including prior exploration and prefeasibility costs.

• Many large-scale investors look for fiscal regime stability, due to the long time horizons of mining projects, which can be provided by governments being willing to consider entering into a fiscal stability agreement between the investor and the government.

• Investors look for Double Taxation Agreements (DTAs) which can reduce aggregate tax payments in different jurisdictions. In particular DTAs can be used to reduce/minimize dividend withholding tax payments by foreign owners

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 37

B.2 INNOVATIONS IN DESIGNING MINERAL FISCAL REGIMES

The Key Decisions in Designing a Mineral Fiscal Regime

Slides 37-48

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 38

The Mineral Fiscal Regime and other Factors that influence a Country’s Attractiveness for

Mining Investment• Geological Prospectivity • Country Stability and Security• Mineral Licensing system – security of tenure etc. • Government mining equity policy• Government institutional capacity• Government track record regarding mining investment • Infrastructure availability • Mineral Fiscal regime

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 39

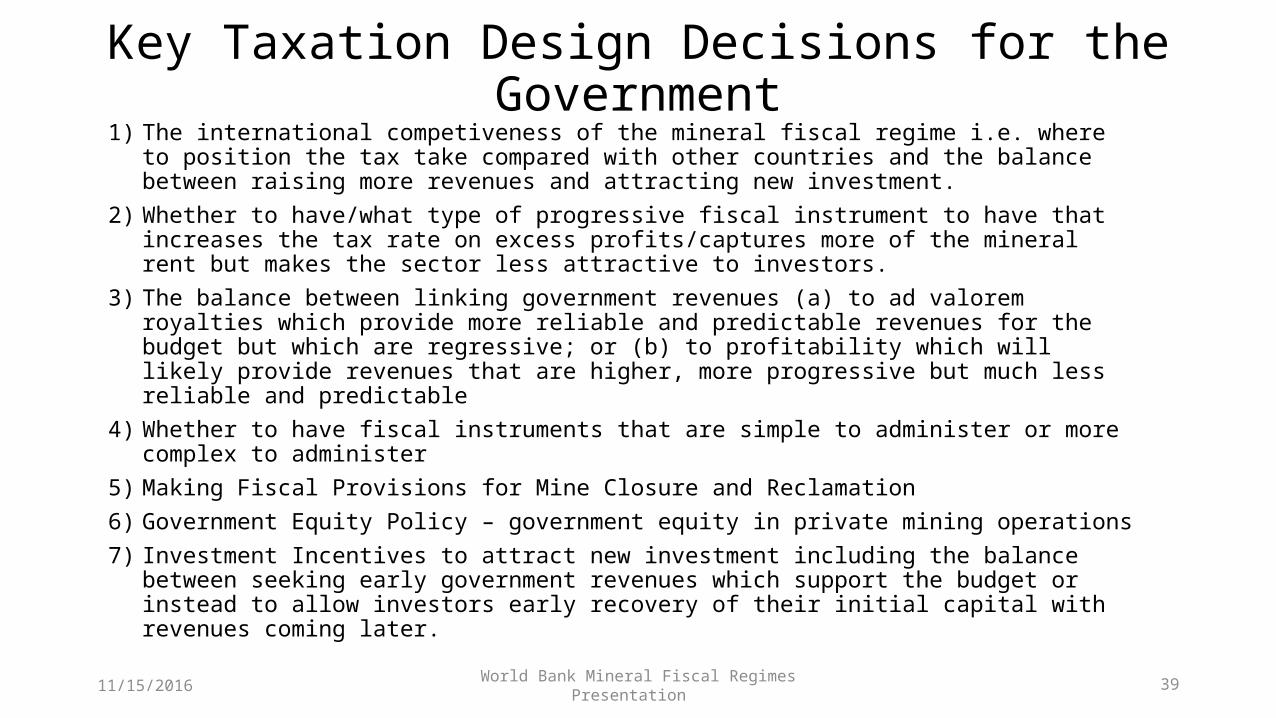

Key Taxation Design Decisions for the Government

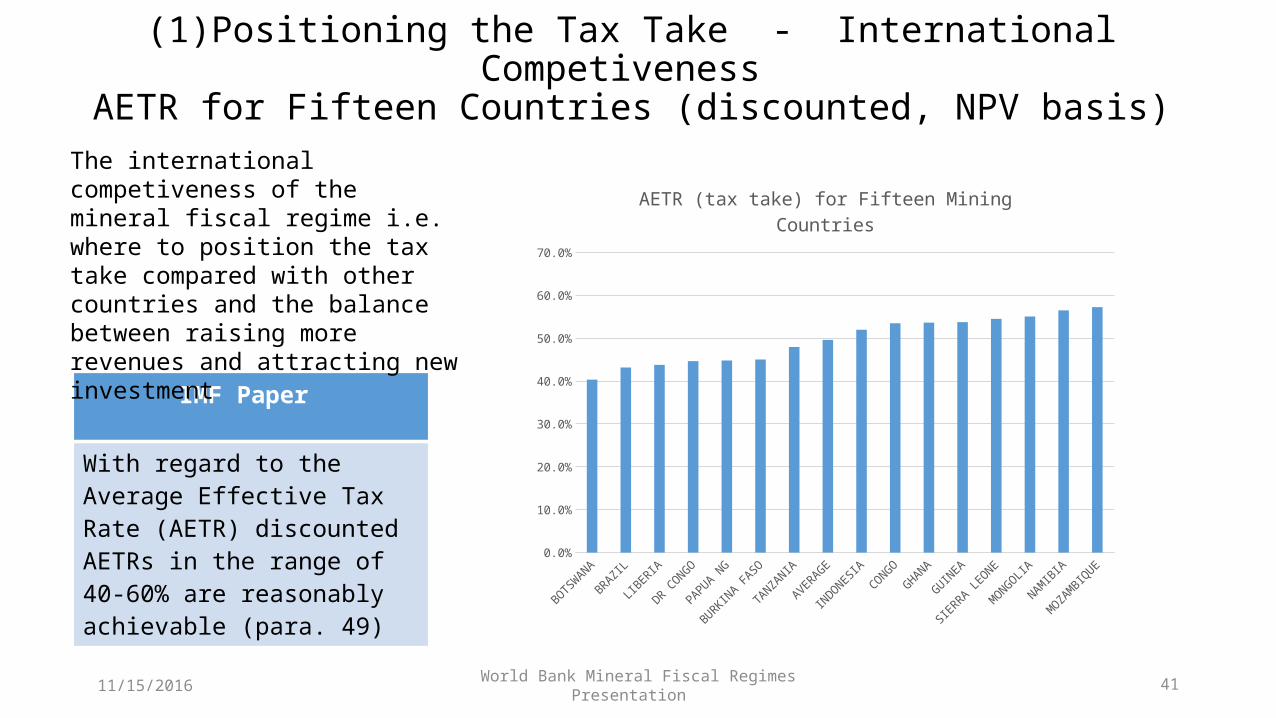

1) The international competiveness of the mineral fiscal regime i.e. where to position the tax take compared with other countries and the balance between raising more revenues and attracting new investment.

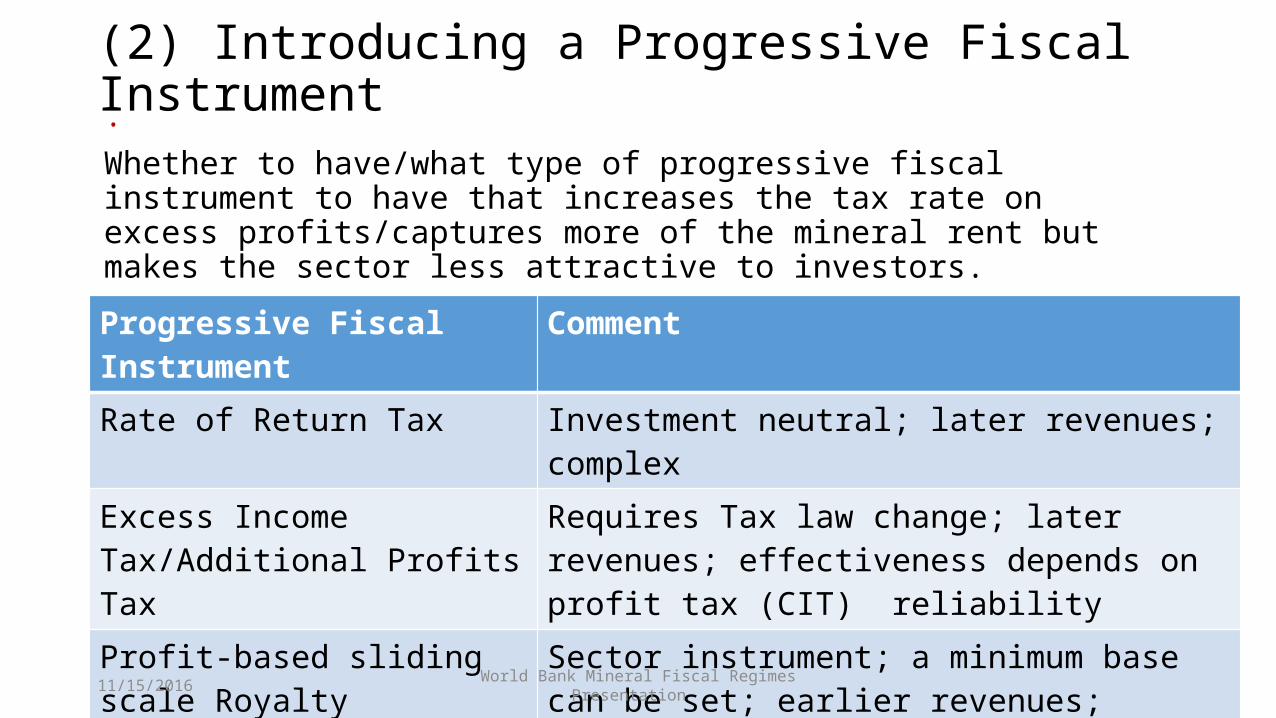

2) Whether to have/what type of progressive fiscal instrument to have that increases the tax rate on excess profits/captures more of the mineral rent but makes the sector less attractive to investors.

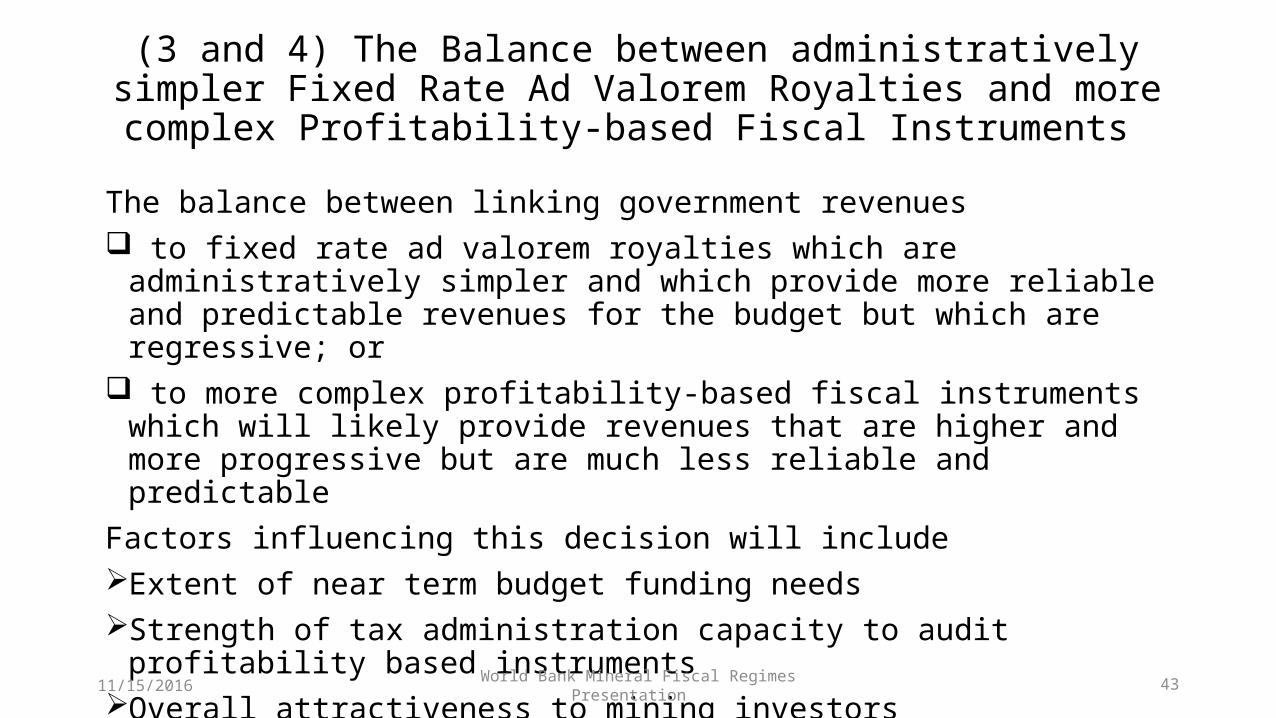

3) The balance between linking government revenues (a) to ad valorem royalties which provide more reliable and predictable revenues for the budget but which are regressive; or (b) to profitability which will likely provide revenues that are higher, more progressive but much less reliable and predictable

4) Whether to have fiscal instruments that are simple to administer or more complex to administer

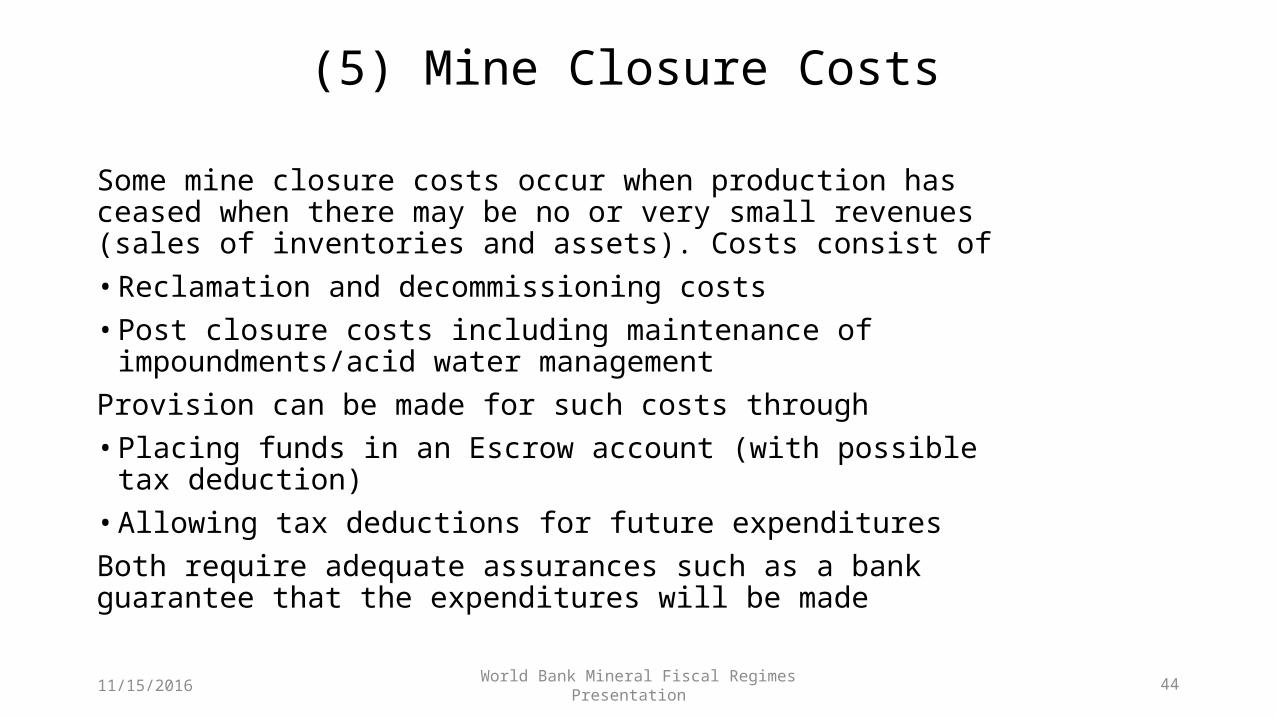

5) Making Fiscal Provisions for Mine Closure and Reclamation6) Government Equity Policy – government equity in private mining operations 7) Investment Incentives to attract new investment including the balance between seeking early

government revenues which support the budget or instead to allow investors early recovery of their initial capital with revenues coming later.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 40

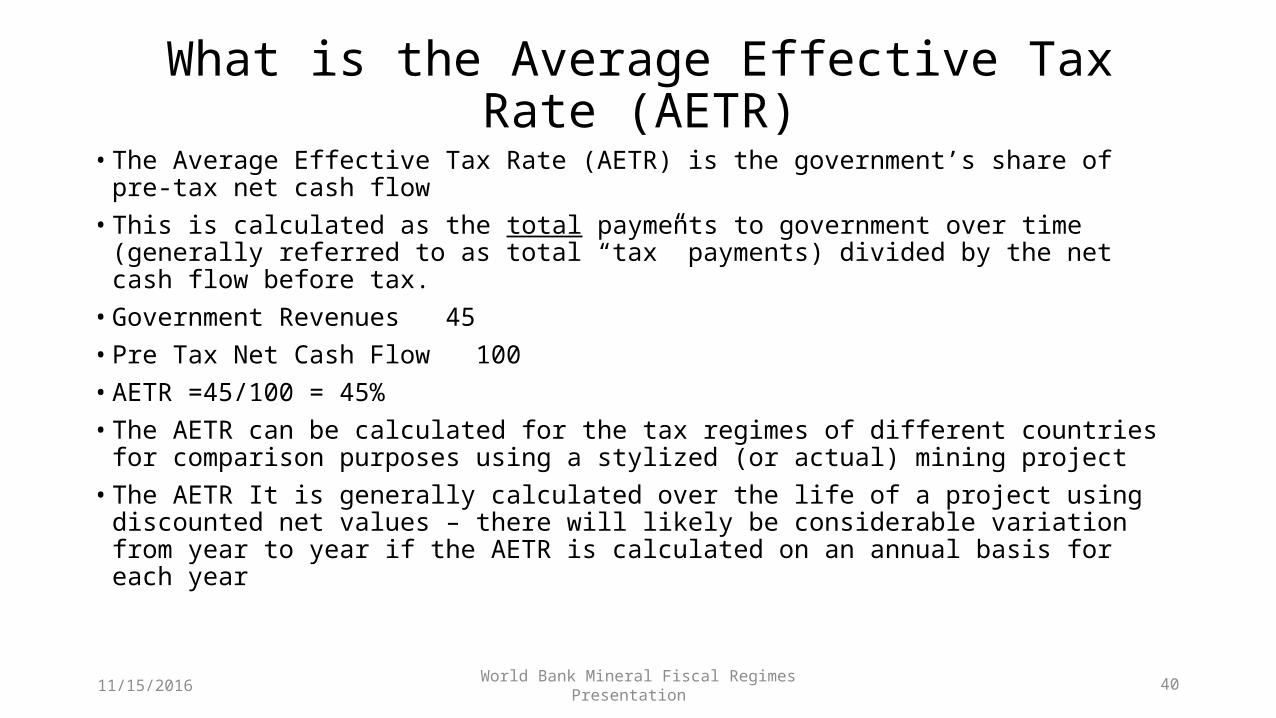

What is the Average Effective Tax Rate (AETR)

• The Average Effective Tax Rate (AETR) is the government’s share of pre-tax net cash flow • This is calculated as the total payments to government over time (generally referred to

as total “tax” payments) divided by the net cash flow before tax.• Government Revenues 45• Pre Tax Net Cash Flow 100• AETR =45/100 = 45%• The AETR can be calculated for the tax regimes of different countries for comparison

purposes using a stylized (or actual) mining project • The AETR It is generally calculated over the life of a project using discounted net values –

there will likely be considerable variation from year to year if the AETR is calculated on an annual basis for each year

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 41

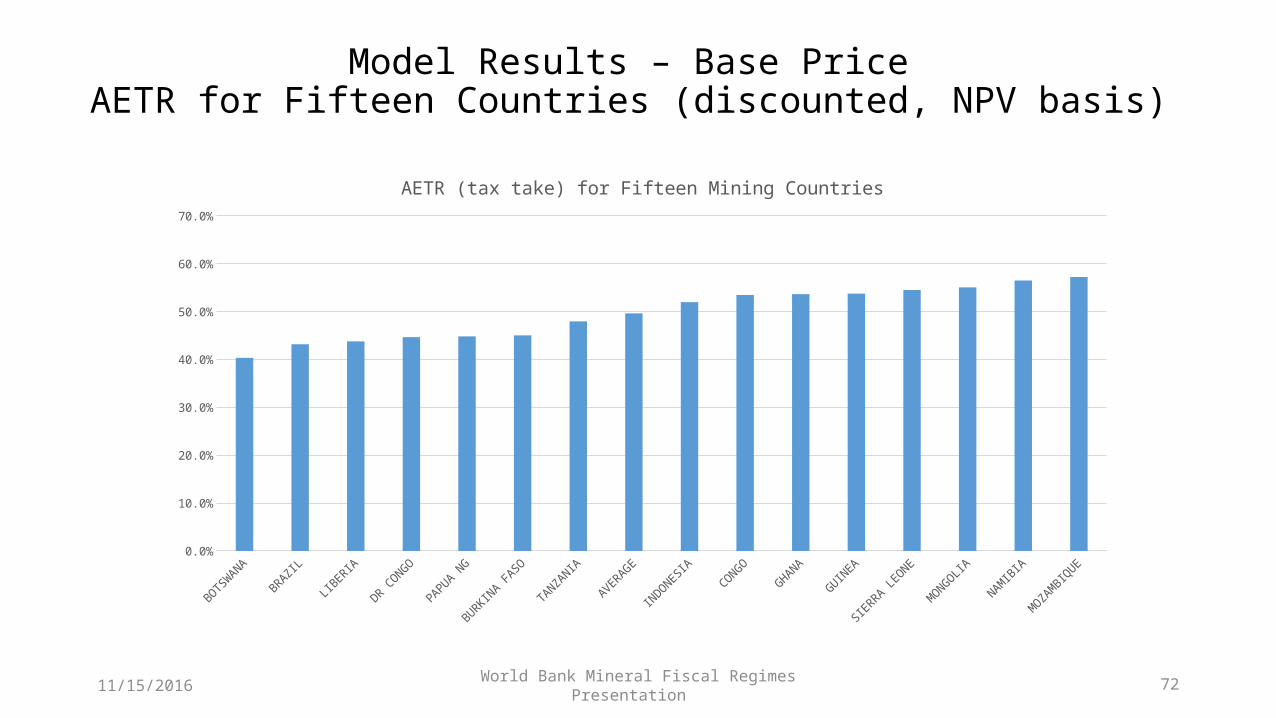

(1)Positioning the Tax Take - International Competiveness

AETR for Fifteen Countries (discounted, NPV basis)

IMF Paper

With regard to the Average Effective Tax Rate (AETR) discounted AETRs in the range of 40-60% are reasonably achievable (para. 49)

BOTSWANA

BRAZIL

LIBERIA

DR CONGO

PAPUA NG

BURKINA FASO

TANZANIA

AVERAGE

INDONESIA

CONGO

GHANA

GUINEA

SIERRA LEONE

MONGOLIA

NAMIBIA

MOZAMBIQUE0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

AETR (tax take) for Fifteen Mining Countries

The international competiveness of the mineral fiscal regime i.e. where to position the tax take compared with other countries and the balance between raising more revenues and attracting new investment

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 42

(2) Introducing a Progressive Fiscal Instrument .Whether to have/what type of progressive fiscal instrument to have that increases the tax rate on excess profits/captures more of the mineral rent but makes the sector less attractive to investors.

Progressive Fiscal Instrument CommentRate of Return Tax Investment neutral; later revenues; complexExcess Income Tax/Additional Profits Tax

Requires Tax law change; later revenues; effectiveness depends on profit tax (CIT) reliability

Profit-based sliding scale Royalty Sector instrument; a minimum base can be set; earlier revenues; depends on CIT reliability

Price-based sliding scale Royalty Sector instrument; a minimum base can be set; earlier revenues; needs frequent adjustment

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 43

(3 and 4) The Balance between administratively simpler Fixed Rate Ad Valorem Royalties and more

complex Profitability-based Fiscal Instruments The balance between linking government revenues to fixed rate ad valorem royalties which are administratively simpler and which

provide more reliable and predictable revenues for the budget but which are regressive; or

to more complex profitability-based fiscal instruments which will likely provide revenues that are higher and more progressive but are much less reliable and predictable

Factors influencing this decision will include Extent of near term budget funding needsStrength of tax administration capacity to audit profitability based instruments Overall attractiveness to mining investors

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 44

(5) Mine Closure Costs

Some mine closure costs occur when production has ceased when there may be no or very small revenues (sales of inventories and assets). Costs consist of • Reclamation and decommissioning costs• Post closure costs including maintenance of impoundments/acid

water managementProvision can be made for such costs through• Placing funds in an Escrow account (with possible tax deduction)• Allowing tax deductions for future expenditures Both require adequate assurances such as a bank guarantee that the expenditures will be made

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 45

(6) Government Equity Participation in Mining ProjectsSome governments have a policy of having the right to obtain a minority share of the equity in a new mining venture.The equity share is generally in the range of 5-10% but Mongolia has taken as much as 34%. For African countries (mostly around 10%) see ADB Paper No 147 Gold Mining in Africa: Maximizing Economic Returns for Countries, March 2012The main benefits are that the Government obtains

• a share in the profits of the project (noting that money is only received when dividends are paid) and another mechanism to obtain mineral rent

• a “seat at the table” in the Boardroom• access to internal company information including company plans and

projections • an asset (i.e. the shares) that may possibly be sold later in project life and may

generate substantial funds if the company is very profitable

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 46

(6) cont - Options for Obtaining Equity• Governments may consider taking paid-up equity on full cost basis which gives them equal

standing with other investors. Paid in equity requires capital but avoids exploration risks• Carried equity means that the private shareholder(s) must fund the government’s equity

share initially. It is subsequently paid for through dividends• Free equity is equivalent to a dividend withholding tax and is resented by investors – but a

modest equity holding of say 10% can be compensated for by exempting foreign shareholders from any prevailing (10%?) dividend withholding tax.

A Shareholder Agreement can be used to clarify the rights and obligations related to the equity participation, including, a seat on the board, access to internal company projections and plans, anti-dilution of the government’s interest and contingent liabilities; shareholder funding of any cash shortfalls that occur But equity comes with shareholder risks - Income is not immediate and it may be a number of years before dividends are paid and dividends can be very uncertain and volatile and Government may need to help

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 47

(6) cont - Main Implications of Government Equity for the Investor

Equity participation is a disincentive for investment• Investors see it as reducing their profits.• If it is “free” the investor must fund the government’s share of investment.• If it is carried the investor must raise all of the the initial capital • Smaller companies may not explore if they have to mobilize capital for the

government's shareholding.• If the percentage is very high or if the government is viewed as unreliable

or unstable, many investors may simply stay away from the country• Even if equity is paid for at full cost, government has not had to bear the

exploration risks.Also Equity creates a potential conflict of interest since government becomes both regulator and owner.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 48

Investment incentives can include – in response to investor concerns:• Low ad valorem royalty rates (less than 3%) • Accelerated Depreciation for tax purposes compared with other sectors. Earlier capital

recovery helps protect against risk that the rules will change and results in faster recycling of capital that can be used for other new projects

• a longer Loss Carryover period (than other sectors) - typically 8-10 years.• Use of Double Taxation Agreements to reduce withholding taxes• fiscal regime stability through fiscal stability agreements.

• To protect from possible abuse, any such agreement should be • time-bound (say 5-10 years from the start of production) and • should only cover the rates of specific fiscal instruments such as profits tax,

withholding taxes to non-residents, mineral royalties and customs duties. • There should be no overall “blanket” fiscal stability agreements.

6 Mineral Fiscal Regime - Investment Incentives

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 49

C.1 MODELING THE MINERAL FISCAL REGIME – QUANTIFYING THE TAX TAKE FROM

THE DIFFERENT FISCAL INSTRUMENTS

An example of a basic Mineral Fiscal Model - structure and inputs

Slides 49-66

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 50

High-level Summary Mine Financial Model Purpose

• The main purpose of this model is to provide an indicative estimate of the (discounted) Net Present Value (NPV) Average Effective Tax Rate (AETR) for the mineral fiscal regimes of fifteen countries.

• It also provides indicative estimates of• The After Tax Internal Rate of Return for an Investor • The time for recovery of the initial capital expenditure by the

Investor• The relative size of government revenues for the three main fiscal

instruments (CIT, DWT, and royalties).

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 51

High-level Summary Mine Financial ModelCharacteristics

• The model is described as a “high-level summary model” for two reasons.• First, it considers instruments that have the most significant financial impact.

Thus, customs duties, VAT and various smaller fees and any municipal-level taxes are not included. However, their impact can be examined through sensitivity analyses

• Second, some of the assumptions are representative but not entirely precise. For example all capital expenditures are depreciated on a straight line basis over a certain number of years (ranging from 1 year to 10 years) based on the tax depreciation rules for a country. Thus, depreciation is very much simpler than the actual tax legislation in most countries.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 52

High-level Summary Mine Financial ModelUsefulness

The high level summary approach is used,• First, to enable to enable high level summary AETR cross-country

comparisons to be made in a manageable manner.• Second, to understand the relative impact of the most important

fiscal instruments on the AETR; and• Third, to examine the extent to which different mineral fiscal

regimes are progressive or regressive • Fourth, to undertake sensitivity analyses regarding different

price and cost assumptions on the AETR

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 53

Using the Results – Important ConsiderationsA cautionary note is needed on two fronts:First, a number of countries have signed Double Taxation Agreements which result in

foreign investors domiciled in the other DTA country being exempt from dividend withholding taxes. o For example, DTAs signed with the Netherlands have this feature. o Therefore, the column with the combined CIT and Dividend Withholding Taxes must be

treated with some caution. o In addition governments must protect against Double Taxation Agreements with other

countries being abused by companies (treaty shopping)Second, where an equity share is taken by the government on a free or carried basis, the

income (i.e. dividends received) should also be included. Such income may help offset reductions in government revenues if dividend withholding taxes are reduced or eliminated by a Double Taxation Agreement.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 54

Overview of Model Structure

Overview of Model Sheets • Inputs – Assumptions for the mine (investment; quantity, costs, sales

price) • Inputs – Assumptions for the Fiscal Regime • Inputs – Assumption for Dividend Distribution and Borrowing • Model structure overview – Income Statement • Model structure overview – Cash flow Statement • Results – Government Revenues • Results – Cash Flow; IRR; AETR

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 55

High-level Summary Mine Financial Model Overview Of Model Sheets

• The model consists of • Sheet 1 Input sheet• Sheets 2-16 one sheet showing results for each of the fifteen countries• Sheet 17 – one sheet showing results for the “average country regime”• Sheet 18 – Results for NPV10 AETR • Sheet 18 – Results for IRRAT • Sheet 20 – Results for Initial Capital Recovery

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 56

High-level Summary Mine Financial Model

Key Assumptions – The Mine• Saleable Metal Content of Production• Capital Expenditures consisting of exploration and development

costs, replacement capital expenditures• Construction period• Mine Life• Production costs and processing costs • Mine closure costsThe model structure also includes, if data is available, • Customs duties on capital expenditures and operating costs • Borrowing (if any) including debt %, interest rate and length

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 57

Setting the mine production, cost and price assumptions

• The IMF practice is to develop a model that fits the characteristics of a particular country

• For the purpose of the presentation, a more generic copper/gold model is used to illustrate how a model works.

• Generally the impact of different tax instruments can be understood by setting investments costs, production costs and revenues that result in a before tax internal rate of return in the range of 20-30% for the base case.

• For this model the base case before tax internal rate of return is 25%.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 58

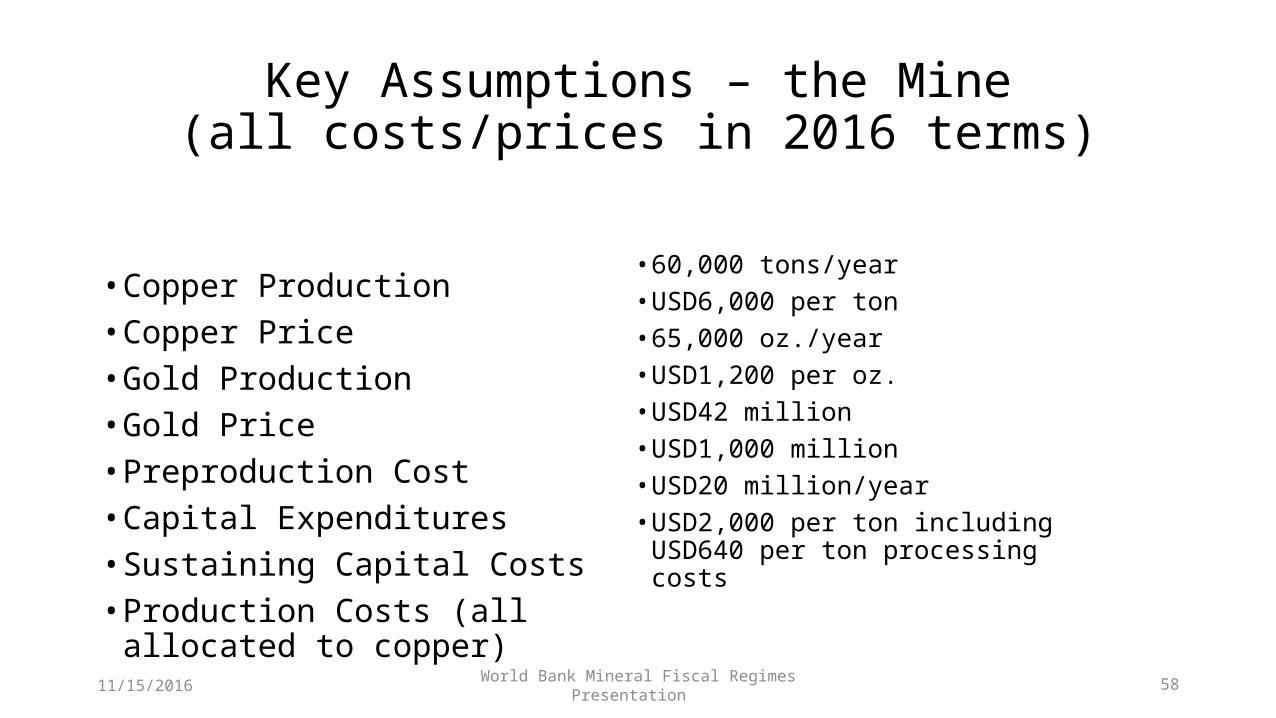

Key Assumptions – the Mine(all costs/prices in 2016 terms)

• Copper Production• Copper Price• Gold Production• Gold Price• Preproduction Cost• Capital Expenditures • Sustaining Capital Costs• Production Costs (all allocated to

copper)

• 60,000 tons/year • USD6,000 per ton• 65,000 oz./year• USD1,200 per oz. • USD42 million • USD1,000 million• USD20 million/year• USD2,000 per ton including

USD640 per ton processing costs

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 59

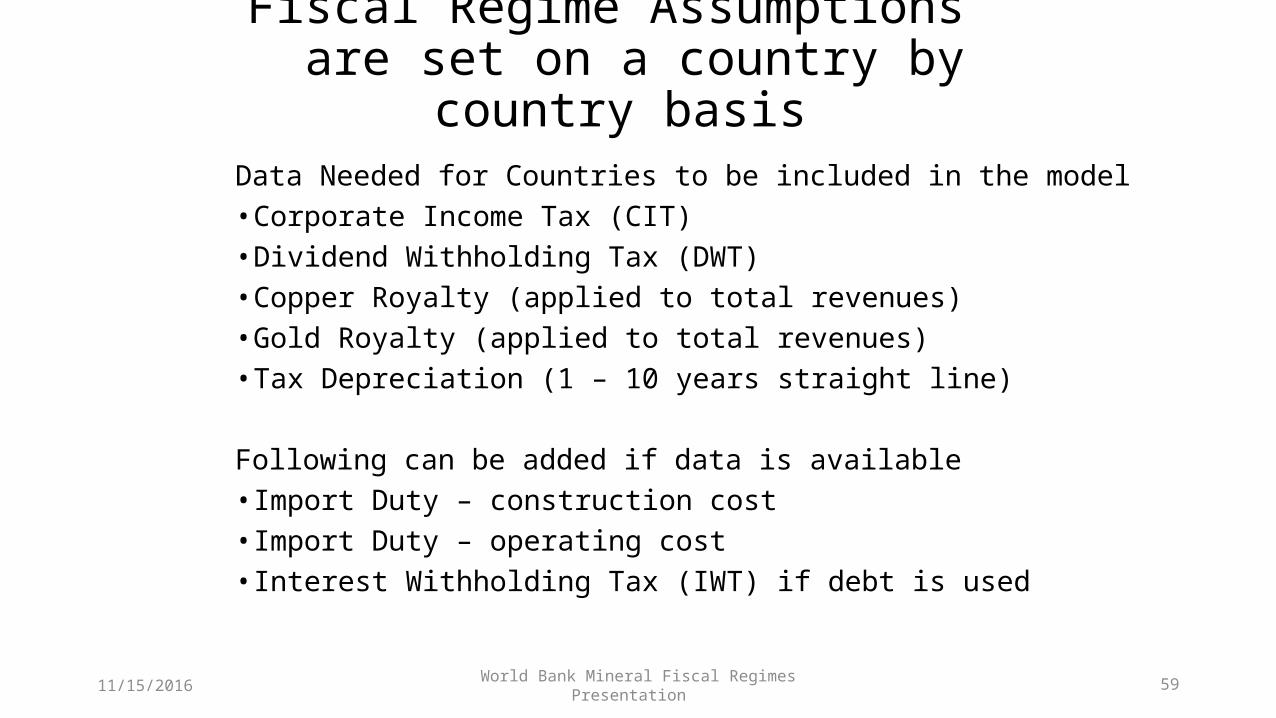

Fiscal Regime Assumptions are set on a country by country

basis Data Needed for Countries to be included in the model• Corporate Income Tax (CIT) • Dividend Withholding Tax (DWT) • Copper Royalty (applied to total revenues)• Gold Royalty (applied to total revenues)• Tax Depreciation (1 – 10 years straight line)

Following can be added if data is available• Import Duty – construction cost• Import Duty – operating cost• Interest Withholding Tax (IWT) if debt is used

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 60

Dividend Distribution and Borrowing Assumptions

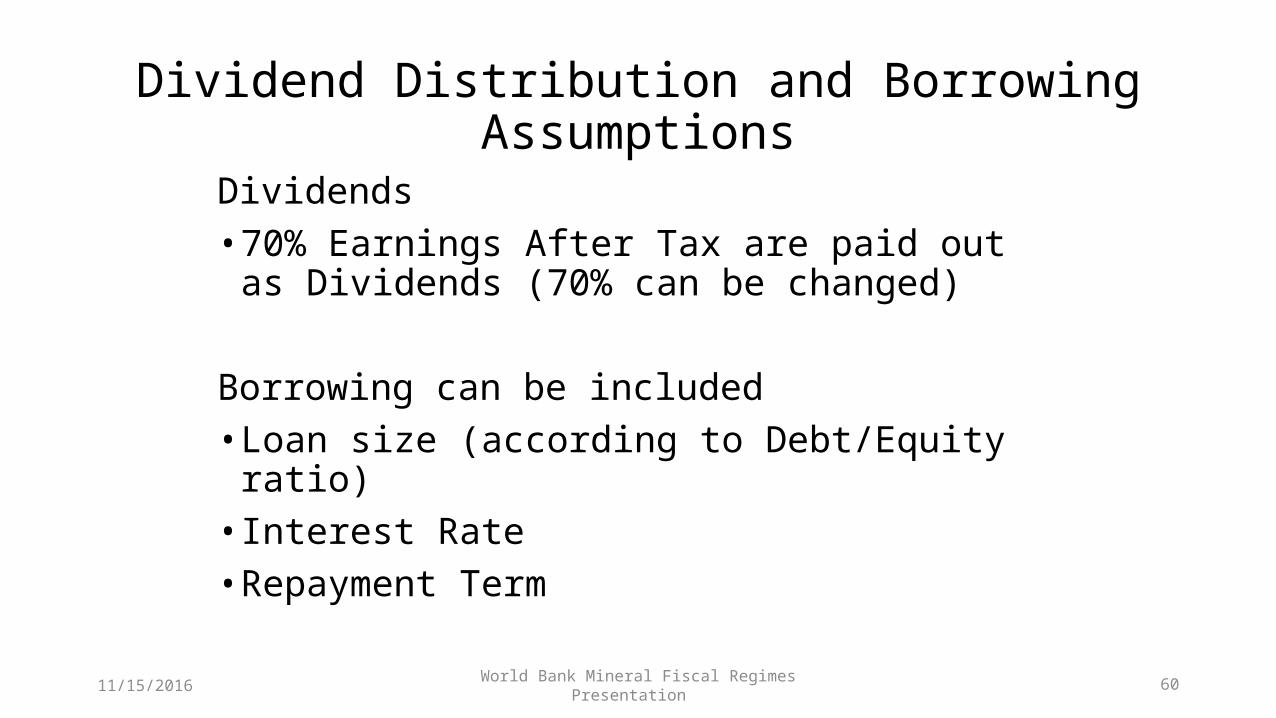

Dividends• 70% Earnings After Tax are paid out as Dividends

(70% can be changed)

Borrowing can be included• Loan size (according to Debt/Equity ratio)• Interest Rate• Repayment Term

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 61

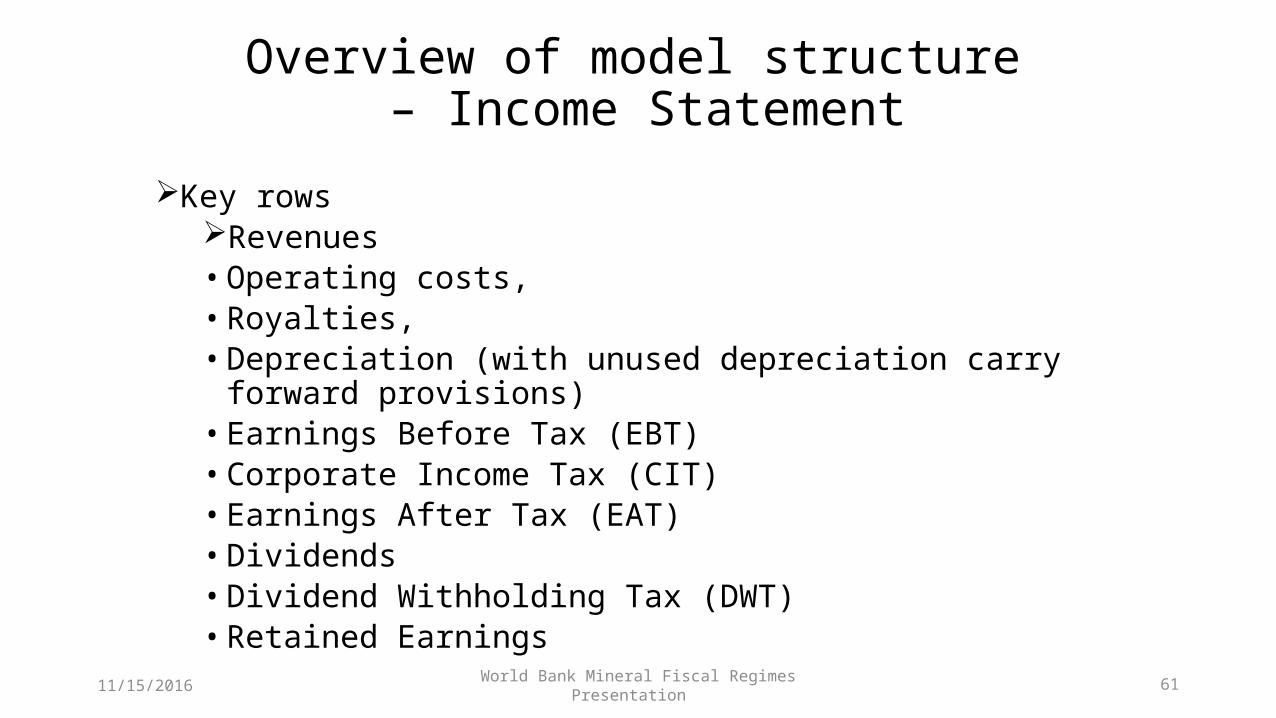

Overview of model structure – Income Statement

Key rowsRevenues • Operating costs, • Royalties, • Depreciation (with unused depreciation carry forward provisions)• Earnings Before Tax (EBT)• Corporate Income Tax (CIT)• Earnings After Tax (EAT)• Dividends• Dividend Withholding Tax (DWT)• Retained Earnings

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 62

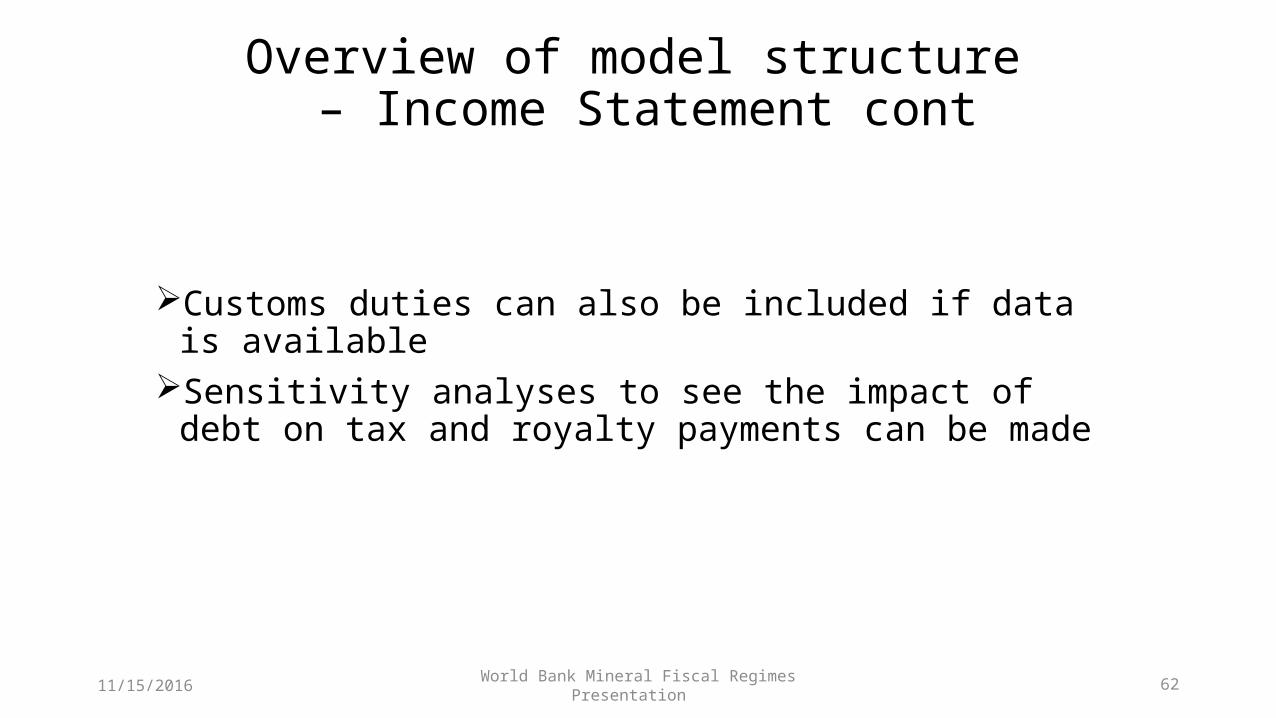

Overview of model structure – Income Statement cont

Customs duties can also be included if data is availableSensitivity analyses to see the impact of debt on tax and royalty

payments can be made

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 63

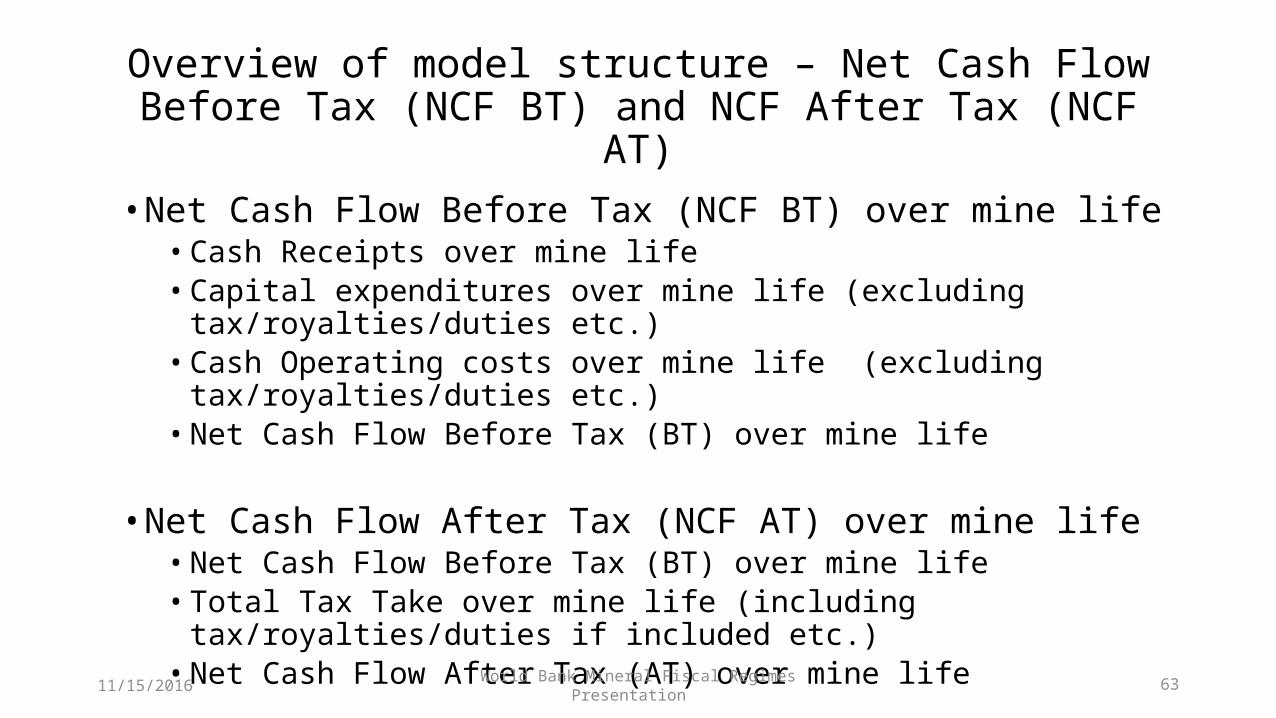

Overview of model structure – Net Cash Flow Before Tax (NCF BT) and NCF After Tax (NCF AT)• Net Cash Flow Before Tax (NCF BT) over mine life

• Cash Receipts over mine life• Capital expenditures over mine life (excluding tax/royalties/duties etc.)• Cash Operating costs over mine life (excluding tax/royalties/duties etc.)• Net Cash Flow Before Tax (BT) over mine life

• Net Cash Flow After Tax (NCF AT) over mine life• Net Cash Flow Before Tax (BT) over mine life• Total Tax Take over mine life (including tax/royalties/duties if included etc.)• Net Cash Flow After Tax (AT) over mine life

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 64

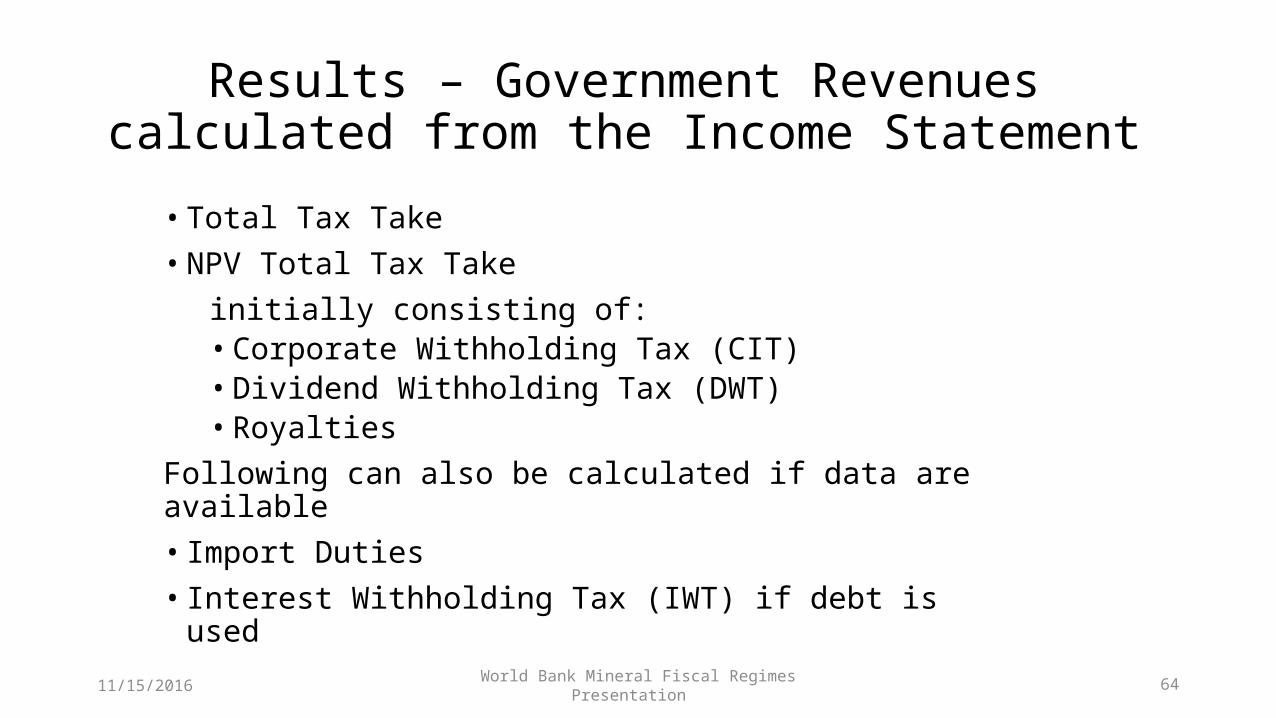

Results – Government Revenues calculated from the Income Statement • Total Tax Take • NPV Total Tax Take

initially consisting of:• Corporate Withholding Tax (CIT)• Dividend Withholding Tax (DWT)• Royalties

Following can also be calculated if data are available• Import Duties• Interest Withholding Tax (IWT) if debt is used

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 65

Results – NCF BT; NCF AT; IRR BT; IRR AT; AETR

In addition to Total Tax Take the following are calculated• Net Cash Flow Before Tax• NPV Net Cash Flow Before Tax• Net Cash Flow After Tax• NPV Net Cash Flow After Tax• IRR Before Tax• IRR After Tax• Average Effective Tax Rate (AETR)• Discounted AETR

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 66

Results – AETR and Total Tax Take • AETR calculations for each of the fifteen countries using the fiscal regime data

(i.e. CIT, DWT, royalty and depreciation) information for each• The absolute size of payments are not very meaningful because they are only

relevant to the mine being modelled. • But they can be used to examine the relative size of payments from each

instrument. • Sensitivity runs can also be made with different prices or costs to see the impact

of different fiscal regimes for very profitable projects and for marginally profitable projects

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 67

C.2 COMPARING COUNTRY-SPECIFIC MINERAL FISCAL REGIMES

Using the Model to calculate the Average Effective Tax Rate (AETR) and Pre-Tax/Post Tax Rates of Returnfor Fifteen Different Mining Countries

Slides 67-82

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 68

Summary Mineral Fiscal Regimes for Fifteen Mining Countries

• Summary data includes the following fiscal instruments for Fifteen Mining Countries

• Corporate Income Tax - CIT• Dividend Withholding Tax - DWT• Ad valorem fixed Royalty• A summary tax depreciation rule

• Data collected for Fifteen Mining Countries

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 69

Summary Mineral Fiscal Regimes for fifteen mining countries

• Data collected for 15 Countries• Sources include

• Corporate income taxes, mining royalties and other mining taxes A summary of rates and rules in selected countries PWC June 2012

• IMF various Country Reports 2010 -2013• Gold Mining in Africa : Maximizing Economic Returns for

Countries African Development Bank March 2013

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 70

Summary Regimes for fifteen mining countries

% CIT DWT CombinedCIT/DWT

Copper/Base

MetalsRoyalty

GoldRoyalty

DepnyearsS/L

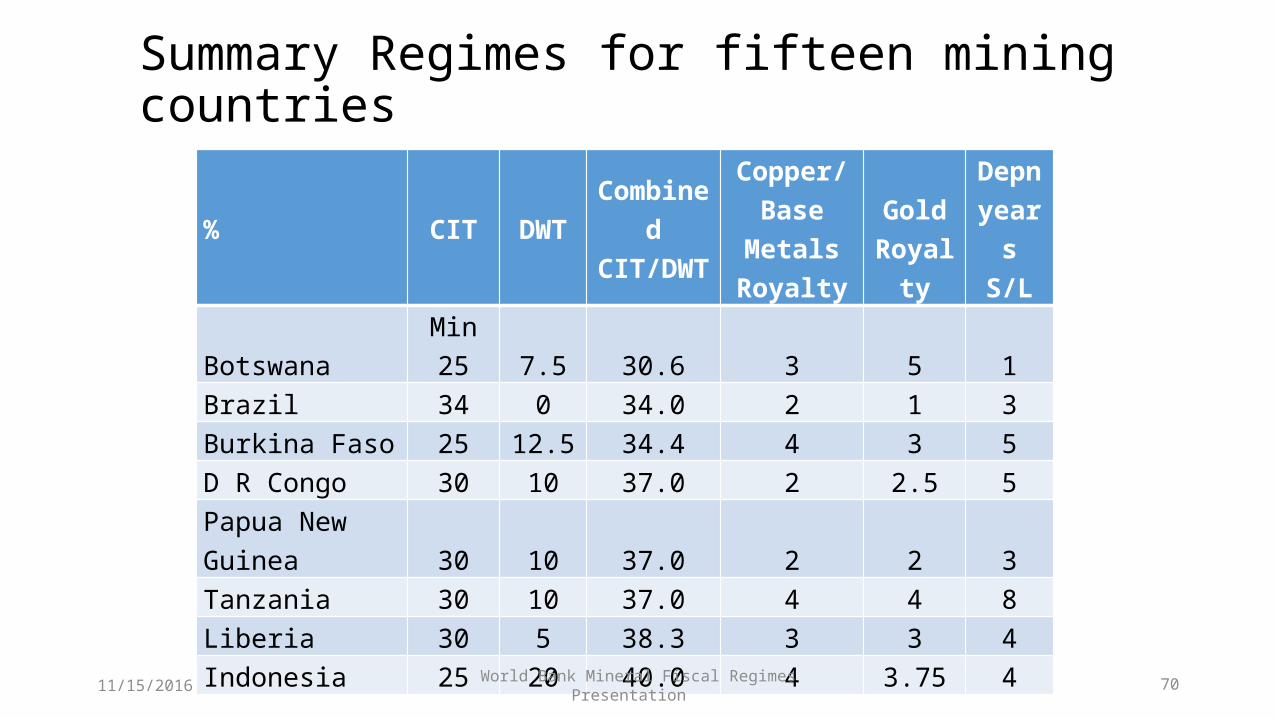

Botswana Min 25 7.5 30.6 3 5 1Brazil 34 0 34.0 2 1 3Burkina Faso 25 12.5 34.4 4 3 5D R Congo 30 10 37.0 2 2.5 5Papua New Guinea 30 10 37.0 2 2 3Tanzania 30 10 37.0 4 4 8Liberia 30 5 38.3 3 3 4Indonesia 25 20 40.0 4 3.75 4

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 71

Summary Regimes for fifteen mining countries

% CIT DWT CombinedCIT/DWT

Copper/Base Metals

RoyaltyGold

Royalty

DepnyearsS/L

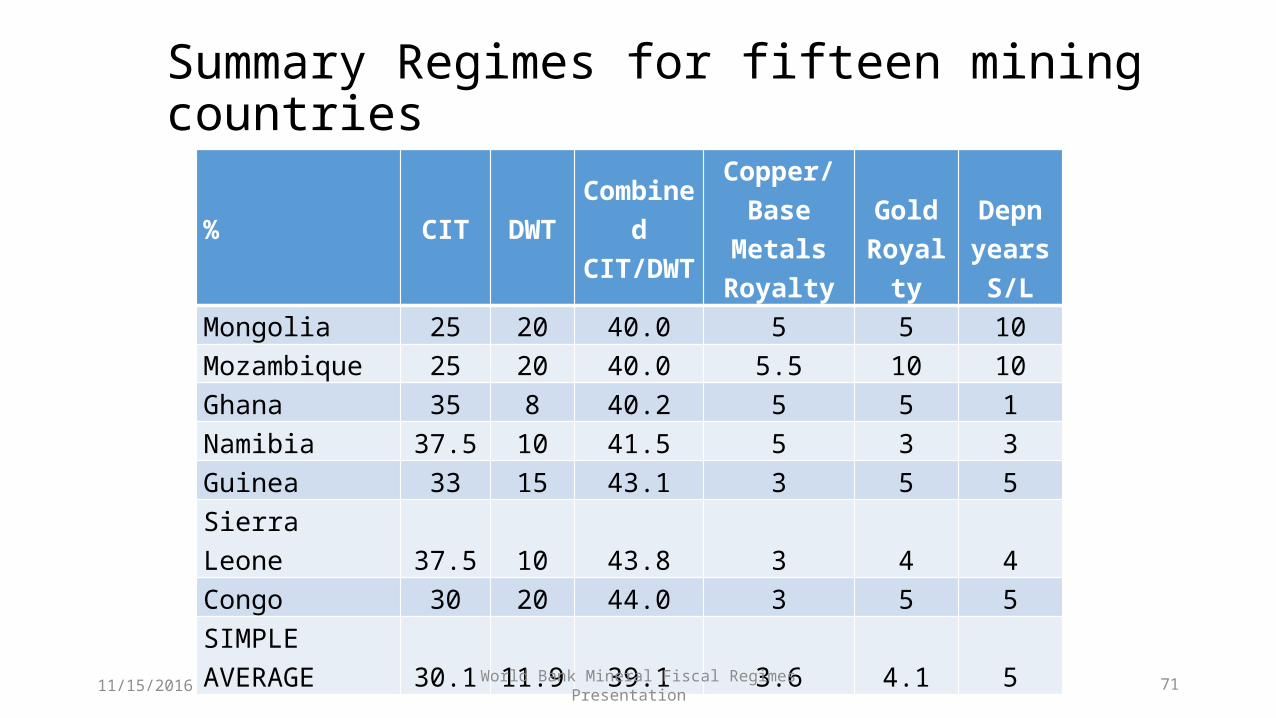

Mongolia 25 20 40.0 5 5 10Mozambique 25 20 40.0 5.5 10 10Ghana 35 8 40.2 5 5 1Namibia 37.5 10 41.5 5 3 3Guinea 33 15 43.1 3 5 5Sierra Leone 37.5 10 43.8 3 4 4Congo 30 20 44.0 3 5 5SIMPLE AVERAGE 30.1 11.9 39.1 3.6 4.1 5

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 72

Model Results – Base PriceAETR for Fifteen Countries (discounted, NPV basis)

BOTSWANA

BRAZIL

LIBERIA

DR CONGO

PAPUA NG

BURKINA FASO

TANZANIA

AVERAGE

INDONESIA

CONGO

GHANA

GUINEA

SIERRA LEONE

MONGOLIA

NAMIBIA

MOZAMBIQUE0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

AETR (tax take) for Fifteen Mining Countries

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 73

Some Sensitivities – Duties, DepreciationBase price representative regime• The next slide plots the three sets of AETR calculations – demonstrating that the

regimes are regressive i.e. as prices and profits rise, the AETR declines.

• The slide after presents the data for the highest, lowest and average AETR and associated fiscal regimes.

Reminder• All AETR references refer to discounted AETR (at 10%)• All references to values are in NPV real terms not nominal terms

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 74

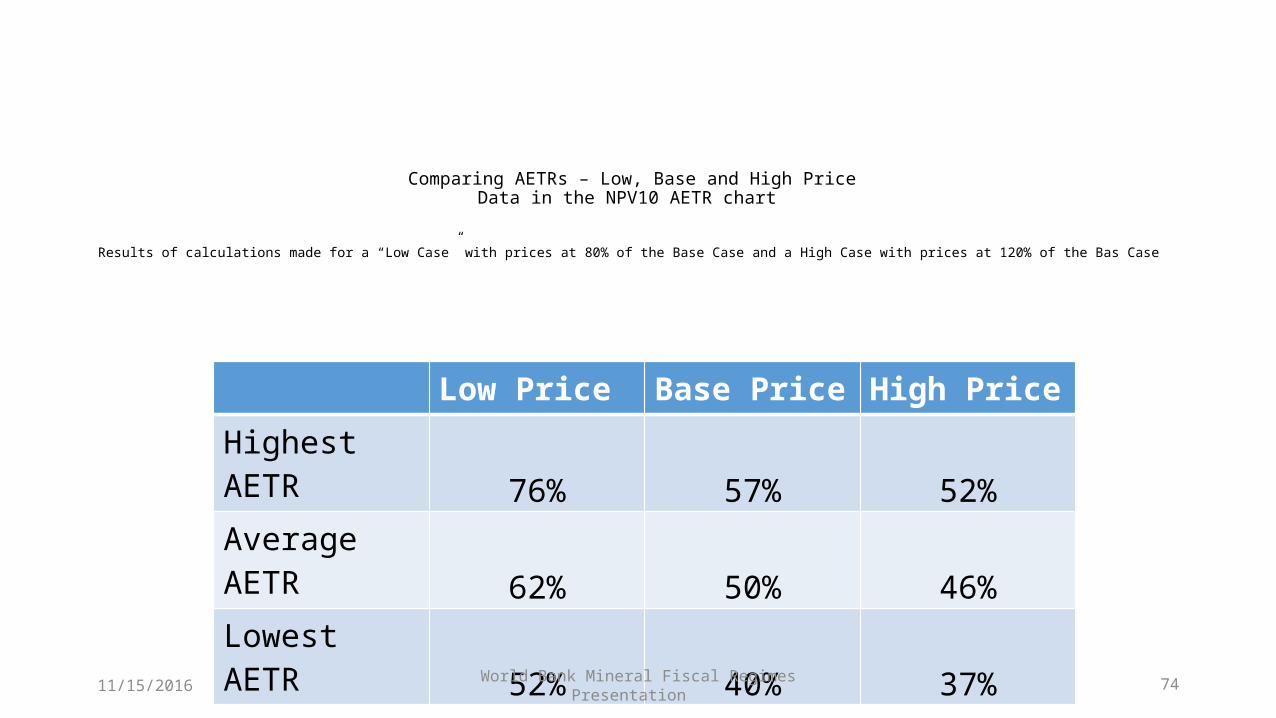

Comparing AETRs – Low, Base and High PriceData in the NPV10 AETR chart

Results of calculations made for a “Low Case” with prices at 80% of the Base Case and a High Case with prices at 120% of the Bas Case

Low Price Base Price High Price Highest AETR 76% 57% 52%Average AETR 62% 50% 46%Lowest AETR 52% 40% 37%

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 75

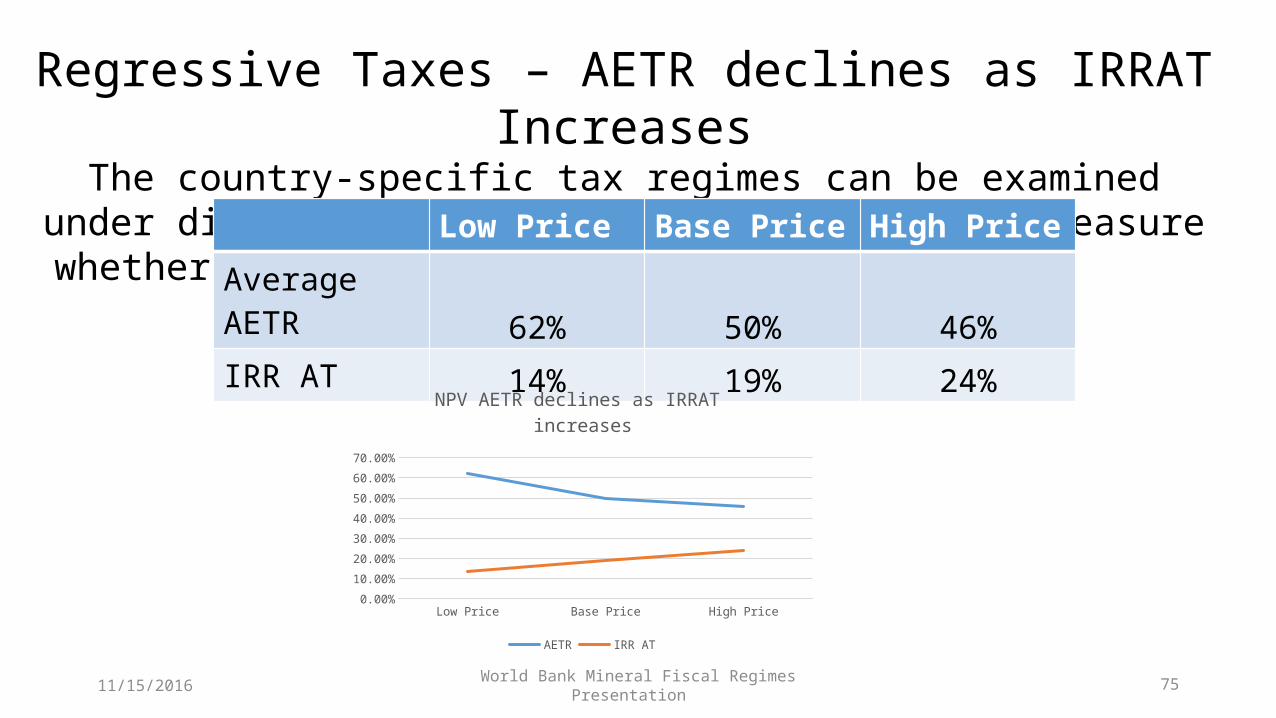

Regressive Taxes – AETR declines as IRRAT Increases

The country-specific tax regimes can be examined under different profitability assumptions to measure whether they

are progressive or regressive

11/15/2016

Low Price Base Price High Price Average AETR 62% 50% 46%IRR AT 14% 19% 24%

Low Price Base Price High Price0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

NPV AETR declines as IRRAT increases

AETR IRR AT

World Bank Mineral Fiscal Regimes Presentation 76

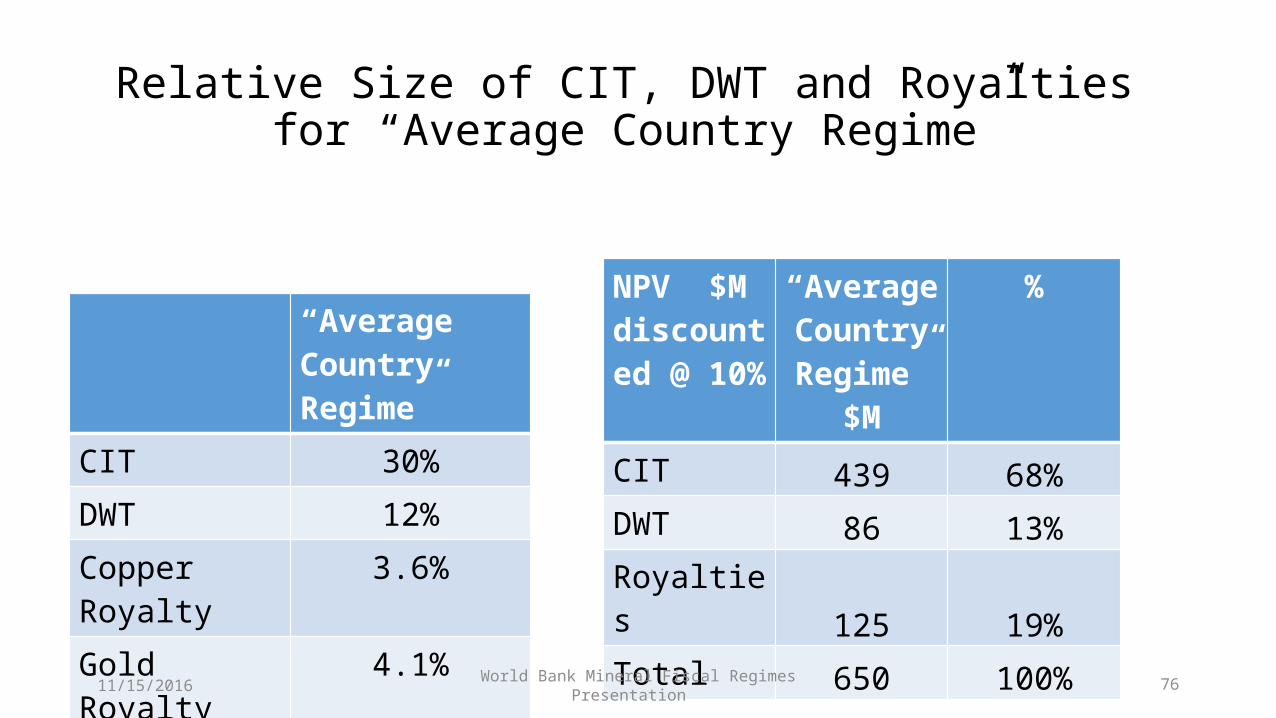

Relative Size of CIT, DWT and Royalties for “Average Country Regime”

NPV $M discounted @ 10%

“Average Country Regime”

$M

%

CIT 439 68%DWT 86 13%Royalties 125 19%Total 650 100%

“Average Country Regime”

CIT 30%DWT 12%Copper Royalty 3.6%Gold Royalty 4.1%

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 77

Relative Size of CIT, DWT and Royalties for “Average Country Regime”

Implications

• CIT revenues are much larger than royalties – so tax administration capacity is crucial to ensure taxes are correctly assessed and collected.

• Based on the 70% dividend payout rule, dividend withholding taxes are about two thirds of royalties – thus DTAs which exempt dividend withholding taxes may be quite costly in reducing the Total Tax Take for profitable mines that pay dividends.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 78

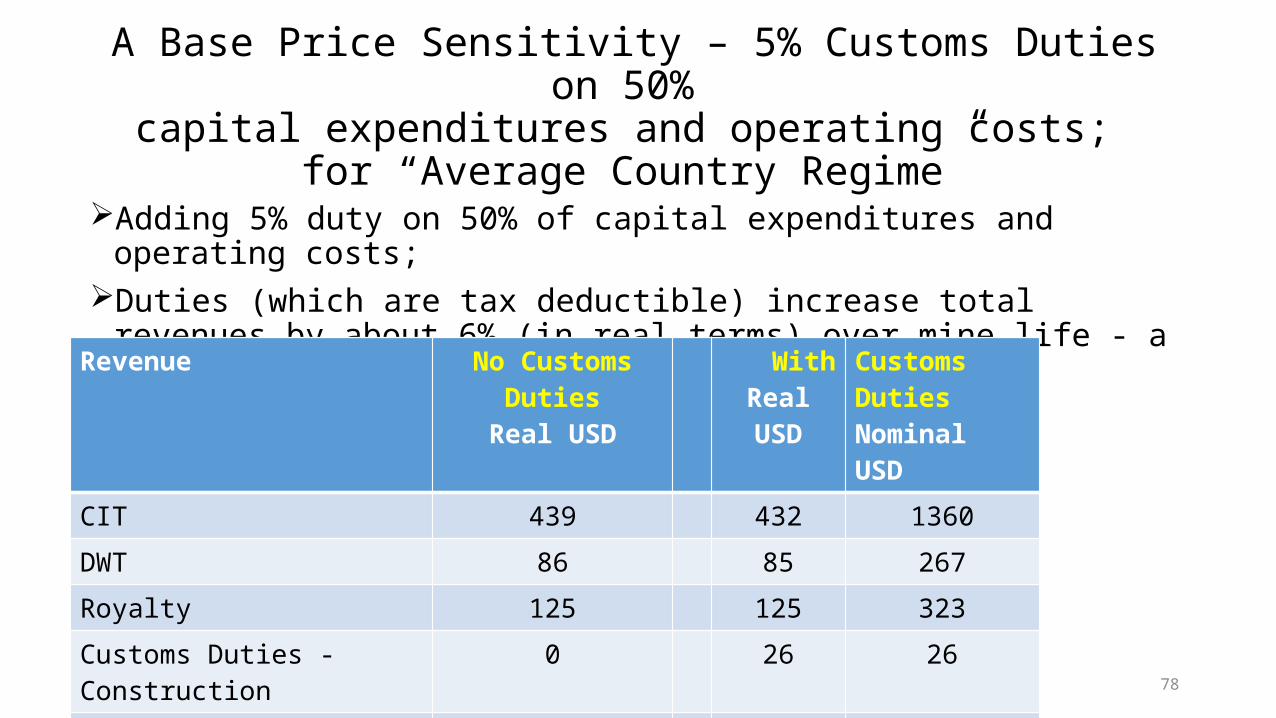

A Base Price Sensitivity – 5% Customs Duties on 50%

capital expenditures and operating costs; for “Average Country Regime”

Adding 5% duty on 50% of capital expenditures and operating costs; Duties (which are tax deductible) increase total revenues by about 6% (in real

terms) over mine life - a rather modest effect.

11/15/2016

Revenue No Customs DutiesReal USD

WithReal USD

Customs DutiesNominal USD

CIT 439 432 1360DWT 86 85 267Royalty 125 125 323Customs Duties - Construction 0 26 26Customs Duties - Operations 0 22 60Total 650 690 2036

World Bank Mineral Fiscal Regimes Presentation 79

Some Base Price Sensitivities – Duties, Depreciationfor “Average Country Regime”

• The next slide considers the possible impacts of companies to reduce profits and taxes through transfer pricing by

• Reducing price and sales revenues by 10%• Increasing capital expenditures by 10%• Increasing operating costs by 10%• The three above combined

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 80

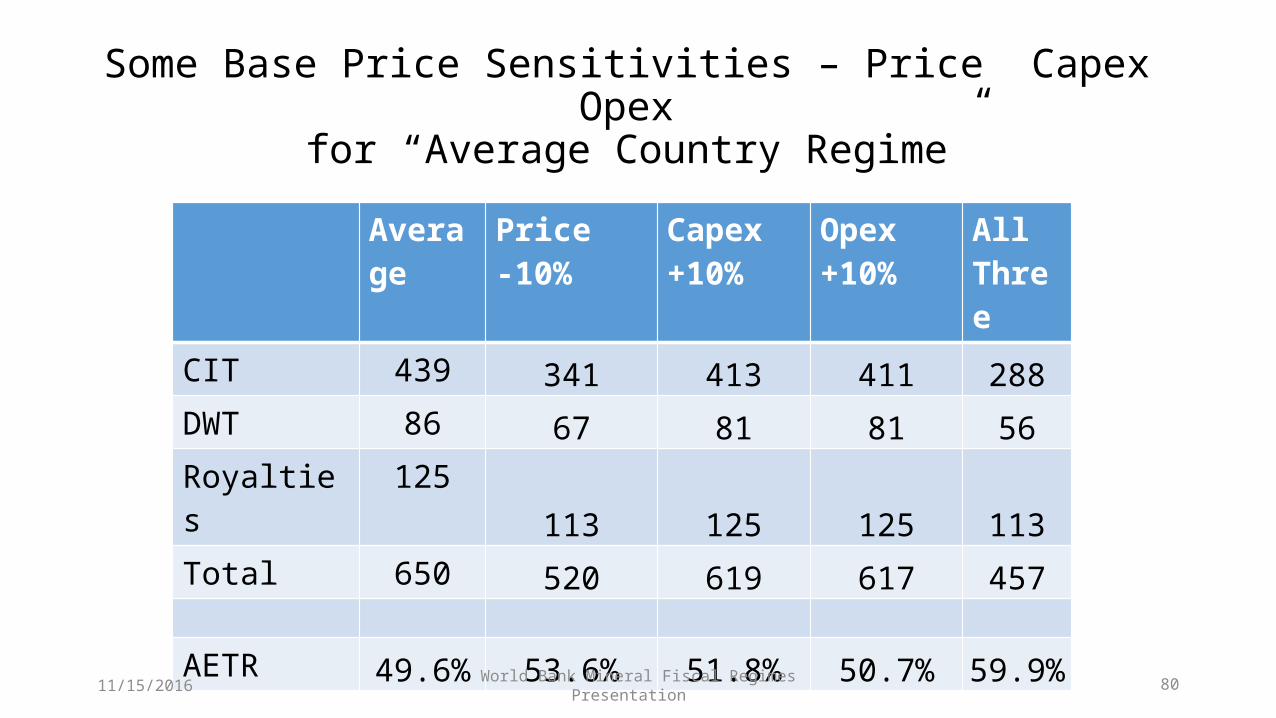

Some Base Price Sensitivities – Price Capex Opex for “Average Country Regime”

Average Price -10% Capex +10%

Opex +10%

All Three

CIT 439 341 413 411 288DWT 86 67 81 81 56Royalties 125 113 125 125 113Total 650 520 619 617 457

AETR 49.6% 53.6% 51.8% 50.7% 59.9%

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 81

Some Sensitivities – Duties, DepreciationBase Price Average RegimeThe impacts are substantial.

The largest impact is transfer pricing of products – government revenues decline by 20%.

Increasing construction costs and operating costs by 10% reduces revenues by about 5% each.

Combined together the three changes reduce government revenues by 30% (all in real (NPV) terms)

This underlines the importance of having the capabilities necessary to prevent transfer pricing abuses.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 82

How Does the Average Effective Tax Regime (AETR) compare to other

countries that are potentially competing for investment?

• A more aggressive fiscal regime with high tax and royalty rates will result in higher state revenues in the near term (about 5-20 years)

• Whereas a less aggressive fiscal regime that encourages investment will likely lead to greater investment and higher state revenues in the longer term (about 20 years and beyond).

• The competiveness of the fiscal regime can be benchmarked against other mining countries to see where the AETR fits compared within the range of AETRs for other countries.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 83

D. PROTECTING AGAINST TAX MINIMIZATION BEHAVIORS

Slides 83-92

IMPORTANT NOTE: Key Resources: • Fiscal Regimes for Extractive Industries: Design and Implementation, IMF Fiscal Affairs Dept, August 2012• How to Improve Mining Tax Administration andCollection Frameworks: A Sourcebook, Pietro Guj, Boubacar Bocoum, James Limerick, Murray Meaton, and Bryan Maybee World Bank 2013• Administering Fiscal Regimes for Extractive Industries: A HandbookJack Calder, IMF July 2014

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 84

How Companies can reduce tax liabilities in the host country - Transfer Pricing between “Related Parties”

Companies can use transactions between “related parties” to shift profits from a host country to another jurisdiction where taxes rates are lower. Related party transactions are typically between a parent company in another jurisdiction and the subsidiary mining company in the host county. But the transactions could also be with other subsidiaries of the parent company or even a third party company with which the parent company has “cut a deal”.

Transfer pricing can take place regarding Product sales between related parties Borrowing and lending between related parties The sale or purchase of goods and services between related parties Management fees between related parties Charges for intangibles such as the value of a license or intellectual property

between related parties .

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 85

OECD Guidelines/Legal Requirements• The OECD Guidelines on Transfer Pricing can help guide the preparation

of modern regulations and legislation.• Companies should be required by law to provide information annually

regarding both expected and actual related-party transactions above a certain level – say USD1 million.

• Transfer pricing abuses can be minimized by requiring in the law that companies demonstrate that prices (or interest rates/lending terms) are in line with arms length market prices or similar arms length transactions. If not the law should give the Revenue Authority the right to set such prices for tax assessment purposes

• Where arms length market prices are not readily available an Advanced Pricing Agreement (APA) can be used.

A combination of modern legislation and strong audit/enforcement capabilities is essential

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 86

How Companies can reduce tax liabilities in the host country - Hedging

• Hedging is used by companies to set prices for future transactions, generally as a risk reduction measure.

• Hedging can then generate profits or losses compared with actual prices on the date the transaction takes effect.

• There is a risk that hedging between related parties may be used to reduce profits and move them to a related party in another jurisdiction.

• Some hedging arrangements can become very complex arrangements involving different foreign parties

• Some governments require companies to prepare their income tax statements with market prices (hedging is excluded)

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 87

How Companies can reduce tax liabilities in the host country – Goods and Services

Mining, Processing, Transportation, Marketing and Other Costs Transfer pricing can also take place in terms of the purchase or sale of goods and services between related parties. For example, a parent company can supply goods such as explosives or services such as marketing services at above arms length market prices. In this case profit is transferred because• the mining company’s costs are increased and profits reduced • the parent company’s revenues and profits are both increasedThe mining company can also sell goods or provide services to the parent company at below arms length market costs. As with product pricing, if the company cannot demonstrate that transactions are priced at market prices, the law should give the Revenue Authority the right to set prices such for transactions for tax assessment purposes.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 88

How Companies can reduce tax liabilities in the host country - Fees and Management Services

Fees: Parent companies can also charge overhead fees, management fees or even intellectual property fees – all of which will increase the costs and reduce the profits and profit taxes paid by the mining company.Management Services Parent companies can provide goods and services such as management or exploration services during the exploration or development stage of a mining operation at highly inflated prices which

• increases profits for the parent company and • increases the value of the assets to be depreciated by the mining company which

results in lower profits and lower taxes in the host country. As with earlier examples, if market prices cannot be demonstrated, then the law should give the Revenue Authority the right to set prices such for transactions for tax assessment purposes

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 89

How Companies can reduce tax liabilities in the host country - Finance charges/Thin Capitalization

Parent companies can increase financing costs for subsidiaries by • charging an above market interest rate on loans • financing the subsidiary with as much as 100% debt• taking only interest payments and leaving all of the debt in place for many years.

• The later two actions above result in “thin capitalization” and would not be possible with a third party lender

• Correspondingly, the mining company could make loans to the parent company at below market rates.

• The law can restrict the level of borrowing that is eligible for tax action purpose – setting a limit of say 60/40 debt-equity ratio.

• As with earlier examples, if market terms cannot be demonstrated, then the law should give the Revenue Authority the right to set terms for tax assessment purposes

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 90

Some Other Useful Points -Separating Expenses from Capital Expenditures; Ring Fencing; Construction Audits

Point from IMF PaperFiscal Regimes for Extractive Industries: Design and Implementation

Comment

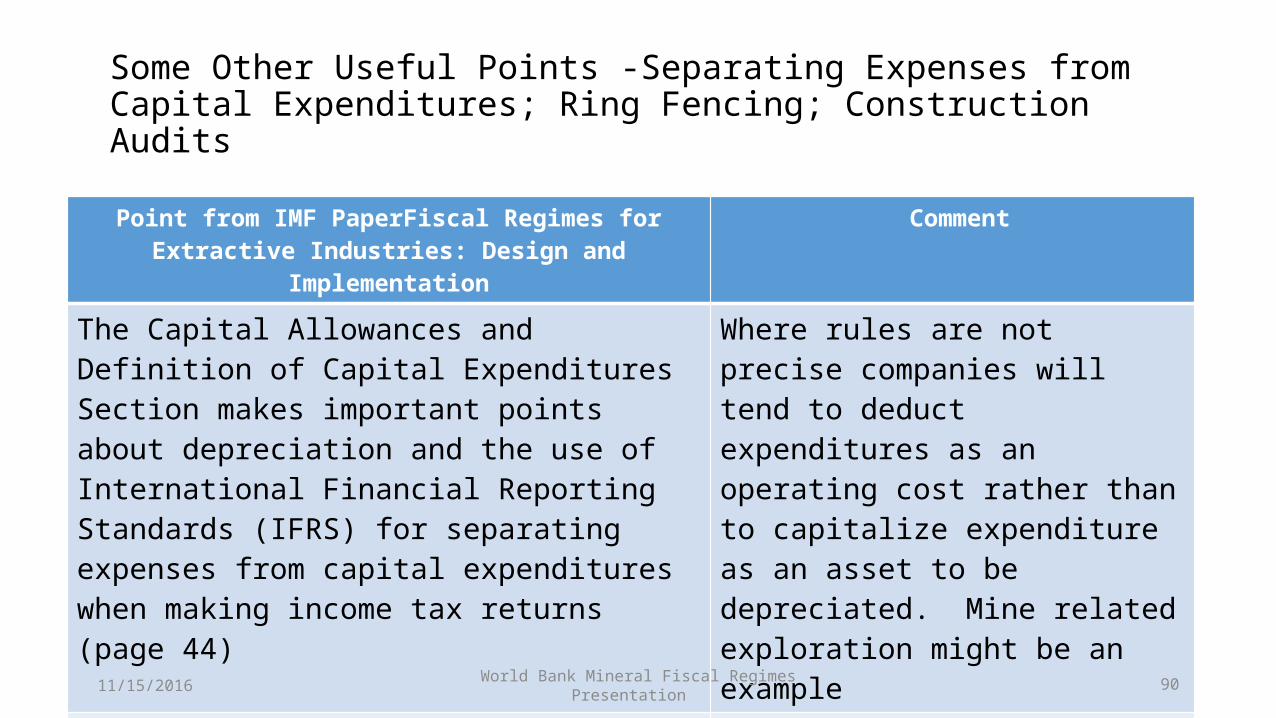

The Capital Allowances and Definition of Capital Expenditures Section makes important points about depreciation and the use of International Financial Reporting Standards (IFRS) for separating expenses from capital expenditures when making income tax returns (page 44)

Where rules are not precise companies will tend to deduct expenditures as an operating cost rather than to capitalize expenditure as an asset to be depreciated. Mine related exploration might be an example

Neglect in auditing exploration and development expenses (that occur before production starts) can reduce the tax base significantly as a project starts to generate income” (page 67)

For large projects, cost audits by the Tax Authority are essential during the construction stage

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 91

Legislation and Contracts; Transfer of an Interest; Double Taxation

AgreementsIssue Comment

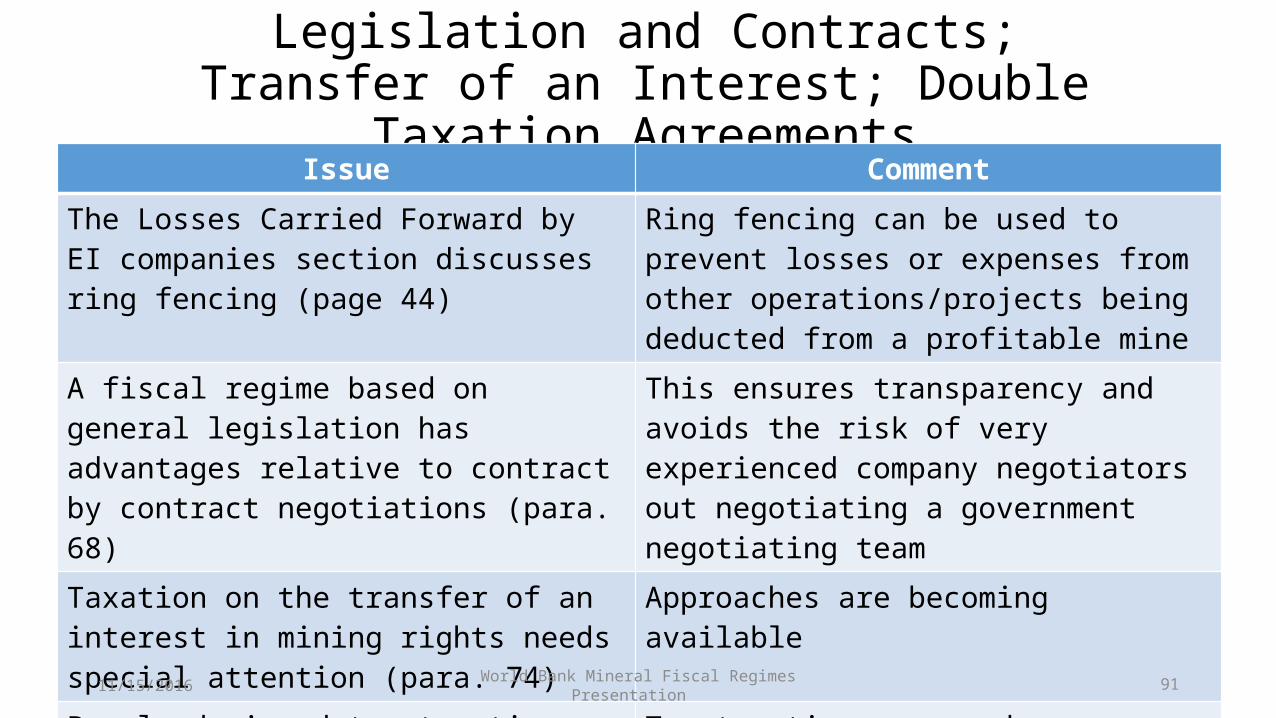

The Losses Carried Forward by EI companies section discusses ring fencing (page 44)

Ring fencing can be used to prevent losses or expenses from other operations/projects being deducted from a profitable mine

A fiscal regime based on general legislation has advantages relative to contract by contract negotiations (para. 68)

This ensures transparency and avoids the risk of very experienced company negotiators out negotiating a government negotiating team

Taxation on the transfer of an interest in mining rights needs special attention (para. 74)

Approaches are becoming available

Poorly designed tax treaties (Double Taxation Agreements – DTAs) can reduce the tax basis of EI projects (para. 75)

Tax treaties may need renegotiation to reduce potential revenue losses. Legislation can protect against “treaty shopping” by investors to reduce/minimize taxes.

11/15/2016

World Bank Mineral Fiscal Regimes Presentation 92

Thank you

11/15/2016