Embed Size (px)

Citation preview

North American Steel IndustryNAFTA Region Update

OECD Steel Committee/WorldSteel AssociationRaw Materials Workshop

December 15-16, 2008 Kuala Lumpur, Malaysia

*American Iron and Steel Institute (AISI)Steel Manufacturers Association (SMA)

Specialty Steel Industry of North America (SSINA)Canadian Steel Producers Association (CSPA)

Mexican Steel Producers Association (CANACERO)

2

Presentation Summary

1. NAFTA Steel Market ConditionsA. Significant Decline in Steel and Major End-Use MarketsB. Growing Trade Concerns

2. North America is a Major Producer, Consumer and Trader of Raw Materials

3. Key Concerns About Raw Materials: Trade and Investment Barriers

4. Key Policy Conclusions

3

1. NAFTA Steel Market Conditions – Part A:Significant Decline in Steel and Major End-Use Markets

4

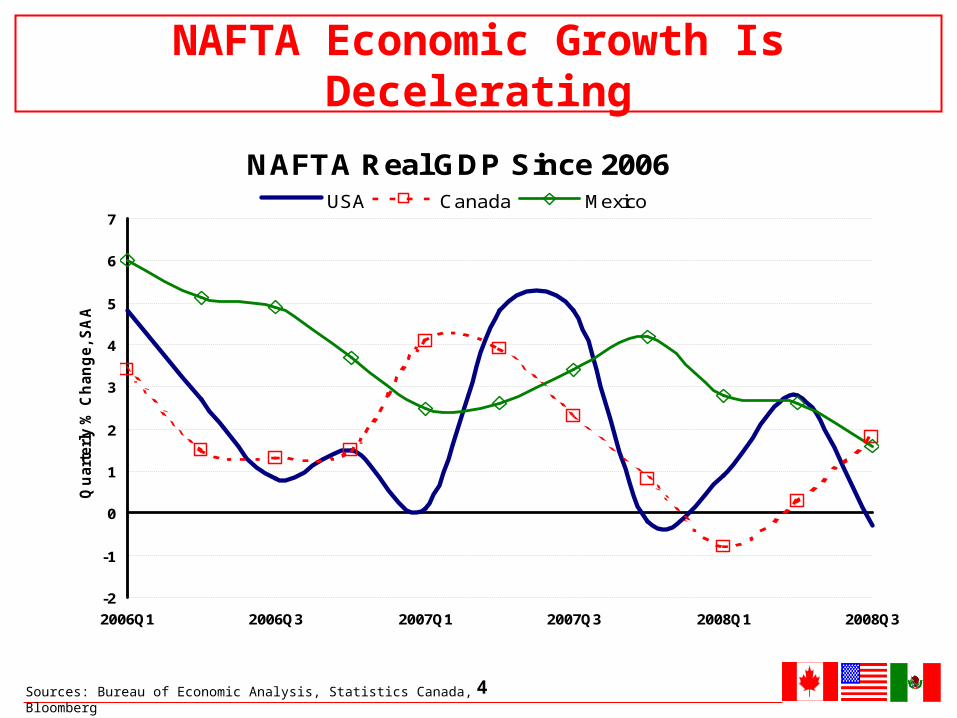

NAFTA Economic Growth Is Decelerating

NAFTA Real GDP Since 2006

-2

-1

0

1

2

3

4

5

6

7

2006Q1 2006Q3 2007Q1 2007Q3 2008Q1 2008Q3

Qu

art

erl

y %

Ch

an

ge, S

AA

R

USA Canada Mexico

Sources: Bureau of Economic Analysis, Statistics Canada, Bloomberg

5

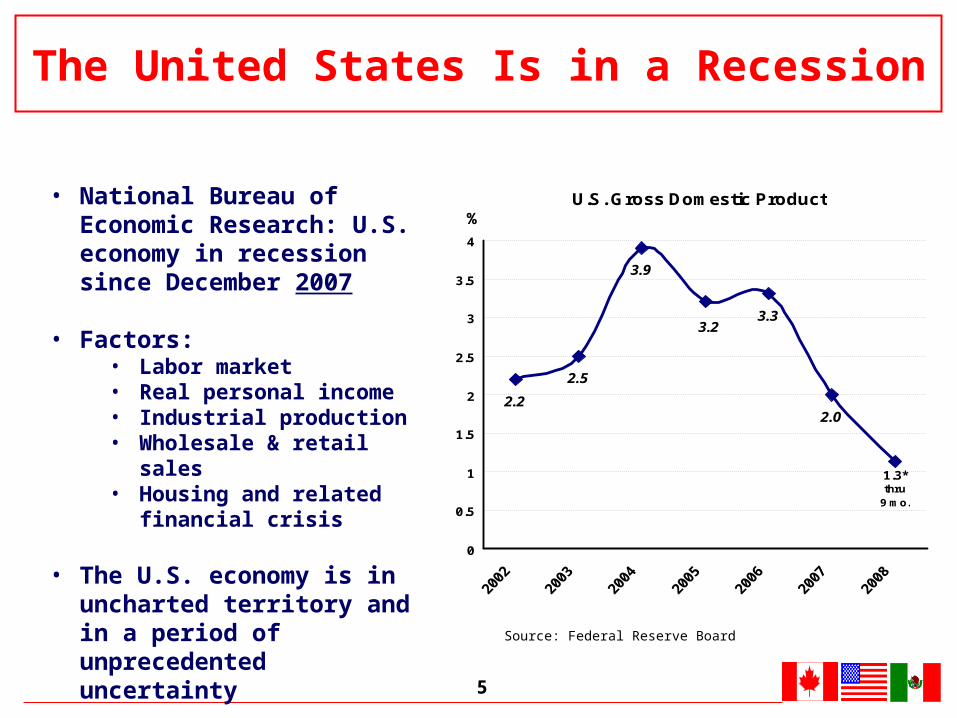

U.S. Gross Domestic Product

2.2

2.5

3.9

3.3

1.3*thru

9 mo.

3.2

2.0

0

0.5

1

1.5

2

2.5

3

3.5

4

%

Source: Federal Reserve Board

The United States Is in a Recession

• National Bureau of Economic Research: U.S. economy in recession since December 2007

• Factors:• Labor market• Real personal income• Industrial production• Wholesale & retail sales• Housing and related financial

crisis

• The U.S. economy is in uncharted territory and in a period of unprecedented uncertainty

6

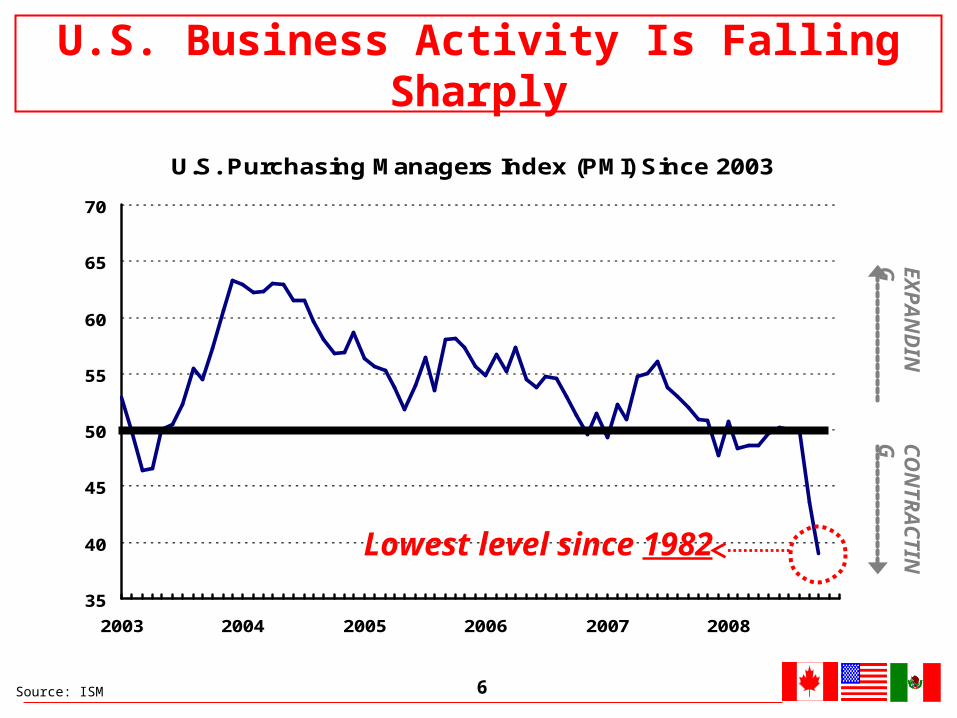

U.S. Purchasing Managers Index (PMI) Since 2003

35

40

45

50

55

60

65

70

2003 2004 2005 2006 2007 2008

EX

PA

ND

ING

CO

NT

RA

CT

ING

Lowest level since 1982

Source: ISM

U.S. Business Activity Is Falling Sharply

7

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2001 2002 2003 2004 2005 2006 2007 2008

Permits Starts Completions

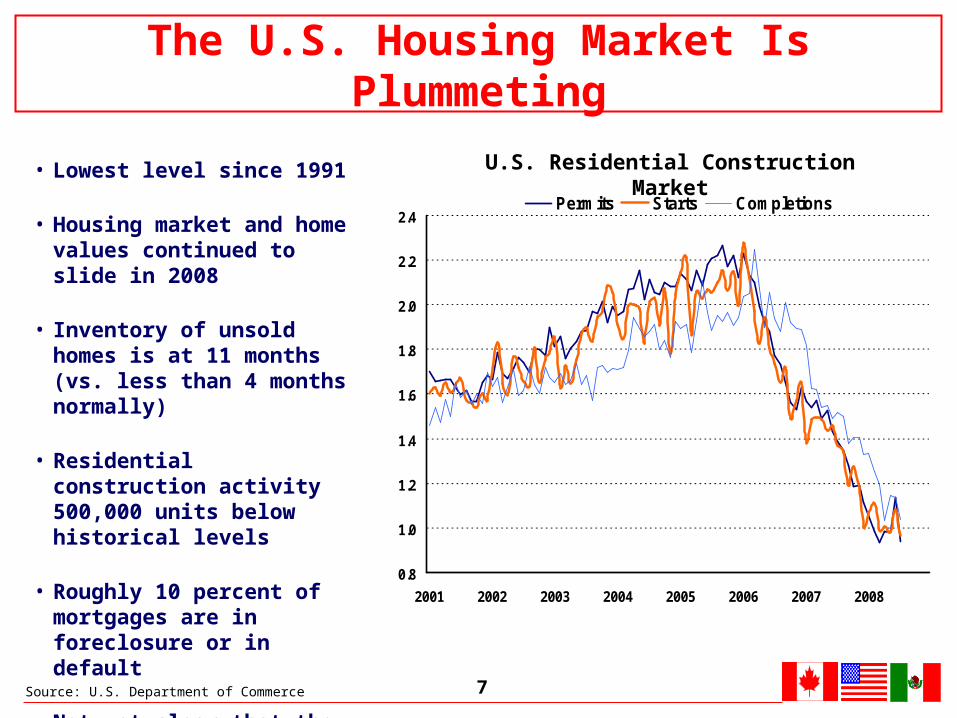

• Lowest level since 1991

• Housing market and home values continued to slide in 2008

• Inventory of unsold homes is at 11 months (vs. less than 4 months normally)

• Residential construction activity 500,000 units below historical levels

• Roughly 10 percent of mortgages are in foreclosure or in default

• Not yet clear that the housing market has hit bottom

U.S. Residential Construction Market

The U.S. Housing Market Is Plummeting

Source: U.S. Department of Commerce

8

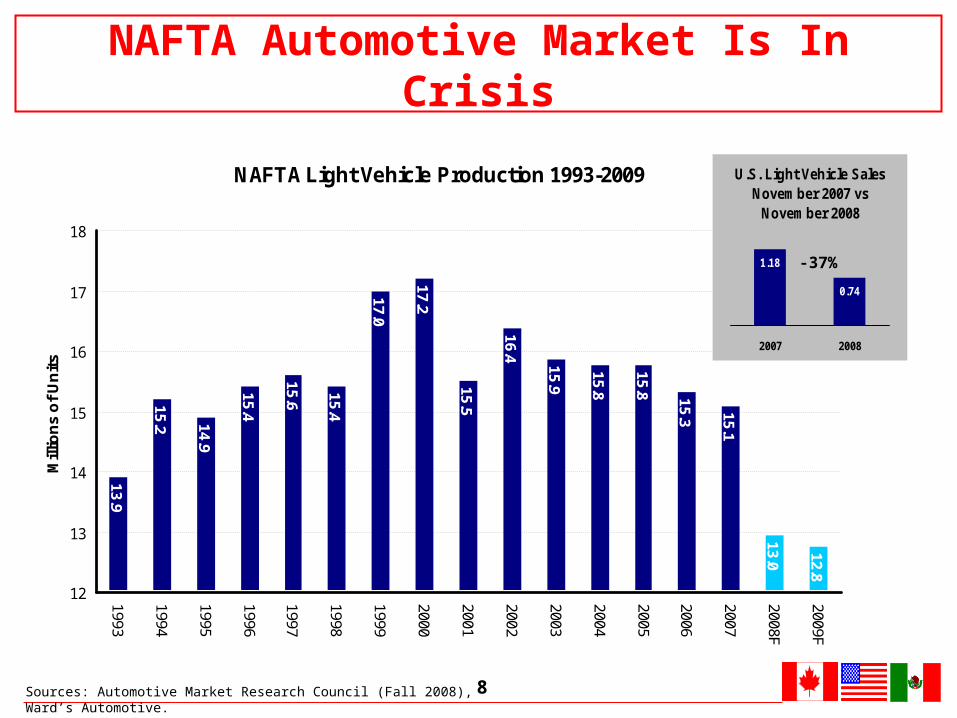

NAFTA Automotive Market Is In Crisis

NAFTA Light Vehicle Production 1993-2009

13.9

15.2 14.9

15.4

15.6

15.4

17.0

17.2

15.5

16.4

15.9

15.8

15.8 15.3 15.1

13.0

12.8

12

13

14

15

16

17

18

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008F

2009F

Mill

ion

s o

f U

nit

s

U.S. Light Vehicle Sales November 2007 vs

November 2008

1.18

0.74

2007 2008

-37%

Sources: Automotive Market Research Council (Fall 2008), Ward’s Automotive.

9

7,000

8,000

9,000

10,000

11,000

12,000

13,000

2008 Weekly

Do

w J

on

es

Va

lue

500

700

900

1,100

1,300

1,500

1,700

1,900

2,100

2,300

2,500

Dow Jones Daily Closing Value U.S. Weekly Raw Steel Production

Prod

uction (000 M

etric Tons)

Source: Dow Jones Industrial Index, AISI

U.S. Steel Production Has Declined Dramatically, Following Both Wall Street And The Real Economy

10

• 3Q08 indicators suggest growing economic challenges in the months ahead

• 3Q08 real GDP growth of +1.3%, but:• September GDP growth only +0.1%• Business inventories up +12%, masking other concerns• Final domestic demand only +0.6%, worst quarter since 1995• Consumer spending slowed to +0.7%, lowest level since 2001• Exports down -5.4%, fifth straight quarterly decline• Real disposable income grew only +0.1%

Source: CIBC World Markets, December 1st, 2008.

Canada: Economic Conditions Are Deteriorating

11

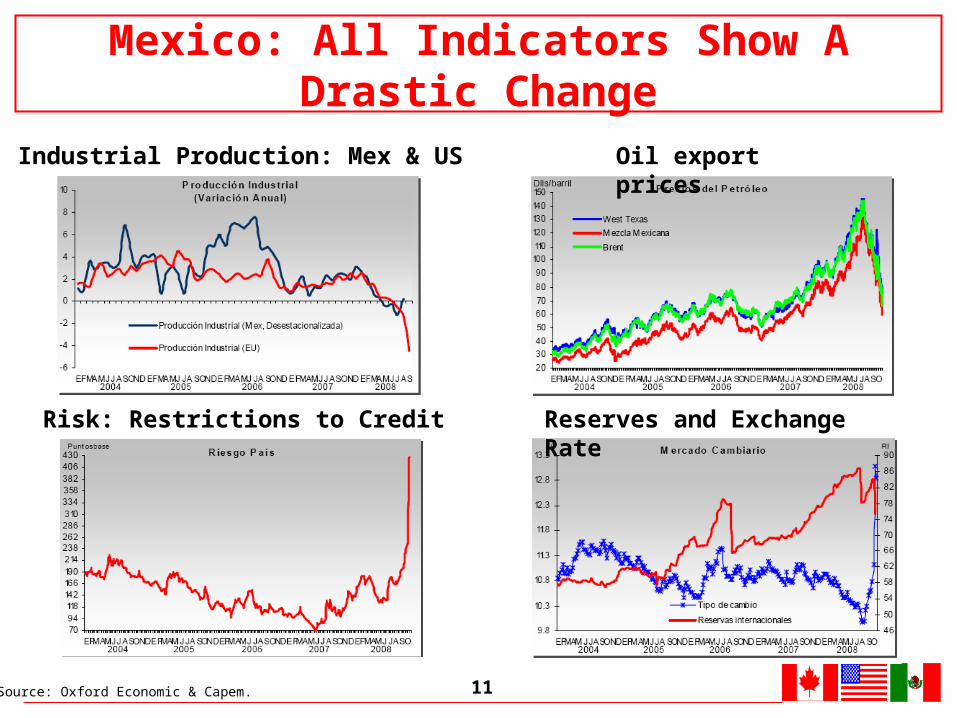

Risk: Restrictions to Credit

Industrial Production: Mex & US Oil export prices

Reserves and Exchange Rate

Source: Oxford Economic & Capem.

Mexico: All Indicators Show A Drastic Change

12

1. NAFTA Steel Market Conditions – Part B:Growing Trade Concerns

13

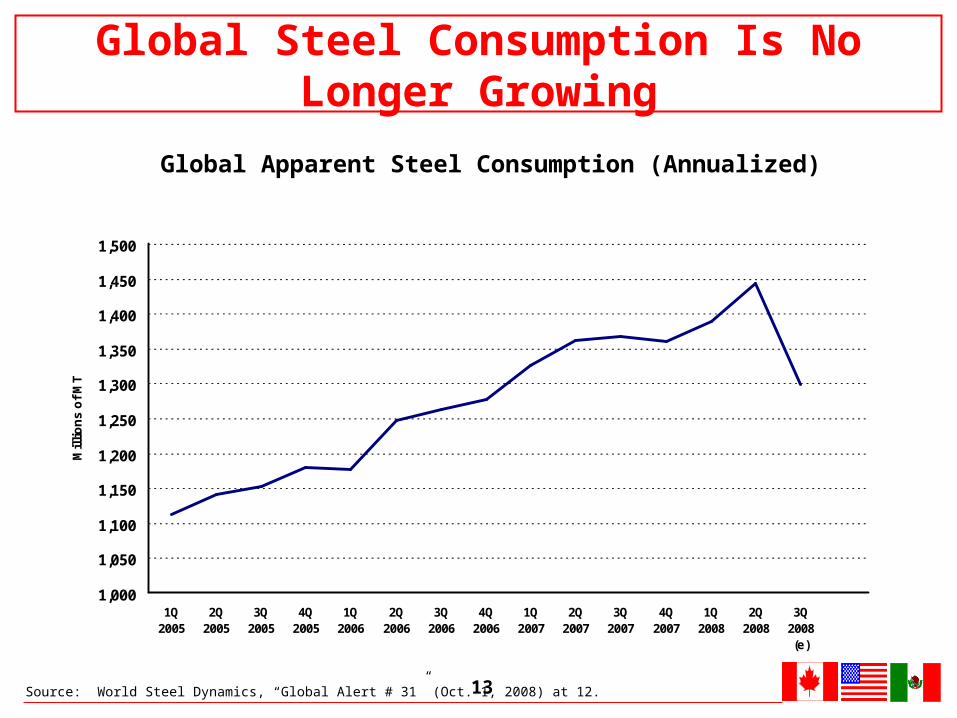

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

1,400

1,450

1,500

1Q2005

2Q2005

3Q2005

4Q2005

1Q2006

2Q2006

3Q2006

4Q2006

1Q2007

2Q2007

3Q2007

4Q2007

1Q2008

2Q2008

3Q2008(e)

Mil

lio

ns

of

MT

Global Apparent Steel Consumption (Annualized)

Source: World Steel Dynamics, “Global Alert # 31” (Oct. 1, 2008) at 12.

Global Steel Consumption Is No Longer Growing

14

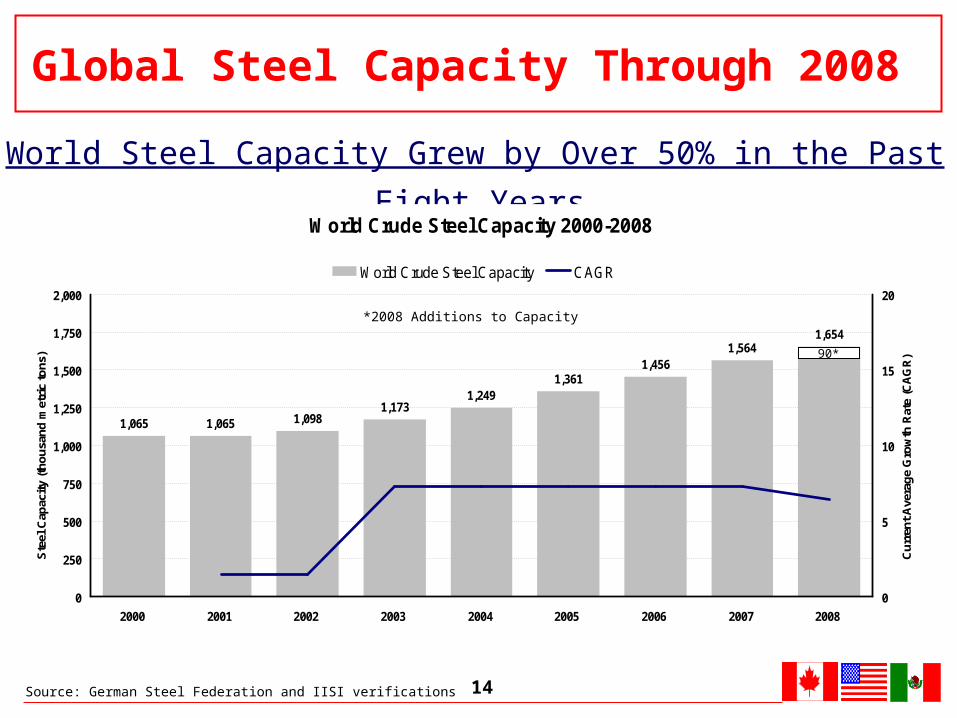

World Steel Capacity Grew by Over 50% in the Past Eight Years

Source: German Steel Federation and IISI verifications

Global Steel Capacity Through 2008

World Crude Steel Capacity 2000-2008

1,065 1,065 1,0981,173

1,2491,361

1,4561,564

1,654

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2000 2001 2002 2003 2004 2005 2006 2007 2008

Ste

el C

apac

ity

(th

ou

san

d m

etri

c to

ns)

0

5

10

15

20

Cu

rren

t A

vera

ge

Gro

wth

Rat

e (C

AG

R)

World Crude Steel Capacity CAGR

90*

*2008 Additions to Capacity

15

NAFTA Steel: Positioned To Compete

• During the crisis of 1998-2003, the NAFTA steel industry strengthened from within through extensive consolidation, restructuring and capital investment

• The new business model that emerged is one that enables us to compete effectively with fairly traded steel in the global marketplace

• When conditions do start to improve, and with pro-competitive policies (e.g., on climate change), the North American steel industry is positioned to participate in the recovery

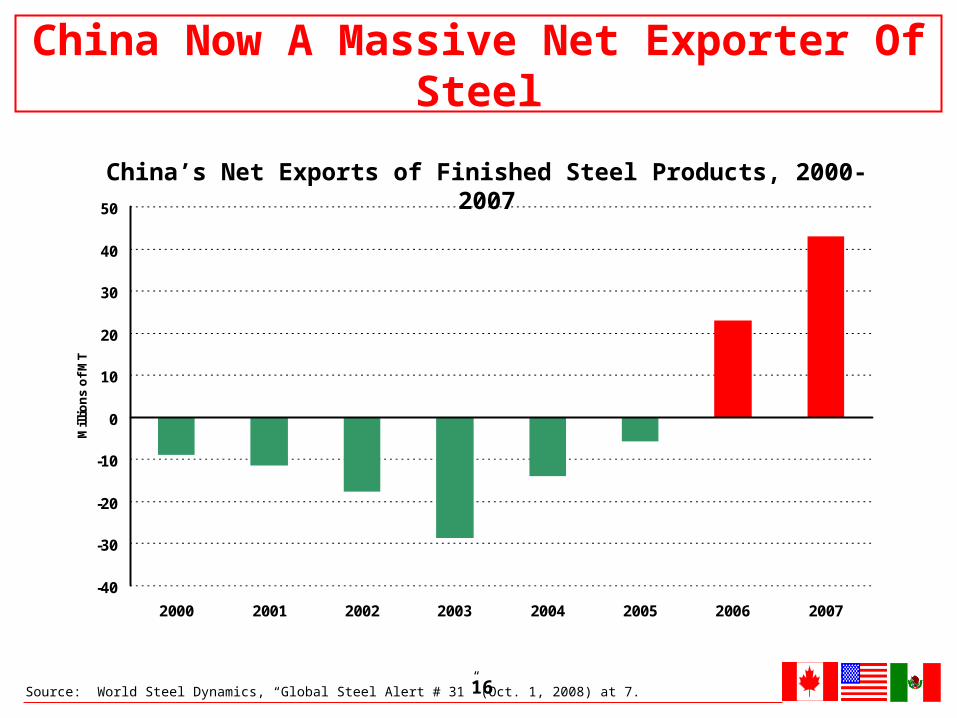

16Source: World Steel Dynamics, “Global Steel Alert # 31” (Oct. 1, 2008) at 7.

-40

-30

-20

-10

0

10

20

30

40

50

2000 2001 2002 2003 2004 2005 2006 2007

Mil

lio

ns

of

MT

China’s Net Exports of Finished Steel Products, 2000-2007

China Now A Massive Net Exporter Of Steel

17

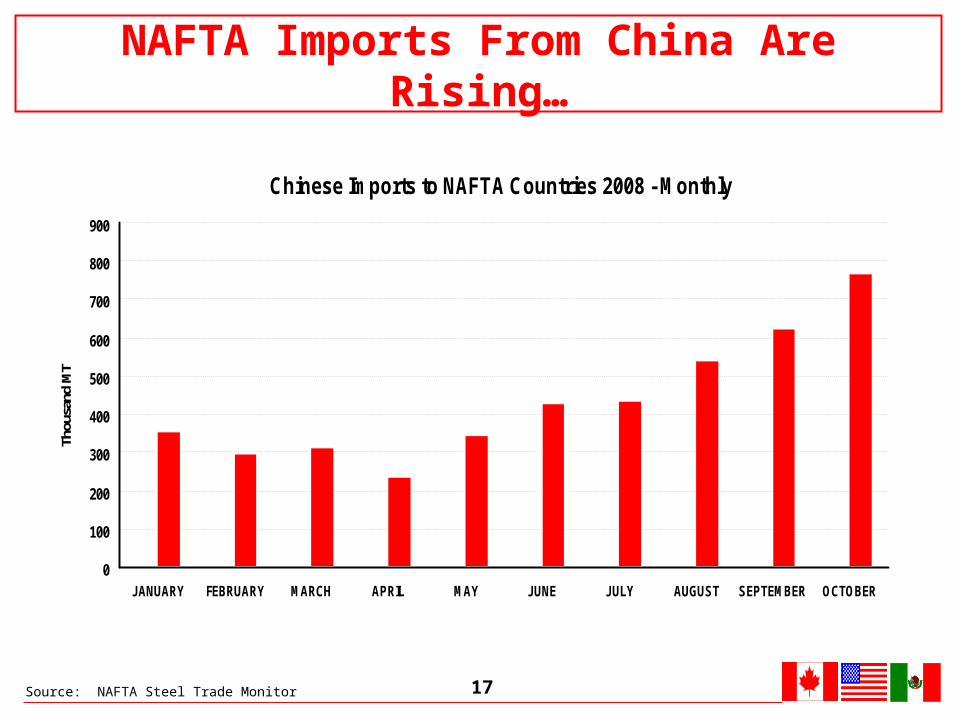

Chinese Imports to NAFTA Countries 2008 - Monthly

0

100

200

300

400

500

600

700

800

900

JANUARY FEBRUARY MARCH APRIL MAY JUNE JULY AUGUST SEPTEMBER OCTOBER

Thou

sand

MT

NAFTA Imports From China Are Rising…

Source: NAFTA Steel Trade Monitor

18

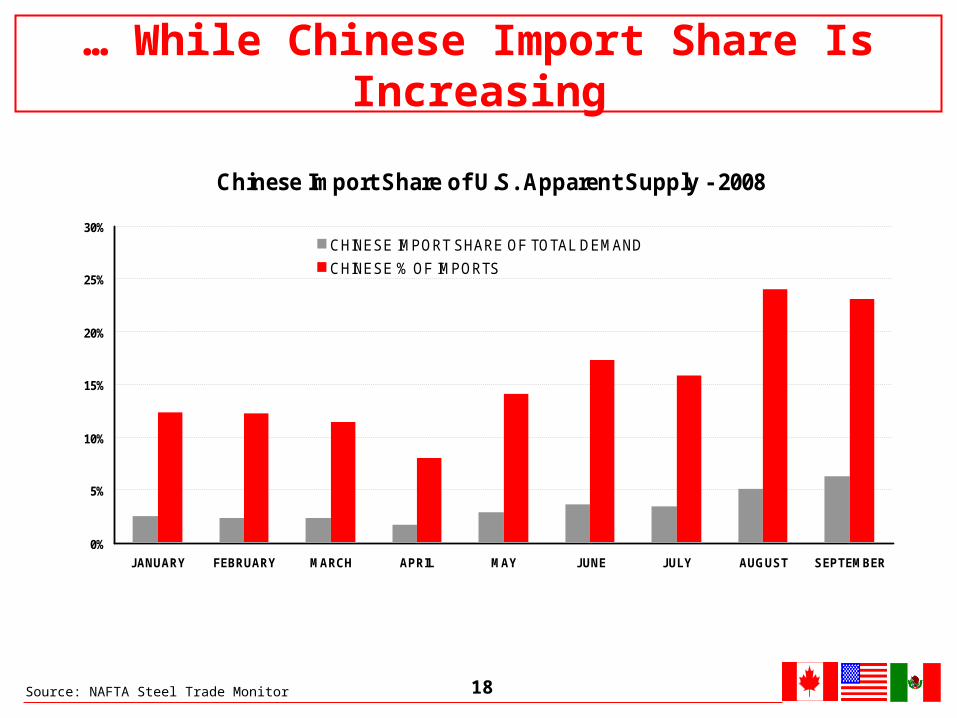

Chinese Import Share of U.S. Apparent Supply - 2008

0%

5%

10%

15%

20%

25%

30%

JANUARY FEBRUARY MARCH APRIL MAY JUNE JULY AUGUST SEPTEMBER

CHINESE IMPORT SHARE OF TOTAL DEMAND

CHINESE % OF IMPORTS

… While Chinese Import Share Is Increasing

Source: NAFTA Steel Trade Monitor

19

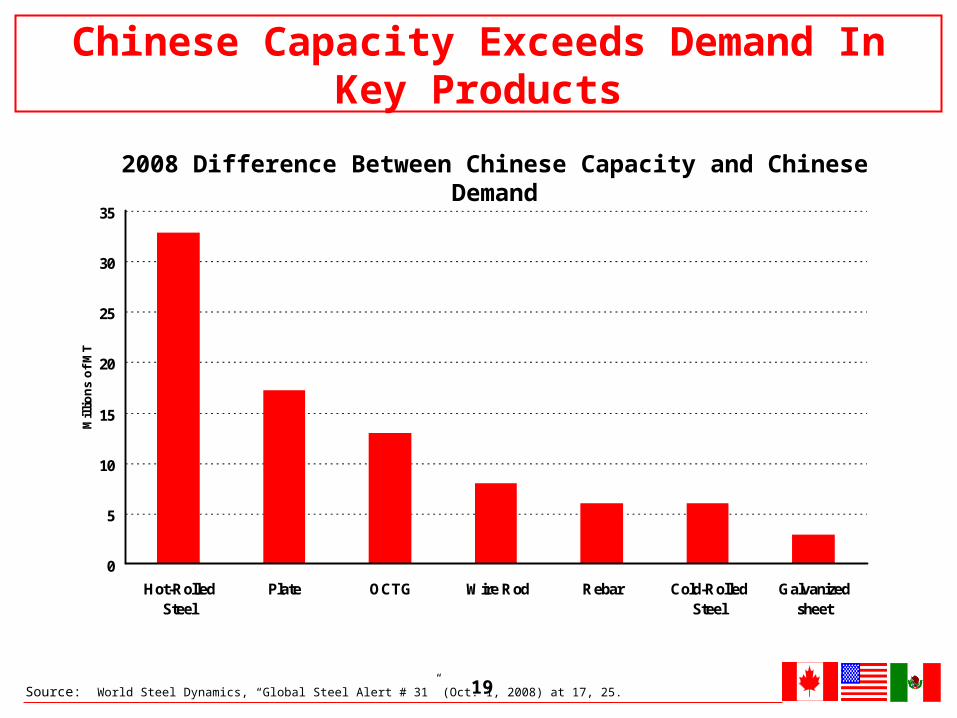

0

5

10

15

20

25

30

35

Hot-RolledSteel

Plate OCTG Wire Rod Rebar Cold-RolledSteel

Galvanizedsheet

Mil

lio

ns

of

MT

2008 Difference Between Chinese Capacity and Chinese Demand

Source: World Steel Dynamics, “Global Steel Alert # 31” (Oct. 1, 2008) at 17, 25.

Chinese Capacity Exceeds Demand In Key Products

20

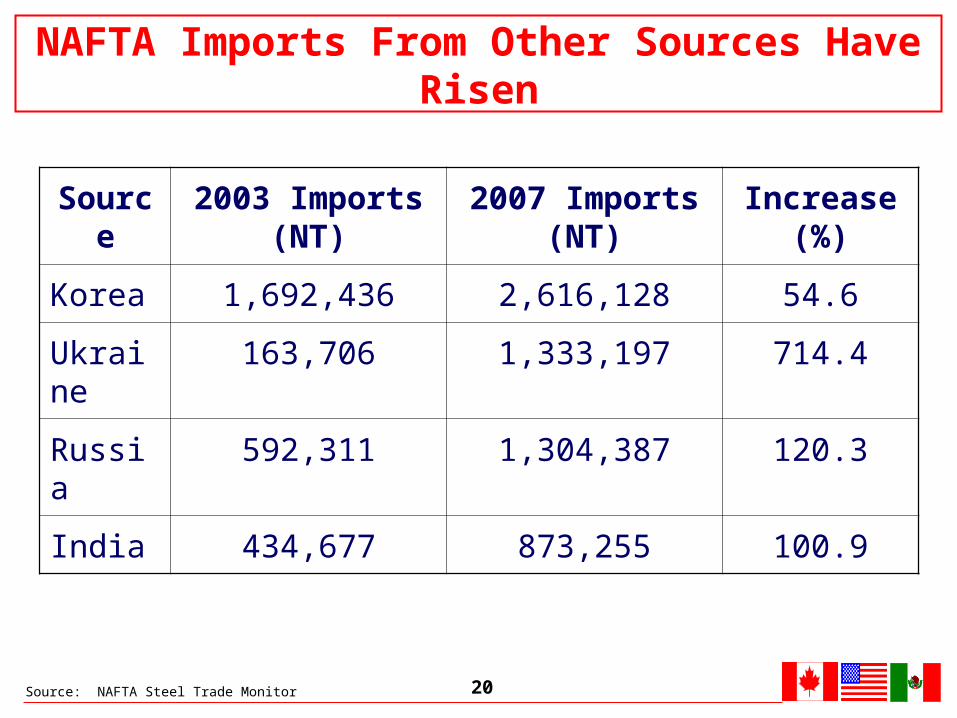

Source 2003 Imports (NT) 2007 Imports (NT) Increase (%)

Korea 1,692,436 2,616,128 54.6

Ukraine 163,706 1,333,197 714.4

Russia 592,311 1,304,387 120.3

India 434,677 873,255 100.9

Source: NAFTA Steel Trade Monitor

NAFTA Imports From Other Sources Have Risen

21Source: AISI Indirect Steel Trade Report, Global Trade Atlas

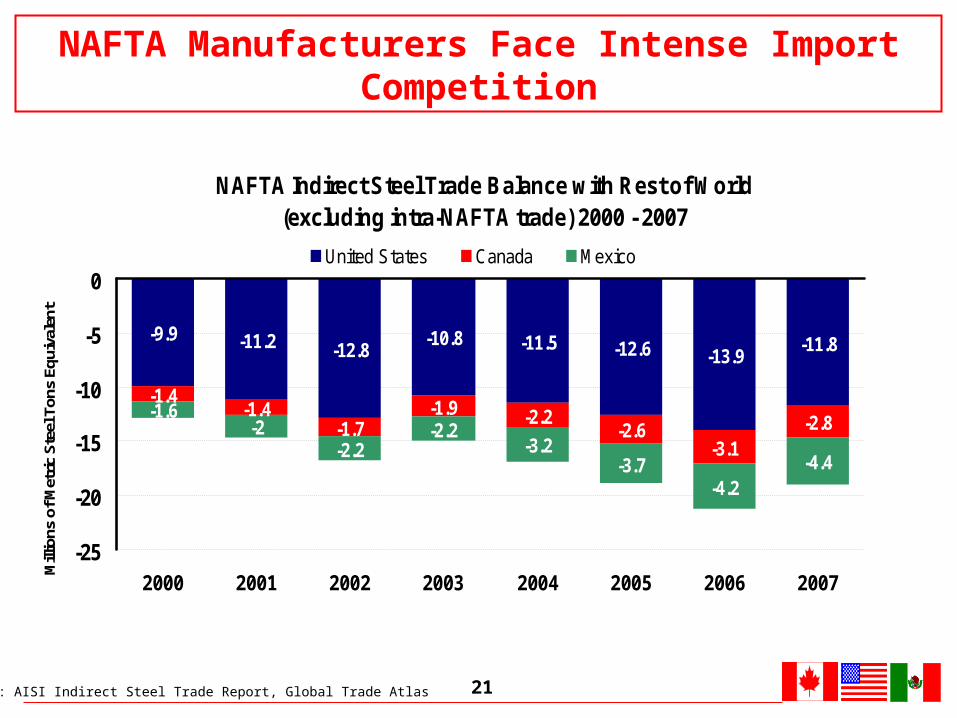

NAFTA Manufacturers Face Intense Import Competition

NAFTA Indirect Steel Trade Balance with Rest of World(excluding intra-NAFTA trade) 2000 - 2007

-9.9 -11.2 -12.8-10.8 -11.5 -12.6 -13.9

-11.8

-1.4-1.4

-1.7-1.9 -2.2

-2.6-3.1

-2.8-1.6

-2-2.2

-2.2-3.2

-3.7-4.2

-4.4

-25

-20

-15

-10

-5

0

2000 2001 2002 2003 2004 2005 2006 2007Mill

ions

of M

etric

Ste

el T

ons

Equi

vale

nt

United States Canada Mexico

22

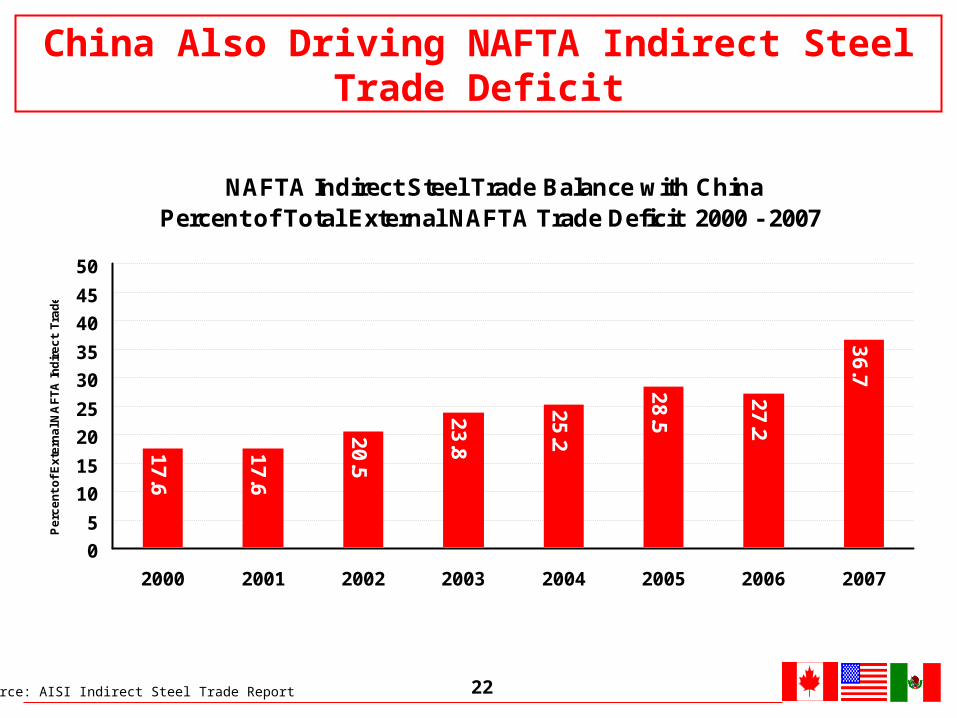

NAFTA Indirect Steel Trade Balance with China Percent of Total External NAFTA Trade Deficit 2000 - 2007

17

.6

17

.6

20

.5

23

.8

25

.2

28

.5

27

.2

36

.7

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007

Pe

rce

nt

of

Ex

tern

al N

AF

TA

Ind

ire

ct

Tra

de

Source: AISI Indirect Steel Trade Report

China Also Driving NAFTA Indirect Steel Trade Deficit

23

A Constructive Response to the Economic Crisis: Steel Market Development in the Home Market

24

Critical Trade Messages

Recognizing the seriousness of the economic downturn and the need to avoid a recurrence of prior steel crises:

• Strong and effective enforcement of trade laws throughout the NAFTA region

• A more effective approach to dealing with global market-distorting practices

• Policies that will reduce the North American indirect steel trade deficit

25

2. North America Is A Major Producer, Consumer And Trader Of Raw Materials

26

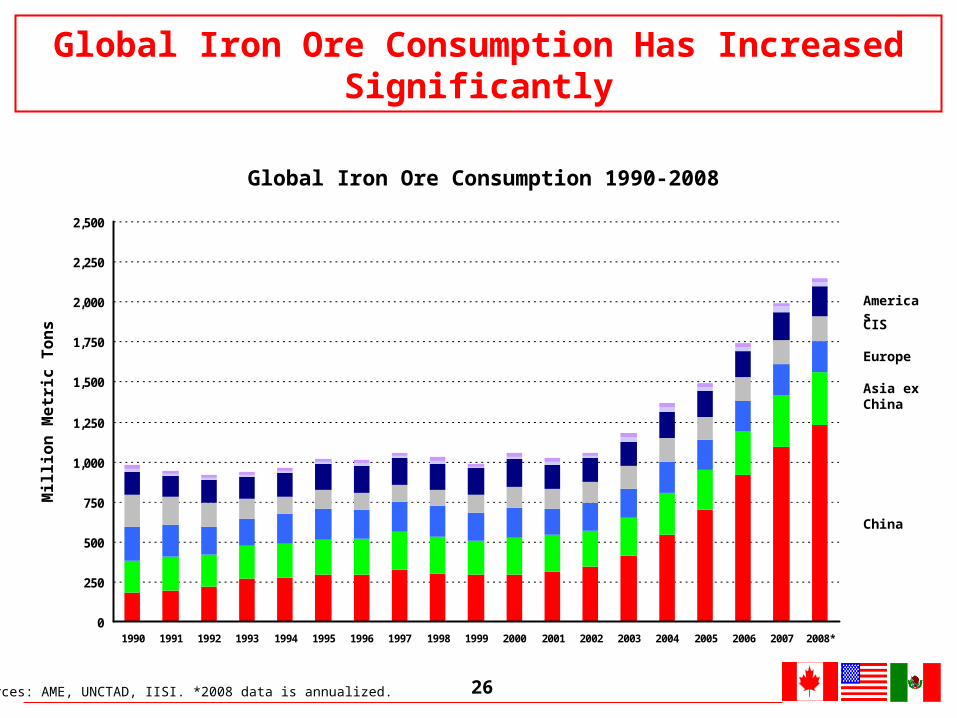

Mil

lio

n M

etr

ic T

on

s

Global Iron Ore Consumption Has Increased Significantly

Sources: AME, UNCTAD, IISI. *2008 data is annualized.

Global Iron Ore Consumption 1990-2008

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008*

China

Asia ex China

Europe

CIS

Americas

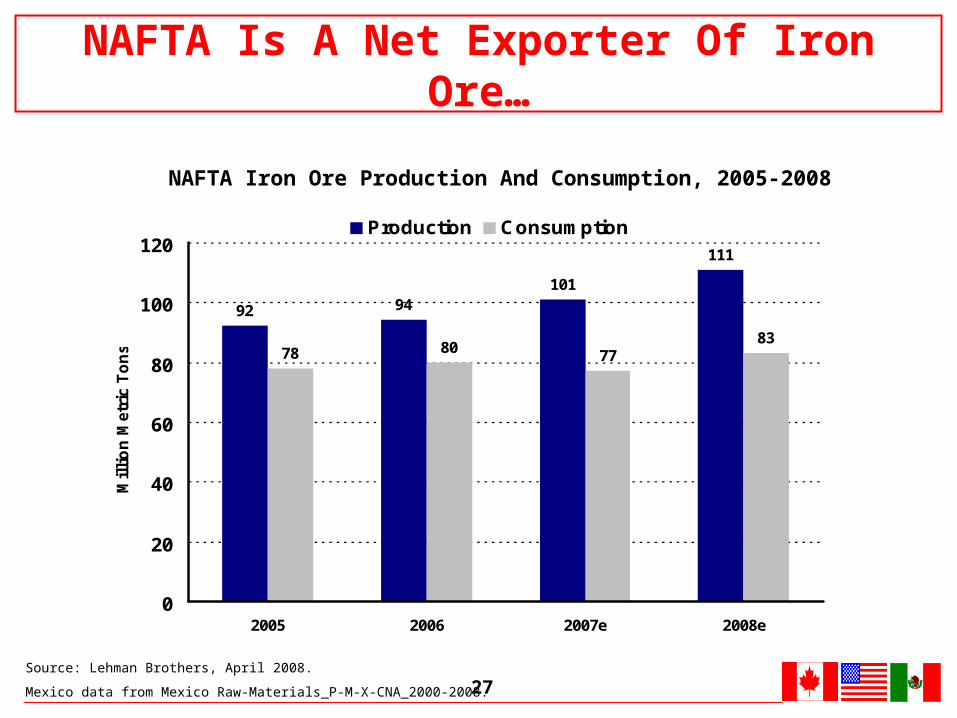

27

92 94101

111

78 80 7783

0

20

40

60

80

100

120

2005 2006 2007e 2008e

Mil

lio

n M

etr

ic T

on

s

Production Consumption

NAFTA Iron Ore Production And Consumption, 2005-2008

Source: Lehman Brothers, April 2008.

Mexico data from Mexico Raw-Materials_P-M-X-CNA_2000-2008.

NAFTA Is A Net Exporter Of Iron Ore…

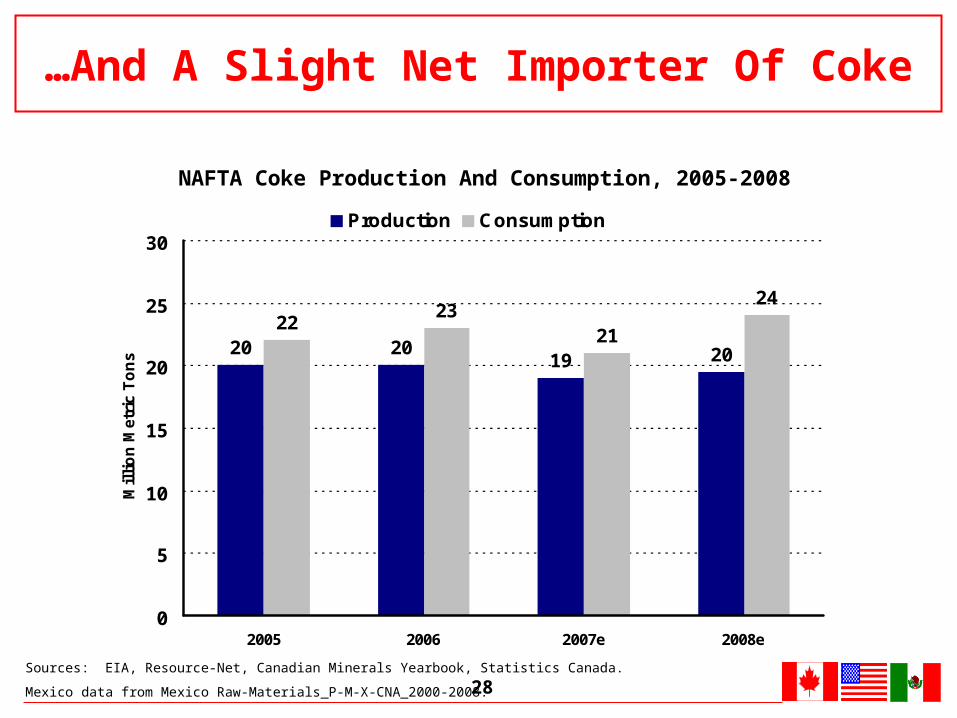

28Sources: EIA, Resource-Net, Canadian Minerals Yearbook, Statistics Canada.

Mexico data from Mexico Raw-Materials_P-M-X-CNA_2000-2008.

…And A Slight Net Importer Of Coke

NAFTA Coke Production And Consumption, 2005-2008

20 2019

2223

21

24

20

0

5

10

15

20

25

30

2005 2006 2007e 2008e

Mil

lio

n M

etri

c T

on

s

Production Consumption

29Source: US Geological Survey, IISI

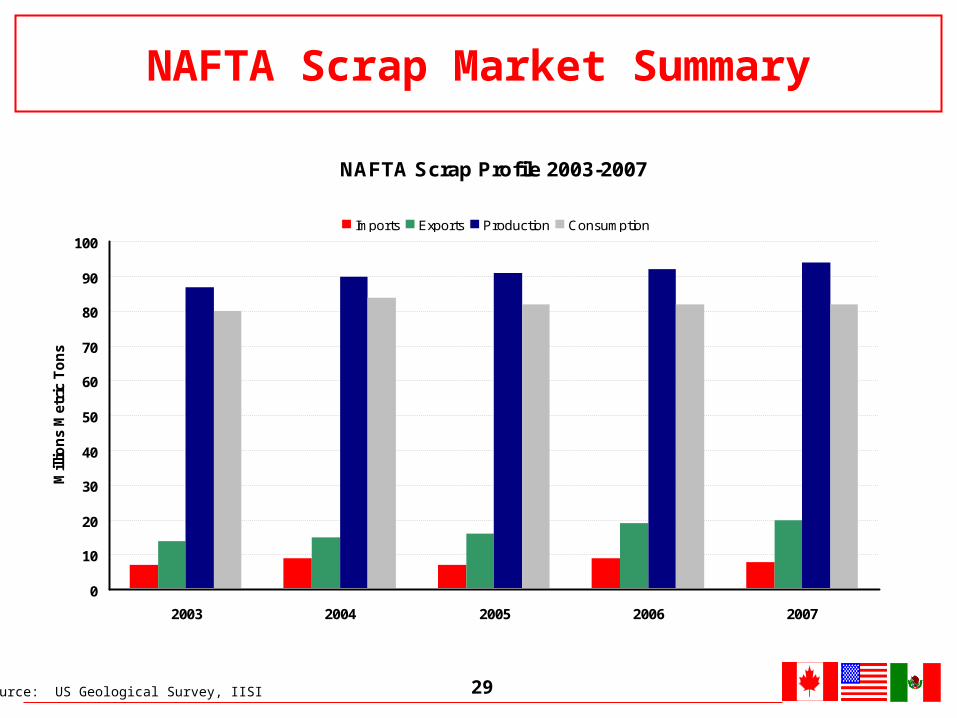

NAFTA Scrap Profile 2003-2007

0

10

20

30

40

50

60

70

80

90

100

2003 2004 2005 2006 2007

Mill

ion

s M

etri

c T

on

s

Imports Exports Production Consumption

NAFTA Scrap Market Summary

30

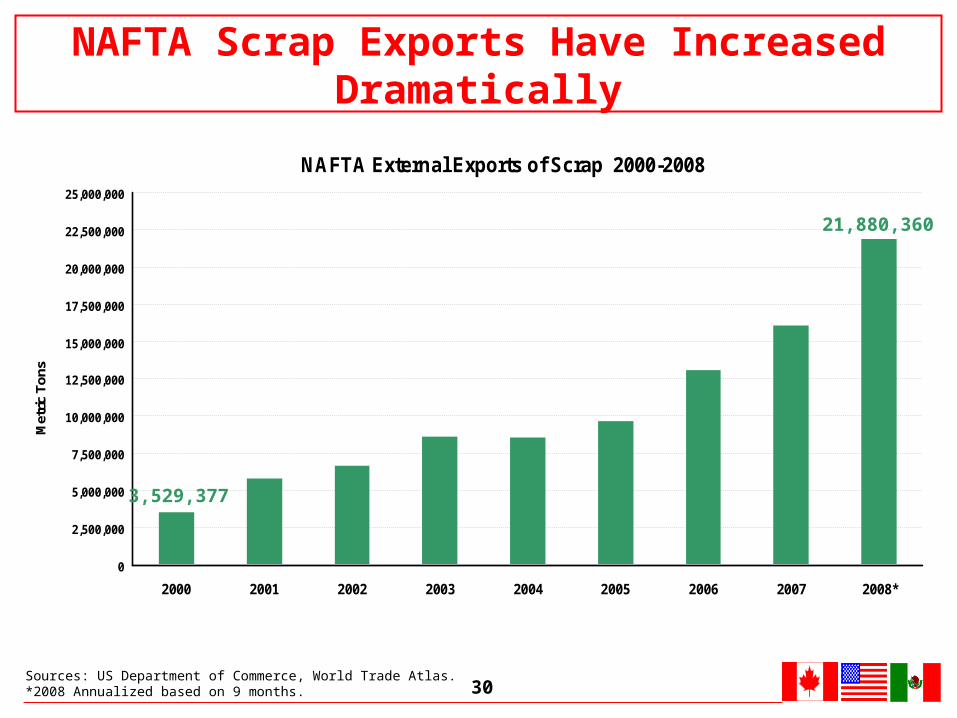

NAFTA External Exports of Scrap 2000-2008

0

2,500,000

5,000,000

7,500,000

10,000,000

12,500,000

15,000,000

17,500,000

20,000,000

22,500,000

25,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008*

Met

ric

To

ns

Sources: US Department of Commerce, World Trade Atlas. *2008 Annualized based on 9 months.

NAFTA Scrap Exports Have Increased Dramatically

21,880,360

3,529,377

31

3. Key Concerns About Raw Materials: Trade And Investment Barriers

32

Metal First % Second % Third % ∑

Iron ore Brazil 22 Australia 21 China 15 58

Chromium South Africa 41 Kazakhstan 27 India 8 76

Manganese China 21 Gabon 20 Australia 16 57

Molybdenum U.S.A. 34 China 23 Chile 22 79

Nickel Russia 19 Canada 16 Australia 13 48

Niobium Brazil 90 Canada 9 Australia 1 100

Rare earths China 95 U.S.A. 2 India 2 99

Tantalum Australia 60 Brazil 18 Mozambique 5 83

Tungsten China 84 Canada 4 E.U. 4 92

Vanadium South Africa 45 China 38 Russia 12 95

Selected Raw Materials Global Production % Share

Raw Materials Supplying Nations Are Highly Concentrated

Source: European Commission Staff Working Document SEC (2008) 2741

33

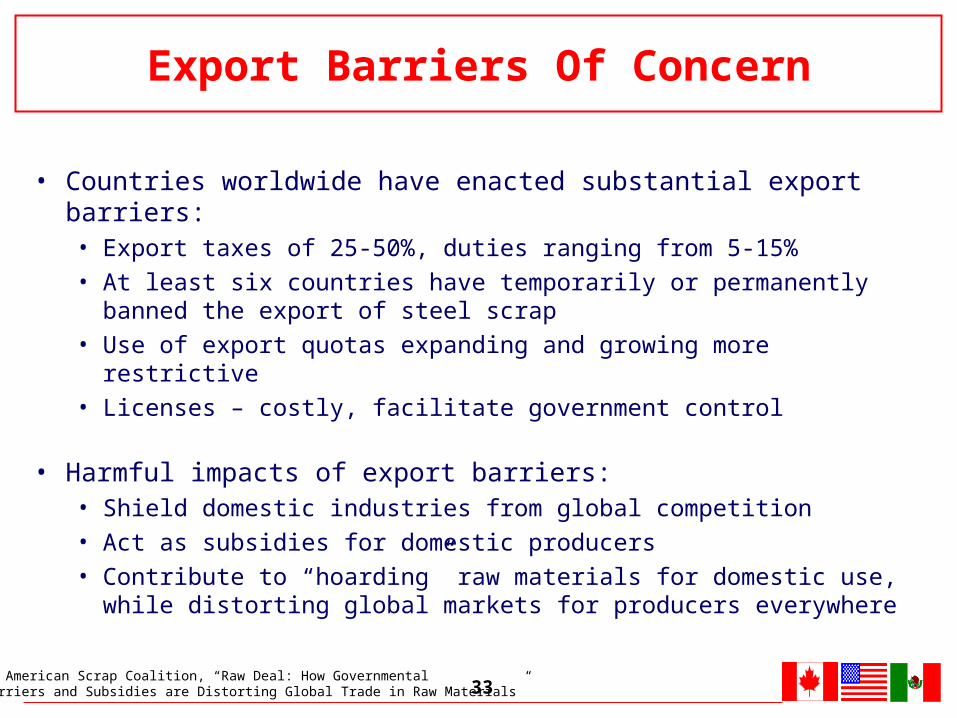

• Countries worldwide have enacted substantial export barriers:• Export taxes of 25-50%, duties ranging from 5-15%

• At least six countries have temporarily or permanently banned the export of steel scrap

• Use of export quotas expanding and growing more restrictive

• Licenses – costly, facilitate government control

• Harmful impacts of export barriers:• Shield domestic industries from global competition

• Act as subsidies for domestic producers

• Contribute to “hoarding” raw materials for domestic use, while distorting global markets for producers everywhere

Export Barriers Of Concern

Source: American Scrap Coalition, “Raw Deal: How Governmental Trade Barriers and Subsidies are Distorting Global Trade in Raw Materials”

34

Raw Material Country

Coke China, Ukraine

Ferroalloys of chromium, nickel, molybdenum and tungsten

China

Ferrous scrap Russia, Ukraine

Iron ore India

Manganese China

Molybdenum China

Nickel China

Rare earth elements China

Tungsten China

Select Raw Material Export Restrictions

Source: European Commission Staff Working Document SEC (2008) 2741

35

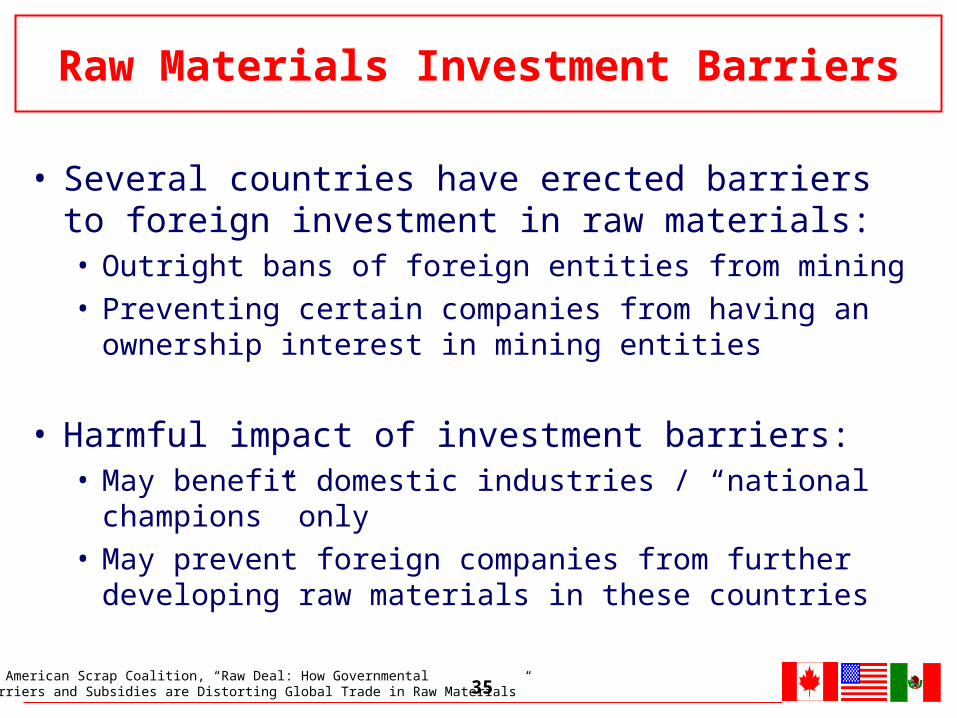

• Several countries have erected barriers to foreign investment in raw materials:• Outright bans of foreign entities from mining

• Preventing certain companies from having an ownership interest in mining entities

• Harmful impact of investment barriers:• May benefit domestic industries / “national champions” only

• May prevent foreign companies from further developing raw materials in these countries

Raw Materials Investment Barriers

Source: American Scrap Coalition, “Raw Deal: How Governmental Trade Barriers and Subsidies are Distorting Global Trade in Raw Materials”

36

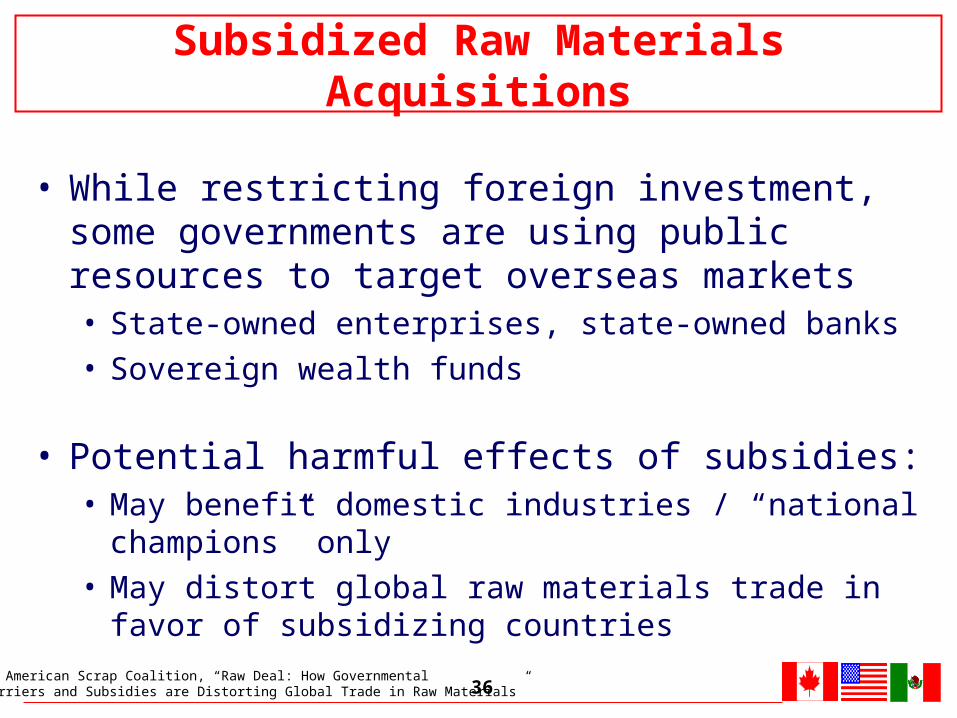

• While restricting foreign investment, some governments are using public resources to target overseas markets • State-owned enterprises, state-owned banks

• Sovereign wealth funds

• Potential harmful effects of subsidies:• May benefit domestic industries / “national champions” only

• May distort global raw materials trade in favor of subsidizing countries

Subsidized Raw Materials Acquisitions

Source: American Scrap Coalition, “Raw Deal: How Governmental Trade Barriers and Subsidies are Distorting Global Trade in Raw Materials”

37

• Distort trade and market outcomes

• Raise costs for material users

• Unfairly tilt the playing field throughout the global manufacturing economy

• Arguably violate WTO agreements, free trade agreements, or bilateral investment treaties

Summary: Raw Materials Trade Barriers Impact

38

4. Key Policy Conclusions

39

• Market forces must apply for steel, raw materials and steel-containing goods• Dumped /subsidized imports and export/investment restrictions

distort market forces

• NAFTA region at risk due to global steel market deterioration

• WTO-consistent trade law application not “protectionism” • Counters trade and market-distorting practices• Restores free market principles and ensures rules-based trade

• Lessons of 1998 steel crisis:• NAFTA will not be “dumping ground” for excess offshore steel • Urge NAFTA governments to remain vigilant and firmly committed

to strong trade laws, strictly enforced

Rules-Based Trade Is Fair Trade

40

• Government interference in raw materials trade and investment is a growing source of steel trade distortions

• Export taxes, minimum price programs, export bans and quotas are all restrictive• Manipulation of export restriction regimes causes significant market

uncertainty, distortions and disruptions

• Raw materials export restrictions create artificial advantages for exporting steel producers• Increasing domestic supply while lowering domestic prices• Simultaneously curbing supply and raising prices for foreign competitors

• Artificially low domestic prices for raw materials also create disadvantages for commodity producers• Reduces incentives for investment and modernization

Market Principles For Raw Materials

41

• WTO Doha “NAMA” negotiations should produce more effective rules on export manipulation• Address export taxes and quotas

• Import/Export licensing must be:• Transparent (e.g notice and public comment)• Non-discriminatory – use of objective criteria

• Metals/minerals investment policies should follow the Extractive Industries Transparency Initiative

• Malaysian government deserves praise for removing its steel scrap export ban • Malaysia and all governments should eliminate all restrictions (including duties) on

raw materials exports

• “Lack of availability” no longer relevant due to global economic crisis and reduced demand• Now is the time to remove market access barriers

Market Principles For Raw Materials